Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1089.40 down $5.50 cents (comex closing time)

Silver $14.52 down 23 cents.

In the access market 5:15 pm

Gold $1085.00

Silver: $14.50

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a good delivery day, registering 256 notices for 25,600 ounces and on Friday we had 16 notices for 80,000 oz . Silver saw 1 notice for 5,000 oz for Friday.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 235.52 tonnes for a loss of 59 tonnes over that period.

In silver, the open interest fell by 1159 contracts. The total silver OI continues to remain extremely high, with today’s reading at 185,926 contracts In ounces, the OI is represented by .930 billion oz or 132% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative.

In silver we had 16 notices served upon for 80,000 oz.

In gold, the total comex gold OI rests tonight at 435,095. We had 256 notices filed for 25,600 oz today.

We had no withdrawals in gold tonnage at the GLD today / thus the inventory rests tonight at 672.70 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in GLD gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had no change in silver inventory at the SLV / Inventory rests at 326.829 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 1159 contracts down to 185,926. We again must have had some shortcovering by the bankers as they feared something was brewing in the silver arena. The OI for gold rose to 435,095 contracts

(report Harvey)

2. Two big commentaries from Bill Holter

first commentary title:

“I Dare You!”

and the second commentary:

“The Great Call.”

(Bill Holter/Holter-Sinclair collaboration)

3. Two important stories on Greece

(zero hedge)

4.One story on Ukraine

(zero hedge)

5.Is GLD being raided to supply China?

(TF Metals, Craig Hemke/Dave Kranzler ird)

6. A superb Ted Butler commentary

(Ted Butler)

7. Huge Chinese demand this past reporting week: 73 tonnes

(Jessie/Americain cafe)

8 Huge demand for gold from India/155 tonnes of demand over the first two months of their fiscal year.

(times of India)

9 Trading of equities/ New York

(zero hedge)

10. Oil related stories (3)

zero hedge/ Andy Tully

11. USA stories:

Data for today:

a)

i). Personal spending down

ii). ISM manufacturing slumps

iii). Construction spending also slumps

b). Puerto Rico defaults on its bonds

c). Another casualty in the coal space: Alpha Natural

(zero hedge)

Here are today’s comex results:

The total gold comex open interest rose from 427,678 contracts up to 435,095 for a gain of 7417 contracts. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month, and today the latter was again the norm. What is interesting is that the LBMA gold is witnessing a 7.40 premium spot/next nearby month as gold is now in backwardation over there. We are now in the contract month of August and here the OI fell by 920 contracts falling to 8,295 contracts. We had 3 notices filed upon on Friday and thus we lost 917 contracts or 91,700 ounces will not stand for delivery.The next delivery month is September and here the OI fell by 73 contracts down to 1993. The next active delivery month if October and here the OI rose by 167 contracts up to 25,194. The estimated volume on today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 121,608. The confirmed volume on Friday (which includes the volume during regular business hours + access market sales the previous day was fair at 196,300 contracts. Today we had 256 notices filed for 25600 oz.

And now for the wild silver comex results. Silver OI fell by 1159 contracts from 187,085 down to 185,926 contracts despite the fact that silver was up by 6 cents yesterday . We continue to have our bankers pulling their hair out with respect to the continued high silver OI as the world senses something is brewing in the silver arena. We are in the delivery month of August and here the OI fell by 20 contracts down to 89. We had one delivery notice filed on Friday and thus we lost 19 contracts or 95,000 ounces will not stand for delivery in this non active August contract month.The next major active delivery month is September and here the OI fell by 2639 contracts to 120,622. The estimated volume today was fair at 26,105 contracts (just comex sales during regular business hours). The confirmed volume on Friday (regular plus access market) came in at 55,076 contracts which is excellent in volume. We had 16 notices filed for 80,000 oz.

August contract month: initial standing

August 3.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1477.46 oz (Scotia,Manfra) |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 256 contracts (25,600 oz) |

| No of oz to be served (notices) | 8036 contracts (803,600 oz) |

| Total monthly oz gold served (contracts) so far this month | 259 contracts(25,900 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 272,871.421 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposits

total dealer deposit: zero

total customer withdrawal: 1,477.46 oz

We had 0 customer deposits:

Total customer deposit: nil oz

We had 1 adjustments

i) Out of Scotia: 200.732 oz was adjusted out of the customer and this landed into the dealer account of Scotia

JPMorgan has only 3.098 tonnes left in its registered or dealer inventory.

.

Today, 0 notices was issued from JPMorgan dealer account and 48 notices were issued from their client or customer account. The total of all issuance by all participants equates to 256 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the August contract month, we take the total number of notices filed so far for the month (259) x 100 oz or 25900 oz , to which we add the difference between the open interest for the front month of August (8295) and the number of notices served upon today (256) x 100 oz equals the number of ounces standing

Thus the initial standings for gold for the August contract month:

No of notices served so far (259) x 100 oz or ounces + {OI for the front month (8295) – the number of notices served upon today (256) x 100 oz which equals 921,200 oz standing so far in this month of July (25.80 tonnes of gold).

We lost 917 contracts or an additional 91700 oz will not stand for delivery in this active month of August.

Total dealer inventory 351,720.09 or 10.939 tonnes

Total gold inventory (dealer and customer) = 7,570,807.473 oz or 235.48 tonnes

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 235.48 tonnes for a loss of 67 tonnes over that period.

end

And now for silver

August silver initial standings

August 3 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,040433.342 oz (CNT,Delaware,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 16 contract (80,000 oz) |

| No of oz to be served (notices) | 73 contracts (365,000 oz) |

| Total monthly oz silver served (contracts) | 17 contracts (85,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,446,601.7oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 0 customer deposits:

total customer deposits: nil oz

We had 3 customer withdrawals:

i)Out of Delaware: 1,968.800 oz

ii) Out of CNT 321,429.900 oz

iii) Out of Scotia; 717,037.642 oz

total withdrawals from customer: 1,040,433.342 oz

we had 1 adjustment

Total dealer inventory: 56.568 million oz

Total of all silver inventory (dealer and customer) 174.630 million oz

The total number of notices filed today for the August contract month is represented by 16 contracts for 80,000 oz. To calculate the number of silver ounces that will stand for delivery in August, we take the total number of notices filed for the month so far at (17) x 5,000 oz = 85,000 oz to which we add the difference between the open interest for the front month of July (89) and the number of notices served upon today (16) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the August contract month:

17 (notices served so far)x 5000 oz + { OI for front month of August (89) -number of notices served upon today (16} x 5000 oz ,= 450,000 oz of silver standing for the August contract month.

we lost 19 contracts or an additional 95,000 oz will not stand in this delivery month of August.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.comorhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

August 3.2015: no change in inventory at the GLD./Inventory remains at 672.70 tonnes

July 31/we had a huge withdrawal of 7.45 tonnes/Inventory rests this weekend at 672.70 tonnes

July 29/no change in inventory/rests tonight at 680.13 tonnes

July 28/no change in inventory/rests tonight at 680.13 tonnes

July 27/no change in inventory/rests tonight at 680.13 tonnes

July 24.2015/we had another massive withdrawal of 4.48 tonnes of gold form the GLD/Inventory rests at 680.13 tonnes.

July 23.2015: we had another withdrawal of 2.68 tonnes of gold from the GLD/Inventory rests at 684.63 tonnes

july 22/another withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 687.31

July 21.2015: a massive withdrawal of 6.56 tonnes of gold from the GLD.

Inventory rests at 689.69 tonnes. China and Russia need their physical gold badly and they are drawing their physical from this facility.

July 2o.2015: no change in inventory

July 17./a massive withdrawal of 11.63 tonnes in gold tonnage tonight from the GLD/Inventory rests at 696.25 tonnes

July 16./we lost 1.19 tonnes of gold tonight/Inventory rests at 707.88 tonnes

August 1 GLD : 672.70 tonnes

end

August 3.2015; no change in inventory at the SLV/inventory remains at 326.829 million oz

And now for silver (SLV) July 31/no change in inventory/rests tonight at 326.829 million oz

July 29/no change in silver inventory/326.829 million oz

July 28/we had a huge withdrawal of 2.005 million oz from the SLV/Inventory rests at 326.829 oz

July 27/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 24/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 23.2015; no change in silver inventory/rests tonight at 328.834 million oz

july 22/no change in silver inventory/inventory rests at 328.834 million oz.

July 21.we had a massive addition of 1.241 million oz into the SLV/Inventory rests tonight at 328.834 million oz.

Please note the difference between gold and silver (GLD and SLV). In GLD gold is being depleted and sent to the east. In silver: no depletions, as I guess this vehicle cannot supply physical metal.

July 20/no change

july 17.2015/no change in silver inventory tonight/inventory at 327.593 million oz

July 16./no change in silver inventory/rests tonight at 327.593 million oz

August 3/2015: tonight inventory rests at 326.829 million oz

end

And now for our premiums to NAV for the funds I follow:

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 11.4 percent to NAV usa funds and Negative 11.0% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 62/2%

Percentage of fund in silver:37.5%

cash .4%

( July 31/2015) Cdn holiday

2. Sprott silver fund (PSLV): Premium to NAV rises to -.55%!!!! NAV (August 3/2015) (silver must be in short supply)

3. Sprott gold fund (PHYS): premium to NAV falls to – .90% to NAV(July August/2015)

Note: Sprott silver trust back into negative territory at- 0.55%

Sprott physical gold trust is back into negative territory at -.90%

Central fund of Canada’s is still in jail.

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64)

Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis.

Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer.

Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer.

* * * * *

>end

And now for your overnight trading in gold and silver plus stories

on gold and silver issues:

Goldcore blog off today.

(courtesy/Mark O’Byrne/Goldcore)

end

(courtesy Craig Hemke/TFMetalsReport)

TF Metals Report: July 19 raid on gold was meant to drain GLD

2:37p ET Sunday, August 2, 2015

Dear Friend of GATA and Gold:

The raid on gold of Sunday night, July 19, was staged by bullion banks to drain more tonnage from the exchange-traded fund GLD to be sent to Asia, the TF Metals Report’s Turd Ferguson writes.

“As GLD is a readily-accessible source of instantly available gold,” Ferguson writes, “its authorized participant bullion banks are once again redeeming their 100,000-share lots for physical gold from the GLD ‘inventory.’ That this gold is then utilized to settle physical demand from around the globe is hardly arguable, given recent history.”

Ferguson’s commentary is headlined “The Gold Raid of July 19” and it’s posted at the TF Metals Report here:

http://www.tfmetalsreport.com/blog/7036/gold-raid-july-19

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

And on the same subject as above

(courtesy Dave Kranzler/IRD)

Was The July 19 Paper Raid On Gold Implemented To Remove Gold From GLD?

Craig Hemke of the TF Metals Report wrote an article which has sniffed out the probable motive behind the shamelessly blatant paper smash of gold on Sunday evening July 19 at one of the quietest trading periods of the week:

As a readily-accessible source of instantly-available gold, The Authorized Participant Bullion Banks are once again redeeming their 100,000 share lots for physical gold from the GLD “inventory”. That this gold is then utilized to settle physical demand from around the globe is hardly arguable, given recent history. – Craig Hemke, TFMetalsReport.com

I believe Craig has hit the nail on head here. Ever since first reading James Turk’s original dissection of the GLD Trust legal structure from the Prospectus, it’s been pretty obvious that GLD was created to act as a “holding reservoir” of physical gold that would be used by the Central Banks/bullion banks as a source of gold to required to settle LBMA forward commitments to buyers (i.e. China, India and Russia) who would refuse to settle in cash. 99% of all Comex trades are settled in cash.

The one unresolved question, for me anyway, is the issue of how much gold really still exists in unencumbered (e.g. leases or hypothecation agreements) physical bar form in HSBC’s vault or the vaults of designated subcustodians. It’s an question that won’t be answered until the system implodes because GLD, by design, has made it impossible for anyone to conduct a bona fide, independent audit.

This is an excerpt from a post I wrote on the The Golden Truth, the predecessor blog to Investment Research Dynamics – it looks like my analysis was correct back then which reaffirms Craig’s analysis of what happened two weeks ago:

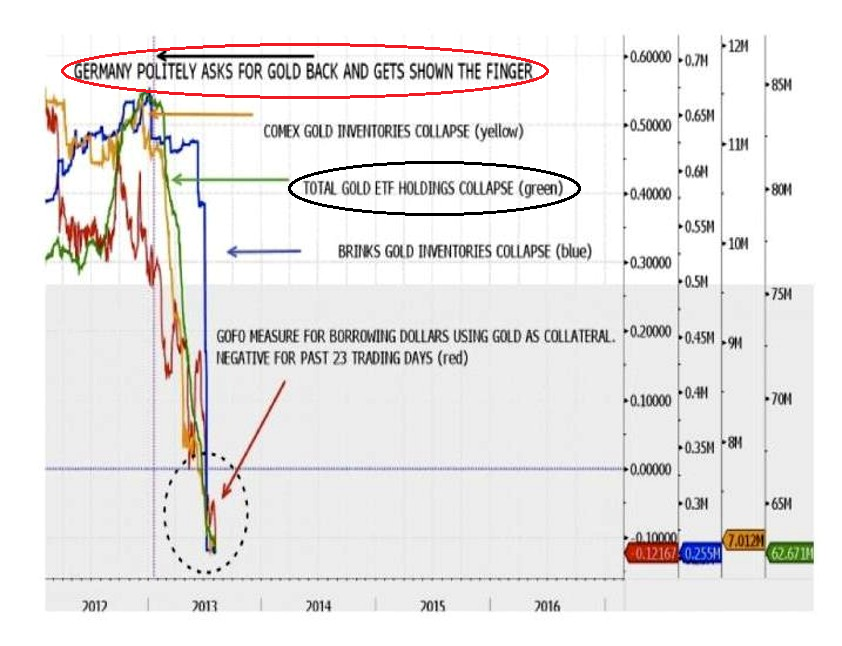

We have witnessed a stunning drain of gold from the GLD ETF trust. Through last Friday, an incredible 479 tonnes – more than 35% – of GLD’s gold has been removed and has disappeared, most likely to Asia – in the space of about 10 months. The biggest chunk of that 479 tonnes was removed shortly after Germany’s Bundesbank issued it’s feeble and hopeless request to the U.S. that the Federal Reserve start shipping back some portion of the 1500 tonnes of gold that is supposedly being “safe-kept” on behalf of Germany by the Fed in its vault in New York City. Gold luck, Angela…

I have looked at GLD suspiciously ever since James Turk issued the first analysis of GLD’s prospectus back in 2004. Those of us who are familiar with securities laws and investor “safe guards” supposedly enforced by the SEC were absolutely shocked that the SEC approved the GLD prospectus as it was filed because of the egregious lack of GLD sponsor and custodian legal accountability standards typically required by the SEC for publicly traded securities.

Given this fact, I believed at the time that GLD was a scheme devised to suck in retail and institutional cash that might otherwise flow in massive quantities into actual physical gold that would be safe-kept in private vaults in this country. Although GLD has a mechanism to enable investors with a minimum of 100,000 shares to convert those shares into gold that would be delivered to the investor, the procedure is exceedingly cumbersome and expensive and there’s a mechanism embedded in the language of the prospectus that enables the trustee of GLD to deny such requests.

But I also knew – through GATA’s invaluable research – that there would eventually be a shortage of physical gold that would be available to allow the western Central Banks and bullion banks to maintain their oppressive and incessant manipulation of the paper gold market for the purposes of maintaining a cap on the price of gold, for the purposes of defending the credibility of the U.S. dollar. I figured that at some point the gold in GLD would used for this purpose once the Central Bank stocks of gold were largely if not fully depleted. In this context, please recall that about three years, the ECB system, which had been selling 400 tonnes per year on average, pretty much stopped selling any gold. That’s sign-post #1 that I was right.

Then along comes the Bundesbank in early 2013, with a request that the Fed start shipping Germany’s gold held in in New York back to Germany. That’s when all hell broke loose:

(The graph above is from the TFMetalsReport.com)

There’s something really wrong with that picture because the intuitive response from the market by Germany’s request of the Fed should have been a quickly rising price of gold. But as you we all know, the Fed defaulted on the request – for all intents and purposes – and that’s when the massive drain of gold from GLD commenced.

The truth is that my original hunch was correct. 100% correct. The gold in the GLD trust is being used to satisfy the enormous physical delivery demands from China and the other big gold buying countries because the western Central Banks have run out of gold to deliver. That is an unmistakable fact. Reports and data ad nauseum have been published in the last six months describing and verifying the voluminous, unprecedented amount of gold bars that have been moved – literally physical transferred – from the Comex in NY and the LBMA and Bank of England vaults in London to Switzerland and then on to Hong Kong, where it flows to its ultimate destinations in China. Anyone who would deny that this is the case has a blatant and catastrophic disregard for the truth as supported by provable facts.

So the question is, how much longer can the depletion of gold from GLD continue before this scheme falls apart? Let me first say that it is likely that the U.S Government’s “Waterloo” in this situation will be the gross miscalculation – when GLD was originally devised – of the growth and size of China’s appetite for physical gold for which actual physical delivery is demanded.

Along with all the other manipulated schemes of the western Central Banks/Governments, I believe that the GLD fraud is starting to unravel. I would argue that the ability to execute successfully the intervention in interest rates, currencies and equities requires the unfettered ability to manipulate the price of gold. In my view, the western Central Banks are losing their grips on gold and this will likely bring the entire western financial system down.

end

My goodness, India is ramping up physical gold deliveries. For the first two months of their fiscal season, the citizens of India (not sovereign) purchased 155 tonnes or an average of 77.5 tonnes per month.

For a recap of the major buyers of gold:

1.China is averaging 252 tonnes per month now.

2. Russia: averaging 30 tonnes per month

3 India: 77 tonnes per month.

total for the three :359 tonnes per month. If they continue at this pace: 4308 tonnes. The world produces 2200 tonnes ex Russia ex China (who both keep every ounce produced)

(courtesy Press Trust of India/Times of India/Mumbai/GATA)

India’s gold imports up 61% at 155 tonnes in April-May

From the Press Trust of India

via The Times of India, Mumbai

Sunday, August 2, 2015

NEW DELHI — India’s gold imports shot up by about 61 percent to 155 tonnes in the first two months of the current fiscal mainly due to weak prices globally and the easing of restrictions by the Reserve Bank.

In April-May of the last fiscal years, gold imports had aggregated about 96 tonnes, an official said.

In the international market, gold has been trading weakly over the past few months. On Friday, it closed at US$1,095.10 in New York market. …

… For the remainder of the report:

http://timesofindia.indiatimes.com/business/india-business/Gold-imports-…

end

And now for China’s demand last week: A monstrous 73.289 tonnes of gold. Ladies and Gentlemen: this is citizen gold demand. Sovereign gold is not included in this mix;

(courtesy Jessie/Americain cafe)

31 July 2015

Shanghai Gold Exchange Has 73.3 Tonnes of Bullion Withdrawn Its Third Largest WeekFor the week ending July 24th there were 73.289 tonnes of gold bullion withdrawn from the Shanghai Exchange into China.

That is about 2,356,296 troy ounces in one week.

I have included the most recent statistics from the Comex Gold Warehouses below. There are currently 351,519 ounces of gold available for delivery at these prices there for the month of August.

Nine out of ten Americans will notice that in terms of technical analysis this is ‘a lot less.’

But as the very serious people like to point out, the Comex is not really ‘a physical exchange.’ Yep.

And as you may have seen in the posting from earlier today showing the sea change in leverage over even the past ten years there, it is seemingly getting a lot less physical all the time, even compared to just five or six years ago. Winning…

Even the US Mint seems to be getting in on the act. The mint sold 202,000 ounces of gold in the form of coins for the month of July, one of its largest monthly sales totals in several years.

That’s a lot of pet rocks.

Do the math. I wonder where the poor, deluded ignoramuses who obviously do not understand finance are getting all that money to spend on such worthless trifles. Does the US Mint take food stamps?

While they last.

This chart is from the date wrangler Nick Laird at sharelynx.com

Gold and the Grave Dancers

August 1, 2015 | Author Pater Tenebrarum

***

end

(courtesy zero hedge)

Comex On The Edge? There Are Now A Record 124 Ounces Of Paper Gold For Every Ounce Of Physical

Over the weekend, we got what was merely the latest confirmation that when it comes to sliding gold prices, consumer of physical gold just can’t get enough. As theTimes of India reported over the weekend, India’s gold imports shot up by about 61 per cent to 155 tonnes in the first two months of the current fiscal “due to weak prices globally and the easing of restrictions by the Reserve Bank. In April-May of the last fiscal, gold imports had aggregated about 96 tonnes, an official said.”

This follows confirmations previously that with the price of gold sliding, physical demand has been through the roof, case in point: “US Mint Sells Most Physical Gold In Two Years On Same Day Gold Price Hits Five Year Low“, “Gold Bullion Demand Surges – Perth Mint and U.S. Mint Cannot Meet Demand“, “Gold Tumbles Despite UK Mint Seeing Europeans Rush To Buy Bullion” and so on. Indicatively, as of Friday, the US Mint had sold 170,000 ounces of gold bullion in July: the fifth highest on record, and we expect today’s month-end update to push that number even higher.

But while the dislocation between demand for physical and the price of paper gold has been extensively discussed here over the years, most recently in “Gold And The Silver Stand-Off: Is The Selling Of Paper Gold And Silver Finally Ending?”, something unexpected happened at the CME on Friday afternoon which may be the most important observation yet.

Recall that in the middle of 2013, in an extensive series of articles, we covered what was then a complete collapse in Comex vaulted holding of registered (i.e., deliverable) gold. At the time the culprit was JPM, where for some still unexplained reason, the gold held in the newest Comex’ vault plunged by nearly 2 million ounces in just six short months.

More importantly, the collapse in registered Comex gold sent the gold coverage ratio (the number of ounces of “paper” gold open interest to the ounces of “physical” registered gold) soaring from under 20 where, or roughly in line with its long-term average, to a whopping 112x. This means that there were a total of 112 ounces of claims for every ounces of physical gold that could be delivered at any given moment.

Gradually, the Comex raid was relegated to the backburner when starting in 2014 the amount of registered gold tripled from the upper 300k range to 1.15 million ounces one year ago, at which point the slide in Comex registered gold started anew.

Which brings us to Friday afternoon, also known as month end position squaring, when in the latest daily Comex gold vault depository update we found that while some 270K in Eligible gold had been withdrawn mostly from JPM vaults, what caught our attention was the25,386 ounces of Registered gold that had been “adjusted” out of registered and into eligible. As a reminder, eligible gold is “gold” that can not be used to satisfy inbound delivery requests without it being converted back to registered gold first, which makes it mostly inert for delivery satisfaction purposes.

Most importantly, this 25,386 oz reduction in deliverable Comex gold from 376,906 on Thursday pushed the amount of registered Comex gold to an all time low: at 351,519 ounces, or just barely over 10 tons,registered Comex gold has never been lower!

Incidentally, as part of the month-end redemption requests, we saw a whopping 22% of the eligible gold in Kilo-bar format (where there is no registered, just eligible) be quietly whisked away from Brink’s vaults: unlike traditional ounce-based contracts, the kilo format traditionally serves as an indication of Chinese demand, and if withdrawals on par with those seen on July 31 persist, it will soon become clear that Chinese buyers are once again scrambling for the safety of gold now that their stock market bubble has blown up.

This covers the sudden surge in demand for physical gold as manifested by CME data.

Meanwhile, over in “paper gold” land, things remained unchanged: as shown in the chart below, the aggregate gold open interest rose modestly to 43.5 million ounces up from 42.9 million the day before.

While on its own, gold open interest – which merely represents the total potential claims on gold if exercised – is hardly exciting, as we have shown previously it has to be observed in conjunction with the physical gold that “backs” such potential delivery requests, also known as the “coverage ratio” of deliverable gold.

It is here that things get a little out of hand, because as the chart below shows, all else equal, the 43.5 million ounces of gold open interest and the record low 351,519 ounces of registered gold imply that as of Friday’s close there was a whopping 123.8 ounces in potential paper claims to every ounces ofphysical gold.

This is an all time record high, and surpasses the previous period record seen in January 2014 following the JPM gold vault liquidation.

Another way of stating this unprecedented ratio is that the dilution ratio between physical gold and paper gold has hit a record low 0.8%.

Indicatively, the average paper-to-physical coverage ratio since January 1, 2000 is a “modest” 19.1x. As of Friday it had soared to more than 6 times greater.

Which brings us to the usual concluding observations:

First: as we have said previously, at a time when all the gold selling (and naked shorting) is in the paper markets and when demand for physical gold is once again off the charts, with soaring purchases not only in India but also in the US, where is this gold going? Clearly not into CME gold vaults, which are once again asource of physical gold, and as the above shows, have never had less deliverable gold.

Second, total Comex gold has dropped to such precarious levels in the past and while on many occasions market observers have asked if the Comex is close to a failure to deliver, aka a default of the CME’s gold warehouse, it has always avoided such a fate. Still, one wonders: the 10+ tons of deliverable gold at the Comex are now worth a paltry $383 million. It would not be very complicated for a next generation “Hunt Brother” to buy some $400 million in Comex gold, and promptly demand delivery: after all the gold crash of two weeks ago saw some $2.7 billion in paper gold dumped in the most illiquid market – why can’t it be done in reverse. What would happen next is unknown, but unless somehow the Comex found a way of converting millions of ounces of Eligible gold into Registered, the CME would simply be unable to satisfy such a delivery request.

Third: while there are still over 7 million ounces of Eligible gold, why the recent spike in “adjustments” of eligible to registered gold (i.e., missing a warehouse receipt)?

Finally, we assume the mainstream press will once again start paying close attention to the total, and especially registered, gold held at the Comex: at a pace of 25K a day, the gold vaults that make up the CME’s vaulting system would be depleted in just under two weeks of daily withdrawals.

In any case, we are very curious to see how this latest dramatic face off in the long-running war between paper and physical gold, concludes.

This should hurt the supply side of the equation:

(courtesy GATA)

South African mineworkers union rejects wage hike from gold producers

By Zandi Shabalala

Reuters

Sunday, August 2, 2015

http://www.reuters.com/article/2015/08/02/safrica-gold-unions-idUSL5N10D…

Members of South Africa’s Association of Mineworkers and Construction Union on Sunday rejected a wage offer from gold producers of increases of up to 17 percent, spokesman Manzini Zungu said.

Gold firms Sibanye Gold and AngloGold Ashanti last week offered an additional 1,000 rand ($80) a month to entry-level workers, while Harmony Gold offered 500 rand a month.

“Harmony’s offer has messed it up — the offer is too low for the members,” Zungu said after a mass rally at Sibanye’s Beatrix mine.

The union is demanding a more than doubling in wages but gold companies say they cannot afford such increases as they battle falling prices and rising costs.

The union will meet with the Chamber of Mines on Tuesday to officially reject what the gold companies called a “final offer.”

“The final offer is just that — final,” Chamber spokeswoman Charmane Russell said. The Chamber would wait until Tuesday to hear from the union, she said.

end

(courtesy Wall Street Journal/GATA)

China’s stock plunge burnishes gold’s appeal

By Biman Mukherji

The Wall Street Journal

Sunday, August 2, 2015

HONG KONG — Until recently, every time Hong Kong-based bullion supplier Padraig Seif would inquire about demand from customers, the answer would be the same: Business is quiet as all eyes — and money — turned to the surging stock market.

Suddenly, though, his sales are booming again in the wake of a plunge in Chinese equities and sliding gold prices.

“It has really taken us by surprise,” says Mr. Seif, co-owner of bullion supplier Finemetal Asia. “We are looking at three times the revenue in June as in May.”

He said demand is particularly strong for small gold bars weighing 250 grams and 500 grams that are popular with price-conscious smaller investors. …

… For the remainder of the report:

http://www.wsj.com/articles/chinas-stock-plunge-burnishes-golds-appeal-1…

end

Ted Butler…

(courtesy Ted Butler/Silverseek.com)

Price Takers and Price Makers

|

July 30, 2015 – 9:09am

In the world of basic commodities nearly every market participant, whether a producer or consumer, is a price taker, accepting the general price level prevailing at the time. For example, the individual consumer of gasoline has little choice but to take the price at the pump or go elsewhere. Same with corporate consumers like airlines and other transportation entities. They can hedge and fix their costs, but that hedging must be based upon current prevailing prices. Even large producers like the oil companies must take what prices the market provides, although the largest oil producers, like Saudi Arabia, could set (make) oil prices if it wanted to (at least temporarily).

That’s the way it is and should be with world commodities – 99.9% of all consumers and producers are price takers, that is, accepting whatever the prevailing price happens to be. Generally, this shouldn’t be considered a problem as it dovetails perfectly with our vision of how a free market sets prices through the magic of aggregate supply and demand. Too much world demand and not enough supply, prices have to rise; not enough demand and/or too much supply and prices must fall enough to regain fundamental balance. If that was occurring currently in the pricing of many world commodities, namely, that actual supply and demand was determining price, I would end this article here. But that is not the case.

Oh, it’s true enough that more than 99.9% of all world consumers and producers are price takers and not price setters. While that is good in terms of how free markets should operate, their total consumption and production has little to do with how prices of many world commodities are determined; and that is bad. How can this be? How can there be no dominant producer or consumer of world commodities capable of making a price; and still I contend that prices are being set to the point of being artificially fixed?

The answer lies in the fact that a great force is setting (making) the price of many world commodities completely apart from the influence of aggregate actual supply and demand. Seemingly out of nowhere, this great force has come to push aside the price effect of the law of supply and demand and render it as almost non-existent.

The great pricing force that I speak of is excessive speculative positioning in the regulated futures markets, mostly exchanges owned and run by the CME Group. Simply put, speculative futures trading has come to supplant actual commodity supply and demand as the main pricing force. Although such excessive speculation is strictly against commodity law, the primary commodities regulator, the CFTC, looks the other way. Ironically, it is the data published by the federal regulator that proves that excessive speculation is setting prices for many world commodities.

Let me be clear – there is nothing wrong with speculation and without it, there would be no functioning commodity market possible. But there is something very wrong when excessive speculation sets prices.

The excessive speculation that I refer to is quite specific – it involves only two types of modern day futures traders. One group are the traders in the category the CFTC refers to as managed money and the other group includes commercial traders (mostly banks) which take the other side of whatever the managed money traders wish to buy or sell. And it’s even more specific than that – I’m only referring to the managed money traders which operate strictly on technical considerations, like moving averages.

In a nutshell, here’s the problem – because managed money technical traders generally do the same thing (buy or sell) under similar pricing circumstances (buying on rising prices and selling on declining prices), even though each technical trader is operating independent of other technical traders, the net effect is that their collective actions transform them into one massive trader – the largest such trader ever known to markets. The price-setting influence the unified managed money traders is having on world commodities is undeniable. Whereas I usually talk in terms of what this collective influence has on silver and gold prices, it has now gone much further than that.

The proof that collective managed money positioning has been the dominate price force in recent moves in corn, crude oil and copper (in addition to silver and gold) can be seen in the data in the CFTC’s Commitments of Traders (COT) report. Other commodities are similarly affected by collective managed money futures market positioning, but let me stick to just these five commodities for the sake of brevity.

On the recent 20%+ jump in corn prices (now reversing), managed money traders bought (mostly in the form of short covering) roughly 400,000 net futures contracts in a matter of weeks, or nearly 30% of the total open interest in the Chicago Board of Trade’s corn futures market . In addition, that’s the equivalent of two billion bushels of corn, nearly 15% of US corn production and the US is the largest corn producer in the world with half the world output. If one trader, effectively and suddenly, bought 30% of an entire major futures market, could there be a more obvious force for driving prices higher?

On the recent $12 plunge in the price of crude oil, managed money traders sold 150,000 net contracts in a matter of weeks. That’s the equivalent of 150 million barrels of oil and close to 10% of the total NYMEX crude oil market. If any one trader sold 150 million barrels of crude oil in a hurry, what would the effect on prices be?

On the plunge in copper prices since May 19 from over $2.90 to under $2.40, managed money traders sold more than 66,000 net COMEX copper futures contracts, an astounding 40% of the total open interest. That’s also the equivalent of 825,000 tons of copper or more than double the combined COMEX and LME inventories. If one trader sold the equivalent of 40% of a major market in a matter of two months, wouldn’t prices drop sharply? (By the way – I’m using data from the most recent COT reports).

On the drop in gold prices of $140 from May 19, managed money traders sold 93,000 net COMEX futures contracts (mostly in the form of new shorts) or more than 20% of the entire COMEX market and the equivalent of 9.3 million oz, worth more than $10 billion. If one large trader sold more than 20% of the world’s largest gold exchange in a little over two months, would you be surprised that prices dropped by 11%?

On the $3 price drop in silver from May 19, managed money traders sold 57,000 net COMEX silver futures contracts (also mostly in the form of new short sales) or roughly 30% of the entire COMEX market, also the largest silver exchange in the world. That’s the equivalent of 285 million oz or close to 35% of world annual silver mine production. How could a large trader selling such incredible percentages of both the COMEX and world mine production not send prices lower?

I know that what I just reported on involves trading in futures contracts and not in the actual commodities, but therein lies the rub. Because all commodity producers and consumers are price takers and not price makers, physical commodities are priced off the futures price. Make the price of silver $3 lower on the COMEX and that automatically becomes the price for all silver producers and consumers. It’s nuts (and illegal) for pure speculators to dictate prices to real producers and consumers, but we live in a mad, mad world. (Perhaps only until real producers stand up against the madness).

Who are these traders that move in lockstep and hold such a dominant role in setting commodity prices? And why are the regulators looking the other way as managed money technical traders evolve into the unquestioned price makers that the data indicate? The answers to these questions have to do with gradualism and not wanting to admit to a problem that should have been rectified long ago.

First off, no one managed money technical trader is responsible for setting prices; but when many different managed money traders do the same thing at the same time, the collective effect is price making and distortion. As a whole, managed money traders control upwards of $300 billion in assets devoted to futures trading. They even have their own powerful lobbying organization, which like any such organization fights any attempt to restrict their activities, even if their collective activities undermine the integrity of our markets.

And as for the CFTC, it has denied so often that there is anything amiss in the silver market that there is no chance it can admit to anything I allege under any circumstances. Unfortunately, because the CFTC is afraid to even discuss this issue, now the silver manipulation disease has spread to most markets controlled by the CME Group. That’s too bad, because there is a simple solution to the problem of collective managed money trading making the price that all consumers and producers of world commodities must take. (For the purpose of this article, I’m leaving out my contention that the commercials are tricking the managed money traders into and out from futures positions, as that’s a separate issue).

The solution (as I’ve maintained for years) is to treat the managed money traders who are buying and selling in unison as the one trading entity that they are effectively functioning as. There is no question that these traders are speculators and, therefore, there is no question that they should be treated as a single speculative entity and be governed by a single collective speculative position limit.

No one speculative trader would be allowed to buy or sell 10%, 20% or 40% of any commodity market in a short period of time and neither should a small group of traders, trading in lockstep, be allowed to do the same. Remember we’re talking about a very small number of managed money traders, close to 30 or 50 traders in most markets. Why should 30 or 50 purely speculative CME traders be allowed to set the price for the millions and even billions of world participants who must then take the prices dictated to them?

Ted Butler

July 30, 2015

end

I Dare You!

A very real problem or flaw in logic exists in the current gold and silver markets. If there is in fact so much selling (panic selling), how is it possible the U.S. Mint had to stop selling Silver Eagles nearly a month ago? It can only be for one of two reasons. Either they had enough silver but could not produce coins fast enough to satisfy demand, or, they could not source enough silver to make the coins. But this does not make any sense. How could there be “too much demand” if everyone is selling? Also, how could there not be enough silver available if everyone is selling and has sold? Where did all of this “sold” silver go to? Again, I dare anyone to come up with a logical answer to this.

We are also seeing the same thing in gold. It is trading in backwardation ($7 plus) in London and with substantial premiums in India and throughout Asia. If the masses are dumping gold then supply should be plentiful, how can physical tightness exist or premiums over the paper price exist if recently sold gold is falling out of dump trucks on their way to refineries? Any logical answers for this? The gold bashers say “see, the price is down, there is your proof”. Do Armstrong and crew deny that the only thing necessary to sell a COMEX gold or silver contract short is the ability to post margin? Do they deny that “money” (margin) can be and is created for free ? And then used to “water down” the futures in the same manner as a company over issues stock or a country over issues money supply?

There is a very real distinction between paper gold and physical gold, this will soon become apparent. The difference is physical in your own control is no one else’s liability. Paper gold on the other hand is the liability of the issuer of the contract. Currently, COMEX has a whopping 11.7 tons left of deliverable gold left. JP Morgan claims to have less than four tons, these are the lowest numbers I can ever remember. To put it in perspective, 11.7 tons of gold is worth less than $400 million dollars. The COMEX can now be broken and exposed with petty cash! As sure as the Sun will rise tomorrow, there will eventually be a “call” on real gold. Not only on COMEX gold but ALL paper gold …any call will not be met because the gold does not exist to meet the call. There are now more than 100 paper ounces of gold sold for every one ounce of real gold that exists to deliver. If there were 100 fake shares of IBM trading and watering down every one real share in existence, the price of IBM stock would be trading in the low single digits! The fake shares would alter perception but not the reality of what the company is worth as an ongoing concern.

Another area to touch on is the “threat” of the Fed raising interest rates. I view a rate hike as ONLY a threat at this point and will get into that shortly. Looking back, the Fed has floated the idea of rate normalization ever since early 2010. It was always six months out …and continually extended. But this time they really mean it? The consensus is now for a rate hike in September. I can only say one thing to Janet Yellen and the gang, I DARE YOU! In my opinion, if the Fed were to raise rates we might only have a functioning financial system for about 48 hours, I cannot see more than a week or two at the most.

Why is this you ask? Let’s count the ways … First, global trade is already imploding. China is entering a margin call scenario on many fronts. An already strong dollar is pressuring an over indebted world that owes in dollars. Internally, the U.S. is missing on many cylinders, retail sales and housing turnover already weak will become disastrous. Reported economic numbers are barely treading water even with bogus assumptions and accounting. Tightening credit will also have a negative effect on the banking system with razor thin margins and even more so in the derivatives complex. Higher rates on their own will create margin calls, not to mention investors scrambling for the door in fear of even more rate hikes. Panic begets panic in other words. The way I see it, there is a very real probability the Fed not only does not raise rates in September, a very real chance exits for QE4 to be announced and implemented in a panic. It should be added that the possibility of forced US Treasury sales by China is a distinct possibility. They may be forced to do this to shore up their panicky markets. Who will be the buyer? Yes of course, the Fed and only the Fed. It is my belief the Fed is about to be tested beyond breaking not only as lender of last resort but also “buyer of only resort” when it comes to the Treasury market. Liquidity is already quite tight world wide, can the Fed really exacerbate the situation by raising rates? Is any economy anywhere in the world strong enough to bare higher rates? Any financial system solid enough? I DARE THEM to raise rates…I bet they will be forced to do the opposite and pump unprecedented new liquidity!!

And now your overnight Monday morning trading in bourses, currencies, and interest rates from Europe and Asia:

1 Chinese yuan vs USA dollar/yuan remains constant at 6.2096/Shanghai bourse: red and Hang Sang: red

2 Nikkei down 37.13 or 0.18%

3. Europe stocks mostly in the green /USA dollar index up to 97.56/Euro down to 1.0946

3b Japan 10 year bond yield: rises to 42% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 124.29

3c Nikkei still just above 20,000

3d USA/Yen rate now just above the 124 barrier this morning

3e WTI 46.42 and Brent: 51.10

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund slightly rises to .65 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate falls to 21.340%/Greek stocks this morning: still expect continual bank runs on Greek banks /stock markets will be allowed to be open as per ECB but restrictions

3j Greek 10 year bond yield remains constant at : 12.12%

3k Gold at $1091.31 /silver $14.71

3l USA vs Russian rouble; (Russian rouble down 83/100 in roubles/dollar) 62.63,

3m oil into the 46 dollar handle for WTI and 51 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9669 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0596 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further away from negativity at +.65%

3s The ELA rose another 900 million euros to 90.4 billion euros. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.19% early this morning. Thirty year rate below 3% at 2.90% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Chinese Stocks Slide Again, Copper Tumbles To 6 Year Low; Greek Market Crashes After One Month Trading Halt

If China had hoped it would root out intervention by eliminating Citadel’s rigging algos, and unleash a buying spree it was wrong: the Shanghai Composite opened negative, and never managed to cross into the green, despite the usual last hour push higher, ending down -1.1% and down for 6 of the past 7 days.

Worse, the high-beta Chinext (Harvey: equals China’s Nasdaq) tumbled 8% from Friday’s late day highs upon opening. Surprisingly, this happened even as China’s final Caixin/Markit manufacturing PMItumbled to 47.8, the lowest since July 2013 as reported previously, a collapse which normally would have been very bullish for stocks as it guarantees even more PBOC intervention. The trouble is that with the PBOC losing the market’s faith, not to mention control, bad economic news are becoming even worse news for stocks.

Adding commodity insult to stock injury, earlier today copper plunged to a fresh 6 year low, and like crude, is back in its second bear market of the past year.

Elsewhere in Asia equities fell with Chinese bourses at the forefront in the wake of disappointing Chinese Official and Caixin Mfg PMI readings. Hang Seng (-0.9%) traded in negative territory as the poor data increased concerns over China’s growth with a PBoC official adding that downward economic pressures are ‘not small’ and further revealing China had fabricated its local government debt numbers. Nikkei 225 (-0.4%) and ASX 200 (-0.4%) fell, as mining and energy names felt the effects of weak commodity prices. JGBs were flat having initially opening higher following the gains seen in USTs, however later pared gains amid a mild bounce back in Japanese equities.

The real action, however, was not in Asia but in Europe, and specifically Greece, where the stock market finally reopened after a 1+ month “capital control” hiatus. Granted, numerous conditions still remained, such as no short selling, and extensive limitations to just what could be sold, but despite the attempt to micro manage the reopening, the result was not pretty, with stocks crashing 23% at the open and staging barely a rebound trading -17% as of this moment, even as banks promptly traded down to the -30% limit as the realization that an equity-eviscerating recapitalization (or bail-in) is now inevitable.

Worse, just as the Greek stock market reopened, the Greek Markit data and at 30.2, down from 46.9 the month before, the best reaction anyone could muster to this complete shutdown in the Greek economy was laughter. The chart below hardly needs commentary…

… but here is some anyway from Phil Smith, Economist at Markit:

“Manufacturing output collapsed in July as the debt crisis came to a head. Factories faced a record drop in new orders and were often unable to acquire the inputs they needed, particularly from abroad, as bank closures and capital restrictions badly hampered normal business activity.

“Demand was hit amid the heightened uncertainty surrounding Greece’s future, leading both total new business and exports to contract sharply, and it remains to be seen how long it takes these to recover.”

“Although manufacturing represents only a small proportion of Greece’s total productive output, the sheer magnitude of the downturn sends a worrying signal for the health of the economy as a whole.”

Don’t expect a quick rebound: Greek economic sentiment likewise tumbled, however it could be worse: unlike the unprecedented collapse in the PMI, this was only at a 3 year low:

The Greek pain was largely confined just to one country as European equities (Euro Stoxx: +0.2%) were bolstered during the European morning as a consequence of the better than expected PMI’s , while also benefiting from stock specific news, with earnings today generally better than expected, with , with HSBC (+0.6%) trading higher after their earnings.

Fixed income markets have seen tight price action in Europe with volumes starting the week in light fashion, while the Greek spread is tighter against its German counterparts on their reopening. Of note, seasonally we are entering the most bullish month of the year for bonds. Treasury Futures have been up 14 of the last 15 Augusts, and have averaged a 1.14% gain over the last 20 years . Interestingly, the curve continues to flatten, as 12-month yields hits a six-year high and 30-year yields touched a two-month low last week.

In FX, the week has kicked off with Manufacturing PM’s from around Europe and the UK, with the data generally better than expected (Eurozone Manufacturing PMI 52.4 vs. Exp. 52.2, UK Manufacturing PMI 51.9 vs. Exp. 51.5). However price action has been fairly muted, with both EUR and GBP down under 10 pips throughout the majority of the session against the USD, which trades flat on the day (USD-Index 0.0%).

Elsewhere the aforementioned lower than expected Chinese PMIs has weighed on AUD/USD to see the pair trade below the 0.7300 handle, while USD/CAD broke above the 1.3100 level to trade at its highest level in 10yrs amid CAD weakness after the commodity currency fell in sympathy with AUD and as a consequence of the ongoing commodity weakness.

Commodities have continued their recent decline this week with both the metals and energy markets experiencing weakness so far. As such, Brent Sep15 futures reside in close proximity to the USD 51.00 handle having earlier touched USD 50.85 , its lowest level since January, while gold remains firmly below the USD 1,100/oz handle amid fears of a China slow down and concerns around a Fed rate hike.

Overall, the story from last week remains the same: crashing commodity demand, sliding Chinese stocks, Europe treading water and ignoring what may still be Greek contagion for the broader economy, with the biggest wildcard now Friday’s US nonfarm payrolls report, which will either be a superstart and send 10Y yield soaring yet again, or confirm the record low ECI print last week and steamroll over the latest batch of Treasury shorts.

In summary: European stocks rise for fifth day while U.S. equity index futures decline with oil, gold. Asian stocks decline. Greek stocks on ASE Index paring losses after 23% drop in early trading; for list of halted Greek stocks, click here. European bourses outperforming include Netherlands, Spain, Germany. Yields on most euro-zone 10-yr notes fall; Italian yields rise. U.S. Markit U.S. manufacturing PMI, ISM manufacturing, construction spending, vehicle sales, personal income, personal spending due later.

Market Wrap

- S&P 500 futures down 0.1% to 2096.5

- Stoxx 600 up 0.4% to 398.1

- US 10Yr yield up 3bps to 2.21%

- German 10Yr yield up 3bps to 0.67%

- MSCI Asia Pacific down 0.8% to 141

- Gold spot down 0.2% to $1093.9/oz

- 15 out of 19 Stoxx 600 sectors rise; food, telecomms outperform; basic resources, autos underperform

Eurostoxx 50 +0.3%, FTSE 100 -0.2%, CAC 40 +0.1%, DAX +0.3%, IBEX +0.4%, FTSEMIB +0.2%, SMI +0.4% - Asian stocks fall with the CSI 300 outperforming and the Shenzhen Composite underperforming; MSCI Asia Pacific down 0.8% to 141

- Nikkei 225 down 0.2%, Hang Seng down 0.9%, Kospi down 1.1%, Shanghai Composite down 1.1%, ASX down 0.3%, Sensex up 0.4%

- German Carmakers to Buy Nokia’s HERE Maps for $3.1b

- Euro down 0.16% to $1.0966

- Dollar Index up 0.06% to 97.4

- Italian 10Yr yield down 1bps to 1.77%

- Spanish 10Yr yield up 9bps to 1.94%

- French 10Yr yield up 2bps to 0.96%

- S&P GSCI Index down 1.4% to 373.1

- Brent Futures down 2.2% to $51.1/bbl, WTI Futures down 1.7% to $46.3/bbl

- LME 3m Copper down 1.4% to $5158/MT

- LME 3m Nickel down 2.9% to $10725/MT

- Wheat futures down 0.9% to 494.8 USd/bu

Bulletin headline Summary from Bloomberg and RanSquawk:

- European equities were bolstered during the European morning as a consequence of the better than expected Manufacturing PMIs

- Today saw the Athens Stock Exchange open for the first time and immediately fell to around 20% in line with expectations

- Today sees US Personal Income, Real Personal Spending, Construction Spending and ISM Manufacturing as well as comments expected from Fed’s Powell

- Treasuries ease before reports on personal income and spending; rose Friday after 2Q ECI increased at slowest pace on record, curbing expectations Fed will begin raising rates in September.

- Caixin/Markit’s China PMI came in at 47.8, less than forecast; followed a reading of 50 for the official Purchasing Managers’ Index on Saturday, compared with analysts’ projections for 50.1

- The Shanghai Stock Exchange said on its microblog Monday that two trading accounts got verbal warnings for a “large amount of sell orders affecting security prices or volume”

- The bourse said the trading was “abnormal,” but didn’t give any details on the two accounts or indicate whether any laws were broken

- Greek stocks fell by as much as 23% as the market reopened after five weeks to the most savage wave of selling in decades, underlining a crisis that’s crippled the economy and pushed the country’s euro membership to the brink

- Obama will today finalize measures that force states and utilities to use less coal and more wind power, solar and natural gas; the plan is estimated to cost $8.4b and is among the most complex in agency history

- There’s been no respite in the commodity rout that’s seen prices tumble to a 13-year low — and that’s sending the currencies of nations that rely on exporting resources toward their worst year since the financial crisis

- Sovereign 10Y bond yields mostly higher. Asian stocks fall, European stocks gain, U.S. equity- index futures retreat. Crude oil, copper and gold lower

DB’s Jim Reid completes the overnight event wrap

With liquidity structurally lower in this cycle anyway, we could do without any big surprises. The main hurdle on this front this week could be US payrolls on Friday where we all have to make a judgement as to whether the report shows “SOME” improvement in the labour market. We still think its a big gamble to raise rates with the global data as it is and commodities and China/EM in a state of flux. Having said this if we get two decent payroll reports in the next 5 weeks then the trigger could very easily be pulled. As you’ll see in the week ahead there’s a lot of other data out this week but it will all reach a crescendo on Friday.

The heavy data week has started with the final reading of China’s Caixin manufacturing index falling short of the flash reading. The final read came in at 47.8 versus the flash of 48.2 and market expectations of 48.3. Accordingly to Bloomberg this marks the fifth consecutive month of contraction and puts the reading at its lowest since July 2013. This clearly does little to reverse what seems to be a broadening worry of Chinese economic slowdown which is also having a considerable impact on growth commodities. As we show in our July recap below it certainly has been a woeful month for these proxies.

As for markets, Asian investors are reacting negatively to the bad China print. In China, the Shanghai and Shenzhen bourses are down 2.4% and 2.9% respectively as we go to print (let’s see where they end the day!). Away from China, equity benchmarks in HK (-1.0%), Korea (-1.1%) and Japan (-0.4%) are also down as we write. Credit spreads are little changed in Asia while Oil markets are touch softer overnight. US Treasuries are about 2-3bp higher to 2.20% in 10yr yields to retrace some of the 8bp rally we saw on Friday.

The bond rally on Friday was helped by the data as the latest wage numbers in the US were soft. The US employment cost index in Q2 rose +0.2% qoq, its smallest increase since data started in 1982 and also fell short of +0.6% qoq expected by the market. Our economists noted that this brings annual labour cost inflation back to 2.0% yoy – which was where it stood a year ago.

Data aside it was also a rather soft finish for US equities on Friday. The S&P 500 fell -0.23% not helped by some weaker energy sector earnings. A Baker Hughes report which noted that the number of US oil rigs count rose for its second consecutive week also did not help. Brent and WTI closed -2.0% and -1.4% lower, respectively. Brent and WTI were some of the worst performers in July (more below) and this capped a bad month. The downturn in commodity prices seems to be also affecting appetite for capex. Per the FT, S&P now expects that global capex will fall more than 10% this year and decline further in 2016 largely driven by belt tightening measures by commodity related sectors.

A quick recap of the current earnings season now. Over 330 US companies have reported so far and the trend is more or less similar to what we’ve been observing in the past. 74% of them have beaten EPS estimates but only 50% have beaten revenue forecasts. The trend is more balanced in Europe with about 63% and 65% of those that have reported so far beating EPS and revenue consensus, respectively.

Staying with Europe, today marks the reopening of the Athens stock exchange after a five week suspension while bailout talks continue. Local traders will be able to buy stocks, bonds, derivatives, and warrants under certain conditions. International investors won’t be restricted as long as they were active in the markets before markets were closed in June (Bloomberg). So it will be interesting to watch today.

end

Overnight, this very reliable indicator is signalling a total global collapse:

Something Just Snapped: Container Freight Rates From Asia To Europe Crash 23% In One Week

One of the few silver linings surrounding the hard-landing Chinese economy in recent weeks has been the surprising resilience and strength of the Baltic Dry Index: even as Chinese commodity demand has cratered in 2015, this “index” has more than doubled in the past few months from all time lows, and at last check was hovering just over 1,100.

Many were wondering how it was possible that with accelerating deterioration across all Chinese asset classes, not to mention the bursting of various asset bubbles, could global shippers demand increasingly higher freight rates, an indication of either a tight transportation market or a jump in commodity demand, neither of which seemed credible.

We may have the answer.

It appears that the recent spike in shipping rates was analogous to the dead cat bounce in crude oil prices: a speculator-driven anticipation for a sustainable rebound that never took place. And now, just like with crude prices, it is all crashing down…. again.

According to Reuters, shipping freight rates for transporting containers from ports in Asia to Northern Europe dropped 22.8 per cent to $400 per 20-foot container (TEU) in the week ended last Friday, data from the Shanghai Containerized Freight Index showed.

Freight rates on the world’s busiest shipping route have tanked this year due to overcapacity in available vessels and sluggish demand for transported goods. Rates generally deemed profitable for shipping companies on the route are at about US$800-US$1,000 per TEU. In other words, at current prices shippers are losing half a dollar on every booked contractual dollar at current rates.

According to Shanghai data, it was the third consecutive week of falling freight rates on the world’s busiest route.Container freight rates have so far increased in 5 weeks this year but fallen in 23 weeks.

In the week to Friday, container freight rates fell 24 percent from Asia to ports in the Mediterranean, fell 4.4 per cent to ports on the US West Coast and were down 3.7 per cent to ports on the US East Coast.

Maersk Line, the global market leader with more than 600 vessels and part of Danish oil and shipping group AP Moller-Maersk, was one of the few container shipping companies to make a profit last year. The company controls around one fifth of all transported containers from Asia to Europe.

Should the dead cat bounce in shipping rates indeed be over, and if the accelerate slide continues at the current pace, not only will shippers mothball key transit lanes, but the biggest concern for global economy, the unprecedented slowdown in world trade volumes, which we flagged a week ago, will be not only confirmed but is likely to unleash yet another global recession.

Unless, of course, central planners learn how to print trade and quite soon at that…

Citadel Barred From Trading In China After Regulator Accuses “Automated Trading” Unit Of Manipulation

Define irony: for the past 7 years, Wall Street’s worst kept secret is that Citadel, the world’s most levered hedge fund, has been the NY Fed’s just slightly more than arms-length enforcer of market stability, by which we mean spoofer, buyer and otherwise “plunge protector” in the equity and E-mini futures markets. The secret got even less “secret” when of all the possible hedge funds blogger Ben Bernanke could have gone to, he picked the Chicago HFT powerhouse, confirming the cozy and tight relationship between the Federal Reserve and the firm which has been increasingly linked to market manipulation not only in equities but bonds and virtually all other asset classes.

Which is why Citadel must have been shocked to learn late last week that China had suspended trading at a brokerage account used by Citadel in China.

When the news first broke last Friday, we asked, somewhat rhetorically, the following question:

Today, the WSJ had more detail on the surprising snafu involving the Fed’s favorite market intervention vehicle, confirming that Citadel said trading in one of its China accounts has been suspended, as Chinese regulators battle a steep slide in stock prices.

The reason: China’s securities regulator said Friday it has launched a probe into automated trading and has restricted 24 stock accounts suspected of influencing stock prices. The government didn’t name any of the companies behind the restricted stock accounts. Citadel said Sunday that one of its accounts was among them.

Of course, China’s crackdown on foreign trading is not news, and had been reported about a week ago: in its endless list of scapegoatees, China had decided that blaming “evil”, if faceless, foreign sellers would be just as effective to boost confidence in a rigged market as accusing “malicious” sellers. That remains to be seen, but what is surprising is that while Citadel is best known for propping the US market higher, China is suggesting that the same NY Fed Plunge Protection Team extension was implicated in the recent downward move, using “automated trading” or otherwise. Surely, China’s regulator would not utter a peep if like in the US, Citadel had been used to support stock prices.

In comments on its website, the China Securities Regulatory Commission said it is investigating more than 50 instances of suspected securities violations and broken promises not to sell down share holdings as the country’s stock markets plunged in June and July. It wasn’t immediately clear why Citadel’s account had been targeted.

WSJ quotes a Citadel spokesman who notes that “We can confirm that while one account managed by Guosen Futures Ltd.—Citadel (Shanghai) Trading Ltd.—has had its trading on the Shenzhen Exchange suspended, we continue to otherwise operate normally from our offices, and we continue to comply with all local laws and regulations.”

What a difference a year makes: recall that in May 2014, Citadel became only the first international hedge fund to complete yuan fundraising from Chinese wealthy individuals and companies through a local unit.

Citadel (Shanghai) Foreign Investment won regulatory approval for currency exchange on March 26, marking the first qualified domestic limited partner, or QDLP, to have successfully completed fundraising in China, according to a statement from the Shanghai government’s information office.

The irony:

China’s leaders have pledged to promote freer movement of capital in and out of the country and make the exchange rate more market-based for investment purposes. Shanghai started the QDLP program last year to allow international hedge funds to raise capital in the local currency in China for overseas investments, aiding the government’s experiment with capital account convertibility and advancing its plan to build Shanghai into a financial center.

Why irony? Because a little over a year later, we find out that China is only interested in “promoting freer movement of capital” as long as it involved its stock market going higher, and the capital flowing into China, not out of it at a record pace as we commented previously.

But still the question remains – how did Citadel attract attention to itself. The answer: “The firm has recently expanded its quantitative hedge funds there, and its securities trading business traded options this year in a trial program on the China Financial Futures Exchange.”

Chinese media reported over the weekend that one of the restricted accounts was co-owned by Citadel and major Chinese brokerage firm Citic Securities. Citic Securities said Sunday it invested in the account in 2010, but it sold off its stake in November 2014 and no longer owns stock in the account, according to China’s official Xinhua News Agency. Citic Securities didn’t immediately reply to a request for comment.

And while a Citadel spokesman didn’t respond to a request for comment on which side of the firm’s business was affected by the suspension, it appears that Citadel’s infatuation with market rigging via algos and “automated trading” is what set China off. Or rather the “selling” via automated trading.

Moments ago Bloomberg confirmed as much when it reported that an official Chinese regulator urges further algorithm trading regulation, adding that China should be prudent on developing algorithm trading, Shanghai Securities News cites an unidentified official with China Securities Regulatory Commission as saying.

Market stability were “seriously damaged” by algorithm trading combined with some abnormal trading activities, the official was cited as saying. Algorithm trading may lead to systematic risks and result would be catastrophic when algorithm trading was used to manipulate market, the official was cited as saying.

Why are none of these risks ever brought up vis-a-vis Citadel’s market manipulation in the US? The answer is glaringly simple: because in the US, unlike China, Citadel always manipulates the market higher.

Which leads to an even more interesting, follow up question: if Citadel’s HFT algos were indeed caught red-handed selling in China, then someone in the US must have given the local Citadel brokerage the green light to spoof Chinese stocks lower. And since by definition Citadel does not do anything market-moving without the Fed’s preapproval, one wonders if China’s paranoia that foreigners are eager to crush its market is not at least partially grounded in reality?

Greek Stocks, Economy Collapse, Suffer Worst Declines In History

The Athens Stock Exchange reopened on Monday and unsurprisingly, some folks were selling.

Trading was suspended five weeks ago after PM Alexis Tsipras’ dramatic midnight referendum call precipitated capital controls and a lengthy bank “holiday.” Shares opened lower by nearly 23% and the country’s banks traded limit-down, which makes sense because they are, after all, largely insolvent. Here’s NY Times:

The Athens Stock Exchange plunged 22.8 percent when it reopened on Monday after a five-week shutdown imposed by Greek authorities as part of efforts to prevent a financial collapse.

Bank stocks, which are particularly vulnerable as Greek lenders are set for new recapitalization in the coming months, took a battering, falling by as much as 30 percent.

Although foreign investors face no restrictions in the Athens exchange, local traders can only use existing cash holdings to buy shares; they are prohibited from tapping local bank deposits to buy shares as the authorities seek to prevent capital flight.

Asked about the harrowing decline, European Commission spokeswoman Mina Andreeva had no comment but did say that Brussels has “taken note” of the reopening. Amusingly, she also said the decision was made by “competent” Greek officials. A ban on short-selling was due to expire on Monday but will be extended, an unnamed official told Reuters.