Gold at (1:30 am est) $1179.70 UP $15.90

silver at $16.58: UP 8 cents

Access market prices:

Gold: $1180.40

Silver: $16.58

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Jan 5/17 (10:15 pm est last night): $ 1188.91

NY ACCESS PRICE: $1740.25 (AT THE EXACT SAME TIME)/premium $14.66

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1195.33

NY ACCESS PRICE: $1177.25 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $18.08

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Jan 5/2017: 5:30 am est: $.1173.05 (NY: same time: $1173.35 5:30AM)

London Second fix Jan 5.2017: 10 am est: $1176.80 (NY same time: $1176.80 (10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 13 NOTICE(S) FOR 1300 OZ. TOTAL NOTICES SO FAR: 1023 FOR 102,300 OZ (3.1819 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 110 NOTICE(s) FOR 550,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 307 FOR 1,535,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 553 contracts UP to 164,365 with respect to YESTERDAY’S TRADING (short covering by the banks). In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .821 BILLION TO BE EXACT or 117% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 110 NOTICES FILED FOR 550,000 OZ.

In gold, the total comex gold FELL BY 1065 contracts DESPITE THE RISE IN THE PRICE GOLD ($3.40 with YESTERDAY’S trading ). WE MUST HAVE HAD SHORT COVERING.The total gold OI stands at 423,608 contracts.

we had 13 notice(s) filed upon for 1300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 813.87 tonnes

.

SLV

we had no changes in silver into the SLV

THE SLV Inventory rests at: 341.199 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver ROSE by 553 contracts UP to 164,305 AS SILVER ROSE by $0.15 with YESTERDAY’S trading. The gold open interest FELL by 1,065 contracts DOWN to 423,608 DESPITE THE FACT THAT THE PRICE OF GOLD ROSE BY $3.40 WITH YESTERDAY’S TRADING

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) FRBNY report on earmarked gold movement

(Harvey)

3. ASIAN AFFAIRS

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

i)Wednesday night/9 pm est

This is nuts: Overnight lending rates between banks skyrockets to 45%. And now Bitcoin is trading higher than gold: Bitcoin $1252.00 usa/gold 1172.usa. Offshore yuan 6.8870 as the shorts are getting crushed!

( zero hedge)

ii)Thursday morning

The interbank lending rate between banks rose to 80% and the USA/CNH lowered (yuan rose) to 6.83. No doubt that this will stem the outflow of dollars temporarily. However China has to worry about the Donald taking control of uSA on January 20 and he will also use his wrath against China

(courtesy zero hedge)

iii)With the Chinese authorities stating that they were going to crack down on cryptocurrencies like Bitcoin, in an attempt to stop the outflow the dollars, finally we see Bitcoin collapse in price down 31% to $893.00 usa. The true currency, gold continues to rise:

( zero hedge)

iv)This is what happens when you try and grow your economy by 7% per year. The steel mills etc are running at full blast despite poor global demand. This causes poor air. Just look at the following story where a cruise ship could not dock in Beijing because they had no visibility

( zero hedge)

4 EUROPEAN AFFAIRS

Now we have Italy’s Grillo slamming mainstream media for fake news

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

i)Mexico is beginning to panic as they now believe that Trump will be true to his word;

( zero hedge)

ii)Next on the list, Donald tells Toyota not to build a plant in Mexico or face a huge border tax. More woes for Mexico

7. OIL ISSUES

i)DOE reports huge inventory build and down goes oil

( zero hedge)

ii)Strange: crude jumps on a report that the Saudi are fully impleminting their OPEC output cut

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)Brought this to your attention yesterday but it is worth repeating. Trump will push for the audit of the Fed and then we can see what the crooks have been doing behind the curtain

( Shroeder/The Hill/GATA)

ii)Saville has been anti gold for decades

( Chris Powell/GATA)

iii)The following bullion star infographic highlights the fractional gold reserve banking system orchestrated by the gold ETF’s. This is what I have been harping on for years:

( Ronan Manly/GATA)

10.USA STORIES

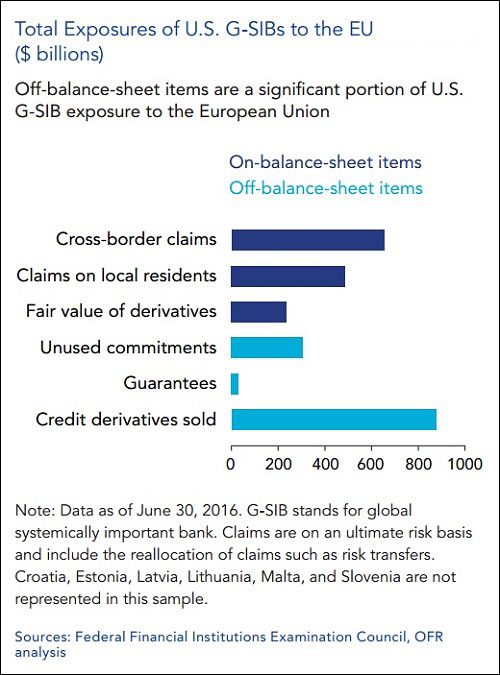

i)The following commentary is an essential reading to all. You must read this to understand what is going on. Five major uSA banks have mainly underwritten over 2 trillion USA credit derivatives on sovereign Europe and its banks. A failure by a European bank like Banco Monte dei Paschi de Sienna and Unicredit will bring the USA financial system:

( PAM AND RUSS MARTENS/WALL STREET ON PARADE)

ii)Just take a look at what the doorknobs are doing in Philadelphia: a huge tax on soda. It heightens their bill dramatically!

( Jim Quinn/BurningPlatform)

endiii)Now we see that the Russian hacking story has changed again. Now the media is suggesting that an intermediary sent the emails to Wikileaks

( zero hedge)

iv)Now Donald is going to attack the merger plan with Time Warner and A T and T

Federal Reserve Bank of New York:

Earmarked gold movements

December report:

Last Oct/2016 we had 7,841 million dollars worth “gold” in inventory at the FRBNY

valued at $42.22 per oz

Last November/2016 we had 7,841 million dollars worth of gold in inventory at FRBNY valued at $42.22 per oz

thus 0 oz moved at $42.22

So far officially, the following has been repatriated to BuBa from NY:

2013: 5 tonnes

2014: 120 tonnes

2015: 99.5 tonnes

2016: to be officially announced

Their total quota from NY is scheduled to be 300 tonnes and another 374 tonnes from Paris of which 177 tonnes of gold has officially been sent (Dec 2015) and thus another 197 tonnes to cross the English channel.

Germany has officially 1237 tonnes of gold “stored ” in NY. On conclusion of the repatriation, Paris will have 0 stored there.

end

Let us head over to the comex:

The total gold comex open interest FELL BY 1,065 CONTRACTS DOWN to an OI level of 423,608 DESPITE THE FACT THAT THE PRICE OF GOLD ROSE $3.40 with YESTERDAY’S trading. We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year.

With the front month of January we had a LOSS of 861 contracts DOWN to 153. We had 875 notices filed so we GAINED 14 contracts or AN ADDITIONAL 1400 oz WILL STAND for gold in this non active delivery month of January. For the next big active delivery month of February we had a LOSS of 5,083 contracts DOWN to 275,537. March had a gain of 80 contracts as it’s OI is now 196. We had considerable short covering yesterday as the bankers saw the writing on the wall.

We had 13 notice(s) filed upon today for 1300 oz

And now for the wild silver comex results. Total silver OI ROSE by 553 contracts FROM 163,812 UP TO 164,365 AS the price of silver ROSE BY $0.15 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI ROSE by 2 contracts RISING TO 466. We had 1 notice(s) filed on yesterday so we GAINED 3 or an additional 15,000 oz will stand for delivery. The next non active month of February saw the OI rise by 1 contract(s) up to 164.

The next big active delivery month is March and here the OI rose by 208 contracts UP to 133,789 contracts.

We had 110 notice(s) filed for 550,000 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 277,631 contracts which is very good.

Yesterday’s confirmed volume was 202,711 contracts which is very good

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

4,147.35

HSBC

129 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

4147.35 oz

JPMorgan

129 kilobars

|

| No of oz served (contracts) today |

13 notice(s)

1300 oz

|

| No of oz to be served (notices) |

140 contracts

14,000 oz

|

| Total monthly oz gold served (contracts) so far this month |

1023 notices

102,300 oz

3.1819 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,539,015.7 oz |

For January:

Today, 0 notice(s) were issued from JPMorgan dealer account and 13 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

1,552,084.880 0z

Scotia

CNT

Brinks

|

| Deposits to the Dealer Inventory |

157,596.400 OZ

CNT

|

| Deposits to the Customer Inventory |

1,221,349.550 oz

CNT

JPM

Scotia

|

| No of oz served today (contracts) |

110 CONTRACT(S)

(550,000 OZ)

|

| No of oz to be served (notices) |

356 contracts

(1,780,000 oz)

|

| Total monthly oz silver served (contracts) | 307 contracts (1,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,764,118.1 oz |

end

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver stories for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE

2017 – The Year of Banana Skin

2016 is behind us and we have started a new year with great gusto and no small measure of anxiety. The potential for unknown unknowns turning into banana skins is very high. Right now we are looking at:

- The broad US stock markets & the UK FTSE are breaking new highs

- Investment flows are rotating from Bonds to Equities on the back of a Trump driven reflation outlook

- Donald Trump is President Elect

- The Fed has initiated a long anticipated rise in interest rates

- Global Debt levels as a percentage of GDP has never been higher

- Britain is going through the painful process of divorcing itself from the EU,

- France is facing elections where far right and and anti EU parties may take power

- Italy’s banking system is in crisis with the weight of EUR 300 Billion in bad debts

- Germany’s Merkel is losing core support and the Anti – EU forces are gathering power

- China is being buffeted by global protectionist rhetoric and lacklustre domestic demand, can she manage the domestic discontented?

What could possible go wrong?

Many of these changes have their genesis in misguided monetary policy, specifically those pursued by the US Fed in the 1990’s and since, with micro management of economies via stimulus, artificial interest rates and the Pandora’s box that is Quantitative Easing. The risk of the “2 a.m. tweet” where policy is poorly stated or misunderstood is very real. What is of real concern is that many of the themes we identify are based on developments that are very new and lack much historic context, especially when one considers the scale of the economies that may be effected.

2017 market performance will be determined by a number of themes.

- Can Trump deliver reflation or are the markets set to be disappointed?

Trump has been elected on with a mandate to shake up the establishment, to protect US jobs and to focus internally. The question is can someone with no political experience, significant conflicts of interest, despised by the right and liberal factions, within the US political establishment, deliver? The short answer is that no one knows, but so far he has proven all is naysayers wrong and you would be a fool to bet against his form. The USD dollar has strengthened to its highest level since 1984 and this will certainly hurt US companies’ capacity to earn from foreign operations and thus suppress GDP. - Can the Fed normalise interest rates?

The Fed has taken that first tentative step and started its long awaited tightening cycle. The concern is with debt levels at such elevated levels, can institutions wishing to refinance do so at newer higher rates and what will this do to debt affordability? - Will Britain and the EU agree an amicable divorce or will it be a nasty drawn-out affair? The EU has appointed a French bureaucrat as its chief negotiator who is seen as a federalist and someone who maybe likely to seek to punish Britain for leaving. On the British side Britain’s ambassador to the EU resigned yesterday. His resignation note hinted at “muddled” thinking within the British camp.

Outlook for Gold

Positive on continued strong 2016 demand. In 2016 GoldCore experienced significant increases in our bullion storage programme. Clients moved cash out of banks which they believe may be subject to bail-in risks as governments and regulator capitalise the banking systems with depositors cash deposits. Clients also sold gold proxy investments such as Gold ETF funds and Digital gold holdings where clients are forced to hold unallocated and unsegregated gold holdings in favour of GoldCore Segregated and Allocated gold storage.

We do not see a change in this trend and with strong account openings and a massive increase in interest from corporate treasurers seeking to diversify bank risk, we are very bullish for gold demand in the year ahead.

Allocations for gold should be between 5% and 20% depending on a clients risk appetite. Significant systemic risk is very real and can materialise from a number of sectors. Bank deposits remain at very real risk and diversification is advisable.

END

the crook Jon Corzine settles with the CFTC over the MF Global scandal

(courtesy zero hedge)

Jon Corzine Settles Over MF Global Collapse: Agrees To Lifetime Ban, $5 Million Fine

Three years ago, in February 2013, traders were outraged upon learning that the National Futures Association refused to ban former MF Global chief Jon Corzine from trading with other people’s money, rejecting a motion brought before that body’s board of directors to do so. The decision was a blow to a vocal group within the commodities trading world who – noting that Corzine has not been held accountable by the government for alleged crimes – wanted to see him publicly upbraided by his peers in the market.

All that changed today when Corzine agreed to pay a $5 million civil fine to settle a lawsuit by the U.S. Commodity Futures Trading Commission over the 2011 collapse of the former New Jersey governor’s brokerage, MF Global Holdings. More importantly, under the settlement disclosed on Thursday, Corzine also agreed to be barred for life and never again work for a futures commission merchant, or register with the CFTC in any capacity.

Which means Corzine’s dreams of running a hedge funds are now over.

“I am pleased to have reached this settlement to resolve the CFTC’s claims,” Corzine, 70, said in a statement. “As the CEO of MF Global in 2011, I have accepted responsibility for its failure, and I deeply regret the impact it had on customers, employees, shareholders and others.”

The CFTC alleged Corzine failed to fix inadequate controls that led to $1 billion in missing customer funds and knew of the New York-based firm’s extreme cash shortage. The agency also said he didn’t ask questions about the origins of funds used to make transfers that he had ordered. Corzine previously said he never directed the misuse of customer funds to help his firm stay afloat as it dealt with margin calls on bad bets in 2011 as Bloomberg notes. He testified to Congress that he asked that overdrafts with JPMorgan Chase & Co. be corrected. In 2013, MF Global’s brokerage unit was fined $100 million by the CFTC and admitted regulatory failures.

Edith O’Brien, MF Global’s former assistant treasurer, agreed to pay a $500,000 civil fine and accept an 18-month ban to settle related claims.

Thursday’s settlement resolves the last piece of litigation against Corzine stemming from MF Global’s Oct. 31, 2011 bankruptcy.

end

Brought this to your attention yesterday but it is worth repeating. Trump will push for the audit of the Fed and then we can see what the crooks have been doing behind the curtain

(courtesy Shroeder/The Hill/GATA)

‘Audit the Fed’ bill gets new push under Trump

Submitted by cpowell on Wed, 2017-01-04 19:55. Section: Daily Dispatches

By Peter Schroeder

The Hill, Washington, D.C.

Wednesday, January 4, 2017

Controversial legislation to subject the Federal Reserve’s monetary policy powers to outside scrutiny is getting new life in Washington.

Rep. Thomas Massie, R-Ky., and Sen. Rand Paul, R-Ky., have re-introduced legislation to “audit the Fed” after a similar effort stalled in the last Congress.

But such a proposal, which has been vocally opposed by Federal Reserve Chairwoman Janet Yellen, may face its best odds ever of becoming law. Both chambers are controlled by Republicans long critical of the Fed’s policies, and President-elect Donald Trump has heaped scorn on the central bank since the beginning of his presidential campaign.

Paul specifically mentioned Trump in a statement about the bill today, making clear the measure’s proponents believe they have an ally in their cause coming to the White House. …

… For the remainder of the report:

http://thehill.com/policy/finance/312662-audit-the-fed-bill-gets-new-pus…

END

Saville has been anti gold for decades

(courtesy Chris Powell/GATA)

Saville doesn’t get it: Rig the gold price and you rig all prices

Submitted by cpowell on Wed, 2017-01-04 20:47. Section: Daily Dispatches

3:49p ET Wednesday, January 4, 2017

Dear Friend of GATA and Gold:

Manipulation of the gold market by investment banks, technical analyst Steve Saville writes this week in the Speculative Investor, is not necessarily long-term price suppression:

http://tsi-blog.com/2017/01/market-manipulation-is-not-price-suppression…

Yes, GATA strives to distinguish between market activity by investment banks and market activity by governments and central banks. GATA is much more interested in the latter activity.

Yet all the investment banks targeted for gold and silver market rigging by the antitrust lawsuit in federal court in New York enjoy the U.S. Federal Reserve’s coveted classification of primary dealer in U.S. government securities:

http://www.gata.org/node/17037

And while the transcripts disgorged by Deutsche Bank in that lawsuit, showing trader collusion in gold market rigging by all the defendant banks, have been public for many weeks now, the Fed has taken no action against the banks. It seems as if the Fed doesn’t mind if its primary dealers manipulate the gold market as long as the manipulation is, as the transcripts suggest, primarily downward. This at least tacit approval would be even more probable if the investment banks lease gold from governments and central banks, making the investment banks effectively the agents of governments and central banks in the gold market.

Saville expresses no curiosity about these connections.

But Saville misses even more when he argues that gold price suppression over a long period is disproved by “the close relationship over the past three years between the U.S. dollar gold price and the bond/dollar ratio (the T-bond price divided by the dollar index).” For even Saville might admit that governments are intervening around the clock in the bond and currency markets. Making such interventions stick requires preventing gold from giving the markets contrary signals, signals that could put bond and currency prices in question.

So why wouldn’t governments intervene surreptitiously in the gold market too to protect their bond and currency market interventions?

In any case no one’s charts or philosophy can contradict the documentation of gold price suppression by governments and central banks that is summarized here —

http://www.gata.org/node/14839

— documentation that Saville and other deniers of gold price suppression never bother to examine and dispute. Maybe one may argue over why governments and central banks intervene surreptitiously in the gold market, but the fact of that intervention right up to the present day is well established.

Indeed, Saville seems determined to abandon the subject entirely before being forced to examine the documentation. He writes: “You are allowed to make money in the financial markets by doing something other than buying or owning gold. Therefore, if you truly believe that a powerful group has both the means and the motive to suppress the gold price, then the solution is obvious: Don’t buy gold.”

The problem is that gold, an international reserve currency, is powerfully connected to all other markets. Manipulate the gold price and you manipulate all currency values. Manipulate all currency values and you manipulate the price of everything valued in currencies. That covers just about everything except maybe your dog’s affections.

Thus the choice is far more profound than Saville’s framing of it — whether to buy gold. It is whether to aspire to free and transparent markets or just try to trade on the side of the governments manipulating markets — that is, whether to accept totalitarianism and totalitarians, who may be grateful for the camouflage offered to them by Saville and his charts.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The following bullion star infographic highlights the fractional gold reserve banking system orchestrated by the gold ETF’s. This is what I have been harping on for years:

(courtesy Ronan Manly/GATA)

Bullion Star ‘infographic’ on gold ETFs shows how they undermine the gold price

Submitted by cpowell on Wed, 2017-01-04 21:03. Section: Daily Dispatches

4:03p ET Wednesday, January 4, 2017

Dear Friend of GATA and Gold:

Bullion Star today has posted an interesting “infographic” about exchange-traded gold funds and its main point seems to be to remind investors that when they buy shares in gold ETFs, they are facilitating the fractional-reserve gold banking system — that is, facilitating the artificial inflation of the gold supply, making gold seem more plentiful than it is and thus undermining the gold price. The Bullion Star “infographic” is here:

https://www.bullionstar.com/blogs/bullionstar/infographic-gold-etf-mecha…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan UP to 6.8920(HUGE REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS COMPLETELY TO 6.83660 / Shanghai bourse CLOSED UP 6.62 POINTS OR 0.21% / HANG SANG CLOSED UP 322.22 OR 1.46%

2. Nikkei closed UP 230.90 POINTS OR 1.23% /USA: YEN FALLS TO 116.61

3. Europe stocks opened ALL IN THE GREEN EXCEPT PARIS CAC ( /USA dollar index FALLS TO 102.33/Euro UP to 1.0500

3b Japan 10 year bond yield: FALLS TO +.060%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 116.61/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.75 and Brent: 56.89

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.296%/Italian 10 yr bond yield UP 11 full basis points to 1.97%

3j Greek 10 year bond yield FALLS to : 6.78%

3k Gold at $1173.45/silver $16.58(8:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 80/100 in roubles/dollar) 59.57-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a BIG REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 116.61 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0196 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0707 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.296%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.437% early this morning. Thirty year rate at 3.037% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Rise To 1.5 Year High After Chinese Intervention Halts Dollar Rally

Asian stocks rose, led by Hong Kong, while European shares and U.S. equity-index futures are little changed. Euro, yen climb as the dollar posted an unexpected loss following some serious fireworks out of China, which intervened in funding market to crush offshore Yuan shorts.

Top news stories include Macy’s and Kohl’s cutting their outlook after weak holiday season, Deutsche Bank exploring lending money to PE firms buying distressed loans, Apple planning to invest $1b in SoftBank’s new technology fund.

Declines in the USD outweighed major peers in the past week as traders interpreted minutes from the last Fed meeting to indicate a slower path to interest-rate increases, boosting demand for bonds and assets of developing nations. The offshore yuan surged the most on record after the government encouraged companies to stock up on the currency before the week of lunar New Year celebrations.

Gold climbed to the highest in a month.

As Bloomberg notes, the growing backlash against the dollar coincides with more-sober outlooks on whether President-elect Donald Trump’s plans to boost fiscal spending will achieve rapid reflation. The Fed reiterated that a “gradual” pace of rate hikes over the coming years would likely remain appropriate, damping speculation officials will step in to counter inflation with higher rates. Stocks have rallied with the dollar, while Treasuries have plunged since Trump’s election.

While the Dow continues to flirt with 20,000, world stocks hit their highest level since mid-2015 on Thursday after strong Chinese data added to the optimism about global growth and inflation that has been driving markets since the start of the new year. The MSCI world equity index was up 0.4% at one stage to hit its highest level since July 2015. At that level it was up over 1.5 percent for the year so far. The index was pushed up by Asian shares, which rose for the eighth consecutive day on Thursday .

Growth in China’s services sector accelerated to a 17-month high in December, a private sector survey showed, adding to upbeat factory and service sector surveys out of the United States, Europe and Asia released this week.

In addition, minutes from the U.S. Federal Reserve’s December meeting showed that many of the central bank’s policy makers are expecting a pick-up in economic growth and inflation in the world’s biggest economy as a result of fiscal, regulatory or other policies, although most expressed concern that the pace of Trump fiscal stimuli could end up overpowering the economy, and pushing inflation (and the dollar) too high.

“Recent economic data is pretty good so markets are in risk-on mode overall,” said Yukio Ishizuki, currency strategist at Daiwa Securities. “But U.S. bond yields are being capped so the dollar is losing the driver behind its rally.”

Stocks and bond yields have been rising ever since the election of Republican Donald Trump as U.S. president on expectations that fiscal stimulus will boost growth and inflation. Trump’s inauguration takes place on Jan. 20. “The FOMC’s minutes to its Dec meeting released post yesterday’s European close could best be characterized as perhaps tilted toward the hawkish side but tempered by a heavy dose of uncertainty,” said Rabobank strategist Richard McGuire. “All the policymakers emphasized the uncertainty of the outlook, reminding investors that the outlook is more nuanced than the market seems to think,” he said.

With just two weeks to go before Trump takes over, investors and policymakers are waiting to see if his actions match his rhetoric and if his policies will be approved by Republican lawmakers. The dollar extended its losses on Thursday, falling 0.42% against a basket of six major currencies – though still near the 14-year high hit on Tuesday – following losses against the Chinese yuan, which soared after Beijing stepped into both its onshore and offshore yuan markets to shore up the faltering yuan for a second day on Wednesday, sparking speculation that it wants a firm grip on the currency ahead of Trump’s inauguration.

“In the past two months it’s really been the U.S. versus the rest of the world,” said Simon Quijano-Evans, a strategist at Legal & General Group Plc in London. “Maybe there will be some wind taken out of the sails. As we move towards the end of January and the lunar new year holidays, the Chinese authorities are being overly cautious to prevent a rout.”

Maybe, but not today as the DJIA is about to try once again to cross the long-awaited 20,000 barrier.

* * *

Markets Snapshot

- S&P 500 futures down less than 0.1% to 2264

- Stoxx 600 down less than 0.1% to 365

- FTSE 100 down less than 0.1% to 7186

- DAX down 0.2% to 11560

- German 10Yr yield up less than 1bp to 0.28%

- Italian 10Yr yield up 4bps to 1.91%

- Spanish 10Yr yield up 5bps to 1.48%

- S&P GSCI Index down less than 0.1% to 396

- MSCI Asia Pacific up 1% to 138

- Nikkei 225 down 0.4% to 19521

- Hang Seng up 1.5% to 22457

- Shanghai Composite up 0.2% to 3165

- S&P/ASX 200 up 0.3% to 5753

- US 10-yr yield down less than 1bp to 2.43%

- Dollar Index down 0.42% to 102.27

- WTI Crude futures down less than 0.1% to $53.25

- Brent Futures down less than 0.1% to $56.41

- Gold spot up 0.8% to $1,173

- Silver spot up 1% to $16.60

Global Headline News

- Macy’s Declines After Reducing Outlook, Moving to Cut 6,200 Jobs: Holiday sales came in at low end of company’s projections

- Kohl’s Tumbles After Cutting Its Fiscal 2016 Profit Forecast: ‘Sales were volatile throughout the holiday season,’ CEO says

- Deutsche Bank Said to Eye Private Equity Help in Settlement: Bank looking to make loans to PE funds buying distressed loans

- Apple to Invest $1 Billion in SoftBank Fund to Support Tech: Qualcomm says it also will invest undisclosed amount in fund

- VW Ordered to Face Investor Suit in U.S. Over Diesel Cheating: Ex-Chairman Winterkorn also loses bid to toss shareholder case

- Barclays Flags ‘Black Swan Threats’ to Commodities This Year: There is ‘a high likelihood of disruption risk,’ bank says

- Amazon and Forever 21 Said to Mull Bidding for American Apparel: Troubled retailer filed for second bankruptcy in November

Looking at Asian markets, stocks here traded mostly higher following the upbeat lead from Wall Street where all 3 major indices closed positive with the consumer discretionary sector underpinned by strong auto sales and the DJIA finished within 60 points of the 20,000 level. ASX 200 (+0.3%) was supported by miners and energy names after a pullback in USD buoyed the commodities complex, while Nikkei 225 (-0.4%) was dampened by a firmer JPY and as the index took a breather from yesterday’s stellar gains. Elsewhere, Hang Seng (+1.5%) outperformed following encouraging Chinese Caixin Services and Composite PMIs, although the Shanghai Comp (+0.2%) lagged amid continuing liquidity concerns and surges in money market rates after the PBoC only conducted a paltry CNY 10bIn open market operation today. Finally, 10-yr JGBs were relatively flat with minimal gains seen amid a slightly cautious tone in Japan, while today’s 10yr JGB auction later also failed to spur demand with the b/c and lowest accepted prices weaker than prior.

Top Asian News

- Bears Scramble for Yuan as China Chokes Flows, Aids Currency: Offshore yuan set for biggest two-day gain on record

- Chinese Media Say ‘Big Sticks’ Await Trump If He Seeks Trade War: The Communist Party’s Global Times newspaper writes in an editorial Thursday

- Philippines’ Duterte Open to Joint Maritime Drills With Russia: Russian ships could exacerbate tensions in South China Sea

- Xiaomi’s India Sales Pass $1 Billion as Chinese Brands Hold Sway: Shipments grow by almost 150% in 2016

- JPMorgan Lashing by Indonesia Signals Global Threat to Analysts: More governments are seeking to stifle negative market views

European equities rebounded from some early downside, into rose into mid-morning trade relatively flat (Euro Stoxx 50: +0.1%), with the FTSE 100 reaching fresh record highs and printing above 7200 for the first time. The FTSE 100 benefitted from GBP softness, with material names among the best performers while Homebuilders also led the way higher after Persimmon (+4.8%) reported earnings pre-market. In a similar fashion to equity markets, fixed income has seen the entirety of the opening moves retraced, with Bunds opening around the 163.50 before closing the opening gap to trade around 163.20. Of note, today we are looking out for the potential pricing of the French 50Y, while participants will also be keeping an eye on the quantity of corporate issuance, given the significant slate so far this week. Finally, Italian yields remain in focus with the short end of curve underperforming significantly while the GE/IT 10Y spread back above 160bps.

Top European News

- U.K. Economy Maintains Solid Growth Momentum as Services Surge: Markit surveys point to 0.5% quarterly economic growth

- Lansdowne’s $9 Billion Hedge Fund Suffers First Loss Since 2012: Lansdowne’s main hedge fund lost almost 15% in 2016

- Ericsson Deepens Cisco Tie-Up to Combine Wi-Fi, Mobile Networks: Partnership to broaden Swedish network builder’s offering

In currencies, the offshore yuan surged 0.6 percent to 6.8913 per dollar as of 11:25 a.m. in London after surging 1.4 percent Wednesday, putting it on track for a record two-day gain. The Bloomberg Dollar Index extended losses, declining 0.2 percent, after touching its highest level since its 2004 inception 4.5 percent since Nov. 9. It fell against The euro was little changed at $1.0490. Overall, it has been a busy session for FX, with the USD finally seeing a little more flexibility after the strong post US election gains seen. In USD/JPY, the pair dropped as low as 115.60, before rebounding 100 pipe higher. Yesterday’s FOMC minutes added to the Dollar pullback, which was largely a function of over-extended levels, but with some Fed members incorporating Trump’s expansionary policy intentions into their forecasts and rate outlook (accordingly), cause for some ‘uncertainty’ to be re-factored into the USD has since taken place. EUR/USD has pushed back through 1.0500 as a result, and with German and EU inflation rises also bolstering. Firmer commodity prices are helping to lift the related FX pairs, with AUD pushing up to fresh highs around .7325-30. NZD has been dragged higher accordingly as we tipped .7000 here also. CAD has been leading the way however, outpacing Oil price gains over the past week or so and reinforcing the resistance seen ahead of 1.3600.

In commodities, crude slipped 0.4% to $53.45 a barrel in New York as investors weighed rising Libyan supply against signs OPEC output began slipping. Gold rose 0.7 percent to the the highest level in almost a month. Aluminum led base metals higher with a 0.7 percent gain. Nickel rose 0.3 percent and zinc was up 0.4 percent.

Looking at the day ahead, the early data print in the US is the ADP employment change reading for last month which should help anchor expectations for tomorrow’s payrolls. Market consensus for the ADP print is currently 175k which compares to 216k in November. Also due out is the latest weekly initial jobless claims reading while the final services and composite PMI’s will also be confirmed. Also of note is the ISM non-manufacturing reading for last month which will come hot on the heels of the strong manufacturing print earlier this week. Market consensus for this is 56.8. Away from the data we’re due to hear from BoE Chief Economist Andy Haldane this afternoon when he speaks at an event in London.

DB’s Jim Reid concludes the overnight wrap

A quick scan through last night’s FOMC minutes will reveal no mention of President-elect Trump’s name but it’s pretty clear where the debates and discussions at the Fed now lie. In a nutshell “almost all” officials made mention of upside risks to their growth forecasts as a result of prospects for more expansionary fiscal policies while interestingly “about half” of the Fed officials incorporated fiscal policy into their forecasts. The caveat though is that the outlook is distinctly uncertain. Indeed the minutes acknowledged that “participants emphasized their considerable uncertainty about the timing, size and composition of any future fiscal and other economic policy initiatives as well as about how those policies might affect aggregate demand and supply”. Officials also acknowledged that this “made it more challenging to communicate to the public about the likely path of the federal funds rate”.

The minutes also acknowledged that the staff’s forecasts for higher real GDP growth over the next few years “were substantially counterbalanced by the restraint from the higher assumed paths for longer-term interest rates and the foreign exchange value of the dollar”. Away from Trump the rest of the minutes didn’t offer a whole lot of new information with officials seemingly a bit more confident about the balance of risks. That said there was a subtle change to the number of officials concerned about a sizable undershooting of the longerrun normal unemployment rate from “a few members” in November to “several members” in December.

So the overall tone fits in with Yellen’s post-meeting statement last month where she said that the Fed is “operating under a cloud of uncertainty at the moment”. So every Trump move will continue to be closely watched and scrutinized. With that in mind it’s worth circling the 11th January in your diary as it’s when Trump is due to hold a ‘general news conference’. It’s his first since the election victory and comes just 9 days before his official inauguration so it should be a closely watched event. Evaluating Trump’s administration appointments in the mean time will continue to be a focus for now though. One which stands out is the appointment of Robert Lighthizer as his new trade representative. Lighthizer is seen as a longstanding advocate of greater protectionism and was formerly a trade official under Ronald Reagan. The WSJ also notes that Lighthizer has three decades of experience arguing for punitive tariffs on overseas companies. So it appears that the appointment confirms what is likely to be a major shift in trade policy under a Trump presidency.

Meanwhile markets turned a fairly blind eye to the minutes yesterday. 10y Treasury yields were hovering around 2.450% leading into the minutes before closing the day at 2.440% and 0.5bps lower on the day. 2y yields finished flat at 1.216% while the USD index, which had struggled as the session wore on, closed -0.67% but again with little reaction post the minutes. It’s been nothing but good news for risk assets in the US so far this year though. The S&P 500 finished +0.57% and so taking the 2017 YTD gain to +1.43%. That’s the best start to the year since 2013. Consumer names were a big driver yesterday although it’s worth noting that both Macy’s and Kohl’s tumbled after market (by -8% and -9% respectively) after both lowered earnings guidance following softer holiday season sales. The MSCI EM equity index also returned +0.35% and has now gained in 7 of the last 8 sessions. The rally in Europe had earlier stalled however with the Stoxx 600 closing down a fairly modest -0.12%. Elsewhere credit has also gotten off to a flier, particularly across the pond and yesterday we saw CDX IG tighten just over 2bps to take the index to the tightest level since May 2015. The new issue market hasn’t taken any time to warm up either with Bloomberg reporting that US IG primary issuance is over $45bn in the first two trading days of the year already and so overtaking that for the first week in 2016 and 2015.

As we refresh our screens this morning it’s been a bit of a mixed performance in Asia so far. While the Hang Seng (+1.30%) has risen strongly led by gains for the energy sector, bourses in China are little changed while the Nikkei is -0.24%. The Kospi (-0.09%) is also a shade lower while the ASX (+0.29%) is up a touch. US equity index futures are also slightly in the red. There was also some data in China this morning where the Caixin services PMI was confirmed as rising 0.3pts to 53.4 in December. That’s helped push the composite reading up to 53.5 from 52.9 and to the highest level in 45 months.

Moving on. Away from the minutes, yesterday’s economic data was also generally supportive. In the US we learned that total vehicles sales increased to an annualized rate of 18.3m in December (vs. 17.7m) from 17.8m in the month prior. Over in Europe it was revealed that the estimate of headline Euro area CPI had risen more than expected in December after printing at +1.1% (vs. +1.0% expected) from +0.6% in November. That puts headline inflation at the highest level since September 2013 and encouragingly while higher energy prices led, the increase was actually relatively broad based. The core was also up after rising one-tenth to +0.9% yoy. Meanwhile the remaining PMI’s were also out in Europe yesterday. The final composite PMI for the Euro area in December was revised up to 54.4 from 53.9 after the services reading was revised up 0.6pts to 53.7. That is the highest PMI reading since 2011, just beating the 54.3 seen in August and December 2015. Our European economists also noted that at the same time, a number of the sub-indices, including the composite input and output prices and the backlog of orders, were confirmed at new cyclical highs. Across countries the news was broadly positive across the EMU countries while Italy was the relative disappointment with the composite down 0.5pts to 52.9, although this came after a 2.2pt rise in November. Our colleagues go on to say that at 53.8 on average in Q4 the composite PMI was back to in line with its 2015 levels, a year in which Euro area GDP grew on average by 0.5% qoq.

Wrapping up the remaining news yesterday. Over in France National Front presidential candidate Marine Le Pen confirmed that she wanted to remove France from the Euro and also redenominate French overnment debt in a new national currency. Le Pen confirmed that she wanted “a national currency with the euro as a common currency” and as the FT made mention to, suggests some softening in her views in favour of a looser form of currency sharing rather than a hard return to a national French currency. Meanwhile in the UK, PM Theresa May moved quickly and decisively to replace Sir Ivan Rogers as the UK Ambassador to the EU by appointing Tim Barrow to the role. He was previously the political director of the government’s Foreign and Commonwealth Office.

Looking at the day ahead, the diary is a bit thinner in Europe this morning with the only notable data due out being the remaining December PMI’s in the UK (services and composite) and the PPI print for the Euro area. This afternoon in the US the early data print is the ADP employment change reading for last month which should help anchor expectations for tomorrow’s payrolls. Market consensus for the ADP print is currently 175k which compares to 216k in November. Also due out is the latest weekly initial jobless claims reading while the final services and composite PMI’s will also be confirmed. Also of note is the ISM non-manufacturing reading for last month which will come hot on the heels of the strong manufacturing print earlier this week. Market consensus for this is 56.8. Away from the data we’re due to hear from BoE Chief Economist Andy Haldane this afternoon when he speaks at an event in London.

end

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 6.22 POINTS OR 0.21%/ /Hang Sang closed UP 322.22 OR 1.46%. The Nikkei closed UP 230.90 POINTS OR 1.23% /Australia’s all ordinaires CLOSED UP 0.29%/Chinese yuan (ONSHORE) closed WELL UP at 6.8920/Oil ROSE to 53.75 dollars per barrel for WTI and 56.89 for Brent. Stocks in Europe: ALL IN THE GREEN EXCEPT PARIS Offshore yuan trades 6.83660 yuan to the dollar vs 6.8920 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS COMPLETELY TRYING TO STOP DOLLARS LEAVING CHINA’S SHORES /

3a)THAILAND/SOUTH KOREA/:

none today

b) REPORT ON JAPAN

c) REPORT ON CHINA

Wednesday night/9 pm est

This is nuts: Overnight lending rates between banks skyrockets to 45%. And now Bitcoin is trading higher than gold: Bitcoin $1252.00 usa/gold 1172.usa. Offshore yuan 6.8870 as the shorts are getting crushed!

(courtesy zero hedge)

Bitcoin Explodes Higher As Chinese Interbank Liquidity Freezes; Overnight Yuan Rate Hits 45%

As one veteran trader noted “something is very broken.” After a massive short-squeeze sent the offshore yuan soaring during the US day session, overnight yuan deposit rates have exploded 31.5 percentage points higher to 45% – just shy of the record highs – as China’s interbank liquidity crisis is front-and-center. At the same time, coincidence or not, Bitcoin denominated in yuan has gone vertical, smashing through previous record highs.

Continuing the recent trend of demonstrably withdrawing liquidity, the People’s Bank of China injected a paltry CNY10 billion via seven-day reverse repos and skipped both 14-day and 28-day reverse repos at its open-market operations Thursday, according to traders. The moves resulted in a net drain of CNY140 billion for the day and a whopping CNY435 billion in liquidity at OMMOs so far this week. Yes, nearly half a trillion yuan in liquidity has been withdrawn in just the past week, a time when banks are already scrambling for every spare source of cheap funding.

As a result of this forced drain which was likely orchestrated by the central bank to crush any remaining shorts, and the utter desperation for liquidity, has prompted deposit rates to explode.

And perhaps whatever liquidity there is left is being placed elsewhere.

Smashing higher in the last few hours.

For now the short squeeze efforts of the PBOC are not extending the move in CNH.

end

Thursday morning

The interbank lending rate between banks rose to 80% and the USA/CNH lowered (yuan rose) to 6.83. No doubt that this will stem the outflow of dollars temporarily. However China has to worry about the Donald taking control of uSA on January 20 and he will also use his wrath against China

(courtesy zero hedge)

“Incredibly Aggressive” China Crushes Yuan Bears: CNH Surges Most On Record As Deposit Rate Hits 80%

Last night we were amazed to report that with China starting its trading day, the overnight offshore yuan (CNH) deposit rate had exploded 31.5% points higher to 45%, in a move which while freezing interbank liquidity and unleashing havoc to short-term bank funding needs, had the more direct intention of crushing Yuan shorts, by making short holding costs soar through the roof and forcing a short squeeze.

As it turns out, that was just the beginning, because before the night was over, the overnight offshore Yuan deposit would hit a record 80%, while the USDCNH would tumble as low as 6.78, resulting in the biggest 2-day move higher in the offshore Yuan on record, or as Bloomberg reports, “the yuan gained 1% at 2:53 p.m. in Hong Kong, taking its two-day move to 2.3%, the most in data going back to 2010.”

But the one chart everyone is talking about today is that of the overnight CNH deposit rate, which after touching 45% at the start of China trading day, surged to a record 80% just a few hours later…

… while the spread between the offshore and onshore exchange rates widened to the on record. Ultimately, the offshore yuan erased the day’s losses in a sudden move around 1:05 p.m as the premium over the onshore rate widened to 1.2%.

This follows after Chinese policymakers explicitly urged SOE banks to sell foreign currencies, and further “punish” short sellers.

The overnight deposit rate in the city surged to a record 80 percent, while the spread between the offshore and onshore exchange rates widened to the most since 2010. Bloomberg News earlier reported Chinese policy makers were encouraging state-owned enterprises to sell foreign currency.

As SocGen summarized the unprecedented indirect intervention by the PBOC, “investors are cutting bullish positions in the dollar after the report underscored China’s determination to support the yuan.”

The overnight fireworks come, of course, after policymakers in Beijing recently unveiled a slew of new capital control measures to tighten control of the currency market, including placing higher scrutiny on citizens’ conversion quotas and stricter requirements for banks reporting cross-border transactions.

“Given the recent capital controls, the channels for domestic institutions and retails to bring out onshore cash to the offshore market have also been tightened,” said Becky Liu, a rates strategist in Hong Kong at Standard Chartered Plc. “There is a lack of supply of yuan liquidity.”

Meanwhile, the liquidity drain which we have followed every day this week continued, and is set to accelerate further as tomorrow forward points surged to a record. In other signs of yuan scarcity, HSBC Holdings raised its three-month yuan deposit rate to 2.85 percent from 1.8 percent, according to the Oriental Daily, while the cost of borrowing yuan overnight in Hong Kong surged by 21.4 percentage points, Bloomberg reported. That’s the most since January 2016, when the authorities choked yuan supply to burn speculators betting on declines.

Paradoxically, the measures have only heightened skepticism among currency watchers: “We know the capital controls aren’t working because that’s why they’re having to raise the overnight deposit rate so aggressively by the PBOC, which is still basically the guiding hand in the offshore yuan market,” said Michael Every, head of financial markets research at Rabobank Group in Hong Kong. “It’s an incredibly aggressive tactic.”

High short-term funding costs, which will continue to trend higher, could dissuade significant short yuan positions from being added in the near term, Societe Generale strategists led by Jason Daw wrote in a note Thursday.

The good news is that, if only briefly, the rebounding Yuan would alleviate capital outflow pressure on Chinese authorities, who are battling to curtail capital flowing offshore after an annual $50,000 quota for citizens to buy foreign exchange reset on Jan. 1 and the imminent inauguration of U.S. President-elect Donald Trump lifts the dollar. Investors have been watching for the yuan to break the psychologically key level of 7 against the greenback for the first time since 2008.

However, make no mistake, this is capital control war to prevent the Yuan from being dragged lower as the dollar surges, a war which overnight spilled over into other Asian currencies, most of which jumped in sympathy with the Yuan.

“The weaker dollar overnight should help push the yuan further away from the 7 level for now, aiding the Chinese authorities’ recent efforts to stabilize the currency,” said Christy Tan, head of markets strategy in Hong Kong at National Australia Bank Ltd. “We expect the authorities to maintain an elevated currency management mode in the run-up to Donald Trump’s inauguration on Jan. 20, and until after the Lunar New Year break from Jan. 27 to Feb. 2.”

Ultimately, the offshore yuan’s strength will be short-lived because the Hong Kong Monetary Authority may add supply of the currency to lower funding costs, and the dollar could rally, said Andy Ji, a Singapore-based currency strategist at Commonwealth Bank of Australia… but not before enough shorts have been carted out feet first. Even so, the long-term direction of the Yuan is clear: the onshore exchange rate will decline 3.6 percent to 7.15 per dollar by the end of this year, according to the median estimate in a Bloomberg survey.

“Fundamental reasons that are driving depreciation, such as capital outflows and concerns on Trump’s China policies, haven’t changed,” said Qi Gao, a Singapore-based foreign-exchange strategist at Scotiabank, quoted by Bloomberg.

end

With the Chinese authorities stating that they were going to crack down on cryptocurrencies like Bitcoin, in an attempt to stop the outflow the dollars, finally we see Bitcoin collapse in price down 31% to $893.00 usa. The true currency, gold continues to rise:

(courtesy zero hedge)

Another Bubble Bursts – Bitcoin China Crashes Over 30%

First it was Chinese stocks, then Chinese real estate (twice), then Chinese commodities (twice), and now Chinese Bitcoin’s bubble has burst as a massive short squeeze on the offshore Yuan combined with comments on ‘virtual’ capital controls has sparked a bloodbath in the cryptocurrency from 8,896 yuan to 6,101 yuan in the last few hours…a 31% collapse.

Despute the collapse – BTC China is only back at 2 week lows…

For those chasers, don’t say we did not warn you, as we noted previously, for those buying into bitcoin here on the momentum, most of which originates in China, we urge readers to be cautious as by now the PBOC has certainly noticed that the digital currency remains one of the final, and most successful, means of bypassing capital controls in China. Should Beijing mandate that bitcoin no longer be a means to illegally transfer capital offshore, there is risk of a dramatic, and sharp, drop in its price.

end

This is what happens when you try and grow your economy by 7% per year. The steel mills etc are running at full blast despite poor global demand. This causes poor air. Just look at the following story where a cruise ship could not dock in Beijing because they had no visibility

(courtesy zero hedge)

Chinese Cruise Ship With 2,000 Passengers Stuck At Sea For Two Days Due To Smog

Beijing’s pollution problem is getting worse by the day.

On Wednesday, the Chinese capital issued its highest “red fog alert” for only the second day in history, keeping highways closed in and around the city which is already under a smog alert after weeks of choking winter pollution. China’s weather bureau warned of visibility of less than 50 meters in some areas, leading many airports to cancel flights.

The heavily polluted Hebei province, which surrounds most of Beijing, said on Tuesday it had ordered all polluting firms in Tangshan, China’s biggest steel-producing city to the east of Beijing, to shut down which likely means that China is in for a substantial “manufacturing” shock in the coming months.

Hebei, which was home to seven of China’s 10 smoggiest cities in 2015, will build the world’s biggest dust prevention barrier, stretching nearly two miles, at the major coal port of Qinhuangdao in a bid to cut pollution, state media said on Wednesday.

For now, however, China is very much defenseless against the toxic byproduct of its rapid industrialization, which also happens to be a major factor permitting the Chinese economy to grow at the goalseeked 6-7% level or somewhere thereabouts. Unfortunately for Beijing, it’s a choice of either stable manufacturing growth or clean air: the two are mutually exclusive.

And nowhere was that more visible today, so to speak, than near the port of Tianjin, where according to the Beijing Evening News, a large cruise ship with more than 2,000 people on board was stuck at sea for two days because it was unable to dock in the heavy smog that has enveloped much of northern China. The vessel finally returned to the Port of Tianjin on Monday afternoon after drifting for two days at sea. The thick air pollution had earlier made it impossible to safely berth the vessel, according to the article

A passenger was quoted as saying that the ship was scheduled to return on New Year’s Eve after traveling to South Korea and Japan. But she was told by the crew that the ship could not dock as visibility was severely compromised by the smog. She said the passengers had been unsure how long they would be stuck at sea but were grateful there was plenty of entertainment on board to kill time.

“Unlike passengers who are stuck at some public facilities like an airport, we got to use the pool and the gym to keep ourselves busy,” she said.

As Reuters adds, poor visibility prompted three major northern ports to suspend the loading of ships on Tuesday, maritime safety agencies said.

Unless Beijing’s leadership is willing to take draconian measures to curb smog production, which inevitably means an economic slowdown, expect scenes such as the ones shown below to continue.

It’s started snowing in Beijing. What do you call smoggy snow? Smow? Snog?

Beijing out my window – the air has taste and texture today.

Beijing from the air as smog blankets the city. Just otherworldly – and alarming

end

4 EUROPEAN AFFAIRS

Now we have Italy’s Grillo slamming mainstream media for fake news

(courtesy zero hedge)

Italy’s Grillo Slams Mainstream Media “Manifest Manipulation Of Reality”

“Fake news” has officially crossed the pond and once again it the mainstream media that is producing more of it (while blaming the alternative media). Beppe Grillo, founder of Italy’s Five Star anti-euro movement lashed out at the country’s journalists for “manufacturing false news,” accusing them of fabricating stories to keep the Five Stars down.

“Newspapers and television news programmes are the biggest manufacturers of false news in the country, with the aim of ensuring those who have power keep it,” he said on his blog on Tuesday.

As Local.It reports, he called for “a popular jury to determine the veracity of the news published,” and said in cases of fake news “the editor must, head bowed, make a public apology and publish the correct version at the start of the program or on the paper’s front page”.

…the politicians are now demanding stronger measures against bloggers…

[BUT], have never urged punishment for those who commit more serious crimes, lying in absolute bad faith, abusing the credibility of institutions. That lie can not be punished. It is not in the interest of mainstream politicians.

All major newspapers should be closed for manifest manipulation of reality, or obliged to go out with a sticker that certifies the lack of credibility.

The media world was – of course – enraged…

The news director of the private TG La7 channel, Enrico Mentana, said he would sue the comedian, while journalists’ union FNSI slammed the “lynching of all journalists”.

What Grillo is proposing “is called Fascism, and those who play it down are accomplices,” PD senator Stefano Esposito said.

Marco Travaglio, editor of the far-left Il Fatto Quotidiano daily, agreed with Grillo but said the popular jury idea would never work.

“The biggest lies are those spread by the television and newspapers, but the solution he is proposing is naive,” he said.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

Mexico is beginning to panic as they now believe that Trump will be true to his word;

(courtesy zero hedge)

Mexico Panics As Trump’s Leverage “Far Greater Than What Mexican Elites Thought”

Earlier this morning we noted that the Mexican Peso was plunging once again – very close to all-time record lows – as fears spread that Ford’s decision yesterday to cancel a $1.6 billion plant may become the norm following president-elect Trump’s tweet that “this is just the beginning.”

Thank you to Ford for scrapping a new plant in Mexico and creating 700 new jobs in the U.S. This is just the beginning – much more to follow

And here is the peso:

And while many senior politicians within the Mexican government dismissed Trump’s campaign speeches as empty rhetoric, per the Associated Press, Ford’s cancellation of it’s $1.6 billion auto plant has served as a “much needed wake-up call” that shows that Trump has far greater leverage “than what Mexican elites thought until recently.”

“Trump leaves Mexico without 3,600 jobs,” read the headline on El Universal. “Ford’s braking jolts the peso,” said Reforma, referring to the Mexican currency’s nearly 1 percent slump following the news.

Two weeks before inauguration, the scuttling of the planned Ford factory and Trump’s pressure on General Motors should be a “much-needed wake-up call,” said Mexico analyst Alejandro Hope.

It shows “how much actual leverage Trump has within specific companies, which is far greater than what Mexican elites thought until recently,” Hope said. “They claimed that at the end of the day economic interests would prevail over political messaging. That’s clearly not the case.”

All of which has caused some level of panic within the Mexican political and media spheres from the elites who are slowly realizing that when Trump says he wants to disrupt the status quo by renegotiating NAFTA and building a border wall, “he means it”….as completely shocking as it may be that a politcian might actually mean what he says.

In an editorial, El Universal also recalled the deal Trump struck in December with Carrier to keep 800 of 1,300 jobs at an Indiana furnace factory from being sent to Mexico, in return for millions of dollars in tax incentives. It also implicitly criticized the Mexican government’s response to the incoming administration.

“Mexico loses thousands of jobs with no word on a clear strategy for confronting the next U.S. government which has presented itself as protectionist and, especially, anti-Mexican,” the paper wrote. “Trump will try to recover as many U.S. companies that have set up in Mexico as possible. He will try to make them return at whatever cost, through threats or using public resources.”

“Ford’s decision is indicative of what awaits the economies of both countries,” the daily La Jornada said. “For ours a severe decrease in investment from our neighboring country, and for the U.S. a notable increase in their production costs.”

Hope said more decisions like Ford’s are likely to come. And while the loss of a single planned plant probably does not fundamentally change the U.S.-Mexico economic relationship, “it certainly shows that the idea that the status quo was entrenched was false.”

“This should put us on notice that when he says that he wants to renegotiate NAFTA, he means it,” Hope said.

As we pointed out a few days ago, with Trump scoring new victories with every passing day, the question no longer seems to be whether or not Vicente Fox will pay for the “f**king wall,” but rather, how he’ll pay for it…cash or credit, Mr. Fox?

Trump Threatens Toyota: “Build New Plant In The US Or Pay Big Border Tax”

Poor Mexico just can’t catch a break.

After its currency crashed to record lows this week after Ford cancelled plans to build a $1.6 billion plant in Mexico, prompting the central bank to intervene and sell $1 billion USD to stabilize the currency, moments ago Trump lobbed another shot at Mexico, this time threatening Toyota with paying a big border tax if it building its new pant in Baja instead of the US.

Just around 1:15pm Eastern, Trump tweeted: “Toyota Motor said will build a new plant in Baja, Mexico, to build Corolla cars for U.S. NO WAY! Build plant in U.S. or pay big border tax”

Toyota Motor said will build a new plant in Baja, Mexico, to build Corolla cars for U.S. NO WAY! Build plant in U.S. or pay big border tax.

Sure enough the selling in the Peso has resumed, and it is now back to where it was before Banxico wasted $1 billion in reserve to push it higher.

It’s not just the peso though: TOYOTA ADRS DROP TO SESSION LOW ON TRUMP TWEET.

end

Mexico now out of control as looting and rioting are on the streets in Mexico due to the huge 20% gas hike.

(courtesy zero hedge)

Looting, Riots In Mexico Spiral Out Of Control Over 20% Gas Hike; Hundreds Arrested

Four days after the first sporadic protests emerged in Mexico City, following the infamous “gasolinazo”, or mandatory 15%-20% increase in Mexican gas prices which went into effect on January 1, the mood across the country has significantly deteriorated, with hundreds of demonstrators blocking highways, snarling traffic, raiding gas stations, jeopardizing critical supplies, and looting stores as angry but impotent motorists lashed out at the price surge, which is only going to get worse as inflation spikes even more following the record plunge in the Mexican Peso.

Residents steal fuel and diesel from a gas station in Veracruz state

As a reminder, the price of oil rose Sunday by as high as 20.1% to 88 cents per liter, with diesel at 83 cents — the equivalent of 12 days of a minimum wage to fill a tank of gas – compared to the U.S.’s seven hours — and the price ceiling will be adjusted daily starting Feb. 18, before letting supply and demand determine them in March.

The unrest has caused some gas stations to close altogether. Antonio Caballero, who heads a network of 800 gas stations, said at a press conference this week he will temporarily close any filling station threatened by violent protesters. According to unconfirmed reports, even the local drug cartels warned ahead of the price hike they would burn down gas stations should the price increase come into effect.

However, as tends to happen during mass civil disturbances, it’s not just gas stations that are being targeted. Some protesters have used the gasolinazo as an excuse to loot supermarkets and other stores in several states.

A man runs with toys as a store is ransacked by a crowd in the port of Veracruz,

Mexico after gas price hikes rage out of control

As of Thursday morning, 250 stores had been looted and 170 were closed or blockaded in all of Mexico, according to the National Association of Self-Service and Department Stores.

At least 430 protesters were detained on charges of vandalism, including four police officers according to El Universal.

Protesters block the entrance to a Pemex gas station as they burn tires during a

protest against the rising prices of gasoline

The unrest ‘resulting in the theft of merchandise put at risk the lives of clients and workers in the stores, primarily in Mexico State, Michoacan, Hidalgo and Mexico City,’ the statement said.

Suspects are detained by navy police after a store was ransacked by a crowd in

the port of Veracruz during gasoline price protests

In the Gulf coast city of Veracruz, store guards were overrun Wednesday

by crowds who carried off clothing, food, washing machines, televisions,

DVD players and refrigerators; 50 establishments including convenience stores, supermarkets and big-box outlets suffered looting, according to a preliminary count by the local chamber of commerce.

A group of people grabs toys as a store is ransacked by a crowd in the port of

Veracruz, Mexico after frustrations over a sharp gas price hike erupt into violence

Store guards were overrun by crowds who carried off clothing, food, washing machines, televisions, DVD players and refrigerators

Extra police patrols were deployed, and at least 14 people were detained, the state government reported. At one supermarket officers fired into the air to disperse the multitudes.

According to Fusion, adding to the chaos on the streets is a wave of unconfirmed news and threats on social media perpetuating rumors about a curfew on Wednesday, pushing some businesses to temporarily close two days before Mexico’s Día de Reyes, a religious holiday that normally has parents flocking to stores to buy toys for their kids.

People form a human chain to block access to a gas station in Mexico City

The state-owned oil company Pemex said Tuesday that blockades of fuel terminals in the states of Chihuahua, Morelos and Durango had caused a “critical situation” in distributing fuel to gas stations there. It said that if the blockades continued, it could interrupt operations at airports in Chihuahua and Baja California.

Mexicans’ collective anger over the situation is being directed mostly at President Enrique Peña Nieto, who in 2015 had promised that country’s frequent pump price hikes would end with his much-touted finance and energy reform plans. However, as a result of the plunge in oil prices , the long-awaited liberalization of the country’s energy sector which would have led to lower prices, the promised relief at the pump has yet to materialize.

Speaking at a press conference on Wednesday, president Nieto called the gas price hike “painful” yet “inevitable.”

2) Gracias a la Reforma Hacendaria, por 1era. vez en 5 años, ya no habrá incrementos mensuales a los precios de la gasolina, diésel y gas LP

“I call society to listen to the reasons for taking this decision, which, without having been made, I must say, would have led to more painful effects and consequences,” he said Wednesday after several days of notable silence. He added that he understands the anger of Mexicans and did not want to make the “painful, difficult and inevitable” move, but had to.

He told Mexicans Wednesday to accept the dramatic hike in gas prices as a necessary move, to the anger of “gasolinazo” protesters, who reiterated their call to take down the country’s most unpopular president on record.

Demonstrators stormed several government buildings on Wednesday, demanding the resignation of Nieto and sympathetic state governors who have promoted the Institutional Revolutionary Party’s neoliberal reforms that have included privatizing the national oil company Pemex. Pena Nieto had promised to lower gas prices in his campaign, but they have kept rising since he took office.

A series of actions, including boycotts, petition signing, meetings, assemblies and civil disobedience are planned for the week, as the prologue to a national march next week. As of earlier this week, tens of thousands have already participated in roadblocks and seized, looted and vandalized gas stations, prompting 400 stations to close and affecting the operations of airports and bus stations.

The tweet below lays out a “map of peaceful protests against gasolinazo. We have the right to protest.”

Meanwhile, the blowback against the unpopular price hike is spreading to the political class. Pemex has requested that state governors help open access to stations to continue business, but several governors have already come out against the hike. The governor of Chihuahua, Javier Corral, said he would not deploy forces to quell the protest, which he supports, and Aristoteles Sandoval of Jalisco, who is a member of the PRI, said Mexicans have a right to be angry. Veracruz Governor Miguel Angel Yunes said he expects the rise to mostly affect the poor and threaten political stability, lamenting that Peña Nieto did not consult governors before implementing the measure.

Taxes represent 44 percent of the price of gasoline, tweeted Guadalajara Mayor Enrique Alfaro, adding to a trending hashtag, #ReversaAlGasolinazo, to reverse the measure by lowering taxes.

Several media and politicians, including Peña Nieto, have denounced the protests as violent, which organizers insist is a mischaracterization of the peaceful actions, which aim to redistribute oil for free or at significantly reduced prices. Many extrapolated their opposition as opposition also to violence, corruption and impunity in the country, with which they hope to create a wider front against Peña Nieto’s administration and business-as-usual in traditionally authoritarian Mexican politics.

“The history of our country is stained with big and deep social problems without resolution,” wrote feminist group MujerEs YA!, “where violence and impunity have marked the path of daily life, until the point of voracious alienation that plays between indifference and immobility, which uses whatever measure to convince the public of its uselessness, of its drowned inert voice, accustomed to the toxic, a population that merits little, because it demands little, because it naturalizes its own death.”

3er día de protestas vs #gasolinazo. Ojalá q en 2018 ésto le cueste muy caro al PRI. RT si estás de acuerdo. pic.twitter.com/UuF8buhON2 @jrisco

But the worst is yet to come. According to increasingly more analysts, who initially were silent on the topic, the price increase will raise the price of basic goods, provoke unemployment, inflation, economic stagnation and potentially economic contraction and even recession.

7. OIL ISSUES

DOE reports huge inventory build and down goes oil

(courtesy zero hedge)

WTI, RBOB Tumble After Massive Product Inventory Builds

Following API’s larger than expected crude draw (and huge product builds), DOE reports massive builds in Distillates (+10mm – biggest sine Jan 2015) and Gasoline (+8.3mm – biggest since Jan 2016) and another big build in Cushing inventories. Crude inventories drew down 7.05mm barrels – confirming API’s data. US crude production also picked up and WTI prices tumbled.

API

- Crude -7.431mm (-2mm exp)- biggest draw since Sept 2016

- Cushing +482k (+900k exp)

- Gasoline +4.25mm (+1mm exp)- most since Jan 2016

- Distillates +5.244mm (-800k exp) – most since Jan 2016

DOE

- Crude -7.051mm (-2mm exp)

- Cushing +1.074mm (+200k exp)

- Gasoline +8.307mm (+1mm exp) – most since Jan 2015

- Distillates +10.051mm (-800k exp) – most since Jan 2016

Total crude stockpiles remain over 35% above the five-year seasonal norm.Cushing jumps to the highest level since May with the sixth gain in seven weeks.

Bloomberg notes that much of that draw in crude stocks looks to be attributable to imports which dropped by 984 kbbls/d across the US with 612 kbbls/d of that coming in PADD 3, that’s a 4,284 kbbls/d drop over the week.