GOLD: $1277.7 DOWN $5.15

Silver: $16.98 DOWN 10 cents

Closing access prices:

Gold $1278.30

silver: $17.01`

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1289.94 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1281.20

PREMIUM FIRST FIX: $9.39

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1292.56

NY GOLD PRICE AT THE EXACT SAME TIME: $1282.40

Premium of Shanghai 2nd fix/NY:$10.16

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1285.70

NY PRICING AT THE EXACT SAME TIME: $1285.70

LONDON SECOND GOLD FIX 10 AM: $1282.20

NY PRICING AT THE EXACT SAME TIME. 1282.60

For comex gold:

NOVEMBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR: 991 FOR 99,100 OZ (3.082TONNES)

For silver:

NOVEMBER

2 NOTICE(S) FILED TODAY FOR

10,000 OZ/

Total number of notices filed so far this month: 874 for 4,370,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7121 OFFER /$7145 up $532.00 (MORNING)

BITCOIN : BID $7257 OFFER: $7282 // UP $668.00 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A SMALL 777 contracts from 199,122 UP TO 199,899 WITH YESTERDAY’S TRADING IN WHICH SILVER ROSE BY 3 CENTS. AGAIN WE DID HAVE NO LONG LIQUIDATION BUT AGAIN IT LOOKS LIKE WE GOT QUITE A FEW MORE COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE AS WE HAD A HUGE 750 DECEMBER EFP’S ISSUED ALONG WITH 300 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 1050 CONTRACTS. THE ISSUANCE FOR MARCH BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY IN THE UPCOMING DELIVERY MONTH. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER TO BE DELIVERED UPON AT THE COMEX AND THEY MUST EXPORT THEIR OBLIGATION TO LONDON.

RESULT: A SMALL SIZED RISE IN OI COMEX WITH THE 3 CENT PRICE RISE. COMEX LONGS REFUSED TO EXIT OUT OF THE COMEX AND FROM THE CME DATA 1050 EFP’S WERE ISSUED FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS WHICH DEFINITELY EXPLAINS THE FALL IN OI. IN ESSENCE WE DID NOT GET A FALL IN DEMAND IN OPEN INTEREST ONLY A TRANSFER TO OTHER JURISDICTIONS.

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.001 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest ROSE BY A SMALLER THAN EXPECTED 654 CONTRACTS DESPITE THE GOOD RISE IN PRICE OF GOLD ($4.00) WITH YESTERDAY’S TRADING . YESTERDAY’S TRADING SAW NO GOLD LEAVES FALL FROM THE COMEX GOLD TREE. THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY TOTALED: 11,839 CONTRACTS WHICH IS HUGE. THE MONTH OF DECEMBER SAW 11,799 CONTRACTS AND FEB SAW THE ISSUANCE OF 40 CONTRACTS. The new OI for the gold complex rests at 533,054.

Result: A SMALLER SIZED INCREASE IN OI DESPITE THE RISE IN PRICE IN GOLD ON YESTERDAY ($4.00). WE HAD A HUGE NUMBER OF COMEX LONG TRANSFERS TO LONDON THROUGH THE EFP ROUTE AS (11,839 EFP’S). THERE OBVIOSULY DOES NOT SEEM TO BE MUCH PHYSICAL AT THE COMEX AND WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER. WE ALSO HAD NO GOLD COMEX OI LEAVE THE COMEX GOLD ARENA.

we had: 18 notice(s) filed upon for 1800 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

A small change in gold inventory at the GLD/ a deposit of .300 tonnes

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 318.074 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 777 contracts from 199,358 DOWN TO 199,899 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE RISE IN SILVER PRICE (A GAIN OF 3 CENTS). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE 750 PRIVATE EFP’S FOR DECEMBER(WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 300 EFP’S FOR MARCH FOR A TOTAL OF 1050 EFP CONTRACTS, WHICH GIVES OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THESE EFP ISSUANCE..USUALLY WE WITNESS THIS ONE WEEK PRIOR TO FIRST DAY NOTICE AND THIS CONTINUES RIGHT UP UNTIL FDN. WE ALSO HAD NO SILVER COMEX LIQUIDATION. TOTAL EFP’S ISSUED YESTERDAY BY THE CME IN SILVER TOTAL 786 CONTRACTS. SO THIS FRAUD IS CONTINUING ON A DAILY BASIS

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 3 CENT RISE IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ANOTHER 1050 EFP’S ISSUED TRANSFERRING OUR COMEX LONGS OVER TO LONDON TOGETHER WITH NO SILVER COMEX LIQUIDATION.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 27.02 points or .79% /Hang Sang CLOSED DOWN 300.43 pts or 1.03% / The Nikkei closed DOWN 351.69 POINTS OR 1.57%/Australia’s all ordinaires CLOSED DOWN 0.60%/Chinese yuan (ONSHORE) closed UP at 6.6220/Oil DOWN to 55.12 dollars per barrel for WTI and 61.47 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6220. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6239 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea//South Korea

This is what scares me the most: the White House is being warned that North Korea is planning a devastating EMP attack on America

( zerohedge)

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)Not good: China’s 10 yr bond yield breaks above 4% as inflation and risk enters into their economy

( zerohedge)

ii)Last night

China is definitely slowing down as we witness commodities falter. Their stock market did not like that we saw and started to dump securities

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

i)SWEDEN

Sweden’s economy is doing quite well as evidenced by the good growth in GDP. However the ultra low interest rates (negative interest rates) are manifesting itself in Sweden’s housing bubble. It is now beginning to crack as authorities began to squeeze mortgage borrowers

( zerohedge)

ii)Zimbabwe

The Military in Zimbabwe have now officially seized power as they are holding the President Mugabe

( zerohedge)

iib)Amazing, with Zimbabwe undergoing a military coup, there is a shortage of cash. Thus the rise in Bitcoin to over $13,000 in Zimbabwe.

I wonder what the price of one oz of gold will be in Harare?

(courtesy zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

i)INDIA

Inflation is starting to get a firm grip in India as their sovereign bond market is now in trouble

( zerohedge)

ii)VENEZUELA/RUSSIA

Russia is acting like a true statesman: they restructure the 3.2 billion USA payments over 10 years with minimal amount up front. They still have USA based CITGO as collateral

( zerohedge)

9. PHYSICAL MARKETS

i)Ed Steer’s commentary today posted in the clear

( Ed Steer/Gata)

ii)Interesting: 2/3 of the top primary silver producers suffered production declines:

( Steve St Angelo/SRSRocco report)

10. USA stories which will influence the price of gold/silver

i)trading today:

1)the treasury curve collapses to 10 year lows which indicate we are heading for a recession

( zerohedge)

2)Despite constant abuse by manipulators the crooks cannot control the rise in volatility as stocks open lower for the 7th straight day

( zerohedge)

ii)Wednesday morning 8 am

A good explanation as to why today’s CPI reading is very important and could send equities southbound:

( zerohedge)

iii)Firstly Retail sales 8;30 am Wednesday (before the biggy CPI)

excluding the car sales, the yearly growth in retail sales falls to 3.3%. Its monthly gain including autos was 0.2% and ex autos it was 0.1%..definitely slowing down.

( zerohedge)

iv)And now the biggy!! CPI

v)Soft data Empire Mfg fed index tumbles…yet hope surges to 5 yr highsgo figure..

( zerohedge)

vi)This is not going to be good for Puerto Rico bond holders as there may be a debt moratorium for us to 5 years. Puerto Rico bond prices fall below that of Venezuela.

( zerohedge)

vii)This is going to be a biggy!! Amazon is ready to test cashierless stores

( zerohedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY ONLY 654 CONTRACTS UP to an OI level of 533,054 DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($4.00 RISE WITH RESPECT TO YESTERDAY’S TRADING). OBVIOUSLY WE DID NOT HAVE ANY GOLD COMEX LIQUIDATION. HOWEVER WE DID HAVE A MONSTROUS 11,839 COMEX LONGS EXIT THE COMEX ARENA THROUGH THE EFP ROUTE AS THEY RECEIVE A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 11,799 EFPS WERE ISSUED FOR DECEMBER AND 40 WERE ISSUED FOR MARCH. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

Result: a SMALL INCREASE IN OPEN INTEREST DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($4.00.) A HUGE 11,939 EFP’S ISSUED FOR A FIAT BONUS AND A DELIVERABLE FORWARD GOLD CONTRACT IN LONDON.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF 0 CONTRACT(S) REMAINING AT 71. We had 0 notices filed YESTERDAY so GAINED 0 contracts or NIL additional oz will stand for delivery in this non active month of November. TO SEE BOTH GOLD AND SILVER RISE IN AMOUNT STANDING (QUEUE JUMPING) IS A GOOD INDICATOR OF PHYSICAL SHORTNESS FOR BOTH OF OUR PRECIOUS METALS.

The very big active December contract month saw it’s OI LOSE 12,605 contracts DOWN to (OF WHICH 11,839 WERE EFP TRANSFERS). January saw its open interest FALL by 20 contracts up to 844. FEBRUARY saw a gain of 12,730 contacts up to 179,972.

.

We had 18 notice(s) filed upon today for 1800 oz

VOLUME FOR TODAY : 244,295 (PRELIMINARY)

CONFIRMED VOLUME YESTERDAY: 385,054

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY 777 CONTRACTS FROM 199,122 UP TO 199,899 WITH YESTERDAY’S 3 CENT GAIN IN PRICE . WE HAD 750 PRIVATE EFP’S ISSUED FOR DECEMBER AND 300 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THE ISSUANCE. USUALLY WE WITNESS THIS EVENT ONE WEEK PRIOR TO FIRST DAY NOTICE AND IT CONTINUES RIGHT UP TO FDN. WE HAD NO LONG SILVER COMEX LIQUIDATION. THUS THE TOTAL EFP’S ISSUED YESTERDAY TO OUR COMEX LONGS TOTAL 1050 AND THUS DEMAND FOR SILVER OPEN INTEREST CONTINUES TO RISE TAKING INTO ACCOUNT THE INCREASE EFP’S ISSUED.

The new front month of November saw its OI FALL by 1 contract(s) and thus it stands at 2. We had 2 notice(s) served YESTERDAY so we gained 1 contracts or an additional 5,000 oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FELL by 3,169 contracts DOWN to 107,243. January saw A LOSS OF 6 contracts FALLING TO 1046.

We had 1 notice(s) filed for 5,000 oz for the OCT. 2017 contract

INITIAL standings for NOVEMBER

Nov 15/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

9772.805

oz

Brinks

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

18 notice(s)

1800 OZ

|

| No of oz to be served (notices) |

53 contracts

(5300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1009 notices

100,900 oz

3.130 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 1 customer withdrawal(s)

i) out of Brinks: 9,772.805 oz

we had 0 adjustment(s)

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 18 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (1009) x 100 oz or 100,900 oz, to which we add the difference between the open interest for the front month of NOV. (71 contracts) minus the number of notices served upon today (18 x 100 oz per contract) equals 106,100 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (1009) x 100 oz or ounces + {(71)OI for the front month minus the number of notices served upon today (18) x 100 oz which equals 106,200 oz standing in this active delivery month of NOVEMBER (3.303 tonnes)

WE GAINED 0 ADDITIONAL CONTRACTS OR NIL OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

THIS IS THE FIRST TIME EVER THAT WE HAVE WITNESSED CONSIDERABLE QUEUE JUMPING IN GOLD AT THE COMEX. SILVER’S QUEUE JUMPING STARTED IN MAY 2017 AND HAS NOT LET UP ONCE COMMENCED.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Total dealer inventory 527,069.052 or 16.394 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,666,465.358 or 269.56 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

625,612.200 oz

CNT

Scotia

|

| Deposits to the Dealer Inventory |

598,717.69 oz

Brinks

|

| Deposits to the Customer Inventory |

1,199,988.100

oz

HSBC

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000,OZ)

|

| No of oz to be served (notices) |

1 contract

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 875 contracts(4,375,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Nov 13/ 2017

today, we had 1 deposit(s) into the dealer account:

i) Into Brinks: 598,717.69 oz

total dealer deposit: 598,717.69 oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 2 customer withdrawal(s):

i) Out of CNT: 605,467.110 oz

ii) Out of Scotia: 20,145.09 oz

TOTAL CUSTOMER WITHDRAWAL 625,612.200 oz

We had 1 Customer deposit(s):

i) Into HSBC: 1,199,988.100 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 1,199.988.100 oz

we had 0 adjustment(s)

The total number of notices filed today for the NOVEMBER. contract month is represented by 1 contracts FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 875 x 5,000 oz = 4,375,0000 oz to which we add the difference between the open interest for the front month of NOV. (2) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 875 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(2) -number of notices served upon today (1)x 5000 oz equals 4,380,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 1 contract(s) or an additional 5,000 oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 32,820

CONFIRMED VOLUME FOR YESTERDAY: 89,838 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 89,838 CONTRACTS EQUATES TO 449 MILLION OZ OR 64.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

Total dealer silver: 43.817 million

Total number of dealer and customer silver: 231.646 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

will try and update later tonight

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.8 percent to NAV usa funds and Negative 1,5% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.3%

Percentage of fund in silver:37.4%

cash .+.3%( Nov 14/2017)

2. Sprott silver fund (PSLV): STOCK RISES TO -0.77% (Nov 14 /2017)

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.70% to NAV (Nov 14/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.77%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.70%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

Oct 17./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

Oct 16/A HUGE WITHDRAWAL OF 5.32 TONNES FROM THE GLD/INVENTORY RESTS AT 853.13 TONNES

0CT 13/ NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 12/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 15/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 272 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 207 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Oct 17/ A MONSTROUS WITHDRAWAL OF 3.494 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 322.271 MILLION OZ

Oct 16/ NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 325.765 MILLION OZ

oCT 13/ NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 12/THE LAST TWO DAYS WE LOST 1.113 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

Nov 15/2017:

Inventory 318.074 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.46%

12 Month MM GOFO

+ 1.72%

30 day trend

end

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

— November 15

– UK debt crisis is here – consumer spending, employment and sterling fall while inflation takes off

– Personal debt crisis coming to fore – litigation cases go beyond 2008 levels

– October consumer spending fell by 2% in October, the fastest year- on-year decline in four years

– Britons ‘face expensive Christmas dinner’ as food price inflation soars

– Gold investors buying physical gold due to precarious UK and US outlook

Editor: Mark O’Byrne

The long heralded UK debt crisis is here and data released in the U.K. this week clearly shows this.

This is seen in UK retail sales and consumer spending which plunged in October, employment falling, pay stagnant and inflation ticking higher as sterling remains under pressure.

Yesterday, official UK figures showed prices were up by 4.2% last month on 12 months earlier, the highest level in four years. Britons ‘face expensive Christmas dinner’ as food price inflation soars reported The Guardian yesterday.

Meanwhile stock markets make new highs every week but the underlying economic data is not reflecting the “irrational exuberance” being seen in global stock markets.

Increased litigation as consumer debt climbs

Personal loans are becoming increasingly dangerous and more bubblelicious than even the stock market.

We have outlined a few times how UK consumer debt levels are at dangerous highs risking a new UK debt crisis. Recently Standard & Poor’s raised their own concerns regarding the rapid rise in UK consumer debts.

The rapid rise in UK consumer debt to ú200bn from car finance, personal loans and credit cards is unsustainable at current growth rates and should raise “red flags” for the major lenders, ratings agency Standard & Poor’s has warned. – The Guardian

The high levels of debt are down to easy monetary policy, according to the standards agency:

Loose monetary policy, cheap central bank term funding schemes and benign economic conditions have supported consumer credit supply and demand.

However this is unsustainable and major lenders should be on high alert due to the low levels of repayments. The situation is now so bad that the number of cases taken to court over late payments have reached levels higher than those seen in 2008.

As explained in the FT:

Consumers who refuse to repay their debts are increasingly being taken to court, with litigation at levels last seen in the run- up to the 2007-08 financial crisis.

New figures show there were 910,345 county court judgments in the nine months to the end of September. This is an increase of 34 per cent per on the same period in 2016, and compares with 827,000 in the whole of 2008, at the onset of the financial crisis.

The rise in court judgments is another indication of the high levels of unsecured debt weighing on British consumers, with Bank of England data showing that borrowing through credit cards, overdrafts and car loans has topped ú200bn for the first time since the global crisis.

All of this is despite low unemployment levels and an apparent increase in real incomes. The Daily Mail provided an interesting snapshot of where some of the excess debt is coming. Namely in the form of car loans which are almost mimicking the subprime market seen in the run up to 2008:

The situation of increased loans doesn’t even seem to be helping the wider economy. Retail sales have fallen sharply.

High borrowing but low spending

October’s retail figures made for some dire reading. According to Visa spending fell by 2% in October, the fastest year-on- year decline in four years.

As outlined in the Guardian:

Clothing and footwear sales slumped by 9%, the biggest year-on-year decline since Visa started its survey in 2009.

Food and drink retailers experienced a 2% drop in takings, the biggest fall since March 2014. Spending on recreation and culture dropped by 2.9%, the biggest decline since March 2011.

Visa explained the poor figures on financial strains on households. Despite the apparent rise in real incomes the fact is inflation is climbing and shrinkflation is really impacting household expenses, not to mention Brexit.

Visa said the poor performance was partly due to the drop in real wages in recent months, as pay rises have failed to keep up with inflation. But it added that the slowdown in growth this year, and Brexit uncertainty, were also gnawing at consumer confidence.

The Bank of England’s decision to raise interest rates, to 0.5%, for the first time in a decade could also hurt household spending in the coming months, Visa said.

The life raft of gold

The above is just a a quick snapshot of how things at the grassroots level of the UK economy are and suggest a new UK debt crisis looms large. Real world economic conditions are really not projecting the same confidence that the stock markets are.

Usually when things are performing as well as they are in equity markets then we see gold outflows and major sales. This has not been the case, as mentioned in Reuters:

“In theory, and in the past, when you have exceptional markets and low volatility, gold was much, much lower – but nobody’s selling gold,” Davis Hall, head of FX and precious metals at Indosuez Wealth Management, said.

“At some point, this stock market run is going to run into some profit-taking, for one reason or another,” he said. “As a hedge, gold’s definitely still the best viable alternative for high exposure to global equity positions.”

Whilst the price might not have performed to the level many were expecting, it is still significantly up on the year – by over 11%.

Gold’s price climb, along with low gold liquidations, increased demand for gold coins and bars and central bank purchases suggests that gold buyers have identified that not all is as it seems in the so called “recovery”.

It is obvious from both political and economic events that the global economic crisis is not over. Data shows that we are fast approaching circumstances worse than those seen prior to 2008. Sadly no one is acknowledging them and solutions and preparations are not being considered.

Gold Britannia (CGT Free in UK)

In response gold owners are hanging onto the one solution they do know has worked time and time again – physical, allocated and segregated gold.

-END-

END

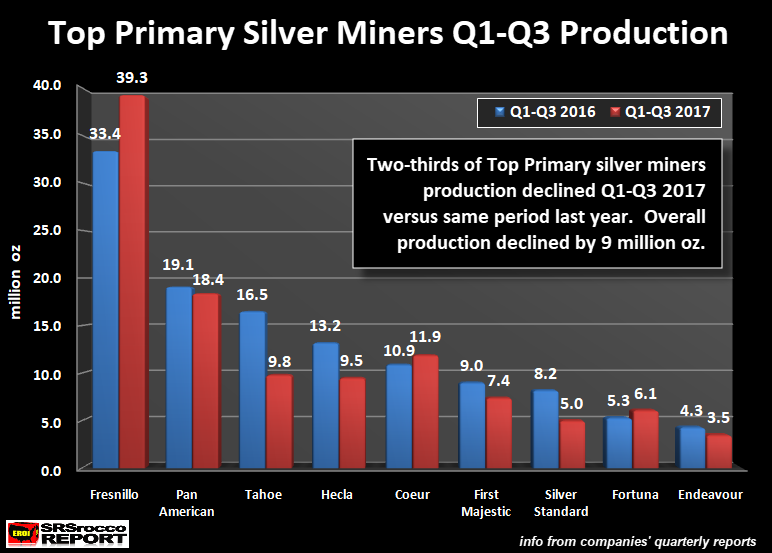

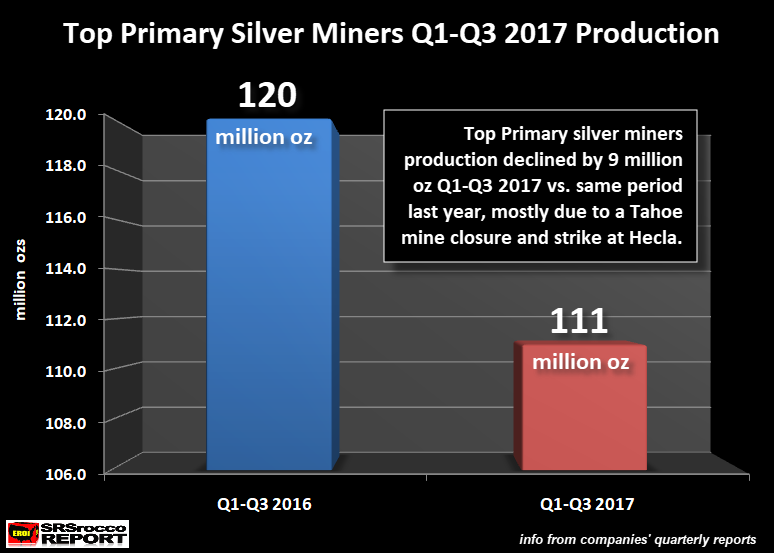

Interesting: 2/3 of the top primary silver producers suffered production declines:

( Steve St Angelo/SRSRocco report)

Two-Thirds Of The Top Primary Silver Miners Suffered Production Declines In 2017

![]()

By the SRSrocco Report,

It has been a rough year for many primary silver miners as two-thirds have suffered declines in production. Also, many high ranking silver producing countries are also experiencing a pronounced reduction in their domestic silver mine supply. According to the data put out by World Metal Statistics, Chile’s silver production is down 20% in the first eight months of the year, while Australia is down 19%, Mexico declined 2% and Peru lower by 1%.

The Silver Institute will be releasing their 2017 Silver Interim Report shortly which will provide an update on current silver production and forecasts for the remainder of the year. However, I believe global silver production will take a big hit this year due to several factors including, falling ore grades, mine closures, and strikes at various projects.

For example, Tahoe Resources was forced to shut down its Guatemalan Escobal Mine in July due to a temporary suspension of its operating license by the country’s Supreme Court. However, even after the Guatemalan Supreme Court reinstated Tahoe Resources Escobal Mine’s license in early September, an ongoing road blockade has hampered the ability of the project to continue mining. Regardless, Tahoe’s silver production declined a stunning 6.7 million oz Q1-Q3 2017 versus the same period last year.

Now, on the other hand, silver production at Fresnillo’s operations in Mexico jumped by nearly six million oz during the first three-quarters of 2017 primarily due to the start-up of its San Julian Mine phase II expansion and a ramp-up of its phase I:

While the gain in silver production at Fresnillo’s operations helped to offset the significant decline at Tahoe’s Escobal Mine, two-thirds of the top primary silver companies in the group experienced a reduction in mine supply this year. Hecla’s silver production fell by 3.7 million oz in the first three-quarters this year due to an ongoing strike at its Lucky Friday Mine in Idaho. Moreover, output at Silver Standard’s Puna operations in Argentina fell by 3.2 million oz due to a 36% decline in ore grade at is open-pit Pirquitas Mine. Silver Standard’s Pirquitas Mine is one of the few open-pit silver operations in the world. The overwhelming majority of primary silver mines in the world are underground operations.

Overall, production at these top primary silver miners fell 9 million oz in 2017 compared to the same period last year:

Now, if Tahoe Resources Escobal Mine was not forced to shut down or if Hecla’s Lucky Friday Mine’s strike was resolved, overall production at these top primary silver miners would have likely increased by approximately one million oz this year. Unfortunately for Tahoe’s Escobal Mine and its investors, it may be quite some time before full production resumes. As I have mentioned in previous articles about the troubles plaguing the Escobal Mine by the local and indigenous peoples living by the operation, there are two very different opinions on the underlying problems.

While I have stated that the negative issues put forth by the local and indigenous peoples about the Escobal Mine are likely more valid than the pro-western stance taken by the Tahoe Managment or the Mainstream financial media, time will tell how this is resolved. However, the notion put forth by Tahoe Management that the problems are stemming from “non-locals” who are supposedly radicalizing the locals around the plant, is unfounded when we understand that it is a huge ground-roots movement led by a large percentage of the inhabitants surrounding the mine.

According to the article, Tahoe Resources’ Social Licence in Guatemala Non-Existent, as Uncertainty Plagues Escobal Permits:

Tahoe CEO Ron Clayton is also wrong when he states in a recent press release that community opposition comes from “non-locals”. Lack of social license has dogged Tahoe Resources since the beginning of its project. Since 2011, tens of thousands of residents in eight municipalities around the Escobal mine have voted in municipal plebiscites demonstrating their opposition to the project, or any mining in the area, out of concern for their water supplies, health, and local agriculture. Five municipalities refuse to receive any royalty payments from Tahoe’s mine operations and are now parties to the legal proceedings over discrimination of the Xinka Indigenous population and the Ministry of Energy and Mines’ failure to consult with them.

As the article states, five municipalities refuse to receive any royalty payments from Tahoe’s mine operations and are now supporting legal proceedings. This does not sound like a small group of non-locals instigating trouble. Rather, this has been an ongoing issue ever since the Escobal Mine was initially planned, during its construction phase and ever since it produced its first ounce of silver in 2014.

Lastly, it looks like global silver production will take a big hit this year. We could see world silver mine supply fall by 40-50 million oz in 2017 if the trend continues for the remainder of the year. One country that I did not report on about silver production was China. According to the World Metals Statistics, they show Chinese silver production down by a stunning 25% in the first eight months of 2017. However, I don’t believe the decline is that high. Even though the World Gold Council stated that Chinese gold production was down 10% so far this year, I doubt their silver production fell 25% this year.

We will have to wait and see what production figures the Silver Insitute will release in their 2017 Silver Interim Report when it’s published in the next few weeks. Regardless, the world’s economies are being propped up by a massive amount of debt, derivatives and money printing. When the markets finally crack, global silver production will fall considerably as for demand for base metals will drop like a rock. We must remember, 58% of world silver production is a by-product of copper, lead and zinc production. So, when base metal demand falls, so will base metal production.

Thus, as the market and economy continue to disintegrate, global silver supply will fall right at the very same time investment demand surges.

Check back for new articles and updates at the SRSrocco Report.

END

Ed Steer’s commentary today posted in the clear

(courtesy Ed Steer/Gata)

Ed Steer’s Gold and Silver Digest for today posted at GoldSeek

Submitted by cpowell on Wed, 2017-11-15 01:56. Section: Daily Dispatches

8:57p ET Tuesday, November 14, 2017

Dear Friend of GATA and Gold:

Today’s edition of GATA Board of Directors member Ed Steer’s Gold and Silver Digest, headlined “JPMorgan’s Silver Short Position Now at 195 Million Ounces” has been posted in the clear at GoldSeek here:

http://news.goldseek.com/GoldSeek/1510688397.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Gold trading today:

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.6220/shanghai bourse CLOSED DOWN AT 27.02 POINTS .79% / HANG SANG CLOSED DOWN 300.43 POINTS OR 1.03%

2. Nikkei closed DOWN 351.69 POINTS OR 1.57% /USA: YEN RISES TO 112.76

3. Europe stocks OPENED RED /USA dollar index FALLS TO 93.54/Euro RISES TO 1.1843

3b Japan 10 year bond yield: FALLS TO . +.0460/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.12 and Brent: 61.47

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.364%/Italian 10 yr bond yield DOWN to 1.810% /SPAIN 10 YR BOND YIELD UP TO 1.523%

3j Greek 10 year bond yield FALLS TO : 5.094???

3k Gold at $1285.70 silver at:17.15: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 60,34

3m oil into the 55 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9861 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1681 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.364%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.341% early this morning. Thirty year rate at 2.802% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Tumble, Asia Plunges On Chinese Commodity Carnage

The euphoria of the past month has ended with a thud and BTFDers are strangely missing as the commodity chill out of China (which overnight became full blown carnage), has unleashed a global risk-off phase ahead of today’s critical CPI data, resulting in broad and sharp selling across global markets, as European stocks followed declines in Asia while bonds and gold advanced. The equity retreat, which spread to U.S. stock futures, started with last night’s sharp puke in Chinese commodities.

As a result, S&P 500 futures dropped 0.5% after U.S. stocks fell for a third time in four days, while Japan’s recent euphoria – which attracted a record influx of foreign investors – is now a distant memory with the Topix falling for the fifth day, its longest losing streak this year, as it declined 2%, while European stocks tumbled for a seventh consecutive day, the worst losing streak since November 2016, to a two month low with the Stoxx 600 down 1%.

“The decline by U.S. equities led by energy shares is having a knock-on effect, dampening sentiment in sectors related to energy and industry,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui Asset Management in Tokyo. “Broadly speaking equities had enjoyed an almost uninterrupted run for the past few months, so we are seeing a bit of a correction finally emerging.”

“So far we don’t see that much disruption in sentiment, so I think we are just taking a bit of froth off the top of the market at the moment,” Michael Metcalfe, global head of macro strategy at State Street Global Markets, said on Bloomberg TV. “It would be dangerous to say this is the unwinding of a bubble – the fact that it’s being led by Japan actually tells you that, because there isn’t a valuation case to sell Japanese stocks.”

The cautious tone has settled into markets in recent days as new obstacles emerged to the U.S. overhauling taxes and after many stock gauges approached record highs. Attention now turns to data coming on U.S. consumer prices and retail sales for further clues on US economic strength after the flattest American yield curve in a decade raised concern that growth will slow. Amusingoy, amid the equity pullback, Morgan Stanley advised staying overweight stocks and avoiding the temptation to sell even as valuations appear stretched. Current indicators used by the New York-based bank’s cross-asset strategy team are showing strong macro-economic data favoring a tilt to shares, with low allocation to high-yield credit.

Asian equities fell, with the regional benchmark poised for its steepest four-day decline this year, as a slump in commodity prices weighed on materials and energy producers shares. The MSCI Asia Pacific Index dropped 1% percent to 167.97 with material and energy sub-gauges each down at least 1.7 percent. Japan’s Topix capped its longest declining streak since September 2016, while Hong Kong’s Hang Seng Index lost 1 percent. Moderation in China’s growth and rising odds of U.S. rate hikes are putting the brakes on Asia’s world-leading rally this year. A Bloomberg gauge of commodity prices extended Tuesday’s steepest slump in six months after Chinese data pointed to slowing industrial output, fixed-asset investment and retail sales. The MSCI Emerging Market Index fell 0.4%, hitting the lowest in almost three weeks with its fifth consecutive decline.

“Commodity prices are sinking on rate-hike expectations as well as China data that missed some analyst forecasts,” said Hao Hong, Hong Kong-based chief strategist at Bocom International Holdings Co. “Investors are taking profits after rallies.” Mitsubishi Gas Chemical Co. slumped 4.3 percent in Tokyo for its biggest drop in more than seven months, while PetroChina Co. lost 3.1 percent in Hong Kong.

European stocks followed in Asia’s example, falling in brisk volumes, with basic resources and energy stocks falling the most on the back of weaker commodity prices, as investors assess the global equity pull-back. The Stoxx Europe 600 Index retreated 0.6% to a near two-month low, breaking below its 200-day moving average for the first time since early September. All but one sector are in the red, with banks among the worst performers as bond yields weaken. The Stoxx 600 is heading for its longest losing streak since November 2016. The U.K.’s FTSE 100 Index decreased 0.6% , hitting the lowest in almost seven weeks with its fifth consecutive decline. Germany’s DAX Index dipped 1.3%, reaching the lowest in almost seven weeks on its fifth consecutive decline.

European stocks fall in brisk volumes, with basic resources and energy stocks falling the most on the back of weaker commodity prices, as investors assess the global equity pull-back. The Stoxx Europe 600 Index retreats 0.6% to a near two-month low, breaking below its 200-day moving average for the first time since early September. All but one sector are in the red, with banks among the worst performers as bond yields weaken. The Stoxx 600 is heading for its longest losing streak since November 2016. Mining and oil-related stocks set the tone, as the Bloomberg Commodities Index continued its longest slide since June.

Benchmark WTI crude fell through $55 a barrel after industry data showed U.S. stockpiles unexpectedly rose last week and as Russia was said to waver on extending output cuts. The dollar traded near a three-week low and Treasuries led bond gains. S&P 500 futures dropped 0.6 percent.

The euro climbed to its highest level in more than three weeks, the EURUSD rising above 1.1800 as increased confidence in the currency bloc was underpinned with concerns that U.S. inflation data due Wednesday may further pressure the dollar. The common currency rose a sixth day, set for its longest winning run since May 2016, as demand for upside exposure intensified in both spot and options markets. Real-money names returned from the sidelines and added fresh longs, while macro accounts also bid the euro, traders in Europe and London told Bloomberg.

Pressured by the euro’s surge, the dollar index against a basket of six major currencies lost about 0.7 percent overnight. It last stood flat at 93.870. The greenback was 0.2 percent lower at 113.230 yen after pulling back from a high of 113.910 the previous day. The yen as well as Japan’s equity and bond markets showed little reaction to Wednesday’s GDP data. Japan’s economy grew for the seventh straight quarter during the July-September period, although this was tempered somewhat as private consumption declined for the first time since the last quarter of 2015.

The immediate focus for the dollar, and a potential catalyst, was data on U.S. consumer prices due later in the global day.

Ahead of today’s closely watched CPI update out of the US, overnight the Fed’s Evans said that the Fed should acknowledge a much greater chance of 2.5% inflation, further stating that he sees solid US economic growth in 2018 and sees a big risk in not getting inflation to 2% before the next recession hits.

Elsewhere, the US Senate Finance Committee Chair Hatch unveiled the modified Chairman’s mark of Senate’s tax overhaul plan, which:

- Repeals Affordable Care Act’s individual mandate tax, according to release from committee

- Increases child tax credit from the current $1,000 to $2,000

- Reduces middle income tax rates from 22.5% to 22%; 25% to 24%; and 32.5% to 32%

The White House is said to strongly support the House tax bill.

Crude oil prices stretched losses, weighed by forecasts for rising U.S. crude output and a gloomier outlook for global demand growth in a report from the International Energy Agency. U.S. crude futures were down 1.1 percent at $55.07 per barrel and on track for their fourth day of losses. Brent lost 1.3 percent to $61.42 per barrel. With oil prices having slid steadily from 28-month highs scaled last week, commodity currencies came under pressure.

On today’s calendar, investors will be looking for consumer prices, retail sales, MBA mortgage applications, Empire State manufacturing, business inventories, and Treasury net capital flows. Tax overhaul update: revisions bring the plan in line with Senate’s tight fiscal constraints, but may create complications for President Donald Trump who have pitched the plan as benefiting the middle class. Several ECB officials speak with Executive Board member Peter Praet chairing the closing policy panel at an ECB conference in Frankfurt.

Market Snapshot

- S&P 500 futures down 0.5% to 2,566.25

- STOXX Europe 600 down 1.0% to 380.00

- MSCI Asia down 0.9% to 168.14

- MSCI Asia ex Japan down 0.6% to 552.69

- Nikkei down 1.6% to 22,028.32

- Topix down 2% to 1,744.01

- Hang Seng Index down 1% to 28,851.69

- Shanghai Composite down 0.8% to 3,402.52

- Sensex down 0.6% to 32,750.40

- Australia S&P/ASX 200 down 0.6% to 5,934.24

- Kospi down 0.3% to 2,518.25

- German 10Y yield fell 2.8 bps to 0.369%

- Euro up 0.4% to $1.1845

- Italian 10Y yield fell 0.5 bps to 1.563%

- Spanish 10Y yield fell 0.9 bps to 1.525%

- Brent Futures down 1.1% to $61.51/bbl

- Gold spot up 0.4% to $1,285.26

- U.S. Dollar Index down 0.4% to 93.47

Top Overnight News

- Chicago Fed President Charles Evans says policy makers should take a more aggressive public stance toward boosting price gains; “harder for me to feel comfortable with the idea that weak

inflation is simply transitory”; concerned something more persistent is

holding down inflation today - While U.K. unemployment rate stayed near a 42-year low, there were signs that the labor market may be slowing as the number of people in work fell for the first time in almost a year

- Britain’s PM May is heading for a showdown with her own Tory party over what one member of Parliament called her “mad” plan to write the date of Brexit into British law

- The armed forces seized power in Zimbabwe after a week of confrontation with President Robert Mugabe’s government and said the action was needed to stave off violent conflict in the southern African nation that he’s ruled since 1980

- U.K. Sept. Average Weekly Earnings: 2.2% vs 2.1% est; Unemployment Rate 4.3% vs 4.3% est.

- ECB’s Hansson: we feel more and more confident that inflation will eventually reach the levels consistent with our aim; short-term economic risks are to the upside

- Australia 3Q wage prices 0.5% vs 0.7% est; y/y 2.0% vs 2.2% est

- API inventories according to people familiar w/data: Crude +6.5m; Cushing -1.8m; Gasoline +2.4m; Distillates -2.5m

- North American Free Trade Agreement (Nafta) negotiators from the U.S., Canada, and Mexico meet in Mexico City for round five of discussions through Nov. 21.

- The armed forces seized power in Zimbabwe after a week of confrontation with President Robert Mugabe’s government

- House leaders cleared the way for a Thursday vote on their tax-overhaul bill as Senate tax writers released a late-night draft that would make many individual breaks temporary and repeal a key part of the Obamacare law

- Airbus SE announced the biggest commercial-plane transaction in its history, securing an order for single-aisle aircraft valued at nearly $50 billion at the Dubai Air Show, outdoing Boeing Co.’s own $20 billion mega-deal

- Amid the worst sell-off in months for junk-rated corporate bonds, money manager Loomis Sayles & Co. has been selectively buying the debt

- Warren Buffett continued to trim a once-major investment in International Business Machines Corp. while adding to newer holding Apple Inc. in the third quarter

- OPEC has yet to convince Russia that it’s necessary to reach an agreement to extend oil-output cuts at a meeting in Vienna later this month, as officials and oil bosses in Moscow still haven’t decided how long the production deal should last

- Deutsche Bank AG has attracted a new top investor whose identity will probably be revealed within days

- SandRidge Energy is nearing agreement to buy Bonanza Creek Energy for about $750 million in cash-and-stock deal, Wall Street Journal reports citing unidentified people familiar

Asian stocks slumped sharply, following the lead of their US counterparts, as negative risk sentiment and the stronger domestic currency weighed on Japan’s Nikkei 225 which finished 1.6% lower, although this was off of worst levels. In Australia, the ASX 200 fell 0.6%, with energy stocks and resource names leading the way on the back of softer oil prices and yesterday’s Chinese data respectively. Chinese and Hong Kong markets also fell afoul of risk off sentiment (Shanghai Comp -0.6%, Hang Seng -0.7%), with the tumble in Shanghai metals heaping further weight on industrial names. Bonds edged higher in the US, Japan & Australia, with Australian 3-year bond futures experiencing notable buy side flow in the wake of the soft wage data. Japanese GDP QQ (Q3) 0.3% vs. Exp. 0.3% (Prev. 0.6%); Australian Wage Price Index QQ (Q3) 0.5% vs. Exp. 0.7% (Prev. 0.5%); New Zealand Finance Minister Robertson reiterates that it is the government’s intention to reduce net debt to 20% of GDP within 5 years. The RBNZ has increased the capital requirements for Westpac’s NZ division as the firm did not comply with regulations.

Top Asian News

- China Throws Lifeline to Builders Facing Record Wall of Debt

- China Seen Supporting Bonds as PBOC Steps Up Liquidity Injection

- Tencent Delivers a Blowout Quarter as Honour of Kings Shines

- India Advances BS-VI Fuel Norm in Delhi to Combat Pollution

- Korea Factories Operating Normally After Big Quake

- China Is Said to Allow Panda Bond Issuers to Use U.S. GAAP Rules

- Investors Lose Faith in Asia’s Top Stock as Downgrades Mount

- Freeport Indonesia Shuts Main Road to Grasberg After Shooting

- Aluminum Supply Cuts in China Set to Disappoint This Winter

European indices lower this morning, with almost every sector in negative territory. A typical risk-off session thus far, with financials and commodity-related names taking the most points off EU bourses. Not all doom and gloom however, as Airbus shares have been flying high after they confirm the largest aircraft deal in its history, valued at over USD 40bln. Gilts initially firmer in wake of the latest jobs and wages update, and indeed inched a bit closer to 125.00 before easing back again, while the Short Sterling strip has held relatively modest gains of 1-2 ticks. The inference is that unemployment and pay did not top estimates by enough to prompt a reaction or change the near term outlook for the BoE, albeit encouraging. Moreover, Bunds and USTs are inching further ahead (former just up to a fresh 162.86 Eurex high) amidst a broader safety flight, which has now seen the 10 year UK benchmark break through 125.00 to 125.09. Germany supply up next, but in the context of risk aversion this should cause any major digestion issues.

Top European News

- EU Is Said to Be Looking to 2018 Summits for Brexit Breakthrough

- Weimer Is Said to Be Lead Candidate for Deutsche Boerse CEO Post

- U.K. Labor Market Shows Signs of Slowing as Employment Falls

- VW Raided by German Prosecutors Over Labor Chief’s Pay

- TalkTalk Plunges as Earnings Outlook Dims on Customer Costs

- Atlantia CEO Says Room to Make Abertis Offer Competitive: FT

- AstraZeneca’s Fasenra Gets FDA OK for Severe Eosinophilic Asthma

- Israel Plans to Issue Tax Bills to Google, Facebook: Haaretz

In FX, cable Retreated from session highs, consolidating back inside the day’s range. In DXY trading, d Dovish comments from Fed’s Evans hardly helped to ease the Greenback’s pain as he bemoans the fact that US inflation remains below target and warns that it may not hit mandate before the next recession. The Index has duly declined further from the 94.000 level and is threatening 93.500 on the downside. It’s onwards and upwards for the Euro with 1.1800 now surpassed and techs turning outright bullish given the break of a negative channel. The early morning upside target of 1.1837 has been breached with the October peak of 1.1880 in sight. EURGBP making a firm breach of 0.90 has weighed on GBP. GBP briefly above 1.32 above post UK jobs data, however wages still continue to lag inflation, while some investors may be looking at the retail sales release tomorrow which has some growing pessimism given how weak the retail sector has been over the recent months. In JPY moves, benefiting from its flight to quality status (along with the Chf) and breaking below the recent 113.00-114.00 range vs the Greenback to around 112.80 and closer to downside option expiries at 112.50 (460 mn). The AUD was a marked and sole underperformer vs the US Dollar among majors, largely due to weaker than forecast Australian wage data, hot on the heels of comments alluding to that fact from RBA deputy Governor Debelle. Aud/Usd has now slipped through 0.7600 where macro offers were evidently seen, and bears are looking at 0.7571 chart support next. Note, a 0.7650 option expiry today (470 mn).

In commodities, oil prices off around 1% following last night’s API report which showed a rather large build of 6.5mln in US crude inventories, while analysts had expected a drawdown of 2.2mln.

Looking at the day ahead, the big focus will be the October CPI print while October retail sales, November empire manufacturing and September business inventories are also due. There is plenty more central bank speak scheduled with the ECB’s Lane, Praet and Hanson all due along with the Fed’s Evans and the BoE’s Haldane. NAFTA negotiators from the US, Canada and Mexico are also scheduled to meet for round 5 of discussions.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 0.0%

- 8:30am: US CPI MoM, est. 0.1%, prior 0.5%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- US CPI YoY, est. 2.0%, prior 2.2%; Ex Food and Energy YoY, est. 1.7%, prior 1.7%

- Real Avg Weekly Earnings YoY, prior 0.63%; Real Avg Hourly Earning YoY, prior 0.7%

- 8:30am: Empire Manufacturing, est. 25.1, prior 30.2

- 8:30am: Retail Sales Advance MoM, est. 0.0%, prior 1.6%; Retail Sales Ex Auto MoM, est. 0.2%, prior 1.0%

- Retail Sales Ex Auto and Gas, est. 0.3%, prior 0.5%; Retail Sales Control Group, est. 0.3%, prior 0.4%

- 10am: Business Inventories, est. 0.0%, prior 0.7%

- 4pm: Total Net TIC Flows, prior $125.0b; Net Long-term TIC Flows, prior $67.2b

DB’s Jim Reid concludes the overnight wrap

So will today’s US inflation numbers give markets an early Xmas present after a ‘bah humbug’ last four trading days which has carried on overnight in the Asian session. At the moment US CPI is probably the most important data release of the month so the stakes are high. The central bank put can continue to be withdrawn slowly and possibly be put back in place if needed whilst inflation remains well behaved. By well behaved the sweet spot for risk markets is a bias for slightly missing expectations more often than it beats but without ever threatening deflation. This describes 2017 perfectly so far. US CPI has missed expectations for 6 out of the last 7 months, with the other month being in-line. Today we expect Core CPI (+0.2% mom vs. +0.1% previous) to firm in line with consensus but the year-over-year growth rate should remain at 1.7%, down from 2.3% at the beginning of the year (headline 2.0% yoy expected). While our economists anticipate core inflation to remain tame near-term, there are signs that we are reaching an inflection point though. Over the last 20 years US inflation has lagged GDP by around five to six quarters, so we think that a lot of the misses this year can be attributed to the weak growth seen at the back end of 2015/ early 2016. The stronger growth seen in the US and globally post H2 2016 should start to impact inflation soon. Today’s print might be too early and our strategists’ models point to a weak 0.2% core reading (0.16% unrounded) so the risks might be on the downside near term but we think to the upside in 2018.

Ahead of this, the US PPI was strong but European inflation data weak. In the US, the headline October PPI was 2.8% yoy – the highest since February 2012. Core PPI was also above expectations at 0.4% mom (vs. 0.2%) and 2.4% yoy (vs. 2.2% expected). In the details, the healthcare services component of the PPI (a direct input into the core PCE deflator) was up 0.18% mom on a seasonally adjusted basis. Across Europe, the UK’s October CPI was slightly below expectations at 0.1% mom (vs. 0.2%), while core annual inflation was steady for the third consecutive month at 2.7% yoy (vs. 2.8% expected).

Elsewhere, the final readings on inflation for Germany (1.5% yoy), Spain (1.7% yoy) and Italy (1.1% yoy) were unrevised.

This morning in Asia, markets have followed the negative lead from yesterday and are trading lower again. The Nikkei (-1.51%), Kospi (-0.29%), Hang Seng (-0.79%) and ASX 200 (-0.42%) are all down with losses led by energy and mining stocks. In Japan, 3Q GDP was a tad softer than expected (0.3% qoq vs. 0.4% expected), but is still an expansion for the 7th consecutive quarter – longest since 2001, and adjusting for prior data revisions, the annual growth was more in line at 1.4% yoy.

Prior to this it was another weak day yesterday for markets. US bourses all weakened, with the S&P 500 (-0.23%), Dow (-0.13%) and Nasdaq (-0.29%) all down modestly. Within the S&P, only the utilities and consumer sectors were in the green, while losses were led by energy (-1.53%) and telco stocks. GE dropped a further 5.9% (-12.6% in two days) after announcing its turnaround plans. European markets were all lower, with the Stoxx 600 down for the 6th consecutive day (-0.59%, cumulative loss of -3.2%) – the longest losing streak since October 2016, with losses led by energy and mining stocks, partly in response to lower oil price and softer than expected Chinese macro data on IP and property sales. Across the region, the FTSE was the relative outperformer (-0.01%) following weaker inflation data, while the DAX (-0.31%), CAC (-0.49%) and FTSE MIB (-0.63%) all fell modestly. Bond markets were slightly firmer, with core 10y bond yields 1-3bp lower (UST: -3.3bp; Bunds -1.9bp; Gilts -0.8bp) while peripheral yields marginally underperformed, ranging from flat to 1bp lower.

Turning to currencies, the US dollar index fell 0.70% – the biggest fall since late June, while Sterling and the Euro gained 0.37% and 1.12% respectively, with the latter likely supported by a solid beat in Germany’s 3Q GDP (0.8% qoq vs. 0.6% expected). In commodities, WTI oil dropped 1.87% – the biggest fall since early October, following the IEA lowering its 2018 demand outlook and cautioning that the global market is likely to remain over supplied in 2Q. This morning, it’s fallen c1% more, after API data showed an unexpected rise in US crude inventory. Elsewhere, precious metal were little changed (Gold +0.15%; Silver -0.20%) but other base metals all weakened following softer Chinese macro data (Copper -1.74%; Zinc -2.25%; Aluminium -0.90%). As a reminder, in China yesterday, both the October IP (6.2% yoy vs. 6.3% expected) and retail sales (10% yoy vs. 10.5% expected) were lower than consensus and monthly property sales turned negative for the first time since March 2015, dropping to -1.7% yoy from 1.6%.

Moving onto Brexit, yesterday we noted that Bloomberg reported that Brexit Secretary Davis told a group of business leaders that the chance for a breakthrough for Brexit talks by December was “a 50/50 chance”. Later on, a spokesman on behalf of Davis said “this is categorically untrue. Davis did not say this”. Elsewhere, Davis noted that he wanted banking employees to retain their ability to transfer between offices in the UK and EU after Brexit and he predicted he will achieve an agreement on a post 2019 transition period “very early next year”. Finally, the House of Commons has voted 318 to 68 to agree to Clause 1 of the EU withdrawal bill which will repeal the 1972 law that is the basis of UK’s EU membership. Notably, the vote is the second in a series of upcoming votes on PM May’s Brexit bill.

As we get closer to 2018 the outlooks will start to come thick and fast. Hot off the presses this morning our European equity strategy team led by Sebastian Raedler have published their 2018 outlook. They expect the Stoxx 600 to end 2018 at 395, 3% above current levels, based on projected 2018 EPS growth of 2% and an end-2018 12-month forward P/E of 15.1x (slightly above the current 14.8x). They remain tactically neutral near-term, but expect a pull-back for the Stoxx 600 to 375 in Q1 as Euro area macro momentum softens from its current elevated levels. They are underweight European cyclicals versus defensives – and expect European equities to continue underperforming US equities over the coming months. Email Sebastian.Raedler@db.com for a copy.

Now wrapping up with a busy day of central bank speak before we recap yesterday’s data and preview today’s. Firstly the Fed’s Bullard reiterated his dovish view, noting the current interest rate “is likely to remain appropriate over the near term” and that even if US unemployment rate declines substantially further, “the effect on inflation are likely to be small”. Further, if the Fed is going to hit its inflation target, “it will likely to occur in 2018 or 19”. Conversely, the Fed’s Kaplan said he is “actively considering appropriate next steps” in terms of a potential December rate hike. Further, he is watching core inflation closely and noted there is a mounting case for moving ahead of signs of price increases.

Following on, the Fed’s Bostic noted that based on anecdotal feedback and monitored indicators, they convince him that the foreseeable future is “more of the same”, with GDP growth at a bit above 2%, unemployment rate in low 4% and modest increase in real wage growth. Hence he believes “it will be appropriate for interest rates to rise gradually over the next couple of years”. Elsewhere, he seemed to attribute the current yield curve flattening in the US to the flow associated with the demand for US securities, rather than as a sign of the economy’s softness. After the PPI data, softer markets and central bankers speak, the odds of a December rate hike fell 5ppt to a still high level of 92% (per Bloomberg).

Staying with the Fed, the WSJ has reported that former Pimco CEO Mohamed El-Erian is among several candidates that are currently being considered for the role of Fed Vice Chairman. Moving onto US tax plans, Senator John Thune noted that Senate Majority Whip Mr Cornyn is confident the chamber can get the votes to pass the bill, “we wouldn’t have proceeded if Cornyn wasn’t confident he could get to 50”.

Back to central bankers and the ‘Fab Four’ panel discussion at the ECB’s conference yesterday. Overall, there was minimal material information for markets. In the details, Mrs Yellen sounded a bit critical of some FOMC members who gave the impression of having made their policy decisions ahead of hearing the views of fellow colleagues. Elsewhere, she noted “all (rates) guidance should be conditional on the outlook for the economy” and the appropriate policy path depends “on expectations about where the medium term outlook is”. Finally, one of the lessons for the Fed from the taper-tantrum was to lay the ground work in a long set of communications to enable the taper process to be orderly, gradual and avoid market disruption.

The BOE’s Carney reiterated his caution on Brexit, noting that the UK is in “exceptional circumstances”, in part as Brexit will “very much depend on the final arrangements with the EU-27 and what the transition path is from here”. However, he noted the potential impact on rates may be evolving. On the one hand, it could be inflationary as there are not much spare capacity in the economy, on the other, there could be an expansive relationship with Europe, a reasonable transition period and demand holds up. For now, “you could paint either picture”. The ECB’s Draghi expressed some disappointment in the continued media

criticism of his Bank’s policies that was evident in some countries and noted that “forward guidance has now become a full-fledged monetary policy instrument”. Elsewhere, the BOE’s deputy governor Cunliffe was one of the two policy makers who oppose the recent rate hike in the UK. He reiterated his dovish view, noting “the low level of domestic pressure on inflation now, the absence of second round effects from the depreciation of sterling…..make it possible to wait before tightening policy until there is clear evidence that pay growth is responding to the level of unemployment”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the NFIB small business optimism index was broadly in line at 103.8 (vs. 104 expected). In Germany, 3Q GDP beat expectations at 0.8% qoq (vs. 0.6% expected) and 2.8% yoy (vs. 2.3% expected) – the highest in 6 years, mainly due to positive contributions from net exports and capital investment. The November ZEW survey on current situations for November slightly beat at 88.8 (vs. 88 expected).

In the Eurozone, the second reading of the 3Q GDP was unrevised at 0.6% qoq and 2.5% yoy along with the September IP at -0.6% mom and 3.3% yoy. The November ZEW survey on expectations was higher than last month’s reading at 30.9 (vs. 26.7 previous). Over in Italy, 3Q GDP was in line at 0.5% qoq and 1.8% yoy – the most since 1Q 2011.

Looking at the day ahead, in Europe we’ll receive the final October CPI report in France and the September/October employment stats in the UK. In the US the big focus will be the October CPI print while October retail sales, November empire manufacturing and September business inventories are also due. There is plenty more central bank speak scheduled with the ECB’s Lane, Praet and Hanson all due along with the Fed’s Evans and the BoE’s Haldane. NAFTA negotiators from the US, Canada and Mexico are also scheduled to meet for round 5 of discussions.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 27.02 points or .79% /Hang Sang CLOSED DOWN 300.43 pts or 1.03% / The Nikkei closed DOWN 351.69 POINTS OR 1.57%/Australia’s all ordinaires CLOSED DOWN 0.60%/Chinese yuan (ONSHORE) closed UP at 6.6220/Oil DOWN to 55.12 dollars per barrel for WTI and 61.47 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6220. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6239 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.

3 a NORTH KOREA/USA

NORTH KOREA/USA

This is what scares me the most: the White House is being warned that North Korea is planning a devastating EMP attack on America

(courtesy zerohedge)

The White House Is Being Warned: North Korea Is Planning A “Devastating EMP Attack” On America

Marine Corps veteran Tommy Waller, director of special projects at the Center for Security Policy, has warned President Trump about the EMP threat facing the United States.

“Winston Churchill once said, ‘History will be kind to me for I intend to write it’…

The surest way for history to be kind to President Trump is for him to write it, by being the first leader to truly address the existential threat of EMP.

The first and foremost thing he must write is an Executive Order establishing his own EMP Commission in the White House – a task force that draws from the experience of the previous EMP Commission.”

The grim warning is directed at North Korea and their ambitions to unleash a devastating atmospheric nuclear explosion above the United States that would collapse the nation’s power grid.

Most are aware by now that North Korea has successfully tested ICBM missiles and detonated nuclear devices throughout 2017. Put two and two together, and this is a dangerous cocktail fueling the regime in North Korea. It’s also a perfect recipe for Waller to further his agenda and urge President Trump to create a special commission to prepare for an EMP attack, such as the Manhattan Project in the 1940s in developing the nuclear bomb.

Here is what he had to say:

For those able to execute an unconstrained analysis of today’s threat environment, the single most urgent concern for America is what threatens her electric grid. Without electricity, the America we know today ceases to exist – and our enemies know this.

Elites in the U.S. government know this too, but most have chosen to ignore these threats and to ridicule, silence, and stymie anyone willing to speak the truth about them.

Waller also warns the whole system of 16 critical infrastructure components are dependent upon electricity and the idea an EMP could wipe out critical systems would be devastating for the survival of the empire.

America’s 16 Critical Infrastructures range from Water & Wastewater Systems to Food & Agriculture to Nuclear Reactors, Materials & Waste – and all of them depend upon electricity.

America’s need for electricity creates the ideal conditions by which an adversary can take advantage of Sun Tzu’s “Supreme art of war,” which is “to subdue your enemy without fighting.”

In 1999, with full recognition of this reality and enraged with American policy in the Balkans, Vladimir Lukin (the head of the Russian State Duma’s Foreign Affairs Committee) threatened a U.S. Congressional delegation by stating: “If we really wanted to hurt you with no fear of retaliation, we would launch a Submarine-launched Ballistic Missile (SLBM), [and] we would detonate a nuclear weapon high above your country and shut down your power grid.”

With fear in place, Waller is pushing for the first Executive order, establishing his own EMP Commission in the White House.

What’s very interesting is that the Obama administration already did this by passing an Executive Order on October 2016 preparing the nation for ‘Space Weather Events’, which would contribute to a total power grid collapse.

Here is snippet of section 1 of the executive order: