GOLD: $1276.90 DOWN $19.70

Silver: $16.93 DOWN 45 cents

Closing access prices:

Gold $1276.90

silver: $16.93

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1296.26 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1291.40

PREMIUM FIRST FIX: $4.86

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1294.99

NY GOLD PRICE AT THE EXACT SAME TIME: $1290.90

Premium of Shanghai 2nd fix/NY:$4.39

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1292.35

NY PRICING AT THE EXACT SAME TIME: $1291.50

LONDON SECOND GOLD FIX 10 AM: $1286.20

NY PRICING AT THE EXACT SAME TIME. 1286.30

For comex gold:

NOVEMBER/

NUMBER OF NOTICES FILED TODAY FOR NOVEMBER CONTRACT: 1 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR: 1052 FOR 105,200 OZ (3.372TONNES)

For silver:

NOVEMBER

3 NOTICE(S) FILED TODAY FOR

15,000 OZ/

Total number of notices filed so far this month: 884 for 4,420,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8100 OFFER /$8125 up $412.00 (MORNING)

BITCOIN : BID $8222 OFFER: $8247 // up $534 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUGE 5,383 contracts from 199,711 UP TO 205,094 WITH RESPECT TO FRIDAY’S TRADING WHICH SAW SILVER RISE BY 24 CENTS AND BREAK THE HUGE $17.25 SILVER RESISTANCE. WE HAD ZERO LONG COMEX LIQUIDATION AND FURTHER WE WERE NOTIFIED THAT WE HAD QUITE A HUMONGOUS NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 1078 DECEMBER EFP’S WERE ISSUED ALONG WITH 0 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 1078 CONTRACTS FOR MONDAY. (THE ISSUANCE FOR MARCH THAT WE HAVE SEEN THESE PAST FEW DAYS BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY IN THE UPCOMING DELIVERY MONTH). I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. THURSDAY WITNESSED 927 EFP’S ISSUED FOR FRIDAY.

RESULT: A HUGE SIZED RISE IN OI COMEX WITH THE 24 CENT PRICE RISE. ZERO COMEX LONGS EXITED OUT OF THE COMEX AND FROM THE CME DATA 1078 EFP’S WERE ISSUED FOR MONDAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.025 BILLION TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

In gold, the open interest SURPRISINGLY ROSE BY A HUMONGOUS 28,707 CONTRACTS WITH THE FAIR SIZED RISE IN PRICE OF GOLD ($10.60) WITH RESPECT TO FRIDAY’S TRADING. WE HAD ZERO COMEX LONGS EXIT THE ARENA. HOWEVER THE TOTAL NUMBER OF GOLD EFP’S ISSUED ON FRIDAY FOR MONDAY TOTALED AN UNBELIEVABLE: 12,711 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 12,711 CONTRACTS AND FEB SAW THE ISSUANCE OF 0 CONTRACTS. ON THURSDAY, WE WITNESSED A TOTAL OF 4394 EFP’S ISSUED THURSDAY FOR FRIDAY. The new OI for the gold complex rests at 561,237. DEMAND FOR GOLD INTENSIFIES DESPITE THE CONSTANT RAIDS. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO METAL!! THIS IS THE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NOT BACKED SILVER (AND GOLD) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING 6 TO 10 WEEKS TO OBTAIN PHYSICAL WHEN FORWARDS ARE DUE.

Result: A HUGE SIZED INCREASE IN OI DESPITE THE FAIR SIZED RISE IN PRICE IN GOLD ON FRIDAY ($10.60). WE HAD A HUGE NUMBER OF COMEX LONG TRANSFERS TO LONDON THROUGH THE EFP ROUTE AS (12,711 EFP’S). THERE OBVIOUSLY DOES NOT SEEM TO BE ANY PHYSICAL AT THE COMEX AS WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER WHICH EXPLAINS THE HUGE ISSUANCE OF EFP’S. WE HAD ZERO GOLD COMEX OI CONTRACTS LEAVE THE COMEX GOLD ARENA.

we had: 1 notice(s) filed upon for 100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

No change in gold inventory at the GLD/

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 318.074 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 5,383 contracts from 199,711 UP TO 205,094 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE CONSIDERABLE RISE IN SILVER PRICE (A GAIN OF 24 CENTS AND THE BREAKING OF THAT HUGE $17.25 RESISTANCE). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE 1078 PRIVATE EFP’S FOR DECEMBER(WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 0 EFP’S FOR MARCH FOR A TOTAL OF 1078 EFP CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THESE EFP ISSUANCE..USUALLY WE WITNESS THIS ONE WEEK PRIOR TO FIRST DAY NOTICE AND THIS CONTINUES RIGHT UP UNTIL FDN. WE ALSO HAD NO AMOUNT OF SILVER COMEX LIQUIDATION.

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 24 CENT GAIN IN PRICE (WITH RESPECT TO FRIDAY’S TRADING). WE HAD ANOTHER 1078 EFP’S ISSUED ,TRANSFERRING OUR COMEX LONGS OVER TO LONDON TOGETHER WITH ZERO SILVER COMEX LIQUIDATION.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 9.49 points or .28% /Hang Sang CLOSED UP 61.27 pts or 0.21% / The Nikkei closed DOWN 135.04 POINTS OR 0.60%/Australia’s all ordinaires CLOSED UP 0.17%/Chinese yuan (ONSHORE) closed UP at 6.6318/Oil UP to 56.44 dollars per barrel for WTI and 61.97 for Brent. Stocks in Europe OPENED GREEN . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6318. OFFSHORE YUAN CLOSED WEAKER TO THE ONSHORE YUAN AT 6.6412 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

South Korea detects an””engine test” at the North Korean Nuclear facility

( zerohedge)

ii)TRUMP DECLARES NORTH KOREA A STATE SPONSOR OF TERROR

( ZEROHEDGE)

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)Xi pledges to strengthen this relationship with Saudi Arabia. Xi has good relations with Iran as well. If conflict breaks out who will they support?

( zerohedge)

4. EUROPEAN AFFAIRS

i)This is a ticking time bomb: ECB is proposing an end to deposit protection:

( GoldCore)

ii)This is the worst case scenario possible as her Jamaica coalition collapses. Therefore a second election is a must and that is something that German citizens will not like and they would send their wrath against Merkel.

The euro sinks badly, but gold holds.

( zerohedge)

iii)Bill Blain on what to expect next with respect to the latest German scenario..basically trouble ahead

( Bill Blain/England/Morning Porridge)

iv)With the ECB monetizing 100% of issuance who needs Government?

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Saudi Arabia

the Saudi corruption probe widens as dozens of military officials have been arrested. The move is obvious: MbS wants to eliminate any threat of a military coup

( zerohedge)

ii)ISRAEL/SUNDAY MORNING

(courtesy zerohedge)

iv)Will Israel navigate across the border into Lebanon? so far I do not think Israel will risk a war

( zerohedge)

v)TURKEY/USA

You will recall that the USA had sanctions on Iran. However the Turkish leadership summoned this guy named Zarrab to accept Iranian oil for gold. The USA is now taking this gold trader to court in the USA for violating USA sanctions and this will certainly implicate the Turkish leadership

down goes the lira and it’s 10 yr bonds which now yield 13%

( zerohedge)

6 .GLOBAL ISSUES

i)Zimbabwe

Zimbabwe’s ruling party has officially ousted Mugabe. However he is still President if he refuses to leave. He will then be impeached:

( zerohedge)

( zerohedge)

iii)Hyperinflation as its finest moment: check on Zimbabwe now:

(courtesy Koning/Bullionstar)

7. OIL ISSUES

Nebraska regulators approve the Keystone pipeline just days after a South Dakota leak.

This will no doubt be challenged in the court

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)As promised, the crooks dumped $2 billion dollars of un backed paper gold to suppress its price

( zerohedge)

ii)Financial times editor Gillian Tett writes that the new futures market for Bitcoin will causes its price suppression in exactly the same form as gold/silver. Chris Powell and zero hedge urges Tett to write about the gold suppression scheme instead of tackling bitcoin

( zerohedge/Gillian Tett/London’s Financial Times/Chris Powell/Gata)

iii)Bitcoin soars above $8,000 on the refusal of Mugabe to resign

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)Global trading:

With the huge amount of negative news throughout last night, somehow the market “reconsidered” the data as the plunge protection team bought everything but gold and silver:

( zerohedge)

ii)Baltimore neighbourhood under lockdown as police have declared Martial law

( zerohedge)

iii)FBI Informant has a video of Russian agents with briefcases of bribe money and this money went to the Clinton’s and the Clinton Foundation

( zerohedge)

iv)My goodness: another USA navy warship crashes

( zerohedge)

v)Stockman slams the USA recovery as a “nothing burger” as well as discuss that the new tax reform bill will accomplish nothing

( David Stockman/ContraCorner)

vi)Next on the list for Amazon to destroy is the health care/pharmacy field

( zerohedge)

END

On Friday night just before closing I stated:

“The way the gold/silver equity shares sold off this afternoon, generally that is the signal for our banker boys to orchestrate a aid on our previous metals on Monday. I receive the preliminary numbers late tonight or early tomorrow morning. If they are extremely high for both metals that would be another indicator for a raid.”

as promised to you, another vicious raid by the crooks was orchestrated..

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY AN ASTOUNDING 28,707 CONTRACTS UP to an OI level of 559,838 DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($10.60 RISE WITH RESPECT TO YESTERDAY’S TRADING). WE DID NOT HAVE ANY GOLD COMEX LIQUIDATION. HOWEVER WE DID HAVE A HUMONGOUS 12,711 COMEX LONGS EXIT THE COMEX ARENA THROUGH THE EFP ROUTE AS THEY RECEIVE A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 12,711 EFPS WERE ISSUED FOR DECEMBER AND 0 WERE ISSUED FOR MARCH. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. DUE TO THE HUGE INCREASE IN OI, THE BANKERS FELT IT OBLIGATORY TO RAID THE COMEX TODAY TRYING TO GET OUR MATHEMATICAL LONGS TO FALL FROM THEIR RESPECTIVE TREE.

Result: a HUGE INCREASE IN OPEN INTEREST DESPITE THE FAIR SIZED RISE IN THE PRICE OF GOLD ($10.60.) A HUGE 12,711 EFP’S ISSUED FOR A FIAT BONUS AND A DELIVERABLE FORWARD GOLD CONTRACT IN LONDON. WE HAD NO COMEX GOLD LIQUIDATION ON FRIDAY.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A LOSS OF 30 CONTRACT(S) FALLING TO 10. We had 31 notices filed YESTERDAY so GAINED 1 contracts or 100 additional oz will stand for delivery AT THE COMEX in this non active month of November. HOWEVER THESE WERE TRANSFERRED TO LONDON FOR POSSIBLE DELIVERY.

The very big active December contract month saw it’s OI SURPRISINGLY GAIN 11,015 contracts UP to 268,091 EFPS. January saw its open interest RISE by 91 contracts UP to 875. FEBRUARY saw a gain of 14,595 contacts up to 212,722. DEMAND FOR GOLD INTENSIFIES.

We had 1 notice(s) filed upon today for 100 oz

VOLUME FOR TODAY : 428,049 (PRELIMINARY)

CONFIRMED VOLUME FRIDAY: 434,888 contracts. (comex volumes are intensifying)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE 5,383 CONTRACTS FROM 199,711 UP TO 205,094 WITH FRIDAY’S FAIR SIZED 24 CENT GAIN IN PRICE AND THE PIERCING OF THAT HUGE RESISTANCE LEVEL OF $17.25 . WE HAD 1078 PRIVATE EFP’S ISSUED FOR DECEMBER AND 0 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THIS IS QUITE EARLY FOR THE ISSUANCE. USUALLY WE WITNESS THIS EVENT ONE WEEK PRIOR TO FIRST DAY NOTICE AND IT CONTINUES RIGHT UP TO FDN. WE HAD ZERO LONG SILVER COMEX LIQUIDATION. THE TOTAL EFP’S ISSUED TODAY TO OUR COMEX LONGS TOTAL 1078 AND THUS DEMAND FOR SILVER INTENSIFIES AGAIN

IN ANOTHER STRANGE PHENOMENA, FOR SOME UNKNOWN REASON THE PRELIMINARY OI FOR SILVER IS LOWER THAN THE FINAL OI. I WISH SOMEONE OUT THERE CAN EXPLAIN THIS!!

The new front month of November saw its OI FALL by 2 contract(s) and thus it stands at 3. We had 5 notice(s) served YESTERDAY so we gained 3 contracts or an additional 15,000 oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FELL by ONLY 3,629 contracts DOWN to 97,984, YET WE HAD 1078 EFP’S ISSUED WHICH MEANS A GOOD PERCENTAGE OF THE ROLLOVERS LANDED INTO EFP’S. January saw A GAIN OF 213 contracts RISING TO 1245.

We had 3 notice(s) filed for 15,000 oz for the NOV. 2017 contract

INITIAL standings for NOVEMBER

Nov 20/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

3697.25

oz

SCOTIA

115 KILOBARS

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

104,107.926

oz

HSBC

|

| No of oz served (contracts) today |

1 notice(s)

100 OZ

|

| No of oz to be served (notices) |

9 contracts

(900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1052 notices

105,200 oz

3.272 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer deposit(s):

i) Into HSBC: 104,107.926 oz

total customer deposits 104.107.926 oz

We had 1 customer withdrawal(s)

i) out of Scotia: 3697.25 oz

Total customer withdrawals: 3697.25 oz ( 155 kilobars)

we had 1 adjustment(s)

i) Out of Scotia: 15,297.480 oz was adjusted out of the dealer and this landed into the customer account of Scotia

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (1052) x 100 oz or 105,200 oz, to which we add the difference between the open interest for the front month of NOV. (10 contracts) minus the number of notices served upon today (1 x 100 oz per contract) equals 106,100 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (1052) x 100 oz or ounces + {(10)OI for the front month minus the number of notices served upon today (1) x 100 oz which equals 106,100 oz standing in this active delivery month of NOVEMBER (3.30 tonnes)

WE GAINED 1 ADDITIONAL CONTRACTS OR 100 OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

THE COMEX GOLD CONTRACT AT AROUND THE SAME TIME AS LAST YEAR: (NOV 22) WE HAD 199,751 GOLD CONTRACTS STANDING AND THIS COMPARES TO 269,755 TODAY . THE DIFFERENCE IS HUGE

ON FIRST DAY NOTICE FOR DECEMBER, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 514,112.106 or 15.999 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,826,580.395 or 274.54 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 80 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

25,083.870oz

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

299,903.780

oz

BRINKS

|

| No of oz served today (contracts) |

3 CONTRACT(S)

(15,000,OZ)

|

| No of oz to be served (notices) |

0 contract

(NIL oz)

|

| Total monthly oz silver served (contracts) | 885 contracts(4,420,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of Scotia: 25,083.870 oz

TOTAL CUSTOMER WITHDRAWAL 25,-83.870 oz

We had 1 Customer deposit(s):

i) Into Brinks:

299,903.780 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: nil oz

we had 0 adjustment(s)

The total number of notices filed today for the NOVEMBER. contract month is represented by 3 contracts FOR 15,000 oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 884 x 5,000 oz = 4,420,0000 oz to which we add the difference between the open interest for the front month of NOV. (3) and the number of notices served upon today (3 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 884 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(3) -number of notices served upon today (3)x 5000 oz equals 4,420,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 3 contract(s) or an additional 15,000 oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE.

AT THIS TIME LAST YEAR WE HAD 56,352 NOTICES STANDING FOR DELIVERY FOR SILVER. THIS YEAR WITH ONE EXTRA DAY: 97,551.

ON FIRST DAY NOTICE FOR THE DECEMBER CONTRACT WE HAVE 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 173,740 867 MILLION OZ OR 123% OF ANNUAL SILVER PRODUCTION

CONFIRMED VOLUME FOR YESTERDAY: 124,967 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 124,967 CONTRACTS EQUATES TO 773 MILLION OZ OR 110% OF ANNUAL GLOBAL PRODUCTION OF SILVER

THE COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 43.817 million

Total number of dealer and customer silver: 231.687 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.9 percent to NAV usa funds and Negative 2.8% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.2%

Percentage of fund in silver:37.5%

cash .+.3%( Nov 20/2017)

2. Sprott silver fund (PSLV): NAV RISES TO -0.87% (Nov 20 /2017)

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.51% to NAV (Nov 20/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.87%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.51%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 20/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 275 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 210 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Nov 17/2017:

Inventory 318.074 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.57%

12 Month MM GOFO

+ 1.78%

30 day trend

end

end

Major gold/silver trading/commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Money and Markets Infographic Shows Silver Most Undervalued Asset

Money and Markets Infographic Shows Silver Most Undervalued Asset

– Silver remains severely under owned and under valued asset

– Entire silver market worth tiny $100 billion shown in one tiny square

– “All of the World’s Money and Markets in One Visualization”

– Must see ‘Money and Markets’ infographic shows relative size of key markets: silver bullion, gold bullion, cryptocurrencies/ bitcoin, largest companies, 50 richest people, Fed balance sheet, currency, stocks, property, cash, debt & derivatives

– Small allocation by investors and world’s richest will see silver surge like bitcoin

Click to enlarge. Source: Visual Capitalist

Click to enlarge. Source: Visual Capitalist

Millions, billions, and trillions…

When we talk about the giant size of Apple, the fortune of Warren Buffett, or the massive amount of global debt accumulated – all of these things sound large, but they are actually extremely different in magnitude.

That’s why visualizing things spatially can give us a better perspective on money and markets.

HOW MUCH MONEY EXISTS?

This infographic was initially created to show how much money exists in its different forms. For example, to highlight how much physical cash there is in comparison to broader measures of money which include saving and checking account deposits.

Interestingly, what is considered “money” depends on who you are asking.

Are the abstractions created by Central Banks really money? What about gold, bitcoins, or other hard assets?

A NEW MEANING

However, since we first released this infographic in 2015, “All the World’s Money and Markets” has taken on a different meaning to us and many others. It’s a way of simplifying a complex universe of currencies, assets, and other financial instruments in a way that people can understand.

Numbers represented in the data visualization range from the size of the above-ground silver market ($17 billion) to the notional value of all derivatives ($1.2 quadrillion as a high-end estimate). In between those two extremes, we’ve added many other familiar measures, such as the GDP of California, the value of equities, the real estate market, along with different money supply metrics to give perspective.

The end result? A visually pleasing, but enlightening new way to understand the vast universe of global assets.

All of the World’s Money and Markets in One Visualization via Visual Capitalist

Related Content

Silver Very Undervalued from Historical Perpective of Ancient Greece

Silver Production Has “Huge Decline” In 2nd Largest Producer Peru

Silver Bullion Prices Set to Soar

News and Commentary

Gold holds near one-month peak despite firmer dollar (Reuters.com)

Euro Drops as German Talks Fail; Asian Stocks Slip (Bloomberg.com)

Fed readiness to raise rates next month and a wariness about next recession (MarketWatch.com)

Bitcoin Soars Past $8,000 as Technology Shift Concern Vanishes (Bloomberg.com)

Gold smugglers now prefer Europe over Gulf countries: Customs (IndiaTimes.com)

Source: Bloomberg

Source: Bloomberg

Prepare to bet against bitcoin as it becomes civilised – Tett (FT.com)

Gold Price Suppression – Zero Hedge invites Financial Times to heed GATA (ZeroHedge.com)

Gold Versus Bitcoin: The Pro-Gold Argument Takes Shape (GoldSeek.com)

Upsurge in big earthquakes predicted for 2018 as Earth rotation slows (ZeroHedge.com)

Arab League Holds Emergency Session: Iran And “Terrorist” Hezbollah Must Be Stopped (ZeroHedge.com)

Gold Prices (LBMA AM)

20 Nov: USD 1,292.35, GBP 974.82 & EUR 1,096.43 per ounce

17 Nov: USD 1,283.85, GBP 969.31 & EUR 1,088.19 per ounce

16 Nov: USD 1,277.70, GBP 969.01 & EUR 1,085.53 per ounce

15 Nov: USD 1,285.70, GBP 976.62 & EUR 1,086.29 per ounce

14 Nov: USD 1,273.70, GBP 972.47 & EUR 1,086.59 per ounce

13 Nov: USD 1,278.40, GBP 977.59 & EUR 1,097.89 per ounce

10 Nov: USD 1,284.45, GBP 976.44 & EUR 1,102.19 per ounce

Silver Prices (LBMA)

20 Nov: USD 17.15, GBP 12.94 & EUR 14.56 per ounce

17 Nov: USD 17.09, GBP 12.95 & EUR 14.49 per ounce

16 Nov: USD 17.04, GBP 12.92 & EUR 14.48 per ounce

15 Nov: USD 17.12, GBP 13.00 & EUR 14.45 per ounce

14 Nov: USD 16.94, GBP 12.92 & EUR 14.45 per ounce

13 Nov: USD 16.93, GBP 12.93 & EUR 14.53 per ounce

10 Nov: USD 17.00, GBP 12.92 & EUR 14.60 per ounce

Recent Market Updates

– Is New Fed Chief A “Swamp Critter Extraordinaire”?

– Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

– Gold Coins and Bars Saw Demand Rise 17% to 222T in Q3

– Prepare For Interest Rate Rises And Global Debt Bubble Collapse

– Platinum Bullion ‘May Be One Of The Only Cheap Assets Out There’

– World’s Largest Gold Producer China Sees Production Fall 10%

– German Investors Now World’s Largest Gold Buyers

– Gold Price Reacts as Central Banks Start Major Change

– Why Switzerland Could Save the World and Protect Your Gold

– Invest In Gold To Defend Against Bail-ins

Gold trading today:

As promised, the crooks dumped $2 billion dollars of un backed paper gold to suppress its price

(courtesy zerohedge)

Gold Drops To Key Technical Support After $2 Billion Purge

After surging above its 50-day moving-average on Friday, it appears someone is keen for that key technical level not to hold as they dumped almost $2 billion notional in seconds this morning, testing down to the 50DMA (but holding for now).

15,000 contracts dumped in under two minutes… but for now the 50DMA is holding…

The Dollar Index has been flying around after the Merkel headlines over the weekend…

end

Financial times editor Gillian Tett writes that the new futures market for Bitcoin will causes its price suppression in exactly the same form as gold/silver. Chris Powell and zero hedge urges Tett to write about the gold suppression scheme instead of tackling bitcoin

(courtesy zerohedge/Gillian Tett/London’s Financial Times/Chris Powell/Gata)

Zero Hedge invites Financial Times to heed GATA’s urging on gold suppression

Submitted by cpowell on Sat, 2017-11-18 17:51. Section: Daily Dispatches

12:56p ET Saturday, September 18, 2017

Dear Friend of GATA and Gold:

Last night Zero Hedge called attention to Friday’s column by Gillian Tett of the Financial Times, to which GATA also had called attention —

http://www.gata.org/node/17808

— in which Tett speculated, as many in the gold sector have done, that the futures market being planned in bitcoin by CME Group would tend to suppress the cryptocurrency’s price.

Of course the use of futures markets to suppress gold and commodity prices has been one of GATA’s themes for a long time, and a theme of the British economist Peter Warburton for even longer:

So Zero Hedge concluded its post last night by suggesting that Tett now pursue the gold price suppression angle, noting that GATA has been urging just that on the FT for quite a while.

Zero Hedge wrotes: “According to the Reserve Bank of India’s estimate, the ratio of ‘paper gold’ trading to physical gold trading is 92 to 1, meaning that the price of gold on the screens has almost nothing to do with the buying and selling of physical gold.

“This makes the gold market and, therefore, the gold price something of a mockery. As Zero Hedge has highlighted time after time, the gold price has frequently been subject to waterfall declines, as huge volumes of gold futures are dumped on the market with no regard for price. …

“Perhaps the FT journalist, Gillian Tett, could write an article on gold, instead of bitcoin, explaining how the price of the former — a widely viewed indicator of financial risk — is being suppressed by derivative trading. Indeed, Tett was present at a private dinner in Scott’s of Mayfair several years ago when the Gold Anti-Trust Action Committee gave a presentation on exactly the same process she expects to lower the bitcoin price.”

Zero Hedge’s commentary is headlined “Financial Times: Sell Bitcoin Because the Market Is about to Become ‘Civilized'” and it’s posted here:

http://www.zerohedge.com/news/2017-11-17/financial-times-sell-bitcoin-be…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Our monetary metals gold and silver are holding up rather well despite the constant raids

(courtesy Sprott/GATA)

Monetary metals holding up well despite raids, Sprott says

Submitted by cpowell on Sun, 2017-11-19 16:19. Section: Daily Dispatches

11:23a ET Sunday, November 19, 2017

Dear Friend of GATA and Gold:

Mining entrepreneur Eric Sprott, just back from Australia, was interviewed Friday by Craig Hemke for Sprott Money and reflected on last week’s activity in the monetary metals. Sprott says bitcoin is making currencies look weak even as gold and silver suffer short-selling in the futures markets, but the monetary metals are holding up well despite the raids against them.

Sprott adds that the U.S., U.K., and Canadian economies are far weaker than generally portrayed, with real wages stagnant and more inflation than government data admits. In these circumstances, Sprott says, increases in interest rates would not make much sense.

The interview is 10 minutes long and can be heard at the Sprott Money internet site here:

https://soundcloud.com/sprottmoney/sprott-money-news-weekly-wrap-up-1117…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

You can now pay for goods in gold with this new gold based debit card

(Dunkley/London’s Financial Times/GATA)

Gold-based debit card Glintpay gets started

Submitted by cpowell on Sun, 2017-11-19 18:15. Section: Daily Dispatches

Glint App Brings Gold into the Digital Age

By Emma Dunkley

Financial Times, London

Sunday, November 19, 2017

The world’s oldest currency is being brought into the digital age with the launch of a debit card and app that will allow people to pay for goods in gold.

Fintech group Glint (http://glintpay.com) has teamed up with Lloyds Banking Group in the UK and MasterCard to create an app that enables people to load credit in various currencies, which can then be used to buy a portion of a physical gold bar. Customers use the app at the checkout to select whether to pay in a currency or gold, before transacting with their MasterCard.

… The development marks the first time people in the UK and overseas can own just a portion of a gold bar through an app, which can then be used in mobile and debit card-based payments. The app also allows people to send gold to peers in the form of a digital payment. …

Glint’s new service is riding the wave of alternative payments, such as bitcoin, as more people seek payment methods that can store value in a way that differs from traditional currencies.

Ben Davies, a co-founder of Glint, said: “We want to create a fairer form of money whereby we give you choice and control over how you protect your money in an era where central banks issue more currency, and so the value of your currency is falling.”

Glint is working with Lloyds in the UK as the deposit holder for customers storing money on their app. When a customer decides to buy gold through the app, this is used to purchase part of a gold bar that is physically allocated in vaults in Switzerland. …

… For the remainder of the report:

https://www.ft.com/content/cb177256-cd1b-11e7-9dbb-291a884dd8c6

END

Golden Catalysts

Authored by James Rickards via The Daily Reckoning,

The physical fundamentals are stronger than ever for gold.

Russia and China continue to be huge buyers. China bans export of its 450 tons per year of physical production.

Gold refiners are working around the clock and cannot meet demand.

Gold refiners are also having difficulty finding gold to refine as mining output, official bullion sales and scrap inflows all remain weak.

Private bullion continues to migrate from bank vaults at UBS and Credit Suisse into nonbank vaults at Brinks and Loomis, thus reducing the floating supply available for bank unallocated gold sales.

In other words, the physical supply situation has been tight as a drum.

The problem, of course, is unlimited selling in “paper” gold markets such as the Comex gold futures and similar instruments.

One of the flash crashes this year was precipitated by the instantaneous sale of gold futures contracts equal in underlying amount to 60 tons of physical gold. The largest bullion banks in the world could not source 60 tons of physical gold if they had months to do it.

There’s just not that much gold available. But in the paper gold market, there’s no limit on size, so anything goes.

There’s no sense complaining about this situation. It is what it is, and it won’t be broken up anytime soon. The main source of comfort is knowing that fundamentals always win in the long run even if there are temporary reversals. What you need to do is be patient, stay the course and buy strategically when the drawdowns emerge.

Where do we go from here?

There are many compelling reasons why gold should outperform over the coming months.

Deteriorating relations between the U.S. and Russia will only accelerate Russia’s efforts to diversify its reserves away from dollar assets (which can be frozen by the U.S. on a moment’s notice) to gold assets, which are immune to asset freezes and seizures.

The countdown to war with North Korea is underway, as I’ve explained repeatedly in these pages. A U.S. attack on the North Korean nuclear and missile weapons programs is likely by mid-2018.

Finally, we have to deal with our friends at the Fed. Good jobs numbers have given life to the view that the Fed will raise interest rates next month. The standard answer is that rate hikes make the dollar stronger and are a head wind for the dollar price of gold.

But I remain skeptical about a December hike. As I explained above, the market is looking in the wrong places for clues to Fed policy. Jobs reports are irrelevant; that was “mission accomplished” for the Fed years ago.

The key data are disinflation numbers. That’s what has the Fed concerned, and that’s why the Fed might pause again in December as it did last September.

We’ll have a better idea when PCE core inflation comes out Nov. 30.

Of course, the Fed’s main inflation metric has been moving in the wrong direction since January. The readings on the core PCE deflator year over year (the Fed’s preferred metric) were:

January 1.9%

February 1.9%

March 1.6%

April 1.6%

May 1.5%

June 1.5%

July 2017: 1.4%

August 2017: 1.3%

September 2017: 1.3%

Again, the October data will not be available until Nov. 30.

The Fed’s target rate for this metric is 2%. It will take a sustained increase over several months for the Fed to conclude that inflation is back on track to meet the Fed’s goal.

There’s obviously no chance of this happening before the Fed’s December meeting.

A weak dollar is the Fed’s only chance for more inflation. The way to get a weak dollar is to delay rate hikes indefinitely, and that’s what I believe the Fed will do.

And a weak dollar means a higher dollar price for gold.

Current levels look like the last stop before $1,300 per ounce. After that, a price surge is likely as buyers jump on the bandwagon, and then it’s up, up and away.

Why do I say that?

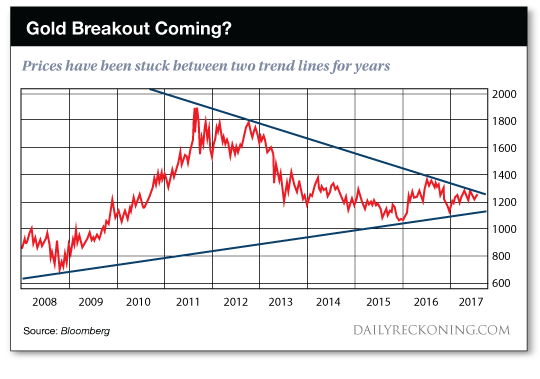

There’s an old saying that “a picture is worth a thousand words.” This chart is a good example of why that’s true:

Gold analyst Eddie Van Der Walt produced this 10-year chart for the dollar price of gold showing that gold prices have been converging into a narrow tunnel between two price trends – one trending higher and one lower – for the past six years.

This pattern has been especially pronounced since 2015. You can see gold has traded up and down in a range between $1,050 and $1,380 per ounce. The upper trend line and the lower trend line converge into a funnel.

Since gold will not remain in that funnel much longer (because it converges to a fixed price) gold will likely “break out” to the upside or downside, typically with a huge move that disrupts the pattern.

At the extreme, this could imply a gold price on its way to $1,800 or $800 per ounce. Which will it be?

The evidence overwhelmingly supports the thesis that gold will break out to the upside. Central banks are determined to get more inflation and will flip to easing policies if that’s what it takes.

Geopolitical risks are piling up from North Korea, to Saudi Arabia, to the South China Sea and beyond.

The failure of the Trump agenda has put the stock market on edge and a substantial market correction may be in the cards. Acute shortages of physical gold have also set the stage for a delivery failure or a short squeeze.

Any one of these developments is enough to send gold soaring in response to a panic or as part of a flight to quality. The only force that could take gold lower is deflation, and that is the one thing central banks will never allow. The above chart is one of the most powerful bullish indicators I’ve ever seen.

Get ready for an explosion to the upside in the dollar price of gold. Make sure you have your physical gold and gold mining shares before the breakout begins.

end

Bitcoin soars above $8,000 on the refusal of Mugabe to resign

(courtesy zerohedge)

Bitcoin Soars To Record High Above $8000 After Mugabe Speech

With Bitcoin trading at $13,499 on Golix, the chaotic environment in Zimbabwe has spread to the global price of the cryptocurrency driving it beyond $8000 for the first time in history as President Mugabe fails to resign in a national address following the nation’s coup.

It appears many Zimbabweans have found an alternate way to store/transfer wealth away from Mugabe’s prying (and confiscatory) eyes.

In September we noted the hyperbitcoinization occurring in Zimbabwe. In October, Zimbabwe demand started to impact the global price of the cryptocurrency, and two weeks ago we noted the doubling of the price of Bitcoin in Zimbabwe as uncertainty about the nation’s stability sent citizens into a decentralized currency that was out of Mugabe’s reach.

image courtesy of CoinTelegraph

Now, after the ‘successful’ military coup but failure of Mugabe to resign – as expected – Bitcoin is trading at over $13,499 on Zimbabwe exchange Golix – a premium of over 80% over the USD exchange price as demand surged.

As CoinTelegraph reports, the Zimbabwean army assaulted Harare on November 14 following a week of confrontation with the administration of President Robert Mugabe. According to the army, the move was aimed at preventing an expected violent and deadly civil war in the country. Mugabe has been the country’s head since 1980.

Due to the political crisis, the demand for Bitcoin in the country has skyrocketed to new highs because of a shortage of hard currency. The situation was exacerbated by the lack of national currency in Zimbabwe. In 2009, the country’s government adopted several fiat currencies like the US dollar and South African rand as a legal tender after hyperinflation turned the local dollar virtually worthless.

According to Golix, it has processed over $1 million worth of transactions in the past 30 days, a sharp increase from its turnover of $100,000 for the entire year of 2016.

According to Golix co-owner Taurai Chinyamakobvu, the prices for Bitcoin are determined by supply and demand. The sellers of the digital currency are paid in US dollars that are deposited electronically. The money, however, can only be converted into hard cash at a sizeable discount on the black market.

On November 15, an “electronic” dollar can purchase around eight South African rands, compared with the market exchange rate of 14.32 rands.

image courtesy of CoinTelegraph

According to a local trader, bitcoin isn’t just being bought by individuals, but by businesses with bills to pay.

Bitcoin, as every bitcoiner would expect, is helping people in the country survive times of economic uncertainty, as Zimbabwe has been embroiled in a crisis for years.

* * *

As CoinTelegraph noted previously, Zimbabwe is beginning to act like an interesting case study for what happens when a country begins to collapse around its monetary system – it is also being witnessed in Venezuela.

Moving money out of Zimbabwe is starting to become impossible, and as people try and flee monetarily out of the crumbling state, they are finding refuge in Bitcoin.

Soon, banks in Zimbabwe have stated that Visa debit cards would no longer be usable for international payments without prior arrangements and pre-funding with hard currency.

“You will be required to make prior limit arrangements with the bank,” Stanbic said in a message to depositors last week.

Econet Wireless has also stopped foreign payments on its MasterCard linked EcoCash mobile money debit card.

Bitcoin as a refuge

Because of the decentralized nature of Bitcoin, there is no impact on it from this political upheaval, in fact, it is only benefiting from it. The Bitcoin premium of almost 100 percent is not because of the political issues, rather the high demand surrounding worry of collapse.

Bitcoin again shows its potential and power when the banking system again shows its potential for mass collapse and hysteria.

end

Wow@@!! only 39% think that Bitcoin price is in a bubble

(courtesy zero hedge)

As Bitcoin Tops $8,200, Only 39% Of Survey Respondents Say It’s A Bubble

Having first surged above $8000 overnight amid Zimbabwe’s chaos, it appears uncertainty in the core of Europe has driven further demand for cryptocurrencu protection, sending Bitcoin to a new record high of $8247 – up 50% from the ‘Bitcoin Cash’ crash weekend lows.

image courtesy of CoinTelegraph

As CoinTelegraph reports, the latest milestone for Bitcoin, which came following news the first Bitcoin-to-Litecoin Lightning Network ‘atomic swap’ successfully debuted, caps its comeback after Bitcoin Cash volatility.

BTC currently has a market cap of almost $134 bln against a cross-crypto combined cap of just under $240 bln, both numbers representing new records.

Bitcoin’s dominance has also recovered over the past few days to top 56 percent of the market after struggling to maintain supremacy as BCH caused considerable fluctuations.

BCH itself has come down off previous highs to languish around $1,200 – around 50 percent of its best prices. Staunch proponents of the Bitcoin fork as the ‘real Bitcoin’ are currently locked in a forking battle of their own as two strands of BCH emerged last week.

The product of a “malicious fork,” Bitcoin Clashic now represents the original Bitcoin Cash or developers describe it, “Satoshi’s true vision.”

As major supporter Roger Ver’s Bitcoin.com continues to point new users towards BCH, however, the Bitcoin community is coming out in increasing support of naive newcomers potentially unaware that BCH is not in fact Bitcoin.

Welcome to Bitcoin, newcomers! Here’s your FAQ:

Q: Who should I trust?

A: Nobody.Q: When should I sell?

A: Never.Q: Is Bitcoin dying because ____?

A: No.Q: What have I gotten myself into?

A: Nobody knows.Q: How do I learn more?

A: https://lopp.net/bitcoin.html

For once the rest of the crypto space is not being sold to fund Bitcoin buys…

“The inflation in this thing is massive,” Luke Hickmore, a senior investment manager at Aberdeen Standard Investments in London, said in an interview with Bloomberg TV.

“When will it collapse? Who knows. It will cause a lot of pain.”

But there are some traders who are noting the worrying divergence between price action and volume in the latest surge…

“I find it remarkable and somewhat frightening how, no matter how much Bitcoin is pummelled by sellers, it simply bounces back even stronger,” said Lukman Otunuga, an analyst at currency brokerage ForexTime Ltd.

“Will bitcoin hit $10,000 before year end? This is the question every investor is asking.”

A recent survey by Nicholas Colas at DataTrek Reserach, done in conjunction with Triad Securities Corp…

The results of our bitcoin survey are in! We got over 300 responses, and there are three key takeaways from the data.

First, less than half of respondents (39%) think bitcoin is a bubble.

Second, there are still plenty of fence sitters, with more individuals who have considered a purchase than already invested.

Lastly, the median estimate for where bitcoin will end the year is below where it trades today ($7,800). Apparently Santa Claus rallies haven’t reached the crypto currency world just yet.

Here is a summary of the results and our comments:

Question: Where will bitcoin close the year (2017)?

- Average response: $7,381

- Median response: $7,800

- Standard Deviation of Responses: $2,555

Our comments: As expected, we had a wide range of responses here.Overall, the wisdom of this particular crowd says bitcoin may be range-bound through the end of the year. Still, with a standard deviation of $2,500, it could top $10,000 or drop close to $5,000 and still be within one sigma of the distribution.

Question: Where is bitcoin going?

- This is a bubble – it must crash: 39.4%

- Continue to rise at a much slower pace: 27.1%

- Value doubles in the next 6 months or sooner: 16.4%

- Don’t know/no opinion: 17.0%

Our comments: we were surprised the bubble response was less than 40% given widespread commentary in that direction and the age/experience of the respondents. By age, at least, our survey takers has seen their fair share of bubbles. We were ready to see +70% responses indicate bitcoin’s price is unsustainable. Less than 40% is, well, remarkable.

“Have you ever bought bitcoin or other crypto currencies?”

- Yes, but only in the last 6 months: 14.5%

- Yes, and I have been involved for +6 months: 16.7%

- No, never: 30.9%

- No, but I have considered it: 36.3%

- No, and I am unfamiliar with bitcoin/cryptos: 1.6%

Our comments: there are still plenty of fence sitters here, with those who have considered purchasing (36%) outnumbering those that have bought (31%). The big question is if they are waiting for a pullback, or further gains?

“Would you ever see bitcoin as a safe haven similar to gold?”

- Yes: 40.7%

- No: 42.9%

- Don’t know, no opinion: 16.4%

Our comments: this may be the most surprising finding of the survey. Even with widely reported wallet hacks and other systematic challenges, 41% of respondents think bitcoin can become something akin to gold as an investment safe haven.

Do you see bitcoin as a hedge against monetary policy?

- Yes: 39.1%

- No: 43.2%

- Don’t know/no opinion: 17.7%

Our comments: almost as surprising as the gold question, these responses show a sizeable minority believe bitcoin’s algorithm-driven limited supply can act as a non-correlated buffer against central bank policy.

Have you ever participated in an Initial Coin Offering or looked at such opportunities?

- Yes, and I have invested: 7.9%

- No, but I have considered investing: 29.0%

- No, and I won’t without more regulation: 14.8%

- No, and I have not looked at these offerings: 48.3%

Our comments: over a third of respondents have looked at or invested in ICOs. Not bad for a fund raising approach that is just a few years old. And over half might consider ICOs if/when the regulatory framework improves.

If you look at ICOs, how do you assess these opportunities?

- The three most popular answers, in order: Founders/Key Employees, Total Addressable Market, and Sector Addressed

- Less popular: Token type, Deal Pricing and Time to Market

Our comments: no surprise here, with ICO investors looking at exactly the same issues as venture capitalists.

What is your level of confidence in current bitcoin custodial offerings?

- High: 9.1%

- Medium: 29.7%

- Low: 25.9%

- Don’t know/no opinion: 30.0%

- I prefer traditional custodians: 5.4%

Our comments: this is a critical issue for institutional investors. In order for crypto currencies to achieve true “Asset class” status, investor confidence in custodial solutions has to improve.

What is your level of confidence in crypto asset liquidity?

- High: 7.9%

- Medium: 39.7%

- Low: 31.2%

- Don’t know/no opinion: 21.1%

Our comments: same thoughts here as the previous point. While respondents may feel marginally better about crypto liquidity, over half rate their confidence here as low or they just don’t know enough to judge.

Our final thoughts on the data presented:

- Institutional investors are taking bitcoin/cryptos seriously. If you’ve ever run an in-depth survey, you know getting 300 responses is difficult. The fact that we got even more shows there is tremendous interest in bitcoin and crypto currencies.

- Initial Coin Offerings are getting real attention as well. Investors already understand the due diligence process here – it is the same as venture-stage investing. Custody and liquidity across the crypto space do need to improve, however.

- A sizeable minority of respondents (39 – 40%) see bitcoin as a potential analog to physical gold, both as a safe haven and a hedge against mistakes in central bank monetary policy. Until blockchain technology becomes more widespread, that is probably the best way to consider buyers’ motivation for bitcoin.

|

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.6318/shanghai bourse CLOSED UP AT 9.49 POINTS .28% / HANG SANG CLOSED UP 61.27 POINTS OR 0.21%

2. Nikkei closed DOWN 135.04 POINTS OR 0.60% /USA: YEN RISES TO 112.21

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 93.78/Euro FALLS TO 1.1779

3b Japan 10 year bond yield: RISES TO . +.038/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.21/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.24 and Brent: 61.97

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.360%/Italian 10 yr bond yield UP to 1.829% /SPAIN 10 YR BOND YIELD UP TO 1.548%

3j Greek 10 year bond yield RISES TO : 5.263???

3k Gold at $1291.95 silver at:17.19: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 40/100 in roubles/dollar) 59.43

3m oil into the 56 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.21 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9909 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1674 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.360%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.339% early this morning. Thirty year rate at 2.777% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

What German Political Turmoil? Global Markets BTFD, Don’t Look Back

US index futures are unchanged, having recovered virtually all overnight session losses alongside the EURUSD following Merkel’s failure to form a government, while European shares rise despite Angela Merkel’s failure to form a new government. In the span of just hours, the goalseeked “hot take” consensus was that Germany’s collapsed coalition talks aren’t expected be a deal breaker for European equities due to the “strength of the German economy.”

As we pointed out earlier, the euro reversed losses as the London session unwound a sell-off in Asian time exacerbated by thin liquidity, while early strength in bunds was also faded. According to Citi, there were 3 possible reasons for the brief dip and subsequent strong rebound: 1. Merkel’s failure was already discounted; 2. The market was positioned short ahead of the announcement; 3. There is too little clarity to trade.

The Bloomberg Dollar Spot Index shed gains and stood little changed as the pound found a steady bid amid optimism that the U.K. is willing to move toward EU demands on a Brexit divorce bill.

The Stoxx Europe 600 Index rose as Germany’s DAX rebounded from a seven-week low; the Stoxx 600 rose 0.3% while Germany’s benchmark DAX Index climbed 0.2%; DAX futures earlier were down nearly -1%, on concerns surrounding the failed coalition talks in the country. Among European stocks, Automakers and health-care shares outperform after Volkswagen raised sales forecasts, while insurers are worst decliners on the European gauge. European equity traders and analysts say that the political uncertainty in Germany will likely not serve as a trigger for a broader market correction.

Still, some were concerned: “You can imagine this will be bearish for the euro, at least in the tactical near-term, while the market comes to grips with what’s going on and will take a look at what her options are,” Kay Van-Petersen, global macro strategist at Saxo Capital Market, said in an interview with Bloomberg Television. “I’m fairly confident though that she’ll be able to come up with a different coalition at some point over the next few weeks.”

Asia began the week subdued following the losses on Wall St. last Friday and with focus on political uncertainty after Trump campaigners were subpoenaed and German coalition talks broke down. Japanese sentiment was dampened by a firmer JPY and a miss on trade data. Hang Seng (+0.3%) and Shanghai Comp. (+0.3%) were initially negative with underperformance in the mainland as Shenzhen stocks resumed Friday’s sell off and amid reports that China tightened asset management rules to curb risky lending. However, prices then recovered heading into the close as markets took a closer look at plans to curb shadow banking. Finally, 10yr JGBs were uneventful with prices flat, as demand from the dampened risk appetite in the region was counterbalanced by the absence of a BoJ Rinban announcement.

The recent pause in the relentless global rally which only cost central banks $2 trillion in liquidity in 2017 comes as investors gauge whether there are sufficient drivers to continue the march to historic highs. Solid earnings are offset by record valuations in virtually all markets, meanwhile red warning signs are being issued by the flattening U.S. yield curve: on Friday, the 2s10s again hit the tightest level in a decade, adding to concern about the pace of future economic growth.

On the domestic agenda where recent euphoria was boosted by the momentum of GOP tax reform, over the weekend, Treasury Secretary Steven Mnuchin said he can’t guarantee Congress would preserve tax cuts (let Congress pass them first before worrying about preserving them), while Senator Susan Collins said the Senate tax plan passed by Committee needs work.

In international geopolitics, German coalition talks broke down after FDP pulled out of discussions with German Chancellor Merkel’s conservatives due to unrealistic differences. S&P affirmed Switzerland at AAA; Outlook Stable and affirmed Netherlands at AAA; Outlook Stable. UK Chancellor Hammond stated that UK is on the brink of serious progress in Brexit discussions, while he also stated the UK will finally begin to see a reduction in public debt and that they will seek to curb health service measures in a balanced way. Reports further suggested that Hammond has put PM May under pressure to promise more money for the Brexit “divorce bill” by suggesting an improved offer will be made to Brussels within three weeks; an offer that the Times believe will be unveiled today.

The dollar was steady, while West Texas oil held above $56 a barrel. Meanwhile, pound and gilts traders will focus on a potential downgrade to the U.K. growth outlook this week and the government’s efforts toward agreeing a Brexit divorce bill. Sterling was boosted on Monday by reports that the U.K. was preparing to make an enhanced divorce bill offer to the EU ahead of crucial talks starting next month.

South Korea spy agency says North Korea can conduct nuke test at anytime, although there is no sign of an imminent test according to reports in Yonhap, reports also suggest that the North conducted engine tests.

This week may see lower than normal volumes due to the Thanksgiving holiday in the U.S. Minutes from the Reserve Bank of Australia’s November meeting are due Tuesday, while those from the European Central Bank’s October meeting due out on Thursday could show dissent in the discussion about tapering. Federal Reserve Chair Janet Yellen gives a talk at New York University. Later in the week, reports on sales of previously owned homes and durable goods orders for October are due in the U.S. The minutes from the Fed’s latest policy meeting are out on Wednesday. Market participants will gauge Fed officials’ eagerness to boost the benchmark interest rate in December, which is widely expected by the market. On Wednesday, the U.K. announces its budget Wednesday; that could see a significant economic downgrade amid a continued impasse in its negotiations with the EU on Brexit.

Bulletin Headline Summary from RanSquawk

- German concerns short – lived with EUR paring back losses seen in the wake of coalition talks breaking down

- Weekend press reports in the UK suggest that UK PM May could be on the cusp of promising more money to the EU in order settle the “Brexit Bill”

- Looking ahead, highlights include potential comments from ECB’s Lautenschlaeger, Draghi, Constancio and BoE’s Ramsden

Market Snapshot

- S&P 500 futures down 0.1% to 2,572.25

- MSCI Asia down 0.07% to 170.29

- MSCI Asia ex Japan up 0.09% to 559.78

- Nikkei down 0.6% to 22,261.76

- Topix down 0.2% to 1,759.65

- Hang Seng Index up 0.2% to 29,260.31

- Shanghai Composite up 0.3% to 3,392.40

- Sensex up 0.2% to 33,396.87

- Australia S&P/ASX 200 down 0.2% to 5,945.67

- Kospi down 0.3% to 2,527.67

- STOXX Europe 600 up 0.01% to 383.85

- German 10Y yield rose 0.4 bps to 0.365%

- Euro up 0.08% to $1.1799

- Italian 10Y yield fell 0.2 bps to 1.57%

- Spanish 10Y yield fell 0.8 bps to 1.547%

- Brent Futures down 0.4% to $62.46/bbl

- Gold spot down 0.03% to $1,292.09

- U.S. Dollar Index down 0.05% to 93.61

Top Overnight news

- German Chancellor Angela Merkel declared failure in her bid to form a new government, throwing the future of Europe’s longest- serving leader into doubt and potentially pointing toward new elections

- Possibilities now include setting up a minority government headed by her Christian Democratic-led bloc or asking President Frank-Walter Steinmeier to order a national election just months after the last one in September

- Special Counsel Robert Mueller directed the Justice Department to turn over a broad array of documents, ABC reports; Mueller’s investigators seek emails related to firing of FBI Director James Comey and the decision of Attorney General Jeff Sessions to recuse himself from the entire matter

- U.S. Treasury Secretary Steven Mnuchin says he doesn’t know whether Congress would extend individual tax cuts that would expire after 2025 in current tax proposal; White House chief economist Kevin Hassett argues that the tax overhaul will boost productivity

- Chile’s presidential election is heading for a hotly contested second round after billionaire Sebastian Pinera took a smaller-than-expected lead in Sunday’s vote

- The value of Japan’s exports rose 14% y/y (forecast +15.7%) in Oct.; imports increased 18.9% (forecast +20.2%); the trade surplus was 285.4b yen, less than the forecast of 330 billion yen

- After nine years, two presidential decisions, multiple lawsuits and

environmental protests, TransCanada Corp. is about to learn whether it

will receive the final state permit needed to build the Keystone XL oil

pipeline - The Republican tax-overhaul effort is in for a marathon debate on the Senate floor at the end of this month, with dozens of doomed Democratic amendments. But the real action will be elsewhere, behind closed doors

- Global investment banking revenues may decline 9 percent this quarter on low volatility and a selloff of high-yield debt, analysts at JPMorgan Chase & Co. said

- Marvell Technology Group Ltd., a chipmaker looking to build itself a future outside of a declining area of the market, agreed to buy Cavium Inc. for about $6 billion

- President Robert Mugabe shocked Zimbabwe on Sunday night with a televised address that failed to announce his highly anticipated resignation, a dramatic twist that means the 93-year-old may face immediate impeachment hearings

- The U.K. could be about to improve its financial offer to the European Union ahead of a crucial meeting of the bloc’s leaders in December

- HNA CEO Casts Doubts on SkyBridge Deal Completion, WSJ Says

- Novomet Purchase by Halliburton Said to Be Delayed: Kommersant

- U.S. Businesswoman Said to Bid for Weinstein Co.: WSJ

- Some Chrysler Pacifica Owners Complain of Engine Issues: NYT

- ProSieben Is ‘Obvious’ M&A Target, Possibly for NBC: Liberum

- Cellcom in Talks With Partner Comm to Deploy Fiber Network

- Eurocastle Reports NPL Transaction, Reschedules Results Release

- Goldman CEO Sees Frankfurt, Paris As His Bank’s EU Hubs: Figaro

Asia began the week subdued following the losses on Wall St. last Friday and with focus on political uncertainty after Trump campaigners were subpoenaed and German coalition talks broke down. ASX 200 (-0.2%) and Nikkei 225 (-0.5%) were in the red although recent strength across commodities helped stem losses in Australia, while Japanese sentiment was dampened by a firmer JPY and a miss on trade data. Hang Seng (+0.3%) and Shanghai Comp. (+0.3%) were initially negative with underperformance in the mainland as Shenzhen stocks resumed Friday’s sell off and amid reports that China tightened asset management rules to curb risky lending. However, prices then recovered heading into the close. Finally, 10yr JGBs were uneventful with prices flat, as demand from the dampened risk appetite in the region was counterbalanced by the absence of a BoJ Rinban announcement. PBoC injected CNY 70bln via 7-day reverse repos, CNY 20bln via 14-day reverse repos and CNY 10bln via 63-day reverse repos. PBoC set CNY mid-point at 6.6271 (Prev. 6.6277). Chinese Property Prices (Oct) Y/Y 5.4% (Prev. 6.3%). Chinese Property Prices rose M/M in 50 out of 70 cities (Prev. 44) and rose Y/Y in 60 out of 70 cities (Prev. 67). Japanese Exports (Oct) Y/Y 14.0% vs. Exp. 15.8% (Prev. 14.1%) Japanese Imports (Oct) Y/Y 18.9% vs. Exp. 20.2% (Prev. 12.0%)

Top Asian News

- Soros’ Wang Said to Leave to Start Hedge Fund in Hong Kong

- Thailand’s Economic Growth Beats Forecasts as Exports Rise

- Barcelo Makes Offer for NH in Bid to Create Spanish Hotel Giant

- Zarrab Case Aims to Implicate Turkish Leaders, Erdogan Aide Says

- Alibaba Bets $2.9 Billion It Can Take on Wal-Mart in China

- Asia Shares Fall as Investors Lock in Gain Amid U.S. Tax Wrangle

- Toshiba’s Share Sale Plan Cheers Bond Market as Stocks Fall

European bourses have had a mixed start for the week, with the EuroStoxx 50 relatively flat amid the collapse of German government coalition talks, while on the corporate front, German Utilities RWE and Innogy are rising over divestiture speculation. Roche are among the best performing stocks this morning after the drugmaker announced a double dose of trial wins. No further political news or fundamental inputs to spark movement, but Bunds are back in the black and it looks like short term or intraday chart levels are impacting. Contacts were flagging 162.82 on the downside and that just held in to keep sellstops intact and the 10 year German bond has subsequently bounced towards 163.00 again. Back to the Government coalition impasse, the President will address the nation at 13.30GMT and could call another election given the failure of talks and Chancellor Merkel to form a new regime, but there is a train of thought that he might make a last ditch effort to get the parties back around the table. Meanwhile, Gilts continue to track moves elsewhere awaiting more concrete Brexit developments and Wednesday’s Budget, ticking back up to 124.65 from a 124.53 low. US Treasuries maintaining a firmer bias, and with the long bond outperforming yet again – so even more flattening.

Top European News

- Merkel’s Attempt to Form a New German Government Collapses

- German Liberals Would Support a Merkel Minority Government: Bild

- Michael Spencer’s NEX Group Picks Amsterdam as Post- Brexit Base

- Vestas Shares Fall; Goldman Sees Margin Pressure in 2018

- Jana Novotna, Former Wimbledon Champion, Dies at 49

- Akbank’s Rota Is Said to Become Bank Audi’s Turkey Unit CEO

In FX, the EUR roundtriped as Germany’s FDP walks out of talks to form a 4-party Jamaican coalition after a month of negotiations, citing irretrievable differences. Chancellor Merkel must now inform the President of the situation and the risk is a snap election and failure to secure a 4th term in office. EUR/USD slumped to a 1.1723 base before recovering, with bids touted at 1.1710, while EUR/GBP held key support at 0.8871 (21 DMA) despite filling bids at 0.8875 before rebounding towards 0.8900. GBP: A firmer tone independent of the EUR’s travails on latest reports suggesting material progress in Brexit negotiations in the offing, while UK Chancellor Hammond is apparently encouraging PM May to up her divorce settlement offer to the EU. Cable back up near 1.3250. Benefiting from broad risk-off sentiment, with USD/JPY briefly/marginally below 112.00, but now pivoting the big figure and likely to be eyeing a spread of option expiries in nearby proximity (300 mn at 111.90, 901 mn at 112.00, 2.3 bn at 112.30 and 1 bn from 112.50-60).

In commodities, price action WTI and Brent has been relatively tepid with investors turning their attention to the bi-annual OPEC meeting, in which it is expect that the cartel will extend production cuts to cover the whole of next year. On Friday, the latest Baker Hughes showed that rig counts were unchanged in week to November 17th. WTI slightly off best levels having run into resistance just ahead of USD 57.

US Event Calendar

- 10am: Leading Index, est. 0.7%, prior -0.2%

DB’s Jim Reid concludes the overnight wrap

The most interesting thing to get your teeth stuck in to this week is likely to be the turkey on Thankgiving on Thursday. As such it’ll likely be a quietish week unless we see a renewed bout of the Wednesday to Wednesday sell-off of last week. Things calmed down from the lows during Wednesday’s session even if we closed out the week on Friday with a softer session for equities.

That said, things have already got to an interesting start as talks to form the next coalition German government have failed after a 12 hour negotiation session ended at around midnight last night, with the pro-market FDP walking out citing large differences with the environmentalist Green party. The head of the FDP Mr Lindner noted “it’s better not to govern than to govern badly”. If no compromise is eventually found, Germany may enter into unchartered territory, potentially involving a new election or even a minority led government. The Euro is down c0.5% this morning.