Gold at (1:30 am est) $1190.60 UP $12.40

silver at $16.58: UP 12 cents

Access market prices:

Gold: 1293.75

Silver: 16.61

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

MONDAY gold fix Shanghai

Shanghai morning fix Nov 28 (10:15 pm est last night): $ 1221.43

NY ACCESS PRICE: $1192.80 (AT THE EXACT SAME TIME)/premium $28.63

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1218.64

NY ACCESS PRICE: 1192.20 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $26.44

China rejects NY pricing of gold as a fraud

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Nov 28: 5:30 am est: $1189.10 (NY: same time: $1189.50 5:30AM)

London Second fix Nov 28: 10 am est: $1187.00 (NY same time: $1187.20 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR NOVEMBER CONTRACT MONTH: 2 NOTICE(S) FOR 200 OZ TONNES

For silver:

NOTICES FOR NOVEMBER CONTRACT MONTH FOR SILVER: 1 NOTICE(s) OR 5,000 OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1409 contracts DOWN to 166,174 with YESTERDAY’S trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .831 BILLION TO BE EXACT or 119% of annual global silver production (ex Russia & ex China).

In November, in silver, 1 notice(s) filings: FOR 5,000 OZ

In gold, the total comex gold FELL by 7,799 contracts WITH THE HUGE FALL IN THE PRICE OF GOLD ($10.90 with FRIDAY’S trading ).The total gold OI stands at 415,587 contracts. The gold specs have been blown out of the water again

In gold: we had 2 notice(s) filed for 200 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD: (to be reported on Sat/Sun)

We had no changes in tonnes of gold at the GLD,

Inventory rests tonight: 885.04 tonnes

.

SLV

we HAD NO CHANGES at the SLV/

THE SLV Inventory rests at: 346.150 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver FELL by 1,409 contracts DOWN to 166,174 as price of silver FELL by $0.8 with FRIDAY’S trading. The gold open interest FELL by 7799 contracts DOWN to 415,587 as the price of gold FELL BY $10.90 WITH FRIDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

2d) FRBNY foreign gold movement

(Harvey)

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 15.06 POINTS OR 0.46%/ /Hang Sang closed UP 107.12 OR 0.47%. The Nikkei closed DOWN 24.33 OR .13%/Australia’s all ordinaires CLOSED DOWN 0.68% /Chinese yuan (ONSHORE) closed UP at 6.912/Oil ROSE to 46.33 dollars per barrel for WTI and 47.66 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.9360 yuan to the dollar vs 6.9120 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

This is the market’s next big headache: China is raising interest rates on its short and long term bonds and this is being accomplished with lower growth in their model:

(courtesy zero hedge)

4 EUROPEAN AFFAIRS

ITALY

i)I have been detailing to you the major problem affecting Italy and that is their insolvent banks, namely their non performing loans which is 18% of total loans or totaling 360 billion euros. If a bail in is ordered and we now have the new EU rules, then the Italian general public will be burned alive as they are the dominant holders of Italian debt. If Renzi leaves and a not vote, then a private bailout will not be done and Italy will face their doom@@@!

( zero hedge)

ii)It will be THE REPUBLICAN Fillon up against ULTRA RIGHT Marine LePen with a possibility of a socialist like Hollande also competing in the final battle in May 2017:

iii)The fear in Italy is reflected in Italian bond yields rising to 30 month highs( zero hedge)

iv)GREECE

Will Greece become the new India? Greek authorities are proposing a tax of cash withdrawals

(courtesy zero hedge)

v) Portugal

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

none today

7. OIL ISSUES

i)Oil last night opens at 2 week lows as hopes of a deal fade

( zero hedge)

ii)11th hr tension as OPEC scrambles for a deal:

( zero hedge/Sunday night)

iii)Then out of nowhere an Iraqi oil minister states he is hopeful of a deal and oil spikes northbound:

( zero hedge)

iv)Great reason for oil to be up today. The combatants cannot agree on anything:

( zero hedge)

8. EMERGING MARKETS

As I pointed out to you on the weekend, Venezuela has now officially entered the hyperinflation world. Today, the currency crashes 155 in one day. Each and every ay it will crash further until they issue a sound money policy

( zero hedge)

9. PHYSICAL MARKETS

i)Koos Jansen talks about the strong demand for gold inside China. For 3/4 of the year: net imports: 905 tonnes. Annualized over 1200 tonnes and total demand = withdrawals of over 1800 tonnes. Koos Jansen also talks about the huge premiums: why they are so and the relationship to the price of gold..

a must read..

( Koos Jansen/Bullionstar)

ii)Bill Murphy interviewed by Wealth Research Group

( zero hedge)

iii)A must read.. the silver institute that now forecasted a drop in silver production for 2016. The supply for silver is around 887 million oz. If you remove both China and Russia from the equation we get around 700 million oz but that will decline. Demand keeps rising which puts silver in a continual annual deficit;

( Steve St Angelo/SRSRocco report)

iv)This should provide increased demand for gold as now Islam allows gold purchases:

( Reuters/)

10.USA STORIES

i)Trading early last night: Dow futures drop as well as the USA/Yen

( zerohedge)

ii)The Trump victory has given new life to the Dallas Fed mfg sector. It soared to 10.2 , the first positive reading in over 22 months. Naturally the big gain was in the “hope” category

iii)On line sales have been doing OK on Black Friday but box department stores are having their troubles. Wolf Richter discusses the death of the department store

iv)Zero hedge weighs in on the lacklustre performance of holiday season so ar in the USA( zero hedge)

v)David Stockman, on the USA economy: he states that this the greatest suckeer’s rally of all time

( David Stockman/Price/CNBC)

vi)This is a biggy: you will recall that Trump has David Malpass and Judy Shelton as senior economic advisors and both are sound money and gold advocates. Now Trump is looking at John Allison, of the CATO institute. He wants to abolish the Federal Reserve and return to a gold standard..coincidence>>>??

( Business Insider)

Let us head over to the comex:

The total gold comex open interest FELL by 7799 CONTRACTS to an OI level of 415,587 AS GOLD FELL $10.90 with YESTERDAY’S trading In the front month of November we had 29 notices standing for a LOSS of 192 contracts. We had 0 notices served ON FRIDAY so we LOST 192 GOLD CONTRACTS OR AN ADDITIONAL 19200 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF NOVEMBER. The next contract month and the biggest of the year is December and here this month showed a DECREASE of 28,513 contracts DOWN to 77,556. The December contract month is still highly elevated compared to a year ago. On FRIDAY Nov 27/2015 comex reading day, we had a total of 24,018 contracts standing ( a loss of 36,141 contracts from Nov 25/2015. To give you more detail as to how the front month of December/2015 contracted, the final Nov 30 contract had an OI of 7,849 contracts standing or 24.41 tonnes standing as we lost 16,169 contracts.) The OI for the entire complex was around 393,000 or similar to the low readings this year. It certainly emphasizes the huge demand for physical gold.We have exactly 2 more trading days left. THIS SHOULD EXPLAIN TO YOU WHY THE BANKERS ARE CONSTANTLY WHACKING OF GOLD (AND SILVER): THE HIGH OI FOR DECEMBER AND THE HIGH PROBABILITY THAT MANY WILL TAKE DELIVERY. It looks to me like we will have 22,000 contracts or higher standing: 2.2 million oz or 68.4 million oz. That should break the bank.

And now for the wild silver comex results. Total silver OI FELL by 1409 contracts from 167,583 DOWN to 166,174 as the price of silver FELL BY $0.08 with FRIDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). The front month of November had an OI of 1 and thus a LOSS of 0 contracts. We had 0 notice(s) filed yesterday so we neither lost nor gained any contracts (oz) that will stand for delivery in this non active month of November. The next major delivery month is December and here it FELL BY 13,247 contracts DOWN to 27,148. The December contract month is a little elevated compared to a year ago. On Nov 27/2015 reporting day, we had a level of 16,868 contracts having lost 10,053 contracts on the day. On the final day of November/2015, we had 5,975 contracts stand for 29.875 million oz. We lost 4078 contracts on the last day prior to first day notice. It looks like we will end up with around 6,000 contracts standing for 36 million oz.

In silver had 1 notice(s) filed for 5,000 oz

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery.

Note how much paper settlements occurred in December last yr and I surely doubt if we will get any paper settlements this year.!!

VOLUMES: for the gold comex

Today the estimated volume was 310,392 contracts which is HUGE.

Friday’s confirmed volume was 405,569 contracts which is really huge

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz nil |

nil

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

96,450.000 oz

3000 kilobars Scotia

|

| No of oz served (contracts) today |

0 notice(s)

NIL oz

|

| No of oz to be served (notices) |

27 contracts

2700

oz

|

| Total monthly oz gold served (contracts) so far this month |

2673 contracts

267,300 oz

8.314 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 633,712.5 oz |

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

1 contracts

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 469 contracts (2,345,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,766,529.7 oz |

end

end

NPV for Sprott and Central Fund of Canada

will provide on Saturday/Sunday

END

At 3:30 pm est today, we received the COT report which gives us position levels of our major players.

Here is the gold COT:

— Published: Monday, 28 November 2016 | Print | Comment – New!

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 241,646 | 74,561 | 68,746 | 97,975 | 290,147 | 408,367 | 433,454 |

| Change from Prior Reporting Period | ||||||

| -4,104 | 6,471 | -310 | -17,216 | -25,010 | -21,630 | -18,849 |

| Traders | ||||||

| 143 | 95 | 73 | 52 | 54 | 232 | 190 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 52,695 | 27,608 | 461,062 | ||||

| 3,455 | 674 | -18,175 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, November 22, 2016 | |||||

Interesting report!!:

Our large speculators:

those large speculators that have been long in gold pitched 4,104 contracts from their long side

those large speculators that have been short in gold added 6471 contracts to their short side

Our commercials:

those commercials that have been long in gold pitched a huge 17,216 contracts from their long side

those commercials that have been short in gold covered a whopping 25,010 contracts from their short side

Our small specs:

those small specs that have been long in gold added 3455 contracts to their long side

those small specs that have been short in gold added 674 contracts to their short side

Conclusion:

the commercials go net long again by 7794 contracts. The boat is now not overloaded to one side. this is bullish for gold.

And now for our silver COT:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 81,835 | 21,668 | 11,493 | 46,804 | 125,036 | |

| -3,740 | -1,301 | 881 | -4,555 | -4,844 | |

| Traders | |||||

| 90 | 45 | 45 | 42 | 37 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 169,661 | Long | Short | |

| 29,529 | 11,464 | 140,132 | 158,197 | ||

| 2,244 | 94 | -5,170 | -7,414 | -5,264 | |

| non reportable positions | Positions as of: | 157 | 109 | ||

| Tuesday, November 22, 2016 | © SilverSeek.com | ||||

Our large speculators:

those large speculators that have been long in silver pitched 3740 contracts from their long side

those large speculators that have been short in silver covered 1301 contracts from their short side.

Our commercials:

those commercials that have been long in silver pitched a huge 4555 contracts from their long side (as they knew a raid was forthcoming)

those commercials that have been short in silver covered a huge 4844 contracts from their short side.

Our small specs;

those small specs that have been long in silver added 2244 contracts to their long side

those small specs that have been short in silver added 94 contracts to their short side.

Conclusion:

the commercials go net long by 289 contracts and that would be mildly bullish

end

Major gold/silver stories for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE

Bail In Risk – €4 Trillion Banking System In Italy Poses Contagion Risk as Referendum Looms

-

Bail in risk – €4 Trillion Italian banking system at risk as referendum looms Sunday according to Financial Times

-

Concerns of multiple bank failures – Eight banks at risk of failure and bail ins

-

Monte dei Paschi di Siena, third largest by assets and mid-sized banks Popolare di Vicenza, Veneto Banca and Carige and four smaller banks

-

Italy’s banks have €360 billion of problem loans

-

Contagion poses risks to Unicredit, Italy’s largest bank by assets and only globally significant financial institution

-

Bail in risks highlight importance of deposit diversification and gold

-

Imprudent to have all ‘savings eggs’ in ‘bankers basket’

(Copyright The Financial Times Limited 2016)

(Copyright The Financial Times Limited 2016)

“Up to eight of Italy’s troubled banks risk failing if prime minister Matteo Renzi loses a constitutional referendum next weekend and ensuing market turbulence deters investors from recapitalising them, officials and senior bankers say.

Mr Renzi, who says he will quit if he loses the referendum, had championed a market solution to solve the problems of Italy’s €4 trillion banking system and avoid a vote-losing “resolution” of Italian banks under new EU rules.”

Financial Times

The Italian banking system looks vulnerable to collapse whether the referendum is passed in Italy or not. Were the referendum passed, it may allow senior Italian and international bankers to further ‘kick the can down the road’ and delay the inevitable.

Financial and economic contagion in the EU is the likely outcome of the financial and political mess that both Italy and other EU states find themselves in. The question is increasingly not if, but when.

Bail-ins are “now the rule” and depositors need to begin preparing by diversifying and not have all their ‘saving eggs’ in the ‘bankers basket’.

An important way to protect investments and savings is to be diversified and have a healthy allocation to physical gold – both in one’s possession and in secure storage, in the safest vaults in the world.

Read full Financial Times article on Irish Times here

Gold and Silver Bullion – News and Commentary

Gold rises from multi-month lows as dollar eases (Reuters.com)

Gold recovers in Asia as investors see buying opportunities (Investing.com)

No proposal to restrict gold holding by individuals in India (IndiaTimes.com)

Gold not safe enough, hoarders opt for silver bars (NewIndianExpress.com)

Trump Claims Millions Voted Illegally, Without Giving Proof (Bloomberg.com)

Italian Prime Minister Matteo Renzi addresses supporters ahead of the constitutional reform referendum this Sunday (AFP PHOTO/ANDREAS SOLARO)

This Week “Could Shake The World …” (TheAustralian.com)

First Brexit then Trump. Is Italy next for the west’s populist wave? (TheGuardian.com)

Trump, Draghi May Bring A Return Of “European Solvency Crisis”: Barclays (ZeroHedge.com)

Venezuela’s currency is so devalued it no longer fits in ordinary wallets (WashingtonPost.com)

Stocks In Greatest Suckers’ Rally Of All Time: Stockman (CNBC.com)

Gold Prices (LBMA AM)

28 Nov: USD 1,189.10, GBP 956.51 & EUR 1,117.99 per ounce

25 Nov: USD 1,187.50, GBP 953.30 & EUR 1,121.83 per ounce

24 Nov: USD 1,187.25, GBP 953.60 & EUR 1,125.04 per ounce

23 Nov: USD 1,213.25, GBP 980.00 & EUR 1,143.00 per ounce

22 Nov: USD 1,217.55, GBP 978.91 & EUR 1,144.98 per ounce

21 Nov: USD 1,214.95, GBP 984.72 & EUR 1,143.39 per ounce

18 Nov: USD 1,206.10, GBP 971.15 & EUR 1,135.54 per ounce

Silver Prices (LBMA)

28 Nov: USD 16.68, GBP 13.45 & EUR 15.73 per ounce

25 Nov: USD 16.47, GBP 13.21 & EUR 15.55 per ounce

24 Nov: USD 16.31, GBP 13.09 & EUR 15.43 per ounce

23 Nov: USD 16.56, GBP 13.36 & EUR 15.59 per ounce

22 Nov: USD 16.76, GBP 13.46 & EUR 15.77 per ounce

21 Nov: USD 16.68, GBP 13.47 & EUR 15.69 per ounce

18 Nov: USD 16.51, GBP 13.30 & EUR 15.54 per ounce

Recent Market Updates

– Gold Down 13.5% In 13 Days – Trump Bearish For Gold?

– War On Cash Just Got Real – India and Citibank In Australia

– Russia Gold Buying In October Is Biggest Monthly Allocation Since 1998

– Stocks, Bonds, Pension Funds “Will Be Wiped Out…” – Rickards

– Physical Gold Is A “Long-Term Position” as “Hedge Against Governments”

– Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

– Islamic Gold – Vital New Dynamic In Physical Gold Market

– Peak Gold Globally – “Bullish For Gold”

– Gold Price Should Go Higher On Global Risks and Trump – Capital Economics

– President Trump – Why Market Loves Him and Experts Wrong

– ‘Helicopter Money President’ Trump To Create Inflation and Gold Will Rise

– Central Bank Gold Demand continues in Q3

– Trump Victory Sends Gold Surging 5%

end

Koos Jansen talks about the strong demand for gold inside China. For 3/4 of the year: net imports: 905 tonnes. Annualized over 1200 tonnes and total demand = withdrawals of over 1800 tonnes. Koos Jansen also talks about the huge premiums: why they are so and the relationship to the price of gold..

a must read..

(courtesy Koos Jansen/Bullionstar)

Q1 – Q3 2016 China Net Gold Import Hits 905 Tonnes

Withdrawals from the vaults of the Shanghai Gold Exchange, which can be used as a proxy for Chinese wholesale gold demand, reached 1,406 tonnes in the first three quarters of 2016. Supply that went through the central bourse consisted of at least 905 tonnes imported gold, roughly 335 tonnes of domestic mine output, and 166 tonnes in scrap supply and other flows recycled through the exchange.

Core Supply & Demand Data Chinese Gold Market Q1-Q3 2016

Chinese gold demand is still going strong this year, albeit less than in 2015. The most likely reason for somewhat lower demand has been the strength in the price of gold in the first three quarters of this year, to which the Chinese reacted by subduing purchases. From 1 January until 30 September 2016, the gold price went up 24 % in US dollars per troy ounce, from $1,061.5 to $1,318.1; measured in renminbi the price went up 28 % over the same period.

Now I have proven the gold on Chinese commercial bank balance sheets has little to do with physical gold ownership of these banks, but mainly reflects back-to back leases and swaps, we can be positive that data on withdrawals from the vaults of the Shanghai Gold Exchange (SGE) roughly equals Chinese wholesale demand. For now that is, as future developments can always alter our metrics.

Below is a chart showing withdrawals from the vaults of the SGE and the price of gold in yuan per gram. The most significant trends of recent years are still in effect; in the short term, when the gold price is falling Chinese demand increases (2013 and 2015), when the gold price is rising Chinese demand declines (2016). This trend is supported by SGE premiums that have an inverse correlation with the price of gold, when the price of gold declines, SGE premiums escalate and vice versa – I will show charts below. Furthermore, in the long term we can observe consistent growth in Chinese gold demand due to the opening up and development of the domestic market.

SGE withdrawals in the first three quarters of 2016 accounted for 1,406 tonnes – still impressive – down 29 % from 1,986 tonnes in 2015, which was a record year. Annualized SGE withdrawals are set to hit 1,877 tonnes in 2016.

Notable, “known net import” by China is relatively strong compared to SGE withdrawals in 2016. Total net import in the first three quarters of this year has aggregated to 905 tonnes – annualized 1,206 tonnes – or 64 % of SGE withdrawals, versus an import/withdrawals ratio of 53 % in 2015. As mine supply to the SGE is fairly constant, recycled gold through the SGE must be lower this year than last year. As a rule of thumb, we use the equation:

SGE withdrawals = domestic mine output + import + recycled

For Q1-Q3 2016 that gives:

1,406 tonnes = 335 tonnes + 905 tonnes + 166 tonnes

The largest net exporter to China is still Hong Kong, having transhipped 608 tonnes to the mainland from January until September 2016, up 5 % compared to 2015. The volume Hong Kong exports to the mainland has been quite constant since 2014, while in 2013 China’s special administrative region was a substantial larger supplier.

(There have been rumors that Hong Kong ’s export to China is overstated in the official data by the Hong Kong Census & Statistics Department, caused by fake exports. In the chart below you can see that the share of exports relative to re-exportsfrom Hong Kong to China this year has increased from previous years. Potentially this signals fake exports, as it’s easier to over invoice an export than re-export, though I haven’t found hard evidence for this scheme. When I do I will report accordingly.)

The second largest exporter to China is Switzerland, having supplied a net 229 tonnes so far this year, which is 22 % more than last year. Clearly, direct shipments from Switzerland to China have replaced shipments via Hong Kong.

Direct net exports by the UK to China mainland have collapsed by 92 % this year compared to 2015, from 210 tonnes to a mere 18 tonnes. The reason being, the UK has been the largest net importer globally this year, which is related to the strength in the gold price early this year. UK net gold trade is a proxy for Western institutional supply and demand.

Australia’s direct export to China is down this year as well (in the first eight months, data for September has not yet been released). I’ve computed the data as described in my post Australia Customs Department Confirms BullionStar’s Analysis On Gold Export To China. Following this method, the land of down under has sent 50 tonnes of gold directly to China during the first eight months of this year, down 23 % from 65 tonnes in 2015.

Despite press releases suggesting Russian gold enterprises are strengthening ties with the SGE, I have identified only one shipment of 30 Kg by the Russian Federation directly to China in 2016. In 2013 the Russians directly net exported 50 Kg to China.

Data on gold export from South Africa to China is not publicly available.

In exhibit 7 we can see that, although the level of SGE withdrawals in 2016 is lower than in 2013, 2014 and 2015, net imports are higher than in 2014. It’s very difficult to know the exact explanation for relative high imports this year. Though, in my opinion, it’s connected to increased Chinese ETF demand, which grew by 34 tonnes and is all required to be stored in SGE vaults, and less gold being recycled through the SGE.

Since 2014, when the Shanghai International Gold Exchange (SGEI) was erected, there is a possibility “SGE withdrawals” are inflated by withdrawals from vaults in the Shanghai Free Trade Zone; gold that is allowed to be exported abroad – the free trade zone is not part of the domestic market. But as far as I know any activity on the SGEI lacks foreign enterprises that buy gold to withdraw and export. A couple of months ago a source at a large Chinese bank told me the SGEI is mainly used by Chinese banks to import gold into Chinese domestic market. In addition, I haven’t bumped into any large importers fromChina. Occasionally India imports a few hundred Kg, but that’s it.

The emblematic difference between “Chinese gold demand as disclosed by GFMS” and SGE withdrawals – displayed in exhibit 7 – is due to GFMS’ incomplete metrics. For decades this consultancy firm has been denying the existence of institutional supply and demand in above ground gold, which is far more important to price formation than retail sales and mine supply, the predominant flows published by GFMS. The essence of this swindle can be read in my blog post The Great Physical Gold Supply & Demand Illusion. I also have a few more blog posts in the pipeline that discuss GFMS’ most recent gold supply and demand data.

SGE Premiums November Highest Since 2013

I expect November to be a very strong month for SGE withdrawals. Mentioned in the introduction segment of this post, there is a trend in Chinese wholesale gold demand in relation to the gold price. Whenever, the gold price is climbing, Chinese demand is subdued, accompanied by low SGE premiums; when the gold price is decreasing, SGE withdrawals and premiums in China shoot up. The relationship between the gold price and SGE withdrawals can be viewed in exhibit 1. Below in exhibit 8 & 9, readers can see the relationship between “SGE end of day prices and premiums”.

Note, the gold price on the SGE and the premium have an inverse correlation.

I already mentioned that SGE withdrawals in the first nine months of 2016 have been subdued due to a rally in the gold price. However, high premiums at the SGE in November forecast elevated withdrawals for the month. Since Trump got elected on November 9, and price of gold started tumbling, SGE premiums have broken a three-year record. This signals strong demand.

In the next chart from Goldchartsrus.com we can see the premium on the SGE’s most traded physical contract Au99.99 has risen since November 9 and reached 3 % by 24 November. Levels not seen since 2013 (exhibit 8).

Although the relationship between the gold price and SGE premiums has been in place for years, Reuters reports the high premiums in November are caused by worries on import restrictions. From Reuters:

Gold premiums in top consumer China jumped to the highest in nearly three years this week on worries over a supply shortage that traders said were due to Beijing’s efforts to restrict import licenses.

…

“While we don’t have the exact numbers, we hear that they (Chinese government) have limited the number of importers,” said Dick Poon, general manager at Heraeus Precious Metals in Hong Kong.

To me this statement doesn’t make sense. At this moment that are 15 banks approved by the PBOC to import gold. Limiting the number of importers would cause less importers to import more gold in order to balance the domestic market (supply gold from abroad when necessary). In the Measures for the Import and Export of Gold and Gold Products drafted by the PBOC in March 2015 it states:

… An applicant for the import … of gold … shall have corporate status, … it is a financial institution member or a market maker on a gold exchange [SGE] approved by the State Council.

… The main market players with the qualifications for the import … of gold shall assume the liability of balancing the supply and demand of material objects on the domestic gold market. Gold to be imported … shall be registered at a spot gold exchange [SGE] approved by the State Council where the first trade shall be completed.

The Chinese government could lower imports by distributing less “import licences” to approved banks. As, every approved bank still needs to submit for a license for every gold import batch. Logically, lowering imports would be done by the PBOC through handing out less licences.

There shall be one Import … License of the People’s Bank of China for … Gold Products for each batch … and the License shall be used within 40 work days since the issuing date.

If the PBOC wanted to lower imports, it would simply hand out less licences. No need to “limit the number of importers”.

Either way, I expect SGE withdrawals to be strong for November.

Koos Jansen

E-mail Koos Jansen on: koos.jansen@bullionstar.com

END

Bill Murphy interviewed by Wealth Research Group

(courtesy zero hedge)

GATA Chairman Murphy interviewed by Wealth Research Group

Submitted by cpowell on Sat, 2016-11-26 19:33. Section: Daily Dispatches

2:36p ET Saturday, November 26, 2016

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy was interviewed this week by Wealth Research Group editor Lior Gantz about GATA’s work exposing government rigging of the gold market and other markets. The interview is a half hour long and can be heard at YouTube here:

https://www.youtube.com/watch?v=Ra1m7-uAr6k

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

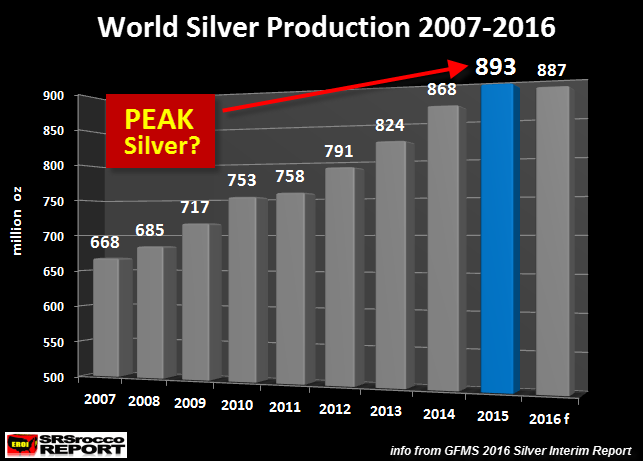

A must read.. the silver institute that now forecasted a drop in silver production for 2016. The supply for silver is around 887 million oz. If you remove both China and Russia from the equation we get around 700 million oz but that will decline. Demand keeps rising which puts silver in a continual annual deficit;

(courtesy Steve St Angelo/SRSRocco report)

Peak Silver & Continued Supply Deficits Warn Of Future Higher Prices

by SRSrocco on November 28, 2016

If the market has finally experienced a peak in world silver production, this warns of higher prices in the future. In addition, the global silver market suffered another large net supply deficit in 2016. These factors point to a big upcoming trend change in the future silver market.

The Silver Institute just published its 2016 Silver Interim Report. This report is published by Thomson Reuters GFMS. According to their forecast for 2016, global silver production will decline to 887 million oz (Moz), down from 893 Moz in 2015:

While forecasted global silver production for 2016 is down only slightly versus last year, GFMS also stated this in their report:

- We estimate that mine supply peaked in 2015 and will trend lower in the foreseeable future.

- Declining total supply is expected to be a key driver of annual deficits in the silver market going forward.

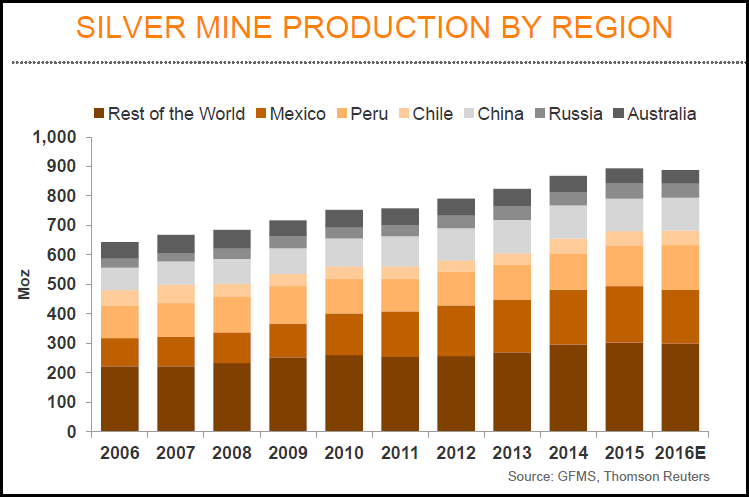

I will get to the annual silver deficits in a minute, but let’s look at their world silver mine supply by region:

What is interesting here, is that GFMS forecasts the number one silver producer, Mexico, to be down in 2016 by more than 6 Moz. Last year, I forecasted that global silver production would likely be lower in 2015. I was going by data by the “World Metals Statistics.” However, Mexico’s INEGI (government agency) considerably revised their figures higher for 2015. While I have seen revisions take place, the revisions by Mexico’s INEGI for 2015 were quite substantial.

Regardless, GFMS does a pretty good job with the silver mine supply data. The important take-away here is that the trend of global silver production will likely be lower going forward.

The Majority Of Global Silver Production Declines Will Come From By-Product Base Mining

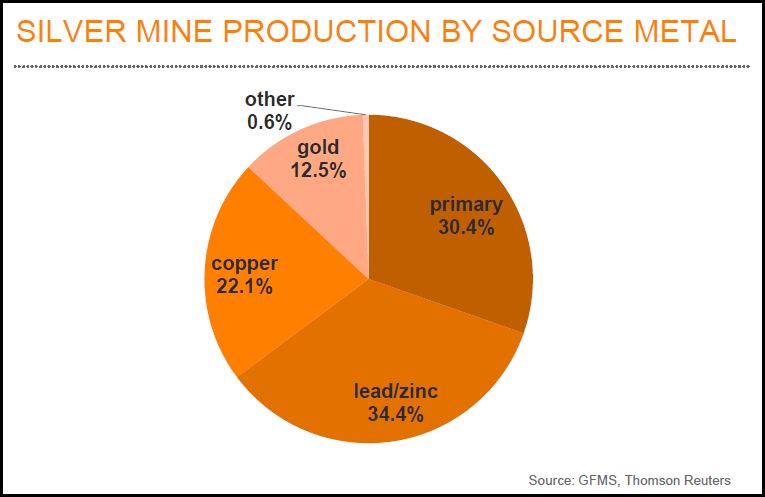

The majority of silver production comes from the by-product of base metal mining. According to GFMS 2016 Silver Interim Report, lead & zinc accounted for 34.4% of silver supply, while copper yielded 22.1%. Thus, the mining of these three base metals supplied 56.5% of global silver production in 2016. Primary silver production accounted for 30.4% and gold mining supplied 12.5%:

As I have mentioned in prior articles, the decline in global oil production will impact base metal mining to a larger degree than primary silver production. It takes a great deal of liquid fuels to produce the world’s base metals.

For example, the Chilean Copper Commission stated in a 2014 report, that the country consumed 535 million gallons of liquid fuel to produce 5.7 million tons of copper. Thus Chile’s copper industry consumed 94 gallons of liquid fuel for each tonne of copper produced.

On the other hand, Pan American Silver burned 20.5 million gallons of liquid fuel to produce their 26.5 million oz of silver in 2015. Which means, each ounce of silver production took 0.80 gallons of liquid fuel. If we use Pan American Silver as a guide, then the 269 Moz of primary silver production in 2016 consumed 215 million gallons of liquid fuel. However, I would imagine the global primary silver production average is much less, more like 0.50 gallon per ounce of silver. So, we are talking about 135-150 million gallons of liquid fuel to produce all the primary silver in the world.

Now, the world produced a total of 18.4 million tons of copper in 2014. Taking Chile’s average of 94 gallons per tonne of copper produced and providing a conservative estimate of say 75 gallons per tonne for entire globe, then the world consumed roughly 1.4 billion gallons of liquid fuels to produce its copper in 2014. This is about ten times the amount of fuel it took to produce all the primary silver production. Of course this is a simple estimate, but there you have it.

Once the world enters into the next financial collapse, U.S. and world oil production will plummet. This will impact base metal mining a great deal more than primary silver production. Which means, overall silver production will decline more rapidly due to more than half coming from zinc, lead and copper.

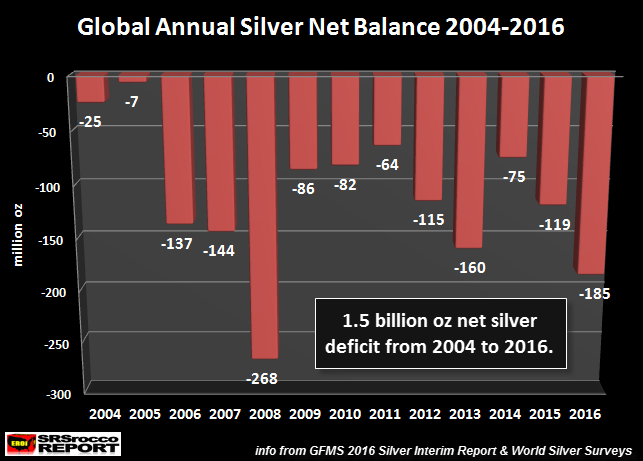

Global Annual Silver Deficits Continue For 13 Consecutive Years

Due to the huge increase in Global Silver ETF demand as well as a large Exchange Inventory build, the silver market will suffer a forecasted 185 Moz annual deficit in 2016. If we look at the annual silver deficits since 2004, it equals a stunning 1.5 billion ounces:

GFMS calculates their “net balance” by subtracting physical demand from supply, then deducted or added changes in Silver ETF and Exchange inventories. According to their data (as of Sept 2016), Silver ETF’s and Exchanges added 133.3 Moz of silver to their inventories. Furthermore, total physical demand exceeded total supply by 52.2 Moz to arrive at the total 185.5 Moz (rounded to 185 Moz) net deficit.

These annual deficits have been supplemented by silver surpluses of the 1980’s and 1990’s. However, annual deficits are forecasted to continue as mine supply continues to decline along with subdued scrap supply.

Why Do These Supply & Demand Factors Matter For the Future Price Of Silver?

Recently I have stated that new information on the Thermodynamic Oil Collapse, based on the Hills Group and Louis Arnoux’s work, suggests that supply and demand are not the real factor that determines price, rather it’s the cost of production.

However, gold and silver are different from most other metals, commodities and energy. While silver is consumed more than gold, it still functions as “MONEY” or a “STORE OF VALUE.” Thus, it should be valued differently than copper, wheat or oil.

I don’t look at global mine supply or the annual silver deficits as factors that will impact the market price of silver by certain degrees, rather I look at them as a TELLTALE sign that the overall trend is changing, and has been for nearly a decade. It is the longer term fundamental trend change that interests me, not the year by year supply and demand factors on price.

Currently, the silver price is based on its cost of production (90-95%) plus some supply and demand factors. While many believe the BIG BANKS can push the price of silver anywhere they see fit, this is pure nonsense. If the Big banks pushed the price of silver 25-50% below its average primary silver cost of production, traders would come in by the droves. While traders may be uninterested in long-term fundamentals, they aren’t stupid as it pertains to short-term market forces.

That being said, silver’s ultimate value is not based on its cost, it will be based on its STORE OF VALUE properties when the MOTHER OF ALL DEFLATIONS finally arrives. I am talking about deflation of most paper assets (stocks & bonds) and real estate.

Because there is so little real physical silver out in the market, 3-4 billion oz, any significant amount of capital moving into it will push its value to seriously high levels. This may seem a play on hype, especially for those who are a bit disillusioned by the price smash since the Trump President election.

Unfortunately, for those who continue BELLY-ACHING about low silver prices, there isn’t much I can say to change your opinion. I have come to realize that a significant percentage of silver investors who continue to understand the long-term fundamentals, will never complain about lower prices. They just suck it up and know that insane Central Bank policies won’t last forever.

Unfortunately, the precious metals community also has its group of individuals who will complain when the going gets rough. This should be expected as this is the typical nature of a FICKLE public. All slaps on the back when things are good and the first to bad mouth when things turn south.

I get a kick out of the BELLY-ACHERS who seem to forget that the Central Banks have embarked on the most insane monetary policy in history. They have pushed debt and money supply to an exponential trend. I find it simply amazing how a disgruntled silver investor points out how wrong the precious metals analysts were on the silver price since 2012, while totally dismissing massive Central Bank monetary invention.

Regardless, peak silver production on top of the continued annual deficits point to a trend that will reach an INFLECTION POINT in the future. So, here is the BEEF. If you think exponentially increasing debt and monetary liquidity will continue for the next 5-10 years, then maybe you should stay in Dollars, U.S. Treasuries, Stocks and Real Estate. However, if you aren’t suffering from brain damage as many in the markets are today, you may want to consider staying put in the 2,000+ year monetary history and store of value of silver.

end

This should provide increased demand for gold as now Islam allows gold purchases:

(courtesy reuters/Vizcaino)

UPDATE 1-Islamic Finance Group Approves Standard for Gold Products

By Reuters

Monday November 28, 2016 11:53

(Updates with comments)

By Bernardo Vizcaino

Nov 28 The Bahrain-based group that issues guidelines generally followed by Islamic financial institutions has approved a sharia standard for gold-based products in a bid to expand the use of bullion in Islamic finance.

Traditionally, gold has been viewed as a currency in Islamic finance, confining it to spot trades in fixed weights and measures. Investors have been unable to speculate on its future value and there has been no clear policy on how to trade gold.

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) approved the final version of its new standard on gold and trading controls last week and an official launch will be announced soon, it said in a statement.

The new standard addresses issues such as collateral, set-off, screening and the exchange of gold in spot and deferred transactions. Sharia compliant products backed by gold could include exchange-traded funds and savings accounts.

AAOIFI issues guidelines that are followed wholly or in part by Islamic financial institutions across the world, so its efforts would help align the industry to global practices.

Uncertainty about how gold can be used in Islamic finance has kept sharia-compliant bullion transactions at a minimum, Matthew Keen, founder of Dubai-based precious metals consultancy Evidens and an adviser to the World Gold Council, said.

London-based ETF Securities, for example, launched a sharia-compliant exchange-traded commodity product for gold, silver, platinum and palladium in 2008 but it never gained traction.

“There is such a lack of understanding of what sharia law would mean in terms of gold investing and this standard would at least provide a common ground,” ETF Securities director of commodity research Nitesh Shah said.

“However, this is not going to be a game changer for global gold consumption,” he said, as sharia law does not prohibit the ownership of gold jewellery or coins.

The final standard will be made available on a complimentary basis by AAOIFI and the World Gold Council (WGC), an industry organisation that supported the development of the standard.

Proponents hope the new guidance will help address muted consumer appetite for gold in the Middle East, where demand has actually fallen in recent years.

With Islamic financial assets seen at about $2 trillion, a one percent allocation to gold would boost demand by $20 billion, or about 500 tonnes.

“I am a bit sceptical as even in the developed world, where access to gold investing has been there for many decades, you don’t see a one or two percent of anyone’s aggregate portfolio allocated to gold, so it is highly unlikely in a new emerging market,” Shah at ETF Securities said.

AAOIFI also approved a standard on the liability of investment managers, which addresses issues including negligence and breach of contract. It details liability on the part of service agents in transactions including Islamic bonds (sukuk) and in syndicated financing contracts and other products. (Additional reporting by Andrew Torchia in Dubai and Clara Denina in London; editing by Simon Cameron-Moore and David Clarke)

end

FEDERAL RESERVE BANK OF NEW YORK; FOREIGN GOLD MOVEMENTS

(HARVEY)

Last month I reported to you that 5 tonnes of gold moved out of the FRBNY which was much smaller than before as Germany was not getting its required amount of gold.

Now this month:

FRBNY gold holdings Sept: 7841

FRBNY gold holdings Oct: 7841

all figures are million dollars worth of gold at the official rate of 42.22 dollars per oz

amount leaving: 0

Amount repatriated: zero

Germany must be royally angry!

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan UP to 6.912(SMALL REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS TO 6.9360 / Shanghai bourse CLOSED UP 15.06 POINTS OR 0.46% / HANG SANG CLOSED UP 107.12 OR 0.47%

2. Nikkei closed DOWN 24.33 POINTS OR .13% /USA: YEN FALLS TO 112.73

3. Europe stocks opened ALL IN THE RED ( /USA dollar index RISES TO 101.52/Euro UP to 1.0584

3b Japan 10 year bond yield: FALLS +.022%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 46.33 and Brent:47.66.

3f Gold UP /Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS TO +.194%

3j Greek 10 year bond yield RISES to : 6.96%

3k Gold at $1188.00/silver $16.64(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 15/100 in roubles/dollar) 64.98-

3m oil into the 46 dollar handle for WTI and 47 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a HUGE DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.73 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0155 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0748 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.234%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.334% early this morning. Thirty year rate at 2.99% /POLICY ERROR)

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Slide On Italian Bank Worries; Dollar Dips As Trumpflation Takes A Back Seat

European shares dipped and U.S. equity-index futures (-0.3%) pointed to a lower open as traders questioned the stability of the Italian banking sector ahead of next weekend’s referendum as well as the longevity of the Trumpflation rally, pressuring the dollar, sending the USDJPY sliding as low as 111.355 overnight, before rebounding over 112. That was the dollar’s biggest fall against its Japanese rival since October 7 and against a basket of top world currencies it was the greenback’s worst day since November.

The euro rose to an 11-day high $1.0686 as it got a lift too from the election of Francois Fillon as the center-right candidate in next year’s French presidential election. The reformist former prime minister is now favorite to become president, with a flash opinion poll showing he would easily beat National Front leader Marine Le Pen in a run-off second round. Markets worry the far-right Le Pen, who has promised a referendum on membership of the European Union if she wins, would threaten the future of the currency bloc.

“It’s a bit of a pull back in the dollar,” said Societe Generale strategist Alvin Tan. “The fall in oil is pushing back U.S. bond yields and that is leading the consolidation in the dollar.. there is more scepticism about an (OPEC) output cut now.”

“The Trump trades were a distraction for a while but now people are starting to look elsewhere for market drivers,” said Kevin Lilley, a manager of euro-area equities at Old Mutual Global Investors in London. “People are getting worried about the impact that a power vacuum in Italy could have on the refinancing needs of its banks. It’s a nervous market at a time when liquidity isn’t great.”

“Starting this week, the thinking is that people will probably pull to the sidelines and adopt a wait-and-see approach,” said Sim Moh Siong, a currency strategist at Bank of Singapore Ltd. Much of the optimism flowing from expectations of increased U.S. fiscal stimulus has been priced in by the market and investors will probably pause until “further clarification of Trump’s policy stance,” he said.

The dollar weakness lifted Treasuries while latest incarnation of the

China commodity bubble boosted industrial metals, sending zinc surging. Industrial metals have been red hot in recent weeks on hopes of strong demand for property and infrastructure investment in China and the United States. Chinese steel futures jumped over 6% , while iron ore futures also gained about six percent and zinc powered to a nine-year high on the London Metal Exchange. As shown in the chart below, an index of industrial metals is now up 22% in just the past month, and up 40% since January.

Oil in New York was trading flat at $46 as OPEC tries a last-minute salvage of the Algiers production cut agreement ahead of the Wednesday meeting in Vienna. Italian banks led declines in European shares Prime Minister Matteo Renzi faces a key referendum on Sunday that may see voters reject his constitutional reform and prompt his resignation. As many as eight Italian banks are at risk of failing if the Renzi loses a constitutional referendum this weekend the FT reported. Shares in the nation’s largest bank UniCredit SpA fell for the the fourth day, heading for the lowest since August. Banca Monte dei Paschi di Siena SpA, which holds the most Italian sovereign debt relative to tangible equity and is under pressure to raise 5 billion euros of fresh money, fell as much as 12 percent before being halted.

Asian shares rose 0.4 percent overnight, led by gains in Hong Kong and Taiwan .TWII though Japan’s Nikkei which has been performing even better than a record high Wall Street in recent weeks thanks to the yen’s fall, ended down 0.1 percent.

Global growth got a welcome boost, if only on paper, when in its twice-yearly report on global economic prospects, the OECD said that while the exact form it would take is uncertain, it does expect Mr. Trump to offer some fiscal stimulus from the early months of his presidency, and that its likely scale that would boost U.S. economic growth to 2.3% from 1.9% in 2017, and to 3% from 2.2% in 2018. There would also be benefits for other parts of the world as U.S. demand for imports rises, with global economic growth raised to 3.3% from 3.2% in 2017, and to 3.6% from 3.3% in 2018. The OECD is the first international economic policy agency to publish an estimate of the likely impact of Mr. Trump’s proposals.

Global yields dipped as dollar weakness, and thus a brake on inflation expectations, sent Treasuries around the world modestly higher, however the one outlier was once again German 2Y yields, which dropped to fresh record lows on continuing fears about European collateral scarcity.

The yield on 10-year U.S. Treasuries dropped almost 5 basis points to 2.323%, off its 16-month high of 2.417%touched last week. Europe’s benchmark, German Bunds, saw their equivalent yield drop 3 basis points.

Other top news stories include lower consumer spending on Black Friday,

Philips panning to roll out medical software to challenge GE.

* * *

Bulletin Headline Summary From RanSquawk

- European equities enter the North American crossover lower as ongoing concerns surrounding Italian banks and downside in energy names hampers sentiment

- FX markets have seen some correct moves in the USD with USD/JPY lower by just under a point while EUR/GBP has been supported by month-end flows

- Looking ahead, highlights include potential comments from ECB’s Coeure and Draghi

Market Snapshot

- S&P 500 futures down 0.3% to 2205

- Stoxx 600 down 0.6% to 341

- FTSE 100 down 0.7% to 6795

- DAX down 0.9% to 10607

- German 10Yr yield down 3bps to 0.21%

- Italian 10Yr yield down less than 1bp to 2.09%

- Spanish 10Yr yield down less than 1bp to 1.56%

- S&P GSCI Index up 0.1% to 365.7

- MSCI Asia Pacific up 0.7% to 137

- Nikkei 225 down 0.1% to 18357

- Hang Seng up 0.5% to 22831

- Shanghai Composite up 0.5% to 3277

- S&P/ASX 200 down 0.8% to 5464

- US 10-yr yield down 4bps to 2.32%

- Dollar Index down 0.4% to 101.08

- WTI Crude futures down 0.4% to $45.88

- Brent Futures down 0.4% to $47.04

- Gold spot up 0.7% to $1,192

- Silver spot up 0.9% to $16.68

Global Headline News

- OPEC Seeks Oil Deal as Saudis Open Door for No Output Cut: Algeria, Venezuela ministers travel to Russia to seek support

- Bargain Hunters Roil Retailers Looking for Black Friday Bounce: The average amount shoppers spent fell 3.5%, including both online and offline purchases, according to the National Retail Federation

- Philips to Start Selling Smart Software for Doctors to Rival GE: Medical software market could grow twice as fast as devices

- Samsung Investors Voice Support for Elliott Proposals: Elliott seeking split, new directors, special dividend

- Hulu CEO Plots a Way to Stand Out From the Crowd in Online TV: Company will be first streaming provider to offer live video

- China Said to Prepare Overseas Dealmaking Curbs Amid M&A Spree: Overseas deals of at least $10 billion to be generally barred

- Trump Claims Millions Voted Illegally, Without Giving Proof: Trump offered nothing to back up his allegations of wrongdoing in the Nov. 8 election

- Time Inc. Said to Have Rejected Edgar Bronfman’s Bid: NY Post

- WTO May Rule Boeing Received Illegal Subsidy on Jetliner: WSJ

- CME Group Tables Bid for LSE’s Clearing Ops in France: S. Times

- Amazon to Announce Matson Moved Core Computing Ops to AWS: WSJ

- Fidel Castro, Communist Former Leader of Cuba, Dies at 90

* * *

Looking at regional markets, we start in Asia where stocks shrugged off another record US close on Friday and began the week mixed with weakness in energy and JPY strength dampening sentiment in the region. ASX 200 (-0.8%) finished lower with oil names pressured as WTI crude futures extended on losses to below USD 46/bbl after informal producer talks set for today were cancelled and Saudi’s energy minister Al-Falih further added to the uncertainty as his comments suggested the door was open to the possibility of no cut in output. A firmer JPY ensured the Nikkei 225 (-0.3%) snapped a 7-day win streak, while Shanghai Comp (+0.5%) and Hang Seng (+0.7%) were buoyed by stronger growth in Industrial Profits and after the announcement the Shenzhen-Hong Kong stock connect will launch next Monday.

Top Asian News

- China Has Quietly Hiked Borrowing Costs With PBOC Operations: Move is latest sign of selective tightening to temper leverage

- Yen at 120 Lonely Call No More for Analyst Who Got It Right: AMP Capital, BNP Paribas see yen surpassing 125.86 low

- CSC Financial Hong Kong IPO Seeks to Raise Up to $1.06 Billion: Company and National Social Security Fund are offering combined 1.13b shares at HK$6.36-HK$7.26 apiece

- India Said to Mull Foray Into Plane Leasing to Support Modi Plan: Proposal would see state-run firm leasing out 20- seater planes

- Singapore’s GIC Hires Big Data Expert in Quant Strategy Push: GIC expands Systematic Investment Group started this year

In Europe, the focus this morning has fallen upon Italian bankswhich has soured sentiment across Europe (overall Italian banking index down over 3%), in particular Banca Monte Dei Paschi with the troubled lender beginning its debt-equity swap with the bank hitting limit down shortly after the European open before falling 12%. While the sector has also been gripped by the near term risk factor in the form of the constitutional reform referendum, whereby an article stated that 8 Italian banks would fail if Renzi loses the vote as investors would be deterred from recapitalisation. Oil names have also been pressured following weekend reports suggesting that Saudi Arabia could be open to the idea of no reduction in output as the Energy Minister Al-Falih stated that demand is expected to recover next year and prices will stabilize which will occur without OPEC intervention.

Elsewhere, fixed income markets have been supported by safe haven flow early on, while a continuation of last week’s theme has seen Gilts slightly outperform its German counterpart thus far as participants await ECB President Draghi. While the looming Italian referendum has kept the ITA-GER 10yr spread at its widest in around 3-yrs.

Among the biggest weekend stories in Europe, Alain Juppe conceded defeat in the French presidential conservative primary against Fillon who won with nearly 70% of votes. Additionally, a Harris Interactive poll suggested conservative candidate Fillon would beat Far-Right candidate Le Pen in the French Presidential Election by 67% vs. 33%. BoE’s Carney wants Britain to remain in the single market for at least two years after Britain leaves the EU to cushion the impact on businesses, although his efforts may be viewed as an attempt to water down the Brexit. There were also reports that Brexit campaign leaders are said to reject plan by BoE Governor Carney to negotiate a buffer during the Brexit process. The UK Government is set to face a legal battle as to whether the UK can remain in the single market after its departure from the EU, according to the BBC.

Top European News

- ECB to Be ‘Pillar of Stability’ in Risky Year, Policy Maker Says: Governing Council member Stournaras speaks in interview

- Fillon Unites French Right After Primary as Socialists Split: Former prime minister records overwhelming victory in primaries

- Aberdeen Rises After Maintaining Dividend in Face of Outflows: Shares rose the most in seven weeks

- Biggest U.K. Banks Seen Struggling in Toughest Stress Tests Yet: All likely to top lower bar, some may stumble on new measure

- Investor Who Backed Brexit Sees Euro Breaking Up Within 5 Years: Euro as it stands is an inappropriate mechanism, Burnbrae’s Jim Mellon says

- Engie CEO Shifts Gear on Asset Sales, Cost Cuts as Shares Tank: Kocher says divestment plan will progress ahead of schedule

In currencies, the Bloomberg Dollar Spot Index, which tracks the greenback against 10 major peers, fell for a second day, declining 0.4 percent as of 10:47 a.m. in London. The rand gained against all of its 31 major counterparts, surging 1.7 percent to 13.8692 per dollar. A senior party official said there’s significant support in the ruling African National Congress’s executive committee to oust South African President Jacob Zuma, whose administration has been plagued by corruption and mismanagement.

In commodities, as the OPEC talks get under way, WTI and Brent prices are lagging though with ever present hope in the air, aggressive selling is absent for now. That said, few expect a significant deal — which can be logistically implemented — to transpire, so this may have been partially priced in to the drop in WTI from USD 50.00+ levels to circa USD 45.00 again. Some are suggesting another ‘breakdown’ in talks could send Oil down through USD 40.00, but all hangs in the balance for now. Elsewhere, Copper prices have managed to claw out some fresh highs, but failing to hold onto these levels — touching on USD 2.75 before easing back a little. Gold has come back off the lows near USD 1175 seen last week, but it is a tepid pullback as USD buyers will continue to buy the dip into the Dec FOMC and maintain pressure on the yellow metal accordingly. Saudi Arabia, Iran and Iraq have been seen arriving at OPEC technical meeting according to Twitter reports. Iran is still attempting to make themselves exempt from an OPEC output cut but expected the cartel to still strike a deal this week. Saudi Arabia left the door open for the possibility of no reduction in output as Energy Minister Al-Falih stated that demand is expected to recover next year and prices will stabilize which will occur without OPEC intervention and also added there in no single path to reduce output at the OPEC meeting as a recovery in consumption could also be depended on.

Looking at the day’s events, It’s a fairly quiet start to the week today. In Europe we’ll get the latest M3 money supply data for the Euro along with the latest OECD economic outlook while in the US the sole release is the Dallas Fed’s manufacturing survey.

Economic Event Calendar:

- 9am: ECB’s Draghi speaks in Brussels

- 10:30am: Dallas Fed Manufacturing Activity, Nov., est. 1.5 (prior -1.5)

- 7:45pm: Bank of Canada’s Poloz speaks in Toronto

* * *

DB’s Jim Reid concludes the overnight wrap

The main news from the weekend concerns the result of the final centre-right primary vote in France. The result has gone heavily in favour of the victor from the first round, Francois Fillon, who, with over 10,000 of the 10,229 polling stations accounted for, has gained 66.5% of the votes over Alain Juppe who garnered 33.5% of the vote. Juppe has officially conceded. With that result, Fillon is now the Republican candidate at next May’s presidential election in France and likely to face a Socialist candidate and also his main rival, the far-right’s Marine Le Pen. Ahead of the result, our European economists noted in their Focus Europe piece on Friday that at the last reported poll in September, Fillon held a roughly 20pp lead in the 2nd round presidential election versus Le Pen. In fact Bloomberg are reporting two polls this morning, both of which show Fillon as beating Le Pen in both rounds of the presidential election and by a fairly comprehensive margin too. More significantly for the 2nd round, an Odoxa poll shows Fillon as defeating Le Pen by 71% to 20% and a Harris Interactive poll shows Fillon winning by 67% to 33%. I’m sure if we hadn’t had Brexit and the US election result there would be less financial market concern over the French election next year. However these events have happened and therefore the market will remain on edge ahead of the poll next year.

Meanwhile, much of the remaining weekend headlines focus on this week’s main event, that being the much anticipated OPEC meeting this Wednesday in Vienna. WTI was the big mover in markets on Friday after plummeting nearly – 4% to close a smidgen above $46/bbl after Saudi Arabia pulled out of a planned producers meeting for today between OPEC and non-OPEC countries, calling the meeting ‘not beneficial’ before ‘holding meetings within OPEC and deciding whether to cut or continue with current levels of production’. According to the WSJ, OPEC is demanding Russia and other producers outside of the cartel to cut production by 500k-600k barrels a day, however Russia’s energy minister has on a number of occasions reiterated his desire for a production freeze over a cut. We’ll no doubt have plenty of headlines over the next couple of days leading into the meeting. Although this is the big event of the trading week, it is worth noting also that this time next week we should likely know the results of the Italian referendum with voting ending at 10pm GMT/11pm CET. There’s some suggestion that exit polls will also be released by several TV networks just after this time while the actual vote counting is expected to take a few hours.

Also worth highlighting this morning is some of the early retail sales stats from Black Friday in the US. According to the National Retail Federation, shoppers were said to have spent on average $289.19 over the four-day weekend period if you include both purchases made online and bricks and mortar sales. That is down from $299.60 in the same period last year. The number of shoppers did however increase with the NRF also reporting that the total number of shoppers increased by 2% to about 154 million consumers. 44% of purchases were said to have been done online, compared to 40% in-store.

Over in markets, despite the tumble for Oil and the subsequent knock on to energy names, it was another broadly positive day for US equities on Friday and another which saw the S&P 500 (+0.39%), Dow (+0.36%), Nasdaq (+0.34%) and Russell 2000 (+0.38%) indices all notch up fresh record highs, with gains for defensive sectors dominating. Volumes were unsurprisingly low in a holiday shorted session, while 10y Treasury yields tempered an early move higher to just north of 2.400% to close little changed around 2.357%. In Europe equity markets also closed in positive territory (Stoxx 600 +0.18%) while rates markets were a touch firmer. 10y Bund yields edged down a couple of basis points to 0.236% to finish just over 3bps lower for the week.

This morning in Asia it’s been a bit more of mixed start to trading to the week. Most notable is the decline for the Nikkei (-0.36%) which has weakened for the first time in eight sessions. That appears to be as a result of the decent rally for the Yen (+1.32%) which, in the absence of any material news, appears to be strengthening on technical factors more than anything else, with the Greenback also lower versus most EM currencies this morning. The ASX (-0.59%) is also weaker but the Hang Seng (+0.71%), Shanghai Comp (+0.51%) and Kospi (+0.36%) are all up. Bourses in China appear to have been boosted by the October industrial profits data which was released yesterday. It showed profits as climbing +9.8% yoy in October, up from +7.7% in the month prior.

Wrapping up the data on Friday. In the US the advance goods trade balance for October revealed a slight widening in the deficit to $62bn from $56.5bn after data showed that imports rose +1.1% mom during the month and exports fell -2.7%. Meanwhile wholesale inventories were down unexpectedly in October (-0.4% mom vs. +0.2% expected), while the flash services PMI for November was down a very modest 0.1pts to 54.7, which when combined with the manufacturing reading, has left the composite at 54.9. Following last week’s data the NY Fed subsequently revised up their Q4 GDP forecast to 2.5% from 2.4%. The Atlanta Fed continue to forecast for a much greater 3.6% growth rate meanwhile.

Over in Europe much of the data was focused in the UK. There was no surprise from the second reading of Q3 GDP which came in unchanged at +0.5% qoq and +2.3% yoy. The details of the report showed that a slightly lower than expected increase in exports was more than offset by a positive contribution from government spending and decrease in imports. Perhaps the more interesting data however was the CBI distributive trends survey in the UK. The survey showed retail sales volume of +26 in November versus +21 on October, far exceeding expectations for +12. In fact it is the highest print since September 2015 and evidence that the big decline for Sterling is keeping consumer spending buoyant.

Turning over to the week ahead now. It’s a fairly quiet start to the week today. In Europe we’ll get the latest M3 money supply data for the Euro along with the latest OECD economic outlook while in the US the sole release is the Dallas Fed’s manufacturing survey. Tuesday kicks off early in Japan with the latest jobless rate, retail sales and household spending data. Closer to home we’ll get Q3 GDP in France, Germany CPI for November, UK money and credit aggregates data and also the latest confidence indicators for the Euro area. In the US tomorrow all eyes are on the second revision to Q3 GDP while the November consumer confidence print is also due out, along with the latest S&P/Case-Shiller house price index. We start in Japan again on Wednesday where the latest industrial production data is due, along with housing starts data. China will also release the MNI consumer sentiment reading while the UK will release its latest consumer confidence print. During the European session we’ll get the latest CPI print out of France and also the Euro area, along with unemployment data in Germany. There’s important data in the US on Wednesday too with the ADP employment change print, personal income and spending reports for October and also the PCE core and deflator readings for last month too. Pending home sales data and the Chicago PMI will also be released followed by the Fed’s Beige Book in the evening. Turning to Thursday, China will get things going with the November PMI data, while during the European session we’ll also get the manufacturing PMI’s including a first look at the data for the UK and the periphery. In the US it’s another busy session with initial jobless claims, manufacturing PMI, construction spending, ISM manufacturing and vehicles sales data all due out. It’s a quiet end to the week in Asia and Europe on Friday with PPI data for the Euro area the sole release. In the US it’s all eyes on the November employment report including the latest payrolls print.

Away from the data, in terms of Fedspeak this week we’ve got Dudley and Powell due to speak tomorrow, Kaplan and Powell on Wednesday, Kaplan again on Thursday and Brainard on Friday. In Europe today we’ll hear from ECB President Draghi this afternoon at European Parliament, while Coeure will also speak before him. Draghi will then speak again on Wednesday. The BoE will also publish its Financial Stability Report on Wednesday with BoE Governor Carney due to speak after. The other big event this week and which may end up being the focus for the week is the aforementioned OPEC meeting in Vienna on Wednesday where ministers are due to discuss finalizing the September accord to curb oil production

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 15.06 POINTS OR 0.46%/ /Hang Sang closed UP 107.12 OR 0.47%. The Nikkei closed DOWN 24.33 OR .13%/Australia’s all ordinaires CLOSED DOWN 0.68% /Chinese yuan (ONSHORE) closed UP at 6.912/Oil ROSE to 46.33 dollars per barrel for WTI and 47.66 for Brent. Stocks in Europe: ALL IN THE RED Offshore yuan trades 6.9360 yuan to the dollar vs 6.9120 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS AS MORE USA DOLLARS ATTEMPT TO LEAVE CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

b) REPORT ON JAPAN

c) Report on CHINA

The Market’s Next Headache: China’s (Not So) Stealth Tightening

While much of the attention in the past month has focused on the rising interest rates among the Developed markets, a just as troubling development is taking place in China where as BofA’s David Cui observes, interest rates are set for sustained upward pressure over the next few quarters, for the fifth time since 2006.

Since Oct 21, yield of 10Y Chinese Government Bond (CGB) has risen by 20bps, from 2.65% to 2.85%, partly in response to the strong global rates and USD move since the US election. Cui expects the yield to rise further to 3.40% by the end of 2017. Furthermore, with credit spreads near all-time lows, the bank warns that there is a risk that it may widen sharply at some point.

As Cui further writes, the local equity market reacted progressively less favorably to rising rates the last four times as investors turned progressively less optimistic about growth outlook. The bank believes that “the rising rates this time may put pressure on equities in general as it would occur in an environment of lackluster growth.” Sector wise, property, materials and utilities may suffer the most; while insurers, IT and consumer may benefit. That said, please bear in mind that interest rate is only one of the major drivers of the equity market.

To be sure, how the equity market reacts to rising rate depends on reasons behind the upward pressure. If it is caused by strong economic growth outlook, it is typically good for stocks, at least in the early stage of the tightening cycle (when the market tends to enjoy upside revenue surprise). This was clearly the case with Episodes 1 and 2 (Chart 6).

However, when rising rate was caused by no-growth factors, such as inflation and the government’s desire to control debt growth (which seemed to be the case with Episodes 3 and 4), the market reacted much more cautiously. This time, the pressure appears to be mainly driven by a less accommodating monetary policy as a result of housing bubble risk, debt control need and exchange rate pressure, despite a fairly lackluster economic growth outlook. In this case, Cui concludes, “the rising rate should not be a net positive to the equity market, in our view.”

What makes China’s situation especially curious, because the implications from higher rates for a country which has a record corporate debt bubble are pernicious, is that while market forces have already tightened financial conditions as a result of recent developments in the US, this move has not only not been offset by the PBOC, but has been blessed by the Chinese central bank: as Bloomberg writes overnight, “without a policy announcement, China’s central bank has effectively tightened monetary conditions in recent weeks, an analysis of its transactions shows.”

The PBOC has quietly tightened by gradually shifting the maturity distribution of repo operations away from 7-Day toward 14- and 28-day operations, which both have modestly higher rates. Specifically, in recent weeks, the PBOC has cut back on seven-day open-market operations and is instead injecting more funds through 14-day and 28-day contracts. That’s had the effect of raising short-term borrowing costs and pressing up bond yields.

While the central bank injects money with seven-day reverse repurchase operations at 2.25%, it has started offering 14-day and 28-day contracts at rates as much as 30 basis points higher. The end result is secondary market one-week funding costs of around 2.5%. According to Bloomberg, this is another sign of selective tightening by the PBOC that’s reinforced the views of many economists that China has turned the corner away from monetary stimulus.

A breakdown of recent repo operations is shown below:

As a result, interbank rates have “basically gone up 20 to 30 basis points,” said Ming Ming, the head of fixed-income research at Citic Securities Co. and an ex-PBOC official. “China’s central bank has essentially raised rates by 25 basis points through money market operations,” said Deng Haiqing, chief economist at JZ Securities Co. in Beijing. “The bond market adjustment is only beginning. We expect the yield curve steepening to be the main feature of the market in 2017, driven by mild PBOC tightening.”

Why the quiet shift? One explanation is that with economic growth stable, policy makers are trying to rein in leverage in the world’s No. 2 economy. The impact is being felt in the debt market, where the government yield curve has reached the steepest since April and the yield premium on three-year AAA corporate bonds is set for the biggest jump in seven months.