Gold: $1246.10 UP $12.50

Silver: $17.55 UP 15 cents

Closing access prices:

Gold $1245.00

silver: $17.55

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: 1242.36 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1229.35

PREMIUM FIRST FIX: $13.01

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: 1245.73

NY GOLD PRICE AT THE EXACT SAME TIME: 1229.50

Premium of Shanghai 2nd fix/NY:$16.23

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est 1232.05

NY PRICING AT THE EXACT SAME TIME: 1231.25

LONDON SECOND GOLD FIX 10 AM: 1241.60

NY PRICING AT THE EXACT SAME TIME. 1241.60

For comex gold:

MARCH/

NOTICES FILINGS TODAY FOR MARCH CONTRACT MONTH: 0 NOTICE(S) FOR NIL OZ. TOTAL NOTICES SO FAR: 72 FOR 7200 OZ (0.2239 TONNES)

For silver:

For silver: MARCH

118 NOTICES FILED TODAY FOR 590,000 OZ/

Total number of notices filed so far this month: 3418 for 17,090,000 oz

Today caught the bankers totally offside as they were in the process of raiding gold and silver throughout the night. Unbeknownst to them there would be trouble in the USA House getting the Trumpcare bill passed. The estimated volume today was 313,000 contracts for the gold comex and you can probably add another 100,000 for the final as they add the previous access market for their final calculations which will be published tomorrow. I will be very interested to see the preliminary and final open interest for both gold and silver of which I will report to you

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY 546 contracts UP to 187,069 with the RISE IN PRICE ( 2 CENTS) WITH RESPECT TO YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 0.936 BILLION TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH: THEY FILED: 118 NOTICE(S) FOR 590,000 OZ OF SILVER

In gold, the total comex gold also ROSE BY 1096 contracts WITH THE RISE IN THE PRICE OF GOLD ($3.80 with YESTERDAY’S TRADING). The total gold OI stands at 430,386 contracts.

we had 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a huge change in tonnes of gold at the GLD: a deposit of 4.15 tonnes

Inventory rests tonight: 834.40 tonnes

.

SLV

We had no changes in inventory at the SLV/

THE SLV Inventory rests at: 332.504 million oz

CONTRAST THE GLD INVENTORY LOSS WITH THE SLV SILVER INVENTORY GAIN!!

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 546 contracts UP TO to 187,069 AS SILVER WAS UP 2 CENT(S) with YESTERDAY’S trading. The gold open interest ROSE BY 1,096 contracts UP to 430,386 WITH THE RISE IN THE PRICE OF GOLD OF $3.80 (YESTERDAY’S TRADING).

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 10.80 POINTS OR .33%/ /Hang Sang CLOSED UP 91.13 POINTS OR 0.37% . The Nikkei closed down 65.71 .34% /Australia’s all ordinaires CLOSED DOWN 0.03%/Chinese yuan (ONSHORE) closed DOWN at 6.8890/Oil rose to 49.32 dollars per barrel for WTI and 51.99 for Brent. Stocks in Europe ALL IN THE GREEN EXCEPT LONDON ..Offshore yuan trades 6.87743 yuan to the dollar vs 6.8890 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AGAIN/ ONSHORE YUAN STRONGER AS IS THE OFFSHORE YUAN AND THIS IS COUPLED WITH THE HUGELY WEAKER DOLLAR. CHINA SENDS HER DISPLEASURE SIGNAL TO WASHINGTON

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA

This must give you a very warm and fuzzy feeling: North Korea reveals a propaganda video of them blowing up a USA aircraft

( zerohedge)

ii)Ladies and gentlemen: Kim is a madman and must be taken out:

he threatens the USA with a “first strike” nuclear iCBM

( zero hedge)

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

This is interesting: the German Federal Auditor group is calling for an audit of the ECB as they need more supervision

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

7. OIL ISSUES

i)This is how OPEC lost the battle against the shale boys as our American friends learned how to lower their cost curve and break even points;

( zero hedge)

ii)Russia mentions production cut ( of which it does not mean) and up goes oil and then it fails

( zerohedge)

iii)API reports bigger and expected crude and a much bigger buildup at Cushing. However gasoline did have a drawdown. Oil initially rose and then plummeted on the news:

( zero hedge)

8. EMERGING MARKETS

Venezuela stops publishing money supply data. Who would have thought that they could do such a horrible act?

(courtesy zero hedge)

9. PHYSICAL MARKETS

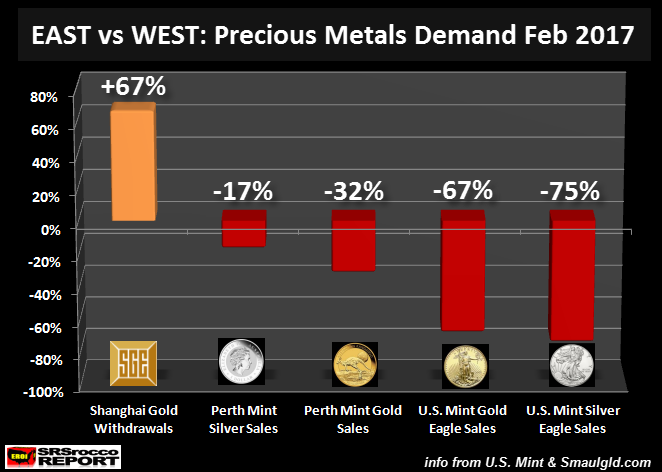

i)Although the West slowed their appetite for gold and silver, China and Russia did not. In Feb the withdrawals (equals demand) at the Shanghai Gold Exchange showed 179 tonnes. If we extrapolate that demand for the coming year we would obtain a demand equal to 2200 tonnes or greater. China is back in demand for gold in a big way:

( Steve St Angelo/SRSRocco report)

ii)As many of you know, I am not a fan of technical analysis especially with manipulation occurring continually on the paper gold and silver markets. However very long term charts are quite intriguing as it is does give meaningful direction for these markets;

( Kingworldnews/James Turk)

10.USA STORIES

i)Early trading

ii)Then this: bank shares plummet, gold rises bond yields rise (bond prices fall) as Trumpcare vote is now in doubt:

( zerohedge)

iii)Then: liquidity collapses! as stocks tumble!!

(zero hedge)

iv)The GOP unveils changes to the Health bill but it looks like it is not enough. A failure on Thursday will be devastating to the House. Even if it does pass, it will not pass the Senate

v)Trump issues a threat to Freedom Caucus member of the Republican House who still will vote no to the bill( zerohedge)

vi)Somehow the current account deficit beats by a huge 8 standard deviations and it shrinks to only 112 billion. This would be a positive to revisions to 4th quarter GDP

( zero hedge)

vii)And now the truth behind Trump’s skiiny budget and why everything will fail:

( David Stockman/Daily Reckoning/ContraCorner)

viii) Meet the 26 holdouts to the Trumpcare bill

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 1096 CONTRACTS UP to an OI level of 430,386 WITH THE RISE IN THE PRICE OF GOLD ( $3.80 with YESTERDAY’S trading). WE PROBABLY AGAIN HAD SOME MORE SHORT COVERING BY THE BANKERS. We are now in the contract month of MARCH and it is one of the poorer delivery months of the year. In this MARCH delivery month we had a LOSS of 15 contract(s) DOWN to 17. We had 13 contact(s) served ON FRIDAY, so we LOST 2 CONTRACT(S) or AN ADDITIONAL 200 ounces will NOT stand for delivery. The next active contract month is April and here we saw it’s OI LOST 7335 contracts DOWN TO 172,575 contracts.

For comparison purposes, the April 2016 contract at this time had an OI of 237,867 contracts. At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month GAINED 136 contract(s) and thus its OI is 1088 contracts. The next big active month is June and here the OI ROSE by 7,261 contracts up to 161,531.

We had 0 notice(s) filed upon today for NIL oz

We are in the active delivery month is March and here the OI decreased by 4 contracts down to 549 contracts. We had 0 notices served upon yesterday so we LOST 4 CONTRACTS OR AN ADDITIONAL 20,000 OZ WILL NOT STAND in this active delivery month of March.

For historical reference: on the first day notice for the March/2016 silver contract: 19,020,000 oz stood for delivery . However the final amount standing at the end of March 2016: 6,755,000 oz as the banker boys were busy convincing holders of many silver contracts to cash settle just like they did today.

The April/2017 contract month GAINED 6 contract(s) to 1009 contracts. The next active contract month is May and here the open interest GAINED 445 contracts UP to 140,706 contracts.

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz as bankers needed much silver to fill major holes elsewhere.

We had 118 notice(s) filed for 590,000 oz for the MARCH 2017 contract.

VOLUMES: for the gold comex

Today the estimated volume was 313,387 contracts which is very good.

Yesterday’s confirmed volume was 145,762 contracts which is very poor

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

32,976.96 oz

HSBC

|

| No of oz served (contracts) today |

0 notice(s)

NIL oz

|

| No of oz to be served (notices) |

17 contracts

1700 oz

|

| Total monthly oz gold served (contracts) so far this month |

72 notices

7200 oz

0.1835 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 57,961.1 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

181,774.05 oz

Brinks

Scotia

|

| Deposits to the Dealer Inventory |

531,570.75 oz

CNT

|

| Deposits to the Customer Inventory |

667,044.965 oz

CNT

JPM

|

| No of oz served today (contracts) |

118 CONTRACT(S)

(590,000 OZ)

|

| No of oz to be served (notices) |

431 contracts

(2,155,000 oz)

|

| Total monthly oz silver served (contracts) | 3418 contracts (17,090,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,744,030.1 oz |

end

And now the Gold inventory at the GLD

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

march 7/a huge withdrawal of 3.81 tonnes from the GLD inventory/inventory rests at 836.77 tonnes

March 6/No change in gold inventory at the GLD/Inventory rests at 840.58 tonnes

March 3/ a huge withdrawal of 2.96 tonnes of gold from the GLD/Inventory rests at 840.58 tonnes

March 2/a deposit of 2.37 tonnes of gold into the GLD/Inventory rests tat 843.54 tonnes

March 1/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 28/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 27/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

Feb 24/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 23/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 22/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 21/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

end

NPV for Sprott and Central Fund of Canada

will update later tonight the central fund of Canada figures

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNEet.

Silver 1/ 70th The Price of Gold” – Silver Eagles Sales Jump

By Mark O’Byrne March 21, 2017

– Silver just 1/70th the price of gold

– Silver at $17.50 per ounce set to rise “faster than gold”

– Silver Eagles (1 oz) buying jumps to 715,000 this week

– “Supply may drop following mine closures” – Standard Chartered

– Industrial demand “will remain strong” – CPM Group

– Silver is substantially undervalued versus gold

– Gold silver ratio to fall back below 30

Silver looks set to outperform gold again in the coming months due to falling mine supply and continuing robust global demand.

Source: Bloomberg

Source: Bloomberg

Silver at just $17.50 per ounce remains about 1/ 70th of the price of gold at $1,230/oz today. This gold silver ratio of 70.3 continues to drive silver ‘stackers,’ value investors and those seeking a better return than gold to accumulate silver at what are seen at these still relatively cheap levels.

This is seen in continuing robust demand for the very popular silver bullion coin this week. The U.S. Mint sold 715,000 of Silver Eagles ( 1 oz) this week, to bring the year to date sales totals for 2017 to a robust – 7,557,500 Silver Eagle coins.

|

US Mint Bullion Coin Sales (Number of coins) |

|||||

|

Monday Sales |

Last Week |

Feb Sales |

Mar Sales |

2017 Sales |

|

| Silver Eagles (1 oz) |

715,000 |

220,000 |

1,215,000 |

1,215,000 |

7,557,500 |

| Gold Eagles (1 oz) |

4,000 |

2,500 |

21,000 |

10,000 |

117,500 |

| Gold Buffalos (1 oz) |

1,500 |

2,500 |

15,000 |

4,500 |

51,500 |

Source: GoldCore via Coin News

We have seen very robust demand for silver again this year, especially from clients in the UK and Ireland buying silver bullion coins (now VAT free) such as Silver Eagles. We are seeing even greater demand for Silver Maples and Silver Philharmonics.

The increasingly favorable supply and demand fundamentals of the silver market were reported on by Bloomberg in an article entitled ‘Silver Seen Climbing Faster Than Gold as Yellen Wakens Bulls’.

According to Bloomberg:

Investors may be better off with silver rather than gold. The Federal Reserve’s pledge to stick to its dovish outlook on U.S. monetary policy has fueled a rally in precious metals and silver usually beats its more valuable peer in a rising market.

After the Fed raised interest rates by a quarter percentage point Wednesday, Chair Janet Yellen said the central bank was willing to tolerate inflation temporarily overshooting its 2 percent goal and intended to keep its policy accommodative for “some time.” UBS Group AG said the gradual pace of tightening means negative rates will deepen, the dollar weaken and gold rise.

The gold-to-silver ratio rose to 71 on March 14, the most in two months, and above an average of 62 in the past decade and a low of 32 in 2011, showing there’s potential for silver to appreciate versus its peer. Spot silver added 0.9 percent to $17.4964 an ounce, extending a 2.7 percent gain a day earlier.

The metal, sometimes called “poor man’s gold,” has risen more than 9 percent this year, while gold’s up less than 7 percent. The unpredictability of President Donald Trump’s administration and risks surrounding the outcome of elections in France and Germany this year have driven haven demand.

Supply may drop following mine closures and prices need to rise to boost output, according to Suki Cooper, analyst with Standard Chartered Plc in New York.

On demand, industrial use is expected to be roughly flat this year, though still near a record, said Jeffrey Christian, managing director of CPM Group. “Use in solar panels, electronics, batteries, jewelry, chemical process catalysts, and other manufactured products will remain strong,” he said.

We see silver as undervalued vis-à-vis gold but more especially vis-à-vis stocks, bonds and many property markets. Rather than selling the financial insurance that is gold, we would advise reducing allocations to stocks, bonds and property and allocating to physical silver.

We expect the gold silver ratio to fall back below 30 in the coming months and years. Indeed, given the favorable supply demand dynamics in the silver market and the fact that a huge amount of silver, unlike gold, has been used in industrial applications in the last 150 years and this continues with new tech uses today, we expect the gold silver ratio to mean revert to the long term average of 15 to 1 (see chart above).

http://www.goldcore.com/us/gold-blog/silver-1-70th-price- gold-silver-eagles-sales-jump/

-END-

Although the West slowed their appetite for gold and silver, China and Russia did not. In Feb the withdrawals (equals demand) at the Shanghai Gold Exchange showed 179 tonnes. If we extrapolate that demand for the coming year we would obtain a demand equal to 2200 tonnes or greater. China is back in demand for gold in a big way:

(courtesy Steve St Angelo/SRSRocco report)

Trump Market Euphoria Impacts Precious Metals Demand: Plummets In West, Surges In East

BySRSROCCO on March 20, 2017

With the Trump euphoria pushing the broader markets to new all-time highs, it has impacted precious metals demand considerably… especially in February. Precious metals investors believing the White House “Grandiose plans”, of making American great again, have cut back seriously on their precious metals buying.

There seems to be a percentage of the alternative community that believe Trump will actually put the U.S. back to the way it was in the 1960’s. And that is, back to a manufacturing powerhouse with high-paying jobs. While this would be a wonderful thing to do, the disintegrating ENERGY situation in the future just won’t allow it to happen.

IT WAS A ONE-TIME DEAL, and that period has come and gone…. FOREVER

Regardless, Western demand for precious metals declined considerably in February versus the same month last year. I used to spend more time publishing articles on gold and silver demand, but have refocused my analysis on how energy will impact the precious metals, mining and the overall economy.

However, Louis at Smaulgld.com does an excellent job publishing articles on precious metals demand. So, I have used some of his data and one of his charts.

As I stated above, the Trump market euphoria has taken the wind out of precious metals buying recently. According to the data from Smaulgld.com and the U.S. Mint, sales of gold and silver have plummeted in the West (especially USA), but surged in the East:

As we can see, Shanghai Gold Exchange withdrawals surged 67% in February versus the same month last year, while Perth Mint silver sales declined 17%, Perth Mint Gold sales dropped 32%, U.S. Gold Eagles fell 67% and Silver Eagle sales plummeted 75%.

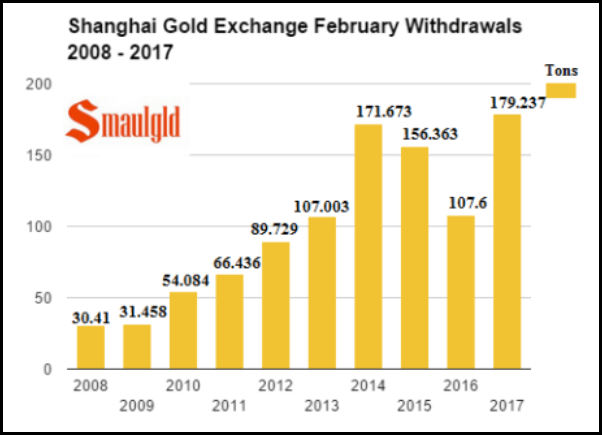

According to Louis’s article, Shanghai Gold Exchange February Withdrawals Highest On Record, he published the following chart:

Chinese Shanghai Gold Exchange withdrawals were 179 metric tons (mt) in February compared 107 the same month last year. Gold withdrawals from the Shanghai Gold Exchange are a pretty good proxy for the physical metal demand taking place in China. We must remember, global monthly gold mine supply is approximately 265 mt. Which means, Shanghai Gold Exchange withdrawals of 179 mt accounted for two-thirds of global gold monthly mine supply. That’s a heck of a lot of demand… from just one country.

If we tally up the decline in U.S. Gold Eagle and Perth Mint gold coin sales in February versus last year, they equaled 67,806 oz. However, Shanghai Gold Exchange withdrawals increased 2,315,000 oz in February compared to the same month last year. So, we can clearly see that the increase in just Chinese demand, via the Shanghai Gold Exchange withdrawals, more than made up for the decline in Western retail official cold coin purchases.

Unfortunately, the Royal Canadian Mint does not publish their Gold or Silver Maple Leaf sales until the end of each quarter. That being said, Canadian Gold and Silver Maple Leaf sales parallels what is taking place in U.S. Eagle sales. Thus, Gold & Silver Maple Leaf sales are probably down considerably as well.

I would imagine most precious metals investors came across this article published on Zerohedge a few days ago, Demand For Physical Gold Is Collapsing. It seems as if the intent of this article was to generate a lot of READS. Because, if we look at what is taking place in China, there is no collapse in physical gold buying. Matter-a-fact, there was a record amount of gold withdrawn off the Shanghai Gold Exchange last month.

The author of that article, needed to include a footnote stating the following:

Western physical precious metal demand (especially in the USA) decreased significantly due to the Trump Market Euphoria, while Shanghai Gold Exchange withdrawals hit a new record in February as the Chinese realize the U.S. economy and Dollar is still toast.

I am completely dumbfounded by recent decline in precious metals demand and sentiment in the West. While I can understand the reason precious metals investors believe Trump will make America great again, the future ENERGY DYNAMICS will not allow us to return to the good ‘ole days of a manufacturing super-power. Rather, the upcoming collapse will change our lives forever.

When the Dow Jones Index and broader markets finally crack, there won’t be too many SAFE HAVENS to invest in. Along with a collapse of the Dow Jones Index, Real Estate prices in all sectors will head down the toilet. Investors scrambling for something to protect wealth will move into precious metals. Unfortunately, there won’t be much available supply… only at MUCH HIGHER PRICES.

So, this current downturn in Western physical gold and silver purchases do not phase me one bit. It only indicates that most Americans are completely insane when it comes to sound fundamental investing.

IMPORTANT NOTE: I will be publishing an article on the continued disintegration of the Global Oil Industry. I provide data showing how Mexico’s national oil company, PEMEX, is literally BANKRUPT. By looking at the data, logic suggests that the global oil industry is in serious trouble.

Lastly, the data for the Perth Mint sales came from two articles at Smaulgld.com, Perth Mine Silver Sales Slump In February and Perth Mint Gold Sales February Drop 32%. Sales of Gold & Silver Eagles were found on the U.S. Mint website.

END

Russia adds another 9.33 tonnes to official reserves”‘

(courtesy Lawrie Williams/Sharp Pixley)

LAWRIE WILLIAMS: Russia adds another 9.33 tonnes to its gold reserves in February

The Russian central bank continued to add to its gold reserves in February, but at a slower rate than in January or in November last year, it is too early to say whether the fall in the reported increase is significant given that the amount taken in is still greater than in three individual months last year. In the event, the Russian central bank reported that it had added 300,000 ounces of gold during February, bringing its total holding to around 1,654 tonnes – still keeping it in sixth place among national gold holders, behind China, which has reported gold reserves of 1,842.6 tonnes, but is still closing the gap on its neighbour. We speculated earlier this month that Russian gold reserves could even rise to match, or exceed, China’s officially reported gold reserve figure this year, although that was based on a continuation on a monthly basis of Russian reserve increases of 31.1 tonnes, as recorded in January – see: Russia’s gold reserves could overtake China’s this year. Given that China currently does not appear to be adding to its gold reserves – at least according to its official announcements – Russian reserves are still on the way to exceeding those of China assuming the latter’s buying hiatus continues. (It has added no gold to its reported reserves since October last year)

See below the world’s biggest gold holding nations as reported to the IMF. *Note Russia’s figure updated to take account of the latest central bank announcement of yesterday.

Table: World’s Top 10 National gold holders

| Tonnes | % of reserves | ||

| 1 | United States | 8,133.5 | 74.6% |

| 2 | Germany | 3,377.9 | 68.8% |

| 3 | Italy | 2,451.8 | 67.8% |

| 4 | France | 2,435.8 | 63.8% |

| 5 | China | 1,842.6 | 2.3% |

| 6 | Russia* | 1,654.4 | 16.4% |

| 7 | Switzerland | 1,040.0 | 6.0% |

| 8 | Japan | 765.2 | 2.4% |

| 9 | Netherlands | 612.5 | 63.9% |

| 10 | India | 557.8 | 6.0% |

As can be seen from the above table, Russia now only lags China by some 188 tonnes in terms of its gold reserves. Last year Russia added just over 200 tonnes to its reserves and a continuation at this kind of rate – if China continues its halt of official gold buying – would mean Russia’s reported reserves would be pretty much on a par with those of China by the year end.

Even so adding Russian and Chinese reported reserves together would only come to 3,497 tonnes – a little more than those of Germany in second place and still hugely behind the reported US holding which has, officially, remained unchanged since 2006 when it reported a reduction of 1.6 tonnes. All the IMF reported reserve figures are somewhat open to question as leased gold – and a number of nations have reported gold leasing activities – remains in reserve figures although it may not actually be available.

China has also been seen to add gold into its reserves surreptitiously by holding it in non-reported accounts and then updating its total figures at five or six year intervals, although it has been officially been reporting monthly changes in its holdings since July 2015 – but who knows? Other countries could also be non-reporters of changes in their gold reserves to the IMF for various reasons, so we can only really take the IMF figures as being the best guide available. We can’t vouch for their overall accuracy!

end

As many of you know, I am not a fan of technical analysis especially with manipulation occurring continually on the paper gold and silver markets. However very long term charts are quite intriguing as it is does give meaningful direction for these markets;

(courtesy Kingworldnews/James Turk)

Last week’s pops in gold and silver herald trend change, Turk tells KWN

Submitted by cpowell on Tue, 2017-03-21 00:47. Section: Daily Dispatches

7:47a ICT Tuesday, March 21, 2017

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk tells King World News today why he thinks last week’s sharp increases in gold and silver herald a trend change for the monetary metals. Turk’s comments are posted at KWN here:

http://kingworldnews.com/james-turk-mega-cup-and-handle-formation-has-si…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Bill Holter interviewed by X22 spotlight

(courtesy Bill Holter)

|

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER AT 6.8890( HUGE REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES STRONGER TO ONSHORE AT 6.8743/ Shanghai bourse UP 10.80 POINTS OR .33% / HANG SANG CLOSED UP 91.13 POINTS OR 0.37%

2. Nikkei closed DOWN 65.71 POINTS OR .34% /USA: YEN FALLS TO 112.53

3. Europe stocks opened ALL IN THE GREEN EXCEPT LONDON ( /USA dollar index FALLS TO 99.83/Euro UP to 1.0809

3b Japan 10 year bond yield: FALLS TO +.066%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.53/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 49.32 and Brent: 51.99

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.480%/Italian 10 yr bond yield DOWN to 2.325%

3j Greek 10 year bond yield RISES to : 7.441%

3k Gold at $1232.85/silver $17.41(8:15 am est) SILVER RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 24/100 in roubles/dollar) 57.09-

3m oil into the 49 dollar handle for WTI and 51 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT REVALUATION NORTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9954 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0761 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.480%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.493% early this morning. Thirty year rate at 3.105% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Rise; Euro Surges To 6 Week High After French Presidential Debate

European stocks are modestly in the green as gains in banks and oil companies offset declines in miners. Asian stocks and S&P futures rise with Emerging-market stocks extending their longest winning streak since August on the back of the 5th consecutive daily drop in the USD.

The euro rose to the strongest in six weeks after a French presidential debate eased market concerns about a possible Le Pen win: the first French debate was reportedly won by centrist Emmanuel Macron. For those who missed it, last night saw the first televised debate between the candidates. Those who tuned in may be feeling a little jaded as the debate ended up lasting a whopping three and a half hours. There were plenty of head to head moments between Macron and Le Pen in particular which included much finger pointing and also amusing bouts of sarcasm. Immigration was unsurprisingly a hot topic while the exchanges also moved over to the economy and various policy measures. The general feeling was certainly one of it being lively however. Markets were largely waiting for some sort of conclusion about who came out on top though and following the debate an Elabe poll (covering 1157 respondents) found that Macron was seen as the winner of the debate at 29% with Melenchon second with 20%. Fillon and Le Pen came in joint third at 19% and Hamon came in fifth at 11%. An Opinionway poll showed 25% for Macron; in both polls Fillon and Le Pen were tied at 19%.

“From the point of view of international investors, this is a positive as it keeps France’s position in the euro zone secure, or at least not weaker,” said DZ Bank analyst Rene Albrecht.

As a result, the average probability of Macron win implied from betting odds climbed 2ppts to over 63%…

… boosting the Euro and peripheral bonds while pressuing Bunds. It’s worth noting that there are another two debates to come prior to the first round election on April 23rd. It’s also worth noting that Hillary Clinton was seen as the comfortable winner in all the US Presidential debates.

Taking a cue from the debate polling which showed Macron as the most convincing, German bonds slid from the open, with French election risks seen waning. Losses extended in bunds after stronger-than-expected U.K. inflation data pressured gilts lower, with 10y U.K. yields climbing by around 6bps. MPC-dated SONIA rate jumps to price in almost one full hike by August 2018. The easing of French election risk has firmed rate-hike expectations for the ECB. Euribor strip has bear steepened from the open, with market pricing now showing over 20bps of rate increases priced by Sept. 2018. ECB rate expectations have seen the 5y sector on the German curve underperform, now cheaper by around 2bps on the 2s5s10s fly. French bonds meanwhile opened higher after the debate, with 10y yields dropping as much as 4bps. The move was quickly faded, as has been repeatedly observed in similar bouts of optimism around the French election. OATs now little changed.

The biggest winner, however, was the Euro, which rose to just shy of 1.08, the strongest in more than a month.

“When you consider how many people have been worried about this election and how cheap the euro is, if that risk were to go away then there’s the potential for money to flow into Europe,” said Andrew Sheets, chief cross-asset strategist at Morgan Stanley in London. “That would be another form of volatility. There’s always a risk of large moves when valuations are extreme — and the euro is quite cheap.”

The dollar index fell below 100 for the first time since early February and was down almost half a percent on the day. The currency was on the defensive after Chicago Federal Reserve President Charles Evans reinforced the perception that the U.S. central bank will not accelerate the pace of its interest rate hikes. He said on Monday that two more interest rate hikes this year were likely, disappointing investors who had anticipated rates would be increased more quickly. The greenback is on its longest losing streak since November after the Federal Reserve’s dovish message on the speed of monetary tightening last week.

European stock markets opened higher after a rally in Asia, where MSCI’s broadest index of Asia-Pacific shares outside Japan hit 21-month highs. U.S. stock futures pointed to a positive start for Wall Street, which had suffered on Monday as investors worried that President Donald Trump’s plan to cut taxes and boost the economy would take longer than expected to realize. South Korea led gains among Asian emerging markets, with the Kospi jumping 1 percent to the highest since July 2011. Hyundai Motor Co. climbed 8.6 percent amid market speculation over a possible stake purchase by Elliott Management. The Stoxx Europe 600 Index added less than 0.1 percent at 9:48 a.m. in London. Banking stocks outperformed, led by Italian and French lenders, as worries over the French presidential election further abated. Mining stocks lost ground, trimming recent sharp gains. Futures on the S&P 500 rose 0.1 percent. The benchmark gauge fell 0.2 percent on Monday.

The 10-year U.S. Treasury yield briefly fell to two-week lows following the comments to 2.461 percent. It last stood at 2.48%. Oil prices rallied on expectations that an OPEC-led production cut to prop up the market could be extended. Prices for front-month Brent crude futures LCOc1, the international benchmark for oil, gained 1 percent to $52.13 per barrel. OPEC members increasingly favor extending the output curb beyond June to balance the market, sources within the group said, although they added this would require non-OPEC members such as Russia to also step up their efforts.

Elsewhere, Deutsche Bank was in focus as the subscription period for a capital raising began on Tuesday. Also today, Nike, FedEx, and General Mills are among companies scheduled to publish results

* * *

Bulletin Headline Summary from RanSquawk

- Sentiment in Europe received a lift from the open as participants reacted to a perceived strong performance from Macron in last night’s French presidential debate.

- GBP ramps higher after inflation rises to the highest level since Sep’13

- Looking ahead, focus will Canadian retail sales, API crude report as well as comments from Fed’s George and Mester.

Market Snapshot

- S&P 500 futures up 0.2% to 2373.5

- STOXX Europe 600 up less than 0.1% to 378

- MXAP up 0.1% to 149

- MXAPJ up 0.3% to 483.23

- Nikkei down 0.3% to 19,455.88

- Topix down 0.2% to 1,563.42

- Hang Seng Index up 0.4% to 24,593.12

- Shanghai Composite up 0.3% to 3,261.61

- Sensex down 0.3% to 29,432.19

- Australia S&P/ASX 200 down 0.07% to 5,774.62

- Kospi up 1% to 2,178.38

- German 10Y yield rose 2.8 bps to 0.468%

- Euro up 0.5% to 1.0795 per US$

- Brent Futures up 0.9% to $52.06/bbl

- Italian 10Y yield rose 0.7 bps to 2.364%

- Spanish 10Y yield fell 0.4 bps to 1.843%

- Gold spot down 0.4% to $1,229.24

- U.S. Dollar Index down 0.4% to 100.01

Top Overnight News from BBG

- PPG Said to Ready New Akzo Offer After Failed $22.4 Billion Bid

- Fed’s Dudley Says Wells Fargo Shows Bank Culture Needs Improving

- Google Overhauls Policies After Uproar Over YouTube Videos

- Deutsche Bank Said to Face Regulatory Fines Over Currency Trades

- Mideast Airlines Say New U.S. Restrictions Will Force Changes

- BlackRock Likes Property Even After Yellen Calls Prices ‘High’

- BMW Sees 2017 Profit Rising Slightly as Spending Exceeds Target

- Banking Panel Senators Make Bipartisan Call for Growth Proposals

- Baidu’s iQiyi Signs Pact With Warner Bros. on Movie Rights

- Chevron Says New LNG Projects Unlikely in West Australia

- NYSE Says It Has Identified, Fixed Cause of Arca Disruption

In Asian Markets, the major equity indices traded somewhat mixed following a similar lead from Wall St., where financials underperformed and participants were indecisive amid a lack of tier-1 data releases. ASX 200 (-0.1%) was dampened by weakness in telecoms and underperformance in the financial sector, while Nikkei 225 (-0.4%) lagged on return from an extended weekend, although downside was stemmed as USD/JPY nursed losses. Elsewhere, Hang Seng (+0.3%) and Shanghai Comp. (+0.3%) were kept afloat following the continued liquidity operations by the PBoC which resulted in a 2nd day of net injections. Finally, 10 year JGBs traded higher amid a dampened risk tone in Japan and with the BoJ present in the market for a total JPY 1.15tIn of JGBs ranging from 1-10yr maturities. PBoC injected CNY 50bIn 7-day reverse repos, CNY 20bIn in 14-day reverse repos and CNY 10bIn in 28-day reverse repos

Top Asian News

- SoftBank Is Said to Invest in WeWork at $17 Billion Valuation

- Downer Makes A$1.26 Billion Takeover Offer for Spotless

- McDonald’s China Says It’s Not Affected by Ban on Brazil Meat

- Billionaire Damani’s Avenue Supermarts Shares Double on Debut

- Modi-Backed ETF May Fuel India Sales After $1.4 Billion Haul

- China H Shares Rise to Highest Since 2015; Power Producers Gain

- M1 Bids May Not Come Above S$2.20/Share, Religare’s Jin Says

- India’s HPCL to Use Honeywell Clean-Fuel Technology

- Freeport Indonesia Restarts Copper Concentrate Mill: Spokesman

European risk sentiment received a lift from the open as participants reacted to a perceived strong performance from Macron in last night’s French presidential debate. As such European equities opened higher, with Euro Stoxx 50 spending much of the session higher by around 0.5%. On a sector breakdown, financials are among the best performers as Deutsche Bank trades higher on the session after going ex-subscription to their capital raising plans. Elsewhere Akzo Nobel are among the best performers on a stock specific basis as M&A news continues to circulate, with pre-market reports today suggesting PPG is preparing a renewed takeover offer for the Co. The notable data of the session, came in the form of UK CPI, with the higher than exp. reading (Y/Y 2.3% vs. Exp. 2.1%) seeing gilts underperform and sending GBP/USD towards 1.2450. The GBP strength has further exacerbated pressure on the USD, with the USD-index slipping below 100, while the French presidential election saw EUR/USD touch 1.0800. Fixed income markets have been pressured by the aforementioned risk on sentiment, with Bunds down 35 ticks on the session, while OATs saw a paring of some of their initial losses in the wake of reports that PM Cazeneuve asked govt. members not to back Macron.

Top European News

- EU Makes U.K. Wait to Start Brexit Talks as Trigger Date Set

- Macron on Top After First Debate of French Presidential Election

- Porsche SE Posts Profit as Owner Clan Plans to Buy Out Piech

- Swiss Watch Slump Extends Record Decline as U.S. Exports Slide

- Fingerprint Cards Withdraws Dividend Plan as Revenue Plummets

- Abertis Gives Information on Ruling on AP-7 Accounting Treatment

- Swedish Casino Company Takes Breather From Deals to Drive Growth

- Poland Needs Innovation to Catch Up With West, World Bank Says

In currencies, the Bloomberg Dollar Spot Index slipped by 0.2 percent, following a 0.1 percent drop Tuesday. The euro was up by 0.5 percent at $1.0796, while it rose versus all of its G-10 peers. The British pound traded 0.7 percent higher after data showed U.K. inflation rose faster than expected. The main mover of the morning has been GBP, which had been trending higher ahead of the inflation report to trip above 1.2400. In the wake of the release, GBP continued its ascension after CPI beat expectations, subsequently stoking expectations that the overshoot will force the Bank of England to act through potentially hiking rates, as such, a 25bps hike is now fully priced in by Aug’18. Elsewhere, a reassuring performance from Macron in the first presidential TV debate has buoyed EUR, with the currency touching 1.08 against the greenback. RBA minutes from Mar 7th meeting stated that it judged steady policy was consistent with growth and inflation targets and that rising AUD/USD would complicate economic transition. RBA also stated that economic growth is to accelerate gradually to above potential over the next 2 years and higher commodity prices could last longer than first thought given the stronger global demand.

In commodities, West Texas Intermediate oil climbed 0.8 percent to $48.60 before U.S. inventory data on Wednesday and as Libya prepared to restart crude shipments from major ports. Copper slumped 0.7 percent amid signs supplies are returning; disruptions caused the metal to surge last month to the highest level since 2015; prices slipped after reports that the union for workers on strike at the BHP Billiton Escondida copper mine held talks with the company and also coincided with a 4% drop in Dalian iron ore futures during Asian trade. Gold (-0.4%) prices pulled back from 2 week highs after four days of gains, while the softness in the USD index has supported oil prices with Brent futures above USD 52/bbl and WTI above USD 49/bbl ahead of the API inventories after market.

Looking at the day ahead, in the US the diary remains sparse with just the Q4 current account balance reading expected. Away from the data this morning we are expected to hear from the Fed’s Dudley and BoE’s Carney at a bank ethics event in London, while this afternoon we are due to hear from the Fed’s George and then this evening the Fed’s Mester is due to speak. The EU finance ministers meeting will also continue in Brussels this morning.

US Event Calendar

- 8:30am: Current Account Balance, est. $129.0b deficit, prior $113.0b deficit

Central Banks

- 6:35am: Fed’s Dudley, BOE’s Carney Speak at Bank Ethics London Event

- 12pm: Fed’s George Speaks in Washington on U.S. Economy and the Fed

- 6pm: Fed’s Mester Speaks at University of Richmond

- 9:45pm: Boston Fed Rosengren Speaks in Bali at Asia-Pacific Meeting

DB’s Jim Reid concludes the overnight wrap

Will France wake up this morning feeling more confident about the upcoming Presidential race? Well last night saw the first televised debate between the candidates. Those who tuned in may be feeling a little jaded as the debate ended up lasting a whopping three and a half hours. There were plenty of head to head moments between Macron and Le Pen in particular which included much finger pointing and also amusing bouts of sarcasm. Immigration was unsurprisingly a hot topic while the exchanges also moved over to the economy and various policy measures. The general feeling was certainly one of it being lively however. Markets were largely waiting for some sort of conclusion about who came out on top though and following the debate an Elabe poll (covering 1157 respondents) found that Macron was seen as the winner of the debate at 29% with Melenchon second with 20%. Fillon and Le Pen came in joint third at 19% and Hamon came in fifth at 11%. It’s worth noting that there are another two debates to come prior to the first round election on April 23rd. It’s also worth noting that Hillary Clinton was seen as the comfortable winner in all the US Presidential debates.

Prior to the outcome from that poll the Euro did touch as low as 1.072 overnight versus the US Dollar but bounced post the news and hit a high of 1.078, or up just under half a percent with the market seemingly comforted that the debate failed to yield any further support to Le Pen’s chances. The Euro is now sitting at 1.076 as we go to print. Meanwhile equity markets are once again a bit mixed. Having been closed on Monday bourses in Japan are open again with the Nikkei currently -0.27%. The ASX (-0.16%) is also down however there are small gains for the Hang Seng (+0.31%), Shanghai Comp (+0.19%) and more notably the Kospi (+1.02%). US equity index futures are also up about +0.20% while Gold is -0.57% so suggesting a slightly more positive environment for risk at the margin this morning.

While we’re on France, we thought it would be worth highlighting a report published by our colleagues yesterday in Europe summarising the results of their recently conducted global cross asset survey about investors’ views of asset returns one week after the French presidential election. They summarise that a Le Pen or a Left win is, perhaps unsurprisingly, strongly associated with Negative or Very Negative risk asset outcomes. A Centre win is mainly associated with Positive (but not Very Positive) outcomes, suggesting investors remain cautious about the economic environment, regardless of outcome. Many investors are neutrally positioned, but of non-neutral investors there is a distinct tilt towards long volatility and long hedges. A negative outcome is largely associated with high equity vol and sharp equity falls. In a positive outcome, the majority expectation is for limited equity upside only; however, we highlight a notable tail of expectations in the highly positive scenario, i.e. for very low vol and large equity upside. In rates the dominant expectation is for stable / higher yields regardless of election outcome. FX markets show a more bearish tilt, with EURUSD below parity in a negative outcome. In addition, upside is more limited – only 26% of respondents see EUR/USD above 1.10 in a positive outcome.

Moving on. In what was an otherwise very quiet day for the most part yesterday, it was the chorus of Fedspeak which markets were most concentrated on. Of particular focus was the Chicago Fed’s Evans who made the case for the Fed hiking 2 or 3 more times this year. Evans also said that he expects inflation to hit 2% in 2018 and that things are “much more balanced around the outlook” than they were two years ago. The Philadelphia Fed President Harker also spoke and said that he expects the Fed to overshoot the 2% inflation target “a little bit” and that he would not rule out a faster or slower pace of hikes in 2017 than the three he has projected so far. Finally there was a much more dovish angle to the Fedspeak yesterday too with Minneapolis Fed President Kashkari also speaking. He said that “we do not have a high inflation threat right around the corner” and that ‘I’d be very surprised if core inflation reaches 2% this year”. He also said that “the data are basically moving sideways, so I’m asking, what’s the rush to raise rates”.

Aside from the Fedspeak, there wasn’t a huge amount more for markets to feed off aside from some political related stories. The G-20 news from the weekend came and went however a lot of the focus was on the news that the FBI has confirmed that it is conducting a broad inquiry into a possible link between President Trump’s presidential campaign in 2016 and Russia. Meanwhile here in the UK we got the confirmation that PM Theresa May will trigger Article 50 on March 29th and so officially starting the clock on negotiations. The European Council President Donald Tusk confirmed that he will present the draft Brexit guidelines to the EU27 members states within 48 hours. It’s worth noting also that a provisional plan for the EU to hold a summit on April 6th to discuss early negotiation plans has been pushed back to late April/early May, all of which obviously eats into PM May’s negotiating time frame.

Over in markets the end result of all the Fedspeak and various political related headlines was a very modest risk off start to the week. The S&P 500 ended -0.20% by the closing bell and so confirming a third consecutive daily decline following last Wednesday’s big post-FOMC rally. The Stoxx 600 (-0.17%) was down a similar amount and fell for the first time since last Tuesday. The exception was once again in EM however where the MSCI EM index (+0.70%) rose for the seventh consecutive session. In government bonds 10y Treasury yields dipped 4bps to 2.462% and are now down to the lowest yield since March 6th having touched an intraday high of 2.628% a week ago. In Europe bond markets didn’t really do much although Greek bonds were a bit weaker after Eurogroup head Jeroen Dijsselbloem said at a finance minister’s meeting that “some key issues” still remain to be sorted out between Greece and its creditors and that talks will continue and intensify in coming days.

Moving on. Yesterday’s data was fairly thin on the ground. In the US the sole release was the Chicago Fed national activity index which came in at a better than expected 0.34 in February (vs. 0.03 expected) and in doing so has pushed the three-month average up to 0.24 which is the highest since December 2014. In Germany PPI was reported as rising +0.2% mom in February which was a little less than expected. Meanwhile in the UK the Rightmove index of house prices showed prices as stable at +2.3% yoy in March. The other data concerned the latest weekly ECB CSPP holdings where the average daily run rate last week of €363m more or less matched the average €367m since the program started.

Looking at the day ahead, this morning in Europe the focus will be on the UK where we will get the February CPI/RPI/PPI data (with headline CPI expected come in at +0.5% mom and headline RPI at +0.8% mom). We will also get the February public sector net borrowing data in the UK and then the March CBI industrial trends survey. This afternoon in the US the diary remains sparse with just the Q4 current account balance reading expected. Away from the data this morning we are expected to hear from the Fed’s Dudley and BoE’s Carney at a bank ethics event in London, while this afternoon we are due to hear from the Fed’s George and then this evening the Fed’s Mester is due to speak. The EU finance ministers meeting will also continue in Brussels this morning.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 10.80 POINTS OR .33%/ /Hang Sang CLOSED UP 91.13 POINTS OR 0.37% . The Nikkei closed down 65.71 .34% /Australia’s all ordinaires CLOSED DOWN 0.03%/Chinese yuan (ONSHORE) closed DOWN at 6.8890/Oil rose to 49.32 dollars per barrel for WTI and 51.99 for Brent. Stocks in Europe ALL IN THE GREEN EXCEPT LONDON ..Offshore yuan trades 6.87743 yuan to the dollar vs 6.8890 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AGAIN/ ONSHORE YUAN STRONGER AS IS THE OFFSHORE YUAN AND THIS IS COUPLED WITH THE HUGELY WEAKER DOLLAR. CHINA SENDS HER DISPLEASURE SIGNAL TO WASHINGTON

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA

This must give you a very warm and fuzzy feeling: North Korea reveals a propaganda video of them blowing up a USA aircraft

(courtesy zerohedge)

North Korea Blows Up US Aircraft Carrier, Bomber In New Propaganda Video

North Korea’s disgruntled dictator – whose fate is looking more precarious by the day – Kim Jong-un has released a propaganda video in which a US aircraft carrier is blown up while a US strategic bomber shot down in flames. The clip also includes footage from the communist state’s recent ballistic missile launches are shown alongside a simple message: “a knife will be stabbed into the throat of the carrier.” The video declares: “The bomber will fall from the sky after getting hit by a hail of fire.” Footage also shows the USS Carl Vinson nuclear-powered aircraft carrier up in flames.

The 2 minute clip has emerged just days after Kim threatened to reduce the US “to ashes” as tensions with North Korea continue to increase, which in turn followed a warning by Tillerson that the US is preparing for a “first strike” against the irrational dictator, while US special forces conduct drills in South Korea to “eliminate” the country’s ruler.

It comes after a statement earlier this month warned Donald Trump of nuclear destruction if America fires “even a single bullet” towards Pyongyang. In it the country warned that “the Korean People’s Army will reduce the bases of aggression and provocation to ashes with its invincible Hwasong rockets tipped with nuclear warheads and reliably defend the security of the country and its people’s happiness in case the US and the South Korean puppet forces fire even a single bullet at the territory of the DPRK.”

The menacing talk came as South Korea warned over the weekend that its northern neighbor’s latest rocket-engine test showed “meaningful” progress. As reported on Sunday, the KCNA news agency said the engine would help the country achieve world-class satellite-launch capability – indicating a new type of rocket engine for an intercontinental ballistic missile.

In further acts of defiance, North Korea has declared it is not scared of recent US threats of possible pre-emptive military action to stop its nuclear build-up.

US President Donald Trump told reporters he held meetings on North Korea during the weekend at his Florida resort. While he did not refer specifically to the rocket-engine test, he said Kim Jong-un was “acting very, very badly.” Trump and members of his administration have been talking tough on North Korea since the Republican took office back in January.

As a reminder, last Friday Secretary of State Rex Tillerson announced the “policy of strategic patience” was over and refused to rule out military action. He said: “The diplomatic and other efforts of the past 20 years to bring North Korea to a point of de-nuclearisation have failed. So we have 20 years of a failed approach.

“And that includes a period in which the US provided $1.35billion (£1.08billion) in assistance to North Korea as an encouragement to take a different pathway.” He added: “If they elevate the threat of their weapons program to a level we believe requires action that option is on the table.”

Meanwhile, as Reuters reported, fearing a possible attack, Japan started staging mass evacuation drills. In the first exercise of its kind saw civilians young and old scrambling for cover as air-raid sirens wailed.

The video is below:

end

Ladies and gentlemen: Kim is a madman and must be taken out:

he threatens the USA with a “first strike” nuclear iCBM

(courtesy zero hedge)

North Korea Threatens US With “First-Strike” Nuclear ICBM

In the latest troubling development to come out of North Korea’s increasingly irrational leadership, Reuters reports that the communist country has nothing to fear from any U.S. move to broaden sanctions aimed at cutting it off from the global financial system and will pursue “acceleration” of its nuclear and missile programs, according to a Pyongyang envoy. This includes developing a “pre-emptive first strike capability” and an inter-continental ballistic missile, according to Choe Myong Nam, deputy ambassador at the DPRK (North Korean) mission to the United Nations in Geneva.

The latest development follows a previous report also from Reuters, in which it said the Trump administration is considering sweeping sanctions as part of a broad review of measures to counter North Korea’s nuclear and missile threat. “I think this is stemming from the visit by the Secretary of State (Rex Tillerson) to Japan, South Korea and China…We of course are not afraid of any act like that,” Choe told Reuters.

“Even prohibition of the international transactions system, the global financial system, this kind of thing is part of their system that will not frighten us or make any difference.” He called existing sanctions “heinous and inhumane”.

Choe said his country wants a forum set up to examine the “legality and legitimacy of the sanctions regime” and denounced joint annual military exercises currently being carried out by the United States and South Korea on the divided peninsula and criticized remarks by Tillerson during his talks with regional allies last week.

“All he was talking about is for the United States to take military actions on DPRK (the Democratic People’s Republic of Korea,” Choe said.

Additionally, North Korea rejects claims by Washington and Seoul that the military drills taking place at this moment are defensive. They involve strategic nuclear bombers and a nuclear submarine Columbus that recently entered South Korean ports, he said.

“In the light of such huge military forces involved in the joint military exercises, we have no other choice but to continue with our full acceleration of the nuclear programs and missile programs.”

“It is because of these hostile activities on the part of the United States and South Korea.” “We strengthen our national defense capability as well as pre-emptive strike capabilities with nuclear forces as a centerpiece,” Choe said.

He declined to give technical details of North Korea’s latest rocket engine test on Sunday – seen as a possible prelude to a partial ICBM flight – calling it a great historical event that would lead to “fruitful outcomes”.

“I can tell you for sure that the inter-continental ballistic rockets of the DPRK will be launched at any time and at any place as decided by our Supreme Leadership,” Choe said, recalling leader Kim Jong Un’s pledge in a New Year’s address.

Analysts say North Korea has likely mastered the technology to power the different stages of an ICBM and may show it off soon, but is likely still a long way from being able to hit the mainland United States. Of course, it woudl be preferrable not to confirm this in practice either way.

“The United States has been talking about launching pre-emptive strikes at North Korea,” Choe said. “And we have been prepared to deter, to counter-attack such attacks on the part of the United States. We would utilize every possible means in our hands and the inter-continental ballistic rocket is one of them.”

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

This is interesting: the German Federal Auditor group is calling for an audit of the ECB as they need more supervision

(courtesy zero hedge)

“Audit The ECB”? – German Officials Call For Greater Oversight Of Central Bank

With the omnipotence of the world’s central banks suddenly all too evidently exposed as nothing more than ‘Oz’-like smoke-and-mirrors, it is not just US politicians that are losing faith and calling for more oversight of the most-powerful unelected officials in the world. Handelsblatt reports today that Germany’s federal auditor says The ECB lacks accountability in banking sector oversight and government will work to close that oversight gap.

Handelsblatt reports, citing a parliamentary report it obtained, that the European Court of Auditors is unable to perform an “extensive review” of the bank supervisory functions at ECB. Furthermore, the German Federal Court of Auditors says in a report submitted to the German parliament’s budget committee

Germany should explore all options for closing the oversight gap.

In its report, the federal auditor says bank oversight is an important public function that does not fall under the rubric of central bank independence, noting that national banking regulators like Germany’s used to be fully audited before the ECB took over the responsibility in 2015.

“The federal government should explore all options for closing this oversight gap,” the report said.

The ECB has argued that the European Court of Auditors only has the authority to review the central bank’s efficiency in terms of personnel and budgeting, not its decisions as Europe’s top banking supervisor. The European Court of Auditors has complained in the past that the ECB has used this argument to justify its refusal to turn over some documents for review.

That, according to the German agency, has left a gap in oversight that didn’t exist before 2015, since national regulators in the euro zone tended to be separate from their country’s central banks.

In a statement, the ECB said that it works closely with the European Court of Auditors and has made “a considerable number of documents and explanations available.”

While we fully understand the concerns at the lack of transparency and oversight of Europe’s most powerful entity, it is comewhat ironic that it is the Germans complaining when they just used the “well, it’s not us messing with the currency, the ECB is independent” argument to eschew Trump’s currency war tweets.

We are sure Dragh is not too worried for now, but if this escalates, this is what we would expect him to look like…

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

7. OIL ISSUES

This is how OPEC lost the battle against the shale boys as our American friends learned how to lower their cost curve and break even points;

(courtesy zero hedge)

How OPEC Lost The War Against Shale, In One Chart

At the start of March we showed a fascinating chart from Rystad Energy, demonstrating how dramatic the impact of technological efficiency on collapsing US shale production costs has been: in just the past 3 years, the wellhead breakeven price for key shale plays has collapsed from an average of $80 to the mid-$30s…

… resulting in drastically lower all-in breakevens for most US shale regions.

Today, in a note released by Goldman titled “OPEC: To cut or not to cut, that is the question”, the firm presents a chart which shows just as graphically how exactly OPEC lost the war against US shale: in one word: the cost curve has massively flattened and extended as a result of “shale productivity” driving oil breakeven in the US from $80 to $50-$55, in the process sweeping Saudi Arabia away from the post of global oil price setter to merely inventory manager.

This is how Goldman explains it:

Shale’s short time to market and ongoing productivity improvements have provided an efficient answer to the industry’s decade-long search for incremental hydrocarbon resources in technically challenging, high cost areas and has kicked off a competition amongst oil producing countries to offer attractive enough contracts and tax terms to attract incremental capital. This is instigating a structural deflationary change in the oil cost curve, as shown in Exhibit 2. This shift has driven low cost OPEC producers to respond by focusing on market share, ramping up production where possible, using their own domestic resources or incentivizing higher activity from the international oil companies through more attractive contract structures and tax regimes. In the rest of the world, projects and countries have to compete for capital, trying to drive costs down to become competitive through deflation, FX and potentially lower tax rates.

The implications of this curve shift are major, all of which are very adverse to the Saudis, who have been relegated from the post of long-term price setter to inventory manager, and thus the loss of leverage. Here are some further thoughts from Goldman:

- OPEC role: from price setter to inventory manager In the New Oil Order, we believe OPEC’s role has structurally changed from long-term price setter to inventory manager. In the past, large-scale developments required seven years+ from FID to peak production, giving OPEC long-term control over oil prices. US shale oil currently offers large-scale development opportunities with 6-9 months to peak production. This short-cycle opportunity has structurally changed the cost dynamics, eliminating the need for high cost frontier developments and instigating a competition for capital amongst oil producing countries that is lowering and flattening the cost curve through improved contract terms and taxes.

- OPEC’s November decision had unintended consequences: OPEC’s decision to cut production was rational and fit into the inventory management role. Inventory builds led to an extreme contango in the Brent forward curve, with 2-year fwd Brent trading at a US$5.5/bl (11%) premium to spot. As OPEC countries sell spot, but US E&Ps sell 30%+ of their production forward, this was giving the E&Ps a competitive advantage. Within one month of the OPEC announcement, the contango declined to US$1.1/bl (2%), achieving the cartel’s purpose. However, the unintended consequence was to underwrite shale activity through the credit market.

- Stability and credit fuel overconfidence and strong activity: A period of stability (1% Brent Coefficient of Variation ytd vs. 6% 3-year average) has allowed E&Ps to hedge (35% of 2017 oil production vs. 21% in November) and access the credit market, with high yield reopen after a 10- month closure (largest issuance in 4Q16 since 3Q14). Successful cost repositioning and abundant funding are boosting a short-cycle revival, with c.85% of oil companies under our coverage increasing capex in 2017.

That said, the new equilibrium only works as long as credit is cheap and plentiful. If and when the Fed’s inevitable rate hikes tighten credit access for shale firms, prompting the need for higher margins and profits, the old status quo will revert. As a reminder, this is how over a year ago Citi explained the dynamic of cheap credit leading to deflation and lower prices:

Easy access to capital was the essential “fuel” of the shale revolution. But too much capital led to too much oil production, and prices crashed. The shale sector is now being financially stress-tested, exposing shale’s dirty secret: many shale producers depend on capital market injections to fund ongoing activity because they have thus far greatly outspent cash flow.

This is the key ingredient of what Goldman calls the shift to a new “structural deflationary change in the oil cost curve” as shown in chart above. As such, there is the danger that tighter conditions will finally remove the structural pressure for lower prices. However, judging by recent rhetoric by FOMC members, this is hardly an imminent issue, which means Saudi Arabia has only bad options: either cut production, prompting higher prices and even greater shale incursion and market share loss for the Kingdom, or restore the old status quo, sending prices far lower, and in the process collapsing Saudi government revenues potentially unleashing another budget crisis.

end

Russia mentions production cut ( of which it does not mean) and up goes oil and then it fails

(courtesy zerohedge)

Oil Pumps’n’Dumps After Russia Mentions Production Cut

It appears the weight of positioning is too much to maintain any OPEC/NOPEC jawboning. After yesterday’s failure by the Saudis, Russia’s comments that it “doesn’t rule out extending the oil pact with OPEC” prompted an immediate algo panic buy… but seconds later that was sold into as we suspect over-extended longs are now using rips to reduce risk.

#Fail

It appears $49 is the new jawbone line in the sand…

end

API reports bigger and expected crude and a much bigger buildup at Cushing. However gasoline did have a drawdown. Oil initially rose and then plummeted on the news:

(courtesy zero hedge)

WTI/RBOB Pump’n’Dump After Surprise Inventory Data

After last week’s surprise draw (but big build at Cushing), API reports a bigger than expected crude (and Cushing) build and bigger than expected draw in Gasoline inventories. For now, both WTI and RBOB kneejerked higher but WTI faded very rapidly.

API

- Crude +4.539mm (+3mm exp)

- Cushing +1.968mm

- Gasoline -4.934mm (-2.4mm exp)

- Distillates -883k

Another big Cushing build and another big gasoline draw…

And the immediate reaction in WTI and RBOB – after both sold off today despite Russian jawboning –

Bloomberg reports:

“The catalyst is concern over demand due to potential difficulties with President Trump getting his pro-growth agenda through,” Bart Melek, the head of global commodity strategy at TD Securities in Toronto, says by phone. “The crude market acted technically here.”

“We’re still pretty high when it comes to inventories and if they keep getting higher, it’s only going to put more pressure on the market,” Carl Larry, principal consultant for Oil Outlooks and Opinions in Houston, says by phone

8. EMERGING MARKETS

Venezuela stops publishing money supply data. Who would have thought that they could do such a horrible act?

(courtesy zero hedge)

Venezuela Stops Publishing Money Supply Data For Obvious Reasons

More than a year after hyperinflating banana republic Venezuela stopped reporting official inflation data, Venezuela has stopped publishing money supply data, depriving the general public of the last, and best, available tool to ascertain soaring inflation in what has become the world’s worst-performing economy. Then again, one hardly needs official data to confirm the blistering wave of hyperinflation sweeping through the nation which has seen the value of the bolivar disintegrate under the Maduro regime.

The money supply indicator suddenly stopped appearing on the central bank’s website on Feb. 24. The data in question, which will no longer be updated, looked as follows most recently.

Despite the halt of CPI data, consumer price rises are widely seen to be in triple digits, driven by an unraveling socialist system in which many people struggle to obtain meals and medicines. The M2 money supply was up by nearly 180% in mid-February from a year earlier, according to the central bank before it halted the release of the weekly data without explanation last month Reuters reports. In contrast, Reuters reports that neighboring Colombia’s M2 was up 7 percent in the same period and the United States’ was up 6 percent.

“If they are not publishing, you know it must be skyrocketing,” Aurelio Concheso, director of the Caracas-based business consultancy Aspen Consulting, stated the obvious. The central bank and ministry of communications did not respond to a request for comment, Reuters adds.

An increase in M2, the sum of cash together with checking, savings and other deposits, means more currency is circulating. That can accelerate inflation when coupled with a decline in the output of goods and services – such as in Venezuela, which is in the fourth year of a recession. When money supply is growing exponentially, as it has been in Venezuela, academics usually point to the infamous example of the Weimar Republic and leave it at that.

Slowly but surely Venezuela has stopped publishing all economic data. In addition to money supply and CPI, the government ceased the dissemination of gross domestic product data more than a year ago. Before that, it put an end to the release of balance of payments figures and its consumer product scarcity index.

For those who are somehow unfamiliar, Venezuela’s money supply, as measured by M2, has risen exponentially since Hugo Chavez, a devout socialist, came to power in 1999 and is a major factor behind what is thought to be the world’s highest inflation.