Good evening Ladies and Gentlemen:

Here are the following closes for gold and silver today:

Gold: $1102.40 down $18.20 (comex closing time)

Silver $14.57 down 18 cents.

In the access market 5:15 pm

Gold $1106.50

Silver: $14.65

First, here is an outline of what will be discussed tonight:

At the gold comex today we had a poor delivery day, registering 4 notices for 400 ounces Silver saw 3 notices for 15,000 oz.

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 219.98 tonnes for a loss of 83 tonnes over that period.

In silver, the open interest fell by 1891 contracts despite the fact that silver was up in price by 21 cents yesterday. Again, our banker friends used the opportunity to cover as many silver shorts as they could but failed. The total silver OI now rests at 155,615 contracts In ounces, the OI is still represented by .778 billion oz or 111% of annual global silver production (ex Russia ex China).

In silver we had 3 notices served upon for 15,000 oz.

In gold, the total comex gold OI surprisingly rose to 421,732 for a gain of 2,730 contracts. We had 4 notices filed for 400 oz today.

We had no changes in tonnage at the GLD today/ thus the inventory rests tonight at 682.59 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold. It sure looks like 670 tonnes will be the rock bottom inventory in GLD gold. It looks to me that China has taken the last amounts of physical gold from the GLD. I guess the only place left for China to receive physical gold will be the FRBNY and the comex. In silver, we had a big withdrawal in silver inventory at the SLV to the tune of 1.336 million oz/Inventory rests at 322.06 million oz.

We have a few important stories to bring to your attention today…

1. Today, we had the open interest in silver fall by 1891 contracts up to 155,615 despite the fact that silver was up by 21 cents in price with respect to yesterday’s trading. The total OI for gold rose by 2739 contracts to 421,732 contracts, despite the fact that gold was down by 20 cents yesterday.

(report Harvey)

2.Gold trading overnight, Goldcore

(/Mark OByrne)

3. Trading overnight from Japan

4. Trading overnight from China.

5. You have to love this guy Gartman. Last night he covered his short position on the markets and then went long..just in time to lose a fortune again as the Dow plummeted

(zero hedge)

6. World bank economist warns the USA not to raise interest rates on Sept 17.

7.Willem Buiter states that only “Helicopter Money” can save the world

(Citibank/Buiter)

8.David Stockman puts everything into perspective with respect to Japan’s collapsing economy, China’s imploding economy together with the massive liquidation of USA treasuries from the entire globe

(David Stockman/Contra CornerBlog)

9. Spain votes on Sept 27 for independence. The Spanish defense minister warns that he may have to call in the army to defend Spain.

Unbelievable!!

(zero hedge)

10. The Mises institute economist, Wilson states that the Greek government should repudiate their debt

(Mises Institute/Wilson)

11. Russia continues to supply armaments to Syria and they are warned by the USA. Showdown coming

(zero hedge)

12. Turkey now closer and closer to civil war as citizens torch Kurd operations in Istanbul, Izmir, Ankara and southern cities

(zero hedge)

13. USA stories/Trading of equities NY

a) Puerto Rico will run out of cash by either year end or the latest in June 2016. trouble ahead! (zero hedge)

b) the JOLTS report shows a big increase in job openings. This is the figure that Janet Yellen likes to show that slack in the job market is waning

(JOLTS/zero hedge)

c First off today, it was World Bank Economist Basu who stated that the USA should not raise interest rates on Sept 17. Later in the day it was Keynesian and Nobel prize winner Krugman also stated that the raising of USA rates will be harmful

(Paul Krugman/zero hedge)

d) Dave Kranzler talks about the USA’s latest retail sales reporting:

(Dave Kranzler/IRD)

14. Physical stories:

- Something snapped at the comex (zero hedge)

- One commentaries on the faulty data at the comex (Dave Kranzler IRD)

- One commentary explaining the high ratio of paper gold to real gold at 207/1

- Greg Hunter interviews David Morgan who states categorically that the silver market has seized up.

- The Indian government again is trying to coax its citizens to give up their physical gold to receive paper gold and an interest rate on that. Good luck to them. They fail each time they try (Bloomberg)

- Bill Holter’s commentary tonight is titled: “The Breaking Point?”

- Peter Hambro explains to Bloomberg that there is a difference between paper gold and real gold (Bloomberg/Peter Hambro)

- Silver premiums rising exponentially/Profit Confidential

and well as other commentaries…

Let us head over and see the comex results for today.

September contract month:

Initial standings

September 9.2015

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 229.645 oz

Manfra, Scotia |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 4 contracts (400 oz) |

| No of oz to be served (notices) | 211 contracts (211,000 oz) |

| Total monthly oz gold served (contracts) so far this month | 16 contracts(1,600 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil |

| Total accumulative withdrawal of gold from the Customer inventory this month | 153,840.9 oz |

Total customer deposit: nil oz

JPMorgan has only 0.6133 tonnes left in its registered or dealer inventory. (19,718.722 oz) and only 863,683.63 oz in its customer (eligible) account or 26.86 tonnes

September silver initial standings

September 9 2015:

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory | 1,843,791.062 oz

(CNT,Scotia) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,197,145.082 JPMorgan |

| No of oz served (contracts) | 3 contracts (15,000 oz) |

| No of oz to be served (notices) | 700 contracts (3,500,000 oz) |

| Total monthly oz silver served (contracts) | 807 contracts (4,035,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | nil |

| Total accumulative withdrawal of silver from the Customer inventory this month | 7,865,087.3 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit; 0 oz

total customer deposits: 1,197,145.082 oz

total withdrawals from customer: 1,843,791.062 oz

And now SLV:

Sept 9.2015:

we had another huge withdrawal of 1.336 million oz of silver from the vaults of the SLV/Inventory rests at 322.06 million oz

Sept 8/we had a huge withdrawal of 1.524 million oz of silver from the SLV/Inventory rests tonight at 323.396 million oz.

Sept 4.2015:no changes in inventory at the SLV/rests tonight at 324.923 million oz

sept 3/we had a small withdrawal of 140,000 oz of silver from the SLV/Inventory rests at 324.923 million oz

Sept 2: we had a small withdrawal of 859,000 oz of silver from the SLV vaults/inventory rests tonight at 325.063 million oz

September 1/no change in inventory over at the SLV/Inventory rests tonight at 325.922 million oz

August 31.a huge addition of 954,000 oz were added to inventory today at the SLV/Inventory rests at 325.922 million oz

August 28.2015: no change in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 27.no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 26.2015/no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 25.2015:no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 24./no change in inventory at the SLV/Inventory rests at 324.698 million oz

August 21.2015/ no change in inventory at the SLV/Inventory rests at

324.698 million oz

August 20.2015:/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

August 19/no changes in inventory at the SLV/Inventory rests tonight at 324.698 million oz

Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to CentralGoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64) Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis. Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer. Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer. * * * * *

(courtesy/Mark O’Byrne/Goldcore)

Please note:

1.the huge increase in UK household debt

2. in London the huge 5% premium on gold bullion USA eagles and 8,5% on sovereigns, 4% on Krugerrands and Canadian maples

3. in silver, premiums on regular bars: 9.5%

4. in silver, silver maples are 32% ie. spot plus $4.75 and the huge delays in receiving them.

Britain’s £173 Billion “Debt Timebomb”

UK households are sitting on a £173 billion debt time bomb after once again being lured into a spending splurge by banks and credit card companies.

The startling rise in debt levels due to people splashing out on new cars, TVs, conservatories, luxury items, consumer goods and home improvements was uncovered in an investigation by Money Mail.

With a rise in interest rates imminent for the first time in more than eight years, fears are growing that many families will be left struggling with repayments.

The amount of borrowing being taken on by households continues to grow at a startling rate, spurred on by hundreds of offers for credit cards and loans.

Bank of England governor Mark Carney has sent a letter to all fund managers asking for reassurance they are able to deal with an anticipated rush of investors making emergency cash withdrawals to cover their mortgages and other debts.

Read full This Is Money article

DAILY PRICES

Today’s Gold Prices: USD 1122.30, EUR 1002.50 and GBP 730.38 per ounce.

Yesterday’s Gold Prices: USD 1120.85, EUR 1003.49 and GBP 728.27 per ounce.

(LBMA AM)

Note: Premiums on gold have remained steady but silver premiums continue to move higher – especially on silver eagles.

Gold has moved marginally lower today but remains just above $1,120 per ounce, not far from where they were this time yesterday, after they snapped four days of losses yesterday to rise 0.2%.

Gold in Singapore was marginally lower and in early European trading as it gave up the gains from yesterday. Lacklustre trading continues and gold remains locked in a tight $19 range between $1,117.50/oz and the high yesterday of $1,126.30/oz for the last three days.

Silver is down 0.3%, after it outperformed yesterday rising 1.8%, its biggest one-day rally in nearly two weeks.

Platinum’s down 0.3%, and palladium is up 0.6% up for a third day and up 11% in recent days as it bounces from five year lows.

IMPORTANT NEWS

Gold Climbs for Second Day on Dollar Weakness Amid Asian Rally – Bloomberg

Gold firms above 3-wk low as traders await Fed’s rate view – Reuters

Gold prices gain in Asia as investors cautious ahead of Fed next week – Investing.com

Palladium Poised for Biggest Gain This Month on Supply Threat – Bloomberg

Treasure hunter says he has found 100 tons of Soviet gold hidden from Nazis during WWII – RT Question More

IMPORTANT COMMENTARY

Platinum upgrade to golden reserve status seen as monetary alchemy – Reuters

Advice to Putin: Default on foreign debt, put reserves into gold and BRICs bonds – Goldseek.com

When Governments mess with the price of money… – Casey Research

Britain sitting on a £173bn debt time bomb – and with rates set to rise its ticking even louder – The Mail Online

Isle of Man tax haven with tailless cats becomes Bitcoin hub – Bloomberg

end

I brought this to your attention last night with the release of inventory movements. Needless to say, is the fact that gold is bleeding from the comex and they may not have enough registered or “for sale’ gold to cover what is asked for delivery in Oct, November and December:

(courtesy zero hedge)

Something Just Snapped At The Comex

Just over one month ago, when looking at the latest changes in registered gold held at the Comex ,we were stunned not only by the collapse in this series to a record low of just over 350k ounces or barely over 10 tons, but also by the surge in “gold coverage”, or the amount of paper gold claims on physical gold, which exploded to a record high 124 per ounce.

This is what we said on August 3:

While on its own, gold open interest – which merely represents the total potential claims on gold if exercised – is hardly exciting, as we have shown previously it has to be observed in conjunction with the physical gold that “backs” such potential delivery requests, also known as the “coverage ratio” of deliverable gold.

It is here that things get a little out of hand, because as the chart below shows, all else equal, the 43.5 million ounces of gold open interest and the record low 351,519 ounces of registered gold imply that as of Friday’s close there was a whopping 123.8 ounces in potential paper claims to every ounces of physical gold.

This is an all time record high, and surpasses the previous period record seen in January 2014 following the JPM gold vault liquidation.

Another way of stating this unprecedented ratio is that the dilution ratio between physical gold and paper gold has hit a record low 0.8%. Indicatively, the average paper-to-physical coverage ratio since January 1, 2000 is a “modest” 19.1x. As of Friday it had soared to more than 6 times greater.

We showed this record surge in gold claims as follows:

But if last month was shocking, then what the COMEX revealed yesterday was absolutely jaw-dropping.

Here is the most recent update provided by the CME on eligible and registered gold.

What it reveals is that while JPM saw another 90,000 ounces of gold once again withdrawn from its vault, this time in the eligible category, for some reason a whopping 121,124 ounces of registered gold were reclassified as eligible. In doing so, JPM’s registered gold (red line in chart below) tumbled to a record low of just 19,718 ounces – an 86% collapse in just one day – and well under 1 ton of gold, some 600 kilos of physical gold available to meet delivery requests to be specific!

JPM’s dramatic adjustment also meant that total Comex registered gold has likewise tumbled to the lowest in history of just 202,054 ounces – just over 6 tons – available for delivery.

Zooming in only on the registered gold since 2014:

Not surprisingly, the latest collapse in registered gold took place while the gold open interest remained flat, and in fact has been modestly rising in the past year as seen below:

Which brings us to the punchline chart: the Comex gold “coverage” ratio, or the amount of paper claims for every ounce of physical. As of Friday this number was literally off the chart (it would not have fit on the chart below), soaring to a mindblowing 207 ounces of paper gold claims for every ounce of deliverable gold. This also means that the dilution ratio between physical gold and paper gold has hit a new all-time low of just 0.48%!

And while we know what caused this epic surge in potential claims on gold – namely the relentless outflow in registered gold – what we don’t know is whether this is a systemic event, one which threatens the next Comex gold delivery request with an “insufficient product” response, and a potential default, or simply a one day abnormality.

What we do know is that, if only for one day, something at the Comex has snapped.

We will keep a close eye on today’s Comex update to see if JPM reverse this “adjustment” and adds at least a few more tons of deliverable gold to its vault, and if not, perhaps a phone call or two may be in order.

Anyone Who Believes The Comex Numbers Is Very Naive

“The information in this report is taken from sources believed to be reliable; however, the Commodity Exchange, Inc. disclaims all liability whatsoever with regard to its accuracy or completeness. This report is produced for information purposes only.” – disclaimer now posted on the Comex gold and silver daily warehouse stock report as of Monday, June 3, 2013 – Investment Research Dynamics – June 4, 2013

Yesterday I published an article detailing the Comex gold futures to deliverable physical gold ratio that is now north of 200:1. But an erudite colleague of mine, John Titus of “Best Evidence,” correctly pointed out that: “They are probably bluffing. In other words, the real number is significantly higher than 200:1.”

For the record, John does more thorough research on the economic numbers and reports that he studies than anyone I’ve ever come across. And he does it with the trained analytic eye of a seasoned patent litigation attorney.

Let’s put everything in perspective. The numerical reports from which fancy graphs and and dry detailed data presentations are created originate from the Too Big To Fail Banks. I’ve said for quite some time that IF the bullion banks who control the Comex and the LBMA are submitting honest data reports for the Comex and LBMA, it would be the only business line in which they do not hide the truth and report fraudulent numbers. What is the probability of that?

JP Morgan was recently caught stuffing proprietary Comex futures short-sell trades into the “Managed Money” account category of the COT report. The CFTC scolded JPM and slapped them with a whopping $650,000 – LINK. Does anyone really believe that the CFTC wrist-slapping corrected any fraudulent data reporting by the likes of JP Morgan? Really?

Put your “think like a criminal hat” on for a moment. You know that the people who care about this sort of thing already know that the there’s a paper vs. physical problem in the market. So just show them a number that they’ll buy into and that will be “the number.” Most analysts will accept that number at face value and use that in their articles and blog posts. That number then becomes accepted in goldbug circles as the “real” number.

But the truth of the matter is that they are more than likely reporting numbers they want us to see, not the real numbers. For instance, the silver market is now seizing up from lack of supply. Please see this report from Greg Hunter and David Morgan if you are still skeptical: Retail Silver Has Seized Up.

Yet, the Comex bank custodians are reporting over 51 million ounces of silver available fore delivery – LINK. In fact, CNT – an official supplier to the U.S. mint – is showing 13.3 million ounces of deliverable silver. So why is there’s a shortage of silver at the U.S. mint? IF that silver were actually in the vault, the U.S. mint could buy a spot contract – September has a silver contract open – and take immediate delivery.

Also, why did the CME, unannounced, start slipping that little accuracy disclaimer into its daily gold and silver inventory reports in 2013? I’ll let you draw your own conclusion about the truth.

The silver market is seizing up which means that there’s a severe shortage of silver available. It is also showing up in the LBMA wholesale market based on the backwardation in gold and silver forward contracts that have been observed for several weeks. It means that any visible inventories reports from ETFs and Comex/LBMA banks custodial vaults are fraudulent. That includes SLV reports.

It also means that the recent discovery that the LBMA altered its gold refining flow statistics, revising what was originally reported to be 6,601 tonnes of gold cleared by the LBMA in 2013 down by 2,000 tonnes to 4600 tonnes, are likely off the mark. That’s a big miss, given that the total global mine production annually is around 2500 tonnes.

The significance of this is that it’s easier to explain how 4600 tonnes of gold was refined into bars and sent to Asia than 6600 tonnes, given that the total global supply of gold from mine production + scrap production was reported to be slightly more than 3000 tonnes.

From where did that extra 1600 tonnes come? The REAL question is, from where did the extra 2600 tonnes come if we use the original number? And is the 6600 tonne number a good number? Was the real number even higher?

The obvious conclusion is that the supply deficits in gold and silver are being remedied by hypothecating gold and silver bars from allocated accounts held at bullion banks, including the accounts held in behalf of the gold/silver ETFs, like GLD and SLV. This is why ABN Amro and Rabobank stopped allowing their physical gold account investors to take physical delivery of the gold they thought they have invested in – the gold was not there to deliver. This also occurred in 2013.

Now for the final blow to any skeptics. You’ll note that the LBMA revised down the amount of gold it cleared from refineries in 2013. But you’ll also note that the Comex inventory report disclaimer at the top of this post was first inserted into the daily Comex inventory reports in June 2013. See any coincidences? Bueller…

Bill Murphy and GATA have maintained for years that the fraud and corruption in the precious metals market would eventually be revealed as the biggest financial fraud scheme in history. It would seem that the cracks in the wall of this scheme are growing wider and it’s becoming easier to see rays of truth.

History tells us that all Ponzi schemes and market interventions fail. I believe we are on the cusp of a massive failure in the scheme to cover up the truth about the precious metals market.

end

(courtesy Dave Kranzler /IRD)

The Comex Is Facing A Gold Crisis

Sure, you can’t eat a bar of gold and it just sits in storage like a Pet Rock that’s been cast aside by its bored owner. But try selling the Indians or Chinese a paper gold bar and see how far you get. You might end up with a knife in your forehead.

The stench has been growing stronger by the day. Many of us have been writing for years about the extreme imbalance between the paper futures open interest vs. the underlying amount of gold being reported as available for delivery. The latest disclosure from the CME is that the ratio of paper gold vs. the amount of deliverable ounces has spiked to over 200:1.

As of last Friday, JP Morgan had 89.4k ounces withdrawn from the “customer”/ eligible account in its vault and it moved 122k ounces of gold from its “deliverable”/ registered account into its customer account. What the true nature of those transactions were – i.e. who the counterparties were and did in fact any real gold actually leave JP Morgan’s gold vault – is anyone’s guess due the intentional opacity of disclosure on the Comex.

But the bottom line is that, as of last Friday, the Comex vaults collectively now show 202k ounces of gold in the “registered” / deliverable accounts of the Comex vault custodians. As of today’s trading, the “preliminary” gold futures open interest rose to 419k contracts representing 41.9 million ounces of paper gold. This would, preliminarily, put the ratio of paper gold to deliverable physical gold at an astonishing 207:1 ratio.

The amount of “deliverable” gold on the Comex is the lowest that I’ve seen it in the time I’ve been following the Comex data avidly since 2002. Please note that the preliminary open interest is almost always revised, most typically a bit lower, by the time the Final report is issued the next day. But based on many years of tracking this data, it is likely that any revision will not move the “needle” on that 207:1 ratio by much in either direction.

Nothwithstanding all the other information contained in this disclosure, this number represents the confirmation that the Comex is nothing more than a pure paper gold market. It’s nearly 100% derivatives. It’s the imposition of derivatives by the Fed and the U.S. Treasury – via their agent bullion banks – on the gold market in order to control the pricing discovery mechanism.

In other words, the Comex gold market is now a 100% artificial gold market.

I find it it quite interesting that the elitists overseeing this operation on the Comex are willing to advertise the 200:1 paper:gold ratio when they have the means at their disposal to hide that number or to make it look a lot smaller.

There’s some kind of message they’re sending to anyone who cares about this sort of thing. It’s either “f*ck you” we’re in control” or “help, we’re in trouble on our paper gold short position.” Or a combination of both.

The implications embedded in all three of those possibilities are quite horrifying to contemplate.

It’s quite obvious that there’s a problem with the supply of physical gold that is readily available for delivery. The same is true of the retail silver market, in which available supply at the retail level shrinks by the day. Premiums on a simple roll of 20 silver eagles are now over $5 at big coin dealers claiming to have inventory. Most dealers have been wiped out of most if not all of their entire inventory of silver SKU’s.

In my opinion, that head-splitting 200:1 ratio of paper to deliverable gold on the Comex is the surest sign that the market for gold and silver is in crisis mode. The term “crisis” also describes the state of condition of the U.S. stock market and, ultimately, the entire current U.S. financial and economic system.

end

My goodness, we must be hitting home: mainstream is beginning to get the idea that there is a difference between paper gold and real gold

(courtesy Bloomberg/Peter Hambro)

Mining exec Hambro tells Bloomberg that ‘paper gold’ isn’t real metal

Submitted by cpowell on Wed, 2015-09-09 15:05. Section: Daily Dispatches

11:04a ET Wednesday, September 9, 2015

Dear Friend of GATA and Gold:

Mining entrepreneur Peter Hambro, founder and chairman of the Russian mining firm Petropavlovsk, today explained to a couple of Bloomberg Television journalists the difference between “paper gold” and real metal in hand. The former, Hambro noted, carries serious counterparty risk. Hambro also noted that central banking has turned into the propaganda business, the business of “managing expectations.”

The interview with Hambro is a little less than 5 minutes long and can be viewed at the Bloomberg News Internet site here:

http://www.bloomberg.com/news/videos/2015-09-09/is-gold-still-a-safe-hav…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The Indian government continues to try and confiscate the wealth of its citizens’ gold. This scheme is 4 years old and every time they try it, the citizens say absolutely no, “we are not handing in our physical gold to receive paper gold”

(courtesy GATA/Bloomberg)

Indian government approves scheme for paperizing gold

Submitted by cpowell on Wed, 2015-09-09 15:33. Section: Daily Dispatches

India’s Modi Moves Closer to Tapping Gold Hoard to Cut Imports

By Bibhudatta Pradhan and Swansy Afonso

Bloomberg News

Wednesday, September 9, 2015

India moved a step closer to selling gold-backed bonds and allowing banks to tap idle jewelry and bars held by households and temples to cut reliance on imports.

Prime Minister Narendra Modi’s cabinet today approved the gold monetization plan and sale of sovereign bonds by the Reserve Bank of India, the government said in a statement. The plans were announced by Finance Minister Arun Jaitley in February as measures to woo Indians away from physical gold. …

The monetization plan will allow Indians to deposit their jewelry or bars with banks and earn interest, while the banks will be free to sell the gold to jewelers, thereby boosting supply. The deposits can be for a period of one year to 15 years with the interest on short-term commitments to be decided by the banks and those on long-term deposits by the government in consultation with the central bank. …

The plan may fail to draw people in large numbers because of Indians’ inherent love for holding physical gold and low interest rates likely to be offered by the banks.

Inadequate banking facilities in rural India, which makes up for 60 percent of physical gold demand, may also scupper the plan, according to the All India Gems & Jewellery Trade Federation.

“The schemes will succeed only if the banks offer interest rates of about 2.5 percent and do not require customers to declare the source of deposited gold below a certain limit,” Bachhraj Bamalwa, director of the federation, said by phone from Kolkata. “Indians’ love for physical gold and investment sentiment in the rural areas, which do not believe in such investment products, will determine the success of the plans.”

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2015-09-09/india-s-modi-moves-clo…

end

Silver premiums skyrocketing (spot plus 32%)

(courtesy Profit Confidential)

Silver Price Forecast: Rush to Physical Silver Indicates System is On the Verge of Economic Collapse

![]() By • Wednesday, September 9, 2015

By • Wednesday, September 9, 2015

There is no doubt that silver prices have been crushed in recent years. Since its peak of around $50.00 per ounce in April 2011, the silver spot price has plunged more than 70% to $14.55. However, to establish an outlook for the price of the grey metal, we have to set one thing straight first: what do we mean by silver price?

There is no doubt that silver prices have been crushed in recent years. Since its peak of around $50.00 per ounce in April 2011, the silver spot price has plunged more than 70% to $14.55. However, to establish an outlook for the price of the grey metal, we have to set one thing straight first: what do we mean by silver price?

You see, silver trades on many different venues. You can get paper silver on futures exchanges such as COMEX; you can buy silver exchange-traded funds (ETFs) on stock exchanges; or you can get physical silver from your local bullion store. To me at least, the real price of silver should be the price you pay to get the physical metal into your vault.

And on that front, here is an interesting pattern about the different silver prices:

The phenomenon we see is this: the premium of 90% silver coins over the spot price of silver has been surging. Sure, these silver coins seem to have always commanded a higher price than the spot price. But since June 2015 the price difference has been expanding quite dramatically. In two months, the premium of 90% silver coins over spot has more than doubled from below 10% to 22%!

What this high premium reflects is the tight conditions in the physical market where demand outweighs supply. In July, the U.S. Mint reported that the popular 2015 American Eagle silver bullion coins were sold out due to “significant demand.” In June, silver coin sales totaled 4.84 million ounces, more than double the amount sold in May. (Source: Reuters, last accessed September 8, 2015.)

Sponsored Content: (Video) Dow Jones 7,000 Trigger Leaked by 28-year Old Stock Research Firm

Mind you, it is not just silver bullion that investors are chasing after. According to the Silver Institute, consumer demand for silver jewelry in the U.S. “increased significantly” in the first half of 2015. Through the end of May, the U.S. imports of silver jewelry surged 11%. For the entire year of 2015, GFMS Thomson Reuters expects silver jewelry to grow by five percent globally. (Source: The Silver Institute, last accessed September 8, 2015.)

The chart above shows that investors are nervous about the state of the financial system. Rather than hope for a paper (or digital) promise in the future, buyers would rather have the real thing in their hands. When investors are not even willing to wait a few weeks for delivery, it’s a clear sign the system is on the verge of economic collapse.

There you have it; unlike the price of paper silver, the price of silver bullion better reflects the forces of supply and demand in the marketplace. And from what we are observing right now, demand has been strong and a big squeeze is coming.

end

Greg Hunter talks with David Morgan who states that the silver market is seized up:

Retail Silver Market Has Seized Up-David Morgan

By Greg Hunter’s USAWatchdog.com

By Greg Hunter’s USAWatchdog.com

Silver expert David Morgan says prices of the white metal may be low, but demand is huge. Morgan explains, “I did a survey of many of the top wholesalers and retailers in the country and came to the conclusion that the retail side of the market has basically seized up. One of the biggest mints in the U.S. is backlogged about 4 million ounces. You have two other main government mints that are basically on halt and not producing, or trying to catch up. You have huge premiums in the silver bar market and extremely high premiums in the silver bag market, or what is referred to in the industry as junk silver. Dealers are paying $5 above spot to source silver bags. What that equates to for the cost of silver is about $19.25 an ounce, and we are in the mid-$14 range for an ounce of silver. So, obviously, there is a huge demand that cannot be met with the current supply in the retail market.”

Morgan also says silver is an inflation adjusted deal. Morgan contends, “The average mining cost used to be about $22 an ounce, but with the oil price dropping, it’s now about $15. In most cases, you are buying it for less than the best producers on the planet can produce it for. . . . We are basically at the same price, using the true money supply, when it was $5 silver in the early 2000’s. So, if you look at all the fiat currency floating around now, and you use that metric, you are buying silver at the same price (inflation adjusted) as you were in the early 2000’s.”

So, why all the demand? It could be fear of what is coming, and Morgan thinks what is coming is the same thing that has happened to Argentina when its currency crashed. Morgan explains, “People lost their bank savings. People lined up in the street and grabbed pots and pans and spoons and go to the banks at lunchtime and, in unison, pound on the bank in protest. People took to the streets. 40% of the middle class became below the poverty line. You could not access your savings. You could go to the bank, but you could only withdraw a certain amount. Sound familiar? It’s exactly what happened Greece. There were many people unemployed and people taking to the streets saying that they were victims of the IMF (International Monetary Fund). . . . The U.S. could turn into Argentina, and I believe it will happen. Why did this happen in Argentina? Overspending–this is the bottom line of why it took place.”

On the Fed raising interest rates, Morgan says, “I think they will, and they are going to show how tough the Fed is and that they do what they say. They are going to raise them a quarter of a point. It’s a very small amount. It’s not like they are going to raise interest rates up to 4% or 5%. That would be devastating, and that is not going to happen.”

The main problem America and the world has is what Morgan calls “the debt bomb.” He says the debt is at the center of the black hole of our problems. Morgan explains, “We are reaching a limit. All systems reach a limit. No tree grows to the sky.”

In March, Morgan predicted September as a time of increasing turmoil in financial markets and thinks it’s downhill from here. On the continuing turmoil, Morgan says, “It will be ebb and flow, but the trend is increasing, increasing and increasing. It will, unfortunately, in my strong opinion, it will get worse before it gets better.”

Join Greg Hunter as he goes One-on-One with David Morgan of Silver-Investor.com.

(There is much more on the video interview.

There is free information on the home page of Silver-Investor.com. You can also buy a subscription to get David Morgan’s detailed market analysis by (clicking here.) If you would like to buy a copy of“The Silver Manifesto,” (click here.)

end

And now Bill Holter…

1 Chinese yuan vs USA dollar/yuan lowers in value, this time at 6.3667/Shanghai bourse: green and Hang Sang: green

Surprisingly, last week, officially, China added another 19 tonnes of gold to its official reserves now totaling 1677.

2 Nikkei up 1343.43 or 7.71.%

3. Europe stocks all in the green (on USA/Yen ramp) /USA dollar index up to 96.28/Euro up to 1.1150

3b Japan 10 year bond yield: rises to .366% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 120.69

3c Nikkei now above 18,000

3d USA/Yen rate now well above the important 120 barrier this morning

3e WTI: 45.25 and Brent: 48.83

3f Gold down /Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund rises to .693 per cent. German bunds in negative yields from 4 years out

Greece sees its 2 year rate falls to 10.32%/Greek stocks this morning up by 3.11%: still expect continual bank runs on Greek banks /

3j Greek 10 year bond yield falls to : 8.78% (ridiculous!!)

3k Gold at $1120.00 /silver $14.71 (8 am est)

3l USA vs Russian rouble; (Russian rouble down 6/100 in roubles/dollar) 68.01,

3m oil into the 45 dollar handle for WTI and 48 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9773 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0897 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund now enters in negative territory with the 10 year moving further from negativity to +.693%

3s The ELA lowers to 89.1 billion euros, a reduction of .6 billion euros for Greece. The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Greece votes again and agrees to more austerity even though 79% of the populace are against.

4. USA 10 year treasury bond at 2.22% early this morning. Thirty year rate below 3% at 2.996% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Risk-On Euphoria: Japan’s Nikkei Soars 7.7%, Biggest One Day Move In Seven Years; Futures Surge

And to think all it took was Gartman going short of stocks in 25% correction terms yesterday…

Yesterday morning we remarked that while China staged a massive intervention in the market in the last hour of trading to push stocks higher, it came far too late to benefit Japan’s Nikkei 225, which closed red for the year, just before a dramatic move lower in the Yen prompted by the latest Chinese intervention. Because it was just after yesterday’s Nikkei close that we saw the coordinated effort of Chinese and Japanese authorities send the world’s carry trade, the USDJPY, soaring by over 100 pips, and combined with today’s latest jump of over 50 pips, the result has been nothing short of a near-record one-day move in the Japanese Nikkei stock average, which jumped the most in nearly seven years in percentage terms, and the biggest point move in over 21 years.

The Nikkei Stock Average surged 7.7%, or 1343.43 points, to 18,770.51, marking the benchmark’s biggest daily percentage gain since October 2008. In point terms, it was the biggest gain since January 1994.

In addition to the central bank intervention to push the USDJPY higher over the past 24 hours, a major catalyst of the move was short covering. According to Mizuho’s head of equity research, Yoshihisa Okamoto, hedge funds shorted Japanese index futures Tuesday afternoon speculating that Chinese stocks would fall after weak trade data, and are pushing Japan shares higher Wednesday as they close out positions. In other words, China’s terrible trade data was just the equity surge catalyst the world needed.

Mizuho added that hedge funds had used Japanese futures as China proxy because regulations restrict their mainland trading, and very much incorrectly observed that “investors also closing out shorts amid growing speculation that BOJ will add to easing.” Needless to say, not only will the BOJ not boost QE, but as a result of no marginal sellers, will soon be forced to taper it. But for now, price action dictates the newsflow, and certainly logic, and after a 7.7% move, there is no logic left.

Meanwhile, a modest two day rebound is all China needed to proclaim the “systemic financial risk” over:

Supposedly this means no more monetary easing or market intervention, right? Yeah, that’s what we thought…

The ongoing intervention in China where the Composite closed +2.3% now that index futures no longer trade, and Japan’s mega short squeeze unleashed the biggest jump in the MSCI Asia-Pacific index since September 2011, pushing equities higher across the board. There were also broad based gains across the region’s bourses with the ASX 200 (+2.1 %) and Hang Seng (+4.1 %) up on increased speculation of additional measures after yesterday’s weak trade data.

JGBs traded lower as strength in equities dampen demand, while the BoJ also entered the market to purchase JPY 780b1n in government bonds ranging between 5yr to the super long end. In other meaningless from a trading standpoint news, Japan PM Abe said he will reduce corporate tax next year by a minimum of 3.3 percentage points and could seek a larger reduction if feasible. Considering Japan’s actual underlying economy is in a tailspin, and about to undergo its 5th recession since Lehman, we somehow doubt any Japanese predictions and plans, especially those about the future, will hold.

Asia’s euphoria carried over into Europe where stocks opened broadly higher, in reaction to the bolstered sentiment, with Asian equity indices rallying to see the Nikkei 225 posted its largest gain in a session since 2008. Despite opening sharply lower in reaction to the pick-up in sentiment, Bunds have gradually come off the worst levels throughout the European morning as stocks pared part of the initial gains, but remain in the red as supply factors keep prices lower.

Europe’s Stoxx 600 rises 2.1% as of 12:30 pm CET time on volume that is ~105% of the 30-day average, tracking a sharp rally on Wall St and in Asian shares. Europe’s basic resources sector leads rally, up 4.1%; still down ~16% YTD, Europe’s worst sector performance so far in 2015. Despite this week’s gains, Stoxx 600, S&P 500 have not yet retraced 50% of July-August slump. German 2025 Bond Sale Yield 0.69% Vs. 0.61% Prior Auction

In FX, JPY continues to trade weaker across the board in reaction to the overnight announcement by PM Abe to cut corporate tax next year, with USD/JPY above 120.00 and in close proximity to the 200DMA line . The optimism filtered through to money market rates, where the 2y swap rate fell to its lowest since early January amid expectation of more aggressive policy easing measures.

Elsewhere, AUD continued to consolidate above 0.7000 level , as commodity sensitive currencies benefited from the pick-up in copper prices and expectation of further accommodation by China.Also of note, GBP/USD tested the 200DMA level to the downside following the release of disappointing industrial and manufacturing production reports, with the ONS attributing the drop to decline in motor vehicle output.

But keep a close eye on the USD: last night Krugman joined Goldman in saying he doesnt think the Fed will hike rates next week: “I don’t think they are moving next week,” economist Paul Krugman says at conference in Tokyo on Wednesday when asked about timing of possible interest rate increase by U.S. Federal Reserve.

“I still think it would be a terrible mistake to move. But I’m not confident that they won’t make a mistake.” Krugman added that the Fed keeps sounding like it’s eager to raise rates. “It’s almost as if there exists an urge at the Fed to repeat the mistakes of the BOJ and ECB.”

So a big part of today’s move higher in US equity futures, which are up another 18 points most recently, is the market is now pricing in that the Fed is getting cold feet about a rate hike now that both Goldman and Krugman are saying a delay is inevitable.

The irony of course is that the higher stocks rise, the greater the probability the Fed does hike rates, so we go right back to square one.

In commodities, the price action was fairly muted across the energy complex amid light newsflow and a relatively flat USD. In the metals complex, copper prices advanced to its highest level since mid-July , benefiting from the pick-up in sentiment and also in reaction to the announcement made by Glencore earlier in the week which would result in the removal of 400,000 tonnes of copper from the market. Looking ahead, today sees the API crude oil inventories aftermarket having been delayed a day due to the long Labour Day weekend, as a reminder last week saw a build of 7,600K.

Going forward, today sees market participants digest the release of the latest US JOLTS report and the Bank of Canada rate decision.

Market Wrap

- S&P 500 rose 2.5%, second-biggest gain this year

- Nikkei 225 jumped 7.7%, largest surge since 2008

- Shanghai Composite Index up 2.3%

- S&P 500 futures up 1% at 1985.6

- Indexes: FTSE 100 up 1.9%, CAC 40 up 2.6%, DAX up 1.8%, IBEX 35 up 2.4%, FTSE MIB up 1.8%, Euro Stoxx 50 up 2.4%

- All of 19 Stoxx 600 sectors rise; autos sector up 2.9%, second-best performance after basic resources

- V2X down 12% at 28.5

- Euro spot down 0.4% at 1.1162; yen spot down 0.6%

- GBP drops to 1.5361 vs USD session low after July IP, manufacturing data miss est

- LME 3m Copper up 0.6% at $5375/MT

- Brent crude down 0.3% at $49.35/bbl

Bulletin Headline Summary from Bloomberg and RanSquawk

- Asian equities traded higher led by the Nikkei 225 (+7.7%) which soared nearly 1000 points after PM Abe announced a reduction in corporate tax next year

- USD/JPY trades above 120.00 and in close proximity to the 200DMA after PM Abe’s announcement, while GBP/USD tested the 200DMA level to the downside following disappointing industrial & manufacturing production

- Today’s highlights include US JOLTS report, Bank of Canada rate decision and API crude oil inventories after the closing bell on Wall Street

- Treasury yields rise in overnight trading, led by the long-end as equities rally; U.S. will auction $21b 10Y (reopen), WI yield 2.215% vs. 2.115% in August.

- Japanese stocks soared, with the Nikkei 225 Stock Average staging the steepest advance since the aftermath of the 2008 Lehman Brothers bankruptcy, amid speculation a selloff that drove valuations to an 11-month low was overdone

- Five-year Treasury notes are near their most expensive level in 15 months relative to two- and 30-year securities before the Federal Reserve meets next week to decide whether to raise interest rates for the first time in almost a decade

- U.K. industrial production unexpectedly declined and goods exports plunged the most in nine years, indicating a loss of economic momentum that may keep the Bank of England on a cautious policy footing

- Citigroup’s chief economist, Willem Buiter, said there is a 55% chance of some form of global recession in the next couple of years, most likely one of moderate depth and length

- Chinese Premier Li Keqiang sought to soothe global concern about the nation’s economy and stock market, saying growth is stabilizing and employment data show that it’s operating in a reasonable range

- Add the world’s biggest stock-index futures market to the list of casualties from China’s interventionist campaign to stop a $5 trillion equity rout

- Sovereign 10Y bond yields mixed, with Greek 10Y yield falling ~23bps. Asian and European stocks gain, U.S. equity- index futures rise. Crude oil and gold fall; copper gains

DB’s Jim Reid concludes the overnight wrap:

Onto the latest in Asia this morning and following a late surge in Chinese equities yesterday, which in turn kick started a strong relief rally across markets in Europe and the US, bourses have followed it up this morning with another strong showing with the Shanghai Comp (+1.69%), CSI 300 (+1.69%) and Shenzhen (+2.70%) all heading into the midday break with decent gains. The latest rally appears to have been supported by comments from China’s Ministry of Finance late yesterday, stating that it would ‘accelerate the implementation and improvement of proactive fiscal policy and related measures’ as well as speeding up reform measures to support stable growth and promoting healthy economic development.

The better sentiment has spread to the rest of bourses in Asia this morning. The Nikkei has bounced +5.69% and the most since March 2011, while the Topix is currently up +4.98%. Elsewhere, the Hang Seng (+2.97%), Kospi (+2.25%) and ASX (+1.70%) have all followed suit. Asia credit markets are also benefiting from the strong risk tone, trading 4bps tighter this morning while S&P 500 futures are currently up just over half a percent, with 10y Treasury yields a couple of basis points higher.

Back to yesterday. More state intervention chatter was attributed to the strong surge in Chinese equities yesterday as the Shanghai Comp reversed course shortly after the midday break (and after we went to print), rallying over 5% off the intraday lows to close up just shy of 3%. As discussed above this triggered a relief rally wave across risk assets yesterday. In Europe the Stoxx 600 ended up +1.18%, while over in the US markets surged following a three-day break with the second best daily returns this year for the S&P 500 (+2.51%), Dow (+2.42%) and Nasdaq (+2.73%). It was similar story in credit markets too. In Europe Crossover rallied 8bps while across the pond CDX IG was over 4bps tighter and buoyed by a bumper day for primary market issuance following a 13-day drought for new deals. Meanwhile the VIX fell over 10% to close at 24.9 and back to the lowest level since August 20th.

In the Oil space Brent (+3.97%) had a strong day and more or less wiped out Monday’s losses, although WTI (-0.24%) closed slightly down after playing catch up from the three-day break. Copper (+3.83%) surged on the back of production cuts while Aluminium (+1.91%), Zinc (+2.31%) and Nickel (+2.56%) also had a strong showing. The relief also spread through to a decent session for commodity sensitive currencies with +1% gains for currencies in South Africa, Russia, Colombia, NZ, Australia, Norway and Mexico.

The better tone in markets saw Treasury yields rise steadily over the day. The 10y eventually closed up 5.8bps at 2.184% while 2y yields finished +2.6bps higher at 0.735% and back pretty much to the highs for the year. Data wise there wasn’t too much to report in the US with the calendar light as usual post payrolls. The highlight was a slight rise in the August NFIB small business optimism index, up 0.5pts to 95.9 (vs. 96.0 expected). This was the second consecutive monthly gain but still well off the December 2014 highs of 100.4. The labour market conditions index rose 0.3pts last month to 2.1, while consumer credit for the month of July came in slightly above market ($19.1bn vs. $18.8bn expected). All told, the probability of a September hike from the Fed now is sitting at 28%, a slight fall from 30% on Friday. On this note, the World Bank’s Chief Economist has added to the recent chorus of opinions, warning that a move in September risks triggering ‘panic and turmoil’ in emerging markets and adding that it’s the compounding effect of the last two weeks of bad news with China’s devaluation that would likely trigger this panic.

Closer to home in Europe yesterday, sentiment was also given a lift following the preliminary Q2 GDP print for the Euro area, coming in at +0.4% qoq and a tenth ahead of expectations. That saw the annualised rate edge up three-tenths to 1.5% yoy and the highest since June 2011. Meanwhile, Germany’s trade data surprised to the upside in July with the trade balance of €22.8bn reaching a new historical peak. This was after exports out of Germany bounced back in July (+2.4% mom vs. +1.0% expected and -1.1% mom in June), although imports were also notably higher during the month, rising 2.2% mom (vs. +0.7% expected) after a negative showing in June. Our colleagues in Germany noted that nevertheless, despite the good start to Q3, sentiment indicators (PMI and IFO export expectations in particular) point to a strong deceleration of German exports in the coming months. They point out that so far about half of nominal export growth was driven by the valuation effect caused by a mainly weaker Euro and that this depreciation has already faded. They also expect the demand side momentum to slow, especially given the slowdown of US vehicle sales and ongoing challenges in larger EM’s.

Onto today’s calendar now. We kick off in the UK this morning where the focus will be on the July trade data along with industrial and manufacturing production readings. Over in the US this afternoon the main focus will be on the July JOLTS job openings print, which as we’ve noted previously is an important release given that the data is among Fed Chair Yellen’s favorite series with the jobs openings rate, hiring rate and quits rate of particular significance.

end

Tuesday night, 9:30 pm/Wednesday morning Shanghai 9:30 am

China calls for global stability/asks for market intervention and gets it!

(courtesy zero hedge)

China Panics: Calls On US To “Jointly Ensure Global Stability”, Exclaims “Economic Outlook Is Very Bright”

Hot on the heels of The World Bank demanding The Fed not hike rates, China issued a statement “calling on US to jointly ensure global economic stability”tonight following a farcical intervention last night on record low volumes and a small devaluation of the Yuan. Foreign Minister Wang added “China and U.S. should also properly handle disagreements and safeguard current international order,” just as another minister spewed forth “China’s economic outlook is very bright,” – well apart from the record debt, collapsing asset values, and massive over-capacity, you mean. Further measures detailing the new capital restrictions for forward FX transactions were announced (which will likely do for CNH what regulators did to Chinese index futures). Chinese stocks are extending their gains in the pre-open on vapid volume as China leaves Yuan practically unchanged.

As a reminder, here is last night’s (and Monday’s) epic farce of a “market”… after dropping 100s of billion of Yuan to “stabilize” the market already, why not do some more…

On the lowest volume EVER!!!

And then have the balls to issue a ststement, demanding this…

- *CHINA CALLS ON U.S. TO JOINTLY ENSURE GLOBAL ECONOMIC STABILITY

China and the U.S. should jointly ensure global financial and economic stability, Chinese Foreign Minister Wang Yi said when meeting with a former U.S. National Security Council official.

China and U.S. should also properly handle disagreements and safeguard current international order, as China President Xi Jinping is scheduled to visit the U.S. later this month, Wang said Sept. 7

But the propaganda did not stop there…

Liu He, director at the Office of China’s Central Leading Group on Financial and Economic Affairs, said that China’s economic outlook is “very bright” and the country will overcome current difficulties, Zhejiang Daily reports, citing Liu who commented during a trip to Zhejiang province.

Middle class is on the rise and domestic demand is “huge”

China needs to stabilize market expectation while working on reforms

Margin Debt dropped – after rising yesterday for the first time in over 2 weeks.

But stocks are extending gains in the pre-market futures trading…

- *CHINA’S CSI 300 STOCK-INDEX FUTURES RISE 2.8% TO 3,364

As PBOC leaves Yuan practically unchanged…

- *CHINA SETS YUAN REFERENCE RATE AT 6.3632 AGAINST U.S. DOLLAR

Charts: Bloomberg

Japan’s Nikkei 225 Just Gained 1000 Points In 20 Hours

Presented with little comment aside to ask, just what did The G-20 agree to behind the scenes?

After ripping 500 points instantly at Japan’s open yesterday, then crashing back 900 points lower, Nikkei 225 Futures have now soared over 1000 points off last night’s lows…

6% in 20 hours? makes perfect sense!!

Because – despite what G-20 said… China does not seem to have got the message…

- FORMER CHINA SAFE OFFICIAL SEES FOREX INTERVENTION NECESSARY

end

and our illustrious buffoon covered his shorts, keeping his perfect record of 100% losses on his calls.

However, bulls be warned: after covering his losses he then went net long!!

The above was written at 10 am with the Dow up by 80 points or so. And as luck may have it, the Dow plummeted on the day causing Gartman to lose again.

(courtesy zero hedge)

Gartman Covers His Shorts, Goes “Marginally Net Long” One Day After Calling For Bear Market

Yesterday we asked a simple question: “is this the real reason futures are soaring” and pointed to Gartman’s latest flipflop as follows:

Trend Line Support, We Fear, Is A Very Long Way Down: This is a sobering thought, but this chart… which we included in our commentary yesterday… should give everyone a case of very real concern for support for the S&P is several hundred points below where the market closed on Friday. Strength is to be sold into…. We remain here at TGL modestly net short of the market generally and we’ve no intention of changing that focus other than to become a bit shorter still as time and market conditions demand.

Less than 24 hours later we find that he did indeed have an “intention of changing that focus.” Here is his latest “focus”:

In our retirement fund here at TGL… the only money which we manage directly… we came into yesterday’s session decently net short; not aggressively so, but not marginally so either. However, it made no difference; we were short in a rampaging bullish move and we had no choice but to rush to cover much of the net short position immediately upon the opening of trade on the NYSE.... Within moments of the opening we had reduced that net short position almost entirely. Would that we had had the temerity and the foresight to have reversed our derivatives position entirely, but we are neither that insightful nor that heroic.

Today, almost certainly we’ll be covering in a bit more of our derivatives positionand at the same time we’ll be buying more of our single “tanker” stock to take our “net” position to one that is modestly, marginally net long. We’ve no choice. The market has spoken and it has spoken loudly.

Bulls you have been warned.

(zero hedge/World Bank Economist,Basu)

Fed Hike Will Unleash “Panic And Turmoil” And A New Emerging Market Crisis, Warns World Bank Chief Economist

If it was the Fed’s intention to make the upcoming rate hike seem like a welcome event, one that presaged a new Golden Age in the US (and global) economy because, lo and behold, the wise Fed would never hike unless the economy is flourishing and thus create a self-fulfilling prophecy in which the rate hike itself – an event of tightening financial conditions even when inflation expectations are the lowest they have been in years – becomes a catalyst for growth, then it has failed spectacularly.

First, it was the IMF warning a rate hike would be a big mistake, then Larry Summer (who for some reason progressives thought was hawkish when it was a choice between him and Aunt Janet), then even China got into the fray saying the Fed should delay its rate hike as it could push emerging markets (such as China) into crisis.

But it wasn’t until today that we got the most glaring confirmation there had been absolutely zero coordination at the highest levels of authority and “responsibility”, when the World Bank’s current chief economist (a position previously held by such ‘luminaries’ as Larry Summers, Joseph Stiglitz and Stanley Fischer), Kaushik Basu warned that the Fed risks, and we quote, triggering “panic and turmoil” in emerging markets if it opts to raise rates at its September meeting and should hold fire until the global economy is on a surer footing, the World Bank’s chief economist has warned.

While apparently the World Bank economist is unfamiliar with the concept of reflexivity, and does not understand that the only reason the global economy is not on “surer footing” is because of the 12+ month , near endless pricing in of the Fed’s first rate hike since 2006, which has unleashed an unprecedented capital flight out of all emerging markets, a record series of rate cuts across the globe including NIRP in Europe, and China’s first official currency devaluation in years not to mention the first stock market correction in 4 years, what is critical is that by making this statement, Basu destroys with just two words the narrative that i) the Fed knows what it is doing and that ii) contrary to logic, a rate hike at a time when the world clearly and desperately needs, and is addicted, to global central bank liquidity, will lead to even further asset price plunges.

In fact, Basu may have just admitted, in not so many words, that Deutsche Bank’s sinking feeling that the Fed’s rate hike is nothing but a “controlled demolition” of the market, one which would send global equities 20-40% lower, is spot on.

This is what else Basu told the FT:

Rising uncertainty over growth in China and its impact on the global economy meant a Fed decision to raise its policy rate next week, for the first time since 2006, would have negative consequences.

His warning highlights the mounting concern outside the US over the Fed’s potential “lift-off”. It follows similar advice from the International Monetary Fund where anxieties have also grown in recent weeks about the potential repercussions of a September rate rise.

That means that if the Fed’s policymakers were to decide next week to raise rates they would be doing so against the counsel of both of the institutions created at Bretton Woods as guardians of global economic stability.

And just in case casually tossing the words “panic in turmoil” was not enough, Basu decided to add a few more choice nouns, adding a rate hike “could yield a “shock” and a new crisis in emerging markets… especially as it would come on the back of concerns over the health of the Chinese economy that have grown since Beijing’s move last month to devalue its currency.”

He said that, even though it had been well-advertised by the Fed, any rise would lead to “fear capital” leaving emerging economies as well as to sharp swings in their currencies. The likely strengthening in the dollar would also hamper US growth, he said.

Finally at least one person in a position of authority realized just what Quantitative Tightening means:

“I don’t think the Fed lift-off itself is going to create a major crisis but it will cause some immediate turbulence,” Mr Basu said. “It is the compounding effect of the last two weeks of bad news with that [China devaluation] . . . In the middle of this it is going to cause some panic and turmoil.

Precisely, and as a reminder between the Fed’s tightening and China’s QT, the world would suddenly find itself starting at a finacial liquidity abyss, and abyss which forDeutsche Bank means the S&P could trade at “half its value.”

His conclusion: “The world economy is looking so troubled that if the US goes in for a very quick move in the middle of this I feel it is going to affect countries quite badly,” he said.

And if someone should know (clearly not the Fed whose predictions have become the butt of all jokes even for tenured economists), that would be the chief economist of the World Bank.

But fear not: recall that over the weekend Goldman made it very clear that a September rate hike (and maybe December) is not coming. And what Goldman wants, Goldman always gets, even if it means the Fed ends up losing all credibility in the process.

Finally, just in case there is still any confusion what a Fed rate hike means, we repeat what Bank of America said last week:

Should the Fed decide to raise interest rates, it will be the first Fed hike since June 29th 2006. In the 110 months that have since past, global central banks have cut interest rates 697 times, central banks have bought $15 trillion of financial assets, zero [or negative] interest rates policies have been adopted in the US, Europe & Japan. And, following the Great Financial Crisis of 2008, both stocks and corporate bonds have soared to all-time highs thanks in great part to this extraordinary monetary regime.

As noted above, a rate hike with a stroke ends this era.

Buiter: Only “Helicopter Money” Can Save The World From The Next Recession

It is to be expected that economists – even economists working for the same team – have different views about the likelihood of different future outcomes. Economics isn’t rocket science, and even rockets frequently land in the wrong place or explode in mid-air.

That rather hilarious characterization of the pseudoscience that is economics comes from the desk of Citi’s Chief Economist Willem Buiter and it’s apparently evidence that even if you don’t think too much of his views on “pet rocks” (gold is a 6,000 year-old bubble) or on the efficacy and/or utility of physical banknotes (ban cash), you’d be hard pressed to disagree with him when it comes to critiquing his profession. Of course we don’t want to give Buiter too much credit here because the quote shown above could simply be an attempt to stamp a caveat emptor on his latest prediction in case, like his predictions on when Greece would ultimately leave the euro, it turns out to be wrong.

As tipped by comments made at the Council of Foreign Relations in New York late last month, Buiter is out with a damning look at the global economy which he says will be drug kicking and screaming into a recession by the turmoil in China and the unfolding chaos in EM. Here’s the call:

In the Global Economics team, however, we believe that a moderate global recession scenario has become the most likely global macroeconomic scenario for the next two years or so. To clarify further, the most likely scenario (40% probability), in our view, for the next few years is that global real GDP growth at market exchange rates will decline steadily from here on and reach or fall below 2%.

The culprit, as mentioned above, is China (where Citi says real GDP growth is actually somewhere in the neighborhood of 4%) and EMs more broadly which are suffering mightily in the face of sluggish Chinese demand, slumping commodity prices, and, most recently, the devaluation of the yuan:

Should China enter a recession – and with Russia and Brazil already in recession – we believe that many other EMs, already weakened, will follow, driven in part by the effects of China’s downturn on the demand for their exports and, for the commodity exporters, on commodity prices.

The main driver of global underperformance during the past two years has been EM weakness. No EM of any significant size is outperforming our forecasts since the beginning of the year or earlier; most are underperforming. Even the success stories, like India, central and eastern Europe, and to a certain extent Mexico, are not outperforming our forecasts. Brazil and Russia are in recession, and GDP growth there has turned negative. South Africa is in a recession, with output below potential and output growth below potential output growth. The most significant underperformer is China. For reasons explained earlier, we don’t think there is much point in forecasting official GDP growth. We therefore focus on our best guess as to the ‘true’ growth rate of real GDP, which, as noted earlier, is probably somewhere around 4% now.

Evidence of weakness, Buiter continues, is everywhere:

The evidence for a global slowdown is everywhere. Global growth is weakening since 2010 as is evident from Figure 6, which shows global real GDP growth since 1980 at both market and PPP exchange rates, as well as EM and DM real GDP growth at PPP exchange rates. A modest pickup in GDP growth in the DMs since 2012 is swamped by a sharp decline in EM growth. There are other informative indicators of global weakness, notably the very weak – indeed negative – world trade growth in the first half of 2015, the continued weakening of (real) commodity prices, the weakness of the global inflation rate (measured by the GDP deflator), the recent decline in global stock prices, measured by the MSCI ACWI, plus indications that corporate earnings growth is slowing down in most countries, and the unprecedented decline in nominal interest rates, shown in Figure 7 – Figure 11.

And China – the epicenter of it all – is ill-equipped to cope because, as we’ve discussed at length, the country’s many spinning plates have elicited an eye-watering array of conflicting directives and policies which are now tripping over each other at nearly every turn:

The policy response to the weakening of domestic (and external) demand in China is likely to be too little and too late. China is not a command economy or a centrally planned economy – indeed, unlike the former Soviet Union, it never was. Like most real-world economies today, it is a messy market economy of the state-capitalist/crony-capitalist variety, where policy ambitions are not matched with effective policy instruments and where macroeconomic management and financial crisis prevention and mitigation competence are in short supply.

The mishandling of the housing boom, bubble and bust, and of the latest stock market boom, bubble and bust together with the recent RMB kerfuffle don’t inspire confidence in the ability of the authorities to prevent a cyclical hard landing for China.

Finally, DM central planners are in no shape to combat the China/EM contagion because – and this will come as no surprise – they are simply out of ammunition having thrown everything in the Keynesian toolbox at their respective economies in the post-crisis years with limited (and swiftly diminishing) returns:

Most advanced economies are, as regards countercyclical policy ammunition, in the position that either they don’t have very much of it or are unwilling and/or unable (because of domestic or external political constraints) to use what ammunition they have.

Expansionary monetary policy in the US, the UK, the Eurozone, Japan and most smaller advanced economies is operating in the zone of severely diminishing returns.

As you might have guessed, Buiter thinks there’s only one way out of this: helicopter money.

And not just in the US, but in Europe (against the protestations of what Buiter calls the “Teutonic fringe”) and indeed across all DMs and also in China.

Helicopter money drops would be the best instrument to tackle a downturn in all DMs.

In the Eurozone, a significant Teutonic fringe believe that a fiscal stimulus is contractionary and that monetization of public debt and deficits is a sure road to hyperinflation. It is a widely held view that Article 123 of the Treaty on the Functioning of the European Union forbids monetization of public debt and thus makes a helicopter money drop in the Eurozone impossible. Debt-financed (non-monetised) fiscal expansions run into the twin obstacles of an already excessive public debt in most Eurozone member states and the pro-cyclical nature of the constraints imposed by the Stability and Growth Pact and its myriad offspring, operated out of Brussels.

In the US, the fiscal stance is, from a cyclical perspective, not unlike a clock that is halted and points at the right time only twice a day. Fortunately, today is one of these times. Should the country need a fiscal stimulus (or indeed a fiscal contraction), it is in our view highly unlikely that the Congressional gridlock could be overcome sufficiently to do what is necessary when it is necessary. So as regards countercyclical policy, the US, like the Eurozone, has to rely on progressively less effective monetary stimulus alone.

The fiscal position of the Japanese sovereign is by far the worst of any large advanced country, despite its large stock of foreign exchange reserves and the positive net foreign investment position of Japan as a whole. Only a permanently monetised fiscal stimulus would be feasible if the markets were to wake from their decades-long slumber and wonder whether, and how, the Japanese sovereign can reach the shores of solvency without inflating its debt away.

Fiscal policy can undoubtedly come to the rescue and prevent a recession in China.But what is needed is not another dose of the familiar post-2008 fiscal medicine: heavy-lifting capital expenditure on infrastructure with dubious financial and social returns, and capital expenditure by SOEs that are already struggling with excess capacity, all funded, as if these were commercially viable ventures, through the banking or shadow banking sectors. As regards funding the fiscal stimulus, only the central government has the deep pockets to do this on any significant scale.The first-best would be for the central government to issue bonds to fund this fiscal stimulus and for the PBOC to buy them and either hold them forever or cancel them, with the PBOC monetizing these Treasury bond purchases. Such a ‘helicopter money drop’ is fiscally, financially and macro-economically prudent in current circumstances, with inflation well below target and likely to fall further.

So basically, these central banks which Buiter just admitted are already “operating in the zone of severely diminishing returns,” should not only do more of the same, but a lot more of the same and in fact, they should all dive head first into the Keynesian abyss by simultaneously cranking the knob on their respective printing presses to the max:

We expect to see QE #N, where N could become a large integer, as part of the monetary policy response in the US and the UK, and QEE2 in Japan. The ECB will likely have to continue its asset purchases beyond September 2016 and it may cut its policy rates further. All this will not be enough to prevent most advanced economies from performing worse in 2016 and 2017 than in 2015, and worse than our current forecasts for the next two years.

There you have it. “QE#N where N could become a large integer”, and paradoxically, by not normalizing policy when it had the chance, the Fed has now made this inevitable because as we’ve shown, tightening into an EM FX reserve drawdown will only exacerbate said drawdown making an embarrassing about-face by the FOMC a foregone conclusion. In other words, this is game over. We’ve entered the monetary Twilight Zone where the only way to keep the increasingly wobbly house of cards standing is to continue to monetize everything that’s monetizable and when we hit the limit we must then move to issue more debt for the sole purpose of monetizing it and immediately canceling it.

But as Buiter noted at the outset, these are all just the musings of a pseudo-scientist, who, by the very nature of his profession, is prone to making predictions that, much like the Fed’s “liftoff”, are just as likely to “explode in mid-air” as not.

end

30Y Treasury Yield Bursts Above 3.00% – 6-Week Highs

30Y Treasury yields are up 40bps from the Black Monday flash-crash panic low yields, breaking back above 3.00% for the first time since the end of July. It appears China selling (and rate locks) is trumping Element Capital’s buying (for now).

At 3.02%, 30Y just broke another resistance level and is at its highest since July 23rd.

Charts: Bloomberg

end

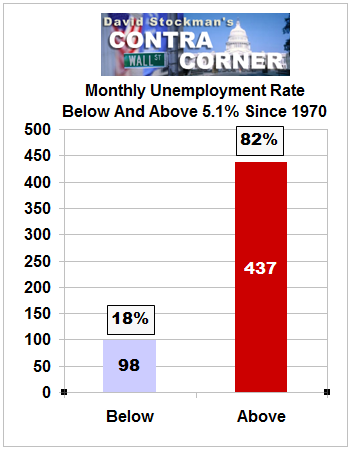

Your most important read of the day. David Stockman tackles ZIRP, the phony Japanese stock market, the huge bond purchases by Japan of its bonds as well as the phony jobs report and what it means…

a must read…

(courtesy David Stockman/ContraCornerBlog)

The Endless Emergency – Why It’s Always ZIRP Time In The Casino

Submitted by David Stockman via Contra Corner blog,

Based on the headline from the latest Jobs Friday report you wouldn’t know that we are still mired in an economic emergency – one apparently so extreme that it might entail moving to the 81st straight month of zero interest rates at next week’s FOMC meeting. After all, the unemployment rate came in smack-dab on the Fed’s full-employment target at 5.1%.