Gold $1254.40 UP $1.30

Silver 17.43 UP 4 cents

In the access market 5:15 pm

Gold: 1255.20

Silver: 17.48

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est and 2:15 am est

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix OCT 17 (10:15 pm est last night): $ 1257.83

NY ACCESS PRICE: $1252.50 (AT THE EXACT SAME TIME)

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1260.31

NY ACCESS PRICE: 1255.60 (AT THE EXACT SAME TIME)

HUGE SPREAD TODAY!! 5 dollars

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: OCT 17: 5:30 am est: $1252.70 (NY: same time: $1253.50: 5:30AM)

London Second fix OCT 14: 10 am est: $1254.80 (NY same time: $1255.50 , 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

530 NOTICES FILED FOR 53,000 OZ

For silver:

for the Oct contract month: 1 notice for 5,000 oz.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 2,899 contracts UP to 188,990. The open interest FELL as the silver price was DOWN 2 cents in yesterday’s trading .In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .945 BILLION TO BE EXACT or 135% of annual global silver production (ex Russia &ex China).

In silver for October we had 1 notice served upon for 5,000 oz

In gold, the total comex gold FELL by 6,387 contracts with the FALL in price of gold( $1.90 ON FRIDAY) . The total gold OI stands at 491,627 contracts. The bankers continue with their quest of fleecing our comex gold longs

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

TODAY WE HAD A HUGE CHANGES AT THE GLD: A DEPOSIT OF 3.86 TONNES

Total gold inventory rests tonight at: 965.43 tonnes of gold

SLV

we had NO CHANGES at the SLV/

THE SLV Inventory rests at: 362.285 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 2,899 contracts UP to 188,990 as the price of silver FELL by 2 cents with yesterday’s trading.The gold open interest fell by 6,387 contracts down to 491,627 as the price of gold FELL $1.90 IN FRIDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

end

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed DOWN 22.64 POINTS OR 0.74%/ /Hang Sang closed DOWN 195.77 POINTS OR 0.84%. The Nikkei closed UP 43.75POINTS OR 0.26% Australia’s all ordinaires CLOSED DOWN 0.83% /Chinese yuan (ONSHORE) closed DOWN at 6.7378/Oil FELL to 50.30 dollars per barrel for WTI and 52.19 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.7491 yuan to the dollar vs 6.7260 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AS MORE USA DOLLARS LEAVE CHINA’S SHORES

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

Last night 3 biggies:

i) rising inflation which would stop the POBC from monetary easing

ii) a jump in the dollar (fall in CNH/CNY) which again causes inflation risks/and sends deflation scares throughout the world/

iii)Shanghai B share index crashes over 6% in last 90 minutes of trading

( zero hedge)

4 EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SAUDI ARABIA

Rising Sibor rates causes Saudi bank stocks to tumble as its bailout of the economy fails to stem liquidity problems:

( zero hedge)

ii)RUSSIA VS USA

Putin describes that it is Hillary that is banging the war drums. He is very concerned that the world is rushing irreversibly towards a nuclear showdown

( zero hedge)

iii)RUSSIA

(courtesy zero hedge/RT)

6.GLOBAL ISSUES

Another indicator that the global economy is in trouble: Caterpillar CEO retires immediately. This is after 45 straight months without an uptick in global sales.

( zero hedge)

7.OIL ISSUES

Iran disagrees with OPEC production estimates and they also state that they will increase production from 4.8 million barrels per day up to 5 million by the end of the year:

( zerohedge

8.EMERGING MARKETS

This could spell trouble for Venezuela’s state owned oil company PDVSA. They need to swap a bond issue for a longer duration back into 2020. If investors say no then this might cause a default

( Julieanne Geiger/OilPrice.com)

9.PHYSICAL STORIES

i)A terrific commentary from Egon Von Greyerz as he indicates that central banks if they are lucky have only 12,000 tonnes and much of this gold has been leased out (probably many times over). Eastern nations like China and Russia have been mopping up this gold and storing the yellow stuff on their shores.

( Egon Von Greyerz/Matterhorn)

ii)Actually gold denominated in other currencies is doing quite well.

(Egon Von Greyerz/Kingworldnews)

iii)A PHD thesis starts the ball rolling on our now famous gold-silver price fixing case.

Yet this is only 1% of the fraud, they will uncover more as the banks collude to fix prices on a daily basis outside of the fix as well

( Burrell/.Austalian/Syndey/GATA)

iv)This is interesting: Perth Mint tests out the Indian gold excise import tax

( Garvey/Australian/GATA)

v)For the first time, the Bank of England ready to tolerate higher inflation

( London Telegraph/GATA)

vi)Ice will start gold futures trading for clearing at London’s daily auction

( Bloomberg News/Eddie VanDer Walt)

10.USA STORIES WHICH MAY INFLUENCE THE PRICE OF GOLD/SILVER

i)A huge miss for the all important NY Empire Manufacturing Fed report showing contraction at -6.8 vs 1.0 expectation. The June dead cat bounce is officially over.

( NY Mfg Empire (NY) Fed index/zero hedge)

ii)Industrial production contracts for the 13th straight month. This is another important indicator suggesting that the real USA economy is in turmoil

( zero hedge/Industrial production)

iii)The truth behind the true budgetary deficit and the real added national debt for Fiscal year 2016:

( Jim Quinn/Burning Platformblog)

iv)Michael Snyder: 35% of Americans have debt that is at least 1/2 year past due

( Michael Snyder/EconomicCollapse Blog)

v)the FED is now geared to steepen the yield curve and thus increase inflation beyond their magical 2%

(courtesy zero hedge)

vi)The USA tries to silence Assange: the Brits pull the plug on Assange’s interest connection in the Ecuadorian embassy inside London.

( zero hedge)

vii)Over the last two months we have brought to you the story of fraud and pension shortfalls in the Dallas police and firefighters pension fund. Since the police there know full well that at the end of the tunnel there will be no money for them, they are leaving the force right now and collecting big lump sum payment:

( zero hedge)

viii) closing interview of Rob Kirby with Greg hunter/

Let us head over to the comex:

The total gold comex open interest FELL BY 6,387 CONTRACTS to an OI level of 491,627 as the price of gold FELL $1.90 with FRIDAY’S trading.

We are in the delivery month is October and here the OI GAINED 292 contracts UP to 661. We had 41 notices filed yesterday so we gained another 333 contracts or 33,300 additional oz will stand.

The next delivery month is November and here the OI ROSE by 46 contracts UP to 2986 contracts. This level is extremely elevated as generally November is a very poor delivery month.To give you an idea of size, on Oct 14 2015, we had an OI of only 240 contracts.The next contract month and the biggest of the year is December and here this month showed an decrease of 6,623 contracts down to 366,762.

And now for the wild silver comex results. Total silver OI rose BY 2899 contracts from 186,091 up to 188,990 as the price of silver fell to the tune of 2 cents yesterday. We are moving further from the all time record high for silver open interest set on Wednesday August 3: (224,540). The next non active delivery month is October and here the OI rose by 26 contracts up to 147. We had 2 notices filed yesterday so we gained 28 contracts or 140,000 additional oz will stand for delivery.The November contract month saw its OI lose 4 contracts down to 329. The next major delivery month is December and here it ROSE BY 765 contracts UP to 150,145

VOLUMES:

Today the estimated volume was 109,702 contracts which is poor.

Yesterday, the confirmed volume was 193,787 which is also fair.

today we had 1 notice filed for 5,000 oz of silver:

| Gold |

Ounces

|

| Withdrawals from Dealers Inventory in oz | NIL |

| Withdrawals from Customer Inventory in oz nil |

NIL oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

803.75 oz

MANFRA

|

| No of oz served (contracts) today |

530 notices

530,000 oz

|

| No of oz to be served (notices) |

131 contracts

13.100

oz

|

| Total monthly oz gold served (contracts) so far this month |

8519 contracts

851,900 oz

26.49 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 175,209.0 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued form their client or customer account. The total of all issuance by all participants equates to 530 contractS of which 482 notices were stopped (received) by jPMorgan dealer and 1 notice(s) was (were) stopped received) by jPMorgan customer account.

| Silver |

Ounces

|

| Withdrawals from Dealers Inventory | NIL |

| Withdrawals from Customer Inventory |

856,649.226 oz

DELAWARE

SCOTIA

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

1,004,022.39 oz

CNT

HSBC

JPM |

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

146 contracts

(865,000 oz)

|

| Total monthly oz silver served (contracts) | 356 contracts (1,780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4.778,130.5 oz |

end

NPV for Sprott and Central Fund of Canada

will not provide today.

end

And now your overnight trading in gold,MONDAY MORNING and also physical stories that may interest you:

Property Bubble In Ireland Developing Again

Budget 2017: “Good Work To Halt Second Property Crash Undone In A Day”

David McWilliams has pointed out in two of his most recent articles how Budget 2017 and the latest mortgage tax grant risk creating a “second property crash”:

“We are faced with similar concerns on the horizon now. Unlike 2008, when this country went bust, or in 2012, when the euro as a currency was in real danger of falling apart, there is no serious internal threat. In 2012, the world’s central bankers cutting interest rates to zero prevented the disintegration of the euro. This may have saved the currency then, but it means that today central bankers have no ammunition left if there is another downturn. Interest rates are as low as they can go.

Unfortunately, the trading economies that Ireland depends on have not responded to zero interest rates with any real gusto. They are sluggish at best. This sluggishness means that the average guy feels left behind and sees real gains going to the very rich. As a result, the mainstream political players are now being rejected in favour of populists. This is happening everywhere, particularly in the UK, the US and France.”

The stupidity of this latest populist government gimmick and tampering in the property market was further underlined in an article published today:

“I have no problem with paying civil servants well. But I do have a problem with rewarding stupidity. These mandarins are trained economists who should explain to politicians what is likely to happen in a dysfunctional housing market when you introduce tax breaks for first time buyers.

On Friday, it was widely reported that many developers automatically increased the price of starter homes in response to the budget. They didn’t even wait for the Finance Bill to be enacted, prices all over the country simply jumped overnight.

This is exactly what I would have expected a decent ordinary level Leaving Cert economics student to have replied in answer to the opening question.”

Another property bubble in Dublin is gradually forming. Prices at the high end of the market have surged in recent years and some areas are back at record levels seen in 2007/2008. Already, there have been sharp falls of 15% to 20% in the leafier suburbs of Dublin – in Dublin 4, Dublin 6 and high end Killiney and Foxrock-Carrickmines as reported in detailed analysis by the Sunday Business Post recently.

The government’s latest measure will add to the overheating that is already being seen in the lower end and the mid end of the Dublin market. There is a real risk that another generation of young people are saddled with massive debts and we see another “negative equity generation”.

Another property crash would further devastate our banks and have an attendant impact on Irish assets – from property to stocks, bonds, Irish bank deposits and government “guaranteed” savings products.

McWilliams recent articles on the latest property madness can he found here andhere

Gold and Silver Bullion – News and Commentary

Singapore makes another bid for Asia to help set gold price (Reuters)

Asian shares fall, dollar at 7-month high after Yellen comments (Reuters)

Gold to Sell Off, Then Rebound to $1,350 Next Year, TD Says (Bloomberg)

ICE Will Start Gold Futures for Clearing London’s Daily Auction (Bloomberg)

Gold drops on dollar rise as U.S. data supports rate-hike prospect (Reuters)

Video: Is It Over For Gold? No (Forbes)

US Debt Soars To $19.7 Trillion (ZeroHedge)

Standard & Poor’s warns on UK reserve currency status as Brexit hardens (Telegraph)

Tiny Startups Revamp Gold Market After Besting Big Exchanges (Bloomberg)

Tangible and intangible factors will support the gold price (MineWeb)

Gold Prices (LBMA AM)

17 Oct: USD 1,252.70, GBP 1,029.59 & EUR 1,139.58 per ounce

14 Oct: USD 1,256.15, GBP 1,028.79 & EUR 1,140.08 per ounce

13 Oct: USD 1,258.00, GBP 1,029.93 & EUR 1,141.76 per ounce

12 Oct: USD 1,255.70, GBP 1,024.53 & EUR 1,139.05 per ounce

11 Oct: USD 1,256.40, GBP 1,021.58 & EUR 1,130.76 per ounce

10 Oct: USD 1,262.10, GBP 1,016.62 & EUR 1,129.71 per ounce

07 Oct: USD 1,255.00, GBP 1,012.91 & EUR 1,127.62 per ounce

Silver Prices (LBMA)

17 Oct: USD 17.40, GBP 14.30 & EUR 15.83 per ounce

14 Oct: USD 17.47, GBP 14.28 & EUR 15.86 per ounce

13 Oct: USD 17.59, GBP 14.40 & EUR 15.95 per ounce

12 Oct: USD 17.44, GBP 14.23 & EUR 15.83 per ounce

11 Oct: USD 17.48, GBP 14.26 & EUR 15.78 per ounce

10 Oct: USD 17.78, GBP 14.31 & EUR 15.92 per ounce

07 Oct: USD 17.33, GBP 14.01 & EUR 15.55 per ounce

Recent Market Updates

– “Gold Is A Great Hedge Against Politicians” – Goldman

– Sell Gold Now – Time To Liquidate Gold ETF, Pooled and Digital Gold

– Gold In GBP Up 43% YTD – “Massive Twin Deficits” To Impact UK Assets

– Ron Paul Says “Gold Going Up” Whether Trump Or Clinton Elected

– Gold Trading COT Report “Means Lower – Then Much Higher – Prices Coming”

– Currency Shock Sees Sterling Gold Surges 5% In One Minute “Flash Crash”

– Top Gold Forecaster: “As Quickly As Gold Fell” May “Rally Back” on Global Risks

– Gold Buying ‘Opportunity’ After Surprise 3.4% Drop

– Deutsche Bank “Is Probably Insolvent”

– GBP Gold Rises 1.3% as Sterling Slumps On ‘Hard Brexit’ Concerns, Up 36% YTD

– Why Krugman, Roubini, Rogoff And Buffett Hate Gold

– ECB Refused “To Answer Questions” – Deutsche Bank “Systemic Threat” Is “Not ECB Fault”

– Euro “Might Start To Unravel” If Collapse Of Deutsche Bank

end

A terrific commentary from Egon Von Greyerz as he indicates that central banks if they are lucky have only 12,000 tonnes and much of this gold has been leased out (probably many times over). Eastern nations like China and Russia have been mopping up this gold and storing the yellow stuff on their shores.

(courtesy Egn Von Greyerz/Matterhorn)

The Gold Manipulators Will Be Punished

By Egon von Greyerz

The selling of gold we saw last week was another desperate attack by the BIS and some central banks, together with the bullion banks, to manipulate the gold market lower. We saw over 40% of annual production of gold being sold last week which is 1,000 tons. The physical market continues to be strong which I will discuss further on.

Western Central Banks hold less than 50% of official quantities

Obviously, the sellers had no physical gold to sell so they conveniently dumped all this gold in the paper market. It would have been totally impossible for them to do this trade in the real gold market which is only physical of course. Western Central banks have no physical gold of any quantity to sell. This is why they must fabricate paper gold out of thin air in order to dump it in the market. In total these banks officially have around 23,000 tons of gold. I doubt they even hold half that figure. The rest is likely to have been sold covertly.

No major central bank has had an official audit of their physical gold in modern times. Last time the US gold was audited was in the 1950s. A proper audit would not just reveal that these bank have a lot less gold than they officially declare, but it would also expose the true position of their gold lending or leasing. Most of the gold they have left has been leased to the market in order to depress the price. But this gold no longer stays within the LBMA bullion banks like in the past. No, instead the intelligent buyers of gold today like China, India and Russia take delivery. This means that the leased gold now becomes a paper claim with no chance of getting physical gold back. So what has happened in the physical market in recent years is that central banks have continuously depleted their physical stock by selling and leasing their gold with most of the buying having taken place in the East.

This transfer from West to East is the reason why Western governments and central banks are desperate to keep the gold price down. Official gold is no longer held in “safe” Western hands that are easy to control. Instead the gold has been acquired by nations and people who understand the value of gold. These new gold buyers also know that it is the best protection against the total destruction of paper money that is taking place in our debt infested world. And the countries that are now buying gold are not sellers.

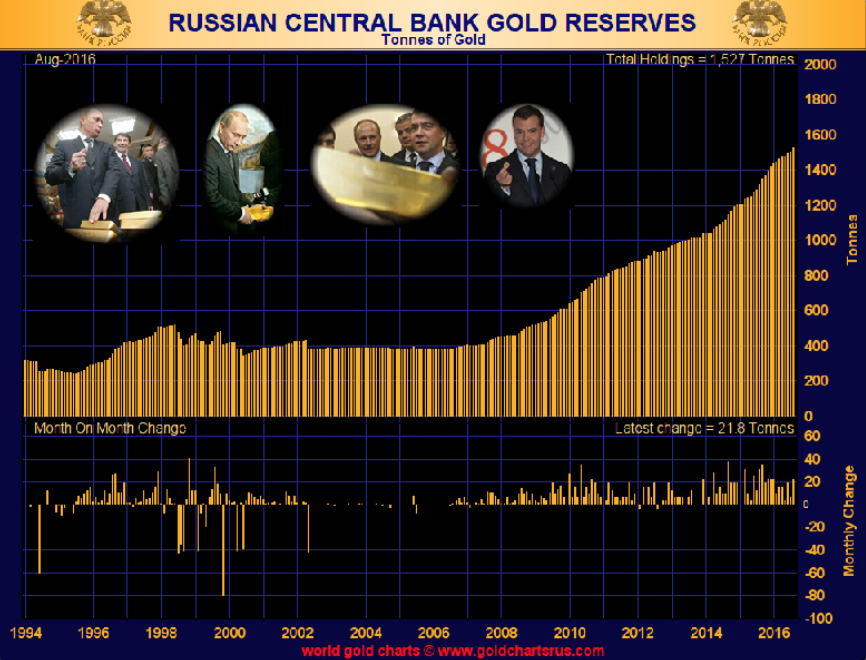

Russia accumulates gold in spite of economic difficulties

The Russian government for example has been expected by the West to sell their gold every time they are under economic pressure. But if we look at the chart below, the picture looks very different. Since 2006, Russia’s gold reserves have gone up almost 4X.

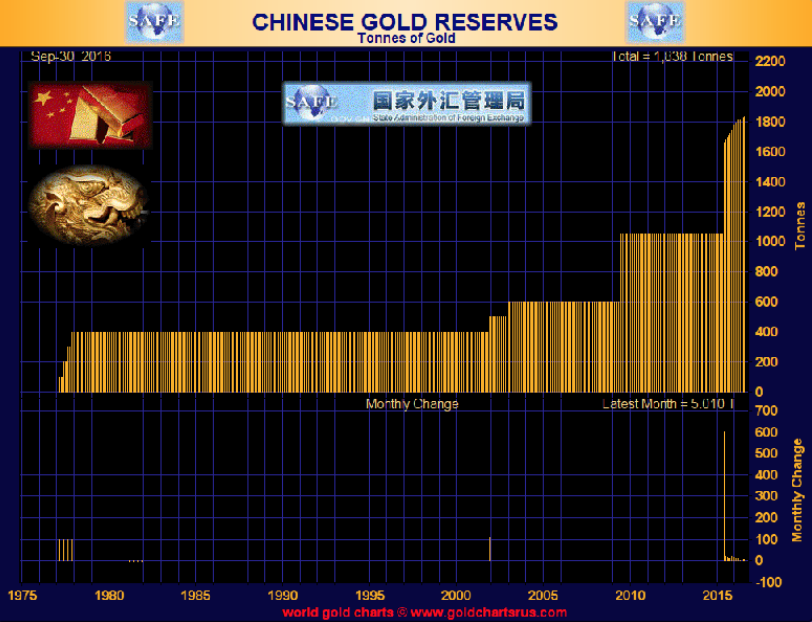

And it is the same in China. Official Chinese holding have increased more than fourfold since 2006 to 1,800 tons.

China has accumulated more gold than any nation in this century

But since China has produced and imported over 11,000 tons of gold since 2009, it is assumed that the official gold holdings are substantially higher than the 1,800 tons reported, maybe as high as 8-12,000 tons which would be higher than the official 8,000 tons that the US holds.

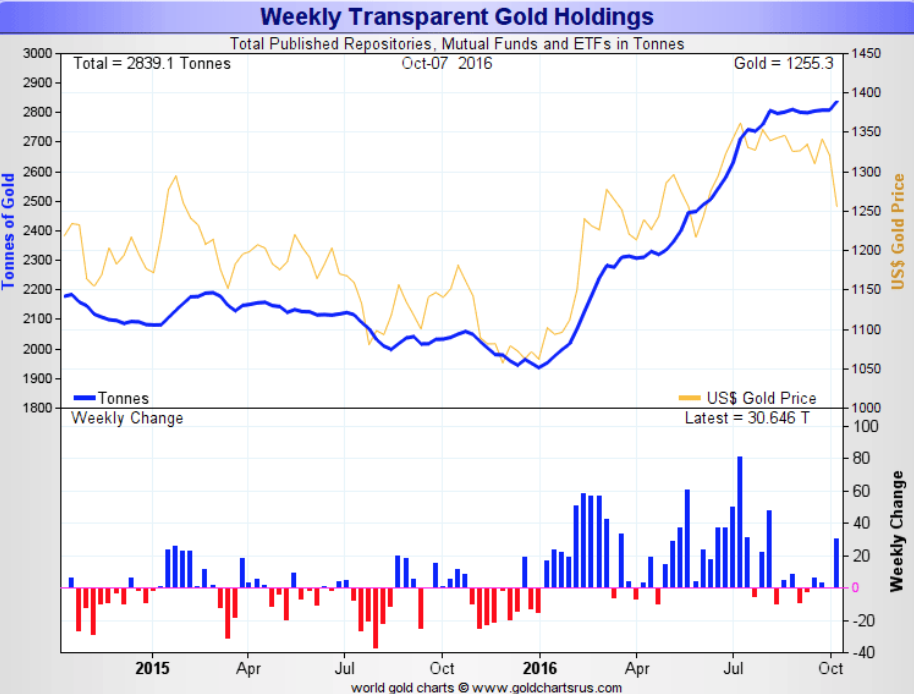

As paper gold is dumped physical gold buying continues

So whilst the West is dumping paper gold, the East is buying physical. And this is exactly what happened last week. Gold fell almost $100 on selling of massive amounts of paper gold. But something very different happened in the physical market. Mutual Funds and ETFs bought over 30 tons of physical gold last week. In total these funds have increased their holdings this year by over 46% or 900 tons to 2,840 tons. As we can see in the chart below, the buying by these funds has been strong all year. When gold corrected by $100 in May, their gold holdings continued to increase.

As some speculative gold buyers are becoming nervous due to another manipulative attack in the paper gold market, the wealth preservationists see this as a real opportunity to add to positions in physical gold.

We are seeing the same thing in our company with continued strong buying from investors who understand that what we have just seen is another desperate attack by the BIS and some central banks together with the bullion banks. When this group dump half a year’s physical gold production in a very short time, they know they temporarily can drive the price down. Banks can of course manufacture unlimited amounts of worthless paper gold and sell it to buyers who don’t understand the massive risk they are taking. But at some point, holders of paper gold will realise that they can’t get rid of it at any price. At that time, the price of physical gold will go up by hundreds of dollars or more in a day.

Thus, last week’s takedown is absolutely nothing to worry about even if we see a bit more pressure. We have seen these manipulations time and time again in this bull market which so far has lasted 16 years and is likely to last at least another 5 years and maybe a lot longer.

Egon von Greyerz

Founder and Managing Partner

Matterhorn Asset Management AG

matterhorn.gold

goldswitzerland.com

end

Actually gold denominated in other currencies is doing quite well.

(Egon Von Greyerz/Kingworldnews)

Gold is actually doing great, von Greyerz tells King World News

Submitted by cpowell on Mon, 2016-10-17 01:02. Section: Daily Dispatches

9p ET Sunday, October 16, 2016

Dear Friend of GATA and Gold:

Gold lately has been doing spectacularly in currencies other than the U.S. dollar, Swiss gold fund manager Egon von Greyerz tells King World News tonight, and in the long term has been doing spectacularly against the dollar too. He thinks the short term is starting to turn against the dollar as well. Von Greyerz’s remarks are posted at KWN here:

http://kingworldnews.com/this-will-shock-world-financial-markets/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A PHD thesis starts the ball rolling on our now famous gold-silver price fixing case.

Yet this is only 1% of the fraud, they will uncover more as the banks collude to fix prices on a daily basis outside of the fix as well

(courtesy Burrell/.Austalian/Syndey/GATA))

PhD thesis stirs up a $1 billion gold-price trial for global banks

Submitted by cpowell on Fri, 2016-10-14 12:32. Section: Daily Dispatches

By Andrew Burrell

The Australian, Sydney

Friday, October 14, 2016

http://www.theaustralian.com.au/business/mining-energy/phd-thesis-stirs-…

PERTH, Australia — An Australian academic’s discovery of global gold price collusion has sparked a looming US trial in which four of the world’s major banks are being sued for up to $1 billion over claims they rigged the price of the precious metal at the expense of investors over a decade.

Perth-based Andrew Caminschi can be revealed as the academic who unwittingly exposed a scandal during a painstaking study of tens of millions of gold transactions that took him 18 months.

“It was needle in the haystack-type stuff,” Associate Professor Caminschi said yesterday of the anomalies he discovered in the data. “But once we found it, it was pretty damning.”

In a key development, a US judge ruled last week that the four banks — Barclays, Bank of Nova Scotia, HSBC and Societe Generale — had a case to answer and that a lawsuit filed by investors would proceed to trial.

Germany’s Deutsche Bank was also accused of manipulation but settled its case in April and has agreed to help the plaintiffs in their claims against the remaining defendants.

Assistant Professor Caminschi, 42, said he would act as an expert consultant at the trial in New York and admitted he was surprised his otherwise obscure PhD thesis at the University of Western Australia — for which he had to build his own server — had damaged the banks and led to a shake-up of the century-old gold pricing system.

“I never thought it would get to this,” he said. “I didn’t go out cartel-busting or bank-bashing — it was more like the data was just yelling at me.”

During his research, the academic discovered apparent manipulation during the twice-daily meetings held by banks in London that determined the benchmark price of gold, which was then used by dealers, central banks and mining companies to trade the precious metal.

The analysis of 14 years of raw data found that during these meetings, and before the benchmark price became known, trading volumes in gold derivatives would rise substantially. This suggested the banks were trading on, and potentially profiting from, information that was not available to the wider market — a theory that had been rumoured for years but never proven.

“I went into my supervisor’s office and I had this heat map and there was a thin white line which runs through the heat map which symbolised areas of very, very intense trading,” Associate Professor Caminschi recalled.

“We were only expecting to see that white line when the news came out, when people would adjust their positions based on the news.

“When I showed it to my supervisor, and after I explained it, he said, ‘Oh shit’.”

The research was first published in an academic journal in 2013.

It was later picked up by industry publications and financial news provider Bloomberg, sparking attention from regulators and leading to scores of lawsuits.

END

This is interesting: Perth Mint tests out the Indian gold excise import tax

(courtesy Garvey/Australian/GATA)

Perth Mint ‘tests out’ Indian gold import excise abuse

Submitted by cpowell on Fri, 2016-10-14 21:10. Section: Daily Dispatches

By Paul Garvey

The Australian, Sydney

Saturday, October 15, 2016

The Perth Mint sent an estimated $1 billion worth of gold to India for refining without the apparent consent of its Australian customers, with the West Australian government-owned refiner being dragged into a court case examining the alleged abuse of an Indian excise rebate scheme.

The Weekend Australian can reveal that the Mint arranged for semi-refined gold — or dore — from its mining customers to be sold to a third party for export into India to “test out” an Indian excise scheme. This is despite the mint having earlier complained to the Indian and Australian governments about the “unfairness” of the excise discount.

India in 2013 introduced a scheme that saw the excise charged on gold dore cut by 2 percentage points compared to the excise charged on the refined pure gold produced by the Perth Mint and other international refiners.

The excise discount drove a surge in gold refining activity in India — the world’s second-biggest market for gold — boosting the prospects of the mint’s refining rivals there and prompting several Australian gold miners to consider exporting their dore directly to India. …

… For the remainder of the report:

http://www.theaustralian.com.au/business/mining-energy/mint-tests-out-in…

END

Obama willing to move China off the currency manipulating list

(courtesy London’s Financial times)

China moves closer to coming off U.S. currency watch list

Submitted by cpowell on Fri, 2016-10-14 21:16. Section: Daily Dispatches

By Shawn Donnan

Financial Times, London

Friday, October 15, 2016

The Obama administration has taken a step toward dropping China from a U.S. currency manipulation watchlist even as Republican candidate Donald Trump promises to declare Beijing a manipulator on Day 1 of his presidency.

Mr. Trump has accused China repeatedly of currency manipulation and using the policy to suck jobs out of the United States. He has vowed to impose punitive tariffs on its imports into the U.S. in a move economists fear could set off a trade war between the world’s two biggest economies.

But the U.S. Treasury said today that by its reckoning China now met just one of the three criteria for inclusion on a currency watch list after its current account surplus fell below 3 percent of gross domestic product in the year to June. Under Treasury’s current guidelines that means that, if nothing changes, Beijing could fall off the watch list as soon as next year.

For their twice-yearly foreign exchange report to Congress Treasury officials also monitor a country’s trade balance with the US as well as any “persistent one-sided intervention” in currency markets. …

… For the remainder of the report:

https://www.ft.com/content/9bb2e3ee-9246-11e6-a72e-b428cb934b78

END

For the first time, the Bank of England ready to tolerate higher inflation

(courtesy London Telegraph/GATA)

Bank of England warns UK’s elected officials that it runs the country

Submitted by cpowell on Fri, 2016-10-14 21:23. Section: Daily Dispatches

Carney: Bank of England Will Tolerate Higher Inflation for the Sake of Growth

By Szu Ping Chan and Tim Wallace

The Telegraph, London

Friday, October 14, 2016

The Bank of England is prepared to tolerate higher inflation over the next few years and will keep interest rates low to support economic growth, according to Governor Mark Carney.

Mr. Carney told an audience in Nottingham that the current environment of low inflation was “going to change” with the drop in the value of the pound likely to push up prices across the economy.

He said food prices were likely to be affected first, signalling that the situation was “going to get difficult” for those on the lowest incomes as the United Kingdom moves “from no inflation to some inflation.”

Speaking later in Birmingham, Mr. Carney defended the bank’s independence, insisting that policymakers would not “take instruction” from politicians on how to do their jobs.

“The objectives are what are set by the politicians, the policies are done by technocrats,” he said. “We are not going to take instruction on our policies from the political side.” …

… For the remainder of the report:

http://www.telegraph.co.uk/business/2016/10/14/carney-bank-of-england-wi…

END

A few questions for Sharps Pixley CEO Ross Norman and other bullion bankers

Submitted by cpowell on Sat, 2016-10-15 18:43. Section: Daily Dispatches

2:50p ET Saturday, October 15, 2016

Dear Friend of GATA and Gold:

Ross Norman, CEO of London bullion dealer Sharps Pixley, yesterday disputed the 2013 study by a professor at the University of Western Australia that concluded that prices in the twice-daily London gold fixings were manipulated, a study publicized this week by the Sydney-based newspaper The Australian:

http://www.gata.org/node/16835

Norman wrote that the study had not discovered market manipulation at all but only that gold trading volume in London increases around the fixings because of the greater liquidity at those times:

http://news.sharpspixley.com/article/london-fixings-the-case-is-laid-bar…

Norman concluded: “It is no surprise that U.S. courts have seized upon the academic report, prompting a flurry of lawsuits to be filed in what is clearly looking like a pre-ordained desire for a guilty verdict in search of evidence to support it.”

Not having seen the study, GATA has no position on it, but Norman’s disparagement of the lawsuits brought against the bullion banks in the London fixes is weak. For of course the plaintiffs would not have sued if they lacked a “pre-ordained desire for a guilty verdict.” Further, every lawsuit in the United States is brought “in search of evidence to support it.” That’s what the discovery and deposition processes in lawsuits are about.

Norman’s response is also weak because according to a filing in one of the lawsuits Deutsche Bank has confessed to manipulating the gold market with other banks and has agreed to supply evidence against them:

http://www.gata.org/node/16380

More details are needed in this regard but Deutsche Bank has a big publicity department —

https://www.db.com/newsroom/en/news.htm

— and thus has had every opportunity to dispute the filing but does not seem to have done so.

But Norman’s response is weakest because he surely knows that the biggest complaints about manipulation of the gold market long have been directed against governments and central banks, which have intimate relationships with the London bullion banks.

How clarifying it might be if Norman, other bullion bankers, and all those who dispute or at least resent complaints of gold market manipulation could answer a few simple questions:

1) Are governments and central banks surreptitiously involved in the gold market, directly or through intermediaries, or not?

2) If governments and central banks are surreptitiously involved in the gold market, is it just for fun — to see whose trading desk can outperform the others — or is it for the traditional policy objectives of government intervention, to protect government currencies and bonds and national stock markets against adverse developments in free markets?

3) Is government subversion of free markets in the public interest? Even if governments should intervene in markets, should that intervention be open and accountable instead of deceptive, or would open and accountable intervention quickly lose effectiveness?

4) Are there any forgeries among the documents of this surreptitious intervention that are compiled here?:

http://www.gata.org/node/14839

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ice will start gold futures trading for clearing at London’s daily auction

(courtesy Bloomberg News/Eddie VanDer Walt)

ICE will start gold futures for clearing London’s daily auction

Submitted by cpowell on Mon, 2016-10-17 01:13. Section: Daily Dispatches

By Eddie Van Der Walt and Ranjeetha Pakiam

Bloomberg News

Sunday, October 16, 2016

Intercontinental Exchange Inc., which runs the daily London gold auction, will start a futures contract for the metal in the United States in February, jumping the gun on the London Metal Exchange, which is also working on a London-focused product.

The contract, subject to regulatory approval, will be for bullion held in London and traded on ICE Futures U.S. in New York. Each contract will be for 100 troy ounces of metal and will be used to clear the London gold auction, starting in March. The London Metal Exchange is scheduled to begin its own futures contracts in the first half of next year. …

… For the remainder of the report:

http://www.bloomberg.com/news/articles/2016-10-17/ice-will-start-gold-fu…

END

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.7378( DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS TO 6.7491 / Shanghai bourse CLOSED DOWN 22.64 POINTS OR 0.74% / HANG SANG CLOSED DOWN 115.77 POINTS OR 0.84%

2 Nikkei closed UP 43.75 OR 0.26% /USA: YEN RISES TO 104.13

3. Europe stocks opened ALL IN THE RED ( /USA dollar index DOWN to 97.99/Euro UP to 1.0991

3b Japan 10 year bond yield: LOWERS TO -.052%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 103.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY.

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.30 and Brent:52.19

3f Gold UP /Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES QUITE A BIT to +078%

3j Greek 10 year bond yield FALLS to : 8.39%

3k Gold at $1254.00/silver $17.46(8:45 am est) SILVER FINAL RESISTANCE AT $18.50 WILL BE DEFENDED

3l USA vs Russian rouble; (Russian rouble UP 8/100 in roubles/dollar) 62.90-

3m oil into the 50 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 104.13 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9892 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0874 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISES to +.078%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 1.792% early this morning. Thirty year rate at 2.550% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Slide, Futures Pressured As Bond Yields Jump To Highest Since June

World stocks started the week in the red Monday as the dollar touched a 7-month high and U.S. and European government bond yields climbed to their highest since June following the Friday speeches by Eric Rosengren and Janet Yellen which hinted the Fed’s next step could be to pursue a steepening of the TSY yield curve the same as the BOJ.

(Harvey; tolerating inflation)

Echoing what we said previously, Ric Spooner, chief market analyst at CMC Markets in Sydney, wrote that “markets are reacting to the possibility that the Fed might join the Bank of Japan in conducting policy to steepen the yield curve. In the Fed’s case, this might amount to running the gauntlet of higher inflation with a very slow pace of monetary tightening.”

According to Reuters, despite the specifics, all the overnight moves came amid signs that inflation is finally starting to wake from its slumber and that top central banks may let inflation “run hot” as Janet Yellen suggested on Friday.

Among the hardest hit treasuries were U.K. gilts, with losses accentuated by the turmoil arising from ongoing concerns about a “Hard Brexit.” As a result, 10-year yields rose to the highest since the Brexit vote, amid speculation the weaker pound is already pushing up prices for consumers. Sterling continued to fall, dropping another 0.2%.

Turkey’s lira and South Korea’s won led emerging-market currencies lower. The Stoxx Europe 600 Index fell for the fourth time in five days and equity gauges declined across most of Asia as oil traded around $50 a barrel.

“We have the two month window where there will be a lot of uncertainty about what the European Central Bank will do, and we had a poor gilt opening this morning and that has spooked the market,” said Mizuho interest rate strategist Antoine Bouvet. “We expected another 20 basis point rise in Bund yields by mid-November.”

Even as the outlook for inflation picks up, central bank policy makers have reiterated commitments to keep stoking prices to spur economic growth. As Bloomberg notes, BOE Governor Mark Carney said last week that he’ll tolerate an inflation-target overshoot, with Yellen echoing that sentiment, saying there are “plausible ways” that running the economy hot for a while could repair some damage caused to growth during the recession. Fed Vice Chair Stanley Fischer is due to speak Monday, while American companies’ earnings are also being watched closely for signs of sustainable growth.

“The Fed, in allowing inflation to run above target, may be changing the game in rates,” said Peter Chatwell, head of rates strategy at Mizuho International Plc in London. “We finally have a fundamental reason for long-term yields to push higher and for inflation premia to re-rate.”

In addition to the broad global selling in rates instruments, attention turned to China’s ongoing and unexpected devaluation of the Yuan, where the USD/CNH rose above the psychological level of 6.75 before dipping back to 6.7486 as the PBOC appears to no longer care about setting a ceiling. As we showed previously, concerns about the currency and a pick up in capital outflows may have been responsible for the dramatic plunge in China B-Shares, which crashed by nearly 7% in the last 90 minutes of trading.

But the underlying catalyst was a return to concerns about global VaR shocks rising from the sharp move in the long end of the curve as we warned last night. The yield on 30-year Treasuries rose to 2.57% in early trading, set for the highest close since June 2, and following an eight basis-point jump on Friday. The two-year note yield was little changed for a second day after futures prices indicated the chance of a Fed rate hike in 2016 held steady at 66% in the last session. Gilt yields have been climbing for the past three weeks as sterling’s 18 percent slide since the vote to leave the EU drove a market gauge of inflation expectations to the highest in 2 1/2 years. Faster inflation erodes the fixed payments on bonds, while also making it less likely the BOE will be able to cut interest rates and extend its asset purchases. The yield on the benchmark 10-year security jumped eight basis points to 1.17 percent, after touching 1.22 percent, the highest since the June 23 referendum. The yield on Germany’s 10-year bonds increased by three basis points to 0.09 percent, while that on similar-maturity notes in Australia rose by four basis points to 2.31 percent.

Looking at stocks, Europe’s Stoxx 600 slid 0.7% in early trading with energy producers falling the most as oil slipped. The equity benchmark ended last week little changed as investors weighed central bank policy and the health of the global economy following mixed data from China. Pearson Plc tumbled 9.6% as the world’s largest education company reported a sales decline. S&P 500 Index futures retreated 0.3 percent, after U.S. equities ended Friday little changed following a late-afternoon selloff. The MSCI Asia Pacific excluding Japan Index slipped 0.6 percent and the MSCI Emerging Markets Index also fell 0.6 percent. The Hang Seng China Enterprises Index of mainland companies listed in Hong Kong declined 0.6 percent. A report due Wednesday may show China’s economy grew 6.7 percent in China the third quarter, the same as in the previous two periods, according to a Bloomberg survey of economists. Crown Resorts tumbled 14% in Sydney after Chinese authorities detained 18 of its employees, including the head of its international high-roller operations. Gaming stocks elsewhere were also hurt, with Sands China Ltd. and Galaxy Entertainment Group Ltd. both dropping at least 3 percent in Hong Kong.

Investors will look to data Monday for further indications of the health of the world’s biggest economy in light of Yellen’s comments on inflation. Among reports scheduled for release, industrial production is forecast to have increased in September after August’s contraction.

The earnings season is also in focus, with Charles Schwab Corp., International Business Machines Corp. and Bank of America Corp. among the main companies posting quarterly results on Monday. Analysts forecast a 1.4 percent contraction in third-quarter profits for S&P 500 members.

Bulletin Headline Summary from RanSquawk

- Heavy selling pressure in fixed income markets this with Bunds breaking below 163.00 while Gilts continue to underperform as participants become less bullish on expectations for further BoE easing

- A quiet morning in the FX markets, but there are plenty of data/event risks through the week to keep players on the side lines until we get some clearer signals to trade off.

- Looking ahead, highlights include US Empire State Manufacturing Index, US Industrial and Manufacturing Production

Market Snapshot

- S&P 500 futures down 0.3% to 2121

- Stoxx 600 down 0.7% to 338

- FTSE 100 down 0.8% to 6959

- DAX down 0.7% to 10506

- German 10Yr yield up 3bps to 0.09%

- Italian 10Yr yield up 6bps to 1.44%

- Spanish 10Yr yield up 3bps to 1.15%

- S&P GSCI Index down less than 0.1% to 375.4

- MSCI Asia Pacific down 0.1% to 138

- Nikkei 225 up 0.3% to 16900

- Hang Seng down 0.8% to 23038

- Shanghai Composite down 0.7% to 3041

- S&P/ASX 200 down 0.8% to 5389

- US 10-yr yield up less than 1bp to 1.8%

- Dollar Index down 0.08% to 97.94

- WTI Crude futures down 0.3% to $50.20

- Brent Futures down 0.1% to $51.89

- Gold spot up 0.1% to $1,253

- Silver spot down 0.2% to $17.39

Global Top News

- Deutsche Bank Said to Explore Shrinking U.S. Operations: Such an option being considered as part of bank’s broader strategy review, evaluating businesses in context of regulatory, capital requirements.

- Ohio Joins California, Illinois in Suspending Wells Fargo: Gov. John Kasich barring WFC from state bond deals, contracts for a year; WFC’s New CEO Sloan Leaves Analysts Unsatisfied in Debut

- Dynegy Unit Creditors Agree on $825m Debt Restructure: Bondholders to exchange 2018, 2020, 2032 notes for $139m in cash, $210m in new 7-year Dynegy notes.

- Mortgage Insurers’ Pilot Program Draws Investor Scrutiny: Money managers raised concerns about Fannie Mae, Freddie Mac pilot programs to share more risk with the guarantors; are pressing trade groups to lobby against parts of plans.

- Over 1 Million to Lose Obamacare Plans as Insurers Quit: At least 1.4m people in 32 states will lose Obamacare plan they have now: state officials.

- ‘Accountant’ Topples ‘Girl on the Train’ at Box Office: Drama collected an estimated $24.7m at theaters in U.S., Canada: ComScore.

- LendingClub Increases Interest Rates for Riskiest Borrowers: Co. lifted interest rates by weighted average 26 basis points, primarily for riskier transactions.

- Apple Seeking Newer Screens to Make or Break Japan Suppliers: Co. plans to adopt OLED screen technology for next major upgrade to its flagship product.

- Tesla Deepens Panasonic Ties With Solar Parts Deal: PV cell, module production for solar energy systems used by SolarCity will begin in 2017 at factory in Buffalo; Musk Moves Tesla Announcement to Weds.; Needs ‘Refinement’: Tesla CEO Elon Musk comments on Twitter.

- Lululemon 3Q Comp. Sales View Cut at Goldman Amid Competition: Est. lowered to 3% from 4.5%; now below co. forecast of mid-single digits: Goldman.

- Medtronic Recalls Some Lots of Embolization, Retrieval Devices: 84,278 units potentially affected by it had been distributed worldwide.

- GameStop to Sell Out of PlayStation VR Goggles: COO: Co. has asked Sony to supply more of the headsets.

- Nevada Approves Record $750m Subsidy for NFL Stadium: Lawmakers authorized a tax incentive to entice NFL’s Oakland Raiders to move to Las Vegas.

- McDonald’s Executives King, Hess Said to Leave Co.: WSJ: Chief field officer, also senior VP for customer experience are planning to retire this year: WSJ.

- Trump Says Polling-Place Cheating Leading to ‘Rigged’ Election: “They leave dead people on the rolls, and then they pay people to vote those dead people four, five, six, seven, eight, nine times:” Trump surrogate Rudolph Giuliani.

- PayPal May Have Mulled Buying GoFundMe: TechCrunch: Price potentially above $1b.

Looking at regional markets, we start as usual in Asia, where stock markets began the week subdued following last Friday’s flat close on Wall St. and quiet news flow over the weekend. ASX 200 (-0.8%) was led lower by the consumer discretionary sector after 18 Crown Resorts employees were detained in China regarding the promotion of gambling on the mainland. Nikkei 225 (+0.3%) swung between gains and losses alongside choppy JPY movements in which USD/JPY fluctuated around 104.00. Chinese markets were mixed as the Hang Seng (-0.8%) conformed to the negative tone seen across Asia, while Shanghai Comp. (-0.7%) fluctuated between gains and losses with the PBoC upping its liquidity injections to the interbank market. 10yr JGBs saw muted trade with price action hampered by quiet news flow and with participants side-lined ahead of tomorrow’s enhanced liquidity auction for the long to super long end. China is to provide more policy support to boost the growth of the service sector, according to the cabinet.

PBOC injected CNY 50bIn in 7-day reverse repos and CNY 20bIn in 14-day reverse repos. The central banks set the Yuan mid-point at 6.7379 (Prey. 6.7157), the lowest in 6 years.

Top Asian News

- China’s Currency Dilemma Deepens as Yuan Surges Versus Euro, Won: Allowing faster depreciation versus dollar could spur outflows.

- Hedge Funds Cut Bullish Yen Bets Amid Currency’s Three-Week Drop: Dollar gains set to accelerate versus euro, yen year- end, RBS says.

- Thai Bonds Suffer Record Outflows as King’s Death Sparks Concern: Selling is overdone, according to ING’s Tim Condon.

- Crown Resorts Plunges After China Detains 18 Casino Employees: Detentions spark concern of clampdown on overseas marketing.

- JR Kyushu Sets IPO Price at 2,600 Yen/Share, Top of Range: Co.’s share offering would be worth 416b yen, according to Bloomberg calculation.

- KKR-Backed Cofco Meat Seeks Up to $333m in Hong Kong IPO: Chinese pork producer offers shares at HK$2 to HK$2.65 apiece.

In Europe, heavy selling pressure in fixed income markets this with Bunds breaking below 163.00 while Gilts continue to underperform as participants become less bullish on expectations for further BoE easing. More specifically, participants have continued to scale back expectations of further easing by the BoE as the softer GBP has continued to heighten the possibility of a firmer uptick in inflation than initially thought when the BoE acted in August (Goldman Sachs pushed back BoE easing to Feb’17 from Nov’16). Alongside this, Bunds have seen a couple of key levels breached this morning with the yield breaking back above 0.10% reaching levels last seen since the UK referendum, while USTs also remain softer as participants further price in expectations of a 25bps cut by the Fed in their Dec meeting, albeit with a potentially shallower path ahead as shown by comments from Fed chair Yellen on Friday. Price action in equities have been somewhat contained this morning with the Eurostoxx 50% (-0.3%) modestly in

the red, however EU bourses have marginally pared their opening losses amid broad based gains across financial names with reports suggesting that Deutsche Bank (+0.3%) could be considering an exit from their US operations. Elsewhere, energy names underperform in the wake of the losses seen on Friday despite prices being relatively stable this AM.

Top European News

- Draghi Seen Embracing More Before Less QE as Inflation Edges Up: With consumer prices barely rising, recovery still fragile, majority of Bloomberg survey respondents predict that ECB president will prolong bond-buying.

- Coty Said to Be Near >GBP400m Purchase of U.K.’s GHD: Sky: Deal for hair-care products co. may be announced as soon as this month: Sky.

- Sonnen Considering IPO in Bid to Rival Tesla Powerwall Storage: German solar-energy-storage maker may pursue IPO as early as 2017 to develop additional services.

- U.K. Falls Out of Top 5 Investment Sites Post Brexit: EY: British businesses rank behind investments in U.S., China, Germany, Canada, France; London Becoming U.K.’s Housing Market Laggard: London asking prices +2.5% in past year, second-weakest performance out of 9 areas surveyed by Rightmove.

- U.S. Banks Slashed Share of U.K. Property Loans Before Brexit: U.S., Canadian banks’ market share fell to 7% vs 14% in 1H 2016: survey of 78 lenders by De Montfort University

In FX, the MSCI Emerging Markets Currency Index fell 0.3 percent, headed for its lowest close since Sept. 16. The lira weakened for a second day, dropping 0.5 percent. The won weakened 0.4 percent, while Malaysia’s ringgit retreated 0.3 percent. The yen advanced 0.1 percent to 104.03 per dollar, following declines in each of the last three weeks. Hedge funds and other large speculators cut bullish bets on the currency by the most since May in the week ended Oct. 11. Australia’s dollar slipped 0.3 percent. The yuan fell to a six-year low in Shanghai, while Taiwan’s dollar dropped to levels last seen in August.

In commodities, oil extended declines after U.S. producers ramped up drilling even as crude inventories remained at the highest seasonal level in at least three decades. Futures fell 0.3 percent to $50.19 a barrel. Aluminum dropped 1.4 percent as an Indonesian producer group said it will ask the government to lift a bauxite export ban imposed in 2014, threatening to increase supply of the raw material. Nickel slipped as much as 0.7 percent. Copper rose as much as 0.6 percent after the biggest two-week decline in four months. Gold advanced after posting a three-week slide as investors weighed the outlook for U.S. interest rates against signs of robust demand. Bullion for immediate delivery climbed 0.2 percent to $1,253.62 an ounce.

On today’s calendar, we’ll get the September industrial and manufacturing reports along with capacity utilization data and the Empire manufacturing report for October.

* * *

US Event Calendar

• 8:30am: Empire State Mfg, Oct., est. 1.00 (prior -1.99)

• 9:15am: Industrial Production, Sept., est. 0.2% (prior -0.4%)

• 12:15pm: Fed’s Fischer speaks in New York

• 5:10pm: Reserve Bank of Australia’s Lowe speaks in Sydney

• U.S. Rates Weekly Agenda

• FX Weekly Agenda

DB’s Jim Reid concludes the overnight wrap

It’s a varied week of highlights ahead over the next 5 days to grab our attentions. The main events being UK and US inflation and ECB lending standards tomorrow, China’s monthly main data dump and the final US presidential TV debate on Wednesday, the ECB meeting on Thursday and earnings season getting into full swing (96 US and 40 European companies) through the week. A key macro theme at the moment is potential central bank tapering/tightening what with the Fed itching to hike, the BoJ potentially tapering until the government picks up the baton and vague speculation about the ECB wanting to rein in QE. DB’s Mark Wall still expects a 9-12 month extension in December but if the ECB is thinking differently we may get some hints on Thursday. If they do extend then they need to solve the eligibility conundrum soon so that’s another thing to look out for at the meeting.

Given that the market is sensing a slight shift in emphasis from central banks, the focus on the bond market continues with UK Gilts leading the sell-off during the European session on Friday (more below) with US Treasuries adding to the losses after Yellen spoke on Friday night. The key theme seemed to be her wondering whether there was room to let the US economy ‘run hot’ and whether such a ‘high pressure’ economy could enhance things like labour force participation. While this could be potentially dovish for the front end, the perception was that it could allow inflation to be allowed to run higher which helped the long-end sell-off and steepened the curve. The Boston Fed’s Rosengren (a dissenter last month) also spoke and said that the market is pricing in an ‘appropriately’ high probability of a Fed rate hike in December however it was Yellen’s comments which got Treasuries moving. Indeed 2y yields finished the session flat at 0.835% however 5y, 10y and 30y yields were up 2.8bps, 5.7bps and 8.1bps respectively by the end of play. The 5.5bp move in the 5y 30y spread was in fact the most since March 30th and takes the spread to just below the highs of midway through last month.

In terms of Gilts there was a similar bear steepening effect across the curve on Friday. 2y yields edged less than 1bp higher however 10y and 30y yields were up 7.2bps and 6.0bps to 1.094% and 1.762% respectively. Comments from BoE Governor Carney seemed to be at the forefront of the selloff when he suggested that the Bank will ‘tolerate a bit of overshoot in inflation over the course of the next few years’ in order to cushion the blow of an anticipated increase in unemployment. Carney also added that ‘our job is not to target the exchange rate, our job is to target inflation’ but ‘that doesn’t mean we’re indifferent to the level of sterling’ however ‘it does matter ultimately to where inflation is and over the course of two or three years out, it matters to the conduct of monetary policy’. BoE MPC member Forbes added separately on Friday that the BoE might overshoot its inflation target ‘sharply’ over the next couple of years and that the days of ‘inflation bouncing around zero are gone’. Sterling fell -0.51% on Friday versus the Dollar and is down another -0.19% this morning at $1.2168. The five-day loss of -1.95% last week means Sterling has now weakened in five of the last six weeks.

Meanwhile, as we noted earlier, this week will see earnings season start to ramp up, particularly across the pond. The Banks sector will again be under the spotlight with BofA (today), Goldman Sachs (Tuesday) and Morgan Stanley (Wednesday) due. That comes after some better than expected earnings and revenue numbers from Citi, JP Morgan and Wells Fargo on Friday where decent beats in fixed income trading revenue appeared to be a big driver and consistent theme at both Citi and JPM in particular. DB’s US equity strategist David Bianco expects most companies to beat the last minute estimates this quarter but beats to be smaller than usual and Q4’16 and 2017 EPS outlooks to be tempered. He’s forecasting the S&P 500 EPS to be flat year-on-year and up 2% quarter-on-quarter (or 3% ex-energy).

Those banks earnings had initially seen US equity markets get off to a decent start on Friday with Europe (Stoxx 600 +1.29%) also finishing on a strong note for much the same reason. However as Europe closed markets in the US faded with the S&P 500 (+0.02%) eventually finishing little changed as rates spiked higher and the Dollar strengthened which weighed on utilities and REITS in particular.

As we look at our screens this morning it’s a bit of a mixed start to the week in Asia. The Nikkei (+0.29%) and Kospi (+0.47%) are currently posting modest gains however the Hang Seng (-0.42%) and ASX (-0.68%) have dipped lower. Bourses in China are generally flat although its been a fairly directionless start with indices trading between gains and losses. Sovereign bond markets are generally weaker in the region. Longer dated JGB yields are a couple of basis points higher while benchmark 10y yields in the likes of Australia, New Zealand and Korea are 5-7bps higher.

In terms of the weekend newsflow there’s some focus on Italy with the news that Banco Popolare and Banca Popolare di Milano shareholders’ have approved Italy’s biggest bank merger in nearly a decade. The tie-up will create a €171bn asset lender according to the FT and should provide a boost for PM Renzi who made a push for the deal. Away from this, the latest Brexit news is that a group of legislators including former Lib Dem PM Nick Clegg and former Labour Leader Ed Miliband have demanded PM May’s government to publish a ‘substantive outline’ of its Brexit plans and submit to a vote in Parliament prior to triggering Article 50. This of course follows that Parliament session which had Labour calling for a ‘proper scrutiny’ of PM May’s strategy last week.

Before we look at the week ahead, just a quick recap on the rest of the newsflow on Friday. In terms of the US data, retail sales were a bit mixed with the headline (+0.6% mom) and core ex auto and gas (+0.3% mom) in line with the market consensus, but the GDP input control group component (+0.1% mom vs. +0.4% expected) missing which led to the Atlanta Fed cutting its Q3 GDP forecast to 1.9% from 2.1%. As a reminder this forecast was as high as 3.8% in early August. Meanwhile, headline PPI (+0.3% mom vs. +0.2% expected) was a little higher than expected, while the core ex food, energy and trade (+0.3% mom vs. +0.1% expected) also rose more than expected. A first look at the October University of Michigan consumer sentiment survey was mixed. The sentiment reading dipped 3.3pts to 87.9 (vs. 91.8 expected) and while the current conditions component rose 1.3pts to 105.5, the expectations component was down 6.1pts to 76.6 and the lowest since September 2014. We’d imagine that the upcoming President election is weighing on the latter in particular.

Elsewhere, business inventories (+0.2% mom vs. +0.1% expected) printed a little higher than expected and the September Monthly Budget statement revealed a $33.4bn surplus. There was nothing of particular note released in Europe.

Turning over to this week’s calendar now. This morning in Europe the only notable data due out is the final revision to September CPI in the Euro area. Over in the US this afternoon we’ll get the September industrial and manufacturing reports along with capacity utilization data and the Empire manufacturing report for October. Tuesday morning should be an interesting session in Europe with the ECB bank lending survey due out along with the UK CPI/RPI/PPI data in September. Over in the US we’ll also get the September CPI report too, along with the October NAHB housing market index print. Wednesday is all about China with the September data dump released in the morning which includes Q3 GDP, industrial production, retail sales and fixed asset investment. Away from that there’s more data due in the UK in the form of the August and September employment data, while in the US we’ll get the September housing starts and building permits numbers, along with the Fed’s Beige Book in the evening. In Europe on Thursday the data includes Germany PPI and UK retail sales. That’s before we get the ECB policy meeting outcome shortly after midday. Over in the US on Thursday the data releases include initial jobless claims, Philly Fed manufacturing survey, existing home sales and Conference Board’s leading index. We end the week in China on Friday with the latest property prices data and MNI business indicator reading. In the UK there’s more data, this time the latest public sector net borrowing reading, while the Euro area consumer confidence print is due in the afternoon. There’s no data due in the US on Friday.

Away from the data the Fedspeak this week includes Fischer this evening, Williams and Kaplan on Wednesday, Dudley on Thursday and finally Tarullo and Williams on Friday. Of course the third and final Presidential Debate on Wednesday evening in Las Vegas will be closely watched. In the UK Chancellor Hammond is due to testify before the Treasury Committee on Wednesday. The ECB’s Draghi holds his usual post-ECB meeting press conference on Thursday too. The other big focus for markets this week is of course earnings. 96 S&P 500 companies are set to report including BofA, Netflix and IBM today, Goldman Sachs, Johnson & Johnson and Intel on Tuesday, eBay and Morgan Stanley on Wednesday, American Airlines, Verizon, Microsoft, Walgreens Boots and Schlumberger on Thursday and McDonald’s and GE on Friday. We’ll also get earnings from 40 Stoxx 600 companies this week.

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late SUNDAY night/MONDAY morning: Shanghai closed DOWN 22.64 POINTS OR 0.74%/ /Hang Sang closed DOWN 195.77 POINTS OR 0.84%. The Nikkei closed UP 43.75POINTS OR 0.26% Australia’s all ordinaires CLOSED DOWN 0.83% /Chinese yuan (ONSHORE) closed DOWN at 6.7378/Oil FELL to 50.30 dollars per barrel for WTI and 52.19 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.7491 yuan to the dollar vs 6.7260 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AS MORE USA DOLLARS LEAVE CHINA’S SHORES

3a)THAILAND/SOUTH KOREA/SOUTHEAST ASIA:

b) REPORT ON JAPAN

none today

c) Report on CHINA

Last night 3 biggies:

i) rising inflation which would stop the POBC from monetary easing

ii) a jump in the dollar (fall in CNH/CNY) which again causes inflation risks

iii)Shanghai B share index crashes over 6% in last 90 minutes of trading

(courtesy zero hedge)

Shanghai B-Shares Unexpectedly Crash Over 6% In Last 90 Minutes Of Trading

In recent days, China has been hit with a triple whammy of rising inflation, reducing the likelihood of more monetary easing; a jump in the dollar which has pressured the Yuan sending it to its lowest fixing since 2010 at 6.7379, while the USDCNH rising above 6.75 in early trading; and rising interest rates which have resulted in another spike in revulsion to EM stocks. Perhaps as a result of this perfect storm of catalysts, overnight China’s foreign currency shares, the Shanghai B-share index, plunged the most since January in late trading, and as Bloomberg notes, “sending traders scrambling for reasons to explain the sudden volatility in a largely moribund market.”

The Shanghai B-share index of dollar-denominated stocks suddenly crashed as much as 6.7%, the biggest drop since January 11, with virtually all the losses coming in the last 90 minutes of trading, before closing down 6.2%.

Kama Co. and Shanghai Lingyun Industries Development Co. were among companies falling by the 10% limit. Predictably, a measure of the 10-day volatility on the 52-member index jumped to its highest level in six months, after falling in September to its lowest in at least a decade.

As Bloomberg summarizes, B-share markets, where foreign institutions and Chinese individuals are allowed to trade, were set up in 1992 to give local companies a way to raise funds from global investors banned from buying securities denominated in yuan. Interest in B shares has waned as the government allowed qualified overseas investors to access the larger, more liquid A-share market and eased limits on foreign exchange. Monday’s drop came as the yuan extended a slide against the dollar to a six-year low.

“There’s no clear explanation on the sudden drop,” said Castor Pang, head of research at Core-Pacific Yamaichi Hong Kong. “But most investors are deeply concerned about the yuan’s depreciation and capital outflows as the yuan approaches 6.8. Overall market sentiment is very poor and selling in the B-shares index is spreading.” But we thought China was fixed, or at least that’s what the “objective” media said?

Turns out the media was wrong as usual: Northeast Securities strategist Shen Zhengyang also blamed the Yuan exchange rate is one major factor for movement in B shares, adding that investors are worried yuan might depreciate further against the USD after recent weakness. It appears China’s capital outflows are also nowhere near done, refuting yet another optimistic media fable.

Investors are “probably selling dollar-denominated B shares and want to get the money out if they still have forex quota” he added.

Then there is the fact that the plunge was long overdue: the Shanghai-B market is a bubble, which trades 30x reported earnings, almost double the 18 multiple for the Shanghai Composite Index. The Shanghai Composite, comprising both yuan-denominated A and foreign-currency B shares, slid 0.7 percent, erasing an earlier 0.2 percent advance. The selloff comes amid a period of stability for Chinese equities after last year’s $5 trillion rout, with turnover on the Shanghai exchange near two-year lows and the benchmark gauge treading water. That said, the only reason for the stability is that as retail investors have fled the local stock market, the government has effectively taken over and no longer allows material swings in underlying risk.

But ultimately, today’s crash is likely a confirmation that Chinese capital outflows continue.

Mainland investors have been looking at ways to protect against a weakening yuan, with net buying of Hong Kong stocks via a Shanghai link swelling to a record last month. The Chinese currency slid 0.2 percent to 6.74 per dollar at 3:49 p.m., after sinking 0.8 percent last week.

“There is market speculation that B shares can no longer be used as a tool to hedge against the yuan,” said Jackson Wong, associate director at Huarong International Securities Ltd. in Hong Kong. The State Administration of Taxation last week published rules requiring banks to perform due diligence on non-resident financial accounts from 2017.

“We saw some unknown institutions’ heavy selling around 2 p.m.,” said William Wong, Hong Kong-based head of sales trading at Shenwan Hongyuan Securities Ltd. “It is very likely that some overseas investors want to move money out” after the new rules.

One thing is certain: if this capital outflow pathway is closing, Chinese intrepid residents will just find another way to transfer more of theit $25 trillion in domestic savings abroad.

end

4 EUROPEAN AFFAIRS

none today

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

SAUDI ARABIA

Rising Sibor rates causes Saudi bank stocks to tumble as its bailout of the economy fails to stem liquidity problems:

(courtesy zero hedge)

Saudi Bank Stocks Tumble As Bailout Fails To Stem Liquidity Stress

Saudi bank stocks’ dead-cat-bounce – following the central bank’s cash injection ‘bailout – is dying once again as Bloomberg reports funding pressures remain in The Kingdom’s financial system.

The interest rate banks charge one another for loans rose by the most since August on Sunday, extending a trend that’s slowing earnings and corporate borrowing in the world’s biggest oil exporter. The increase is defying the central bank, which has sought to ease the cash crunch by relaxing lending limits, offering new borrowing facilities and injecting funds into the financial system, including 20 billion riyals ($5.3 billion) pledged Sept. 25.

Financial institutions in the Arab world’s largest economy are bearing the brunt of a halving of oil prices since 2014. Economic growth in the kingdom is slowing, curtailing bank deposits just as the government increases borrowing to help plug a budget deficit that last year was the widest since 1991.

“Rates won’t easily come down with one $5 billion injection,” said John Sfakianakis, director of economic research at the Gulf Research Center Foundation in Riyadh.

“Bringing them down would require a significant liquidity injection effort. The $5 billion is a good step forward, but given the asset size of Saudi banks it would require several additional injections.”

And it appears investors are rapidly realizing that (as the market demands more)…

Saudi Arabia will post a budget deficit of 13.5 percent of economic output this year, the highest since 1992, declining to 9.6 percent in 2017, according to forecasts from the International Monetary Fund. Amid the shortfall, direct local government debt climbed to $63 billion at the end of August from almost $38 billion at the end of 2015, according to information in the Saudi bond prospectus obtained by Bloomberg.

Rising Saibor rates reflect the “extent of the liquidity challenge in the banking system,” said Raza Agha, the London-based chief economist for the Middle East and Africa at VTB Capital Plc. “The outlook for government borrowing has risen sharply and even if next year’s deficit declines to perhaps 8 percent of gross domestic product, you’re still looking at deficit-financing needs of $56 billion.”

END

RUSSIA VS USA

Putin describes that it is Hillary that is banging the war drums. He is very concerned that the world is rushing irreversibly towards a nuclear showdown

(courtesy zero hedge)

Hillary’s ‘War Drums’ Confirm Putin’s Fears Of A World “Rushing Irreversibly” Towards Nuclear Showdown

As election day looms in America, it appears the writing that Vladimir Putin drew on the wall just a few short months ago is coming to fruition. Having lost his patience with the constant spewing of anti-Russia propaganda – missing the bigger picture of vicious circle towards muclear confrontation – Putin implored the western media, for the sake of the world, to listen:

We know year by year what’s going to happen, and they know that we know. It’s only you that they tell tall tales to, and you buy it, and spread it to the citizens of your countries. You people in turn do not feel a sense of the impending danger – this is what worries me. How do you not understand that the world is being pulled in an irreversible direction? While they pretend that nothing is going on. I don’t know how to get through to you anymore.

In calm tones, not reflective of the angry allegations lobbed at Americans every day of a Russia hell-bent on the election of Trump (for whatever reason they dreamed up of this week), Putin reminded a ‘deaf’ press corps of what lies ahead and implicitly what happens if and when Americans vote for Hillary.

And, as Lawrence Murray (via Atlantic Centurion) explains why Donald Trump is the anti-war candidate…

From the Jordan to the Moskva, war drums beat. The powder keg that set off the first world war was ethno-religious conflict in the lands of the former Ottoman Empire, and in a sense it threatens to do so once more. The Balkan nations were not impressed with the botched settling of the Eastern Question, and a mix of state and non-state actors took matters into their own hands, leading to a globalized conflict. As late as 2006, the borders of the region were still being contested, when Montenegro voted to break away from Serbia.

Today, millions of people in the Levant, especially in Syria and Iraq, reject the imposed settlement of their borders. These were drawn by imperialists and zionists nearly a century ago under the Sykes-Picot Agreement to serve the interests of Britain, France, and the overseas Israeli community—and the successors of those diplomats wish to maintain those same borders. The ethno-religious conflict I am referring to in the former Ottoman Empire is of course the:

- Syrian civil war

- Iraqi civil war

- Turkish-Kurdish conflict

- American intervention in Iraq

- American intervention in Syria

- Iranian intervention in Iraq

- Iranian intervention in Syria

- Russian intervention in Syria

- Hezbollah campaign in Syria

- Yemeni civil war

- Libyan civil war

- NATO intervention in Libya

- Egyptian counter-insurgency

- War on Terror / global Islamic jihad

- US-Russian Middle Eastern proxy war

- Arab-Israeli conflict

Oh. Too many? This is the scope of conflicts that the Leviathan on the Potomac has gotten itself into, and just in the former Ottoman Empire. This does not include the:

- South China Sea territorial dispute

- Korean civil war

- War in Afghanistan

- Russian-Ukrainian border war

- Combat support in various African countries

- Occupation of Germany

In November, Americans will roll to the polls on their motorized scooters to elect the next Commander-in-Chief of the Armed Forces of the United States.