GOLD: $1278.50 up $0.90

Silver: $17.09 UP 11 cents

Closing access prices:

Gold $1278.60

silver: $17.08`

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1286.38 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1278.35

PREMIUM FIRST FIX: $8.03

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1287.39

NY GOLD PRICE AT THE EXACT SAME TIME: $1276.15

Premium of Shanghai 2nd fix/NY:$11.19

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1277.70

NY PRICING AT THE EXACT SAME TIME: $1277.70

LONDON SECOND GOLD FIX 10 AM: $1280.00

NY PRICING AT THE EXACT SAME TIME. 1280.00

For comex gold:

NOVEMBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH:11 NOTICE(S) FOR 1100 OZ.

TOTAL NOTICES SO FAR: 1020 FOR 10,200 OZ (3.172TONNES)

For silver:

NOVEMBER

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 876 for 4,380,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7452 OFFER /$7479 up $186.00 (MORNING)

BITCOIN : BID $7756 OFFER: $7781 // UP $490.00 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE 1557 contracts from 199,122 UP TO 201,456 EVEN THOUGH YESTERDAY’S TRADING SAW SILVER FALL BY 10 CENTS. WE DID HAVE ZERO LONG LIQUIDATION AND FURTHER WE WERE NOTIFIED THAT WE HAD QUITE A FEW MORE COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE AS WE HAD A HUGE 1312 DECEMBER EFP’S ISSUED ALONG WITH 0 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 1312 CONTRACTS. THE ISSUANCE FOR MARCH BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY IN THE UPCOMING DELIVERY MONTH. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER TO BE DELIVERED UPON AT THE COMEX AND THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WE HAD 1050 TOTAL EFP’S ISSUED.

RESULT: A GOOD SIZED RISE IN OI COMEX DESPITE THE 10 CENT PRICE FALL. COMEX LONGS REFUSED TO EXIT OUT OF THE COMEX AND FROM THE CME DATA 1312 EFP’S WERE ISSUED FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER INTENSIFIES

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.007 BILLION TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest ROSE BY A LARGER THAN EXPECTED 3244 CONTRACTS DESPITE THE FALL IN PRICE OF GOLD ($5.15) WITH RESPECT TO YESTERDAY’S TRADING IN WHICH WE SAW NO GOLD LEAVES FALL FROM THE COMEX GOLD TREE. THE TOTAL NUMBER OF GOLD EFP’S ISSUED TODAY TOTALED A MONSTROUS: 12,392 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 12,352 CONTRACTS AND FEB SAW THE ISSUANCE OF 40 CONTRACTS. The new OI for the gold complex rests at 536,298. DEMAND FOR GOLD INTENSIFIES DESPITE THE RAIDS.

Result: A HUGE SIZED INCREASE IN OI DESPITE THE FALL IN PRICE IN GOLD ON YESTERDAY ($5.15). WE HAD A HUGE NUMBER OF COMEX LONG TRANSFERS TO LONDON THROUGH THE EFP ROUTE AS (12,392 EFP’S). THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL AT THE COMEX AS WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER. WE OBVIOUSLY HAD NO GOLD COMEX OI LEAVE THE COMEX GOLD ARENA.

we had: 11 notice(s) filed upon for 1100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

A small change in gold inventory at the GLD/ a deposit of .300 tonnes

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 318.074 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver UNEXPECTEDLY ROSE BY 1557 contracts from 199,899 UP TO 201,456 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN SILVER PRICE (A LOSS OF 10 CENTS). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE 1312 PRIVATE EFP’S FOR DECEMBER(WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 0 EFP’S FOR MARCH FOR A TOTAL OF 1050 EFP CONTRACTS EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THESE EFP ISSUANCE..USUALLY WE WITNESS THIS ONE WEEK PRIOR TO FIRST DAY NOTICE AND THIS CONTINUES RIGHT UP UNTIL FDN. WE ALSO HAD NO SILVER COMEX LIQUIDATION. TOTAL EFP’S ISSUED YESTERDAY BY THE CME IN SILVER TOTAL 1050 CONTRACTS. SO THIS FRAUD IS CONTINUING ON A DAILY BASIS

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 10 CENT FALL IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ANOTHER 1312 EFP’S ISSUED TRANSFERRING OUR COMEX LONGS OVER TO LONDON TOGETHER WITH NO SILVER COMEX LIQUIDATION.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 3.27 points or .10% /Hang Sang CLOSED UP 167.07 pts or 0.58% / The Nikkei closed UP 322.80 POINTS OR 1.47%/Australia’s all ordinaires CLOSED UP 0.19%/Chinese yuan (ONSHORE) closed DOWN at 6.6320/Oil DOWN to 55.27 dollars per barrel for WTI and 61.62 for Brent. Stocks in Europe OPENED GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6320. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.638 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS OT VERY HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea//South Korea

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

And this guy is deputy Governor of the Bank of England?

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

iib)Seems to be working: Saudi Arabia has offered the arrested royals a deal: Lots of cash (up to 70% of net worth) for your freedomIt is now clear: the whole exercise was nothing but to replenish the treasury

( zerohedge)

6 .GLOBAL ISSUES

Zimbabwe

Mugabe refuses to resign which in turn causes their stock market to collapse

( zerohedge)

7. OIL ISSUES

Somehow Norway now does not believe oil will rise in the next few years: They are planning a divestiture of 35 billion in oil stocks.

( zerohedge)

8. EMERGING MARKET

i)Now the fun begins as underwriters of credit default swaps must pay out and there will be a considerable amount that they have to muster up:

( zerohedge)

ii)At 5:30 pm est, Bitcoin surges near $8,000.00 on the announcement of a credit event and bankers must pay out:

( zerohedge)

9. PHYSICAL MARKETS

i)A joke: the one exchange that the CME plans to use when it starts with its futures operation is down again and it is having serious issues

(Russo/Bloomberg)

ii)What a joke: this one BIS official urges accountability while it undergoes in secret huge gold swaps

( GATA/Chris Powell)

10. USA stories which will influence the price of gold/silver

v)The house is expected to pass the GPO tax reform bill this afternoon but the less friendly senate will not affirm it

( zerohedge)

v b)The house passes the tax reform bill by 227 to 205

( zerohedge)

vi)We now have the identity of our secret informant in the FBI Clinton probe on the Uranium One deal: his name is Christopher Campbell and he was formerly a lobbyist for Tenex, the USA based arm of Russian government’s Rosatom

(courtesy zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY 3244 CONTRACTS UP to an OI level of 536,298 DESPITE THE FAIR SIZED FALL IN THE PRICE OF GOLD ($5.15 FALL WITH RESPECT TO YESTERDAY’S TRADING). OBVIOUSLY WE DID NOT HAVE ANY GOLD COMEX LIQUIDATION. HOWEVER WE DID HAVE A MONSTROUS 12,392 COMEX LONGS EXIT THE COMEX ARENA THROUGH THE EFP ROUTE AS THEY RECEIVE A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 12,352 EFPS WERE ISSUED FOR DECEMBER AND 40 WERE ISSUED FOR MARCH. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

Result: a HUGE INCREASE IN OPEN INTEREST DESPITE THE FAIR SIZED FALL IN THE PRICE OF GOLD ($5.15.) A HUGE 12,392 EFP’S ISSUED FOR A FIAT BONUS AND A DELIVERABLE FORWARD GOLD CONTRACT IN LONDON AND ZERO COMEX GOLD LIQUIDATION DESPITE THE RAID.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF 9 CONTRACT(S) FALLING TO 62. We had 18 notices filed YESTERDAY so GAINED 9 contracts or 900 additional oz will stand for delivery in this non active month of November. TO SEE BOTH GOLD AND SILVER RISE IN AMOUNT STANDING (QUEUE JUMPING) IS A GOOD INDICATOR OF PHYSICAL SHORTNESS FOR BOTH OF OUR PRECIOUS METALS.

The very big active December contract month saw it’s OI LOSE 10,236 contracts DOWN to 269,029 (OF WHICH 12,392 WERE EFP TRANSFERS). THUS ALL THE ROLLOVERS ARE TURNING INTO EFP’S. January saw its open interest RISE by 67 contracts up to 911. FEBRUARY saw a gain of 12,241 contacts up to 192,213. DEMAND FOR GOLD INTENSIFIES.

.

We had 11 notice(s) filed upon today for 1100 oz

VOLUME FOR TODAY : 279,714 (PRELIMINARY)

CONFIRMED VOLUME YESTERDAY: 467,777 contracts. (comex volumes are intensifying)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI UNEXPECTEDLY ROSE BY 1557 CONTRACTS FROM 199,899 UP TO 201,456 DESPITE YESTERDAY’S 10 CENT LOSS IN PRICE . WE HAD 1312 PRIVATE EFP’S ISSUED FOR DECEMBER AND 0 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THE ISSUANCE. USUALLY WE WITNESS THIS EVENT ONE WEEK PRIOR TO FIRST DAY NOTICE AND IT CONTINUES RIGHT UP TO FDN. WE HAD NO LONG SILVER COMEX LIQUIDATION. THE TOTAL EFP’S ISSUED TODAY TO OUR COMEX LONGS TOTAL 1312 AND THUS DEMAND FOR SILVER INTENSIFIES

The new front month of November saw its OI FALL by 0 contract(s) and thus it stands at 2. We had 1 notice(s) served YESTERDAY so we gained 1 contracts or an additional 5,000 oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FELL by ONLY 649 contracts DOWN to 106,594, YET WE HAD 1312 EFP’S ISSUED WHICH MEANS ALL THE ROLLOVERS LANDED INTO EFP’S AND THEN SOME!!. January saw A GAIN OF 9 contracts RISING TO 1055.

We had 1 notice(s) filed for 5,000 oz for the NOV. 2017 contract

INITIAL standings for NOVEMBER

Nov 16/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil

oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

65,829.761 oz

HSBC

Scotia

|

| No of oz served (contracts) today |

11 notice(s)

1100 OZ

|

| No of oz to be served (notices) |

51 contracts

(5100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1020 notices

102,000 oz

3.172 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 2 customer deposit(s):

i) into HSBC: 56,056.956 oz

ii) into Scotia: 9,772.805 oz

total customer deposits 65,829.761 oz

We had 0 customer withdrawal(s)

Total customer withdrawals: nil

we had 1 adjustment(s)

i) Out of Delaware: 2341.534 oz was adjusted out of the customer account and this landed into the dealer account

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 11 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (1020) x 100 oz or 102,000 oz, to which we add the difference between the open interest for the front month of NOV. (62 contracts) minus the number of notices served upon today (11 x 100 oz per contract) equals 107,100 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (1020) x 100 oz or ounces + {(62)OI for the front month minus the number of notices served upon today (11) x 100 oz which equals 107,100 oz standing in this active delivery month of NOVEMBER (3.303 tonnes)

WE GAINED 9 ADDITIONAL CONTRACTS OR 900 OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

THIS IS THE FIRST TIME EVER THAT WE HAVE WITNESSED CONSIDERABLE QUEUE JUMPING IN GOLD AT THE COMEX. SILVER’S QUEUE JUMPING STARTED IN MAY 2017 AND HAS NOT LET UP ONCE COMMENCED.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Total dealer inventory 529,409.586 or 16.406 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,732,195.729 or 271.60 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 83 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

3000.08 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

Brinks

|

| Deposits to the Customer Inventory |

22,251.620

oz

HSBC

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000,OZ)

|

| No of oz to be served (notices) |

1 contract

(5,000 oz)

|

| Total monthly oz silver served (contracts) | 876 contracts(4,380,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

Nov 13/ 2017

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of Delaware: 3000.08 oz

TOTAL CUSTOMER WITHDRAWAL 3000.08 oz

We had 1 Customer deposit(s):

i) Into HSBC: 22,251.620 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 22,251.620 oz

we had 0 adjustment(s)

The total number of notices filed today for the NOVEMBER. contract month is represented by 1 contracts FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 876 x 5,000 oz = 4,380,0000 oz to which we add the difference between the open interest for the front month of NOV. (2) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 876 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(2) -number of notices served upon today (1)x 5000 oz equals 4,385,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 1 contract(s) or an additional 5,000 oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 90,208

CONFIRMED VOLUME FOR YESTERDAY: 121,980 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 121,980 CONTRACTS EQUATES TO 610 MILLION OZ OR 87.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

Total dealer silver: 43.817 million

Total number of dealer and customer silver: 231.665 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.4 percent to NAV usa funds and Negative 1,4% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.2%

Percentage of fund in silver:37.5%

cash .+.3%( Nov 16/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -1.00% (Nov 16 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.56% to NAV (Nov 16/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -1.00%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.56%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 16/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 273 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 208 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Nov 16/2017:

Inventory 318.074 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.60%

12 Month MM GOFO

+ 1.79%

30 day trend

end

Major gold/silver trading/commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

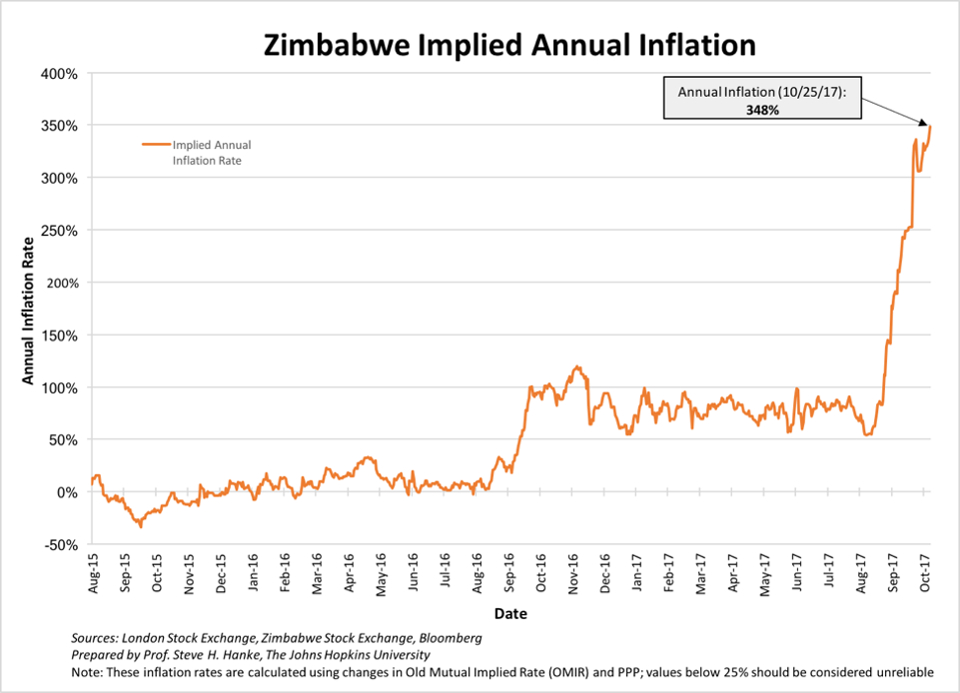

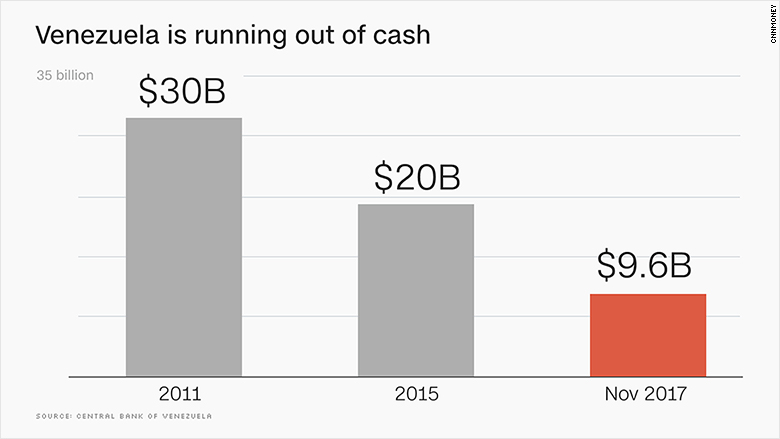

Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe Show Why Physical Gold Is Ultimate Protection

Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– Real inflation in Zimbabwe is 313 percent annually and 112 percent on a monthly basis

– Venezuela’s new 100,000-bolivar note is worth less oday thehan USD 2.50

– Maduro announces plans to eliminate all physical cash

– Gold rises in response to ongoing crises

A military coup-de-grace in Zimbabwe and a bankrupt Venezuela. Both countries have extreme hyperinflation, citizens are starving and basic medical treatment is near impossible to find. These are the real world problems 47.5 million people are currently facing.

Presidents Robert Mugabe and Nicolas Maduro both deny the crises in their respective countries. For Maduro it is the media propagating false truths. In Zimbabwe the response to hyperinflation has been to declare it illegal.

Both countries are in the media spotlight after a significant week that has left one man powerless and another scrambling to restore faith in his bankrupt country.

Each country’s mess is thanks to mismanagement of resources and the central banking system. Citizens have had their rights almost decimated as the cash in the bank is worth increasingly less and fewer people are receiving income. Basic goods and services are near impossible to come by, with little sign of let-up.

The hyperinflation and economic situations in both the Latin American and south African country are a reminder of the damage caused by governments. Both Maduro and Mugabe have acted under the premise of serving the electorate. Citizens as a result have only suffered and seen their wealth diminish on a daily basis.

Both countries may seem a million miles away from the West in terms of political situation and cultures. However there is a strong lesson to be learnt. Savers should learn the need to protect their earnings and wealth from the manipulative decisions of governments and destructive monetary policies.

Zimbabwe: The tyranny of a despot and his central bank

“Zimbabwe, welcome back to the record books! You have once again entered the inglorious world of hyperinflation. It is a world of economic chaos, wrenching poverty and death,”

– Steve Hanke, economics professor at Johns Hopkins University

Venezuela reminds me of a quote that is often misattributed to Milton Friedman:

“If you put the federal government in charge of the Sahara Desert, in 5 years there’d be a shortage of sand.”

Today you could say the same about oil and the Venezuelan government. The country was once the richest in Latin America but can no longer cover its own debts.

On Monday it missed interest payments on two government bonds. Even after a 30-day grace period it is unable to muster up $280 million owed in payments.

Meanwhile the value of the bolivar continues to plunge, causing major financial problems for Venezuelans. As explained by Business Insider:

After the country’s economic collapse in 2016, high inflation caused the bolivar’s value to plummet. By December, the then-largest note of 100 bolivares, which was worth about $US0.02, was pulled from circulation. To counter this, new denominations of 500, 1,000, 2,000, 5,000, 10,000, and 20,000 bolivares were introduced.

Maduro’s unveiling of the 100,000 bolivar note means it’s possible that some of these smaller notes may soon be phased out. This would cause serious problems for Venezuelans who, on average, are only allowed to withdraw about 10,000 to 20,000 bolivares a day. In October, the daily withdrawal allowance equalled roughly $3 to $6 at black market exchange rates. On the current market, 20,000 bolivares are worth around 50 cents.

To ‘combat’ the problem of cash shortages Maduro recently announced in a public broadcast that he planned to phase out physical cash, saying “the use of the physical currency is being replaced.”

This is something that was also seen in Zimbabwe. During their first notable hyperinflation era of 2005-2009, the government ran out of money to pay for money. The local currency cost US Dollars, which they could not afford to buy.

Should this happen this will be even more damming for those with cash in the bank. Currently they are able to withdraw physical cash in order to keep on top of the daily increase in inflation. Now they will have little choice but to sit and watch its value disappear.

The enforced holding of cash in the bank will no doubt bring with it capital controls as citizens are prevented from exchanging the bolivar for stronger currencies such as the US dollar. The first step has already been taken as Maduro has tried to contain the financial rout by banning the publication of black market rates. Something Mugabe also tried.

Venezuela’s default should also be of concern to citizens elsewhere, especially in the US. It has come to light that a number of Americans with 401(k) own a hefty amount of Venezuela’s $60 billion debt. How will this work out if the country is unable to pay or has its debt restructured?

Avoid exposure to hyperinflation

Here in the West we are currently extremely fortunate as we are not facing political leaders such as Maduro or hyper inflationary scenarios as those seen in both Zimbabwe and Venezuela.

However, as evidenced just above we may still be exposed in the immediate sense to the failings of these countries, whether through our pension plans or investments elsewhere.

Even if you can be certain that you hold no Venezuelan debt or exposure to the Zimbabwean economy this is still a lesson in how one must diversify their assets outside of cash and the banking system. This is thanks to ultimate control institutions and governments have over these entities, should they so choose.

By holding assets outside of the system you can work to protect your wealth from such measures as those seen in Zimbabwe and Venezuela. Gold is one of the best examples. When held in a physical, allocated and segregated manner the owner cannot be prevented from accessing it whenever they so wish. Nor can it be devalued at will or suddenly illegal to trade. It is a borderless currency that acts without the control of governments looking to further their own wealth or political beliefs.

News and Commentary

Gold steady as dollar gains amid U.S. rate hike expectations (Reuters.com)

Asia Stocks Gain, Halting Slide; Aussie, Won Rise (Bloomberg.com)

Stocks Fall, Treasuries Rise as Commodities Slump (Bloomberg.com)

U.S. business inventories unchanged in September (Reuters.com)

U.S. consumer prices edge up; retail sales unexpectedly increase (Reuters.com)

Source: ref: Twitter:@Gold_Advice

Source: ref: Twitter:@Gold_Advice

TURKS follow Erdogan’s call to get rid of dollars & buy gold (RT.com)

Chinese buying more gold as global demand falls (CGTN.com)

Gold inches down as U.S. rate hike looms (Reuters.com)

Paulson Holds Stake in Gold Steady, Soros Stays on Sidelines (NewsMax.com)

Why We’re Buying Physical Gold with a $1700 Target (ZeroHedge.com)

Gold Prices (LBMA AM)

16 Nov: USD 1,277.70, GBP 969.01 & EUR 1,085.53 per ounce

15 Nov: USD 1,285.70, GBP 976.62 & EUR 1,086.29 per ounce

14 Nov: USD 1,273.70, GBP 972.47 & EUR 1,086.59 per ounce

13 Nov: USD 1,278.40, GBP 977.59 & EUR 1,097.89 per ounce

10 Nov: USD 1,284.45, GBP 976.44 & EUR 1,102.19 per ounce

09 Nov: USD 1,284.00, GBP 980.98 & EUR 1,106.29 per ounce

08 Nov: USD 1,282.25, GBP 976.82 & EUR 1,105.43 per ounce

Silver Prices (LBMA)

16 Nov: USD 17.04, GBP 12.92 & EUR 14.48 per ounce

15 Nov: USD 17.12, GBP 13.00 & EUR 14.45 per ounce

14 Nov: USD 16.94, GBP 12.92 & EUR 14.45 per ounce

13 Nov: USD 16.93, GBP 12.93 & EUR 14.53 per ounce

10 Nov: USD 17.00, GBP 12.92 & EUR 14.60 per ounce

09 Nov: USD 17.10, GBP 13.03 & EUR 14.69 per ounce

08 Nov: USD 17.00, GBP 12.96 & EUR 14.65 per ounce

Recent Market Updates

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

– Gold Coins and Bars Saw Demand Rise 17% to 222T in Q3

– Prepare For Interest Rate Rises And Global Debt Bubble Collapse

– Platinum Bullion ‘May Be One Of The Only Cheap Assets Out There’

– World’s Largest Gold Producer China Sees Production Fall 10%

– German Investors Now World’s Largest Gold Buyers

– Gold Price Reacts as Central Banks Start Major Change

– Why Switzerland Could Save the World and Protect Your Gold

– Invest In Gold To Defend Against Bail-ins

– Stumbling UK Economy Shows Importance of Gold

END

A joke: the one exchange that the CME plans to use when it starts with its futures operation is down again and it is having serious issues

(Russo/Bloomberg)

The bitcoin exchange CME plans to use for futures is down

Submitted by cpowell on Wed, 2017-11-15 18:27. Section: Daily Dispatches

By Camila Russo

Bloomberg News

Wednesday, November 15, 2017

This is exactly what the bitcoin futures naysayers have been warning about: One of the exchanges which CME Group Inc. would use to price the contracts is having serious issues.

Clients of San Francisco-based Kraken are seeing slow responses from the website, connection timeouts, and delays in withdrawals, the cryptocurrency exchange said in a statement late Tuesday. “We are investigating these issues and working to resolve as quickly as possible,” the statement said.

Problems in the fifth-biggest exchange by bitcoin trading volume come just three days after Seoul-based Bithumb’s servers crashed as a sudden surge in usage caused a connection failure. The issues raise concerns about whether largely unregulated exchanges, without the safeguards of securities bourses, will be able to reliably provide prices for indexes tied to futures and exchange traded funds, and cope with higher trading volume that could come if institutional investors start buying cryptos. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-11-15/bitcoin-exchange-that…

END

German Precious Metals Association honors GATA consultant Dimitri Speck

Submitted by cpowell on Wed, 2017-11-15 18:39. Section: Daily Dispatches

1:40p ET Wednesday, November 15, 2017

Dear Friend of GATA and Gold:

Financial analyst and GATA consultant Dimitri Speck, author of “The Gold Cartel,” has been given the German Precious Metals Association’s Winged Sculpture prize, which is awarded annually to people or projects whose work has engaged the public with precious metals and related topics.

Association board member said: “Dimitri Speck succeeded already as far back as 2002 in discovering statistical proof for the manipulation of the London gold fixing. In 2011 he followed up by providing statistical proof for the manipulation of the silver fixing as well, followed in 2014 by statistical proof for the manipulation of the platinum fixing.”

The announcement of Speck’s award is posted in German at the association’s internet site here:

http://www.goldseiten.de/artikel/352515–Dimitri-Speck-mit-Preis-der-Deu…

And in an English translation at Speck’s own internet site, Seasonax, here:

https://seasonax.com/news/dimitri-speck-winner-2017-prize-german-preciou…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

What a joke: this one BIS official urges accountability while it undergoes in secret huge gold swaps

(courtesy GATA/Chris Powell)

BIS official urges accountability while his press office rejects it

Submitted by cpowell on Wed, 2017-11-15 19:24. Section: Daily Dispatches

2:33p ET Wednesday, November 15, 2017

Dear Friend of GATA and Gold:

Even as the Bank for International Settlements was refusing on Tuesday to answer GATA’s questions about the bank’s activity in the gold market —

http://www.gata.org/node/17793

— the bank’s economic adviser and head of research, Hyun Song Shin, was addressing a conference at the European Central Bank in Frankfurt, Germany, giving a speech titled “Can Central Banks Talk Too Much?”:

https://www.bis.org/speeches/sp171114.pdf

And:

http://www.gata.org/files/BIS-HyunSongShinSpeech-11-14-2017.pdf

Shin echoed the 2005 remarks of another BIS official, William R. White, who said a major objective of central banking is “to influence asset prices (especially gold and foreign exchange) in circumstances where this might be thought useful”:

Shin told the ECB conference: “If central banks talk more to influence market prices, they should listen less to the signals emanating from those same markets. Otherwise, they could find themselves in an echo chamber of their own making, acting on market signals that are echoes of their own pronouncements.

On the other hand,” Shin continued, “talking less is hardly a viable option. Central bank actions matter too much for the lives of ordinary people to turn the clock back to an era when silence was golden. Accountability demands that central banks make clear the basis for their actions.”

In fact at the moment accountability seems to mean little at the BIS, whose press office replied as follows to GATA on Tuesday: “We do not comment on specific accounts / holdings of central banks or of the BIS.”

(See: http://www.gata.org/node/17793)

So much for “the lives of ordinary people,” who, instead of being told how the BIS is meddling in the markets, can just drop dead.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Gold trading today:

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.6320/shanghai bourse CLOSED DOWN AT 3.27 POINTS .10% / HANG SANG CLOSED UP 167.07 POINTS OR 0.58%

2. Nikkei closed UP 322.80 POINTS OR 1.47% /USA: YEN RISES TO 113.14

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 93.94/Euro FALLS TO 1.1766

3b Japan 10 year bond yield: RISES TO . +.052/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.27 and Brent: 61.62

3f Gold DOWN/Yen DWON

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.386%/Italian 10 yr bond yield DOWN to 1.850% /SPAIN 10 YR BOND YIELD DOWN TO 1.515%

3j Greek 10 year bond yield RISES TO : 5.18???

3k Gold at $1277.15 silver at:17.05: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 24/100 in roubles/dollar) 59.97

3m oil into the 55 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9925 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1678 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.386%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.359% early this morning. Thirty year rate at 2.797% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Jump, Global Stocks Rebound From Longest Losing Streak Of The Year

After five consecutive daily losses on the MSCI world stock index and seven straight falls in Europe, there was finally a bounce, as investors returned to global equity markets in an optimistic mood on Thursday, sending US futures higher after several days of losses as global stocks rebounded following a Chinese commodity-driven rout.

The House is poised to vote, and pass, on tax legislation although what happens in the Senate remains unclear. European shares rebounded for the first time in eight sessions, following Asian stocks higher as the global risk-off mood eased. The euro, Swiss franc and yen all weakened as the dollar edged higher. “After five or six days of steady selling you have got people coming back in looking for bargains,” said CMC Markets’ Michael Hewson. “I think it’s temporary though. We haven’t had a significant sell off this year and the fact of the matter is that equity markets have done so much better than anyone dared to envisage.”

As Bloomberg echoes, “investors seem to be regaining their appetite for risk after several days of global declines in stocks and high-yield credit that had many questioning whether the selloff could become a rout.”

Still, investor concern over the progress of a massive U.S. tax reform plan showed no sign of abating as two Republican lawmakers on Wednesday criticized the Senate’s latest proposal. U.S. President Donald Trump hit back, tweeting that “Tax cuts are getting close!”

“If we look at what the markets are focusing on, it’s still very much the tax cut debates in the U.S., and how much progress there’s going to be on this front,” Barclays’ Mitul Kotecha told Reuters.

Indices in Tokyo, Shanghai and Hong Kong and Seoul all rallied overnight, while London, Frankfurt and Paris started 0.3-0.4% higher as cyclical stocks which had driven the sell-off made a comeback. In Japan the Topix index ended its longest losing streak in a year, rising 1% with technology stocks providing the biggest boost, and the Nikkei 225 advances 1.5%. The ASX (+0.2%) also managed to shake off its early losses, closing higher with the energy sector outperforming as consumer staples and utilities weighed. Chinese stocks edged lower despite a massive cash injection by the PBOC, while the Hang Seng moved higher. Hong Kong stocks rebounded from their worst day in four weeks, as insurers led by Ping An Insurance Group Co. jumped on optimism that rising bond yields will boost investment income. Tencent Holdings climbed after posting its fastest revenue growth in seven years.

China’s sovereign bonds finally rebounded, advancing after the central bank boosted cash injections by the most in 10 months, fueling speculation that the authorities are looking to stabilize sentiment after a debt selloff. Having flirted with 4% in recent days, the yield on 10-year government notes dropped 3 basis points to 3.95%; the 5-year yield fell 1 basis point to 3.95%. The 10-year yield surpassed 4% this week for the first time since 2014. The People’s Bank of China added a net 310 billion yuan ($47 billion) through reverse-repurchase agreements on Thursday, bringing this week’s open-market operation additions to 820 billion yuan, also the most since January.

European stocks bounce back from a seven-day rout – the longest losing streak of the year – that had erased almost 400 billion euros ($471 billion) from the value of the region’s benchmark. The Stoxx Europe 600 Index adds 0.7%, following gains in Asia and climbing from a two-month low. All national benchmarks in the region are in the green, except those in Italy and Greece. Most industry groups also rise, with automakers rebounding from an eight-day slump on data showing European car sales grew in October. Financial services firms and builders were among the biggest gainers in the broad advance of the Stoxx Europe 600 Index.

There was some relief too that oil prices had pulled out of what had been a near 5 percent drop and that upbeat U.S. data on Wednesday had helped the dollar halt the euro’s sharp recent rise.

In currencies, the pound fluctuated as Brexit rhetoric rumbled on, and data showed U.K. retail sales barely rose in October. Concerns about Brexit continue to mount: an article in ‘The Sun’ newspaper, stated that UK PM May, could increase her divorce bill offer to the EU in December; deal would add GBP 20bln to the GBP 18bln said to already be on offer. Source reports indicate that EU is said to reject UK bid for `bespoke’ trade deal, according to Politico. BoE’s Carney states that the Bank will do whatever they can to support the UK economy during the Brexit transition period. Chancellor Hammond said to stick to fiscal rules and resist demands for spending surge in upcoming UK budget. Michael Gove is reportedly facing a Conservative party backlash as he is accused of using the cabinet to audition for UK Chancellor

The dollar index was slightly higher on the day at 93.828 having hit four- and five-week lows against the yen and euro. The euro was down around 14 ticks at $1.1760 retreating from a one-month top of $1.1860 on Wednesday. Havens underperformed on Thursday, with gold trading little changed, and the yen and Swiss franc among the worst-performing major currencies. The Swiss franc decreased 0.3 percent to $0.9918, the largest dip in more than two weeks.

Commodities largely stabilized as China’s central bank boosted the supply of cash in the system by the most since January, though oil eventually reversed a gain. Gold edged 0.1% lower to $1,277.29 an ounce. It reached $1,289.09 overnight, its highest since Oct. 20. Oil prices gained despite pressure after the U.S. government reported an unexpected increase in crude and gasoline stockpiles. They had lost ground to this week’s International Energy Agency (IEA) outlook for slower growth in global crude demand.

European government bonds took their cue from the U.S. benchmark, turning lower as the yield on 10-year Treasuries increased. Bond markets saw a broad rise in yields after mostly upbeat U.S. economic news on Wednesday had added to expectations the Federal Reserve will hike interest rates again next month as well as multiple times next year. Two-year Treasury yields US2YT=RR crept to fresh nine-year peaks in European trading, though significantly the U.S. yield curve remained at its flattest in a decade. European yields nudged higher too but the standout there was a fall in the premium investors demand to hold French debt over German peers to its lowest in over two years, almost to record lows.

Wal-Mart, Viacom, Best Buy and Applied Materials are among companies due to release results. Economic data include initial jobless claims, Philadelphia Fed Business Outlook.

Market Snapshot

- S&P 500 futures up 0.4% to 2,574

- STOXX Europe 600 up 0.7% to 384.61

- MSCI Asia up 0.8% to 169.14

- MSCI Asia ex Japan up 0.7% to 555.93

- Nikkei up 1.5% to 22,351.12

- Topix up 1% to 1,761.71

- Hang Seng Index up 0.6% to 29,018.76

- Shanghai Composite down 0.1% to 3,399.25

- Sensex up 1% to 33,095.23

- Australia S&P/ASX 200 up 0.2% to 5,943.51

- Kospi up 0.7% to 2,534.79

- German 10Y yield rose 1.3 bps to 0.389%

- Euro down 0.1% to $1.1779

- Brent Futures down 0.03% to $61.85/bbl

- Italian 10Y yield rose 0.7 bps to 1.57%

- Spanish 10Y yield rose 1.1 bps to 1.561%

- Brent Futures down 0.03% to $61.85/bbl

- Gold spot down 0.02% to $1,277.91

- U.S. Dollar Index up 0.1% to 93.91

Top Overnight News

- After a month of discussions, German Chancellor Angela Merkel faces a self-imposed end-of-week deadline to unlock coalition negotiations

- British PM Theresa May saw some support from officials of her German counterpart Merkel

- Manfred Weber, who leads Merkel’s Christian Democrats in the European Parliament and is a self-proclaimed skeptic on Brexit, changed his tone dramatically after meeting May saying the U.K. had a “credible” position and there was a “willingness to contribute to a positive outcome”

- Sterling came under pressure after a Politico report said the EU’s Chief Brexit Negotiator Michel Barnier’s team flatly reject May’s bid for a “bespoke” trade deal

- Fed officials are pushing for a potentially radical revamp of the playbook for guiding U.S. monetary policy. With inflation and interest rates still low, the central bank has little room to ease policy in a downturn

- U.S. Treasury Secretary Steven Mnuchin is trying to persuade businesses and the Republican faithful to get behind a proposed tax overhaul from the Trump administration that so far lacks broad public support

- The tax plan has provisions that may affect coverage and increase medical expenses for millions of families

- President Robert Mugabe’s refusal to publicly resign is stalling plans by Zimbabwe’s military to swiftly install a transitional government after seizing power on Wednesday

- Tax overhaul update: President Donald Trump is scheduled to head to the House, rallying Republican members before vote on tax bill

- German Chancellor Angela Merkel meets heads of her Christian Democratic-led bloc, Free Democrats and Green party to kick coalition talks into gear

- Cisco Sees First Revenue Growth in Eight Quarters; Shares Up

- Koch Brothers Are Said to Back Meredith Bid to Buy Time Inc.

- Health Care for Millions at Risk as Tax Writers Look for Revenue

- Cerberus’s Feinberg Switches Strategy to Shake Up German Banking

- Mattel Drops on Report That It Rebuffed Approach From Hasbro

- New SUVs at Peugeot, Ford Offset U.K. Drag on Europe Car Sales

- Google Sued for Using ‘Bait and Switch’ to Hook Minority Hires

- Santos Seen Luring More Bids After Rejecting $7.2 Billion Offer

- AT&T’s Clash With America Movil Slows Nafta Telecom Talks

- Mobileye’s $15 Billion Deal Masks Drop in Israel Tech M&A

- Mugabe’s Refusal to Resign Is Said to Stall Zimbabwe Transition

In Asian markets, a modest uptick in US stock index futures helped the Nikkei 225 stem some of its recent losses, with financials and retailers leading the way; as a result, he Japanese blue-chip index closed up 1.5%. The ASX (+0.2%) also managed to shake off its early losses, last closing up, with the energy sector outperforming (although this was on the back of confirmation of a rebuffed Santos takeover offer) as consumer staples and utilities weighed. Chinese stocks edged lower, while the Hang Seng moved higher Treasuries operated in a narrow range throughout the APac session, while JGBs were relatively listless, with a solid 20-year auction the highlight of the session. Aussie bond yields moved to session highs in the wake of the aforementioned labour market release, where they consolidated.

In European markets, equities kicked off the session on the front-foot in a continuation of some of the sentiment seen overnight during Asia-Pac trade (Nikkei 225 +1.5%). Some slight underperformance has been observed in the FTSE 100 with gains capped by a slew of ex-dividends which have trimmed 14.56 points off the index. Notable ex-dividends include both of Royal Dutch Shell’s listings, with the oil-heavyweight subsequently hampering the energy sector as WTI and Brent crude have failed to make any meaningful recovery from Thursday’s losses. Elsewhere, the likes of Fiat Chrysler (+2.5%) and Volkswagen (+2.4%) have been giving a help hand by the latest EU new car registration data. In fixed income, a limited reaction to better than forecast UK consumption data, and clear reservations about retail activity over the key Xmas and New Year period based on bleaker signals from anecdotal surveys and non-ONS data. Hence, Gilts dipped to 124.72 (-15 ticks vs +8 ticks at best), while the Short Sterling strip reversed pre-data gains to stand flat to only 1 ticks adrift before stabilising again. In truth, core bonds were already on the retreat from early highs (ie Bunds down to 162.43 vs 162.71 at best) in what appears to be a broad retracement within recent ranges rather than anything more meaningful.

In FX, GBP has once again been a key source of focus with GBP/USD hit early doors amid reports in Politico that the EU are leaning towards rejecting the UK’s request for a bespoke trade deal. However, sentiment saw a mild recovery after reports in the Sun suggested that PM May could be on the cusp of upping her Brexit settlement offer in an attempt to kick-start trade talks. The main data release of the session thus far came in the form of UK retail sales which painted a less dreary picture of the UK economy than some had feared, although gains were short-lived as Brexit remains the focus. Marginal sterling buying was seen in EUR/GBP, trading around session lows, helped by a stop hunt through yesterday’s lows. Cable too saw a bid later in the session, benefiting from the weaker USD. Elsewhere, EUR/USD is back below 1.1800 vs the USD after topping out just ahead of October’s 1.1880 high, and now in a fresh albeit higher range flanked by big option expiries between 1.1795-1.1800 (913mln) and 1.1815-25 (4.8bln). Another roller-coaster ride for the Antipodeans, with AUD choppy on mixed labour data (headline count miss, but jobless rate and full employment upbeat) and pivoting the 0.7600 handle vs the USD.

In the commodities complex, as mentioned above, WTI and Brent crude futures have failed to make any noteworthy recovery from the sell-off seen on Tuesday with energy newsflow particularly light during today’s session thus far with markets looking ahead to the November 30th OPEC meeting which is set to give nations the instruction to extend oil production cuts. In metals markets, gold prices have traded in a relatively similar manner with prices unable to be granted any reprieve from their latest tumble. Elsewhere, Nickel and Copper have been weighed on, sending prices to multi-week lows as concerns around Chinese growth prospects continue to linger.

Looking at the day ahead, weekly initial jobless claims, Philly Fed PMI for November, import price index for October, industrial production for October and NAHB housing market index for November will be released. The BoE Carney’s, Broadbent and Haldane will all participate at a public plenary session while the ECB’s Villeroy de Galhau and Constancio are due to speak, along with the Fed’s Williams, Mester and Kaplan.

US Event Calendar

- 8:30am: U.S. Initial Jobless Claims, Nov. 11, est. 235k (prior 239k); Continuing Claims, Nov. 4, est. 1900k (prior 1901k)

- 8:30am: U.S. Philadelphia Fed Business Outl, Nov., est. 24.6 (prior 27.9)

- 8:30am: U.S. Import Price Index MoM, Oct., est. 0.4% (prior 0.7%); U.S. Export Price Index MoM, Oct., est. 0.4% (prior 0.8%);

- 9:15am: U.S. Industrial Production MoM, Oct., est. 0.5% (prior 0.3%); Capacity Utilization, Oct., est. 76.3% (prior 76.0%)

- 9:15am: U.S. Bloomberg Consumer Comfort, Nov. 12, no est. (prior 51.5); Economic Expectations, Nov., no est. (prior 47.5)

Central Bank speakers:

- 9:10am: Fed’s Mester delivers keynote address at Cato Conference

- 1:10pm: Fed’s Kaplan speaks to CFA society in Houston

- 3:00pm: ECB’s Constancio speaks in Ottawa

- 3:45pm: Fed’s Brainard delivers keynote at OFR FinTech Conference

- 4:45pm: Fed’s Williams speaks at Asia Economic Policy Conference

DB’s Jim Reid concludes the overnight wrap

There has been a lot of noise around the HY market in the past week or so as a combination of macro factors along with some notable earnings misses have weighed on the market. iTraxx Crossover and CDX HY have widened by around 25bps and 30bps respectively from their most recent tights, while the price level of the largest USD HY ETF (HYG US) is basically back to the same level as where it started the year, however this overstates the move in the US cash market and even more so in Europe. Looking in more detail at the cash market US HY has widened by around 60bps and EUR HY is 46bps wider from the recent cycle tights only a few weeks back but both are still around 25bps and 100bps tighter on the year respectively.

In a broad historic context the recent moves hardly register but in the context of a year that has been headlined by extremely low levels of volatility they are certainly significant. For EUR HY there were two other periods where we saw some sort of correction this year. In March/April (ahead of the French elections) the index widened 27bps in 42 days and then in August/September (after the North Korean escalation) we saw a 29bps widening over 30 days. So the current 46bps of widening in just 12 days has been somewhat more aggressive than anything else we’ve seen this year.

Looking at similar data for the US we have also seen two previous corrections. In March spreads widened 61bps in 20 days and then in July/August we saw 45bps of widening in 15 days. So the current c.60bps widening over 22 days is actually of a similar magnitude to this year’s previous corrections. The moves look even more stark when we focus on single-Bs though. EUR single-Bs have widened by more than 100bps from the most recent tights, more than halving the YTD tightening we had seen. For USD single-Bs the recent widening (65bps) has actually reversed more than 80% of the YTD spread tightening we had seen to the recent tights.

The question from here is whether this recent back-up in spreads is simply going to lead to a fresh buying opportunity or whether it will lead to something more significant. Despite some of the recent profit warnings we think that it is more likely to be the former at the moment. But at the very least the pace of this turn around highlights how quickly market sentiment can change, especially when spreads are so tight. HY was looking very very stretched relative to IG in Europe and this corrects some of that. Overall it certainly provides us with some food for thought as we look to publish our 2018 outlook in the next 10 days.

Even though US HY has been one of the weaker markets of late there’s no doubt that the recent global equity sell off has struggled to gather momentum as the US session has progressed over the last week. Following through on this, Asia has been weak since the Nikkei sudden sell-off last week and Europe has followed with yesterday seeing the 7th successive daily fall in the Stoxx 600 (-0.49%) – the longest losing streak since October/November 2016. Meanwhile yesterday the US (S&P 500 -0.55%) again closed off the early session lows showing that this equity sell-off isn’t really being US led. For the record since last Wednesday’s close the S&P 500, Stoxx 600 and Nikkei are down -1.15%, -3.17% and -3.86% respectively which helps illustrate this.

Volatility has been on the way up though even in the US over this period. The VIX spiked to 14.51 intraday which was the highest since August 18th. It closed at 13.13 (+13%) which is still the highest since the same period. Meanwhile the VSTOXX index was up +2.25% and is now at the highest level since early September.

This morning in Asia, markets have stemmed losses and are trading higher. The Nikkei (+1.24%), Kospi (+0.52%), Hang Seng (+0.53%) and ASX 200 (+0.30%) are all up as we type. WTI oil is trading marginally higher and after the bell in the US, Cisco was up c6% after guiding to its first revenue gain in eight quarters.

On now to the big data of the yesterday and possibly the month. US Core CPI inflation surprised modestly to the upside in October, rising 0.225% in month-on-month terms (a firmer 0.2% print than DB expected). This raised the year-overyear rate to 1.8% (1.7% expected). The data provide additional evidence that the core inflation trend is firming after a string of very weak prints earlier this year. According to our economists, the three-month annualised change in core CPI inflation is now at 2.4%, the strongest since February 2017. We think inflation is turning a corner and regular consistent misses vs expectations will not be a feature of markets in 2018.

Staying in the US, the House’s version of the tax plan is reportedly on track for a vote on Thursday (local time). In terms of the Senate’s version, rhetoric appears to be heating up as the mark up process continues. The Democrats were reportedly not impressed with the last minute change to add in the repeal of the Obamacare individual mandate, to which Republican Senator Collins partly agrees on, noting that it “gravely complicated our efforts to combine tax reform and changes”, although she has not decided whether to vote against the bill or not. Elsewhere, Republican Senator Johnson has publicly confirmed that he is opposed to the revised GOP plan as it stands, in part as it does not do enough to help partnerships relative to the larger tax cuts for corporates.

Quickly recapping other markets performance from yesterday. Bond markets were firmer with core bond yields down 2-5bp (UST 10y -5bp; Bunds -2.1bp; Gilts -3.5bp) while peripherals underperformed with Portugal bonds leading the softness (+2.5bp). Key currencies were little changed, with US dollar index marginally higher, while Euro dipped -0.06% but Sterling rose 0.05%. In commodities, WTI oil fell another -0.70% (-3.2% for the week), in part following reports that Russia believes it’s too early to announce a potential extension of production cuts at OPEC’s meeting at end of the month. Notably, WTI is still up c18% from late August. Elsewhere, precious metals softened a little (Gold -0.16%; Silver -0.14%) and other base industrial metals were little changed (Copper -0.45%; Zinc -0.54%; Aluminium +0.36%).

Away from the markets, there were a deluge of Fed and ECB central bankers commentaries yesterday but overall contained minimal market moving information. In the details, the Fed’s Evans noted he was open-minded regarding policy action at the December FOMC ahead of discussions with fellow colleagues and sounded dovish on inflation, noting “I feel we are facing below target inflations” while reiterating the US labour market is “vibrant” and unemployment rate “could go below 4%”.

In Europe, the ECB’s Hansson was upbeat on the demand side of the economy and “feel more confident that inflation will eventually reach the levels consistent with our aim”. Elsewhere, the ECB’s Praet pointed to the importance of interest rates post QE, noting that “policy rates will eventually regain their status as the main instrument of policy, and our forward guidance will revert to a singular approach”. Finally, the ECB’s Coeure noted that it’s important for the ECB “to ensure that our own measures do not adversely affect the intermediation capacity of repo markets”.

Over in China yesterday, there were more signs that the government may tolerate slower economic growth in 2018. The Economic Daily reported that the deputy head of the Research Office of the State Council Ms Han has flagged that GDP growth at 6.3% in 2018-2020 would be sufficient to achieve the Party’s 2020 growth target. As a reminder, our Chinese economists expect GDP growth to slow to 6.3% yoy by 1Q.

Finally, over in Zimbabwe, President Mugabe’s c40 years of power may be coming to an end with Bloomberg reporting the 93 year old was confined to his home, with military forces taking control of state owned media outlets and sealing offthe parliament and central bank’s offices.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the core retail sales for October (ex-auto & gas) was in line at 0.3% mom, but with the prior reading upwardly revised by 0.1ppt. Elsewhere, the September business inventories was flat and in line for the month. Finally, the November empire manufacturing index fell from a c3 year high of 30.2 to a still solid reading of 19.4. After the recent economic data, the Atlanta Fed’s GDPNow estimate of 4Q GDP growth has edged 0.1pp lower to 3.2% saar.

In the UK, the September unemployment rate was in line and steady at 4.3% – still at a 42 year low, while the average weekly earnings remains low but was slightly above expectations at 2.2% yoy (vs. 2.1% expected). Elsewhere, jobless claims (1.1k vs. 1.7k previous) and claimant count rate (2.3% vs. same as previous) were broadly similar to prior readings. The Eurozone’s September trade surplus widened to EUR$25bln (vs. EUR$21bln expected), while the final reading for France’s October CPI was unrevised at 0.1% mom and 1.2% yoy.

Looking at the day ahead, the final October CPI report for the Euro area will be out. UK retail sales data for October and Q3 employment data for France will also be released. In the US weekly initial jobless claims, Philly Fed PMI for November, import price index for October, industrial production for October and NAHB housing market index for November will be released. The BoE Carney’s, Broadbent and Haldane will all participate at a public plenary session while the ECB’s Villeroy de Galhau and Constancio are due to speak, along with the Fed’s Williams, Mester and Kaplan.

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 3.27 points or .10% /Hang Sang CLOSED UP 167.07 pts or 0.58% / The Nikkei closed UP 322.80 POINTS OR 1.47%/Australia’s all ordinaires CLOSED UP 0.19%/Chinese yuan (ONSHORE) closed DOWN at 6.6320/Oil DOWN to 55.27 dollars per barrel for WTI and 61.62 for Brent. Stocks in Europe OPENED GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6320. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.638 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS OT VERY HAPPY TODAY.

3 a NORTH KOREA/USA

NORTH KOREA/USA

3b) REPORT ON JAPAN

3c CHINA REPORT.

4. EUROPEAN AFFAIRS

And this guy is deputy Governor of the Bank of England?

(courtesy zerohedge)

BoE Deputy Governor Gives Crazy Speech Warning Markets Have Underestimated Rate Rises

On 2 November 2017, the Bank of England raised rates for the first time in a decade and Sterling’s initial rise was promptly sold off by forex traders as we discussed.

The 7-2 vote by the Monetary Policy Committee was not the unanimous decision some had expected, while Cunliffe and Ramsden saw insufficient evidence that wage growth would pick up in line with the BoE’s projections from just over 2% to 3% in a year’s time. Ben Broadbent, MPC member, deputy governor and known to be a close confidant of Governor Carney, gave a speech today at the London School of Economics (LSE) in which he warned markets that Brexit issues didn’t necessarily mean that interest rates have to remain low.

Bloomberg reports that Broadbent stated that the Brexit impact on monetary policy depends on how it affects demand, supply and the exchange rate.

“There are feasible combinations of the three that might require looser policy, others that lead to tighter policy.”

Which sounds alot like he doesn’t know, although he stuck to the central bankers trusty tool, reassuring LSE students the Phillips Curve “still seems to have a slope”.

According to the FT.

The deputy governor of the Bank of England has warned that financial markets have underestimated the chance of further interest rate rises. In a speech at the London School of Economics on Wednesday, Ben Broadbent said markets had placed too much emphasis on the idea that interest rates needed to be kept low in the face of Brexit uncertainty. The deputy governor said it was “uncertain” and “complex” to anticipate how Brexit would affect inflation. But he rejected the assertion that Brexit “necessarily implies low interest rates”.

“Even as inflation rose, and the rate of unemployment fell further, interest-rate markets continued to under-weight the possibility that (the) bank rate might actually go up this year,” he said.

The BoE’s Monetary Policy Committee announced its first interest rate rise in more than a decade earlier this month. But the central bank has struggled to convince financial markets that it is likely to raise rates further.

BoE officials were taken aback when sterling sold off on the day it announced the rate rise, and two-year gilt yields remain below the BoE base rate, suggesting markets are sceptical that the MPC will raise rates further while there is still considerable uncertainty around the UK’s economic future outside of the EU.

Broadbent acknowledged that there is a risk that Brexit uncertainty could adversely impact UK demand. However, he sees the potential for other factors, a reduction in trade, for example, which could crimp UK capacity and necessitate a rise in rates. While Broadbent’s thinking is flawed, and his barley field example plainly ridiculous, the FT continues.

Brexit-related uncertainty could weigh on demand and motivate the MPC to keep interest rates low to support the economy, but other factors could push the central bank to raise rates.

For example, if Brexit reduced the UK’s openness to trade, the country’s output capacity could suffer, which would require the BoE to raise rates to temper inflation.

“Economists often presume that changes in an economy’s underlying productivity occur only slowly,” Mr Broadbent said. However, he added: “A sharp reduction in the degree of openness (to trade) could have a more immediate impact. “A field currently producing barley, sold into the European market, can’t easily or as fruitfully be replanted with olive trees”. He said the challenge for monetary policymakers was that “reductions in supply can add inflationary pressure even as they lower aggregate (gross domestic product)”.

So, let’s consider Broadbent’s example…

The UK suffers a drop in aggregate demand due to a contraction in trade, the BoE raises rates in an over-leveraged economy to stem the inflation and…undoubtedly makes the contraction in GDP much worse. That makes no sense and is the kind of one dimensional thinking that we’ve had to put up with from central bankers. What’s worse is that Broadbent has specific responsibility for monetary policy and a c.v. as long as your arm – Cambridge, Harvard PhD, Fulbright Scholar, Columbia University, Goldman Sachs and UK Treasury.

It’s no wonder we are in such a mess with people like this pulling the levers of policy in the central banks. Crazy ideas aside, Broadbent and his BoE colleagues might be unhappy with market projections for the future path of interest rates, but they can hardly blame investors for being sceptical.

Which way are rates going, Ben?

END

5. RUSSIA AND MIDDLE EASTERN AFFAIRS

SAUDI ARABIA

Brandon Smith Warns: The Saudi Coup Signals War And The New World Order Reset

Authored by Brandon Smith via Alt-Market.com,

For years now, I have been warning about the relationship of interdependency between the U.S. and Saudi Arabia and how this relationship, if ended, would mean disaster for the petrodollar system and by extension the dollar’s world reserve status.

In my recent articles ‘Lies And Distractions Surrounding The Diminishing Petrodollar’ and ‘The Economic End Game Continues,’I point out that the death of the dollar as the premier petrocurrency is actually a primary goal for establishment globalists.

Why?

Because in an effort to achieve what they sometimes call the “global economic reset,” or the “new world order,” a more publicly accepted centralized global economy and monetary framework is paramount. And, this means the eventual implementation of a single world currency and a single global economic and political authority above and beyond the dollar system.

But, it is not enough to simply initiate such socially and fiscally painful changes in a vacuum. The banking powers are not interested in taking any blame for the suffering that would be dealt to the masses during the inevitable upheaval (or blame for the suffering that has already been caused). Therefore, a believable narrative must be crafted. A narrative in which political intrigue and geopolitical crisis make the “new world order” a NECESSITY; one that the general public would accept or even demand as a solution to existing instability and disaster.

That is to say, the globalists must fashion a propaganda story to be used in the future, in which “selfish” nation-states abused their sovereignty and created conditions for calamity, and the only solution was to end that sovereignty and place all power into the hands of a select few “wise and benevolent men” for the greater good of the world.

I believe the next phase of the global economic reset will begin in part with the breaking of petrodollar dominance. An important element of my analysis on the strategic shift away from the petrodollar has been the symbiosis between the U.S. and Saudi Arabia. Saudi Arabia has been the single most important key to the dollar remaining as the petrocurrency from the very beginning.

The very first oil exploration and extraction deal in Saudi Arabia was sought by the vast international oil cartels of Royal Dutch Shell, Near East Development Company, Anglo-Persian, etc., but eventually fell into the hands of none other than the Rockefeller’s Standard Oil Company. The dark history of Standard Oil aside, this meant that Saudi business would be handled primarily by American interests. And the Western thirst for oil, especially after World War I, would etch our relationship with the reigning monarchy in stone.

A founding member of OPEC, Saudi Arabia was one of the few primary oil-producing nations that maintained an oil pipeline that expedited processing and bypassed the Suez Canal. (The pipeline was shut down, however, in 1983). This allowed Standard Oil and the United States to tiptoe around the internal instability of Egypt, which had experienced ongoing conflict which finally culminated in the civil war of 1952.

Considered puppets of the British Empire at the time, the ruling elites of Egypt were toppled by the Muslim Brotherhood, leading to the eventual demise of the British pound sterling as the top petro-currency and the world reserve. The British economy faltered and has never since returned to its former glory.

Perhaps we are seeing some parallels here?

Civil war may not be in the cards for Saudi Arabia; so far a quiet coup has been rather effective in completely changing the power base of the nation over the past few years. The primary beneficiary of that change in power has been crown prince Mohammed Bin Salman, who only answers to King Salman, an 81-year-old ruler barely involved in leadership.

To understand how drastic this coup has been, consider this – for decades Saudi Kings maintained political balance by doling out vital power positions to separate, carefully chosen successors. Positions such as Defense Minister, the Interior Ministry and the head of the National Guard. Today, Mohammed Bin Salman controls all three positions. Foreign policy, defense matters, oil and economic decisions and social changes are now all in the hands of one man.

But the real question is, who is behind that man?

Well, the recent political purge of various “neo-conservative” tied Saudis might lead some to believe that Prince Mohammed is seeking an end to globalist control of Saudi oil and politics.

These people would be wrong for a number of reasons.

Prince Mohammed’s revolutionary “Vision for 2030” developed as he entered power was touted as a means to end Saudi reliance on oil revenues to support economic stability. However, I believe this plan is NOT about ending reliance on oil, but ending reliance on the U.S. dollar. In fact, the plan indicates a move away from the dollar as the world’s petrocurrency and a de-pegging of the Riyal from the dollar.

Prince Mohammed has also established much deeper ties to Russia and China, creating bilateral agreements which may end up removing the dollar as the mechanism for oil trade between the nations.

You would think that this kind of strategy would be highly damaging to the West and to American interests in particular and that the corporate establishment would be doing everything in their power to stop it. However, this is not at all the case. In reality, the globalist establishment is fully behind Mohammed Bin Sulman’s “Vision for 2030.”

Corporate behemoths such as the Carlyle Group (Bush family, etc), Goldman Sachs, Blackstone and Blackrock have ALL been backing the Vision for 2030 and Prince Mohammed through his Public Investment Fund (PIF), of which he is the chairman.

Trillions in capital are flowing through PIF, most of it from the coffers of globalist establishment companies. Once again I point out that the so-called “East versus West division” and the Eastern “opposition” to the globalists is complete nonsense; banking elites and globalists are the true influence behind the move away from the dollar, as the Saudi example and the Vision for 2030 shows. The end of the dollar as world reserve works in their favor — it is planned.

This does not end with the death of the dollar’s petro-status, though. These kinds of upsets in the power dynamic invariably lead to war. War acts as a kind of cleansing of the historical record; it tends to distract the public, for generations, from those that truly benefit from geopolitical and economic strife.