Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1090.70 up $1.30 (comex closing time)

Silver $14.55 up 3 cents.

In the access market 5:15 pm

Gold $1087.80

Silver: $14.60

First, here is an outline of what will be discussed tonight:

At the gold comex today, we had a good delivery day, registering 84 notices for 8400 ounces Silver saw 1 notice for 5,000 oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 235.52 tonnes for a loss of 67 tonnes over that period.

In silver, the open interest rose by 2,736 contracts despite the fact that silver was down by 23 cents yesterday. The total silver OI continues to remain extremely high, with today’s reading at 188,662 contracts In ounces, the OI is represented by .9430 billion oz or 135% of annual global silver production (ex Russia ex China). This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end as they continue to raid as basically they have no other alternative.

In silver we had 1 notice served upon for 5,000 oz.

In gold, the total comex gold OI rests tonight at 435,095. We had 84 notices filed for 8400 oz today.

We had no withdrawals in gold tonnage at the GLD today / thus the inventory rests tonight at 672.70 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. I thought that 700 tonnes is the rock bottom inventory in GLD gold, but I guess I was wrong. However we must be coming pretty close to a level of only paper gold and the GLD being totally void of physical gold. In silver, we had a small change in silver inventory at the SLV,a withdrawal of 478,000 oz / Inventory rests at 326.351 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver rose by 2736 contracts up to 188,662 even though silver was down in price by 23 cents yesterday. The OI for gold rose by 6863 contracts to 441,958 contracts despite the fact that gold was down by $5.50. We still have over 22 tonnes of gold standing with only 11 tonnes of registered gold in the dealer vaults.

(report Harvey)

2. ONE big commentary from Bill Holter titled:

They will say “YOU WERE WARNED”!

(Bill Holter/Holter-Sinclair collaboration)

3. One important stories on Greece on the collapse of their banks

(zero hedge)

4.Gold trading overnight, Goldcore

(Stephen Flood/Mark OByrne)

5. Saudi Arabia invades Yemen

(zero hedge)

6. Dept of Justice in the USA launches another probe against Deutsche bank with respect to laundering of USA dollars

(zero hedge)

7. Japan’s real wages instead of rising, it plummets by 2.4% totally throwing cold water on Abenomics:

(zero hedge)

8 Six warning signs that the economy is in deep trouble

(Mauldin Economics/Sagami

9 Trading of equities/ New York

(zero hedge)

10. USA stories:

i) Data for today:

a) Gallup consumer spending report (down)

b) Factory orders down.

ii)

Fed governor Lockhart opens his mouth and states that September is the right time to raise interest rates

(zero hedge)

11. Steve St. Angelo delivers a terrific commentary on the rapidly depleting silver inventory at the Shanghai silver commodity exchange in Shanghai

(Steve St Angelo/SRSRoccoReport)

Here are today’s comex results:

The total gold comex open interest rose from 435,095 up to 441,958 for a gain of 6,863 contracts despite the fact that gold was down $5.50 yesterday. For the past two years, we have strangely witnessed two interesting developments with respect to the gold open interest: 1) total gold comex collapse in OI as we enter an active delivery month, and 2) a continual drop in the amount of gold standing in an active month, and today the latter was again the norm. What is interesting is that the LBMA gold is witnessing a 7.40 premium spot/next nearby month as gold is now in backwardation over there. We are now in the contract month of August and here the OI fell by 1401 contracts falling to 6,894 contracts. We had 256 notices filed upon on yesterday and thus we lost 1145 contracts or 114,500 ounces will not stand for delivery. The next delivery month is September and here the OI rose by 297 contracts up to 2290. The next active delivery month if October and here the OI rose by 496 contracts up to 25,690. The estimated volume on today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was poor at 139,721. The confirmed volume on yesterday (which includes the volume during regular business hours + access market sales the previous day was poor at 117,719 contracts. Today we had 84 notices filed for 8400 oz.

And now for the wild silver comex results. Silver OI rose by 2736 contracts from 185,926 to 188,662 contracts despite the fact that silver was down by 23 cents yesterday . We continue to have our bankers pulling their hair out with respect to the continued high silver OI as the world senses something is brewing in the silver arena. We are in the delivery month of August and here the OI fell by 29 contracts down to 60. We had 16 delivery notices filed yesterday and thus we lost 13 contracts or 65,000 ounces will not stand for delivery in this non active August contract month. The next major active delivery month is September and here the OI rose by 315 contracts to 120,937. The estimated volume today was fair at 33,052 contracts (just comex sales during regular business hours). The confirmed volume yesterday (regular plus access market) came in at 47,878 contracts which is excellent in volume. We had 1 notice filed for 5,000 oz.

August contract month: initial standing

August 4.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64.30 oz (,Manfra)2 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 84 contracts (8400 oz) |

| No of oz to be served (notices) | 6810 contracts (681,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 343 contracts(34,300 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 272,935.7 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposits

total dealer deposit: zero

total customer withdrawal: 64.30 oz

We had 0 customer deposits:

Total customer deposit: nil oz

We had 1 adjustments

i) Out of Scotia: 10,005.78 oz was adjusted out of the customer and this landed into the dealer account of Scotia

JPMorgan has only 3.098 tonnes left in its registered or dealer inventory.

.

Today, 0 notices was issued from JPMorgan dealer account and 12 notices were issued from their client or customer account. The total of all issuance by all participants equates to 84 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the August contract month, we take the total number of notices filed so far for the month (343) x 100 oz or 34,300 oz , to which we add the difference between the open interest for the front month of August (6894) and the number of notices served upon today (84) x 100 oz equals the number of ounces standing

Thus the initial standings for gold for the August contract month:

No of notices served so far (343) x 100 oz or ounces + {OI for the front month (6894) – the number of notices served upon today (84) x 100 oz which equals 921,200 oz standing so far in this month of August (22.24 tonnes of gold).

Thus we have 22.24 tonnes of gold standing and only 11.25 tonnes of registered or dealer gold to service it.

We lost 1145 contracts or an additional 114,500 oz will not stand for delivery in this active month of August. These were most likely cash settled.

Total dealer inventory 361,725.87 or 11.25 tonnes

Total gold inventory (dealer and customer) = 7,570,743.173 oz or 235.48 tonnes

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 235.48 tonnes for a loss of 67 tonnes over that period.

end

And now for silver

August silver initial standings

August 4 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | 85,818.470 oz (HSBC) |

| Withdrawals from Customer Inventory | 1,190,475.78 oz (CNT,HSBC) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,687.510 (CNT) |

| No of oz served (contracts) | 1 contract (5,000 oz) |

| No of oz to be served (notices) | 59 contracts (295,000 oz) |

| Total monthly oz silver served (contracts) | 18 contracts (90,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 85,818.47 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 2,380,951.6 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 1 dealer withdrawal:

i )out of HSBC: 85,818.470

total dealer withdrawal: 85,818.47 oz

We had 1 customer deposits:

i) Into CNT; 600,687.510 oz

total customer deposits: 600,687.510 oz

We had 2 customer withdrawals:

i)Out of HSBC: 590,534.38 oz

ii) Out of CNT 599,941.400 oz

total withdrawals from customer: 1,190,475.78 oz

we had 2 adjustment

Total dealer inventory: 55.764 million oz

Total of all silver inventory (dealer and customer) 173.954 million oz

The total number of notices filed today for the August contract month is represented by 1 contract for 5,000 oz. To calculate the number of silver ounces that will stand for delivery in August, we take the total number of notices filed for the month so far at (18) x 5,000 oz = 90,000 oz to which we add the difference between the open interest for the front month of August (60) and the number of notices served upon today (1) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the August contract month:

18 (notices served so far)x 5000 oz + { OI for front month of August (60) -number of notices served upon today (1} x 5000 oz ,= 385,000 oz of silver standing for the August contract month.

we lost 13 contracts or an additional 65,000 oz will not stand in this delivery month of August.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.comorhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

August 4.2015: no change in inventory/rests tonight at 672.70 tonnes

August 3.2015: no change in inventory at the GLD./Inventory remains at 672.70 tonnes

July 31/we had a huge withdrawal of 7.45 tonnes/Inventory rests this weekend at 672.70 tonnes

July 29/no change in inventory/rests tonight at 680.13 tonnes

July 28/no change in inventory/rests tonight at 680.13 tonnes

July 27/no change in inventory/rests tonight at 680.13 tonnes

July 24.2015/we had another massive withdrawal of 4.48 tonnes of gold form the GLD/Inventory rests at 680.13 tonnes.

July 23.2015: we had another withdrawal of 2.68 tonnes of gold from the GLD/Inventory rests at 684.63 tonnes

july 22/another withdrawal of 2.38 tonnes of gold from the GLD/Inventory rests at 687.31

July 21.2015: a massive withdrawal of 6.56 tonnes of gold from the GLD.

Inventory rests at 689.69 tonnes. China and Russia need their physical gold badly and they are drawing their physical from this facility.

July 2o.2015: no change in inventory

July 17./a massive withdrawal of 11.63 tonnes in gold tonnage tonight from the GLD/Inventory rests at 696.25 tonnes

July 16./we lost 1.19 tonnes of gold tonight/Inventory rests at 707.88 tonnes

August 4 GLD : 672.70 tonnes

end

August 4.2015: a small withdrawal of 476,000 oz of inventory at the SLV/Inventory rests at 326.351 million oz

August 3.2015; no change in inventory at the SLV/inventory remains at 326.829 million oz

And now for silver (SLV) July 31/no change in inventory/rests tonight at 326.829 million oz

July 29/no change in silver inventory/326.829 million oz

July 28/we had a huge withdrawal of 2.005 million oz from the SLV/Inventory rests at 326.829 oz

July 27/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 24/no change in silver inventory/inventory rests tonight at 328.834 million oz

July 23.2015; no change in silver inventory/rests tonight at 328.834 million oz

july 22/no change in silver inventory/inventory rests at 328.834 million oz.

July 21.we had a massive addition of 1.241 million oz into the SLV/Inventory rests tonight at 328.834 million oz.

Please note the difference between gold and silver (GLD and SLV). In GLD gold is being depleted and sent to the east. In silver: no depletions, as I guess this vehicle cannot supply physical metal.

July 20/no change

july 17.2015/no change in silver inventory tonight/inventory at 327.593 million oz

July 16./no change in silver inventory/rests tonight at 327.593 million oz

August 4/2015: tonight inventory rests at 326.351 million oz

end

And now for our premiums to NAV for the funds I follow:

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 11.4 percent to NAV usa funds and Negative 11.0% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 62.1%

Percentage of fund in silver:37.6%

cash .3%

( August 4/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to -.68%!!!! NAV (August 4/2015) (silver must be in short supply)

3. Sprott gold fund (PHYS): premium to NAV falls to – .90% to NAV(July August4/2015)

Note: Sprott silver trust back into negative territory at- 0.68%

Sprott physical gold trust is back into negative territory at -.90%

Central fund of Canada’s is still in jail.

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64)

Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis.

Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer.

Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer.

* * * * *

>end

And now for your overnight trading in gold and silver plus stories

on gold and silver issues:

(courtesy/Mark O’Byrne/Goldcore)

Gold Sentiment Is Just Ugly

The headlines are dramatic, ugly and depressing to anyone who holds gold right now. Broad market sentiment has shifted from disdain and dismissive to highly negative. Hedge funds are shorting gold aggressively, hedge funds that own gold are being “outed”. The market pundits are are sticking the proverbial knife in and twisting it with glee. The Financial Times published an interesting article over the weekend.

“Why gold has lost its shine for investors”

by Mohamed El-Erian. He is one of the world’s most respected investors and market commentators. In his piece he makes a number of interesting observations.

According to El Erian gold is falling because:

- In a world of ETFs investors can mange risk more effectively and therefore do not need a traditional safe haven such as gold.

- Gold does well in inflationary environments, we don’t have one right now, ergo, gold does poorly.

- Central banks are not buying gold as aggressively as they once did; lower demand, lower prices.

- Gold has not reacted as a safe haven as it should. Greece should have sent the price soaring but it did not.

- Official and institutional demand for gold has not materialised.

- Physical market demand at lower prices is not strong enough to create a firm bid for gold, there are not enough small guys in the market.

- Gold’s recent price move up $1,000 from $700 in 2008 was the outlier and not the norm and gold is now priced more correctly then it was then.

- But then he drops the biggest bomb of all. He states that gold could buck its recent trend and the reason he gives should give you all reason to take notice.

“This situation is unlikely to change soon but it need not be terminal. A shift would probably require a broader normalisation of financial markets, including a diminution in the direct and indirect role of central banks in determining asset prices and their correlations.”

Does this not strike you as a particularly insightful statement, from one of the world’s foremost investment minds no less?

I read it as follows, “the game is rigged until it is not rigged and then and only then will gold normalise to its true market value (straw poll please), as will other assets.”

Nearly all his previous points are rendered mute if in fact the market is rigged and we lack an effective fair price discovery mechanism.

The fact is the markets are massively dependent on central bank funding, central bank benchmark rates and central bank meeting minutes. The small matters of risk premia, allocations, efficiencies, debt levels, productivity, ROCE, even dividends are not so important any more. Just look at the rise of the Fed balance sheet and the S&P500. Literally, they are one for one.

Nope, its the unelected masters of the universe that now control the financial destiny of every human on the planet. Not one of them was ever elected. We are witness to the most extraordinary concentration of power that has ever existed, and our political representatives have allowed this to happen.

If you are foolish enough to trust in the markets’ internal risk pricing mechanism, efficient market theory, think again.

For example do a search on “Alladdin”. You will find that it is a centralised risk management service and asset manager monster that now controls a massive, circa $17 trillion, of the global capital market, or circa 8% of the world’s stocks, bonds and loans. 17,000 traders the world over rely on its risk models directly or partially.

We may all be witness to the first chapter of the MBA class of 2025’s required course “Failed Monetary Theories of the Last 100 Years”. Your grand kids may even ask you what it was like…. before the great reset.

Trust me this will get a lot worse before it gets better. I would wager that the central bank officials of the Fed and the BOE, BOJ and that intellectual vacant organisation that is the ECB, wear with great unease the new found power that they have.

If you need proof look at the number of market mechanisms that have been wholesale rigged for the past 15 years. These operators never operated in absolute secret. The watchers that watched knew and their silence implied unofficial sanction. Soon the banks again will be recapitalised, this time not with nameless tax payers but with your pensions and your savings. Bail-ins are coming, google “bail-ins” and read up.

Gold may well fall further in the near term and the powers that be may well keep the bus on the road for the near future, but if history teaches us anything is that you never bet against the wisdom of the crowd. Ultimately, these markets will be freed up and when they do gold will be bid up aggressively. On the other hand, the markets can stay irrational longer then you can stay liquid, so don’t put all your money into gold but do keep a small percentage (5% – 20%) and look at it as a firm of financial insurance. If it is falling in value then the rest of your assets should be rising and that is the essence of investing: asset diversification.

end

From the Kitco site: (notice that they are not allowed to say the word manipulation)

(courtesy Kitco.com)

Christensen: “The one bright spot for the precious metals market appears to be the physical market as the U.S. Mint reported a 469% increase in July coin sales, compared to last year.”

After that, Christensen talking to Hug: “It is not just the mint that has seenunprecedented demand for bullion as prices significantly dropped last month. In his morning commentary, Peter Hug, global trading director for Kitco.com said that many bullion dealers have been struggling to obtain a supply of silver coins and small gold bars. However, he added that he does not see this reemergence of physical bullion to help support prices as gold trades under $1,100 an ounce and silver under $15 an ounce.”

So, let me get this straight: the only bright spot for gold and silver is the huge demand for it????

Ladies and Gentlemen: we do not make this up!!

end

(courtesy Mike Kosares/USAGold.com/GATA)

Mike Kosares: The gold investment demand juggernaut

By Michael J. Kosares

USAGold.com, Denver

Monday, August 3, 2015

Whenever the mainstream media decides to undertake one of its periodic attacks on gold and gold ownership, it almost always begins by laying out gold’s long history as a proven inflation hedge. It proceeds to explain that inflation is not a problem at the present, and, as a result, no one with any common sense would bother to own it. This argument is a setup — a pretext meant to confuse investor thinking and redirect interest away from the one investment vehicle likely to do them some good in these uncertain times.

In mid-2007, the year the financial crisis began, gold was trading at $650 per ounce. As financial markets courted collapse in the following two years, gold rose steadily. By the time the global economy came up for air in late 2010, gold was trading at $1,400 per ounce and well on its way to an interim top of $1,900 in September, 2011. …

… For the remainder of the commentary:

end

(courtesy Chris Powell/GATA)

Is there any limit to creation of paper gold on the Comex?

3:32p ET Monday, August 3, 2015

Dear Friend of GATA and Gold:

A week ago the TF Metals Report disclosed that leverage in gold futures contracts on the New York Commodities Exchange had reached 116 times the metal available for delivery:

http://www.gata.org/node/15598

Today Zero Hedge reports that the leverage is up to 124 claims per ounce. Zero Hedge’s report is headlined “Comex On The Edge? Paper Gold ‘Dilution’ Hits a Record 124 for Every Ounce of Physical” and it’s posted here:

http://www.zerohedge.com/news/2015-08-03/comex-edge-deliverable-gold-dro…

Zero Hedge suspects that the growing leverage signifies that refugees from China’s stock market are frantically reaching out for golden insurance, and wonders about a default on Comex gold contracts.

Since the JPMorganChase gold vault seems to be connected to the gold vault of the Federal Reserve Bank of New York, your secretary/treasurer isn’t sure that the Comex leverage figure means all that much. For if the United States is prepared to compromise all the gold it holds in custody for foreign governments, the gold futures price well could go to zero.

Indeed, gold now is priced substantially below its cost of production mainly because Western central banks and their bullion bank agents have figured out how to make metal appear to be in many places at once, perhaps in as many as 124 places. That gold mining company shares continue their fall toward zero suggests that investors figure that no one ever again will need actual metal, at least not for investment purposes, and that the gold mining industry, remaining silent amid the overwhelming evidence of surreptitious central bank intervention in the gold market, has agreed to die quietly and thus truly is worth nothing.

The TF Metals Report last week may have posed the crucial question: What’s to stop Comex gold contract leverage from going to 200 times or even 500 times the metal available for delivery?

If there’s anything to stop that, it won’t be the World Gold Council or mainstream financial journalism.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATa.org

end

(courtesy James Turk/Kingworldnews/Eric King)

Despite media’s propaganda, gold has performed well in Europe, Turk tells KWN

9:05p ET Monday, August 3, 2015

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk tells King World News tonight that despite the mainstream financial news media’s ever-intensifying propaganda against gold, the monetary metal has been performing well in Europe, protecting the wealth of Greeks who own it and providing superior returns against the euro. An excerpt from Turk’s interview is posted at the KWN blog here:

http://kingworldnews.com/propaganda-greece-gold-and-are-people-really-pr…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Why you own gold

(courtesy Simon Black/Sovereign Man Blog)

Some Clear Thinking About The Price Of Gold

Submitted by Simon Black via Sovereign Man blog,

On April 2, 2001, the price of gold closed the market trading session at $255.30.

And that was the lowest price that gold has seen ever since.

In US dollar terms, gold closed the 2001 calendar year higher than it did in 2000. Then it did the same thing again in 2002. And again in 2003.

In fact, after reaching its low in April 2001, gold closed higher for twelve consecutive years– something that had never happened before in ANY financial market with ANY asset.

Then came a correction; the price started falling, and gold is now on track for 2015 to be its third down year in a row.

What’s incredible is that, despite its history of gains, and 5,000 years of tradition behind it, gold is rapidly becoming one of the most widely despised assets.

But before we pronounce it dead and write the final gold eulogy, however, let’s consider the following:

1) Nothing goes up (or down) in a straight line. After 12 straight years of unprecedented gains with any asset class, it’s not unusual to have a meaningful correction.

(Just imagine how severe the correction in stocks will be. . .)

And like all frantic booms which go way past sustainable levels, corrections also overshoot fair value.

This correction in the gold market could easily last for several more years, with prices potentially well below $1,000.

But then we could just as easily see another massive surge all the way past $2,000 and beyond.

That’s the nature of these markets– to be extremely fickle (and highly manipulated).

Even over a period of a few years, the market can show about as much maturity as a middle school lunchroom, complete with pubescent gossip and inane popularity contests.

But it’s rather short-sighted to completely lose confidence in an asset that has a 5,000 year track record because of a few down years.

2) The gold price shed nearly 5% after the government of China announced recently that they owned 1,658 metric tons of gold.

This amount was lower than what many investors and analysts had been expecting, and the price of gold dropped as a result.

My question- since when did anyone start believing official reports from the Chinese government?

Seriously. The Chinese have a vested interest in understating their gold holdings.

They know that doing so will push the price of gold LOWER, which is exactly what they want.

China is sitting on trillions of dollars in reserves right now, a portion of which they’re rapidly trying to rotate OUT of US dollars.

So it’s clearly beneficial to the Chinese government if they can sell dollars while they’re strong and buy gold while it’s cheap.

And if they can push gold to become cheaper, even better for them.

3) Remember why you own gold to begin with.

Gold is a very long-term store of value. Notwithstanding a few down years, gold has maintained its purchasing power for thousands of years.

Paper currencies come and go. They get devalued, revalued, and extinguished altogether.

How much would you be able to buy today with paper money issued by the 7th century Tang Dynasty? Nothing. It no longer exists.

Or a pound sterling from 1817? Very little. It’s barely pocket change today.

Yet the gold backing up that same pound sterling from 1817 is worth over $250 today (165 pounds).

Even in modern history, the gold backing up a single US dollar from 1971 is worth vastly more than the paper currency that was printed 44 years ago.

But even more importantly, aside from being a long-term store of value, gold is a hedge— a form of money that acts as an insurance policy against a dangerously overleveraged financial system.

How much will your dollars and euros buy you in the event of real financial calamity? Or if there’s a major government default or central bank failure?

No matter what happens in the financial system– whether it collapses under its own weight, or cryptofinance technology revolutionizes how we do business– gold ensures that you’re protected.

4) Resist the urge to value gold in paper currency.We all have this tendency– we invest in something, and then hope it goes up in value.

But that’s a mistake with gold. It’s a hard thing for some people to do, but try to stop yourself from thinking about gold in terms of its paper price.

(It’s also important to remember that there’s a huge disconnect between the ‘paper price’ of gold, and the physical price of gold.)

Remember, gold is not an investment; there are plenty of better options out there if you’re looking for a great speculation.

So the notion of trading a stack of paper currency for gold, only to trade the gold back for a taller stack of paper currency misses the point entirely.

5) Having said that, if you find it too difficult to do this, and you catch yourself constantly refreshing the gold price and checking your portfolio, you might own too much.

Listen to your instincts; if you’re always feeling frantic about the daily gyrations in the market, lighten your load.

Don’t love anything that won’t love you back. Stay rational. Own enough gold that, in the event of a crisis, you will feel comfortable that you have enough ‘real savings’… but don’t own so much that you’re constantly worrying about the paper price.

SHANGHAI SILVER STOCKS PLUMMET: More Signs Of A Global Run On Silver?

Filed in News, Precious Metals by SRSrocco on August 4, 2015

There seems to be more evidence indicating the beginning stages of a global run on silver. How so? Well, ever since the middle of June, something significantly changed in the silver market. Physical silver investment demand skyrocketed. Why June? This was at the time Greece was voting on whether or not to remain in the European Union.

Since the middle of June, investment demand for silver has increased considerably. Matter-a-fact, the U.S. Mint suspended sales of the Silver Eagle for two weeks starting on July 12th. When Silver Eagle sales resumed on July 27th, over 2.5 million were sold over the next two days.

Furthermore, the Royal Canadian Mint has put its Gold and Silver Maple Leaf sales on allocation to its Authorized Participants. In addition, India has imported a record 3,824 metric tons (mt) in the first six months of the year. This is up 35% compared to the same time last year. And according to theBankBazzar.com July 28th press release:

Generally, as far as market observation goes, silver imports rise in the second half of the year. The rise in demand in August, is a result of the jewellery making and silverware industry, just before the festive season in Autumn as well as supplying for exports before Christmas.

So, if India imported a record 3,824 mt in the first half of the year, this will only increase in the second half as jewelry and silverware demand pick up considerably due to the festive season in the Autumn.

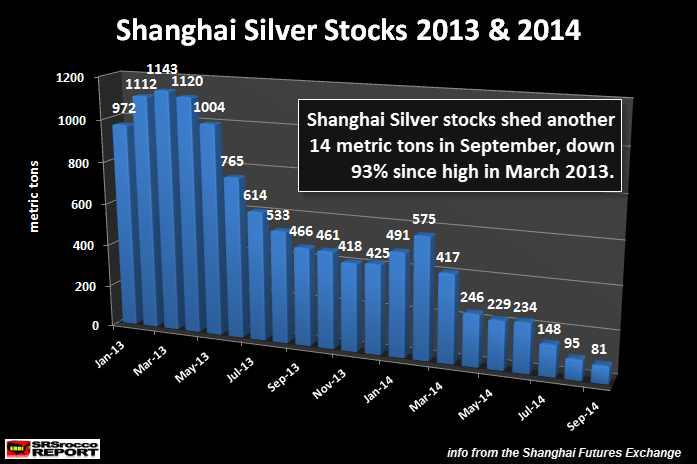

Another factor in a rise in global silver demand is the recent decline in silver stocks at the Shanghai Futures Exchange. Some of my readers have sent me emails stating, “Whatever happened to the silver stocks at the Shanghai Futures Exchange?” Well, let’s first look at my last update from September, 2014:

Shanghai silver stocks peaked in May of 2013 at 1,143 mt and fell to a low of 81 mt in September of 2014. Since the last update, silver stocks at the Shanghai Futures Exchange (SHFE) continued to slowly build until they reached a peak in the middle of June:

As we can see, SHFE silver warehouse stocks increased from 176 mt at the end of January to a peak of 394 mt on June 15th. However, silver stocks began to decline at the latter part of June, then plummeted in July falling 34% to 261 mt by the beginning of August.

And then we had this from a Money Metals Exchange article, Investment Silver Demand Draining COMEX Vaults:

One or more major players “jumped the queue” and took delivery of about 6.5 million more ounces of silver out of COMEX warehouses than anticipated at the beginning of the month.

The July data should send a shiver down the spine of anyone with a naked short position on silver, i.e. anyone who doesn’t have physical silver to deliver if a counter-party demands it. Short sellers are counting on being able to settle in cash – or grab silver bars from exchange vaults if necessary.

Mints Scouring America for Raw Silver

The big spike in investment coins, rounds, and bars is almost certainly behind the unusual delivery activity at COMEX warehouses.

Our sources indicate mint and refinery demand is largely responsible for this “jumping [of] the queue” and offtake of 1,000-ounce bars. The silver is needed for manufacturing into smaller retail products currently in very short supply.

Some major precious metals depots around the country, such as those in Los Angeles, completely ran out of all forms of pure silver last week, and mint owners are scouring the country to lock up the silver they need to keep production running.

Folks, we have to remember, this huge spike in physical silver demand is still from a fraction of investors. The only folks buying silver are either a few wealthy individuals (some who are finally waking up) and the diehard precious metals investors that make up 1-2% of the total investment market.

What happens when more wealthy individuals, institutions and the masses finally get on board? There just isn’t enough silver if any of these individual classes of investors wanted to purchase physical silver.

Lastly, physical silver investment demand continues to get stronger every year… even as the price declines. Savvy investors realize the Fed and Central Banks haven’t fixed anything so the day of reckoning is still coming. The situation today is is much different than the two and a half decade lull in silver prices after its meteoric rise in 1979.

The Fed and Central Banks had 35 years of rising global oil production to increase paper leverage and debt. Now that the world has plateaued in conventional oil production (U.S. shale oil peaked months ago), the peak and decline will wreak havoc on the world’s highly leverage paper Ponzi Scheme.

Investors better take notice in the huge increase of physical silver investment demand and market shortages as this will likely to only get worse in the future. Better to have your silver now, then wait until it’s nearly impossible to acquire.

end

They will say “YOU WERE WARNED”!

After the biggest financial and social crash in history occurs, “they” will say you were warned! Who are “they” and how exactly were we warned? For several years and in particular the last 12 months, the IMF (International Monetary Fund) and the BIS (Bank for International Settlements) have been issuing warning after warning. They have truly warned us as I will show you. Do I believe they did this out of the goodness of their hearts? No, I believe it has been in “c.y.a” fashion followed by their laughter because the sheep have and will sleep through it all until it’s too late.Thanks to Larry White from www.Lonestarwhitehouse.blogspot.com a full listing of the recent warnings has been compiled and logged. I had seen each one of these over the last year and have even commented on a couple of them but it never really registered with me there were so many. Normally I try not to “link” articles to death, this one is different because it is important you see how many and just how in depth the warnings have been! I will asterisk the three most important articles in my opinion, there have been 16 such warnings over the last 12 months!July 2014 – BIS –BIS Issues Strong Warning on “Asset Bubbles”July 2014 – IMF –Bloomberg: IMF Warns of Potential Risks to Global GrowthOctober 2014 – BIS –“No One Could Foresee this Coming”October 2014 IMF Direct Blog — What Could Make $3.8 Trillion in global bonds go up in smoke?October 2014 IMF Report –“Heat Wave”-Rising financial risk in the U.S.******** December 2014 – BIS –BIS Issues a new warning on markets

December 2014 – BIS —BIS Warnings on the U.S. Dollar

February 2015 – IMF – Shadow Banking — Another Warning from the IMF – This Time on “Shadow Banking”

March 2015 – Former IMF Peter Doyle – Don’t expect any warning on new crisis-Former IMF Peter Doyle: Don’t Expect any Early Warning from the IMF –

*******April 2015 IMF – Liquidity Shock –IMF Tells Regulators to Brace for Liquidity Shock

May 2015 BIS – Need New “Rules of the Game” –BIS: Time to Think about New Global Rules of the Game?

June 2015 BIS Credit Risk Report –BIS: New Credit Risk Management Report

June 2015 IMF (Jose Vinals) –IMF’s Vinals Says Central Banks May Have to be Market Makers

*******BIS June 2015 (UK Telegrahph, no blog article) –The world is defenceless against the next financial crisis, warns BIS

July 2015 – IMF – Warns US the System is Still Vulnerable (no blog article) –IMF warns U.S.: Your financial system is (still) vulnerable

July 2015 – IMF – Warns Pension Funds Could Pose Systemic Risk (no blog article) –IMF warns pension funds could pose systemic risks to the US

And there you have it in black and white! You have been warned! MANY TIMES in fact…and from the most inside and official of sources! Yet on a daily basis we hear from our own mainstream press, Washington and Wall St. …don’t worry be happy! These are very real articles with well thought out and cogent logic. They are not to be ignored!

One piece by the BIS last October talked about the “no one could have seen it coming” meme we heard so often back in 2008-09. THEY see it coming and have been telling you for over a year! Please understand this, the BIS is the central bank for central banks. No one knows the inside situation (particularly in derivatives) better than they do. If you don’t believe me or others who have worked so hard to get the warnings out, listen to what both the BIS and IMF are telling you. They have gotten out in front of this and will only say “we tried to warn you” after the fact.

Standing Watch,

Bill Holter

Holter-Sinclair collaboration

Comments Welcome! bholter@hotmail.com

And now your overnight Tuesday morning trading in bourses, currencies, and interest rates from Europe and Asia:

1 Chinese yuan vs USA dollar/yuan remains constant at 6.2095/Shanghai bourse: green and Hang Sang: red

2 Nikkei down 27.75 or 0.14%

3. Europe stocks all in the red /USA dollar index down to 97.33/Euro up to 1.0975

3b Japan 10 year bond yield: rises to 42% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.93

3c Nikkei still just above 20,000

3d USA/Yen rate now just below the 124 barrier this morning

3e WTI 45.89 and Brent: 50.35

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund slightly rises to .62 per cent. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate falls to 20.940%/Greek stocks this morning down badly: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield remains constant at : 12.00%

3k Gold at $1091.17 /silver $14.54

3l USA vs Russian rouble; (Russian rouble down 15/100 in roubles/dollar) 62.77,

3m oil into the 45 dollar handle for WTI and 50 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9681 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0625 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving closer to negativity at +.62%

3s The ELA rose another 900 million euros to 90.4 billion euros. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.16% early this morning. Thirty year rate below 3% at 2.86% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Greek Banks Crash Limit Down For Second Day; China And Commodities Rebound; US Futures Slide

After a lukewarm start by the Chinese “market”, which had dropped for the past 6 out of 7 days despite ever escalating measures by Beijing to manipulate stocks higher, finally the Shanghai Composite reacted favorably to Chinese micromanagement of stock prices and closed 3.7% higher as Chinese regulators stepped up their latest measures by adjusting rules on short-selling in order to reduce trading frequency and price volatility, resulting in several large brokerages suspending short sell operations. At this pace only buy orders will soon be legal which just may send the farce of what was once a “market” limit up.

Elsewhere in Asia, equities traded mixed following a lackluster Wall Street close amid further declines in commodity prices, after Brent crude dropped below $50/bbl for the first time since January, only to rebound in overnight trade. ASX 200 (+0.3%) traded in the green with gains in financials offsetting losses seen in commodity names. Elsewhere, the Nikkei 225 closed lower by 0.1% while JGBs rose following the latest 10-yr auction which drew highest b/c since Jan with 10-yr yields at a 9-week low.

Speaking of “buy only” trading, Greece may want to consider that soon because on the second day after reopening its market for trading, Greek banks traded limit down for the second day in a row. End result: banks such as Piraeus is now down over 50% in two days.

The reason: the same one we explained in “Greek Banks Just Became A “Strong Sell” At Any Price” – a recapitalization and an equity wipe out are now virtually assured, In fact, judging by the amount of jawboning against it, as seen by these headlines that hit the BBG tape moments ago…

- GREEK BANKS SAID TO SEE DEPOSIT INFLOWS SINCE JULY 20 REOPEN

- GREEK BANKS’ STRESS TEST TO BE COMPLETED BY END-OCT: OFFICIAL

- GREEK DEPOSITORS WILL NOT BE BAILED-IN: CENTRAL BANK OFFICIAL

… a bail in of depositors is also practically assured. Only this time anyone who puts their money in the bank really has nobody but themselves to blame.

Elsewhere, the energy sector continues to underperform despite the complex seeing a mild turnaround with Brent and VVTI Sep’15 futures both in the green, with the former retaking $50.00 handle. The European morning has seen Brent Crude pare some of its recent losses to rise above $50 heading into the NYMEX pit open, with WTI following suit and also residing in firm positive territory on the session . The metals complex have also seen a modest bout of strength during European hours, with gold trading higher by around $5.00 at USD 1090, while platinum and palladium are both off their multi year lows, with platinum earlier reaching its lowest level since 2009 and Palladium reaching its lowest level since 2012.

Brent oil, which has slumped more than 20 percent over the last month, was up almost 1 percent. Copper seen as a bellwether of global growth, nudged off a six-year low.

The dollar also helped relieve the pressure, with it pegged back by another bout of weak U.S. data on Monday. Raw material reliant Canadian and Australian dollars both got lifts, alongside Russia’s rouble and other emerging FX.

The Aussie dollar was by far the biggest mover. It rose 1.25 percent to an almost two-week high of $0.7375 after a major change in tone from its central bank that suggested it was now more satisfied with the currency level. “You have had a key shift from the RBA that they don’t need to intervene as strongly, so that has triggered a considerable Aussie bounce,” said John Hardy, head of FX strategy at Saxo Bank.

“And the (U.S.) dollar view is just flat and we are just waiting for payrolls on Friday. We have had a relatively hawkish set-up from Yellen and co (that interest rates may go up next month) but the rates market just doesn’t believe it.”

European Equities reside in mixed territory (Euro Stoxx: -0.3%) heading into the North American crossover, with financials the worst performing sector after Credit Agricole (-9.5%) reported earnings pre-market and announced that they are delaying structural reforms.

Bunds reside in positive territory albeit off their best levels, gaining amid the weakness in equities, while the German curve has flattened in line with the post FOMC trend, following the trend set in USTs. While also of note, the ECB announced further QE details yesterday, which showed extending maturities in German debt. Bunds also took out yesterday’s highs to reach their highest level since May 29th before paring some of these gains amid profit taking with macro news flow fairly light, while the UK 30Y also reached 2.5%, its highest level since April before the weak UK Auction (b/c 1.37, Prey. 1.54, tail 0.4bps, Prey. 0.2bps) saw a weakness in UK fixed income products.

In FX, AUD was the notable outperformer after the RBAdropped comments that a further fall in AUD is ‘likely and necessary’, with the central bank leaving rates unchanged, while Australian retail sales (0.7% vs. Exp. 0.4%) and trade balance data both beat expectations. Meanwhile the USD (USD-Index: -0.1%) remains relatively flat today amid a tight range in major pairs.

The notable tier one data from the European morning saw UK Construction PMI (57.1 vs. Exp. 58.5) print its lowest figure since May, but fail to have a sustained affect in GBP. Also of note, the Greek finance and economy ministers are set to meet the Quadriga (Troika + ESM) regarding bank recapitalisation and privatisation.

Looking ahead, today’s highlights include US ISM New York, factory orders and IBD/TIPP economic optimism, Canadian Manufacturing PMI and New Zealand unemployment.

In Summary: European shares decline, though pare the worst of earlier declines as U.S. equity index futures also slip. Asian shares gain. Oil rises for first day in 4. Gold, silver rise with metals, food commodities, cotton, while platinum, palladium fall. Italian, Spanish stocks among largest underperformers in Europe. Yields on eurozone 10-yr notes fall; dollar also declines. U.S. ISM New York, factory orders, IBD/TIPP economic optimism, due later.

Market Wrap

- S&P 500 futures down 0.1% to 2089

- Stoxx 600 down 0.2% to 398.5

- US 10Yr yield up 1bps to 2.16%

- German 10Yr yield down 2bps to 0.61%

- MSCI Asia Pacific up 0.3% to 141.5

- Gold spot up 0.4% to $1091.1/oz

- Eurostoxx 50 -0.2%, FTSE 100 +0.3%, CAC 40 -0.2%, DAX +0%, IBEX -0.4%, FTSEMIB -0.8%, SMI +0.1%

- Asian stocks rise with the Shenzhen Composite outperforming and the Sensex 30 underperforming; MSCI Asia Pacific up 0.3% to 141.5

- Nikkei 225 down 0.1%, Hang Seng down 0%, Kospi up 1%, Shanghai Composite up 3.7%, ASX up 0.3%, Sensex down 0.4%

- Apollo Buys Spain’s Lico Leasing From Fortress: El Confidencial

- Euro up 0.18% to $1.097

- Dollar Index down 0.14% to 97.36

- Italian 10Yr yield down 4bps to 1.74%

- Spanish 10Yr yield down 4bps to 1.91%

- French 10Yr yield down 3bps to 0.91%

- S&P GSCI Index up 1% to 372.3

- Brent Futures up 1.4% to $50.2/bbl, WTI Futures up 1.5% to $45.9/bbl

- LME 3m Copper up 0.3% to $5236/MT

- LME 3m Nickel up 1.3% to $10885/MT

- Wheat futures up 1.1% to 504.5 USd/bu

Bulletin Headline Summary from Bloomberg and RanSquawk

- Treasuries drift lower as commodities recover from yesterday’s rout; markets wait for ADP tomorrow, nonfarm payrolls Friday for clues on Fed’s next move; data calendar light, with Factory Orders at 10am.

- European Equities reside in mixed territory heading into the North American crossover, with financials the worst performing sector, weighed on by Greek banks and Credit Agricole, who reported earnings pre-market

- AUD is the notable outperformer after the RBA dropped comments that a further fall in AUD is ‘likely and necessary’, with the central bank leaving rates unchanged

- Oil and industrial metals led a rebound in commodities, boosting Russia’s ruble as emerging-market currencies rallied and supporting shares of raw-material producers

- Stocks in Athens fell almost 5%, extending biggest slump since at least 1987 as the nation seeks a return to normal after a five-week shutdown of its exchange; Piraeus Bank SA slumping 30%, while National Bank of Greece SA tumbled 29%

- Daniel Yu, best known for betting against companies via his short-selling firm Gotham City Research LLC, says he’s waiting in the wings for Greece to leave the euro – so he can start buying

- Puerto Rico’s debt crisis escalated as it suspended deposits into a fund that pays its general-obligation bonds and one of its agencies defaulted for the first time, jeopardizing the cash-strapped government’s ability to raise money

- Indian central bank Governor Raghuram Rajan kept interest rates unchanged, rebuffing pressure from the Finance Ministry to reduce borrowing costs that are among the highest in Asia

- Aetna Inc. raised its full-year earnings forecast after reporting profit that topped analysts’ estimates as it added more members in government insurance programs

- Sovereign 10Y bond yields mixed. Asian stocks mixed, European stocks, U.S. equity-index futures fall. Crude oil, copper and gold rise

DB’s Jim Reid completes the overnight event recap

Commodities continue to be the main game in town at the moment with the highlight being Brent (-5.15%) hitting 6 month lows yesterday at $49.52/bbl. This helped send 10 year Treasuries to two-month lows at 2.149% (-3.2bps) while Fed Funds contracts fell for a second consecutive session with the Dec15 (-0.5bps), Dec16 (-2.5bps) and Dec17 (-4.0bps) contracts down to 0.300%, 0.960% and 1.555% respectively. Despite some resilience, US equity markets succumbed to the sell-off in energy stocks with the S&P 500 eventually finishing -0.28% with the energy component tumbling 2% as some of the larger cap names including Chevron (-3.25%) and Exxon Mobil (-1.45%) led the move lower.

China’s soft PMI numbers from the weekend and yesterday, as well as the latest ISM numbers out of the US didn’t help but it was supply noise out of Iran where the bulk of the blame was centered. Iran’s Oil Minister, speaking on Sunday, said that production out of the country can increase by as much as 500k barrels a day within a week after sanctions end and by 1m barrels a day within a month following that. The Minister added that he expects sanctions against the country to be lifted by late November.

Talking of Iran, I was reading over the weekend that the country has been enduring a ‘heat dome’ with a heat index of 72C (162F) which measures heat and humidity and is kinda the opposite of the wind chill factor reading (ie how warm/cold it actually feels). Such a number is extraordinary and reflects a heatwave in the region. I’ve cooked pizzas at lower temperatures than this!! I showed this article to my wife who at the moment is struggling when it gets above 18 degrees and she nearly had a funny turn just reading it.

Once again it wasn’t just Oil markets where we saw weakness yesterday with most of the commodity complex enduring another tough session. In the metals space Gold (-0.82%), Silver (-1.79%) and Platinum (-2.22%) tumbled while Aluminum (-0.37%) and Copper (-0.19%) followed suit. Commodity sensitive currencies also felt some of the pain yesterday too with the Aussie Dollar (-0.30%), Russian Ruble (-2.84%), Norwegian Krone (-0.90%) and Canadian Dollar (-0.52%) some of the notable movers.

Staying on credit, DB’s Oleg Melentyev touched upon the latest moves in US credit markets on the back of the recent fall in oil in a note at the back end of last week. Oleg noted that last week we saw US HY energy spreads touch their peak levels from mid-December of last year (860bps) and that that weakness has now extended to metals where spreads are now at their widest level since the 2011-2012 peaks. Interestingly, Oleg notes that cross-asset volatility has experienced its biggest drop since October in recent weeks despite the weakness in commodities. The fall has come since the resolution in Greece in mid-July and right around the time of the commodity-driven widening in HY resulting in the regression-estimated HY spread being materially inside of its actual values (50-75bps depending on the time horizon) for the first time since December 2014. Oleg notes that, absent any meaningful bouts in volatility higher in the coming days and weeks, this should help encourage a rebound in US credit. However this hasn’t yet convinced Oleg that it’s a good enough reason to tighten spread target levels. In particular he notes of material headwinds from commodities, EM, rising credit risks and deteriorating issuer fundamentals which muddles the picture leaving him predisposed to keep existing longer term spread targets in place.

Looking at how markets in Asia are trading this morning, it’s been another choppy session in China but bourses are in positive territory as we hit the midday break with the Shanghai Comp (+1.34%), Shezhen (+1.76%) and CSI 300 (+1.16%) all up, supported in part by news on Reuters that the Shanghai and Shezhen bourses are cracking down on short-selling. The new rules are restricting the ability for day-traders to short-sell, forcing investors now into a T+1 settlement and so mitigating intraday volatility. Elsewhere this morning the Kospi (+0.50%) and ASX (+0.32%) are also up, however it’s a weaker start for the Nikkei (-0.20%) and Hang Seng (-0.13%). It’s been a much quieter session for commodities meanwhile. Brent (+0.34%) and WTI (+0.71%) have recovered slightly while Gold (-0.19%) is modestly lower. Asia and Australia credit markets are +2bps and +1bp respectively. The RBA have left rates unchanged as we go to print.

Back to yesterday, data in the US, which along with the moves in Oil, helped support the move lower in yields. Despite no change in the final July manufacturing PMI reading of 53.8, the ISM manufacturing reading for the same month attracted some disappointment with the print falling 0.8pts to 52.7 (vs. 53.5 expected) with employment, export orders and order backlogs components all falling. The ISM prices paid print was also disappointing, falling 5.5pts to 44.0 (vs. 49 expected). Construction spending data for June was the other notable disappointment yesterday, with just a +0.1% mom rise during the month versus expectations of +0.6%, the smallest monthly increase since January although we did see a reasonable upward revision to the May print (+1.8% from +0.8% previously). Elsewhere the June personal spending print of +0.2% mom was as expected while the personal income reading print came in a touch ahead of consensus (+0.4% mom vs. +0.3% expected). In terms of the PCE readings the deflator was as expected at +0.2% mom for June, although the annualized rate ticked up a notch to +0.3% yoy (from 0.2%). The core was also as expected for the month at +0.1% mom, keeping the annualized rate unchanged at +1.3% yoy. Finally July vehicle sales rose to a slightly firmer than expected 17.46m saar pace (vs. 17.20m expected), up a touch from June.

It was a quieter session on the earnings front yesterday with just a post-market beat from AIG the notable report yesterday. At the latest count of 370 S&P 500 companies having now reported, both earnings and sales beats are unchanged versus yesterday’s tally at 74% and 50% respectively. Over in Europe meanwhile, the trend has also remained unchanged at 63% and 65% respectively.

Elsewhere in the US yesterday we also saw the latest Fed Senior Loan Officer Opinion Survey on Bank Lending which showed that on the whole banks reported little change in their standards on commercial and industrial and commercial real estate loans, while on the household side the survey suggested that banks have reported a slight easing of lending standards for a number of residential mortgage loans over the past three months.

Moving on, Puerto Rico attracted its fair share of attention yesterday after halting payments into a fund used to cover its general obligation debt and as a result defaulting on a $58m bond payment. The default looks likely to be the trigger to start a restructuring of Puerto Rico’s roughly $72bn debt load with the WSJ noting that a group of policy makers are working on a restructuring plan and are due to present their findings at the of the month.

In the European session yesterday there was much focus on the reopening of the Greek stock market after a five-week closure. The ASE closed the session down 16.23% having initially plunged as much as 25% with banks (-26%) unsurprisingly leading the move lower. Elsewhere it was actually a fairly constructive day for European markets, offsetting a weak start on the back of the China data to close in positive territory with earnings reports from Heineken, Commerzbank and TomTom in particular helping sentiment. The Stoxx 600 (+0.77%), DAX (+1.19%) and CAC (+0.75%) all enjoyed their fifth consecutive daily gain. A 0.2pt upward revision to the final Euro area manufacturing PMI print to 52.4 in July only helped support a better tone in the European session yesterday. Regionally Germany (+0.3pts to 51.8) and Italy (+1.2pts to 55.3) were both revised up, with France unchanged at 49.6 and Spain (-0.9pts to 53.6) falling. In the UK the print was revised up 0.5pts and above expectations to 51.9. It was a much more mixed session in the European sovereign bond market. 10y Bunds eventually closed 1.6bps lower in yield at 0.627% as the US session kicked in while Gilts closed 1.5bps lower. The periphery was generally a basis point wider. Elsewhere the Euro closed down 0.3% versus the Dollar, not helped by the news that S&P has revised the outlook on the European Union to Negative from Stable (at AA+) on the expectation that the EU will provide first-loss guarantee support for financing connected to the Juncker Plan as well as the repeated use of its balance sheet to provide higher-risk financing to EU member states.

Taking a look at today’s calendar now, data-wise June factory orders is the highlight in the US while the ISM New York and IBD/TIPP economic optimism survey are also due. Earnings season continues meanwhile with Walt Disney and CVS Health Corp two of the notable reporters.

Greek Bank Stocks Crash Again Amid Fresh Signs Of Economic Disintegration

After trading limit-down on Monday when Greek stocks opened for trading for the first time since PM Alexis Tsipras called a referendum that would later prove to be a complete waste of time, shares of Greek banks once again flirted with the daily 30% loss limit on Tuesday as there were simply no bids for a set of institutions that everyone knows is insolvent.

The banks, which are only operational because the ECB has decided to keep the ELA liquidity drip on at least until the central bank sees whether or not Greece will be able to make a €3.2 billion bond payment on August 20, are in desperate need of recapitalization, and according to Brussels’ estimates, will need somewhere on the order of €25 billion to stabilize the system.

Of course that total effectively grows by the day, as the collapsing Greek economy (and we mean “collapsing” in the most literal sense of the word after yesterday’s astonishingly bad PMI print) takes its toll, driving up NPLs in a vicious circle wherein capital controls meant to stem the deposit outflow cripple the economy which in turn serves to further cripple the banks.

Speaking of this self-feeding loop, here’s Kathimerini with more on how the banking sector deep freeze has reverberated through the broader economy:

The state’s losses from indirect taxes alone in the first couple of weeks of capital controls and the shuttering of banks is more than half a billion euros, according to a study published on Monday by the Hellenic Confederation of Professionals, Craftsmen and Merchants (GSEVEE).

The drop in consumption in the first two weeks after June 28 amounted to 50 percent, or 3.8 billion euros, with corporate turnover falling 48 percent on average. This meant the state coffers missed out on 570 million euros in taxes.

Nine out of 10 enterprises reported a decline in turnover, with three in 10 seeing a drop of at least 70 percent.

The medium-term impact will be more serious, argued the report, as it is unknown for how long the capital controls will remain in place, and small and medium-sized enterprises are in a difficult position as the measures came during a period when they were completely defenseless.

Meanwhile, Greek FinMin Euclid Tsakalotos is meeting with the country’s creditors today to discuss the recap effort. Here’s Kathimerini with that story (Google translated):

The issue of recapitalization also becomes urgent, given that the aim is the share capital increases of the four systemic banks to be completed in October. The timetable provides that the details of the stress test (under way) will be known on September 4, and, based on them, they will proceed with the recapitalization, which will require at least 10 billion. However, the final amount will depend on the assumptions to be adopted in the stress test, the most important is the economic downturn and the duration will, handling deferred tax and the management of non-performing loans.

Japan’s Real Wages Just Plunged The Most In Six Years

When it comes to Japanese wage data, that weakest link of Abenomics simply because real wages haven’t grown in 24 consecutive months – and without wage growth no economy can ever possibly grow – there is little to add to what we said previously: all the data is not only fabricated, but manipulated to comply with policy. Recall our post from April in which we exposed just how Japan’s Monthly Labor Survey adjusted all historical data so that the “rising” wages into Japan’s election were subsequently revealed to be a lie and in fact Japan never had a single month of rising base wages in 2014!

Since then the Japanese department of data fabrication has gone “full Chinese” and last month, the wage data was presented as the long overdue “smashing success” for Abenomics, as it was the first month in two years whenreal wages posted a meager 0.1% increase.

Unfortunately, just a few weeks later that 0.1% increase was promptly adjusted down to an unchanged 0.0%, thereby confirming not only that Abenomics remains a failure but that no Japanese wage data is even modestly credibly.

And then, last night, we got the latest data for the month of July which was an absolute disaster.

The ministry of health and labor reported that total average monthly cash earnings per regular employee in Japan for June stood at Y425,727, plunging 2.4% from a year earlier and posting the first year-on-year drop in seven months after +0.7% in May, which was distorted by irregular summer bonus payment patterns.

Bonuses and other special pay slumped 6.5% on year for the first drop in eight months after +25.2% in May. But base wages, the key to a recovery in cash earnings, rose 0.4% on year in June for the fourth straight rise.Overtime pay fell 0.4% for the fourth straight drop, indicating a GDP slump in the April-June quarter.

Not surprisingly, the fall in bonuses in June was attributed to an increase in entities that paid bonuses early in May at businesses with more than 30 employees where payments are large and a decline in businesses that paid bonuses in June compared with last year (ratio of businesses paying in June: 37.7%, June 2014: 41.9%).

In other words, as Abe pushes more and more companies to compensate for soaring import costs with higher bonuses, companies have simply slashed the number of bonuses paid out by 10% in one years! And it’s only going to get worse, with the Federation of Economic Organizations’ (Keidanren) summer bonus survey showing a sharp slowdown in bonuses this year to +2.8% from +7.2% last year, excessive expectations are unwarranted.

The punchline: all important real wages, even those including bonuses and special payments, once again failed to keep up with inflation, and in June crashed by a whopping 2.9% reflecting a 0.5% yoy increase in the CPI excluding imputed rent. As the chart below shows, there has now been 24 consecutive months without a single Y/Y monthly increase in real wages (we fully expect May’s unchanged print to be revised negative in the final report).

What’s worse is that when one adjusts the inflationary surge from the consumption tax hike last April, which has now been fully anniversaried and is no longer part of the base effect, this was the largest decline in Japan’s real wages since December 2009, or the biggest monthly plunge in 6 years!

The irony here is that even as Abenomics is pushing Japan’s economy ever deeper into total ruin, overnight an economic adviser to Japan’s prime minister said that he saw no need for the Bank of Japan to deploy additional stimulus to meet its 2 percent inflation goal next year, warning that it could cause the yen to weaken and prices to overshoot.

Quoted by Reuters, Etsuro Honda, special adviser to the Cabinet and a leading architect of Prime Minister Shinzo Abe’s reflationary economic policy, told Reuters in an interview that the next step for the central bank could be to taper its massive asset purchases.

So tapering Japan’s QQE just as the Japanese consumer has not been weaker in 6 years (a state for which the BOJ takes all the blame).

Back to the real deterioration in Japan’s economy, Market News reminds us that many firms are still using lower-paid part-time and contract workers as a buffer against business cycles. And a big reason for the ongoing weakness in wages is that just like in the US, the number of full-time employees rose 1.5% on year in June after +1.4% in May while the number of part-time workers gained 3.4% in June after +3.5% in May.

We already covered all this previously in “This Is What Keynesian “Success” Looks Like: Soaring Part-Time Jobs, Record Low Real Wages” when we showed how Japan, like the US, is becoming a nation of part-time workers…

… consisting of “senior citizens and housewives”

With Abenomics solely to blame for the collapse in real wages which are now at a record low indexed level:

We leave the conclusion to MarketNews:

The economy is widely expected to have contracted in the April-June (preliminary Q2 GDP due out on Aug. 17) but is forecast to rebound in the July-September quarter, which should support a modest improvement in nominal wages. But it takes time to push up wages above inflation, which is keeping consumption weak. The long decline in real wages, which has been on a general downtrend in the past four years, has hurt the average household income as the cost of living has been pushed up by high import costs and the sales tax hike last year.

So another Keynesian success. And by success we of course mean complete failure.

But how is it possible that Japan could singlehandedly destroy its economy? We wondered long and hard, and then we remembered that it was never alone.

Recall: “And The Person Responsible For Japan’s Economic Endgame Is… Paul Krugman“

At that point everything falls into place.

end

DOJ Launches Criminal Investigation Into Deutsche Bank Russian Trades

Deutsche Bank just can’t seem to get out of its own way and indeed, it’s becoming increasingly clear that when it comes to malfeasance, the German lender is without equal.

Just days after WSJ revealed that the bank’s $2.5 billion LIBOR settlement could be in jeopardy due to the apparent mishandling of chat records dating back to 2005 (which, incidentally, is when Anshu Jain instituted a new seating arrangement that placed LIBOR submitters next to traders), Bloomberg says Loretta Lynch’s Justice Department has launched a criminal probe into the bank’s alleged role in facilitating a series of trades which may have allowed Russian clients to launder billions through the bank’s trading desks.

The “mirror trades” in question aren’t terribly complicated and indeed, it appears as though they would have been quite easy to identify if you knew what you were looking for. Here’s Bloomberg:

The trades under investigation involve stocks bought by Russian clients in rubles through Deutsche Bank, and simultaneous trades through London in which the bank bought the same securities for similar amounts in U.S. dollars, people familiar with the matter have said.

Got it. So basically, Deutsche Bank moved some money out of the country for a few Russians.

Here’s what the bank had to say about the trades in its latest interim report:

Deutsche Bank is investigating the circumstances around equity trades entered into by certain clients with Deutsche Bank in Moscow and London that offset one another. The total volume of the transactions under review is significant. The ongoing internal investigation includes a review as to whether violations of law, regulation or policy have occurred, as well as a review of Deutsche Bank’s related internal controls. Deutsche Bank has advised regulators and law enforcement authorities in several jurisdictions (including Germany, Russia, the UK and US) of this investigation. Deutsche Bank has taken disciplinary measures with regards to certain individuals in this matter and will continue to do so with respect to others as warranted.

But as one analyst in Hamburg notes, “the sums we’re talking about aren’t peanuts,” which means this isn’t going to be swept under the rug before every regulator from New York to Moscow extracts its fair share of protection money from the bank.

As for the Justice Department, Loretta Lynch’s ongoing effort to prove how serious the US is about prosecuting criminality on Wall Street has led to at least one other open investigation involving Deutsche Bank. As we noted in “DoJ To Tax Wall Street (Again) In MBS Probe,” the DoJ is now pursuing a fresh round of MBS-related settlements with banks that knowingly packaged and sold shoddy CDOs, cementing Lynch’s role as the person in charge of shaking down Wall Street for government protection money, and Deutsche Bank is among the targets.

Amusingly, the New York DFS (which is investigatingwhether the bank might have deliberately scrubbed an “unknown number” of LIBOR chats from its system) is also looking into the Russian trades. Here’s Bloomberg again:

Those mirror trades have also come under scrutiny of New York’s banking regulator, a person familiar with the matter has said. The state’s Department of Financial Services has asked Deutsche Bank for e-mails, memos, client lists and other documents as it looks into whether those trades were used to help Russian clients skirt U.S. sanctions laws, according to the person. The DFS also asked for information about whether any of the bank’s other operations, including those in New York, were connected with the trades, the person has said.

So in other words, once Deutsche Bank has finished explaining to the DFS how, despite its best efforts, it just can’t seem to find all of the LIBOR-related DB Chat messages regulators are interested in reviewing, the bank will get around to digging up any “e-mails, memos, and other documents” it can (or can’t) locate related to the mirror trades.

In the end, the story will be the same. More evidence of endemic corruption will come to light allowing government entities to extract still more settlement payouts.

Chances that any actual Deutsche Bank employees get “Tom Hayes-ed“: slim.

Chances that a few traders are fired and then promptly find lucrative new work somewhere in the Swiss financial community: pretty good.

Dramatic Footage Of Saudi Tanks Invading Yemen

There are competing accounts as to exactly what happened at the Al Anad airbase in Yemen on Monday, where Saudi-backed forces loyal to President Abed Rabbo Mansour Hadi reportedly routed Houthi rebels, marking the latest in a series of setbacks for the Iran-backed group which forced Hadi to flee to Riyadh earlier this year, plunging Yemen into a bloody civil war.

According to the Houthis, coalition forces were “crushed” and their vehicles destroyed, but a spokesman for the Popular Resistance said most of the base was in coalition hands. Here’s WSJ:

Forces fighting for a Saudi-led military coalition in Yemen have defeated the country’s Houthi rebels at a strategic southern air base, the Yemeni defense ministry said Tuesday.

The Houthis denied that the base had fallen. However, if it has been captured this would extend a recent turning of the tide in favor of the coalition in the four-month-old conflict.

The defense ministry said the operation at Al Anad, a large complex from which the U.S. had launched drone attacks against Al Qaeda in the Arabian Peninsula before the recent instability, was “a true representation of national will and noble sacrifices that are being made to liberate Yemen from the grip of overthrowing militias.”

A report Tuesday by the Houthi-run Saba news agency denied that Al Anad base had been taken, citing an unnamed military official. The Houthis had “crushed all [coalition] offensives” against the base and destroyed scores of military vehicles, Houthi spokesman Nasruddin Amer said Monday evening.

If confirmed, the turn of fortunes in favor of the coalition at Al Anad build upon a string of recent gains in the south by the allies, which include Saudi Arabia, the U.A.E., Qatar, Bahrain, Egypt and a number of other Arab states.

Houthi rebels have been driven from Aden in recent weeks, setting the stage for coalition forces to make a further push northward into other Houthi-controlled areas.

Here’s footage of the actual battle courtesy of RT:

And here’s footage of Saudi tanks pushing north as the coalition offensive gathers steam:

* * *

Importantly, Saudi and coalition boots are now officially on the ground in Yemen, under the guise of tank trainers. Here’s The Washington Post:

Saudi and Emirati troops are assisting Yemeni pro-government forces at al-Anad by operating many of the tanks and sophisticated military equipment, military officials said.

A Yemeni military official said thus far, few Yemeni troops have been trained in operating the tanks that have arrived by sea from Gulf allies in recent weeks. He added that the Yemeni military sought help from coalition countries in the al-Anad operation, calling them “partners in the liberation operation of Aden and other provinces.”