Gold: $1281.40 DOWN $10.30

Silver: $18.14 DOWN 12 cents

Closing access prices:

Gold $1280.00

silver: $18.16!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1294.53 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1287.15

PREMIUM FIRST FIX: $7.38

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1290.60

NY GOLD PRICE AT THE EXACT SAME TIME: 1284.35

Premium of Shanghai 2nd fix/NY:$6.25

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1282.05

NY PRICING AT THE EXACT SAME TIME: $1282.40

LONDON SECOND GOLD FIX 10 AM: $1279.05

NY PRICING AT THE EXACT SAME TIME. 1284.40 ??????

For comex gold:

APRIL/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR: 666 FOR 66600 OZ (2.0715 TONNES)

For silver:

For silver: APRIL

86 NOTICES FILED TODAY FOR 430,000 OZ/

Total number of notices filed so far this month: 830 for 4,150,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

The open interest in silver continues to advance with today’s reading just UNDER 228,000 contracts (227,984 contracts/a new record) or about 4000 contracts ABOVE the record set last year AND 200 CONTRACTS ABOVE THE RECORD SET YESTERDAY. It seems that the boys want to attack our precious metals as they are quite nervous about silver and its gigantic high OI for the front month of May.

I wrote the following last night:

“Tonight’s open interest for gold should rise by about 2,000 contracts. The silver OI should fall because the price fell by 24 cents. A rise will cause migraines galore for our bankers.”

I guess I was right about the migraines as they attacked again today.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY 209 contracts UP to 227,984 WITH THE HUGE FALL IN PRICE ( 24 CENTS) WITH RESPECT TO YESTERDAY’S TRADING. THE HEDGE FUNDS (MANAGED MONEY) CONTINUE TO REMAIN STEADFAST WITH THEIR POSITIONS ON DOWNDRAFT DAYS LIKE YESTERDAY WHILE ADDING TO THEIR LONGS ON GOOD DAYS. THE BANKERS ARE DESPERATELY TRYING TO COVER THEIR EVER BURGEONING SHORTS (OVER 555 MILLION OZ) BUT TO NO AVAIL. In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.139 BILLION TO BE EXACT or 163% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 86 NOTICE(S) FOR 430,000 OZ OF SILVER

In gold, the total comex gold FELL BY 1194 contracts DESPITE THE SMALL RISE IN THE PRICE OF GOLD ($2.30 with YESTERDAY’S TRADING). The total gold OI stands at 472,263 contracts.

we had 8 notice(s) filed upon for 800 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had A BIG changes in tonnes of gold at the GLD: A DEPOSIT OF 11.84 TONNES OF GOLD

Inventory rests tonight: 860.76 tonnes

.

SLV

We had A HUGE change in silver inventory at the SLV today/ A WITHDRAWAL OF 1.893 MILLION OZ/

THE SLV Inventory rests at: 326.308 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 209 contracts UP TO 227984, A NEW COMEX RECORD WITH THE FALL IN SILVER YESTERDAY (24 CENTS). We no doubt had some attempted short covering which badly failed as the longs keep piling on making it difficult for them to cover and overpowered the bankers. Our managed money sector (the hedge funds) continue to remain steadfast in their conviction as they added to their positions again with yesterday’s attempted raid. In gold, the open interest FELL by 1194 contracts DESPITE the accompanying rise in price by $2.30

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 25.45 POINTS OR 0.79%/ /Hang Sang CLOSED DOWN 337.12 POINTS OR 1.39%. The Nikkei closed UP 63.33 OR 0.35% /Australia’s all ordinaires CLOSED DOWN 79%/Chinese yuan (ONSHORE) closed UP at 6.8837/Oil DOWN to 52.19 dollars per barrel for WTI and 54.75 for Brent. Stocks in Europe CLOSED DEEPLY IN THE RED ..Offshore yuan trades 6.8817 yuan to the dollar vs 6.8837 for onshore yuan. NOW THE OFFSHORE IS SLIGHTLY WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY STRONGER AND THE OFFSHORE YUAN STRONGER TO THE ONSHORE AND THIS IS COUPLED WITH THE WEAKER DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA

China warns that the next likely test for North Korea is April 25.2017.

(courtesy zerohedge)

b) REPORT ON JAPAN

The central bank of Japan is targeting the 10 yr yield to .10%. Strangely last night, that yield dropped into the negative column at -.003%, Seems another central bank failure trying to stop deflation from gripping Japan.

( zero hedge)

c) REPORT ON CHINA

i)As the dollar weakens, China is easing capital controls. Watch for more uSA dollars to leave China.

( zero hedge)

ii) Much of China’s shadow banking sector is fraud built on fraud. Today 150 investors are in full rage as they found out that their money is gone after China’s largest Bank Minsheng banking Corp has found itself in a 3 billion fraud fraud case. A bank chief in Beijing issued false bank acceptance bills and then he secured the funds from individual sectors to cover up the misdeed.

(courtesy zero hedge)

4. EUROPEAN AFFAIRS

UK general election is set for June 8

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

Another flip: Trump tells Congress that Iran is compliant with their nuclear deal. However there is movement by the Trump team to end this lousy deal.

( zero hedge)

ii) RUSSIA/USA

6 .GLOBAL ISSUES

7. OIL ISSUES

i)Surprise gasoline build with a huge crude production 20th month highs sinks oil this morning;

( zerohedge)

ii)Then late this afternoon crude and gasoline prices plunge:

( zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

i)Gold trading:

another 3 billion in notional sold ahead of the London fix:

( zerohedge)

( zero hedge)

iii)Murphy interviewed by Kennedy Financial

( GATA)

iv)John Embry highlights the 22,000 contracts of gold dumped in 22 minutes yesterday and that process failed

( John Embry/Kingworldnews)

( New York Sun/Ron Paul)

vi) Now this makes sense!! Russia’s largest bank Sberbank is going to facilitate direct gold trading between Russia and India

( Russia insider)

10. USA stories

i)David Stockman talks about the upcoming economic disaster we are facing

(David Stockman/Craig Wilson/DailyReckoning)

ii)We now have Goldman Sachs pouring cold water on trump’s fiscal stimulus plan exactly how David Stockman envisioned it

( Goldman Sachs/zero hedge)

iii)As we have outlined to you on many occasions, the plunging used car prices are playing havoc to the industry. Look at what is going on with respect to rental car bond holders

( zero hedge)

iv)The truth behind the chemical attack two weeks ago

( Daniel Lang/SHTFplan.com)

Let us head over to the comex:

The total gold comex open interest FELL BY 1,994 CONTRACTS UP to an OI level of 472,263 DESPITE THE RISE IN THE PRICE OF GOLD ( $2.30 with YESTERDAY’S trading). The bankers again were certainly not shy in supplying the necessary paper to our newbie longs. We are now in the contract month of APRIL and it is one of the BETTER delivery months of the year. In this APRIL delivery month we had A LOSS OF 166 contract(s) FALLING TO 930. We had 26 notices served yesterday so we LOST 140 contracts or 14,000 oz will NOT stand for delivery in the active delivery month of April AND THESE GUYS WITHOUT A DOUBT WERE CASH SETTLED THROUGH THE OBSCURE EFT ROUTE DESCRIBED BY JAMES TURK.

At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month LOST 29 contract(s) and thus its OI is 2265 contracts. The next big active month is June and here the OI FELL by 3453 contracts UP to 341,968.

We had 8 notice(s) filed upon today for 800 oz

We are in the NON active delivery month is APRIL Here the open interest GAINED 0 contracts REMAINING AT 86 contracts. We had 0 notices filed yesterday so we neither gained nor lost any silver ounces standing and nothing was lost through the EFP route.

The next active contract month is May and here the open interest LOST 13,486 contracts DOWN to 111,262 contracts which is astonishingly high. It is this front month that the crooked bankers are targeting as they must be frightened to see such a mammoth amount of contracts still standing for metal. Also remember that Good Friday was much earlier last year: we have only 7 trading days before first day notice. The non active June contract GAINED 31 contracts to stand at 217. The next big active month will be July and here the OI gained 12,803 contracts up to 83,997

FOR COMPARISON SAKE, ON APRIL 19/2016 WE HAD 92,381 CONTRACTS STANDING FOR DELIVERY. SO YOU CAN VISUALIZE FOR YOURSELF THE HUGE DIFFERENCE BETWEEN 2016 AND THIS YEAR.

For those keeping score, the initial amount of silver oz that stood for delivery for the May 2016 contract month: 28.01 million oz. By conclusion of the month only 13.58 million oz stood and the rest was cash settled.(EFP ROUTE)

.

We had 86 notice(s) filed for 430,000 oz for the APRIL 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 244,002 contracts which is good.

Yesterday’s confirmed volume was 295,360 contracts which is very good.

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

16,075.000 oz

Scotia

500 kilobars

|

| Deposits to the Dealer Inventory in oz | 99.935 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

8 notice(s)

800 OZ

|

| No of oz to be served (notices) |

922 contracts

92,200 oz

|

| Total monthly oz gold served (contracts) so far this month |

666 notices

66600 oz

2.0715 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 451,966.5 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 5 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

611,453.910 oz

SCOTIA

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

611,453.910 oz

JPMorgan

|

| No of oz served today (contracts) |

86 CONTRACT(S)

(430,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(nil oz)

|

| Total monthly oz silver served (contracts) | 830 contracts (4,150,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 10,834,213.1 oz |

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz stood as bankers needed much silver to fill major holes elsewhere.

NPV for Sprott and Central Fund of Canada

will update later tonight the central fund of Canada figures

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

I will update gold inventory and silver inventory (GLD and SLV) at 11 pm tonight.

And now the Gold inventory at the GLD

April 19/A HUGE 11.84 TONNES ADDED INTO THE GLD INVENTORY/INVENTORY RESTS AT 860.76 TONNES

April 18/no changes at the GLD/Inventory remains at 848.92 tonnes

April 17/no changes at the GLD/Inventory remains at 848.92 tonnes

April 13/a deposit of 6.51 tonnes into the GLD/Inventory rests at 848.92 tonnes

this no doubt is a paper deposit/

APRIL 12/no changes in gold inventory at the GLD/Inventory rests at 842.41 tonnes

April 11/a huge deposit of 4.12 tonnes into inventory/Inventory rests at 842.41 tonnes

this would no doubt be a paper gold entry. It would be difficult to find that amount of physical gold.

April 10/1.77 tonnes added into inventory at the GLD/inventory rests at 838.29 tonnes

April 7/a small withdrawal of .28 tonnes from the GLD/Inventory rests at 836.49 tonnes

April 6/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 5/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 4/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 3.2017: a huge deposit of 4.45 tonnes of gold into the GLD/Inventory rests at 836.77 tonnnes

March 31/another withdrawal of 1.19 tonnes of gold inventory fro the GLD/this inventory would no doubt be heading for Shanghai/GLD inventory: 822.32 tonnes

March 30/no changes in gold inventory at the GLD/Inventory rests at 833.51 tonnes

March 29/a withdrawal of 1.78 tonnes of gold out of the GLD/Inventory rests tongith at 833.51 tonnes

March 28/this is good!! A deposit of 2.67 tonnes of gold into the GLD/Inventory rests at 835.29 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory rests at 832.62 tonnes

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

end

Now the SLV Inventory

April 19/A WITHDRAWAL OF 1.893 MILLION OZ FROM ITS INVENTORY/INVENTORY RESTS AT 326.308 MILLION OZ.

April 18/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 17/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 13/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 12/no changes in inventory at the SLV/Inventory rests at 328.201 million oz/

April 11/a paper deposit of 11.131 million oz into the SLV/no doubt yesterday’s entry of a withdrawal of 11.231 million oz was in error/328.201 million oz

April 10/ a paper withdrawal of 11.231 million oz of silver from the SLV and this silver was used in the raid today. Inventory rests at 317.231 million oz

April 7./ a withdrawal of 947,000 oz of silver from the SLV/Inventory rests at 328.201 million oz.

April 6/a tiny withdrawal of 136,000 oz of silver from the SLV/Inventory rests at 329.148 million oz

April 5/ a withdrawal of 1.042 million oz from the SLV/Inventory rests at 329.284 million oz

April 4/no change in inventory at the SLV/Inventory rests at 330.326 million oz/

April 3.2017; a withdrawal of 568,000 oz from the SLV/Inventory rests at 330.326

million oz/

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

END

Gold trading:

another 3 billion in notional sold ahead of the London fix:

(courtesy zerohedge)

Gold Slammed For Second Day As ‘Someone’ Panic Dumps $3 Billion Notional Ahead Of London Fix

Yesterday, ahead of the London Fix, Gold was monkeyhammered lower on yuuge volume, only to rip back higher.

Today, having failed to keep the precious metal down (25,000 contracts dumped in a minute), they went for it again with a $3 billion notional pummeling in futures…

And the dollar is deja vu-ing too…

end

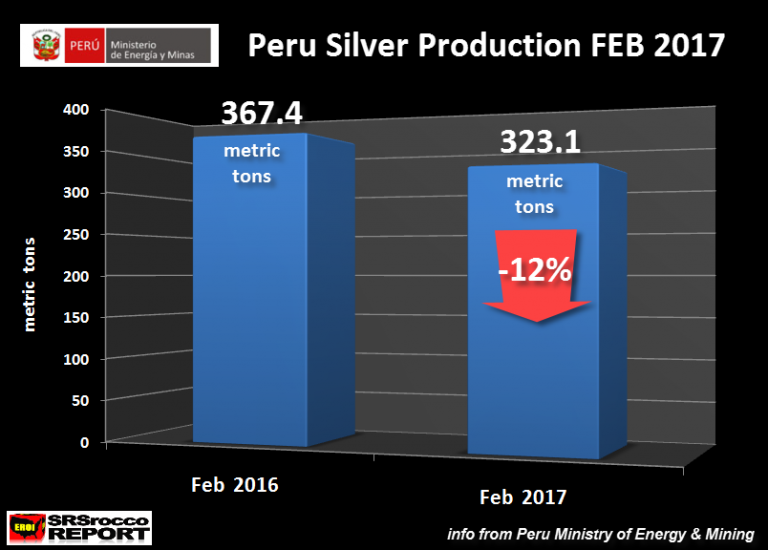

Silver Production Has “Huge Decline” In 2nd Largest Producer Peru

Silver Production Has “Huge Decline” In 2nd Largest Producer Peru

– Silver production sees “huge decline” in Peru

– Production -12% in one month in 2nd largest producer

– Silver decline is due to ‘exhaustion of reserves’ in Peru

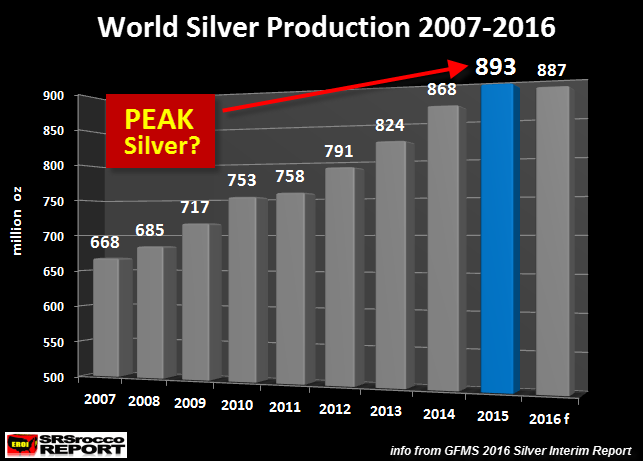

– GFMS recognise that ‘Peak Silver’ was reached in 2015

– Global silver market had large net supply deficit in 2016

– Silver rallied 13.5% in Q1 in 2017

– Base metal production accounts for 56% of silver mining

– Base metal demand under threat from global economy

– Own financial insurance of silver coins and bars

Investors and silver stackers should position themselves for falling silver production around the globe. Peru has just posed another 12% fall in silver production – Peak Silver is here.

SRSrocco Report has drawn attention to falling silver production in Peru and how this is likely to be echoed across the globe in the wake of the looming debt crisis in an article published yesterday.

The world’s second largest silver producer, Peru, has reported a 12% fall in February’s silver production to 323.1 metric tons, from the same period last year.

As written about in SRSrocco’s report on the matter, Peru’s ‘silver production fell 12% to 323.1 metric tons (mt) this February versus 367.4 mt the same month last year.’

The author calculates that this is a fall of 1.5 million ounces (44mt) in just one month. The Peruvian Ministry of Energy and Mining explains the fall:

The decrease is explained by the lower results (-23.53%) of the main producer: Minera Yanacocha S.R.L. Whose operations in Cajamarca have been affected by an exhaustion of the reserves in the current deposits in operation.

Both GoldCore and SRSrocco have been bringing the issue of Peak Silver to the word’s attention. Concern regarding Peak Silver has yet to impact the silver market in a material way.

In 2016 the uptick in demand for silver was (according to GFMS) primarily due to safe haven demand but also due to ‘swelling concern about mine supply reduction in the future.’

This latest set of data from Peru confirms the declining situation regarding global silver supply. The situation in Peru is not unique, it is a story that will likely appear in many silver producing countries.

The story will not be about defining silver production because of silver price but because of its place in the much wider global economy – the impact of base metal mining, falling energy fuel levels and the damage the debt-laden economy will have on the sector.

Silver is a special metal – it is a hedging instrument, money and it is a valuable commodity. The nature of how it is mined means it is intricately tied to both the performance of the economy and other commodities.

Silver is 56% byproduct

Only 30% of silver is mined as a primary source, it is more often a byproduct of base metal production. 34% of silver production (in 2015) came from lead/zinc mining and 22% from copper.

According to the 2016 World Silver Survey, the biggest increase in silver production as a byproduct has come from copper mines, which saw a 7% increase 2015-2016.

Therefore, silver production is not just a matter of which mine is producing it and what the demand for the metal is at that time, but it is also affected by the global markets and their demand for the base metals. Base metal prices have taken significant hits in recent years thanks to the financial crisis and recently base metal prices have been falling as precious metal rose on concerns about economic growth and increased risk aversion.

Should copper demand decline, which it is likely to as we look ahead to an impending burst of the global debt bubble and slowing economic activity then silver production will also begin to fall.

An economic slowdown means reduced industrial demand for the base metals, which means some 56% of silver supply will be under threat.

Silver – an energy drain

We must also not forget that mining is not just about demand for the metals and their byproducts. It also takes a huge amount of energy to mine precious metals.

As SRSrocco explains in a November article, it takes a huge amount of fuel to produce base metals (and therefore silver).

…the Chilean Copper Commission stated in a 2014 report, that the country consumed 535 million gallons of liquid fuel to produce 5.7 million tons of copper. Thus Chile’s copper industry consumed 94 gallons of liquid fuel for each tonne of copper produced.

On the other hand, Pan American Silver burned 20.5 million gallons of liquid fuel to produce their 26.5 million oz of silver in 2015. Which means, each ounce of silver production took 0.80 gallons of liquid fuel. If we use Pan American Silver as a guide, then the 269 Moz of primary silver production in 2016 consumed 215 million gallons of liquid fuel. However, I would imagine the global primary silver production average is much less, more like 0.50 gallon per ounce of silver. So, we are talking about 135-150 million gallons of liquid fuel to produce all the primary silver in the world.

Now, the world produced a total of 18.4 million tons of copper in 2014. Taking Chile’s average of 94 gallons per tonne of copper produced and providing a conservative estimate of say 75 gallons per tonne for entire globe, then the world consumed roughly 1.4 billion gallons of liquid fuels to produce its copper in 2014.

This is about ten times the amount of fuel it took to produce all the primary silver production.

A financial collapse will see oil and energy fuels levels fall as there will be a global slowdown. Demand will fall as will production. Given what appears to be a rising cost in terms of the amount of energy used to mine base and precious metals, it is not a leap too far to estimate that silver production will fall further on account of falling energy stockpiles.

Physical silver deficit at 1.5 billion ounces

Falling mine supply means that there is a growing deficit in above ground silver stocks, as the demand for physical silver shows little respect for mining figures.

Since 2011 there has been an annual physical deficit of silver (the one exception was in 2012 when there was a surplus of just 2 million ounces). Between 2014 and 2015 the deficit grew by 60%. Since 2004 the total annual silver deficits are 1.5 billion ounces, judging by past World Silver Surveys.

This is exactly as it sounds, we are at Peak Silver and the situation is unlikely to improve. Even the mainstream is beginning to see and acknowledge it.

In the December release of the World Silver Survey GFMS stated:

• We estimate that mine supply peaked in 2015 and will trend lower in the foreseeable future.

• Declining total supply is expected to be a key driver of annual deficits in the silver market going forward.

Conclusion – Own silver coins and bars as insurance

We write ‘unlikely to improve’ but actually this depends on which side of the silver pile you’re on. In reality a declining silver supply is excellent for those who have chosen to invest in silver, it is also good news for those who are holding assets in silver mines as the product will be come increasingly sought after. A weak economy means more demand for safe havens, such as gold and silver bars and coins.

The factors that point towards declining silver supply – reduced economic activity, declining energy markets and weakening base metal markets – are all the same reasons to own it. Whilst GFMS might separate the safe haven demand from the demand for silver because of reduced mining levels, in truth they are one and the same thing. Investors are rushing to own silver because they know that it is a useful and very rare commodity and a valuable hedge and form of financial insurance.

When it comes to the base metals they suffer when they can no longer be ‘used’ by the booming economy. They have no role when the producing economy no longer needs them. Silver demand contrasts this. When the economy is no longer able to buy, sell, produce and grow things then we know that governments are in trouble. Silver still has a role – as a hedge and insurance.

Silver is a necessary safe haven during times of financial turmoil. During these times (as we see now) governments greatly increase the production of fiat paper and electronic money.

With silver, this cannot happen and this is why we should own safe haven silver coins and bars. A fall in silver production is beneficial sign and a positive fundamental both in terms of its price but also as an indication of its value vis a vis other assets.

Full article on SRSrocco Report

-END-

Maduro is contemplating swapping Venezuela’s last amount of gold (7.7 billion dollars worth ). I believe that this gold has already been hypothecated by Citibank

(courtesy zero hedge)

Maduro Preparing To Swap Venezuela’s Gold For Dollars

It was almost exactly two years ago when a cash-strapped Venezuela quietly conducted its first, little-noticed gold-for-cash swap with Citigroup, as part of which Maduro converted part of his nation’s gold reserves into at least $1 billion in cash courtesy of the US bank. As Reuters reported then, the motive was simple: convert $1 billion of the country’s gold into much needed dollars to fund imports and keep the economy from sinking. However, instead of selling the gold outright, a move which would have been met with a firestorm of protests from political opponents and allies alike, Maduro merely leased it to Citi instead.

Specifically, Venezuela provided 1.4 million troy ounces of gold to Citi in exchange for cash. And while Venezuela would have to pay interest on the funds, it got the key benefit of being able to maintain the gold as part of its foreign currency reserves. After all, the gold was “merely rehypothecated”, if only on paper, the actual physical gold would be transferred to an unknown vault of Citi’s choosing where it would become an asset effectively controlled by the bailed out US ban (there was a brief scare last July when Citi warned it would close the account of the Venezuela Central Bank, which prompted us to ask if Citigroup was about to confiscate $1 billion in Venezuela gold).

While it is still unknown if Citi did in fact confiscate a substantial chunk of Venezuela’s sovereign gold, what is worth noting is that even just two years ago, Venezuela was in far better economic and social shape than it is currently, which ultimately prompted Maduro’s choice of picking a swap instead of an outright sale of the country’s gold. Now, however, with hyperinflation rampant, with daily protests, many of which turn violent and deadly, and with the opposition set to unleash the “mother of all protests” on Wednesday even as Maduro has ordered the army to take to the streets, the president has far fewer qualms about preserving even the illusion of stability at this point. What he does need, however, is access to dollars, be it to pay Venezuela’s creditors, provide funds to the cash strapped state-owned energy company PDVSA, or simply to pay the army which is the only thing keeping the nation away from a revolution, and Maduro from facing a deadly endgame.

Which is why Maduro is about to do what he did two years ago, only on a vastly greater scale, and perhaps simply sell Venezuela’s gold outright.

That is the allegation made by Venezuela’s opposition, which according to Bloomberg has reached out to Wall Street banks to dissuade them from helping Maduro sell Venezuela’s $7.7 billion in gold reserves (as of February) With Venezuela’s foreign reserve hoard rapidly declining, gold now represents one of its most valuable assets; total foreign reserves stood at $10.3 billion on Monday, near a 15-year low

The letter sent by the opposition-led congress on Monday to top US banks, warns that Venezuela is going to try to stave off default by seeking to swap its gold reserves into cash, and any investment bank that helps will be effectively “supporting a government recognized by the international community as dictatorial.” Furthermore, lawmakers also approved a measure today that they say would nullify any government debt issuance, as well as any debt swaps and pledges of gold as collateral, not explicitly approved by congress.

“The national government, through the central bank, is going to try to swap gold held as reserves for dollars to stay in power unconstitutionally,” according to the letter signed by National Assembly President Julio Borges. “I have the obligation to warn you that by supporting such a gold swap you would be taking actions favoring a government that’s been recognized as dictatorial by the international community.”

Lawmaker Angel Alvarado, a member of the National Assembly’s Finance Committee, said the letter has gone to banks including Citigroup Inc., Goldman Sachs Group Inc. and Bank of America Corp.

Meanwhile, as Maduro rides a wave of anger over triple-digit inflation and chronic shortages of basic staples, investors are trying to determine the odds that the country will continue servicing its debt amid a dollar shortage worsened by the collapse in oil prices.

And speaking of Maduro, on Tuesday evening, speaking on state television the president said he would make declaration later Tuesday. “I will reveal tonight the right wing’s complete plans for the coming days and I will make a special declaration so the republic is alert,” Maduro said, adding that supporters should be alert to “defeat the coup d’etat and intervention.” And then, moments ago, Maduro accused opposition leader Borges of calling for a coup.

As a reminder, we reported yesterday that Maduro has ordered the army into the streets as the insolvent nation braces for what the opposition has vowed will be the “mother of all protests” on Wednesday.

Whatever the outcome of tomorrow’s protest, or Maduro’s upcoming gold lease or sale, one thing is certain: Hugo Chavez, who spent the last years of his life repatriating Venezuela’s gold is spinning in his grave.

end

Murphy interviewed by Kennedy Financial

(courtesy GATA)

GATA Chairman Murphy interviewed by Kennedy Financial and Future Money Trends

Submitted by cpowell on Tue, 2017-04-18 11:50. Section: Daily Dispatches

7:49a ET Tuesday, April 18, 2017

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy has just done two interviews about the battle in the gold market between governments and market forces.

The first is with market analyst Philip Kennedy of Kennedy Financial. It’s 25 minutes long and begins at the 18:45 mark at You Tube here:

https://www.youtube.com/watch?v=m3o-uebhzXM

The second is with Dan Ameduri of Future Money Trends. It’s 15 minutes long and can be found here:

https://www.futuremoneytrends.com/trend-videos/interviews/theres-gold-ca…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

John Embry highlights the 22,000 contracts of gold dumped in 22 minutes yesterday and that process failed

(courtesy John Embry/Kingworldnews)

Today’s dumping of paper gold failed, Embry tells KWN

Submitted by cpowell on Tue, 2017-04-18 18:56. Section: Daily Dispatches

2:56p ET Tuesday, April 18, 2017

Dear Friend of GATA and Gold:

Sprott Asset Management’s John Embry, interviewed today by King World News, discusses this morning’s attack on gold with the dumping of $3 billion in contracts on the futures market, an attack that nevertheless seems to have been repelled. Embry’s comments are excerpted at KWN here:

http://kingworldnews.com/john-embry-3-billion-paper-gold-selling-scam-ba…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ron Paul questions why does the IMF insist that a nation’s currency cannot be connected to gold

(courtesy New York Sun/Ron Paul)

New York Sun: Ron Paul’s IMF question emerges in sharp relief in the era of Trump

Submitted by cpowell on Tue, 2017-04-18 19:02. Section: Daily Dispatches

From The New York Sun

Tuesday, April 18, 2017

If the International Monetary Fund does nothing else at its meeting that starts Thursday in Washington, it would be nice to see it — or someone — answer the Ron Paul question: Why do its articles of agreement actually prohibit members from linking their currencies to gold?

To those who didn’t know the IMF prohibits member countries from linking their currencies to the classic measure of monetary value, no need to feel abashed. One of the savviest envoys America ever sent to the IMF just told us that he himself was nonplussed to discover that fact.

It cries out for an explanation in the wake of the election of a president who, in Donald Trump, campaigned on the notion that bringing back the gold standard would be “wonderful.” Particularly because Congress is wrestling with the question of monetary reform. …

… For the remainder of the commentary:

http://www.nysun.com/editorials/ron-pauls-imf-question-emerges-in-sharp-…

END

Boy, do these guys flip: Mnuchin states that Trump is not trying to talk down the dollar

(courtesy Reuters/GATA)

Trump ‘absolutely not’ trying to talk down dollar, Treasury’s Mnuchin says

Submitted by cpowell on Wed, 2017-04-19 11:02. Section: Daily Dispatches

By David Milliken

Reuters

Wednesday, April 19, 2017

U.S. President Donald Trump is “absolutely not” trying to talk down the strength of the dollar, Treasury Secretary Steven Mnuchin was quoted as saying in the Financial Times today.

Trump said last week in an interview with the Wall Street Journal that the dollar was “getting too strong,” and backed away from labelling China a currency manipulator.

Mnuchin had played down that comment on the dollar in an interview first published late on Monday in the FT. In a more detailed version published on Wednesday, he directly rejected the idea that Trump was trying to talk down the dollar, saying, “Absolutely not, absolutely not.” …

… For the remainder of the report:

http://www.reuters.com/article/us-usa-trump-mnuchin-idUSKBN17L0PF

END

Now this makes sense!! Russia’s largest bank Sberbank is going to facilitate direct gold trading between Russia and India

(courtesy Russia insider)

Russia’s Largest Bank to Facilitate Direct Gold Trade Between Russia and India

Sberbank says direct gold trade between the two BRICS members would be immensely beneficial to both countries bypassing the dollar — one gold bar at a time

Sberbank is looking to finance the direct import of gold to India, according to Aleksei Kechko, Managing Director of Sberbank’s Indian subsidiary.

Sberbank is Russia’s largest, state-owned bank.

The announcement comes as no surprise to those who have been following the gold-buying spree by BRICS members, especially Russia and China.

Direct gold trade between India and Russia would be immensely beneficial to both countries. “We hope to sign the transaction by September or October this year,” [Kechko] said. “We are also exploring the possibility of entering the gold loans sector as well.”

India is the world’s second largest importer of gold. The country imported $35 billion worth of gold in 2015. However India’s imports of the precious metal fell in 2016.

Russian officials have already signaled their desire to conduct transactions with BRICS nations using gold. On a visit to China last year, deputy head of the Russian Central Bank, Sergey Shvetsov, said that Russia and China are interested in facilitating more transactions in gold.

As we wrote last month, creating a BRICS “gold marketplace” would be an excellent way of bypassing the dollar while also using a valuable commodity that could be easily recycled for trade with other member nations.

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER 6.8863( REVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES STRONGER TO ONSHORE AT 6.8803/ Shanghai bourse DOWN 26.406 POINTS OR 0.81% / HANG SANG CLOSED DOWN 98.66 POINTS OR 0.41%

2. Nikkei closed UP 13.61 POINTS OR 0.07% /USA: YEN RISES TO 108.96

3. Europe stocks opened ALL MIXED ( /USA dollar index RISES TO 99.64/Euro DOWN to 1.0724

3b Japan 10 year bond yield: RISES TO +.011%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.96/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.53 and Brent: 54.99

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.198%/Italian 10 yr bond yield DOWN to 2.231%

3j Greek 10 year bond yield FALLS to : 6.68%

3k Gold at $1281.30/silver $18.21 (8:15 am est) SILVER ABOVE RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 10/100 in roubles/dollar) 56.15-

3m oil into the 52 dollar handle for WTI and 54 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.96 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9968 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0691 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.198%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.211% early this morning. Thirty year rate at 2.8711% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

European Stocks, Futures Rebound As Stronger Dollar Eases Haven Demand

European stocks rebounded after the biggest one-day drop since November, alongside S&P futures, while Asian equities posted modest declines after yesterday’s weak US close. Gold and yen slid, while the dollar gained on the latest Mnuchin comments to the FT according to which Trump was “absolutely not” trying to talk down the dollar.

European equities rose 0.4% in early trading, hinting at some cautious optimism following a day of risk off sentiment, and reversing the 0.6% fall in Asian equities outside Japan which dipped to a one-month low. U.K. shares initially traded lower as the pound held much of its gains following the surprise election announcement, however have since rebounded back to unchanged. Having dragged it lower on Tuesday after another major rout in China, commodity companies helped prop the Stoxx Europe 600 Index, which rebounded following the biggest one-day loss since November. Sterling pulled back slightly after reaching the strongest level since October on Tuesday. Oil fluctuated after dipping on yesterday’s API data which showed U.S. oil inventories fell 840,000 barrels last week, a lower than expected draw. On Wednesday official EIA data is expected to show a larger drop of 1.4 million barrels.

“Sterling rallied across the board yesterday on the back of Prime Minister May’s announcement of snap UK elections. The market interpreted the move as an effort to strengthen the prime minister’s majority and reinforce a more unified stance for the upcoming negotiations with the EU,” Unicredit analysts said in a note on Wednesday. “Geopolitical tensions are providing strong support to U.S. Treasuries … (and) in the euro zone Bunds are receiving support from the general decline in risk appetite and uncertainty related to the French presidential election.”

The flight to Treasury safety pushed JGB yields briefly back into the negative overnight, however modest selling in the complex has since seen the 10Y yield rebound back over 0.00%

As Bloomberg highlights in its overnight wrap, after declines on Tuesday, investors seem to be taking the addition of yet another macro risk in their stride. The U.K. vote joins a slew of elections to be held this year against a backdrop of rising populism in the Europe, while geopolitical tensions are simmering over both North Korea and Syria and the pace of monetary tightening in the world’s biggest economy looks uncertain. Meanwhile, the reflation trade has soured, with June rate hike odds dropping below 50% for the first time in two months.

Asian shares failed to benefit from the eventual rebound in risk sentiment, and the Shanghai Composite Index fell 0.8%, taking its four-day loss to 3.2%. The main Shenzhen market was also down a fourth day. The Hang Seng Index slid 0.4 percent and the Hang Seng China Enterprises Index dropped below the 10,000 level for the first time in two months. Japan’s Topix index was little changed, while Australia’s S&P/ASX 200 Index lost 0.6 percent and South Korea’s Kospi index fell 0.5 percent.

Risk was firmer in Europe, where the Stoxx Europe 600 increased 0.3% as of 10:10 a.m. in London, after dropping 1.1% on Tuesday.

In the US, S&P futures rose 0.3% offsetting yesterday’s 0.3% drop in the cash market. IBM slumped in after-hours U.S. trading after its 20th consecutive quarterly sales decline.

Sterling was just off a six-month peak against the dollar above $1.28 having surged when British Prime Minister Theresa May called an early general election for June 8, seeking to strengthen her party’s majority ahead of Brexit negotiations.

The dollar was undermined in part by an eroding interest rate advantage as U.S. bond yields dived to five-month lows. Yields on 10-year Treasury paper sank to 2.17%, far away from the 2.629% peak seen in March. They were last up slightly on the day at 2.20%.

A run of disappointing U.S. economic data and doubts that the Trump administration will progress with tax cuts have quelled expectations of faster inflation and boosted fixed-income debt. That, in turn, has taken the steam out of Wall Street. The Dow fell 0.55 percent on Tuesday, while the S&P 500 lost 0.29 percent and the Nasdaq 0.12 percent. Goldman Sachs lost 4.7 percent in the largest daily drop since June after its earnings missed expectations as trading revenue dropped.

In commodity markets, profit taking nudged gold down 0.4 percent to $1,287.10 an ounce, and away from Monday’s peak of $1,295.42. Oil prices slipped as U.S. crude stockpiles fell by less than expected and a U.S. government report said shale oil output in May was likely to post the biggest monthly increase in more than two years

Economic data include weekly mortgage applications. Scheduled earnings include U.S. Bancorp, Qualcomm, Morgan Stanley.

Bulletin Overnight Summary from RanSquawl

- European equities trade modestly higher ahead of further notable earnings from the US with macro newsflow from the EU session relatively light

- Across FX markets, GBP has given back some of its gains against the greenback after having met resistance at 1.2920 to move within proximity to the 1.2800 level

- Looking ahead, highlights include DoEs, Fed’s George, Rosengren and ECB’s Coeure

Global Market Snapshot

- S&P 500 futures up 0.3% to 2,343.00

- STOXX Europe 600 up 0.4% to 377.49

- MXAP down 0.5% to 145.52

- MXAPJ down 0.6% to 473.43

- Nikkei up 0.07% to 18,432.20

- Topix down 0.01% to 1,471.42

- Hang Seng Index down 0.4% to 23,825.88

- Shanghai Composite down 0.8% to 3,170.69

- Sensex up 0.05% to 29,333.48

- Australia S&P/ASX 200 down 0.6% to 5,804.01

- Kospi down 0.5% to 2,138.40

- German 10Y yield rose 2.1 bps to 0.177%

- Euro down 0.1% to 1.0718 per US$

- Brent Futures up 0.1% to $54.95/bbl

- Italian 10Y yield fell 5.6 bps to 1.966%

- Spanish 10Y yield fell 0.9 bps to 1.661%

- Gold spot down 0.6% to $1,282.57

- U.S. Dollar Index up 0.2% to 99.70

Top Overnight News from Bloomberg

- Fed June Hike Odds Below 50% After Inflation Expectations Tumble

- Markets Start to Ponder the $13 Trillion Gorilla in the Room

- IBM Sales Miss Shows Return to Growth Not Without Roadblocks

- Trump Mulls Military Options for North Korea. They’re All Grim.

- European Car Sales Surge 11% as Fiat, Renault Lure Buyers

- Currency Traders Spot Fatal Flaw in Republicans’ Border Tax Plan

- Ford’s Schoch Sees ‘Strong 2017’ in China

- Maserati CEO Bigland Seeing No Signs of Any China Sales Slowdown

- Nasdaq Seeks German Power Futures Amid Potential Market Split

- Goldman Sachs Australia’s Steve Maartensz Said Leaving Bank

- Havertys to Name Richard B. Hare as CFO

- KKR, Stone Point Buy Wealth Management Firm Focus Financial

- American Air Wins Arbitration Over Flight Attendant Pay Raise

Asian equity markets traded negative following a weaker lead from Wall Street, where disappointing earnings from the likes of IBM, Johnson & Johnson and Goldman Sachs dampened sentiment. This resulted in early pressure in Nikkei 225 (Unch.) and ASX 200 (-0.5%) with weakness in financials and commodities leading the declines in the latter. Shanghai Comp (-0.8%) and Hang Seng (-0.4%) also conformed to the downbeat tone observed across their global counterparts amid mild increases in Chinese money market rates, with the PBoC’s liquidity operations failing to provide an uplift. 10yr JGBs traded higher as participants sought after safer assets due to the dampened tone in the region, while the 10yr yield declined to 0% which was its lowest since November.

PBoC injected CNY 40bIn 7-day reverse repos, CNY 20bIn in 14-day reverse repos and CNY 20bIn in 28-day reverse repos.

Top Asian News

- China’s $8.5 Trillion Shadow Bank Industry Is Back in Full Swing

- Jakarta’s Chinese Christian Governor Trails in Run-off: Polls

- Samsung Heir’s Trial Homes in on Five Minutes With Ex- President

- Alcohol Ban Another Drain on India’s Weak State Finances

- Indian Stocks Fluctuate; TCS Is Biggest Drag on Sensex Benchmark

European markets have rebounded among an air of caution this morning with the Eurostoxx trading higher by a modest 0.3% as participants continue to digest yesterday’s news that PM May is to call a snap election for June 8th. Before that though, focus remains firmly on the 1st round of the tense French election, in which some polls indicate that Macron still holds a slight advantage over his nearest rivals (Le Pen, Fillon). In stock specific news, earning updates have been coming in thick and fast with AB Foods supported by strong results this morning, while Burberry notably underperforms after the retailer stated that revenue fell short of analyst expectations. In credit markets, prices had been subdued for much of the morning with Bunds relatively flat, however recent comments from ECB’s Hansson who noted that it is not too early to discuss ECB policy (change) has pressured the German benchmark in recent trade.

Top European News

- French Election Shocker: Pollsters Baffled by Four-Way Race

- Banks and Clients Tussle Over What It Will Cost to Read Analysts

- How May’s Election Bet Could Help Scots Independence Forces

- Pound May Top $1.30 on Short-Gamma Positioning, Charts: Analysis

- Michael Spencer’s NEX Group Plans Relocation in New York, London

- Burberry Sales Miss Estimates as New CEO’s Task Gets Tougher

- Germans Fly to U.S. Ready to Counter Trump’s Surplus Complaints

- Zalando Drops After Reporting Quarterly Profit to Miss Estimates

In currencies, the yen dropped 0.4 percent to 108.86 per dollar after gaining 0.5 percent Tuesday. The Bloomberg Dollar Spot Index rose 0.2 percent following a two-day decline. The pound dropped less than 0.1 percent to $1.2836 after its 2.2 percent surge Tuesday. The euro also slipped less than 0.2 percent. Cable has given back some of its gains against the greenback after having met resistance at 1.2920 to move within proximity to the 1.2800 level with markets now awaiting the Parliamentary confirmation for the go-ahead from yesterday’s announcement. Elsewhere, USD/JPY has continued to climb throughout the European session as geopolitical fears continue to abate, at least for the time being with the pair approaching 109.00 to the upside. Elsewhere, commodity currencies have been a touch softer this morning with USD/CAD tripping above 1.34, while there has been no respite for the AUD as we are back testing 0.7500 against the USD, but the flow looks to be going through AUD/NZD, which is now just below the 1.0700 mark. Finally, EUR has lost some modest ground to the broadly firmer USD with this morning’s inflation data from the Eurozone coming broadly in line with expectations.

In commodities, gold declined 0.5 percent to $1,282.84 an ounce after closing at the highest since November in the previous session. West Texas Intermediate crude oil was little changed at $52.43 a barrel, after two days of losses. Trade across the commodities complex remained uneventful with WTI crude futures only slightly pressured following a smaller than expected headline crude drawdown in the latest API Inventory Report. EU trade has seen some rhetoric from OPEC Sec-Gen Barkindo who said that March compliance data is showing higher conformity with supply cut pact but this has failed to provide too much traction for energy prices ahead of the US crossover. Elsewhere, gold (-0.2%) continued to pull back from 5-month highs as the USD attempted to nurse yesterday’s weakness, while copper found some reprieve and rebounded from 3-months lows.

Looking at the day ahead, this morning in Europe the only data due is the final CPI report for the Euro area where headline CPI is expected to come in at +0.8% mom and +1.5% yoy, and the core at +0.7% yoy. There is no data due in the US although we will get the Fed’s Beige Book while the Fed’s Rosengren is also due to speak. The ECB’s Coeure also speaks this afternoon in NY. Earnings wise, today we will get 16 S&P 500 companies including Morgan Stanley and eBay.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 1.5%

- 12:30pm: Fed’s Rosengren Speaks at Bard College Conference

- 2pm: U.S. Federal Reserve Releases Beige Book

* * *

DB’s Jim Reid concludes the overnight wrap

We were actually watching the news on TV last night after the surprise snap UK election decision. On this the biggest call out of DB over the last 24 hours was to reverse the 2 year bearish house view on Sterling immediately after the announcement yesterday. Our FX strategists argued last year that an early general election was the only way to resolve the political impasse the U.K. government faces in conducting Brexit negotiations. The 2020 General Election was a problem domestically (small dwindling majority likely forcing policy gridlock and compromises) and externally in as far as negotiating with Europe from a weak position in 2019 as the Brexit deadline approached.

The election on June 8th will likely result in a larger Conservative majority (see latest polls below). This should have three material implications, in their opinion. First, it makes the deadline to deliver a “clean” Brexit without a lengthy transitional arrangement by 2019 far less pressing given that no general election will be due the year after. Second, it will dilute the influence of MPs pushing for hard Brexit, strengthening the government’s domestic political position and allowing earlier compromise over key EU demands for a transitional arrangement. Third, it strengthens the PM’s overall negotiating stance who in recent weeks has clearly fallen in line with the European negotiating approach. This will involve a settlement of the Brexit payments and other divorce aspects first, to be followed by a lengthy transitional period during which the final outcome of Brexit will emerge. This sequenced approach materially reduces the “crash risk” of Brexit negotiations as well as strengthening the Prime Minister’s hand in pursuing an orderly (and very lengthy) withdrawal. All of the above in turn reduce downside risks for the U.K. growth outlook over Brexit negotiations. Our FX team will look to publish fresh targets in the coming days. In terms of the economic impact, DB’s Mark Wall believes that a larger government majority should also reduce Brexit-related downside risks. However, he hesitates from assuming much upside yet for economic growth or for BoE policy rates. Mark believes that the Conservatives are likely to campaign on an uncompromising “hard Brexit” message and the capacity to concede in negotiations in the EU will come later. He holds his 1.8% GDP growth forecast for 2017 and sees little upside relative to his 1.1% GDP forecast for 2018. A link to both reports can be found here.

Just on those polls, a snap online ICM poll released yesterday in the hours following the election announcement showed that, with a polling sample of 1000 people, support for the Conservatives stands at 46%, with Labour at 25% and the Lib Dems at 11%. The 3 polls prior to this (ICM, YouGov, ComRes) showed the Conservatives as holding an average 20% lead over Labour, so not too dissimilar. The FT poll tracker also shows the Conservatives as holding 43% of the support compared to 25% for Labour (or an 18% lead). The FT also references Electoral Calculus which predicts a Conservative majority of 130 seats in the 650-seat House of Commons. That compares with a working majority of just 17 seats currently.

Unsurprisingly the news of the snap election was initially most felt in FX with Sterling rallying immediately and closing 3 big figures higher or +2.20% at $1.284 – the highest level since October 3rd. That was the biggest rally for the Pound versus the Dollar since January 17th when PM May delivered what was largely considered a fairly balanced Brexit speech. That move in Sterling yesterday weighed heavily on UK equities with the FTSE 100 (-2.46%) ironically suffering its biggest one-day loss since the post-Brexit aftermath on June 27th. The index is also now back to within just 0.7% of the February lows. The big dollar earning blue-chips suffered most of all with some of the biggest losers including BHP (-5.59%), Glencore (-5.58%), BP (-3.93%), GlaxoSmithKline (-3.67%) and Antofagasta (-3.41%). In contrast the more domestically orientated FTSE 250 closed down just -1.16%. For me I have to weigh up whether the potential cheaper cost of my next iPhone purchase (never too far away) offsets my declining domestic share portfolio. It’s a close one!!!

There wasn’t much better news for risk assets outside of the UK yesterday either. In Europe the Stoxx 600 closed down -1.11% while last night the S&P 500 bounced back to pare its loss to a more modest -0.29%. One sector which notably underperformed was US Financials (-0.83%) which came after Goldman Sachs disappointed analysts with a miss at both the revenue and earnings lines following its Q1 report yesterday. In contrast to what we’ve seen with other US banks this reporting season – including BofA yesterday – the miss was largely as a result of disappointing performance in the FICC business. The other story in markets yesterday was the move in rates. In keeping with the largely risk-off tone but perhaps also reflecting the lingering geopolitical concerns and also the upcoming French presidential election this weekend to some degree, 10y Bund yields initially rallied 3.1bps to 0.153% for the lowest closing yield this year before 10y Treasuries then rallied 8.2bps to 2.169% for the lowest close since November.

This morning in Asia the majority of bourses are following the lead from Wall Street and Europe yesterday and are currently tracking lower. The Hang Seng (-0.74%), Shanghai Comp (-1.10%), Kospi (-0.50%) and ASX (-0.56%) are all in the red. It’s worth noting that materials names are underperforming, which isn’t a surprise given the moves for metals over the last 24 hours. Most notable is the latest leg lower for iron ore which fell another -4.60% yesterday and is now down over -33% from the February highs. Elsewhere, the Nikkei is currently little changed, helped by a slightly weaker Yen. US equity index futures are a touch higher however despite IBM reporting softer than expected sales figures after closing bell last night which saw shares tumble 5% in extended trading. Meanwhile in bond markets this morning the most notable move is that for JGB’s where the 10y (using the March-2027 maturity bond) has fallen below 0% (touching -0.005%) for the first time since mid-November. It’s worth adding that the BoJ today maintained the amount of 5y and 10y bond purchases in its regular bond buying exercise.

Yesterday we saw the latest CSPP numbers and it’s looking like I might have to say ‘I was wrong’ soon which are words a research analyst always struggles with. I thought that the ECB might taper corporate purchases alongside Government bonds but the early evidence suggests some evidence otherwise. However the ‘strong’ numbers of the last two weeks (post taper) might be slightly distorted by two pretty weak weekly numbers in March and the Easter break but the average daily purchases in the 4 business days last week of €423mn were comfortably above the daily average of €368mn since the program started. But if you average it over 5 days it goes down to €338mn/day. So until we see the full month’s purchases on May 2nd (two weeks time) we really can’t be sure. At that point the ECB will surely want to have signalled how they have split the taper. To be fair my colleague Michal has been more of the opinion that they’ll keep CSPP ‘stronger for longer’ than me. It’s important as for the last few months I’ve felt that although technicals have been strong for credit, the technicals for Bunds have been even stronger (see a recent Credit Bites for more https://goo.gl/XmY0dQ) thus creating headwinds for spreads. If the CSPP is staying ‘stronger for longer’ it will help redress that balance a little but it’s too early for this to be confirmed.

Away from that, yesterday’s macro data was largely a sideshow. In the US industrial production was confirmed as increasing +0.5% mom as expected with capacity utilization also edging up four-tenths to 76.1%. Manufacturing production did however decline -0.4% mom, led by the auto sector. Elsewhere, housing starts were confirmed as declining a relatively steep -6.8% mom (vs. -3.0% expected) although that was somewhat offset by a two percentage point upward revision to the February print to +5.0%. Building permits was reported as rising +3.6% mom (vs. +2.0% expected). Away from this, there was no data of note in Europe however we did get other economic news out of the IMF with the latest quarterly forecasts released. The fund revised its global growth forecast up one-tenth to 3.5% this year and left its 2018 forecast for 3.6% unchanged.

The forecast for the US was also left unchanged at 2.3% and 2.5% for this year and next. There was also a little bit of Fedspeak yesterday from Kansas City Fed President Esther George, although again it didn’t do much to move the dial. George said that “balance sheet adjustments will need to be gradual and smooth” and that “importantly, once the process begins, it should continue without reconsideration at each subsequent FOMC meeting”.

Looking at the day ahead, this morning in Europe the only data due is the final CPI report for the Euro area where headline CPI is expected to come in at +0.8% mom and +1.5% yoy, and the core at +0.7% yoy. There is no data due in the US although we will get the Fed’s Beige Book while the Fed’s Rosengren is also due to speak. The ECB’s Coeure also speaks this afternoon in NY. Earnings wise, today we will get 16 S&P 500 companies including Morgan Stanley and eBay.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 26.06 POINTS OR 0.81%/ /Hang Sang CLOSED DOWN 98.66 POINTS OR 0.41%. The Nikkei closed UP 13.61 OR 0.07% /Australia’s all ordinaires CLOSED DOWN 49%/Chinese yuan (ONSHORE) closed DOWN at 6.8863/Oil UP to 52.53 dollars per barrel for WTI and 54.99 for Brent. Stocks in Europe MIXED ..Offshore yuan trades 6.8808 yuan to the dollar vs 6.8863 for onshore yuan. NOW THE OFFSHORE IS SLIGHTLY WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY WEAKER AND THE OFFSHORE YUAN STRONGER TO THE ONSHORE AND THIS IS COUPLED WITH THE STRONGER DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

China warns that the next likely test for North Korea is April 25.2017.

(courtesy zerohedge)

April 25 Is “Highest Probability” Day For North Korean Nuclear Test China Warns

According to a report by Korea JoongAng Daily, China appears to be preparing measures in case North Korea tests a nuclear device or performs another provocation, including possibly suspending oil to the regime, and adds that relations between Beijing and Pyongyang appear frostier than ever before.

Additionally, the Korea publication references the Chinese-language Boxun News, which cites a Beijing source, according to whom Chinese President Xi Jinping attempted to send Wu Dawei, China’s special representative for Korean Peninsula affairs, to Pyongyang after his summit with U.S. President Donald Trump, but North Korean leader Kim Jong-un allegedly rejected Wu’s visit.

Boxun adds that it was unclear if North Korea did not conduct a sixth nuclear test last Saturday because of Beijing’s warning not to do so, however it adds that according to “analysts” there’s a high likelihood of a provocation on the 85th anniversary of the founding of the North Korean People’s Army next Tuesday and the days leading up to the South Korean presidential election on May 9.

Citing its Chinese source, Boxun said that “China believes there is the “highest possibility” of a nuclear test on April 25, but “does not leave out the possibility it might take action in early May.”

One assumes the Carl Vinson, wherever it may be in the world currently, will eventually make it to North Korea by then.

Meanwhile, South Korean officials cited by JoongAng Daily confirmed that Wu, China’s top nuclear envoy, during a visit to Seoul last week said he proposed to visit Pyongyang in person to persuade the North to refrain from further provocations but he was spurned.

Lu Chao, a Chinese expert on Korean studies at the Liaoning Academy of Social Sciences, was among multiple analysts that told the state-affiliated tabloid Global Times Tuesday that if North Korea did not refrain from conducting its sixth nuclear test, it would “definitely trigger” more intense United Nations sanctions, and that China will implement them.

Victor Cha, the Korea Chair at the Washington-based Center for Strategic and International Studies (CSIS), said the “provocation window” between South Korean elections and North Korean provocations has become narrower over time, referring to database collected over the past 60 years. That window refers to the proximity in time between a South Korean election and a provocative act by North Korea, meaning a nuclear or missile test.

Cha said such a pattern “suggests a provocation as early as two weeks” before the South Korean presidential elections on May 9. That two-week window overlaps with North Korea’s military foundation day on April 25.

* * *

Meanwhile, amid escalating military tensions in the region, the Chinese navy tested its new guided-missile destroyer, the Xining, in its first live-fire exercise conducted in the Yellow Sea, near the Korean Peninsula, broadcast on China’s state-run CCTV on Tuesday. The Xining, China’s Type 052D-class missile destroyer with was put into service by the People’s Liberation Army Navy in January.

The exercise, possibly warning against a North Korean military provocation, was reported to have lasted several days and comes as Beijing has called for North Korea to give up its nuclear ambitions under renewed pressure from the Trump administration. U.S. Vice President Mike Pence warned Monday in Seoul the “era for strategic patience is over.”

Trump has been lauding Beijing for helping with the Pyongyang situation, especially over sending back North Korean vessels bringing coal to a Chinese port. Trump told Fox News Tuesday in reference to Chinese President Xi Jinping, “He’s working so nicely that many coal ships have been sent back. Fuel is being sent back. They’re not dealing the same way. Nobody’s ever seen it like that.” As reported previously, in February, China announced it would suspend all coal imports from North Korea to the end of the year in accordance with a UN Security Council resolution.

Meanwhile, the Chinese Foreign Ministry Wednesday warned Pyongyang to exercise restraint on any actions that could heighten tension on the Korean Peninsula in response to Pyongyang’s recent bellicose rhetoric.

Lu Kang, a spokesman of the ministry, said at a briefing, “China objects to any words that could heighten tensions since the current situation on the Korean Peninsula is highly complicated and sensitive.” Within China, there is talk about playing a key card to pressure North Korea – cutting off oil supplies to the Kim Jong-un regime.

In an editorial last week, the state-run tabloid Global Times said that if Pyongyang engaged in further provocations, Chinese society would approve of “severe restrictive measures that have never been seen before, such as restricting oil imports to the North.” On Monday, the paper again called for China to cut off most oil supplies to North Korea if there was another nuclear test.

In an editorial Tuesday, it pointed out that China and U.S. cooperation is increasing over the North Korean problem, and that the possibility of dragging out the North Korea issue indefinitely has “decreased drastically.”

“North Korea and China are a blood alliance, interdependent like no other,” said a South Korean government official Tuesday. “But the atmosphere in China, which has left a back door open to North Korea regardless of the international community’s sanctions, is changing little by little.”

North Korea depends on China for some 90 percent of its crude oil supply.

Lee Gee-dong, head of the Strategic Team on North Korea at the Seoul-based Institute for National Security Strategy, said, “Though it may not be immediate, if North Korea conducts a strategic provocation such as a sixth nuclear test or launches an intercontinental ballistic missile (ICBM), Beijing will have to use the halting of oil exports card.” However, some analysts think the threat of cutting oil supplies to the North is mere rhetoric.

“In the 1990s, when the North Korea nuclear issue first escalated, China could have blocked oil then,” one former South Korean official said. “The oil supply card could be a performance by China to impress President Trump, but bears more watching.”

end

3b REPORT ON JAPAN

The central bank of Japan is targeting the 10 yr yield to .10%. Strangely last night, that yield dropped into the negative column at -.003%, Seems another central bank failure trying to stop deflation from gripping Japan.

(courtesy zero hedge)

Japan’s 10Y Yield Drops Below Zero Again: All Eyes On The BOJ

With every other asset class roundtripping the November election outcome, it was only a matter of time before Japan’s 10Y JGB – which on February 2 briefly peaked above the BOJ’s “yield curve controlling” 0.10% yield ceiling, rising as high as 0.15% to the shock of a market ready to declare that Japan had finally lost control of its bond market – retraced the entire “reflationary” move from 0.0% to 0.1%. And, sure enough, following today’s violent deflationary capitulation moments ago Japan’s JGB 0.1% of 2027 once again dipped back under 0%, sliding as low as -0.003% on Wednesday morning in Japan.

What happens next?

According to traders, focus will turn to whether the BOJ, in pursuing “yield curve control”, will reduce the amount of JGBs it monetizes. “Amid favorable environment for bonds, focus is on BOJ as whether there will be a reduction in purchase amounts will test the bank’s tolerance for 10-year yield falling into negative,” Katsutoshi Inadome, senior bond strategist at Mitsubishi UFJ Morgan Stanley Securities, wrote in note according to Bloomberg.

As a reminder, in the BOJ’s latest “rinban” or open market operation, it bought around 280bn yen of 1-to-3, 350bn yen of 3-to-5 and 450bn yen of 5- to-10-year maturities at previous operation. And material declines from these amounts may lead result in the market roiling again, on fears the BOJ is being forced into an involuntary taper by external deflationary forces.

Meanwhile, the USDJPY continues to track treasury yields tick for tick, and as Yujiro Goto, senior FX strategist at Nomura in London said, the “dollar/yen remains top-heavy with yields falling and weak U.S. economic data. It’s hard to take risk aggressively ahead of the French election, keeping it in 108-109 range.”

Which means that while continued declines in Japanese yields are virtually assured all else equal, it will be up to the BOJ to telegraph to the market just how low it will let the 10Y drop. Should Kuroda unveil another “taper”, the result may be the uncoordinated move in global bond markets, leading to a negative feedback loop of JGB selling and TSY bond buying, which incidentally is the worst case scenario for global central bankers whose primary intention over the past year has been to achieve as much rate coordination as possible.

END

3c) REPORT ON CHINA

As the dollar weakens, China is easing capital controls. Watch for more uSA dollars to leave China.

(courtesy zero hedge)

China Eases Capital Controls As Dollar Weakens

In discussing the key overnight news in an otherwise quiet session, JPM writes that “the most important headline was prob. the one concerning China loosening some currency outflow curbs” so focusing on that, Reuters, and SCMP before it, reports that after months of draconian and ever tightening capital control, China’s central bank has relaxed some of the curbs on cross-border capital outflows it put in place just months ago to shore up the yuan currency.

Specifically, as of last week, the People’s Bank of China (PBOC) is no longer demanding that banks match outflows with equal inflows, the sources said. The South China Morning Post first reported the relaxation of the capital controls earlier on Wednesday.

There was no immediate comment from the People’s Bank of China when contacted by Reuters. The State Administration of Foreign Exchange (SAFE) did not have an immediate response to Reuters’ questions on the SCMP report. While expectations of further yuan depreciation have eased in recent months, opening a window for authorities to relax recent measures, Beijing is not likely to let go totally, said Raymond Yeung, chief Greater China economist at ANZ in Hong Kong. In addition to checking exchange rate expectations, the authorities were also using capital controls to control where Chinese money flows, limiting investments in foreign sectors deemed undesirable, he noted.

“The current macro environment obviously favors an easing of the (rules on) fund flows, but that doesn’t mean that it is going to have solved the structural issue of the mismatch between the corporate desire to go out versus the central government’s centrally-driven approach when they talk about offshore investment,” Yeung said.

This first easing of capital flught measures comes as “China’s leaders and financial markets feel more confident that pressure on the yuan and the country’s foreign exchange reserves has diminished, thanks largely to a pullback in the surging U.S. dollar.” It also comes at a time when increasingly more Chinese companies have complained they are unable to consummate offshore M&A due to the PBOC’s limit on how much capital they can park offshore.

In March the U.S. owner of Dick Clark Productions Inc said that one of its affiliates terminated an agreement to sell assets to Chinese conglomerate Dalian Wanda Group, with Reuters reporting earlier the deal was under pressure amid tight scrutiny by Beijing on outbound deals.

Facilitating Beijing’s decision has been the steep drop in the US Dollar in 2017. As a reminder, the yuan slumped around 6.5% against the USD last year, but has since firmed nearly 1% in 2017, defying many analysts’ expectations of further depreciation, and benefiting from Trump’s recent attempt to talk down the dollar, no matter how hard Mnuchin may try to deny it. Suggesting that Yuan appreciation may just be getting started, a Reuters poll earlier this month indicated investors likely increased their bullish bets on the yuan to the most since July 2015.