Gold $1253.10 up $1.90

Silver 17.39 DOWN 2 cents

In the access market 5:15 pm

Gold: 1251.80

Silver: 17.40

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix OCT 14 (10:15 pm est last night): $ 1263.11

NY ACCESS PRICE: $1258.90 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1262.18

NY ACCESS PRICE: 1255.25 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!! 7 dollars

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: OCT 14: 5:30 am est: $1256.15 (NY: same time: $1256.20: 5:30AM)

London Second fix OCT 14: 10 am est: $1251.75 (NY same time: $1258.10 , 10 AM)**STRANGE!! SECOND FIX!!

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

0 NOTICES FILED FOR NIL OZ

For silver:

for the Oct contract month: 2 notices for 10,000 oz.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

As I have pointed out to you on several occasions the criminals like to raid on Friday’s due to the fact that Shanghai has already been put to bed by the time comex gold/silver starts trading. By noon time, London is also fully put to bed and it is at that time that the crooks whack again.

However they must face the music on Monday when Shanghai demands gold at that cheaper price.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 131 contracts UP to 186,091. The open interest FELL as the silver price was DOWN 5 cents in yesterday’s trading .In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .930 BILLION TO BE EXACT or 133% of annual global silver production (ex Russia &ex China).

In silver for October we had 2 notices served upon for 10,000 oz

In gold, the total comex gold ROSE by 2,557 contracts with the RISE in price of gold( $3.10 yesterday) . The total gold OI stands at 498,014 contracts. The bankers have done a great job fleecing our comex gold longs

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

TODAY WE HAD NO CHANGES AT THE GLD:

Total gold inventory rests tonight at: 961.57 tonnes of gold

SLV

we had A HUGE CHANGE at the SLV/ A DEPOSIT OF 1.138 MILLION OZ INTO THE SLV

THE SLV Inventory rests at: 362.285 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 131 contracts UP to 186,091 as the price of silver FELL by 5 cents with yesterday’s trading.The gold open interest ROSE by 2,557 contracts UP to 498,014 as the price of gold rose $3.10 IN YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

2c) Federal Reserve Bank of New York/earmarked gold removal

(Harvey)

2d) COT report

Harvey

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 2.43 POINTS OR 0.08%/ /Hang Sang closed UP 202.01 POINTS OR 0.88%. The Nikkei closed UP 82.13POINTS OR 0.49% Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed UP at 6.7260/Oil ROSE to 50.95 dollars per barrel for WTI and 52.29 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.7346 yuan to the dollar vs 6.7260 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

none today

4 EUROPEAN AFFAIRS

i)GERMANY/DEUTSCHE BANK

The hits just keep coming to Deutsche bank as one day after announcing a hiring freeze, they decide to fire another 10,000 workers. A great reason for gold to be whacked today by the crooks:

( zero hedge)

ii)Qatar is now worried about their investment in Deutsche bank

(courtesy zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

Raoul Pal is one smart cookie. Pay attention to him as he discusses the global economy:

( Raoul Pal/Barbara Kollmeyer/Market Watch)

7.OIL ISSUES

i)That did not last long: stocks begin to fall as crude crumbles back below 50 dollars per barrel

( zero hedge)

ii)Oil rig counts continue to rise and this will have a huge damper effect on the price in the coming months as production increases

( zero hedge)

8.EMERGING MARKETS

none today

9.PHYSICAL STORIES

i)We brought this story to you yesterday but it is worth repeating; Gold prices in this hugely physical geographical zone has now gone to a premium for the first time this year despite the huge 10% tax

( David Forest/OilPrice.com/GATA)

ii)Your weekly commentary tonight from Alasdair Macleod:

( Alasdair Macleod

iii)Copper is falling badly and it is killing Freeport McMoran, B. H. Billiton along with huge derivative player Glencore:

( Steve St Angelo/SRSRocco report)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

ia)This data is important as retail sales is the dominant force behind the growth in GDP. It has now slumped to its weakest level since 2015:

( zero hedge)

ib)Dave Kranzler discusses the real unadjusted retail sales number. It shows a contraction of 2.6%

( Dave Kranzler/IRD)

ii)Another biggy!! Producer Prices rose much higher than expected. This is the forerunner to a rise in actual inflation:

( PPI/zero hedge)

iii)The following was not suppose to happen: consumer confidence right before the election crashes to a 2 yr low:

( zerohedge)

iv)Eliz. Warren demands Obama fire SEC chief Mary Jo White for her decision not to craft rules requiring public companies to disclose their political spending activities. That would be a good start:

( zero hedge)

v)Finally, we have one newspaper, the Wall Street Journal that lashes out as all of the press that have been burying Hillary Clinton’s crimes and concentrating just on Trump’s sexual prowess.

( Wall Street Journal/zero hedge)

vi)Supreme Court Justice Roberts sold his soul to Obama in the passing of Obamacare as President Obama applied huge pressure on the court.

unbelievable…

( zero hedge)

viia)Another state in trouble because of Obamacare: Minnesota Governor Mark Dayton: “Affordable Care is no longer affordable”

that says it all!

( zero hedge)

viib)At least 1.4 million Americans who liked their healthcare plan will lose it in 2017:

viii)For the whole year, the Atlanta Fed has come out with figures to suggest that the entire year will grow at 1.4% having slashed Q3 GDP down to 1.9%

( Atlanta Fed/zero hedge)

ix)Total debt rises by 1.422 trillion dollars. The deficit rose by 587 billion dollars up from 439 billion. Thus the budgetary deficit rose by 34% and it is represented by 3.2% of GDP (very high)

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 2,557 CONTRACTS to an OI level of 498,014 as the price of gold rose by $3.10 with YESTERDAY’S trading.

We are in the delivery month is October and here the OI GAINED 177 contracts UP to 369. We had 41 notices filed yesterday so we gained another 218 contracts or 21,800 additional oz will stand.

The next delivery month is November and here the OI FELL by 12 contracts DOWN to 2940 contracts. This level is extremely elevated as generally November is a very poor delivery month.The next contract month and the biggest of the year is December and here this month showed an increase of 731 contracts up to 373,385.

And now for the wild silver comex results. Total silver OI rose BY 131 contracts from 185,960 up to 186,091 as the price of silver fell to the tune of 5 cents yesterday. We are moving further from the all time record high for silver open interest set on Wednesday August 3: (224,540). The next non active delivery month is October and here the OI rose by 5 contracts up to 121. We had 0 notices filed yesterday so we gained 5 contracts or 25,000 additional oz will stand for delivery.The November contract month saw its OI lose 8 contracts down to 333. The next major delivery month is December and here it FELL BY 1477 contracts DOWN to 149,380

VOLUMES:

Today the estimated volume was 164,898 contracts which is fair.

Yesterday, the confirmed volume was 169,215 which is also fair.

today we had 2 notices filed for silver:

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

43,440.35 oz

brinks

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

0 notices

nil oz

|

| No of oz to be served (notices) |

369 contracts

36,900

oz

|

| Total monthly oz gold served (contracts) so far this month |

7989 contracts

798,900 oz

24.849 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 175,209.0 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 0 contract of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

821,470.75 oz

Brinks

HSBC

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

420,389.039 oz

DELAWARE

|

| No of oz served today (contracts) |

2 CONTRACTS

(10,000 OZ)

|

| No of oz to be served (notices) |

119 contracts

(595,000 oz)

|

| Total monthly oz silver served (contracts) | 355 contracts (1,775,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,921,481.3 oz |

end

NPV for Sprott and Central Fund of Canada

will not provide today.

end

COT REPORT

At 3:30 pm we receive the COT which gives us position levels of our major players and we also get to see how many contracts the commercial crooks covered:

Let us now head over and see what the gold COT offers:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 283,386 | 88,167 | 50,883 | 112,362 | 333,561 | 446,631 | 472,611 |

| Change from Prior Reporting Period | ||||||

| -40,750 | 9,539 | -2,983 | 498 | -49,545 | -43,235 | -42,989 |

| Traders | ||||||

| 169 | 112 | 86 | 51 | 52 | 268 | 206 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 53,697 | 27,717 | 500,328 | ||||

| -1,261 | -1,507 | -44,496 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, October 11, 2016 | |||||

criminals in the highest order and nobody does anything to stop these crooks

Our large speculators:

those large specs that have been long in gold pitched a gigantic 40,750 contracts from their long side and they were royally fleeced by the crooked bankers

those large specs that have been short in gold added a huge 9539 contracts to their short side and they are now coming over to the short side of the boat.

And wait until you see this:

OUR ILLUSTRIOUS CRIMINAL COMMERCIALS

those commercials that have been long in gold added only 498 contracts to their long sidethose commercials that have been short in gold covered a gigantic 49,545 contracts

we thus thank the regulators for free markets.

Our small specs:

Those small specs that have been long in gold pitched a large 1261 contracts from their long side

Those small specs that have been short in gold covered 1507 contracts from their short side.

Conclusions:

(to our class action lawyers)

criminal activity!/

however it is bullish that the commercials go net long by 49,000 contracts.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Now let us now see how the crooks slaughtered our specs in silver

SILVER COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 97,527 | 34,634 | 11,453 | 52,174 | 129,809 | |

| -13,237 | -327 | -664 | 3,289 | -9,972 | |

| Traders | |||||

| 103 | 56 | 38 | 36 | 38 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 187,469 | Long | Short | |

| 26,315 | 11,573 | 161,154 | 175,896 | ||

| -666 | -315 | -11,278 | -10,612 | -10,963 | |

| non reportable positions | Positions as of: | 159 | 115 | ||

| Tuesday, October 11, 2016 | © SilverSeek.com | ||||

Just as bad!

Our large specs:

Those large specs that have been long in silver were fleeced out of 13,237 contracts.

those large specs that have been short in silver covered a tiny 327 contracts.

Our commercials;

those commercials that have been long in silver added 3289 contracts to their long side

those commercials that have been short in silver covered a huge 9972 contracts from their short side.

Our small specs:

those small specs that have been long in silver pitched a tiny 666 contracts from their long side.

those small specs that have been short in silver covered a tiny 315 contracts.

Conclusions;

Bullish as the commercials go net long by 6308 contracts. However judging from the huge fleecing in gold, the commercials seem to be having a little problem exiting all of their shorts in silver.

FEDERAL RESERVE BANK OF NEW YORK/GOLD INVENTORY MOVEMENT:

Last month we had a reading of 7883 million dollars worth of gold at the FRBNY at $42.22 dollars per oz. This month we had a reading of 7849 million dollars

Thus we had 34 million dollars worth of gold valued at $42.22 shipped out.

In oz:

34,000,000 divided by $42.22 = 805,305 oz

in tonnage:25.048 tonnes

Since Germany is the only official nation seeking its gold, no doubt that this gold was repatriated towards Frankfurt.

end

And now your overnight trading in gold,FRIDAY MORNING and also physical stories that may interest you:

“Gold Is A Great Hedge Against Politicians” – Goldman

“Gold Is A Great Hedge Against Politicians” – Goldman Sachs

Gold has risen another 1.7% in British pound terms this week and is 1.8% higher in euro terms and is again acting as a hedge against currency devaluations, Brexit, eurozone and heightened political and geo-political risk in the UK, EU, U.S. and most of the world.

Gold is marginally higher in dollar terms this week after surging on the open in Asia on Sunday night. Gold quickly rose 1% from $1,251/oz to $1,264/oz as China and the Shanghai Gold Exchange (SGE) began trading again after being closed for the Chinese Golden Week.

Since then gold prices moved lower despite the return of the world’s largest gold buyer – India – as seen in the return of gold premiums in the Indian gold market. Gold in dollar terms is now marginally higher for the week.

Goldman Sachs has long been the most vocal, prominent and widely quoted bear in the gold market. However, in recent weeks there is a marked change in their tune and they are now bullish on gold in the medium and long term. They are concerned about further price weakness in the short term as we run into year end but believe this will be a buying opportunity.

Goldman is now saying that the precious metal will be good to own in an environment of “political uncertainty” ahead of the November elections.

Goldman Sachs Head of Commodities Research Jeff Currie told CNBC’s “Power Lunch” this week that it is good to own gold in our current political state.

“I always like to say gold is a great hedge against politicians, and we have a lot of political risk in the market right now. So gold has a strategic purpose,” he explained.

“Why? What’s the tie between gold and politicians?” Brian Sullivan of CNBC asked Currie.

“Well, if you think about the correlation between rates and you think about when you debase a currency or weak dollar, what people gravitate to are hard assets and gold is the epitome of the hard asset,” Currie explained.

In a recent note, Goldman analysts Max Layton, Mikhail Sprogis and Jeffrey Currie wrote:

“Indeed, we would view a gold sell-off substantially below $1,250 an ounce as a strategic buying opportunity, given substantial downside risks to global growth remain, and given that the market is likely to remain concerned about the ability of monetary policy to respond to any potential shocks to growth.”

The bank also believed Chinese investment demand for gold may pick up after the current selloff, particularly from medium to long-term asset allocators.

“The potential drivers of increased Chinese physical buying include purchasing gold as a way to hedge for potential currency depreciation in the face of capital controls, and purchasing gold as a way of diversifying away from the property market, which has this year to date had a remarkable rally (with the government moving to rein in speculation and price growth),” the analysts added.

‘Peak gold‘, the largely unappreciated phenomenon of peak gold production is also another bullish fundamental factor that Goldman has written about.

Given the particularly poor caliber of politicians in office and seeking office in much of the western world today, author, political activist and intellectual George Bernard Shaw’s witty quote regarding voting for gold, rather than for politicians and governments is very apt today.

Ironically, the socialist agreed with Goldman Sachs and wrote:

“You have to choose, as a voter, between trusting to the natural stability of gold and the natural stability and intelligence of the members of the government. And with due respect to these gentlemen, I advise you, as long as the capitalist system lasts, to vote for gold.”

Gold and Silver Bullion – News and Commentary

Gold prices in India go to premium for first time this year (OilPrice)

Gold prices hold gains in Asia as China prices data stronger than seen (Investing)

Gold ticks higher as dollar, stocks markets slip (Reuters)

Irish retailers in price row with Unilever (RTE)

Putin ally tells Americans: vote Trump or face nuclear war (Reuters)

Buy gold, UBS says (BusinessInsider)

How low can the pound go? (MoneyWeek)

Great Marmite war is a sign of things to come (MoneyWeek)

Royal Air Force Pilots Ordered To Shoot Down “Hostile” Russian Jets Over Syria (ZeroHedge)

Goldman Sachs: 5 reasons sterling could fall 7% in two months (Nasdaq)

Gold Prices (LBMA AM)

14 Oct: USD 1,256.15, GBP 1,028.79 & EUR 1,140.08 per ounce

13 Oct: USD 1,258.00, GBP 1,029.93 & EUR 1,141.76 per ounce

12 Oct: USD 1,255.70, GBP 1,024.53 & EUR 1,139.05 per ounce

11 Oct: USD 1,256.40, GBP 1,021.58 & EUR 1,130.76 per ounce

10 Oct: USD 1,262.10, GBP 1,016.62 & EUR 1,129.71 per ounce

07 Oct: USD 1,255.00, GBP 1,012.91 & EUR 1,127.62 per ounce

06 Oct: USD 1,265.50, GBP 994.30 & EUR 1,131.23 per ounce

Silver Prices (LBMA)

14 Oct: USD 17.47, GBP 14.28 & EUR 15.86 per ounce

13 Oct: USD 17.59, GBP 14.40 & EUR 15.95 per ounce

12 Oct: USD 17.44, GBP 14.23 & EUR 15.83 per ounce

11 Oct: USD 17.48, GBP 14.26 & EUR 15.78 per ounce

10 Oct: USD 17.78, GBP 14.31 & EUR 15.92 per ounce

07 Oct: USD 17.33, GBP 14.01 & EUR 15.55 per ounce

06 Oct: USD 17.76, GBP 13.98 & EUR 15.88 per ounce

Recent Market Updates

– Sell Gold Now – Time To Liquidate Gold ETF, Pooled and Digital Gold

– Gold In GBP Up 43% YTD – “Massive Twin Deficits” To Impact UK Assets

– Ron Paul Says “Gold Going Up” Whether Trump Or Clinton Elected

– Gold Trading COT Report “Means Lower – Then Much Higher – Prices Coming”

– Currency Shock Sees Sterling Gold Surges 5% In One Minute “Flash Crash”

– Top Gold Forecaster: “As Quickly As Gold Fell” May “Rally Back” on Global Risks

– Gold Buying ‘Opportunity’ After Surprise 3.4% Drop

– Deutsche Bank “Is Probably Insolvent”

– GBP Gold Rises 1.3% as Sterling Slumps On ‘Hard Brexit’ Concerns, Up 36% YTD

– Why Krugman, Roubini, Rogoff And Buffett Hate Gold

– ECB Refused “To Answer Questions” – Deutsche Bank “Systemic Threat” Is “Not ECB Fault”

– Euro “Might Start To Unravel” If Collapse Of Deutsche Bank

– Do You Really Own Your Gold?

END

We brought this story to you yesterday but it is worth repeating; Gold prices in this hugely physical geographical zone has now gone to a premium for the first time this year despite the huge 10% tax

(courtesy David Forest/OilPrice.com/GATA)

Gold prices in India go to premium for first time this year

Submitted by cpowell on Thu, 2016-10-13 20:23. Section: Daily Dispatches

Gold Prices Just Did Something They Haven’t Done All Year

By Dave Forest

OilPrice.com, London

Thursday, October 13, 2016

Finally the global gold market is getting some good news from its top consuming nation — India.

Reports this week suggest that something very unusual has just happened with India’s local gold prices: They’ve jumped to a premium above worldwide bullion prices.

That’s big news because — so far this year — India’s prices have been lagging the rest of the world. With gold here selling at discounts of $50 or more per ounce below average global prices.

But that situation has now apparently reversed itself. With local media reporting that gold sellers in Mumbai’s Zaveri Bazar were quoting gold at $1 to $2 above benchmark pricing. Marking the first time this year that India’s prices have pulled back to parity. …

… For the remainder of the report:

http://oilprice.com/Metals/Gold/Gold-Prices-Just-Did-Something-They-Have…

END

Your weekly commentary tonight from Alasdair Macleod:

(courtesy Alasdair Macleod)

Alasdair Macleod: How not to manage a currency

Submitted by cpowell on Thu, 2016-10-13 15:11. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney.com, St. Helier, Jersey, Channel Islands

Thursday, October 13, 2016

Make no mistake, sterling’s collapse is a very serious development, and has serious consequences for sterling interest rates.

While it is becoming apparent that interest rates are going to have to rise possibly for all currencies on a one-year view, sterling’s problems are the consequence of bad judgement, and perhaps intellectual arrogance on the part of the Bank of England’s Monetary Policy Committee. The committee in turn is not and cannot be independent from the influence of Mark Carney, the bank’s governor, who made the expensive error of intervening in the Remain campaign.

Many commentators are saying that sterling was overvalued, and the fall will stimulate exports. But value is wholly subjective and not formulaic, as the ivory-tower economists would have us believe. The idea of stimulating exports through lower currency rates overlooks the depressing effect of the transfer of wealth it triggers from ninety per cent plus of the population, in favour of foreigners and owners of export businesses. That is the point about stagflation. …

It is a process that cannot continue indefinitely, because, as the adage goes, markets eventually reassert themselves. This adage is a summation of all that’s wrong with monetary and financial collectivism, the inability of central planning to allocate capital resources as efficiently as free markets. Sooner or later, a mistake, changing circumstances, or a black swan event leads to a financial or currency crisis. This happens from time to time, and every time the lenders of last resort manage to save their carefully constructed artifices, they say there are lessons learned, and it won’t happen again. Hubris. …

… For the remainder of the commentary:

https://wealth.goldmoney.com/research/goldmoney-insights/how-not-to-mana…

END

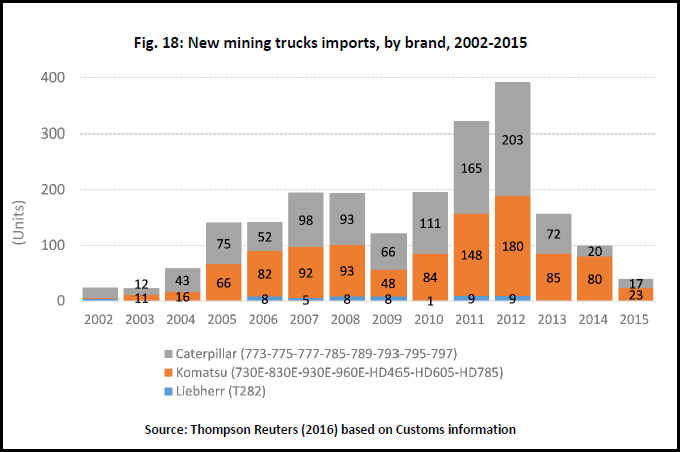

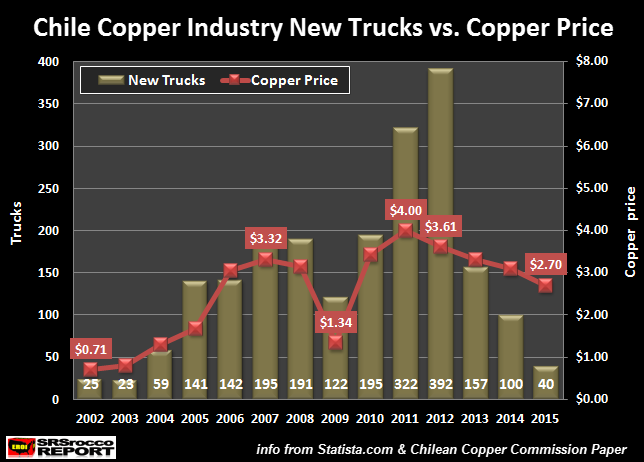

Copper is falling badly and it is killing Freeport McMoran, B. H. Billiton along with huge derivative player Glencore:

(courtesy Steve St Angelo/SRSRocco report)

BIG TROUBLE FOR COPPER: The Breakdown Of The Industry Has Begun

by SRSrocco on October 13, 2016

The king of base metals is in big trouble as indicators point to a breakdown of the global copper industry. This goes well beyond the typical “slowdown” or “downturn” in the copper market. Instead, we are going to witness what I refer to as “Copper Industry Carnage.”

While some readers may feel as if I am being a bit “doom and gloomy” here, the situation in the global copper industry is much worse than most analysts realize. This is due to the fact that many analysts are forecasting copper supply deficits in the next few years, which would push the price of copper higher.

Unfortunately, this sort of industry analysis is well behind the curve or even worse, guilty of wishful thinking. The world economy is slowing down… and this will likely pick up speed by the end of the year. Which means, demand for copper will continue to weaken, pushing prices even lower.

Today, the price of copper is down 2%, impacting the copper miners. Freeport’s stock price was hammered lower by over 7% today in market trading.

Low copper prices are already causing damage in the top two copper mining companies in the world. The second largest copper producer, Freeport-McMoran, suffered an adjusted income loss of $214 million in the first half of 2016. Part of the loss was due to their lousy shale oil and gas investments.

For some stupid reason, many base metal mining companies jumped into the oil and gas business with both feet when the shale energy bonanza took off in the United States. For example, BHP Billiton reported a hefty $7.2 billion impairment (write off) on its onshore shale oil and gas assets last year (for their year ending Q2 2016).

While that may seem like one hell of a lot of money for BHP Billiton to write-off on its shale oil and gas assets, Freeport-McMoRan did one even better. According to FreePort-McMoRan’s annual report, they reported a staggering $13 billion impairment on their oil and gas properties in 2015 on top of another $3.7 billion write off in 2014.

As they say… easy come, easy go.

So, not only are the big base metal miners suffering from low base metal prices, they are also enjoying a wonderful shale oil and gas enema from the other end. I don’t mean to be harsh here, but who on earth was in charge of making these lousy shale energy investment decisions for these base metal mining companies??

And it gets even worse. I just read this jewel of an article yesterday on the Financial Times, BHP Billiton Bets Long On U.S. Shale Assets:

Five years after BHP Billiton plunged $20bn into the US shale revolution, the wait goes on for shareholders.

Even if oil prices rally by one-third the fields will not generate significant free cash flow until the turn of the decade, the mining company cum oil producer revealed at investor briefings last week.

….. BHP’s acquisition of two US shale producers in 2011 was followed by $17bn of investment, beefing up an oil business that has long set the world’s most valuable mining company apart from its peers. About one-third of BHP’s group earnings before interest, tax, depreciation and amortisation have come from petroleum over the past five years.

The timing of its shale bet proved ill-judged. Following a savage market downturn that has seen oil prices more than halve, BHP has racked up $12bn of impairments and the US shale business is now valued at just $12.6bn. Output is expected to fall by a quarter this year, the consequence of a much reduced drilling programme.

So, the Einsteins at BHP Billiton acquired U.S. shale oil and gas assets that are now only worth $12.6 billion, after they racked up $12 billion of losses in impairments since 2011. Furthermore, even if the oil price increases by one-third, they won’t generate any significant free cash flow until 2020.

Warning to BHP Billiton shareholders….. GET OUT WHILE YOU CAN.

I tell ya, it is amazing to see supposedly savvy businessmen in high-dollar suits making these sort of insane investment decisions.

Okay, let’s get back to the destruction of the copper mining industry.

The First Signs of the Gutting Of The Copper Mining Industry

We are we witnessing the first signs of the gutting of the copper mining industry when we see a collapse of mining truck purchases by Chile. This is bad news as Chile is the largest copper producer in the world. Chile produced 5.7 million tons of copper in 2015, way ahead of the second ranked country, China, that mined 1.6 million tons.

According to a report by the Chilean Copper Commission, new mining truck sales fell to a low of 40 units in 2015, down from a peak of 392 in 2012. As you can see, this is not a slowdown. Rather, truck purchases have fallen off a cliff:

We have to go all the way back to 2004 to see a unit number that low. Even with the huge downturn in the global markets in 2009, Chile still imported 122 new mining trucks that year… more than triple the figure for 2015.

Why is this such a big deal? I took the total number of new trucks imported (purchased) by Chile and compared it to the annual average price of copper:

There seems to be a correlation between the copper price and new truck purchases by the Chilean Copper Industry. When the price of copper fell to $1.34 a pound in 2009, Chile still imported three times more new mining trucks that year than in 2015, when the copper price was double ($2.70). Sadly, Chile’s new mining truck purchases are down 90% from their peak in 2012.

Of course, there were new projects coming online to justify some of the large number of truck purchases in 2011 and 2012. However, Chile’s copper production has only increased from 5.4 million tons in 2010 to 5.7 million tons in 2015. Would a 5% increase in Chile’s total copper production justify the need for 322 new trucks in 2011 and 392 new units in 2012??

Regardless, demand for new mining trucks in Chile has fallen 90% from its peak.just a few years ago I would imagine new truck sales in 2016 will likely be even weaker. This is not a good sign for the largest copper producer in the world.

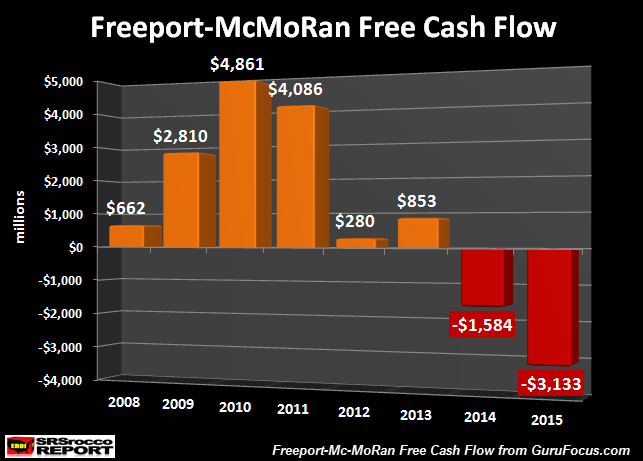

The Top Copper Mining Companies Are Getting Hammered

As I mentioned in the beginning of the article, Freeport-McMoRan suffered a $214 million adjusted income loss in the first half of 2016. That’s pretty bad because “adjusted” income removes many items (such as impairments) from the bottom line to arrive at figure that represents a more realistic day-to-day cost of mining copper.

For example, Freeport also suffered an additional $4 billion impairment on its shale oil and gas assets in the first half of 2016. So, if we add that to the $13 billion of shale asset impairments last year, Freeport has racked up a cool $17 billion in shale asset write-downs in just a year and a half.

Maybe it would have been a good idea for the management at Freeport to stick with mining copper, rather than blowing big money on the U.S. Shale Oil & Gas Black Hole.

If we look at Freeport-McMoran’s free cash flow for the past eight years, something is dreadfully wrong now. For a quick refresher, free cash flow comes from deducting CAPEX (capital expenditures) from their cash from operations:

Here we can see that 2010 and 2011 were good years for Freeport as they enjoyed $4.8 and $4 billion respectively in positive free cash flow. However, this took a turn for the worse in 2014 as free cash flow turned negative to the tune of $1.5 billion, then doubled in 2015 to a negative of $3.1 billion.

Even though some of that negative free cash flow can be blamed on losses from their shale oil and gas assets (liabilities… haha), the majority of Freeport’s revenues are from copper and metal mining. For example, of the $15.8 billion in Freeport’s net revenues in 2015, only $1.9 billion was from U.S. shale oil and gas proceeds.

While the change in Freeport’s balance sheet to negative free cash flow in the past two years is not a good sign, the situation is even worse when we add in their dividends. From 2013-2015, Freeport paid out nearly $5 billion in dividends. Thus, they forked out $8.8 billion more during the past three years than the cash they made from operations.

Now, if we look at the largest copper producing company in the world, their results aren’t any better. In the first quarter of 2016, Chile’s Codelco mining company reported a $125 million net income loss. This loss is purely on producing copper as Codelco doesn’t have any U.S. shale oil or gas assets.

According to Codelco’s financial highlights on their website, they enjoyed a $7.4 billion pre-tax profit in 2012, $3.8 billion in 2013 and $3 billion in 2014. However, things turned south in 2015 as they suffered a $1.4 billion pre-tax loss that year.

Coledco produced 1.9 million tons of copper in 2015, while Freeport came in second at 1.5 million tons. So, the two top mining companies that produced 3.4 million tons of copper in 2015… didn’t really make any money. And it looks like 2016 will be even less fun for these large copper miners

The global copper mining industry is getting ready to face some serious hard times. Again, the falling copper price and the financial trouble taking place in the world’s top copper producers is not the typical market correction awaiting a turnaround in the global economy. Rather the copper industry is heading towards a disintegration to a much smaller size.

Unfortunately, investors and analysts who continue to believe the situation will recover in the global economy, will lose a lot of fiat money holding onto these copper and base metal mining companies. Even though investors should have realized something was wrong when several base metal mining companies moved into the U.S. Shale Oil & Gas Ponzi, and lost a lot of money, they will continue to hold onto these stocks as we enter into the next phase… the Copper Industry Carnage.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.7260( REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.7346 / Shanghai bourse CLOSED UP 2.43 POINTS OR 0.08% / HANG SANG CLOSED UP 202.02 POINTS OR 0.88%

2 Nikkei closed UP 82.13 OR 0.49% /USA: YEN RISES TO 104.26

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index UP to 97.86/Euro DOWN to 1.1005

3b Japan 10 year bond yield: REMAINS AT -.054%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 103.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.95 and Brent:52.29

3f Gold DOWN /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES QUITE A BIT to +064%

3j Greek 10 year bond yield RISES to : 8.42%

3k Gold at $1251.60/silver $17.42(8:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 62.98-

3m oil into the 50 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 104.26 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9894 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0889 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISESto +.064%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.780% early this morning. Thirty year rate at 2.522% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, Futures Jump On Strong China Inflation; Oil Rises Above $51

One day after a slump in Chinese trade sparked a global market selloff on concerns the world’s second biggest economy had once again hit a downward inflection point, overnight China surprised once again, this time to the upside when the latest inflationary data printed hotter than expected, sending European and Asian stocks higher and pushing the yen lower after China’s producer price index rose for the first time since March 2012, while the PBOC fixed the Yuan modestly higher ending a week-long series of declines tracking the stronger dollar and easing concerns of rising capital outflows.

- China CPI (Aug) Y/Y 1.9% vs. Exp. 1.6% (Prey. 1.3%); 3-month high.

- China PPI (Aug) Y/Y 0.1% vs. Exp. -0.3% (Prey. -0.8%); 1st increase in 55 months.

CPI inflation came in at 1.9% year-on-year in September, above market expectations and also higher than the level in August. Both a low base in the same period last year and a sequential price increase contributed to the higher headline CPI year-over-year growth. Food prices were higher (especially fresh vegetables and fruits) and nonfood CPI inflation also increased, driven by higher tourism and education prices. Core CPI inflation (excluding food and energy) was 1.7% yoy in September, vs 1.6% in August.

PPI inflation was +0.1% yoy in September, the first positive reading since March 2012. This implies an annual rate of +3.3% (s.a.) in September, vs. +2.2% in August. The recent sequential pickup of headline PPI in 2016 has been due primarily to a depreciation of the RMB and recovery of oil prices. In addition, favorable base effects (falling oil prices over the course of 2015) have contributed to a moderation in year-on-year PPI deflation. Among major sub-industries, producer prices in smelting and pressing of ferrous metal rebounded visibly to 10.1% yoy from 6.5%yoy in August, and in coal mining and washing industry PPI inflation turned positive to +4.1% yoy, after 51 months of price contraction in year-over-year terms.

As Goldman wrote after the print, policymakers have likely tried to fine-tune the degree of stimulus in September, dialing back a little from the relatively aggressive easing stance and strong growth in August. Targeted tightening measures especially on the property market have been rolled out by the local governments, in an attempt to curb the fast upturn of property prices.

And while some analysts predicted that the rebound in inflation would mean less monetary stimulus out of the PBOC, Goldman was not so sure: “we do not think the recent higher CPI and PPI readings should trigger a sharp turn in monetary policy/overall policy stance, as overall inflation remains mild, and the recently higher CPI and PPI readings are partly driven by the low base last year. We continue to expect supportive fiscal and credit policies going into Q4. ”

Others were simply happy to watch the market reaction: “The turn up in China PPI is indicative of receding deflation risks globally,” said Shane Oliver, Sydney-based head of investment strategy at AMP Capital Investors Ltd., which oversees about $121 billion. “It’s another sign that global deflation is fading. Today’s data was certainly a lot stronger than I thought it would be.

“The turnaround seems to have happened in Asia,” said Frances Hudson, an Edinburgh-based global thematic strategist at Standard Life Investments, which oversees 269 billion pounds ($328 billion). “Following the data on producer prices, we are getting a strong performance from miners. At this stage, any kind of inflation is welcome.”

In other headline news, HP announced plans to cut up to 4,000 job cuts, Reuters reports Hershey CEO preparing to step down.

As a result of the Chinese data, Asian stocks snapped a while stock in Thailand surged on prospects for a smooth transition following the death of King Bhumibol Adulyadej. European shares were close to erasing a weekly decline and emerging markets also rebounded on China’s hotter than expected inflation, even if there . Crude oil extended a fourth week of gains in the longest winning streak since April. The yen fell with bonds as demand for havens eased. Thailand’s stocks jumped the most in three years and currency surged on prospects for a smooth transition of power after the king’s death.

The Stoxx Europe 600 Index gained 1.2 percent at 10:11 a.m. in London, leaving it down less than 0.1 percent in the week. Rio Tinto Group and BHP Billiton Ltd. contributed the most to gains among commodity producers. The MSCI Emerging Markets Index rose 0.6 percent Man Group Plc jumped 16 percent, the most in almost six years, after it posted a 6 percent increase in funds under management for the quarter, announced a share buyback and said it will acquire Aalto Invest Holding AG to branch out into private market investing. Syngenta AG fell 2 percent on speculation that its $43 billion takeover by China National Chemical Corp. could be disrupted after a person familiar with the matter said China is planning to merge the buyer with another state-owned entity, Sinochem Group. In Shanghai, ChemChina’s Aeolus Tyre Co. rose 3.8 percent and Sinochem International Corp. jumped 10 percent.

Among the banking sector, Banco Popolare SC and Banca Popolare di Milano Scarl rose the most among the biggest European banks on optimism that shareholders will this weekend back their merger to create Italy’s third-largest lender.

S&P 500 Index futures rose 0.4%, erasing the previou day’s losses. In commodities, oil climbed 1.2 percent rising above $51.00 a barrel. Distillate and gasoline supplies declined as refineries processed less crude, while inventories at Cushing, Oklahoma, fell to the lowest level since December.

Data on Friday will include retail sales, producer prices and consumer sentiment. Earnings will also be in focus. While analysts are forecasting a 1.6 percent contraction in third-quarter profits for S&P 500 members, U.S. firms have beaten projections by an average margin of 3.6 percentage points in the past five years. Investor attention will turn Friday to earnings from companies including JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. as well as data on retail sales before Federal Reserve Chair Janet Yellen speaks at a conference in Boston.

Bulletin headline summary from RanSquawk

- Encouraging data from China overnight in the form of CPI and PPI has lifted sentiment this morning, with European bourses supported by the upside in material names

- Some early signs that the USD rally is suffering some exhaustion, with EUFt/USD finding bids ahead of 1.1000 while Cable dips into the 1.2100’s are bought up

- Looking ahead, highlights include U. of Michigan, Retail Sales and PPI and comments from Fed Chair Yellen

Market Snapshot

- S&P 500 futures up 0.5% to 2136

- Stoxx 600 up 1.1% to 339

- FTSE 100 up 0.7% to 7023

- DAX up 1.2% to 10535

- German 10Yr yield up 2bps to 0.06%

- Italian 10Yr yield up 1bp to 1.39%

- Spanish 10Yr yield up 1bp to 1.13%

- S&P GSCI Index up 0.6% to 378.1

- MSCI Asia Pacific up 0.2% to 138

- Nikkei 225 up 0.5% to 16856

- Hang Seng up 0.9% to 23233

- Shanghai Composite up less than 0.1% to 3064

- S&P/ASX 200 down less than 0.1% to 5434

- US 10-yr yield up 3bps to 1.77%

- Dollar Index up 0.32% to 97.83

- WTI Crude futures up 1% to $50.96

- Brent Futures up 0.7% to $52.39

- Gold spot down 0.1% to $1,257

- Silver spot up 0.2% to $17.53

Global Headline News

- HP Plans Up to 4,000 Job Cuts Over Three Years Amid PC Slump: Plans to cut 3,000 to 4,000 jobs over the next three years, restructuring may generate $300m in savings in 2020

- Hershey CEO Bilbrey Preparing to Step Down, Reuters Reports: Board has formed committee to seek successor, report says

- China Said to Be Planning Mega-Merger of Sinochem, ChemChina: Deal would combine giants with >$100b in assets; Syngenta Falls as ChemChina Said to Plan Merger With Sinochem

- Apollo Said Close to Deal for Anglo’s Australian Coal Mines: Apollo and Xcoal Energy are poised to buy Anglo American’s Australian metallurgical coal assets, agreement may ultimately value mines at more than $1.5b

- McDonald’s Global Shake-Up Will Add $130 Million in Expenses: To Take 12c/share restructuring charge in 3Q

- Boeing’s Head Salesman Said to Retire as China Veteran Ascends: Mounir said to succeed Wojick as top global sales executive

- Trump Said to Block Campaign’s Requests to Do Self- Opposition Research: Rebuffed political aides’ requests to research his past, people familiar with the matter said

- Bristol-Myers Asked to Seek Special Coverage for Opdivo in U.K.: Opdivo not cost-effective for all lung-cancer patients: NICE

- PepsiCo Said to Near Deal to Buy KeVita: Reuters: May be finalized as early as this month and likely value co. at less than $500m, Reuters reports

- NY Pension Fund Said to Demand 10% Return From Hedge Funds: NYP: State’s $178.6b pension privately told hedge funds in recent weeks must earn minimum 10% annual return: New York Post

* * *

Looking at regional markets, Asia stocks shrugged off the weak Wall Street close and traded with mild gains, as the region gets to digest more data from China. ASX 200 (Unch.) and Nikkei 225 (+0.4%) were initially both higher, although weakness in mining names capped advances in Australia, while Japanese stocks traded choppy alongside JPY movements. Hang Seng was supported after firmer than expected Chinese CPI and PPI figures as CPI printed a 3-month high and PPI rose for the first time in 55 months.

- Chinese CPI (Aug) Y/Y 1.9% vs. Exp. 1.6% (Prey. 1.3%); 3-month high.

- Chinese PPI (Aug) Y/Y 0.1% vs. Exp. -0.3% (Prey. -0.8%); 1st increase in 55 months.

However, Shanghai Comp failed to benefit as the firmer data along with recent measures dampened prospects of future PBoC easing, while the central bank also conducted a net weekly drain of CNY 410bIn. 10-year JGBs were uneventful with demand dampened due to improvement in risk appetite in Asia, while the result of today’s 5-year auction was stronger as laic, lowest price and average price all exceeded the prior month resulting to mild outperformance in the belly.

Top Asian News

- China Sees First Factory-Gate Inflation in Almost Five Years: PPI rose 0.1% y/y in Sept., first gain since January 2012

- Infosys Cuts Sales Forecast Again as Clients Trim Spending: CEO Vishal Sikka stands by $20b revenue goal by 2020

- Oil From $50b Kazakh Kashagan Field Starts Flowing for Export: 7,700 tons of crude shipped to Caspian Pipeline Consortium network

- Singapore Withholds Stimulus, Reserving Tools as GDP Shrinks: Manufacturing plunges 17.4%; services industry declines 1.9%

- Thai Prince Awaits Crown, Groomed Since Birth for Throne: Vajiralongkorn is the sole son of King Bhumibol Adulyadej

- SoftBank Tech Fund to Invest Up to $100 Billion With Saudis: Japanese internet company will put in $25 billion over 5 years

As in Asia, so in Europe encouraging data from China overnight in the form of CPI and PPI has lifted sentiment this morning, with European bourses supported by the upside in material names, which have also staged a recovery from yesterday’s losses. As such, the FTSE 100 has reclaimed the 7,000 level, while the index has also been buoyed by gains in supermarket giant Tesco after the retailer settled a dispute with Unilever over prices. In credit markets, bond yields are a touch firmer with prices pressured by the improved risk sentiment. Additionally, Gilts yet again underperform against its counterparts as the rating agency S&P hints at another downgrade from the AA sovereign after highlighting risks to the economy’s future growth amid negotiations with the EU. Gold (-0.1%) saw minor losses amid improvement in risk sentiment while remained near yesterday’s lows alongside weakness across the metals complex.

Top European News

- VW Fails to End Europe Market-Share Drop a Year After Crisis: September sales rose 5.6% versus market’s 7.3% gain; EU28 September Car Registrations Rise 7.2% Y/y to 1.455m Units

- UniCredit Plans to Raise Up to $14 Billion, Repubblica Says: Increase is part of a plan that will be presented on Dec. 13, the newspaper reported on Friday

- Banco Popolare Sells EU618m NPL Portfolio to Hoist Finance Unit

- Ericsson Credit Rating Cut by Moody’s as Crisis Intensifies: Rating was reduced one level to Baa2 from Baa1

- Man Group Soars on Quarterly Asset Growth That Beats Estimates: Net inflows were $1.3b in 3Q as investors allocated money to its computer-driven hedged and long only funds

- Marmite Skirmish Averted Won’t Stop Brexit Biting Retailers: Asda cuts price on Unilever’s spread after Tesco feud settled

- BOE Says Mortgage Demand Fell ‘Significantly’ in 3Q: Says both demand for prime and buy-to-let lending decreased significantly.

- Spotify Co-Founder Lorentzon Steps Down as Company Chairman: Will remain at the Swedish music startup as vice chairman

In FX, the yen fell against all of its 16 major counterparts, dropping 0.5 percent to 104.21 per dollar. The Bloomberg Dollar Spot Index rose 0.2 percent, extending this week’s advance to 0.7 percent. The pound fell, extending its October decline to almost 5.7 percent. Thailand’s baht led emerging-market currencies higher, gaining 0.9 percent, the most in a year and paring this week’s slide to 1.1 percent. The SET Index jumped 4.2 percent after slumping for the first three days of the week. Financial markets in the Southeast Asian nation are open as usual Friday following the death of King Bhumibol Adulyadej on Thursday. Thailand’s government called on the nation to avoid “joyful events” for 30 days, to dress in mourning for a year and pray for the king’s soul to protect the nation. It also signaled the 88-year-old king’s only son will take the throne.

In commodities, oil climbed 1.2 percent rising above $51.00 a barrel. Distillate and gasoline supplies declined as refineries processed less crude, while inventories at Cushing, Oklahoma, fell to the lowest level since December, according to an Energy Information Administration report Thursday. Industrial metals were broadly higher in Shanghai and London. Aluminum in China rose to the highest level in almost five months, following a rise in the local spot price amid a new Chinese regulation that clamps down on truck overloading, which is disrupting deliveries. Gold slipped in London trading, giving back gains from Thursday.

DB’s Jim Reid concludes the overnight wrap

Life can carry on as normal here in the UK as ‘Marmitegate’ has been resolved as the largest food retailer has put it back on the shelves after a 24 hour dispute with its supplier. This has been a fascinating story that will rumble on and on as at some point soon shoppers are going to face a big rise in the cost of their basic products given the significant post Brexit fall in Sterling. It seems for now prices have not climbed but surely it can’t be long. Maybe the best trade you can do at the moment is to stock up on all the non-perishable items that will eventually be forced up in price once stocks have been depleted or contracts renegotiated. Given my wife’s obsession with Ben and Jerry’s (one of the other products that was temporarily withdrawn) it might be prudent to buy a chest freezer for the garage and stock up this weekend.

Today the main event will probably be Yellen’s speech at 6.30pm BST where she is the keynote speaker at the annual economics conference hosted by the Boston Fed. The conference topic is ‘The Elusive Great Recovery: Causes and Implications for Future Business Cycle Dynamics”. It’s unclear what she’ll say about the current outlook but clearly the market will be looking for any policy morsels, especially after the minutes on Wednesday night. Possibly more important will be the triple hit of US bank earnings with JPM, Citibank and Wells Fargo reporting either just before or at the opening bell. With all the attention on financials of late these results will give us a good guide to earnings on both sides of the Atlantic for the sector. If that’s not enough we have US retail sales as the main data event of the day. While the data only captures about one quarter of the consumer spending data that are used in GDP, the figures are important in showing us the state of underlying spending in the US economy. The market is expecting a decent bounceback in September. The headline print is expected to increase +0.6% mom while the ex auto and ex auto and gas components are expected to increase +0.5% mom and +0.3% mom respectively. The important control group component is also expected to have increased +0.4% mom.

So between the packed schedule today and the FOMC minutes on Wednesday, markets yesterday were caught in a bit of a vacuum. Instead investors were left to feed off that soft China export data nearly 24 hours ago which seemed to reinvigorate some concern about the world’s second largest economy. Europe followed the risk off lead from Asia with the Stoxx 600 edging -0.87% lower. Across the pond the S&P 500 initially opened down as much as -1.16% with financials under pressure ahead of today’s bank earnings, but the index then rallied back into the close to pare the bulk of that decline and finish -0.31% as defensive sectors led the rebound. As we noted yesterday, while clearly still of significant importance, that China trade data does have a tendency to be quite volatile month to month. However it lines the market up for a busy next five days of data in China culminating with the Q3 GDP print on Wednesday.

On that note, this morning the latest inflation numbers are out in China. Headline CPI rose to +1.9% yoy in September from +1.3% in August. Expectations were for +1.6% and that reading is the highest since June. Meanwhile, producer prices surged last month. The +0.1% yoy reading (vs. -0.3% expected) compares to -0.8% yoy in August and marks the first time in 54 months that annual factory gate prices have risen. The MoM reading for PPI was +0.5%.

In terms of the market reaction, it’s been a bit of a reversal of yesterday’s price action with China bourses lower but Asia ex-China equity markets gaining. The Shanghai Comp is currently -0.53% while the Hang Seng (+0.58%), Nikkei (+0.41%), Kospi (+0.52%) and ASX (+0.05%) have all gained. The Aussie Dollar is up while other emerging market currencies have strengthened with Oil. Also of note was data in Singapore this morning where Q3 GDP printed at a seasonally adjusted QoQ rate of -4.1% (vs. 0.0% expected). That is the steepest fall since Q3 2012. Despite that data, the MAS held stimulus unchanged this morning.

There are also a couple of interesting micro level stories out there this morning. According to Bloomberg, China is planning to merge SOE’s Sinochem Group and China National Chemical Corp. Shares of Sinochem are up close to 10% following the news. Also Japan telecom giant Softbank announced that it is to form a tech focused investment fund which could manage up to $100bn with Saudi Arabia’s sovereign wealth fund being a lead partner.

In one final mention of China for today, yesterday DB’s Chief Economist for China, Zhiwei Zhang, published an update to his special report on China’s property bubble. He notes that the Shanghai government has tightened credit supply for developers over the past week. In particular, the government tightened regulation on property developers’ financing of land purchase. Developers are not allowed to buy land using financing from banks, trust, capital market, asset management companies or insurance companies. They need to commit in land auctions that they will only use their own funds to buy land. Zhiwei sees this as a significant step by the government to contain the property bubble and shows that the government has become aware of the problem, and have started to take tough actions to stop it. He expects other cities to follow suit. A link to the report for those interested is attached here.

Back to markets yesterday. Given the broadly risk-off moves, it was a stronger day in rates with 10y Treasury yields closing nearly 3bps lower at 1.742%, while 10y Bunds were down a similar amount to 0.036%. The US Dollar was actually close to half a percent weaker although that did follow a gain of nearly +1.50%. Gold was a touch higher while WTI (+0.52%) rebounded modestly following two days of consecutive declines. Credit indices in both Europe and the US generally pared earlier losses into the close. The more notable news in credit markets perhaps was the latest corporate bond holdings data out of the Bank of England. The BoE confirmed that it held £1.042bn of corporate bonds at the close on Wednesday. That compares to the £507m it held in the first week so the strong run rate has continued for a second week. As a reminder the initial aim was to buy £10bn over 18 months so they are well ahead on a run rate basis. It clearly also raises the question of a possible increase in the total quantum of purchases being targeted. So far though the BoE is certainly putting forward a big statement.

Staying in the UK, at yesterday’s SNP party conference, Scotland’s First Minister Nicola Sturgeon confirmed that she will publish a draft Scottish Independence Referendum Bill next week. Sturgeon said ‘I am determined that Scotland will have the ability to reconsider the question of independence – and to do so before the UK leaves the EU – if that is necessary to protect our country’s interests’. According to the FT Sturgeon also pledged to issue specific proposals to keep Scotland in the single market as well as also calling for new powers over immigration and international relations. While we’re on the Brexit theme, EU President Donald Tusk was as black or white as one can be with his comments yesterday at a conference in Brussels. Tusk said that ‘the only real alternative to a hard Brexit is no Brexit, even if today hardly anyone believes in such a possibility’. He also said that ‘the essence of Brexit as defined in the UK referendum campaign‘ means ‘radically loosening relations with the EU, a de facto hard Brexit’. Tusk also offered a slightly different perspective on how he saw things, saying that a hard Brexit will be a loss for everyone and that ‘there will be no cakes on the table for anyone’ but rather ‘only salt and vinegar’. Whatever that means.

Before we look at today’s calendar, the data didn’t add much to the debate yesterday. Initial jobless claims printed a little better than expected at 246k although that was unchanged on the prior week, while the US import price index rose a little bit less than expected last month (+0.2% mom vs. +0.1% expected). Philadelphia Fed President Harker (hawkish leaning non-voter) also spoke and said that ‘what I’m worried about is, depending on the outcome of the election and what happens after that, if there are policies that would have distortive effects that we would have to respond to’. Given that, Harker thinks it may be prudent ‘to wait until we resolve some of that uncertainty’.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 2.43 POINTS OR 0.08%/ /Hang Sang closed UP 202.01 POINTS OR 0.88%. The Nikkei closed UP 82.13POINTS OR 0.49% Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed UP at 6.7260/Oil ROSE to 50.95 dollars per barrel for WTI and 52.29 for Brent. Stocks in Europe: ALL IN THE GREEN Offshore yuan trades 6.7346 yuan to the dollar vs 6.7260 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES

3a)THAILAND/SOUTH KOREA/SOUTHEAST ASIA:

b) REPORT ON JAPAN

none today

c) Report on CHINA

4 EUROPEAN AFFAIRS

GERMANY/DEUTSCHE BANK

The hits just keep coming to Deutsche bank as one day after announcing a hiring freeze, they decide to fire another 10,000 workers. A great reason for gold to be whacked today by the crooks:

(courtesy zero hedge)

Deutsche Bank To Fire Another 10,000 Bankers, Bringing Total Layoffs To 20% Of Workforce

The hits for Deutsche Bank just keep on coming. One day after a report that the German lender has imposed a hiring freeze in the latest bid to reassure investors that it has expenses under control and is stemming the outflow of cash, moments ago Reuters reported that Deutsche Bank’s finance chief told his staff that job cuts at the bank could be double that planned, a step that could remove 10,000 further employees.

Such cuts would likely take many years but setting such a goal could reassure investors that the bank is determined to tackle costs that sources said the European Central Bank sees as bloated. Unless, of course, they are forced to cut much faster. If 10,000 job losses were ultimately to follow the 9,000 announced by management in October 2015, roughly one in five of the bank’s workforce around the globe would be affected.

“Schenck said that the bank would need to cut another 10,000 staff to bring down costs,” said a person who attended the meeting with the chief financial officer cited by Reuters. Although no such decision has yet been taken, Marcus Schenck’s remarks, at an internal meeting, signal the lender is considering further significant cost cuts, as it faces a multi-billion-euro fine and a crisis of confidence among investors.

The discussion about further job cuts comes as Deutsche’s chief executive, John Cryan, reassesses a year-old strategy to revive the flagging group, as ebbing market confidence sends its stock price tumbling and prompts some customers to withdraw funds.. A second person familiar with these discussions said the management was also examining the countries where the bank was active to see “whether it was really worth its while (staying in those countries)”.

DB’s latest announcement follows Commerzbank, Germany’s second biggest bank rival, which recently announced it would ax more than a fifth of its workforce – almost 10,000 staff.

Still, it is not clear if DB can achieve the cuts: given potential high severance costs and revenue losses, it remains unclear whether a further attempt by Deutsche to trim staff can be achieved. Headcount has actually risen at the bank, despite the plans announced by Cryan in October 2015 to slash staff. Employee numbers, which stood at more than 101,300 in the middle of this year, are higher than the roughly 98,600 one year earlier.

One hurdle in removing staff is that many are based in Germany, where strict labor law makes it difficult and expensive to fire employees. Of the 9,000 job cuts announced in October 2015, 4,000 are in Germany.

In Germany, unlike Britain, for instance, labor representatives have an important say and appoint non-executive directors to Deutsche’s supervisory board. They will argue for fewer cuts.

Additionally, DB’s layoffs are getting to the point where it is now cutting into the muscle, and any additional terminations could result in a drop in revenue. Regardless of this, however, the heavy fine demanded by the U.S. authorities could prompt Cryan to act.

Once Germany’s only bank to go head-to-head with U.S. rivals on Wall Street, stricter regulation, rock-bottom borrowing costs and still heavy costs has squeezed Deutsche’s profits. Politicians in Germany, who are preparing for national elections in 2017, are watching developments nervously.

end

Qatar is now worried about their investment in Deutsche bank

(courtesy zero hedge)

Deutsche Bank’s Biggest Investor Is Getting Worried As Government Rules Out State Bailout

Just a week after Qatar investors were ‘used’ as the headline ammunition for short squeeze momentum ignition in Deutsche Bank’s stock, WSJ reports the beleaguered bank’s biggest shareholder is getting worried, questioning management’s long-term strategy. The shares are slipping further as the German government rules out any state aid for the most dangeorus bank in the world.

Following yesterday’s dip, Deutsche stock is bid today but remains the same 12-12.50 range it has been in for a week… as credit markets remain near record wides…

Which perhaps helps explain Deutsche bank’s biggest shareholders’ concerns… (via The Wall Street Journal)…

The Qataris have reiterated their patience as long-term shareholders, with an interest in even eventually boosting their stake further, the people say.

But they don’t plan to do so immediately, some of the people said. First, the Qataris have said they want more clarity.

They are concerned about an erosion of profits and loss of talent in key businesses like investment banking and asset management, the people say. The asset-management business has had three leaders in the past 18 months, and managers have been in the position of reassuring both clients and employees of the bank’s commitment to it, people close to it say.

The Qataris have sought assurances that Deutsche Bank executives and its supervisory board are actively weighing all options, including a sale of the asset-management business, should legal fines or other factors press them to take more-dramatic steps than planned earlier.

Mr. Cryan has said asset management is an essential part of the bank.

The Qataris’ concerns increased after The Wall Street Journal reported Sept. 15 that the Justice Department suggested Deutsche Bank pay $14 billion to settle longstanding mortgage-securities cases, the people said. That opening bid from the U.S. government, which Deutsche Bank confirmed, is widely seen by investors and lawyers—and the bank itself—as much higher than what Deutsche Bank ultimately will end up paying.

Bankers and others who have spoken with existing and potential investors, or been briefed on discussions with them, say one concern is that most of Deutsche Bank’s management board lacks experience running the bank. Only one of its 11 members belonged to the board before January 2015. Five joined this year.

None of this is helped by the fact the German government has just come out and ruled out taking any stake in Deutsche Bank…

Aides to German Chancellor Angela Merkel have told lawmakers the state wouldn’t take a stake in Deutsche Bank AG if it were to issue new stock to shore up its thin capital cushion, one person who attended the briefing said.

The fact that Berlin appears to have ruled out any help for the embattled lender as both unnecessary and politically unfeasible could put Deutsche Bank under renewed pressure as it works to stabilize its share price and stay out of the news while negotiating an acceptable settlement in a U.S. misconduct investigation.

In a closed-door briefing with a small group of lawmakers last week, Chancellery aides and senior Finance Ministry officials said it was “inconceivable for the state to take a stake in Deutsche Bank,” said one person who declined to be named because the briefing was confidential.

“We have a different bank resolution system than in 2009 and this must apply to us in Germany too,” the government officials said according to this person. This referred to recent legal changes that now force European governments to bail-in creditors—and in some cases depositors—before they shore up a struggling bank with taxpayer money.

Still the fact that the credit and equity market remain so violently opposed here and the bank’s biggest shareholder is publicly noting its concern… is probably nothing.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6. GLOBAL ISSUES

Raoul Pal is one smart cookie. Pay attention to him as he discusses the global economy:

(courtesy Rauol Pal/Barbara Kollmeyer/Market Watch)

A recession is coming — so hide in gold, says influential investor Raoul Pal

Goldman Sachs alum says negative rates mean gold should be a lot more expensive

By

By

BARBARAKOLLMEYER

Real Vision

Real VisionMirror, mirror on the wall, which asset is most mispriced of all? According to a Goldman Sachs alum who predicted the financial crisis in 2008, it’s gold.

The precious metal should be a lot more expensive when the likelihood of a global financial collapse and a move toward negative interest rates is accounted for, says Global Macro Investor founder Raoul Pal, who now sees a U.S. recession within 12 months.

Recent losses for gold may have dented investor confidence. Gold GCZ6, -0.37% is up 18% this year, but the first full week of October marked its worst seven-day performance in over three years; it also posted a three-month loss of nearly 6% on a continuous basis.

Uncertainty about Brexit and the timing of a Federal Reserve rate hike triggered a rush into the dollar, which often moves inversely to the metal. (Higher rates can work against gold, but the metal becomes a safe haven if the economy slows.)

“As we get to negative interest rates, gold is a good place to park your cash,” said Pal, who discussed his outlook with MarketWatch in a September interview and a follow-up conversation over email.

“I’m not a gold bug,” the former GLG Global Macro Fund co-manager — who is also watching the dollar closely — “but this is the currency I would choose now.”

Pal, an economist and strategist, also co-founded Real Vision TV, which conducts interviews with prominent investors. Many of his recent guests share his enthusiasm for gold, according to Pal.

“All the really serious thinkers are interested in gold,” he said.

How a U.S. recession could boost gold and the dollar

Pal’s core presumption — one he’s held since 2014 — is bad news for the U. S: He is convinced the country is headed for recession within a year. “The business cycle points to that,” he said, “and 100% of all two-term elections have had a recession within 12 months since 1910.”

His view contrasts with the Federal Reserve’s own indicator, based on corporate-bond spreads, that predicts just a 12% chance of a pullback in the next year.

But Pal does have some prominent company: Savita Subramanian, Bank of America’s head of equity strategy, recently predicted the same; Janus Capital’s Bill Gross spoke of a lagging U.S. recovery in his September investment note; and bond investor Jeffrey Gundlach showed a chart during a recent webcast that revealed the start of a recession. And Wilbur Ross sees one coming in 18 months.

Should his prediction come true, Pal says, gold prices could double. If central banks want to get active and combat a slowing economy, he says, they will try to stimulate the economy via printing money or more easing, all of which plays “into the hands of gold.”

This view brings Pal to the asset he favors most over the next year out of bonds, equities, currencies and commodities: the dollar. He told MarketWatch he’d buy U.S. dollars, selling the euro, pound and Aussie dollar; he expects the euroEURUSD, -0.7867% to eventually drop to 75 cents against the dollar — about 3% below current levels — over time.

“The world has shifted because of negative interest rates,” Pal said. “We know the dollar will go higher, [and] gold may outperform over time, the reason being because of negative interest rates. If I get it right, I have dollars and gold…I don’t make much of a loss if that correlation breaks.”

Year-to-date, the dollar index DXY, +0.57% is down nearly 1%, which some blame in part on an inactive Fed. Interest-rate increases can have a positive effect on a country’s currency by making it more attractive to foreign investors.

But Pal insists that his dollar call is not tethered to central bank policy, saying investors should let go of the belief that those institutions are like “the Wizard of Oz.” Investors, Pal said, believe the Fed’s policy choices can keep stocks from falling even as Japan and Switzerland have proven otherwise.

Read: Central banks ‘have never been on thinner ice’

The Bank of Japan “has done more easing, as has the Swiss,” Pal said. “It’s not achieved anything. Stock markets there have fallen, yet the market wants to believe the Fed that there is an implicit put on the stock market in the U.S.”

Switzerland has had negative interest rates in place since early 2015, yet stocksSMI, +1.12% fell 1.6% in 2015 and are down nearly 10% so far this year.

Japan moved to negative interest rates this year, yet the Nikkei 225 NIK, +0.49% is down nearly 12%.

Real Vision

Real VisionHe believes the market is currently short the dollar and should a banking crisis crop up in Europe, he says, euros will get less attractive as investors prefer dollars. In a recent interview on Real Vision, Pal discussed the problems at Deutsche Bank DB, +0.52% — but also how the problems extend far beyond Germany’s borders.

Spanish banks — ones like Banco Sabadell SAB, +0.81% Banco PopularPOP, +0.59% — they’re all in free fall, [at] all-time lows,” Pal said. Italian banks, with still unresolved bad debt issues, are still a problem, and then Swiss and U.K. banks also look unwell, he said.

“I think it’s the start of something,” he said of Deutsche Bank’s woes.

Read: How Deutsche Bank is Lehman Brothers and how it isn’t

The dollar, Pal said, also looks favorable against the backdrop of the three-month U.S. dollar Libor (London interbank offered rate), the benchmark rate some of the world’s biggest banks charge each other for short term loans. When those rates are rising, he says, dollars are more attractive.

In the last 12 months, Libor has nearly tripled, he said, moving from 0.31% to 0.88%.

“It is also a sign that there is distress among dollar borrowers abroad, so they might need to buy dollars to close out their risk,” said Pal. Financial institutions, in other words, are fretting about potential market downside, and when they get worried, the Libor moves higher.

The one chart he uses to track economic cycles

Pal is not a fan of U.S. stocks — the S&P 500 index SPX, +0.02% is up just 3.7% so far in 2016 — largely because of what he sees in a chart he says that has failed him just once when he didn’t trust it. Now, he says, it’s telling him his recession prediction is spot on.

That chart is the Institute for Supply Management index, which is based on surveys of more than 300 manufacturing firms and gauges the health of the industry. The ISM rebounded in September, to 51.5% from 49.4% the previous month. But economists still say the U.S. manufacturing sector faces challenging conditions.

“There’s a difference between the narrative, which is what you’re being told, versus the reality of the economic data,” said Pal. “It’s in no one’s interest ahead of the election to say the U.S. economy is a mess — [that] world trade freight shipments, container shipments, retail sales, restaurant sales, factory orders, durable orders are all showing a recession.”

Pal says the ISM correlates well with U.S. assets. “It peaked in 2011 and has been bouncing around 50 for a while now,” he said. “The moment it starts to get to 47, 46, the odds of a full-on recession explode to 85%. We’re very close now, getting to the point where the probability is very high.”

Real Vision