Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1120.40 down $0.20 (comex closing time)

Silver $14.75 up 21 cents.

In the access market 5:15 pm

Gold $1121.50

Silver: $14.78

In this commentary I have spent a lot of time discussing Quantitative tightening by China coupled with the threat of an increase in rates by the USA. Both of these countries can be viewed as in the mode of tightening ie. removing liquidity from the markets. The two entities that are increasing QE and thus adding liquidity is the ECB and Japan. The problem with the latter two entities is the fact that they are running out of bonds to monetize so they too may be finished from increasing liquidity. I have provided many important commentaries on this subject. I urge you to take your time read them. You will be glad you did.

First, here is an outline of what will be discussed tonight:

At the gold comex today we had a poor delivery day, registering 0 notices for 0 ounces Silver saw 140 notices for 700,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 219.99 tonnes for a loss of 83 tonnes over that period.

In silver, the open interest rose by 886 contracts despite the fact that silver was down in price by 16 cents on Friday. Again, our banker friends used the opportunity to cover as many silver shorts as they could but failed. The total silver OI now rests at 157,506 contracts In ounces, the OI is still represented by .787 billion oz or 112% of annual global silver production (ex Russia ex China).

In silver we had 53 notices served upon for 265,000 oz.

In gold, the total comex gold OI surprisingly rose to 419,002 for a gain of 5,125 contracts. We had 0 notices filed for nil oz today.

We had a slight change in tonnage at the GLD today/ a slight withdrawal of .24 tonnes and this was to pay for fees./ thus the inventory rests tonight at 682.59 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had a big withdrawal in silver inventory at the SLV to the tune of 1.527 million oz/Inventory rests at 323.396 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver rise by 886 contracts up to 157,506 despite the fact that silver was down by 16 cents in price with respect to Friday’s trading. The total OI for gold rose by 5125 contracts to 419,002 contracts, despite the fact that gold was down by $3.10 on Friday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. Trading overnight from Japan

4. Trading overnight from China.

5. Understanding Quantitative Tightening/POBC trying to shore up their economy

seven important stories/Stockman/Deutsche bank, Ray Dalio/Bridgewater/zero hedge)

6. Tensions mounting against Russia:

three stories/zero hedge

7. Why Soc Generale is worried this time with the world’s 9 trillion USA losses. It is due to the huge debt taken on by public companies buying back their stock

(Soc Generale/zero hedge)

8 Oil related stories

Berman/OilPrice.com

9. USA stories/Trading of equities NY

a) Goldman Sachs states 7 reasons why the USA will not raise rates on Sept 17

b) In the jobs report 698 native Americans have lost their jobs in August and yet over 200 foreign born Americans got jobs

(zero hedge)

c) Three Nomura traders charged criminally for skimming

(zero hedge)

d) retail sales as reported by Gallup shows a big downfall/numbers far different from the conference board junk

(Gallup/zero hedge)

e. A good look at the public school finances inside Chicago

(zero hedge)

10. Physical stories:

- Peter Stoeferle on Gold metrics “IN Gold We Trust” 2015

- Bill Holter’s paper tonight: “Be Careful What You Wish For”

- Craig Hemke on the addition of 16 tonnes of gold added to China’s official reserves

- Bloomberg: on Bitcoins use in the Isle of Man

- Jessie of Amercain cafe on Ronan Manly’s paper on huge discrepancies reported by the LBMA on gold supplied for refining and supplied to China.

- John Embry interviewed by Kingworldnews

11. Two concluding pieces:

i) Greg Hunter interviews one of my favourites: Rob Kirby

ii) Dave Kranzler of IRS believes the USA will start a war to get out of its mess of huge debts and no gold

and well as other commentaries…

Let us head over and see the comex results for today.

September contract month:

Initial standings

September 8.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 105,025.05 oz

Brinks,Scotia JPMorgan |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 0 contracts (nil oz) |

| No of oz to be served (notices) | 175 contracts (175,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 12 contracts(1,200 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 153,611.2 oz |

Total customer deposit: nil oz

JPMorgan has only 0.6133 tonnes left in its registered or dealer inventory. (19,718.722 oz) and only 863,683.63 oz in its customer (eligible) account or 26.86 tonnes

September silver initial standings

September 8 2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,282,159.83 |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 700 contracts (700,000 oz) |

| No of oz to be served (notices) | 712 contracts (3,560,000 oz) |

| Total monthly oz silver served (contracts) | 804 contracts (4,020,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,021,596.2 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit; 0 oz

total customer deposits: 0 oz

total withdrawals from customer: 1,282,159.83 oz

And now SLV:

Sept 8/we had a huge withdrawal of 1.524 million oz of silver from the SLV/Inventory rests tonight at 323.396 million oz.

Sept 4.2015:no changes in inventory at the SLV/rests tonight at 324.923 million oz

sept 3/we had a small withdrawal of 140,000 oz of silver from the SLV/Inventory rests at 324.923 million oz

Sept 2: we had a small withdrawal of 859,000 oz of silver from the SLV vaults/inventory rests tonight at 325.063 million oz

September 1/no change in inventory over at the SLV/Inventory rests tonight at 325.922 million oz

August 31.a huge addition of 954,000 oz were added to inventory today at the SLV/Inventory rests at 325.922 million oz

August 28.2015: no change in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 27.no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 26.2015/no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 25.2015:no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 24./no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 21.2015/ no change in inventory at the SLV/Inventory rests at

324.698 million oz

August 20.2015:/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 19/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

(courtesy/Mark O’Byrne/Goldcore)

China Buys 16 Tons Gold In August – Dumps $94 Billion

Given the strong demand fundamentals, particularly out of China, gold should go higher but as ever there is a risk of selling in the futures market leading to weakness in the short term as traders follow momentum and ignore fundamentals.

This demand continues and is being bolstered by official Chinese demand. The People’s Bank of China (PBOC) added another 15.98 tonnes of gold in August – at the same time its foreign exchange reserves fell a whopping $94 billion. The Chinese continue to diversify out of the dollar and into gold.

DAILY PRICES

Today’s Gold Prices: USD 1120.85, EUR 1003.49 and GBP 728.27 per ounce.

Yesterday’s Gold Prices: USD 1121.00, EUR 1004.03 and GBP 734.75 per ounce.

(LBMA AM)

Gold was marginally lower in gold trading in Singapore and this slight weakness continued to European trading with gold tethered to a remarkably tight $3 range between $1,123.70/oz and $1,120.50/oz.

IMPORTANT NEWS

Gold Inches up in Asia Trade – The Wall Street Journal

Gold stable, net long position up for fifth consecutive week – The Bullion Desk

Perth Mint Gold and Silver Sales Solid in August – CoinNews.net

China FX reserves fall record $93.9 bln in Aug as central bank supports yuan – Yahoo Finance

Hollande Readies Syria Air Strikes as Response to Refugee Crisis – Bloomberg

IMPORTANT COMMENTARY

Data retention and the end of Australians’ digital privacy – The Sydney Morning Herald

China “Officially” Adds Another 16 Metric Tonnes – TF Metals Report

LBMA Apparently Altered Its Gold Refining Flow Statistics By 2,200 Tonnes – Jesse’s Café Américain

Did COMEX Counterparty Risk Just Reach A Record High? -Zero Hedge

end

Despite the turmoil in China by the selling of 115 billion dollars worth of treasuries, they still found time to buy 16 tonnes of gold in August. You could bet the farm that this gold was bought long ago as China will slowly “add” to their official reserve each month.

(courtesy Turd Ferguson/Craig Hemke/GATA)

TF Metals Report: People’s Bank of China adds 16 tonnes of gold in August

Submitted by cpowell on Mon, 2015-09-07 19:33. Section: Daily Dispatches

3:30p ET Monday, September 7, 2015

Dear Friend of GATA and Gold:

Even while it has been selling a lot of U.S. Treasury bonds, the People’s Bank of China continues to add to its gold reserves, in the amount of 16 tonnes in August, the TF Metals Report’s Turd Ferguson reports today. The monthly additions, Ferguson adds, are running at a rate of about 200 tonnes per year. His report is posted at the TF Metals Report here:

http://www.tfmetalsreport.com/blog/7124/china-officially-adds-another-16…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

(courtesy Peter Stoeferle/Mark Valek/zero hedge)

In Gold We Trust – 2015 Edition

Monetary history, staggering mountains of debt, demographic problems, metrics relevant to the gold market, central bank debauchery and currency debasement in all their terrible glory, and even the beer price of gold – the latest Incrementum “In Gold We Trust”chartbook has it all…

There has been an astonishing synchronization between equity markets and the gold-silver ratio until 2011. A rising stock market almost always coincided with a declining gold-silver ratio, i.e. with silver outperforming gold. This may have been due to re-inflation being accomplished with conventional monetary policy – i.e., credit expansion by commercial banks – in previous cycles . This affected the real economy more quickly and fostered consumer price inflation. This time, re-inflation has been attempted by means of central bank securities purchases, which has led to price increases in investment assets, but has not been able to spur consumer price inflation.

Full Chartbook below…

Chartbook – In Gold We Trust 2015 & Status Quo

end

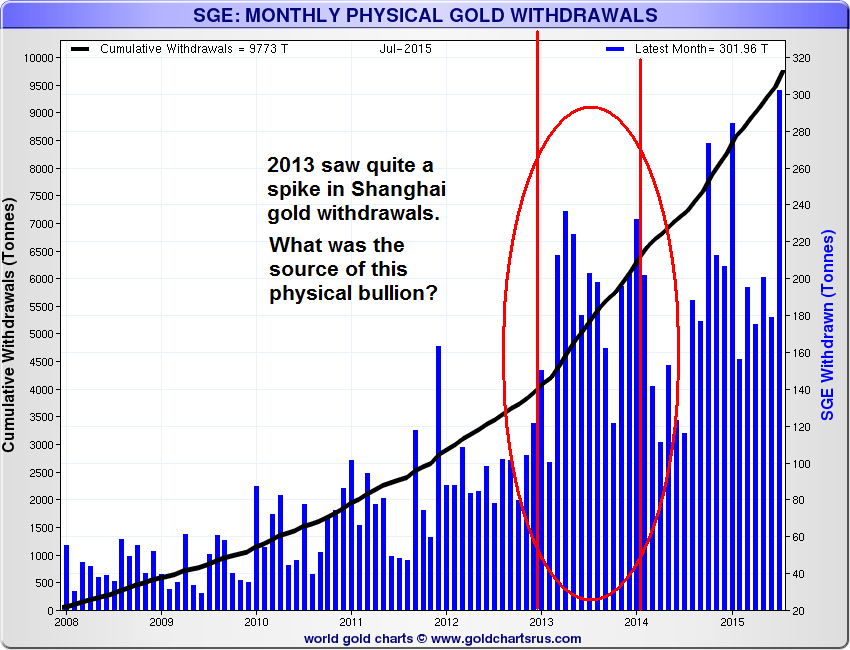

Further to our discussion yesterday whereby Ronan Manly noted that the LBMA altered its gold refining stats into Hong Kong by 2200 tonnes:

(courtesy Jessie/American cafe)

LBMA Apparently Altered Its Gold Refining Flow Statistics By 2,200 Tonnes

Ronan Manly has published a fascinating analysis of the LBMA gold refining statistics today.

The gold refined by LBMA ‘good delivery’ refiners is sometimes involved in converting existing gold bars into kilobars which are suitable for export to the Asian Markets.

Ronan Manly offers quite a bit of detail with regard to a very large revision in the LBMA 2013 refining data and suggests that such a large restatement of gold statistics, almost 1/3, without explanation, seems odd.

The supposition is that the LBMA originally counted gold bars that were taken from existing sources, such as their own stores, ETFs, and the Bank of England and re-refined them into kilobars for delivery into Asia. Later they restated the number much lower, by 2,200 tonnes. We have not been given the exact reason for this, but one suggestion is that the gold did not come from new mining or traditional recycling. And the LBMA was reluctant to advertise such a huge spike in gold refining spurred on by Asian demand.

Depending on how the GFMS and the WGC uses the statistics and sources, this could result in a significant (~2,200 tonnes) understatement of the flow of gold from Western sources into Asia in just that one year. Considering how tight gold supplies have been this might explain quite a bit.

What exactly is the LBMA policy decision here, and what about subsequent years of 2014 and 2015?

What is the source of this gold? And what is so special about 2013?

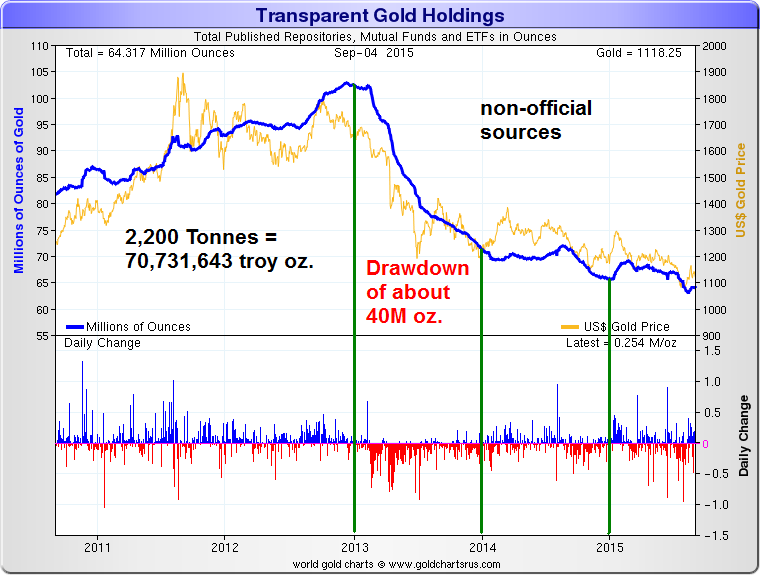

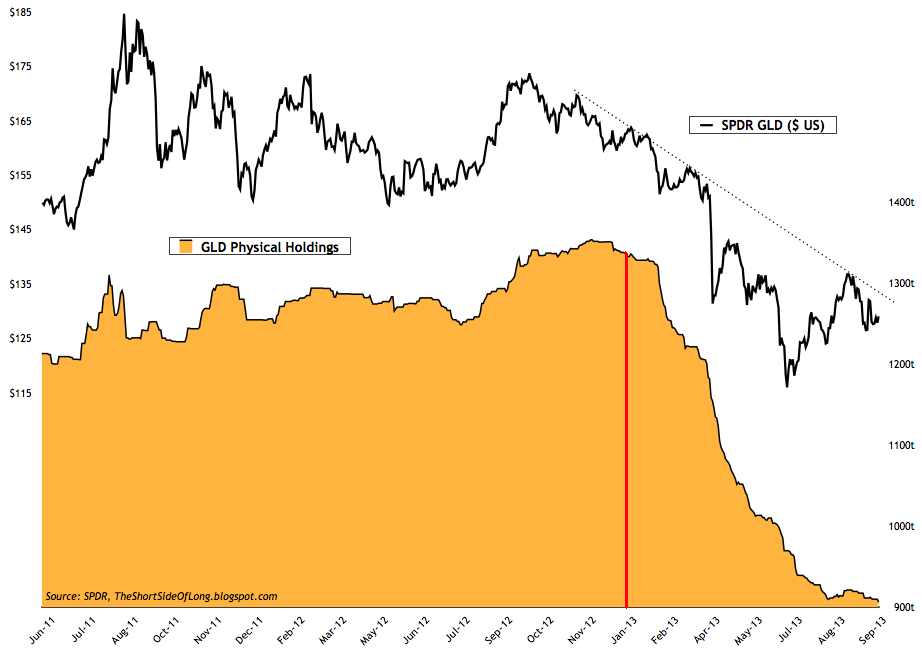

The one thing that seems significant about 2013 is that the price of gold was hit rather hard by selling after hitting a peak in 2012, and the total amount of gold held in Western depositories and ETFs dropped considerably concurrent with that hit in price. A chart is included below for your convenience.

So far we have more questions than answers. Perhaps more information will be forthcoming. I am given to understand that the LBMA is not open to discussing the matter.

I have my own hypothesis. There was a major effort to hold down the price of gold in 2013 after it had run to a new high. That effort to suppress the price resulted in a huge spike in physical demand from China.

‘Stopgap measures’ were taken to meet that physical demand, but without allowing the price to increase.

As more and more gold was shaken loose from various sources, a campaign of stifling Western interest in gold was undertaken to permit even more gold to be taken out of ETFs and repositories.

However, the demand from China and India were not passing events, and have continued until even now. And so the stopgap measures of 2013 have turned into an ongoing shuffling around of existing bullion to try and keep the price of gold from running higher, and threatening some of the bullion banks and institutions who cannot possibly replace all that has been loaned out and sold at anything near today’s prices.

Or it *could* be something else entirely. Time will tell I am sure. But I think that there are now two events that might be remembered as potentially pivotal: one in 2007 in which the world’s central banks became net buyers of gold for the first time in about thirty or more years, and 2013, in which the flow of gold from West to East put the Gold Pool into unsustainable endgame from which it could not recover without allowing prices to eventually run higher.

Ronan Manly suggests that he will have a follow up article explaining his own analysis, and I will most likely defer to his more informed judgement and wait to see what he says. I do not have all the information and a few things still puzzle me a bit. But I do congratulate him on finding this and writing it up so well with so much thought.

For the detailed analysis about what happened read the entire piece Ronan Manly, The LBMA’s shifting stance on gold refinery production statistics

This is a quote from his article:

“There are 2,200 tonnes of 2013 gold refining output in excess of combined mine production and scrap recycling being signalled within the 6,601 tonnes figure that was removed from the LBMA’s reports on 5th August 2015.

Could it be that this 6,601 tonne figure included refinery throughput for the huge number of London Good Delivery gold bars extracted from gold ETFs and LBMA and Bank of England vaults and converted into smaller gold bars in 2013, mainly using LBMA Good Delivery Swiss gold refineries?And that maybe this 6,601 tonne figure stood out as a statistical outlier for 2013 which no one wanted to talk about?

The objectives of HM Treasury’s Fair and Efficient Markets Review (FEMR) include transparency and openness. It would appear that altering already published gold refinery statistics, especially for 2013, seems not to be in the spirit of these FEMR objectives.

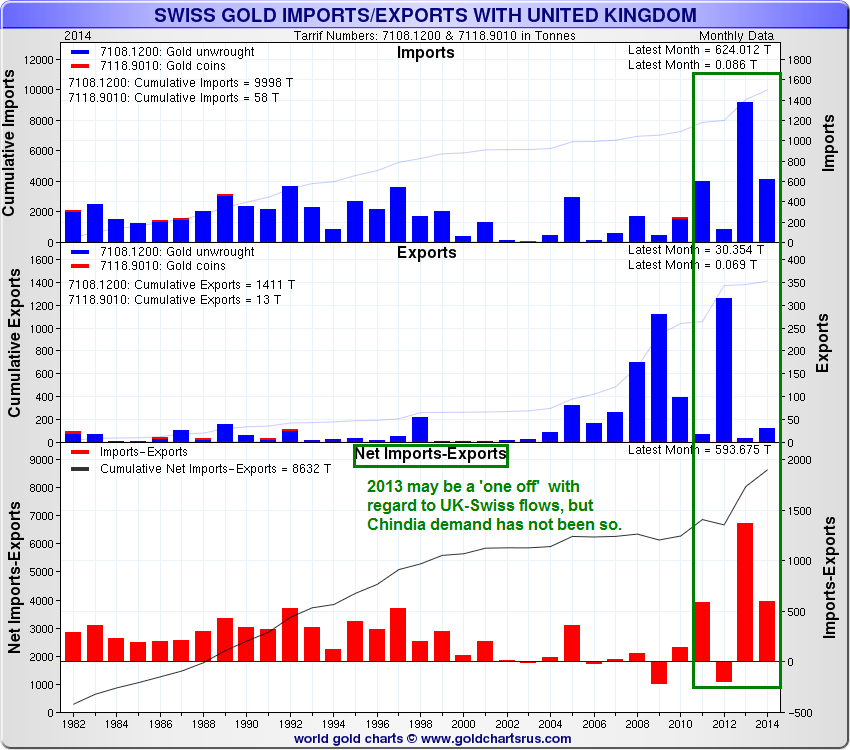

Part 2 of this analysis of the LBMA’s 2013 gold refinery statistics looks behind the 6,601 tonne number at the phenomenon of Good Delivery bars being processed through the Swiss gold refineries in 2013, the gold withdrawals from the London-based gold ETFs, and the huge shipments of gold from the UK to Switzerland in 2013. Part 2 also examines the 2013 withdrawal of gold from the Bank of England, and how GFMS and the World Gold Council tried to, or tried not to, explain the non-stop processing of Good Delivery gold bars into smaller finer kilobars during 2013.”

Related follow up article from Ronan Manly: How Many Gold Bars Are In the London Vaults

Greetings from Bitcoin Island

Submitted by cpowell on Tue, 2015-09-08 00:56. Section: Daily Dispatches

By Jeremy Kahn

Bloomberg News

Monday, September 7, 2015

The Isle of Man is a strange place. Home to four-horned sheep, cats without tails, and perfectly preserved Victorian-era steam locomotives, this rock in the middle of the Irish Sea is perhaps best known for hosting the world’s most dangerous motorcycle race, the Manx TT.

It’s also a place where, after you take a 70-minute flight from London, a car service called The Lady Chauffeurs will meet you at the airport in a silver Mercedes-Benz S-Class. Imagine my surprise, then, when I’m greeted at arrivals by Keith, who, while courteous, impeccably dressed in a gray suit, and an able driver, is most decidedly not a lady. “All of our regular drivers are busy,” says an apologetic Nula Perren, who owns the company and has accompanied Keith to the airport. Not that I mind. I didn’t choose The Lady Chauffeurs for its ladies; I booked for the bitcoin.

Lady Chauffeurs is one of a growing number of businesses on the island that accept the digital currency. Bitcoin startups tend to cluster where the venture capital money is: London, New York, San Francisco. Taking on these behemoths might appear to be a stretch for a tiny British protectorate that can seem more time capsule than Tomorrowland. Yet the Manx government is indeed seeking to make the island the world’s foremost hub for the technology. Some 25 startups working with digital currencies or the blockchains that underpin them are already based here—and that number is growing steadily. …

… For the remainder of the report:

http://www.bloomberg.com/news/features/2015-09-07/isle-of-man-tax-haven-…

Putin aide’s advice: Default on foreign debt, put reserves into gold and BRICs bonds

Submitted by cpowell on Tue, 2015-09-08 12:37. Section: Daily Dispatches

8:35a ET Tuesday, September 8, 2015

Dear Friend of GATA and Gold:

Russia’s government long has understood gold’s secret power over the international monetary system. In an address in June 2004 at the summer meeting of the London Bullion Market Association at the Kempinsky Hotel in Moscow, the Russian central bank’s deputy chairman, Oleg Mozhaiskov, spoke only four words in English: “Gold Anti-Trust Action Committee”:

As far as GATA itself knew at that time, it had never had any contact with anyone in Russia or anyone connected with the Russian government.

But Russia’s expressions of interest in gold have multiplied since then and another one was reported today by the Moscow-based financial newspaper Kommersant (“The Businessman”), which described a plan to achieve Russia’s economic sovereignty that is to be presented next week to Russia’s Security Council by Sergei Glazyev, a politician and economist who is an assistant to President Vladimir Putin:

http://www.kommersant.ru/doc/2805251

Glazyev is among the small number of Russian officials targeted specifically by U.S. economic sanctions, and according to Kommersant his plan includes a section about “neutralizing anti-Russian sanctions.”

Kommersant’s report is available only in Russian, but a Google translation of its 12th paragraph says Glazyev proposes authorizing Russian companies to “declare force majeure” against loans from countries that have imposed financial sanctions against Russia, “in effect the legalization of non-repayment of all private foreign debt”; converting the reserves of Russia’s central bank and the government’s Reserve Fund and National Welfare Fund into gold and obligations of the “BRICs” countries; and creating a system of international payments separate from the Western-controlled SWIFT system that would operate with China’s UnionPay system.

Of course these aren’t terribly original or insightful ideas. No country that uses another country’s currency for its international commerce is fully sovereign, and only gold is a neutral international reserve currency. It is precisely to rope the world into the U.S. imperial system that the International Monetary Fund prohibits its members from formally linking their currencies to gold, though commodity-producing countries like Russia, South Africa, Mexico, and those in the rest of the developing world are particularly oppressed by such rules.

The question long has been whether any of them will ever have the nerve to do something about it. Glazyev’s report may be an invitation.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

(courtesy John Embry/Kingworldnews)

Intensifying suppression of monetary metals hints at racket’s end, Embry says

Submitted by cpowell on Tue, 2015-09-08 17:55. Section: Daily Dispatches

1:55p ET Tuesday, September 8, 2015

Dear Friend of GATA and Gold:

Central bank intervention against the monetary metals is now so intense as to lead Sprott Asset Management’s John Embry to think that the racket is almost finished. Embry’s comments come in an interview with King World News that is excerpted here:

http://kingworldnews.com/the-endgame-is-now-in-sight-as-the-propaganda-a…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Exhaustion… Be careful what you wish for

Dear CIGAs,

Doom and gloom “porn”, this is the new troll term to describe the realities being described by those who use math and pure logic to derive conclusions. What other conclusions can one come to than “it’s been a great ride but it’s nearly over”? We are only a week away from the Fed meeting where interest rates may come off of “zero” (I dare them). Just reported was an unemployment rate at 5.1% …while 47 million Americans are on food assistance. Totally “unexpected” was the chemical “explosion of the week” in ChinaAnother Chinese Chemical Plant Explodes, Huge Clouds Of Black Smoke Billow Skyward.

I ask, what happens when you raise interest rates on a wobbly creditor (system) living day to day shuffling funds around just to settle? What happens when one of these well known creditors cannot and do not “settle”? I am talking of course about derivatives. You know, those wonderful contracts that allow creditors (even entire countries like Greece, Italy etc.) to hide true debt because they are “insured”. What happens when the insurance does not pay or the insurer goes broke?

As for unemployment, how can nearly 15% of your population eat on food assistance while the country is at or near “full employment”? Does anyone, even for a moment believe the country is at full employment? How does a country survive when more than half the population “gets” while the other, less than half “gives”. All of these social programs may have been noble in their infancy. Now they are used and abused as a “way of life”. The only problem is the unsustainable nature means there is an end date … an “exhaustion” so to speak!

As for most recent and “coincidental” chemical explosion in China, why now? Why didn’t they have lots of explosions along the way to their industrialization? Have they forgotten safety measures, just now? I do want to point out if these are not “accidents”, more “accidents” will occur in the West.

I could of course write 24/7 for a month or more on what has gone wrong and what is unsustainable. The point of this writing is not to give you new information or dots to connect. The dots have been identified and connected by many in what is termed the “alternative media”. Is common sense logic and truth actually “doom porn” for sensationalism or is it getting out because for some, truth still matters? In my opinion truth doesn’t “still matter”, it is ALL that matters and WILL matter.

I write this to tell you “be careful what you wish for”. I receive several hundred e-mails each day. Some are nuts, a few are trolls, some are well intentioned but uninformed, some are inquisitive and others demanding. The one response that seems to be standing out and growing are of the “I just want to get it over” type. I understand this and sometimes I feel the same way. It is a feeling of exhaustion while waiting for the exhaustion to happen! The problem with this is we are wishing for a “crashed” standard of living. Our current standard of living has been on borrowed money and is on borrowed time, I have to say it’s really been fun while it lasted!

Why do I write this now? It is safe to say, if you look around it is obvious. The computer algorithms have taken over, the little guy is long gone and we watch as volatility increases with volume continually decreasing …THE classic sign of exhaustion. Markets all over the world have unsettled and the carefully choreographed stability is being shaken. Debt, which the entire system has been built on has now come front and center with skepticism. Central banks far and wide (including The Fed) are having their “omnipotence” questioned …and thus so are their issued currencies.

Many of you have heard of or read the “Shemitah” http://usawatchdog.com/great-shaking-and-collapse-is-coming-jonathan-cahn/ seven year cycle ends next Saturday September 13th. Some believe it while others do not. Going back every seven years, 2008, 2001, 1994, 1987, 1980, 1973 ..etc. does show some very large and in some cases life changing inflection points. In fact, if we go back 10 seven year cycles, it was the end of WW II, 1945. I might add, this was the dawn of the American dominance of finance kicked off with Bretton Woods cementing the dollar as the world reserve currency.

Some believe in this seven year cycle while others do not. I believe with my own eyes and sense of history the world has been changed by something or some event each and every seven years. Some believe in God and his written word The Bible, while others do not. The Shemitah is Biblical and the seven year cycle is identified several times in The Bible. I am a Christian and thus believe the cycle exists because the Bible says it does, it does not hurt that I can observe this personally.

While not trying to turn this into a God “blog”, I would urge anyone with a religious belief to get your spiritual house in order. No matter what or who your own personal God is, it is quite clear something very big and very bad is about to occur. Whether you have religious belief or not, you must prepare physically for what is coming, this much is obvious. If it is not obvious to you, I am quite sorry as many good and well intentioned people have been trying for years to show you how, what and why this final debt exhaustion would occur. I will end with this piece of advice. Life is not a dress rehearsal and there are no do overs in life. You must not be one second too late in any of your preparations whether they be physical, mental or spiritual. The exhaustion of nearly every facet of our known way of life is upon us!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

Comments welcome! bholter@hotmail.com

1 Chinese yuan vs USA dollar/yuan lowers in value, this time at 6.3674/Shanghai bourse: green and Hang Sang: green

Surprisingly, last week, officially, China added another 19 tonnes of gold to its official reserves now totaling 1677.

2 Nikkei down 433.39 or 2.43.%

3. Europe stocks all in the green (on USA/Yen ramp) /USA dollar index up to 96.14/Euro up to 1.1161

3b Japan 10 year bond yield: falls to .365% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 119.92

3c Nikkei now below 18,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI: 45.31 and Brent: 48.70

3f Gold up /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil up for WTI and up for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .68 per cent. German bunds in negative yields from 4 years out

Greece sees its 2 year rate falls to 10.65%/Greek stocks this morning up by 3.11%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield falls to : 9.02%

3k Gold at $1121.40 /silver $14.70 (8 am est)

3l USA vs Russian rouble; (Russian rouble down 85/100 in roubles/dollar) 68.27,

3m oil into the 45 dollar handle for WTI and 48 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9779 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0914 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now enters in negative territory with the 10 year moving further from negativity to +.68%

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.15% early this morning. Thirty year rate below 3% at 2.92% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Soar After Dramatic Chinese Last Hour Intervention Scrambles To Mask Latest Terrible Trade Data

The last time we looked at Chinese stocks, just a few hours ago, they were down 2%, and on pace to close back under 3000, following the latest collapse in official Chinese trade data (so one can imagine what the real data was), where in August exports dropped 5.5% (vs -8.3% in July) while imports tumbled -13.8% in dollar terms (worse than the -8.1% prior). As the Reuters chart below shows, this was the 10th month in a row of declines and the worst stretch since the 2008 crisis, confirming China will need far more currency devaluation to stabilize the trade pain.

The terrible Chinese trade data was enough to initially push not only Chinese, but Asian stocks broadly lower, and served to slam the USDJPY back under 119 on the heels of another ugly Japan GDP report which rose only due to another surge in inventory accumulation even as capital spending dropped, which in turn pushed the Nikkei to a -2.4% close (despite a flash smash 400 points higher at the open), wiping out all Japanese stock gains for 2015.

And then Chinese authorities intervened with gusto, having learned from the mistake of its Monday intervention where it stepped in early in the session only to see all gains fizzle throughtout the day, this time the PBOC and various other state banks waited until the afternoon session, at which point a massive buying orgy ensued, and pushed the SHCOMP from down more than 2% to close at the day highs, up some 2.9%!

At the same time that China was buying stocks, its banks were intervening in FX and the newswires blasted that dealers reported big USD sales by Industrial and Commercial Bank of China and CITIC Bank in the final hour of trading.

The Chinese intervention in both equities and FX was in turn tracked by the USDJPY, and perhaps the BOJ, which sent the critical carry pair from below 119 over 100 pips higher in the span of an hour, pushing the USDJPY over 120 by the time Europe opened…

… and in turn dragged both the Dow Jones futures higher by 300 points while the S&P was up 2% at last check. Just because global trade is slowing down so much, China had no choice but to take out the big guns and get the first bazooka effect after 4 days of trying… and failing.

The waterfall from China’s intervention sent not only European equities and US futures higher, but helped Brent halt its two day selloff to lowest settlement since Aug. 27 while WTI traded above $45 before return of U.S. traders following Labor Day holiday. Ole Hansen, Saxo Bank head of commodity strategy commented that “we are stabilizing a bit, although there has not really been much to cheer about from a news perspective,” adding that “Russia saying ‘no thanks’ to cutting output, loading from the Atlantic looks like rising to 2-3 year high, China imports falling in August – so both increasing supply and slowing demand.”

In the new normal this appears to be bullish for oil, and when central banks are intervening, supply and demand are irrelevant.

Taking a closer look at Asian equities, the Nikkei 225 (-2.4%) as reported above, initially led the region lower after GDP final readings confirmed the economy contracted albeit at a slower than expected pace, before Chinese equities rose out of negative territory in the hours before the close to finish firmly in the green , with Shanghai Comp. (+2.9%) and Hang Seng (+3.6%) spending the session swinging between gains and losses following discouraging trade figures where both imports and exports continued to contract. ASX 200 (+1.7%) spent the day in positive territory led by the energy sector, following M&A flow for the index. Finally, JGBs traded in positive territory as stocks began to soften, this move also came in the context of a mixed 30yr JGB auction which saw a lower than prey. b/c and a narrower than previous tail.

Stocks in Europe traded have higher since the get-go (Euro Stoxx: +1.7%), with market participants shrugging off the release of the uninspiring trade balance data from China and instead focusing on M&A related flow. The less than impressive data from China came as no surprise and will likely reinforce the view that the PBOC and fellow government officials will continue to keep liquidity ample. The upside was led by financials sector in reaction to the takeover of Amlin by Mitsui Sumitomo.

Firmer stocks resulted in lackluster performance by Bunds, which traded lower, albeit marginally, with the downside likely propped up by the dovish stance by the ECB . At the same time, despite the upside in stocks, peripheral bond yield spreads were mixed, with 2y sector broadly wider, highlighting the cautious nature of the rally.

FX translation stemming from M&A related flow supported GBP, which outperformed its major peers, while EUR/GBP edged below 0.7300 level which is said to make up to USD 1bIn worth of expiring strikes . While the USD (USD-index: -0.2%) heads into the North American crossover in negative territory, weighed on by the aforementioned GBP strength and strength in EUR after the long US Labor Day weekend.

Elsewhere, despite the ongoing weakness in energy complex, AUD traded firmer and benefited from the ongoing upside in copper prices which is a by-product of the announcement by Glencore yesterday which would remove 400,000 tonnes of copper from the market, while the likes of CAD and NZD also head into the US session stronger against the USD.

Commodities have seen some strength overnight on the back of a slightly weaker dollar, with gold trading in the green. Copper has also continued in the same trend as yesterday, gaining on the back of the aforementioned Glencore news. The energy complex has also seen strength today on the back of comments from the Iranian Oil minister, who said they were prepared to take any measures necessary to improve the oil market.

In Summary: Europe’s Stoxx 600 rises 2% as of 12:05pm CET time, with gains accelerating following data that showed euro-area economy grew more than estimated in 2Q. European GDP rose 0.4% after expanding a revised 0.5% in 1Q. Shanghai Composite Index rises 2.9%; 1st gain in 5 sessions. China exports slide as tepid demand adds to growth challenge. Maersk Line Cuts Capacity by 16% on West Central Asia to Europe. The US econ calendar is virtually empty: we get NFIB small business conditions (95.9 vs Exp. 96.0), also labour market conditions index and consumer credit data. Kocherlakota speaks after the closing bell.

Market Wrap:

- DAX +2.3%; Shanghai Composite +2.9%; Nikkei 225 -2.4%, erases 2015 gain

- LME 3m Copper +2.3%

- Euro spot -0.1% at 1.1158, yen spot -0.7%

- V2X -9.9% at 31.6

- S&P 500 futures +2% at 1959.3

- For detailed market snapshot, click here

- Indexes: FTSE 100 up 1.7%, CAC 40 up 2%, DAX up 2.3%, IBEX 35 up 1.6%, FTSE MIB up 2.1%, Euro Stoxx 50 up 2.1%

- All of 19 Stoxx 600 sectors rise; autos the top gainer, up 3%; insurance up 2.3%, boosted by MS&AD takeover of Amlin

Bulletin headline summary from Bloomberg and RanSquawk

- Stocks in Europe traded higher since the get-go, with market participants shrugging off the release of the uninspiring trade balance data from China and instead focusing on M&A related flow

- FX translation stemming from M&A related flow supported GBP, which outperformed its major peers, while EUR/GBP edged below 0.7300 handle

- There is little in terms of tier 1data, with market participants likely focusing on any monetary policy related comments by Fed’s Kocherlakota due after the closing bell on Wall Street as well as the USD 24b1n note auction

- Treasuries decline before expected post-holiday resumption of U.S. investment-grade issuance, $24b 3Y auction; WI yield 1.045% vs. 1.013% in August.

- Shanghai stocks climbed in late trading, a pattern consistent with state intervention, leading most global equities higher despite trade data showing China’s exports fell last month

- China exports fell 5.5% in August, slightly above the median forecast of 6.6% decline in Bloomberg survey; imports fell 13.8%, leaving a trade surplus of $60.2b

- Japanese GDP shrank 1.2% in 2Q, less than expected, thanks to a buildup in inventories; businesses reduced investment more than first estimated, in a rebuff to Abe’s call for firms to deploy record cash holdings and profits into capex

- Euro-area GDP rose 0.4% in 2Q, est. 0.3%, after expanding a revised 0.5% in 1Q, the EU’s statistics office in Luxembourg said Tuesday

- Europe’s diverging approaches to the refugee crisis came into focus on Tuesday, with Germany vowing to prioritize funding to aid migrants and Hungary promising to speed up work on a barrier to keep them out

- Sovereign 10Y bond yields mixed. Asian and European stocks gain, U.S. equity-index futures decline. Crude oil mixed, with Brent higher, WTI lower; gold and copper gain

DB’s Jim Reid completes the market wrap in his own words:

It’s straight to China this morning where the latest trade numbers are out. Export numbers continue to remain soft, falling -5.5% yoy in US$ terms in August, although better than the -6.6% yoy expected drop and improving from an -8.3% yoy fall in July. Imports have declined significantly however, falling -13.8% yoy (in US$ terms) after expectations for a fall of -7.9%. That’s seen a surge in China’s surplus, rising $17bn to $60.2bn (vs. $48bn expected). The numbers in Yuan terms are similar, with exports down 6.1% and imports down 14.3%. Chinese equity markets have fallen into the midday break, with the Shanghai Comp down -1.38% and CSI 300 down -1.60%.

This morning’s release is also hot on the heels of the much anticipated foreign reserves data from the PBoC yesterday, with the decline coming in larger than expected. Reserves fell last month by $94bn (vs. $71bn expected) to $3.557tn. In absolute terms that represented the largest fall on record, while the -2.6% decline was the largest percentage fall in more than three years. Much of the commentary has suggested that taking account of valuation adjustments, the drop could well have been over $100bn. As we mentioned yesterday, this data is likely to become a closely watched monthly release with the QT debate now starting to move into focus.

Markets elsewhere this morning are fairly mixed. In Japan the Nikkei (-1.55%) and Topix (-1.12%) have both declined despite an upward revision to Japan’s Q2 GDP reading, revised up one-tenth to -0.3% qoq after expectations of a fall to -0.5%. Elsewhere it’s been a better start for the ASX (+0.77%), however the Hang Seng (-0.12%) and Kospi (-0.66%) are both lower. S&P 500 futures are pointing to a reasonable start, up half a percent while Treasury yields are more or less unchanged.

Taking a look back at markets yesterday now. With the US out is was unsurprisingly a fairly quiet day although European equities started the week on a firmer footing, seemingly helped by the comments from the PBoC Governor over the weekend and also a boost from mining stocks after Glencore’s announcement of a bumper debt reduction plan. Indeed the Stoxx 600 finished the session up +0.48%, although it did pare a stronger opening. The same of which was true for the DAX (+0.70%) and CAC (+0.59%). Gains were fairly broad-based across sectors, but energy stocks proved to be the exception after another decent leg lower for Brent (-3.99%) following suggestions that a Russian official has ruled out cooperation with OPEC on cuts in production. It was a weaker session for Gold (-0.22%) too although Copper (+0.55%) benefited from the Glencore news with copper production set to be suspended as part of the company’s plans.

There was little to report in fixed income markets yesterday. The Euro (+0.19%) saw some modest gains while Bund yields finished more or less unchanged. That was after a data-light calendar with just a weaker than expected German industrial production print for July (+0.7% mom vs. +1.1% expected) – although an upward revision to June gave our colleagues in Europe confidence that the production numbers are supportive of their +0.4% qoq Q3 GDP forecast.

Elsewhere, the latest ECB asset purchases data was released yesterday for the month of August. The data showed that last month saw the lowest level of purchases since the start of the program, with just €42.8bn of public sector purchases which compares to over €51bn we saw in each of the previous two months. Our colleagues note that this August slowdown in buying now moves the ECB’s total purchases across PSPP, covered bonds and ABS back in line after ‘frontloading’ through May, June and July. Looking ahead to September, therefore, this reduces any need to moderate purchase further and so limits concerns of any ‘backloading’ highlighted by Coeure back in March.

Staying in Europe, Spain was the subject of some underperformance yesterday with the IBEX (-0.17%) one of the few equity markets to suffer a decline, while 10y Spanish bond yields widened nearly 7bps with the yield premium (+25bps) over similar maturity BTP’s now the widest in two years. That weakness is being attributed to the release of stronger new opinion polls for the Catalan pro-independence parties on Sunday which showed momentum turning in their favour. As DB’s Marco Stringa noted yesterday, the polls suggest that if they were able to join forces in the Catalan parliament, then they would have the majority of the seats. This is important given that they argue that this would be sufficient to declare a victory in the de-facto referendum for independence regardless of the share of votes. Marco continues to believe that to build a strong case, the pro-independence parties would need to obtain 50%+1 of the votes rather than the seats. That said, he notes that this gap has been closed quickly and that in any case the pro-independence camp, however, seem satisfied with a lower hurdle. With the Catalan elections due September 27th, it’s a situation worth watching closely and another important date for our diaries.

Taking a look at the day ahead now. It’s set to be a busier morning in Europe for data today with Euro area Q2 GDP and German and French trade data all due. On the back of the usual post payrolls lull in the US, there’s just the NFIB small business optimism reading, labour market conditions index and consumer credit print out across the pond this afternoon. The Fed’s Kocherlakota will be due to speak later this evening meanwhile.

end

Monday night: 8:30 pm/liftoff with the USA/JPY algo as Japan will get 3 more years of QE. Remember, however that they will have extremely difficulty in finding the necessary bonds to monetize:

USA/JPY started its ramp up to 119.53 at 8:30, by 9:30 lowered to 119.39 and then in the wee hours of the morning, it zoomed to 120.00 providing the necessary ramp for European stocks and the NYSE/Nasdaq

(courtesy zero hedge)

Japan’s Nikkei Flash-Smashes 400 Points Higher In Milliseconds After Abenomics Gets Three-Year Extension

Whether it is due to thin holiday liquidity, due to the BOJ intervening just ahead of its usual time, because Japan’s “legendary” Twitter trader “CIS” just went bullish (again), because prime minister Abe just learned he would be reinstalled as head of his ruling LDP party because no challenger had emerged unleashing three more years of unchallenged Abenomics, because Japan’s Q2 GDP was just revised modestly higher (to a less negative number) or just because this is how the New Normal rolls, moments ago the Nikkei flash smashed higher some 400 points higher, in a well-choreographed algorithmic frenzy, to take out Friday’s high stops.

Perhaps this latest ridiculous move was predicated by the USDJPY momentum ignition which today came 30 minutes ahead of its usual time…

… or by some of the economic data is neither relevant nor worth digging into. In this “market” things just happen…

Speaking of the economic data, this is what Japan reported: instead of a -1.8% drop in Q2 GDP, Japan – like the US – revised the number higher to “only” -1.2% (versus the initial -1.6% report) with the real sequential decline of -0.3% fractionally better than -0.5%, even as nominal GDP posted the smallest possible sequential gain.

Additionally, Japan reported that its July Current Account balance was higher than the JPY1.732 trillion expected, and rose to JPY1.809 trillion, up from JPY 559 billion in June.

Perhaps the catalyst was the report that Prime Minister Shinzo Abe has returned as president of the ruling Liberal Democratic Party on Tuesday, as rival Seiko Noda failed to garner signatures of support from 20 LDP Diet members, a requirement to file a candidacy for the Sept. 20 election. According to the Japan Times the deadline for filing the candidacy was set at 8:30 a.m. Tuesday, but Noda held a news conference to tell reporters that she gave up running prior to that the same day.

In other words, Abe’s new term as LDP president continues for another three years, which means his term as the prime minister will be extended for that period as well, assuming the increasingly jerky Nikkei – the only thing that has allowed Abe to keep his position as long he has – does not crash in the interim.

As a result, Abe is on course to become Japan’s longest-serving prime minister in more than four decades after standing unopposed in his party’s latest leadership election.

Abe’s re-selection Tuesday as president of the Liberal Democratic Party comes as protests flare over unpopular legislation to expand the role of the Japanese military;Abe isn’t required to hold a general election for another three years. If he stays in office until 2018, he would become the third-longest serving prime minister since World War II

There is no term limits for the prime minister, but a general election of the Lower House will be held at least once in every four years, and a new prime minister will be elected each time by members of the chamber.

“I tried to run for the presidential election, but I was unable to accomplish that,” Noda said. Noda continued her last-minute efforts to garner support from other LDP members but the LDP leadership led by Abe kept putting pressure on them not to support her.

Top LDP executives feared that if Noda succeeded to run, it could trigger internal strife within the party and give ammunition to opposition parties to further delay deliberations on contentious government-sponsored security bills, which are now being deliberated on in the Upper House.

And while Abe’s reign is now literally supreme and unopposed, Japan Times cautions that Abe’s ruling camp is now set to bulldoze the bills through the chamber and have the legislation enacted next week. This is expected to cause a big public stir and will likely push down the Cabinet’s approval rating in media polls.

Whether that means more or less Abenomics, read printing of money to make the rich richer, remains to be seen. Recall on Friday the IMF joined the chorus of warnings that the BOJ’s QQE will soon need to be tapered as Kuroda runs out of willing sellers.

Judging by today’s early market kneejerk reaction, the algos have not gotten the memo.

end

Dead Market Walking – Chinese Stock Trading Volume Collapses To 3 Year Lows

With “selling” outlawed and anything but cheer-leading strocks higher subject to detainment, it appears the Chinese government has managed to undo 3 years of liberalization and financial deregulation in the space of a week. Futures trading volume on the CSI-300 (China’s S&P 500) which for a while in May became the most actively traded financial contract in the world(surpassing S&P 500 e-minis), has utterly collapsed in the last week – since the arrests and detainment of various brokerage executives – to its lowest levels in three years. As one local trader noted – Chinese index futures trading is dead.

In May, CSI-200 Futures were the most actiuvely traded financial instrument in the world – topping S&P e-minis…

But that has all collapsed now to its lowest levels inm 3 years…

in the space of just over a week…

Re-capitalize your zombified over-leveraged SOEs now!!

Charts: Bloomberg

end

WOW!!!!

China spends 600 billion yuan (94.4 billion USA) on its plunge protection team shoring up its worthless stock market.

(courtesy zero hedge)

Back on July 20, Caijing reporter Wang Xiaolu suggested that China Securities Finance – the state-owned plunge protection vehicle – may be set to exit the market. That sent futures plunging and ultimately led to Mr. Wang’s arrest late last month. Under duress, Wang would later “admit” that he “shouldn’t have released a report with a major negative impact on the market at such a sensitive time.”

Of course Wang wasn’t the last person to speculate about how long China would be willing to spend billions propping up the market, and indeed it certainly seems as though Beijing tried to scale back the manipulation two weeks ago only to see the SHCOMP crash 8%, a move which promptly triggered a global rout of epic proportions. One additional 8% decline and a dual policy rate cut later, and CSF was back in the market desperately trying to arrest the inexorable slide ahead of Xi Jinping’s lavish military parade on September 3.

So in case anyone still harbored any doubts about the degree to which China most certainly has not wound down the plunge protection effort, Goldman has updated its analysis on the “national team’s” efforts on the way to concluding that China spent an additional CNY600 billion propping up the market in August.

Here’s Goldman:

In our note: China musings: How much has the government bought in the market? (Aug 5), we estimated potential government purchases in the stock market based on: (1) our top-down liquidity model; and (2) bottom-up analysis on fund flow changes in key investment channels based on public information released by relevant media sources. Our last estimate published in early Aug (based on July month-end data of 5 liquidity factors) was Rmb900bn, largely consistent with the July monetary data release which showed Rmb900bn of non-bank financial institutions lending and we suspect a majority of which went to China Securities Finance Corp (CSFC) which has been directly supporting the market during the correction. Using our top-down model and refreshing inputs based on Aug month-end data, we estimate that the “national team” has spent another Rmb600bn in August, raising the potential aggregate amount of buying to Rmb1.5tn, representing 3.5% and 9.2% of current total and free-float market cap.

And based on history (and probably also based on what we know about China’s unwillingness to relinquish control), the effort isn’t likely to end any time soon:

Overall, we reiterate our view that the lingering market concern over the Chinese government’s potential exit from its market support is probably overdone based on cross-country experiences, including the intervention from HKMA in Aug 1998 and the Quantitative Easing in the US since March 2008.

Speaking of futile attempts on the part of Beijing to manage expectations and get control of a potentially disastrous situation, MNI is out reporting that in the wake of the August 11 deval, SAFE began “urging” Chinese companies to “actively take measures to limit foreign exchange purchase for advance payment under imports… and postpone forex purchases.”

Although MNI does note that this represents more of a tightening of existing measures than it does the imposition of new capital controls, the writing on the wall is clear.That is, it’s all about capital controls at this point (as we tipped last week) as China desperately needs to stem the outward flow if it wants to limit costly interventions to stabilize the yuan, interventions which, as we learned on Monday, led directly to the liquidation of $94 billion in FX reserves during the month of August alone. “SAFE said the focus is outbound direct investment and remitting money overseas. It ordered branches and banks to check whether such investment is genuine, including the source of the money and where the money is being invested,” MNI adds.

As we said earlier this month, “while China is doing everything in its power to not give the impression that it is panicking, the truth is that it is one viral capital outflow report away from an outright scramble to enforce the most draconian capital controls in its history, which – as every Cypriot and Greek knows by now – is a self-defeating exercise and assures an ever accelerating decline in the currency, which authorities are trying to both keep stable while also devaluing at a pace of their choosing. Said pace never quite works out.”

And the same goes for the stock market. The more authorities have to intervene, the more readily apparent it becomes that the market can’t stand on its own which only serves to undermine investor confidence leading to more selling pressure, necessitating still more intervention, until finally, Beijing will either be a majority owner of every mainland listed company or else will simply halt the entire market until such a time as the Politburo believes people’s “malicious” propensity to sell has subsided.

end

Peter Schiff explains perfectly the term: Quantitative Tightening vs QE.

QE allowed nations to massively accumulate dollars (otherwise known as the “great accumulation” to lower its exchange rate to keep their individual countries competitive. The USA dollar would lower due to this massive accumulation by emerging nations plus others. The USA benefited as they had a means of purchase of their bonds as 2007 -2008 saw massive deficits and the need to fund these deficits.

Now the process is reversed as nations must dishoard their bonds. Thus as nations sold their USA treasuries and also the resultant dollar short derivatives, USA dollars must rise in price. This should cause USA longer term interest rates to rise. With the massive cashing in of these bonds, you can say that this is tightening and the reverse of the multiplier effect and thus massive liquidity is withdrawn from the system. The big question that Peter raises is this: who will buy this massive amount of bonds that will be thrust onto the market.

This is an extremely important paper for you to read..

(courtesy Peter Schiff/Euro Pacific Capital)

Peter Schiff Warns: Meet QT – QE’s Evil Twin

Submitted by Peter Schiff via Euro Pacific Capital,

There is a growing sense across the financial spectrum that the world is about to turn some type of economic page. Unfortunately no one in the mainstream is too sure what the last chapter was about, and fewer still have any clue as to what the next chapter will bring. There is some agreement however, that the age of ever easing monetary policy in the U.S. will be ending at the same time that the Chinese economy (that had powered the commodity and emerging market booms) will be finally running out of gas. While I believe this theory gets both scenarios wrong (the Fed will not be tightening and China will not be falling off the economic map), there is a growing concern that the new chapter will introduce a new character into the economic drama. As introduced by researchers at Deutsche Bank, meet “Quantitative Tightening,” the pesky, problematic, and much less disciplined kid brother of “Quantitative Easing.” Now that QE is ready to move out…QT is prepared to take over.

end

Emerging markets are in serious trouble as aggregate demand has fallen off the face of the earth. These guys were already suffering with plunging currencies prior to the Chinese devaluation. On August 11, China devalued which caused further deterioration in the currency rates of our emerging nations such as Mexico, Chile, Columbia, Brazil and Peru. Brazil is no doubt the worse off as their twin deficits (fiscal and currency accounts) go off the charts.

In the following commentary, Goldman Sachs believes that these countries will have to raise interest rates to stem the decline in the currency despite the awful shape that their economy is in.

a must read..

(courtesy Goldman Sachs/zero hedge)

“This Time May Be Different”: Desperate Central Banks Set To Dust Off Asia Crisis Playbook, Goldman Warns

Early last month, Bloomberg observed that plunging currencies were “handcuffing bankers from Chile to Colombia.” The problem was described as follows:

Central bankers in commodity-dependent Andes economies aren’t even considering interest-rate cuts to revive growth, even as prices for oil, copper and other raw materials collapse.

That’s because the deepening price slump is also dragging down currencies in Colombia and Chile — a swoon that’s fanning inflation and tying policy makers’ hands.

That was six days before China’s decision to devalue the yuan.

Needless to say, Beijing’s entry into the global currency wars did nothing to help the situation and indeed, since the yuan devaluation, things have gotten materially worse. The real, for instance, has plunged 10.5%, the Colombian peso is down 6.6%, the Mexican peso is off 4.4%, and the Chilean peso is down a harrowing 8% (thanks copper). And again, that’s just since China’s devaluation.

Meanwhile, plunging commodity prices, falling Chinese demand, and depressed global trade aren’t helping LatAm economies. Just ask Brazil, where the sellside GDP forecast cuts are coming in fast (Morgan Stanley being the latest example) now that virtually every data point one cares to observe shows an economy that’s sliding into depression.

Of course a plunging currency, FX pass through inflation, and a soft outlook for growth is a pretty terrible place to be in if you’re a central bank, but that’s exactly where things stand for the “LA-5”(believe it or not, that’s not a reference to the Lakers, it’s short for Brazil, Chile, Colombia, Mexico, and Peru), who very shortly will be forced to decide whether the risks associated with further FX weakness outweigh those of hiking rates into a poor economic environment.

For Goldman, the outlook is clear: LatAm central banks will, in “stark” contrast to counter-cyclical measures adopted during the crisis, hike in a desperate attempt to shore up their currencies and control inflation.

First, we have the test:

The LA-5 economies are, once again, being tested. They currently face an acute external shock involving a combination of: low (likely for long) commodity prices, incoming monetary policy normalization in the US, and weaker CNY and growth in China with the latent risk of a sharper economic slowdown.

The last time these countries were tested, they had sufficient room to maneuver counter-cyclically:

The Global Financial Crisis of 2008-09 (GFC) provided almost the perfect applied experiment to test the shock-absorbing capacity of the new institutional framework. And the results were remarkably positive. The spike in risk aversion in the initial stages of the crisis was followed by sizeable capital outflows from EMs. Yet, officials across the LA-5 did not attempt to stop the hemorrhage of capital and the ensuing pressures on local currencies by hiking interest rates or by tightening fiscal belts (which would have been the classic pro-cyclical response of the past).To the contrary, the authorities managed to loose fiscal stances and cut interest rates aggressively to support domestic demand, letting exchange rates depreciate significantly along the way.

This time around, however, policy flexibility is severely constrained:

Financial conditions are very accommodative and most currencies are now slightly in undervaluation territory. Initial conditions differ considerably from those prevalent at the beginning of the GFC. Broad financial conditions are, on average, more accommodative today than before (lower real rates and currencies that underwent large adjustments since mid-2013 and are now, on average, slightly undervalued versus domestic fundamentals). Furthermore, with the notable exception of Mexico, inflation has been accelerating across the region (Exhibit 3) and is now tracking above the respective targets, the fiscal stances are on average weaker, and external imbalances are generally wider.

And the crisis – at least as it relates to LatAm, is actually more acute:

Arguably, these combined shocks may pose greater risks to the region compared to the challenges faced during the GFC as the later was largely a DM centered event. In fact, current external headwinds have compounded the effects of domestic developments in places (e.g., Brazil and to some extent Chile), imparting a sizeable adverse shock to sentiment and a negative impulse to growth across the LA-5 economies.

With less policy flexibility and a more acute crisis, comes a divergent response:

Against this backdrop, the continuation of a bearish FX market may be soon followed by higher policy rates, despite admittedly sluggish real business cycles all across the region. That is, a pro-cyclical monetary reaction may be imminent in a number of places – Chile, Colombia, Mexico, and Peru. Policy pro-cyclicality is knocking on the door.

What’s particularly interesting here is that round after round of the type of counter-cyclical policy measures Goldman suggests saved the LA-5 in the wake of the 2008 meltdown have not only failed to resuscitate the global economy, but have in fact contributed to the current worldwide deflationary supply glut that is at least partially to blame for the economic malaise plaguing EMs and the attendant pressure on commodity currencies.

That pressure has now put LatAm’s financially integrated countries in the position of having to hike rates even as the outlook for their economies – the same economies which were presumably saved by counter-cyclical post-crisis measures – deteriorates. Meanwhile, if the Fed hikes, it will only put further pressure on EM FX, which could serve to drive inflation still higher, prompting a still more hawkish EM CB response which would in turn put still more pressure on their underlying economies.

In the end, Goldman concludes that should LatAm resort to pro-cyclical measures to shore up their currencies at the expense of their economies, it will represent a return to the policies adopted by EMs during the Asian Financial Crisis. This would appear to provide the final piece of evidence we need to conclusively determine that all pundit/analyst protestations aside, we have indeed turned back the clock two decades and sit on the verge of another outright emerging market meltdown. And on that note, we’ll give the final word to Goldman:

The LA-5 economies have already spent part of their policy ammunition fighting the initial stages of the current turmoil.In the meantime, a number of economies are still grappling with visible domestic (inflation/fiscal deficits) and external (current account deficits) imbalances. Therefore, the room to ease policy further, i.e., to adopt counter-cyclical policies, is now much more limited than in the past. To the contrary, in some cases monetary tightening may be needed (despite weaker real business cycles) in order to continue to attract foreign capital, anchor domestic currencies and preserve the integrity of the respective inflation targeting frameworks. Hence, we may soon enter a period of weaker FX and higher policy and market rates: i.e., market dynamics thatwould resemble more the 1997 Asian Financial Crisis (where the authorities hiked rates to stabilize the respective domestic currencies despite the recessionary real sector dynamics) rather than the 2008-09 Global Financial Crisis (where weakening currencies coincided with sharply declining short-term interest rates).

end

You will need to read the following passage a few times to understand the importance of what zero hedge and Deutsche bank are stating:

We basically have two entities: the USA (threatening a rate rise and thus tightening) and China (devaluing and thus Quantitative tightening). Both of these countries by tightening are thus “recalling liquidity”. The two other nations who have been adding liquidity, namely the Bank of Japan and the EU are still in QE mode and increase liquidity.

Europe’s Biggest Bank Dares To Ask: Is The Fed Preparing For A “Controlled Demolition” Of The Market

Why did we focus so much attention yesterday on a postin which the IMF confirmed what we had said since last October, namely that the BOJ’s days of ravenous debt monetization are coming to a tapering end as soon as 2017 (as willing sellers simply run out of product)? Simple: because in the global fiat regime, asset prices are nothing more than an indication of central bank generosity. Or, as Deutsche Bank puts it: “Ultimately in a fiat money system asset prices reflect “outside” i.e. central bank money and the extent to which it multiplied through the banking system.“

The problem is that the BOJ and the ECB are the only two remaining central banks in a world in which Reverse QE aka “Quantitative Tightening” in China, and the Fed’s tightening in the form of an upcoming rate hike (unless the Fed loses all credibility and reverts its pro-rate hike bias), are now actively involved in reducing global liquidity. It is only a matter of time before the market starts pricing in that the Bank of Japan’s open-ended QE has begun its tapering (followed by a QE-ending) countdown, which will lead to devastating risk-asset consequences. The ECB, which is also greatly supply constrained as Ewald Nowotny admitted yesterday, will follow closely behind.

But while we expanded on the Japanese problem to comein detail yesterday, here are some key observations on what is going on in both the US and China as of this moment – the two places which all now admit are the culprit for the recent equity selloff, and which the market has finally realized are actively soaking up global liquidity.

Here the problem, as we initially discussed last November in “How The Petrodollar Quietly Died, And Nobody Noticed“, is that as a result of the soaring US dollar and collapse in oil prices, Petrodollar recycling has crashed, leading to an outright liquidation of FX reserves, read US Treasurys by emerging market nations. This was reinforced on August 11th when China joined the global liquidation push as a result of its devaluation announcement, a topic which we also covered far ahead of everyone else with our May report “Revealing The Identity Of The Mystery “Belgian” Buyer Of US Treasurys”, exposing Chinese dumping of US Treasurys via Belgium.

We also hope to have made it quite clear that China’s reserve liquidation and that of the EM petro-exporters is really two sides of the same coin: in a world in which the USD is soaring as a result of Fed tightening concerns, other central banks have no choice but to liquidate FX reserve assets: this includes both EMs, and most recently, China.

Needless to say, these key trends covered here over the past year have finally become the biggest mainstream topic, and have led to the biggest equity drop in years, including the first correction in the S&P since 2011. Elsewhere, the risk devastation is much more profound, with emerging market equity markets and currencies crashing around the globe at a pace reminiscent of the Asian 1998 crisis, while in China both the housing and credit, not to mention the stock market, bubble have all long burst.

Before we continue, we present a brief detour from Deutsche Bank’s Dominic Konstam on precisely how it is that in the current fiat system, global central bank liquidity is fungible and until a few months ago, had led to record equity asset prices in most places around the globe. To wit:

Let’s start from some basics. Global liquidity can be thought of as the sum of all central banks’ balance sheets (liabilities side) expressed in dollar terms. We then have the case of completely flexible exchange rates versus one of fixed exchange rates. In the event that one central bank, say the Fed, is expanding its balance sheet, they will add to global liquidity directly. If exchange rates are flexible this will also mean the dollar tends to weaken so that the value of other central banks’ liabilities in the global system goes up in dollar terms. Dollar weakness thus might contribute to a higher dollar price for dollar denominated global commodities, as an example. If exchange rates are pegged then to achieve that peg other central banks will need to expand their own balance sheets and take on dollar FX reserves on the asset side. Global liquidity is therefore increased initially by the Fed but, secondly, by further liability expansion, by the other central banks. Depending on the sensitivity of exchange rates to relative balance sheet adjustments, it is not an a priori case that the same balance sheet expansion by the Fed leads to greater or less global liquidity expansion under either exchange rate regime. Hence the mere existence of a massive build up in FX reserves shouldn’t be viewed as a massive expansion of global liquidity per se – although as we shall show later, the empirical observation is that this is a more powerful force for the “impact” of changes in global liquidity on financial assets.

That, in broad strokes, explains how and why the Fed’s easing, or tightening, terms have such profound implications not only on every asset class, and currency pair, but on global economic output.

Liquidity in the broadest sense tends to support growth momentum, particularly when it is in excess of current nominal growth. Positive changes in liquidity should therefore be equity bullish and bond price negative. Central bank liquidity is a large part of broad liquidity and, subject to bank multipliers, the same holds true. Both Fed tightening and China’s FX adjustment imply a tightening of liquidity conditions that, all else equal, implies a loss in output momentum.

But while the impact on global economic growth is tangible, there is also a substantial delay before its full impact is observed. When it comes to asset prices, however, the market is far faster at discounting the disappearance of the “invisible hand”:

Ultimately in a fiat money system asset prices reflect “outside” i.e. central bank money and the extent to which it multiplied through the banking system. The loss of reserves represents not just a direct loss of outside money but also a reduction in the multiplier. There should be no expectation that the multiplier is quickly restored through offsetting central bank operations.

Here Deutsche Bank suggests your panic, because according to its estimates, while the US equity market may have corrected, it has a long ways to go just to catch up to the dramatic slowdown in global plus Fed reserves (that does not even take in account the reality that soon both the BOJ and the ECB will be forced by the market to taper and slow down their own liquidity injections):

Let’s start with risk assets, proxied by global equity prices. It would appear at first glance that the correlation is negative in that when central bank liquidity is expanding, equities are falling and vice versa. Of course this likely suggests a policy response in that central banks are typically “late” so that they react once equities are falling and then equities tend to recover. If we shift liquidity forward 6 quarters we can see that the market “leads” anticipated” additional liquidity by something similar.This is very worrying now in that it suggests that equity price appreciation could decelerate easily to -20 or even 40 percent based on near zero central bank liquidity, assuming similar multipliers to the post crisis period.

Some more dire predictions from Deutsche on what will happen next to equity prices:

If we only consider the FX and Fed components of liquidity there appears to be a tighter and more contemporaneous relationship with equity prices. The suggestion is at one level still the same, absent Fed and FX reserve expansion,equity prices look more likely to decelerate and quite sharply.

The Fed’s balance sheet for example could easily be negative 5 percent this time next year, depending on how they manage the SOMA portfolio and would be associated with further FX reserve loss unless countries, including China allowed for a much weaker currency. This would be a great concern for global (central bank liquidity).

Once again, all of this assumes a status quo for the QE out of Europe and Japan, which as we pounded the table yesterday, are both in the process of being “timed out”

The tie out, presumably with the “leading” indicator of other central bank action is that other central banks have been instrumental in supporting equities in the past. The largest of course being the ECB and BoJ. If the Fed isn’t going doing its job, it is good to know someone is willing to do the job for them, albeit there is a “lag” before they appreciate the extent of someone else’s policy “failure”.

Worse, as noted yesterday soon there will be nobody left to mask everyone one’s failure: the global liquidity circle jerk is coming to an end.

What does this mean for bond yields? Well, as we explained previously, clearly the selling of TSYs by China is a clear negative for bond prices. However, what Deutsche Bank accurately notes, is that should the world undergo a dramatic plunge in risk assets, the resulting tsunami of residual liquidity will most likely end up in the long-end, sending Treasury yields lower. To wit: