Gold: $1291.70 UP $2.30

Silver: $18.25 DOWN 24 cents

Closing access prices:

Gold $1290.00

silver: $18.30!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1290.01 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1285.20

PREMIUM FIRST FIX: $4.81

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1291.69

NY GOLD PRICE AT THE EXACT SAME TIME: 1284.00

Premium of Shanghai 2nd fix/NY:$7.69

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1285.00

NY PRICING AT THE EXACT SAME TIME: $1286.50

LONDON SECOND GOLD FIX 10 AM: $1278.95

NY PRICING AT THE EXACT SAME TIME. 1285.08 ??????

For comex gold:

APRIL/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 26 NOTICE(S) FOR 2600 OZ.

TOTAL NOTICES SO FAR: 658 FOR 65,800 OZ (2.0466 TONNES)

For silver:

For silver: APRIL

0 NOTICES FILED TODAY FOR nil OZ/

Total number of notices filed so far this month: 744 for 3,720,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

The open interest in silver continues to advance with today’s reading just under 228,000 contracts (227,775 contracts/a new record) or about 4000 contracts ABOVE the record set last year. The price of silver is a good $2.14 below the previous record price when that record OI was set last year. It seems that the boys want to attack our precious metals as they are quite nervous about silver and its gigantic high OI for the front month of May.

Tonight’s open interest for gold should rise by about 2,000 contracts. The silver OI should fall because the price fell by 24 cents. A rise will cause migraines galore for our bankers.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY 277 contracts UP to 227,775 WITH NO RISE IN PRICE ( 0 CENTS) WITH RESPECT TO YESTERDAY’S TRADING. THE HEDGE FUNDS (MANAGED MONEY) CONTINUE TO REMAIN STEADFAST WITH THEIR POSITIONS ON DOWNDRAFT DAYS WHILE ADDING TO THEIR LONGS ON GOOD DAYS. THE BANKERS ARE DESPERATELY TRYING TO COVER THEIR EVER BURGEONING SHORTS (OVER 555 MILLION OZ) BUT TO NO AVAIL. In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.139 BILLION TO BE EXACT or 163% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the total comex gold ROSE BY 513 contracts WITH THE SMALL RISE IN THE PRICE OF GOLD ($3.50 with YESTERDAY’S TRADING). The total gold OI stands at 474,257 contracts.

we had 26 notice(s) filed upon for 2600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD:

Inventory rests tonight: 848.92 tonnes

.

SLV

We had no changes in silver inventory at the SLV today/

THE SLV Inventory rests at: 328.201 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 277 contracts UP TO 227,775, A NEW COMEX RECORD WITH NO RISE IN SILVER YESTERDAY ( 0 CENTS). We no doubt had some attempted short covering which badly failed as the longs keep piling on making it difficult for them to cover and overpowered the bankers. Our managed money sector (the hedge funds) continue to remain steadfast in their conviction as they added to their positions again with yesterday’s attempted raid. In gold, the open interest rose by 513 contracts with the accompanying rise in price by $3.50

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 25.45 POINTS OR 0.79%/ /Hang Sang CLOSED DOWN 337.12 POINTS OR 1.39%. The Nikkei closed UP 63.33 OR 0.35% /Australia’s all ordinaires CLOSED DOWN 79%/Chinese yuan (ONSHORE) closed UP at 6.8837/Oil DOWN to 52.19 dollars per barrel for WTI and 54.75 for Brent. Stocks in Europe CLOSED DEEPLY IN THE RED ..Offshore yuan trades 6.8817 yuan to the dollar vs 6.8837 for onshore yuan. NOW THE OFFSHORE IS SLIGHTLY WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY STRONGER AND THE OFFSHORE YUAN STRONGER TO THE ONSHORE AND THIS IS COUPLED WITH THE WEAKER DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA

see USA stories

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

i)UK/MAY CALLS ELECTION

Bill Blain explains what to expect with the upcoming election in the UK

( Bill Blain/MINT Partners)

ii)Deutsche bank explains why early elections are a game changer and will bring huge gains to the pound:

(courtesy zero hedge)

iii)British stocks in an absolute bloodbath with the surprise election:

( zero hedge)

iv) Then the pound explodes killing a huge number of shorts along the way:

the pound now: 1.28417 up 0.0250 or 250 basis points

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)RUSSIA/USA

USA fighter jets intercept two Russian tactical bombers only 100 miles from the Alaska coast. Getting scary!

( zero hedge)

ii)RUSSIA/VENEZUELA

I warned you about this. Russia seizes a tanker due to an unpaid shipping fees

( zerohedge)

6 .GLOBAL ISSUES

Reuters: Toronto Canada

Government officials meet in Toronto trying to solve the biggest bubble ever created in real estate

( Reuters)

7. OIL ISSUES

Oil slides after the market realizes that the Saudis will not extend their production cuts due to the increase in shale production from the uSA

( zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

i)Gold trading early this morning:

a massive 22,000 contracts thrown by the bankers but this will be to no avail

( zero hedge)

ii)Asia’s richest man Li Ka-Shing is now buying gold aggressively’

( Mac Slavo)

10. USA stories

i)USA trading early Tuesday morning:

The USA dollar begins to sink as Goldman Sachs covers its losing trade. It blames the Fed and Trump. Goldman exits all long dollar trades.

( zerohedge)

ii)Gold skyrockets, bonds tumble as the Pentagon is planning on knocking out North Korea’s missiles once fired:

( zero hedge)

iii)Today’s big story; The Pentagon is now considering shooting down North Korea Missile tests:

( zero hedge)

vi)Vacancy rates skyrocket in the USA’s 4 largest city Houston.

( zero hedge)

vii(And the USA is still having a massive increase in bartenders and waiters: the USA restaurant industry suffers its worst collapse since 2009

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 513 CONTRACTS UP to an OI level of 474,257 WITH THE RISE IN THE PRICE OF GOLD ( $3.50 with YESTERDAY’S trading). The bankers again were certainly not shy in supplying the necessary paper to our newbie longs. We are now in the contract month of APRIL and it is one of the BETTER delivery months of the year. In this APRIL delivery month we had A LOSS OF 24 contract(s) FALLING TO 1,096. We had 7 notices served yesterday so we LOST 17 contracts or 1700 oz will NOT stand for delivery in the active delivery month of April AND THESE GUYS WITHOUT A DOUBT WERE CASH SETTLED THROUGH THE OBSCURE EFT ROUTE DESCRIBED BY JAMES TURK.

At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month LOST 21 contract(s) and thus its OI is 2294 contracts. The next big active month is June and here the OI ROSE by 718 contracts UP to 345,421.

We had 26 notice(s) filed upon today for 700 oz

We are in the NON active delivery month is APRIL Here the open interest GAINED 6 contracts UP to 86 contracts. We had 0 notices filed yesterday so we GAINED 6 contracts or an additional 30,000 oz will stand for delivery AND NO CONTRACTS WERE PAPER SETTLED THROUGH THE ERP ROUTE.

The next active contract month is May and here the open interest LOST ONLY 4,759 contracts DOWN to 124,748 contracts which is astonishingly high. It is this front month that the crooked bankers are targeting as they must be frightened to see such a mammoth amount of contracts still standing for metal. Also remember that Good Friday was much earlier last year: we have only 8 trading days before first day notice. The non active June contract GAINED 3 contracts to stand at 186. The next big active month will be July and here the OI gained 4442 contracts up to 71,194.

FOR COMPARISON SAKE, ON APRIL 18/2016 WE HAD 97,642 CONTRACTS STANDING FOR DELIVERY. SO YOU CAN VISUALIZE FOR YOURSELF THE HUGE DIFFERENCE BETWEEN 2016 AND THIS YEAR.

For those keeping score, the initial amount of silver oz that stood for delivery for the May 2016 contract month: 28.01 million oz. By conclusion of the month only 13.58 million oz stood and the rest was cash settled.(EFP ROUTE)

.

We had 0 notice(s) filed for NIL oz for the APRIL 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 104,691 contracts which is poor.

Yesterday’s confirmed volume was 201745 contracts which is good.

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

417.96 oz

Manfra

Delaware

13 kilobars

|

| Deposits to the Dealer Inventory in oz | 1799.855 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

26 notice(s)

2600 OZ

|

| No of oz to be served (notices) |

1070 contracts

107,000 oz

|

| Total monthly oz gold served (contracts) so far this month |

658 notices

65800 oz

2.0466 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 445,891.5 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 26 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

101,118.243 oz

BRINKS

CNT

DELAWARE

SCOTIA

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,207,357.251 oz

JPMorgan

597,304.73 oz

Brinks

1029.82 oz

Delaware

total: 1,805,691.801 oz

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

86 contracts

(430,000 oz)

|

| Total monthly oz silver served (contracts) | 744 contracts (3,720,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,222,760.2 oz |

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz stood as bankers needed much silver to fill major holes elsewhere.

NPV for Sprott and Central Fund of Canada

will update later tonight the central fund of Canada figures

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

April 18/no changes at the GLD/Inventory remains at 848.92 tonnes

April 17/no changes at the GLD/Inventory remains at 848.92 tonnes

April 13/a deposit of 6.51 tonnes into the GLD/Inventory rests at 848.92 tonnes

this no doubt is a paper deposit/

APRIL 12/no changes in gold inventory at the GLD/Inventory rests at 842.41 tonnes

April 11/a huge deposit of 4.12 tonnes into inventory/Inventory rests at 842.41 tonnes

this would no doubt be a paper gold entry. It would be difficult to find that amount of physical gold.

April 10/1.77 tonnes added into inventory at the GLD/inventory rests at 838.29 tonnes

April 7/a small withdrawal of .28 tonnes from the GLD/Inventory rests at 836.49 tonnes

April 6/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 5/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 4/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 3.2017: a huge deposit of 4.45 tonnes of gold into the GLD/Inventory rests at 836.77 tonnnes

March 31/another withdrawal of 1.19 tonnes of gold inventory fro the GLD/this inventory would no doubt be heading for Shanghai/GLD inventory: 822.32 tonnes

March 30/no changes in gold inventory at the GLD/Inventory rests at 833.51 tonnes

March 29/a withdrawal of 1.78 tonnes of gold out of the GLD/Inventory rests tongith at 833.51 tonnes

March 28/this is good!! A deposit of 2.67 tonnes of gold into the GLD/Inventory rests at 835.29 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory rests at 832.62 tonnes

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

end

Now the SLV Inventory

April 18/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 17/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 13/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 12/no changes in inventory at the SLV/Inventory rests at 328.201 million oz/

April 11/a paper deposit of 11.131 million oz into the SLV/no doubt yesterday’s entry of a withdrawal of 11.231 million oz was in error/328.201 million oz

April 10/ a paper withdrawal of 11.231 million oz of silver from the SLV and this silver was used in the raid today. Inventory rests at 317.231 million oz

April 7./ a withdrawal of 947,000 oz of silver from the SLV/Inventory rests at 328.201 million oz.

April 6/a tiny withdrawal of 136,000 oz of silver from the SLV/Inventory rests at 329.148 million oz

April 5/ a withdrawal of 1.042 million oz from the SLV/Inventory rests at 329.284 million oz

April 4/no change in inventory at the SLV/Inventory rests at 330.326 million oz/

April 3.2017; a withdrawal of 568,000 oz from the SLV/Inventory rests at 330.326

million oz/

Major gold/silver trading/commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

END

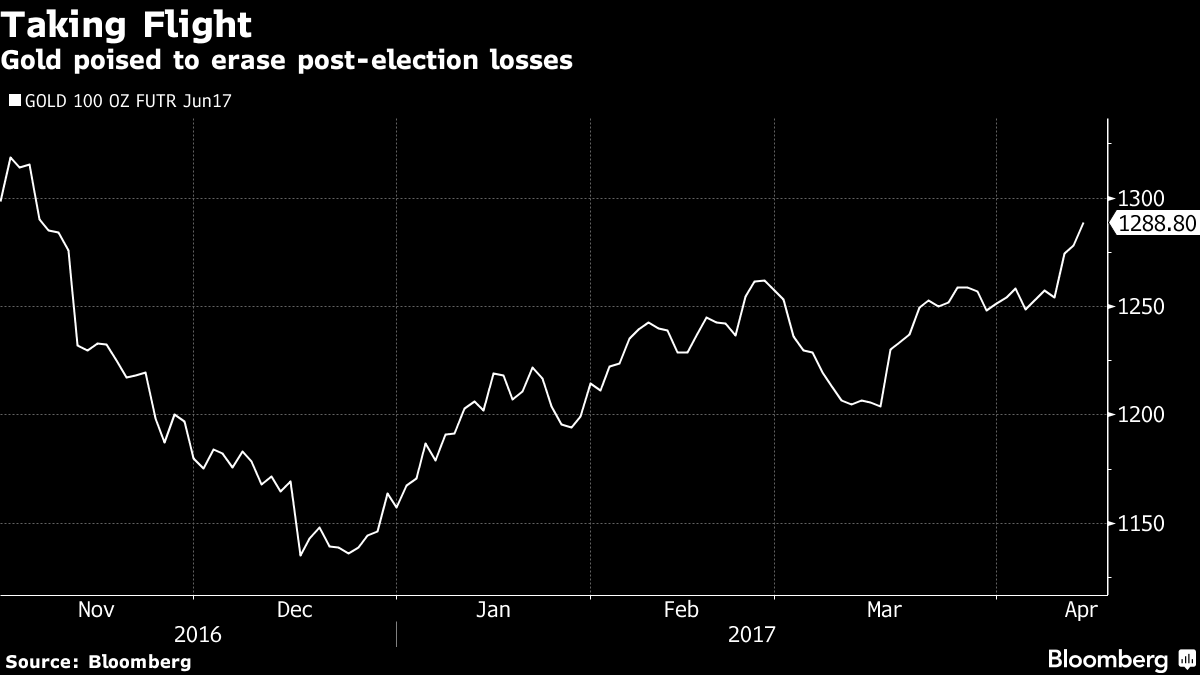

Gold Erases Post- Election Fall as Trump Wrong on Dollar

Gold Bullion Erases Post- Election Fall as Trump Wrong on Dollar – Daily Prophet

Robert Burgess of Bloomberg Prophets

President Donald Trump sent currency markets into a tizzy late Wednesday when he signaled his preference for a weaker dollar. “I think our dollar is getting too strong, and partially that’s my fault because people have confidence in me,” Trump told the Wall Street Journal.

Although the greenback immediately dropped before stabilizing Thursday, that’s only part of the story. In fact, it has been falling all year as traders lose confidence in Trump’s ability to push his pro-business, pro-growth policies through Congress. Judging by the Federal Reserve’s U.S. Trade Weighted Real Broad Dollar Index, the currency is weaker now than at the end of November, the month of Trump’s election victory. Other markets are sending similar signals. Stocks are rolling over and yields on Treasuries suggest optimism for stronger economic growth is quickly fading.

BULLISH ON GOLD

It’s no wonder that perhaps the only market hotter than the one for Treasuries is the one for gold. Bullion is up 11.4 percent this year to $1,289.10 an ounce. In a survey this week, traders and analysts were the most positive on gold since December 2015, according to Bloomberg News’ Eddie van der Walt and Ranjeetha Pakiam.

In yet another bullish sign, prices have climbed above the 200-day moving average and Britain’s Royal Mint said bullion purchases jumped 20 percent in the first quarter.

“We have all these latent threats that have been around for a while, Trump, European elections, Brexit, and they’re all just becoming a little more acute,” said Mark O’Byrne, a director at broker GoldCore Ltd. in Dublin.

Full article on Bloomberg Prophets here

END-

Gold trading early this morning:

a massive 22,000 contracts thrown by the bankers but this will be to no avail

(courtesy zero hedge)

Despite Dollar Dump, Gold Just Got Slammed By $3 Billion Notional Sale

While the dollar index tumbles to its lowest level since days after the election…

Someone decided this morning was an opportune time to dump over 22,000 gold futures contracts (almost $3 billion notional) sparking a quick plunge in the precious metal…

end

Asia’s richest man Li Ka-Shing is now buying gold aggressively’

(courtesy Mac Slavo)

Asia’s Richest Man Is “Aggressively Adding Direct Exposure To Gold”

Authored by Mac Slavo via SHTFplan.com,

The world is awash in crisis with wars looming, economies crashing and revolutions brewing. Doomsday bunkers sales are soaring and individuals from coast to coast are getting ready for whatever tomorrow may bring. Moreover, even governments like China and Russia are preparing, having gone so far as to create their own exchange mechanism to trade directly with gold in the event of a global currency crisis or financial meltdown.

But it’s not just governments who have taken notice of the problems facing the globe. According to Gold Mining Chairman Amir Adnani and Sprott U.S. Holdings CEO Rick Rule, some of the biggest billionaire investors on the planet are actively seeking out precious metals like gold as wealth protection insurance amid the uncertainty of the current geo-political climate.

In a recent interview with SGT Report, Adnani explains that several super wealthy individuals with whom he works very closely, including mainland China’s biggest billionaire investor and the richest man in all of Asia Li Ka-shing, have a renewed and urgent interest in diversifying their assets into both, gold mining firms and the physical asset itself:

This individual’s net worth is about $35 billion… For the first time in a number of years of working with his team when it comes to investments in commodities that they believe were important to the strategic growth of China… for the first time they are looking for gold related investments.

The comment from the person heading this initiative for Li Ka-shing is very interesting… His right had man said to me ‘He’s not just looking for investing in gold mines… he literally wants to find more ways to take physical gold back to Hong Kong and have that exposure.’

This is the largest individual investor in mainland China and I tell you over the last few years of having worked with him on the energy side, this is the first time I have seen him so aggressively looking for gold related opportunities.

In the full interview, insiders Amir Adnani and Rick Rule share their experiences working with others large investors, current strategies and expectations of what’s to come:

(Watch at Youtube)The reason for why these high net worth individuals are rapidly moving into gold related assets, notes Adnani, is that they are not necessarily all that concerned with the current price and how high it may go in the future, but rather, because precious metals are backed with thousands of years of evidence that they are the asset of last resort during crisis:

That’s one… the second one… we’re very fortunate at Gold Mining… one of the board members of our company who has been a founder of the company since day one is a Brazilian billionaire by the name of Mario Garnero…

When I look at the level of interest that his organization has in terms of wanting that direct exposure to gold… I talked to them about why they are looking at this…

They’re focused on one factor that we seldom think about… We’re so fixated on price of gold… what they’re focused on… what the super wealthy are focused on… what the billionaires are focused on… is the fact that gold plays that hedge in your portfolio… that’s it’s the insurance in the portfolio…

It may not necessarily be as critical to think whether it’s $1200 an ounce or $1300… we fixate so much on the price… and we forget that irrespective of what it’s trading at on any given day it’s meant to be an insurance policy… it’s meant to be protection of wealth and preservation of wealth…

It’s a great reminder when you look at the first trading day after Brexit… I remember looking at my own portoflio.. and looking at the market… and everything is red… the Dow is down over 500 points… the only thing up are gold stocks…

But while insurance and wealth preservation are the key motivating factor for the super wealthy, another billionaire, Sprott U.S. Holdings CEO Rick Rule, says that even a tiny boost in investor demand could drive prices to new highs from here as investors stampede into hard asset stocks and physical holdings as the current bull market gains steam:

Let me give you a startling statistic that tells you what an awakening might do… physical precious metals, certificated precious metals, and precious metals equities occupy about one-third of one percent of the savings and investment assets of the United States.

The corresponding number at the top of the last bull market.. real bull market in 1981… was 8%…

One third of 1% now… 8% at the top.

I’m not suggesting to you that gold and precious metals related investments will ever get back to 8% but I would suggest to you that they will, in this bull market, approach the three decade median, which was 1.5%.

If that occurred, you would see a more than four-fold increase in demand for precious metals and precious metals related equities… I think that could be reasonably dramatic.

I am not one of these doom and gloom guys who says that gold is going win the war against the U.S. dollar.

But if gold lost the war a little less badly… in other words, if gold and gold equities market shares got up to 1.5% of the investment savings matrix of the United States, that would represent a four-fold increase in demand.

The world is primed for a serious, potentially devastating collapse of life as we know it. That may come with war, economic collapse, or both simultaneously. What we know from history is that those who prepared ahead of time and understood the ramifications of such events were positioned to not only survive, but thrive.

The high net worth individuals who are moving into gold related assets see the writing on the wall, and they are positioning themselves now to ensure their wealth will be preserved.

We strongly encourage you to do the same.

end

India over the January through March period saw imports of gold total 230 tonnes which is excellent. I should also point out that this does not include smuggling which is significant. If this continues India will be back to importing over 1000 tonnes per year”

The World’s Top Gold Market Just Had Its Strongest Buying In 3 Years

By PiercePoints on April 17, 2017 10:50 am in Politics

Sentiment has turned up in the gold market the last few weeks. And new data from the world’s top consuming center — India — shows there may indeed be cause for optimism amongst bullion buyers.

Data reported in the local press showed that India’s gold imports saw a big jump during the most recent quarter, January to March 2017. With total imports for the period hitting 230 tonnes.

To put that in perspective, consider some numbers from recent quarters — during which India’s gold imports showed some of the weakest figures on record.

During April to October 2016, gold imports totalled just 264 tonnes. Meaning that incoming shipments for that entire seven-month period were barely above the figures for the most recent three months.

That suggests a major surge in gold demand is happening here. In fact, imports for the Jan-Mar 2017 quarter were the strongest for those months since 2013.

The pick-up in buying appears to be related to the Indian government’s recent crackdown on cash. With the government having banned small banknotes effective as of early November.

Since that event, gold imports have jumped to 360 tonnes for the five months from November to March. More than 35% higher than total imports for the preceding seven months.

India’s citizens are reportedly turning to gold as a safe haven amid doubts about paper money. Which bodes well for continued support in this key gold market as 2017 goes on.

How big a lift could that give to global gold prices? If we annualize the figures from the past quarter, India is on pace to import 920 tonnes for this year. Which would represent a massive improvement from the 13-year low imports of 571 tonnes the country saw in 2016.

It’s notable that global gold prices also perked up during the past quarter. As the chart below from Kitco shows, we’ve gone from $1,150/oz at the beginning of January to $1,280 recently.

http://www.valuewalk.com/wp-content/uploads/2017/04/Gold- Market.gifhttp://www.valuewalk.com/wp-content/uploads/2017/04/Gold- Market.gifThe gold price jumped in Q1 as imports to India also showed a notable rise

Gold Market

It’s actually unusual to see India’s demand growing when gold prices are going up — with Indian buyers usually cutting back purchases when the metal gets more expensive.

The fact that prices and demand are rising in tandem could signal an important and positive shift in fundamentals — watch for April import figures in a few weeks to see if the trend continues.

Here’s to coming back to life,

Dave Forest

Article by Pierce Points

http://www.valuewalk.com/2017/04/worlds-top-gold-market- just-strongest-buying-3-years/

-END-

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER 6.8837( REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.8817/ Shanghai bourse DOWN 25.45 POINTS OR 0.79% / HANG SANG CLOSED DOWN 337.12 POIONTS OR 1.39%

2. Nikkei closed UP 63.33 POINTS OR 0.35% /USA: YEN FALLS TO 108.87

3. Europe stocks opened ALL DEEPLY IN THE RED ( /USA dollar index FALLS TO 100.28/Euro UP to 1.0636

3b Japan 10 year bond yield: RISES TO +.01%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.19 and Brent: 54.75

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.193%/Italian 10 yr bond yield DOWN to 2.267%

3j Greek 10 year bond yield RISES to : 6.69%

3k Gold at $1285.00/silver $18.41 (8:15 am est) SILVER ABOVE RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 15/100 in roubles/dollar) 56.06-

3m oil into the 52 dollar handle for WTI and 54 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT BIG REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.87 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0012 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0687well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.193%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.237% early this morning. Thirty year rate at 2.901% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Slide As Iron Ore Crashes; Pound Jumps After UK Calls Snap Elections

European stocks slide as traders returned from a 4-day Easter holidays, Asian equities likewise drop pressured by the ongoing rout in iron ore, while U.S. stock-index futures point to a lower open. British markets were roiled after U.K. Prime Minister Theresa May said she would seek an early election on June 8, in a move aimed at strengthening her hand going into Brexit talks; the FTSE 100 dropped 1.3%, on the news, hitting the lowest since Feb. 24 while 10Y Gilts dropped below 1% for the first time since October.

The British pound first tumbled then surged on the news. Tracking today’s surprise announcement by the UK PM, sterling swung from gain to loss and back again versus the dollar before May set the vote for June 8. U.K. stocks fell by the most since January. The export-heavy FTSE 100 hits a seven-week low. The broader, more domestically focused FTSE 250, however, doesn’t see this as much of a negative:

Meanwhile, the Stoxx Europe 600 Index dropped to the lowest level in about three weeks as mining shares plunged, and government bonds in the region mostly rose as the build up to the French election intensified. Iron ore reeled as Citigroup Inc. said it’s bearish on the raw material’s outlook.

The catalyst for the overnight selloff came from Asia, where the iron ore rout continued, and after the latest 5% drop, the commodity has plunged 32% from high point in Feb this year.

The drop pressured Australian stocks (ASX 200 -1.0%) which declined to a 2-week low, as recent losses in iron ore and gold weighed on mining names. MSCI’s broadest index of Asia-Pacific shares outside Japan dropped 0.7 percent, while Tokyo’s Nikkei closed up 0.4 percent on earlier yen weakness.

A bounce in U.S. stocks Monday failed to cheer investors in the European session, as the standoff over North Korea’s nuclear weapons program rumbles on and the French presidential vote looms: here two candidates who want to take the country out of Europe’s common currency remain in contention in the most unpredictable race in recent history. As a result, the spread between German and Italian bonds continued to widen. “Expect a lot of noise and probably elevated volatility this week” as the first round of voting approaches, Jim Reid, a strategist at Deutsche Bank AG in London, wrote in a note.

The dollar dipped fractionally against a basket of major currencies. It earlier lifted off five-month lows versus the yen after U.S. Treasury Secretary Steven Mnuchin told the Financial Times a strong dollar was a positive in the long term while agreeing with U.S. President Donald Trump that it hurt exports in the short term.

Investors were also watching trade talks between the United States and Japan, whose deputy premier, Taro Aso, said the two sides agreed to combat unfair trade practices. “There was quite strong thinking in the market that the U.S. would maybe put pressure on Japan in terms of currency manipulation,” said Neil Jones, head of hedge fund FX sales at Mizuho in London.

Investor nervousness ahead of Sunday’s French election made itself felt in currency and debt markets. French 10-year government bond yields initially rose while ultra-safe German equivalents dipped, taking the gap between the two close to six-week highs. But French yields later fell and the spread with Germany narrowed to its tightest since April 13 after an opinion poll put centrist Emmanuel Macron first in the first round of voting, just ahead of far-right, anti-euro candidate Marine Le Pen with a bigger gap to far-left representative Jean-Luc Melenchon.

The cost of hedging against big moves in the euro against both the dollar and the yen over the next month jumped on Monday to their highest levels since Britain’s vote to leave the European Union.

“(Euro government bond) investors are going to be very careful this week and clearly the only thing that’s going to be on their minds is what happens in France,” said Chris Scicluna, head of economic research at Daiwa Capital Markets. Implied volatility in the STOXX 600 index hit its highest since early November 2016.

Oil prices fell after a U.S. government report indicated U.S. shale production was rising. Brent, the international benchmark crude, fell 29 cents a barrel to $55.07. Copper was down 0.6 percent at $$5,655 a tonne. Gold was marginally higher on the day at $1,283 an ounce, having touched a five-month high of $1,295 on Monday.

Economic data include March housing starts, industrial production. Scheduled earnings include J&J, Bank of America, IBM, UnitedHealth, Goldman Sachs.

Market Snapshot

- S&P 500 futures down 0.4% to 2,336.00

- STOXX Europe 600 down 0.6% to 378.44

- MXAP down 0.5% to 146.17

- MXAPJ down 0.8% to 476.46

- Nikkei up 0.4% to 18,418.59

- Topix up 0.4% to 1,471.53

- Hang Seng Index down 1.4% to 23,924.54

- Shanghai Composite down 0.8% to 3,196.71

- Sensex up 0.3% to 29,512.93

- Australia S&P/ASX 200 down 0.9% to 5,836.74

- Kospi up 0.1% to 2,148.46

- Brent Futures down 0.6% to $55.03/bbl

- Gold spot little changed at $1,284.90

- U.S. Dollar Index little changed at 100.31

- German 10Y yield fell 0.9 bps to 0.178%

- Euro up 0.07% to 1.0650 per US$

- Brent Futures down 0.6% to $55.03/bbl

- Italian 10Y yield rose 1.7 bps to 2.022%

- Spanish 10Y yield fell 2.0 bps to 1.687%

Top Overnight News

- Trump Seeks Shift in Visa Allotments Crucial to Tech Outsourcing

- Netflix Trades User Growth for Profits With No ‘House of Cards’

- Post to Buy Weetabix From Bright Food in $1.8 Billion Deal

- U.S. Trade Deal With South Korea Falling Short, Pence Warns

- Blackwater Founder Erik Prince Said to Have Advised Trump Team

- CDH Investments Said to Lead Buyout of Shoe Retailer Belle

- United Gains 1% on 1Q Beat, 2Q Prasm View; Peers AAL, DAL Rise

- Barracuda Falls After 2018 Revenue View Midpoint Trails Estimate

- Freeport Workers to Rally Against Grasberg Lay Offs April 20-22

- Allergan, Novartis to Run Phase 2b Study for NASH Treatment

- Arconic Shareholder Orbis Says Board Should Seek New Leadership

- Gigamon, CBL & Associates, Cytokinetics to Join S&P SmallCap 600

- Cardiovascular Systems to Recall 900 Pumps, Sees $1.5m Expense

- HP CEO Says Import Tax May Boost Prices for Users in Industry

- AdCare CEO Ousted After Board Says He Lied About MBA From UCLA

- Cemex to Sell Pacific Northwest Unit to Cadman for $150M

Asian equity markets dropped, failing to keep up with the positive momentum from Wall Street, where stocks rebounded as focus shifted to earnings and financials outperformed. ASX 200 (-1.0%) declined to a 2-week low, as recent losses in iron ore and gold weighed on mining names. Conversely, Nikkei 225 (+0.3%) was positive as exporter names benefited from a weaker JPY, while the financial sector performed similarly to its US counterparts. Shanghai Comp. (-0.8%) and Hang Seng (-1.4%) were subdued despite the PBoC resuming liquidity operations and firm Chinese Property Prices, as a continued rampant property sector could attract funds away from stocks. 10yr JGBs traded lower amid spillover selling from USTs and a somewhat positive risk tone in Japan, although losses were stemmed following a 5yr auction in which the b/c and accepted prices were higher than prior. Chinese House Price Index (Mar) Y/Y 11.3% (Prey. 11.8%). China house prices increased M/M in 62 out of 70 cities (Prey. 56) and increased Y/Y in 68 out of 70 cities (Prey. 67). PBoC injected CNY 40bIn in 7-day reverse repos, CNY 20bIn in 14-day reverse repos and CNY 20bIn in 28-day reverse repos.

Top Asian News

- Stock’s 9,800% Rise Shows Hong Kong Billions Exist Just on Paper

- Drugs and Booze Shares Benefit as China Investors Turn Defensive

- Japan, U.S. Eco Talks Should Have Near-Term, Concrete Results

- Hongqiao Drops $1.6 Billion Loften Purchase Citing New Rules

European equities have failed to hold on to opening gains and trade lower across the board with the FTSE 100 the laggard throughout the session. The commodity-heavy FTSE 100 bucked the trend at the open and started the week off on the backfoot alongside softness in energy and materials names with losses in gold overnight and iron ore prices hitting two week lows. Thereafter, European equities followed suit and shed their opening gains amid ongoing key risk factors as participants eye Sunday’s first round of voting for the French Presidential election with polls showing an increasingly narrow margin between the four main candidates. Elsewhere, downbeat comments from US treasury secretary Mnuchin on the fate of tax reform and mounting geopolitical tensions have also added to the sombre tone. In fixed income markets, prices saw a relatively tentative start to the session before then being lent a helping hand by some of the softness in European equities. The focus however has been on French paper which trades relatively flat ahead of the 1st round election in which the election polls have narrowed somewhat, indicating the 1st round is a now a 4-horse race amid the surge in support for far-left Melenchon. Additionally, the shock announcement by PM Theresa May that the UK will hold a snap election on June 8 has thrown local traders for a loop, unleashing volatility both in sterling and the FTSE100, which hit its lowest level since Feb. 24

Top European News

- French Race Up for Grabs Days Before First Ballot Is Cast

- Bank Brexit Exodus Seen Hastened by Close Regulator Scrutiny

- London House-Price Growth at Five-Year Low as Luxury End Slumps

- Deutsche Bank Sees 2017 High-Yield Market Defying Political Risk

- Swiss Aren’t Manipulating Their Currency, Gasser Tells CNBC

- JPMorgan Stays Constructive Europe Banks Long Term; Nordics Best

- European Miners Post Worst Drop on Stoxx 600 as Iron Ore Tumbles

In currencies, a choppy morning for GBP as the early running saw near term ‘radio silence’ prompting a fresh push higher in Cable as we pierced 1.2600. This proved short lived however as news that UK PM May announced a snap election sent cable tumbling then rebounding sharply higher. The EURGBP will struggle for upside traction ahead of the French elections, with the first round voting set for Sunday 23 April. The polls are tight, but looking at the EUR across the board, there does not seem to be any major panic, with EUR/USD sticking close to 1.0650 (large expiry here today), and EUR/JPY finding some near-term demand below 116.00. EUR/CHF treads a very tight range under 1.0700, but no prizes for guessing what is behind this. The JPY ‘relief’ looks to be based on what some perceive to be a near term ‘verbal’ impasse between the US and North Korea. Further JPY strength may be unwarranted at this stage, but resuming to steady risk on is still further out on the horizon. USD/JPY is back under 109.00 though, but techs point to a strong support zone in the 107.00-108.00 which may be tempting in value buyers irrespective of the mood in equities. AUD has suffered on the RBA minutes overnight as their concerns over the labour market and household indebtedness edge a rate cut back into policy considerations. AUD/USD is languishing in the lower 0.7500’s, but downside momentum has faded here for now as traders focuses on AUD/NZD, which has now taken out modest support at 1.0750. NZD/USD propped above 0.7000 as a result. Oil prices take a dip to push USD/CAD back above 1.3350, but as we have seen in recent weeks, selling interest through 1.3400 has been strong, so we may see orders marked down given the domestic data has been supportive in recent months.

In commodities, Gold has come off better levels in line with a modest uptick in the USD, with the key USD1300.00 having held amid last week’s fall and heightened risk aversion. We see little which would have arrested the drop off in risk sentiment, but this is not an unfamiliar scenario, but the yellow metal is likely remain underpinned alongside Silver. The latter has comfortably established a foothold above USD18.00. Oil prices continue to turn up and down on inventory data and rig counts, but with WTI inside USD50-55, we again see little cause for concern unless the risk mood in equities turns sharply. The same can be said for base metals with Copper prices largely range bound after coming off better levels in recent weeks. Palladium and aluminium modest outperformers on the day.

US Event Calendar

- 8:30am: Housing Starts, est. 1.25m, prior 1.29m; MoM, est. -2.95%, prior 3.0%

- Building Permits, est. 1.25m, prior 1.21m; MoM, est. 2.8%, prior -6.2%

- 9:15am: Industrial Production MoM, est. 0.4%, prior 0.0%; Capacity Utilization, est. 76.1%, prior 75.4%; Manufacturing (SIC) Production, est. 0.0%, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

One wonders how many Italian Governments there will be in the next 117 years but in the near-term there will be more focus on this coming Sunday’s first round in the French Presidential elections which will dominate a week that also includes the first busy week of US earnings season (46 S&P 500 companies report) and the influential flash PMIs on Friday. In our 2017 outlook written nearly 6 months ago now (how time flies) the French election was one of those events where we thought volatility would increase notably into it even though we thought there’d be a market friendly outcome at the end of it. So far this year vol has been much lower than we anticipated but it has been picking up of late ahead of this election and also due to geopolitical rumblings, some slightly disappointing data and market concerns that Mr Trump’s growth agenda may be faltering. We still think 2017 will ultimately be ok from a growth and risk asset point of view but it might be that we’re now past the calmest point of the year.

As we approach the election, the polls are now incredibly close with all four main candidates within a few percentage points of each other. Indeed the last 3 polls (Elabe, Ifop-Fiducial and OpinionWay) have an average high-low range amongst the top 4 candidates of 4.5% with the most notable trend now being a slight dip in support of Le Pen to around 22-23% from closer to 25% earlier this month. Market friendly candidate Macron remains well ahead of his 3 main rivals in a straight head-to-head run-off (16-26% lead) but obviously there’ll be some concern with the first round getting tighter that he’ll fail to be in that run-off with the worst case market scenario a Le Pen/Melenchon battle. So expect a lot of noise and probably elevated vol this week. The VSTOXX index closed at 23.39 on Thursday (double where it was back in mid-March) which as a reminder is the highest level this year and also the highest level since November 8th. Meanwhile the VIX closed at 14.66 last night which is down from Thursday’s YTD high of 15.96 but still well above the 2017 average of 12.01.

That move lower in the VIX yesterday reflects what was a fairly calm session on Wall Street last night. Coming off the back of a -1.13% weekly loss last week the S&P 500 bounced back +0.86% yesterday on low volumes while there was a similar rebound for the Dow (+0.90%) and Nasdaq (+0.89%) as well. Ahead of today’s results it was the Banks that led the way with the sector up just over 2% – as a recap both JP Morgan and Citigroup set a decent pace last week with Q1 revenue and earnings both coming in slightly ahead of the consensus estimate. Geopolitics was less of a factor yesterday despite that weekend news of the failed North Korea missile launch. Instead some decent data out of China including the Q1 GDP report helped to support a strong start to the week.

Indeed China’s Q1 GDP print of 6.9% came in one-tenth ahead of the consensus estimate and also improved from 6.8% and 6.7% in Q4 and Q3 of 2016 respectively. At the same time all headline activity indicators in March were supportive. Industrial production came in at 7.6% yoy (vs. 6.3% expected) from 6.0% in February. Retail sales stabilised at 10.9% yoy (vs. 9.7% expected) and fixed asset investment grew to 9.2% yoy (vs. 8.8% expected) from 8.9%. It’s worth noting that the latter was driven by property investment growth as opposed to infrastructure investment. Our economists in China also highlighted that property sales growth moderated slightly in March on a monthly basis but was still picking up if you look at the 3-month moving averages. At the same time growth of land sales and new housing starts also continued to grow. As a result of the data our economists have now revised up their GDP growth forecast to 6.7% in 2017 and 6.3% in 2018 (6.5% and 6.0% before revision). Importantly though, our team believe that growth has likely peaked in Q1 as credit growth slows and indeed they maintain the view that growth will drop on a quarterly basis to 6.8%, 6.6% and 6.5% in Q2, Q3 and Q4 respectively.

That data in China yesterday was attributed to the leg up for Copper (+1.14%), Aluminium (+0.58%) and Zinc (+0.88%) prices although the rest of the commodity complex was a little softer with Gold (-0.08%) and WTI Oil (-1.00%) both easing – although that does follow a decent rally last week. In sovereign bond markets 10y Treasury yields initially dipped below 2.200% at the open before steadily rising back as the session progressed to finish up just over 1bp at 2.251%. The focus in FX meanwhile was on the Turkish Lira which was as much as 2.5% stronger at the open before paring gains into the close. The rally came after President Erdogan secured victory in Turkey’s referendum which will now hand him sweeping powers including economic and monetary policies. Notwithstanding a possible recount as demanded by the opposition parties, our economist in Turkey notes that the bulk of the amendments, including a formal shift to an executive presidency, will kick in with the next dual elections (Parliamentary and Presidential) scheduled to be held in November 2019. The immediate changes post referendum are (i) removal of the current constitutional ban on the President’s formal association with a political party, (ii) restructuring of the Supreme Council of Judges and Prosecutors, and (iii) abolishment of military courts. The Parliament will now have six months to make subsequent amendments in the related laws, including the electoral law, as well as Parliamentary bylaws.

Before we recap the rest of the news since we’ve been away, this morning in Asia it’s been a fairly mixed start to the day with most major bourses open again following the long weekend. While the Nikkei (+0.23%) and CSI 300 (+0.08%) have edged a bit higher, the Hang Seng (-0.96%), Kospi (-0.18%) and ASX (-1.13%) are all lower while US equity index futures are also slightly in the red. There’s not been much new newsflow to report overnight although the latest house price data is out in China with house prices reported as rising in 62 of the 70 cities tracked by the government in March. That compares to 56 cities in February.

Moving on. Another story which attracted a bit of attention yesterday was US Treasury Secretary Steven Mnuchin’s interview with the FT. In it he said that the target to get tax reforms through Congress by August was “highly aggressive to not realistic at this point” and that “it is fair to say it is probably delayed a bit because of the healthcare (reform pushback)”. Mnuchin also responded to Trump’s statement about the strength of the dollar last week by saying that “the President was making a factual comment about the strength of the dollar in the short term” and that there is “a big difference between talk and action”. Mnuchin also suggested that the border-adjustment tax plan is not off the table but that there may be other ways of raising revenues.

Before we look at the week ahead, it’s worth quickly wrapping up what has been a busy last couple of days for US data. The significant release on Friday was the March CPI report where headline inflation came in at a well below market -0.3% mom (vs. 0.0% expected). The core was also softer than expected at -0.1% mom (vs. +0.2% expected). The end result of that is a drop in the annual rates for both the headline (to +2.4% from +2.7%) and core (to +2.0% from +2.2%). Also out on Friday was the March retail sales figures where headline sales were reported as retreating -0.2% mom as expected. Excluding autos and gas, pending was up +0.1% mom while the control group component was up a more robust +0.5% mom (vs. +0.3% expected) removing the impact of building materials. Meanwhile yesterday we learned that the NY Fed’s empire manufacturing index fell 11.2pts to 5.2 in April and the lowest since November, while the NAHB housing market index declined 3pts to 68 from what had been a 12-year high. It’s worth noting that the Atlanta Fed is now forecasting for Q1 GDP growth of just +0.5% (from +0.6%).

Moving now to this week’s calendar. With no data due out in Europe this morning the focus will instead be on the US this afternoon where March housing starts and building permits data is due out alongside the March industrial and manufacturing production reports. Turning to Wednesday, data due out in Europe includes the March CPI report for the Euro area along with the latest trade balance print. In the US tomorrow there is no data due out although in the evening the Fed’s Beige Book will be released. Japan kicks things off on Thursday with the March trade data due out. In Europe we’ll get PPI in Germany as well as the April consumer confidence reading for the Euro area. In the US on Thursday initial jobless claims, Philly Fed business outlook and Conference Board’s leading index are the scheduled releases. We end the week on Friday with a first look at the global flash April PMI’s including the manufacturing print in Japan and manufacturing, services and composite readings in Europe and the US. Also due out is retail sales data in the UK and existing home sales data in the US. Away from the data, this week’s Fedspeak includes George today, Rosengren on Wednesday, Powell on Thursday and Kashkari on Friday. Over at the ECB Hansson, Coeure and Praet are amongst the speakers this week while the BoE’s Carney speaks on Thursday. Also worth highlighting this week is US Vice- President Mike Pence’s meeting with Japan PM Abe and the release of the IMF’s World Economic Outlook today, Italy PM Gentiloni’s meeting with President Trump on Thursday and the annual Spring Meetings of the World Bank Group and IMF kicking off on Friday. Earnings wise this week we’ve got 46 S&P 500 companies accounting for 10% of the index market cap. The highlights include Goldman Sachs, Bank of America, Yahoo, Johnson & Johnson and IBM today, eBay and Morgan Stanley on Wednesday, Verizon on Thursday and Schlumberger on Friday.

END

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 25.45 POINTS OR 0.79%/ /Hang Sang CLOSED DOWN 337.12 POINTS OR 1.39%. The Nikkei closed UP 63.33 OR 0.35% /Australia’s all ordinaires CLOSED DOWN 79%/Chinese yuan (ONSHORE) closed UP at 6.8837/Oil DOWN to 52.19 dollars per barrel for WTI and 54.75 for Brent. Stocks in Europe CLOSED DEEPLY IN THE RED ..Offshore yuan trades 6.8817 yuan to the dollar vs 6.8837 for onshore yuan. NOW THE OFFSHORE IS SLIGHTLY WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY STRONGER AND THE OFFSHORE YUAN STRONGER TO THE ONSHORE AND THIS IS COUPLED WITH THE WEAKER DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

4. EUROPEAN AFFAIRS

UK/MAY CALLS ELECTION

Bill Blain explains what to expect with the upcoming election in the UK

(courtesy Bill Blain/MINT Partners)

What Does Theresa May’s Stunning Announcement Mean: Bill Blain Explains

Authored by Bill Blain via MINT Partners,

There will be load of unhappy Labour politicians this afternoon… even though many of them hold “safe seats”, I suspect many will be updating their CVs and looking for new jobs.

May’s intent is to clear the decks of dissent. SNP leader Nicola Sturgeon was the only person name checked in May’s announcement rant. That is a clear message to the Scottish Nationalists: the Conservatives intend to win this election nationally, and I should imagine we’ll see a massive effort to back up the resurgent Scottish Conservatives over the next 6 weeks. Scottish Conservatives will focus on the SNPs domestic track record running the country rather than pushing for independence – its not a good one.

There are risks:

May does risk losing her overall majority – its only 16 – especially if voters responds favourably to the Liberals who will try to turn it into a vote on Brexit.

However, this is a national election where its the country that matters – the Conservatives have lost by-elections on Brexit protest last year, but I suspect we are beyond that in the coming national plebiscite. Wont stop the Liberals telling people how wrong they were last year.

The SNP will try to make it a Brexit/Independence vote, but the Tories only hold one seat in Scotland so the SNP have little to gain and everything to lose. I’ll be looking at Scottish seats in detail.

Labour are the party in trouble. Although many of their seats are supposedly safe, electoral dissatisfaction with Corbyn and their pro-Brexit demograph means they’ll have to play a real election with muddled policies, a disorganised party under a hapless leader… which must have been irresistible to May. Shame.

The election notice and vote in Westminster should pass tomorrow. If she can’t get the 2/3rd majority to overturn the 2011 fixed-term government act, a simple no-confidence vote will suffice to trigger the election.

What does it mean for markets?

Sterling Spiked Higher.

GBPUSD is at its highest since early Feb on the news – breaking aboive its 200-day moving average for the first time since Brexit.

Gilts went down (up in yield). FTSE done little.

Generally this should be seen as dampening Scottish Uncertainty, giving the Tories a clearer mandate on Brexit by default, and positive for the economy.

But let’s look at the electoral constituencies in detail to work out the likely trends. Might the Tories lose their majority to a resurgent Liberal crew (doubt it). Might Labour get wiped.. (perhaps).

Fascinating…

And don’t believe the polls…

end

Deutsche bank explains why early elections are a game changer and will bring huge gains to the pound:

(courtesy zero hedge)

Deutsche Bank: “Early UK Elections Are A Gamechanger; We Are Closing Our Bearish GBP Trades”

This morning’s shocking announcement caught virtually everybody by surprise, and is prompting one bank after another to thoroughly revise their cable forecasts, case in point Deutsche Bank, whose strategist George Saravelos just announced he is changing his view on sterling because the “early elections are a game-changer”, something which the market clearly anticipated judging by the surge in cable…

… a surge which will prompt the near record number of GBP shorts to cover en masse.

To be sure, May’s announcement does make sense in retrospect: as Unicredit’s Vasileios Gkionakis notes, May’s logic is sound: “It’s good to have the elections now that you have good U.K. numbers, which are mostly dependent on global growth, because when you start seeing the U.K. idiosyncratic factors filtering through, potentially her popularity is going to throb a bit”

As for Saravelos, his full note below:

Changing view on sterling: early elections a game-changer

This morning’s announcement from PM May of a snap general election on the 8th June is in our view a game-changer for both the UK’s Brexit negotiations and sterling. We argued last year that an early general election was the only way to resolve the political impasse the U.K. government faces in conducting Brexit negotiations. The 2020 General Election imposed a hard deadline on delivering Brexit on an unrealistic timeline as well as making the Prime Minister reliant on a small Euro-sceptic majority. Both of these factors would have required political and market pressure to impose the appropriate political shifts that would have allowed a realistic deal to emerge.

In contrast, today’s general election announcement changes the outlook. We do not see the election as a mandate for hard Brexit. Instead, assuming current polling proves correct, it should result in a larger Conservative majority. This will have three material implications, in our opinion.

- First, it makes the deadline to deliver a “clean” Brexit without a lengthy transitional arrangement by 2019 far less pressing given that no general election will be due the year after.

- Second, it will dilute the influence of MPs pushing for hard Brexit, strengthening the government’s domestic political position and allowing earlier compromise over key EU demands for a

- transitional arrangement.

- Third, it strengthens the PM’s overall negotiating stance who in recent weeks has clearly fallen in line with the European negotiating approach.

This will involve a settlement of the Brexit payments and other divorce aspects first, to be followed by a lengthy transitional period during which the final outcome of Brexit will emerge. This sequenced approach materially reduces the “crash risk” of Brexit negotiations as well as strengthening the Prime Minister’s hand in pursuing an orderly (and very lengthy) withdrawal. All of the above in turn reduce downside risks for the U.K. growth outlook over Brexit negotiations.

We have been structurally bearish on sterling for the last two years but are now changing view. We are closing out all our bearish FX trades. We intend to review our sterling forecasts in coming days.

That said, some disagree. As Bloombergs Richard Jones writes after the announcement, the early election is not likely to shift the dial “much” for investors. Key highlights from his take:

It’s hard to see how an early U.K. election will be a game changer for markets.

The process to leave the European Union has already been initiated with the triggering of Article 50. And polls show the Conservatives will win hands down and return to the government with an increased majority. Domestic politics hasn’t been a great source of uncertainty. It is rather the economic implications of Brexit and the attendant lack of clarity that has ratcheted up consumer, business and investor anxiety.

The clock is ticking, the political dynamics aren’t likely to shift, so investors have no reason to radically alter their views on the implications of Brexit with Tuesday’s announcement.

The longer-term implications of Brexit are perhaps best summarized in a recent paper from the San Francisco Fed, a prognosis not dissimilar to the views expressed by Bank of England Governor Mark Carney.

The lack of access to the EU single market will likely damp potential U.K. growth for years, with Britain both less specialized and less efficient post-Brexit, the San Francisco Fed argued.

If today’s price action is any indication, market moves will probably be noisy during the election campaign. But unless there is any unexpected shift in domestic political dynamics, the issues currently in place will remain after June 8.

For now, however, it’s the short covering panic that is driving price at least for the immediate future.

end

British stocks in an absolute bloodbath with the surprise election:

(courtesy zero hedge)

British Bloodbath – Stocks Plunge Most Since Brexit After Surprise Election News

While most eyes were on the surge in sterling, British stocks plunged almost 2.5%…

The biggest daily drop since the Brexit referendum in June 2016.

This has erased all FTSE 100 gains for 2017…

end

Then the pound explodes killing a huge number of shorts along the way:

the pound now: 1.28417 up 0.0250 or 250 basis points

(courtesy zerohedge)

Cable Flash Smash: Pound Explodes As Stops Taken Out

In what looks and smells like a combination of a margin call and an algo stop-run, cable just exploded through 1.28 and 1.29 in seconds only to quickly fade back on massive volume…

Spot FX…

Sterling Futures show the surge in volume…

That’s what happens when you have a record speculative net short position…

Which hammered the dollar to 3-week lows…

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

RUSSIA/USA

USA fighter jets intercept two Russian tactical bombers only 100 miles from the Alaska coast. Getting scary!

(courtesy zero hedge)

US Fighter Jets Intercept Two Russian Tactical Bombers 100 Miles Away From Alaska

The U.S. Air Force scrambled two F-22 stealth fighters on Monday night to intercept a pair of Russian nuclear-capable bombers which came as close as 100 miles from Alaska’s Kodiak Island, Fox reports. This was the first time since President Trump took office that Moscow has sent bombers so close to the U.S.

The two Russian Tu-95 “Bear” tactical bombers flew roughly 280 miles southwest of Elmendorf Air Force Base, within the Air Defense Identification Zone of the United States. The U.S. Air Force promptly scrambled two F-22 stealth fighter jets and an E-3 airborne early warning plane to intercept the Russian bombers.

The American jets flew alongside the Russian bombers for 12 minutes, before the Russian bombers reversed course and headed back to their base in eastern Russia.

An official quoted by the Washington Examiner said that while TU-95s are capable of carrying nuclear weapons, the planes involved in Monday’s incident did not appear armed. The interception was conducted in a “safe and professional” manner, the official added, as the bombers did not violate U.S. airspace or break international norms.

Monday’s incident comes amid escalating tension between Russia and the U.S., particularly over Syria’s ongoing civil war. Trump’s decision to strike Assad’s government earlier this month put the U.S. at odds with Russia, which has long supported Assad. Russian Foreign Minister Sergei Lavrov said last week that the chemical attack was staged.

Lavrov also said that another U.S. military strike in Syria could prompt “grave consequences not only for regional but global security.” Secretary of State Rex Tillerson said earlier this month that U.S.-Russia relations have hit “a low point” following the strike. The top U.S. diplomat added that “improvement in the long-term relationship” between both nations is required to resolve the conflict in Syria.

* * *

The last time Russian bombers flew near the U.S. was July 4, 2015, when a pair of Russian bombers flew off the coasts of Alaska and California, coming as close as 40 miles to Mendocino, Calif. Russian President Vladimir Putin called then-President Barack Obama to wish him a happy Independence Day while the bombers cruised the California coastline.

end

RUSSIA/VENEZUELA

I warned you about this. Russia seizes a tanker due to an unpaid shipping fees

(courtesy zerohedge)

Russia Takes $30 Million In Venezuela Oil Hostage Over Unpaid Debt

Despite having made its bond payment due last week, Venezuela’s state oil company, PDVSA, remains in fire financial straits, with virtually no funds or liquidity, and regardless of the close Russia-Venezuela ties, a Russian state-run shipping company has taken a tanker of PDVSA crude “hostage” in the Caribbean over $30 million worth of unpaid shipping fees.

Russia’s shipper Sovcomflot sued PDVSA in the Dutch island St. Maarten in the Caribbean and “imposed garnishment on the aforementioned oil cargo,” Reuters reported on Tuesday, citing a St. Maarten court decision. PDVSA had sent the oil cargo to the Caribbean in October last year, hoping it could net around $20 million from the sale of the crude, but Sovcomflot claims the cash-strapped state-run Venezuelan company owes $30 million in unpaid shipping fees.

Nearly half a year after crossing the Caribbean, the NS Columbus has transfered its cargo of crude to a storage terminal on St. Eustatius, an island just south of St. Maarten, under the court court. Another tribunal in England will decide if Sovcomflot will ultimately take the oil. Reuters adds that the dispute, which is being heard by the United Kingdom Admiralty Court, highlights how shipping companies are becoming increasingly aggressive in pursuing PDVSA’s debts.

It also shows that political allies such as Russia are losing patience with delinquent payments from Venezuela, whose obsolete tankers are struggling to export oil and even to supply fuel to the domestic market.

Making matters even more complicated, PDVSA owes not only shipping fees to the Russian company, but also millions of U.S. dollars to terminals around the Caribbean, including the St. Eustatius terminal – where the oil is currently held – owned by U.S. company NuStar Energy, Reuters reported citing a PDVSA executive and an employee at one of the terminals. Furthermore, PDVSA’s “tangled web of payment disputes” now spans the entire world, from unpaid shipyards in Portugal and half-built tankers in Iran and Brazil to the seized cargo in tiny St. Eustatius, whose strategic location in the Caribbean made it an 18th century colonial-era trading hub.

That’s not all: as a result of the recent liquidity crunch at PDVSA, the oil company also finds itself months behind on shipping crude oil and fuel to China and Russia under oil-for-loan agreements with its two key political allies. The shipments that PDVSA has failed to deliver to Chinese and Russian state-held companies were worth around $750 million, a Reuters analysis showed back in February.

Will the issue be resolved amicably?

On one hand, Russia has consistently supported President Nicolas Maduro with financing arrangements and oilfield investments. State-run oil firm Rosneft has lent money to PDVSA since 2016 and last month was in talks to help PDVSA make a hefty bond payment. However, problems had been brewing for months between Venezuela and Sovcomflot, which provides about 15% of vessels that PDVSA charters to ship crude to its clients amid a steady deterioration of its own fleet, according to a captain and two shipbrokers working with PDVSA.

Debts to Sovcomflot had by 2016 swelled enough that company’s top brass complained in person to PDVSA President Eulogio Del Pino in the Russian city of Sochi, according to source from PDVSA’s trade department with knowledge of the meeting.

Del Pino agreed to a payment schedule proposed by his trade and fleet executives and accepted by Sovcomflot, the source said. But PDVSA – saddled with heavy bond payments and billions of dollars in unpaid bills to oilfield services providers – was unable to make sufficient payments to avoid Sovcomflot’s unusually public debt-collection gambit.

“Hostage” situations such as this one are rare: detentions of oil cargoes have been unusual because creditors rarely have sufficiently detailed information on tanker movements to obtain timely court orders.

Furthermore, since Venezuela also tends to ensure that any cargoes that leave its ports legally belong to the clients rather than to PDVSA – meaning they are rarely in a position to be seized – suggests that either the company made a rookie contractual error or it can’t even afford to buy insurance on its cargo. Additionally, the Sovcomflot dispute was unique in that the creditors are the tanker owners. Although the crude onboard the NS Columbus had already been sold to Norway’s Statoil, the cargo was being carried in a tanker navigating with a bill of lading under PDVSA’s name, according to two inspectors and a representative of one of the companies involved.

Meanwhile, the liquidity crisis at PDVSA, not to mention the economic crisis in Venezuela, has spiraling so far out of control, that the nation with the world’s largest oil reserves recently raged after a gasoline shortage developed in its capital of Caracas.

end

6 .GLOBAL ISSUES

Reuters: Toronto Canada

Government officials meet in Toronto trying to solve the biggest bubble ever created in real estate

(courtesy Reuters)

Canada, Ontario face hard choice as Toronto home bubble builds

Officials from Canada and its most populous province will meet on Tuesday to bring Toronto’s hot housing market to heel, under pressure from voters angry that speculators or foreigners are fueling a bubble in Canada’s largest city.

While no immediate action is expected from the gathering of Sousa and Toronto Mayor John Tory, the first concerted effort to Finance Minister Bill Morneau, Ontario Finance Minister Charles rein in Toronto house prices, all three are pushing for policy options to cool prices without crashing the market.

Toronto prices rose 33 percent in March from a year earlier and the average price of a detached home surpassed C$1.2 million ($903,000) last month, sparking warnings from Bank of Canada Governor Stephen Poloz last week that speculation is likely at play.

Sousa and Morneau have jockeyed back and forth over who is responsible for the increasingly feverish market, and appear at odds over whether a tax on speculation or foreign investment is the best approach.

“Everyone is worried: what if this is the measure that crashes the market?” said John Andrew, director of Queen’s University Real Estate Roundtable.

In the end, it may be voter anger that drives Sousa to act first, with the provincial Liberal government suffering in opinion polls and measures to address “affordability” already promised in his April 27 budget.

“You’re looking to raise your family and grow in the community and you’re being outbid and outpriced by people that are just using it as a commodity,” said Fred Altbaum, 34, a marketing professional struggling to buy a home with his wife and daughter.

Like many others, Altbaum is calling for either a foreign buyers tax – like the one imposed in Vancouver in August – or a change to capital gains taxes to discourage investors from flipping properties.

A foreign buyers tax will slow but not stop money coming from Chinese investors, said real estate broker Tony Ma, whose HomeLife Landmark Realty Inc is one of the largest brokerages in Toronto serving buyers of Chinese descent.

But even Ma, who said only 5 to 8 percent of the 10,000 deals his 1,100 agents did last year involved foreign investors, thinks it is time for the government to do something about the housing bubble.

“Prices have jumped too fast … anything over a 10 (percent) increase is an overheated market. As a broker nobody likes it – every night you are a loser (in a bidding war),” said Ma.

(Writing by Andrea Hopkins in Ottawa; Editing by Chizu Nomiyama)

7. OIL ISSUES

Oil slides after the market realizes that the Saudis will not extend their production cuts due to the increase in shale production from the uSA

(courtesy zero hedge)

Oil Slides After Saudis Unexpectedly Cast Doubt On Production Cut Extension

One week after “unnamed sources” reported that Saudi Arabia had backed the proposed 6 month extension to oil production cuts, this morning oil is lower after the world’s biggest oil producer appeared to backtrack on its trial balloon from last week, when Saudi Arabia’s energy minister said it is “too early” to decide whether OPEC will extend its crude-production-cutting agreement for the rest of the year.

Quoted by the WSJ, Khalid al-Falih, told reporters in Riyadh Monday that “it is premature to talk about extending the cut.” OPEC’s 13 national ministers are scheduled to decide that question on May 25.

Falih’s unexpectedly cautious tone “has taken some of the wind out of the bulls’ sails,” according JBC analysts.

It wasn’t just the sudden Saudi retiscence: as the WSJ adds, Falih’s comments were among a range of factors keeping pressure on oil prices, chief among them that U.S. drilling is now set to increase by 123,000 barrels a day in May, according to the U.S. Energy Information Administration, the steepest monthly rise since February 2015. The EIA figures are the latest sign that U.S. companies have been quick to increase production because of higher prices and has “added another bearish element to the market,” said JBC analysts.

A surge in U.S. production is a major threat to OPEC’s effort to reset the still-oversupplied global oil market. The U.S. oil rig count has been on the rise 13 weeks and now stands at its highest level in two years, according to oil-field services firm Baker Hughes Inc. The number of U.S. active drilling rigs rose again last week—by 11 to 683.