GOLD: $1282.00 UP $5.10

Silver: $17.00 UP 7 cents

Closing access prices:

Gold $1280.70

silver: $16.97

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1287.34 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1280.10

PREMIUM FIRST FIX: $7.24

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1288.21

NY GOLD PRICE AT THE EXACT SAME TIME: $1279.95

Premium of Shanghai 2nd fix/NY:$8.26

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1280.00

NY PRICING AT THE EXACT SAME TIME: $1280.55

LONDON SECOND GOLD FIX 10 AM: $1283.30

NY PRICING AT THE EXACT SAME TIME. 1283.30

For comex gold:

NOVEMBER/

NUMBER OF NOTICES FILED TODAY FOR NOVEMBER CONTRACT: 1 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR: 1053 FOR 105,300 OZ (3.375 TONNES)

For silver:

NOVEMBER

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 884 for 4,420,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8198 OFFER /$8224 down $30.00 (MORNING)

BITCOIN : BID $8206 OFFER: $8235 // down $22 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A LARGELY ANTICIPATED 7611 contracts from 205,094 DOWN TO 197,483 WITH RESPECT TO YESTERDAY’S TRADING WHICH SAW SILVER FALL BY A CONSIDERABLE 45 CENTS AND FALL WELL BELOW THE HUGE $17.25 SILVER RESISTANCE. WE HAD CONSIDERABLE LONG COMEX LIQUIDATION. HOWEVER WE WERE ALSO NOTIFIED THAT WE HAD QUITE A HUMONGOUS NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 2998 DECEMBER EFP’S WERE ISSUED ALONG WITH 0 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 2998 CONTRACTS. (THE ISSUANCE FOR MARCH THAT WE HAVE SEEN THESE PAST FEW DAYS BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY IN THE UPCOMING DELIVERY MONTH). I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. THURSDAY WITNESSED 1078 EFP’S ISSUED FOR YESTERDAY.

RESULT: A HUGE SIZED RISE IN OI COMEX WITH THE 45 CENT PRICE FALL. WE HAD CONSIDERABLE COMEX LONGS EXITED OUT OF THE COMEX . HOWEVER FROM THE CME DATA 2998 EFP’S WERE ISSUED FOR TUESDAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY LOST ONLY 4613 CONTRACTS.

In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.987 BILLION TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

In gold, the open interest FELL BY A LESS THAN EXPECTED 9,277 CONTRACTS WITH THE HUGE SIZED FALL IN PRICE OF GOLD ($19.70) WITH RESPECT TO YESTERDAY’S TRADING. WE HAD CONSIDERABLE COMEX LONGS EXIT THE ARENA. HOWEVER THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED A TOTALLY UNBELIEVABLE: 21,428 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 21,428 CONTRACTS AND FEB SAW THE ISSUANCE OF 150 CONTRACTS. YESTERDAY, WE WITNESSED A TOTAL OF 12,711 EFP’S ISSUED FRIDAY FOR MONDAY. The new OI for the gold complex rests at 550,561. DEMAND FOR GOLD INTENSIFIES DESPITE THE CONSTANT RAIDS. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NOT BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING 6 TO 10 WEEKS TO OBTAIN PHYSICAL WHEN FORWARDS ARE DUE.

Result: A HUGE SIZED DECREASE IN OI WITH THE MAMMOTH FALL IN PRICE IN GOLD ON YESTERDAY ($19.70). WE HAD AN UNBELIEVABLE HUMONGOUS NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 21,428. THERE OBVIOUSLY DOES NOT SEEM TO BE ANY PHYSICAL GOLD AT THE COMEX AN YET WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS NO GOLD PRESENT AT THE GOLD COMEX. IF YOU TAKE INTO ACCOUNT THE 21,428 EFP CONTRACTS ISSUED, WE HAD A NET GAIN OPEN INTEREST OF 12,151: 21,428 CONTRACTS MOVE TO LONDON AND 9277 LEAVE THE COMEX.

we had: 1 notice(s) filed upon for 100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

No change in gold inventory at the GLD/

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 318.074 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 7611 contracts from 205,094 DOWN TO197,483 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE HUGE FALL IN SILVER PRICE (A LOSS OF 45 CENTS ). HOWEVER, OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE A MONSTROUS 2998 PRIVATE EFP’S FOR DECEMBER (WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 0 EFP’S FOR MARCH FOR A TOTAL OF 2998 EFP CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THESE EFP ISSUANCE..USUALLY WE WITNESS THIS ONE WEEK PRIOR TO FIRST DAY NOTICE AND THIS CONTINUES RIGHT UP UNTIL FDN. WE ALSO HAD CONSIDERABLE AMOUNT OF SILVER COMEX LIQUIDATION.

RESULT: A HUGE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 45 CENT LOSS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). HOWEVER, WE HAD ANOTHER 2998 EFP’S ISSUED ,TRANSFERRING OUR COMEX LONGS OVER TO LONDON TOGETHER WITH CONSIDERABLE SILVER COMEX LIQUIDATION. YESTERDAY WE EXPERIENCED 1078 EFP’S ISSUED FOR TRANSFER TO LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 18.10 points or .53% /Hang Sang CLOSED UP 557.76 pts or 1.91% / The Nikkei closed UP 154.72 POINTS OR 0.70%/Australia’s all ordinaires CLOSED UP 0.27%/Chinese yuan (ONSHORE) closed DOWN at 6.6336/Oil UP to 56.55 dollars per barrel for WTI and 62.36 for Brent. Stocks in Europe OPENED GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6336. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6362 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(MARKETS STRONG)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

b) REPORT ON JAPAN

c) REPORT ON CHINA

China to crackdown online lenders and they are crashing

( zerohedge)

4. EUROPEAN AFFAIRS

Bill Blain outlines 4 major threats that can bring Europe crashing down:

( Bill Blain/Mint Partners)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Lebanon/Israel

The Lebanese army is now on full combat readiness at the southern border ready to counter Israel

( zerohedge)

ii)Saudi Arabia

Publicly traded Kingdom holdings seems to be in trouble as the Saudi purge is playing havoc to its financing

( zerohedge)

iii)Russia/Syria

Putin hold a surprise meeting with Assad on what he wants with Syria now that the terrorists have been defeated. He will phone Trump later today to discuss the matter:

( zerohedge)

6 .GLOBAL ISSUES

i)Zimbabwe

The impeachment process to remove Mugabe as begun:

( zerohedge)

ii)Mugabe resigns

(courtesy zerohedge)

iii)Bloomberg reports on some positive developments with respect to NAFTA being saved. Both the Cdn loonie and the Mexican peso rise.

( zerohedge)

7. OIL ISSUES

Oil tops 57 dollars per barrel after another big drawdown

( zerohedge)

8. EMERGING MARKET

This is going to hurt joint venture partners as bankrupt Venezuela is demanding oil without payment. Obviously when dividends are declared they will get nothing. This oil is being used internally to feed its people

( zerohedge)

9. PHYSICAL MARKETS

ii)Doomsday preppers are starting to switch from gold to bitcoin. Good luck to them. There is nothing backing bitcoin. It needs to be backed by gold.

iii)We brought this to your attention yesterday; The raid dropped the gold price right at its 50 day moving average of $1275. This resistance level held(courtesy zerohedge/GATA)

10. USA stories which will influence the price of gold/silver

ii)A very good question: why is the Dept of Justice downplaying reports and proof linking both Obama and Clinton to the Uranium 1 scandal

iii)Journalist Sara Carter provides proof of Obama/Clinton involvement in the Uranium 1 scandal and how the DOJ is trying to credit Campbell, the FBI informanta must read..

(courtesy Zero Point Now)

( zerohedge)

( zerohedge)

vi)both Trump and Putin are acting like true statesmen:

(courtesy zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ONLY FELL BY ONLY 9277 CONTRACTS DOWN to an OI level of 5550,561 DESPITE THE MAMMOTH FALL IN THE PRICE OF GOLD ($19.70 DROP WITH RESPECT TO YESTERDAY’S TRADING). WE EXPERIENCED SOME GOLD COMEX LIQUIDATION. HOWEVER WE DID HAVE A HUMONGOUS 21,428 COMEX LONGS EXIT THE COMEX ARENA THROUGH THE EFP ROUTE AS THEY RECEIVE A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 21,278 EFPS WERE ISSUED FOR DECEMBER AND 150 WERE ISSUED FOR MARCH. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. DUE TO THE HUGE INCREASE IN OI YESTERDAY, THE BANKERS FELT IT OBLIGATORY TO RAID THE COMEX TRYING TO GET OUR MATHEMATICAL LONGS TO FALL FROM THEIR RESPECTIVE TREE.

ON A NET BASIS IN OPEN INTEREST WE GAINED: 12,201 CONTRACTS IN THAT 21,428 LONGS WERE TRANSFERRED AS LONGS TO LONDON AS A FORWARD AND WE LOST 9227 COMEX CONTRACTS. NET GAIN 12,201

Result: a HUGE DECREASE IN COMEX OPEN INTEREST WITH THE HUGE SIZED FALL IN THE PRICE OF GOLD ($19.60.) HOWEVER A HUGE 21,428 EFP’S ISSUED FOR A FIAT BONUS AND A DELIVERABLE FORWARD GOLD CONTRACT IN LONDON. WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION YESTERDAY.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF 0 CONTRACT(S) REMAINING AT 10. We had 1 notices filed YESTERDAY so GAINED 1 contracts or 100 additional oz will stand for delivery AT THE COMEX in this non active month of November.

The very big active December contract month saw it’s OI LOSS OF 24,513 contracts DOWN to 243,578. January saw its open interest RISE by 85 contracts UP to 960. FEBRUARY saw a gain of 13,742 contacts up to 226,514. DEMAND FOR GOLD INTENSIFIES TO THE HIGHEST DEGREE.

We had 1 notice(s) filed upon today for 100 oz

VOLUME FOR TODAY : 428,049 (PRELIMINARY)

CONFIRMED VOLUME YESTERDAY: 474,373 contracts. (comex volumes are intensifying)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A HUGE 7611 CONTRACTS FROM 204094 DOWN TO 197,483 WITH YESTERDAY’S HUGE SIZED 45 CENT FALL IN PRICE. HOWEVER WE DID HAVE A MONSTROUS 2998 PRIVATE EFP’S ISSUED FOR DECEMBER AND 0 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THE ISSUANCE. USUALLY WE WITNESS THIS EVENT ONE WEEK PRIOR TO FIRST DAY NOTICE AND IT CONTINUES RIGHT UP TO FDN. WE HAD CONSIDERABLE LONG SILVER COMEX LIQUIDATION. THE TOTAL EFP’S ISSUED TODAY TO OUR COMEX LONGS TOTAL 2998 AND THUS DEMAND FOR PHYSICAL SILVER INTENSIFIES AGAIN

The new front month of November saw its OI FALL by 3 contract(s) and thus it stands at 3. We had 3 notice(s) served YESTERDAY so we gained 0 contracts or an additional NIL oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FELL by 22,620 contracts DOWN to 75,364, YET WE HAD 2998 EFP’S ISSUED WHICH MEANS A GOOD PERCENTAGE OF THE ROLLOVERS LANDED IN LONDON AS A TRANSFER OF OI FOR A FORWARD. January saw A GAIN OF 59 contracts RISING TO 1304.

We had 0 notice(s) filed for NIL oz for the NOV. 2017 contract

INITIAL standings for NOVEMBER

Nov 21/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil

oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

oz

|

| No of oz served (contracts) today |

1 notice(s)

100 OZ

|

| No of oz to be served (notices) |

9 contracts

(900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1053 notices

105,300 oz

3.275 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 0 customer withdrawal(s)

Total customer withdrawals: nil oz

we had 0 adjustment(s)

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (1053) x 100 oz or 105,300 oz, to which we add the difference between the open interest for the front month of NOV. (10 contracts) minus the number of notices served upon today (1 x 100 oz per contract) equals 106,200 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (1053) x 100 oz or ounces + {(10)OI for the front month minus the number of notices served upon today (1) x 100 oz which equals 106,200 oz standing in this active delivery month of NOVEMBER (3.303 tonnes)

WE GAINED 1 ADDITIONAL CONTRACTS OR 100 OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

THE COMEX GOLD CONTRACT AT AROUND THE SAME TIME AS LAST YEAR: (NOV 22) WE HAD 199,751 GOLD CONTRACTS STANDING AND THIS COMPARES TO 243,578 TODAY . THE DIFFERENCE IS HUGE!

ON FIRST DAY NOTICE FOR DECEMBER, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 514,112.106 or 15.999 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,826,580.395 or 274.54 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 80 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

700,530.500oz

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

600,685.34

oz

CNT

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL,OZ)

|

| No of oz to be served (notices) |

0 contract

(NIL oz)

|

| Total monthly oz silver served (contracts) | 885 contracts(4,420,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of Scotia: 700,530.500 oz

TOTAL CUSTOMER WITHDRAWAL 700,530.500 oz

We had 1 Customer deposit(s):

i) Into CNT:

261,594.766 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 600,685.34 oz

we had 1 adjustment(s)

i) out of CNT: 261,594.76 oz leaves the dealer and lands into the customer account of CNT

The total number of notices filed today for the NOVEMBER. contract month is represented by 0 contracts FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 884 x 5,000 oz = 4,420,0000 oz to which we add the difference between the open interest for the front month of NOV. (0) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 884 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(0) -number of notices served upon today (0)x 5000 oz equals 4,420,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 0 contract(s) or an additional NIL oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE. THE TRANSFER OF EFP’S TO LONDON FURTHER INTENSIFIES THE DEMAND FOR PHYSICAL METAL!!

AT THIS TIME LAST YEAR WE HAD 56,352 NOTICES STANDING FOR DELIVERY FOR SILVER. THIS YEAR 75,364 WITH THE SAME NUMBER OF TRADING DAYS LEFT.

ON FIRST DAY NOTICE FOR THE DECEMBER CONTRACT WE HAVE 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 173,740

CONFIRMED VOLUME FOR YESTERDAY: 197,483 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 197,483 CONTRACTS EQUATES TO 987 MILLION OZ OR 141% OF ANNUAL GLOBAL PRODUCTION OF SILVER

THE COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 43.555 million

Total number of dealer and customer silver: 231.587 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.4 percent to NAV usa funds and Negative 2.1% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.3%

Percentage of fund in silver:37.4%

cash .+.3%( Nov 21/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -1.06% (Nov 21 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.60% to NAV (Nov 21/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -1.06%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.60%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 21/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 277 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 212 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Nov 17/2017:

Inventory 318.074 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.57%

12 Month MM GOFO

+ 1.78%

30 day trend

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Versus Bitcoin: The Pro-Gold Argument Takes Shape

– Gold versus Bitcoin: The pro-gold argument takes shape

– Why cryptocurrencies will not replace gold as a store of value

– Similarities between crypto and gold but that does not make them substitutes

– Gold remains a highly liquid market, cryptocurrencies continue to be fragmented and difficult to spend

– Bitcoin does not make it an effective hedge against stocks

– Gold coins and bars cannot be hacked and vaults are insured

This weekend saw bitcoin shoot up over $8,000 and Bloomberg covered how some preppers were turning to bitcoin over gold. Does this mean it’s all over for gold? Is it set to be supplanted as a safe haven by crypto currencies?

Hardly. People read such information and continue to believe that gold and cryptocurrencies are substitute assets. They are not. So why are they so often pitched against one another?

Bitcoin and its contemporaries clearly have a role to play, the volume of demand demonstrates this and the technology is powerful. But, that role is not as a replacement for gold as a store of value.

Risk Hedge sums it up saying:

“Despite what the crypto-evangelists will tell you, digital tokens will never and can never replace gold as your financial hedge.”

Risk Hedge provided a great summary of the major flaws and differences in the gold versus crypto debate and the six reasons are listed below.

#1: Cryptocurrencies Are More Similar to a Fiat Money System Than You Think.

The definition of “fiat money” is a currency that is legal tender but not backed by a physical commodity.

Since the United States abandoned the gold standard in the 1970s, this has been the case with all major currencies, including the US dollar.

Ever since then, US money supply has kept increasing, and so has the national debt. In contrast, the dollar’s purchasing power has been on the decline.

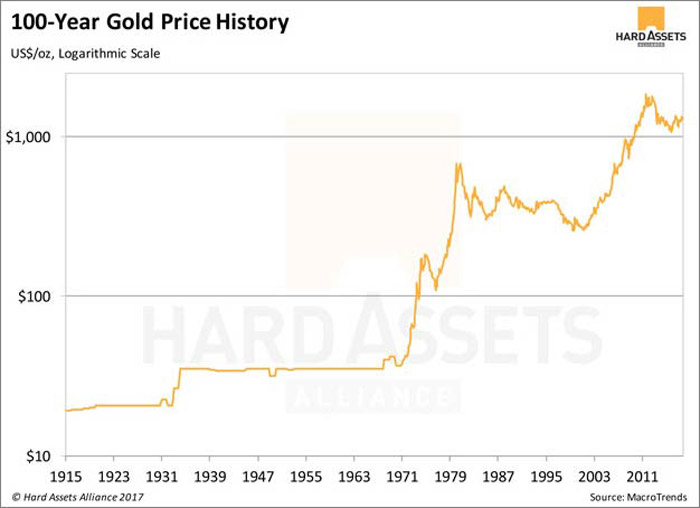

Take a look at this historical gold price chart.

The huge spike in gold prices started right around the time when the Bretton Woods agreement collapsed in 1971 and US paper dollars couldn’t be converted to gold anymore. A clear sign of the decline in the dollar’s purchasing power since the move into a pure fiat money system.

It’s clear that cryptocurrencies partially fit the definition of fiat money. They may not be legal tender yet, but they’re also not backed by any sort of physical commodity. And while total supply is artificially constrained, that constraint is just… well, artificial.

You can’t compare that to the physical constraint on gold’s supply.

Some countries are also exploring the idea of introducing government-backed cryptocurrencies, which would take them one step closer toward fiat-currency status.

As Russia, India, and Estonia are considering their own digital money, Dubai has already taken it one step further. In September, the kingdom announced that it has signed a deal to launch its own blockchain-based currency known as emCash.

So ask yourself, how can you effectively hedge against a fiat money system with another type of fiat money?

#2: Gold Has Always Had and Will Always Have an Accessible Liquid Market.

An asset is only valuable if other people are willing to trade it in return for goods, services, or other assets.

Gold is one of the most liquid assets in existence. You can convert it into cash on the spot, and its value is not bound by national borders. Gold is gold—anywhere you travel in the world, you can exchange gold for whatever the local currency is.

The same cannot be said about cryptocurrencies. While they’re being accepted in more and more places, broad, mainstream acceptance is still a long way off.

What makes gold so liquid is the immense size of its market. The larger the market for an asset, the more liquid it is. According to the World Gold Council, the total value of all gold ever mined is about $7.8 trillion.

By comparison, the total size of the cryptocurrency market stands at about $161 billion as of this writing—and that market cap is split among 1,170 different cryptocurrencies.

That’s a long shot from becoming as liquid and widely accepted as gold.

#3: The Majority of Cryptocurrencies Will Be Wiped Out.

Many Wall Street veterans compare the current rise of cryptocurrencies to the Internet in the early 1990s.

Most stocks that had risen in the first wave of the Internet craze were wiped out after the burst of the dot-com bubble in 2000. The crash, in turn, gave rise to more sustainable Internet companies like Google and Amazon, which thrive to this day.

The same will probably happen with cryptocurrencies. Most of them will get wiped out in the first serious correction. Only a few will become the standard, and nobody knows which ones at this point.

And if major countries like the US jump in and create their own digital currency, they will likely make competing “private” currencies illegal. This is no different from how privately issued banknotes are illegal (although they were legal during the Free Banking Era of 1837–1863).

So while it’s likely that cryptocurrencies will still be around years from now, the question is, which ones? There is no need for such guesswork when it comes to gold.

#4: Lack of Security Undermines Cryptocurrencies’ Effectiveness.

Security is a major drawback facing the cryptocurrency community. It seems that every other month, there is some news of a major hack involving a Bitcoin exchange.

In the past few months, the relatively new cryptocurrency Ether has been a target for hackers. The combined total amount stolen has almost reached $82 million.

Bitcoin, of course, has been the largest target. Based on current prices, just one robbery that took place in 2011 resulted in the hackers taking hold of over $3.7 billion worth of bitcoin—a staggering figure. With security issues surrounding cryptocurrencies still not fully rectified, their capability as an effective hedge is compromised.

When was the last time you heard of a gold depository being robbed? Not to mention the fact that most depositories have full insurance coverage.

#5: Hype and Speculation Continue to Drive Cryptocurrencies’ Value.

Since the beginning of the year, the value of Bitcoin has more than quadrupled—a tremendous spike in value that has sent investors rushing to invest in cryptocurrencies. But could this be nothing more than a market bubble?

One of the world’s most successful hedge fund managers, Ray Dalio of Bridgewater Associates, certainly seems to think so.

In September 2017, he told CNBC, “It’s not an effective store hold of wealth because it has volatility to it, unlike gold. Bitcoin is a highly speculative market. Bitcoin is a bubble.”

The spike in Bitcoin prices seems to only lend credence to this view. With such an extreme degree of volatility, cryptocurrencies’ value as a hedge is questionable. Most people buy them for the sole reason of selling them later at higher prices.

This is pure speculation, not hedging.

#6: Cryptocurrencies Do Not Have Gold’s History as a Store of Value.

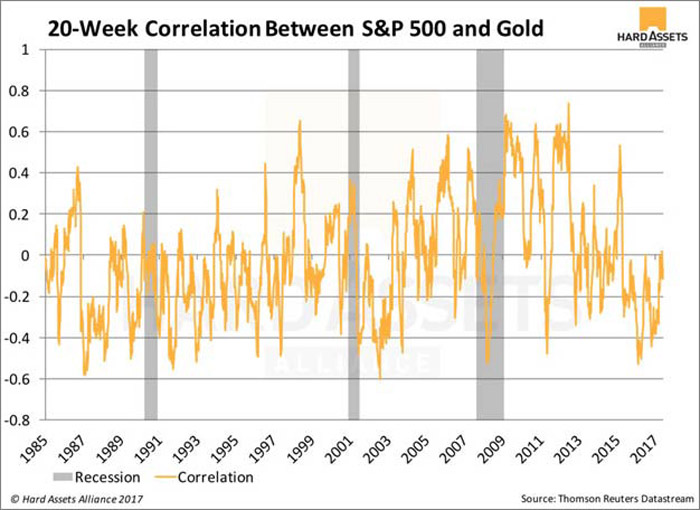

Cryptocurrencies have been around for less than a decade, whereas gold has been used as a store of value for thousands of years. Because of this long history, we know for a fact that stocks and bonds have low or negative correlations with gold, particularly during periods of economic recession. This makes gold a powerful hedge.

What little data we have on cryptocurrencies does not show the same. Consider this year alone: while the US stock market continues to run record highs, the same goes for Bitcoin.

It’s true that gold has also gone up, but the correlation has been very low and, during times of recessions, tends to swing to the negative side, as you can see in the graph below.

Since 2010, there have been 15 times where the S&P 500 has seen drops of 5% or more. Out of those 15 stock market downturns, Bitcoin has been down for 10 of them.

How is that a good hedge?

Read the original article here

Related Content

Millennials Can Punt On Bitcoin, Own Gold and Silver For Long Term

Gold Is Better Store of Value Than Bitcoin – Goldman Sachs

Bitcoin and Gold – Outlook and Safe Haven?

News and Commentary

Gold falls on pressure from stronger dollar, rate hikes in focus (Reuters.com)

Asian Stocks Advance; Dollar, Treasuries Steady (Bloomberg.com)

Gold, Euro Slump As Merkel Admits “New Elections Are The Better Way” (ZeroHedge.com)

Yellen Says She’ll Leave Fed Once Powell Sworn in as Chair (Bloomberg.com)

No EU deposit insurance if bad loans not cut: ECB’s Draghi (Reuters.com)

Source: Bloomberg

Source: Bloomberg

Gold Drops To Key Technical Support After $2 Billion Purge (ZeroHedge.com)

Gold is rising despite threat of higher interest rates – Rickards (DailyReckoning.com)

Thorne, Magic Money, and Cyberbucks: Three pre-Bitcoin monetary experiments (JPKoning.Blogspot.ie)

The Fed Plans For The Coming Recession – Next-Generation Crazy (DollarCollapse.com)

ECB wants to end deposit protection & offer savers ‘appropriate amount’ of their own money (RT.com)

Gold Prices (LBMA AM)

21 Nov: USD 1,280.00, GBP 967.04 & EUR 1,090.69 per ounce

20 Nov: USD 1,292.35, GBP 974.82 & EUR 1,096.43 per ounce

17 Nov: USD 1,283.85, GBP 969.31 & EUR 1,088.19 per ounce

16 Nov: USD 1,277.70, GBP 969.01 & EUR 1,085.53 per ounce

15 Nov: USD 1,285.70, GBP 976.62 & EUR 1,086.29 per ounce

14 Nov: USD 1,273.70, GBP 972.47 & EUR 1,086.59 per ounce

13 Nov: USD 1,278.40, GBP 977.59 & EUR 1,097.89 per ounce

Silver Prices (LBMA)

21 Nov: USD 17.00, GBP 12.85 & EUR 14.50 per ounce

20 Nov: USD 17.15, GBP 12.94 & EUR 14.56 per ounce

17 Nov: USD 17.09, GBP 12.95 & EUR 14.49 per ounce

16 Nov: USD 17.04, GBP 12.92 & EUR 14.48 per ounce

15 Nov: USD 17.12, GBP 13.00 & EUR 14.45 per ounce

14 Nov: USD 16.94, GBP 12.92 & EUR 14.45 per ounce

13 Nov: USD 16.93, GBP 12.93 & EUR 14.53 per ounce

Recent Market Updates

– Money and Markets Infographic Shows Silver Most Undervalued Asset

– Is New Fed Chief A “Swamp Critter Extraordinaire”?

– Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

– Gold Coins and Bars Saw Demand Rise 17% to 222T in Q3

– Prepare For Interest Rate Rises And Global Debt Bubble Collapse

– Platinum Bullion ‘May Be One Of The Only Cheap Assets Out There’

– World’s Largest Gold Producer China Sees Production Fall 10%

– German Investors Now World’s Largest Gold Buyers

– Gold Price Reacts as Central Banks Start Major Change

– Why Switzerland Could Save the World and Protect Your Gold

Gold trading today:

Gold, Bonds, & Yen Surge As US Equity Markets Open

US equity futures were deleriously bid from the moment Europe opened overnight…

But as US equity cash markets opened, ‘risk off’ flows suddenly hit sending Yen, bonds, and gold kneejerking higher…

“Foundation For A Rebound?” – Gold Jumps Above Key Technical Level On Heavy Volume

The last 3 days have been ‘nosiy’ in precious metals markets with gold swinging from the best day in 5 months to the worst day in 4 months and now to another high volume surge, breaking the barbarous relic back its 100-day moving-average…

It sems the 100DMA is a key level with heavy volume being used to push gold futures around it.

UBS asks “Is gold establishing a foundation for a rebound?”

Gold longs rebuild while shorts continue to hesitate

Gold is holding reasonably well near the highs of the range established in the past couple of months. A few macro factors have been supportive of late: the pullback in the dollar, a pause in the rise in US nominal and real rates particularly on the long end, consolidation in equities, and political and fiscal uncertainty in the US. Latest political headlines out of Europe are probably helping at the margins, although currency moves could complicate the impact. Stepping back from near-term developments, it’s worth noting that the gold market’s correction and subsequent consolidation has generally been orderly. The relatively measured unwinding of positions on Comex from the year’s highs reached in September is a reflection of this. Latest CFTC data shows that gold net long positions have been tentatively rebuilding over the past couple of weeks; at 22.33moz, market net length looks relatively lean around 60% of the all-time high, albeit still higher than the 12-month average around 17 moz. The recent build in net positioning was mainly due to gains in gross longs. Although gold shorts increased for the first time in four weeks as of November 14, volumes were very modest.

Gold resilience helps position the market for a rebound up ahead

A combination of resilient longs and hesitant shorts has helped gold form a decent base and enabled prices to climb above some support levels, improving the overall technical picture. As we have previously noted, we think gold’s resilience is in large part due to lingering uncertainty; although macro risks in general are perceived to be lower, there is an acknowledgment that known unknowns and unknown unknowns continue to lurk. Additionally, some seasonal demand is likely also keep gold supported. Bits and pieces of interest are evident out of China, although there seems to be no urgency to stock up for the Lunar New Year holidays which will occur later in February this time around. Market participants have also indicated a preference to hold off until after the FOMC December meeting is out of the way. We think gold’s performance of late and the prospect for further seasonal demand to kick in – albeit with unexceptional volumes – should put gold in a reasonably healthy position for a rebound above $1300 towards the year-end through to early 2018.

LAWRIE WILLIAMS: Russian gold reserves – now 1,800 tonnes and rising

The Russian central bank added another 700,000 ounces of gold (21.8 tonnes) to its gold reserves in October, which now puts it within a whisker of China’s 1,842.6 tonnes with a total holding of 57.9 million ounces – or just over 1,800 tonnes. Given that China is currently reporting zero month by month increases in its reserves (which we believe is not its true gold accumulation position), it looks as though Russia, which has been expanding its gold reserves by around 200 tonnes a year (around 185 tonnes so far this year – with 2 months to go), remains on target to overtake China’s ‘official’ reserve figure by the end of the current year, or early next.

As we have noted here before, we consider the Chinese reports of zero additions to its officially reported gold reserve figure, which has remained static for 12 months, as dubious at the very least. While we don’t think Russia’s gold reserves increases are designed to leapfrog China as the world’s No. 5 national official holder of gold, they will do this if the country continues to add to reserves at the current rate and China continues to report zero increases.

Rather, the Russian gold reserve building programme is in place in part to reduce the nation’s reserve dependence on the U.S. dollar. This is in recognition that the increasingly hostile rhetoric that is arising from the neocon element in the U.S. hierarchy could lead to Russia being cut off from the U.S. financial system as the possibility of economic sanctions being increased, as suggested by U.S. Treasury Secretary Steve Mnuchin, is seen as real. While President Trump may well be disinclined to raise the ante in any U.S. – Russian stand- off, his lack of success in ‘draining the Washington DC swamp’, which still seems to call the tune on U.S. foreign relations policy, suggests Russia’s current policy vis- à-vis gold may be a sensible one.

-END-

Bitcoin Tumbles Then Rebounds After Hackers Steal $31 Million Tethers

The rise in Bitcoin’s price was approaching “warp speed” above $8,200 overnight when, as so often happens, it went into another sharp reversal. After hitting an intra-day high of almost $8,265 in early trading on Tuesday, the price crashed more than $400 to $7,827, its biggest drop since November 13. This time it wasn’t another Dimon-esque rant, or the prospect of another fork (technically, these are bullish) but an old-fashioned theft in another cryptocurrency, Tether. Tether is a controversial crypto-business which provides a wallet service allowing crypto exchanges to store and convert fiat currencies to “safe” tokens (not to be confused with an ICO token) and vice versa.

What an amazing ending to our 3hr live #Tether talk on @jimmysong‘s Channel to learn that $USDT just got hacked for $30 Million. More on that tomorrow, but for now check out the video w/ @Bitfinexed@flibbr & @BTCVIX#Bitcoinhttps://www.youtube.com/watch?v=TerIjELO7IY …pic.twitter.com/rN6I3V0nNO

Tether has a market cap of roughly $673 million and is the world’s nineteenth largest cryptocurrency, based Coinmarketcap.com data. Regarding the theft, Tether alleges that $31MM of USDT tokens (Tethers trading at parity with the dollar) were stolen on 19 November 2017.

From the Tether press release:

Tether Critical Announcement

Yesterday, we discovered that funds were improperly removed from the Tether treasury wallet through malicious action by an external attacker. Tether integrators must take immediate action, as discussed below, to prevent further ecosystem disruption.

$30,950,010 USDT was removed from the Tether Treasury wallet on November 19, 2017 and sent to an unauthorized bitcoin address. As Tether is the issuer of the USDT managed asset, we will not redeem any of the stolen tokens, and we are in the process of attempting token recovery to prevent them from entering the broader ecosystem. The attacker is holding funds in the following address: 16tg2RJuEPtZooy18Wxn2me2RhUdC94N7r. If you receive any USDT tokens from the above address, or from any downstream address that receives these tokens, do not accept them, as they have been flagged and will not be redeemable by Tether for USD.

What is especially troubling, is how easy it was – in retrospect – to “steal” over $30MM worth of cryptos and send them on to a “non-extradition” address. As per Tether’s announcement, the $31MM was simply sent to “an unauthorised Bitcoin address.” While likely futile, the company took steps to recover the loast money: as The Crunch reports:

In response Tether said it has flagged the tokens — meaning that it will track them and prevent the holder from exchanging them through its service — and that it is working to recover them. For partners, the back-end wallet service has been suspended. Tether said it will investigate the incident while it rolls out an update to Omni Core — its software for partners — that will prevent the stolen coins from recirculating into its ecosystem by essentially locking them into the alleged hacker’s wallet.

Where things begin to get murky, is the extent to which there may or may not be a relationship between Tether and another controversial player in the cryptocurrency space, Bitfinex. The latter is the major crypto exchange which was famously hacked in 2016, after which the Bitcoin price fell 20%. The Crunch notes that some crypto players are already expressing concern about a potential “inside job”.

One of the partners that uses Tether is crypto exchange Bitfinex, which itself lost 119,756 bitcoin — then worth $72 million but valued at over $950 million today — in a hack over a year ago. As Coindesk reports, the incident is sure to throw up more questions about the relationship between Tether and the secretive exchange Bitfinex. The duo are rumored to share owners, and have been accused of leaning on each other to manipulate the market. Already, there are theories circulating that suggest this new attack could be an inside job.

This latest hit to Bitcoin is likely to prompt more discussion of the relative advantages of gold versus Bitcoin. In a recent post On Zero Hedge, John Rubino cited an article on the Risk Hedge website “All the Reasons Cryptocurrencies Will Never Replace Gold as Your Financial Hedge” in which security was highlighted as one of the key risks for cryptos.

#4: Lack of Security Undermines Cryptocurrencies’ Effectiveness.

Security is a major drawback facing the cryptocurrency community. It seems that every other month, there is some news of a major hack involving a Bitcoin exchange. In the past few months, the relatively new cryptocurrency Ether has been a target for hackers. The combined total amount stolen has almost reached $82 million.

Bitcoin, of course, has been the largest target. Based on current prices, just one robbery that took place in 2011 resulted in the hackers taking hold of over $3.7 billion worth of bitcoin—a staggering figure. With security issues surrounding cryptocurrencies still not fully rectified, their capability as an effective hedge is compromised. When was the last time you heard of a gold depository being robbed? Not to mention the fact that most depositories have full insurance coverage.

In another recent post, “Doomsday Preppers Are Switching Allegiance From Gold To Bitcoin”, the issue of security was also prominently discussed. However, for preppers, the main issue was what would happen if the grid failed. As we’ve suggested, it’s hardly surprising given Bitcoin’s performance that investors and preppers alike have switched their allegiance towards the pre-eminent crypto-currency. However, more events like this, will only add to the view that there is a place in portfolios (and bunkers) for both. After Bitcoin topped $8200 yesterday, we noted the following amusing comment from currency brokerage ForexTime.

“I find it remarkable and somewhat frightening how, no matter how much Bitcoin is pummeled by sellers, it simply bounces back even stronger.”

We’re not there yet, but the price is already closing in on the pre-theft record high of $8,300 as we write.

And, as Bloomberg adds, the incident is the latest in a long list of hacks which while denting confidence in the security of cryptocurrencies, “typically have fleeting market impact: bitcoin has surged to one record after another during the past few years despite major thefts from exchanges including Bitfinex and Mt. Gox.”

These doomsday preppers are starting to switch from gold to bitcoin

Submitted by cpowell on Mon, 2017-11-20 12:24. Section: Daily Dispatches

By Eddie VanDer Walt

Bloomberg News

Monday, November 20, 2017

Wendy McElroy is ready for most doomsday scenarios: a one-year supply of nonperishable food is stacked in a cellar at her farm in rural Ontario. Her blueprint for survival also depends upon working internet: part of her money, assuming she needs some after civilization collapses, is in bitcoin.

Across the North American countryside, preppers like McElroy are storing more and more of their wealth in invisible wallets in cyberspace instead of stockpiling gold bars and coins in their bunkers and basement safes.

They won’t be able to access their virtual cash the moment a catastrophe knocks out the power grid or the web, but that hasn’t dissuaded them. Even staunch survivalists are convinced bitcoin will endure economic collapse, global pandemic, climate change catastrophes and nuclear war. …

At first glance, it seems counter-intuitive that some of bitcoin’s most ardent proponents are people motivated by the belief that public infrastructure will collapse in times of social and political distress. Bitcoin isn’t yet widely accepted as a method of payment and steep transaction costs make it inconvenient to use at vendors that do take it. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-11-20/can-bitcoin-survive-a..

Zero Hedge: Gold drops to key support after $2 billion purge

Submitted by cpowell on Mon, 2017-11-20 15:35. Section: Daily Dispatches

From Zero Hedge

Monday, November 20, 2017

After surging above its 50-day moving-average on Friday, it appears someone is keen for that key technical level not to hold as they dumped almost $2 billion notional in seconds this morning, testing down to the 50-day moving average.

Fifteen thousand contracts dumped in under two minutes. … But for now the 50-day moving average is holding. …

… For the remainder of the report:

http://www.zerohedge.com/news/2017-11-20/gold-drops-key-technical-suppor…

END

We brought this to your attention yesterday; The raid dropped the gold price right at its 50 day moving average of $1275. This resistance level held

(courtesy zerohedge/GATA)

Zero Hedge: Gold drops to key support after $2 billion purge

Submitted by cpowell on Mon, 2017-11-20 15:35. Section: Daily Dispatches

From Zero Hedge

Monday, November 20, 2017

After surging above its 50-day moving-average on Friday, it appears someone is keen for that key technical level not to hold as they dumped almost $2 billion notional in seconds this morning, testing down to the 50-day moving average.

Fifteen thousand contracts dumped in under two minutes. … But for now the 50-day moving average is holding. …

… For the remainder of the report:

http://www.zerohedge.com/news/2017-11-20/gold-drops-key-technical-suppor..

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.6336/shanghai bourse CLOSED UP AT 18.10 POINTS .53% / HANG SANG CLOSED UP 557.76 POINTS OR 0.21%

2. Nikkei closed DOWN 135.04 POINTS OR 1.91% /USA: YEN RISES TO 112.56

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 94.09/Euro FALLS TO 1.1725

3b Japan 10 year bond yield: RISES TO . +.033/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.56/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.55 and Brent: 62.36

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.352%/Italian 10 yr bond yield DOWN to 1.775% /SPAIN 10 YR BOND YIELD DOWN TO 1.487%

3j Greek 10 year bond yield RISES TO : 5.298???

3k Gold at $1278.21 silver at:16.98: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 40/100 in roubles/dollar) 59.43

3m oil into the 56 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9943 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1659 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.353%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.361% early this morning. Thirty year rate at 2.771% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Bonds, Futures, Global Stocks All Rise, Boosted By “Germany’s Brexit Moment”; TSY Curve Collapse Continues

S&P 500 futures are higher, continuing on yesterday’s momentum, after European and Asian shares also rose alongside a rebound in oil, as the year-end performance chase appears to be accelerating. There were several different moving parts in a mixed European session, in which early Euro strength gave way to weakness…

… which in turn pushed the Stoxx 600 and US index futures higher, rising above yesterday’s session high on negligible volumes.

Global equity futures rallied with Hang Seng futures outperforming and flash smashing to close the session, after a strong finish for Chinese equities following a report out of MNI that Chinese deleveraging may not be as stringent next year.

European stocks rose this morning (Stoxx 600 +0.3%) as the Euro sank, helped by positive notes out from Goldman Sachs, who are overweight European automakers. Goldman said in a Europe strategy note that “deep value sectors” (autos, oil, and utilities) will help Stoxx Europe to return 12% in next 12 months. As a result, European automakers outperform led by VW for a second straight day, with the SXAP index advancing as much as 1.9%, best of 19 groups on the Stoxx Europe 600 benchmark (Volkswagen +3.8%, Porsche +2.7%, BMW +2%, Daimler +1.7%). Additionally, Imperial Brand shares rallied after their CEO change, as analysts speculate that this could increase the likelihood that the company will be taken over by Japan Tobacco. Airliner EasyJet is flying high this morning following strong financial results. Bunds are taking another look at 163.00+ levels having faded rallies above the big figure on several occasions recently.

Stocks have already moved on from this weekend’s German government crisis: German President Frank-Walter Steinmeier said Germany was facing its worst governing crisis in the 68-year history of its post-World War Two democracy and pressed all parties in parliament “to serve our country” and try to form a government.

“The events have already been likened to Germany’s Brexit-moment,” said Daniel van Schoot, an economist at Rabobank. “That is perhaps exaggerated, but the German political situation is now very unpredictable, more than in the past three decades.”

Bonds across the region followed a rise in Treasuries after the

European Central Bank was said to be likely to make only small

adjustments to its guidance on monetary policy next year. EGBs rallied led by gilts which are supported ahead of index extension tomorrow, additionally some focus from European traders on dovish ECB sources piece from yesterday.

The dollar stayed within relatively tight ranges versus its major peers, with average volumes. The euro and the pound edged higher, backed by leveraged interest, only to be capped by their respective 55-DMAs before shedding gains. The Swedish krona led G-10 losses on the back of record low interbank rate fixings, while the Turkish lira pared a drop to an all-time low after the central bank raised borrowing costs. Meanwhile, sterling was steady and gilts advanced amid reports Prime Minister Theresa May has the backing of ministers to offer the European Union more money to break the Brexit deadlock. The Australian dollar dropped to a five-month low after suggestions from the central bank that interest rates will stay lower for longer; EUR/SEK breache’d 10.00 briefly before fading back. Turkey’s lira hit a new record low against the dollar but pared some of the drop after its central bank tightened liquidity, as the standoff between Erdogan and central bank continues.

In overnight central bank announcements, the Bank of England’s Deputy Governor Cunliffe said inflation has been a bit lower than BoE forecast in Autumn and that it’s possible to wait before tightening policy until there is clear evidence that pay growth is responding to unemployment level. Elsewhere, RBA minutes from November 7th meeting stated that any further appreciation in AUD would slow expected pick-up in inflation and the economy. The minutes also stated that there is considerable uncertainty on how fast wages might pick up and add to inflation, while it added that a pass through to inflation may be delayed by many factors. RBA’s Lowe stated that there is ‘not a strong case’ for near-term change in interest rates with the bank paying attention to soft wage growth.

In the U.S., confirmation that Federal Reserve Chair Janet Yellen will leave the board in February creates a fourth vacancy for President Trump to fill, making it trickier for investors to bet on the central bank’s interest rate trajectory next year. While the Thanksgiving holiday gives traders an excuse to pause, equities are heading into the end of the year near their peaks, with investors optimistic about global growth and company earnings.

Meanwhile the collapse in the US Treasury curve continued, with 2s10s moving below 60bps, and screaming inversion as soon as early next year. At the same time, The gap between French and German borrowing costs on Tuesday narrowed to its tightest level since before the euro zone debt crisis of 2010-2012. Germany’s 10-year yield fell two basis points to 0.34%, the lowest in almost two weeks. Britain’s 10-year yield decreased four basis points to 1.257%, the lowest in almost two weeks. Japan’s 10-year yield dipped one basis point to 0.033%, the lowest in more than a week.

Oil prices rose on expectations of an extended OPEC-led production cut, although rising output in the United States capped gains. Brent crude futures were up 0.78 percent to $62.72. West Texas Intermediate crude fell 0.6 percent to $56.09 a barrel. Gold increased 0.3 percent to $1,280.39 an ounce. Copper gained 0.3 percent to $3.13 a pound, the highest in more than a week.

Expected economic data include Chicago Fed National Activity Index and existing home sales. Companies including Medtronic, Lowe’s, Salesforce, Analog Devices, HP Enterprise and HP Inc. are reporting earnings

Bulletin Headline Summary from RanSquawk

- EU bourses firmer this morning with auto names racing away amid a positive note from Goldman Sachs

- FX price action fairly tepid thus far.

- Looking ahead, highlights include US existing home sales, APIs, ECB’s Coeure and Fed’s Yellen

Market Snapshot

- S&P 500 futures up 0.2% at 2,586.75

- STOXX Europe 600 up 0.3% at 387.49

- MSCI Asia up 0.9% to 171.57

- MSCI Asia ex Japan up 1.1% to 565.37

- Nikkei up 0.7% to 22,416.48

- Topix up 0.7% to 1,771.13

- Hang Seng Index up 1.9% to 29,818.07

- Shanghai Composite up 0.5% to 3,410.50

- Sensex up 0.4% to 33,492.20

- Australia S&P/ASX 200 up 0.3% to 5,963.52

- Kospi up 0.1% to 2,530.70

- German 10Y yield fell 1.7 bps to 0.346%

- Euro down 0.08% to $1.1724

- Italian 10Y yield fell 2.7 bps to 1.543%

- Spanish 10Y yield fell 2.4 bps to 1.491%

- Brent futures up 0.8% to $62.69/bbl

- Gold spot up 0.3% to $1,280.53

- U.S. Dollar Index little changed at 94.08

Top Overnight News

- U.K. Prime Minister Theresa May won the backing of ministers on both sides of her divided cabinet to offer the European Union more money to break the Brexit talks deadlock; Barring some major breakthrough, global banks will implement their relocation plans early next year to guarantee they’re able to have new offices inside the EU running by the time the U.K. exits

- German Chancellor Angela Merkel said she’s ready to face voters again to break the country’s political stalemate, betting they won’t blame her for failed talks on forming a coalition

- Germany: FDP chairman reaffirms rejection of four-party talks; SPD reiterates they will not be part of a grand coalition

- Putin held a surprise meeting with Syria’s Bashar al-Assad, kicking off a diplomatic drive this week to outline the terms of an end to the Middle Eastern country’s civil war; Putin will speak by phone with Trump later Tuesday, the Kremlin said

- The ECB is likely to make multiple small adjustments to its guidance on monetary policy next year rather than any major change in language as it ends quantitative easing, according to euro-area officials familiar with the thinking of policy makers

- BOE: Cunliffe says CPI will peak in 4Q 2017, it’s possible to wait before tightening; McCafferty says equilibrium unemployment rate may be below 4.5%

- RBA’s Lowe: no strong case for a near-term adjustment in policy, more likely that next move in rates will be higher; increasingly likely that inflation will be subdued for some time yet

- MNI: PBOC deleveraging campaign may ease somewhat in 2018; PBOC will continue to manage currency and capital controls for at least another decade, according to people familiar

- Turkey Central Bank: has decided to provide all funding from its late liquidity window effective Wednesday, which will raise the weighted average cost of funding by 25bps

- Nestle Is Said to Be Among Potential Hain Celestial Suitors

- AT&T, U.S. Prepare to Battle in Court Over Time Warner Merger

- Cannabis Grower Aurora Plans to Go Hostile With CanniMed Bid

- ECB Is Said Likely to Take Small Steps in QE Exit Guidance

Asian equity markets were higher across the board as the region took the impetus from the positive close on Wall St, with Nikkei 225 (+0.9%) underpinned as exporters benefitted from JPY weakness. The benchmark Japanese index briefly broke above the 22,500 level as stocks coat-tailed on the rebound in USD/JPY, with Toshiba reprieved from yesterday’s slump to sit among the biggest gainers. ASX 200 (+0.3%) also traded with broad-based optimism across its sectors albeit to a lesser extent and Chinese markets completed the upbeat picture following another significant liquidity operation by the PBoC, with the Hang Seng (+1.5%) leading on continued gains in its largest weighted stock Tencent which recently became a member of the exclusive USD 500bln market-cap-club. Finally, 10yr JGBs were relatively flat throughout the session with demand subdued by the broad positive risk tone and a tepid longer-dated enhanced liquidity auction, although a mild uptick was seen in late trade as prices broke above 151.00. PBoC injected CNY 130bln in 7-day reverse repos, CNY 40bln in 14-day reverse repos and CNY 10bln in 63-day reverse repos. Net of maturities, the injection was only CNY 10bn however. PBoC also set the CNY mid-point weaker at 6.6356 vs Prev. 6.6271. Elsewhere, the Japanese Government to cut 30 and 40 year JGB supply in FY 2018/2019.

Top Japanese News;

- Top Fund Backs Tencent to Drive Hong Kong Index Even Higher

- China H Shares Jump to Two-Year High as Financial Firms Rally

- Richest Asian Banker Sees Once-in-Lifetime India Opportunity

- Turkey Lifts Bank-Funding Costs as Lira Weakens to All-Time Low

European equities modestly higher this morning (Stoxx 600 +0.2%), with positive notes out from Goldman Sachs, who are overweight European automakers. Goldman said in a Europe strategy note that “deep value sectors” (autos, oil, and utilities) will help Stoxx Europe to return 12% in next 12 months. As a result, European automakers outperform led by VW for a second straight day, with the SXAP index advancing as much as 1.9%, best of 19 groups on the Stoxx Europe 600 benchmark (Volkswagen +3.8%, Porsche +2.7%, BMW +2%, Daimler +1.7%). Additionally, Imperial Brand shares rallied after their CEO change, as analysts speculate that this could increase the likelihood that the company will be taken over by Japan Tobacco. Airliner EasyJet is flying high this morning following strong financial results. Bunds are taking another look at 163.00+ levels having faded rallies above the big figure on several occasions recently. The bullish fundamentals and flow/positioning motives are well known and documented, but chart-wise market contacts note that support around 162.86 (rising trendline and Monday’s late Eurex base) held on the downside, prompting some intraday buying for a bounce to 163.06 resistance initially and then 163.16 (yesterday’s session peak) vs a high so far at 163.15. Beyond that, 163.22 needs to be breached to expose 163.40 and this month’s 163.63 peak. However, another retreat and failure to retain grasp of the 163.00 handle will bring 162.82 back into play as support (Monday’s actual intraday low), and on a break those short term longs not booking profit at 163.06 are expected to bail. Turning to Gilts, more upside also seen and a return to the 125-plus zone, at 125.29 for a 33 tick gain on the day vs 12 tick loss at one stage, before easing back slightly on larger than forecast UK PSNB shortfalls.

Top European News

- Brexit-Hit Banks Said to Start Moving Staff Abroad in Early 2018

- Paris, Amsterdam Brexit Winners as Coin Toss Assigns EU Agencies

- May Prepares New Brexit Offer After Talks With Ministers

- U.K. Budget Deficit Widens as Inflation Boosts Debt Costs

- Uniper Tells Shareholders to Reject Fortum’s Takeover Offer

- EasyJet Reaping Benefit of Ryanair Retreat as Winter Prices Gain

In FX markets, price action has been relatively contained thus far. The USD index is firmer around the 94.000 handle in thin holiday-impacted trade, with the USD gaining ground vs most major counterparts on a generally more risk-on mood. EUR has been resilient in the face of Germany’s struggles to form a new Government and the threat of another election. EUR/USD continues to find support ahead of stops around 1.1720 and bids at 1.1700, with reported fixing demand in Asia propping the pair, but the 100 DMA around 1.1745-50 capping recovery gains. Elsewhere, AUD has rebounded from overnight lows post-RBA minutes, as Governor Lowe underlined that the next move in rates will be up, although the lead time to any tightening remains lengthy. Meanwhile, GBP was unreactive to the latest public borrowing data as markets look to see whether or not PM May will get the green-light for an enhanced divorce bill offer to the EU.

In commodities, WTI and Brent crude futures have continued to climb through the European session with energy related newsflow on the light-side as prices retrace some of the declines seen in the early stages of yesterday’s session. Energy markets are looking ahead to next week’s OPEC meeting, however, markets are firmly expecting an extension to existing production cuts in lieu of recent rhetoric from the cartel. In metals markets, gold only managed to nurse some of yesterday’s losses overnight as a broad positive risk tone kept safe-haven demand subdued. Copper maintained most of the prior session’s gains with prices supported by the risk appetite and amid gains in Chinese steel and iron ore prices on optimism for increased demand following the winter season.

Looking at the day ahead, central bank speakers will likely be the centre of attention again with Fed Chair Yellen due to speak in the evening as part of a series with former BoE governor Mervyn King, while the ECB’s Coeure chairs a panel in Frankfurt in the afternoon. Datawise, UK public sector net borrowing and CBI trends data for October and November are due, while in the US the Chicago Fed national activity index and existing home sales data for October is due.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0.2, prior 0.2

- 10am: Existing Home Sales, est. 5.4m, prior 5.39m

- 10am: Existing Home Sales MoM, est. 0.19%, prior 0.7%

- 6pm: Fed’s Yellen Speaks at Stern Business School

DB’s Jim Reid concludes the overnight wrap

There wasn’t much contagion yesterday after the surprise collapse in German coalition talks late on Sunday night. Over the last couple of years negative market reaction to political shocks has often been over before you can digest it fully. Examples being the Greek and Brexit referendums and the Trump election results. Although the German coalition talks collapsing is much lower key than these events, it was still interesting that the DAX was only negative for 1 hour 16mins and that the Euro had snapped back into positive territory 37 minutes earlier even if it did soften again as the day progressed closing -0.49% against the dollar. The DAX closed +0.50% (high to low had been as much as +1.23%) and the Stoxx 600 +0.67% (range 0.91%).

Overall it’s hard to see what the solution is to the gridlock in Germany but it’s also hard to see it being that negative for markets other than at the margin. Mrs Merkel yesterday effectively ruled out a minority government and the SPD continue to rule out a return to a Grand Coalition so unless talks can be reignited, a snap election early next year seems increasingly likely. As an outsider not as familiar with the German election process as many of my readers I can’t help wondering how a fresh election will help much with recent polls seemingly not changing that much from the September 24th election. However, perhaps the campaigning would persuade enough voters to change their mind that the coalition math might be easier. Unlikely but possible.

The good news from our economists in Germany is that the political system means there’s no power vacuum and thus no time pressure to progress things. This probably helped prevent the market reacting too negatively yesterday although it can’t be too positive at the margin for Brexit talks and for fresh Macron/ Merkel European initiatives in the near-term. For more on the technicalities and options open now see the note “Coalition talks collapsed – unchartered territory ahead” from our German economists yesterday.

Overnight, the Fed’s Yellen has confirmed that she will be stepping down from the Board of Governors once Mr Powell is sworn into the office. Her vacancy will give President Trump a fourth spot to fill in the new Fed, including the Vice Chairman spot. Elsewhere, Trump has redesignated North Korea as a state sponsor of terrorism and the Treasury department is expected to announce additional sanctions today. Notably, Secretary of State Tillerson “still hopes for diplomacy” with the State. We wonder whether North Korea will retaliate with some form of defiance after this so watch out for that. This morning in Asia, markets have followed the positive lead from the US. The Hang Seng (+1.30%), Nikkei (+0.93%), Kospi (+0.15%) and Shanghai Comp (+0.40%) are all up as we type.

Turning to Brexit headlines, it seems that in addition to the stalemate on UK’s financial settlement to the EU, there are other unresolved issues before talks can move onto trade and a transition deal. Chief EU Brexit negotiator Barnier has noted that the Irish border will require a specific solution and it’s up to “those who wanted Brexit” to come up with those solutions. Elsewhere, he has warned “the legal consequence of Brexit is that the UK financial services providers lose their passport (rights to the EU bloc)”. Also press reports last night suggested that PM May has cabinet approval to double the settlement offer from the current EUR20bln.

Moving onto central bankers’ commentaries now. The ECB’s Draghi reiterated that despite the sound economic recovery, “underlying inflation pressures are still subdued as labour market slack remains significant….(and that we) still need time to translate into dynamic wage growth”. On non-performing loans in the EU bloc, he cautioned that we need to “…work together to cope with this problem….but at the same time doesn’t create the destabilizing effects that people fear”. On Brexit, he noted it was difficult to properly analyse, mainly because “we don’t have yet a precise or even imprecise view of what the negotiating platform will be”. Notably, he said that the Brexit “transition can be managed in a smooth way…but it should be done without compromising over the integrity of the single market”, although “this is easier to be said than done”.

Following on, BOE policy maker Mr Ramsden has warned that Brexit could put the economy in an “unusual” slow down for years. He noted “given the long horizon over which the effects of Brexit could play out, we’re likely to be on the flat part of the saucer for some time”. On his decision to dissent on the recent rate hike, he noted there may be more room for the economy to grow without price gains, noting “…one must pay close attention to any signs that above target inflation is feeding through to second-round effects in domestic costs…so far, that doesn’t seem to be the case”.

Now recapping other markets performance from yesterday. US equities all strengthened, with both the S&P and Nasdaq up c0.1% and Dow up 0.31%. Within the S&P, telco (+0.97%) and financials stocks rebounded and led the gains, with partial offsets from health care and utilities names. European markets were all modestly higher despite the German political instability. Across the region, the Stoxx 600 (+0.67%), DAX (+0.50%) and CAC (+0.40%) rose modestly, while the FTSE 100 was the relative underperformer (+0.12%). The modest risk on bias was evident in volatility measures, with the VIX down for the third consecutive day (-6.8% to 10.65) while the VSTOXX also fell -7.05% after spending only 43 minutes higher at the open.

Over in government bonds, core bond yields were mixed but little changed (UST 10y: +2.3bp; Bunds +0.2bp; Gilts -0.3bp), while peripherals outperformed with Italy and Spanish yields down 3-4bp. Elsewhere, the flattening across the Treasury curve has continued with the 5s30s curve c3bp flatter to 68.8bp, marking a fresh 10 year low.

Turning to currencies, the US dollar index and Sterling gained 0.44% and 0.12% respectively, while Euro fell 0.49% following the aforementioned developments in Germany. In commodities, WTI oil dipped 0.58%, in part as investors await potential confirmation of production cuts in the upcoming OPEC meeting on 30th November. Elsewhere, precious metals weakened (Gold -1.20%;Silver -2.30%), with Gold down the most since late September, while other base metals were mixed (Copper +0.91%; Zinc -0.06%; Aluminium -1.44%).

Away from the markets, DB’s China research team have published another note looking at China’s macro risks. They have noticed new signs of a tightening in fiscal and monetary policies over the past week. For example, on the fiscal front, the Ministry of Finance issued a document to tighten control over public private partnership projects. On monetary front, the government released draft guidelines on the asset management sector, which from a macro perspective could structurally constrain financial leverage and further tighten credit growth. Overall, the team believes these new measures are positive for China in the long term, but in the next 6 months they will likely cause the economy to slow.