GOLD: $1270.00 down $6.15

Silver: $16.70 down 13 cents

Closing access prices:

Gold $1270.20

silver: $16.72

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1289.75 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1275.85

PREMIUM FIRST FIX: $13.90(premiums getting larger)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1291.50

NY GOLD PRICE AT THE EXACT SAME TIME: $1276.70

Premium of Shanghai 2nd fix/NY:$14.80 PREMIUMS GETTING LARGER)

CHINA REJECTS NEW YORK PRICING OF GOLD!!!!

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1274.40

NY PRICING AT THE EXACT SAME TIME: $1275.60

LONDON SECOND GOLD FIX 10 AM: $1270.15

NY PRICING AT THE EXACT SAME TIME. 1271.70 ??

For comex gold:

NOVEMBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH: 523 NOTICE(S) FOR 52300 OZ.

TOTAL NOTICES SO FAR: 523 FOR 52300 OZ (1.626TONNES)

For silver:

NOVEMBER

427 NOTICE(S) FILED TODAY FOR

2,135,000 OZ/

Total number of notices filed so far this month: 427 for 2,135,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: $6196 bid /$6216 offer up $84.00 (MORNING)

BITCOIN CLOSING;$6309 BID:6329. OFFER UP $197.00

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A tiny sized 451 contracts from 195 ,953 UP TO 196,434 with YESTERDAY’S TRADING IN WHICH SILVER ROSE BY 8 CENTS. THE CROOKS ARE STILL HAVING AN AWFUL TIME TRYING TO COVER THEIR MASSIVE SILVER SHORTS SO THEY CONTINUE TO TORMENT. TODAY ALL OPTIONS ON THE LBMA/LONDON BOARD HAVE EXPIRED.

RESULT: A TINY SIZED RISE IN OI COMEX WITH THE 8 CENT PRICE GAIN. OUR BANKERS COULD NOT COVER ANY OF THEIR HUGE SHORTFALL.

In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.981 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 427 NOTICE(S) FOR 2,135,000 OZ OF SILVER

In gold, the open interest SURPRISINGLY ROSE BY A HUGE 9,033 CONTRACTS DESPITE THE SMALL RISE IN PRICE OF GOLD ($5.30) . The new OI for the gold complex rests at 528,459. NO DOUBT MANY OF THE PAPER LONGS THAT RECEIVED THEIR NOV. EFP’S SOLD AND BOUGHT NOVEMBER AND DECEMBER GOLD COMEX CONTRACTS AS THEY CONTINUE WITH THEIR PAPER GAME.

Result: A HUGE SIZED INCREASE IN OI DESPITE THE SMALL RISE IN PRICE IN GOLD ($5.30). IT SEEMS THAT OUR PAPER EFP’S SOLD LONDON AND BOUGHT BACK COMEX NOVEMBER AND DECEMBER COMEX CONTRACTS.

we had: 523 notice(s) filed upon for 52,300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

No change in inventory at the GLD/

Inventory rests tonight: 850.77 tonnes.

SLV

STRANGE: WITH SILVER UP THESE PAST TWO TRADING DAYS WE HAD A BIG WITHDRAWAL IN SILVER INVENTORY AT THE SLV: 1.133 MILLION OZ

INVENTORY RESTS AT 319.155 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A TINY 451 contracts from 195,983 UP TO 196,434(AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) . OUR BANKERS WERE AGAIN UNSUCCESSFUL IN THEIR ATTEMPT TO COVER ANY OF THEIR SILVER SHORTS.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 8 CENT GAIN IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKER FRIENDS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO COVER ANY OF OUR SILVER SHORTS . .NO EFP’S WERE ISSUED FOR THE UPCOMING NOVEMBER CONTRACT

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 3.00 points or .09% /Hang Sang CLOSED DOWN 90.65 pts or 0.32% / The Nikkei closed UP 0.06 POINTS OR 0.00/Australia’s all ordinaires CLOSED DOWN 0.12%/Chinese yuan (ONSHORE) closed UP at 6.6315/Oil UP to 54.02 dollars per barrel for WTI and 60.86 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6315. OFFSHORE YUAN CLOSED AT VALUE OF THE ONSHORE YUAN AT 6.6335 AND //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea//

We warned you that this could happen. More than 200 are dead after tunnels collapse at the North Korean nuclear test site after suffering minor quakes last month:

( zerohedge)

b) REPORT ON JAPAN

Japan leaves its policy unchanged and that puts a little damper on the yen value. The bank of Japan lowered its purchases of ETF’s dramatically.

( zerohedge)

c) REPORT ON CHINA

i)China is definitely slowing down as its manufacturing and service PMI disappoint by tumbling in October.

( zerohedge)

ii)China;’s yield curve has now been inverted for 10 days signifying a huge slowdown in China and this inversion spells an upcoming disaster

( zerohedge)

4. EUROPEAN AFFAIRS

i)Europe

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

Both oil and gasoline rise after major inventory draw downs

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)We brought you this story yesterday and it is quite concerning: somebody made a fake one oz Canadian gold bar with fake mint wrapping. So far only one bar has shown up( Ottawa Citizen/GATA)

iii)Nothing new her The gold market is moving from West to East;

( Xinhua News Agency, Beijing)

10. USA Stories

iib)Trump calls on both Podesta brothers to ‘drain the swamp’ by revealing the real earth shattering dirt perpetrated by the Democrats with their fake news that it was the Republicans only that tried to influence the elections with the help of Russian authorities

( zerohedge)

ii c) The real plot as described by Pat Buchanan: they were all trying to bring down Trump

(courtesy Pat Buchanan)

iii)John Kelly reports that the White House is totally unfazed by the Mueller Indictments as nothing relates to the Russian investigation

iv)Soft data Chicago PMI surges to its highest point since 2011 despite employment faltering. All soft data reports are fudged.

( zerohedge)

v)The pharmaceutical industry is to immune to corruption: Generic companies colluded by diving up the market. Six manufactures are involved

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY 9,033 CONTRACTS UP to an OI level of 528,459 WITH THE SMALL RISE IN THE PRICE OF GOLD ($5.30 RISE IN YESTERDAY’S TRADING). IT SEEMS THAT THE NEWBIE LONG EFP’S SOLD THEIR LONDON BASED CONTRACTS AND BOUGHT BACK COMEX NOVEMBER AND DECEMBER AND POCKETED THE FIAT BONUS.

HERE IS A SUMMARY OF EFP’S ISSUED TO LONGS IN EACH OF THE PAST 3 MONTHS:

The amount of EFP’s issued for each of the past 3 months at month’s end;

Sept: 6500

Oct 7200

Nov: 8500

Result: a GOOD SIZED open interest INCREASE WITH THE RISE IN THE PRICE OF GOLD ($5.30.)

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF ONLY 42 CONTRACTS DOWN TO 610 AND BY DEFINITION THAT IS THE PRELIMINARY AMOUNT OF GOLD CONTRACTS STANDING FOR DELIVERY OR 61000 OZ (1.897 TONNES)

The very big active December contract month saw it’s OI GAIN OF 4426 contracts UP to 382,729. FEBRUARY saw a gain of 3893 contacts up to 84,741.

.

We had 523 notice(s) filed upon today for 52300 oz

VOLUME FOR TODAY (PRELIMINARY) 266,119

CONFIRMED VOLUME YESTERDAY: 272, 175

We had 427 notice(s) filed for 2,135,000 oz for the OCT. 2017 contract

Oct.31/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

32.15

Brinks oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

523 notice(s)

52300 OZ

|

| No of oz to be served (notices) |

87 contracts

(8700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

523 notices

52,300 oz

1.626 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 337 notices were issued from their client or customer account. The total of all issuance by all participants equates to 532 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 124 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

460,323.095 oz

Brinks

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

600,837.460

CNT

Delaware

oz

|

| No of oz served today (contracts) |

427 CONTRACT(S)

(2,135,000,OZ)

|

| No of oz to be served (notices) |

166 contract

(830,000 oz)

|

| Total monthly oz silver served (contracts) | 427contracts

(2,135,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | xx oz |

NPV for Sprott and Central Fund of Canada

will update later tonight

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott Inc. to take control of rival gold holder Central Fund of Canada

Posted Oct 2, 2017 8:43 am PDT

Last Updated Oct 2, 2017 at 9:20 am PDT

TORONTO – Sprott Inc. (TSX:SII) says it has struck a deal to take control of rival gold-holding firm Central Fund of Canada Ltd. (TSX:CEF.A) after a protracted takeover effort.

Toronto-based Sprott said Monday it will pay $120 million in cash and stock for Central Fund of Canada Ltd.’s common shares and for the right to administer and manage the fund’s assets.

The deal, which requires approval from Central Fund shareholders, would see its class A shareholders transferred to a new Sprott Physical Gold and Silver Trust.

Sprott says the deal would add $4.3 billion to its assets under management, which are focused largely on holding physical precious metals on behalf of clients, and 90,000 investors to its client base.

In March, Sprott tried to go through the Court of Queen’s Bench of Alberta to allow Central Fund’s class A shareholders to swap their shares to Sprott after the family that controls Central Fund rebuffed their attempt to make a deal.

Last year Sprott took over Central GoldTrust, a similar fund controlled by the same family, after securing support from more than 96 per cent of shareholder votes cast.

END

And now the Gold inventory at the GLD

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

Oct 17./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

Oct 16/A HUGE WITHDRAWAL OF 5.32 TONNES FROM THE GLD/INVENTORY RESTS AT 853.13 TONNES

0CT 13/ NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 12/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

SEPTEMBER 29/no changes in gold inventory at the GLD/Inventor rests at 864.65 tonnes

Sept 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.65 TONNES

Sept 27/WOW!! WITH GOLD DOWN $13.25, WE HAD A HUGE 8.57 TONNES OF GOLD ADDED TO THE GLD/

Sept 26/no changes in gold inventory at the GLD/Inventory rests at 856.08 tonnes

Sept 25./Another big deposit of 3.84 tonnes into GLD/Inventory rests tonight at 856.08 tonnes

Sept 22/with gold up only 1 dollar on the day we had a massive 6.21 tonnes of gold added to the GLD/.this is a good sign that gold will advance nicely this coming week.

Sept 21/no change in gold inventory tonight/inventory rests at 846.03 tonnes

Sept 20/no change in gold inventory tonight/inventory rests at 846.03 tonnes

end

Now the SLV Inventory

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Oct 17/ A MONSTROUS WITHDRAWAL OF 3.494 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 322.271 MILLION OZ

Oct 16/ NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 325.765 MILLION OZ

oCT 13/ NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 12/THE LAST TWO DAYS WE LOST 1.113 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

SEPTEMBER 29/no changes in silver inventory at the SLV/inventory rests at 326.757 million oz/

Sept 28/NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ/

Sept 27/STRANGE!! SILVER IS HIT FOR 24 CENTS YESTERDAY AND. 9 CENTS TODAY AND YET NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 326.757 MILLION OZ

Sept 26./no change in silver inventory at the SLV/.inventory rests at 326.757 million oz

Sept 25./ a big deposit of 1.842 million oz into the SLV/inventory rests at 326.757 million oz/

Sept 22/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz/

Sept 21/no change in silver inventory at the SLV/Inventory rests at 324.915 million oz

Sept 20/no changes in silver inventory/Inventory remains at 324.915 million oz

Oct 31/2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.40%

Indicative gold forward offer rate for a 6 month duration+ 1.40% -

+ 1.60%

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

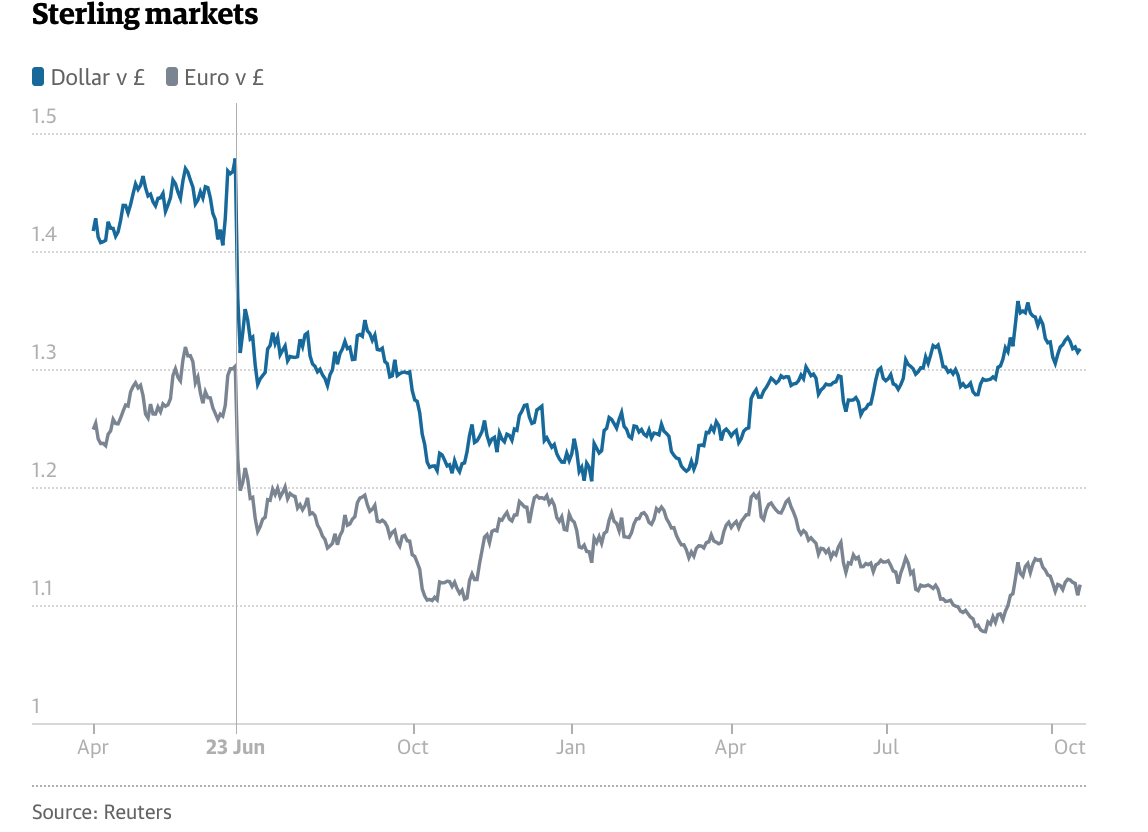

Stumbling UK Economy Shows Importance of Gold

Stumbling UK Economy Shows Importance of Gold

– UK economy outlook bleak amid Brexit, debt woes and rising inflation

– Confidence in UK housing market at five-year low

– UK high street sales crash at fastest rate since 2009

– Number registering as insolvent in England and Wales hit a five-year high in Q3

– UK public finance hole of almost £20bn in the public finances set to grow to £36bn by 2021-22

– Protect your savings with gold in the face of increased financial woes in UK

This week markets will be watching the UK with baited breath as the Monetary Policy Committee meets this Thursday to discuss a potential rate rise.

Expectations of a rise have increased to 80% in the last week. If the Bank of England does raise rates it will be for the first time in a decade. It is unlikely to be a dramatic increase though, probably a rise of 25 basis points to reverse the emergency rate cut which followed the Brexit vote.

Should the UK decide to raise rates this will likely boost confidence somewhat in the economy. However any increase in positivity regarding the UK will be short lived once markets realise it will take more than a small rate rise to get the country out of the huge red hole it is currently digging its way into.

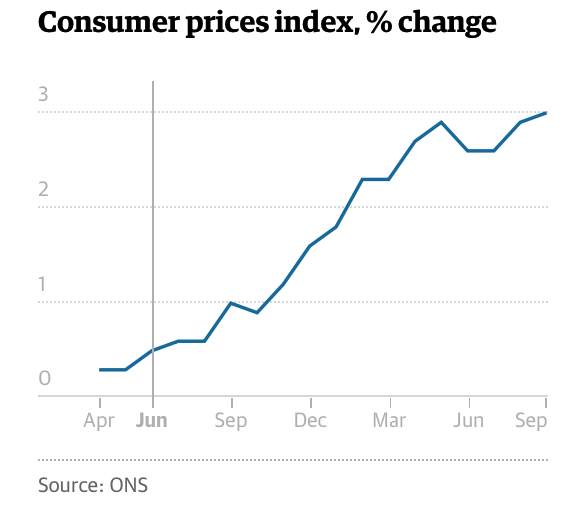

Brexit is being blamed for the majority of the UK’s woes at present, however this is merely a politician’s scapegoat. Confidence in the UK housing market has slipped to its lowest level in five years, family spending power has declined in five out of the last six months, the hole in public finances is likely to increase over 100% from the initial forecast by 2020, personal insolvencies are at a five year high and inflation has hit 3%.

These plus many more financial and economic problems have long been brewing. Problems with money naturally lead to social problems which end up exacerbating themselves further as individuals find continue to struggle on a daily basis.

Sadly the UK is in a real state of limbo thanks to Brexit, how the government will manage to solve the other significant issues such as rising debt levels (public and private), inflation and a slowing economy whilst managing EU negotiations is a feat yet to be witnessed.

We have been approaching a juncture for some time where we must decide as individual savers, investors, pensioners and future pensioners what the best way to prepare for the future is. Do we stand back and believe that the government has our best interests at heart or do we prepare for their failure? Their inability to support the value of the pound, protect interest rates, avoid bank bail-ins and solve the debt crisis are all situations that could see our own savings put at real risk.

Falling confidence both in and inside the UK

Despite expectations of a rate rise, sterling stumbled in October thanks to weak economic data and more negative headlines regarding Brexit.

What’s the one thing governments like to say positively about a weak currency? That it’s good for exports…but not in the UK it’s not.

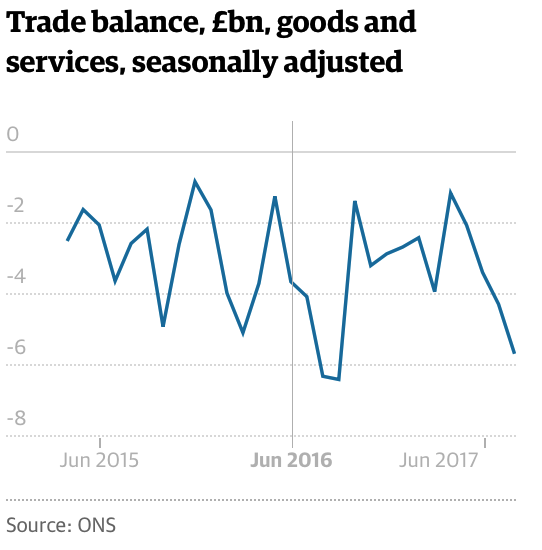

As we explained earlier this month, a much revered boost to UK exports following the Brexit vote was most likely down to our gold market. Now that the Chinese have calmed down on their gold shopping spree we are seeing what state the rest of the export market is really in.

The trade deficit in goods hit a record high, as the gap between what the UK bought and sold widened in August to £14.2bn. That was much bigger than expected, and up from £12.8bn in July. Imports surged by 4.2% during the month, while exports only rose by 0.7%. The overall trade deficit, including services, widened to £5.6bn in August from £4.2bn in July.

…and from within things aren’t much better

Currency and export markets are not the only ones having a problem with the UK. There are nervous feelings much closer to home – in people’s own homes and on the high street.

A Halifax bank survey found one in five British adults surveyed expect house prices to fall over the next 12 months. This is the weakest reading for consumer expectations since October 2012.

This negativity regarding the housing market is thanks to concerns over the economy, weak wage growth and concerns over rising inflation. For years the UK government has rallied around the UK housing market, convincing citizens that owning a home was a right of passage. It seems the jig is up.

Most new buyers are losing faith in the housing market as not only is the cost of borrowing set to raise but raising the funds for a deposit is near impossible. In the three months to August there was negative wage growth, bringing the total number of months of negative growth to six for 2017, alone.

In all regions of the UK incomes have failed to rise by more than the current inflation rate of 3%. This is not only placing pressure on the housing market but also on consumer spending.

A ‘steep drop’ in retail sales was reported in the CBI survey this month, alongside orders placed with suppliers dropping at their fastest rate since the spring of 2009.

But people still need to eat, clothe themselves, keep a roof over their families’ heads and this is where the government has gone so badly wrong. By fuelling an era of cheap credit, stealthflation, zero-hour contracts and low wage growth families and individuals no longer know how to survive on their wage packets.

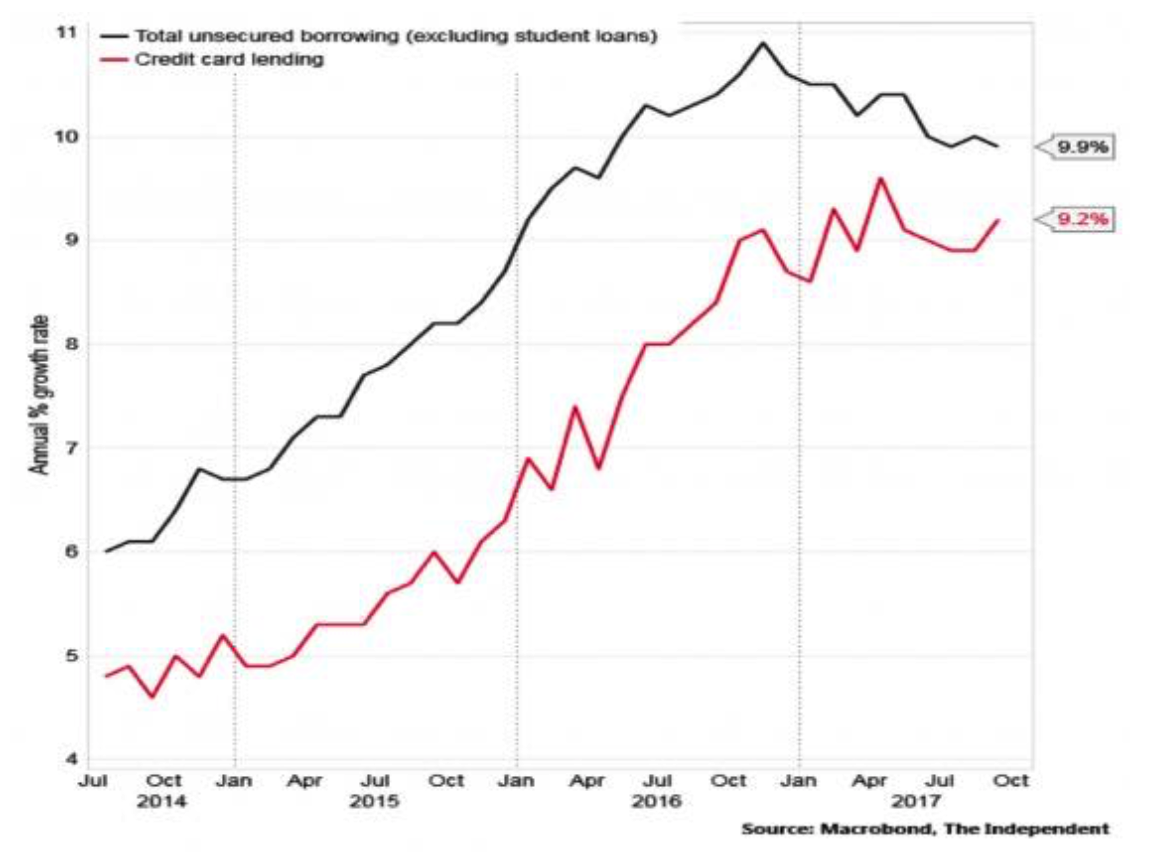

The annual rate of growth of consumer credit climbed is currently at 9.9%, having been as high as 10% in the summer.

According to Bank of England data, another £641m was put onto plastic in the month of September, the sharpest increase in debt since May 2016. The total credit card debt stock reached £69.4bn, the highest on record.

Unsurprisingly, this isn’t sustainable. The number of people registering as insolvent in England and Wales hit a five-year high in the third quarter

The number of those registering as insolvent is only set to get worse should interest rates rise. A hike would push up the cost of both secured and unsecured borrowing.

As Gillian Guy, the chief executive of Citizens Advice, told the Independent:

“The rise and rise of consumer debt is a cause for alarm at a time when large numbers of people are already in financial difficulty.”

Broken government = broken economy

Of course, very little of the ‘on the ground’ problems such as wage growth and consumer debt levels are making the headlines.

The headlines are the same as they have been for the last 18 months or so: BREXIT DISASTER.

Is it a disaster? Who knows, but what we do know is that it is costing a huge amount of money with even more expected to be paid out in the coming years. This is all money that the UK simply does not have.

It was only a fortnight ago that we found out Britain’s stock of wealth had fallen from a surplus of of £469 billion to a net deficit of £22 billion. This is down to a massive write-down of the UK’s assets and a drop in foreign direct investment (again, a lack of confidence in the UK).

Meanwhile the gap between government spending and tax receipts is also expected to ‘outperform’ expectations. The Institute for Fiscal Studies (IFS) expects it to reach £36bn by 2021-22, more than twice the initial official forecast of £17bn.

On the issue the IFS said:

“It is hard to see how the chancellor can both maintain the credibility of his fiscal targets and respond effectively to the growing demands for spending”

Quite. The outlook is not good. Productivity is expected to decline in the UK as the majority of jobs being created are low-skilled, low-wage jobs created for those in need. How this helps the UK tax receipts? It doesn’t.

The Office for Budget Responsibility (OBR) has said the UK government will need to significantly lower its estimates for the economic output per hour worked in Britain. In a massive miscalculation admission it states that it views the 0.2% rate of productivity growth over the past five years as a better guide for 2017 than its forecast of 1.6% in March.

EU, it holds the first charge

Not only does the UK government not have the income to sort out its deficit or increase spending but the EU is coming after us for more money.

No one quite knows just yet what the ‘divorce bill’ will be, but more worryingly it looks like we can’t get back the money we placed in a bank we own 16% of.

According to Alexander Stubb (vice president of the European Investment Bank) the UK may have to wait 30 years to get its £3bn back from the EU’s bank after Brexit and could be on the hook for £30billion if “things go sour”.

As bad as this sounds, can we at least enjoy the hint of irony in this situation. A UK government that has done very little to support customers from the tyranny of British banks, supported bail-outs and pushed for bail-ins is now facing its own problems getting back its money from a bank.

UK savers need to start learning from the mistakes of their leaders.

Conclusion: prepare for the long-term

The 2008/09 financial crisis was not the first economic disaster to hit the United Kingdom. Consider the Wall Street crash on 1929. It very quickly affected this small island nation, causing the economy to shrink by more than 5% and unemployment to spiral to 17%. All in just three years.

Today we find ourselves on arguably scarier ground. Despite lower unemployment, it is an increasingly unproductive labour force with which we find ourselves. It’s nine years ago that the last financial crisis started and the economy has rebounded by less than 10% – a far slower pace than after the Great Depression.

The difference? In the 20th century the government put in place policies that worked for the long-term health of the economy. Today, governments are not looking at anything other than day-to-day results. They no longer prepare for the long-term health of the economy.

They are looking at Brexit and how to boost confidence in the UK. They have no idea how to do anymore, Brexit has got their knickers in a twist. This is unlikely to help struggling savers and consumers in the meantime.

Very often plans that result in positive outcomes a few years down the line aren’t good for an election just a couple of years away. This means that we live in a five-year cycle of economic policies, budgets and grand plans.

Unfortunately this leaves savers and investors fending for themselves when it comes to planning their long-term finances. This is made more complex by the increasingly uncertain times in which politicians and central bankers are inevitably navigating us towards.

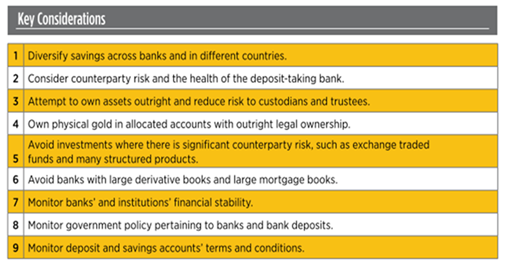

With this in mind we need to take our finances into our own hands. As we explained last week, we must prepare. Failure to prepare is preparing to fail.

Investors should protect themselves from the financial risks of the UK government by diversifying their savings and owning physical gold -not paper or digital gold.

Physical gold that is allocated and segregated cannot fall victim to bail-ins when the government is short of cash or inflation when the central ban needs to print more money.

Physical gold in your portfolio reduces the level of counterparty risk your savings are exposed to and ensures some level of sovereignty and financial safety and freedom when it comes to your wealth.

These financial risks including bail-ins are a threat to all savers in the western world.

News and Commentary

Small Caps Routed as U.S. Stocks Fall, Bonds Rise (Bloomberg.com)

Gold price rises 3.2% in Q3 (MiningWeekly.com)

Gold notches a gain for a second day as strong dollar pauses its climb (MarketWatch.com)

Gold steadies ahead of bumper week for central bank news (Reuters.com)

Trump likely to pick Jerome Powell as next Fed chair: source (Reuters.com)

Credit: Wall Street Journal

Credit: Wall Street Journal

This Could Be Huge: Gold Bar Certified By Royal Canadian Mint Exposed As Fake (ZeroHedge.com)

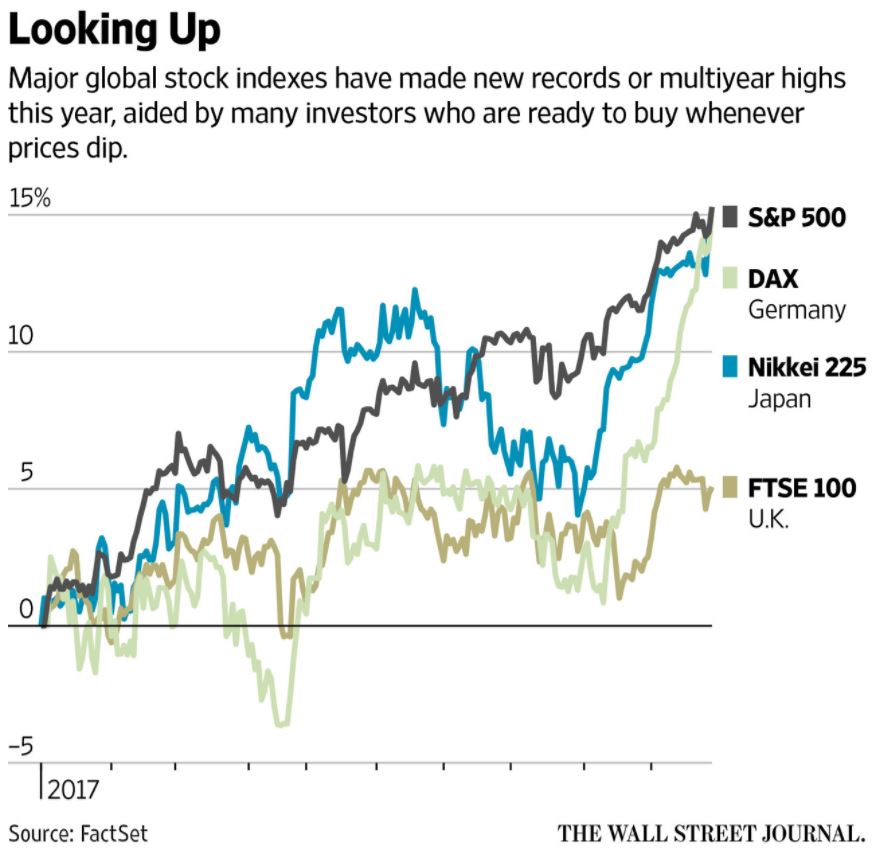

Why Are Markets Rising Everywhere? Investors Can’t Stop Buying Every Dip (WSJ.com)

The US government quietly added $200+ billion to the debt this month alone. (SovereignMan.com)

Are ICOs Replacing IPOs? (USFunds.com)

The economy is failing. We need to think radically about how to fix it (TheGuardian.com)

Gold Prices (LBMA AM)

31 Oct: USD 1,274.40, GBP 964.21 & EUR 1,095.60 per ounce

30 Oct: USD 1,272.75, GBP 966.91 & EUR 1,093.80 per ounce

27 Oct: USD 1,267.80, GBP 968.35 & EUR 1,090.18 per ounce

26 Oct: USD 1,278.00, GBP 968.34 & EUR 1,082.34 per ounce

25 Oct: USD 1,273.00, GBP 964.81 & EUR 1,081.67 per ounce

24 Oct: USD 1,278.30, GBP 970.36 & EUR 1,087.32 per ounce

Silver Prices (LBMA)

31 Oct: USD 16.82, GBP 12.72 & EUR 14.45 per ounce

30 Oct: USD 16.74, GBP 12.69 & EUR 14.39 per ounce

27 Oct: USD 16.72, GBP 12.76 & EUR 14.38 per ounce

26 Oct: USD 16.97, GBP 12.84 & EUR 14.37 per ounce

25 Oct: USD 16.89, GBP 12.75 & EUR 14.34 per ounce

24 Oct: USD 17.04, GBP 12.92 & EUR 14.49 per ounce

Recent Market Updates

– Wozniak and Thiel Fuel Bitcoin-Gold Debate: Gold Comes Out On Top

– Russia Buys 34 Tonnes Of Gold In September

– Gold Will Be Safe Haven Again In Looming EU Crisis

– Gold Is Valuable Due to “Extreme Rarity” – Must See CNN Video

– Gold Is Better Store of Value Than Bitcoin – Goldman Sachs

– Next Wall Street Crash Looms? Lessons On Anniversary Of 1987 Crash

– Key Charts: Gold is Cheap and US Recession May Be Closer Than Think

– Gold Up 74% Since Last Market Peak 10 Years Ago

– How Gold Bullion Protects From Conflict And War

– Silver Bullion Prices Set to Soar

– Brexit UK Vulnerable As Gold Bar Exports Distort UK Trade Figures

– Puerto Rico Without Electricity, Wifi, ATMs Shows Importance of Cash, Gold and Silver

– U.S. Mint Gold Coin Sales and VIX Point To Increased Market Volatility and Higher Gold

Japan Just Killed The “Bitcoin Will Be Banned” Meme

Authored by Charles Hugh Smith via OfTwoMinds blog,

The Japanese recognize the adoption of cryptocurrencies and blockchain technologies as a competitive advantage, and they’re right.

One of the most durable claims of cryptocurrency skeptics is that “governments will ban bitcoin once it threatens their fiat currency or their control.” Ben Bernanke recently gave voice to this claim as if it was received wisdom.

Sorry, crypto-skeptics: Japan just killed the “bitcoin will be banned” meme. Japan has established itself as the safe haven of all legit cryptocurrencies and cryptocurrency exchanges.

Japan is not just the world’s third largest economy; it is a keystone of the global economy in supply chains, ownership of overseas assets, capital flows and technology. Japan’s embrace of cryptocurrencies suggests the Japanese understand that adoption of crypto and blockchain technology offers whatever nation is firstest with the mostest in legal protection of these technologies will have a powerful competitive advantage.

Many crypto skeptics claim the U.S. can browbeat adopters of bitcoin into banning cryptos via various threats such as limiting access to U.S. banking. Memo to skeptics: Japan is too strategically important for the U.S. to browbeat over something as small in scale as cryptos. Furthermore, Japan is long past the point where it will automatically comply with every self-destructive demand of the American Imperial project.

As I have often noted here, the market cap of the entire crypto market–$170 billion– is mere signal noise in the $500+ trillion market of global assets. Even if the crypto market rose 10-fold to $1.7 trillion, it would still be nothing but a tiny blip in the global asset marketplace.

Japan has the regulatory legal and bureaucratic structure to monitor and police crypto exchanges and transactions. This complex structure can be deployed to bog down whatever Japan doesn’t favor in endless red tape, or it can accommodate whatever Japan favors. Clearly, Japan favors the adoption of cryptocurrencies and blockchain technologies.

The legalization of cryptocurrencies is now a done deal. Any nation foolish and self-destructive enough to attempt to outlaw cryptos will simply hasten the flow of capital to Japan and other safe-haven early adopters.

Clearly, the Japanese recognize the adoption of cryptocurrencies and blockchain technologies as a competitive advantage, and they’re right.

“We’re Back”- China’s Largest Crypto Traders Are Relocating

Sorry, Mr. Bernanke, you’re wrong yet again.

Of related interest: Why Governments Will Not Ban Bitcoin (October 23, 2017)

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. Check out both of my new books, Inequality and the Collapse of Privilege($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print, $5.95 audiobook) For more, please visit the OTM essentials website.

END

We brought you this story yesterday and it is quite concerning: somebody made a fake one oz Canadian gold bar with fake mint wrapping. So far only one bar has shown up

(courtesy Ottawa Citizen/GATA)

Elaborate fake gold bar sparks investigation by RBC and police

Submitted by cpowell on Tue, 2017-10-31 01:41. Section: Daily Dispatches

By Vito Pilieci

Ottawa Citizen

Monday, October 30, 2017

http://ottawacitizen.com/news/local-news/elaborate-fake-gold-bar-sparks-…

RBC Royal Bank is working with police to investigate allegations that one of its branches on Bank Street sold a gold bullion 1-ounce bar that turned out to be an elaborate counterfeit.

CBC reported today that on Oct. 18 Samuel Tang walked into the bank, located at the corner of Bank Street and First Avenue, to buy a 1-ounce gold bar. Tang is a gemologist and jewelry designer who works across the road at Joy Creations. The small bar he was provided looked as if it had come from the Royal Canadian Mint, but upon closer inspection, it was found to be a fake.

Alex Reeves, a spokesman for the Royal Canadian Mint, said experts from the federal agency have inspected the bar in question and found it to be a rather elaborate fake. Reeves said the mint has seen fake coins and bullion in the past; however, they are usually of poor quality. He said that whoever made this counterfeit bar tried to copy an older mint design that is no longer in circulation. He said even the wrapper the bar came in was forged by someone.

Reeves said the bar did not come from the mint. Gold is purified at the mint, then immediately used to make coins and bullion, which are sealed in official casings before being sent to distributors. He said the mint is very proud of its reputation as one of the world’s leading refiners of gold and silver and has numerous layers of security in place to prevent counterfeits from making their way into the supply chain.

How RBC ended up with the fake bar is something that Reeves would not speculate about.

AJ Goodman, a spokesman with RBC, said the bank is working closely with police to determine how the counterfeit bar made its way into the bank’s inventory.

“This matter is now with law enforcement for further investigation,” he said. “Instances of counterfeit objects making their way into our inventory are extremely rare. Upon discovering these objects, we immediately investigate to determine the source of the object and engage the appropriate authorities. In all instances we work closely with our clients to keep them informed and to reach a potential resolution.”

Goodman also said that RBC gets its gold from many sources, including the mint, and that the bank guarantees the purity of the products it sells.

Attempts to reach the jewelry designer Tang today for comment were unsuccessful. Tang is traveling to Hong Kong to visit with family for the next three weeks.

END

A futures market for bitcoin will be the death knell for this cryptocurrency as paper shorts will swamp this vehicle

(courtesy zerohedge)

Bitcoin Bounces Back To Record High As CME Launches Bitcoin Futures In Q4

As the mainstream continues to embrace cryptocurrencies – much to the chagrin of Jamie Dimon et al. in the establishment – CME Group is “responding to client interest” and launching a Bitcoin Futures contract in Q4.

CME Group says new contract will be cash-settled, based on the CME CF Bitcoin Reference Rate (BRR) which serves as a once-a-day reference rate of the U.S. dollar price of bitcoin.

This news has sent Bitcoin back up to record highs…

CME Group, the world’s leading and most diverse derivatives marketplace, today announced it intends to launch bitcoin futures in the fourth quarter of 2017, pending all relevant regulatory review periods.

The new contract will be cash-settled, based on the CME CF Bitcoin Reference Rate (BRR) which serves as a once-a-day reference rate of the U.S. dollar price of bitcoin. Bitcoin futures will be listed on and subject to the rules of CME.

“Given increasing client interest in the evolving cryptocurrency markets, we have decided to introduce a bitcoin futures contract,” said Terry Duffy, CME Group Chairman and Chief Executive Officer.

“As the world’s largest regulated FX marketplace, CME Group is the natural home for this new vehicle that will provide investors with transparency, price discovery and risk transfer capabilities.”

Since November 2016, CME Group and Crypto Facilities Ltd. have calculated and published the BRR, which aggregates the trade flow of major bitcoin spot exchanges during a calculation window into the U.S. Dollar price of one bitcoin as of 4:00 p.m. London time. The BRR is designed around the IOSCO Principles for Financial Benchmarks. Bitstamp, GDAX, itBit and Kraken are the constituent exchanges that currently contribute the pricing data for calculating the BRR.

“We are excited to work with CME Group on this product and see the BRR used as the settlement mechanism of this important product,” said Dr.Timo Schlaefer, CEO of Crypto Facilities.

“The BRR has proven to reliably and transparently reflect global bitcoin-dollar trading and has become the price reference of choice for financial institutions, trading firms and data providers worldwide.”

CME Group and Crypto Facilities Ltd. also publish the CME CF Bitcoin Real Time Index (BRTI) to provide price transparency to the spot bitcoin market. The BRTI combines global demand to buy and sell bitcoin into a consolidated order book and reflects the fair, instantaneous U.S. dollar price of bitcoin in a spot price. The BRTI is published in real time and is suitable for marking portfolios, executing intra-day bitcoin transactions and risk management.

Cryptocurrency market capitalization has grown in recent years to $172 billion, with bitcoin representing more than 54 percent of that total, or $94 billion. The bitcoin spot market has also grown to trade roughly $1.5 billion in notional value each day.

* * *

As CoinTelegraph noted previously, mainstream exchange embrace of Bitcoin could lead to less volatility and further acceptance and new opportunities.

In what can be seen as a mainstream financial world’s embrace of Bitcoin, the Chicago Mercantile Exchange (CME Group) and Intercontinental Exchange Inc. (ICE) are all set to publish data on prices of Bitcoin. CME Group is likely to start publishing this data in the fourth quarter of 2016 while ICE, the owner of the New York Stock Exchange (NYSE) is considering if it should include data from various exchanges for a daily settlement price which it has been publishing since May of 2015.

Recently Dwijen Gandhi of ICE told Reuters that NYSE will soon launch a real-time pricing index which he said would provide additional transparency and insight into the Bitcoin price.

CME Group plans two new Bitcoin products

CME Group and ICE taking the Bitcoin dive is good news for the newly established ‘Digital Asset Class’. The participation of exchanges would allow investors and traders alike to easily acquire the information that they need to trade Bitcoin with more confidence.

According to a press release dated May 2, 2016, the CME group has said that they will collaborate with Crypto Facilities Ltd, a digital assets trading platform, and that they will be developing two new products which they plan to launch by Q4, 2016.

CME CF Bitcoin Reference Rate (BRR), which will provide a final settlement price in US dollars at 4 PM London Time on each trading day and the CME Bitcoin Real Time Index (RTI), which allows for real time access to Bitcoin prices.

Cointelegraph talked with Sandra Ro, Executive Director at CME Group about how these developments would affect Bitcoin prices and she says:

“There is no current bitcoin reference rate which is considered “standard” market convention. There are many real time indices but we believe our methodology, inclusion of only the most serious bitcoin exchange data, and focus on developing digital assets will add significant credibility to the nascent digital asset market.”

It is notable that RTI will be calculated by Crypto Facilities and will be calculated based on global demand to buy and sell Bitcoin aggregated into a consolidated order book.

The Price of Bitcoin will be in US dollar terms and will be published once every second according to data made available by CME on the website.

NYSE Bitcoin index NYXBT

On the other hand, the New York Stock Exchange has already wet its feet in the Bitcoin pool by launching the NYSE Bitcoin Index (NYXBT). NYXBT is the first ever exchange-calculated and disseminated Bitcoin index according to ICE.

NYXBT uses a ‘unique methodology’ according to the ICE press release which relies on “rules-based logic to analyse a dataset of matched transactions and verify the integrity of the data to ultimately produce an objective and fair value for one Bitcoin in US Dollars at 4 pm London Time.”

NYXBT will at first take data from transactions from the Coinbase exchange. It is pertinent to mention here that NYSE had made a minority investment in Coinbase in 2015.

Thomas Farley, NYSE Group President, says:

“As a global index leader and administrator of ICE LIBOR, ICE Futures U.S. Dollar Index and many other notable benchmarks, we are pleased to bring transparency to this market. By combining our technology infrastructure with our expertise in index calculation and data management, we will continue to launch complementary products based on our rigorous standards and proprietary index methodology.”

Expect more mainstream participation and new products

It seems that the mainstream financial world is finally ready for Bitcoin. This could mean a new era in which Bitcoin could actually become THE digital asset class and could also lead to further delivery of new financial products for traders and investors.

Cointelegraph talked with Fran Strajnar, Founder and chief executive officer of BraveNewCoin (BNC), an institutional Digital Asset Data provider. Strajnar is excited about these new developments.

Strajnar says to CoinTelegraph:

“What Bitcoin and the entire Digital Asset Class needs to hit mainstream is not just consumer and application adoption but financial infrastructure and the adoption of quality market data services, by well established trading platforms.”

He added that BNC itself provides market data and indexing solutions.

As for opportunities for traders in the form of new products, he thinks that because Bitcoin is global, functions like nothing else and requires a global spot price.

Strajnar expects to see two things evolve from CME’s Bitcoin reference rollout in Q4:

- Creation of various Derivative products & further ETF potential, which will help with reducing volatility.

- A disparity between US Dollar denominated Bitcoin trading activity and other BTC trading pairs, seeing as the CME index only includes BTC/USD trading. A good arbitrage opportunity will come out of this.

end

Nothing new here” The gold market is moving from West to East;

(courtesy Xinhua News Agency, Beijing)

Gold market is moving from West to East, Shanghai exchange chief says

Submitted by cpowell on Tue, 2017-10-31 01:31. Section: Daily Dispatches

Shanghai Gold Exchange Marks 15th Anniversary

From Xinhua News Agency, Beijing

Tuesday, October 31, 2017

SHANGHAI — The Shanghai Gold exchange celebrated its 15th anniversary on Monday.

The exchange started business on Oct. 30, 2002, and the last 15 years have been a journey of the opening up of China’s gold market, the exchange said in a statement.

In 2007 China became the world’s largest gold producer, replacing South Africa, it said. According to the China Gold Association, China produced 453 tonnes of gold and bought 975 tonnes in 2016.

“The exchange has led the international gold market in terms of volumes, and the market is moving from the West to the Dast,” said Jiao Jinpu, chairman of the exchange. …

… For the remainder of the report:

http://news.xinhuanet.com/english/2017-10/31/c_136715806.htm

END

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

2. Nikkei closed UP 0.06 POINTS OR 0.00% /USA: YEN RISES TO 113.33

3. Europe stocks OPENED ALL GREEN /USA dollar index RISES TO 94.62/Euro DOWN TO 1.1634

3b Japan 10 year bond yield: RISES TO +.071/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.72/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.02 and Brent: 60.46

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.381%/Italian 10 yr bond yield DOWN to 1.857% /SPAIN 10 YR BOND YIELD DOWN TO 1.486%

3j Greek 10 year bond yield FALLS TO : 5.523???

3k Gold at $1273.60 silver at:16.83: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 33/100 in roubles/dollar) 58.31

3m oil into the 54 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.33 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9984 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1616 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.381%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.379% early this morning. Thirty year rate at 2.888% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Rebound After Disappointing Chinese, European Data

Yesterday’s sharp Chinese selloff is now a distant memory after the BTFDers emerged, and this morning U.S. equity futures are once again levitating as the FOMC begins its two-day policy meeting, following an uneventful BOJ announcement on Tuesday morning which left all QE parameters unchanged. Asian stocks traded mixed steady while European shares climb.

The key event overnight was the BOJ meeting, in which the central bank maintained QQE with Yield Curve Control and kept NIRP unchanged at -0.1% as expected. The decision to keep QQE with YCC was made by 8-1 vote, with Kataoka the sole dissenter again who suggested the BoJ needs to buy JGBs so that 15yr yield stays below 0.2%, while Kataoka also commented that the BoJ should ease if domestic factors lead to delays in reaching the inflation target. In terms of changes to its outlook forecasts, the BoJ raised FY 17/18 Real GDP growth forecast to 1.9% from 1.8%, while it cut Core CPI forecasts to 0.8% from 1.1% for FY 17/18 and to 1.4% from 1.5% for FY 18/19

Asian shares rose in afternoon trading, with the MSCI Asia Pacific Index gaining 0.1 percent to 168.29 and ignoring the overnight miss across the board in Chinese PMIs…

… Confirming China’s economy is rolling over…

… supported by tech stocks as companies including Sony and Nintendo boosted their forecasts. Samsung gave the biggest boost to the regional gauge and South Korea’s benchmark after announcing a revamp of its executives. Japan’s Nikkei closed just barely lower, technically only its second down day in October, with SoftBank weighing on the index after talks to merge its Sprint unit with T-Mobile US were said to be in peril. Samsung Electronics closed at a record after nominating its Chief Executive Officer Lee Sang-hoon as its next board chairman, along with other management changes, hours after detailing a boost in shareholder payouts. The company’s plans, along with a pledge by South Korea and China to move beyond a year-long dispute over Seoul’s decision to deploy a U.S. missile shield, helped lift the Kospi Index to a new all-time high (remember the North Korea nuclear armageddon threat? Neither does the market).

“South Korean equities gained led by the Korea-China agreement on the Thaad issue and also because of Samsung Electronics’ announcement,” said Min Byungkyu, a global market analyst at Yuanta Securities Korea. Technology stocks rose the most among sub-indexes on the regional gauge, with Nintendo soaring after nearly doubling its annual profit forecast and Sony and Denso Corp. climbing after both companies boosted earnings outlooks. In India, Axis Bank surged after a report that Bain Capital plans to invest in the lender.

Speaking of China, the slump in Chinese government bonds is close to an end, with sentiment set to stabilize as the central bank boosts cash injections, analysts said The yield on the benchmark 10-year government bond fell 3 basis points to 3.90% on Tuesday, halting a four-day increase of 20 basis points that took it to the highest level in three years. The People’s Bank of China injected funds for a fourth day on Tuesday, adding a net 230 billion yuan ($35 billion) in the period.As a result, the SHCOMP halted the recent slump, rising just under 0.1% to 3,393.

In Europe, traders ignored the miss in euro-area inflation data in stride as closed German markets due to a local public holiday has led to a muted European session. The euro-area’s unemployment rate inched lower in September as the economy expanded for an 18th consecutive quarter, but consumer inflation unexpectedly slowed in October, complicating the European Central Bank’s task as it considers tightening policy.

Oil and gas stocks led gains in the Stoxx Europe 600 Index as crude hovered near a six-month high. Most European stocks climb, led by oil and gas sector; FTSE 100 rebounds after BP (+2.6%) earnings and buyback announcement. European energy names lead the way higher in the wake of BP’s earnings (+3.3%) which have subsequently supported the index. Financial names have seen slight underperformance after BNP’s (-3.2%) weak earnings which has also subsequently seen the CAC modestly underperform its peers. Elsewhere, UK gambling names have been granted some reprieve after the UK government’s crackdown on fixed-odd betting terminals does not appear to be as bad as some had initially feared.

Treasuries and core European bonds were mostly steady. Earlier a note of caution had crept into markets in Asian hours following a drop in China’s factory gauge, and equity benchmarks in that region were mixed. Japanese stocks ended the day slightly lower after the Bank of Japan maintained its key policy rate and target for the yield on 10-year government bonds, while showing concerns remain on the inflation outlook.

The yield on 10Y TSY rose less than one basis point to 2.37%. Germany’s 10Y yield decreased less than one basis point to 0.37%, the lowest in two weeks. Britain’s 10Y yield dipped one basis point to 1.335%, the lowest in more than a week.

American tax reform also remains a key theme, with lawmakers said to be considering a phase-in plan. The indictment of former Trump campaign aides in Robert Mueller’s investigation of Russian meddling in the U.S. election, however, may pose a danger to the White House as it tries to push tax cuts though Congress. Fed and BOE rate decisions this week remain in focus for FX, with major currency pairs trading in tight ranges; GBP/USD continues to trade with an upside bias due to positioning into BOE announcement.

West Texas Intermediate crude fell less than 0.05 percent to $54.14 a barrel. Gold decreased 0.1 percent to $1,275.55 an ounce. Oil is poised for its second monthly gain for the first time this year.

Economic data include employment-cost index, Chicago PMI and consumer confidence. Mastercard and Pfizer are among companies reporting earnings today

Bulletin Headline Summary from RanSquawk

- European bourses trade higher with energy names topping the leaderboard after earnings from BP

- EU inflation fell short of expectations but little reaction for EUR with markets already braced for a softer print given German readings yesterday

- Looking ahead, highlights include US APIs

Market Snapshot

- S&P 500 futures up 0.2% to 2,573.25

- MSCI Asia up 0.1% to 168.30

- MSCI Asia ex Japan up 0.3% to 550.81

- Nikkei unchanged at 22,011.61

- Topix down 0.3% to 1,765.96

- Hang Seng Index down 0.3% to 28,245.54

- Shanghai Composite up 0.09% to 3,393.34

- Sensex down 0.06% to 33,245.25

- Australia S&P/ASX 200 down 0.2% to 5,909.02

- Kospi up 0.9% to 2,523.43

- STOXX Europe 600 up 0.08% to 394.22

- German 10Y yield fell 0.8 bps to 0.359%

- Euro down 0.06% to $1.1644

- Brent Futures down 0.4% to $60.67/bbl

- Italian 10Y yield fell 10.0 bps to 1.582%

- Spanish 10Y yield fell 1.8 bps to 1.477%

- Brent Futures down 0.3% to $60.70/bbl

- Gold spot up 0.05% to $1,276.96

- U.S. Dollar Index down 0.04% to 94.52

Top Overnight News

- The Bank of Japan left its massive monetary-stimulus program unchanged even as it trimmed its inflation forecasts, signaling further divergence ahead from its global peers

- France’s economy extended its run of growth into a fifth quarter, marking its best streak in more than six years; the 0.5% expansion in the three months through September, compared with an upwardly revised 0.6% the previous three quarters, was supported by corporate and household investment while trade weighed on growth

- Catalan leader Carles Puigdemont kept his followers guessing as to the next step in his pursuit of an independent republic, after fleeing to Belgium where he’s expected to emerge on Tuesday

- China’s official factory gauge fell to 51.6 in Oct., vs. 52 forecast in Bloomberg survey, and five-year high of 52.4 in Sept., with new orders and prices leading the decline, as officials increasingly prioritize a campaign to clamp down on polluting industries and rein in debt

- White House Downplays Mueller Indictments; Apple Escalates Qualcomm Dispute; Ex-Third Point Partner Drawing SEC Probe

- Congress will put Facebook, Twitter and Google under a public microscope Tuesday about Russia’s use of their networks to meddle in the 2016 election, a day after Special Counsel Robert Mueller’s criminal investigation disclosed its first indictments and guilty plea

- Apple Inc. is designing iPhones and iPads for 2018 that don’t use components from Qualcomm Inc. amid an escalating dispute between the companies

- House tax writers have completed about 90 percent of the tax bill they plan to release this week, Ways and Means Chairman Kevin Brady said Monday — but the last part may be the hardest

- SoftBank Group Corp.’s talks to merge U.S. unit Sprint Corp. with T-Mobile US Inc. have hit a serious snag throwing the deal into jeopardy after months of talks

- The Bank of Japan left its massive monetary stimulus program unchanged even as it trimmed its inflation forecasts, signaling further divergence ahead from its global peers

- Treasury Secretary Steven Mnuchin put to rest for now the idea bubbling in the $14.2 trillion Treasuries market that the government might introduce ultra-long term debt sales

- The old recipe of using bonds to hedge against risks from equity holdings may not be a winner anymore, and investors would be better off with a more complex approach that relies on multiple tactics, according to Pacific Investment Management Co. analysis

A cautious tone persisted in Asia as the region digested softer than expected Chinese PMI data and a dampened lead from the US where reports suggested corporate tax cuts could be gradual. ASX 200 (-0.2%) was indecisive and failed to maintain early energy-led gains, while Nikkei 225 (unch) was kept grounded by a firmer JPY and with SoftBank among the worst performers on reports it plans to abandon merger talks between its unit Sprint and T-Mobile US. KOSPI (+0.9%) gained after reports China and South Korea agree to resolve THAAD-related dispute and with Samsung shares buoyed by record quarterly profits, while Shanghai Comp (+0.1%) and Hang Seng (-0.3%) initially weakened following the miss on Chinese Manufacturing PMI and with some of the big 4 banks pressured post-earnings; the mainland pared losses heading into the clsoe. Finally, 10yr JGBs were relatively flat with only minimal gains seen amid a risk averse tone in Japan and after an unsurprising BoJ policy announcement where dovish dissenter Kataoka suggested more easing.

Top Asian News

- China Factory PMI Falls From Five-Year High on Pollution Cleanup

- BOJ Keeps Stimulus Unchanged as It Trims Inflation Outlook

- China, South Korea Agree to Shelve Thaad Missile Shield Dispute

- Macau Casinos Emerge From Rut as October Revenue Hopes Brighten

- Indian Billionaire Fund Says Bank Boost to Help Clear Loans

With Germany on vacation today, European bourses have started the session on the front-foot (Eurostoxx 50 +0.2%), albeit modestly so. In terms of sector performance, energy names notably lead the way higher in the wake of FTSE-heavyweight BP’s earnings (+3.3%) which have subsequently supported the index. Financial names have seen slight underperformance after BNP’s (-3.2%) lacklustre earnings which has also subsequently seen the CAC modestly underperform its peers. Elsewhere, UK gambling names have been granted some reprieve after the UK government’s crackdown on fixed-odd betting terminals does not appear to be as bad as some had initially feared. A really low key final business day of October in the sovereign bond markets, thus far. Turnover has been extremely light, even allowing for Germany’s Reformation holiday with Bund volume on Eurex around 100k lots (at writing). The German benchmark has also been very rangebound, albeit mainly on the plus side of a 162.64-162.83 trading band, and it appears that many are sitting tight ahead of the key risk events later this week. Indeed, UK Gilts are even more contained within 124.37-54 parameters, awaiting BoE ‘super Thursday’ when a widely anticipated first rate hike in a decade comes with an uncertain vote split, policy meeting minutes, forward guidance and the latest QIR. US Treasuries largely consolidating on Monday’s decent gains made on risk aversion and month end positioning, which saw the 10 year yield retreat clearly below 2.40%, ahead of the FOMC, new Fed chair announcement and monthly jobs report.

Top European News

- Standard Chartered Retail Banking Chief Karen Fawcett to Retire

- Ryanair Chief Seeks Solution to Pilot Crisis as Earnings Slide

- Davis to Brief Cabinet on Brexit Amid Plans to Ramp Up Talks

- MiFID Investment Research May Face VAT Hit From U.K. Taxman

- BNP Slides as 3Q Earnings Miss Estimates on Weaker CIB Revenue

- WPP Lowers Revenue Forecast as Ad Industry’s Woes Deepen

In FX, trade has been particularly tentative thus far with the BoJ only causing a modest uptick in USD/JPY towards 113.00 after the Bank stood pat on rates as expected with 1 dissenter suggesting the need to buy 15yr JGBs to keep yields below 0.2%. EUR saw little in the way of a reaction to the latest miss on expectations for Eurozone inflation (Y/Y 1.4% vs. Exp. 1.5% and core 0.9% vs. Exp. 1.1%) with markets potentially already braced for a lacklustre figure given yesterday’s German prints.

Commodities continue to trade in a particularly tight range with WTI crude futures consolidating around USD 54/bbl. Elsewhere, the metals complex has been relatively non-committal ahead of this week’s FOMC and NFP, while copper lacked impetus overnight amid a cautious risk tone and after weaker than expected PMI data from its largest consumer China.

Looking at today’s key data, notable data includes the flash October CPI print for the Euro area and France, the advanced Q3 GDP report for the Euro area and consumer confidence for the UK for October. In the US the Q3 employment cost index, October Chicago PMI, October consumer confidence and the August S&P/ Case-Shiller house price index is amongst the data due. Onto other events, the ECB’s Visco and Padoan are also due to speak while UK Brexit Secretary David Davis is questioned by the House of Lords EU Committee about the state of Brexit talks. BP and BNP Paribas are amongst the companies reporting results.

US Event Calendar

- 8:30am: Employment Cost Index, est. 0.7%, prior 0.5%

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.4%, prior 0.35%; YoY NSA, est. 5.93%, prior 5.81%; US HPI YoY NSA, prior 5.94%;

- 9:45am: Chicago Purchasing Manager, est. 60, prior 65.2

- 10am: Conf. Board Consumer Confidence, est. 121.3, prior 119.8; Present Situation, prior 146.1; Expectations, prior 102.2

DB’s Jim Reid concludes the overnight wrap

The bond bullish/bearish switch that has alternated at regular intervals over the last few weeks has firmly switched to bull mode since the ECB meeting less than 72 business hours ago. Yesterday this got an additional boost by good news from the Peripherals, weaker German inflation, a former Trump campaign manager charged in connection with the Russia probe and reports that the US corporate tax rate may only be lowered in increments over 5 years.

In the US, House tax writers are discussing a phase-in approach for corporate tax cuts, allowing the tax rate to gradually fall from 35% in 2018 to 20% by 2022 (ie: -3ppt per year), as per Bloomberg. The plans are not yet final and when asked, House Ways and Means Chairman Brady only said “we want to get the growth up front”. Treasury secretary Mnuchin noted “the objective is not to have that phase in, but we will see how that goes”. Looking ahead, the Ways and Means panel is expected to release the draft bill this Wednesday for further debate.

Staying in the US, Bloomberg reported that three people have been indicted by Robert Mueller’s Special Counsel in relation to potential Russian influence on the 2016 US presidential election, including: 1) President Trump’s former campaign chairman (Paul Manafort) for conspiracy and money laundering (receiving payments from Ukrainian political parties and then laundered some of the payments back into US, 2) Ex-foreign policy adviser to Trump (George Papadopoulos), who reportedly lied about the timing of his contacts with foreign nationals, where he communicated with an overseas professor during the campaign (March 2016), who told him about Russians possessing “dirt” on Hillary Clinton in the form of “thousands of emails” and 3) a business partner of Mr Manafort. Elsewhere, President Trump tweeted “sorry, but this is years ago, before Paul Manafort was part of the Trump campaign”. However, the indictment noted Manafort’s illegal acts lasted into early 2017.

It’s too early to know if there’s are any ramifications for politics or even the tax reforms but the guilty plea by George Papadopoulos, who served as a foreign-policy adviser to President Trump during the campaign suggests the Investigators may have someone who appears to be fully cooperating. This could potentially have a material impact.

Turning to Catalonia where tensions have cooled. The Spanish government retook control of the Catalan region yesterday with little resistance and the ousted Catalan President Puigdemont has reportedly fled to Brussels, potentially seeking asylum while other party members will continue with the new election scheduled for 21 December. Puigdemont is expected to make an address later today. Elsewhere, El Mundo reports that opinion polls conducted early last week (before independence was declared) show that support for Catalan independence fell to 33.5% in the region. As a reminder, El Mundo also reported yesterday that opinion polls suggest Catalan secessionists could win 65 seats in a new election, but fall short of the 68 seats needed for new majority. The Spanish markets responded favourably, with the IBEX up 2.44% and 10y yields down 9.3bp. To put the mini bond rally in context, Spanish 10y yields are now the lowest since early September and 20bp lower than the day after referendum took place (1 October) and 15bp lower than the day before last week’s ECB meeting.

Staying in government bonds, core European bond yields fell c2bp yesterday (Bunds -1.6bp; Gilts -1.4bp; OATs -2.9bp) while UST 10 fell 3.8bp driven by the aforementioned factors. Peripherals outperformed with 10y yields down 9-12bp (Spain -9.3bp; Italy -10.4bp; Portugal -11.9bp), with Italian bonds likely supported by S&P’s credit rating upgrade late last Friday, where it lifted the country’s rating 1 notch higher to BBB, citing strengthening economic outlook, an uptick in employment and a stronger banking sector.

This morning, the BOJ voted 8-1 to retain its monetary stimulus policy, with the new board member dissenting. As our Japanese economist expected, the BOJ has trimmed its near term core inflation outlook to 0.8% for 2017 (-0.3ppt) and 1.4% for 2018 (-0.1ppt). However, the outlook for 2019 remains unchanged at 1.8%. In China, the October manufacturing PMI was softer than expectations at 51.6 (vs. 52), but remember that last month’s reading of 52.4 was the highest since 2012. This morning, Asian markets have followed the negative lead from the US and are trading slightly lower. The Nikkei (-0.24%), Hang Seng (-0.08%) and Shanghai Comp. (-0.25%) are down slightly, but the Kospi is up 0.66%, after China and South Korea agreed to restore bilateral relations and put aside a yearlong disagreement over the deployment of a US missile shield.

Recapping other market performance from yesterday now. US bourses softened from their record highs with the S&P and Dow both down slightly (-c0.3%), while the Nasdaq was broadly flat (-0.03%), partly aided by Apple where its shares rose 2.25% following reports of strong demand for its new iPhone X. Indeed my devise won’t be shipped for 4-5 weeks!!! Within the S&P, modest gains in the real estate and tech sectors were more than offset by losses from health care and t elco stocks (-1.41%), with the latter partly impacted by reports suggesting the merger between Sprint and T-Mobile may not occur. Core European markets were little changed, with the Stoxx 600 and DAX up 0.1% while the FTSE dipped 0.23%. Elsewhere, Spain’s IBEX led the gains (+2.44%) as tensions cooled in the region, while Italy’s MIB also rose 0.39%.

Turning to currencies, the US dollar index fell 0.38%, while the Euro gained 0.37% and Sterling rose 0.61% ahead of the BOE rate meeting this Thursday where the majority expect a rate hike (85.9% odds per Bloomberg). In commodities, WTI rose slightly (+0.46%) while Iron ore fell (-2.21%) for the fourth consecutive day. Elsewhere, both precious metals (Gold +0.23%; Silver -0.07%) and other base metals were mixed but little changed (Copper +0.28%; Zinc +0.57%; Aluminium -0.22%).

Away from the markets, Treasury secretary Mnuchin has backed away from the notion of issuing US treasuries with ultra-long maturities. He noted “we’ve done a bunch of research…at least for now, we don’t see a lot of demand for it” and that “if we could issue ultra-long bonds at the same yield as 30-year bonds, it makes a lot of sense”, but “if it turns out there’s a big premium….there’s no reason for us to do that”.

Turning to Brexit, perhaps in a bid to fast track progress before the big EU summit on 14 December where EU leaders may give the green light to start talks on trade and transition deals, the UK PM May and Brexit Secretary Davis are seeking to change the timing and structure of the negotiations with the EU, from four day sessions held once a month to more regular and ongoing talks as it may help both sides to make the necessary compromises. We shall find out more today as Mr Davis is scheduled to speak to the cabinet.

The latest ECB holdings were released yesterday. Net CSPP averaged €352mn/ per day last week (€367mn before April 2017 and €321mn since then, i.e. -12.3% since QE trimming). Net PSPP averaged €2,286mn/per day last week (€3,178mn before April 2017 and €2,440mn since then, i.e. -23.2% since QE trimming). This left the CSPP/PSPP ratio at 15.4% last week (13.5% over last 4 weeks vs. 11.5% before QE was trimmed in April 2017). We still think the ECB will likely keep CSPP relatively unscathed when they halve their APP in January.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the macro data was a bit mixed. The September PCE Core was in line at 0.1% mom and 1.3% yoy. On a six-month annualized basis, core inflation is running slightly higher at 1.5%, but still remains below the Fed’s target of 2%. Elsewhere, personal spending grew at the fastest pace since 2009 up 1% mom (vs. 0.9%) and outpacing an in line personal income growth of 0.4% mom. Finally, the October Dallas Fed manufacturing activity index was above expectations at 27.6 (vs. 21 expected) – marking the highest reading since March 2006.

In Germany, October CPI was lower than expected, at -0.1% mom (vs. 0.1% expected) and 1.5% yoy (vs. 1.7% expected) – the lowest annual rate since November 2016. The September retail sales was in line at 0.5% mom, but datarevisions to prior readings meant annual growth was higher at 4.1% yoy (vs. 3% expected). In Europe, the final reading of consumer confidence was in line at -1, while the business climate confidence (1.44 vs 1.4 expected) and economic confidence (114 vs 113.3 expected) both beat expectations, the latter is now at the highest level since January 2001. In the UK, the September mortgage approvals was broadly in line at 66.2 (vs. 66k expected). Over in Spain, 3Q GDP was in line at 0.8% qoq, leaving a solid through year growth of 3.1%. Elsewhere, October Spanish inflation rose 0.6% mom, leading to an annual reading of 1.7% yoy (vs. 1.7% expected).

Looking at the day ahead, notable data includes the flash October CPI print for the Euro area and France, the advanced Q3 GDP report for the Euro area and consumer confidence for the UK for October. In the US the Q3 employment cost index, October Chicago PMI, October consumer confidence and the August S&P/ Case-Shiller house price index is amongst the data due. Onto other events, the ECB’s Visco and Padoan are also due to speak while UK Brexit Secretary David Davis is questioned by the House of Lords EU Committee about the state of Brexit talks. BP and BNP Paribas are amongst the companies reporting results

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 3.00 points or .09% /Hang Sang CLOSED DOWN 90.65 pts or 0.32% / The Nikkei closed UP 0.06 POINTS OR 0.00/Australia’s all ordinaires CLOSED DOWN 0.12%/Chinese yuan (ONSHORE) closed UP at 6.6315/Oil UP to 54.02 dollars per barrel for WTI and 60.86 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6315. OFFSHORE YUAN CLOSED AT VALUE OF THE ONSHORE YUAN AT 6.6335 AND //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA//

We warned you that this could happen. More than 300 are dead after tunnels collapse at the North Korean nuclear test site after suffering minor quakes last month:

(courtesy zerohedge)

“More Than 200” Dead After Tunnel Collapses At North Korean Nuclear Test Site

North Korean nuclear scientists apparently ignored warnings from a group of Chinese scientists who briefed them back in September that the North’s Punggye-ri nuclear test site was slowly imploding following the country’s sixth nuclear test, which involved a 100-kiloton hydrogen bomb roughly seven times more powerful than the atomic bomb the US dropped on Hiroshima in 1945.

As Japanese TV station Asahi TV reported Tuesday, more than 200 North Koreans were killed earlier this month when several tunnels in the underground complex collapsed, killing more a crew of laborers and a crew of rescue workers sent to save them. As we’ve reported previously, scientists in the US, China and South Korea have warned that further tests at the site could blow the top off the mountain, causing it to collapse. Meanwhile, it could send a plume of radioactive particles into the atmosphere that could deleteriously impact population centers in Northern China and across the region.

Scientists detected a series of small earthquakes under Punggye-ri after the country’s Sept. 3 nuclear test. The seismic activity, combined with satellite images of landslides and depressions forming on the mountain’s surface, led a group of American scientists to declare that Punggye-ri was suffering from “tired mountain syndrome” – a condition previously observed at Soviet nuclear test sites. South Korea’s weather agency chief Nam Jae-Cheol told a meeting of the lawmakers Monday that any future nuclear test at the site could cause a collapse. One of the Korea Meteorological Administration researchers, Lee Won-Jin, presented an analysis of satellite images indicating landslides occurred near the facility following the September test.

The small-scale quakes at the facility, built south of the Mantapsan mountain, suggest it may not be stable enough to conduct any further tests. However, the construction of new underground tunnels in the complex would suggest the North – unwilling or unable to build an entirely new facility in a different location – has instead opted to move its tests to another area of the mountain.

“If North Korea were to attempt to continue testing under this mountain (such as in the area more to the eastern side), then we would expect to see new tunneling in the future near the North Portal, still under Mt. Mantap,” researchers Frank Pabian and Jack Liu wrote in a report published earlier this month.

Of course, the condition of the test site would be irrelevant if the North decides to follow through with a threat to conduct “an unprecedented scale hydrogen bomb” test over the Pacific. North Korean officials have insisted in recent weeks that these threats are serious. Perhaps the Kim regime has been so preoccupied assessing the damage at Pyungge-ri, where five of the North’s six nuclear tests held since 2006 have taken place, that it has been forced to put any future tests on hold.