Gold: $1233.60 UP $3.80

Silver: $17.40 UP 2 cents

Closing access prices:

Gold $1234.80

silver: $17.45

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: 1247.78 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1233.50

PREMIUM FIRST FIX: $14.28

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: 1241.60

NY GOLD PRICE AT THE EXACT SAME TIME: 1233.85

Premium of Shanghai 2nd fix/NY:$7.75

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est 1233.00

NY PRICING AT THE EXACT SAME TIME: 1233.00

LONDON SECOND GOLD FIX 10 AM: 1232.40

NY PRICING AT THE EXACT SAME TIME. 1232.40

For comex gold:

MARCH/

NOTICES FILINGS TODAY FOR MARCH CONTRACT MONTH: 13 NOTICE(S) FOR 1300 OZ. TOTAL NOTICES SO FAR: 72 FOR 7200 OZ (0.2239 TONNES)

For silver:

For silver: MARCH

0 NOTICES FILED TODAY FOR NIL OZ/

Total number of notices filed so far this month: 3296 for 16,480,000 oz

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY 467 contracts DOWN to 186,523 despite the RISE IN PRICE ( 9 CENTS) WITH RESPECT TO FRIDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 0.931 BILLION TO BE EXACT or 133% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH: THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the total comex gold also ROSE BY 3,573 contracts WITH THE RISE IN THE PRICE OF GOLD ($3.30 with FRIDAY’S TRADING). The total gold OI stands at 431,292 contracts.

we had 13 notice(s) filed upon for 1300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a huge change in tonnes of gold at the GLD: a withdrawal of 6.81 tonnes

no doubt that this gold is heading to Shanghai.

Inventory rests tonight: 830.25 tonnes

.

SLV

We had a big changes in inventory at the SLV/ a big inventory deposit of 1.232 million oz

THE SLV Inventory rests at: 332.504 million oz

CONTRAST THE GLD INVENTORY LOSS WITH THE SLV SILVER INVENTORY GAIN!!

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 467 contracts DOWN TO to 186,523 DESPITE THE FACT THAT SILVER WAS UP 9 CENT(S) with FRIDAY’S trading. The gold open interest ROSE BY 3,573 contracts UP to 429,290 WITH THE RISE IN THE PRICE OF GOLD OF $3.30 (FRIDAY’S TRADING).

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 13.36 POINTS OR .41%/ /Hang Sang CLOSED UP 192.06 POINTS OR 0.79% . The Nikkei closed FOR HOLIDAY /Australia’s all ordinaires CLOSED DOWN 0.35%/Chinese yuan (ONSHORE) closed DOWN at 6.9072/Oil FELL to 48.16 dollars per barrel for WTI and 51.30 for Brent. Stocks in Europe ALL IN THE RED ..Offshore yuan trades 6.8957 yuan to the dollar vs 6.9072 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AGAIN/ ONSHORE YUAN WEAKER AS IS THE OFFSHORE YUAN WHICH IS ALSO WEAKER AND THIS IS COUPLED WITH THE SLIGHTLY WEAKER DOLLAR. CHINA TIGHTENS

3a)THAILAND/SOUTH KOREA/NORTH KOREA

North Korea is now one step closer to an ICBM after a successful test of a “new type” of rocket engine. The USA. South Korea and China have a problem that they must deal with:

( zero hedge)

b) REPORT ON JAPAN

Shinzo Abe seems to be embroiled in a school scandal as the government sells land at 1/7 the official going rate and Abe lies about a donation receipt to that school

( zero hedge)

c) REPORT ON CHINA

i)China prepares for the worst as they will counter all USA trade penalties.

( zero hedge)

ii)China now expands its non existent marine force by over 400%

( Daniel Lang/SHFTPlan.com

4. EUROPEAN AFFAIRS

i)USA is now pressuring the IMF to walk away from Greece. If they do, then Greece will default in July and much of the derivative mess with its accompanying debt crisis will be upon Europe and the ECB

( Mish Shedlock)

ii)GERMANY/DEUTSCHE BANK

Wow!! that is a huge discount in the new rights offering of Deutsche bank. It closed on Friday with the stock trading at 17.86 euros. The existing shareholders have a right to buy the stock at 11.65 euros for a discount of 35%. The dilution will be a huge 688 million shares.

( zero hedge)

iib The market reacts to two big news items:

- a massive dilution of their stock with the above rights offering

- another huge revenue warning

( zerohedge)

iii)EU/EUBANKS

My goodness: a new plan.!! An EU bad bank which will buy up much of the 1 trillion in bad loans. And the party who will end up holding the bag: the taxpayer

( Don Quijones/WolfStreet)

iv)HOLLAND/EUROPE/ POPULISM VS GLOBALISM

The Dutch election did not change the tide; citizens are still anti migrant and are titlting more to far fight populsim than globalism

(courtesy Gorka/StrategicCulture Foundation)

v)Theresa May now will officially trigger Article 50 on March 29. The long arduous process begins

( zero hedge)

vi)The bad news is already out: so why did the Article 50 headlines this morning cause CABLE (Pound/USA) to fall:

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia

They are dropping like flies! Another senior Russian official has died of stab wounds while he faces embezzlement charges/ He was being held in prison awaiting trial…probably nothing…

( zero hedge)

Israel threatens Syria that it will destroy it’s air defense systems if it continues to engage in military action. Israel fires on a convoy bringing weapons to Hezbolloh in Lebanon.

( zerohedge)

6.GLOBAL ISSUES

Friday night:

Disagreements with the USA and the rest of the G20 over the future of global trade. The USA wants protectionism and the others free trade. They cannot agree on wording.

(zerohedge)

7. OIL ISSUES

OPEC tries to jawbone oil higher but are having great difficulty

(courtesy zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

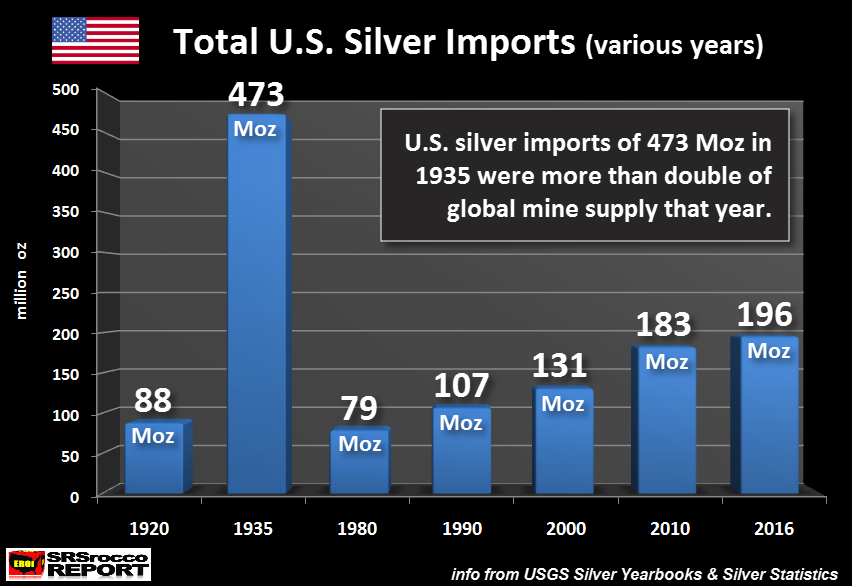

i)A terrific commentary from Steve St Angelo. He comments that China has always been a silver nation. However he reports that China supplied the USA in 1935 almost 1/2 billion oz of silver. After that year, the amounts supplied were less and they ended probably around 1939. As I have speculated and now Steve, that China did supply the USA once the “Manhattan project silver” had been used up.

( Steve St Angelo/SRSRocco report)

ii)Silver according to this Bloomberg author is going to climb faster than gold

( Bloomberg/Pakiam)

iii)Hedge funds were surprised at the slowness of the Feds to raise rates in the long term.e.g the “dots”

( Bloomberg/GATA)

iv)Bill Murphy is interviewed by Reluctant Preppers

( GATA)

v)Bill Murphy interviewed by Mark Leibovit of Wall Street Raw

( GATA)

vi) Craig Hemke is interviewed with his views on manipulation of the precious metals, the latest on the class action lawsuits and how the physical markets will overpower the paper markets

( Mike Gleeson/Gold-eagle.com.Craig Hemke)

vii) An excellent commentary from Lawrie Williams as he describes the fake data coming out of all governments e.g. the CPI etc.

(courtesy Lawrie Williams/Sharp’s Pixley)

10.USA STORIES

a)Market trading

(graph/zero hedge)

b)OH!OH! The markets are negatively to reports that Fed President Evans warns of rising uncertainty and that if Trump gets his fiscal stimulus they will need to raise rates faster. Not what the market wanted to hear:

( zero hedge)

i)A must read..David Stockman

Two major points here:

- If the uSA wants to raise rates so that the 1o yr bond rate rises to 3.0% by 2019 then a massive amount of excess bank reserves must be drained which will cause huge harm to the economy.’

- the debt ceiling crisis is upon as as both sides of the House and Senate will not agree on anything!

(courtesy David Stockman/Daily Reckoning)

ii)Saturday

Trump warns Germany that it owes vast sums of money to the USA because Germany has not committed to spending 2% of her GDP on defense. Trump is correct on his figures

( zerohedge)

iii)Sunday

Germany is angry at Trump’s claims that it owes vast sums to NATO and the USA. However it is true that Germany only spends 1.2% of her GDP on defense

( zerohedge)

iv)Saturday.

G20 results: Trump wins and the G20 drop the “anti protectionist, free trde and climate change funding committment

( zero hedge)

v)Trump is now beginning to roll back some of Obama’s protections for students who have been hit with agencies trying to collect on defaulted loans

( zero hedge)

The Intelligence Chair states on Sunday there is no collusion between Trump and Russia. However the Chair does state that the only crime is the leak of the transcript of private citizen Flynn talking to the Russian ambassador

( zero hedge)

vii)Used car prices continue to crash and generally when they do, we see a shift in purchases from brand new cars to the used car. This should hurt the USA car industry quite hard

( Mike Shedlock/Mishtalk)

Let us head over to the comex:

The total gold comex open interest ROSE BY 3,573 CONTRACTS UP to an OI level of 429,290 WITH THE RISE IN THE PRICE OF GOLD ( $3.30 with FRIDAY’S trading). WE PROBABLY HAD SOME MORE SHORT COVERING BY THE BANKERS. We are now in the contract month of MARCH and it is one of the poorer delivery months of the year. In this MARCH delivery month we had a LOSS of 6 contract(s) DOWN to 32. We had 0 contact(s) served ON FRIDAY, so we LOST 6 CONTRACT(S) or AN ADDITIONAL 600 ounces will stand for delivery. The next active contract month is April and here we saw it’s OI LOST 2966 contracts DOWN TO 179,914 contracts.

For comparison purposes, the April 2016 contract at this time had an OI of 237,867 contracts. At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month GAINED 45 contract(s) and thus its OI is 952 contracts. The next big active month is June and here the OI ROSE by 3,497 contracts up to 154,270.

We had 13 notice(s) filed upon today for 1300 oz

We are in the active delivery month is March and here the OI decreased by 67 contracts down to 553 contracts. We had 72 notices served upon yesterday so we GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND in this active delivery month of March.

For historical reference: on the first day notice for the March/2016 silver contract: 19,020,000 oz stood for delivery . However the final amount standing at the end of March 2016: 6,755,000 oz as the banker boys were busy convincing holders of many silver contracts to cash settle just like they did today.

The April/2017 contract month LOST 2 contract(s) to 1003 contracts. The next active contract month is May and here the open interest LOST 2122 contracts DOWN to 140,261 contracts.

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz as bankers needed much silver to fill major holes elsewhere.

We had 0 notice(s) filed for 360,000 oz for the MARCH 2017 contract.

VOLUMES: for the gold comex

Today the estimated volume was 81,383 contracts which is poor.

Yesterday’s confirmed volume was 185,20 contracts which is very fair

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | 1299.95 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

13 notice(s)

1300 oz

|

| No of oz to be served (notices) |

19 contracts

1900 oz

|

| Total monthly oz gold served (contracts) so far this month |

72 notices

7200 oz

0.1835 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 57,961.1 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 13 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

5088.128 oz

Delaware

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

553 contracts

(2,765,000 oz)

|

| Total monthly oz silver served (contracts) | 3296 contracts (16,480,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,592,256.0 oz |

end

And now the Gold inventory at the GLD

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

march 7/a huge withdrawal of 3.81 tonnes from the GLD inventory/inventory rests at 836.77 tonnes

March 6/No change in gold inventory at the GLD/Inventory rests at 840.58 tonnes

March 3/ a huge withdrawal of 2.96 tonnes of gold from the GLD/Inventory rests at 840.58 tonnes

March 2/a deposit of 2.37 tonnes of gold into the GLD/Inventory rests tat 843.54 tonnes

March 1/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 28/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 27/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

Feb 24/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 23/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 22/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 21/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

end

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

Major gold/silver trading/commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNEet.

The Best Ways to Invest in Gold Today

The Best Ways to Invest in Gold Today

– The cost of buying and selling gold

– How to buy gold on the cheap

– How to avoid paying capital gains tax (CGT) on your gold

– Open an account with one of the online bullion dealers – the likes of GoldMoney, GoldCore or Bullion Vault

– Gold Sovereigns and Gold Britannias make for a considerable saving on cost because of the CGT exemption

Gold Britannias and Sovereigns are free of Capital Gains Tax (CGT)

Gold Britannias and Sovereigns are free of Capital Gains Tax (CGT)

Dominic Frisby has looked at the best ways to invest in gold in the UK’s best selling financial publication Money Week.

Frisby looks at the various ways to invest in and own gold and points how gold ETFs are not much cheaper than online gold bullion dealers such as GoldMoney, GoldCore or Bullion Vault and yet there is the difficulty of taking delivery which is “cumbersome.”

The other important consideration when investing in gold is to consider the tax implications and the capital gains tax (CGT).

Buyers of gold ETFs and digital gold through e-gold providers like Bullion Vault and GoldMoney are subject to capital gains tax. However buyers of Gold Britannias and Gold Sovereigns are not subject to this expensive tax:

Competition between ETFs and bullion dealers has conspired to drive down prices, much to the benefit of the consumer. But there is one huge cost that neither of these methods is able to avoid – tax. This assumes you’re not buying your gold via an ISA or a SIPP, which it is, for the most part, possible to do via ETF or bullion dealer.

Capital gains tax (CGT) currently stands at 20% in the UK for higher rate taxpayers and 10% for lower. Funds don’t pay CGT. It is paid by the investor when they sell or redeem, assuming they made a profit. It kicks in once you have made profits of more than £11,100 in a year (£11,300 from next tax year).

So over and above that level, you’re facing an unavoidable 10% or 20% cost for buying and selling gold at a profit. It used to be 18% or 28%. We have George Osborne and his team to thank for lowering it – but even at current rates, it’s a considerable dent to profits.

There’s another method of buying gold (and silver), which, quite legally, avoids this cost altogether. There is a slightly higher premium to spot when you buy, there are slightly higher storage costs, and there is a slight discount to spot when you sell – but we are talking about a few per cent here, nothing like 20%.

Given the potential savings involved, it’s surprising that more UK investors don’t buy their gold and silver in this way. The method I’m describing, if you haven’t already figured it out, is to buy sovereigns and Britannias.

Frisby concludes the piece by pointing out how GoldCore offer capital gains tax (CGT) free gold sovereigns and gold britannias and how Frisby likes GoldCore:

“I like Goldcore. You can deal with them either over the phone or open an account online. You can buy sovereigns, Britannias, bars and probably even bells, and they’ll take care of the storage too.”

end

A terrific commentary from Steve St Angelo. He comments that China has always been a silver nation. However he reports that China supplied the USA in 1935 almost 1/2 billion oz of silver. After that year, the amounts supplied were less and they ended probably around 1939. As I have speculated and now Steve, that China did supply the USA once the “Manhattan project silver” had been used up.

(courtesy Steve St Angelo/SRSRocco report)

The Record Year The U.S. Imported Nearly A Half Billion Ounces Of Silver

by SRSROCCO , March 18, 2017

How many precious metals investors know the year the United States imported a record amount of silver? This figure is so great, there is no other single year in U.S. history that comes anywhere close to this amount. Even more impressive than that, it turns out to be more than double the global annual mine supply that year. It is such an unbelievable amount, its record has never been surpassed to this day.

Actually, I was quite surprised by the data when I was researching through some old official records. Even though the United States currently imports a lot of silver to supply its growing jewelry, industrial and investment demand, it pales in comparison to the nearly half a billion ounces imported this record year.

For example, U.S. silver imports are estimated to reach 6,100 metric tons (mt) in 2016, or 196 million oz (Moz), up from 191 Moz in 2015. Thus, 196 Moz of U.S. silver imports last year accounted for 22% of global mine supply which is estimated to be 887 Moz.

However, if we look at the following chart, we can plainly see, it doesn’t remotely compare to the massive 473 Moz of silver imported by the United States in 1935:

As we can see, total U.S. silver imports in 1935 stick out like a sore thumb. Even though U.S. silver imports trended higher from 1980 to 2016, there was this huge anomaly in 1935. So, what gives?

Well, due to the U.S. Silver Purchase Act of 1934, the U.S. Treasury went on a massive buying spree by jacking up the price of silver to $0.77 in 1935 from $0.44 in 1934. There is a lot that can be written about the U.S. 1934 Silver Purchase Act, but the motivation by the U.S. Government was to acquire more silver to back their outstanding currency base.

According to a paper written in 1936 titled, Effect Of The Silver Purchase Act Of 1934 On The United States, China, Mexico and India, it stated the following:

Source: Effect Of The Silver Purchase Act Of 1934 On The United States, China, Mexico and India

In order to increase the proportion of silver monetary stocks to gold, the U.S. had to get its hands on a lot of silver. In this paper, it stated that the U.S. Treasury would have to purchase 1,244,000,000 oz of silver to arrive at this 4:1 Gold-Silver monetary stock ratio.

So, where did the United States import this amazing 473 Moz of silver in one year?? Well, if you guessed China, you are correct. Of course, not all the silver came from China (India as well), but one hell of a lot did. This next bit of text from the same paper quoted above shows just how much silver China imported between 1918 and 1931:

Source: Effect Of The Silver Purchase Act Of 1934 On The United States, China, Mexico and India

During that time period (1918-1931), the Chinese imported one billion oz of silver, or 30% of total global mine supply during that time. After the signing of the U.S. Silver Purchase Act in June 19, 1934, Shanghai silver stocks plummeted:

Source: Effect Of The Silver Purchase Act Of 1934 On The United States, China, Mexico and India

Not all Chinese silver was heading to the United States, but a large percentage. Unfortunately, this paper did not list and Chinese silver stock figures for 1935, but I do have one from the U.S. Bureau of Mines Mineral Yearbook:

Source: U.S. Bureau of Mines 1937 Mineral Yearbook

In 1935, the United States imported a total of $354.5 million worth of silver. It is hard to tell exactly what was the average price the U.S. Treasury paid for all of its silver imports that year, but if we apply the $0.77 stated price, the $354.5 million worth of silver imports equals approximately 460 Moz… very close to the 473 Moz stated figure in the first chart published by the USGS silver statistics.

In order for the U.S. Treasury to build up its silver stocks, it pushed up the price it would pay for silver to acquire the metal from various countries throughout the world. Because of this large increase in the silver price by the U.S. Treasury, it forced the Chinese to go off their silver standard.

Again, there is a lot that could be written about this historic point in time, but that will be for another time. I just wanted to show just how much silver the U.S. imported in a single year. If we compare the same figures shown in the first chart above to global mine supply, this is the result:

Thus, U.S. silver imports of 473 Moz in 1935, were more than double the global mine supply of 221 Moz. Which means, the U.S. Treasury realized it would take a great deal of time to purchase the 1.24 billion oz of silver unless it motivated the rest of the world to let go of some of their silver. By pushing the price of silver from $0.44 in 1934 to $0.77 in 1935, the U.S. was able to import nearly 40% of their 1.24 billion oz target in just one year.

While the U.S. Silver Purchase Act of 1934 nationalized silver, the U.S. Treasury only purchased 109 Moz from American citizens during the 90-day time limit (source: 1939 Silver Money book). Which means, the majority of silver the U.S. Treasury needed came from foreign countries like China and India.

There has been articles written by several analysts (Charles Savoie for example) that state the U.S. Silver Purchase Act of 1934 was instrumental in removing the silver standard in several countries like China and Mexico. While this may be true, the United States was becoming the power-house of the world due to its massive oil discoveries. We must remember, the U.S. was the Saudi Arabia of the world during World War II.

Regardless, the 473 Moz of silver the U.S. imported in 1935 was the largest amount ever. Even though U.S. silver imports were quite high in 1936 at 222 Moz, they were less than half of the previous year.

Lastly, many precious metals investors believe the Chinese have a massive hoard of silver. Honestly, I do not belong to that mindset. While the Chinese did have a lot of silver at one time, they sold quite a lot of it during the 1930’s and also more in the 2000’s. Very few Central banks hold any silver. Most of the silver today is held in private hands or by large institutions… not Central Banks.

The advent of modern technology also forced the United States to remove silver from its coinage in 1965. However, times are rapidly a-changing. In the future, the value of silver will not be based on how much is consumed by industry, jewelry or investment demand, but rather how it functions as a HIGH QUALITY STORE of VALUE compared to most other assets that will be disintegrating as the massive amount of debt and derivatives implodes.

end

Craig Hemke is interviewed with his views on manipulation of the precious metals, the latest on the class action lawsuits and how the physical markets will overpower the paper markets

(courtesy Mike Gleeson/Gold-eagle.com.Craig Hemke

Craig Hemke Exclusive: Physical Metals Demand Plus Manipulation Suits Will Break Paper Market

Mike Gleason: It is my privilege now to welcome in Craig Hemke of the TF Metals Report. Craig runs one of the most highly respected and well known blogs in the industry and has been covering the precious metals for close to a decade now, and he puts out some of the best analysis on banking schemes, the flaws of Keynesian economics and evidence of manipulation in the gold and silver markets.

Craig, it’s great to have you back and thanks for joining us again today and how are you?

Craig Hemke: Mike, I’m fine thank you. It’s always a pleasure and I appreciate the invitation.

Mike Gleason: Well, I know time is short here so we’ll get right into it. First off, we’ve been seeing a decent little correction in the metals over the last few weeks although they’re rallying a bit here today and now that the Fed decision is out, as we’re talking on Wednesday afternoon. Gold and silver were probably due for a pullback after a very strong first eight or nine weeks of the year. So how do things look technically speaking here, Craig, after this recent pause and the uptrend? Do you think we’re still in the midst of a bull run and has this just been a healthy correction? How do you see things here?

Craig Hemke: Well, I guess the biggest picture possible we pulled back these couple last weeks, once it became obvious that the Fed was going to hike rates again, and we pulled back in a manner, very similar to what we saw in November of 2015 and November of 2016 before the previous two rate hikes, and now here we are in the hours immediately following the hike, we’re rallying. Now, the last two rate hikes that came in December of ’15 and December of ’16, gold bottomed the very next day and began to rally quite strongly. Now, here we apparently bottomed earlier today, and are rallying quite strongly this afternoon as Mother (Fed Chair Janet Yellen) is just slaughtering the dollar bowls with all of her press conference and everything else.

Well, I guess the biggest picture possible we pulled back these couple last weeks, once it became obvious that the Fed was going to hike rates again, and we pulled back in a manner, very similar to what we saw in November of 2015 and November of 2016 before the previous two rate hikes, and now here we are in the hours immediately following the hike, we’re rallying. Now, the last two rate hikes that came in December of ’15 and December of ’16, gold bottomed the very next day and began to rally quite strongly. Now, here we apparently bottomed earlier today, and are rallying quite strongly this afternoon as Mother (Fed Chair Janet Yellen) is just slaughtering the dollar bowls with all of her press conference and everything else.

From a technical standpoint, both gold and silver have recently seen a bullish cross of moving their 50-day moving averages up through their 100-day moving averages, so that’s pretty important. And if price can now get above that 50-day – and we’re making a run at it here on Wednesday – if we can get above there and close there on Friday, there’s going to be a lot of folks who will start getting very interested in the metals from a technical standpoint.

Mike Gleason: Craig, you regularly discuss just how manipulated and phony the gold and silver future markets are. You’ve been doing that for years, people called you out as a conspiracy theorist for it. For some reason, lots of folks couldn’t accept the notion that banks employ a combination of crooked traders and high frequency trading machines to dominate these exchanges. Now, in recent months however we’ve seen smoking gun evidence in the form of documents and recordings from Deutsche Bank where traders working at various banks colluded with one another to rig markets and cheat their own clients. WikiLeaks published a memo sent to the Treasury Department for the future exchanges were launched in the early ’70s.

Officials were clear regarding their intent for those exchanges. They sought to create enormous price volatility and to discourage physical ownership of the metal and they’ve succeeded. We can be pretty sure that the bought and paid for regulators will manage somehow to ignore the evidence and fail once again to hold any bank to account, but Deutsche Bank has agreed to pay roughly 100 million dollars in damages and other banks involved could be in even bigger trouble. So, my question is whether you have gotten any apologies from the people who labeled you as crazy for talking about manipulation? And then give us your thoughts on these revelations… can the civil courts help us get to more honest markets and is there any fixing this broken and rigged system, Craig?

Craig Hemke: Yeah I tell you, no I haven’t gotten any apologies, Mike. I guess we should start there and I’m not expecting any, but that doesn’t matter. Most of those folks that always claim that the gold and silver paper markets were free and fair were just simply trolls for the establishment. I remember one guy in particular was a particularly virulent troll and he admitted to be a former Deutsche Bank trader. Okay, well you can connect the dots there, right? Look, none of this is surprising and obviously it’s nice to know as we’ve always said, it’s conspiracy fact, historical fact, not some kind of whacked out conspiracy theory.

But nonetheless, it’s the market that we have to deal with for now, where this trading of these paper derivatives is somehow allowed to discover a physical price. I mean, it’s nonsense. It’s a fraud, it’s a sham, and until those paper markets break because they don’t have the physical to deliver into the demand, it’s pretty much what we’re stuck with. Where this all goes from here in terms of the manipulation is – we have to let the process play out. When this news first broke, heck, it’s almost a whole year ago, Mike. This was back in what? April or May last year when we learned that Deutsche Bank was being pressured by the German regulators to settle. A lot of folks thought that was going to change things overnight.

No, it’s not going to change things overnight but it is a huge change because in all of the history of class action lawsuits, alleging price manipulation and seeking damages, they’ve all been thrown out by the courts before we could ever get to the process of legal discovery. Well, not only are we moving forward on legal discovery for the first time, Mike, there are now going to be countless new lawsuits to join as information comes out. The emails and the text messages that you referenced came out through the discovery process. That’s going to bring even more lawsuits, and then additionally we’ve got a bank at one of the major players in the manipulation, Deutsche Bank, who has essentially turned state’s evidence, that is singing like a mafia songbird, a mafia informant, providing information.

So, people have to let this play out, these legal processes never move too quickly, but this is some serious blood in the water and if nothing else, if the physical demand doesn’t break the paper markets, I’m pretty confident that this whole legal process eventually will.

Mike Gleason: Speaking of manipulators, the FOMC just made their announcement, we had a bit of a respite as markets stopped obsessing quite so much about Fed policy for a few months following Trump’s election, but Janet Yellen and the FOMC are back in the news today. We may see some renewed focus on what to expect from our central planners going forward. Now, Trump and some of his surrogates have been critical of the strong dollar, but the Fed is hiking rates and pushing the dollar even higher, this despite the fact that the economic growth estimates keep being revised lower. Is there a conflict brewing between the president and the Fed? Are Janet Yellen and other bankers working to undermine Trump perhaps, by withdrawing stimulus and throwing a wrench into the equity and bond markets, or is this simply just to preserve what little credibility they have left by delivering some hikes instead of just jawboning? Give us your thoughts there, and do you have any guesses about where the Fed Funds rate might be say a year from now?

Craig Hemke: Well, it makes you wonder doesn’t it? The latest first quarter of this year guess that’s been put out by the Atlanta Fed… which is always about the most accurate in trying to predict where GDP is… the latest guess came out earlier today and it’s actually under 1%. It’s only 0.9%, if you want to call that growth. That gentleman that does that model actually had it 3.4% just six weeks ago, so you can see the trend here. After all of last year came in at just 1.6%, we’re going to begin this year at .9, and into that environment, Mother Fellen (Janet Yellen) has now hiked twice in 90 days and these three rate hikes are the first ones we’ve seen in almost 10 years. Doesn’t make any sense, and it kind of underlies what is really going on there. People think that the Federal Reserve is part of the federal government, and it’s not.

People think that the Federal Reserve is some altruistic, benevolent organization that’s trying to help the American people, it’s not. Their primary people is to help their banks. Hiking rates into a flat economy does nothing for the average American, but it does help the banks which is why they’re doing it. Going forward, Mother said today, and all of the FOMC said today that they think GDP for all of 2017 is going to be 3%. Well, here’s the problem with that, Mike. If we do come in at quarter one at just 1% and again, the latest guess is .9, that means the next three quarters of this year are going to have to average 3.7%, average 3.7%, just to get Mother’s 3% target. I mean, you think that’s going to happen, my friend? No.

I’ll give you one more problem that this is happening. We’ve always maintained that the Fed cannot raise rates because of what it would do to the American fiscal situation, the debt and the deficit. Well, Mother is raising the short end, but what isn’t happening and this is what we’ve always contended, is you can’t move the long end up because of what it’ll do to blow out the deficit and the debt. That’s exactly what we’re seeing, the yield curve is flattening. The spread between the 2-year note and the 10-year note is under 120 basis points. This is a terrible sign for the U.S. economy. So yeah, where is this going to go? Mother’s going to be cutting rates in 2018, if not by the end of this year, and not hiking them, simply because they are inducing recession that may have already begun.

So, this is going to be quite a wild ride as we go through this year, not the easy, predictable rising interest rates and stronger dollar that so many predicted just three months ago.

Mike Gleason: If we do get that about face and when it comes to interest rates, you’ve got to think that’s going to be very bullish for gold, and negative real interest rates, of course, would be a fantastic thing for the yellow metal, would you agree?

Craig Hemke: Always has been in the past, Mike. That’s always been something. More importantly, what I watch on a daily basis is the Dollar-Yen, which is the Forex pair trade of the value of the U.S. dollar in Yen or vice versa. That seems to be the key driver of the HFT trading machines that dominate the COMEX paper market. The Dollar-Yen clearly peaked out with a double top back in December and into early January, and has been a downtrend since. That’s what has helped to drive algo demand for paper gold so far this year. That thing rolls back over and heads back down to, oh, currently it’s around 113 and a half. If it heads back down to 100, which is where it was last July, then you’re going to see COMEX gold go back to near $1,400 where it was last July. They may not be able to contain it at that point.

Again, for me, I’ve been preaching to people on my site not to buy this what we call the “generally accepted narrative for 2017.” There’s so many people talking about how the bond bubble’s about to burst, the 35 year bond bubble’s finally going to burst, and it was supposedly a fait accompli. In fact, I saw a chart just last weekend that showed there was record net short position of hedge funds in the treasury market. Man, it never works. When everybody’s on the same side of the trade, it never goes that direction. Again, that’s what we’re seeing right now. The long end, the 10-year note and the 30-year long bond are actually lower in yield than they were 90 days ago, while the fed has jacked up the short end.

Again, that’s a flatting of the yield curve. Anybody that’s ever taken Econ 101 in college knows that a flat yield curve is a precursor of recession and I just have very little doubt at this point that that’s where we’re headed.

Mike Gleason: Again, that’s a flatting of the yield curve. Anybody that’s ever taken Econ 101 in college knows that a flat yield curve is a precursor of recession and I just have very little doubt at this point that that’s where we’re headed.

Craig Hemke: Well, most folks at TFMR are general, aggressive stackers of physical metal, whether it’s gold or silver. Buying on a regular basis and just simply adding to their stack in preparation for this great economic financial reset that’s eventually going to come, because the debt just can’t simply going parabolically higher without either having to be reset or debt jubilee or whatever. We all stack metal and take advantage of the lower prices when they come. A lot of folks are trading the miners as well for leverage, and so folks have been very concerned, I can tell you that, over the way the miners have performed in the last few weeks. But they’re up today, too, and they have very well have put in their own higher low on the chart, and so folks are excited about that.

Eventually, we’re really watching, we’re going to be paying very close attention to what Theresa May does over the next couple of weeks in England, regarding Brexit and moving it forward. And that French election coming up, I think it’s on May the 7th, is going to be a really big event. Even if it’s not France, if it’s Italy, if it’s Greece, there are major, major problems with the euro currency, that being the second largest, second most heavily used currency in the world. If you factor in that currency may very well be going the way of the dodo bird, and negative interest rates across the continent of Europe, that’s a double whammy, extremely positive fundamental for physical gold ownership. And it is that physical gold ownership that eventually breaks the paper system.

So, we’re keeping a real close eye on events in Europe in the, let’s just call it the months ahead, because again some of those things might actually hold the key to finally breaking the shackle hold that the paper derivatives market has on the physical price. Because that’s what we’re all waiting for, is the day that the paper market fails and it’s probably not going to happen tomorrow, but events sure seem to still be trending that direction.

Mike Gleason: Well, wonderful insights as usual, Craig. We always enjoy hearing from you and before we say goodbye for today, please tell people how they can learn more about the TF Metals Report and what it is they’ll find when they visit your site?

Craig Hemke: Well, they’re going to find a vibrant community of people that are… all here to help each other out. I provide content on a daily basis and there’s a subscription component there that’s I don’t know, about $3 a week I guess. It’s not very expensive. But there’s also free content, too, and the great value comes not just from my input but from the input of all the subscribers and the members who are constantly discussing the metals, the global economy, politics, everything else, finding links, providing information to everybody else. It’s like a recognition that we’re all in it together like I said, in a community trying to help each other out. If anybody’s listening to this and they think, “Hey, sounds like me,” stop by and join us, TFMetalsReport.com.

Mike Gleason: Outstanding stuff. Hope you have a great weekend and look forward to speaking with you again soon, Craig.

Craig Hemke: Mike, thanks so much. All the best.

Mike Gleason: Well that will do it for this week. Thanks again to Craig Hemke. The site isTFMetalsReport.com, definitely a fantastic source for all things precious metals and a whole lot more. We urge everyone to check that out and you’ll want to check it out regularly for some of the best commentary on the metals markets that you will find anywhere.

Silver according to this Bloomberg author is going to climb faster than gold

(courtesy Bloomberg/Pakiam)

Silver seen climbing faster than gold as Yellen wakens bulls

Submitted by cpowell on Fri, 2017-03-17 23:31. Section: Daily Dispatches

By Ranjeetha Pakiam

Bloomberg News

Thursday, March 16, 2017

Investors may be better off with silver rather than gold. The Federal Reserve’s pledge to stick to its dovish outlook on U.S. monetary policy has fueled a rally in precious metals and silver usually beats its more valuable peer in a rising market.

After the Fed raised interest rates by a quarter percentage point Wednesday, Chair Janet Yellen said the central bank was willing to tolerate inflation temporarily overshooting its 2 percent goal and intended to keep its policy accommodative for “some time.” UBS Group AG said the gradual pace of tightening means negative rates will deepen, the dollar weaken and gold rise.

“Silver is substantially undervalued compared to gold and has plenty of space to appreciate both in dollar terms and relative to gold,” Gregor Gregersen, founder of Singapore-based Silver Bullion Pte, said in a email. “Currently the move into silver is a trickle, but it might very well become a flood once the mood of the market at large shifts.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-03-16/silver-seen-advancing…

END

Hedge funds were surprised at the slowness of the Feds to raise rates in the long term.e.g the “dots”

(courtesy Bloomberg/GATA)

Yellen surprises hedge funds that cut gold wagers before rally

Submitted by cpowell on Mon, 2017-03-20 02:21. Section: Daily Dispatches

By Luzi-Ann Javier

Bloomberg News

Sunday, March 19, 2017

Janet Yellen’s soothing words on the pace of U.S. interest rate hikes were a day late for hedge funds losing faith in the metal.

Money managers cut their bullish bets on bullion by the most since 2015 in the week ended March 14. The next day, Federal Reserve Chair Yellen reiterated that monetary policy will remain accommodative for “some time,” easing market fears that there might be more than three rate hikes this year. Her words sparked the biggest gold rally since November.

Gold, which climbed through the first two months of the year, had foundered in March as the prospect of higher borrowing costs curbed the appeal of non-interest-bearing assets. Yellen’s remarks came as the Bank of Japan maintains its unprecedented monetary easing program and the Bank of England holds its benchmark rate at a record low, helping to keep yields on trillions of dollars worth of debt below zero. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-03-19/yellen-surprises-hedg…

END

Bill Murphy is interviewed by Reluctant Preppers

(courtesy GATA)

GATA Chairman Bill Murphy interviewed by Reluctant Preppers

Submitted by cpowell on Mon, 2017-03-20 03:30. Section: Daily Dispatches

10:30a ICT Monday, March 20, 2017

Dear Friend of GATA and Gold:

In an interview with Dunagun Kaiser of Reluctant Preppers, GATA Chairman Bill Murphy discusses what might become indicators of a breakdown in the suppression of gold and silver prices. Murphy says that with Goldman Sachs people renewing their control of the U.S. Treasury Department under President Trump, he doesn’t expect a change in U.S. policy, though he acknowledges that the president could change it. Murphy’s interview is a half-hour long and can be heard at You Tube here:

https://www.youtube.com/watch?v=pH9HxyQDkZU&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Bill Murphy interviewed by Mark Leibovit of Wall Street Raw

(courtesy GATA)

Mark Leibovit of ‘Wall Street Raw’ interviews GATA Chairman Murphy

Submitted by cpowell on Mon, 2017-03-20 04:22. Section: Daily Dispatches

11:21a ICT Monday, March 20, 2017

Dear Friend of GATA and Gold:

Mark Leibovit, editor of the VR Gold Letter (http://leibovitvrnewsletters.com/the-leibovit-newsletters-products/leibo…) and host of the “Wall Street Raw” internet radio program, just interviewed GATA Chairman Bill Murphy about the organization’s work to expose the manipulation of the gold market by governments and central banks. The interview is eight minutes long and begins at the 41:30 mark of the audio download available here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

An excellent commentary from Lawrie Williams as he describes the fake data coming out of all governments e.g. the CPI etc.

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: Lies, Damn Lies, Fake News, Fake Views and Gold

So much of the data we are fed by governments and quasi-governmental outfits like the US Fed are so massaged in favour of trying to maintain a positive sentiment among the great unwashed that they cannot be seen as comparable with supposedly the same stats from the the past. I am indebted once again to Grant Williams (no relation) who points some of these anomalies out in great detail in his latest Things than make you go hmm… newsletter entitled ‘Fake Views Part II’ bringing the oft-quoted “There are three kinds of lies: lies, damned lies, and statistics” into mind. Interestingly the quote is often attributed to Mark Twain but he himself is said to have attributed it to British Prime Minister Benjamin Disraeli who may have been ahead of his time in forecasting statistical manipulation as political spin!

To illustrate his point Grant draws heavily on data and charts provided by yet another member of the Williams clan, John Williams (again no relation to Grant or myself) who runs the fascinatingShadowStats website which calculates government data the way it used to be calculated before the current era of using statistics as political weaponry. This has distorted the figures used by US government entities, on which many, or most, of their economic decisions are justified, beyond recognition. Indeed a significant part of the problem is that those making these decisions no longer question government-provided economic data but automatically assume its accuracy.

Take the cost of living for example. If one goes by Fed figures CPI is growing at an annual rate of around 1.8-2% – a figure few consumers would recognise as applying to them! If one calculates the Cost of Living index the way it was calculated back in 1980, inflation is actually rising on that basis at the much more recognisable figure of nearer 9% per annum – see the Shadowstats chart below:

As John Williams, as quoted in the TTMYGH newsletter, points out: In the early-1990s, political Washington moved to change the nature of the CPI. The contention was that the CPI overstated inflation (it did not allow substitution of less-expensive hamburger for more-expensive steak for example). Both sides of the aisle and the financial media touted the benefits of a “more-accurate” CPI, one that would allow the substitution of goods and services.

The plan was to reduce cost of living adjustments for government payments to Social Security recipients, etc. The cuts in reported inflation were an effort to reduce the federal deficit without anyone in Congress having to do the politically impossible: to vote against Social Security.

The inflation-calculation changes had the further benefit to government fiscal conditions of pushing taxpayers artificially into higher tax brackets, thus increasing tax revenues. The changes afoot were publicized, albeit under the cover of academic theories. Few in the public paid any attention.

And so it goes with much of the other data on which the US Government bases its figures, although CPI (and perhaps the calculation of GDP) are the most obvious examples. And it is not just the US which massages its figures thus. Most developed world politicians/economies have done likewise. It’s a way of keeping the population in check by releasing government-calculated figures which appear to show everything is rosy and under control when a deeper analysis might show that we are actually sinking into the abyss.

These massaged figures – described by Grant Williams as ‘Fake Views’ – have to be of considerable importance to the gold investor who is told that gold benefits in times of negative interest rates and where the gold price can be knocked back by the prospect of interest rates rising by tiny amounts even though they may still remain at zero or are, in fact, marginally negative. But as the ShadowStats CPI figures show, real interest rates as experienced by the person in the street are not just marginally negative, they are in fact HUGELY negative and wealth is being eroded at an unprecedented rate. On this basis the gold price should be going through the roof, but unfortunately for the precious metals investor, the financial world at large is mesmerised by the official statistics and unless, and until, there is a realisation that the data is just not representative of reality, a lacklustre gold price will continue to result. I don’t know what one can do to change this reality of the belief in government data – shouting it from the rooftops in the hope that someone in authority will listen is almost certainly not enough. Those in authority have a vested interest in maintenance of the status quo.

There is also currently the Trump effect – he is seen as the second coming of Ronald Reagan – and equities markets have been booming. Trump rails against ‘Fake News’ as trying to damage his Presidential plans, but he is also himself a source of equally ‘Fake News’ in support of his policies and no doubt ‘Fake News’ on the strength of the US economy, and how well, and how fast he is proceeding to ‘Make America great again’ will continue to be broadcast by his spin doctors and press aides.

Grant Williams in his newsletter also questions the level of the VIX (uncertainty) index which is extremely low, yet perhaps should be riding high given the difficulties Trump appears to be having in getting his policies and appointees in place. He also appears to be having continuing problems with the judiciary over his immigration executive orders. This has to bring the fruition of some of his other forthcoming plans into doubt – notably the proposed changes to Obamacare – even with a Republican dominated Congress given that he appears to be having problems keeping some members of his adopted political party on side.

So what is the take-away from all this. We live in such a spin-dominated world where even ‘official’ statistics and data have to be suspect. These may be accurate as far as the calculation process is concerned but often one will find the goalposts have been made to make true comparisons with the past difficult to correlate. Ultimately one has to trust one’s own judgement and hope the truth will come out which will, in this case, be long term positive for gold and silver in particular but they may have a tough time finding their true value in the light of concerted efforts to hide it.

-END-

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER AT 6.9072( DEVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES CLOSER TO ONSHORE AT 6.8957/ Shanghai bourse UP 13.36 POINTS OR .41% / HANG SANG CLOSED UP 192.06POINTS OR 0.79%

2. Nikkei closed HOLIDAY /USA: YEN FALLS TO 112.85

3. Europe stocks opened ALL IN THE RED ( /USA dollar index RISES TO 100.40/Euro DOWN to 1.0742

3b Japan 10 year bond yield: REMAINS AT +.075%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.85/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 48.16 and Brent: 51.30

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.463%/Italian 10 yr bond yield UP to 2.390%

3j Greek 10 year bond yield RISES to : 7.44%

3k Gold at $1232.00/silver $17.41(8:15 am est) SILVER RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 30/100 in roubles/dollar) 57.48-

3m oil into the 48 dollar handle for WTI and 51 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT DEVALUATION SOUTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.85 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9972 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0726 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.463%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.506% early this morning. Thirty year rate at 3.122% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, US Futures Slide Spooked By G20 Protectionist Shift; Dollar Drops For 4th Day

Global markets start the week mixed with Asian stocks rising (Japan was closed for holiday), European stocks sliding, weighed down by declines in oil-and-gas shares and banks, and S&P500 futures also down. The dollar fell to a six-week low, falling four days in a row for the first time since early November as G20 leaders scrap a long-standing commitment to reject all forms of trade protectionism, suggesting the “weak Dollar” camp in Trump’s inner circle is winning.

Equities retreated in Europe, Australia and New Zealand, as did S&P 500 Index futures. Japan’s stock market was closed Monday for a holiday. Indexes rose in Hong Kong, Malaysia and Thailand. The Australian 10-year yield resumed a retreat after rising at the end of last week. The yen touched its strongest in three weeks, while the Korean won was the highest in five months. Oil fell for the ninth day in 11.

“European equity markets have started the week with a heavy risk-off sentiment after the G20 communiqué explicitly reflected U.S. intentions to establish trade protectionist measures,” Ipek Ozkardeskaya, senior market analyst at London Capital Group, told Reuters. “As the world’s number one economy is preparing to set significant barriers against the world, investors are increasingly worried,” she said.

MSCI’s broadest index of Asia-Pacific shares outside Japan rose almost 0.4 percent to hit its highest level in more than two years on Monday. As a result, MSCI’s global benchmark equity index was little changed.

On Friday, Wall Street was flat to negative, dragged lower by bank shares that fell along with Treasury yields. Futures on the S&P 500 Index were down 0.1 percent. The underlying gauge rose 0.2 percent last week. The Stoxx Europe 600 index fell 0.2 percent. The FTSE 100 and Dax index were also both down 0.2 percent. Australia’s S&P/ASX 200 Index and South Korea’s Kospi lost 0.4 percent. The Hang Seng Index advanced 0.8 percent, while the Shanghai Composite Index rose 0.4 percent. New Zealand’s S&P/NZX 50 Index slid 1.4 percent, the most since November, dragged lower by Fletcher Building Ltd., which identified more expected losses in its construction division.

For those readers who missed the weekend’s big news, the G20 omitted a pledge to resist all forms of protectionism in its communique from its meeting in Germany over the weekend. That shift followed hours of wrangling that kept officials in suspense on whether the G-20 would even mention trade, with occasional doubts that a communique might be produced at all.

Despite some modest weakness, global stocks are coming off their best week since January, even as the dollar has slumped 1.7% after the Federal Reserve raised interest rates on March 15 yet didn’t accelerate the timeline for future tightening. The dollar index of its value against a basket of six currencies fell to a six-week low of 100.02 on Monday. It fell 0.2 percent against the yen before recovering to trade flat on the day at 112.70 yen JPY=D4, while the euro rose 0.3 percent to $1.0770 EUR=. Citi became the latest major bank to abandon its headline forecast for a fall in the euro to below parity with the dollar, upping its prediction for the single currency over the next six to 12 months to $1.04 from $0.98 previously.

The dollar index of its value against a basket of six currencies fell to a six-week low of 100.02 on Monday. It fell 0.2 percent against the yen before recovering to trade flat on the day at 112.70 yen, while the euro rose 0.3 percent to $1.0770.

Volatility remains low across markets from equities to currencies and fixed-income as investors strive to assess how sustainable the nascent global economic recovery is. As the chart below shows, following the recent volley of central bnk announcements, FX volatility has tumbled.

The greenback extended its recent decline, with the Bloomberg Dollar Spot Index touching its lowest level since November, pressured by investors who kept the latest bearish trend intact. A Japanese holiday and the previously noted Group-of-20 meeting that left most business unfinished suppressed flows in the major currencies; dropping a reference from the G-20 statement to resist trade protectionism weighed on the dollar, with macro and leveraged accounts adding to shorts positions, according to a London-based trader. Volumes were near the lowest they have been in March, a Europe-based trader noted. The Bloomberg dollar index, the BBDXY dropped, as much as 0.3% to 1223.95, lowest since Nov. 11, before paring decline; investors may look for guidance by speeches by Fed’s Dudley and Yellen expected later this week before meaningfully adjusting their current positioning.

Currency markets will also be focused on a raft of speeches by Fed officials this week, including Chicago’s Charles Evans on Tuesday and Friday, Chair Janet Yellen on Thursday, Dallas’s Robert Kaplan and Minneapolis’s Neel Kashkari on Friday and New York’s William Dudley on Saturday. “Sentiment towards the dollar has deteriorated significantly,” Societe Generale FX analysts said in a note to clients on Monday.

In rates, the 10-year U.S. Treasury yield has fallen around 10 basis points below 2.50 percent since the Fed raised rates last week for only the third time in over a decade. The gap between two- and 10-year yields has shrunk, meaning the yield curve has flattened. This suggests investors are skeptical growth and inflation will be strong enough to warrant a sustained cycle of rate hikes, and has subsequently weighed on the dollar.

In commodities, oil prices continued their downward trend as OPEC supplies remained steady despite touted cuts and rising U.S. drilling contributed to concerns about a supply glut. U.S. crude dropped 1% to $48.29 a barrel. Global benchmark Brent fell 0.7% to $51.40. The weaker dollar boosted gold which rose 0.4 percent at $1,233 an ounce, after touching a two-week high earlier in the session.

Bulletin Headline summary from RanSquawk

- European equities trade modestly lower so far, with Deutsche Bank weighing on the financial sector has they begin their capital raising

- FX price action has been relatively muted amid light newsflow, while oil trades lower after lEA’s Birol highlighted an increase in US oil output

- Highlights include, Chicago Fed National Activity Index, Bundesbank Report and comments from Fed’s Evans and BoE’s Haldane.

Market Snapshot

- S&P 500 futures down 0.2% to 2,371.00

- MXAP up 0.2% to 148.64

- MXAPJ up 0.4% to 481.53

- Nikkei down 0.4% to 19,521.59

- Topix down 0.4% to 1,565.85

- Hang Seng Index up 0.8% to 24,501.99

- Shanghai Composite up 0.4% to 3,250.81

- Sensex down 0.5% to 29,516.48

- Australia S&P/ASX 200 down 0.4% to 5,778.91

- Kospi down 0.4% to 2,157.01

- STOXX Europe 600 down 0.1% to 377.86

- German 10Y yield rose 0.5 bps to 0.44%

- Euro up 0.3% to 1.0766 per US$

- Brent Futures down 0.4% to $51.58/bbl

- Italian 10Y yield fell 0.9 bps to 2.357%

- Spanish 10Y yield rose 0.5 bps to 1.886%

- Brent Futures down 0.4% to $51.58/bbl

- Gold spot up 0.4% to $1,233.53

- U.S. Dollar Index down 0.2% to 100.15

Top Overnight News via BBG

- German Chancellor Angela Merkel and Japanese Prime Minister Shinzo Abe called for a concerted effort to defend free trade, expanding the list of economic powers joining together to counter the U.S. shift toward protectionism

- Money managers cut bets on rising West Texas Intermediate crude by a record amount during the week ended March 14, while wagers on a further price drop doubled as oil remained below $50 a barrel

- Deutsche Bank to Raise $8.6 Billion After Pricing Share Sale

- Deutsche Bank Says Revenue to Stay ‘Broadly Flat’ This Year

- Cerberus-Backed Albertsons Said to Consider Merger With Sprouts

- Blackstone Venture Acquires $1.4 Billion of Hansteen Properties

- Hansteen Rises to Highest in 10 Years on Blackstone Asset Sale

- Alphapharm Begins Recall of Epipen Auto-Injector in Australia

- Ford’s Lincoln to Offer Its First Hybrid Model in China

- Arconic Reports Multi-Year Deal Supply With Toyota North America

- FDA Investigating Rate of Cardiac Events With Abbott’s BVS

- Cognizant Said to Likely Fire Over 6,000 Employees, ET Now Says

In Asian markets, stocks traded mixed amid a lack of key drivers and with Japanese trade closed for the Spring Equinox public holiday, while ASX 200 (-0.5%) was led lower by telecoms and profit-taking in gold related stocks. China was positive with Hang Seng (+0.7%) the outperformer after a firm liquidity injection of CNY 100bIn by the PBoC and as participants digested earnings releases, while Shanghai Comp. (+0.4%) lagged after Chinese property prices continued to surge with Bejing prices up over 20% Y/Y, which could essentially attract funds away from stocks. Elsewhere, US equity futures were pressured and broke below Friday’s lows, while Nikkei 225 remained shut due to the public holiday. Chinese Property Prices (Feb) Y/Y 11.8% (Prey. 12.2%). PBoC injected CNY 60bIn in 7-day reverse repos, CNY 20bIn in 14-day reverse repos and CNY 20bIn in 28-day reverse repos.

Top Asian News

- Risk Appetite Goes Missing as Asia Starts the Week: Markets Wrap

- Yellen’s Shadow Looms Large Over China Central Bank Policy

- Selling Dollars Is Becoming The New Trump Trade: Markets Live

- Meitu Erases 28% Surge as Shares Seen Volatile Before Earnings

- China Said to Temporarily Suspend Beef Imports From Brazil

- Hong Kong Stocks Extend Weekly Rally as Shenhua Jumps on Payout

- Credit Suisse Co-Head of Asia Cash Equities Lee Said to Leave

- Malaysia Should Improve ‘Fragmented’ Military, Honeywell Says

- Morgan Stanley Said to Lose Second Senior M&A Banker in Asia

European bourses have kicked off the week in tentative fashion with the calendar looking somewhat light. EU bourses are trading with minor losses amid slight weakness in the financial sector with Deutsche Bank commencing their EUR 8bIn capital raising plan, while UBS are set to go on trial in their tax case in France. Elsewhere, Vodafone initially saw telecoms as the only sector in the green after agreeing to merge their Indian unit with Idea Cellular, however with Co. shares paring the initial upside amid suggestions that the merger may struggle to pass through regulatory requirements. Price action in fixed income markets has been somewhat contained with Bunds only modestly lower, with slight underperformance observed in the belly of the curve. Ahead of the French TV debate in the presidential race, OATs had been underperforming for much of the morning with the German/French spread widening the most in 2 weeks.

Top European News

- Deutsche Bank Says DoJ Closed Criminal Inquiry in FX Matter

- Merkel, Abe Call for EU-Japan Deal to Stem Trade Barriers

- Visco Says ECB Could Shorten Break Between QE Exit And Rate Hike

- Atos Denies Worldline Preparing Ingenico Bid, Reuters Says

- Hugo Boss Drops After Report Frere’s GBL Isn’t Shareholder

- Ingenico Rises After La Lettre Report Worldline Preparing Bid

- Troim’s Borr Buys Transocean’s Jack-Up Fleet for $1.35 Billion

- Paris Climate Accord Could Make the World $19 Trillion Richer

- Vodafone, Idea Agree on Merger to Create India Mobile Leader

In currencies, the yen was little changed at 112.74 per dollar as of 8:26 a.m. in London after reaching its strongest since Feb. 28. The euro climbed 0.3 percent to $1.0769, while the Australian and New Zealand dollars rose 0.3 percent and 0.4 percent, respectively. The British pound gained 0.2 percent. The South Korean won jumped 1 percent to its highest since Oct. 20, leading gains in emerging Asian markets. The baht also reached its strongest level since October. The USD-index continues to weakn post the G20 meeting as finance leaders caved into pressure from the US and scrapped a commitment to reject all forms of trade protectionism. As such, the pullback in the greenback has supported its major counterparts, with GBP making a break above 1.2400. Additionally, from a UK stand point reports report have been circulating that PM May’s closest have been calling for a potential snap election on May 4th in order to take seats from the SNP and reduce the likelihood of a second Scottish referendum. Another thing to keep an eye out for will be the French Election TV debate scheduled at 1900GMT, consequently, price action in EUR could be somewhat tame throughout the day, as has been the case so far, with the notable data of the morning coming I the form of Eurozone labour cost index, which was in line with Exp. ECB’s Visco (Dove) said that deflation risk seems to have passed and that the ECB could shorten the time gap between exit from QE and first rate hike.

In commodities, another rise in oil rigs continues to put the pressure on crude prices as WTI looks to test USD 48 to the downside, while lEA’s Birol added to these concerns having noted that he expects a major boom in US oil output and shale gas volumes. Elsewhere, copper will be in focus after labour unions at Chile’s Escondida mine slams new offer from management. West Texas Intermediate crude slid 0.7 percent to $48.42 a barrel. It has dropped 10 percent this month, heading for the steepest one-month slide since July. Gold rose 0.3 percent to $1,232.97 an ounce, climbing for a fourth day. Base metals fell on the London Metal Exchange, with copper forwards down 0.2 percent and tin retreating 0.3 percent.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0.03, prior -0.05

* * *

DB’s Jim Reid concludes the overnight wrap

Markets look set to be a little less interesting than my bedroom arrangements this week with perhaps the highlights being lots of Fed speakers, the first televised French Presidential debate tonight and the flash global PMIs on Friday. The Fed speakers will likely reinforce the message from the FOMC but watch for signs of increased confidence in their outlook. The French debates might start to lead to some bigger moves in the polls which have been relatively steady of late. As for the PMIs, volatility has been very subdued in the face of high political uncertainty due to continued strong data, especially survey data so the flash PMIs are often the best real time update of the global economic pulse.

Over the weekend the G-20 meeting ended with the “resist all forms of protectionism” line dropped from the previous communiqué. The US were the stumbling block but it’s still early days in the new Trump administration so for now it seems that markets will wait and see before becoming too scared by the implications. Indeed the more significant meeting may be the G-20 meeting in Hamburg in July by which time some of that uncertainty around the new US administration may have started to clear up. Aside from that the rest of the weekend news has been fairly light. The general view of the meeting between President Trump and Chancellor Merkel was that it was inconclusive with the President also tweeting after that “Germany owes vast sums of money to NATO and the United States must be paid for the powerful, and very expensive, defence it provides to Germany”.

Over in markets there hasn’t been too much a reaction to the weekend headlines with bourses generally mixed in Asia, albeit with fairly modest moves. Indices in China are little changed while the Kospi (-0.52%) and ASX (-0.47%) are down. The Hang Seng (+0.53%) is up however and in doing so has passed the 24,000 level for the first time since 2015. Elsewhere, US equity index futures are down about -0.20% while in FX the USD is a smidgen weaker.

Staying in Asia, there was also some data released in China over with the weekend with the release of the February house prices data. For new homes excluding subsidized housing, prices were reported as rising in 56 out of the 70 major cities which compares to 45 cities in January. It’s worth noting that Beijing’s municipal government on Friday increased the down payment requirement on second homes by 10% in an attempt to cool prices. The maximum length of a mortgage was also cut to 25 years from 30 years.

The relatively quiet start this morning follows Friday’s session in which markets appeared to run out of steam following a packed week. That was certainly the case for equity markets where the S&P 500 closed with a modest -0.13% loss and so capping the weekly return at +0.24%. In Europe the Stoxx 600 did however end +0.16% despite Banks underperforming and so making the weekly return a solid +1.36%. Last week’s winner was EM however with the MSCI EM index rising every day last week, including a +0.25% gain on Friday, to finish +4.26% for the week and the strongest week since July last year.