Gold at (1:30 am est) $1160.40 UP $10.40

silver at $16.35: UP 41 cents

Access market prices:

Gold: $1159.25

Silver: $16.29

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

TUESDAY gold fix Shanghai

Shanghai morning fix Jan 3/17 (10:15 pm est last night): $ 1181.81

NY ACCESS PRICE: $1157.00 (AT THE EXACT SAME TIME)/premium $24.81

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 119.39

NY ACCESS PRICE: $1156.15 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $23.25

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Jan 3/2017: 5:30 am est: $.1148.65 (NY: same time: $1148.09 5:30AM)

London Second fix Jan 3.2017: 10 am est: $1151.00 (NY same time: $1151.10 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 2 NOTICE(S) FOR 200 OZ. TOTAL NOTICES SO FAR: 135 FOR 13,500 OZ (.420 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 1 NOTICE(s) FOR 5,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 196 FOR 980,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 386 contracts UP to 164,787 with respect to FRIDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .824 BILLION TO BE EXACT or 118% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 1 NOTICES FILED FOR 5,000 OZ.

In gold, the total comex gold ROSE BY 7844 contracts WITH THE FALL IN THE PRICE GOLD ($6.40 with FRIDAY’S trading ).The total gold OI stands at 423,354 contracts.

we had 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a huge change in tonnes of gold at the GLD, a withdrawal of 9.49 tonnes of gold leaving the GLD

Inventory rests tonight: 813,87 tonnes

.

SLV

we had n0 changes in silver into the SLV

THE SLV Inventory rests at: 341.348 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver ROSE by 386 contracts UP to 164,787 DESPITE THE FACT THAT the price of silver FELL by $0.22 with FRIDAY’S trading. The gold open interest ROSE by A WHOPPING 7,844 contracts UP to 423,354 DESPITE THE FACT THAT the price of gold FELL BY $6.40 WITH FRIDAY’S TRADING (AND WHACKING OF GOLD).

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) FRBNY report on earmarked gold movement

(Harvey)

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 32.28 POINTS OR 1.04%/ /Hang Sang closed UP 149.84 OR .68%. The Nikkei closed /Australia’s all ordinaires CLOSED UP 1.15%/Chinese yuan (ONSHORE) closed DOWN at 6.9605/Oil ROSE to 54.93 dollars per barrel for WTI and 58.02 for Brent. Stocks in Europe: ALL IN THE GREEN . Offshore yuan trades 6.9716 yuan to the dollar vs 6.9605 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES /

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)Sunday night

More capital controls in China and that sends bitcoin over $1,000 to $1024

( zero hedge)

ii)Monday night:

The yuan slumped last night which caused bitcoin to rise over $1050.00 Many researchers have suggested to China to do a one off huge devaluation and avoid capital controls

( zero hedge)

iii)Monday night:

Government bond trading froze last night after huge increases in interbank lending rates. The POBC withdraw huge amounts of money trying to drain liquidity: Overnight lending rates: 18%

( zero hedge)

iv)Capital controls seems to have worked on day one of the new year.

( zero hedge)

v)If Donald Trump recognizes Taiwan as independent, this would cross China’s one China policy. The Chinese military are considering measures now to cripple Taiwan by cutting off trade etc.

( zero hedge)

4 EUROPEAN AFFAIRS

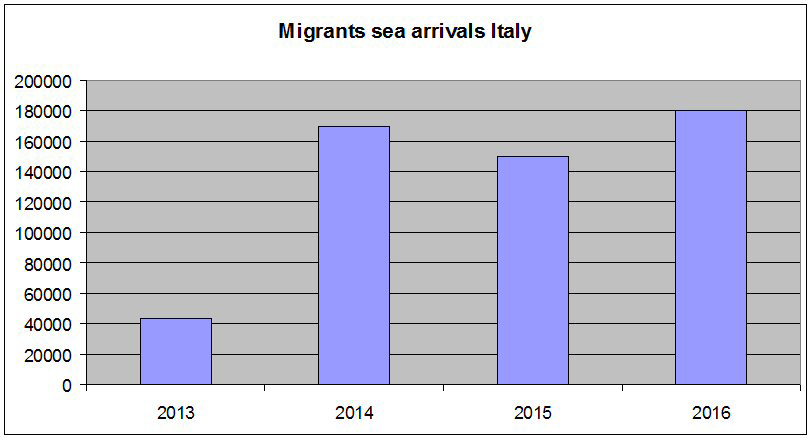

i)Italy

Why Italian government cannot or will not stop the refugee smuggling.

( Gefira)

ii)England

This does not look good: The popular ambassador to the EU who was set to negotiate England’s exit from the EU unexpectedly resigns

(courtesy zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Islamic attack in Istanbul. Now there are 39 dead:

( zero hedge/two stories)

ii)India

India announced that 14.9 of the 15 trillion in old notes have been handed in. Thus almost zero has been withheld because of the tax evasion. The government was set to make a killing on notes not being returned to the banking system. However the economy tanked as India is basically a cash economy. The central bank of India immediately lowered rates but confidence is waning

( zero hedge)

iii)Israel:Palestine

6.GLOBAL ISSUES

7. OIL ISSUES

i)Oil rises on reports that Kuwait and Oman will cut output:

( zero hedge)

ii)Libya is set to increase production to over 900,000 barrels per day. The increase of 125,000 barrels per day represents 1/3 of cut production by other OPEC/non OPEC members

( zero hedge)

iii)The non compliance in the OPEC oil production curtailment is already is jeopardy as Iraq accuses the Kurds of producing more oil than permitted

( zero hedge)

8. EMERGING MARKETS

Very strange: Venezuela’s government is selling 5 billion USA to its central bank. They have no means whatsoever of getting dollars. It is well known that China advanced huge sums of money with collateral being the oil. It looks like China has now asked for a bond to back up the collateral.

( zero hedge)

9. PHYSICAL MARKETS

i)Iran receives huge amounts of cash and gold for sanction relief:

( Wall Street Journal/GATA)

ii)Interesting: almost all of the outlawed money has been redeposited in the bank. The government was expecting almost 1/3 not to be returned because of tax evasion. They guessed wrong and thus their plan was basically gone for naught.

( zero hedge)

iii)The USA dollar’s share of global currency reserves slips a bit in the 3rd quarter

( Lang/Reuters/GATA)

iv)This should be very alarming: Germany’s gold reserves in the uSA were only paper claims. Now Peter Boehringer, the head of the organization that wants all of Germany’s gold on its soil will pound the table asking for the gold to be repatriated in full at once.

It think it would be appropriate for the uSA to change their definition of “earmarked gold”

( Peter Boehringer/Chris Powell)

v)A terrific commentary from Alasdair Macleod showing the stupidity of Modi in his attempts to curb the appetite of gold by Indian citizens

( Alasdair Macleod)

vi)First Majestic silver, a large primary silver producer is set to join the class action suit. They have little gold so they would be ideal in this action. Neumeyer is one angry CEO!!

( Mac Slavo)

vii)Interview of Bill Holter with SGT

10.USA STORIES

i)Early uSA trading:

( zero hedge)

ii)There is a criminal witch hunt with respect to the Dallas police pension fiasco

( Mish Shedlock)

iii)The Donald is at it again. This time it is General Motors. “Either you make your cars in the USA or you pay a big border tax”:

( zero hedge)

iv)GM responds to Trump; you are wrong. We make the Chevy Cruze in Ohio:

( zero hedge)

v)FORD GOT THE MESSAGE!! THEY ARE CANCELLING PLANS FOR A 1.6 BILLION USA PANT IN SAN LUIS POTOSI, MEXICO

( zero hedge)

vi)Next up for Donald; the repeal of Obamacare:

( zero hedge)

vii)Trump picks Robert Lighthizer as USA trade representative, a very tough negotiator and a tough critic on China: China again will not be too happy!

( zero hedge)

viii)Trump is on a roll: He now ours DHS to prepare for a border wall construction with Mexico:

( zero hedge)

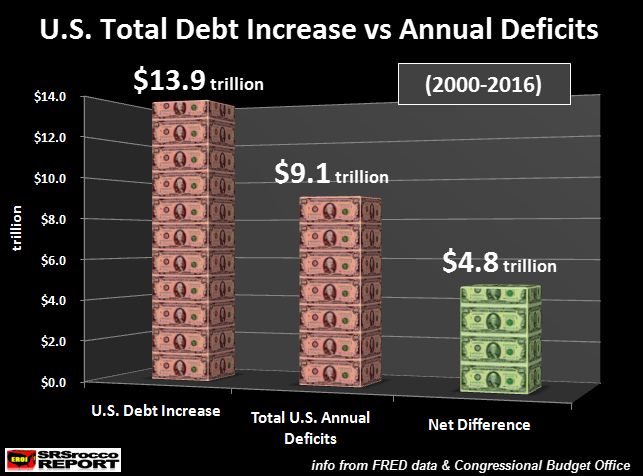

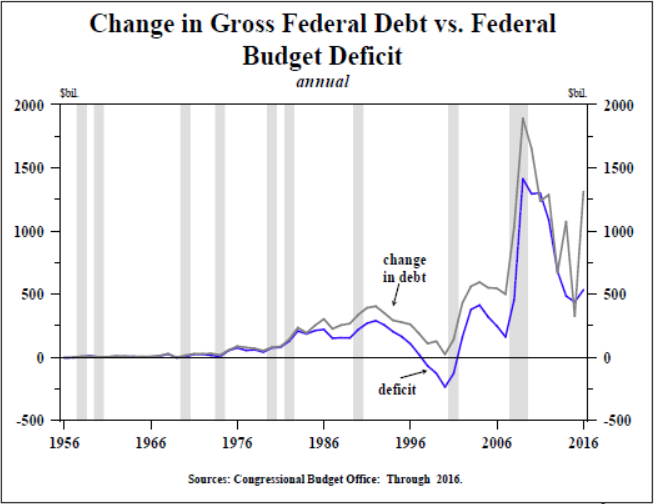

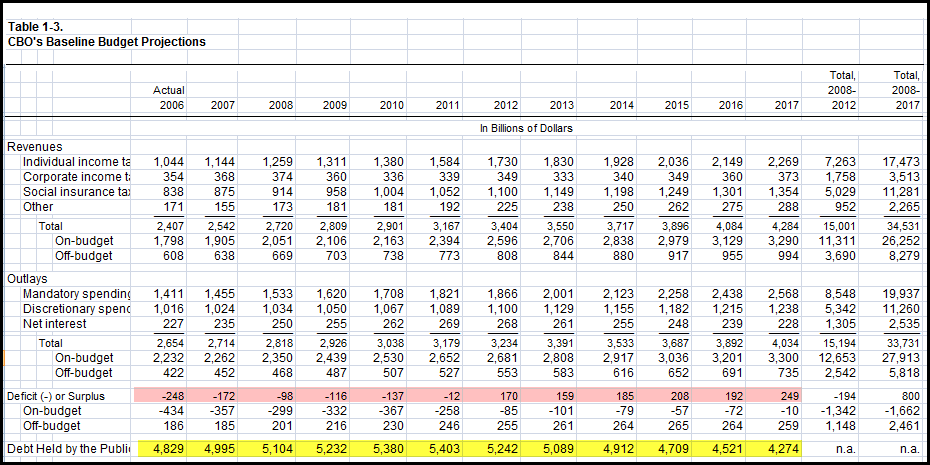

ix) An extremely important commentary from Steve St Angelo on the true USA deficit. He removes the accounting gimmicks used to prop up the system as well as adds to the deficit items like student loans and auto loans which are not assets and should be part of the deficit. The true deficit for the fiscal year ending Sept 30/2016 was 1.2 trillion USA. It will be much higher this year!

( Steve St Angelo/SRSRocco report)

Federal Reserve Bank of New York:

Earmarked gold movements

December report:

Last Oct/2016 we had 7,841 million dollars worth “gold” in inventory at the FRBNY

valued at $42.22 per oz

Last November/2016 we had 7,841 million dollars worth of gold in inventory at FRBNY valued at $42.22 per oz

thus 0 oz moved at $42.22

So far officially, the following has been repatriated to BuBa from NY:

2013: 5 tonnes

2014: 120 tonnes

2015: 99.5 tonnes

2016: to be officially announced

Their total quota from NY is scheduled to be 300 tonnes and another 374 tonnes from Paris of which 177 tonnes of gold has officially been sent (Dec 2015) and thus another 197 tonnes to cross the English channel.

Germany has officially 1237 tonnes of gold “stored ” in NY. On conclusion of the repatriation, Paris will have 0 stored there.

end

Let us head over to the comex:

The total gold comex open interest ROSE BY 7,844 CONTRACTS UP to an OI level of 423,354 DESPITE THE FACT THAT THE PRICE OF GOLD FELL $6.40 with FRIDAY’S trading. We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year.

With the front month of January we had a loss of 136 contracts down to 1007. We had 133 notices filed so we lost only 3 contracts or 300 oz standing for gold in this non active delivery month of January. For the next big active delivery month of February we had a GAIN of 3046 contracts UP to 282,871. March had a gain of 24 contracts as it’s OI is now 24.

We had 2 notice(s) filed upon today for 200 oz

And now for the wild silver comex results. Total silver OI ROSE by 386 contracts FROM 164,401 up to 164,787 DESPITE THE FACT THAT the price of silver FELL BY $0.22 with FRIDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI FELL by 291 contracts FALLING TO 467. We had 195 notices filed on Friday so we lost 96 or an additional 480,000 oz will not stand and no doubt were cash settled. The next non active month of February saw the OI rise by 3 contracts up to 108.

The next big active delivery month is March and here the OI FELL by 276 contracts DOWN to 133,802 contracts.

We had 1 notice(s) filed for 5,000 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 233,456 contracts which is very good.

Yesterday’s confirmed volume was 161,797 contracts which is fair

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

2 notice(s)

200 oz

|

| No of oz to be served (notices) |

1005 contracts

100,500 oz

|

| Total monthly oz gold served (contracts) so far this month |

135 notices

13,500 oz

.420 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,475,021.1 oz |

For January:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

974,476.700 0z

Scotia

CNT

|

| Deposits to the Dealer Inventory |

515,901.35 OZ

Brinks

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

466 contracts

(2,330,000 oz)

|

| Total monthly oz silver served (contracts) | 196 contracts (980,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,725,668.6 oz |

end

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver stories for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE

Holiday will be back soon

END

Iran receives huge amounts of cash and gold for sanction relief:

(courtesy Wall Street Journal/GATA)

A tally of Iran sanctions relief includes more than $10 billion in cash, gold

Submitted by cpowell on Sat, 2016-12-31 01:40. Section: Daily Dispatches

By Carole E. Lee and Jay Solomon

The Wall Street Journal

Friday, December 30, 2016

WASHINGTON — In the three years since a preliminary nuclear deal was struck with Iran, Tehran has received more than $10 billion in sanctions relief from around the world in the form of cash and gold, according to current and former U.S. officials.

The large shipments of gold and cash, from oil funds unfrozen in numerous countries, represent the kind of financial relief that made Iran’s leaders eager to complete the international nuclear accord. Some of the cash and gold went to Iran while the U.S. and other world powers negotiated with Tehran on a final nuclear deal. More shipments took place after final deal went into effect last January.

This tallying of the sanctions relief to date includes payments previously announced and others that haven’t been. In one previously unreported payment, the U.S. authorized Iran to receive $1.4 billion in sanctions relief between when the final deal was struck in July 2015 and when it took effect, according to the U.S. officials.

Some U.S. lawmakers and Middle East allies contend that the shipments of cash and gold, a highly liquid form of money, can be used to fund Iran’s allies in the region, including the Assad regime in Syria, the Lebanese militia Hezbollah, and the Houthi political movement in Yemen. …

… For the remainder of the report:

http://www.wsj.com/articles/a-tally-of-iran-sanctions-relief-includes-mo…

END

Interesting: almost all of the outlawed money has been redeposited in the bank. The government was expecting almost 1/3 not to be returned because of tax evasion. They guessed wrong and thus their plan was basically gone for naught.

(courtesy zero hedge)

Currency revocation seems unlikely to generate windfall for Indian government

Submitted by cpowell on Sat, 2016-12-31 03:45. Section: Daily Dispatches

Indians Rush to Exchange Cash Ahead of Deadline

Demonetisation Has Seen More Money Returned to the System than Originally Expected

By Kiran Stacey

Financial Times, London

Friday, December 30, 2016

https://www.ft.com/content/699c0d30-ce56-11e6-864f-20dcb35cede2

Indians rushed to exchange the last of their expired currency notes ahead of a deadline on Friday, amid initial signs that the country’s controversial demonetisation policy will fail to generate the windfall expected by the government.

New Delhi has claimed its decision, announced last month, to scrap 86 per cent of India’s currency and replace it with a smaller quantity of new banknotes would eliminate illicitly earned or unaccounted for income that has been beyond the reach of tax authorities.

But figures show that as Indians queued to deposit the last of their old Rs500 and Rs1,000 notes, almost all of the old currency had been returned. Economists said this suggested the move had not eliminated as much illicit cash as expected, and would derail the government’s hope of a windfall gain from the scheme.

Narendra Modi, India’s prime minister, defended his experimental demonetisation policy on Friday evening, saying it had been necessary to root out India’s well-established black economy.

“Some politicians criticised the demonetisation exercise saying the government broke a mountain only to catch rats,” he said during the final hours of a 50-day transition period. “They are right. We want to catch the rats who are stealing the poor people’s hard-earned money.”

The Reserve Bank of India has not said when it will publish the final figures on how much has been returned. However their latest data show that over Rs14tn out of the Rs15.5tn that was scrapped has now successfully been deposited despite stringent checks for untaxed income — far more than the Rs10 trillion that the government initially predicted.

According to some experts, this means the RBI will not be given a sudden windfall for the government to disperse in the new year.

“The government thought that trillions of rupees wouldn’t come back, and those liabilities could then be written off by the Reserve Bank of India,” said Sanjeev Ahluwalia, an adviser at the Observer Research Foundation think-tank.

“They thought they would be able to pull out that money as a windfall in what would have been a neat accounting trick, but at best, they were only ever going to get 5-10 per cent remaining outside the system.”

However, “people have been clever at finding ways round the rules”, he said.

Mr Modi first announced his decision to scrap 86 per cent of the country’s currency on November 8, in what amounted to the biggest economic experiment since Japan’s trial of negative interest rates.

With banks overwhelmed by customers looking to change money in the immediate aftermath of that announcement, Mr Modi pleaded with Indians to give him 50 days for normality to return.

By Friday — the end of that 50-day period — some sense of calm had returned to the banking system, albeit in the middle of holiday season and with most ATMs still shut for lack of new notes.

But as economists processed the initial results of the policy, many warned that the early signals show that it has significantly slowed growth.

“Growth will definitely have been lower because of demonetisation,” said Kunal Kundu, India economist at Societe Generale. “Inflation data looks weak, as do early figures on consumer durables.” Reports on Friday suggested spending on durable consumer goods fell by up to 38 per cent in November on the previous year.

India’s army of small traders have reported a similar effect, with customers staying away either to stand in bank queues or simply to conserve their supplies of cash.

Kailash Ashtakwani, a hardware store owner from Delhi, said he had lost 70 per cent of his business as a result of demonetisation. Standing in line to deposit cash at his bank in New Delhi, Mr Ashtakwani said: “Putting the [old] money in is easy but to take anything out is impossible when queues are eight or nine hours.”

India’s finance minister, Arun Jaitley, has announced a jump in tax revenue in the period from April until mid-December, which he said showed that the move had not damaged growth. Economists warned, however, that the increase was also caused by multiple tax rises in that period.

Mr Modi will give another speech on Saturday during which he is expected to announce a sweetener to win over voters ahead of regional elections next year.

He may also say when the curbs on withdrawals from ATMs will be lifted. Bank customers can currently only take out Rs24,000 per week over the counter from banks, and some had predicted this limit would be lifted on Friday. With banks lobbying for the limits to be extended, neither the government nor the RBI has said when they will finally end.

END

The USA dollar’s share of global currency reserves slips a bit in the 3rd quarter

(courtesy Lang/Reuters/GATA)

U.S. dollar’s share of global currency reserves slips in third quarter

Submitted by cpowell on Sat, 2016-12-31 13:56. Section: Daily Dispatches

By Jason Lange

Reuters

Friday, December 30, 2016

The U.S. dollar’s share of currency reserves reported to the International Monetary Fund slipped in the third quarter of 2016 to its lowest level in two years, data from the IMF showed today.

The July-September period was the third consecutive decline in the dollar’s share of allocated currency reserves, or those reported to the IMF. The decline could reflect increased optimism about the global economy, with the European economy seen on improved footing.

In the third quarter the dollar comprised 63.3 percent of allocated reserves, the smallest share since the third quarter of 2014. The dollar made up 63.8 percent of allocated reserves in the second quarter.

The euro’s share rose to 20.3 percent in the same period from 20.0 percent the quarter before, while the yen’s share increases to 4.5 percent from 4.4 percent. …

… For the remainder of the report:

http://www.reuters.com/article/us-forex-reserves-idUSKBN14J1BV?il=0

END

This should be very alarming: Germany’s gold reserves in the uSA were only paper claims. Now Peter Boehringer, the head of the organization that wants all of Germany’s gold on its soil will pound the table asking for the gold to be repatriated in full at once.

It think it would be appropriate for the uSA to change their definition of “earmarked gold”

(courtesy Peter Boehringer/Chris Powell)

Peter Boehringer: Germany’s gold reserves in U.S. were only paper claims

Submitted by cpowell on Sat, 2016-12-31 15:38. Section: Documentation

That explains why the Bundesbank and New York Fed could never produce proof of the gold’s existence.

* * *

By Peter Boehringer, Founder

German Precious Metals Society

http://www.gold-action.de/

Saturday, December 31, 2016

As it often has done before, Germany’s Bundesbank has released news at Christmastime to avoid critical examination and discussion, this time news about its repatriation of the nation’s gold reserves.

The repatriated tonnage volume reported — “approximately 200 tonnes,” bringing the total of gold repatriated to approximately 1,580 tonnes or 47 percent of Germany’s gold reserves — is OK, not spectacular. And this month there was far more important news about Germany’s gold, though it was overlooked.

The important news came December 21 from the major German news agency, DPA-AFX, and most likely was written by the Bundesbank itself for DPA-AFX. The news agency published a German-language news brief that was uncritically republished by most German newspapers and magazines without anyone recognizing its political, economic, and historical sensitivity.

The news item said: “… in den 1950er und 1960er Jahren wuchs der deutsche Goldschatz rasant. Denn. … Bundesrepublik [hatte] dank des Exports viele Dollar, die bei der US-Zentralbank gegen Goldforderungen eingetauscht werden konnten.”

In English: “Germany’s gold hoard grew rapidly in the 1950s and 1960s. Thanks to its export surplus, the Federal Republic amassed many dollars that could be exchanged at the U.S. central bank against gold claims.”

The news brief’s term was “gold claims” — not “physical gold bars,” which both the Bundesbank and the U.S. Federal Reserve contend have constituted the German gold reserves held in the United States.

We have the official text from DPA-AFX from December 21 containing the cited sentence, which was published without change by at least 20 major news organizations by the next day. As an example, here’s the item in the German news magazine Der Spiegel:

http://www.spiegel.de/wirtschaft/soziales/bundesbank-sammelt-goldbarren-…

We as yet have no proof that Bundesbank itself wrote this sentence. (DPA-AFX would have that proof.) But it would be unusual if a mere apprentice at the news service had fabricated the term.

So it is reasonable if we now consider nearly official what gold “conspiracy theorists” have been assuming for decades. That is, the German gold reserves supposedly stored abroad and especially at the Federal Reserve Bank of New York most likely never existed in physical form since the 1960s. Rather the German gold supposedly stored abroad most likely has been only a matter of accounting book entries.

Of course the Bundesbank is unlikely to admit this. Otherwise its tale of its melting gold bars stored untouched at the New York Fed for more than 50 years would have been in vain.

For years now the German Precious Metal’s Society’s “Repatriate our Gold” campaign has demanded to see the original German gold bars in the New York, London, and Paris vaults where they supposedly were stored. But neither the Bundesbank nor the New York Fed have ever provided any evidence — photos, complete bar numbers, videos of the bar melting, etc.

All we ever received were foggy statements with incomplete bar numbers, worthless bar lists, and incomplete “internal audit” reports.

But if Germany’s gold bars stored abroad were actually only paper gold claims and book entries, everything that has happened would make perfect sense.

Only now, after years of public pressure, some of the gold seems to be becoming physical in the course of its transmission over the Atlantic Ocean.

Only now does the Federal Reserve seem to “wire” the gold to Europe, where the Bundesbank can buy new gold bars.

Now the Fed and Bundesbank can avoid forever having to display 120,000 bars of German gold from the 1950s and 1960s, most of which likely never existed.

Thank you, DPA-AFX, and thank you, Bundesbank, for some truth after all this time. Thank you for this overdue admission of the Bretton Woods “gold book entry” world of the 1960s.

Thank you for a peek into the obscure world behind the curtains and vaults of central banking, back in the 1960s as well as today.

Unfortunately, the misleading news about our gold continues in Germany.

While Bundesbank director Carl-Ludwig Thiele announced December 24 that the Bundesbank has “repatriated” another 200 tonnes of gold from New York and Paris —

http://www.reuters.com/article/germany-bundesbank-gold-idUSL5N1EI4IY

— details will come only in January, and we still lack transparency in the Bundesbank’s own vault in Frankfurt. Here too we have never received a full bar number list — an “inventory number” list, which we have, is worthless — have never seen photos or video of the approximately 125,000 bars that supposedly are in Frankfurt now, have never seen a signature by an external auditor who has performed a physical audit on site in the Frankfurt vault.

Our conclusion: Our Repatriate our Gold campaign is satisfied with some material progress both on the physical and information front. Here at the end of 2016, Germany now has about 47 percent (1,580 tonnes) of its gold in Frankfurt.

But we remain unsatisfied with the evidence given by the Bundesbank to support its claim that “all bars are in Frankfurt physically and ownership is exclusive — that is, no multiple owners of individual bars, no fractional gold banking.”

And the DPA-AFX news item indicating that the German gold held at the New York Fed was just paper gold, just book entries, prompts us again to urge the Bundesbank to repatriate not just half our gold, the Bundesbank’s official objective since 2013, but all of it.

A golden currency reserve has to be on a country’s own soil without counterparty risk, especially when our new currency, the euro, is being rescued every day with billions in guarantees and illegal bond purchases by the European Central Bank and seems to be approaching the natural end of its unnatural existence as a supranational currency.

* * *

end

A terrific commentary from Alasdair Macleod showing the stupidity of Modi in his attempts to curb the appetite of gold by Indian citizens

(courtesy Alasdair Macleod)

| The economic consequences of Mr Modi |

— Published: Friday, 30 December 2016 | Print | 3 Comments

By: Alasdair Macleod – .comTwo weeks ago, India’s Prime Minister Narendra Modi demonetised an estimated 86% of rupees in circulation, offering conversion into a bank account or into smaller currency notes until 31 December, after which these notes will have no redemption value.Together with forgeries in circulation, it could be over 90% of all circulating money. The terms of redemption are so inconvenient for anyone other than black-marketeers, that for all purposes $50bn equivalent of rupees have been eliminated from the economy at a stroke, pending the introduction of new currency notes. The sadness in all this is that Modi should have foreseen the extent of the disruption to the poor and rural communities, but has obviously forgotten the hard lessons of life learned in his youth as a lowly chai wallah. It could be that the Reserve Bank went along with it as a government puppet, consoling itself with the thought it would be a good way to write off obligations, believing a significant quantity of notes is likely never to be redeemed by black-marketeers and tax evaders. It effectively reduces the central bank’s obligations to the private sector at the expense of those the state likes least. However, the $10-20bn equivalent the state will make from it is less important than the disruptive economic effect and the likely impact on the rupee’s future purchasing power. The purpose of this article is to look at the economic consequences of Modi’s action. Initial estimates by western macroeconomists of the effect on GDP seems to be benigni. It could be because their contacts in India are typically the more highly-paid city bourgeoisie, who rarely spend cash except for tips, using bank and credit cards more normally for everyday purchases. These people would almost certainly welcome moves to bring illegal trading under control and extend the income tax base, playing down the negatives. However, the cash immediately removed amounts to about 2.5% of GDP, eventually to be replaced at an unspecified time in the future by the new notes bearing a portrait of the Mahatma. But while these notes are shortly to become available, it could take months to convert ATMs and ensure their widespread availability. If the long-term consequences will be to bring unrecorded transactions into the GDP statistic, some western macroeconomists postulate recorded GDP could end up rising faster than anyone expected before Modi’s action. This misses the point. Banning high denomination notes worth as little as $7.50 equivalent to be replaced by the new Ghandi notes has been a major disruption in most Indians’ lives, particularly for the rural population. Removing everyday money is like trying to run an engine without any oil in it. It seizes up, which is what the Indian economy is certain to do. India’s economy is therefore likely to face a short-term slump, which government economists will counter by reflating, in other words by increasing the quantity of money. It will do the economy no good, but nominal GDP, which is not the same thing, will eventually rise, to the satisfaction of the central planners. Behind the confusion in government economists’ minds is a false conviction that GDP records the performance of an economy. This is wrong. GDP is just a money-total at a previous point in time, and no more than that. It is not a measure of economic progress or regress. A change in GDP reflects only a change in the quantity of money in the economy, so it is perfectly possible for an economy to contract, or even collapse, while nominal GDP rises. Not only is this fatally misunderstood by today’s economists, but this outcome has become far more likely for India, and will simply end up generating more monetary inflation from the banking system. Behind the Indian authorities’ poor grasp of the economic consequences of their actions are misconceptions common with establishment economists everywhere. However, it is likely that central bankers in India and elsewhere are at least vaguely aware of the long-term danger of increasing price inflation. But the consensus in banking circles is that more money and credit may be required to stave off recession, and even systemic risk. And in the case of systemic risk, cash is a danger because it allows the public to expose a bank’s insolvency. If only cash was somehow replaced, there could perhaps be greater control over economic and systemic outcomes. All the signs of this loose thinking are there. We keep on hearing of central banks planning to do away with cash, and Modi’s action is consistent with this standpoint. His government is not only trying to eliminate black markets, but it is also brutally trying to eliminate economic dependence on physical cash. It rhymes with the direction of travel for central bank policy in the advanced economies as well as in the emerging. Doubtless, for this reason, central banks everywhere will be watching the Indian experiment closely. But we can easily guess what their analysis will conclude. If the experiment succeeds, it will encourage them to proceed with their own plans to digitise money and dispense with the folding sort. If it doesn’t, failure will be deemed to be due to the peculiarities of the Indian economy and the failure of the Reserve Bank to implement policy effectively, so they will proceed with their plans anyway. However, hopes that the elimination of cash will give central banks greater control over inflationary outcomes appear to be badly misplaced. Not only does history tell us the exact opposite is the case, and that the reality is central banks have no control over price outcomes, but subjective price theory also confirms. The pricing power of money is not and never has been in the control of central banks; it is a matter only for the users of money in their day-to-day transactions. Money’s use as money is wholly down to its public acceptance as money, as experience proves, and central banks’ abuse of this trust is ultimately dangerous, as so often demonstrated. For example, despite government diktats and heavy-handed enforcement, Zimbabwe’s currency has become at best, to put it politely, a replacement for another form of paper whose vital supply has been disrupted. The digital version has even less value, because it has no alternative use. India and GoldWe must return to the specific subject of India, and the likely outcome of Modi’s clumsy attempt to eliminate means of payment using cash. It is almost certainly going to backfire. Indians have little respect for government as it is, and this action will only convince them with renewed purpose to have as little to do with the government and its money as possible. When the new Gandhi notes come into circulation, they will likely be rejected as the preferred money by growing numbers of a rightly suspicious public. This means that the rupee’s purchasing power will diminish more rapidly than if Modi had not disrupted what had become a relatively stable monetary situation. Ordinary people in their actions are well ahead of western financial analysts, having quickly anticipated this outcome for themselves. Despite longstanding government attempts to persuade them otherwise, they are rushing to convert worthless rupees into the one form of money they have trusted for millennia and over which government has no control, gold. They know that priced in rupees, gold will be more expensive in the months to come, so anything that can be encashed will be encashed for gold, not rupees. This is the reason why gold in India is now trading at a substantial premium to international prices. The Indian government restricts its supply because it has always seen gold, correctly, as a challenge to its own fiat money. Accordingly, the central planners condemn gold as being more appropriate to history than today’s economic environment. And having dismissed its relevance as money and as a superior store of value to the rupee, they see gold imports as unproductive hoarding. The government and central bank also appear to make the mistake of believing that if gold imports were eliminated, the balance of trade would improve accordingly. The result is various acts and regulations since the Gandhi era have only encouraged gold smuggling. The importation of gold has never halted, and responding to every twist and turn of monetary policy has increased over the long-term, and will continue to do so following Modi’s clumsy action. The impact of government ineptness on the gold market is likely to be considerable. After a period of relative currency stability, gold demand, at the officially recorded level, had in fact declined earlier this year. The premium on gold was less than the new sales tax, putting many jewellers out of business, because they could not compete with smuggled gold, which bore no tax and attracted a lower premium than the sales tax. More jewellers will probably be put out of business by this latest action. Smuggling will consequently rise and rise, particularly if the rupee’s purchasing power declines because of escalating public distrust of it as money. The central banking community, headed by the Bank for International Settlements, was concerned at Indian gold demand increasing at a time when Chinese citizens were absorbing most of the world’s free supply of newly-mined and scrap gold. It is almost certain that the appointment of Raghuram Rajan in September 2013 as Governor of the Reserve Bank of India had much to do with the urgency to bring Indian demand for gold under control, because he was and still is the BIS’s establishment man. He has generally failed in this mission, and his tenure was not renewed for reasons unknown, other than he preferred to return to the calmer pastures of academe and his Vice-Chairmanship of the Bank for International Settlements. This is not characteristic of a career central banker at the height of his powers and influence. Perhaps Rajan realised his attempt to manage gold demand would never work, and Modi was proving too dangerous for his own legacy at the Reserve Bank to survive unblemished. He was recently quoted as saying that the RBI’s ability to say no to the government must be protected, some months after he declined the opportunity to serve a second term. Was this a reflection of something that happened? In conclusion, the surprise money-grab by the Indian authorities intensifies the public’s perception of a corrupt, overly-bureaucratic, and ineffective government. The public’s suspicion that government paper money is ultimately worthless will have, in its collective mind at least, gained immeasurable credence. An accelerating decline in the purchasing power of the rupee is the most likely economic consequence of Mr Modi, ultimately destabilising for both the country and his government. By: Alasdair Macleod – .com |

It’s War: World’s Purest Silver Producer Prepares To Join Class Action Lawsuit Against Bullion Banks For Price Rigging

Though Wall Street regulators and the mega-banks they purport to regulate have long said that there exists no manipulation in markets and that anyone making claims to the contrary is nothing short of a conspiracy theorist, recent revelations suggest that even the most well known financial institutions on the planet have been actively involved in rigging asset prices. We need look no further for confirmation of this fact than Deutsche Bank, which last year admitted the precious metals market has been rigged all along and agreed to pay nearly $100 million in settlements resulting from their direct involvement in the manipulation of gold and silver prices.

Now that the cat is out of the bag and Deutsche Bank has agreed to turn over documents implicating other banks in related schemes, major mining companies are preparing lawsuits of their own. Straight-shooting First Majestic Silver CEO Keith Neumeyer, who in 2015 was the first mining company head to issue a public statement on the manipulation of precious metals prices by a small concentration of players, has said that the company’s legal team is closely monitoring the situation

Citing loss of revenue, jobs and shareholder value Neumeyer said in an interview with SGT Report that his company will likely be preparing legal action against the bullion banks involved in the rigging of prices.

I have an intimate knowledge of what goes on on the trading floors… how front running occurs, how wash trading occurs, how spoofing occurs… I’ve been looking for an opportunity to step in… I’ve been very vocal… I’ve talked to many executives that are running other silver companies… When the Deutsche news came out I sent an email to the law firm that’s responsible for this lawsuit and I had a conference call with two lawyers… we spoke about this case… I can tell you that a couple of the CEO’s of some very prominent silver companies in the States have no interest in pursuing this… Other CEOs have said that they are interested in pursuing this with First Majestic.

We’re monitoring this. We’re going to follow it. We’re likely going to, at some point, add our name to the class action lawsuit.

Watch the full interview detailing Neumeyer’s views on global cash bans, what silver prices may do once the manipulation comes to an end, how precious metals will be affected by the incoming Trump administration, current supply and demand fundamentals and an update on his latest projects including Silver One Resources:

(Watch At Youtube)

Neumeyer and what appears to be a handful of other CEO’s in the industry are preparing to declare war on the banks that have been responsible for the price suppression schemes many knew to exist but couldn’t prove until now.

The problem was that the fox was left to guard the hen house, which of course led to an inevitable bloodbath:

It’s quite shocking to me… It’s very harmful to the shareholders…

…It is manipulation and it’s used frequently. There’s ways that the regulators can monitor it. They can see it happening. The exchanges know when false bids and offers get put into the system… Yet, the exchanges don’t step in because the exchanges are owned by the banks… and the banks are doing that kind of trading… It’s the self policing system, which doesn’t work because no one wants to police themselves because they’re all making too much money.

How does Bank of America or JP Morgan not have a losing day year-after-year of trading… it’s actually impossible… traders lose money… it happens all the time… yet they have not had a single losing day for at least a couple of years as far as I know.

As Neumeyer correctly highlights, it’s impossible for a trader or firm to have such a perfect record, unless of course they are working the system, which certainly appears to be the case based on the evidence.

Now that market manipulations have been proven at the highest levels of the bullion banking system, and with the pressure of lawsuits mounting, there is a distinct possibility that precious metals prices will be allowed to trade freely on the open market.

Such a development bodes well for precious metals investors, especially with Donald Trump set to take over the Presidency in a few short weeks. Neumeyer notes that several Trump appointees are gold-friendly, which could add further upside potential:

On a positive note regarding Trump, he’s got a couple of pro-gold individuals that he’s appointed to his inner circle and I’m looking forward to them starting to make some gold favored policies that will help us as a mining company and our investors as well.

Summing up, Neumeyer hints that precious metals could do very well in the years to come:

We’re in very uncertain times… the world is changing.

If history is any guide, global changes of this magnitude mean that the entrenched systems run by central banks and Deep State politics are set to be destabilized on a level we may have not witnessed in our lifetimes, which means assets like bitcoin, gold, and silver could become the safe havens of choice for investors.

end

|

end

Bill Holter with his message for the New Year:

by Bill Holter, JS Mineset:

While I had not planned on writing until next week, current events warrant commentary. This past week has been an absolute embarrassment for the U.S. The actions taken by Mr. Obama are unprecedented for any outgoing president. Thousands of pages of executive orders, land grabs, multiple accusations against Russia and of course throwing Russian diplomats out and the placing of new sanctions.

While I had not planned on writing until next week, current events warrant commentary. This past week has been an absolute embarrassment for the U.S. The actions taken by Mr. Obama are unprecedented for any outgoing president. Thousands of pages of executive orders, land grabs, multiple accusations against Russia and of course throwing Russian diplomats out and the placing of new sanctions.

It is crystal clear Obama is trying his best to sabotage Mr. Trump’s presidency, whether he starts World War III in the process is the obvious danger. The next three weeks may be the most dangerous three weeks in our planet’s history as the “launch codes” are in the hands of someone obviously not thinking correctly. Most all of the hurdles and traps being laid by Obama can be corrected, altered or abolished. I would imagine the easiest way to do this would be to investigate and prove that Obama is not a natural born citizen and thus never eligible to sit in the office of U.S. President. If this avenue is pursued (I truly hope it will be), anything signed by Obama’s pen would then be null and void. The ramifications could be far reaching and include all sorts of appointments including federal judges.

The one draconian act which cannot be reversed as I see it is the UN vote recognizing Palestinian land. The U.S. did not veto the vote which every previous president has done. I do not see a remedy for this as the vote was 14-0 with the U.S. abstaining and not using our veto power. This vote truly looks like it was brokered by Mr. Obama, one of his few well thought out dangerous acts. The situation with Israel and the Middle East will now be altered permanently unless I am missing something?

The question of whether Mr. Trump is a Trojan horse or not should be answered almost immediately after the inauguration. I personally believe (and truly hope) Mr. Trump is real and does care about the United States as a nation. One area I am skeptical of is Congress. It is not clear to me whether or not both houses will do what the American people put them in office to do. It is very possible the republicans try to obstruct Mr. Trump’s nationalist/populist policy with their own bought and paid for globalist policy. It is 100% clear to me the takedown of the U.S. (from within) has been the plan for many years. I do not believe Mr. Trump was any part of “the plan” but we will soon find out.

We may even find out on January 6th as Congress counts the electoral votes. They do have a Constitutional avenue to still rebuff the vote and make their own choice. I do not believe this will be done as riots will follow with Congressman hanging from lampposts across the nation. Rather, I do believe it’s a good possibility the republican Congress will be obstructionist in subtle if not outward ways.

Folks, do not let your guard down. The next three weeks are certainly scary, any number of false flags could be unleashed. At least the previous efforts to spread bogus news have not worked as the evidence has not existed and the American people (for the most part) have seen through it. These are unprecedented times in every fashion, the “normal” we as Americans used to know will unfortunately never return during our lifetimes. Stay focused, whether you know it or not yet, we are at war!

Standing watch,

Bill Holter

Holter-Sinclair collaboration

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan DOWN to 6.9605(HUGE DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS A BIT TO 6.9716 / Shanghai bourse CLOSED UP 32.28 POINTS OR 1.04% / HANG SANG CLOSED UP 149.84 OR .68%

2. Nikkei closed /USA: YEN RISES TO 118.22

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index RISES TO 103.50/Euro DOWN to 1.0384

3b Japan 10 year bond yield: RISES TO +.046%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 118.22/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.93 and Brent: 58.02

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +238.%/Italian 10 yr bond yield UP 3 full basis points to 1.836%

3j Greek 10 year bond yield FALLS to : 6.97%

3k Gold at $1150.75/silver $16.06(8:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 59/100 in roubles/dollar) 60.56-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a BIG DEVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 118.22 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.03.06 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0701 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.196%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.501% early this morning. Thirty year rate at 3.115% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

2017 Starts Off With A Bang: US Futures, Oil Jump On Upbeat China Data; Europe Enters Bull Market

Rumors of the Trumpflation rally’s death have been greatly exagerated, and not only is the Dow 20,000 back on the radar, following a 124 point surge in Dow futures, bringing the “key psychological level” back within 100 points, but European stocks rose for a third day and entered a bull market, rising 20% from theor lows set last February, following strong Chinese manufacturing and services PMI data, both of which ended 2016 on robust notes well inside expansion territory.

While much of Europe had been open on Monday, it was the first day back for its biggest stock market, Britain’s FTSE 100 and it wasted no time in hitting a new record high of 7,196 points with a 0.7% gain. Germany’s DAX and France’s CAC 40 climbed too and among individual stock movers, Italian banks were back amongst the top risers, with newly-merged Banco BPM up 4.6 percent on its second day of trading. Overall, the Stoxx Europe 600 Index advanced 0.8% at 8:33 a.m. in London, with 18 of 19 industry segments climbing. The benchmark index, up 20 percent since a low last February, will confirm a bull market should the day’s gains hold into the close. The U.K.’s FTSE 100 Index, trading for the first time in 2017, is up 0.7 percent and heading for a record close.

US equity futures on the S&P 500 Index rose 0.7 percent, back over 2,251, while the Dow Jones was set to open back over 19,900.

In a reversal from the first trading days of 2016, when a selloff in Chinese equities roiled markets globally, the world’s second-largest economy has been a source of strength at the start of 2017. Weekend reports showed China’s official factory gauge steadied while services remained robust, capping a year of improvement in both indicators. A private manufacturing measure released Tuesday came in better than anticipated.

“A year ago, the Chinese markets kept everyone on their toes,” said Jingyi Pan, a market strategist at IG Asia Pte. “A year later, the outlook certainly appears to be more optimistic, though we may have to bring back the catchphrase of ‘cautious optimism’ going into the new year as we search for clarity.” “I don’t think that we will see a repeat given that the global economy has a better foothold compared to a year ago,” Pan said.

Overnight in Asia, MSCI’s broadest index of Asia-Pacific shares rose 0.6 percent as most regional markets reopened after the New Year holiday although Japan’s Nikkei was still closed. Australian shares were the best performers in the region, closing up 1.2 percent. Hong Kong’s Hang Seng .HSI rose 0.7 percent while in China, both the CSI 300 index and the Shanghai Composite .climbed 1 percent. China was Asia’s worst performing major stock market in 2016 with a 11.3 percent loss in its worst year in five.

Commodity-linked stocks jumped 1.3 percent as oil and metals prices cheered the China data that had showed output from the country’s giant manufacturing sector reaching a near six-year high. It bolstered the ‘reflation’ theme that dominated the latter stages of 2016 and helped get currency and bond markets back in their pre-break rhythm after a mixed recent run. The U.S. dollar racked up its biggest rise in almost three weeks against a basket of the world’s other major currencies to leave it just 1 percent off December’s 14-year high. As shown in the chart below, the Dollar Index (DXY) jumped as US yields moved sharply higher, w/ 10y yields rising from 2.4350% to over 2.51%.

In commodities, oil prices jumped over 2% in Europe as the China data fed into a market that is being buoyed by hopes a deal including OPEC and non-OPEC producer countries will drain the recent global supply glut. Oil was the world’s best-performing major asset class in 2016, with a gain of around 50 percent and global benchmark Brent was up 2.7% at $58.31 by 0945 GMT as U.S. crude topped $55 a barrel.

“Markets will be looking for anecdotal evidence for production cuts,” Ric Spooner, chief market analyst at CMC Markets said. “The most likely scenario is OPEC and non-OPEC member countries will be committed to the deal, especially in early stages.”

The positive Chinese news lifted the Australian dollar, which added 0.6 percent to $0.7230, while gold sagged, with the precious metal dropping 0.3 percent to $1,148 an ounce. Back in Europe, the pick ups in Germany and French inflation came on the heels of data on Monday showing manufacturers ramped up activity at the fastest pace in more than five years in December.

In China, Starting on Jan. 1, the number of currencies in the CFETS basket increased to 24 from 13, with new entrants including the Korean won, the South African rand and the Mexican peso. The country’s foreign exchange regulator also said it would step up scrutiny of individuals’ foreign currency purchases and strengthen punishment for illegal outflows, although the $50,000 annual individual quota will remain unchanged. The renminbi posted its biggest annual loss since 1994 last year, with the dollar up almost 7 percent versus the Chinese currency.

Long-term inflation expectations in the euro zone, measured by the five-year, five-year forward rate are near their highest levels in more than a year and close to the ECB’s near 2 percent target, as the central bank prepares to pare back the pace of its money-printing scheme. “Until just a few weeks ago, the general consensus was that upside inflation risks were very limited however… the inflation rate scheduled to be published today is likely to reveal a significant uplift,” DZ Bank strategist Birgit Figge told Reuters.

So with stocks rising on hopes of a return in inflation, it would mean that rates should dip, and indeed Treasuries dropped, with 10-year yields rising 7 bps basis points to 2.514%. U.S. cash bonds opened in London this morning having been closed since Dec. 30. German bonds fell as regional data showed inflation is accelerating. The yield on the nation’s 10-year securities dropped to the lowest level since November on Monday. French bonds were among the biggest decliners in Europe after the nation was said to mandate banks for the sale of a new Green bond in the 15- to 30-year area. France is due to sell 10-, 20-, 30- and 50-year bonds on Jan. 5.

* * *

Market Snapshot

- S&P 500 futures up 0.7% to 2251

- Stoxx 600 up 0.7% to 366

- FTSE 100 up 0.7% to 7194

- DAX up less than 0.1% to 11603

- German 10Yr yield up 2bps to 0.21%

- Italian 10Yr yield up less than 1bp to 1.75%

- Spanish 10Yr yield up 2bps to 1.36%

- S&P GSCI Index up 0.7% to 400.9

- MSCI Asia Pacific down 0.2% to 135

- Nikkei 225 closed

- Hang Seng up 0.7% to 22150

- Shanghai Composite up 1% to 3136

- S&P/ASX 200 up 1.2% to 5733

- US 10-yr yield up 4bps to 2.48%

- Dollar Index up 0.38% to 103.17

- WTI Crude futures up 1.4% to $54.46

- Brent Futures up 1.6% to $57.71

- Gold spot down less than 0.1% to $1,151

- Silver spot up 0.4% to $16.00

Top Healdine News

- Jain Finds His Second Act as Ex-Deutsche Bank Chief Joins Cantor: Smaller firm hires global bank’s former rainmaker as president

- China’s Sogou Targets IPO at $5 Billion Valuation to Chase Baidu: Listing of about 10% of shares in U.S. may happen this year

- LSE Agrees to Sell Clearing Unit to Euronext for $533 Million: Deal may be completed by the end of the second quarter

- China’s Factories, Services Cap Year of Gains as Prices Rise: Private manufacturing PMI by Caixin and Markit confirmed the strength in official data

- SpaceX Plans Return to Flight With Jan. 8 Launch After Explosion: Liftoff from Vandenberg Air Force Base first since Sept. 1

- BlackRock ETFs Attract Record $140 Billion on Bonds, Smart Beta: Investors added $27 billion to U.S. Core ETF after price cut

- Fiat Chrysler Pauses From Gas-Guzzlers to Show Electric Minivan: Automaker unveils self-driving Chrysler Portal concept at CES

- ‘Rogue One’ Takes in $64.3 Million for Disney Over Weekend: Movie industry sets record with $11.4 billion in annual sales

- Pence, House Republicans to Talk Obamacare Repeal Wednesday

- Comcast, 21st Century Fox Reach Agreement on Fox News: WSJ

Asian equity markets began the first session of 2017 on the front-foot despite last Friday’s negative close on Wall St where all 3 major indices finished lower and the DJIA retreated further away from 20,000. ASX 200 (+1.1%) led the Asia-Pac region and posted a fresh 16-month high amid broad based gains, with only the gold sector trading in the red. Shanghai Comp. (+1.0%) and Hang Seng (+0.6%) conformed to the upbeat tone following better than expected Chinese Caixin Manufacturing PMI data which rose to a near 4-year high and printed a 6th consecutive month in expansion territory, although gains across the region have been somewhat reserved amid rising money market rates in China and several market closures including Japan.

Top Asian News

- China Gets Stricter on Forex Transactions to Limit Outflows: Citizens face extra disclosure requirements even as yearly quota of foreign currency was unchanged

- Indonesia Terminates JPMorgan Partnerships After Downgrade: Finance ministry will stop using JPM as primary dealer, underwriter of sovereign bonds

- South Korea Halts Some Nissan, BMW Sales in Emissions Probe: Total fines of $5.9 million slapped on three companies

- Infosys, Wipro Leaders Warn of Challenging Times for Indian IT: Warn that industry faces grave threat from rising political, economic conflict around the world

- China to London Freight Train Kicked Off as Xi Boosts Trade Ties: Train will cover more than 7,000 miles in about 18 days

In Europe, 2017 has kicked off as 2016 finished, with equities trading higher for much of the morning as the FTSE hits fresh all-time highs (+0.6%). Stock specific news has been relatively light so far today, however notable outperformance has been seen in the financial sector, with energy names also outperforming amid WTI crude futures printing 18-month highs. The Stoxx Europe 600 Index advanced 0.8% at 8:33 a.m. in London, with 18 of 19 industry segments climbing. The benchmark index, up 20 percent since a low last February, will confirm a bull market should the day’s gains hold into the close. The U.K.’s FTSE 100 Index, trading for the first time in 2017, is up 0.7 percent and heading for a record close. The latest data has been supportive of bond yields, with the German 10Y briefly moving above 0.24% amid the higher than previous regional CPIs, which have printed around 1.8-1.9% Y/Y so far. The latest German unemployment figures saw a fall in unemployment, further supporting yields. Elsewhere, Gilt yields have also seen strength this morning in the wake of a significant beat in UK Manufacturing PMI (56.1 vs. Exp. 53.3), seeing the highest reading since June 2014.

Top European News

- Pound Drop Boosts U.K. Manufacturing, Pushes Up Factories’ Costs: Manufacturing grew at the fastest pace in 2 1/2 years in December

- German Unemployment Extends Drop as Economic Growth Picks Up: Unemployment fell by 17,000 versus estimated 5,000 decline

- Paris Eyes Luring 20,000 Bankers From London Amid Brexit Rupture: French lobby group sees banks ‘accelerating’ their planning

- Biggest Swedish Business Group Predicts Weak Krona Won’t Last: Stronger currency could have ‘fast and unpleasant’ effect

In commodities, crude oil rose to $55.24 a barrel in New York, touching the highest level since July 6, 2015, buoyed by hopes that a deal between OPEC and non-OPEC members to cut production, which kicked in on Sunday, will drain a global supply glut. Benchmark Brent crude jumped more than 2 percent to a high of $58.37, up $1.55 a barrel and its highest since July 2015. By 0940 GMT (4:40 a.m. ET), Brent eased slightly to trade at $58.22, up $1.40. Gold added 0.1 percent to $1,148.5. Aluminum increased 0.1 percent to $1,694 per metric ton on the London Metal Exchange, while nickel jumped 1.6 percent to $10,180 a ton and copper rallied 1 percent to $5,593 an ounce.

In currencies, the Dollar Index was up 0.7 percent. The yen slid 0.5 percent to 118.14 per dollar, giving up an earlier advance. The euro erased earlier gains against to trade down 0.4 percent against the greenback. South Korea’s won rose 0.4 percent, while the Australian dollar strengthened 0.3%.

US Event Calendar

- 9:45am: Markit U.S. Manufacturing PMI, Dec. F, est. 54.2 (prior 54.2)

- 10am: ISM Manufacturing, Dec., est. 53.7 (prior 53.2)

- 10am: Construction Spending MoM, Nov., est. 0.5% (prior 0.5%)

* * *

DB’s Jim Reid concludes the overnight wrap

A very Happy New Year to all our readers this morning and a warm welcome to 2017. Today’s EMR is a bit of a bumper edition and concludes with the December, Q4 and 2016 performance review at the end. It would probably be an understatement to say that 2016 has been – more than ever – a year in which we’ve all had to put our political analyst hats on. Trump and Brexit were the obvious headline events which characterised 2016 but that’s not to say that Central Banks haven’t been busy too with the Fed, BoJ, ECB and BoE all keeping us busy and laying the platform to what we think will be a volatile year ahead for rates. Commodity markets have also more than played their part, with a number of benchmark commodities hitting record lows early in the year before staging a remarkable rebound into year end. The good news is that the vast majority of assets ended the year on a high in December with 30 of the 39 assets within our sample (excluding currencies) delivering a positive total return last month in USD hedged terms.

As well as this, we’ve also got the usual week ahead preview at the end. Despite it being a holiday shortened week there’s little easing into the New Year with the diary fairly jam-packed with important releases. One of the highlights will be the FOMC minutes from the December meeting, due on Wednesday evening, which could be interesting given the slightly more hawkish than expected elements from the statement and of course the excitement caused by the moves in the dots. Also on the cards for this week is the US December employment report on Friday including the ever-important nonfarm payrolls print. We’ll preview that later in the week. The manufacturing and services ISM prints will also be due out while in Europe we’ll also get a number of December inflation reports due out over the next few days. Away from the data President-elect Trump should also continue to fill in the blanks of his administration ahead of his official inauguration later this month. So plenty to keep us on our toes and to talk about.

For those that took a break over the holiday season, in truth you haven’t missed too much. Markets did reopen in parts of Europe yesterday although unsurprisingly with the usual holiday impacted low volumes. That said it was a decent start for the most part to 2017. The Stoxx 600 kicked off the year by closing up +0.49% with all sectors ending a tad higher while the DAX (+1.02%) and the periphery (IBEX +0.71% and FTSE MIB +1.73%) also closed firmer. European Banks (+0.89%) also started the year stronger while in sovereign bond markets it was BTP’s which outperformed. Indeed 10y BTP yields were 7.3bps lower at 1.735% while 10y Bund yields edged down 1.8bps to 0.182%. The outperformance in Italy likely reflected the better than expected December manufacturing PMI yesterday with the print rising a full point to 53.2 and the highest reading since June. There were no surprises in the final revision for the data for the Euro area at 54.9 while France and Germany were also little changed at 53.5 and 55.6 respectively. Spain however also surprised to the upside after printing 0.8pts higher at 55.3 (vs. 54.6 expected).

Two days ago we also got the official PMI’s for China for last month with the manufacturing PMI down slightly to 51.4 (vs. 51.5 expected) from 51.7 the month prior and the non-manufacturing PMI coming in at 54.5 versus 54.7 in November. This morning we’ve also had the Caixin manufacturing PMI for China which, unlike the official data last week, surprised to the upside at 51.9 (vs. 50.9 expected) from 50.9 in November. As we look across markets this morning, bourses have started the year in a fairly upbeat mode. In China the Shanghai Comp and CSI 300 are currently +0.75% and +0.82% respectively while the Hang Seng is +0.51%. The Kospi is +0.52% and the ASX +1.17%. Markets in Japan are closed for a public holiday. Elsewhere Oil is a shade higher while Gold and other precious metals are up close to +1%. US equity index futures are also pointing to a reasonable start (up around +0.35% as we type).

Much of the remaining newsflow this morning and over the past few days revolves around other developments in China and also the tragic terrorist attack in Istanbul on New Year’s Day which follows a number of other geopolitical events in the month of December and which will do little to ease tensions. The Turkish Lira has weakened about half a percent in the last two days since that attack. With regards to the former, there are various reports out there suggesting that China is looking to tighten controls on personal FX transactions in a bid to curb money laundering. According to the FT the $50k resident quota on foreign currency buying was also reset as of January 1st. In addition to this, last week we learned that China has also expanded the currencies included in its official CFETS basket to 24 from 13. The associated statement highlighted that this change is aimed at improving the mechanism generating the RMB index and so making the basket more representative. It also means that the US Dollar’s weighting in the new basket falls to 22.4% from 26.4% and so the lower USD weight means that less USD strength translates into the basket.

Turning over to the week ahead now. This morning in Europe we’re kicking off the New Year in France where the preliminary December CPI report will be released. We’ll also get last month’s CPI report in Germany along with unemployment data while in the UK the December manufacturing PMI is due to be released. It’s a reasonably busy start to the week in the US this afternoon with the main focus likely to be on the December ISM manufacturing print, while the final manufacturing PMI and construction spending in November is also due. Wednesday starts in Japan where the final manufacturing PMI for December is due while China will also release the MNI consumer sentiment print for last month. Over in Europe all eyes will be on the final December PMI revisions (services and composite prints) along with a first look at the data for the periphery. Euro area CPI in December will also be released along with money and credit aggregates data for the UK. In the US tomorrow the lone data release is December vehicle sales before all eyes turn to the FOMC minutes later in the evening from last month’s meeting. Turning to Thursday, Japan and China get the day started again with the remaining December PMI’s (services and composite). In the UK we’ll also get the remaining services and composite PMI’s while PPI data for the Euro area will also be released. In the US we’ll also get those final PMI’s (services and composite) along with the ADP employment change print for last month, initial jobless claims and ISM non-manufacturing for December. We close out the week on Friday in Europe with retail sales and factory orders data in Germany, trade data in France and confidence indicators for the Euro area. In the US we’ll get the November trade balance along with the all important December employment report including nonfarm payrolls. Also due out will be November factory orders and the final revisions to November durable and capital goods orders.

Away from the data there’s also a bit of Fedspeak this week with both Evans and Lacker due to speak on Friday, while over at the ECB Mersch is also scheduled to speak on Friday. Also potentially interesting this week is a planned television interview in France on Thursday with Socialist Party nominee Manuel Valls.

end

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 32.28 POINTS OR 1.04%/ /Hang Sang closed UP 149.84 OR .68%. The Nikkei closed /Australia’s all ordinaires CLOSED UP 1.15%/Chinese yuan (ONSHORE) closed DOWN at 6.9605/Oil ROSE to 54.93 dollars per barrel for WTI and 58.02 for Brent. Stocks in Europe: ALL IN THE GREEN . Offshore yuan trades 6.9716 yuan to the dollar vs 6.9605 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS MORE USA DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES /

3a)THAILAND/SOUTH KOREA/:

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

Sunday night

More capital controls in China and that sends bitcoin over $1,000 to $1024

(courtesy zero hedge)

Bitcoin Surges Above $1,000 As China Unveils New Capital Controls

As noted yesterday, for the first time in three years, and only the second time in history, bitcoin rose above $1,000 in Yuan-denominated Chinese trading, however it was limited to the lower side of this “round number” psychological barrier in US trading, as BTC flirted with $999.99 for most of the day on the popular Coinbase exchange, without crossing it.

Overnight, however, Chinese demand proved too great and US markets had no choice but to arb the difference. So with Bitcoin trading in China at an implied price of over $1,050 at this moment, bitcoin finally soared above $1,000 in the US as well, trading just around $1,024 on Coinbase as of this moment.

Various catalysts for the recent surge have been cited, chief among which is the ongoing crackdown against cash in India providing a new source of demand for bitcoin. However, the most immediate driver of the recent burst in Chinese demand originates, not unexpectedly, from China where Beijing over the weekend implemented even more of what we have said since September 2015 will keep pushing bitcoin relentlessly higher: capital controls.

Recall that as we noted over the weekend, in order to further curb capital outflows, Chinese banks will be required to report all yuan-denominated cash transactions exceeding 50,000 yuan (around 7,100 US dollars) to the People’s Bank of China (PBOC), down from the current level of 200,000 yuan, according to a PBOC document released on Friday. Cross-border transfers more than 200,000 yuan by individuals will also be subject to the report process. In terms of foreign currencies, the report threshold remains at the equivalent of 10,000 US dollars for both cash transactions and overseas transfers.

How do we know that this latest PBOC intervention in capital markets was merely the latest form of capital controls? Because the PBOC immediately said it wasn’t.

As Xinhua reported overnight, “the policy stoked worries that the government is trying to impose capital control in a disguised form.”

“It is not capital control at all,” central bank economist Ma Jun said.

Actually, imposing limits on capital movement, i.e. controls, is by definition just that.

Logic, however, did not prevent Ma from continuing on a tangent, and he “explained” that the responsibility of report will be assumed by financial institutions, and there will be neither extra documentation nor official approval procedures for businesses and individuals. “They will not feel any change,” Ma added. He also noted that each person’s current annual foreign exchange purchase quota of 50,000 US dollars is unchanged, and normal activities, ranging from business investment and operation abroad to individuals’ overseas trips and study, will not be affected, Ma said.

The PBOC has said the move aims to improve monitoring of money laundering, financing for terrorists, graft and tax fraud, instead of targeting common business activities. Appealing to the Chinese savers not to withdraw their money out of fears of even more capital controls, Ma said that the world’s major countries also have similar rules, citing that transactions worth 10,000 US dollars or more are subject to reporting in the United States, Canada and Australia. Regulators in those countries can even adopt stricter rules if necessary after obtaining legal authorization, Ma said.

Judging by the move in Bitcoin since the announcement, nobody believes Mr. Jun.

And yet, what is surprising is that if China indeed wishes to limit capital flight by bitcoin it could easily do so with the flip of a switch, sending the price plunging. As we noted recently, according to Bloomberg sources, Chinese officials have been considering policies including restricting domestic bitcoin exchanges from moving the cryptocurrency to platforms outside the nation and imposing quotas on the amount of bitcoins that can be sent abroad. Further indicating that Chinese regulators were “just a little behind the curve”, they allegedly noticed only recently that some investors bought bitcoins on local exchanges and sold them offshore, evading rules on foreign exchange and cross-border fund flows, the report further reveals.

A quick look at the uncanny correlation between the decline in the Yuan and the rise in the bitcoin, confirms that the digital currency has indeed been largely used to evade capital controls.

Based on this chart alone, the recent surge in Bitcoin would imply that a substantial devaluation of the yuan is looming. That, or even more aggressive capital controls.