Gold at (1:30 am est) $1171.90 DOWN $7.80

silver at $16.46: DOWN 12 cents

Access market prices:

Gold: $1177.40

Silver: $16.52

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai morning fix Jan 6/17 (10:15 pm est last night): $ 1196.45

NY ACCESS PRICE: $1179.10 (AT THE EXACT SAME TIME)/premium $17.35

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1191.97

NY ACCESS PRICE: $1174.30 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $17.67

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Jan 6/2017: 5:30 am est: $.1174.20 (NY: same time: $1178.40 5:30AM)

London Second fix Jan 6.2017: 10 am est: $1175.85 (NY same time: $1176.60 (10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 0 NOTICE(S) FOR nil OZ. TOTAL NOTICES SO FAR: 1023 FOR 102,300 OZ (3.1819 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 0 NOTICE(s) FOR 0 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 307 FOR 1,535,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 1172 contracts UP to 165,537 with respect to YESTERDAY’S TRADING (short covering by the banks). In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .828 BILLION TO BE EXACT or 118% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 0 NOTICES FILED FOR 0 OZ.

In gold, the total comex gold ROSE BY 8,215 contracts WITH THE RISE IN THE PRICE GOLD ($15.90 with YESTERDAY’S trading ). The total gold OI stands at 431,537 contracts.

we had 0 notice(s) filed upon for 0 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 813.87 tonnes

.

SLV

we had no changes in silver into the SLV

THE SLV Inventory rests at: 341.199 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver ROSE by 1172 contracts UP to 165,537 AS SILVER ROSE by $0.08 with YESTERDAY’S trading. The gold open interest ROSE by 8,215 contracts UP to 431,823 AS THE PRICE OF GOLD ROSE BY $15.90 WITH YESTERDAY’S TRADING

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) FRBNY report on earmarked gold movement

(Harvey)

2d) COT report

Harvey

3. ASIAN AFFAIRS

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

Japan is angry at Trump especially that he got the facts on Japanese production of the Corolla wrong. Let us see what will happen in a few weeks when Trump takes over:

( zero hedge)

c) REPORT ON CHINA

i)Overnight the lending rate between banks soars to 105%. The offshore yuan (CHN ) continues its strength with POBC intervention as the shorts are getting squeezed:

( zero hedge)

ii)Chinese volatility explodes as the offshore yuan goes all over the map. The POBC are very worried about the new Trump administration labeling the country as a currency manipulator and they may wish to keep a stronger yuan in the following few weeks. Also the yuan shorts are temporarily getting killed. However in the long run, the yuan should retreat to the 7.3-8.0 level

( zero hedge)

iii)After China warns its citizens on capital outflowing from China, today they came out and warns more directly against Bitcoin. They urged its citizenry to take a rational approach to investing in virtual currencies. It lowered in value immediately but gold rose.

( zero hedge)

4 EUROPEAN AFFAIRS

How European immigration, mainly Muslims are creating problems for the politicians in Europe. In order to deflect attention, government impose bans of the burka.

( Murray/Gatestone Institute)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

The Central bank of Mexico intervenes in the currency market trying to prop up the Peso but failed again. It seems that they sold a considerable amount of silver in their failed attempt. Is there something under the hood in the Mexican economy that we should be cognizant about:

( zero hedge)

7. OIL ISSUES

i)Back in April we reported on a huge amount of oil Iran was storing on vessels because of no room on land. We now now that 13 million barrels of oil held offshore has been sold mainly to China and other Asian interests and at discounts. Iran needs to get its market share back. The question now becomes will Saudi Arabia offer more discounts and/or cheat on its production!

( zero hedge)

ii)do not worry, the crooks have this under control as they are long oil. USA oil rig counts continue to rise as well as total USA production. OIl prices continue to rise:

(/zero hedge)

8. EMERGING MARKETS

A good snapshot of Venezuela’s finances. The author claims that the country still has 190 tonnes of gold. I find that hard to believe:

(courtesy Mueller/Mises Institute)

9. PHYSICAL MARKETS

i)An excellent Reuters report on the huge risks to the global economy as China burns through its foreign FX reserves. It is probably now below 3 trillion USA

( Reuters/GATA)

ii)A good background on China’s secretive gold reserves

(Ronan Manly/GATA)

iii)Alasdair Macleod’s weekly message for us;

( Alasdair Macleod)

iv)An excellent presentation by Koos Jansen on gold fundamentals between East and West

(Koos Jansen/Bullionstar)

v)Despite its manipulation gold advances against most currencies in the past 15 years

( Goldprice.org/GATA)

10.USA STORIES

i)Another phony jobs report. The BLS reports a gain of only 156,000 workers instead of the expected 178,000. However average earnings jumped .4% in December.

( BLS/zerohedge)

ii)Now for the real story on the jobs report:

iii)Only the supervisory level jobs saw growth in the earnings not the vast majority of American workers:

iv)What a complete utter nonsense: we had a huge increase again in waiter jobs (plus nurses and waste cleaners). We know the job report on the waiters is false because of massive layoffs in that field due to Obamacare, and health care costs that I brought to your attention in the past few days)( zero hedge)

v)a very ugly number: November factory orders plunge the most in over 2 years. And this is after a big rise in defense factory orders:

( zero hedge)

vi) a.What on earth is going on: The democrats refused FBI access to their hacked servers and then the FBI claim that Russians hacked their system without the access to those servers?

Give me a break..

( zero hedge)

vi) b. And now the report: what a joke!! No proof whatsoever on the Russian hacking

vii) Dave Kranzler reports on a true state of affairs with respect to the USA auto industry, the restaurant industry and on the consumer.

This should pour gasoline on the real jobs report issued today

( Dave Kranzler/IRD)

viii)The TIC report: the trade deficit increased because of the high USA dollar. Exports fell because of the high dollar while imports rose due to the same factor

Federal Reserve Bank of New York:

Earmarked gold movements

December report:

Last Oct/2016 we had 7,841 million dollars worth “gold” in inventory at the FRBNY

valued at $42.22 per oz

Last November/2016 we had 7,841 million dollars worth of gold in inventory at FRBNY valued at $42.22 per oz

thus 0 oz moved at $42.22

So far officially, the following has been repatriated to BuBa from NY:

2013: 5 tonnes

2014: 120 tonnes

2015: 99.5 tonnes

2016: to be officially announced

Their total quota from NY is scheduled to be 300 tonnes and another 374 tonnes from Paris of which 177 tonnes of gold has officially been sent (Dec 2015) and thus another 197 tonnes to cross the English channel.

Germany has officially 1237 tonnes of gold “stored ” in NY. On conclusion of the repatriation, Paris will have 0 stored there.

end

Let us head over to the comex:

The total gold comex open interest ROSE BY 8,215 CONTRACTS UP to an OI level of 431,823 AS THE PRICE OF GOLD ROSE $15.90 with YESTERDAY’S trading. We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year.

With the front month of January we had a GAIN of 17 contracts UP to 170. We had 13 notices filed so we GAINED 30 contracts or AN ADDITIONAL 3000 oz WILL STAND for gold in this non active delivery month of January. For the next big active delivery month of February we had a GAIN of 1,730 contracts UP to 277,267. March had a gain of 80 contracts as it’s OI is now 276.

We had 0 notice(s) filed upon today for nil oz

And now for the wild silver comex results. Total silver OI ROSE by 1172 contracts FROM 164,365 UP TO 165,537 AS the price of silver ROSE BY $0.08 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI FELL by 111 contracts FALLING TO 355. We had 110 notice(s) filed on yesterday so we LOST 1 CONTRACT or an additional 5,000 oz will NOT stand for delivery. The next non active month of February saw the OI rise by 40 contract(s) up to 204.

The next big active delivery month is March and here the OI rose by 548 contracts UP to 134,337 contracts.

We had 0 notice(s) filed for 0 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 232,980 contracts which is good.

Yesterday’s confirmed volume was 299,421 contracts which is very good

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

8037.500

SCOTIA

250 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

0 notice(s)

nil oz

|

| No of oz to be served (notices) |

170 contracts

17,000 oz

|

| Total monthly oz gold served (contracts) so far this month |

1023 notices

102,300 oz

3.1819 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,547,053.2 oz |

For January:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

2,126,813.02 0z

Scotia

CNT

JPM

|

| Deposits to the Dealer Inventory |

nil

|

| Deposits to the Customer Inventory |

1,081,872.270 oz

SCOTIA

JPM

Scotia

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(0 OZ)

|

| No of oz to be served (notices) |

355 contracts

(1,775,000 oz)

|

| Total monthly oz silver served (contracts) | 307 contracts (1,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 8,890,931.1 oz |

end

At 3:30 pm est we receive the COT report which gives us position levels of our major players. You will recall last week, that the bankers were going net long and the specs were going net short as the bankers goaded the specs. Let us see what today’s report brings:

First gold:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 208,855 | 112,305 | 71,021 | 97,410 | 215,022 | 377,286 | 398,348 |

| Change from Prior Reporting Period | ||||||

| 2,317 | 4,110 | 15,185 | 7,435 | 4,080 | 24,937 | 23,375 |

| Traders | ||||||

| 157 | 88 | 83 | 50 | 46 | 244 | 185 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 47,387 | 26,325 | 424,673 | ||||

| -1,777 | -215 | 23,160 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, January 03, 2017 | |||||

Our large speculators;

those large specs that have been long in gold added 2317 contracts to their long side

those large specs that have been short in gold, added another 4110 contracts to their short side.

Our commercials:

those commercials who have been long in gold added 7435 contracts to their long side.

those commercials who have been short in gold added 4080 contracts to their short side.

Our small specs:

those small specs that have been long in gold pitched 1777 contracts from their long side.

those small specs that have been short in gold covered 215 contracts from their short side.

Conclusion: commercials go net long by another 3355 contracts.large specs go net short by another: 1793 contracts. thus extremely bullish as the specs are again goaded into going net short.

And now for silver:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 86,821 | 25,530 | 9,877 | 42,493 | 118,307 | |

| 2,491 | 111 | -1,432 | 519 | 2,326 | |

| Traders | |||||

| 98 | 39 | 35 | 34 | 39 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 163,812 | Long | Short | |

| 24,621 | 10,098 | 139,191 | 153,714 | ||

| -863 | -290 | 715 | 1,578 | 1,005 | |

| non reportable positions | Positions as of: | 145 | 103 | ||

| Tuesday, January 03, 2017 | © SilverSeek.com | ||||

Our large speculators:

those large specs that have been long in silver added 2491 contracts to their long side

those large specs that have been short in silver added a tiny 111 contracts to their short side.

Our commercials;

those commercials that have been long in silver added 519 contracts to their long side.

those commercials that have been short in silver added 2326 contracts to their short side.

Our small specs:

those small specs that have been long in silver pitched 814 contracts from their long side.

those small specs that have been short in silver covered 179 contracts from their short side.

Conclusions:

it seems that our commercials are having a great difficulty in covering their huge shortfall as they continue to go net short by another 1807 contracts.

end

And now the Gold inventory at the GLD

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for Friday

GOLDCORE/BLOG/MARK O’BYRNE

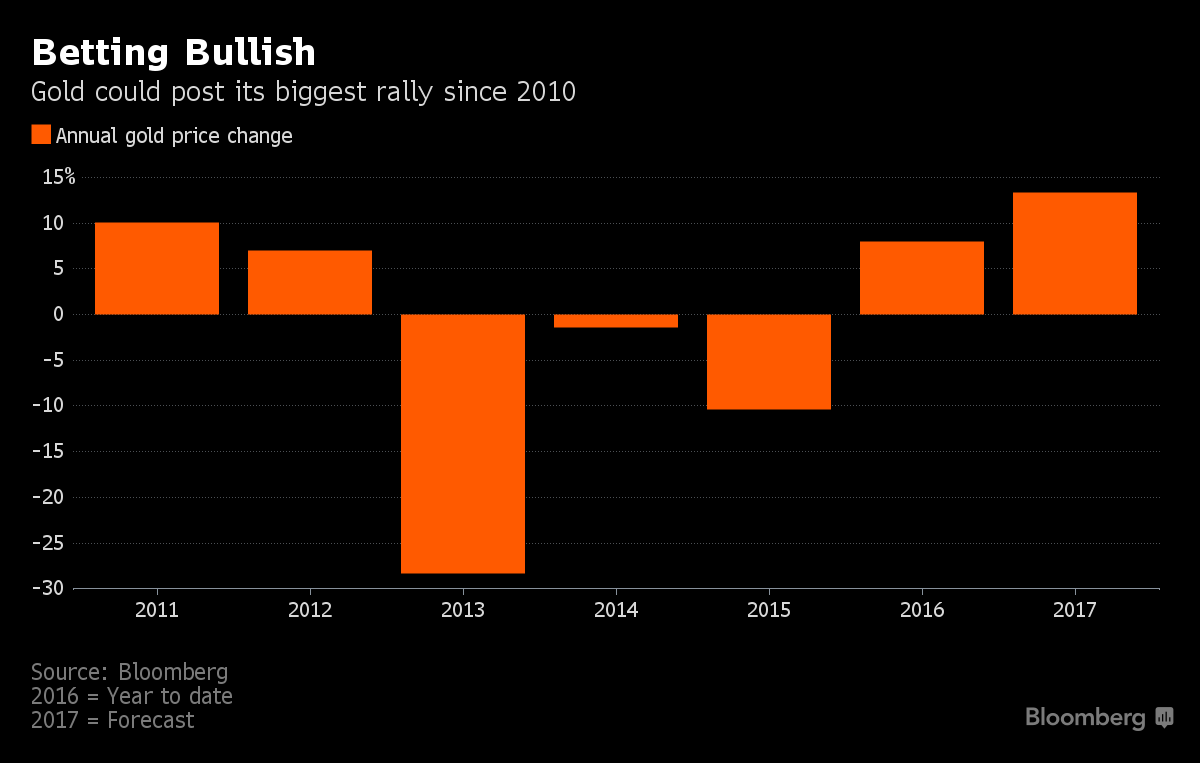

Trump’s Twitter “140 Characters” To Push Gold To $1,600/oz in 2017?

http://www.goldcore.com/us/gold-blog/trumps-twitter-140-characters-push-gold-1600oz-2017/

Trump’s Twitter Age Could See Gold Rise 13% In 2017

-

Gold price seen jumping 13% in 2017 after 9% gain in 2016, Bloomberg analyst survey shows

-

140-character missives by President-elect means new paradigm

-

“140 characters of unfiltered Trump is likely to create tensions with America’s largest trading partners…”

-

Bloomberg Intelligence poll shows 42 percent of respondents predict gold will be the best-performing metal in 2017

-

Two Bloomberg respondents including GoldCore say gold to reach $1,600/oz

-

“Markets that are already shaken by the fallout from Brexit, the coming elections in Europe and indeed the increasing specter of cyber warfare could again see a safe-haven bid…”

-

Gold is not “irrational” today – politicians, policy markers and markets are

-

Gold that can inspect and take delivery of easily a vital hedge against massive irrationality in world of 2017

From Bloomberg:

“The Donald J. Trump era is marking a new age for gold as an investor safe haven.

While the precious metal has always been hoarded in times of trouble, a bevy of political and economic surprises in 2016 sparked a surge in buying that sent bullion to the first annual gain in four years. Prices may rally about 13 percent in 2017, according to a Bloomberg survey of 26 analysts.

Fueling the bullish outlook is the risk of chaos on multiple fronts: a possible trade war from America’s fraying relationship with China, the alleged Russian hack of U.S. political parties, the U.K.’s complicated exit from the European Union, and elections slated in France, Germany and the Netherlands that may see a rise of nationalist groups.

And then there are Trump’s frequent Twitter posts, in which the U.S. president-elect feuded with rivals and made declarations that unsettled allies even before he takes office Jan. 20.

“140 characters of unfiltered Trump is likely to create tensions with America’s largest trading partners,” Mark O’Byrne, a director at broker GoldCore Ltd, said by e-mail.

“Markets that are already shaken by the fallout from Brexit, the coming elections in Europe and indeed the increasing specter of cyber warfare could again see a safe-haven bid.”

Gold for immediate delivery is up 8.9 percent this year (2016) to $1,155.12 an ounce, halting a three-year slide. More than two thirds of the analysts and traders surveyed from Singapore to New York said they were bullish for 2017.

The median year-end forecast was $1,300, with the year’s peak seen at $1,350. Two, including O’Byrne, said the metal may reach $1,600.”

President elect Trump, Twitter and his tweets being a popular topic du jour, the Bloomberg article was syndicated and published very widely internationally and can be read in full on Bloomberg here Gold ‘Lures’ Investors Worried About Trade Wars and Trump Tweets and Bloomberg Quint here Trump’s Twitter Age Brings Chaos Risk Reviving Gold as Haven

http://www.goldcore.com/us/gold-blog/trumps-twitter-140-characters-push-gold-1600oz-2017/

end

I am very happy to report that Keith Neumeyer is joining us in the class action suit against the major banks We need to have a major producer as plaintiffs

(courtesy Kitco)

Keith Neumeyer on Why He Joined Silver Manipulation Class Action Suit

Jan 06, 2017

Guest(s): Keith Neumeyer CEO, First Majestic

First Majestic’s chief executive officer, Keith Neumeyer speaks out on his role in the silver manipualtion class action suit including various banks. Neumeyer shares his thoughts on the silver price rigging case and shares what he plans to do about it.

-END-

An excellent Reuters report on the huge risks to the global economy as China burns through its foreign FX reserves. It is probably now below 3 trillion USA

(courtesy Reuters/GATA)

China’s choices narrowing as it burns through FX reserves to support yuan

Submitted by cpowell on Thu, 2017-01-05 15:21. Section: Daily Dispatches

By Nichola Saminather

Reuters

Thursday, January 5, 2017

SINGAPORE — As China’s foreign exchange reserves threaten to tumble below the critical $3 trillion mark, the biggest fear for investors is not whether Beijing can continue to defend the yuan but whether it will set off a vicious cycle of more outflows and currency depreciation.

Data this week is expected to show China’s forex reserves precariously perched just above $3 trillion at end-December, the lowest level since February 2011, according to a Reuters poll.

While the world’s second-largest economy still has the largest stash of forex reserves by far, it has been churning through them rapidly since August 2015, when it stunned global investors by devaluing the yuan CNY=CFXS and moving to what it promised would be a slightly freer and more transparent currency regime.

Since then, authorities have repeatedly intervened to support the yuan when it weakened too sharply, burning through half a trillion dollars of reserves and prompting them to sell some of their massive holdings of U.S. government bonds.

They also have put a tightening regulatory chokehold on individuals and businesses who want to move money out of the country, while denying they were imposing new capital controls. …

… For the remainder of the report:

http://www.reuters.com/article/us-china-economy-forex-reserves-analysis-…

END

A good background on China’s secretive gold reserves

(Ronan Manly/GATA)

Bullion Star posts primer on China’s especially secretive gold reserves

Submitted by cpowell on Thu, 2017-01-05 15:25. Section: Daily Dispatches

10:25a ET Thursday, January 5, 2017

Dear Friend of GATA and Gold:

Bullion Star’s latest primer on central bank gold reserves is about China’s, which, Bullion Star notes, are among the world’s most secret. The primer is posted here:

https://www.bullionstar.com/gold-university/central-bank-gold-policies-p…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod’s weekly message for us;

(courtesy Alasdair Macleod)

Alasdair Macleod: Fiat money quantity breaks $15 trillion

Submitted by cpowell on Thu, 2017-01-05 19:12. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney.com, St. Helier, Jersey, Channel Islands

Thursday, January 5, 2017

The fiat money quantity has now breached the $15 trillion level, standing at $15,108 trillion on November 1, 2016, the last calculable date. This is now $6.3 trillion above the pre-Lehman crisis trendline, exceeding it by 72 percent. Instead of the Lehman rescue being a temporary fix, the increase in the quantity of fiat money has continued to grow over eight years later.

After the Fed responded to the financial crisis, monetarist commentators warned that the accumulation of bank reserves at the Fed would one day be unleashed into an expansion of bank lending, because every dollar held in reserves could become more than $10 of bank credit. The accumulation of these reserves had had no precedent, and monetary policy was therefore in uncharted territory.

The only way bank reserves can be discouraged from leaving the Fed’s balance sheet is for the Fed to increase the Fed Funds Rate (FFR), which is the interest rate the Fed pays commercial banks on these reserves. The original concern is now becoming justified, because banks have been gradually withdrawing reserves held at the Fed over the last 18 months. For this reason, the Fed had no alternative but to raise the FFR in December 2015 and in December 2016, to start the process of normalizing rates. The Federal Open Markets Committee should be watching the withdrawal of reserves as a key indicator in formulating interest rate policy, not that it is openly admitted in the FOMC’s statements. …

… For the remainder of the commentary:

https://wealth.goldmoney.com/research/goldmoney-insights/fmq-breaks-15-t…

END

An excellent presentation by Koos Jansen on gold fundamentals between East and West

(courtesy Koos Jansen/Bullionstar)

Koos Jansen: How the West has been selling gold into a black hole

Submitted by cpowell on Fri, 2017-01-06 14:50. Section: Daily Dispatches

9:50a ET Friday, January 6, 2017

Dear Friend of GATA and Gold:

Gold market researcher Koos Jansen writes today that while gold flows in and out of the London market, once gold gets into China, it doesn’t come back. Jansen sees this pattern as gradually reducing the above-ground metal available for affecting gold’s price and indicating that prices will increase eventually. Jansen’s analysis is headlined “How the West Has Been Selling Gold into a Black Hole” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/how-the-west-has-been-sell…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Despite its manipulation gold advances against most currencies in the past 15 years

(courtesy Goldprice.org/GATA)

GoldPrice.org chart shows metal gained in all major currencies in 15 years

Submitted by cpowell on Fri, 2017-01-06 15:03. Section: Daily Dispatches

10:03a ET Friday, January 6, 2017

Dear Friend of GATA and Gold:

GoldPrice.org has posted a chart of gold’s performance in major currencies since 2002, and it shows far more green than red and net gains in all of them, ranging from a low of 156 percent in the Chinese yuan and a high of 496 percent in the Indian rupee. The chart is posted here:

http://goldprice.org/charts/history/gold-price-performance_x.png?1924122…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan UP to 6.9180(SMALL DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS COMPLETELY TO 6.83161 / Shanghai bourse CLOSED DOWN 11.09 POINTS OR 0.35% / HANG SANG CLOSED UP 46.32 OR 0.21%

2. Nikkei closed DOWN 66.32 POINTS OR 0.34% /USA: YEN RISES TO 115.97

3. Europe stocks opened ALL IN THE RED ( /USA dollar index RISES TO 101.71/Euro DOWN to 1.0577

3b Japan 10 year bond yield: FALLS TO +.056%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.97/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.17 and Brent: 56.77

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.251%/Italian 10 yr bond yield DOWN to 1.932%

3j Greek 10 year bond yield RISES to : 6.88%

3k Gold at $1176.10/silver $16.50(8:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 5/100 in roubles/dollar) 59.39-

3m oil into the 54 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a SMALL DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.97 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0112 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0705 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.251%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.355% early this morning. Thirty year rate at 2.952% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Flat Ahead Of December Payrolls; Dollar Rebounds

European shares fell modestly, Asian equities declined for the first day in three, and US equity futures were unchanged before the December U.S. nonfarm payrolls report. China’s offshore yuan fell the most in a year to pare a record weekly rally, while Mexico’s peso climbed after the central bank sold dollars. Oil was trading lower in early trading.

The main economic event on the financial calendar is today’s 8:30am ET December payroll report. The market consensus for today’s print is 178k which is in line with the 178k in November. It’s worth noting that there’s a reasonable range between economists though with the low forecast at 125k and the high forecast at 221k. DB’s Joe LaVorgna is at the lower end of the range and has pegged a 150k print which is more or less where yesterday’s ADP private employment survey came in at for December (153k vs. 175k expected). What might be more interesting though is whether or not the drop in the unemployment rate is sustained. As a reminder the U3 rate fell to 4.6% in November and the lowest since 2007 from 4.9% in October. The drop has been a focus for Fed officials with more talking about an undershooting of the longer run rate so it is worth watching. As always also keep an eye on average hourly earnings. The consensus is for a +0.3% mom rise in December which would have the effect of pushing the annual rate up to +2.8% yoy from +2.5%.

Should the report come in stronger than expected and provide evidence of a healthy U.S. labor market, we could see a second wind to a flagging dollar hit by doubts that Donald Trump will usher in an era of fiscal easing and rapid growth. The employment report is expected to confirm a sixth straight year with more than 2 million jobs added, which may help to stem the steepest losses on a Bloomberg gauge of 10 major currencies this week. Market positioning in options signals the dollar is poised for further gains against the euro.

Ahead of the report, world stocks held near 1-1/2 year highs and the dollar moved up from a three-week low on Friday, with investors looking to upcoming U.S. jobs data to provide clues on the pace of U.S. interest rate rises this year. The MSCI’s gauge of the world’s stock markets hit its highest since July 2015, taking its gains so far this year to 1.7 percent, helped by this week’s generally upbeat economic readings in the U.S., China and Europe. The yen, euro and British pound all weakened for the first time in three days and the Turkish lira extended its loss. European equities declined the most in a week and U.S. futures signaled losses, while the MSCI Asia Pacific Index declined for the first day in three. The three-month interbank lending rate for the offshore yuan rose to a record in Hong Kong.

A quick rundown of global indices from Bloomberg:

- The Stoxx Europe 600 Index was down 0.2 percent, as was the Dax in Germany.

- The MSCI Asia Pacific Index slipped 0.3 percent. The gauge is still headed for its best start to a year since 2010. Japan’s Topix Index fell 0.2 percent, though gainers outnumbered losers 996 to 859 on the gauge.

- Hong Kong’s Hang Seng rose 0.2 percent and Australia’s S&P/ASX 200 Index was little changed. South Korea’s Kospi advanced 0.4 percent as Samsung climbed. Singapore’s Straits Times Index rose 0.2 percent in a fourth day of gains.

- The Shanghai Composite slid 0.4 percent, while Taiwan’s Taiex index rose 0.2 percent, gaining for the fifth day. India’s S&P BSE Sensex lost 0.1 percent after climbing 0.4 percent earlier.

- The MSCI Emerging Markets Index was little changed after rising for three straight days. The benchmark index in the Philippines rose 0.5 percent to bring its weekly gain to 6 percent.

- Futures on the S&P 500 Index edged lower after the underlying gauge fell 0.1 percent Thursday, just below its record set on Dec. 13.

Weaker-than-expected private-sector ADP payrolls data on Thursday contributed to the dip in the dollar, despite strong data elsewhere. Investors were looking to today’s jobs figures to see if the bounceback for the dollar could be sustained.

“It’s likely that a stronger jobs number will, in the shorter term, strengthen the dollar. But (soon) people will start questioning how much of a strong dollar the Fed can stomach,” ETF Securities’ head of research and investment strategy, James Butterfill, told Reuters. “Given the sell-off in the dollar, there could be appreciation over the next few weeks, but in the coming few months we could see further dollar weakness.”

Already under pressure as the Trump rally wanes, the dollar extended losses on Thursday as China stepped up efforts to support the yuan, sparking speculation that it wants a firm grip on the currency ahead of Trump’s Jan. 20 inauguration. As noted last night, the cost of borrowing the yuan in Hong Kong, the main offshore yuan trading center, sky-rocketed and at one point hit 105%, making it too costly for speculators to sell the yuan against the dollar.

The offshore yuan has gained more than 2 percent in the last two sessions, its biggest two-day gain on record, to a two-month high of 6.7833 per dollar before it eased back about 1 percent in Asia on Friday to 6.8610. Having posted its biggest gain for 7 months, of 1.1 percent, in the previous session, it fetched $1.0589 EUR= on Friday.

“What’s going on is a correction of the ‘Trump trade’ since the election. The markets have been trying to fully price in his policies just based on hopes,” Standard Chartered’s executive director of finance, Koichi Yoshikawa, said. “From now on, it’s not going to be a simple one-way bet.”

Investors also closed short positions in U.S. bonds, one of the most popular plays since the election because Trump’s policies are seen as stoking inflation.

Oil prices were steady as Saudi Arabia and Abu Dhabi stared promised supply cuts, but doubts that all producers will implement output reductions agreed in a landmark OPEC deal last year kept markets from rising further. Gold retreated 0.4 percent to $1,175.17 per ounce after a three-day, 2.9 percent climb. Bitcoin slumped again and was trading at $900 at last check.

In rates, Australian bonds climbed, sending 10-year yields down five basis points to 2.68 percent, a level last seen in November; similar New Zealand rates dropped five basis points to 3.19 percent. U.S. Treasuries rallied Thursday by the most since the post-Brexit jolt, with the yield on the 10-year benchmark falling nine basis points to 2.34 percent. That was the biggest drop since June 27.

Markets Snapshot

- S&P 500 futures down less than 0.1% to 2262

- Stoxx 600 down 0.2% to 365

- FTSE 100 down less than 0.1% to 7194

- DAX down 0.2% to 11561

- German 10Yr yield up less than 1bp to 0.25%

- Italian 10Yr yield down 2bps to 1.92%

- Spanish 10Yr yield up 2bps to 1.5%

- S&P GSCI Index up 0.5% to 399.8

- MSCI Asia Pacific down 0.2% to 139

- Nikkei 225 down 0.3% to 19454

- Hang Seng up 0.2% to 22503

- Shanghai Composite down 0.4% to 3154

- S&P/ASX 200 up less than 0.1% to 5756

- US 10-yr yield up less than 1bp to 2.35%

- Dollar Index up 0.08% to 101.6

- WTI Crude futures up 0.9% to $54.25

- Brent Futures up 0.9% to $57.38

- Gold spot down 0.2% to $1,178

- Silver spot down 0.6% to $16.49

Global Headline News

- Carlyle Said to Explore Sale of Vitamin Maker Nature’s Bounty: Company said to be valued at about $6 billion

- China Said to Mull Scrutiny of U.S. Firms Amid Trump Tension: Options include antitrust, tax probes of American companies

- Trump Axing Obama Power Plan Means Coal Supplying 61% More Power: U.S. would use 523 billion kilowatt-hours more of electricity generated from coal in 2050 if Obama’s Clean Power Plan is dropped

- Trump Hits Toyota on Mexico as Car Criticism Spreads to Japanese: threatens to tax Toyota into building a plant in the U.S. instead

- FBI Says Democrats Refused Access to Hacked E-Mail Servers: Trump scheduled to be briefed Friday on campaign breach

- Marchionne Enters Final Push to Free Fiat Chrysler From Debt: Executives have expressed increasing confidence at recent investor meetings that they’ll reach their goals, according to people familiar

- Mylan’s EpiPen Sales Plan: Schools Today, Everywhere Tomorrow: wants to set up its own pharmacy to cut out middlemen and lobby for new laws that could expand sales of its biggest product

- Boeing Said Close to $10.1 Billion Order From India SpiceJet: Deal for 92 jets may grow based on outcome of negotiations

- Brevan Howard’s Hedge Fund Posts First Gain in Three Years: Returns 3% according to an investor letter

- McDonald’s Japan Same- Store Dec. Sales Rose 17% Y/y; 2016 Same-Store sales rose 20%

- Frontier Airlines Said to Aim to Raise About $500m in IPO that would imply a valuation of ~$2b company: NYT

- Morgan Stanley Said to Cut Equities Traders’ Bonus Pool Up to 4%: Firm is set to pay annual bonuses to employees next month

In Asian markets, stocks traded mixed following a lacklustre lead from Wall Street where financials underperformed, although the NASDAQ 100 still finished positive on strength in pharmaceuticals and FANG stocks. Asian stocks decline for first day in three. With MSCI Asia Pacific down 0.3% today it’s still headed for its best start to a year since 2010. Hong Kong stocks post their biggest weekly advence in three months. 6 out of 11 sectors drop as retail, material stocks underperform, real estate, telecoms outperform. Asian bourses were also indecisive as participants were tentative ahead of NFP, with Nikkei 225 (-0.3%) dampened by JPY strength and losses in Fast Retailing after Uniqlo same-store sales fell 5% Y/Y in December. ASX 200 (Unch.) was uneventful and traded flat while the KOSPI (+0.3%) was underpinned by better than expected Q4 preliminary results from Samsung Electronics. Chinese markets were mixed with the Hang Seng (+0.2%) led by energy names, while Shanghai Comp (-0.4%) lagged following a large net weekly drain of CNY 595BN by the PBoC. 10-yr JGBs traded higher amid the dampened risk sentiment in Japan with the yield curve flatter on outperformance in the long end, while the recent weekly securities transactions data also showed foreign investors returned to net buying of Japanese bonds.

Top Asian News

- Tata Sons Calls Shareholders Meeting to Oust Mistry From Board: Extraordinary general meeting scheduled to be held Feb.

- Bitcoin Buyers Eye Beijing Nervously as Price Drops Off High: Yuan accounts for 98% of bitcoin trading due to zero fees

- Wartime Sex Slave Dispute Resurfaces to Rattle Japan-Korea Ties; Tokyo suspends talks with Seoul over a foreign currency swap arrangement; temporarily recalls ambassador to South Korea; halts high-level economic talks

- Fiery Booze Drinkers Drive China’s Biggest Gains in Stocks: consumer staples surge led by baijiu-makers Moutai, Wuliangye

- China Seen Keeping Reserves Near $3 Trillion to Avoid Alarm: Stockpile is seen holding above key level for December

In Europe equity markets (Stoxx600 -0.1%) are trading mildly in the red as mining underperform in the FTSE 100 (flat) in what has been a particularly quiet session ahead of NFP. Stoxx Europe 600 Index declines 0.3% as travel & leisure, utility and commodity stocks underperform; real estate stocks gain. 18 of 19 sectors decline. 31% of Stoxx 600 members gain; 56% decline. Financials are the outperforming sector after some notable broker moves for Worldpay (WPG LN) and Lloyds (LLOY LN), subsequently both Co.’s are at the top of the FTSE leader board. Fixed income markets have not seen too much action thus far, with Bunds trading lower by 8 ticks and in the periphery 10 year PGB yield has found support at the 4% psychological area.

Top European News

- Sanofi Shares Slump After Amgen Wins Ban on Cholesterol Medicine: Court ruling blocks Sanofi and partner Regeneron Pharmaceuticals from selling the cholesterol-lowering medicine Praluent in the U.S. because it infringes Amgen’s patents

- Euro-Area Confidence Jumps to Highest Since 2011 on ECB Stimulus: recovery in the 19-nation region showed further signs of strengthening

- Draghi’s German Problem Flares as Inflation Jump Stirs Anger: Germans fret that the guardian of price stability will let them down

- BOE’s Haldane Says ‘Fair Cop’ to Getting Brexit Forecasts Wrong: Says economists have a lot of work to do to recover from failed predictions over the global financial crisis and Brexit

- U.K.’s May Tries to Charm Trump, Hoping for Early 2017 Meeting: Premier’s chiefs of staff made secret trip to U.S. in December

- TP ICAP Shares Soar After U.S. Election Boosts Revenue Growth: Company says 2016 revenue will probably rise 12% to 796 million pounds

- France Sees Three-Way Race for President as Fillon Bounce Fades: Independent Emmanuel Macron gains support, Socialist Party’s Valls would be well out of run- off range

In currencies, the offshore yuan fell 1.1 percent to 6.8599 per dollar after a four-day climb. The onshore yuan fell 0.6 percent. The euro declined 0.2 percent to 1.05843 per dollar and the pound was down 0.3 percent at 1.23793. The Bloomberg Dollar Spot Index rose 0.2 percent after falling 1 percent Thursday in its biggest slide since July on a closing basis. Companies added fewer jobs than forecast in December, according to a private research group. The yen fell 0.7 percent to 116.18 per dollar after strengthening 1.7 percent Thursday. The Aussie and kiwi dropped 0.3 percent and 0.2 percent, respectively. South Korea’s won lost 0.6 percent. Mexico’s peso jumped 0.5 percent after Banxico sold dollars to bolster the exchange-rate. The currency Thursday erased an advance of 1.5 percent after Trump threatened Toyota Motor Corp. with a border tax for planning to build a factory in Mexico. The Turkish lira was down 0.8 percent at a record low 3.6226 per dollar following a 0.6 percent drop the previous day.

In commodities, crude was down 0.4 percent at $53.55 a barrel after climbing 0.9 percent Thursday following a report that Saudi Arabia is cutting production as it implements an agreement to ease a global supply glut sparked the turnaround. However, further gains have been struggling on trader caution over OPEC implementation of last year’s output agreements. This morning there have been reports of Kuwait making a larger cut in production than required. Oil pushed higher but holds off weekly highs. Performance in base metals also staggering, and with recent gains all on fiscal spending hopes, while Gold prices come off better levels, but marginally so as yet. Gold retreated 0.4 percent to $1,175.17 per ounce after a three-day, 2.9 percent climb.

US Event Calendar

- 8:30am: Trade Balance, Nov., est. -$45.4b (prior -$42.6b)

- 8:30am: Change in Nonfarm Payrolls, Dec., est. 175k (prior 178k); Unemployment Rate, Dec., est. 4.7% (prior 4.6%)

- 10am: Factory Orders, Nov., est. -2.3% (prior 2.7%); Durable Goods Orders Nov. F, est. -4.6% (prior -4.6%)

- 11:15am: Fed’s Evans Speaks on Economy and Policy in Chicago

- 1pm: Baker Hughes rig count

- 3:30pm: Fed’s Kaplan Speaks in Chicago

DB’s Jim Reid completes the overnight wrap

It may be a holiday shortened week but there’s been more than enough news to keep markets on their toes in the first few days 2017. Global growth hopes have been boosted following the latest round of PMI’s. The FOMC minutes revealed that “uncertainty” is the new buzzword while one eye has been closely kept on the latest appointments by President-elect Trump. Meanwhile European politics continues to bubble below the surface. The latest food for thought though and the big focus over the last 24 hours has been in China where we’re back to watching the moves in the Renminbi closely after the offshore currency posted the biggest two-day rally on record.

We’ll dig into that shortly but before we get there we’ve got the final US employment report of 2016 to preview. As always nonfarm payrolls will be the big focus and the market consensus for today’s print is 175k which is just a shade below the 178k in November. It’s worth noting that there’s a reasonable range between economists though with the low forecast at 125k and the high forecast at 221k. Our US economists are at the lower end of the range and have pegged a 150k print which is more or less where yesterday’s ADP private employment survey came in at for December (153k vs. 175k expected). What might be more interesting though is whether or not the drop in the unemployment rate is sustained. As a reminder the U3 rate fell to 4.6% in November and the lowest since 2007 from 4.9% in October. The drop has been a focus for Fed officials with more talking about an undershooting of the longer run rate so it is worth watching. As always also keep an eye on average hourly earnings. The consensus is for a +0.3% mom rise in December which would have the effect of pushing the annual rate up to +2.8% yoy from +2.5%. All that to look forward to at 1.30pm GMT.

Back to China where yesterday the offshore Renminbi rallied a further +1.12% to 6.7889 and in doing so clocked a +2.51% two-day gain and the most on record. In fact up to yesterday’s close the currency had rallied +2.76% in 2017 already having weakened -6.20% last year. As a result the PBoC also moved to strengthen the fixing in the onshore currency this morning by the most since 2005 or since the Renminbi was de-pegged from the US Dollar. The rally for the offshore Renminbi has however faded a bit this morning (currently -0.50%). The catalyst for that earlier surge appears to be the crackdown by the PBoC on capital outflows at the end of last year – something we talked about in Tuesday’s EMR. In addition overnight lending rates in Hong Kong have surged in recent days (CNH Hibor touched 61% this morning and the second highest level on record) and liquidity is thin which is helping to exacerbate the moves.

It wasn’t just the Renminbi which had a good day against the Greenback yesterday with EM currencies also surging. The USD index actually closed -1.15% and is already back to mid-December levels. It’s little changed this morning. The Mexican Peso was also back in focus yesterday after Mexico’s Central Bank stepped in to stem the recent slide which helped the currency to rally back over +2%. However that was short lived with President-elect Trump taking to social media again and targeting Toyota this time with a border tax for planning to build a new plant in Mexico to import into the US. Meanwhile Treasuries were notably stronger with the benchmark 10y yield rallying 9.5bps to 2.345% – the lowest level since December 7th. Similar maturity Bund yields also edged down 3.3bps although the periphery was notably weaker (yields 5bps to 14bps higher).

There wasn’t much to report at the other end of the risk spectrum. The S&P 500 (-0.08%) paused for breath with financials and retailers suffering while in Europe the Stoxx 600 finished the day +0.10%. Elsewhere, over in credit markets the focus continues to be on the flying start for primary issuance in the US. Another $10bn priced in US IG yesterday which takes the week-to-date figure past $50bn and making it one of the biggest weeks of all time. What perhaps makes this more incredible is that, unlike in other record weeks, this week’s issuance total has not been boosted by one or two jumbo deals. Rather it’s been a steady diet of benchmark size deals.

Over in Asia this morning it’s been another fairly mixed start. The Nikkei (-0.39%) is in the red while the Hang Seng (+0.54%) and Kospi (+0.42%) are firmer. The Shanghai Comp and ASX are little changed. There’s been some focus on a Bloomberg story this morning too which suggests that China is prepared to step up measures aimed at scrutinizing US companies conducting business in China should Trump take punitive measures against the country. It’s hard to gauge how reliable the story is but it’s one to watch.

Moving on. While yesterday’s ADP print in the US may have come in a tad disappointing, data out of the services sector was less so. The services PMI was revised up at the final count to 53.9 in December from the earlier 53.4 flash reading. Meanwhile the ISM non-manufacturing print came in at 57.2 which, while unchanged versus November, was still better than expected (56.8 expected). Notably the new orders component ticked up to 61.6 from 57.0. The remaining data was the latest weekly initial jobless reading which saw claims fall steeply to 235k from 263k. There was also some Fedspeak yesterday with San Francisco Fed President Williams saying that three hikes in 2017 is a “pretty reasonable” assumption. Meanwhile in Europe yesterday the only significant data was in the UK where the services PMI for the December was reported as rising 1pt to 56.2 and to the highest since July 2015.

Before we look at today’s calendar a quick mention that this morning our European Equity Strategist Sebastian Raedler has raised his year-end Stoxx 600 target from 345 to 375 (3% upside from current levels). He expects 9% EPS growth this year, helped by the rebound in global growth momentum, stronger commodity prices and euro weakness. This would make 2017 the first year of meaningful European EPS growth since 2010. He argues that European equities benefit from two important inflection points. First, global growth is accelerating for the first time since 2013. Secondly, European earnings are rising again,

end

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 11.09 POINTS OR 0.35%/ /Hang Sang closed UP 46.32 OR 0.21%. The Nikkei closed DOWN 66.32 POINTS OR 0.34% /Australia’s all ordinaires CLOSED UP 0.07%/Chinese yuan (ONSHORE) closed WELL DOWN at 6.9180/Oil ROSE to 54.17 dollars per barrel for WTI and 56.77 for Brent. Stocks in Europe: ALL IN THE RED. Offshore yuan trades 6.83161 yuan to the dollar vs 6.9180 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS COMPLETELY TRYING TO STOP DOLLARS LEAVING CHINA’S SHORES /

3a)THAILAND/SOUTH KOREA/:

none today

b) REPORT ON JAPAN

Japan is angry at Trump especially that he got the facts on Japanese production of the Corolla wrong. Let us see what will happen in a few weeks when Trump takes over:

(courtesy zero hedge)

An Angry Japan Responds To Trump’s Toyota Taunts

After Trump’s Thursday morning twitter taunt targeted Toyota, when the President-elect warned Japan’s biggest carmaker that it will face heavy penalties if it chooses to make cars for the US market in Mexico, writing “Toyota Motor said will build a new plant in Baja, Mexico, to build Corolla cars for U.S. NO WAY! Build plant in U.S. or pay big border tax“, a tweet which sent shares of Japanese carmakers sliding on Friday with a 1.7% fall for Toyota, 2.2% for Nissan and 3.2% for Mazda, an angry Japanese government and corporate establishment pushed back against Trump’s criticism of Toyota as the attack on the country’s most powerful corporate name sent shockwaves across “Japan Inc.”

As the FT notes, CEOs of Japanese companies including Sony’s Kazuo Hirai and Nissan’s Carlos Ghosn weighed in, while analysts feared the president-elect’s targeting of Toyota would lead to a broader fallout on Japan-US trade relations, similar to concerns about an escalating trade war between the US and China.

“Toyota is responsible for large employment at US plants such as in Kentucky. It’s questionable whether the new US president has a grasp of how many vehicles Toyota builds in the US,” said Taro Aso, Japan’s finance minister. Hiroshige Seko, minister for trade and industry, added that the Japanese government would do its part to explain to the US administration about the contribution of the country’s car industry to the US economy.

“Toyota is equivalent to Japan as a whole, so Mr Trump’s criticism could be interpreted as a message to the Japanese government,” said Koji Endo, motor industry analyst at SBI Securities, expressing concerns about the impact on bilateral trade negotiations once Mr Trump is officially appointed later this month.

Analysts said Trump’s focus on Toyota, after Ford this week announced that it would pull plans for a $1.6bn Mexican plant, is not surprising but ironic for the Japanese carmaker who was the latecomer among global rivals in shifting production to Mexico. They noted that Toyota, which has an existing manufacturing facility in Baja to build the Tacoma pick-up truck, only made about 6% of 2.2m vehicles sold in the US in Mexico during the January to November period, compared with 33% for Nissan and 47 per cent for Mazda, according to SBI Securities, both of which companies are said to be far more exposed to Trump’s future ire than Toyota.

As the FT adds, in 2015, Toyota announced plans to spend $1 billion building a new facility in the central state of Guanajuato that will make Corolla vehicles from 2019.

The decision was a symbolic one for Akio Toyoda, Toyota’s chief executive, as it marked the lifting of a three-year moratorium on plant construction. It also underscored the company’s recovery since Mr Toyoda faced a US congressional grilling in 2010 in the wake a massive recall of spontaneously accelerating Toyota vehicles.

Having experienced the US recall crisis and the subsequent political backlash, analysts say Toyota may eventually adjust its strategy in Mexico, either by reducing the planned number of vehicle production or increasing the capacity of existing US plants in Texas or Mississippi.

“The company will carefully try to avoid taking action that would leave a negative impression on the new US administration,” said Masahiro Akita, analyst at Credit Suisse. “Considering how Toyota has operated in the past, it wouldn’t be surprising if the company makes a policy shift.”

In response to Trump’s tweet, Toyota has said no US jobs would be lost as a result of its planned new plant in Mexico. CEO Toyoda also said the company would “see what policies the incoming president adopts” before deciding whether to take action.

Still, Mr Akita said a complete reversal of Toyota’s plan to construct a new plant in Guanajuato was unlikely considering Mr Toyoda’s concerns about the impact on employment and the regional economy.

* * *

Then again, the Trump twitter effect may soon fizzle according to Reuters Breakingviews, which noted that Toyota’s day in Donald Trump’s crosshairs “could mark peak Twitter-Trump.”

On Thursday, the U.S. president-elect threatened tariffs on the Japanese carmaker, if it sold Mexico-made Corollas in the United States. Yet a 2 percent fall in Toyota’s Tokyo-listed shares looks muted considering Ford and General Motors performed as poorly or worse on New York trading. That’s because it quickly became clear Trump had all his facts wrong. The more that happens, the less impact his tweet storms will have.

Trump’s bully pulpit, both online and at rallies, can certainly be effective. General Motors, Lockheed Martin and Boeing have all scrambled to respond. This week Ford ditched a plan to build a new plant in Mexico that Trump had slated.

In Toyota’s case, a 35 percent import tax on 200,000 Corollas built annually at its new plant in Mexico would add $1.4 billion to their overall cost, assuming a $20,000 sticker price per car. That’s around 10 percent of this year’s expected earnings, which either Toyota or customers would have to swallow.

That’s never going to happen, though, for one very simple reason: Toyota’s new plant would replace one in Canada, not America. All Corolla production for U.S. sales remains in the company’s Mississippi factory. The plant is also in Guanajuato, not Baja, as Trump asserted.

Getting such basic facts wrong might not bother Trump’s supporters. But shareholders are more likely to get wise to such antics and start focusing on more concrete issues.

Contrast Toyota with Constellation Brands, the $30 billion alcoholic drinks firm. Its shares dropped more than 7 percent on Thursday, despite strong earnings. The maker of Corona and other Mexican brews faces higher costs if tax breaks are scrapped for overseas costs. That’s a central tenet of tax reforms sought by congressional Republicans and Trump. And these would be easier to put in place than long-term cross-border tariffs, which break trade agreements.

None of this means Trump’s ability to micromanage via social-media bullying is over. But the more his punches fall wide of the mark, the more inclined investors will be to ignore him.

While that may eventually pan out, for now the market (and various Trump tweet scanning apps) is far more transfixed by what Trump tweets in his daily social media sermons than even statements made by many if not all Fed members.

end

c) REPORT ON CHINA

Overnight the lending rate between banks soars to 105%. The offshore yuan (CHN ) continues its strength with POBC intervention as the shorts are getting squeezed:

(courtesy zero hedge)

Chinese Overnight Funding Rate Hits Unprecedented 105%

It appears Chinese authorities are deadly serious about crushing shorts and halting speculative outflows as the liquidity freeze in Chinese markets has sent overnight deposit rates to a record 105% as one or more bank’s utter desperation for funds looks like a giant fat finger.

Today’s spike is up 45 percentage points from yesterday’s 60% rate…

and at the same time, PBOC strengthened the Yuan fix by the most since 2005 to narrow the gap to the massive short squeeze move in offshore yuan...

END

Chinese volatility explodes as the offshore yuan goes all over the map. The POBC are very worried about the new Trump administration labeling the country as a currency manipulator and they may wish to keep a stronger yuan in the following few weeks. Also the yuan shorts are temporarily getting killed. However in the long run, the yuan should retreat to the 7.3-8.0 level

(courtesy zero hedge)

Chinese Volatility Explodes: Yuan Tumbles Most In One Year After Biggest 2-Day Rally Ever

While China’s unprecedented currency moves have quickly become the main talking point across global markets which otherwise have started off 2017 in an eerily calm fashion, it is the sudden surge in two-way volatility that has emerged a major threat to global market stability.

Case in point, the offshore Yuan fell as much as 1.1% to 6.8623 a dollar in Hong Kong, the most in exactly one year, after a record 2.5% surge over the past two sessions. This took place as a result of conflicting signals, as on one hand China continued to drain liquidity and sent overnight deposit rates into all time high territory, yet on the other the PBOC raised its fixing less than projected, but still the most since 2005, and Goldman Sachs advised its clients that the best time to short the yuan are just after interventions – like the recent one – which flush out bearish positions, or when China concerns were off traders’ radar screens.

China’s central bank raised its daily reference rate by 0.92% to 6.8668 per dollar on Friday the biggest rise since unpegging from the US dollar in 2005, following a 1 percent drop in a gauge of the greenback’s strength overnight. The offshore yuan was trading 0.8 percent weaker at 6.8457 per dollar as of 5:23 p.m. in Hong Kong, paring its weekly gain to 1.9 percent, the most in data going back to 2010. The onshore rate slumped 0.6 percent. Friday’s fixing was weaker than Mizuho Bank Ltd.’s prediction of 6.8447 and Australia & New Zealand Banking Group Ltd.’s estimate of 6.8456.

As we observed on Thursday evening, Yuan short sellers were once again squeezed in Hong Kong this week after interbank borrowing rates soared, and the dollar weakened as Bloomberg News reported that Chinese policy makers were preparing contingency plans to support the exchange rate even as they prepared for trade war with Donald Trump.

The three-month yuan interbank rate in Hong Kong, known as Hibor, surged to a record high, while the overnight rate jumped 23 percentage points to 61 percent, the highest since last January’s cash crunch. Rising interbank rates can make some short positions prohibitively expensive.

The move widened the offshore yuan’s premium over the onshore rate to 1.6%, the most since February last year. While borrowing rates in Hong Kong remained elevated on Friday, a broad recovery in the U.S. currency eased some of the pressure on bears.

Speaking to Bloomberg, Roy Teo, senior currency strategist at ABN Amro Bank NV in Singapore said that “The offshore yuan is sinking because there is some recovery in the dollar, perhaps the unwinding of short-yuan positions has mostly been done, and it’s closing the gap with the onshore currency.” The yuan is likely to weaken this year as capital outflows continue and the U.S. Federal Reserve increases interest rates, Teo said.

As shown in the chart below, in wildly volatile swings, the gave back much of its gains after a week that echoed the short squeeze in January of last year. That abrupt reversal marked the beginning of a nearly 5 percent rally lasting two months.

Chinese policy makers have several reasons to engineer a stronger or stable yuan in the short term. U.S. President-elect Donald Trump has pledged to label the country a currency manipulator on his first day in office, while the exchange rate came close to breaking through the psychologically-important level of 7 per dollar earlier this week. Policy makers also want to avoid a flood of capital outflows as citizens’ annual foreign-exchange quotas reset for the new year.

Meanwhile, Goldman warned that the Yuan will probably drop to 7.3 per dollar by December, emerging-market strategists led by Kamakshya Trivedi in London predicted in a note dated Thursday.

“The squeeze will have a temporary impact,” Luke Spajic, head of emerging Asia portfolio management at Pacific Investment Management Co., said in Hong Kong. “But I don’t think it necessarily changes the challenge, and the challenge is they still have to worry about the $50 billion to $60 billion a month of outflows and what they’re going to do about the value of their currency. And they have to face the fact that the U.S. is probably going to keep hiking rates.”

Benjamin Fuchs, chief investment officer at the $2 billion hedge fund BFAM Partners (Hong Kong), said China’s moves to repeatedly tighten capital controls risk eroding confidence in its currency. The dollar’s advance against the yen and other currencies has also increased competitive pressure on China to let the yuan depreciate, he said.

“We’re starting to see more and more of a negative cycle being created,” Fuchs said. China’s attempts to curb outflows are “just making people want to take money out quicker, and make companies change their behavior.”

The biggest problem, however, is that this volatility is starting to spillover into other currency, and asset markets, and as a result of the Chinese interventions even the dollar is starting to backoff from its recent 13 yearhighs.

Finally, in what may be a mockery of what traders observe every day, moments ago the PBOC said that China will keep the Yuan exchange rate “Basically Stable.” It added that it “will continue to improve yuan exchange rate formation mechanism this year” according to a statement after PBOC annual meeting on 2017 work.

Among other PBOC focuses:

- To improve policy framework, infrastructure for global yuan: PBOC

- To maintain prudent, neutral monetary policy: PBOC

- To keep liquidity basically stable: PBOC

Considering that China has failed abysmally at all three so far, markets are increasingly concerned that the worst possible outcome may be inevitable: China losing control over the currency. The global consequences would be severe.

END

After China warns its citizens on capital outflowing from China, today they came out and warns more directly against Bitcoin. They urged its citizenry to take a rational approach to investing in virtual currencies. It lowered in value immediately but gold rose.

(courtesy zero hedge)

Bitcoin Tumbles After China Urges Investors To Be “Rational”

After warning about cracking down on ‘virtual’ capital outflows earlier in the week, Chinese officials have come out more directly against Bitcoin this morning with the country’s central bank urging China’s institutional and individual investors should take a rational approach to investing in virtual currencies. Bitcoin in China has legged lower on the news.

Bitcoin prices had showed abnormal fluctuations, the Shanghai head office of the People’s Bank of China (PBOC) said in a notice.

This prompted branch officials to meet representatives of a major bitcoin trading platform in China, BTCC.

They cautioned against potential risks in the platform’s operations and asked it to carry out “self-inspection” according to the law, the bank said.

It stressed bitcoin is not a currency and cannot be circulated as a real currency in the market.

The reaction is clear with Bitcoin China tumbling to 5700 Yuan – down 35% from record highs…

Of course, this is no surprise, as we noted earlier, for those buying the dip here in bitcoin, having been driven by Chinese momentum, we urge readers to be cautious as by now the PBOC has certainly noticed that the digital currency remains one of the final, and most successful, means of bypassing capital controls in China. Should Beijing mandate that bitcoin no longer be a means to illegally transfer capital offshore, there is risk of an even more dramatic, and sharp, drop in its price.

4 EUROPEAN AFFAIRS

How European immigration, mainly Muslims are creating problems for the politicians in Europe. In order to deflect attention, government impose bans of the burka.

(courtesy Murray/Gatestone Institute)

European Immigration: Mainly Muslim, Mainly Male, Mainly Young

Submitted by Douglas Murray via The Gatestone Institute,

- In the wake of the attack in Nice, there should have been a fullsome public discussion over what if anything can be done to ensure that people who have been in France for many years — in some cases their entire lives — are not indoctrinated to hate the country so much that they drive a truck through a crowded sea-front on Bastille Day.

- Or there could have been a wide public debate over whether, with so many radicalised Muslims already in France, it was a wise or foolish idea to continue to import large numbers of Muslims into this already simmering situation.

- Merkel seems to hope that with this raising of a burka ban the German public will forgive or forget the fact that here is a political leader so devoid of foresight that she unilaterally chose to allow an extra 1-2% of the population to be added to her country in a single year, mainly Muslim, mainly male and mainly young.

- The burka and burkini, like the headscarf, are only issues because millions of people have been allowed, unchecked, into Europe for years. The garment is merely the simplest issue at which to take aim. Far harder are the issues of immigration and integration. It is possible that Europe’s politicians cannot answer these questions, because any and all answers would point the finger at their own failings.

- The European publics might get fed up with the distraction tactics of talking about garments and instead seek answers to the challenge we now face, as well as retribution at the polls for the politicians who brought us here.

2016 was a fine year for Islamist terrorism and an even finer year for Western political distraction. While Islamic terrorists repeatedly succeeded in carrying out mass-casualty terrorist attacks, as well as a constant run of smaller-scale strikes, the political leadership of the free world continued to try to divert their public.

The most striking example of the year came in the summer with the French debate over whether or not to ban the “burkini” from the beaches of France. The row erupted in the days after another 86 people were murdered in a jihadist terrorist assault — this time in Nice, France. With no one sure how to prevent access to vehicles or any idea how many French Muslims might want to follow suit, the French media and authorities chose to debate an item of beachwear. The carefully staged decision by an Australian Muslim woman to have herself filmed while wearing a burkini on a French beach ignited the row, which was eagerly seized upon by politicians.

At the local and national level, the decision to discuss the burkini allowed all the larger political issues behind Europe’s growing security problem to be ignored. In the wake of Nice, there should have been a fullsome public discussion over what if anything can be done to ensure that people who have been in France for many years — in some cases their entire lives — are not indoctrinated to hate the country so much that they drive a truck through a crowded sea-front on Bastille Day. Or there could have been a wide public debate over whether, with so many radicalised Muslims already in France, it was a wise or foolish idea to continue to import large numbers of Muslims into this already simmering situation.

As it was, neither of these debates did occur, and no meaningful political action was taken. Instead, the issue of the burkini sucked all the oxygen out of the debate, leaving no room to discuss anything more serious or longer term than beachwear.

In the wake of the July 14 attack in Nice, France, in which 86 people were murdered, there should have been a fulsome public discussion over what if anything can be done to ensure that people who have been in France for many years — in some cases their entire lives — are not indoctrinated to hate the country so much that they drive a truck through a crowded sea-front on Bastille Day. (Image source: France24 video screenshot) |

Across the continent in 2016, it appeared that other politicians realised the enormous advantage of such distraction debates. For instance, in the Netherlands in November, the country’s MPs voted for a ban on wearing a burka in public places. Prime Minister Mark Rutte apparently found this an enormously convenient debate. Not only did it temporarily reduce some of the pressure that his government is feeling at the rise of Geert Wilders’s Freedom Party to the top of opinion polls, but it also distracted attention from the years of mass immigration and lax integration demands which have been a hallmark of the Dutch experience.

After importing hundreds of thousands of people whose beliefs the Dutch authorities rarely bothered to question, the public would be satisfied — the Rutte government hoped — if only the small number of Dutch Muslim women who wear the burka were prevented from doing so. The Netherlands will have to see whether its implementation of such a law works any better than it does in neighbouring France, where “white knights” routinely show up to pay the fines of women fined for violating the burka ban there.

The Rutte government was not the only one to adopt this cynical strategy. Its most cynical deployment of all came in December, with the announcement by the German Chancellor, Angela Merkel, that she would ban the burka in Germany.

As with the Dutch government, Merkel clearly hoped that in throwing this tidbit to the German public she might head off the threat that the Alternative for Germany party (AfD), among others, now poses to her party in this year’s election. But the move also raises the question of just how stupid does Angela Merkel believe the German people to be? It would seem that Merkel hopes that with this burka ban the German public will forgive or forget that here is a political leader so devoid of foresight that she unilaterally chose to allow an extra 1-2% of the population to be added to her country in a single year, mainly Muslim, mainly male and mainly young.

This is a Chancellor who, even having previously admitted that Germany’s multicultural model had “failed,” revved immigration up to unprecedented and unsustainable levels. Now, like her counterparts across the continent, she must hope that the German public are satisfied by this burka morsel and that, as a result, they will return Merkel and her party to power so that they can repeat whichever of their mistakes they choose in the years ahead.

It is possible, of course, that the European publics are wiser than their leaders and that they will see through these cynical and distracting tactics. There are extremely good reasons to ban any garment which covers a person’s face and allows them to wander as an anonymous stranger in our societies. There are some — though fewer — reasons to ban wearing a burkini on a beach. Certainly the governments of France, the Netherlands and Germany are within their rights to instigate and enforce any and all such bans. Such moves, however, are but the smallest register imaginable of a problem that seems far beyond this generation of politicians.

The burka and burkini, like the headscarf, are only issues because millions of people have been allowed, unchecked, into Europe for years. The garment is merely the simplest issue at which to take aim. Far harder are the issues of immigration and integration. It is possible that Europe’s politicians cannot answer these questions because any and all answers would point the finger at their own failings. Or it is possible that they have no answers to the problems with which they have presented the continent. Whichever it is, they would do well to reflect that in 2017, the European publics might get fed up with the distraction tactics of talking about clothing and instead seek answers to the challenge we now face, as well as retribution at the polls for the politicians who brought us here.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

The Central bank of Mexico intervenes in the currency market trying to prop up the Peso but failed again. It seems that they sold a considerable amount of silver in their failed attempt. Is there something under the hood in the Mexican economy that we should be cognizant about:

(courtesy zero hedge)

Silver Dumps, Peso Jumps As Mexican Central Bank Intervenes (Again)

If at first you don’t succeed, intervene again! For the second time today (at midnight ET), Banxico officials confirmed the central bank entered the market to sell US dollars in an attempt to strengthen the peso. Now we await the next Trump tweet to take the peso back down…

As Bloomberg reports, according to a Banxico official who asked not to be identified, the central bank is looking to strengthen Mexican peso.

For now the move is far less impressive – which is odd given the lack of liquidity and an irrational peso buyer…

We have one other question… Is Banxico dumping its silver to receive dollars to sell to buy pesos?

Around $200mm notional of Silver was dumped in those few minutes.

As we noted at their earlier attempt, we can’t really blame Banxico for intervening: with the local population, of which over half lives in poverty, angry and protesting the recent “Gasolinazo”, or 20% increase in the price of gas, the crashing currency is sure to send many other prices, especially of imported goods, through the roof while sending much of the population over the edge. Which is why Goldman’s Alberto Ramos agrees that the central bank had to do something:

“In our assessment, some FX market intervention at this juncture is justified since market liquidity conditions became somewhat tighter, the MXN entered overshooting territory (excessively undervalued) and from current levels, significant additional exchange rate weakness, while making exporters even more competitive, can threaten two valuable public goods: price and local financial market stability. A very weak currency can have significant medium-term costs for the broader economy as it is likely to add pressure on inflation and wages (which would over time reduce the cost-competitiveness of the Mexican exporters) and prompt to a tighter monetary stance. Overall, higher inflation/wages and higher rates would be a clear negative shock to the non-tradable sectors of the Mexican economy, for they would not enjoy the exporters (tradable sectors) benefit of a weak currency.