GOLD: $1291.40 UP $8.90

Silver: $17.16 UP 23 CENT(S)

Closing access prices:

Gold $1288.10

silver: $17.11

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1294.21 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1285.95

PREMIUM FIRST FIX: $8.26 (premiums getting larger)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1304.05

NY GOLD PRICE AT THE EXACT SAME TIME: $1287.05

Premium of Shanghai 2nd fix/NY:$17.00 (PREMIUMS GETTING LARGER)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1289.60

NY PRICING AT THE EXACT SAME TIME: $1288.75

LONDON SECOND GOLD FIX 10 AM: $1291.40

NY PRICING AT THE EXACT SAME TIME. 1292.25 ???

For comex gold:

OCTOBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR: 2329 FOR 232,900 OZ (7.241TONNES)

For silver:

OCTOBER

1 NOTICES FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 391 for 1,955,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A STRONG 1688 contracts from 186,144 UP TO 187,832 WITH RESPECT TO YESTERDAY’S TRADING (UP 23 CENTS). THE CROOKS ARE HAVING AN AWFUL TIME TRYING TO COVER THEIR MASSIVE SILVER SHORTS. IT IS OBVIOUS THAT THE HUGE RISE IN PRICE YESTERDAY NEGATED ANY ATTEMPT TO COVER THAT SHORTFALL

RESULT: A GOOD SIZED RISE IN OI COMEX WITH THE 23 CENT PRICE RISE. OUR BANKERS FAILED AGAIN IN THEIR ATTEMPT TO COVER ANY OF THEIR MASSIVE SILVER SHORTFALL.

In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.939 BILLION TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER.

In gold, the open interest SURPRISINGLY FELL BY 336 CONTRACTS DESPITE THE GOOD SIZED RISE in price of gold ($8.00 ) . The new OI for the gold complex rests at 513,815. IT SURE LOOKS LIKE OUR BANKER FRIENDS SEEM A LITTLE EDGY AS THEY WERE INTENT ON COVERING SOME OF THEIR HUGE GOLD SHORTFALL WHICH WILL EXPLAIN THE DROP IN OI DESPITE THE GAIN IN GOLDPRICE.

Result: A SMALL SIZED DECREASE IN OI WITH THE RISE IN PRICE IN GOLD ($8.00). WE PROBABLY HAD SOME GOLD SHORT COVERING BY THE BANKERS.

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Tonight , NO CHANGES in gold inventory at the GLD/

Inventory rests tonight: 858.45 tonnes.

SLV

Today: NO changes in inventory:

INVENTORY RESTS AT 326.898 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A STRONG 1688 contracts from 186,144 UP TO 187,832(AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) . IT SEEMS THAT OUR BANKERS WERE AGAIN UNSUCCESSFUL IN COVERING THEIR SILVER SHORTS. THE DATA SEEMS TO SUGGEST SOME GOLD SHORT COVERING BUT IN SILVER IT IS BECOMING IMPOSSIBLE FOR THE CROOKS TO COVER. AS SUCH THEY RETREATED TO HIGHER GROUND AND THEN THEY WILL TRY AGAIN.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE RISE IN PRICE OF 23 CENTS WITH RESPECT TO YESTERDAY’S TRADING. OUR BANKER FRIENDS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO COVER ANY OF OUR SILVER SHORTS

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed up 8.61 points or .26% /Hang Sang CLOSED UP 164.24 pts or .58% / The Nikkei closed UP 132.80 POINTS OR .64/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed WELL up at 6.5792/Oil UP to 50.23 dollars per barrel for WTI and 56.30 for Brent. Stocks in Europe OPENED RED EXCEPT FTSE . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.5792. OFFSHORE YUAN CLOSED STRONGER TO THE ONSHORE YUAN AT 6.5704 AND BOTH YUANS ARE STRONGER AGAINST THE DOLLAR. CHINA IS EXTREMELY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/USA

South Korea ready to try out its new graphite “blackout bomb” which can paralyze North Korea’s antiquated power grid and yet cause no loss of life

( zero hedge)

b) REPORT ON JAPAN

USA sends a nuclear submarine to the Korean Peninsula and will engage in more military exercises with South Korea and Japan

( zero hedge)

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

(courtesy zerohedge)

iii)GREAT BRITAIN/NORTH KOREA

Britain draws up plans for war with North Korea;

( Mac Slavo/SHFTPlan.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia finally accuses the uSA of pretending to fight ISIS something that we have been telling you for years.

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)An excellent commentary from Chris Powell who asks Steve Saville why he does not address obvious questions on rigging on the precious metals.

( Chris Powell/GATA)

ii)Jamie Dimon has called bitcoin a fraud so why are they quoting prices?( GATA/Bloomberg)

10. USA Stories

i)In line with what we have been telling you for the past several weeks: Trump’s tax plan has no chance of passing. Today the Corker feud and the Paul rejection has put the plan spiraling towards death.

( zerohedge)

ii)The feud between Corker and Trump intensifies with the NYTtimes releasing part of the phone recording

( zerohedge)

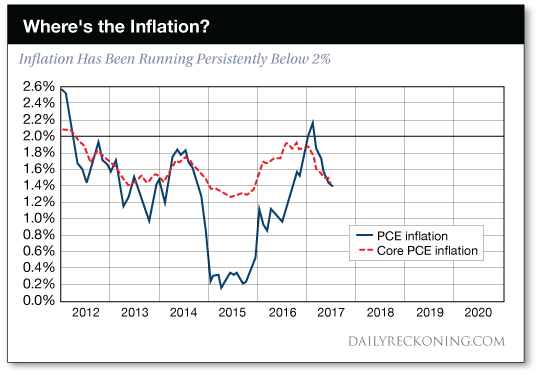

iii)An excellent commentary from James Rickards explaining why Janet Yellen has got her “inflation” numbers wrong. He explains the Fed’s preferred number PCE and also highlights why these numbers are not transitory

(a good read..courtesy James Rickards)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY FELL BY 336 CONTRACTS DOWN to an OI level of 513,815 DESPITE THE RISE IN THE PRICE OF GOLD ($8.00 RISE IN YESTERDAY’S TRADING). IT SEEMS THAT OUR BANKER FRIENDS TRIED TO COVER SOME OF THEIR HUGE GOLD SHORTFALL WITH LIMITED SUCCESS. OCTOBER IS AN ACTIVE DELIVERY MONTH ALTHOUGH IT IS THE WEAKEST IN TERMS OF ACTUAL DELIVERIES AND OPEN INTEREST. WE VISUALIZED THAT THROUGHOUT THE MONTH OF SEPTEMBER, THE CROOKS UTILIZED THE EMERGENCY EFP SCHEME TO TRANSFER OBLIGATIONS OVER TO LONDON. IT THEN STANDS TO REASON THAT IF THE EMERGENCY WAS IN FORCE THROUGHOUT THE MONTH OF SEPTEMBER IT WOULD CONTINUE ON FIRST DAY NOTICE WHEREBY ANOTHER 7200 LONG COMEX CONTRACTS WERE GIVEN 7200 EFP’S. WE HAVE NOW ENDED GOLDEN WEEK WHERE ALL OF CHINA WAS OFF AND AS SUCH WE SHOULD EXPECT GOLD TO BE STRONG THIS WEEK WITH CHINA RETURNING TO ACTIVE DUTY PURCHASING OUR PRECIOUS METALS.

Result: a TINY SIZED open interest DECREASE WITH THE GOOD SIZED RISE IN THE PRICE OF GOLD ($8.00). BANKERS MILDLY SUCCESSFUL IN THEIR ATTEMPT TO COVER SOME OF THEIR GOLD SHORTFALL.

IN SEPTEMBER,CHINA THREW OUT A TRIAL BALLOON LAST MONTH THAT THEY WERE CONSIDERING A YUAN BASED OIL CONTRACT ON THE SHANGHAI EXCHANGE AND THEN THE RECIPIENT OF YUAN WILL ALSO HAVE THE OPTION OF CONVERTING TO GOLD. I NOW STRONGLY BELIEVE THAT THAT IS THE REASON FOR THE CONSTANT TORMENT. THE BANKERS KNOW THAT THEIR GAME WILL BE UP ONCE WE GET A YUAN-PETRO SCHEME WITH A CONVERSION OF YUAN INTO GOLD.

I BELIEVE THE CHINESE WILL INTRODUCE THIS SCHEME AT THEIR BIG 5 YR FORUM BEGINNING ON OCT 18.

I WOULD IMAGINE THAT THE CHINESE WOULD TAKE IN ALL GOLD INITIALLY AT SAY $2,000…AND THE NEW GOLD RECEIVED WOULD BE USED TO SETTLE ON YUAN CASHED. IF 2,000 DOLLARS IS INSUFFICIENT TO RAISE ENOUGH GOLD, THEN FURTHER INCREASES WILL BE THE ORDER OF THE DAY UNTIL EQUILIBRIUM.

THE BANKERS FEARING THIS, HAS ORCHESTRATED HUGE RAIDS THESE PAST 3 WEEKS HOPING TO COVER AS MANY GOLD/SILVER SHORTS AS POSSIBLE.

NOW THAT WE ARE CLOSE TO THE 29TH CHINESE CONGRESS, THE BANKERS ARE TAKING NO CHANCES AS THEY START TO COVER THEIR GOLD/SILVER SHORTFALL.

We have now entered the active contract month of Oct and here we saw a GAIN of 3 contracts UP to 223 contracts. We had 0 notices filed yesterday so we GAINED 3 contracts or 300 oz will stand for delivery at the comex in this active delivery month of October and 0 EFP notices were given. The low number of notices early in the delivery cycle is evidence of a lack of physical gold.

The November contract saw A loss OF 70 contracts down to 1325.

The very big active December contract month saw it’s OI LOSS OF 1261 contracts DOWN to 402,022.

We had 0 notice(s) filed upon today for NIL oz

VOLUME FOR TODAY (PRELIMINARY) NOT AVAILABLE

CONFIRMED VOLUME YESTERDAY: 206,720

We had 1 notice(s) filed for 5,000 oz for the OCT. 2017 contract

Oct.10/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

223 contracts

(22300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2329 notices

232,900 oz

7.2441 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

62,292.650 oz

SCOTIA

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

600,627.490 oz

BRINKS

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

520 contracts

(2,600,000 oz)

|

| Total monthly oz silver served (contracts) | 391 contracts (1,955,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | xx oz |

NPV for Sprott and Central Fund of Canada

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott Inc. to take control of rival gold holder Central Fund of Canada

Posted Oct 2, 2017 8:43 am PDT

Last Updated Oct 2, 2017 at 9:20 am PDT

TORONTO – Sprott Inc. (TSX:SII) says it has struck a deal to take control of rival gold-holding firm Central Fund of Canada Ltd. (TSX:CEF.A) after a protracted takeover effort.

Toronto-based Sprott said Monday it will pay $120 million in cash and stock for Central Fund of Canada Ltd.’s common shares and for the right to administer and manage the fund’s assets.

The deal, which requires approval from Central Fund shareholders, would see its class A shareholders transferred to a new Sprott Physical Gold and Silver Trust.

Sprott says the deal would add $4.3 billion to its assets under management, which are focused largely on holding physical precious metals on behalf of clients, and 90,000 investors to its client base.

In March, Sprott tried to go through the Court of Queen’s Bench of Alberta to allow Central Fund’s class A shareholders to swap their shares to Sprott after the family that controls Central Fund rebuffed their attempt to make a deal.

Last year Sprott took over Central GoldTrust, a similar fund controlled by the same family, after securing support from more than 96 per cent of shareholder votes cast.

END

And now the Gold inventory at the GLD

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

SEPTEMBER 29/no changes in gold inventory at the GLD/Inventor rests at 864.65 tonnes

Sept 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.65 TONNES

Sept 27/WOW!! WITH GOLD DOWN $13.25, WE HAD A HUGE 8.57 TONNES OF GOLD ADDED TO THE GLD/

Sept 26/no changes in gold inventory at the GLD/Inventory rests at 856.08 tonnes

Sept 25./Another big deposit of 3.84 tonnes into GLD/Inventory rests tonight at 856.08 tonnes

Sept 22/with gold up only 1 dollar on the day we had a massive 6.21 tonnes of gold added to the GLD/.this is a good sign that gold will advance nicely this coming week.

Sept 21/no change in gold inventory tonight/inventory rests at 846.03 tonnes

Sept 20/no change in gold inventory tonight/inventory rests at 846.03 tonnes

Sept 19/another deposit of 2.07 tonnes of gold into the GLD/inventory rests at 846.03 tonnes

Sept 18/a huge 5.32 tonnes of gold deposit into the GLD despite gold’s whack today/inventory rests at 843.96 tonnes

Sept 15./strange!!no change in GLD after the whacking of gold/inventory remains at 838.64 tonnes

Sept 14./no changes at the GLD/inventory rests at 838.64 tonnes

Sept 13/late last night a huge 4.14 tonnes of gold was added to the GLD inventory/inventory rests at 838.64 tonnes.

Sept 12/as of 5: 40 pm est, no changes in gold inventory at the GLD/Inventory rests at 834.50 tonnes

Sept 11/Today we had a rather large 2.37 tonnes of gold removed from the GLD/Inventory rests at 834.50 tonnes

Sept 8/we had a tiny withdrawal of .34 tonnes and probably that would be to pay for fees like insurance etc.

Inventory rests at 836.87 tonnes

end

Now the SLV Inventory

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

SEPTEMBER 29/no changes in silver inventory at the SLV/inventory rests at 326.757 million oz/

Sept 28/NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ/

Sept 27/STRANGE!! SILVER IS HIT FOR 24 CENTS YESTERDAY AND. 9 CENTS TODAY AND YET NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ

Sept 26./no change in silver inventory at the SLV/.inventory rests at 326.757 million oz

Sept 25./ a big deposit of 1.842 million oz into the SLV/inventory rests at 326.757 million oz/

Sept 22/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz/

Sept 21/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz

Sept 20/no changes in silver inventory/Inventory remains at 324.915 million oz

Sept 19/strange!! another withdrawal of 1.134 million oz despite the rise in silver/inventory rests at 324.915 million oz

Sept 18/a withdrawal of 1.039 million oz from the SLV/Inventory rests at 326.049 million oz

Sept 15./no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 14/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 13/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 12.2017/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 11.2017: no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 8/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Oct 10/2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.40%

Indicative gold forward offer rate for a 6 month duration+ 1.40% -

+ 1.62%

end

Bitcoin prices for THIS MORNING: Bid $4785.00 offer: $4806.00

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

London House Prices Are Falling – Time to Buckle Up

– London house prices fall in September: first time in eight years

– High-end London property fell by 3.2% in year

– House sales down by over a very large one-third

– Global Real Estate Bubble Index – see table

– Brexit, rising inflation and political uncertainty causing many buyers to back away from market

– U.K. housing stock worth record £6.8 trillion, almost 1.5 times value of LSE and more than the value of all the gold in world

– Homeowners and property investors should diversify and invest in gold

Editor Mark O’Byrne

In what might be a sign of things to come, London house prices have fallen for the first time in eight years.

London house sales have fallen by a third as years of frenzied bidding come to a shuddering halt.

The capital remains expensive. Housing still costs 10 times the average salary and only 50% of Londoners own their own homes, the EU average is 70%.

Currently the rest of the UK appears to be benefiting from the lack of affordability and stock in London. Buyers are moving further out of the capital in order to secure their footing on the housing ‘ladder’… no snakes here …

Last month U.K. house prices regained their fastest pace since February. A Halifax house price survey showed a 4% price rise in the three months to September compared with the same period last year.

Long-term, a fall in London prices may be an indicator that concerns over Brexit, inflation and political stability are beginning to affect the U.K property market.

This will be a hard landing for a country that is so convinced that putting all one’s eggs in the housing basket is the answer to securing and growing wealth.

‘Global Real Estate Bubble’

Last month, UBS Wealth Management published its Global Real Estate Bubble Index. London came sixth with a score of 1.77. The group concluded that London is still firmly in bubble-territory.

The research found that London house prices have climbed 15% in the last year and 45% since the financial crisis, when adjusted for inflation.

This suggests September’s fall in prices might be a signal that the top of the market is just behind us. This is no surprise when one considers both the known and unknown events on the horizon for the city.

Brexit is the most discussed threat. Foreign buyers are wary of what the future holds and there is anecdotal evidence that EU workers are being offered shorter contracts. Four years ago foreign buyers accounted for 82% of property purchases.

Brexit is the main stymie of political progress in the country.

Conferences, policy announcement and parliamentary discussions are dominated by how this may or may not play out. No-one knows what will happen, prompting many to feel uncomfortable with making major financial decisions.

This could go on for some time.

Meanwhile the Bank of England are tasked with sorting out the economy. They continue to encourage inflation and plan to raise interest rates. Thus devaluing the value of the pounds in our accounts and increasing the cost of borrowing.

It is not surprising, therefore, that it is not just in London that we are looking at the bursting of the property bubble.

Rest of the UK still climbing…according to some

London, often an indicator for things to come for the rest of the U.K., should be a beacon for the rest of the country’s housing market.

Halifax data shows in September house prices had their fastest annual rise since February. The year-on-year increase jumped a surprisingly large 4%.

Pundits believe this is an indicator that buyers are shrugging off threats of a rate hike by the Bank of England.

Others aren’t so sure. Nationwide’s own home price survey showed more subdued numbers (2%), suggesting there is a slowdown in house prices across the country, particularly in certain regions.

The pace of national price increases has slowed and is down from a peak of 10% in early 2016, to 4% today.

Halifax said future demand might be limited by ‘a squeeze on spending power from higher consumer price inflation and the high cost of property.’ However it does not think that future interest rate price rises would affect the market.

Despite concerns over inflation stretching affordability, mortgage approvals remain at an average pace of almost 67,000 a month, little changed from 2016.

The economist Samuel Tombs of Pantheon Macroeconomics told the Guardian that he thought Halifax was way off the mark.

“Other surveys show that the pipeline of demand is soft; Rics [the Royal Institution of Chartered Surveyors] has reported that new buyer inquiries have fallen in six of the last seven months. Real wages still have further to fall over the next six months and mortgage rates will rise soon in response to the increase in banks’ funding costs.”

Obsession with home ownership

Last week Prime Minister Teresa May referred to the ‘British Dream’. Judging by Twitter few understood what she meant.

If there is such a thing it has to be the desire to own the roof over your head and then sell it at a ridiculous profit.

In the UK this comes at a serious price, but one which few of us question. Often first-time buyers have to rely on family to help, then be comfortable with a 25-year mortgage and restrict their lifestyles well into middle-age.

Ten years later they have to do it all again as a baby’s on the way, house prices are climbing and they want to climb the proverbial ladder.

Failure to do this is seen as just that … a ‘failure’.

To not pursue home ownership in the UK and in Ireland is seen as pretty nuts and irresponsible.

The problem is that in the UK, renting is enough of an incentive to put yourself in such a dire financial situation. It is very different to continental Europe. In the UK and Ireland few leases are long-term and landlords hold the majority of rights. As a result you feel very insecure in your home.

Brits and Irish want to feel financially secure. Ironically they get this security by getting themselves into hundreds of thousands of pounds worth of debt. But the ‘wealth effect’ is so desired and so encouraged by economists, that this level of debt is both expected and accepted.

The British government has encouraged this. For them this is what capitalism is all about. Home ownership and buy-to-let mortgages. But it may run people and perhaps the economy into the ground.

Consider the number of people who subsidise their lives, savings and retirement with the ‘wealth’ they have locked up in their homes. In 2015 older homeowners borrowed £4.2m a day using equity release loans as pensions are no longer covering retirement costs.

We can only expect this to get worse given the looming pension crisis.

Pensioners will be royally scuppered if they find themselves in negative equity, with no pension to support them. Especially so given a considerable number of pension funds and investment bonds rely on UK property to generate income.

Government has a lot to answer for

The country is consistently coming under fire for a lack of housing supply and lack of affordability.

Earlier this week the government announced plans to extend its “Help to Buy” program to 135,000 buyers. The program offers interest-free loans to homebuyers. This will see an extra £6.7 billion pounds ($8.7 billion) of “stimulus” into the market.

Yet another example of leaders trying to unnecessarily stoke a market which results in increased inflation and higher debt levels for a country which is already one of the most indebted.

Currently the UK housing stock is worth nearly £7 trillion, more than the companies listed on the London Stock Exchange and more than the value of all the gold in the world.

The World Gold Council estimates that all the gold ever mined totaled 187,200 tonnes in 2017. At a price of US$1,250 per troy ounce, one tonne of gold has a value of approximately US$40.2 million.

Thus today, all the gold in the world is worth some $7.5 trillion dollars or £5.7 trillion pounds and less than the value of the UK housing stock.

The ridiculous valuation of the London property in particular is thanks to the government, banks and real estate businesses peddling the Greater Fool Theory.

The theory applies here as buyers bought property they thought was expensive but believed they would be able to sell it at a higher price, for significant profit to an ‘even greater fool’.

Falling house prices will make a fool out of everyone, whilst (no doubt) the government continue to make housing ‘affordable’.

Time to Buckle Up With Physical Gold

Housing in the UK is a single asset class but it accounts for two-thirds of the country’s wealth.

There is not a level in society whether government, businesses, banks or individuals that does not have skin in this game.

The figures and economic outlook suggest we need to start diversifying.

The government needs to stop being so irresponsible and no longer constantly peddle arguments for home ownership. However it is difficult politically to sell that story. Especially when all parties have realised the youth vote has major housing concerns and believes they have the right to own property.

Brexit is the main area of concern and no-one wishes to rock the property market any further. Instead homeowners need to consider how they can both protect themselves from falling prices and diversify their investments and wealth.

It is not prudent to have so much wealth caught up in one falling asset. Especially given that it is inevitable that London property will be affected by a number of issues on the horizon including rising interest rates, inflation and Brexit.

Gold is another real asset that millions of investors have placed their faith in over hundreds of years. Like housing, it is tangible. Unlike housing, it does not come with a massive debt burden and it benefits from rising inflation and uncertainties in both political and economic spheres.

News and Commentary

Gold marks over 1-week high; firm dollar curbs gains (Reuters.com)

South Korea stocks surge, leading Asian market gains (MarketWatch.com)

Germany, China lift world stocks, Spanish worries simmer (Reuters.com)

U.S. Stocks Slip, Dollar Mixed as Gold Advances (Bloomberg.com)

Jewelers Rally on Indian Rule Reversal as Peak Gold Season Looms (Bloomberg.com)

Source: Economyandmarkets.com

Italy Will Default And Create Next Deflationary Crisis (EconomyAndMarkets.com)

The Hated Dollar Resurges. But Why? (WolfStreet.com)

Questions that deniers of monetary metals market rigging won’t answer (Gata.org)

Silver price (InvestingHaven.com)

Donald Trump: Warmonger-in-Chief (Acting-Man.com)

Gold Prices (LBMA AM)

10 Oct: USD 1,289.60, GBP 977.77 & EUR 1,094.61 per ounce

09 Oct: USD 1,282.15, GBP 976.23 & EUR 1,092.01 per ounce

06 Oct: USD 1,268.20, GBP 970.43 & EUR 1,083.93 per ounce

05 Oct: USD 1,278.40, GBP 969.28 & EUR 1,086.51 per ounce

04 Oct: USD 1,275.55, GBP 960.87 & EUR 1,085.11 per ounce

03 Oct: USD 1,270.70, GBP 959.00 & EUR 1,081.87 per ounce

02 Oct: USD 1,273.10, GBP 956.48 & EUR 1,084.55 per ounce

Silver Prices (LBMA)

10 Oct: USD 17.12, GBP 12.98 & EUR 14.53 per ounce

09 Oct: USD 16.92, GBP 12.86 & EUR 14.41 per ounce

06 Oct: USD 16.63, GBP 12.73 & EUR 14.20 per ounce

05 Oct: USD 16.66, GBP 12.64 & EUR 14.19 per ounce

04 Oct: USD 16.83, GBP 12.67 & EUR 14.29 per ounce

03 Oct: USD 16.61, GBP 12.53 & EUR 14.13 per ounce

02 Oct: USD 16.58, GBP 12.46 & EUR 14.12 per ounce

Recent Market Updates

– Perth Mint Gold Coins Sales Double In September

– Survey shows UK and US Pensions Crisis is Imminent

– Gold Investment In Germany Surges – Now World’s Largest Gold Buyers

– Yahoo Hacking Highlights Cyber Risk and Increasing Importance of Physical Gold

– Safe Haven Silver To Outperform Gold In Q4 And In 2018

– Plan For Run On The Pound

– Russia Gold Rush Sees Record Reserves For Putin Era

– China Catalyst To Send Gold Over $10,000 Per Ounce?

– Gold Matches S&P 500 Performance In First 3 Quarters; Up 12% 2017 YTD

– Gold Standard Resulted In “Fewer Catastrophes” – FT

– Financial Advice From Man Who Made $1+ Billion in 1929 – Importance Of Being Patient and “Sitting”

– “Gold prices to reach $1,400 before the end of the year” – GoldCore

– Commodities King Gartman Says Gold Soon Reach $1,400 As Drums of War Grow Louder

END

An excellent commentary from Chris Powell who asks Steve Saville why he does not address obvious questions on rigging on the precious metals.

(courtesy Chris Powell/GATA)

The questions that deniers of monetary metals market rigging won’t answer

Submitted by cpowell on Mon, 2017-10-09 01:11. Section: Daily Dispatches

9:27p ET Sunday, October 8, 2017

Dear Friend of GATA and Gold:

Newsletter writer Steve Saville of The Speculative Investor, who long has denied that manipulation of the monetary metals markets means much, has seized on the recent essay by Keith Weiner of Monetary Metals as the conclusive refutation of silver market analyst Ted Butler’s longstanding complaint that JPMorganChase has been rigging the silver market.

Weiner’s analysis, headlined “Thoughtful Disagreement with Ted Butler” and posted here —

https://monetary-metals.com/thoughtful-disagreement-with-ted-butler/

— argued that JPMorganChase is undertaking only ordinary arbitrage in the silver market, exploiting spreads between bid and ask prices

Saville, in commentary headlined “A Silver Price-Suppression Theory Gets Debunked” —

http://tsi-blog.com/2017/10/a-silver-price-suppression-theory-gets-debun…

— cheers Weiner’s essay and goes on to remark: “Entering a debate with someone who is incapable of being swayed by evidence that invalidates his position is a waste of time and energy, so these days I devote no commentary space and minimal blog space to debunking the manipulation-centric gold and silver articles that regularly appear.”

But when has Saville himself ever addressed evidence of manipulation of the gold and silver markets? Of course if he declines to address the evidence, he too can’t be swayed by it.

The manipulation deniers never address the evidence.

Weiner’s technical analysis is no refutation of silver market manipulation, for even if JPMorganChase is just doing arbitrage in silver, a judgment on manipulation would require knowing for whom the investment house was doing the arbitrage.

JPMorganChase’s former chief of commodity operations, Blythe Masters, said on CNBC five years ago that the investment house had no position of its own in silver and was trading only for clients:

https://www.youtube.com/watch?v=gc9Me4qFZYo

So might those clients include governments and central banks, entities with nearly infinite resources sufficient to nullify markets?

The question is compelling because filings with the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission by CME Group, operator of the major futures exchanges in the United States, assert that governments and central banks are clients of the exchanges and that the exchanges give them special volume trading discounts for trading all futures contracts, not just financial futures contracts:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

Do Weiner and Saville know that JPMorganChase is not trading silver futures for governments and central banks?

Do Weiner and Saville know that governments and central banks are not trading gold and gold derivatives surreptitiously?

If Weiner and Savillete think they know, they’re wrong, for the Bank for International Settlements admits that it operates as a broker in gold and gold derivatives for its member central banks:

http://www.bis.org/banking/finserv.htm

Indeed, in 2005 the director of the BIS’ monetary and economic department, William R. White, told a conference at BIS headquarters in Basle, Switzerland, that a primary purpose of international central bank cooperation is “the provision of international credits and joint efforts to influence asset prices (especially gold and foreign exchange) in circumstances where this might be thought useful”:

The BIS even advertises that its services to its member central banks include surreptitious interventions in the gold market:

http://www.gata.org/node/11012

Anyone who wants to engage in honest argument about gold and silver market manipulation needs to address a few simple questions:

1) Are governments and central banks active in the monetary metals markets or not?

2) Are the documents asserting such activity genuine or forgeries?

3) If governments and central banks are active in the monetary metals markets, is it just for fun or is it for policy purposes?

4) If such activity by governments and central banks is for policy purposes, do those purposes involve the traditional objectives of defeating an independent world currency that competes with government currencies and interferes with government control of interest rates, objectives documented at length by GATA here?:

http://www.gata.org/node/14839

Of course if largely surreptitious intervention in the monetary metals markets by central banks and governments is ever acknowledged, technical analysis of those markets is meaningless, which may explain why technical analysts like Weiner and Saville avoid the crucial questions and just sneer at those who raise them.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Jamie Dimon has called bitcoin a fraud so why are they quoting prices?

(courtesy GATA/Bloomberg)

Dimon called bitcoin a fraud but JPMorgan is quoting prices

Submitted by cpowell on Mon, 2017-10-09 02:05. Section: Daily Dispatches

By Matthew Levine

Bloomberg News

Friday, October 6, 2017

JPMorgan Chase & Co.’s chief executive, Jamie Dimon, famously panned bitcoin. But his bank’s clients apparently aren’t ready to dismiss it as a “fraud.”

The Wall Street firm’s widely followed morning markets note highlights the spot price for the cryptocurrency. There it sits, right below a rundown of commodities and above the 10-year Treasury yield — hardly fringe assets. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-10-06/dimon-called-bitcoin-

END

Russia is not set to block all exchanges offering to buy and sell cryptocurrencies. Bitcoin briefly underwent a flash crash but is now back above par trading at $4795 up 66 dollars.

(courtesy zerohedge)

Bitcoin Briefly Flash-Crashes On Russia ‘Ban’ Headlines

After weeks of uncertainty surrounding Russia’s plans for cryptocurrencies, local news outlet RBC reports overnight that Bank of Russia is working with the country’s general prosecutor to block all exchanges offering Russians the opportunity to buy and sell cryptocurrency.

As CoinTelegraph reports, first deputy of the central bank, Sergey Shvetsov, said during an international finance forum in Moscow:

“It’s obvious that when a pyramid (scheme) grows, interest in this pyramid hots up with the high rate of return.”

Echoing previous comments, Shvetsov added that the pyramid description is a result of “eyeing Bitcoin’s price dynamics over the past two years.”

The move is the most sweeping yet from Russian authorities regarding cryptocurrency access for citizens, and echoes the less coordinated bans of various industry resources common until last year. The debate as to how to handle cryptocurrency has raged throughout 2017 in Russia, with various high-profile entities giving conflicting views as to what the future will hold in terms of regulation.

This regulation is ostensibly due to go public by the end of the year.

In the meantime, not just private investors, but also the business sector faces “too high a risk” using cryptocurrency, Shvetsov said.

“We cannot stand apart. We cannot give direct and easy access to such dubious instruments for retail (investors),”

Financial instruments based on cryptocurrency are “impossible to support,” he continued, adding measures would be taken to “restrict” the ability of the Russian domestic market to interact with them.

The reaction was varied. As Coinivore notes, Bitcoin prices flash-crashed on CoinDesk…

Notably, this would be the third time that the country has issued some form of ban against Bitcoin and digital currency in the past several years.

Russia’s Central Bank just approved its first exchange “Voskhod,” so this is likely a temporary ban until regulations are set which will likely ban normal Russian citizens from investing into cryptocurrency due to high volatility.

However, Bitcoin is now higher on the day (bouncing back as it did from China’s ban), and as BitStamp data shows, not every exchange shows the flash-crash…

It seems the market for Bitcoin is quick to realize that the dcecentralized nature of the cryptocurrency framework means that whiole short-term demand from localized exchange closures may hobble prices, it does not affect the overall value of the independent currency (just as many have found out since China blocked exchanges).

We would not expect this to be the last nation to attempt to ‘ban’ Bitcoin. As Cybersecurity expert John McAfee warns, cryptocurrencies may encompass the sum of all fears for governments the world over.

With no centralized exchange to control or influence, national authorities around the world will find it increasingly difficult to determine a given citizen’s income and thus their income tax owed, undermining a critical source of government revenue.

Our income taxes are the greatest source of revenue, but if everybody’s using Bitcoin, the government doesn’t know what your income is. They can’t tax it, and if you choose to say I didn’t have anything, they cannot prove otherwise,” McAfee told CalvinAyre.com.

“It will eventually frighten every nation state, but it doesn’t matter what they do, there’s no way you can create a law or to legislate something that will stop Bitcoin or any cryptocurrency because technically, you cannot,” he added.

The often outspoken and eccentric McAfee did highlight the need for some regulation, however, preaching caution over the latest trend of government-sponsored Initial Coin Offerings (ICOs).

“China is right about one thing, the ICOs, the initial coin offerings, there are lots of scams, lots of people who are fraudulently taking money from other people, so that’s got to stop. But I don’t think governments can stop it. We as users and the bitcoin community have to be self-regulated,” McAfee said.

“The fear is in the fear of governments and central banks, like JPMorgan, which is America’s largest bank,” he said. “The CEO is so concerned that he acted like a madman and called Bitcoin a fraud, said someone is going to get killed eventually. It’s like, what are you talking about? It’s nonsense.”

McAfee concluded:

“So banks and governments are the ones that have the fear. Well they should have some fear. They have taken control and power away from their citizens for hundreds of years. It’s time that we, as citizens, took that power back.”

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

2. Nikkei closed UP 132.80 POINTS OR .64% /USA: YEN FALLS TO 112,36

3. Europe stocks OPENED RED EXCEPT FTSE ( /USA dollar index FALLS TO 93.39/Euro UP to 1.1791

3b Japan 10 year bond yield: FALLS TO -+.055%/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.44/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.23 and Brent: 56.30

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP or Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.447%/Italian 10 yr bond yield UP to 2.130% /SPAIN 10 YR BOND YIELD UP TO 1.684%

3j Greek 10 year bond yield FALLS TO : 5.60???

3k Gold at $1291.90 silver at:17.20(8:15 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 44/100 in roubles/dollar) 57.85-

3m oil into the 50 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.36 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9769 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1518 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.447%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.359% early this morning. Thirty year rate at 2.893% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

European Stocks On Edge Ahead Of Catalan Independence Call, S&P Futures Rise

S&P futures are again modestly in the green as European shares hold steady ahead of a meeting of the Catalan regional parliament and a possible declaration of independence by Catalan leader Puigdemont, while Asian shares rise a the second day. The dollar declined for the 3rd day, its losses accelerating across the board amid growing concerns that Trump’s tax reform is once again dead following the Corker spat and a rejection from Paul Ryan, with the move gaining traction after China set the yuan’s fixing stronger for the first time in seven days. Monday’s sell-off in Turkish assets seemed to have little follow-through, with emerging-market currencies all trading higher and Treasuries steady. Traders are also waiting for minutes from the Federal Reserve’s last meeting, which may provide more details on the path of interest rates and balance sheet tapering.

“The weak dollar is a cue for investors that the U.S. Fed will not be aggressive in raising interest rates and this supports the outlook for a strong equities market,” said Cristina Ulang, head of research at First Metro Investment Corp. in Manila. “We will see a U.S. rate increase in December but it’s not going to be sharp since we aren’t seeing runaway U.S. economic growth.”

Asia stocks advanced as traders in Japan and South Korea returned from holidays, pushing the regional benchmark to a three-week high amid a broad weakness in the dollar. The MSCI Asia Pacific Index gained 0.7% to 164.49, its highest close since Sept. 20. The biggest boost came from Samsung Electronics which also helped South Korea’s Kospi advance 1.6%. In Japan, the Topix rose to its highest close in more than a decade, driven by a string of positive economic data both at home and abroad. The Asia-wide gauge has rallied 22 percent so far this year, on course for its best performance since 2009. It’s still trading at the biggest discount to the S&P 500 Index in 15 years in terms of price-to-book.

All eyes are on Europe however, and Spain in particular, where Catalan lawmakers will meet today to consider a declaration of independence that risks an ironclad backlash from Madrid. Attention will focus on the form of words used by Catalan President Carles Puigdemont, who is due to address the parliament in Barcelona at 6 p.m. The IBEX fell alongside most national gauges across Europe. The common currency gained for a third day. It is Spain’s biggest political crisis since an attempted military coup in 1981. Madrid’s IBEX stocks index drooped 0.5 percent early on and it is now down almost 9 percent since May, though a sharp rise in the euro has also taken a toll.

“We have not witnessed any relevant statement or signal by the separatists that would hint at a change of strategy ahead of today’s discussion in the Catalonian parliament,” economists at Barclays wrote.

“Consequently, at this point, it seems likely that Catalan President Carles Puigdemont remains on track to announce a unilateral declaration of independence as early as today.”

“Rather than a full universal declaration of independence, we may see a ‘symbolic statement’ from the Catalan government,” said Fabio Balboni, economist at HSBC Bank Plc. “Signs of disagreement are starting to emerge within the regional government, with more moderate members fearing the consequences of a further step towards independence, given the lack of support from the EU, and moves by some banks and firms to leave Catalonia.”

Despite the Spain jitters, The euro remained resilient, rising to a one-week high as data showed German exports had surged in August. Traders were also still upbeat on the currency after one of the European Central Bank’s German policymakers called for an end to its stimulus.

Elsewhere, Turkey’s lira recouped some of yesterdays losses even as the U.S. signaled the crisis between the two countries could drag on. Gold rose as the greenback weakened, and West Texas oil held gains near $50 a barrel before U.S. government data forecast to show crude inventories extended declines for a third week. Japan’s Topix index closed at the highest since July 2007 and Korean stocks staged a catch-up rally after a week-long holiday.

Turkey also got some help from a weaker dollar which was down for a third straight day. The dollar index, which tracks the greenback against six major rivals, dropped 0.2 percent to 93.533 and away from Friday’s almost 3-month peak. It gave the Turkish lira a breather having been sent sprawling to a nine-month low on Monday after the United States and Turkey scaled back visa services.

Meanwhile, Mexico’s peso hovered at its weakest in more than four months, ahead of the latest round of talks over the North American Free Trade Agreement (NAFTA) on Wednesday.

Over in Asia, the offshore Chinese yuan rate surged to its strongest levels in more than two-weeks. The central bank had also set a firmer-than-expected official rate, suggesting authorities are keen to keep the currency in check ahead of next week’s key national leadership meeting.

In commodities, Crude oil prices edged slightly higher, supported by OPEC comments signaling the possibility of continued action to restore market balance in the long-term. But gains were seen as limited as oil production platforms in the Gulf of Mexico started returning to service after the latest U.S. hurricane forced the shutdown of more than 90 percent of crude output in the area. Brent crude inched up 1 cent to $55.80 a barrel. U.S. crude added 2 cents to $49.60. Gold prices hit their highest in more than a week, though gains were capped as expectations of another U.S. interest rate hike this year limited appetite. Spot gold added 0.2 percent to $1,286.52 an ounce

Rate markets were largely unchanged, with the yield on 10-year Treasuries declined one basis point to 2.35 percent. Germany’s 10-year yield dipped one basis point to 0.44 percent, the lowest in two weeks. Britain’s 10-year yield was unchanged at 1.357 percent, the lowest in a week.

Traders are awaiting the start of the earnings season this week, with several major banks due to report, as well as Wednesday’s minutes from the Federal Reserve’s last meeting. Canadian stocks reopen after a holiday. Investors also await speeches by Fed Presidents and the minutes from the most recent Federal Reserve meeting due Wednesday. Economic data include NFIB small-business optimism. No major earnings scheduled.

Market Snapshot

- E-Mini futures on S&P 500, Dow and Nasdaq 100 each up 0.2%

- VIX Index down 1.7% at 10.15

- STOXX Europe 600 down 0.2% to 389.47

- MSCI Asia up 0.7% to 164.49

- MSCI Asia ex Japan up 0.7% to 542.58

- Nikkei up 0.6% to 20,823.51

- Topix up 0.5% to 1,695.14

- Hang Seng Index up 0.6% to 28,490.83

- Shanghai Composite up 0.3% to 3,382.99

- Sensex up 0.3% to 31,929.41

- Australia S&P/ASX 200 down 0.02% to 5,738.11

- Kospi up 1.6% to 2,433.81

- German 10Y yield fell 0.4 bps to 0.44%

- Euro up 0.4% to $1.1785

- Brent Futures up 0.4% to $56.01/bbl

- Italian 10Y yield fell 3.3 bps to 1.82%

- Spanish 10Y yield unchanged at 1.677%

- Gold spot up 0.4% to $1,289.21

- U.S. Dollar Index down 0.3% to 93.39

Top Overnight News

- Catalan President Carles Puigdemont is due to address regional lawmakers around noon New York time on the outcome of the Oct. 1 referendum that has been ruled illegal by the Spanish courts

- Minneapolis Fed President Neel Kashkari, a known dove and a candidate in running for the next Fed Chair, delivers opening remarks at a conference

- Allies of President Donald Trump say they fear his feud with Republican Senator Bob Corker risks unraveling the White House tax overhaul effort and that another major legislative failure could hobble the administration for the rest of his term

- The U.S. Ambassador to Turkey issued a video statement saying he “can’t predict” how long the latest crisis between the two countries will last

- Trump may travel to the demilitarized zone separating North and South Korea as part of his first visit to South Korea in Nov., Yonhap News reported, citing an unidentified military official; Trump is expected to send a “significant message” to North Korea during the trip, Yonhap said

- Spanish police are ready to arrest Catalan President Carles Puigdemont immediately if he declares independence in the regional parliament, two people familiar with the matter said; Puigdemont has called a press conference at 1pm in Barcelona

- New Zealand First Party leader to delay his public announcement about the result of talks to form a new government until Friday: NZ Herald

- German exports rose 3.1% m/m in August, beating an estimate 1.1% rise

- Banks in Europe have sold about 33 billion euros ($39 billion) of a new type of bank bond they’re calling “senior non-preferred”; the label allows underwriters to market the notes to managers of funds that can only hold senior debt, even though the securities can be forced by regulators to take losses in a crisis

- U.K. industrial output rose 1.6% y/y in Aug. vs est. 0.9%, while the trade deficit widened to GBP14.2B vs est. GBP11.2B

- Canadian Prime Minister Justin Trudeau will discuss international

security and trade during a meeting with President Donald Trump - Canadian housing data: Median estimate forecasts a drop; still, momentum for a strong housing market will still be strong

Asia equity markets were mixed after a cautious tone in the US, although the KOSPI (+1.8%) surged as it took its turn to play catch up from a 10-day closure. ASX 200 (-0.3%) was indecisive with weakness in energy names offset by strength in gold miners, while Nikkei 225 (+0.5%) found support from a weaker currency following dovish comments from BoJ Governor Kuroda. Hang Seng (+0.6%) and Shanghai Comp. (-0.3%) were subdued with profit taking seen in the mainland after yesterday’s outperformance. Finally, 10yr JGBs were flat with demand dampened amid a positive risk tone in Japan and a reserved BoJ Rinban announcement for just JPY 605bln of JGBs. BoJ Governor Kuroda said Japan’s economy is expanding moderately and expects CPI to pick up pace towards 2% goal, while Kuroda added the BoJ is to expand the monetary base until inflation overshoots target.

Top Asian News

- Japan-Wide Scandal Erupts Over Steelmaker’s Falsified Data

- Bank Indonesia to Keep Inflation Focus Despite Aggressive Easing

- Japan Stocks to Watch: Fujitsu, Honda, Retailers, Rohm, Toyota

- Bank Indonesia to Keep Inflation Focus After Aggressive Cuts

- Chinese Firms List at Fastest Pace Since Market Opened in 1990

- PBOC Chief Quotes Phantom of the Opera in Push for Market Reform

All anticipation is on the upcoming speech from the Catalonian leader, expected at 12:00 London Time, where there overwhelming consensus is that he will officially announce the referendum result. The IBEX underperforms, yet largely in-line with the periphery European bourses, as the FTSE MIB trades close to 1% down close, with the nation clearly seeing the largest reaction to the ECB’s plan to rein in bad loans. Not the best results in terms of UK and German auctions, and the respective 10 year debt futures are acknowledging the signs of indigestion or simply tepid demand accordingly. Specifically, covers were relatively light and for the DMO the tail was lengthy, while the Buba retained around 20% of its inflation linker. Pre-issuance Eurex low holding in, for now, but Liffe setting a marginal new base and it could be a sell into dips market until or unless something changes to provide fresh leads.

Top European News

- Famous Brands Plunges Most in 14 Years on Gourmet Burgers Blow

- U.K. Utilities Heading for Price War to Protect Market Share

- What to Watch for If Catalan Leader Says ‘Independence’ Today

- Italy Industrial Output Rises Above Estimate, Boosting Outlook

- Mirabaud Says Brokerage Business Targets Break-Even This Year

In currencies, the highlight data of the day came from the UK, as sterling was initially propped up by the higher than expected Manufacturing data. Cable tested 1.32 following the data, however, clearly running into offers around this key level. UK Manufacturing Output MM (Aug) 0.4% vs. Exp. 0.2% (Prev. 0.5%, Rev. 0.4%) Manufacturing Output YY (Aug) 2.8% vs. Exp. 1.9% (Prev. 1.9%, Rev. 2.7%) Goods Trade Balance GBP (Aug) 14.24B vs. Exp. -11.20B (Prev. -11.58B, Rev. -12.83B) Goods Trade Bal. Non-EU (Aug) -5.83B vs. Exp. -3.60B (Prev. -3.84B, Rev. -5.34B). The Norwegian Krone took a hit in early European trade, as the nation’s CPI report missed across the board, albeit marginally so. EUR/NOK broke out the week’s early range and spiked through Friday’s highs.

In commodities, gold has continued to recover following the bounce seen ahead of 1260.00, drawing support from global uncertainty, alongside a softer USD. However, the increased expectations of another hike from the Fed, and the tightening likely to move into 2018, upside could be curved. Oil markets have also continued to recover from last week’s lows ahead of 49.00, which is evident of pending bids. WTI trades near session highs, looking to break back through 50.00/bbl, seemingly strengthened by comments from Barkindo stating that growth in US shale had slowed compared to the first half of 2017 and growth in global demand may show further upward revisions, giving the supply cut effort tailwind.

Looking at the day ahead, the only reading due in the US is the September NFIB small business optimism print. Onto other events, The Fed’s Kashkari is scheduled to speak at a regional economic conference. The IMF and World Bank annual meetings also start today and run through to Saturday.

US Event Calendar

- 6am: NFIB Small Business Optimism 103, est. 105, prior 105.3

- 10am: Fed’s Kashkari Speaks at Regional Economic Conference

- 8pm: Fed’s Kaplan Speaks at Stanford Institute

- Oct. 10-Oct. 15: Annual Meetings of the IMF and the World Bank

DB’s Jim Reid concludes the overnight wrap

Markets were given their own lullaby yesterday with the US on partial hols thus resulting in a quiet session. It was actually a landmark day though as it marked 10 years since the pre-GFC peak in the S&P 500. At periodic intervals throughout this year we’ve marked such 10 year crisis related anniversaries with a quick performance review of the major asset classes from our regular monthly’s performance review. We repeat this today for this latest anniversary with the graph and the 10yr performance table today.

To summarise in dollar terms, the S&P 500 (+102%) actually tops our list of 38 global assets even though this point 10 years ago was the local peak. This is followed by US HY (+85%) and 6 of the top 8 in dollar terms are credit assets. Gold (+74%) breaks up the top 8. 26 of the 38 assets are in positive total return territory since this point and 12 are in negative territory led by Greek equities (-85%), European Banks (-54%) with other major underperformers including Portuguese equities (-39%), Oil (-38%), FTSE-MIB (-34%), Bovespa (-33%), Russian Micex (-30%), Shanghai Comp (-18%) and the IBEX (-2%). So although US equities and credit markets have shrugged off the impact of the crisis and have prospered, deep scars still remain especially for the European periphery and some EM equities (all dollar adjusted).

Turning to Catalonia, Spanish markets slightly rebounded on Monday (IBEX +0.50%, 10y bonds -3bp) following increased pressure over the weekend on the Catalan authorities to avoid declaring independence. We should have more clarity today as Catalan President Puigdemont is expected to address the regional Parliament in Barcelona (Tuesday, 6pm local time). Back on Monday, Spanish newswire Efe reported Puigdemont plans to declare independence, but is also likely to insist Catalonia wishes to negotiate with the Spanish government with the help of external mediators. Elsewhere, as per Bloomberg, Catalan secessionists have tried to urge the Spanish opposition Socialists to form a coalition to oust Spanish PM Rajoy, which they have since refused. A member of the Socialists’ executive board (Carmen Calvo) said her party is focused on ensuring that the Spanish Constitution is observed.

Over to Brexit, the UK government has published White papers or contingency plans for leaving EU without a new Brexit deal. In the papers, the UK will set up its own customs regime where it will set its own tariffs, quotas and classification of goods, broadly in line with WTO requirements. However, the FT noted that British officials admit these contingency plans are at early stages and the government has not really invested in staff and systems to build a new customs system yet. Following up, PM May spoke yesterday, noting “it is our responsibility as a government to prepare for every eventuality” and that these white papers “support that work”, which sets out “steps to minimise disruptions for businesses and travellers”. Further, she noted that re the Brexit talks the “ball is in their court”. However, the EU commission spokesman responded “the ball is entirely in the UK court for the rest to happen”. In view of the stalemate, we note that the fifth round of Brexit talks are currently underway and will conclude this Thursday.

This morning in Asia, markets are trading marginally higher as we type. The Kospi is up +1.93% after markets reopened following a 10 day break. Elsewhere, the Nikkei (+0.34%) and ASX 200 (+0.06%) are up slightly, while the Hang Seng (-0.06%) and Shanghai Comp. (-0.25%) are slightly lower.

Turning to Turkey, the Lira/USD fell to a 6 month low (Lira -2.46%; equities -2.73%) yesterday after the US and then Turkey suspended Visa services for citizens seeking to visit the other country over the weekend. While the White House has remained silent, the U S ambassador to Turkey went onto YouTube to say “we hope (the situation) will not last long, but…we can’t predict how long it will take to resolve this matter”. Later on Monday, Turkey’s Erdogan spoke during a news conference, noting “the implementation of such decision (suspending Visa services) by the US ambassador is very saddening. Turkey is a state of law, not a tribal state”. As a reminder, Turkey represents c1% of the MSCI emerging market index, c23% of its government debt is held by foreigners (highest since Aug. 2015) and c37k US citizens travelled to Turkey in 2016.

Onto market performance yesterday now. US bourses softened on limited news flow and trading, with the S&P 500 (-0.18%), Dow (-0.06%) and Nasdaq (-0.16%) all slightly down on light volumes. Within the S&P, marginal gains in the energy and utilities sectors were more than offset by losses from healthcare and industrial names. Conversely, European markets were modestly higher, aided by a rebound in Spain’s IBEX (+0.50%) and a solid IP reading from Germany. Across the region, the Stoxx 600 and DAX both rose c0.2% while the FTSE dipped 0.20%. The VIX has halted its trend of 8th consecutive days of being below 10, rising 0.68 to 10.33, likely reflecting increased geopolitical tensions. The record stretch was 10 days in July this year.

Bond markets were slightly firmer, with core European 10y bond yields down modestly, with Bunds (-1.6bp), OATs (-1.7bp) and Gilts (-0.6bp) all rallying. Elsewhere, peripherals slightly outperformed with Spanish and Italian 10y yields both down 3.4bp. At the 2y part of the curve, changes were more modest, with Bunds (-0.4bp) and OATs (-0.3bp) slightly down while Gilts were unchanged. Most key currencies were little changed with the US dollar index down 0.13% while the Euro gained 0.09%. Notably, Sterling had a solid day (+0.58%), partly due to a positive data revision to the UK labour cost figure (likely a better measure of pay growth). The Office of National Statistics conceded an error in its 2Q growth in unit labour costs, as it should be 2.4% yoy rather than 1.6% as reported on Friday. In commodities, WTI oil rose 0.59%, following reports that Saudi Arabia plans to make further cut to its crude supplies in November. Elsewhere, precious metals (Gold +0.58%; Silver +0.79%) were slightly higher, while other base metals were mixed, but little changed (Copper -0.27%; Zinc -0.13%; Aluminium +0.99%).

Away from the markets, ECB Executive Board member Sabine Lautenschlaeger said “we should begin reducing our bond purchases next year” and exit QE as soon as possible, but noted that “it is important that we really move towards the exit – step by step, but steadily and in a clear direction”. On inflation, she noted “looking to the future, we can be confident that inflation will return to our objective”.

Staying in Europe, some words of caution from politicians and central bankers. The ECB policy maker Klass Knot said it feels “increasingly uncomfortable” to have low volatility in markets while there are risks in the global economy. Elsewhere, in his departing interview with the FT as Germany’s longest servicing finance minister, Schaeuble warned that investors are “concerned about the increased risks arising from the accumulation of more and more liquidity and the growth in public and private debt, “I myself am concerned about this, too”.

Over in Japan, with only 12 days till the election, the latest polls suggests the challenger – Tokyo governor Koike’s new Party of Hope may be losing steam. According to a small survey by Yomiuri newspaper over the weekend, 13% of respondents said they will vote for her party, down from 19% a week ago. Notably, support for Abe’s LDP is at 32% and 27% of respondents are still undecided. Staying in Asia, China’s long serving People’s Bank of China Governor Zhou Xiaochuan reiterated calls for further opening up of China’s financial sector, as per Bloomberg. He said “we could take bigger steps to increase the market access for financial institutions and the opening up of the financial market”. The interview is perhaps conveniently timed before the Chinese Community Party meets tomorrow for a final time before the big party congress later in the month (potentially 18th October).

The latest ECB CSPP numbers were out yesterday. The average daily run rate last week was €356mn (vs. €349mn average since the CSPP started). This is at the low end of the recent range but the CSPP/PSPP ratio is still notably above the pre-taper ratio. The current week saw the ratio at 12.9% and is above the 11.6% seen before the taper (vs. 16.6%, 14.8%, 19.2%, 13.6% in the last few weeks). So still strong evidence that the ECB is tapering PSPP more than CSPP. It’ll be interesting to see what happens after the expected additional taper likely to be announced in just over two weeks.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In Germany, August IP was materially above expectations at 2.6% mom (vs. 0.9% expected) and 4.7% yoy (vs. 2.9%). Notably this stronger month follows two consecutive months of decline, so annualised growth over the quarter is c3.4% saar for total production. Our German team needs a strong Sep. IP and retail sales to get to their expected 0.6% qoq increase in 3Q GDP, although positive sentiment indicators makes them optimistic that we are getting there. Elsewhere, the Eurozone’s October Sentix investor confidence index slightly beat at 29.7 (vs. 28.5 expected) to a new post-GFC high, while France’s business industry confidence was a tad softer at 104 (vs. 105 expected).

Looking at the day ahead, it’s a fairly busy day, particularly in Europe. The most significant releases in Europe include the August industrial production prints for France (1.5% yoy expected), Italy (2.9% yoy expected) and the UK (0.9% yoy expected) along with August trade data for Germany and the UK. The only reading due in the US is the September NFIB small business optimism print. Onto other events, The Fed’s Kashkari is scheduled to speak at a regional economic conference. The IMF and World Bank annual meetings also start today and run through to Saturday.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed up 8.61 points or .26% /Hang Sang CLOSED UP 164.24 pts or .58% / The Nikkei closed UP 132.80 POINTS OR .64/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed WELL up at 6.5792/Oil UP to 50.23 dollars per barrel for WTI and 56.30 for Brent. Stocks in Europe OPENED RED EXCEPT FTSE . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.5792. OFFSHORE YUAN CLOSED STRONGER TO THE ONSHORE YUAN AT 6.5704 AND BOTH YUANS ARE STRONGER AGAINST THE DOLLAR. CHINA IS EXTREMELY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA/USA

South Korea ready to try out its new graphite “blackout bomb” which can paralyze North Korea’s antiquated power grid and yet cause no loss of life

(courtesy zero hedge)

South Korea’s New “Blackout Bomb” Can Paralyze The North’s Power Grid

US and South Korean officials are nervously watching to see if North Korea follows through with its threats to carry out another nuclear test – or to fire a rumored long-range missile capable of accurately striking the west coast of the US into the Pacific – in celebration of the Oct. 10 anniversary of the Communist Party’s creation. Meanwhile, the Telegraph reports that South Korea has developed a new weapon to hobble the North’s infrastructure should an armed conflict erupt on the peninsula. Given that it’s almost daybreak in North Korea, such a test could happen as soon as Monday night, Eastern Time.

The weapon is a graphite bomb – otherwise known as a “blackout bomb” – which South Korean officials say will be capable of shutting down North Korea’s entire power grid. Blackout bombs were first used by the US in Iraq in the 1990 Gulf War and work by releasing a cloud of extremely fine, chemically treated carbon filaments over electrical components. The filaments are so fine that they act like a cloud, but cause short circuits in electrical equipment.

As News.com.au points out, North Korea tends to celebrate the Oct. 10 holiday with military parades and aggressive rhetoric. But this year’s festivities could include new provocative weapons tests.

“The Kim regime usually uses these sorts of occasions to demonstrate some show of strength — in this current climate a missile test is a likely result,” says Dr Genevieve Hohnen, lecturer in politics and international relations at Edith Cowan University.

The Telegraph reports that the South developed the bomb to minimize civilian casualties in the North should a conflict erupt. In a statement to Yonhap, a military official said the South Korean army could assemble a blackout bomb at any time. The weapon was reportedly developed by South Korea’s Agency for Defense Development.

“All technologies for the development of a graphite bomb led by the ADD have been secured. It is in the stage where we can build the bombs anytime,” a military official told Yonhap.

The bomb is often referred to as a “soft bomb” because it only affects targeted electrical power systems.

As the Telegraph explains, the blackout bomb was developed as part of South Korea’s “three pillars” plan for retaliating against the North if it believes a nuclear strike is imminent. Escalating tensions with the North have inspired the South to move its target date for completion forward by three years. The plan was initially slated to be complete by the mid-2020s.

The first two parts of the plan involve detecting – and then intercepting – North Korea missiles. The second part – aptly named the “massive punishment and retaliation plan” involves launching attacks against the country’s leadership, including a plan to assassinate Kim Jong Un.

South Korea is bringing forward the deployment of its “three pillars” of national defence by as much as three years as a result of the growing threat posed by Pyongyang’s nuclear and missile development programmes.

The three-pronged strategy was originally scheduled to be in place by the mid-2020s, but North Korea’s increasingly aggressive and unpredictable behaviour has forced Seoul to revise that timeline.

The Kill Chain programme is designed to detect, identify and intercept incoming missiles in the shortest possible time and operates in conjunction with the Korea Air and Missile Defence system for lower-tier defence against inbound missiles.

The final component of the strategy is the Korea Massive Punishment & Retaliation plan, under which Seoul will launch attacks against leadership targets in North Korea if it detects signs that the regime is planning to use nuclear weapons.

South Korea believes North Korea’s energy grid is outdated and vulnerable, and thus would be incredibly susceptible to a “blackout bomb” attack. Blackout bombs were first used by the US against Iraq in the Gulf War of 1990, when they knocked out about 85 percent of Iraq’s electricity. They were also used by NATO against Serbia in 1999, when it damaged around 70 percent of the country’s electrical supply.

* * *

President Donald Trump fired off his latest threatening tweet about North Korea earlier today, reiterating his view that 25 years of US appeasement and billions of dollars in humanitarian aid for the North clearly have not worked. He ended the tweet with yet another vague hint that the US could soon resort to a military strike.

Our country has been unsuccessfully dealing with North Korea for 25 years, giving billions of dollars & getting nothing. Policy didn’t work!

Though the US has rejected North Korea’s claims that Trump’s rhetoric has amounted to a declaration of war, how much longer can the US credibly claim that “all options are on the table” if North Korea continues to provoke the international community with its missile and nuclear tests?

North Korea Hackers Steal War Plans, Kim Jong-Un Assassination Details

While tensions with North Korea have receded in recent weeks, and especially following the latest uneventful weekend, when markets were on edge that Kim could try another missile test launch to celebrate the country’s national holiday, this could reverse following news from the BBC that North Korea hackers have reportedly stolen a large cache of military documents from South Korea, including a plan to assassinate North Korea’s leader Kim Jong-un.

According to South Korean lawmaker Rhee Cheol-hee – a member of South Korea’s ruling party who sits on its parliament’s defence committee – the compromised documents, which were stolen from the country’s defense ministry, include wartime contingency plans created by the US and South Korea, and also include reports to the allies’ senior commanders. Plans for the South’s special forces are also said to have been accessed, along with information on significant power plants and military facilities in the South.

Rhee also said some 235 gigabytes of military documents had been stolen from the Defence Integrated Data Centre, and that 80% of them have yet to be identified.

Just like in the case of Equifax, the breach itself took place long ago, with South Korea waiting over a year to disclose the full details of the the hack which took place in September last year. In May, South Korea said a large amount of data had been stolen and that North Korea may have instigated the cyber attack – but gave no details of what was taken. The South Korean defence ministry has so far refused to comment about the allegation, while North Korea denied the claim.

According to South Korea’s Yonhap news agency reports that Seoul has been subject to a barrage of cyber attacks by its communist neighbour in recent years, with many targeting government websites and facilities. According to long-running media reports, which have yet to be confirmed with hard evidence however, the isolated, backward state is believed to have specially-trained hackers based overseas, including in China.

One thing that’s certain, is that tews that Pyongyang is “likely to have accessed the Seoul-Washington plans for all-out war” in the Koreas will do nothing to soothe tensions between the US and North Korea. The two nations have been at verbal loggerheads over the North’s nuclear activities, with the US pressing for a halt to missile tests and Pyongyang vowing to continue them.

Meanwhile, away from cyber war, Pyongyang has been far more aggressive in the realm of unconventional warfare, and the North recently claimed to have successfully tested a miniaturised hydrogen bomb, which could be loaded onto a long-range missile. In a speech at the UN in September, US President Donald Trump threatened to destroy North Korea if it menaced the US or its allies, and said its leader “is on a suicide mission”.

Kim responded with a rare televized statement, vowing to “tame the mentally deranged US dotard with fire”. Trump’s latest comment took the form of a cryptic tweet at the weekend, where he warned that “only one thing will work” in dealing with North Korea, after years of talks had proved fruitless. He did not elaborate further.

b) REPORT ON JAPAN

USA sends a nuclear submarine to the Korean Peninsula and will engage in more military exercises with South Korea and Japan

(courtesy zero hedge)

US Sends Nuclear Submarine To Korean Peninsula For More Military Drills

As US forces prepare to join their South Korean partners for yet another round of the military exercises that North Korean Leader Kim Jong Un is so fond of, the US has sent a nuclear-powered sub to participate.

The nuclear-powered submarine Michigan will arrive in the Korean port city of Busan, situated in the southern part of the country, by the end of the week, according to Bloomberg, which cited local media reports.

The sub will conduct joint drills with the US aircraft carrier USS Ronald Reagan in the waters off the peninsula next week.

With North Korea celebrating the founding of the country’s ruling Communist Party on Oct. 10, US and South Korean defense officials are anticipating that the country could launch another provocative missile test as soon as tonight.