GOLD: $1277.10 DOWN $2.55

Silver: $16.95 DOWN 10 cents

Closing access prices:

Gold $1277.00

silver: $16.95

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1290.44 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1281.80

PREMIUM FIRST FIX: $8.64(premiums getting larger)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1291.54

NY GOLD PRICE AT THE EXACT SAME TIME: $1281.30

Premium of Shanghai 2nd fix/NY:$10.24 PREMIUMS GETTING LARGER)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1278.30

NY PRICING AT THE EXACT SAME TIME: $1277.90

LONDON SECOND GOLD FIX 10 AM: $1276.45

NY PRICING AT THE EXACT SAME TIME. 1276.90

For comex gold:

OCTOBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH: 562 NOTICE(S) FOR 56,200 OZ.

TOTAL NOTICES SO FAR: 3005 FOR 300,500 OZ (9.346TONNES)

For silver:

OCTOBER

167 NOTICES FILED TODAY FOR

835,000 OZ/

Total number of notices filed so far this month: 965 for 4,825,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: $5693 bid /$5713 offer DOWN $166.00 (MORNING)

BITCOIN CLOSING;$5665 BID:5685. OFFER DOWN $191.00

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY ONLY 240 contracts from 192 ,364 DOWN TO 192,124 WITH RESPECT TO YESTERDAY’S TRADING (up 2 CENTS). THE CROOKS ARE STILL HAVING AN AWFUL TIME TRYING TO COVER THEIR MASSIVE SILVER SHORTS SO THEY ONCE AGAIN ORGANIZE ANOTHER ATTEMPTED RAID ON OUR PRECIOUS METALS TODAY.

RESULT: A SMALL SIZED FALL IN OI COMEX WITH THE 2 CENT PRICE RISE. OUR BANKERS COULD NOT COVER MUCH OF THEIR HUGE SHORTFALL SO ANOTHER RAID WAS CALLED UPON.

In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.962 BILLION TO BE EXACT or 137% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 167 NOTICE(S) FOR 835,000 OZ OF SILVER.

In gold, the open interest FELL BY 1923 CONTRACTS DESPITE THE TINY RISE IN PRICE OF GOLD ($0.30) . The new OI for the gold complex rests at 527,390. OUR BANKER FRIENDS NO DOUBT COVERED A BIT OF THEIR SHORTFALL WITH THE TINY RISE IN PRICE BUT NOT ENOUGH FOR THEIR LIKING. THUS THEY CALLED FOR ANOTHER RAID TRYING TO SHAKE MORE GOLD/SILVER LEAVES TO FALL.

Result: A SMALL SIZED DECREASE IN OI WITH TINY RISE IN PRICE IN GOLD ($0.30). WE HAD SOME BANKER GOLD SHORT COVERING AS THE BANKERS FAILED MISERABLY TO LOOSEN ANY GOLD LEAVES FROM THE GOLD TREE YESTERDAY..SO THEY ORGANIZED ANOTHER RAID THIS MORNING.

we had: 562 notice(s) filed upon for 56,200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Tonight , NO CHANGES in gold inventory at the GLD/

Inventory rests tonight: 853.13 tonnes.

SLV

Today: STRANGE!! WITH SILVER CLOSING HIGHER WE HAD A WITHDRAWAL OF 1,039,000 OZ FROM THE SLV

INVENTORY RESTS AT 320.288 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY ONLY 240 contracts from 192,364 DOWN TO 192,124(AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) . OUR BANKERS WERE AGAIN UNSUCCESSFUL IN THEIR ATTEMPT TO COVER MUCH OF THEIR SILVER SHORTS.

RESULT: A SMALL DECREASE IN SILVER OI AT THE COMEX WITH THE TINY RISE IN PRICE OF 2 CENTS (WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKER FRIENDS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO COVER MUCH OF OUR SILVER SHORTS SO ANOTHER RAID WAS ORCHESTRATED THIS MORNING.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 7.55 points or .22% /Hang Sang CLOSED DOWN 150.91 pts or 0.53% / The Nikkei closed UP 108.52 POINTS OR .50/Australia’s all ordinaires CLOSED UP 0.09%/Chinese yuan (ONSHORE) closed UP at 6.6314/Oil UP to 52.27 dollars per barrel for WTI and 57.73 for Brent. Stocks in Europe OPENED IN THE GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6314. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6331 AND //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/USA/UK

Boris Johnson, Sec of State for Great Britain refuses to rule out a “preemptive strike” against North Korea

( Mac Slavo/SHFTPlan.com)

b) REPORT ON JAPAN

c) REPORT ON CHINA

The 19th Congress will be over shortly, The Congress has now stated that Xi is the most powerful leader since Mao. As for succession, let us see who walks out with him…

Also now that he is confirmed, let us see if they adopt the new Yuan for oil for gold policy..

( zerohedge)

4. EUROPEAN AFFAIRS

As we have highlighted to you on many occasions, the Muslim migration into Italy is becoming a huge crisis

( GEFIRA)

ii)GERMANY/RUSSIA

Germany’s delegation to Russia is another dagger into the heart of USA hegemony as Merkel is looking for new allies

( George Friedman (Stratfor)/Mauldin Economics)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAQ

Another dagger for the USA: the Shia Militia leader tells the USA to get ready to leave Iraq

( zerohedge)

ii)TURKEY/USA

The fun begins; the USA has just declined to issue visas for a delegation from Turkey’s Justice Ministry

check to Mr Erdogan

( zero hedge)

6 .GLOBAL ISSUES

This Bellwether stock soars 7% to an all time high after smashing earnings as well as boosting guidance. The reason: commodity prices are increasing

( zero hedge)

7. OIL ISSUES

Both WTI and Gasoline extend their gains after major gas and distillate drawdowns

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)I agree with Ted that the real reason that Mocatta wants to get out of the silver short business is due to its huge losses. Their problem will be two-fold:

- nobody will want to take the liability

- even if they try and shut their business, the 75 million oz of silver short remains as it is impossible to cover

( Ted Butler)

ii)No surprise here: Venezuela lost its gold that it pawned off to Deutsche bank.

( zerohedge)

iii)We brought you this story yesterday but it is worth repeating. A jury finds an ex HSBC executive guilty of front running a 3.5 billion currency trade. This is just one trade. You can imagine the thousands of trades that these guys executed in gold and silver

( Reuters/GATA)

iv)Ecuador now seems to be the next gold frontier as the country now wants gold/silver exploration

( Dave Forest/OilPrice.com)

10. USA Stories

i)This will go down as the worst scandal in USA history: the Clinton Foundation and the Uranium deal with Putin

( Ortel)

ii)Hillary is lying through her eye teeth as evidence is mounting against her. She can no longer ignore the burgeoning scandal and Jeff Sessions must detail all of her Clinton Foundation donations which is basically a pay for play criminal organization

( zerohedge)

iii) Hillary is having a bad hair day as House Committees finally announce an investigation into Hillary’s approval of Russia’s Uranium One deal

( zerohedge)

iiib)And now James Comey is having a bad hair day as the House is launching a probe into how the FBI handled the Clinton email scandal

( zerohedge)

iv)Trump heads to the Hill as a feud erupts between the President and Corker, just hours before a critical senate meeting. Trump can ill afford to lose some Republicans in his tax reform bill

( zerohedge)

iv b) As promised, I doubt very much if the USA will get its tax reform. There are 3 Republicans that appear to be against the reform:

Rand Paul, Corker and now McCain

(courtesy zerohedge)

iv c) First it was Bob Corker who stated that he would not run in the 2018 race and now Arizona Senator Jeff Flake stated that he would not run. Looks like the Republican party is disintegrating.

( zerohedge)

v)Despite the 2 hurricanes which wiped out huge numbers of cars, the inventory levels at various GM plants are still high

( zerohedge)

( Ron Paul)

vii)The bond king, Jeff Gundlach warns that the financial system is about to be turned upside down and states to get out of bonds

viii)This will not be good for our big on line advertisers as giant Interpublic tumbles due to its warning on the state of the ad industry. Most of our high tech firms rely on advertising for their profits.( zerohedge)

Let us head over to the comex:

The total gold comex open interest FELL BY 763 CONTRACTS DOWN to an OI level of 527,390 DESPITE THE RISE IN THE PRICE OF GOLD ($0.30 RISE IN YESTERDAY’S TRADING). OUR BANKER FRIENDS HAD MINIMAL SUCCESS IN THEIR ATTEMPT TO COVER THEIR HUGE GOLD SHORTFALL BUT NOT ENOUGH FOR THEIR LIKING. THEY THUS CALLED FOR ANOTHER RAID THIS MORNING HOPING MORE GOLD/SILVER LEAVES WILL FALL.

OCTOBER IS AN ACTIVE DELIVERY MONTH ALTHOUGH IT IS THE WEAKEST IN TERMS OF ACTUAL DELIVERIES AND OPEN INTEREST. WE VISUALIZED THAT THROUGHOUT THE MONTH OF SEPTEMBER, THE CROOKS UTILIZED THE EMERGENCY EFP SCHEME TO TRANSFER OBLIGATIONS OVER TO LONDON. IT THEN STANDS TO REASON THAT IF THE EMERGENCY WAS IN FORCE THROUGHOUT THE MONTH OF SEPTEMBER IT WOULD CONTINUE ON FIRST DAY NOTICE WHEREBY ANOTHER 7200 LONG COMEX CONTRACTS WERE GIVEN 7200 EFP’S.

Result: a SMALL SIZED open interest DECREASE DESPITE THE RISE IN THE PRICE OF GOLD ($0.30.) .THERE WAS MINIMAL SHORT COVERING FRIDAY WITH THE BANKERS SLIGHTLY DECREASING TO THEIR HUGE SHORTFALL.

.

We have now entered the active contract month of Oct and here we saw a GAIN of 66 contracts UP TO 752 contracts. We had 0 notices filed yesterday so we GAINED 66 contracts or an additional 6,600 oz will stand for delivery at the comex in this active delivery month of October and 0 EFP notices were given. The low number of notices early in the delivery cycle is evidence of a lack of physical gold. We have just witnessed yet another queue jumping in the gold comex which is another indicator of physical shortage. TO SEE THIS IN BOTH GOLD AND SILVER MUST BE HEARTENING TO US!!

The November contract saw A loss OF 11 contracts down to 888.

The very big active December contract month saw it’s OI loss OF 3,338 contracts DOWN to 395,986

.

We had 562 notice(s) filed upon today for 56,200 oz

VOLUME FOR TODAY (PRELIMINARY) N/A

CONFIRMED VOLUME YESTERDAY: 297,084

We had 167 notice(s) filed for 835,000 oz for the OCT. 2017 contract

Oct.24/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

562 notice(s)

56,200OZ

|

| No of oz to be served (notices) |

190 contracts

(19,000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

3005 notices

300,500 oz

9.3468 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 562 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 117 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

16,942.54 oz

CNT

|

| Deposits to the Dealer Inventory |

2,402,115.160 oz

Brinks

|

| Deposits to the Customer Inventory |

1,499,296.190

HSBC

Brinks

CNT

oz

|

| No of oz served today (contracts) |

167 CONTRACT(S)

(835,000,OZ)

|

| No of oz to be served (notices) |

61contracts

(305,000 oz)

|

| Total monthly oz silver served (contracts) | 965contracts

(4,825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | xx oz |

NPV for Sprott and Central Fund of Canada

will update later tonight

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott Inc. to take control of rival gold holder Central Fund of Canada

Posted Oct 2, 2017 8:43 am PDT

Last Updated Oct 2, 2017 at 9:20 am PDT

TORONTO – Sprott Inc. (TSX:SII) says it has struck a deal to take control of rival gold-holding firm Central Fund of Canada Ltd. (TSX:CEF.A) after a protracted takeover effort.

Toronto-based Sprott said Monday it will pay $120 million in cash and stock for Central Fund of Canada Ltd.’s common shares and for the right to administer and manage the fund’s assets.

The deal, which requires approval from Central Fund shareholders, would see its class A shareholders transferred to a new Sprott Physical Gold and Silver Trust.

Sprott says the deal would add $4.3 billion to its assets under management, which are focused largely on holding physical precious metals on behalf of clients, and 90,000 investors to its client base.

In March, Sprott tried to go through the Court of Queen’s Bench of Alberta to allow Central Fund’s class A shareholders to swap their shares to Sprott after the family that controls Central Fund rebuffed their attempt to make a deal.

Last year Sprott took over Central GoldTrust, a similar fund controlled by the same family, after securing support from more than 96 per cent of shareholder votes cast.

END

And now the Gold inventory at the GLD

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

Oct 17./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

Oct 16/A HUGE WITHDRAWAL OF 5.32 TONNES FROM THE GLD/INVENTORY RESTS AT 853.13 TONNES

0CT 13/ NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 12/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

SEPTEMBER 29/no changes in gold inventory at the GLD/Inventor rests at 864.65 tonnes

Sept 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.65 TONNES

Sept 27/WOW!! WITH GOLD DOWN $13.25, WE HAD A HUGE 8.57 TONNES OF GOLD ADDED TO THE GLD/

Sept 26/no changes in gold inventory at the GLD/Inventory rests at 856.08 tonnes

Sept 25./Another big deposit of 3.84 tonnes into GLD/Inventory rests tonight at 856.08 tonnes

Sept 22/with gold up only 1 dollar on the day we had a massive 6.21 tonnes of gold added to the GLD/.this is a good sign that gold will advance nicely this coming week.

Sept 21/no change in gold inventory tonight/inventory rests at 846.03 tonnes

Sept 20/no change in gold inventory tonight/inventory rests at 846.03 tonnes

Sept 19/another deposit of 2.07 tonnes of gold into the GLD/inventory rests at 846.03 tonnes

Sept 18/a huge 5.32 tonnes of gold deposit into the GLD despite gold’s whack today/inventory rests at 843.96 tonnes

Sept 15./strange!!no change in GLD after the whacking of gold/inventory remains at 838.64 tonnes

Sept 14./no changes at the GLD/inventory rests at 838.64 tonnes

Sept 13/late last night a huge 4.14 tonnes of gold was added to the GLD inventory/inventory rests at 838.64 tonnes.

Sept 12/as of 5: 40 pm est, no changes in gold inventory at the GLD/Inventory rests at 834.50 tonnes

Sept 11/Today we had a rather large 2.37 tonnes of gold removed from the GLD/Inventory rests at 834.50 tonnes

Sept 8/we had a tiny withdrawal of .34 tonnes and probably that would be to pay for fees like insurance etc.

Inventory rests at 836.87 tonnes

end

Now the SLV Inventory

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Oct 17/ A MONSTROUS WITHDRAWAL OF 3.494 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 322.271 MILLION OZ

Oct 16/ NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 325.765 MILLION OZ

oCT 13/ NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 12/THE LAST TWO DAYS WE LOST 1.113 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

SEPTEMBER 29/no changes in silver inventory at the SLV/inventory rests at 326.757 million oz/

Sept 28/NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ/

Sept 27/STRANGE!! SILVER IS HIT FOR 24 CENTS YESTERDAY AND. 9 CENTS TODAY AND YET NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ

Sept 26./no change in silver inventory at the SLV/.inventory rests at 326.757 million oz

Sept 25./ a big deposit of 1.842 million oz into the SLV/inventory rests at 326.757 million oz/

Sept 22/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz/

Sept 21/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz

Sept 20/no changes in silver inventory/Inventory remains at 324.915 million oz

Sept 19/strange!! another withdrawal of 1.134 million oz despite the rise in silver/inventory rests at 324.915 million oz

Sept 18/a withdrawal of 1.039 million oz from the SLV/Inventory rests at 326.049 million oz

Sept 15./no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 14/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 13/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 12.2017/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 11.2017: no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Sept 8/no change in silver inventory at the SLV/Inventory rests at 327.088 million oz/

Oct 24/2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.34%

Indicative gold forward offer rate for a 6 month duration+ 1.34% -

+ 1.58%

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Is Better Store of Value Than Bitcoin – Goldman Sachs

Gold is better store of value than bitcoin – Goldman Sachs report

– Gold will continue to perform well thanks to uncertainty and wealth demand

– Bitcoin’s volatility continues to impact its role as money

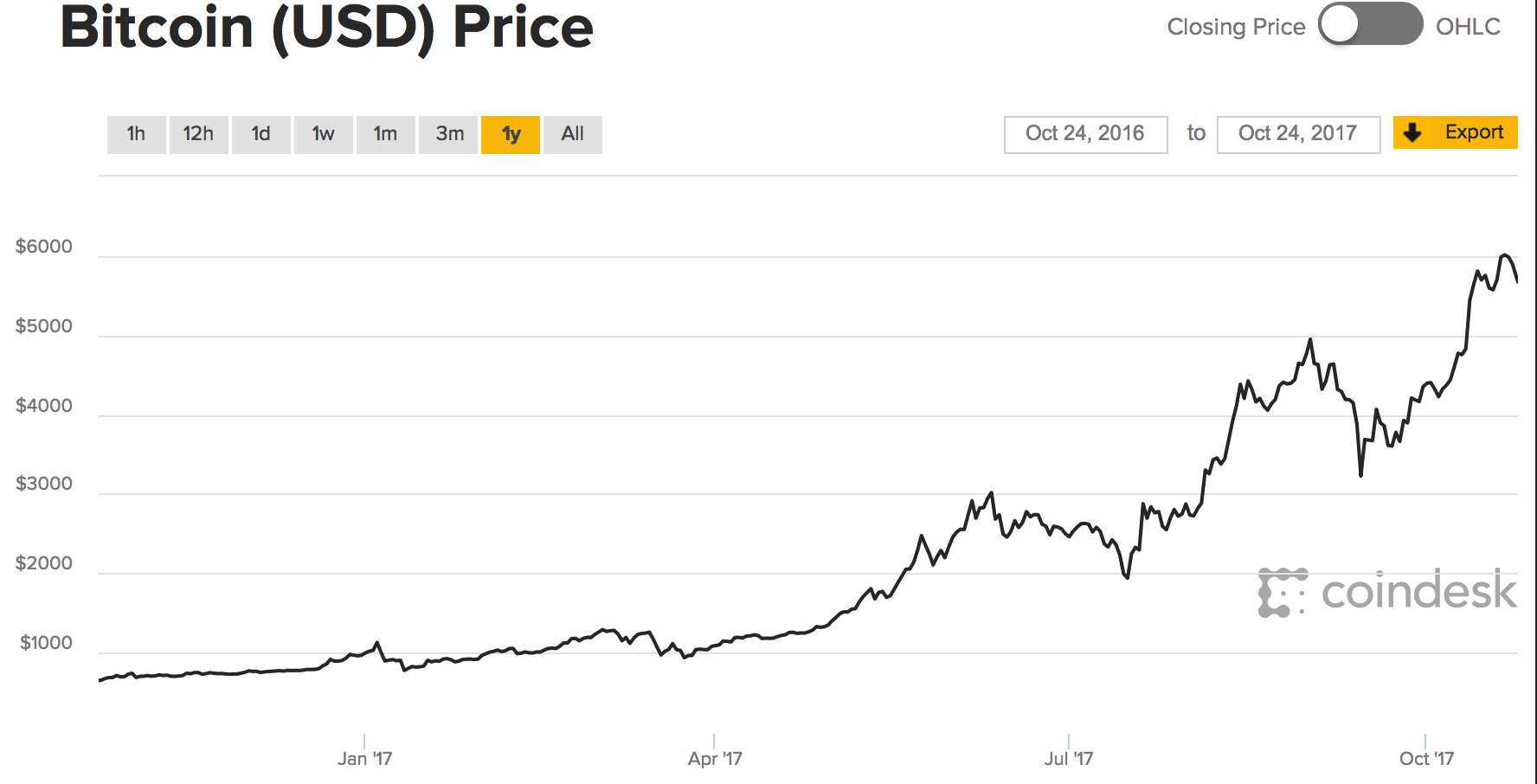

– Gold up 12% in 2017, bitcoin over 600%

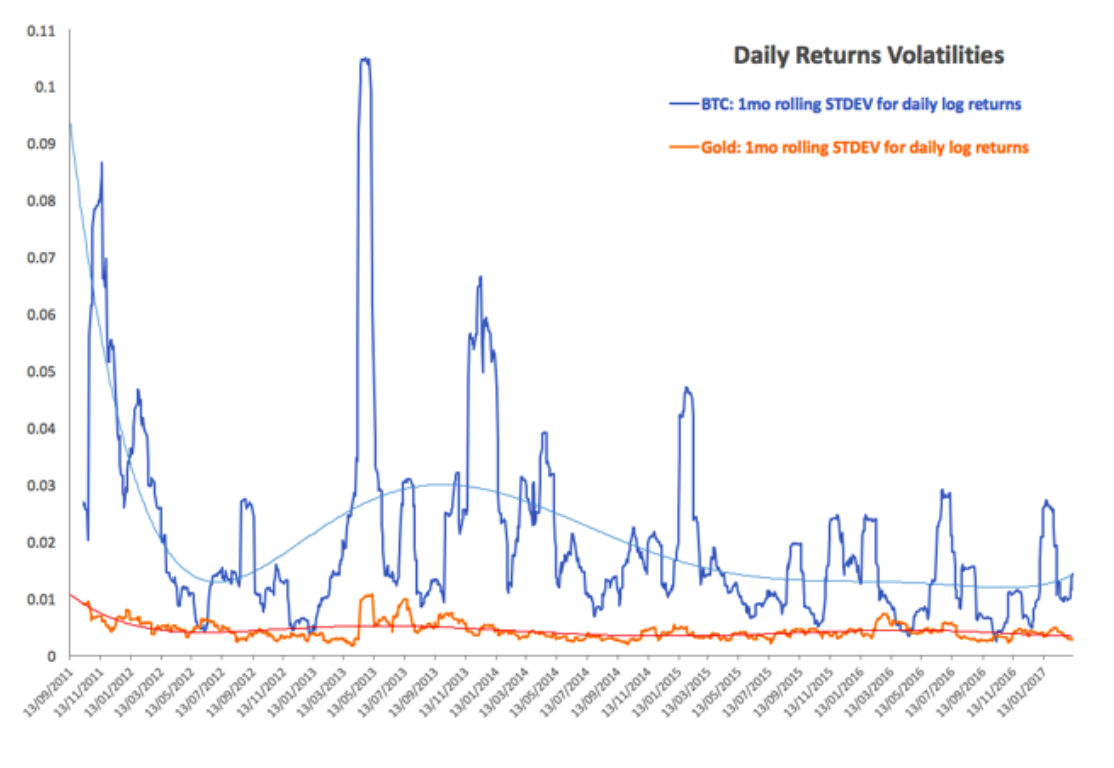

– BTC is six times more volatile than gold – see chart

– Gold’s history and physical property shows it meets requirements as a medium of exchange and store of value

Since the birth of bitcoin there has been one question that has repeatedly grabbed headlines and led debates all over the world – will bitcoin replace gold?

The latest to weigh in on this question is Goldman Sachs which, in a research note entitled ‘Fear and Wealth’, has concluded that gold is better than bitcoin.

Examining gold and bitcoin against the key characteristics of money, the report concludes that “Precious metals remain a relevant asset class in modern portfolios, despite their lack of yield…They are neither a historic accident or a relic.”

Goldman Sachs looked at four key properties of a long-term store of value – durability, portability, intrinsic value and unit of account – concluding that the reasons why gold was originally adopted remain relevant to today.

They believe as the level of uncertainty increases investors increase their exposure to gold. Fear is the medium to short-term driver of the gold price. The long-term driver, Goldman Sachs believes, is wealth.

The debate of gold versus bitcoin is really a rather tedious one. So rarely do you see any other two assets pitched against one another. Yet those choosing to debate it manage to find common ground between the two, so the debate rages on. Bitcoin’s finite supply and occasional rise on the back of geopolitical tensions has led to such comparisons.

Conversely the debate is relevant as both assets are ones which evoke a strong emotive reaction and raise similar questions about the state of the economy and the investment space. As bitcoin’s market cap increases (heading to $100 billion) it is inevitable that it will continue to grab the attention of the likes of Goldman Sachs and institutional investors. Most recently, Ray Dallio, the world’s biggest fund manager felt the need to point out the bitcoin bubble and how he favoured gold over the cryptocurrency.

The debate is of particular interest this year given bitcoin’s performance. It has climbed from around $1,000 at the start of the year to nearly $6,000. In the same period gold is up 12%.

“Gold wins out over cryptocurrencies in a majority of the key characteristics of money,”

The first record of gold being used as money is from around 700 B.C. when the Lydians combined it with silver, to form electrum coins.

Bitcoin’s role as money is one which is still being established. Many of the problems it faces are down to infrastructure and price volatility.

Goldman Sachs addressed the main characteristics that make a medium of exchange and found gold to outperform bitcoin.

The findings were summarised by Bloomberg:

Durability: While both require expertise for correct long-term storage, gold wins because cryptocurrencies are vulnerable to hacking through online wallets or the user’s computer or smartphone, are subject to regulatory risk, and network and infrastructure risk during a crisis.

Portability: Transferring bullion can be expensive, given its weight, need for a high level of security and high import taxes in some countries, such as India. In contrast, it’s much faster and cheaper to move bitcoins.

Intrinsic value: There’s a limited supply of gold and other precious metals in the Earth’s crust, whereas in the case of cryptocurrencies, it’s easy to create alternatives, meaning there’s effectively no control over supply at a macroeconomic level and no intrinsic value due to rarity.

Unit of account: Gold is better at holding its purchasing power, and has much lower daily volatility. Bitcoin/dollar volatility has averaged almost seven times that of gold in 2017, the bank said.

Chart from March 2017

In regard to volatility the Fear and Wealth report stressed how “a 3-day USD/BTC put option at historical average volatility results in a premium of around 2.3%.” This is clearly a prohibitive premium. Fiat to bitcoin volatility this year stands at more than six times that seen with gold.

The authors conclude that these factors “clearly illustrate that Bitcoin as a unit of account and medium of exchange is nowhere near as favourable as it first appears.”

Is gold that immovable?

Goldman Sachs found gold was only at a disadvantage to bitcoin when it came down to portability. This is something that is often cited about gold.

Bullion is often accused of being bulky and therefore dysfunctional as a form of money. However, there are two main factors that are overlooked by those who argue this:

– Size of gold bars and coins relative to value

If you consider that the high income households in the UK are estimated to have around £63,000 (on average) in savings then this would be just 2 kilogram bars of gold. About the size of a smart phone each. Not exactly immovable.

Then consider coins, far more portable and a great way to divide up your gold holdings.

Should you hold gold (either at home or in a vault) then you are rarely under the same requirements to move the gold as you are if you had the equivalent held in a bank. Often banks demand a few days’ notice, or limit the amount of cash you can move in one go. Arguably, less portable than a trusty gold bar.

– Technology

In order to spend bitcoin you are required to be ‘online’. Fantastic for those of us who are able to go anywhere without worrying about connectivity. Not so great for those countries, remote areas or disaster struck places (such as Puerto Rico) that do not find it so easy to just jump online and shift a few bitcoin.

Spending a few gold coins, or even a small gold bar, does not require you to partake in an online transaction. Should you find yourself in a position where you need to spend your gold, a power outage or loss of connection will not be your biggest problem.

Uncertainty and fear: the drivers of gold

It is interesting that given the title of the report is Fear and Wealth, the authors do not consider why gold’s portability is relevant and addresses fears surrounding uncertainty.

There are a number of fears about the direction both the financial and political spheres are heading in. Consider real interest rates issues, debasement, sovereign balance-sheet, geopolitical and other market risks.

The main fear is that no-one knows how bad things will be and so investment decisions are coming down to uncertainty. This is good for gold and its price.

“Stated more simply, we are talking about the drivers of ‘risk-on, risk-off’ behavior in markets…This factor matters so much to gold precisely because it is a safe-haven asset. Accordingly, as uncertainty increases, preferences shift towards having more gold in the portfolio, driving prices higher.”

People like to hold gold because they can balance the uncertainty with the certainty that gold will be accepted regardless of how things pan out. Holders know that they can easily transport and transfer it, in order to make an exchange for goods. They cannot know this with bitcoin, both because of its design and because it has never been tested in such a way.

Gold investors are also exposed to far less uncertainties when it comes to professional storage, something Goldman Sachs does acknowledge:

“While both require expertise for correct long-term storage, gold wins because cryptocurrencies are vulnerable to hacking through online wallets or the user’s computer or smartphone, are subject to regulatory risk, and network and infrastructure risk during a crisis,”

Despite this acknowledgement it is interesting that ‘portability’ is still seen as a negative for gold. This has not restricted gold too much in the past.

Long-term investors are clearly also not too concerned about portability either. Goldman Sachs believes these investors are the key to gold’s long-term performance, thanks to a desire to build and protect their wealth.

Gold’s future

Goldman Sachs forecasts that emerging market economies will be the key drivers of wealth-based demand for gold.

“As more EM economies — including China — are set to grow to these income levels over the next few decades, the underlying long-term demand picture remains supportive of gold prices…While fear can spike or fall relatively quickly, wealth tends to accumulate slowly. This makes wealth an important, but easy to overlook in short-term forecasting, driver of gold.”

The likes of China and India are experiencing a rapidly growing middle-class, all of whom are interested in buying gold. Between the two countries they account for 60% of the global jewellery market.

This is likely to boost long-term demand for the precious metal given rapid accumulation of gold tends to occur when per-capita gross domestic product reaches roughly $20,000 to $30,000.

There is still a long-way to go for 29 developing countries, each of whom have an interest in holding gold.

“Our modeling, based on the historical experiences of 29 countries at various stages of development since the early 1990s, suggests that this is still very far from peak annual demand,”

Uncertainty will lead to wealth protection in the future

Goldman Sachs expects to see the price of gold falter somewhat before reaching nearly $1,400/oz in 2018. The expected stumble is down to tightening of monetary policy and a moderation of the fear factor.

Investors should not be put off by Goldman Sachs’ forecast. If there is any takeaway from their report it is that gold is both a long-term investment and a safe haven.

Whilst fear and uncertainty may well subside, they will not disappear until the factors that cause them also vanish. In all likelihood this is impossible without years of serious economic and political change. Unlikely, especially in the West with short-term policies for maximum political gains and disastrous economic consequences.

By showing gold has true value as a medium of exchange and store of value, Goldman Sachs has demonstrated how important it is to hold some in your portfolio. You may not feel fearful but you cannot be be sure of no uncertainties.

Those who hold gold as a form of financial insurance will benefit in two ways. Firstly, they have a balanced portfolio that will support them in times of unforeseen crises. Secondly, should a crisis be averted then gold will accumulate in value as fiat devaluation continues, thus still protecting the investor and their savings.

Bitcoin has done a stellar job in motivating millennials into taking an interest in money and investments, however the cryptocurrency market is in itself an entire uncertainty. It’s main premise – as a medium of exchange – has been rapidly dismissed on several accounts.

As throughout history, gold remains a vital store of value. It’s role as money and as a safe haven continues to be proven thanks to the actions of central bankers and those using technology to affect monetary markets.

News and Commentary

Gold recovers from two-week low on softer dollar (Reuters.com)

Gold recovers from 2-week lows and rises above $1280 (FXStreet.com)

Wall St. retreats from record highs; tech, industrials drag (Reuters.com)

U.S. Stocks Drop at Start of Big Week for Earnings (Bloomberg.com)

Venezuela allows $1.7 billion gold swap with Deutsche to lapse (Reuters.com)

Spanish Banks Fall on Fresh Political Upheaval (TheStreet.com)

Source: US Funds via Forbes

Here’s Why Bitcoin Won’t Replace Gold So Easily (Forbes.com)

Americans Have More Debt Than Ever — Creating An Economic Trap (BusinessInsider.com)

Here Is The IMF’s Global Financial Crash Scenario (ZeroHedge.com)

Politicians and Unfolding Pensions Disaster – Are You Infuriated Yet? (GoldSeek.com)

History Of Gold and Silver Flows From South America to Medieval Europe and Today (LMBA.org)

Gold Prices (LBMA AM)

24 Oct: USD 1,278.30, GBP 970.36 & EUR 1,087.32 per ounce

23 Oct: USD 1,275.25, GBP 967.79 & EUR 1,085.62 per ounce

20 Oct: USD 1,280.25, GBP 974.27 & EUR 1,084.76 per ounce

20 Oct: USD 1,280.25, GBP 974.27 & EUR 1,084.76 per ounce

19 Oct: USD 1,283.40, GBP 975.64 & EUR 1,087.42 per ounce

18 Oct: USD 1,280.65, GBP 972.53 & EUR 1,090.47 per ounce

17 Oct: USD 1,289.70, GBP 973.47 & EUR 1,097.02 per ounce

Silver Prices (LBMA)

24 Oct: USD 17.04, GBP 12.92 & EUR 14.49 per ounce

23 Oct: USD 17.00, GBP 12.90 & EUR 14.47 per ounce

20 Oct: USD 17.08, GBP 12.96 & EUR 14.46 per ounce

20 Oct: USD 17.08, GBP 12.96 & EUR 14.46 per ounce

19 Oct: USD 17.03, GBP 12.93 & EUR 14.40 per ounce

18 Oct: USD 16.95, GBP 12.86 & EUR 14.42 per ounce

17 Oct: USD 17.11, GBP 12.96 & EUR 14.55 per ounce

Recent Market Updates

– Next Wall Street Crash Looms? Lessons On Anniversary Of 1987 Crash

– Key Charts: Gold is Cheap and US Recession May Be Closer Than Think

– Gold Up 74% Since Last Market Peak 10 Years Ago

– How Gold Bullion Protects From Conflict And War

– Silver Bullion Prices Set to Soar

– Brexit UK Vulnerable As Gold Bar Exports Distort UK Trade Figures

– Puerto Rico Without Electricity, Wifi, ATMs Shows Importance of Cash, Gold and Silver

– U.S. Mint Gold Coin Sales and VIX Point To Increased Market Volatility and Higher Gold

– Global Outlook – Mad, Mad, Mad, MAD World: News in Charts

– Young Guns of Gold Podcast – ‘The Everything Bubble’

– London House Prices Are Falling – Time to Buckle Up

– Perth Mint Gold Coins Sales Double In September

– Survey shows UK and US Pensions Crisis is Imminent

-END-

(COURTESY CHRIS POWELL ON TED BUTLER’S LATEST PIECE)

Ted Butler: Fear of silver shorting spurs Scotia to sell its metals division

Submitted by cpowell on Mon, 2017-10-23 17:39. Section: Daily Dispatches

12:39 CT Monday, October 23, 2017

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler speculates today that the Bank of Nova Scotia is seeking to sell its metals trading division, ScotiaMocatta, because the bank realizes that the silver shorting business in which the division has specialized is a potentially disastrous liability.

Butler writes: “I think the Bank of Nova Scotia’s real motivation for seeking to offload its ScotiaMocatta precious metals unit after 20 years of ownership is liability. It’s the fear of what is to become of a major short seller in silver (and gold) on the Comex. By every count, ScotiaMocatta is one of the seven potential dead men walking who hold large concentrated short positions. It’s not some alleged smuggling ring that is motivating the bank to dump the unit. The only wonder is what took the bank so long to come to this conclusion.”

Butler’s commentary is headlined “Backing Out” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

http://silverseek.com/commentary/backing-out-16919

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

I agree with Ted that the real reason that Mocatta wants to get out of the silver short business is due to its huge losses. Their problem will be two-fold:

- nobody will want to take the liability

- even if they try and shut their business, the 75 million oz of silver short remains as it is impossible to cover

(courtesy Ted Butler)

THE ARTICLE IN FULL:

Backing Out

|

October 23, 2017 – 1:09pm

News reports this week indicated that the Bank of Nova Scotia (ScotiaBank), Canada’s third largest bank, had put its precious metals operation, ScotiaMocatta, up for sale. Various sources said the unit had been for sale for a year or so and it was thought or hoped that Chinese interests might buy the business. It was also reported that the Bank of Nova Scotia would shrink the unit if no buyer could be found. The impetus for the sale was said to be a scandal involving smuggled gold from South America to the US. Somewhat ironic, and interesting, was that the sale “listing” agent was none other than JPMorgan.

I believe there is more to this story than meets the eye and it involves the ongoing gold and silver price manipulation. About the only thing I find suspect in the news accounts is the motive for the sale. I was aware of the smuggling story, but ScotiaMocatta didn’t seem particularly exposed in this matter. I accept that the unit is up for sale, just not the motivation behind the sale. If my reasoning is correct, this could be a very significant development in the ongoing silver and gold price manipulation on the COMEX; on a par with JPMorgan taking over Bear Stearns in March 2008; which, in my opinion, was the most significant event in the silver market in decades.

Truth be told, I could never figure out why a leading Canadian bank would even want to buy and run a business not remotely in keeping with its core banking businesses – it was like trying to put a square peg in a round hole. The Bank of Nova Scotia has roughly 90,000 employees, whereas the ScotiaMocatta unit has less than 200 employees and accounts for a tiny fraction of the bank’s $2 billion quarterly profits.

I think the Bank of Nova Scotia’s real motivation for seeking to offload its ScotiaMocatta precious metals unit after 20 years of ownership is liability. It’s the fear of what is to become of a major short seller in silver (and gold) on the COMEX. By every count, ScotiaMocatta is one of the 7 potential dead men walking who hold large concentrated short positions. It’s not some alleged smuggling ring that is motivating the bank to dump the unit. The only wonder is what took the bank so long to come to this conclusion.

When it comes to the 8 largest concentrated shorts in COMEX silver and gold, JPMorgan, alone, is protected against financial ruin whenever silver prices explode due to its massive physical silver position. I see no evidence that any other entity has accumulated enough physical silver. Because JPM was so far ahead of the pack in recognizing that silver will soar in the future and began buying as much as it could starting six and a half years ago, it’s too late for the 7 others to jump onto the buy side now. That’s because such buying would set off a price spiral – about the very last thing a big short would want. JPMorgan has played this masterfully.

The best thing the Bank of Nova Scotia could hope to achieve now is to unload the problem on someone else, say an unsuspecting Chinese entity. The problem is that you can’t go from being, most likely, the 2nd largest silver short on the COMEX for years running, to suddenly closing out your shorts or getting long in a flash. You can’t just blink your eyes or click your ruby slippers and have the short position closed out – you must buy back the position or deliver physical metal, no easy task when you are talking perhaps upwards of 75 million ounces they hold short in COMEX silver futures (15,000 contracts). And just in case anyone is wondering – there is also no way that the Bank of Nova Scotia could ever admit to this and hope to unload the unit on anyone else. Hence, the BS smuggling cover story.

As to what has finally awoken ScotiaBank to the potential liability inherent in being a large short seller in silver and gold, there a number of explanations. Back in the summer of 2016, the open and unrealized losses to the 8 largest shorts in COMEX gold and silver combined amounted to $4 billion. By the end of last year, the 8 big shorts had succeeded in rigging gold and silver prices lower and with the price decline, the $4 billion open loss was extinguished. Still, at the gold and silver price highs of 2016, the $4 billion open loss had to be dealt with by the 8 big shorts. This meant that the unrealized loss had to be deposited with the clearing house by all shorts who were underwater, including the 8 big shorts (of which ScotiaMocatta was a card-carrying member).

This meant that ScotiaMocatta had to have deposited anywhere from $500 million to $750 million in unexpected margin calls in the summer of 2016, probably the most ever. Where did the margin money come from? In ScotiaMocatta’s case, from the parent bank. But since the demands for margin were so outside the bounds of what the parent bank was used to providing to its precious metals unit, it had to raise some eyebrows at the Bank of Nova Scotia. Large bank CFO’s and treasury officials tend to become concerned when they are pressed for sudden demands for many hundreds of millions of dollars. There is no way that the chief financial officer for ScotiaBank didn’t investigate why the ScotiaMocatta unit was hemorrhaging hundreds of millions of dollars. That person would have to ask what happens if prices continue to rise. Therefore, the bank came to realize what a potentially ruinous liability its precious metals unit was. Not only does the timeline fit regarding how long the unit has been up for sale, but I’m sure the parent bank came to appreciate the regulatory and general liability risk of being found to have manipulated the price of gold and silver for many years.

Only time will tell, but ScotiaBank trying to slip out the back wouldn’t seem to strengthen the dominant hand of the 8 big shorts in COMEX silver and gold. And it is upon the 8 big COMEX shorts that the price manipulation has always been based. I’ll make it simple – without the concentrated short position of the 4 and 8 largest traders in COMEX silver and gold, no manipulation would be possible. So any time a whiff of distress or disunity emerges from the big 8, it’s wise to sit up and take notice. Anything that might change how the real game has been played is, by definition, a potential game changer.

Ted Butler

October 23, 2017

END

The big question: when will China use the oil for yuan for gold threat?

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: China’s gold-for-oil threat to petrodollar

China has recently taken aim at the U.S. petrodollar by announcing a system for paying for imported Arab oil in Chinese yuan which would then be convertible into gold on a Chinese gold exchange. As pointed out by Mike Gleason of Money Metals Exchange in the U.S. this would enable China and its trading partners to bypass the dollar using a common monetary standard.

Mike goes on to comment that “The rise of a “petroyuan” could become the biggest threat to the U.S. dollar’s status as the world reserve currency. China’s appetite for imported oil is enormous and growing. So it makes sense for the country to seek direct trade deals with Saudi Arabia, Russia, and other suppliers. For its part, Russia is all too willing to deal in gold. Russian officials view the monetary metal as integral in combating international economic sanctions and supporting the ruble.”

Even though the United States is no longer on a gold standard, it still holds what is believed to be the world’s largest gold stockpile. Recently, the U.S. Treasury Secretary Steven Mnuchin reportedly did a spot- check on Fort Knox for PR purposes and claims that America’s gold is safe. However how an individual’s ‘spot check’ cold confirm this is very much open to doubt and with no true audit of Fort Knox in more than 60 years, many such doubts remain about who actually holds title to all the gold bars and whether some may be counterfeit, leased out, or just plain missing.

Gleason also notes that “If [U.S.] citizens were allowed to redeem their dollars for gold or silver coins on demand, then nobody would have to take the government’s promises on faith. Of course, there was a time when U.S. currency explicitly stated it was redeemable in precious metal. It’s a history most people today know little about. Those who were around as recently as 1963 may remember when paper dollars were also silver certificates – redeeemable in silver coins.

“Most politicians, bankers, and business titans today quite prefer digital dollars redeemable in nothing. They would prefer the public to not be tangibly connected to its history. There is a war on cash, a war on gold, and a war on history being waged in this country. They all go hand in hand.”

China’s motives here are worth examining. The country is again believed to be building its gold reserves without reporting them to the IMF. Indeed its gold reserves are believed by many observers to be very considerably higher than the reported total of 1,842.6 tonnes in any case – see: The fiction in Chinese gold reserves and media import coverage. Building its gold reserves can be seen as both a move to diversify its foreign exchange holdings away from their current U.S. dollar-related dominance given China sees the dollar as a weak currency given the enormous U.S. debt situation, but also to build up sufficient gold stocks to be able to use them to convert petro-yuan into gold, which would be a popular option for most oil exporting nations – notably Russia, the Middle Eastern oil producers and perhaps Venezuela.

While China has stated that it doesn’t have plans for the yuan to replace the dollar as the global reserve currency, it has seen the many trade benefits which have accrued to the U.S. from the dollar’s dominance and, with the acceptance of the yuan as an integral component of the IMF’s Special Drawing Right (SDR), it has already been able to take the first such step in this direction whether denied or not. The implementation of a ‘petro-yuan’, particularly if redeemable in gold, would be another major step.

While the dollar will almost certainly still remain the worlds’ primary reserve currency for a few years yet, the questin has to be when, not if, the yuan will come to dominate world trade?

24 Oct 2017

-END-

No surprise here: Venezuela lost its gold that it pawned off to Deutsche bank.

(courtesy zerohedge)

Venezuela fails to reclaim the gold it pawned to Deutsche Bank

Submitted by cpowell on Mon, 2017-10-23 23:19. Section: Daily Dispatches

That’s a lot more central bank gold that hit the market since the swap was undertaken in 2016.

* * *

Venezuela Allows $1.7 Billion Gold Swap with Deutsche Bank to Lapse, Legislator Says

By Corina Pons

Reuters

Monday, October 22, 2017

CARACAS — Venezuela this month allowed a $1.7 billion gold swap with Germany’s Deutsche Bank to lapse, according to an opposition legislator who said it weakens the balance sheet of the crisis-stricken OPEC nation’s central bank.

Through the operation, Venezuela had received $1.2 billion in cash in exchange for putting up $1.7 billion worth of gold in guarantee, part of efforts to improve the liquidity of foreign reserves amid heavy foreign debt payments and low oil prices

Legislator Angel Alvarado said the contract’s expiration weakens international reserves, which are hovering near 21-year lows as the country’s socialist economic model collapses under low oil prices.

“Venezuela decided to allow this contract to lapse,” said Alvarado in a telephone interview today. “We think the government could have negotiated better.”

The central bank will receive another $500 million in cash to reflect the difference between the amount of the loan and the value of the guarantee, said Alvarado, who obtained the information from finance industry sources.

Venezuela had to pay $1.2 billion by the middle of October to recover the gold, he said. …

… For the remainder of the report:

http://www.reuters.com/article/us-venezuela-economy/venezuela-allows-1-7…

END

We brought you this story yesterday but it is worth repeating. A jury finds an ex HSBC executive guilty of front running a 3.5 billion currency trade. This is just one trade. You can imagine the thousands of trades that these guys executed in gold and silver

(courtesy Reuters)

Jury finds ex-HSBC executive guilty of fraud in $3.5 billion currency trade

Submitted by cpowell on Mon, 2017-10-23 23:25. Section: Daily Dispatches

By Brendan Pierson

Reuters

Monday, October 23, 2017

NEW YORK — A U.S. jury today found a former HSBC Holdings executive guilty of defrauding Cairn Energy Plc in a $3.5 billion currency trade in 2011.

U.S. prosecutors have said that Mark Johnson, formerly head of HSBC’s global foreign exchange cash trading desk, schemed to ramp up the price of British pounds before executing a trade for Cairn, making millions for HSBC at Cairn’s expense. …

… For the remainder of the report:

https://www.reuters.com/article/us-hsbc-usa-crime/u-s-jury-finds-ex-hsbc..

END

Ecuador now seems to be the next gold frontier as the country now wants gold/silver exploration

(courtesy Dave Forest/OilPrice.com)

Did these mining giants just confirm the next gold frontier — Ecuador?

Submitted by cpowell on Mon, 2017-10-23 23:39. Section: Daily Dispatches

By Dave Forest

OilPrice.com, London

Monday, October 23, 2017

There was a breakthrough deal in the Tanzania gold sector late last week, with major miner Barrick agreeing to pay the government $300 million and surrender a 16-percent stake in operations in order to end an impasse that’s halted production.

But experiences like that aren’t going to encourage further investment in places like Tanzania, with news this week suggesting that the world’s top gold miners are looking to a new spot for growth projects: Ecuador.

That nation’s mining minister, Javier Cordova, told local press over the weekend that numerous major mining players are streaming into Ecuador — after new president Lenin Moreno moved last year to remove a moratorium on new mineral licenses and streamline processes for exploration and mining in the country. …

… For the remainder of the report:

https://oilprice.com/Metals/Gold/Did-These-Mining-Giants-Just-Confirm-Th…

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

2. Nikkei closed UP 108.52 POINTS OR 0.50% /USA: YEN RISES TO 113.72

3. Europe stocks OPENED IN THE GREEN/EXCEPT LONDON ( /USA dollar index FALLS TO 93.80/Euro UP to 1.1766

3b Japan 10 year bond yield: FALLS TO -+.069/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.27 and Brent: 57.73

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and U[ or Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.474%/Italian 10 yr bond yield UP to 2.039% /SPAIN 10 YR BOND YIELD DOWN TO 1.641%

3j Greek 10 year bond yield FALLS TO : 5.558???

3k Gold at $1277.12 silver at:17.02: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 57.41

3m oil into the 52 dollar handle for WTI and 57 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.72 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9869 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1613 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.474%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.391% early this morning. Thirty year rate at 2.911% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

What Selloff: Futures Rebound, Nikkei Extends Record Winning Streak

European shares are modestly lower as investors monitor tense events in Spain and as focus turns to Thursday’s ECB meeting; US equity futures have rebounded from yesterday’s sharp but shallow selloff and are in the green amid rising odds of U.S. tax reform and the imminent unveiling of the next Fed chair while Asian shares rise and Japan extends its winning streak to a record 16 days. The euro edged higher after data showed Europe’s economy is maintaining momentum, while the USDJPY managed to recover all of yesterday’s sharp losses.

The MSCI’s 47-country world share index stayed near all-time highs after a drop in General Electric shares on Wall Street had seen the ViX volatility index spike up, however that move has been largely faded since.

Overnight currency moves were mostly contained, but the greenback strengthened against most peers and U.S. equity futures edged higher amid continued speculation over who will lead the Federal Reserve, and as optimism over tax reform proved resilient. “There is some support building for Donald Trump’s tax reforms,” Ipek Ozkardeskaya, an analyst at London Capital Group, told Bloomberg by email. News reports suggest “that fiscal hawks may be willing to disregard deficit spending to allow Trump to go ahead with his tax cut plans to boost growth. If approved, the fiscal reforms will cost an arm to the government, but on the other hand, it is important for the congress to achieve some progress before the end of the year in order to restore confidence.”

The USD rallied across G-10 for bulk of the session, with the DXY back to top of recent range between 50- and 100-DMAs. The New Zealand’s dollar stumbled to a five-month low as the incoming Labour coalition’s policies unsettled investors. Prime Minister-designate Jacinda Ardern’s tough stance on foreign investment in housing and on immigration could prove negative for the currency, given the country runs a current account deficit. In addition, Ardern said on Tuesday her government plans to review and reform the Central Bank Act to possibly include employment, alongside inflation, as a dual target. “Everything happening so far is something that is creating uncertainty when it comes to central bank independence,” said Manuel Oliveri, currency strategist at Credit Agricole. “But you also have to keep in mind Labour did point in that direction during the election so it’s not a huge surprise that they want such changes.”

As Bloomberg notes, given that the timing of an announcement on the next Fed chair isn’t certain and that tax reform is a lengthy process, investors’ more immediate focus looks set to be Thursday’s European Central Bank meeting. The ECB is expected to offer more insight into its plans for tapering the QE program that is currently planned to continue until the end of 2017. Expectations are for a €30 billion QE extension for at least 9 months, with some more dovish variants possible. Officials have acknowledged that stimulus is still required to nurture inflation and that interest rates will remain “at or below” current levels for the foreseeable future.

Ahead of the ECB, the consensus trade is to go short the 10Y Bund which however has so far failed to move the benchmark paper substantially as any asset volatility now appears a thing of the past.

Overnight, the euro was a little stronger after strong PMI data showed Europe’s economy maintaining momentum, but the region’s stocks drifted downward as investors kept one eye on events in Spain and the all-important ECB gathering; Bunds sold off from the open with further momentum driven by PMIs and related inflation commentary; USTs and gilts dragged lower in tandem, UST curve steepens. German banks rallied after takeover speculation on Commerzbank (+3.9%); energy stocks rally as crude futures react positively to further reports of output cut extension.

Japanese stocks rose again, with the Nikkei 225 Stock Average extending its record-breaking rally to a 16th day to a fresh 21 year high, as investors shifted their focus to corporate earnings from Sunday’s general election helped by the weaker yen which failed to maintain its gains during the US session. The Topix erased an early decline, completing a 12-day gain, the longest since November, with banks and telecommunications companies providing the biggest boost. Japan’s earnings season kicked off in earnest this week, with Canon Inc. and Nidec Corp. releasing results today, followed by Fanuc Corp., Fujitsu Ltd. and NTT Docomo Inc. later this week. “There’s still more room for Japanese stocks to advance, given the firm prospects for companies’ earnings,” said Kyouko Amemiya, a senior market advisor with SBI Securities Co. in Tokyo. “The economy as well as corporate performance are on firm footing globally. Japanese stocks still look cheap in relative to U.S. equities.” While Sunday’s general election result has already been priced in to a degree, stocks still have some “upside”,

Elsewhere in Asia, equity markets traded with modest gains in what was a quiet and rangebound trading session amid a lack of drivers. Regional bourses shrugged off the weak performance by their US counterparts which pulled back from record levels, with ASX 200 (Unch.) indecisive and Hang Seng (Unch.) and Shanghai Comp. (+0.1%) just about kept afloat as another substantial liquidity operation by the PBoC (140BN net on the session and a whopping 840BN in the past week) only provided minimal support heading to the close of the National Congress. Finally, 10yr JGBs were flat with demand subdued by a modest risk tone and after an uneventful enhanced liquidity auction for super-long JGBs.

Europe’s key stock benchmark was little changed, as most European stocks dipped and bond yields drifted higher on Tuesday, as data from the euro zone’s top economies bolstered the case for the European Central Bank to signal a sizeable cut this week to its stimulus measures. Individual equities dominate moves amid earnings reports, while strong manufacturing data provided support to risk. The Stoxx Europe 600 Index fell less than 0.1%, ahead of an ECB meeting later this week. Apple supplier AMS saw a spectacular 15 percent jump after it pointed to strong demand ahead of the iPhone X release while Boliden drops 9.9% on worse-than-expected profit. France’s CAC 40 up 0.3% on earnings and after October manufacturing data beat estimates. Commerzbank outperformed following the company drafting in financial advisers, preparing for potential bids from European rivals. Europe’s earnings season has begun gaining some traction, notably, Essilor, affirming guidance and leading the CAC.

Also overnight as reported earlier President Xi Jinping of China consolidated his power before the Communist Party’s unveiling of its top leaders on the Politburo and supreme Standing Committee on Wednesday. The composition may determine the pace of Xi’s reform plans, from deleveraging to modernizing the military. Stocks in Shanghai gained, while those in Hong Kong dropped.

In commodities, gold dipped 0.3 percent to $1,278.29 an ounce, the weakest in more than two weeks. West Texas Intermediate crude climbed 0.1 percent to $51.94 a barrel. LME zinc gained 1.2 percent to $3,167.50 per metric ton. LME copper advanced 1.3 percent to $7,092.50 per metric ton.

Interest rates were generally higher, with the yield on 10-year Treasuries increased three basis points to 2.39 percent, the highest in more than five months. Germany’s 10-year yield gained four basis points to 0.47 percent, the highest in almost four weeks. Britain’s 10-year yield climbed three basis points to 1.339 percent, the highest in more than a week.

AT&T, Eli Lilly, Lockheed, GM and McDonald’s among companies due to report earnings. Economic data include Markit manufacturing PMI readings.

Bulletin Headline Summary from RanSquawk

- Bunds drag global bonds lower

- In FX, NZD underperformed amid potential reforms at the RBNZ. Trump claims to be close on Fed Chair decision

- Looking ahead, highlights include US Manufacturing and weekly APIs

Market Snapshot

- S&P 500 futures up 0.1% to 2,566.00

- VIX Index falls -0.29 (2.62%) to 10.78

- STOXX Europe 600 down 0.1% to 390.36

- MSCI Asia up 0.1% to 167.20

- MSCI Asia ex Japan down 0.2% to 547.90

- Nikkei up 0.5% to 21,805.17

- Topix up 0.7% to 1,756.92

- Hang Seng Index down 0.5% to 28,154.97

- Shanghai Composite up 0.2% to 3,388.25

- Sensex up 0.2% to 32,559.34

- Australia S&P/ASX 200 up 0.06% to 5,897.61

- Kospi up 0.02% to 2,490.49

- WTI crude futures down 0.5%

- Brent Futures down 0.3% to $57.21/bbl

- Gold spot down 0.3% to $1,278.46

- U.S. Dollar Index down 0.1% to 93.82

- Bloomberg spot dollar index advances 0.1%

- German 10Y yield rose 3.3 bps to 0.465%

- Euro up 0.1% to $1.1762

- Brent Futures down 0.3% to $57.21/bbl

- Italian 10Y yield fell 3.7 bps to 1.737%

- Spanish 10Y yield rose 0.6 bps to 1.633%

Top Overnight News

- BOJ: considering a small cut to its inflation forecast for FY2017;

doesn’t see the need to expand stimulus as improving output gap and

tightening labor market will continue to push inflation higher according

to people familiar with the central bank’s discussions - As OPEC negotiates the extension of its oil production cuts until the end of 2018, it’s also quietly started working on a tapering-style exit strategy

- The euro-area economy maintained its strong momentum at the start of the final quarter of this year, with rising workloads encouraging companies to take on new staff at the sharpest pace in more than a decade, PMIs showed

- U.K. PM May’s cabinet will meet Tuesday as pressure mounts for it to agree the kind of trade pact Britain wants from the EU — a day after she damped expectations of a swift Brexit transition deal

- The EU is also preparing for a “no deal” with the British says Michel Barnier, the EU’s lead Brexit negotiator in an interview to L’Echo newspaper; EU President Donald Tusk revived the notion that the U.K. will stay in the bloc after all

- Flow Traders NV reported a 35 percent plunge in net trading income in the third quarter as Europe’s largest trader of ETFs continued to suffer from reduced trading activity

- On Wednesday, China will finally get an answer to the big question looming over the Communist Party’s biggest political event: Will President Xi Jinping clearly signal a designated successor? On Tuesday Xi’s name was enshrined in the party’s charter under its guiding principles — an honor that eluded his two immediate predecessors

- U.S. Govt: House Republicans aiming to release prelim tax reform legislation as soon as next week; plans to be released about seven days after Thursday’s vote on budget resolution, meaning bill text would be published on or before Nov. 3

- Treasury Secretary Steven Mnuchin got a swift rebuttal after he went on

national television to claim a hypothetical Indiana family would save

$1,000 under President Donald Trump’s tax plan. At virtually the same

time on another network, White House Budget Director Mick Mulvaney

dismissed as flawed any attempt to predict the impact of the plan - European Oct. prelim composite PMIs: France 57.5 vs 57.0 est; Germany 56.9 vs 57.5 est; euro area 55.9 vs 56.5 est; manufacturing above consensus for all three regions; selling prices rose at the sharpest rate since June 2011

- Global bonds: Sumitomo and Nippon Life both plan to buy unhedged foreign bonds in 2H FY2017

- China’s ruling Communist Party approved a revised charter that enshrined President Xi Jinping’s name under its guiding principles, elevating him to a status that eluded his two immediate predecessors

- White House’s Muddled Tax Message Clouds Pitch for Trump Plan

- U.S. Lumber Companies Plan to Combine in $1.16 Billion Deal

- U.S. Will Curb ‘Sneak-and-Peek’ Searches Microsoft Sued Over

- Taylor’s Walk on Supply Side May Leave Him More Dove Than Yellen

- Facebook Privacy Can Be Regulated in Germany, EU Court Aide Says

- NZ PM-elect Ardern says will review, reform Reserve Bank Act

- Tesla Calls on U.S. to Drop Perry’s Plan to Rescue Nukes, Coal

- China Cuts Offshore Yuan Bond Sale on H.K. Market Correction: MOF

- Novartis Plans to Give Ailing Alcon More Time for Turnaround

- Rise in Texas Earthquakes Near Oilfields Prompts New Monitoring

- Canon Boosts Op. Profit View Above Est., Plans Special Dividend

- Boeing Is Said to Have Walked Away From C Series Deal: Globe

Asia equity markets traded with modest gains in what was a quiet and rangebound trading session amid a lack of drivers. Nonetheless, the regional bourses have shrugged off the weak performance by their US counterparts which pulled back from record levels, with ASX 200 (Unch.) indecisive and Nikkei 225 (+0.2%) mildly positive after the index recovered from early weakness triggered by a firmer JPY to print fresh 21-year highs. Hang Seng (Unch.) and Shanghai Comp. (+0.1%) just about kept afloat as another substantial liquidity operation by the PBoC only provided minimal support heading to the close of the National Congress. Finally, 10yr JGBs were flat with demand subdued by a modest risk tone and after an uneventful enhanced liquidity auction for super-long JGBs. PBoC injected CNY 130bln via 7-day reverse repos and CNY 120bln via 14-day reverse repos. PBoC set CNY mid-point at 6.6268 (Prev. 6.6205)

Top Asian News

- Noble Group’s Next Battle Will Be Over $3 Billion Debt Pile

- Bank of Japan Is Said to Consider Lowering Inflation Outlook

- China Signals Steady Economic Policy as Liu Keeps Party Role

- Sony Is Said to Plan Nov. Event for New Robot Roll-Out: WSJ

- HK Stock Gains Evaporate as Caution Reigns Pre-Earnings

- India Bonds Keep Gains as Jaitley to Make ‘Major Announcement’

- Sumitomo Life Plans to Boost Foreign Bond Holdings in Fiscal 2H

European bourses trade subdued, as 9 out of 10 European sectors trade in the marginal red, supported by energy trading up around 0.30%. Despite the lack of direction in the index markets, stock specific news has resulted in volatility, as Commerzbank outperforms in the Dax, following the company drafting in financial advisers, preparing for potential bids from European rivals. Europe’s earnings season has begun gaining some traction, notably, Essilor, affirming guidance and leading the CAC. Early upside faded and reversed as trade turns defensive ahead of major risk events. Firmer than anticipated flash EZ PMIs probably gave sellers some fundamental/macro momentum, but in truth bears had already gained the upper hand in Bunds when the 10 year German bond topped out ahead of near term chart resistance again. Intraday longs are said to have thrown in the towel from the 161.46-40 area, with hefty stops triggered on a break of the lower level down to 161.28 and Bunds subsequently hitting 161.19. Next downside tech support 161.07, 10 year cash yield 0.47% with 0.5% and obvious target. UK Gilts also on the backfoot and down to 124.22, USTs likewise awaiting news on the next Fed chair.

Top European News

- Deutsche Boerse Trading Probe Extended in Blow to Kengeter

- Commerzbank Is Said to Hire Goldman, Rothschild as Advisers: FT

- UniCredit Third-Quarter Net Rises on Gain From Pioneer Sale

- Swedbank Falls as Investors Focus on Smaller Capital Buffers

- Catalan Exiled CaixaBank’s Quarterly Profit Beats Estimates

- Euro-Area Companies Expand Workforce as Order Growth Picks Up

- Hawkish ECB Tapering Surprise to Give Bigger Jolt to Euro, Bunds

- EU Still Floating Idea That Brexit Can Be Reversed Before 2019

In FX, a fresh setback for the NZD which print fresh 5-month lows at 0.6927. This came as NZ PM-elect Ardern unveiled government plans to review and reform the RBNZ’s Central Bank Act to possibly include employment, alongside inflation as a dual mandate. As it stands, unemployment is near decade lows, while jobs growth however, is at a 2-year low (figures for Q3 released at 2245BST). Although, given that the central bank does not exclude labour market data, its arguable whether a dual mandate will significantly alter the monetary policy skew. What has been brought into question however, is the autonomy of the RBNZ. AUDNZD further supported by the soft NZD, with the cross moving to its highest level since Apr’16. Near term resistance resides at 1.13, which could curb gains a see the cross top out, while the 2016 high is situated 1.1333. JPY: The bid in USD/JPY has been revived by the 16 consecutive days of gains for the Nikkei. Although, the upside could potentially top out just north of 114, with the highs seen in May and July at 114.38-49 within sight. Additionally, the price action may well be dictated by US yields as the 10yr approaches the key 2.4% yet again (currently 2.38%).

In commodities, oil commentary has once again leaked into the news, with Russia’s Energy Minister Novak stating that he plans to discuss an extension of oil cuts with Saudi’s Falih. Oil markets are fairly unfazed, dampened by the latest update of crude oil flows via the Iraqi Kurdistan pipeline to Turkey have modestly risen to around 300,000BPD, possibly indicating the restart of Iraqi/Kurdistan pipeline functionality. Copper continues to impress in metal markets, once again looking towards last week’s highs, aided by the stop hunt through USD 3.20. Elsewhere, gold has come off highs around 1300.00, looking at the key October 6th, 1261.30 low. OPEC is to work on exit strategy alongside cuts extension, according to sources.

Looking at the day ahead, the big highlight datawise are the October flash PMIs due in France (Mfg 56.7, exp. 56.0, Services 57.4, Exp. 56.9), Germany (Mfg 60.5, Exp. 60.2, Services 55.2, Exp. 55.6), the Euro area (Mfg. 58.6. exp. 57.8, Services 54.9, exp. 55.6) and the US. French confidence indicators for October and the Richmond Fed PMI in the US for October are also due. Onto other events, the ECB Bank Lending Survey will also be worth watching while in the UK Chancellor Hammond is scheduled to face questions in the House of Commons. The Bundestag convenes for its inaugural session following the election while in China the CPC wraps up with the appointment of the Central Committee. AT&T, General Motors, Novartis and McDonalds all report earnings.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.1

- Markit US Services PMI, est. 55.2, prior 55.3

- Markit US Composite PMI, prior 54.8

- 10am: Richmond Fed Manufact. Index, est. 16.5, prior 19

DB’s Jim Reid concludes the overnight wrap

The dull start to the important ECB week should get a little impetus today with the release of the various flash PMIs which are currently at around multiyear highs in many countries. For example the Eurozone and both Germany and France’s manufacturing PMI are at 10 and 6 year highs respectively. For today consensus is expecting a small pullback in October, with manufacturing PMI in the Eurozone expected to be 57.8 (vs. 58.1 previous), Germany at 60 (vs. 60.6 previous) and France at 56 (vs. 56.1 previous). This morning, the Nikkei Japan manufacturing PMI was slightly lower at 52.5 (vs. 52.9 previous).

The quiet start to the week so far is partly due to market participants waiting for ‘Super Thursday’ when the ECB will announce their long awaited updated tapering decision. As we’ll see later it’s also the day the Catalan parliament meet to respond to Madrid’s threat of direct rule and possibly declare independence. There was also a story from thehill.com and Politico yesterday that Thursday may see the US House vote on passing the Senate version of the budget that was approved last week. If so, and successful, this would accelerate the possibility of tax cuts as the weeks of reconciling the two budgets would be sidestepped. So all in all potentially a big day on Thursday.

Ahead of all that, tensions around Catalonia continue to bubble along as we build to a potential crescendo towards the end of the week. Overnight, Bloomberg reported that Catalan activists are considering mobilising human shields near government buildings to deter the Spanish government from taking control of the region. The leader of the main separatist group (Lluis Corominas) said “we’re calling for a peaceful and democratic defence of the

institutions”. Looking ahead, the full Catalan Parliament will meet this Thursday (9am local time), with prior Bloomberg reports suggesting Catalan President Puidgement may consider formally declaring independence. On the other side, the Spanish Senate will debate the Article 155 measures proposed by PM Rajoy on Thursday afternoon with final votes on Friday morning (9:30am local time). If the measures are passed, Rajoy’s new constitutional powers would take effect from next Monday. Elsewhere, El Confidential reported the Spanish Senate would approve intervention of Catalan government even if President Puigdemont calls for early regional election.

Staying with the trend, over in Italy, two of its wealthiest Northern regions have also voted on Sunday in referendums for more autonomy from the central government. The Lombardy region (includes Milan) had a 38% eligible voter turnout and of that, 95% voted for in favour of higher autonomy, while the Veneto region (includes Venice) had 57% voter turnout with 98% voting in favour. The two regions account of c25% of Italy’s population and c30% of economic output. Note the votes are non-binding and unlikely to lead to referendum for independence, in part as Milan and Venice had relatively lower voter turnout, at 31% and 45% respectively. However, it does partly highlight the recent shifts in European politics and perhaps lends greater support to the Northern League Party ahead of next year’s Italian election.

Staying with politics, it seems that a swift Brexit transition deal is increasingly less likely and may instead be part of a wider agreement that will be finalised later on. The PM’s spokesman James Slack said “everybody has always been clear that we’re looking to wrap all this up in one single go….everything will be agreed at the same time”. When asked later on, PM May avoided directly answering the question, but alluded that transitions is about “practical arrangements to reach the future partnership”, but you don’t know those arrangements “until you know what the future partnership is”. Her parliament address was relatively upbeat, signalling progress has been made on Brexit talk, in particular on EU citizen rights and the northern Irish border, but conceded that “we’re preparing for every eventuality to ensure that we leave in a smooth and orderly way”.

Elsewhere, the EC President Junker noted “nothing is true” in reference to a German newspaper article (Frankfurter Allgemeine) which noted the UK PM May “begged for help” from him during their working dinner last week and appeared disheartened and discouraged. Earlier on, Juncker reiterated that the UK must agree on a financial settlement with the EU before parallel talks can begin on the country’s future trade ties with the bloc.

Turning to the US and its search for the next Fed Chair. President Trump told reporters on Monday that he is “very very close” to finalising the winning candidate, but did not provide further details. DB’s Peter Hooper takes an updated look at the three candidates and believes if Ms Yellen do not get re-elected, then a Powell-led Fed makes more sense, in part as i) he would provide the highest degree of continuity to current policy, ii) he has had c5 years of experience working inside the Fed with a reputation as a consensus builder, and iii) while not a PHD trained economist, he has learned the trade well, as evidenced by his speeches and Q&A performance. For more details, refer to link.