Gold at (1:30 am est) $1150.0 DOWN $6.40

silver at $15.94: DOWN 22 cents

Access market prices:

Gold: $1151.80

Silver: $15.96

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

FRIDAY gold fix Shanghai

Shanghai morning fix Dec 30 (10:15 pm est last night): $ 1177.86

NY ACCESS PRICE: $1159.25 (AT THE EXACT SAME TIME)/premium $18.61

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1177.76

NY ACCESS PRICE: $1159.95 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $17.91

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Dec 30: 5:30 am est: $.1159.10 (NY: same time: $1159.85 5:30AM)

London Second fix Dec 30: 10 am est: $1145.80 (NY same time: $1159.90 ??? 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 133 NOTICE(S) FOR 13,300 OZ. TOTAL NOTICES SO FAR: 133 FOR 13,300 OZ (.413 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 195 NOTICE(s) FOR 975,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 195 FOR 975,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 858 contracts UP to 164,401 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .823 BILLION TO BE EXACT or 118% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 195 NOTICES FILED FOR 990,000 OZ.

In gold, the total comex gold ROSE BY 10,244 contracts WITH THE RISE IN THE PRICE GOLD ($17.00 with YESTERDAY’S trading ).The total gold OI stands at 415,510 contracts.

we had 133 notice(s) filed upon for 13300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD,

Inventory rests tonight: 823.36 tonnes

.

SLV

we had n0 changes in silver into the SLV

THE SLV Inventory rests at: 341.348 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver ROSE by 858 contracts UP to 164,401 as the price of silver ROSE by $0.17 with YESTERDAY’S trading. The gold open interest ROSE by 10,244 contracts UP to 415,510 as the price of gold ROSE BY $17.00 WITH YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 7.59 POINTS OR 0.24%/ /Hang Sang closed UP 209.65 OR .96%. The Nikkei closed DOWN 30.77 OR 0.16% /Australia’s all ordinaires CLOSED DOWN 0.48%/Chinese yuan (ONSHORE) closed UP at 6.9440/Oil FELL to 53.76 dollars per barrel for WTI and 56.61 for Brent. Stocks in Europe: ALL IN THE RED EXCEPT LONDON . Offshore yuan trades 6.9682 yuan to the dollar vs 6.9440 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES /

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

A terrific commentary tonight from Meijer on the hard choices China must make:

i) devalue and face the wrath of the west and wipe out much of the savings of the Chinese people

ii) stringent capital controls and with it social unrest

pick your poison, China

a must read..

( Raul Meijer)

4 EUROPEAN AFFAIRS

i)The cost so far to rescue Paschi is 6.6 billion euros. Trust me it is going to escalate: the problem will be contagion of other banks and the 2.2 billion euros of bail in to be borne by institutions. Plus they have to deal with Germany:

( Bloomberg)

ii)I am speechless!! Totally insolvent Monte dei Paschi plans on issuing 15 billion in debt for 2017. Who in the right frame of mind will buy this junk?

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Lavrov recommends Putin that 35 USA diplomats should be expelled after the USA expelled 35 of its diplomats

( zero hedge)

ii)Putin takes the high road as we states: “we will not expel anyone, we refuse to sink to Obama’s level”

Putin continues to act like a true statesman!

( zero hedge)

iii)The Syrian ceasefire is holding much to the anger of the USA

( zero hedge)

6.GLOBAL ISSUES

7. OIL ISSUES

The following 5 countries can increase production which will threaten the OPEC unity

( Rizvi/OilPrice.com)

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)This is interesting: Trump’s pick for budget chief (same position held by David Stockman) likes gold:

( Bloomberg/GATA)

ii)This was brought to your attention yesterday but it is worth repeating: China expands her forex basket in order to dilute the role of the dollar:

( Times of India/GATA)

iii)It seems that gold is luring investors who are worried about trade wars and of course Trump’s famous tweets:

iv) Why investors are hoarding gold and the problems they face:(courtesy Schmid/EpochTimes of NY)

10.USA STORIES

i)The “hard” data seems to be correct and the soft data wrong as the Chicago’s Purchasing Managers report showed the index sliding from 57.6 down to 54.6 as the indicators seem to suggest that the economy is slowing down: it seems that inflation is picking up against a background of no growth or in other words: stagflation

( zero hedge)

ii)This does not look good for world growth: Apple cutting iphone production by 10% in the first quarter of 2017:

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 10,244 CONTRACTS UP to an OI level of 415,510 AS THE PRICE OF GOLD ROSE $17.00 with YESTERDAY’S trading.It sure looks like we had considerable short covering as the banks did not supply as much paper shorts as I thought they would. We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year. Today is first day notice for the non active January contract month

With January we had a loss of 141 contracts down to 1143. For the next big active delivery month of February we had a GAIN of 7107 contracts UP to 279,825.

We had 195 notice(s) filed upon today for 99000 oz

And now for the wild silver comex results. Total silver OI ROSE by 858 contracts FROM 163,543 up to 164,401 as the price of silver ROSE BY $0.17 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI FELL by 0 contracts REMAINING AT 758. The next non active month of February saw the OI rise by 6 contracts up to 105.

The next big active delivery month is March and here the OI ROSE by 691 contracts UP to 134,078 contracts.

We had 195 notices filed for 990,000 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 75,603 contracts which is awful.

Yesterday’s confirmed volume was 168,022 contracts which is fair

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

52,243.75 oz

International services of Delaware

(1625 kilobars)

|

| No of oz served (contracts) today |

133 notice(s)

13,300 oz

|

| No of oz to be served (notices) |

1010 contracts

101,000 oz

|

| Total monthly oz gold served (contracts) so far this month |

133 notices

13,300 oz

.4136 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,475,021.1 oz |

For January:

Today, 0 notice(s) were issued from JPMorgan dealer account and 401 notices were issued from their client or customer account. The total of all issuance by all participants equates to 133 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

1,023.55 0z

Scotia

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

195 CONTRACT(S)

(990,000 OZ)

|

| No of oz to be served (notices) |

563 contracts

(2,815,000 oz)

|

| Total monthly oz silver served (contracts) | 990 contracts (990,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,751,191.9 oz |

end

At 3:30 pm we received the COT report which gives position levels of our major players in gold and silver

First gold:

| COT Gold, Silver and US Dollar Index Report – December 30, 2016 |

— Published: Friday, 30 December 2016 | Print | Disqus

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 84,330 | 25,419 | 11,309 | 41,974 | 115,981 | |

| 801 | 2,784 | 1,513 | -123 | -64 | |

| Traders | |||||

| 100 | 40 | 38 | 30 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 163,097 | Long | Short | |

| 25,484 | 10,388 | 137,613 | 152,709 | ||

| 1,209 | -833 | 3,400 | 2,191 | 4,233 | |

| non reportable positions | Positions as of: | 145 | 102 | ||

| Tuesday, December 27, 2016 | © SilverSeek.com | ||||

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver stories for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE

Holiday will be back tomorrow

end

As I have pointed out to you throughout the year, JPMorgan dealer has accumulated a huge amount of gold throughout the 2016 yr. The totals: 31 tonnes or 996,650 oz of gold. Avery Goodman believes that the end game is being played out and JPMorgan has loaded up in gold. Avery Goodman did not comment on JPMorgan’s huge 1/2 billion oz of silver accumulation!

(courtesy Avery Goodman/seeking alpha)

JP MORGAN GOBBLES UP A MINIMUM OF OVER 31 TONS (POSSIBLY UP TO 186 TONS!) OF PHYSICAL GOLD!

Avery Goodman

Back in August 2015, I noted that Goldman Sachs and HSBC had taken delivery of a huge tonnage of physical gold, probably purchased near the lows. Physical bars of gold are, by definition, a very long term investment in the yellow metal. At the time, the two banks were telling clients and others not to buy gold, even as they were loading up on it, themselves.

Let’s fast forward…

Starting in December 2015, JP Morgan began buying tremendous quantities of physical gold, as opposed to paper/electronic gold futures, forwards, ETF certificates etc. From December 1, 2015 to December 29, 2016, the big bank purchased and took physical delivery of over 31 metric tonnes worth of bars of the yellow metal for its house account at COMEX alone.

In other words, it now has a physical gold pile which, at minimum, is worth over $1.1 billion at $1,140 per troy ounce, and it is an asset of the corporate bank. By May, 2016, unlike the actions of GS and HSBC in buying while advising clients to sell, analysts at JP Morgan were beginning to encourage customers to buy gold also. Let me repeat that the enormous purchase of 31+ tonnes of physical gold occurred at New York’s COMEX exchange.

The so-called “OTC” gold market in London is five times larger than the gold market in New York City, and if they were buying at COMEX, they were probably buying in London also. The problem with London is that the “LBMA” is not a formal exchange with disclosure rules and regulatory oversight. It is simply an informal collection of banks who operate by agreeing to a common set of rules of engagement. Transactions are secret.

We will never know how much physical gold has been purchased in London by JP Morgan, HSBC, Goldman Sachs or anyone else. However, if JPM’s purchases happen to be synchronized to market size, with New York’s COMEX, they will have purchased another 155 metric tons, for a total of 186 tonnes of gold. Either way, JPM is now in the realm of a sovereign sized gold holdings. Most countries hold less than 31 tonnes of gold. Only a handful own more than 186 tonnes.

Why would a commercial bank, like JPM, make such a huge investment in physical gold bars? Is it just opportunism? Do they know that gold prices are going to rise dramatically? Do they know this because, as many have alleged, they are the key or one of the key gold manipulators? Fun to say but it makes no sense. JPM may or may not be a gold manipulator. It doesn’t matter with respect to this question.

If the idea is simply to mint a quick paper profit, as is usual for market manipulators, there is no good reason to choose physical gold. Shares of GLD, other ETFs, gold futures contracts, and mining company shares are more efficient investment avenues if the question of being able to get your hands on something that is real doesn’t come up. In fact, all the big banks, including JPM have bought significant stakes in various gold mining companies over the last 2 years. However, why spend money to store and insure physical bars of gold when it is more efficient to mint a quick profit by buying more mining company shares? It seems to me that something bigger must be going on.

JP Morgan is the US Treasury’s most important proxy in financial markets. Only it’s top management could have authorized this type of enormous investment in physical gold because it is not something that traders can use. Top JPM management knows a lot more about the inside story about what is going on, behind the scenes, than we know. Is something big about to happen that will dramatically raise the value of real physical gold bars, above more convenient forms of gold ownership?

I can think of only two scenarios that would make a large pile of physical gold bars the best corporate investment for a big bank (as opposed to its customers). One scenario is that JP Morgan knows we have reached the end game and are on the cusp of the long anticipated collapse of the synthetic gold market (ie: gold futures, forwards, “unallocated” storage, maybe GLD etc.). If the gold derivatives market collapses, people will accept only physical gold for a very long time afterward. That would make a physical gold hoard far more profitable than even shares of a mining company. Remember, it takes time to mine more gold. But, the holder of a huge pile of bars can sell them, right away, at the very top of the market, when demand (and prices) are at their highest.

Another scenario is that we are on the cusp of a massive change in the world’s monetary system. If JP Morgan knows that physical gold is going to be a key part of what replaces the US dollar as the international standard of exchange, it would make perfect sense to buy physical gold. Again, the holder would be in a perfect position to sell the gold bars to third parties (mainly, I suppose, other banks) at the top of the market.

Perhaps, someone else has more ideas?

-END-

This is interesting: Trump’s pick for budget chief (same position held by David Stockman) likes gold:

(courtesy Bloomberg/GATA)

Trump’s pick for budget chief liked gold, had dim view of dollar

Submitted by cpowell on Thu, 2016-12-29 14:46. Section: Daily Dispatches

It will be a rare politician who still likes gold AFTER coming to power.

* * *

By Noah Buhayar

Bloomberg News

Thursday, December 29, 2016

President-elect Donald Trump’s pick for budget chief, Mick Mulvaney, has been an active investor in gold and gold-mining stocks, often seen as a hedge against collapsing currency.

The South Carolina Republican congressman has accused the Federal Reserve of debasing the value of the greenback and has praised bitcoin, an alternative currency. He held between $50,000 and $100,000 in precious metals as of the end of 2015, filings show.

Now, as Trump’s nominee to run the Office of Management and Budget, Mulvaney, 49, is poised to influence U.S. fiscal policy. As director of OMB, he would help the president set government spending and could end up working on an overhaul of the federal tax code. At least one other member of Congress appointed by Trump to a cabinet-level position, Rep. Tom Price, also has a history of trading stocks while in office.

Mulvaney’s investments in mining companies date to at least 2010, the year he was elected to the House of Representatives as part of the Republican Tea Party wave. A filing detailing his holdings at the end of that year shows he and family members owned stocks and funds of gold- and silver-mining companies — including Eldorado Gold Corp., Agnico Eagle Mines Ltd., and Pan American Silver Corp. — with a total value of between $252,000 and $855,000. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2016-12-29/trump-s-pick-for-budg…

END

This was brought to your attention yesterday but it is worth repeating: China expands her forex basket in order to dilute the role of the dollar:

(courtesy Times of India/GATA)

China expands forex basket to dilute role of dollar

Submitted by cpowell on Fri, 2016-12-30 01:59. Section: Daily Dispatches

From Agence France-Presse

via The Times of India, Mumbai

Thursday, December 29, 2016

BEIJING — China said Thursday it would almost double the number of foreign currencies it uses to determine the official value of the yuan, thereby diluting the role of the dollar.

The move to expand the foreign exchange basket used to set a daily reference rate for the yuan, or renminbi, will help Beijing shake off the weakness of the currency against the greenback and project an image of stability in the unit.

The dollar will see its prominence in the basket dented by the newcomers, with its share falling from 26.4 percent to 22.4 percent. It is followed by the euro at 16.34 percent.

Among the 11 currencies to join the 13 existing ones are the South Korean won, the South African rand, the Hungarian forint, the Turkish lira, and the Polish zloty, according to the Chinese Foreign Exchange Trade System, which is run by the central bank. …

The expansion is designed to “strengthen the representativeness” of the basket and will come into force on January 1, it added. …

… For the remainder of the report:

http://economictimes.indiatimes.com/news/international/business/china-ex…

Gold lures investors worried about trade wars and Trump tweets

Submitted by cpowell on Fri, 2016-12-30 02:06. Section: Daily Dispatches

By Eddie Van Der Walt, Luzi-Ann Javier, and Ranjeetha Pakiam

Bloomberg News

Thursday, December 29, 2016

The Donald J. Trump era is marking a new age for gold as an investor safe haven.

While the precious metal has always been hoarded in times of trouble, a bevy of political and economic surprises in 2016 sparked a surge in buying that sent bullion to the first annual gain in four years. Prices may rally 13 percent in 2017, almost double this year’s advance, according to a Bloomberg survey of 26 analysts.

Fueling the bullish outlook is the risk of chaos on multiple fronts: a possible trade war from America’s fraying relationship with China, the alleged Russian hack of U.S. political parties, the U.K.’s complicated exit from the European Union, and elections slated in France, Germany, and the Netherlands that may see a rise of nationalist groups. And then there are Trump’s frequent Twitter posts, in which the U.S. president-elect feuded with rivals and made declarations that unsettled allies even before he takes office Jan. 20.

“One hundred forty characters of unfiltered Trump are likely to create tensions with America’s largest trading partners,” Mark O’Byrne, a director at broker GoldCore Ltd. in Dublin, said by e-mail. “Markets that are already shaken by the fallout from Brexit, the coming elections in Europe, and indeed the increasing specter of cyber warfare could again see a safe-haven bid.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2016-12-29/trump-twitter-age-bri…

END

Why investors are hoarding gold and the problems they face:

(courtesy Schmid/EpochTimes of NY)

Getting gold back into the system with a market-based interest rate on gold

Submitted by cpowell on Fri, 2016-12-30 02:13. Section: Daily Dispatches

By Valentin Schmid

The Epoch Times, New York

Thursday, December 29, 2016

There are people who think the financial system based on the dollar will collapse sooner rather than later. For this event, they are hoarding gold, silver, and sometimes guns and canned food.

“If people lose confidence in the other forms of money, they’ll go to gold,” said James Rickards, author of “The New Case for Gold.”

“Sometimes gold rallies because it’s an inflation hedge, which it is, but gold can also be a deflation hedge. But most importantly gold is money, and when I see the dollar price of gold going up in this environment, it tells me that people are losing confidence in central banks, thinking of gold as money, thinking they want to allocate part of their portfolio not to dollars, or yen, or euros, or yuan, but to gold.” Rickards recommends a 10 percent allocation to physical gold to protect the investor from extreme economic risk.

The problem with this strategy is that hoarding gold outside the financial system in safe-deposit boxes, or by burying it in the back yard, is akin to taking your chips off the poker table and going home. You are not participating in the economic game anymore.

Keith Weiner, CEO of Monetary Metals, wants to fix this. Similar to Rickards, he recognizes the weaknesses in the fiat-based monetary system, like close-to-zero interest rates for savers and too much debt. He also recommends that people hold a certain amount of gold. …

… For the remainder of the report:

http://www.theepochtimes.com/n3/2203217-getting-gold-back-into-the-syste…

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan UP to 6.9440(SMALL REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS A BIT TO 6.9682 / Shanghai bourse CLOSED UP 7.54 POINTS OR 0.24% / HANG SANG CLOSED UP 209.65 OR .96%

2. Nikkei closed DOWN 30.77 OR 0.16% /USA: YEN RISES TO 116.98

3. Europe stocks opened ALL IN THE RED EXCEPT LONDON ( /USA dollar index FALLS TO 102.22/Euro UP to 1.0547

3b Japan 10 year bond yield: RISES TO +.046%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 116.98/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.76 and Brent: 56.61

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES TO +196.%/Italian 10 yr bond yield FALLS 2 full basis points to .180%

3j Greek 10 year bond yield RISES to : 7.15%

3k Gold at $1157.60/silver $16.18(8:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 90/100 in roubles/dollar) 61.12-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a SMALL REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 116.98 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0185 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0743 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.196%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.474% early this morning. Thirty year rate at 3.084% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Set To End Turbulent 2016 On Mixed Note Following Dollar Flash Crash

Aside from the previously noted FX fireworks early in the illiquid Asian session, which saw the US Dollar “flash crash” briefly against most pairs, including the Euro and the Swiss Franc…

… only to gradually recover most if not all losses, it has been a generally quiet session, as markets look to close out 2016 in orderly fashion. The MSCI World Index was flat on Friday, with investors having booked profits off the benchmark’s 13% run since end-June and European shares opening a touch weaker. It was poised to end the year 5.7% higher despite a rough start and the worst January for stocks in history.

Global markets have fared surprisingly well in a year marked by major political shocks, including June’s Brexit vote and the unexpected election of Donald Trump as U.S. president in November. U.S. stocks have hit successive record highs and emerging equities have rebounded 8 percent after three years in the red. As a result, global stocks are set to close out the tumultuous 2013 with the biggest gain since 2013, ironically even as Japan’s benchmark Topix index and the Stoxx Europe 600 Index were set for the first yearly decline since 2011. Oil headed for its first annual climb in three years. A gauge of the dollar shifted lower after reaching the highest level in more than a decade earlier this week.

Quickly looking back at the year that was, equities posted a resilient recovery after tumbling at the start of the year. Political risk punctuated the calendar, with Britain’s vote in June to leave the European Union presageing Donald Trump’s victory over Hillary Clinton in November. As Bloomberg adds, the year for financial assets started on a sour note from the first day of trading, with the MSCI World gauge tumbling 2 percent. China-fueled turmoil sent stock markets from Tokyo to India into bear markets in the first two months of 2016. Oil reached a 13-year low while the dollar slid to its weakest level in a year. The second half of the year surprised many analysts, as financial markets powered past the Brexit shock while Donald Trump’s presidential victory provided an unexpected boost.

Ironically, every major political catalyst that had been dubbed a material market risk, materialized and the result was a surge in risk assets as markets no longer respond negatively to any adverse news flow courtesy of central bank promises to prop and support global “markets.”

“2016 was perhaps one of the biggest roller-coasters driven by political events,” said Dmitri Petrov, a strategist at Nomura International Plc in London. “It’s not so much the actual realized volatility of asset markets, but volatility of market view around the global macro and policy outlook that made it exceptional.”

The yield on 10-year Treasury notes was little changed at 2.48 percent after dropping three basis points Thursday. It slid to 2.46 percent earlier in the week, the lowest since Dec. 14. U.K. gilts fell with the 10-year yield climbing 2 basis points to 1.257 percent. Yields are still on course for their first monthly decline since August.

Looking at other asset classes, Brent crude futures have bounced more than 50 percent after three years of losses, thanks to output cuts by key crude producers. The benchmark rose half a cent on Friday. Other commodities too have rallied, with zinc, steel and rubber posting annual gains of around 60 percent after suffering heavy losses last year.

In a note headlined, “The underdogs bite back”, asset manager Schroders said government bonds were the only major asset class not to have delivered positive returns in 2016, with equities and commodities receiving a boost from President-elect Trump’s $1 trillion economic stimulus plan.

“Investors have bought into the Trump or reflation trade on hopes of stronger growth, rising inflation and higher interest rates. Risk assets are rallying, the dollar has strengthened and capital has flowed out of emerging markets,” Schroders told clients.

The year is also notable for the growing chorus of voices calling an end to the three-decade bond bull run. With inflation on the rise, U.S. 10-year yields have hit two-year highs US10YT=RR and the European Central Bank has signaled it will start trimming bond purchases.

The dollar pulled back 0.3 percent on Friday against a currency basket following its early “flash crash” but has strengthened in 2016 for the third straight year, recently hitting near 14-year highs. Britain’s pound, which hit 31-year lows after the June 23 vote to leave the European Union, is closing 16 percent lower against the dollar, its biggest yearly fall since 2008. Most analysts expect the greenback to rise further in 2017, along with U.S. Treasury yields, with Trump’s policies seen boosting inflation and prompting the U.S. Federal Reserve to hike interest rates more frequently. The euro, however, has fought back this week, rising to three-week highs versus the dollar, though the widening interest rate gap with the United States has seen it fall 3 percent this year.

The single currency faces some key tests in 2017, with Dutch, French and German elections expected to see a lurch toward anti-establishment, anti-euro parties while concerns remain over the health of Italian banks.

“Political risk shifts to Europe in 2017 with the risk of an upset in France or Italy potentially threatening a break-up of the euro,” Schroders wrote.

The other major risk on the horizon could be China, where the yuan has posted its biggest annual loss against the dollar since 1994 when it started trading. Fears are growing that capital outflows will spiral out of control, further weakening the currency, depleting foreign exchange reserves and possibly raising debt default rates.

Market Snapshot

- S&P 500 futures up 0.2% to 2250

- Stoxx 600 down 0.3% to 359

- FTSE 100 down 0.3% to 7098

- DAX down 0.2% to 11431

- German 10Yr yield up 2bps to 0.19%

- Italian 10Yr yield up less than 1bp to 1.8%

- Spanish 10Yr yield up 1bp to 1.34%

- S&P GSCI Index up 0.3% to 399.6

- MSCI Asia Pacific up 0.1% to 135

- Nikkei 225 down 0.2% to 19114

- Hang Seng up 1% to 22001

- Shanghai Composite up 0.2% to 3104

- S&P/ASX 200 down 0.6% to 5666

- US 10-yr yield up less than 1bp to 2.48%

- Dollar Index down 0.62% to 102.04

- WTI Crude futures up 0.4% to $53.96

- Brent Futures up 0.3% to $57.03

- Gold spot up 0.2% to $1,160

- Silver spot up 0.5% to $16.24

Top Global News

- Trump Left a Tough Choice by Obama Sanctions on Russian Hacking: Obama imposed penalties on Russian intelligence officials and agencis, expelling 35 Russian operatives

- Qualcomm to Gain Fees From China’s Meizu in Lawsuit Settlement: Meizu will pay patent fees similar to those accepted by other Chinese phone makers

- Nomura to Deepen Cost Cuts as CEO Seeks to Keep Ship Afloat: CEO Nagai unveiled “Waterline Project” seeking to improve cost-effectiveness over the next three years

- NBCUniversal Says Channels May Go Dark in Charter Cable Dispute: Charter has been “unyielding” in demanding better terms, NBC says

- Oil Market Seen as Surprise Haven From Political Risk in 2017: OPEC output cut creates capacity to respond to supply outages

- Euro Jumps 1.6 Percent in Minutes as Algo Orders Surprise Market: Liquidity evaporated as euro buy orders surged above $1.05, currency pares gains

- Grab Your Ear Muffs, the New Year’s Arriving With a Frigid Bang: Warmer Arctic weather will spur a very chilly start to 2017

- China to Boost Coal Output Amid Capacity Cuts in 5-Year Plan: Coal output will increase to 3.9 billion metric tons in 2020, about 18% higher than this year

- Wall Street’s Trump Bonanza Won’t Avert Job Cuts at Banks in ’17: Even if profits surge, analysts say banks will keep automating

In Asia, stocks edged just barely higher with the MSCI Asia Pacific up 0.1%, while Japan’s Topix index caps its first annual retreat since 2011. 6 out of 11 MSCI Asia Pacific sectors rise, with health care outperforming and industrials underperforming.

Top Asian News

- Hong Kong Parking Garage May Fetch $2.2 Billion in 2017 Sale: First commercial land sale in central business district in more than 20 years

- Fairfax Wins Central Bank’s Approval to Take Over Indian Lender: Approval to buy 51% stake in Catholic Syrian Bank

- Japan Wants Its Overworked Citizens to Start Weekends Early: The country wants companies to let workers finish early on the last Friday of every month

In Europe, stocks are ending the year in a subdued fashion, falling fractionally some 0.3% in thin trading, and poised to end the year with the first annual decline since 2011. 17 out of 19 Stoxx 600 sectors decline, with real estate and household goods outperforming, oil & gas underperforming. 70% of Stoxx 600 members decline, 27% gain

Top European News

- Bank of Italy Says Paschi Rescue Will Cost State $6.9 Billion: Bank of Italy makes estimates in note posted on website

- Fiat Said to Be Developing Autonomous Vehicle: The Information: Report says co. already has prototype vehicles on the road

In commodities, the Bloomberg Commodity Index, which measures returns on raw materials, rallied 0.3 percent, putting it on course for a 12 percent advance. This would be the first increase since 2010. Crude futures gained 0.5 percent to $54.01 a barrel, after Thursday’s 0.5 percent decline. Prices are up about 46 percent this year. Supply cuts from OPEC and other producing nations next month are intended to stabilize the market and reduce swelling global inventories. Gold’s 0.2 percent advance to $1,160.55 an ounce extended its rally into a fifth day, the longest since Nov. 4. The metal has rebounded 3.3 percent from an 11-month low, and is up more than 9 percent for the year.

In currencies, the euro rallied as much as 1.6 percent before paring its advance to 0.7 percent and trading at $1.0566 as of 10:38 a.m. in London. The yen fell 0.3 percent to 116.8 per dollar, erasing an earlier advance of 0.4 percent. The currency was up more than 20 percent for the year in August, but has pared that to 2.9 percent. The Bloomberg Dollar Spot Index slipped 0.4 percent after dropping 0.5 percent Thursday, although it remains up 2.7 percent for the year. The pound was on track for a monthly decline versus the dollar, its ninth this year and wrapping up its steepest annual drop since the global financial crisis of 2008. Sterling was on track for a more than 16 percent drop against the dollar this year and was the worst performing Group-of-10 currency in 2016 despite the recent stabilization.

US event calendar:

- 9:45am: Chicago Purchasing Manager, Dec., est. 56.8 (prior 57.6)

- 1pm: Baker Hughes rig count

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 7.59 POINTS OR 0.24%/ /Hang Sang closed UP 209.65 OR .96%. The Nikkei closed DOWN 30.77 OR 0.16% /Australia’s all ordinaires CLOSED DOWN 0.48%/Chinese yuan (ONSHORE) closed UP at 6.9440/Oil FELL to 53.76 dollars per barrel for WTI and 56.61 for Brent. Stocks in Europe: ALL IN THE RED EXCEPT LONDON . Offshore yuan trades 6.9682 yuan to the dollar vs 6.9440 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES /

3a)THAILAND/SOUTH KOREA/:

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

A terrific commentary from Meijer on the hard choices China must make:

i) devalue and face the wrath of the west and wipe out much of the savings of the Chinese people

ii) stringent capital controls and with it social unrest

pick your poison, China

a must read..

(courtesy Raul Meijer)

China Hits A Fork In The Road

Submitted by Raul Ilargi Meijer via The Automatic Earth blog,

The end of the year is always a time when there are currency and liquidity issues in China. This has to do with things like taxes being paid, and bonuses for workers etc. So it’s not a great surprise that the same happens in 2016 too. Then again, the overnight repo rate of 33% on Tuesday was not exactly normal. That indicates something like a black ice interbank market, things that can get costly fast.

I found it amusing to see Bloomberg report that: “As banks become more reluctant to offer cash to other types of institutions, the latter have to turn to the exchange for money, said Xu Hanfei at Guotai Junan Securities in Shanghai. Amusing, because I bet many will instead have turned to the shadow banking system for relief. So much of China’s financial wherewithal is linked to ‘the shadows’ these days, it would make sense for Beijing to bring more of it out into the light of day. Don’t hold your breath.

Tyler on last night’s situation: ..the government crackdown on the credit and housing bubble may be serious for once due to fears about “rising social tensions”, much of the overnight repo rate spike was driven by the PBOC which pulled a net 150 billion yuan of funds in open-market operations..”. And the graph that comes with it:

It all sounds reasonable and explicable, though I’m not sure ‘core leader’ Xi would really want to come down hard on housing -he certainly hasn’t so far-, but there are things that do warrant additional attention. The first has to be that on Sunday January 1 2017, a ‘new round’ of $50,000 per capita permissions to convert yuan into foreign currencies comes into effect. And a lot of Chinese people are set to want to make use of that, fast.

Because there is a lot of talk and a lot of rumors about an impending devaluation. That’s not so strange given the continuing news about increasing outflows and shrinking foreign reserves. And those $50,000 is just the permitted amount. Beyond that, things like real estate purchases abroad, and ‘insurance policies’ bought in Hong Kong, add a lot to the total.

What makes this interesting is that if only 1% of the Chinese population -close to 1.4 billion people- would want to make use of these conversion quota, and most of them would clamor for US dollars, certainly since its post-election rise, if just 1% did that, 14 million times $50,000, or $700 billion, would potentially be converted from yuan to USD. That’s almost 20% of the foreign reserves China has left ($3.12 trillion in October, from $4 trillion in June 2014).

In other words, a blood letting. And of course this is painting with a broad stroke, and it’s hypothetical, but it’s not completely nuts either: it’s just 1% of the people. Make it 2%, and why not, and you’re talking close to 40% of foreign reserves. This means that the devaluation rumors should not be taken too lightly. If things go only a little against Beijing, devaluation may become inevitable soon.

In that regard, a remarkable change seems to be that while China’s always been intent on keeping foreign investment out, now all of a sudden they announce they’re going to sharply reduce restrictions on foreign investment access in 2017. While at the same time restricting mergers and acquisitions by Chinese corporations abroad, in an attempt to keep -more- money from flowing out. Something that has been as unsuccessful as so many other pledges.

The yuan has declined 6.6% in value in 2016 (and 15% since mid-2014), and that’s probably as bad as it gets before some people start calling it an outright devaluation. More downward pressure is certain, through the conversion quota mentioned before. After that, first there’s Trump’s January 20 inauguration, and a week after, on January 27, Chinese Lunar New Year begins.

May you live in exciting times indeed. It might be a busy week in Beijing. As AFP reported at the beginning of December:

Trump has vowed to formally declare China a “currency manipulator” on the first day of his presidency, which would oblige the US Treasury to open negotiations with Beijing on allowing the renminbi to rise.

Sounds good and reasonable too, but how exactly would China go about “allowing the renminbi to rise”? It’s the last thing the currency is inclined to do right now. It would appear it would take very strict capital controls to stop the currency from plunging, and that’s about the last thing Xi is waiting for. For one thing, the hard-fought inclusion in the IMF basket would come under pressure as well. AFP continues:

China charges an average 15.6% tariff on US agricultural imports and 9% on other goods, according to the WTO.

Chinese farm products pay 4.4% and other goods 3.6% when coming into the United States.

China is the United States’ largest trading partner, but America ran a $366 billion deficit with Beijing in goods and services in 2015, up 6.6% on the year before.

I don’t know about you, but I think I can see where Trump is coming from. Opinions may differ, but those tariff differences look as if they belong to another era, as in the era they came from, years ago. Lots of water through the Three Gorges since then. So the first thing the US Treasury will suggest to China on the first available and convenient occasion after January 20 for their legally obligatory talk is: let’s equalize this. What you charge us, we’ll charge you. Call it even and call it a day.

That would both make Chinese products considerably more expensive in the States, and open the Chinese economy to American competition. There are many hundreds of billions of dollars in trade involved. And of course I see all the voices claiming that it will hurt the US more than China and all that, but what would they suggest, then? You can’t leave this tariff gap in place forever, so what do you do?

I’m sure Trump and his team, Wilbur Ross et al, have been looking at this a lot, it’s a biggie, and have a schedule in their heads for phasing out the gap in multiple steps. Steps too steep and short for China, no doubt, but then, I don’t buy the argument that the US should sit still because China owns so much US debt. That’s a double-edged sword if ever there was one, and all hands on the table know it.

If you’re Xi, and you’re halfway realist, you just know that Trump will aim to cut the $366 billion 2015 deficit by at least 50% for 2017, and take it from there. That’s another big chunk of change the core leader stands to lose. And another major pressure point for the yuan, obviously. How Xi would want to avoid devaluation, I don’t know. How he would handle it once it can no longer be avoided, don’t know that either. Trump’s trump card?

One other change in China in 2016 warrants scrutiny. That is, the metamorphosis of many Chinese people from caterpillar savers into butterfly borrowers. Or gamblers, even. It’s one thing to buy units in empty apartment blocks with your savings, but it’s another to buy them with money you borrow. But then, many Chinese still have access to few other investment options. That’s why the $50,000 conversion to USD permission as per January 1 could grow real big.

But in the meantime, many have borrowed to buy real estate. And they’ve been buying into a genuine absolute bubble. It’s not always evident, because prices keep oscillating, but the last move in that wave will be down.

If I were Xi, all these things would keep me up at night. But I’m not him, and I can’t oversee to what extent his mind is still in the ‘omnipotent sphere’, if he still has the impression that in the end, come what may, he’s in total control. In my view, his problem is that he has two bad choices to choose from.

Either he will have to devalue the yuan, and sharply too (to avoid a second round), an option that risks serious problems with Trump and other leaders (IMF), and would take away much of the wealth the Chinese people thought they had built up -ergo: social unrest-.

Either that or he will be forced, if he wants to maintain some stability in the yuan’s valuation, to clamp down domestically with very grave capital controls, which carries the all too obvious risk of, once again, serious social unrest. And which would (re-)isolate the country to such an extent that the entire economic model that lifted the country out of isolation in the first place would be at risk.

This may play out relatively quickly, if for instance sufficient numbers of people (the 1% would do) try to convert their $50,000 allotment of yuan into dollars -and the government is forced to say it doesn’t have enough dollars- But that is hard to oversee from the outside.

There are, for me, too many ‘unknown unknowns’ in this game. But I don’t see it, I don’t see how Xi and his crew will get themselves through this minefield without getting burned. I’m looking for an escape route, but there seem to be none available. Only hard choices. If you come upon a fork in the road, China, don’t take it.

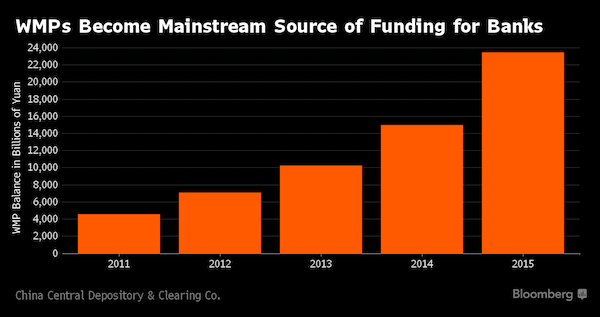

And mind you, this is all without even having touched upon the massive debts incurred by thousands upon thousands of local governments, and the grip that these debts have allowed the shadow banks to get on society, without mentioning the Wealth Management Products and other vehicles in that part of the economy, another ‘industry’ worth trillions of dollars. I mean, just look at the growth rates in these instruments:

There’s simply too much debt all throughout the system, and it’s due for a behemoth restructuring. You look at some of the numbers and graphs, and you wonder: what were they thinking?

end

4 EUROPEAN AFFAIRS

The cost so far to rescue Paschi is 6.6 billion euros. Trust me it is going to escalate: the problem will be contagion of other banks and the 2.2 billion euros of bail in to be borne by institutions. Plus they have to deal with Germany:

(courtesy Bloomberg)

Paschi Rescue to Cost Italy 6.6 Billion Euros, Central Bank Says

byItaly’s rescue of troubled lender Banca Monte dei Paschi di Siena SpA will cost the government about 6.6 billion euros ($7 billion), the country’s central bank says, providing the first official estimate of public funding.

About 4.6 billion euros are needed to meet capital requirements and 2 billion euros would be required to compensate the lender’s retail bondholders, the Bank of Italy said in a statement late Thursday. There also would be an additional 2.2 billion euros of costs borne by institutional investors, the Rome-based institute said.

Italy’s central bank also explained the difference between the figure of 8.8 billion euros requested by the European Central Bank under the so-called “precautionary recapitalization” mechanism and the 5 billion euros that Monte Paschi failed to raise on the market.

The higher amount represents the funds needed for Monte Paschi to maintain sufficient capital ratios as decided in a special meeting of the European Central Bank ’s Supervisory Board, the Bank of Italy said.

The Italian cabinet led by Prime Minister Paolo Gentiloni agreed last week to plow as much as 20 billion euros into Monte Paschi and other banks after Monte Paschi, the world’s oldest lender, was unable to find a new core investor — a key part of the 5 billion-euro plan to raise capital on the market.

In an interview published on Thursday by the financial daily Il Sole 24 Ore, Finance Minister Pier Carlo Padoan criticized the ECB’s Supervisory Board for the lack of clarity regarding the criteria used for its calculations. “In addition to a letter of five lines and three numbers, some explanation would have been useful; opaque moves without an explanation lead people to think that there’s something wrong,” the minister told Sole.

In a statement on Monday, the Siena, Italy-based lender said it received received two letters from the ECB including the request of the new amount to bolster its balance sheet.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Lavrov recommends Putin that 35 USA diplomats should be expelled after the USA expelled 35 of its diplomats

(courtesy zero hedge)

Russia Retaliates: Set To Expel 35 US Diplomats After US Sanctions

Russia warned it would respond proportionally to yesterday’s unprecedented sanctions and diplomatic expulsions unveiled by the Obama administration, and this morning it did just that when Russia’s foreign ministry announced plans to expel 35 U.S. diplomats and ban U.S. diplomatic staff from using a dacha and a warehouse in Moscow in retaliation to Washington’s sanctions, Russian news agencies reported.

Foreign Minister Sergei Lavrov was quoted by the agencies as saying he had proposed the measures to President Vladimir Putin, and said that “we cannot leave such acts unanswered. Reciprocity is part of diplomatic law.”

He called the people in question—31 employees at the U.S. embassy in Moscow and 4 in the U.S. consulate in St Petersburg—“persona non-grata.”

Russian Foreign Minister Sergei Lavrov

Mr. Lavrov also said Americans should be banned from using their vacation home near Moscow.

Other joined Lavrov: additional proposed measures are expected though: Ministry of Foreign Affairs spokeswoman Maria Zakharova wrote on her Facebook page Thursday, “there will be official statements, counter-measures” announced on Friday. Dimitry Peskov, Putin’s press secretary, echoed likewise: “We will certainly response adequately…and it will be determined in line with decisions adopted by the Russian President.”

Peskov warned, “there is no doubt that Russia’s adequate and mirror response will make Washington officials feel very uncomfortable as well.”

Ultimately, it is up to Putin to draft such retaliatory measures.

ABC News had previously reported, citing a US official, that Moscow had ordered the the shutdown of the Anglo-American School of Moscow – chartered by the American, British, and Canadian embassies in Moscow – but a US embassy official in Moscow said the school had not been shuttered. Russia’s foreign ministry also denied the school’s closure.

Nonetheless, as the WSJ notes, the “dispute marks one of the biggest diplomatic confrontations between Washington and Moscow since the end of the Cold War.” President Barack Obama in a statement on what he called a partial response to Russia’s alleged hacks, said the cyberattacks “could only have been directed by the highest levels of the Russian government.”

Russia has denied involvement and Lavrov, as well as millions of Americans, have accused the U.S. of neither having nor showing any evidence.

“The outgoing American administration of Barack Obama, who have accused Russia of all mortal sins and tried to blame us for the failure of its foreign policy initiatives, among other things, has groundlessly made additional accusations that Russia interfered in the U.S. election campaign at the state level,” he said.

The Russian act was in retaliation to sanctions imposed on Thursday by the US on Russian intelligence agencies and expelled what the State Department said were 35 intelligence operatives allegedly serving under diplomatic cover from the Russian embassy in Washington and the Russian consulate in San Francisco.

Shortly after Obama’s announcement, Donald Trump, who has shown a far more amenable side to dealing with Russia, said that “It’s time for our country to move on to bigger and better things” but added that “in the interest of our country and its great people, I will meet with leaders of the intelligence community next week in order to be updated on the facts of this situation.”

We anticipate that despite some potential complications, Trump will gradually overturn Obama’s sanctions as relations between the US and Russia renormalize once Trump is inaugurated in three weeks.

END

Putin takes the high road as we states: “we will not expel anyone, we refuse to sink to Obama’s level”

Putin continues to act like a true statesman!

(courtesy zero hedge)

Putin Stunner: “We Will Not Expel Anyone; We Refuse To Sink To Obama’s Level”

Vladimir the merciful?

Following this morning’s reports that Foreign Minister Sergei Lavrov would recommend to Russian President Vladimir Putin a retaliation in kind, and expel 35 American diplomats, saying that “we cannot leave such acts unanswered. Reciprocity is part of diplomatic law” with Putin spokesman Peskov adding that “there is no doubt that Russia’s adequate and mirror response will make Washington officials feel very uncomfortable as well”, it was ultimately up to Putin to decide how to respond to the US.

Which he did on Friday morning, when in a stunning reversal, the Russian leader took the high road, and in a Kremlin statement said that, contrary to expectations, Russia won’t expel any Americans in retaliation to US moves, in a brutal demonstration of just how irrelevant Obama’s 11th hour decision is for US-Russian relations.

In the statement Putin said that Russia won’t cause problems to U.S. diplomats or deport anyone, adding that Russia has the right to respond in tit-for-tat manner, but it will not engage in irresponsible diplomacy.

The punchline, however, was saved for what may be Russia’s final slam of the debacle that is Obama’s administration saying that “It’s a pity that the current U.S. administration is finishing their work in such a manner” saying that Russia refuses “to sink to the level of this irresponsible “kitchen” diplomacy.”

Putin ended the statement by congratulating U.S. President-elect Donald Trump, and the American people on the New Year and invited the hildren of US diplomats to a holiday celebration at the Kremlin.

From the full statement posted on the Kremlin website:

“We reserve the right to retaliate, but we will not sink to the level of this irresponsible ‘kitchen’ diplomacy. We will take further moves on restoring Russian-American relations based on the policies that the administration of President-elect Donald Trump adopts,”

And with that one statement, Obama lost the diplomatic war with Russia.

end

The Syrian ceasefire is holding much to the anger of the USA

(courtesy zero hedge)

“Potential Breakthrough” – Syrian Ceasefire, Which Snubbed The US, Holds On First Day

In the latest snub to the Obama administration, a nationwide Syrian cease-fire brokered by Russia and Turkey – one which explicitly avoided US participation – went into effect at midnight and was holding steady on Friday despite minor violations, marking what Bloomberg said is “a potential breakthrough in a conflict that has been shredding high-level peace initiatives for over five years.”

And all it took was the absence of the US to bring hope of peace back to Syria.

The Britain-based Syrian Observatory for Human Rights reported clashes early Friday between troops and rebels in the central province of Hama and near the capital, Damascus, but said there have been no reports of civilian casualties since the truce began. The group also reported an aerial attack on the rebel-held Barda Valley near Damascus. Cited by Bloomberg, opposition activist Mazen al-Shami, who is based in the Damascus suburb of Douma, said minor clashes nearby left one rebel wounded. Activist Ahmad al-Masalmeh, in the southern Daraa province, said government forces had opened fire on rebel-held areas.

Several past attempts at halting the fighting have failed. As with previous agreements, the current cease-fire excludes both the al-Qaida-affiliated Fatah al-Sham Front, which fights alongside other rebel factions, and the Islamic State group.

As reported yesterday when news of the unexpected ceasefire, which could lead to a peace treaty, broke Vladimir Putin said that the cease-fire will be guaranteed by both Moscow and Turkey, and the agreement has been welcomed by Iran. Moscow and Tehran provide crucial military support to Syrian President Bashar Assad, while Turkey has long served as a rear base and source of supplies for the rebels. Iran’s Foreign Minister Mohammad Javad Zarif called the cease-fire a “major achievement” in a tweet Friday. “Let’s build on it by tackling the roots of extremist terror,” he added, as Bloomberg reports.

Russia said the deal was signed by seven of Syria’s major rebel factions, though none of them immediately confirmed it, and one denied signing it.

The truce came on the heels of a Russian-Turkish agreement earlier this month to evacuate the last rebels from eastern Aleppo after they were confined to a tiny enclave by a government offensive. The retaking of all of Aleppo marked Assad’s greatest victory since the start of the 2011 uprising against his family’s four-decade rule.

“The defeat of the terrorists in Aleppo is an important step toward ending the war,” Assad said in an interview with TG5, an Italian TV station, adding that the capture of the city does not mean that the war has ended because “terrorists” are still in Syria.

* * *

But what is most notable about the ceasefire is that the United States has been demonstratively left out of both agreements, reflecting the deterioration of relations between Moscow and Washington, and to an extent the decline in US-Turkish relations. Meanwhile, like Russia, Syria is hopeful that the arrival of president Trump means a new peace in the region. Assad told TG5 “we are more optimistic, with caution,” about the incoming administration of President-elect Donald Trump, who has suggested greater cooperation with Russia against extremist groups.

“We can say part of the optimism could be related to better relation between the United States and Russia,” Assad said, speaking in English.

“Mr. Trump, during his campaign – (said) that his priority is fighting terrorism, and we believe that this is the beginning of the solution, if he can implement what he announced,” Assad said in the interview, which was apparently filmed before the cease-fire was announced.

Meanwhile, the US was desperate to pretend it still has clout in the regional conflict. James Dobbins, a former senior U.S. diplomat, said the lack of American involvement in the talks between Russia, Iran and Turkey did not preclude the United States from being a major player in the region. In this case, it was frozen out because Obama leaves office in less than a month and because Turkey and Russia are at odds with the United States over its Syria policy and other issues, said Dobbins, a fellow at RAND, a research organization.

Trump has said he would cooperate more closely with Russia to fight terrorism but it was unclear what that policy would look like, given resistance from the Pentagon and the U.S. intelligence community to closer cooperation with Russia on Syria.

end

6.GLOBAL ISSUES

7. OIL ISSUES

The following 5 countries can increase production which will threaten the OPEC unity

(courtesy Rizvi/OilPrice.com)

The Five Countries Threatening OPEC Unity

Submitted by Osama Rizvi via OilPrice.com,

As an apparent wave of populism sweeps through the world, Theresa May prepares to trigger Article 50, and fears of a trade war between China and the U.S grow, financial markets are on edge. But alongside this uncertainty, there has been some good news for markets as well, with oil markets moving towards rebalancing. The recent OPEC production cut agreement, and the additional cuts by non-OPEC countries caused oil prices to touch a post-2014 high. But Saudi Arabia and Russia, among other oil producers, are now in the limelight, as the world waits to see how true to the agreement each country will remain. Perhaps more important at this point are those countries who were never part of the agreement, or who were absolved from it.

One such country is Libya; its rising oil supply can easily offset the effect of the proposed production cut. Recently, oil exports from Libya’s key oil terminals Es-Sider and Zueitina were resumed. This could bring 270,000 bpd back to the market, which is just a taste of how Libya, if peace prevails, could increase its production. The addition of 270,000 barrels alone accounts for almost a quarter of the OPEC production cut.

The second country is Iraq. Iraq fought hard to be exempted from any sort of cut or freeze, arguing that it needed money “to fight ISIS”, and while it eventually accepted a cut, the risk of this huge oil nation cheating on the deal is significant. Iraq’s output has grown at an alarming rate this year and the recently signed a deal with Lukoil, the Russian energy giant, to tap into the West Qurna-2 reservoir adds to the concerns.

Then there is Iran. Iran was not exempted from the deal but agreed to a production freeze at 3.8 million barrels per day. Like Iraq, Iran has also been busy signing deals with oil giants to ramp up its production. On December 7th Iran and Shell signed a deal to explore three oil and gas fields. Saudi Arabia has always seen Iran as a rival, with Iran being the key reason that Deputy Crown Prince Muhammad Bin Salman refused to sign the deal as put forward earlier in the year. This time around things were different, and matters has grown increasingly serious for Saudi Arabia.

The Kingdom had already borne the brunt of its decision in 2014 to not to cut production. We saw how the country’s masses, accustomed to government largesse in the shape of subsidies, extravagant pay and the leisure of not working, turned against the country’s gerontocracy when pay was slashed, holidays curtailed and subsidies removed. Also, the Foreign Exchange reserves of the Saudis were being depleted at an unprecedented rate. These factors explain the display of flexibility by the Kingdom at the Vienna conference on the 30th of December. On the other hand, prospects for Iran are just opening up after the Obama administration signed the controversial nuclear deal with the Islamic Republic. As the sanctions are being lifted gradually from Iran, it now sees the whole world opening up as a potential market – a temptation that may prove very hard to resist.

The Putin Factor: The appointment of Mr. Rex Tillerson as secretary of State and the various insinuations by the President-elect to lift sanctions could be symptomatic of greater production from Russia. Russia has recently claimed that it will beat 2016’s estimated oil production total of 253 million tons in 2017.

“Supposedly 253.5 [million tonnes of oil are expected to be exported from Russia] this year, which is 4.8 percent more than in 2015. In 2017, we will have a little more than this,” Molodtsov said.

Finally, Nigeria. As of now it is busy fighting Boko-Haram and attempting to strike some kind of political deal with the Niger Delta Avengers. Exempted from the oil deal, its production stands around 1.6 mbpd. President Buhari has vowed to increase the production to 2.2mbpd, a statement that will not be welcomed by fellow OPEC producers.

If any of these countries do significantly increase production, then the euphoria that has yet to reach its peak may begin to fade.

8. EMERGING MARKETS

none today

Your early morning currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 10:00 am

Euro/USA 1.0547 UP .0019/REACTING TO + huge Deutsche bank problems + USA election:/TRUMP WINS THE ELECTION/USA READY TO GO ON A SPENDING BINGE WITH THE TRUMP VICTORY/ITALIAN REFERENDUM DEFEAT/AND NOW ECB TAPERING BOND PURCHASES/USA RAISING RATES

USA/JAPAN YEN 116.98 UP 0.690(Abe’s new negative interest rate (NIRP), a total DISASTER/SIGNALS U TURN WITH INCREASED NEGATIVITY IN NIRP/JAPAN OUT OF WEAPONS TO FIGHT ECONOMIC DISASTER/KURODA: HELICOPTER MONEY ON THE TABLE AND DECISION ON SEPT 21 DISAPPOINTS WITH STIMULUS/OPERATION REVERSE TWIST

GBP/USA 1.2310 UP .0026 (Brexit by March 201/UK government loses case/parliament must vote)

USA/CAN 1.3470 DOWN .0009 (CANADA WORRIED ABOUT TRADE WITH THE USA WITH TRUMP ELECTION/ITALIAN EXIT FROM EU)

Early THIS FRIDAY morning in Europe, the Euro ROSE by 20 basis points, trading now WELL BELOW the important 1.08 level RISING to 1.0547; Europe is still reacting to Gr Britain BREXIT,deflation, announcements of massive stimulation (QE), a proxy middle east war, and the ramifications of a default at the Austrian Hypo bank, an imminent default of Greece, Glencore, Nysmark and the Ukraine, along with rising peripheral bond yield further stimulation as the EU is moving more into NIRP, and now the Italian referendum defeat AND NOW THE ECB TAPERING OF ITS PURCHASES/ THE USA’S NON tightening by FAILING TO RAISE THEIR INTEREST RATE AND NOW THE HUGE PROBLEMS FACING TOO BIG TO FAIL DEUTSCHE BANK + THE ELECTION OF TRUMP IN THE USA+ AND TODAY MONTE DEI PASCHI NATIONALIZATION / Last night the Shanghai composite CLOSED UP 7.54 0r 0.24% / Hang Sang CLOSED UP 209.65 POINTS OR 0.96% /AUSTRALIA CLOSED DOWN 0.48% / EUROPEAN BOURSES ALL IN THE RED EXCEPT LONDON

We are seeing that the 3 major global carry trades are being unwound. The BIGGY is the first one;

1. the total dollar global short is 9 trillion USA and as such we are now witnessing a sea of red blood on the streets as derivatives blow up with the massive rise in the rise in the dollar against all paper currencies and especially with the fall of the yuan carry trade. The emerging market which house close to 50% of the 9 trillion dollar short is feeling the massive pain as their debt is quite unmanageable.

2, the Nikkei average vs gold carry trade ( NIKKEI blowing up and the yen carry trade HAS BLOWN up/and now NIRP)

3. Short Swiss franc/long assets blew up ( Eastern European housing/Nikkei etc.

These massive carry trades are terribly offside as they are being unwound. It is causing global deflation ( we are at debt saturation already) as the world reacts to lack of demand and a scarcity of debt collateral. Bourses around the globe are reacting in kind to these events as well as the potential for a GREXIT>

The NIKKEI: this FRIDAY morning CLOSED DOWN 30.77 OR 0.16%

Trading from Europe and Asia:

1. Europe stocks ALL IN THE RED EXCEPT LONDON

2/ CHINESE BOURSES / : Hang Sang CLOSED UP 209.65 OR .96% Shanghai CLOSED UP 7.59 POINTS OR 0.24% / Australia BOURSE CLOSED DOWN 0.48% /Nikkei (Japan)CLOSED DOWN 30.77 OR 0.16% / INDIA’S SENSEX IN THE GREEN

Gold very early morning trading: $1158.60

silver:$16.21

Early FRIDAY morning USA 10 year bond yield: 2.474% !!! DOWN 1 IN POINTS from THURSDAY night in basis points and it is trading JUST BELOW resistance at 2.27-2.32%. THE RISE IN YIELD WITH THIS SPEED IS FRIGHTENING

The 30 yr bond yield 3.084, DOWN 2 IN BASIS POINTS from THURSDAY night.

USA dollar index early FRIDAY morning: 102.22 DOWN 43 CENT(S) from THURSDAY’s close.

This ends early morning numbers FRIDAY MORNING

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now your closing FRIDAY NUMBERS

Portuguese 10 year bond yield: 3.764% UP 1 in basis point yield from THURSDAY (does not buy the rally)

JAPANESE BOND YIELD: +.046% UP 3/5 in basis point yield from THURSDAY/JAPAN losing control of its yield curve

SPANISH 10 YR BOND YIELD:1.384% UP 6 IN basis point yield from THURSDAY (this is totally nuts!!/

ITALIAN 10 YR BOND YIELD: 1.815 UP 2 in basis point yield from THURSDAY

the Italian 10 yr bond yield is trading 44 points HIGHER than Spain.

GERMAN 10 YR BOND YIELD: +.208% UP 3 IN BASIS POINTS ON THE DAY

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IMPORTANT CURRENCY CLOSES FOR FRIDAY

Closing currency crosses for FRIDAY night/USA DOLLAR INDEX/USA 10 YR BOND YIELD/1:00 PM

Euro/USA 1.0532 UP .0061 (Euro UP 61 basis points/ represents to DRAGHI A COMPLETE POLICY FAILURE/

USA/Japan: 116.82 UP: 0.520(Yen DOWN 52 basis points/

Great Britain/USA 1.2335 UP 0.0052( POUND UP 52 basis points)

USA/Canada 1.3431 DOWN 0.0051(Canadian dollar UP 51 basis points AS OIL FELL TO $53.60

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

This afternoon, the Euro was UP by 61 basis points to trade at 1.0532

The Yen FELL to 116.82 for a LOSS of 52 basis points as NIRP is STILL a big failure for the Japanese central bank/HELICOPTER MONEY IS NOW DELAYED/BANK OF JAPAN NOW WORRIED AS AS THEY ARE RUNNING OUT OF BONDS TO BUY AS BOND YIELDS RISE /OPERATION REVERSE TWIST ANNOUNCED SEPT 21.2016

The POUND ROSE 52 basis points, trading at 1.2335/

The Canadian dollar ROSE by 51 basis points to 1.3431, WITH WTI OIL FALLING TO : $53.60

Your closing 10 yr USA bond yield DOWN 4 IN basis points from THURSDAY at 2.446% //trading well ABOVE the resistance level of 2.27-2.32%) very problematic USA 30 yr bond yield: 3.061 DOWN 2 in basis points on the day /

Your closing USA dollar index, 102.23 DOWN 42 CENT(S) ON THE DAY/1.00 PM

Your closing bourses for Europe and the Dow along with the USA dollar index closing and interest rates for FRIDAY: 1:30 PM EST

London: CLOSED UP 22.57 OR .32%

German Dax :CLOSED UP 30.01 POINTS OR 0.26%

Paris Cac CLOSED UP 23.84 OR 0.49%

Spain IBEX CLOSED UP 25.00 POINTS OR 0.27%

Italian MIB: CLOSED UP 30.64 POINTS OR 0.16%

The Dow was DOWN 57.18 POINTS OR .29% 4 PM EST

NASDAQ WAS DOWN 48.97 POINTS OR .90% 4.00 PM EST

WTI Oil price; 53.60 at 1:00 pm;

Brent Oil: 56.55 1:00 EST

USA /RUSSIAN ROUBLE CROSS: 60.43 (ROUBLE DOWN 1 AND 2 /100 roubles from YESTERDAY)

TODAY THE GERMAN YIELD RISES TO +0.208% FOR THE 10 YR BOND 2:30 EST

END

This ends the stock indices, oil price, currency crosses and interest rate closes for today

Closing Price for Oil, 5 pm/and 10 year USA interest rate:

WTI CRUDE OIL PRICE 5 PM:$53.81

BRENT: $56.87

USA 10 YR BOND YIELD: 2.446% (ANYTHING HIGHER THAN 2.70% BLOWS UP THE GLOBE)

USA 30 YR BOND YIELD: 3.063%

EURO/USA DOLLAR CROSS: 1.0512 up .0049

USA/JAPANESE YEN:116.90 UP 0.643

USA DOLLAR INDEX: 102.40 down 25 cents (BREAKS HUGE resistance at 101.80)

The British pound at 5 pm: Great Britain Pound/USA: 1.2318 : up 36 BASIS POINTS.

German 10 yr bond yield at 5 pm: +.208%

END

And now your more important USA stories which will influence the price of gold/silver

TRADING IN GRAPH FORM

2016 Ends With A Whimper: Stocks Slide On Last Minute Pension Fund Selling

When we first warned 8 days ago that in the last week of trading a “Red Flag For Markets Has Emerged: Pension Funds To Sell “Near Record Amount Of Stocks In The Next Few Days”, and may have to “rebalance”, i.e. sell as much as $58 billion of equity to debt ahead of year end, many scoffed wondering who would be stupid enough to leave such a material capital reallocation for the last possible moment in a market that is already dangerously thin as is, and in which such a size order would be sure to move markets lower, and not just one day.

Today we got the answer, and yes – pension funds indeed left the reallocation until the last possible moment, because three days after the biggest drop in the S&P in over two months, the equity selling persisted as the reallocation trade continued, leading to the S&P closing off the year with a whimper, not a bang, as Treasurys rose, reaching session highs minutes before the 1pm ET futures close when month-end index rebalancing took effect.

10Y yields were lower by 2bp-3bp after the 2pm cash market close, with the 10Y below closing levels since Dec. 8. Confirming it was indeed a substantial rebalancing trade, volumes surged into the futures close, which included a 5Y block trade with ~$435k/DV01 according to Bloomberg while ~80k 10Y contracts traded over a 3- minute period.

The long-end led the late rally, briefly flattening 5s30s back to little changed at 112.5bps. Month-end flows started to pick up around noon amid reports of domestic real money demand; +0.07yr duration extension was estimated for Bloomberg Barclays Treasury Index. Earlier, TSYs were underpinned by declines for U.S. equities that accelerated after Dec. Chicago PMI fell more than expected.

Looking further back, the Treasury picture is one of “sell in December 2015 and go away” because as shown in the chart below, the 10Y closed 2016 just shy of where it was one year ago while the 30Y is a “whopping” 4 bps wider on the year, and considering the recent drop in yields as doubts about Trumpflation start to swirl, we would not be surprised to see a sharp drop in yields in the first weeks of 2017. Already in Europe, German Bunds are back to where they were on the day Trump was elected.

So with a last minute scramble for safety in Treasurys, it was only logical that stocks would slide, closing the year off on a weak note. Sure enough, the S&P500 pared its fourth annual gain in the last five years, as it slipped to a three-week low in light holiday trading, catalyzed by the abovementioned pension fund selling.

The day started off, appropriately enough, with a Dollar flash crash, which capped any potential gains in the USD early on, and while a spike in the euro trimmed the dollar’s fourth straight yearly advance, the greenback still closed just shy of 13 year highs, up just shy of 3% for the year.

Meanwhile, the year’s best surprising performing asset, crude, trimmed its gain in 2016 to 52%.

The S&P 500 Index cut its advance this year to 9.7 percent as it headed for the first three-days slide since the election. The Dow Jones Industrial Average was poised to finish the year 200 points below 20,000 after climbing within 30 points earlier in the week. It appears the relentless cheerleading by CNBC’s Bob Pisani finally jinxed the Dow’s chances at surpassing 20,000 in 2016. Trading volume was at least 34 percent below the 30-day average at this time of day. A rapid surge in the euro disturbed the calm during the Asian morning, as a rush of computer-generated orders caught traders off guard. That sent a measure of the dollar lower for a second day, trimming its rally this year below 3 percent.

Actually, did we say crude was the best performing asset of the year? We meant Bitcoin, the same digital currency which we said in September 2015 (when it was trading at $250) is set to soar as Chinese residents start using it more actively to circumvent capital controls, soared, and in 2016 exploded higher by over 120%.

For those nostalgic about 2016, the chart below breaks down the performance of major US indices in 2016 – what began as the worst start to a year on record, ended up as a solid year performance wise, with the S&P closing up just shy of 10%, with more than half of the gains coming courtesy of an event which everyone was convinced would lead to a market crash and/or recession, namely Trump’s election, showing once again that when dealing with artificial, centrally-planned market nobody has any idea what will happen, or frankly, what is happening.