Gold at (1:30 am est) $1188.10 DOWN $1.40

silver at $17.10: up 29 cents

Access market prices:

Gold: $1191.60

Silver: $17.14

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Jan 27/17 (10:15 pm est last night): $ 1204.39

NY ACCESS PRICE: $1185.20 (AT THE EXACT SAME TIME)/premium $19.19

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1213.15

NY ACCESS PRICE: $1183.15 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD/ 2ND FIX TODAY!!: $20.06

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London FIRST Fix: Jan 27/2017: 5:30 am est: $1183.15 (NY: same time: $1183.15 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Jan 27.2017: 10 am est: $1184.85 (NY same time: $1185.10 (10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

Today was quite surprising as silver skyrocketed northbound by 29 cents even though China entered their week long New Years festivities. The gold open interest was obliterated to 438,000 and that should be a sound bottom. Strangely the OI for silver remained elevated despite the constant raid these past two days. Remember that we still have two trading days left before the options on London’s OTC gold/silver expire so expect our two precious metals to be under the weather for those days. Next Friday is also the jobs report and they always manipulate our precious metals on that day.

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 0 NOTICE(S) FOR nil OZ. TOTAL NOTICES SO FAR: 1207 FOR 120,700 OZ (3.7542 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 34 NOTICE(s) FOR 170,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 745 FOR 3,725,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest surprisingly ROSE by 113 contracts UP to 177,408 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .887 BILLION TO BE EXACT or 126% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 34 NOTICES FILED FOR 170,000 OZ.

In gold, the total comex gold FELL BY A MONSTROUS 31,636 contracts WITH THE FALL IN THE PRICE GOLD ($7.80 with YESTERDAY’S trading ).The total gold OI stands at 438,856 contracts and a job well done by our crooked bankers.

we had 0 notice(s) filed upon for nil oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 799.07 tonnes

.

SLV

we had a huge changes in silver into the SLV: a deposit of 758,000 oz into its inventory/

THE SLV Inventory rests at: 335.759 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE by 113 contracts UP to 177,408 AS SILVER WAS DOWN 13 CENTS with YESTERDAY’S trading. The gold open interest FELL by 31,636 contracts DOWN to 438,856 WITH THE FALL IN THE PRICE OF GOLD OF $7.80 (YESTERDAY’S TRADING)

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

b) REPORT ON JAPAN

i)The yen tumbles again to the 115 to one area as the Bank of Japan boosts bond buying again. This action was taken to stop the yield from rising further. However that action failed as yields rose to .84% from .7%

( zero hedge)

c) REPORT ON CHINA

i)With new capital controls in China which commenced on Jan 1 2017, we now see property bubbles blowing up in Sydney, England and Vancouver. Buyers are already walking away from their down deposits:

( zerohedge)

4 EUROPEAN AFFAIRS

i)My goodness: The German editor of newspaper Die Zeit, Joffe, when asked how to end the “Trump Catastrophe” his answer was “assassination”

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

RUSSIA/USA

Putin and Trump will talk by phone tomorrow in their first step for normalization of relations.

( zero hedge)

6.GLOBAL ISSUES

i)Mexico

The war of words continue between Mexico and Donald Trump:

( zero hedge)

7. OIL ISSUES

With each passing week of new rigs being used to produce new amounts of oil, it is now wonder that the USA crude production is near a 10 month high. The number of rigs is at a 6 yr high:

(courtesy zero hedge)

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)As I highlighted to you yesterday, gold exports to China soar as we enter the Chinese New Year

( Bloomberg/GATA)

ii)Now India is trying to revive old colonial era gold mines.

( Reuters/GATA)

iii)Steve St Angelo comments on the future silver supply:

( Steve St Angelo/SRSRocco report)

10.USA STORIES

i)USA GDP grows by 1.9% in the 4th quarter and thus the entire GDP for 2016 was only 1.6%. The sharp drop in GDP was due to faltering exports and higher imports as the higher dollar certainly played a key role

( zero hedge)

ii)Hard data as opposed to soft survey data seems to be the sentiment of the day. The USA durable goods for new orders are tumbling:

( zero hedge)

iii)The Trump factor is certainly bringing consumer confidence back to the USA

iv) a.Trump now questions his decision to border tax Mexico (20%) as avocados, Beer , Chilli Peppers and Tequila will all rise by greater than 20%.( zero hedge)

iv) b

Today’s events in Trumpville:

i) Trump receives a call from Mexican President Nieto

ii) Trump and May (Great Britain) will make a press conference late in the day

iii) Trump pays a visit to the Pentagon

(courtesy zero hedge)

v)Oh OH! our hedge fund billionaires, owners of properties in the Hampton’s are seeing their luxury home prices crash 43% this year:

( zerohedge)

Let us head over to the comex:

The total gold comex open interest FELL BY A MONSTROUS BY 31,636 CONTRACTS DOWN to an OI level of 438,856 WITH THE FALL IN THE PRICE OF GOLD ( $7.80 with YESTERDAY’S trading). We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year.

With the front month of January we had a LOSS of 13 contract(s) DOWN to 47. We had 3 notice(s) filed YESTERDAY so we LOST 10 contract(s) or AN ADDITIONAL 1000 oz WILL NOT STAND for gold in this non active delivery month of January. For the next big active delivery month of February we had a LOSS of 44,325 contracts DOWN to 85,679.(feb 2016: 73,174 contracts). March had a GAIN of 323 contracts as it’s OI is now 1273. We are now CONSIDERABLY ahead with respect to OI when we compare data for open interest this year vs last year with the same amount of time to expire:

We had 0 notice(s) filed upon today for 300 oz

And now for the wild silver comex results. Total silver OI ROSE by 113 contracts FROM 177,295 UP TO 177,408 AS the price of silver FELL IN PRICE TO THE TUNE OF 13 CENTS with respect to YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI REMAINED CONSTANT AT 34 CONTRACTS. We had 0 notice(s) filed on yesterday so we neither gained nor lost any silver contracts that will stand in this delivery month of January. The next non active month of February saw the OI fall by 3 contract(s) DOWN TO 226.

The next big active delivery month is March and here the OI FELL by 650 contracts UP to 132,388 contracts.

We had 34 notice(s) filed for 170,000 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 356,356 contracts which is excellent.

Yesterday’s confirmed volume was 354,371 contracts which is excellent

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

289.35 OZ

Brinks

manfra

9 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

1864.700 oz

Manfra

58 kilobars

|

| No of oz served (contracts) today |

0 notice(s)

nil oz

|

| No of oz to be served (notices) |

47 contracts

4700 oz

|

| Total monthly oz gold served (contracts) so far this month |

1207 notices

120700 oz

3.7542 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 3000.000 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,821,484.0 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

1,813,829.756 0z

Delaware

CNT

HSBC

|

| Deposits to the Dealer Inventory |

nil

|

| Deposits to the Customer Inventory |

3005.200 oz

DELAWARE

|

| No of oz served today (contracts) |

34 CONTRACT(S)

(170,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 745 contracts (3,725,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 22,034,593.8 oz |

end

And now the Gold inventory at the GLD

Jan 27/no changes at the GLD/Inventory rests at 799.07 tonnes

Jan 26/no changes at the GLD/Inventory rests at 799.07 tonnes/

jan 25/another exactly the same withdrawal as yesterday: 50.4 tonnes and again this was used in the whacking of gold today/inventory rests at 799.07 tonnes

jan 24/a huge withdrawal of 5.04 tonnes and probably this was used today in the whacking of gold/inventory rests at 804.11 tonnes

Jan 23/a big change/this time a deposit of 1.19 tonnes of gold into the GLD/inventory rests at 809.15 tonnes. The drainage of gold from the GLD to Shanghai has now stopped!

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

Jan 13/17/there were no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 12/2017/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 11/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 10/no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 9/A WITHDRAWAL OF 8.87 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 805.00 TONNES

end

NPV for Sprott and Central Fund of Canada

end

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 209,854 | 100,447 | 119,798 | 109,000 | 235,374 | 438,652 | 455,619 |

| Change from Prior Reporting Period | ||||||

| -8,290 | -10,656 | 15,399 | 7,601 | 10,864 | 14,710 | 15,607 |

| Traders | ||||||

| 157 | 93 | 90 | 51 | 49 | 253 | 196 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 43,722 | 26,755 | 482,374 | ||||

| -273 | -1,170 | 14,437 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, January 24, 2017

|

|||||

end

At 3:30 pm est we get the COT report which gives position levels of our major players.

Let week we saw the commercials go net short getting ready for their whack which did happen

Our large specs:

those large specs that have been long in gold spilled their guts out by pitching 8290 contracts from their long side.

those large specs that have been short in gold covered 10,656 contracts from their short side.

Our commercials;

those commercials that have been long in gold added 7601 contracts to their long side

those commercials that have been short in gold added 10,864 contracts to their short side.

Our small specs:

those small specs that have been long in gold pitched a tiny 273 contracts from their long side.

those small specs that have been short in gold covered 1170 contracts from their short side.

Conclusions: the commercials go net short by 3263 contracts which we suspected would happen due to the raid on Wed.. and Thur of this week.

And now for silver:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 92,319 | 21,298 | 15,427 | 47,195 | 130,279 | |

| 1,481 | -58 | 2,809 | 2,167 | 3,515 | |

| Traders | |||||

| 93 | 37 | 42 | 34 | 37 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 177,601 | Long | Short | |

| 22,660 | 10,597 | 154,941 | 167,004 | ||

| -912 | -721 | 5,545 | 6,457 | 6,266 | |

| non reportable positions | Positions as of: | 146 | |||

Our large specs:

those large specs that have been long in silver added 1481 contracts to their long side

those large specs that have been short in silver covered a tiny 58 contacts.

Our commercials:

those commercials that have been long in silver added 2167 contracts to their long side

those commercials that have been short in silver from the beginning of time covered 3515 contracts from their short side.

Our small specs:

Those small specs that have been long in silver added 1395 contracts to their long side

those small specs that have been short in silver added 255 contracts to their short side.

Conclusions: the commercials go net short by only 1348 contracts. It seems that they have difficulty in covering their huge shortfall.

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRN

Dow 20K … US Debt $20 Trillion … Trump and $15,000 Gold

by Jan Skoyles, Editor Mark O’Byrne

In case you’ve been hiding under a rock, the Dow Jones Industrial Average reached 20,000 earlier this week for the first time in its 132 year history to much media fanfare.

Bigcharts via Financial Sense

Since Trump’s election US market indicators, including the Dow have been ticking up – it has been labelled the Trump rally. This latest milestone is something that the new President is happy to take credit for. In fact, he tweeted ‘Great! #Dow20K’ in response.

He told ABC News that

“We just hit a record, and a number that’s never been hit before. So I was very honored by that … Now we have to go up, up, up …”

Trump’s senior advisor (and fellow advocate for a weaker dollar) Anthony Scaramucci took to Twitter to thank President Trump for bringing about the best stock-market performance after a presidential election win since 1900. UKIP Leader Nigel Farage agreed that this was thanks to the Donald and saw it has a ‘huge vote of confidence in @POTUS.’

Few commentators pointed out that this latest ‘bubblelicious’ Dow milestone of 20K comes at a time when the U.S. is drowning in a sea of red debt as debt levels continue to surge and will reach the even more important milestone of $20,000,000,000,000 (trillion) in the coming weeks. The digit two is in both and both have a lot of zeros but the latter is actually much more important than the former.

In value terms, the 20,000 milestone means very little. In fact, in real value terms (when priced in gold) the Dow isn’t much higher than when it first hit just 1,000 back in 1972.

Make America Great Again has to mean Make America have Value Again

The Dow has had an impressive performance since November 8th, it has climbed around 9.5%. The actions of Trump since both his election and inauguration (from tweets to signing Executive Orders) have driven positive market reactions … so far.

There is little doubt that since his inauguration the new President has worked hard to show that he will make good on his election promises. All of which come under the umbrella to ‘Make America Great Again.’ In turn, market activity does show signs of what Keynes would have called ‘animal spirits’ – the self-feeding frenzy in markets when confidence is high.

As a result, it appears US markets are doing well and so the DJIA reaches a new all-time high in nominal dollar terms. But, as we have learnt from both Obama’s administration and all the others before that, there is a serious falsehood in claiming new records in markets really mean something, particularly when you are basing your information on an already flawed monetary system involving the increasingly debased currency that is the dollar, not too mention currencies internationally which are all being debased.

The Dow has been on a winning streak since 2009, in the period of Obama’s two term presidency the index climbed 144%, the S&P 500 172% and the Nasdaq Composite 275%. No-one can claim that this was all thanks to the Obama administration and some argue that it is not a reflection of what the 44th President really did for the economy given the actions of central banks both at home and abroad – involving QE on an unprecedented scale and an unprecedented monetary experiment in zero percent and negative interest rates.

It is worth noting that Venezuela and previously Zimbabwe had the best performing stocks markets in recent years.

In fact, whilst Trump will be keen to beat Obama’s stock market performance figures, he was a vocal critic of the ‘falsehoods’ upon which his predecessor based his economic KPIs on. We wonder if Trump will remember this when he continues to publish self-congratulatory tweets about the DJIA’s success.

DJIA – the wrong way to value investment performance and an economy

For a start, the Dow Jones Industrial Average is an odd measure for a economy’s success. There are hundreds of publicly traded companies in the United States, but the DJIA only considers 30 of them. There is no clear reason why it includes those particular 30 and their performance is calculated using the Dow Divisor (which is currently 0.14602128057775).

Trump is celebrating something that has come about in the face of what he called ‘a false economy.’ An economy, that he inherited from Obama and continues to benefit from – the economy that has been pumped up by the Federal Reserve including a massive increase in public and national debt.

When you look at the DJIA against something that has held its value, as opposed to the debased dollar and the artificially stimulated US economy, then you will see a different story.

Dow Jones Versus Gold

‘Sir Charles’ over at pricedingold.com, draws our attention to the fact that the Dow priced in gold is nowhere near its high of 1110 grams of gold (49 oz) seen in 1999 when the DJIA rose to a record of 11,700 and gold was at a record low of $240 per ounce (see chart). Last Friday, when Trump was inaugurated the Dow was at 530g (18.1 oz).

Breaking through 20,000 is clearly an important psychological level for traders and markets, as it was in 1972 when it reached 1,000, then 5,000 in 1995 and 10,000 in 1999 and 15,000 in 2013. The difference though from the first big milestone in 1972 and today is that much of that was driven by a real economy, real company profits and real economic growth.

Sir Charles explains:

“Breaking the 1,000 barrier in November of 1972 was an emotional moment for traders on the floor and investors around the world. It seemed to mark a new era of prosperity, even as, behind the scenes, inflation and recession were preparing to set in. At that time, Dow 1,000 USD meant Dow 482 grams of gold, and through the rest of 1972, the Dow traded between 480 and 500 grams.’

It wasn’t until 1973 that the strings began to unravel and both the dollar and stock market began to fall, the Dow reached its all time low of 37g (1.3oz) in 1980. Were that to happen today with the DJIA at 20,000, we would need to see gold prices surge to $15,384 per ounce.

As you can see from the important chart above, the largest bull-market in the Dow Jones began in 1980, Sir Charles states that we need to ask if we are

“now following the trajectory of the early 1980s (on our way to the moon again) or if we are instead channeling the spirit of 1974 to 1977 (a major bear market rally, on our way to a retest of all-time lows).”

Trump, the Fed and gold

The answer to this question lies with Donald Trump. As we have explained already, whilst the recent highs in the DJIA might not mean much in real-terms, it is an important indicator of the high expectations traders have for Trump and his radical policies – at least in the short term anyway.

This is a President who has won an election on promises to grow a real economy and to bring it back to its former glory days, this surely means a currency that is worth something.

For all of Trump’s comments on the Fed during the election campaign and complaints about the strong dollar in the run-up to the inauguration, he actually hasn’t done much to reassure us that he is aware of how to fix the financial system. Instead, he talks about the strong dollar in relation to its exchange rate with another currency, not in terms of its real value.

For Trump the solution appears to lie in protectionism, which just seems to be a way of papering over very odgy vulnerable and cracked foundations. Economics and the Triffin Dilemma tells us that Trump can’t have his cake and eat it – there is an incompatibility between the domestic policy of a country (which operates a global reserve currency) and the international monetary order.

Instead, the solution may lie in real monetary reform. Something his recent pronouncements and cabinet appointees strongly suggest will not take place.

During the Republican nomination rounds, there was plenty of talk about the value of the dollar and how it could be reformed to some of its past glory through the gold-standard. Since Trump’s nomination, this has not been mentioned again.

From a Libertarian perspective, he is proving himself very disappointing indeed. Both in terms of economic and monetary policies and indeed in terms of his expansionist, some would say quasi-imperialist foreign policies.

If Trump really wants a reason to fist pump on social media, and show that he is bringing real value to the US economy, he would have to begin to focus on honest money and basing his monetary policies on something of real value – gold. So far there is little sign of this – quite the opposite as his fiscal policies are wildly expansionary and this needs to be paid for by the already massively indebted U.S. sovereign.

The New York Sun editorial summed it up well this week:

“This is a moment to press the importance of true monetary reform — a point that was marked on the Journal op-ed page January 24 in a piece by John Mueller. He argues precisely that Mr. Trump’s trade real trade problem is not a lack of protectionism but a lack of the right monetary system. “When America had a gold or silver standard, the federal budget ran an annual surplus averaging 0.4% of gross domestic product,” he writes. “When it hasn’t, the average deficit has been 2.7%.”

Who is going to carry this reform for Mr. Trump? He has an early chance to nominate two governors of the Federal Reserve and, before long, to replace the chairman and vice chairman. These choices will be important. Mr. Trump’s nominee as Treasury Secretary, Steve Mnuchin, seems lukewarm or even indifferent to the cause of honest money. Vice President Pence, however, gets it down to the ground. We’ve already suggested Senator Cruz as the next Fed chairman.

A long-shot, no doubt, though the senator of Texas was the first candidate to thrust monetary policy to the center of the campaign. This week, the editor of the Interest Rate Observer, James Grant, asks a craftier suggestion: “Is it so farfetched,” he quips, “to imagine Stephen Bannon as chairman of a Trumpian Federal Reserve?” We’ve met Mr. Bannon only glancingly, but he strikes us as having the kind of crust that will be needed if Mr. Trump is to get a monetary reform to undergird his radical presidency.”

A return to the gold standard may seem a way off, but if Trump’s presidency continues to be as radical as it initially appears it is not impossible to imagine monetary reform happening.

However, it may be that necessity rather than prudence forces the President’s hand. Given the scale of U.S. debt, a dollar crisis seems increasingly likely. The new President may then be forced to look to gold as a way to restore confidence in a battered greenback.

Conclusion – Dollar ‘great’ or dollar crisis?

To conclude, ‘Sir Charles’ sums it up nicely. He writes that gold is not perfect, but that

“it has stood the test of time, both as cash money and as a measure of value, for thousands of years – while hundreds of other currency systems have come and gone.”

Trump so far appears to be exacerbating and accelerating financial, monetary and geo-political trends that were already taking place. What was happening slowly and almost imperceptibly under Bush II and Obama is now becoming more apparent and intensifying under Trump. Wars are very expensive things to wage and have to be financed. Today they are being financed by stealth currency devaluation.

Will Trump accelerate the decline and devaluation of the US dollar during his Presidency? Or will he make the dollar “great again” and restore the greenback to its former glory?

The signs in the first few days of his Presidency are not good, underlining once again the importance of owning physical gold to protect against geo-political risks, stock and bond market bubbles and the continuing devaluation of all fiat currencies.

http://www.goldcore.com/us/gold-blog/dow-20k-us-debt-20-trillion-trump-15000-gold/

END

As I highlighted to you yesterday, gold exports to China soar as we enter the Chinese New Year

(courtesy Bloomberg/GATA)

Gold exports to China soar in run-up to year of the rooster

Submitted by cpowell on Thu, 2017-01-26 19:55. Section: Daily Dispatches

By Ranjeetha Pakiam and Eddie Van Der Walt

Bloomberg News

Thursday, January 26, 2017

Gold exports to China soared in the run-up to the start of the lunar new year, with volumes increasing in December from major suppliers Switzerland and Hong Kong.

More gold was sent from Swiss refiners to the world’s top consumer than in any month since at least January 2014, according to data on the website of the Swiss Federal Customs Administration, while imports from the Asian city-state also increased compared with November.

China is the world’s top gold consumer, according to data from researcher Metals Focus Ltd., and the start of the Year of the Rooster this week is associated with gifting the precious metal. Lower prices at the end of last year, brought on by a stronger dollar as the U.S. increased interest rates, supported demand. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-01-26/china-s-gold-imports

END

Now India is trying to revive old colonial era gold mines.

(courtesy Reuters/GATA)

India mulls reviving colonial-era gold mines with $2 billion in reserves

Submitted by cpowell on Thu, 2017-01-26 20:00. Section: Daily Dispatches

By Neha Dasgupta

Reuters

Thursday, January 26, 2017

NEW DELHI — India is planning to revive a cluster of colonial-era gold mines — shut for 15 years but with an estimated $2.1 billion worth of deposits left — as the world’s second-largest importer of the metal looks for ways to cut its trade deficit, officials said.

State-run Mineral Exploration Corp. Ltd. has started exploring the reserves at Kolar Gold Fields, in the southern state of Karnataka, to get a better estimate of the deposits, according to three government officials and a briefing document prepared by the federal mines ministry that was seen by Reuters.

The ministry has also appointed investment bank SBI Capital to assess the finances of the defunct state-run Bharat Gold Mines Ltd., which controls the mines, and the dues the company owes to workers and the authorities, said the officials, who are involved in the process.

India, the world’s biggest gold importer behind China, spends more than $30 billion a year buying gold from abroad, making the metal its second-biggest import item after crude oil. …

… For the remainder of the report:

http://www.reuters.com/article/us-india-gold-reserves-idUSKBN15A05N

END

Steve St Angelo comments on the future silver supply:

(courtesy Steve St Angelo/SRSRocco report)

Future Silver Supply Will Be More Vulnerable Than Other Metals

SRSrocco

January 26, 2017

There has been a lot of discussion on the remaining global supply of certain precious metals on the alternative media. I continue to read articles that state there are only ten years worth of silver remaining. Unfortunately, many of these figures are inaccurate. So, I thought I would provide an update based on recent USGS – United States Geological Survey data and information.

For example, some analysts continue to say there are only ten years worth of silver reserves remaining. This was true back in 2009, before the USGS updated their figures. Unfortunately, the USGS had not updated their silver reserve figures for quite some time and the higher silver price (including higher prices for metals associated with by-product silver production) was as an additional factor that led to much higher silver reserve estimates in follow years.

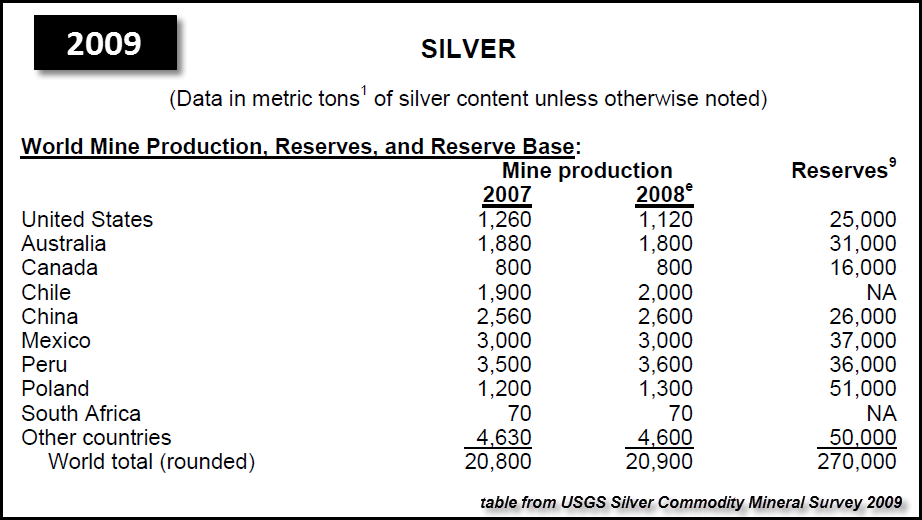

Here is a table from the USGS Silver Commodity Mineral Survey in 2009:

If we take the estimated silver reserves (2009) of 270,000 metric tons (mt) and divide by the annual production of 20,900 mt in 2008, that would equal 12.9 years worth of remaining reserves. Again, this is where many in the precious metals community state that there are only ten years (close enough) worth of silver remaining.

However, the USGS started revising their silver reserve figures in the following years and also replaced the “NA” information in the table above with actual reserves. Basically, the low silver price in the early 2000’s did not motivate governments to revise their silver reserves. But, as the price of silver started to skyrocket after 2009, well then, it was time to put some REAL VALUE to these silver reserves.

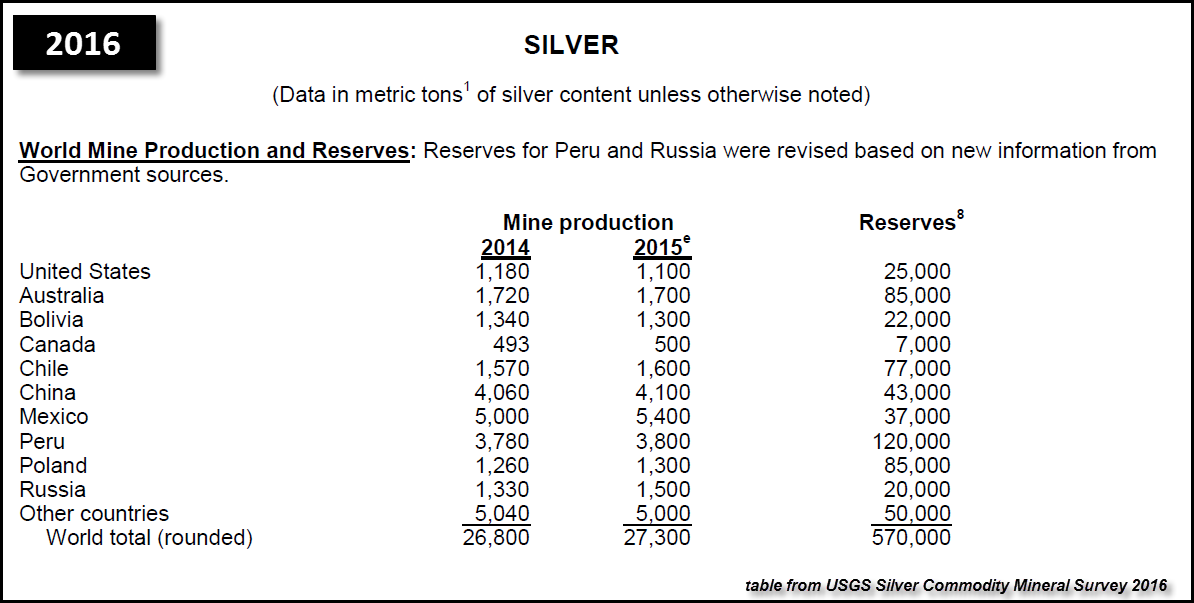

Here is the most recent table by the USGS, of global silver reserves:

According to the USGS, total global silver reserves are now 570,000 mt. Thus, if we divide 2015 production of 27,300 mt, we end up with 20 years worth of global silver reserves remaining… at current rates of annual production. You will notice, that Chile now has silver reserves of 77,000 mt for 2015. However, the USGS had a “NA” next to Chile’s silver reserves in its 2009 Silver Commodity Summary.

Furthermore, the top three countries (Peru, Australia & Poland) account for 51% of the total world silver reserves at 290,000 mt.

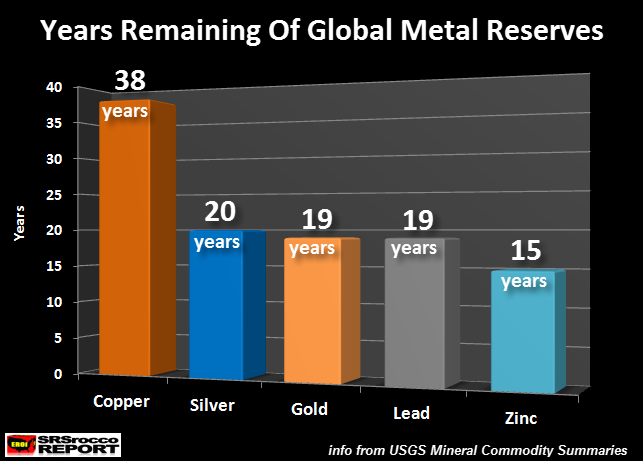

That being said, here is a chart showing the years remaining of the top global precious and base metals:

According to the USGS, copper has the largest amount of reserves remaining at 38 years compared to silver (20 years), gold (19 years), lead (19 years) and zinc (15 years). Of the five metals shown in the chart above, silver has the second highest amount of reserves, based on years worth of supply remaining.

Interestingly, zinc has the least amount of metal reserves, at only 15 years of supply. Regardless, these official estimates are based upon business as usual continuing in the global economy for the next 30-40 years. While these reserve estimates provide an “official gauge” as to how many years worth of supply of each metal is remaining, I doubt they will last that long.

This will be due to the peak and decline of global oil production as well as the continued collapse of net energy from oil supplied to the market. That being said, silver reserves will likely fall the most as 70% of silver production comes as a by-product of base metal and gold production.

Once the global oil industry disintegrates under the weight of falling prices as costs continue to rise, the decline of base metal and gold production will impact silver the greatest. Not only will silver reserves plummet to a greater degree versus the other metal reserves, so will its annual production rate.

These two factors will make the future supply of silver more vulnerable than most other metals… even gold. More on this in future articles.

IMPORTANT NOTE: If you have not listened to my interview with Craig at TFMetals Report, please check it out here: A2A with Steve St. Angelo of SRSrocco Report

END

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan DOWN to 6.8840(ZERO DEVALUATION /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/ CHINA/OFFSHORE YUAN WIDENS TO 6.8646 / Shanghai bourse CLOSED / HANG SANG CLOSED DOWN 13.39 PTS OR 0.06%

2. Nikkei closed UP 65.01 POINTS OR 0.34% /USA: YEN RISES TO 115.10

3. Europe stocks opened ALL IN THE RED ( /USA dollar index RISES TO 100.63/Euro UP to 1.0689

3b Japan 10 year bond yield: FALLS TO +.084%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.10/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.37 and Brent: 55.66

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.477%/Italian 10 yr bond yield UP to 2.23%

3j Greek 10 year bond yield RISES to : 7.11%

3k Gold at $1183.65/silver $16.73(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 45/100 in roubles/dollar) 59.89-

3m oil into the 53 dollar handle for WTI and 55 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT ZERO DEVALUATION from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.10 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9998 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0685 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.477%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.518% early this morning. Thirty year rate at 3.10% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dollar Rebound Continues, Europe Stocks Pressured By Banks As Much Of Asia Goes On Holiday

US equity futures are unchanged, trading near record highs after digesting a spate of earnings results on Thursday. The dollar pared its weekly loss as the yen and pound slid, while gold headed for its longest slump in three months. European equities fell and markets in Asia were mixed, while markets in China, South Korea, Taiwan and Vietnam were closed Friday for the start of Lunar New Year. Hong Kong, Malaysia and Singapore had shortened sessions.

The dollar continued its recovery against a basket of other currencies on Friday, while banks dragged European shares slightly lower following underwhelming results from Swiss major UBS. The two-day recovery comes after the dollar suffered a 4 percent drop in the three weeks from Jan. 3 as doubts emerged about how Trump’s policies will play out for the currency, particularly after both Trump and Treasury Secretary-designate Steven Mnuchin hinted at concerns over its strength. The yen extended its biggest decline in a week and Japanese bonds rose as the BOJ stepped in to buy more debt than expected. The pound also slid ahead of British Prime Minister Theresa May’s meeting with Donald Trump.

“The (dollar) has experienced a powerful rebound re-establishing post-U.S. election relationships between the performance of risk assets and U.S. bond yields on the one hand and the (dollar) on the other hand,” said Morgan Stanley FX strategists led by Hans Redekker, in a note to clients.

Trump suggested overnight he would push ahead with a 20 percent border tax on Mexico, spurring a slump on the peso and refocusing market expectations on his pro-business policies which, along with healthy corporate results, helped stocks on Wall Street to fresh record highs. However, the peso has since rebounded after the White House backtracked on its border tax proposal, when Sean Spicer said it was only “theoretical.”

On the political calendar, all eyes will be on the upcoming meeting between UK PM Theresa May and Donald Trump today. She will be the first leader to meet the President and a lot of attention will be placed on the outcome. May wants to try to pave the way for a free trade deal with the US post-Brexit and Mr Trump, in spite of his protectionist biases, would probably like to help the UK prosper if for no other reason than to help prove his point that the EU is flawed and the UK is better off outside of it. So although it’s a very early meeting where nothing will be decided it’ll be interesting to hear from the leaders afterwards. Trump’s ability to be confrontational on the global stage was demonstrated yesterday as we saw US-Mexico trade relations continue to grow strained as Mexico’s President Enrique Pena Nieto officially cancelled a planned meeting with Trump as the latter continued to signal intentions of building “the wall” and substantially increasing border security. He said that if the Mexicans had no intention of paying for the wall they should cancel next week’s trip. This is precisely what they’ve done.

Back to markets, where the global equity rally fizzled modestly after U.S. benchmarks reached all-time highs this week, as corporate results from Caterpillar Inc. to Microsoft Corp. delivered a mixed picture on the state of the American economy ahead of the Federal Reserve meeting next week. The Bank of Japan also meets and is expected to leave policy unchanged as recovering exports, strength in production and buoyant oil prices support reflation. The MSCI Asia Pacific Index fell 0.1%, while Japan’s Topix climbed 0.3%, bringing it near its highest point in more than a year. Australia’s S&P/ASX 200 Index rose 0.8 percent as the nation’s markets reopened after a holiday. India’s Sensex, also back from a holiday, gained 0.7 percent. Hong Kong’s Hang Seng Index slipped 0.1 percent, while Singapore’s Straits Times Index added 0.4 percent for its highest close since October 2015.

European stocks were headed for a weekly gain of about 1 percent though were slightly lower on Friday as weakness in the banking shares weighed. The Stoxx Europe 600 fell 0.3% following three days of gains. A fall in profits sent UBS shares down more than 3% as investors locked in some gains following a strong rally in financials stocks following the U.S. election. The European banking index fell 1.2 percent.

In the UK, the FTSE was also slightly lower but outperformed other regional benchmarks supported by merger activity as leading supermarket operator Tesco struck a deal to buy up wholesaler Booker to create what it claims will be Britain’s “leading food business”. The deal values Booker at 205.3p a share, or £3.7bn, a premium of 12 per cent over its closing price of 183.1p a share on January 26 according to the FT. Booker acquired grocery chains Budgens and Londis in 2015 and has over 170 cash and carry locations in the UK. Tesco said Booker shareholders will receive 42.6p in cash and 0.86 in new Tesco shares. The merger will result in Booker shareholders owning 16 per cent of the combined company. Tesco shares surged 10 percent.

Futures on the S&P 500 Index were down less than 0.1 percent. The benchmark slipped 0.1 percent Thursday after rising past 2,300 for the first time, while the Dow Jones Industrial Average extended an all-time high.

Benchmark German bonds are headed for their worst week since the aftermath of November’s U.S. election on Friday, as Trump’s first week in office fuels expectations of inflation and growth-boosting policies in the world’s biggest economy. The yield on 10Y Treasuries was up one basis point at 2.52%. It slipped one basis point Thursday after an auction of $28 billion in seven-year notes drew a record amount of buying from indirect bidders, signaling interest from foreign central banks and mutual funds. Japanese 10-year yields fell one basis point to 0.08%. As reported last night, the BOJ boosted the amount of 5-to-10-year bonds it buys in its outright purchase operations, underscoring a commitment to keep its yield-curve target.

In a report citing EPFR data, Bank of America reported that investor flows continue to point to a preference for so-called “reflation” trades. Funds investing in TIPS, high-yield bonds and Japanese equities, attracted inflows over the past week, the data showed. “But the re-positioning feels grudging and flows have yet to show big asset allocation capitulation out of bonds into stocks,” BofA’s Michael Hartnett said.

In commodity markets, oil prices gave up earlier gains as rising crude output from the United States was seen offsetting efforts by OPEC and other producers to prop up the market by cutting supplies. Trading was choppy as volumes were lighter than average with much of Asia closed due to the start of the Lunar New Year holiday. Brent crude futures, the international benchmark for oil prices, were trading at $55.98 per barrel, down 0.5 percent from their last close. U.S. West Texas Intermediate (WTI) crude futures were down 0.2 percent at $53.67 a barrel

Market Snapshot

- S&P 500 futures down less than 0.1% to 2292

- Stoxx 600 down 0.5% to 366

- FTSE 100 down 0.1% to 7152

- DAX down 0.3% to 11816

- German 10Yr yield down less than 1bp to 0.48%

- Italian 10Yr yield up 2bps to 2.26%

- Spanish 10Yr yield up less than 1bp to 1.58%

- S&P GSCI Index down 0.4% to 399.2

- MSCI Asia Pacific down less than 0.1% to 142

- Nikkei 225 up 0.3% to 19467

- Hang Seng down less than 0.1% to 23361

- Shanghai Composite closed

- S&P/ASX 200 up 0.7% to 5714

- US 10-yr yield up less than 1bp to 2.51%

- Dollar Index up 0.24% to 100.62

- WTI Crude futures down 0.7% to $53.41

- Brent Futures down 0.9% to $55.71

- Gold spot down 0.3% to $1,184

- Silver spot down 0.3% to $16.76

Top News

- U.S. Edges Toward Trade War as Trump Clash With Mexico Escalates

- Microsoft, Intel, Alphabet Results Buoyed by Cloud Boom

- PayPal Has Been Talking With Amazon on Payments, CEO Says

- Morgan Stanley to Reduce Wealth Fees Even With Rule Uncertainty

- Resignation Threatens to Bring Federal Pipeline Rulings to Halt

- Biggest U.S. Takeover in China in Decade Hangs on Board Spat

- Tesco Agrees to Buy Wholesaler Booker for About $4.6 Billion

- UBS Clients Pull Net $15 Billion in Quarter as Margins Decline

- Wynn’s New Macau Palace Helps Chinese Unit Beat Estimates

- Asahi Looks for China Beer Exit After Tsingtao Disappointment

- Toshiba Outlines Plans to Raise Capital Via Chip Stake Sale

- Hong Kong Yuan Deposits Post Record Monthly Drop in December

- U.S. Steel to Negotiate With Hesteel on Sale of Slovak Unit: HN

- Ford’s Farley Sees Up to $600m Impact From GBP Drop in ’17: Sky

- Lions Gate in Talks to Sell Epix Stake to MGM, Viacom: Reuters

- Digital Bridge Said to Buy Vantage Data Centers for >$1b: Reuters

- Trump, Merkel Expected to Talk by Phone Saturday: Reuters

In Europe, shares trade lower but only marginally (EuroStoxx 50 -0.6%). The main equity story of the day is Tesco’s (TSCO LN) GBP 3.7bIn merger with wholesaler Bookers (BOK LN). Elsewhere, the banking sector is the worst performing sector with UBS down after an earnings update this morning. Aside from stock specific stories, macro newsflow has remained light for the morning thus far. Bunds are trading sideways this morning stuck with a tight range between 161.35 to 161.80. Italian BTP’s initially showed some weakness again, wider 3bps vs Bund: 10yr yield 2.26%, spread 178bps this after further weakness seen yesterday after the Italian court ruling regarding voting laws. However, Italian paper over the course of the morning has been able to reverse the initial downside to pare the move with little in the way of new fundamental catalysts to sway price action in what has been an erratic morning thus far. Of note, after market we see rating agencies rate Spain, UK and Turkey.

Top European News

- Tesco Agrees to Buy Wholesaler Booker for About $4.6 Billion: CEO Lewis makes M&A debut, entering out-of-home food market

- U.S. Regulators Hang Tough at Basel as Trump Rollback Looms: U.S. will push hard for consensus on output floor, Petrou says

- Betting on Nordic Rain Pays Better Than Your Average Hedge Fund:Danish manager made 15 percent, 5 times commodity fund index

Asia equity markets traded mostly higher despite a mixed lead from Wall Street where earnings were in focus and the DJIA further extended above 20,000, although upside in the Asia-Pac region was reserved amid holiday-thinned trade. ASX 200 (+0.8%) outperformed as it played catch up on return from yesterday’s public holiday and took its first opportunity to react to the DJIA conquering the 20k level, while Nikkei 225 (+0.3%) was kept afloat by a weaker JPY. Hang Seng (+0.1%) slightly lagged on early profit taking and position-squaring heading into the Lunar New Year, with a lack of demand also attributed to various market closures as mainland China, South Korea and Taiwan remained shut for holiday. 10yr JGBs were higher with outperformance in the long-end after the BoJ announced its bond buying operations, in which it increased purchases of government debt with 5yr-10yr maturities to JPY 450b1n from a previous JPY 410bIn.

Top Asian News

- Jakarta Stocks Miss Gain as Governor Race Takes Islamic Turn: Indonesia is only SEAsian market to see stock outflows in 2017

- Little Room to Beat India Cash Ban Gloom With Budget Goodies: Overspending triggers risk of downgrade due to wide deficit

- Biggest U.S. Takeover in China in Decade Hangs on Board Spat: Majority board asks Air Products to proceed with due diligence

In currencies, the Bloomberg Dollar Spot Index rose 0.2 percent as of 8:17 a.m. in London, after jumping 0.6 percent Thursday. The measure is down 0.3 percent for the week, headed for a fifth straight weekly decline — the longest stretch since May 2015. It hit the highest in more than a decade in early January. The yen slid 0.5 percent to 115.13 per dollar after dropping 1.1 percent the previous session. The currency is down 0.4 percent for the week, its worst showing since Dec. 16. The pound fell 0.4 percent following a 0.3 percent decline Thursday, though it remains in line for a 1.4 percent weekly gain. The peso dropped 0.6 percent, extending Thursday’s 0.7 percent retreat. Mexico’s president scrapped his trip to Washington after Donald Trump doubled down on campaign pledges to rewrite the North American Free Trade Agreement and charge his southern neighbor to build a border wall.

The Turkish lira continued to touch new lows, falling 0.8 percent.

In commodities, West Texas Intermediate crude was little changed at $53.79 a barrel after surging 2 percent Thursday on optimism that OPEC and other producing nations would adhere to their pledged output cuts. The standout mover in commodities was Gold, which retreated 0.4 percent to $1,184.32 an ounce after dropping 1 percent Thursday. It is headed for a fourth straight loss, which would be the longest slump since October as the combined pressure from USD upside and risk on sentiment see the safe haven ‘metal’ offloaded. We still have room before we get to the Dec lows ahead of USD1120, but the pressure continues for now. USD based losses having limited impact on Copper, similarly Oil prices showing a small down in this respect also. A standout gainer is Nickel, which has been rising on strong demand out of China (see Copper also), whilst inventories have been falling.

Taking a look at some of the upcoming data today, in Europe we saw the December M3 money supply numbers (+5.0%, Exp. +4.9% YoY, vs. +4.8% previous) for the Euro area and the January consumer confidence indicator in France (100, vs 100 expected; 99 previous). In the US the advance Q4 GDP print (+2.2% QoQ annualized; +3.5% previous) will be closely watched alongside preliminary data on durable and capital goods orders in December, followed by the final University of Michigan sentiment reading for January (98.1 expected; 98.1 previous). So a fairly busy end to the week alongside the Trump/May meeting.

US Event Calendar

- 8:30am: GDP Annualized QoQ, 4Q A, est. 2.2% (prior 3.5%)

- 8:30am: Durable Goods Orders, Dec. P, est. 2.5% (prior -4.5%)

- Capital Goods Orders Nondef Ex-Air, Dec. P, est. 0.2% (prior 0.9%)

- 10am: U. of Mich. Sentiment, Jan. F, est. 98.1 (prior 98.1)

- 1pm: Baker Hughes rig count

DB’s Jim Reid concludes the overnight wrap

The state rooms at the White House will no doubt be prepared for UK PM Theresa May’s visit to see Donald Trump today. She will be the first leader to meet the President and a lot of attention will be placed on the outcome. Mrs May wants to try to pave the way for a free trade deal with the US post-Brexit and Mr Trump, in spite of his protectionist biases, would probably like to help the UK prosper if for no other reason than to help prove his point that the EU is flawed and the UK is better off outside of it. So although it’s a very early meeting where nothing will be decided it’ll be interesting to hear from the leaders afterwards. Mr Trump’s ability to be confrontational on the global stage was demonstrated yesterday as we saw US-Mexico trade relations continue to grow strained as Mexico’s President Enrique Pena Nieto officially cancelled a planned meeting with Mr Trump as the latter continued to signal intentions of building “the wall” and substantially increasing border security. He said that if the Mexicans had no intention of paying for the wall they should cancel next week’s trip. This is precisely what they’ve done. The Peso was down over 1% after the news and the Bovespa -1.4% yesterday. The story took a further twist later as after US markets closed White House Press Secretary Sean Spicer suggested that “When you look at the plan that’s taking shape now, using comprehensive tax reform as a means to tax imports from countries that we have a trade deficit from, like Mexico, if you tax that $50 billion at 20 percent of imports……… we can do $10 billion a year and easily pay for the wall just through that mechanism alone.” After only 4 days of Mr Trump’s presidency this is escalating pretty quickly. Despite volatility being very low now I can’t see this being a permanent feature of 2017 even if overall growth is eventually higher.

Over to markets and global equity bourses were largely mixed yesterday. Broader US equities ran out of steam with the S&P500 -0.07% on the day although the Dow edged up +0.16%. European equities maintained momentum with the Stoxx up +0.25% on the day, driven largely by the healthcare sector (+1.6%). At the other end of the risk spectrum, bonds generally sold off for most of the day although a late US rally led to UST 10yr falling 1bps (4-5bps off the highs) after German 10yr yields climbed +2bps earlier, while UK 10yr yields rose by +4 bps. Euro periphery bonds also sold off with 10yr Italian BTP yields rising by +12bps likely on the back of Wednesday’s court ruling which our own Marco Stringa thinks encourages fragile coalition governments going forward with little chance of serious structural reform. It also perhaps increases the chances of an early election. See yesterday’s EMR with a link to Marco’s piece for more on this.

On the commodity spectrum, crude rose by +1.9% and to around 3-week highs and actually fairly close to 18-month highs. In Asia the BoJ have been active again this morning buying 450bn of 5-10 year paper which has been seen as an attempt to prevent the 10 year climbing further. We hit 0.085% yesterday and many think that the BoJ zero yield target for 10 years has an upper bound of around 0.1%. The 10yr has rallied 1.4% today to 0.067% as we type. We think this area of the curve could face pressure as the year progresses if we’re right on global yields. Remember that the BoJ implemented their change of direction (yield and yield curve targeting) in September last year which was pretty much the lowest level for government bond yields at a global level in history. Elsewhere in Asia the Nikkei is +0.2% and the Hang Seng was slightly lower before the early close with Chinese markets off for Lunar New Year. Many other markets in Asia have closed early with China extending the closure next week.

Staying with Asia, it is worth highlighting that our Chinese economists have published the first edition of a new monthly publication entitled China Macro in Charts. This report aims to provide a comprehensive set of charts tracking, amongst other things, developments in economic activity, trade, inflation, financial markets and fiscal policy.

The data out of Europe yesterday was broadly positive. The GfK consumer confidence reading from Germany for February improved more than expected (10.2 vs. 10 expected; 9.9 previous). We also saw the advance Q4 GDP reading for the UK which beat expectations at +0.6% QoQ (vs. +0.5% expected; +0.6% Q3), although there were concerns about the unbalanced nature of the growth – services accounted for nearly the entire expansion while production and construction sectors dragged on growth.

We had a busy day over in the US where we saw a more mixed bag of data. First we saw the advance goods trade balance data for December where the deficit decreased (-$65.0b vs. -$65.3b expected; -$65.3 previous) while preliminary wholesale inventories unexpectedly grew at +1.0% mom in December (vs. +0.1% expected). The Chicago Fed National Activity Index reading for December was also unexpectedly positive (0.14 vs. -0.05 expected) while the conference board leading index came in line with expectations (+0.5%). Flash PMIs for January beat expectations with the services PMI ticking up to 55.1 (vs. 54.4 expected) and thus driving the flash composite up to 55.4 (vs. 54.1 previous). Labour market data was on the weaker side as initial jobless claims rose more than expected to 259k (vs. 247k expected; 237k previous), and new home sales for December disappointed at 536k (vs. 588k expected; 598k previous). The claims number may still have seasonal distortions in after a strong Xmas period.

Taking a look at some of the upcoming data today, in Europe we will see the December M3 money supply numbers (+4.9% YoY expected vs. +4.8% previous) for the Euro area and the January consumer confidence indicator in France (100 expected; vs. 99 previous). Over in the US the advance Q4 GDP print (+2.2% QoQ annualized; +3.5% previous) will be closely watched alongside preliminary data on durable and capital goods orders in December, followed by the final University of Michigan sentiment reading for January (98.1 expected; 98.1 previous). So a fairly busy end to the week alongside the Trump/May meeting

END

i)Late THURSDAY night/FRIDAY morning: Shanghai closed HOLIDAY/ /Hang Sang closed DOWN 13.39 OR 0.06%. The Nikkei closed UP 65.01 POINTS OR 0.34% /Australia’s all ordinaires CLOSED UP 0.69%/Chinese yuan (ONSHORE) closed DOWN at 6.8840/Oil ROSE to 53.37 dollars per barrel for WTI and 55.66 for Brent. Stocks in Europe ALL IN THE RED. Offshore yuan trades 6.8646 yuan to the dollar vs 6.8840 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS A BIT AS POBC ATTEMPTS TO STOP DOLLARS FROM LEAVING CHINA’S SHORES. HOWEVER BOTH CHINESE YUANS FALL WITH THE HIGHER DOLLAR

3a)THAILAND/SOUTH KOREA/:

END

b) REPORT ON JAPAN

The yen tumbles again to the 115 to one area as the Bank of Japan boosts bond buying again. This action was taken to stop the yield from rising further. However that action failed as yields rose to .84% from .7%

(courtesy zero hedge)

Yen Tumbles After BOJ Boosts Bond Buying

With the Trump reflation trade once again spooking global government bonds and sending rates higher around the world, overnight Japan’s 40-year JGB rose to 1% for the first time in 11 months as Treasuries led a global debt sell-off amid rising inflation fears. Quoted by Bloomberg overnight, Barclays’ rates strategist Naoya Oshikubo said that “the 40-year yield has further to go, but the speed of its rise has been very fast” and suggested that “the BOJ might take action if the yield rises further rapidly.”

On Wednesday, before the latest move, there was some speculation that the BOJ might increase the amount of bonds it buys for super-long zones as yields climbed, but the BOJ bought just the regular amount, which suggested to traders that the BOJ is willing to tolerate the rise, putting pressure on the USDJPY.

Heading into today’s session, the BOJ was expected to announce its last regular market operation for this month. According to Katsutoshi Inadome, a senior bond strategist at Mitsubishi UFJ Morgan Stanley Securities, while the BOJ was expected to offer to buy 420bn yen in 1-to-3 year category, 400bn yen in 3-to-5 year category, and 410bn yen in 5-to-10 year zone, he cautioned that if the BOJ does not expand its purchases on the long end, it would disappoint the market, leading to a jump in the yen and bond selling: “If BOJ does what would be in line with the schedule as above, it is likely to spark bond selling on disappointment.”

He added that “super-long yields have risen to levels the markets saw as the upper end of the range for the BOJ’s yield curve control so if there is no action to stem these rises, it would raise doubts about its stance.”

Moments ago, the BOJ decided to avoid any “doubts about its stance” and when it announced the quantities for today’s POMO operations, it did not disappoint because whereas it previously bought “only” 410bn yen in the 5-10 year zone, today it increased the amount by 10%, to 450bn, effectively increasing the amount of debt the central bank is monetizing on the long end of the belly.

And with the telegraphed explicit support by the BOJ, any further selling in bonds has for now been halted, while the USDJPY spiked, as expected, tagging 115, before modestly dipping now that instead of concerns about tapering its QQE “with yield control” the BOJ has shown it is quite happy to keep the curve under control and from overshooting, despite Japanese December CPI printing stronger than expected across the board earlier in the session.

That said, even today’s “intervention” did not appease everyone, and as SMBC Nikko Securities in Tokyo wrote, the BOJ operation rose uncertainty about the BOJ’s February plan as the central bank’s operations this week suggest it is seeking to flatten the 2s10s curve which had been steepening. SMBC’s Souichi Takeyama added that “it raises uncertainty to what the buying plan will be for February” noting that “raising the amount of longer- dated bonds it buys at this time will strengthen expectations for further changes, such as making 450 billion yen the amount for the 5-to-10 year zone.”

One can sympathize: what until recently was supposed to be an intervention to gradually steepen the JGB yield curve has now become an attempt to flatten it. Our condolences to Kuroda, who lately no matter what he does, he always gets the undesired outcome.

“We Need To Prepare Umbrellas For A Rainy Day”: Japan Gears Up For Trade War

While so far Trump’s trade focus was fallen mostly on Nafta countries, and to a lesser extent China, one country that is taking precautionary steps is the one which recently suffered a major loss when Trump signed an executive order to exit the TPP, effectively killing the trade deal: Japan. The TPP, which took years to negotiate among 12 countries, has often been described as being, at its core, a deal between the United States and Japan, the world’s largest and third-largest economies respectively. Abe has touted TPP as an engine of economic reform and a counterweight to a rising China but said on Thursday it was possible Tokyo and Washington could hold bilateral free trade talks

According to Reuters, Japan is “preparing for all possible contingencies regarding trade talks with the United States“, the top government spokesman said on Friday, after U.S. President Donald Trump ditched the Trans-Pacific Partnership free trade deal this week. PM Shinzo Abe is preparing for a visit Washington next month, and in a sequel of what Trump is expected to unveil with Theresa May today, an official in Trump’s administration said Trump would seek quick progress toward a bilateral trade agreement with Japan in place of the broader Asia-Pacific deal.

“It is true that we are preparing to be able to respond to any possible situation,” Chief Cabinet Secretary Yoshihide Suga told a news conference. He refrained from commenting on U.S. trade policy until it becomes clear.

Trying to keep the tone cordial and not to attract too much attention to Japan’s mounting concerns it will be called out next, he added that “the alliance and the economy between Japan and the U.S. is very important, so we would like to have talks with various levels with the U.S. (about) how we can develop.”

Meanwhile, Japanese officials said Abe’s government should still try to convince Trump of the benefits of the TPP and multilateral free trade deals, while adding that they were not ruling out bilateral trade talks with the United States.

“We still stick to our best scenario (in pursuit of TPP), but that does not mean that we’re inflexible,” Masahiko Shibayama, an adviser to Abe, told Reuters.

“We need to prepare umbrellas for a rainy day. It’s too early to decide what kind to umbrellas to bring, though.”

Abe has touted TPP as an engine of economic reform and a counterweight to a rising China but said on Thursday it was possible Tokyo and Washington could hold bilateral free trade talks.

“Japan will continue to stress to the U.S. the importance of the TPP but it is not totally unfeasible for talks on EPA (Economic Partnership Agreement) and FTA (Free Trade Agreement)” with the United States, Abe told parliament after being asked about trade talks between the two nations.

Trump, who signed an executive order declaring he would seek to pull the US out of multilateral agreements, reiterated on Thursday he would strike numerous bilateral deals, as opposed to multilateral accords, such as the TPP. He has also taken aim at Toyota auto production in Mexico, warning it, too, would face tariffs if it pursued growth in Mexico instead of US for plants that build cars meant for the US.

And the punchline: Japanese officials were cautious about any Free Trade Agreement (FTA) between Japan and the United States, as it could encourage Trump to step up pressure on Tokyo while providing few benefits for Japan’s economy, they said. Trump has threatened a “border tax” on imports into the United States and has said Japan has “unfair” barriers to foreign auto imports. Japanese officials pointed out that there are no tariffs on foreign car imports into Japan and maintain there are no discriminatory non-tariff barriers, either.

“We’ll calmly explain the fact that Japanese carmakers are investing in America and create a lot of jobs there,” Shibayama said.

Of course, using “calmly” to preface any discussion with Trump is rather futile, and only invites the opposite response, especially on twitter.

Furthermore, Japan suggested that while it sought concessions from the US, it would preserve some trade protectsions of its own: Japan’s Kyodo news agency said Abe also suggested Japan would advocate retaining some form of tariffs on rice and four other key agricultural products in any trade negotiations with the United States.

“We will thoroughly protect what we should protect…I want to carry out bilateral negotiations properly, based on the thinking that agriculture is the foundation of this country,” it quoted him as saying.

Suga also said Japan would continue to monitor closely how the relationship between the United States and Mexico affects Japanese companies. On Thursday, the White House floated the idea of imposing a 20 percent tax on goods from Mexico to pay for a wall at the southern U.S. border, sending the peso plummeting and deepening the crisis between the two neighbors.

Japanese manufacturers, including major automakers, operate numerous factories in Mexico.

As a reminder, the last time the US and Japan were engaged in a vicious trade war, the final outcome were two infamous mushroom clouds.

end

c) REPORT ON CHINA

With new capital controls in China which commenced on Jan 1 2017, we now see property bubbles blowing up in Sydney, England and Vancouver. Buyers are already walking away from their down deposits:

(courtesy zerohedge)

Chinese Capital Controls Threaten Property Bubbles All Over The Globe As Buyers Lose Access To Cash

For months/years we’ve covered the many real estate bubbles that have been inflating all over the world courtesy of Chinese billionaires looking to launder money offshore (here are just a couple of examples: Vancouver, Sydney and New York). But a new set of capital controls enacted in China on January 1st, and aimed specifically at curbing foreign real estate investments, may just be the needle that finally pops all those bubbles.

As Bloomberg pointed out earlier this month, the following new restrictions on foreign currency transaction were implemented earlier this year.

- Customers must pledge money won’t be used for overseas purchases of property, securities, life insurance or investment-type insurance. While such rules aren’t new, citizens previously didn’t have to sign such a pledge

- Customers must give a more detailed account of the planned use of funds, such as business travel, overseas study, family visits, medical treatment, merchandise trade or purchases of non-investment insurance policies, including the timing, by year and month

- Violators of foreign-exchange rules will be be added to the currency regulator’s watch list, denied foreign-exchange quota for three years and subjected to anti-money-laundering investigations

- Customers must confirm compliance with restrictions on money laundering, tax evasion and underground bank dealings

- Customers must now confirm they aren’t lending or borrowing quotas to or from other citizens

And while some of the new capital controls above may not seem that onerous, they’re already threatening real estate deals from London to Melbourne as Chinese buyers are finding it increasingly difficult to fund down payments.

In London, Chinese citizens who clamored to purchase flats at the city’s tallest apartment tower three months ago are now struggling to transfer their down payments. In Silicon Valley, Keller Williams Realty says inquiries from China have slumped since the start of the year. And in Sydney, developers are facing “big problems” as Chinese buyers pull back, according to consultancy firm Basis Point.

“Everything changed’’ as it became more difficult to send money offshore, said Coco Tan, a broker at Keller Williams in Cupertino, California.

Less than a month after China announced fresh curbs on overseas payments, anecdotal reports from realtors, homeowners and developers suggest the restrictions are already weighing on the world’s biggest real estate buying spree. While no one expects Chinese demand to disappear anytime soon, the clampdown is deterring first-time buyers who lack offshore assets and the expertise to skirt tighter capital controls.

“If it’s too difficult, I’m out,’’ said Mr. Zheng, 66, a retired civil servant in Shanghai who declined to give his first name to avoid attracting regulatory scrutiny. He may abandon a 2.4 million yuan ($348,903) home purchase in western Melbourne, even after shelling out a 300,000 yuan deposit last August. He’s due to make another big payment next month.

As further evidence that the tighter controls are working, Chinese banks last month registered net inflows under the capital account for the first time since the yuan’s devaluation in August 2015.

Moreover, as Bloomberg points out, several new construction luxury buildings are now at risk of losing contracted sales as Chinese buyers, once flush with cash, are finding it very difficult to make progress payments.

At The Spire in London, a 67-story tower with sweeping views of the River Thames and flats starting at 595,000 pounds ($751,901), prospective buyers were caught off guard by the new rules. Less than 70 percent of clients who signed purchase contracts last year have made their initial payments, with the rest now facing “problems,’’ a press official at Greenland Holdings Corp., the project’s Shanghai-based developer, said on Jan. 12. The official asked not to be named, citing company policy.

While Beijing’s policy tweak may appear symbolic on the surface, it’s likely to cause a “notable reduction” in Chinese purchases of Australian property, according to Christopher Todd ‘CT’ Johnson at Basis Point, a consulting firm that specializes in business relations between the two nations. Australia approved A$24 billion ($18.1 billion) of real estate investments from China in the fiscal year ended June 2015, the most recent figures available, making the country by far the biggest source of foreign buyers.

And with one bubble on the verge of popping, the only question to answer now is which asset class speculative Chinese billionaires will cause to bubble over next?

end

4 EUROPEAN AFFAIRS

My goodness: The German editor of newspaper Die Zeit, Joffe, when asked how to end the “Trump Catastrophe” his answer was “assassination”

(courtesy zero hedge)

German Newspaper Editor: Assassination Easiest Way To End “Trump Catastrophe”

Josef Joffe, the editor-publisher of German weekly Die Zeit, suggests the easiest way to end the “Trump catastrophe” is to murder the president in the White House.

As The Daily Caller’s Jacob Bojesson reports Joffe joined panel show ARD-Presseclub to answer questions from the public. A viewer called in to ask if it was possible to impeach President Donald Trump and end the “catastrophe.”

“There has to be a qualified two-thirds majority of the Senate in order for a removal of office to take place,” a female panelist responded.

“These are politically and legally pretty high hurdles, a lot would have to happen for it, we’re far away from that.”

Joffe then jumped in with a calm response.

“Murder in the White House, for example,” he said.

Joffe recently authored an op-ed in The Guardian where he argues Trump will do “untold damage to Europe.”

The president elect praises Brexit, cosies up to Putin and promises to take an axe to Nato and established trading systems. Prepare for a remake of the 1930s…

Won’t reality bite? Yes, it will. But the 20th century whispers that it may not bite in time, as the depression and the rise of the Pied Pipers of authoritarianism suggest. In the next four years, Trump can do impressive damage. The upside today is that the demagogues of the 1930s did not have to stand for re-election.

One wonders if Joffe and Madonna should get together (in a cell)

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

RUSSIA/USA

Putin and Trump will talk by phone tomorrow in their first step for normalization of relations.

(courtesy zero hedge)

Putin, Trump To Talk By Phone On Saturday: “Getting Along With Russia Is A Great Thing”

Presidents Vladimir Putin and Donald Trump will have their first official discussions since the inauguration in a phone call planned for Saturday, the Kremlin said, a first step towards what Trump has billed as a normalization of relations after three years of tensions marked by open hostility during the Obama regime.

The two leaders are scheduled to exchange views on Russia-U.S. relations while Putin will congratulate Trump on his Jan. 20 inauguration, presidential spokesman Dmitry Peskov told reporters on a conference call Friday cited by Bloomberg. Trump and Putin last spoke in November, when Putin rang Trump to congratulate him on winning the presidential election. Asked by reporters if Ukraine would come up, Peskov said: “This is the first telephone contact since President Trump took office, so one should hardly expect that this phone call will involve substantive discussions across the whole range of issues. We’ll see, let’s be patient.”

Trump has said in the past that, as part of the rapprochement he is seeking with Russia, he is prepared to review the sanctions that Washington imposed on Russia over its 2014 annexation of Ukraine’s Crimea Peninsula. Such a move is likely to face resistance from both domestic and foreign politicians, who argue sanctions should only be eased if Moscow complies with the West’s conditions on Ukraine. Peskov said he had no information on reports that Trump is considering lifting U.S. sanctions on Russia imposed over the 2014 annexation of Crimea and the conflict in eastern Ukraine.

If Putin and Trump can establish a rapport, it could pave the way for deals on Ukraine and Syria, two sources of friction during the administration of Barack Obama according to Reuters.

Trump and Putin have never met and it was unclear how their very different personalities would gel. Trump is a flamboyant real estate deal-maker who often acts on gut instinct, while Putin is a former Soviet spy who calculates each step methodically.

Trump has repeatedly spoken about ending the enmity that has dragged U.S.-Russia relations to their lowest ebb since the Cold War. In an interview with Sean Hannity on Fox News on Thursday night, Trump said it would be to the advantage of both Russia and the US to mend ties and pool their efforts in the fight against terrorism. “I don’t know Putin, but if we can get along with Russia that’s a great thing, it’s good for Russia, it’s good for us, we go out together and knock the hell out of ISIS, because that’s a real sickness,” he said.

“Wouldn’t it be nice if we actually got along with people? Wouldn’t it be nice if we actually got along, as an example, with Russia? I am all for it,” Trump told a news conference in July last year.