GOLD: $1288.40 DOWN $4.00

Silver: $17.05 DOWN 8 cents

Closing access prices:

Gold $1288.50

silver: $17.03

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1299.04 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1292.20

PREMIUM FIRST FIX: $6.84

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1299.04

NY GOLD PRICE AT THE EXACT SAME TIME: $1290.90

Premium of Shanghai 2nd fix/NY:$8.14

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1289.15

NY PRICING AT THE EXACT SAME TIME: $1289605

LONDON SECOND GOLD FIX 10 AM: $1290.50

NY PRICING AT THE EXACT SAME TIME. 1290.30

For comex gold:

NOVEMBER/

NUMBER OF NOTICES FILED TODAY FOR NOVEMBER CONTRACT: 11 NOTICE(S) FOR 1100 OZ.

TOTAL NOTICES SO FAR: 1053 FOR 105,300 OZ (3.375 TONNES)

For silver:

NOVEMBER

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 885 for 4,425,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8228/OFFER $8253 up $231 (morning)

BITCOIN : BID $8215 OFFER: $8240 // UP $218 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY 1530 contracts from 199,402 DOWN TO 197,872 WITH RESPECT TO WEDNESDAY’S TRADING WHICH SAW SILVER RISE BY 13 CENTS AND STILL WELL BELOW THE HUGE $17.25 SILVER RESISTANCE. WE HAD MINOR LONG COMEX LIQUIDATION. HOWEVER WE WERE ALSO NOTIFIED THAT WE HAD ANOTHER HUMONGOUS NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 1204 DECEMBER EFP’S WERE ISSUED ALONG WITH 93 EFP’S FOR MARCH FOR A TOTAL ISSUANCE OF 1297 CONTRACTS. (THE ISSUANCE FOR MARCH THAT WE HAVE SEEN THESE PAST SEVERAL DAYS BOTHERS ME A LOT AS THIS IS SUPPOSE TO BE FOR EMERGENCY USES ONLY IN AN UPCOMING DELIVERY MONTH). I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 1231 EFP’S ISSUED.

RESULT: A SMALL SIZED FALL IN OI COMEX WITH THE 13 CENT PRICE RISE. WE HAD SOME COMEX LONGS EXITED OUT OF THE SILVER COMEX BUT MOST OF THEM TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 1297 EFP’S WERE ISSUED FOR FRIDAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY ONLY LOST IN OI 233 CONTRACTS i.e. 1297 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1530 OI COMEX CONTRACTS.

In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.989 BILLION TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 0 NOTICE(S) FOR nil OZ OF SILVER

In gold, the open interest ROSE BY 7688 CONTRACTS WITH THE GOOD SIZED RISE IN PRICE OF GOLD ($10.40) WITH RESPECT TO WEDNESDAY’S TRADING.THIS IS IN TOTAL CONTRAST TO THE HUGE 18,000 COMEX LOSS ON TUESDAY. WE THUS HAD NO COMEX LONGS EXIT THE ARENA. HOWEVER THE TOTAL NUMBER OF GOLD EFP’S ISSUED THURSDAY FOR TODAY (FRIDAY) TOTALED ANOTHER 14,179 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 13,599 CONTRACTS AND FEB SAW THE ISSUANCE OF 580 CONTRACTS. WE WITNESSED A TOTAL OF 21,428 EFP’S ISSUED THURSDAY FOR FRIDAY. The new OI for the gold complex rests at 539,300. DEMAND FOR GOLD INTENSIFIES DESPITE THE CONSTANT RAIDS. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NOT BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING A FURTHER 6 TO 10 WEEKS TO OBTAIN PHYSICAL FROM THE POINT WHEN FORWARDS BECOME DUE. IN ESSENCE WE HAD A NET GAIN OF 21,867 OI CONTRACTS: 7688 OI CONTRACTS ADDED TO THE COMEX OI AND 14,179 OI CONTRACTS NAVIGATE OVER TO LONDON.

ON WEDNESDAY, WE HAD 8101 EFP’S ISSUED.

Result: A HUGE SIZED INCREASE IN OI WITH THE GOOD SIZED RISE IN PRICE IN GOLD ON YESTERDAY ($10.40). WE HAD AN LARGE NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,179. THERE OBVIOUSLY DOES NOT SEEM TO BE ANY PHYSICAL GOLD AT THE COMEX AND YET WE ARE APPROACHING THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS NO GOLD PRESENT AT THE GOLD COMEX. IF YOU TAKE INTO ACCOUNT THE 14,179 EFP CONTRACTS ISSUED, WE HAD A NET GAIN OPEN INTEREST OF 21,867: 14,179 CONTRACTS MOVE TO LONDON AND 7688 CONTRACT GAIN AT THE COMEX.

we had: 11 notice(s) filed upon for 1100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

No change in gold inventory at the GLD/

Inventory rests tonight: 843.39 tonnes.

SLV

TODAY WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV

INVENTORY RESTS AT 317.130 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 1530 contracts from 199,402 DOWN TO 197,960 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE RISE IN SILVER PRICE (A GAIN OF 13 CENTS ). HOWEVER, OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER HUGE 1204 PRIVATE EFP’S FOR DECEMBER (WE DO NOT GET A LOOK AT THESE CONTRACTS) AND 93 EFP’S FOR MARCH FOR A TOTAL OF 1297 EFP CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE ARE NOW GETTING CLOSE TO FIRST DAY NOTICE AND THIS IS THE SCENE WHERE IN THE PAST WE DID SEE MASSIVE COMEX OI CONTRACTION ALTHOUGH IT WAS MORE PRONOUNCED IN GOLD THAN WITH SILVER. IT STILL CONTINUES UNABATED AND WE NOW KNOW THE REAL REASON FOR THE CONTRACTION: THE TRANSFER OF OI TO LONDON. TODAY WE HAD MINIMAL COMEX SILVER COMEX LIQUIDATION. IF WE ADD THE OI LOSS AT THE COMEX (1530 CONTRACTS) TO THE 1297 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET LOSS OF ONLY 233 OPEN INTEREST CONTRACTS,

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT RISE IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). NOT ONLY THAT BUT WE ALSO HAD ANOTHER 1297 EFP’S ISSUED.. TRANSFERRING OUR COMEX LONGS OVER TO LONDON . ON WEDNESDAY WE EXPERIENCED 1231 EFP’S ISSUED FOR TRANSFER TO LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 1.90 points or .06% /Hang Sang CLOSED UP 158.38 pts or 0.53% / The Nikkei closed UP 27.70 POINTS OR 0.12%/Australia’s all ordinaires CLOSED DOWN 0.07%/Chinese yuan (ONSHORE) closed UP at 6.605-/Oil UP to 58.79 dollars per barrel for WTI and 63.76 for Brent. Stocks in Europe OPENED GREEN. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6050. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.65972 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(MARKETS STRONG)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/China

b) REPORT ON JAPAN

My goodness, we have another scandal from Japan. This time Mitsubishi Materials altered data similar in fashion as to what Kobe steel did

( zerohedge)

c) REPORT ON CHINA

i)Thursday trading /Shanghai

The Shanghai stock exchange fell 2.3% on Thursday with the 10 yr bond climbing to 4% and top rated corporate bonds yielding 5.2%. The total of all debt in China is 40 trillion USA dollars with the problematic shadow banking sector at 10 trillion. It is an accident waiting to happen

( zero hedge)

ii)FRIDAY

China slashes import tariffs on consumer goods in a move to bolster Trump and other Western exporters

( zerohedge)

4. EUROPEAN AFFAIRS

i)Europe trading/Thursday

Strong PMI numbers sends the Euro higher as well as all European bourses

( zerohedge)

ii)I enjoy reading Bill Blain’s focus on the global economy. He is bang on. Today he discusses China’s meltdown Wednesday night and how inflation is beginning to rear its ugly head throughout the globe. He is concentrating on the USA high yield market.

( Bill Blain/Mint Partners)

iii)Friday/Merkel’s poll numbers tank as she heads into discussions with it’s former coalition partner SPD headed by Schultz. This will be troublesome as German citizens are angry at the huge influx of migrants.

( zerohedge)

iv)This is a dumb move on the part of Schultz: he is ready to negotiate with Merkel. If the SPD join with Merkel and Merkel remains Chancellor then in the next election the citizens of Germany will throw out Schultz

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Saudi Arabia

ii)Saudi Arabia arrests its second richest man in their kingdom and MBS will try and extort his wealth to enrich his faltering treasury( zerohedge)

iii)New footage seems to suggest that the extortion by MBS is working

( zerohedge)

iv)In a war of words, MBS calls Iran’s Ayatollah Khamenei a “New Hitler of the Middle East” and must be confronted:

So sad!! Another attack and this time near the Northern Sinai town of El Arish, militants stormed a mosque and murdered at least 235 worshipers

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

The author believes strongly that anything above 58 dollars per barrel brings on huge supply from shale. We should also be cognizant of the huge amount of oil that China is bringing far above what it needs. It is continually adding to its SPR. That that stops demand will falter:

(courtesyParaskova/OilPrice.com)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)this fund manager states that Bitcoin is paving the way for gold’s return as true money and a global currency

(courtesy Pakiam/Bloomberg/GATA)

ii)Persson gives us 28 reasons why we should buy physical gold(Persson/Bullionstar/GATA)

iii)Alasdair’s lesson for this week: deflation

( Alasdair Macleod/GoldMoney)

10. USA stories which will influence the price of gold/silver

i)Soft data USA PMI’s tumble to a 4 month low and this signals just at most a 2% annual growth, not what Trump is stating at 3%

( zerohedge)

ii)Another dandy from David Stockman how the huge overvalued stockmarket

(David Stockman/ContraCorner)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY A LARGE 7,688 CONTRACTS UP to an OI level of 539,300 WITH THE GOOD SIZED RISE IN THE PRICE OF GOLD ($10.40 GAIN WITH RESPECT TO WEDNESDAY’S TRADING). WE EXPERIENCED NO GOLD COMEX LIQUIDATION. HOWEVER WE DID HAVE ANOTHER LARGE COMEX EXIT THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 13,599 EFPS WERE ISSUED FOR DECEMBER AND 580 WERE ISSUED FOR MARCH FOR A TOTAL OF 14,179 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE CONSTANT BANKER RAIDS HAVE NOT BEEN TOO SUCCESSFUL IN GETTING OUR MATHEMATICAL PAPER LONGS IN GOLD TO LIQUIDATE THEIR POSITION. IT HAS FAILED MISERABLY IN SILVER.

ON A NET BASIS IN OPEN INTEREST WE GAINED: 21,867 OI CONTRACTS IN THAT 14,179 LONGS WERE TRANSFERRED AS LONGS TO LONDON AS A FORWARD AND WE GAINED 7688 COMEX CONTRACTS. NET GAIN: 21,867

Result: a HUGE INCREASE IN COMEX OPEN INTEREST WITH THE GOOD SIZED GAIN IN THE PRICE OF GOLD ($10.40.) ON TOP OF THAT WE HAD 14,179 EFP’S ISSUED FOR A FIAT BONUS AND A DELIVERABLE FORWARD GOLD CONTRACT IN LONDON. WE HAD NO COMEX GOLD LIQUIDATION.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A GAIN OF 3 CONTRACT(S) RISING TO 12. We had 1 notices filed YESTERDAY so GAINED 4 contracts or 400 additional oz will stand for delivery AT THE COMEX in this non active month of November.

The very big active December contract month saw it’s OI LOSS OF 40,909 contracts DOWN to 164,753. January saw its open interest GAIN OF 103 contracts UP to 1061. FEBRUARY saw a gain of 45,124 contacts up to 288,583. DEMAND FOR GOLD VERY STRONG

We had 11 notice(s) filed upon today for 1100 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 422,124

FINAL NUMBERS CONFIRMED FOR TODAY: 508,914

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY FELL BY 1530 CONTRACTS (WHEN COMPARED TO GOLD) FROM 199,402 DOWN TO 197,872 DESPITE WEDNESDAY’S 11 CENT RISE IN PRICE. HOWEVER WE DID HAVE ANOTHER STRONG 1204 PRIVATE EFP’S ISSUED FOR DECEMBER AND 93 EFP’S FOR MARCH BY OUR BANKERS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 1297. IT SURE LOOKS LIKE THE BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. IT HAS JUST STARTED IN EARNEST IN SILVER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD MINIMAL LONG SILVER COMEX LIQUIDATION AS DEMAND FOR PHYSICAL SILVER INTENSIFIES AGAIN

The new front month of November saw its OI FALL by 1 contract(s) and thus it stands at 0. We had 0 notice(s) served YESTERDAY so we gained 0 contracts or an additional NIL oz will stand in this non active month of November. After November we have the big active delivery month of December and here the OI FELL by 9536 contracts DOWN to 56,169. YET WE HAD 1297 EFP’S ISSUED WHICH MEANS A GOOD PERCENTAGE OF THE ROLLOVERS LANDED IN LONDON AS A TRANSFER OF OI FOR A FORWARD. January saw A GAIN OF 244 contracts RISING TO 1532.

We had 0 notice(s) filed for nil oz for the NOV. 2017 contract

INITIAL standings for NOVEMBER

Nov 24/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

6,012.05

SCOTIA

oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

56,146.845

oz

HSBC

|

| No of oz served (contracts) today |

11 notice(s)

1100 OZ

|

| No of oz to be served (notices) |

1 contracts

(100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1064 notices

106,400 oz

3.309 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer deposit(s):

i) into HSBC: 56,146.845 oz

total customer deposits 56,146.845 oz oz

We had 1 customer withdrawal(s)

i) Out of Scotia: 6,012.05 oz

Total customer withdrawals: 6012.05 oz

we had 0 adjustment(s)

For NOVEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 11 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the NOVEMBER. contract month, we take the total number of notices filed so far for the month (1064) x 100 oz or 106,400 oz, to which we add the difference between the open interest for the front month of NOV. (12 contracts) minus the number of notices served upon today (11 x 100 oz per contract) equals 106,500 oz, the number of ounces standing in this NON active month of NOV

Thus the INITIAL standings for gold for the NOVEMBER contract month:

No of notices served (1064) x 100 oz or ounces + {(12)OI for the front month minus the number of notices served upon today (11) x 100 oz which equals 106,500 oz standing in this active delivery month of NOVEMBER (3.312 tonnes)

WE GAINED 4 ADDITIONAL CONTRACTS OR 400 OZ OF ADDITIONAL GOLD STANDING FOR METAL AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

THE COMEX GOLD CONTRACT AT AROUND THE SAME TIME AS LAST YEAR: (NOV 25) WE HAD 106,069 GOLD CONTRACTS STANDING AND THIS COMPARES TO 165,772 TODAY . THIS YEAR THERE HAPPENS TO BE 4 DAYS LEFT BEFORE FDN. LAST YEAR THERE WERE 3 DAYS BEFORE FDN WITH THE ABOVE READINGS WERE TAKEN.

ON FIRST DAY NOTICE FOR DECEMBER, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 514,112.106 or 15.999 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,876,397.995 or 276.09 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 78 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE NOVEMBER DELIVERY MONTH

NOVEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

987.000 oz ???

Delaware

|

| Deposits to the Dealer Inventory |

598,157.07 oz

Brinks

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(nil,OZ)

|

| No of oz to be served (notices) |

0 contract

(NIL oz)

|

| Total monthly oz silver served (contracts) | 885 contracts(4,425,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 1 deposit(s) into the dealer account:

i) Into Brinks: 598,152.07 oz

total dealer deposit: 598,152.07 oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of Delaware

TOTAL CUSTOMER WITHDRAWAL 987.0000 oz

We had 0 Customer deposit(s):

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: nil oz

we had 0 adjustment(s)

The total number of notices filed today for the NOVEMBER. contract month is represented by 0 contracts FOR nil oz. To calculate the number of silver ounces that will stand for delivery in NOVEMBER., we take the total number of notices filed for the month so far at 885 x 5,000 oz = 4,425,0000 oz to which we add the difference between the open interest for the front month of NOV. (1) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the NOVEMBER contract month: 885 (notices served so far)x 5000 oz + OI for front month of NOVEMBER(1) -number of notices served upon today (0)x 5000 oz equals 4,425,000 oz of silver standing for the NOVEMBER contract month. This is EXCELLENT for this NON active delivery month of November.

We gained 0 contract(s) or an additional NIL oz will stand for metal in the non active delivery month of November.

AS I MENTIONED ABOVE, WE HAVE BEEN WITNESSING QUEUE JUMPING IN SILVER FROM MAY 1 2017 ONWARD. IT IS NOW COMFORTING TO SEE CONSIDERABLE QUEUE JUMPING OCCURRING CONTINUALLY IN GOLD FOR THE FIRST TIME SINCE RECORDED TIME AT THE GOLD COMEX!!(1974). QUEUE JUMPING CAN ONLY OCCUR ON PHYSICAL METAL SHORTAGE. THE TRANSFER OF EFP’S TO LONDON FURTHER INTENSIFIES THE DEMAND FOR PHYSICAL METAL!!

AT THIS TIME LAST YEAR WE HAD 40,393 NOTICES STANDING FOR DELIVERY FOR SILVER. THIS YEAR 65,705 BUT WITH ONE EXTRA TRADING DAYS LEFT.

ON FIRST DAY NOTICE FOR THE DECEMBER CONTRACT WE HAVE 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 122,269

CONFIRMED VOLUME FOR YESTERDAY: 119,938 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 119,938 CONTRACTS EQUATES TO 597 MILLION OZ OR 85.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

THE COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 44.653 million

Total number of dealer and customer silver: 233.085 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.5 percent to NAV usa funds and Negative 1.4% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.5%

Percentage of fund in silver:37.2%

cash .+.3%( Nov 24/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -0.92% (Nov 24 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.76% to NAV (Nov 24/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.92%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.76%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Nov 24/2017/ Inventory rests tonight at 843.39 tonnes

*IN LAST 279 TRADING DAYS: 97.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 214 TRADING DAYS: A NET 59,72 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.61 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Nov 24/2017:

Inventory 317.130 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.58%

12 Month MM GOFO

+ 1.81%

30 day trend

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Goldcore: Thursday’s commentary

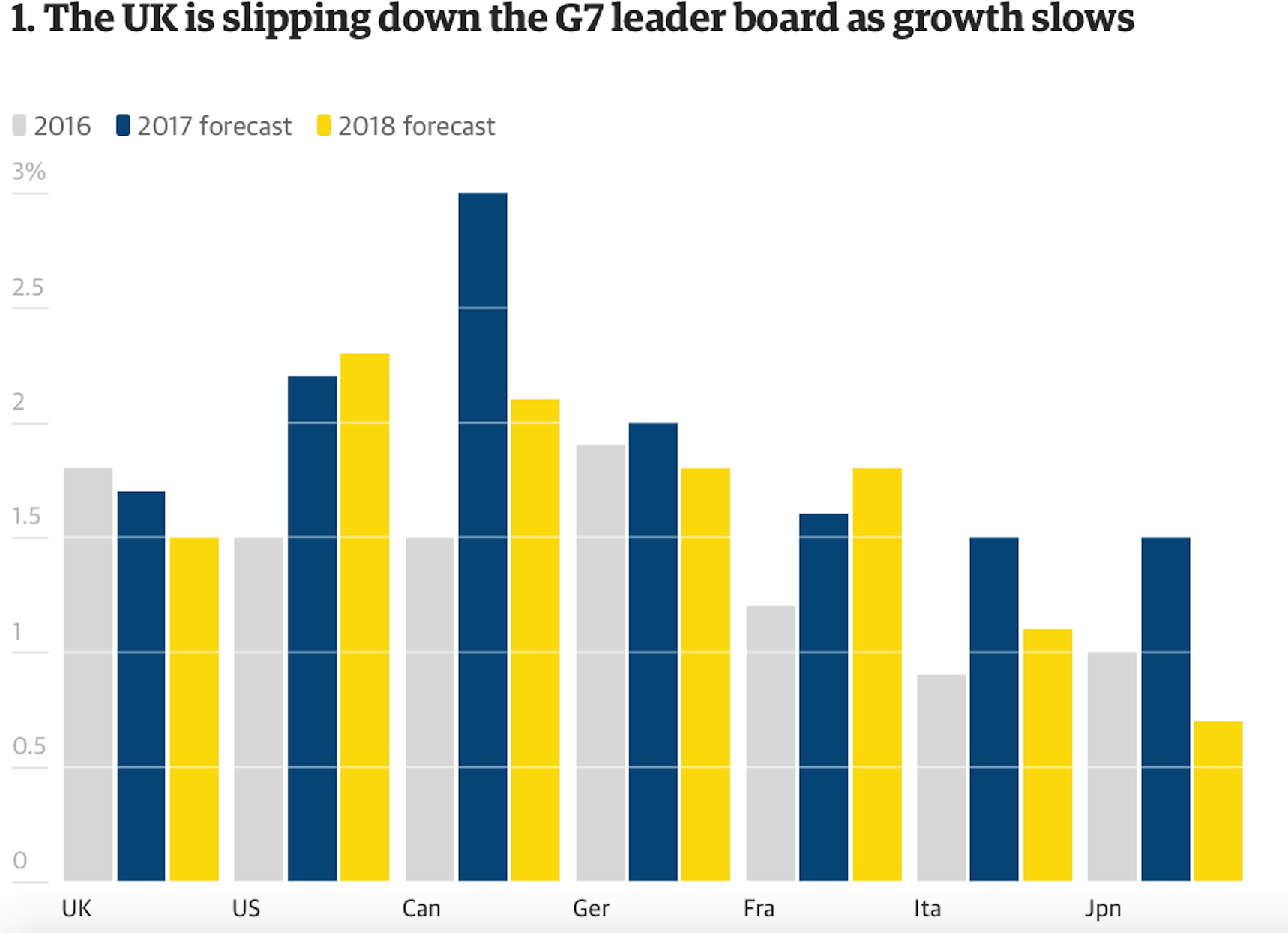

Brexit Budget – Grim Outlook As UK Economy Downgraded

Brexit budget – Grim outlook as UK economic forecasts downgrade

– UK Chancellor uses housing market policy as smoke-screen for deteriorating economy

– UK budget matters more than ever due to BREXIT risks

– Policy on stamp duty will fail to aid worsening housing market

– Real GDP expected to grow by just 1.5%, 40% less than projections 2 years ago

– Households now face an unprecedented 17 years of stagnation in earnings

– Critics claim Budget failed to calm Brexit uncertainty

– UK and especially London property market at “breaking point”

Editor: Mark O’Byrne

Source: FT

Yesterday UK Chancellor Philip Hammond’s long-awaited Autumn Budget was delivered to the Houses of Parliament. He was praised for a ‘good budget in political terms’ and for talking up the UK economy, telling his contemporaries that that it is “confounding those who talk it down” and that “those who underestimated the UK, do so at their peril”.

Hammond’s comments suggest the economy is doing better than its critics said it is. This isn’t the case. The Office of Budget Responsibility (OBR) delivered some depressing statistics yesterday which suggest the recovery post-crisis and post-referendum is still a long way off.

Hammond was praised for his ‘cheery’ budget. His head had been very close to the block ahead of yesterday with many criticising his negative views on Brexit negotiations and general lack of optimism.

In reality this really was a political budget. One designed for some quick-wins and support from the House and the media. It was hardly economic. Brexit was barely addressed, economic growth was referred to as ‘stubborn’ and the housing market was treated with a patronising cut in stamp duty. A band-aid on a haemorrhaging artery.

Is the UK economy proving its critics wrong?

The government statistics agency cut the UK’s projected growth forecast for 2017 from 2% to 1.5%. The OBR believes the economy can only now grow sustainably at a rate of 1.5 per cent, 40 per cent lower than it estimated as recently as two years ago.

On an international level we are expected to fall down the leaderboard of G7 countries in 2017 and into 2018. Just last year we were second only to Germany in terms of growth. Data from both the OBR and the IMF suggest lower forecasts for the UK’s GDP and output.

This does not bode well for workers who have not only failed to see their wage levels increase for nearly a decade but are also worried about the impact of Brexit.

Brexit boost?

Hammond was praised for drawing attention away from the ongoing Brexit-saga. He mentioned the allocation of a further £3bn to help any outcome of the talks. For London May Sadiq Khan this was not enough:

“At a time when there’s uncertainty, at a time where we are being told by the EU we’re going down the road of an extreme, hard Brexit because of the response of this Government, businesses will think ‘you know what? We’re far better going off to Frankfurt, or going to Berlin, or going to Paris.

“This is not me talking down London, it’s me being frustrated by this budget today. This, I think, is the most anti-London budget for a generation.

“…At a time when businesses are frustrated by the lack of Londoners with the skills for the jobs of tomorrow, no rule news in relation to investing in young Londoners.

“This was a chance for the Chancellor to have a big, bolder budget. He’s blown it.”

Khan’s right. Businesses will be looking at yesterday’s budget feeling as much in the dark as they were beforehand. There has been little guidance as to how the UK will work to make the capital city attractive post-Brexit and the incentives there will be to keep people employed here.

It isn’t just infuriating from a business perspective, but also for the London housing market which is nearly impossible for new entrants to join.

“At a time when Londoners can’t afford to rent in London, let alone buy, no new rule news in relation to building affordable homes in London.”

Hammond couldn’t even figure out that this wasn’t an area that could be a quick policy announcement.

The smoke-screen of stamp duty

The media jumped on Hammond’s pièce de résistance – removal of stamp duty for first time buyers. Which in reality is just a massive smokescreen designed to make us believe there is hope for the UK economy and housing market.

The main headline-grabbing announcement from Hammond in his Brexit budget was the removal of stamp-duty for first-time buyers purchasing houses under £300k.

This is unlikely to make any difference to either first-time buyers or the overall property market.

As the OBR concluded from the Chancellor’s announcement, the tax break was likely to push property prices up by about 0.3%, with most of the increase coming in 2018.

“The main gainers from the policy,” said the forecasting group, “are people who already own property, not the FTBs [first-time buyers] themselves.”

It explained that whilst some potential FTBs, with smaller deposits, would now be able to borrow a little more “allowing them to buy properties that they otherwise could not afford” this would now be “more expensive”.

So who is helping who out here, Chancellor? Is the government yet again encouraging citizens to go up and buy things they can’t afford, thus pushing themselves further into debt?

“I welcome the chancellor’s announcement of £15bn of new support for housing but it doesn’t reflect the government’s ambition to solve the housing crisis and, crucially, it’s unclear about how it will help ordinary people to find a truly affordable home,” Lord Kerslake.

The fact is people cannot afford to buy houses right how, not because of stamp duty but because house prices are far beyond the reach of those who have not seen wages and therefore their savings increase in nearly ten years. This is not set to change. Households now face an unprecedented 17 years of stagnation in earnings.

A misunderstood market used as a political puppet

The barrier to entry for first-time buyers is not the prospect of a few thousand pounds extra in tax. It is the near impossibleness of being able to save enough for the initial deposit. This is the main barrier as found in a recent Halifax bank survey. For those who can manage a deposit, that small amount of tax wasn’t particularly prohibitive to them in the first place.

The government seems to be on yet another false-path to trying to prop up the ailing housing market, strong in the belief that it is the elixir of life for the UK economy. Why the constant encouragement to get on a housing ladder that is neither affordable, nor stable?

How can a housing market solve all of the problems when the demand side just cannot afford to get involved? The new figures from the OBR suggest that the downward revisions mean pay will not reach its 2008 level until the mid 2020s.

So with rising inflation, plus expected rising interest rates and now further stagnation in wages it’s not looking as though Hammond’s solution is going to do much at all.

The housing market is long past a quick fix in the Autumn budget. A recent Halifax bank survey recorded the weakest reading for consumer expectations since October 2012. The bank told the Guardian:

“Housing market optimism has declined significantly over the past year, with almost half of people expecting a general slowdown in the market.”

This is what terrifies Hammond and the UK government. A housing market is seen as a measure for the health of an economy. With growth and productivity ‘stubbornly’ refusing to budge, the Chancellor has had to turn his attention to an area he can have a slightly more direct impact on – the housing market.

However there is little evidence that such policies play out well in the long-term. For decades the UK government has worked to try bubble up the UK housing market. It has arguably worked very well. But a financial crisis, wage stagflation and stealth inflation means that it is at breaking point.

This was being seen even before the UK voted for the biggest economic upset (Brexit) seen in modern history.

A depressing yet timely reminder

Yesterday’s Brexit budget was a depressing yet timely reminder of the way politicians can manipulate economies and policies to suit their targets and save their jobs.

It was a reminder for savers and investors everywhere, not just in the UK.

Hammond’s distraction technique using the stamp-duty announcement, as well as the allocation of funds to Brexit, may have worked for the mainstream media but anyone hoping to protect the value of their portfolios should stay alert.

As we explained recently:

The government needs to stop being so irresponsible and no longer constantly peddle arguments for home ownership. However it is difficult politically to sell that story. Especially when all parties have realised the youth vote has major housing concerns and believes they have the right to own property.

For those who are not susceptible to the war-cry to the youth vote they would be wise to remember that there are other real assets out there, ones that cannot be manipulated by policy announcements and are less vulnerable to the machinations of career politicians.

Physical gold coins and bars are like housing. If owned as a diversification, in the safest ways, precious metals are tangible, safe stores of value.

However, they do not come with a massive debt burden, owners do not have to live in fear of rising interest rates and unprecedented uncertainties in both political and economic spheres as we alluded to yesterday

end

Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– FOMC minutes show uncertainty and concern about markets are affecting officials’ decision-making

– Officials were cautious when evaluating market conditions and the ‘damaging effects on the economy’

– Worry about ‘potential buildup of financial imbalances’ and a sharp reversal in asset prices’

– Members seem oblivious to impact of inflation on households and savings

– Physical gold and silver remain the only assets for real diversification and safety

After nearly a decade of pumping up the US and global markets, Janet Yellen and team are now starting to show some concern for financial market prices. The FOMC is concerned that they are getting out of hand and are a danger to the US economy.

The minutes of the Fed’s October meeting show that the committee is largely optimistic about the US economy:

“In their discussion of the economic situation and the outlook, meeting participants agreed that information received since the FOMC met in September indicated that the labor market had continued to strengthen and that economic activity had been rising at a solid rate despite hurricane-related disruptions.”

But caution was the name of the game when it came to looking at overall market conditions:

“In light of elevated asset valuations and low financial market volatility, several participants expressed concerns about a potential buildup of financial imbalances…They worried that a sharp reversal in asset prices could have damaging effects on the economy.”

There isn’t a huge amount you can say in response to the FOMC minutes. There was no surprise, they practically telegraphed a December rate hike. And, when it comes down to ‘financial imbalances’, you really just want to tweet them with ‘…no shi*t sherlock’.

Why the sudden concern?

Really, why the sudden concern about financial imbalances? After all the FOMC has been pumping asset prices for the last decade. They are overjoyed to see the S&P500 regularly breaking through new highs.

The ‘imbalance’ committee members refer to is likely in regard to the risk/reward profile in the price of equity markets. This is somewhat ironic given almost the exact same thing happened with bond markets thanks to QE and the Fed’s balance sheet expansion. Just consider that their own yield curve lies at the heart of the current equities bull market.

The fear seems to be that in the last decade there has been such an expansion of credit that we are now faced with an unprecedented bubble. The Fed has no idea how this can be managed across central banks. They are concerned not only how the bubble will burs but what the contagion will be.

Since the Fed started hiking rates up, markets and financial conditions have not tightened. At all. One could speculate that this shows the market is convinced that the moment equities suffer a selloff, the Fed will either stop hiking altogether, or (worse) revert to the status quo and announce QE4.

At the moment the market is pricing in the risk of further rate hikes into next year. The chart below from HSBC shows “the market has been pricing in more and more 2018 hiking risk. The maroon line in the chart below shows the increase in hiking expectations in recent weeks, with investors pricing in more than 1 1/2 hikes for the first time since April.”

No matter market predictions of Fed rate rises no one can prepare for the aftermath of a $50 trillion debt build-up since the financial crisis of 2008. Nothing like this has been seen before.

In this year alone we have hit a new record when it comes to money printing by central banks. Of course no one knows what we are dealing with. What is more concerning is that the world’s most powerful central bank is only now wondering about financial imbalances in the market.

It’s a fix

As has been the case in many Western countries, central banks have expressed frustration at the stubbornly low levels of inflation. What’s interesting about this is that many of them have spent a long time ensuring that the means by which inflation is calculated gets them closer to their target.

The basket of goods used to calculate the level of price inflation is continuously manipulated.Very often ‘volatile’ food and fuel is not included in the US measure. Why does this matter? Because these are the two main items that affect household finances.

So far this year US inflation has averaged 1.6% so far this year (when you exclude food and fuel) and it came in at just 1.3% in September. This (artificial) low level of inflation appears to have almost baffled FOMC members, with much disagreement amongst them.

For those who believe inflation is low this “might reflect not only transitory factors, but also the influence of developments that could prove more persistent,” according to the minutes. However there were also a few members who expressed concern that it could begin to climb due to “increasing upside risks” to inflation as the labor market continues to tighten.

It was then suggested by ‘a couple’ of members that the Fed tweak its approach to inflation, moving away from the current 2% target and toward a “gradually rising path” in prices instead. A nebulous approach.

We continue to see a divided FOMC, with neither side getting our vote. As they continue to debate inflation and how to manage it, they are failing to do anything about it or even acknowledge what is really going on.

It is concerning enough that the current inflation measures do not reflect the impact on households, savings and the depreciation of the US dollar. It is even worse when the FOMC is discussing whether they should even try and target inflation at all.

Bill Blain of Mint Partners published an email from a reader expressing these very concerns with the FOMC:

On the inflation theme, I got an absolutely classic email y’day from a reader whom I don’t actually know, but had picked up my comments on some financial wire. Thank’s Geoff! His thesis is the global authorities have been spinning us a line when it comes to inflation – pointing out in 1971 it would have taken a low wage worker 2 hours and 10 mins to afford a ticket to the then new Disneyland. Disney prices have experienced 8% y-o-y inflation since the park opened. The same ticket will now require 7 hours and 20 mins work – and they are still playing that damn tune. (The lyrics would almost be profound if the tune wasn’t so inane!)

Geoff went on to point out: “The Indians shamefacedly admit their inflation is 9-13% – they are the only honest country on the planet!”

Not just a nervous Fed

The FOMC’s nervousness should be a cause for alarm but it should not be a feeling alien to market participants. They have long been concerned with the impact of central banks’ planned unwinding of balance sheets.

A shift in monetary tightening has been identified in global surveys as the most likely cause of the next recession. These concerns are based in history.

In 1994 the Fed began boosting rates, in a similar transition to today. The tightening triggered one of the worst corporate bond slides in two decades. The biggest loser was the suddenly devalued Mexican peso.

Adding to this, three of the four most powerful central bank chiefs are set to be replaced. Expectations are that their successors will not want to be seen hanging around delaying monetary tightening. They will most likely continue to set aside inflation concerns in a drive to curb the financial excesses that they have encouraged for a decade.

This will likely come with some problems, ones which the FOMC seems to be blind too. Yellen famously described balance sheet tightening as uneventful as ‘watching paint dry’. However, when one considers that more than half the gains in the S&P 500 from 2008 until the end of 2015 (when the FOMC began raising rates) came on days the Fed announced policy decisions then we should prepare for some harsh market reactions.

A pantomime farce

In the United Kingdom we have a very odd tradition at Christmas of ‘going to the pantomime’. The pantomime to those who haven’t been always seems to be a peculiar way to be entertained. It is not a pantomime as in a mime, as the word means in other countries, but instead it is a form of slap-stick musical entertainment.

One of the ‘hilarious’ parts to every pantomime is when the hero is trying to catch the baddie of the show. The baddie keeps appearing behind the hero, but our protagonist always seems to not notice or just miss him. Meanwhile the audience’s calls for ‘He’s behind you!!’ grow louder and more raucous as the show goes on.

The joke is, of course, that it seems to be near impossible that someone could miss a baddie looming so close and so obviously in the background.

The same can be said of the FOMC and their apparent ignorance of the threat of ‘financial imbalances’ for the last decade. For years we have watched incredulously as the FOMC along with other central bank committees pump away at markets. It is as if we have come nearly to the end of the pantomime where the ‘hero’ is finally getting wise to the baddie’s tricks and is close to catching him.

The only difference between a central bank pantomime and a real one is that there is unlikely to be a happy ending, as it will be the baddie who gets the better of the so-called ‘hero’.

In this pantomime we do not know how it is supposed to end. How can we?

Once again we conclude that this comes down to uncertainty. Whilst we have long-advocated for investors to line their portfolios with assets that offer true diversification and safety, it now seems more pertinent than ever.

Central banks rarely admit that they are confused about the state of markets. This latest statement was the beginning of them starting to scratch their heads and admit they don’t have all the answers. As this uncertainty and confusion seeps through and grows, investors should be prepared for panic in both policy making and financial decisions.

It is times like this when holding allocated, segregated gold in your portfolio makes even more sense. With a central bank wondering how to manage things, you can rest assured that your wealth is out of the reach of central bankers and their reactionary monetary policies.

Related reading

Gold Investment “Compelling” As Fed Likely To Create Next Recession

“This Is Where The Next Financial Crisis Will Come From” – Deutsche Bank

Gold Price Reacts as Central Banks Start Major Change

News and Commentary

Gold steadies as dollar weakens further (Reuters.com)

Japanese Stocks Decline, China Slide in Focus (Bloomberg.com)

Dollar poised for weekly losses, Fed’s inflation caution drags (Reuters.com)

Russian central bank: Gold holdings support national security (Reuters.com)

Putin orders Russian companies to be ready for urgent transition to war-time operations (RT.com)

Kremlin pledges to stand up for Russian billionaire arrested in France (Reuters.com)

Bank Deposits No Longer Off Limits as ECB Seeks Power to Freeze (Bloomberg.com)

Source: Bloomberg

The Party Is Over for Australia’s $5.6 Trillion Housing Frenzy (Bloomberg.com)

China’s Debt Surge May Increase Risk of Financial Crisis (Bloomberg.com)

What Germany’s Political Crisis Means for Your Money (MoneyWeek.com)

Three things you should know about rich people (StansBerryChurcHouse.com)

Guggenheim CIO Warns “Everything Is Liquid Until You ‘Need’ To Sell” (ZeroHedge.com)

Bitcoin Paving Way for Gold’s Return as Global Currency – Ned Naylor-Leyland (Gata.org)

Gold Prices To Quadruple To $5,000 On ‘Money Tsunami’ – McEwen (Bloomberg.com)

Gold Prices (LBMA AM)

24 Nov: USD 1,289.15, GBP 967.89 & EUR 1,086.37 per ounce

23 Nov: USD 1,290.15, GBP 969.93 & EUR 1,089.40 per ounce

22 Nov: USD 1,283.95, GBP 969.25 & EUR 1,092.51 per ounce

21 Nov: USD 1,280.00, GBP 967.04 & EUR 1,090.69 per ounce

20 Nov: USD 1,292.35, GBP 974.82 & EUR 1,096.43 per ounce

17 Nov: USD 1,283.85, GBP 969.31 & EUR 1,088.19 per ounce

16 Nov: USD 1,277.70, GBP 969.01 & EUR 1,085.53 per ounce

Silver Prices (LBMA)

24 Nov: USD 17.05, GBP 12.80 & EUR 14.38 per ounce

23 Nov: USD 17.10, GBP 12.84 & EUR 14.43 per ounce

22 Nov: USD 16.97, GBP 12.81 & EUR 14.44 per ounce

21 Nov: USD 17.00, GBP 12.85 & EUR 14.50 per ounce

20 Nov: USD 17.15, GBP 12.94 & EUR 14.56 per ounce

17 Nov: USD 17.09, GBP 12.95 & EUR 14.49 per ounce

16 Nov: USD 17.04, GBP 12.92 & EUR 14.48 per ounce

Recent Market Updates

– Brexit Budget – Grim Outlook As UK Economy Downgraded

– Geopolitical Risk Highest “In Four Decades” – Gold Demand in Germany and Globally to Remain Robust

– Gold Versus Bitcoin: The Pro-Gold Argument Takes Shape

– Money and Markets Infographic Shows Silver Most Undervalued Asset

– Is New Fed Chief A “Swamp Critter Extraordinaire”?

– Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

– Internet Shutdowns Show Physical Gold Is Ultimate Protection

– Gold Coins and Bars Saw Demand Rise 17% to 222T in Q3

– Prepare For Interest Rate Rises And Global Debt Bubble Collapse

– Platinum Bullion ‘May Be One Of The Only Cheap Assets Out There’

– World’s Largest Gold Producer China Sees Production Fall 10%

end

this fund manager states that Bitcoin is paving the way for gold’s return as true money and a global currency

(courtesy Pakiam/Bloomberg/GATA)

Bitcoin is paving the way for gold’s return as global currency, fund manager says

Submitted by cpowell on Thu, 2017-11-23 15:35. Section:Daily Dispatches

This Gold Fund Is Joining the Bitcoin Frenzy

By Ranjeetha Pakiam

Bloomberg News

Wednesday, November 22, 2017

The Old Mutual Gold & Silver Fund, which manages $220 million of mostly precious metal equities, is jumping on the bitcoin wagon.

The fund started buying in April with a mandate to allocate as much as 5 percent to cryptocurrencies, according to its manager, Ned Naylor-Leyland. The idea is to take profits from bitcoin as it advances and reinvest them in gold and silver assets, he said in an interview on Nov. 16.

“Bitcoin was explicitly designed to be digital gold,” said Naylor-Leyland. “So if you’re going to have a small proportion of a fund in bitcoin, it should be in a gold fund, because that’s exactly the point. It’s about bringing the ownership of disciplined money into the modern world. Bitcoin is paving the way for the reintroduction of gold as global money.”

Bitcoin is up more than eight times this year to top $8,000 as entrepreneurs in the field say its value lies in proof of concept for a new kind of payment system not reliant on third parties like governments, big banks, or credit-card companies. By contrast, gold has held in a tight range since February, with a short break upward in September as U.S. and North Korea tensions spiraled. …

* * *

[And fortunately for all other currency issuers, including bitcoin itself, nobody in authority or financial journalism, including Bloomberg News, ever asks WHY “gold has held in a tight range since February” — or, really, has BEEN held.]

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-11-22/gold-fund-joins-bitco..

END

Persson gives us 28 reasons why we should buy physical gold

(Persson/Bullionstar/GATA)

Torgny Persson: 28 reasons to buy physical gold

Submitted by cpowell on Thu, 2017-11-23 15:49. Section: Daily Dispatches

10:48a ET Thursday, November 23, 2017

Dear Friend of GATA and Gold:

Bullion Star proprietor Torgny Persson today offers “28 Reasons to Buy Physical Gold,” all of them excellent — and all of them also reasons why governments strive to prevent gold’s use as money by individuals and to push the monetary metal out of the world financial system. Persson’s analysis is posted at Bullion Star here:

https://www.bullionstar.com/blogs/bullionstar/reasons-buy-gold/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair’s lesson for this week: deflation

(courtesy Alasdair Macleod/GoldMoney)

Alasdair Macleod: Deflation must be embraced

Submitted by cpowell on Fri, 2017-11-24 00:19. Section: Daily Dispatches

By Alasdair Macleod

GoldMoney.com, Jersey, Channel Islands

Thursday, November 23, 2017

There are two problems with understanding deflation: it is ill-defined, and it has a bad name. This article puts deflation into its proper context. This is an important topic for advocates of gold as money, who will be aware that sound money, in theory, leads to lower prices over time and is often criticixed as an objective, because it is not an inflationary stimulation.

The simplest definition for deflation is that it is when the quantity of money contracts. This can come about in one or more of three ways. The central bank may reduce the quantity of base money, commercial banks may reduce the amount of bank credit, or foreigners, in possession of your currency from an imbalance of trade, sell it to the central bank.

The link with prices is far from mechanical, because the most important determinant of the general price level is the relative appetite for holding money, and not changes of the quantity in issue, as the monetarists would have it. All else being equal, a deflation of the money quantity can be offset by a decline in the public’s desire for cash and deposits in hand, so that the general level of prices is unaffected.

Alternatively, a fall in the general price level can occur without a corresponding monetary deflation. This happens if a general preference for holding money increases. A further consideration is a population might collectively decide, based on increased uncertainty about the future perhaps, to hoard cash instead of leaving their savings in a bank. The resulting mismatch between production on the one side, and consumption (both immediate and deferred) on the other, caused by changes in physical cash withheld from circulation, can have a noticeable effect on prices. …

… For the remainder of the commentary:

https://www.goldmoney.com/research/goldmoney-insights/deflation-must-be-…

https://www.goldmoney.com/research/goldmoney-insights/deflation-must-be-…

* * *

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.6150/shanghai bourse CLOSED UP AT 1.90 POINTS .06% / HANG SANG CLOSED UP 158.38 POINTS OR 0.53%

2. Nikkei closed UP 27.70 POINTS OR 0.12% /USA: YEN RISES TO 111.41

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 93.07/Euro RISES TO 1.1865

3b Japan 10 year bond yield: RISES TO . +.029/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.09/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.79 and Brent: 63.76

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.362%/Italian 10 yr bond yield UP to 1.792% /SPAIN 10 YR BOND YIELD DOWN TO 1.467%

3j Greek 10 year bond yield RISES TO : 5.372???

3k Gold at $1288.35 silver at:17.05: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 6/100 in roubles/dollar) 58.39

3m oil into the 58 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.41 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9813 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1645 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.362%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.342% early this morning. Thirty year rate at 2.766% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Hit Record High As European Euphoria Takes Over Forgotten China Rout

Yesterday’s China stock market rout, in which the Shanghai Composite tumbled the most since June 2016 to three month lows, and which prompted traders to question the dedication of Beijing’s plunge protection team, appears to have been forgotten, with the Composite closing unchanged on Friday after some early session weakness, as Chinese yields declined broadly across the board from 3 years highs. As a result, world stocks hovered just below record highs, and set to reverse two straight weeks of losses, and with Asian markets mostly in the green, as MSCI’s Asia-Pacific ex Japan index rose 0.2%, the optimism spread to Europe where Germany’s IFO Business Climate hit a new record high…

#EUROBOOOM! #Germany‘s #Ifo index hits another record-high!

… and now points to a Y/Y GDP growth of 4%.

It is worth keeping in mind that while European business optimism has never been higher, 90% of the responses to the survey were submitted before Angela Merkel’s coalition talks collapsed. Still, the IFO print was in line with the latest November Markit PMIs, which also printed strong and beat consensus, with Eurozone’s flash composite PMI rising to a 6.5 year high (57.5 vs. 56 expected) and is at a level that is broadly consistent with 3.5% yoy GDP growth, which Deutsche Bank called “a stunning figure for the continent.” In addition to the strong IFO data, there was more good news out of Germany where the SPD is now reportedly ready to negotiate with Merkel to form a government and end the political deadlock. In response to these two developments, the EURUSD rose to the highest level since October 13…

… and despite the strong currency European stocks which were in the red in early trading, turned positive, helped to an extent by news Asia would slash import tarfiffs in a boost for consumer goods companies, benefiting European exporters. The Stoxx Europe 600 advanced, also thanks to bank shares as Italian lenders were buoyed by a new proposal to deal with bad loans.

“It’s a bit of a Goldilocks situation (for economic growth). It is finely balanced and I think the European Central Bank has very much hinted at that in its actions, but at the moment I can’t really see how this is going to be up-ended,” said Ken Odeluga, market analyst at City Index.

Ironically, as Germany’s crisis appeared to easing, a new crisis emerged in Ireland, whose bond yields climbed to a 10-day high. The standoff over the Irish deputy leader may lead to an early election at a time when the government has to make key decisions on the Brexit process.

Finally, with the US coming back from Thanksgiving holiday for a half-trading Friday, S&P futures are up 6 points, in fresh record territory, with early optimism among merchants expected to benefit from strong Black Friday sales.

In FX, the US dollar remained under pressure after the minutes from the U.S. Federal Reserve’s latest policy meeting highlighted concerns over persistently low inflation, pushing the DXY 0.2% lower. The Bloomberg Dollar Spot Index headed for its third week of losses, the longest losing streak since July, and is down 1.6% this month.

While a drop in Treasuries supported the gauge initially, gains were capped by a rally in cable and demand for the yen after London open, although post-Thanksgiving volumes remained subdued. In Europe, bonds slipped as equities were mixed and crude oil rose. Indeed, as Bloomberg writes, a rebound in Treasury yields wasn’t enough for the dollar to sustain early gains as the London session started off with decent demand for the euro and the pound amid modest post-Thanksgiving flows. Downside Dollar risks prevail on the charts, with momentum driven by the dovish tone from Federal Reserve Chair Janet Yellen earlier in the week amid lack of progress on U.S. tax reform.

Meanwhile, “euro bulls added longs in the spot market, according to traders in Europe and London, albeit in low volumes, with some desks understaffed on Friday” Bloomberg added. As we discussed earlier, the common currency rose to its strongest level in six weeks, with hedge funds and interbank accounts leading the move higher. The latter look more confident on euro gains after the latest European Central Bank account showed that a pickup in inflation isn’t a prerequisite for policy makers to end monetary stimulus.

The South African rand heavily underperforms as S&P and Moody’s are due to reassess South Africa sovereign rating and potentially cut further.

In commodities, crude futures hit a two-year high on the shutdown of Keystone pipeline, a major crude pipeline from Canada to the United States. WTI crude futures were up 0.9% at $58.53 a barrel from their last settlement. Brent was flattish at $63.46, down 0.1% on the day. In a sign of a tightening market, both crude benchmarks are in backwardation, making it unattractive for traders to store oil for later sale.

Iron ore climbed to a two-month high, while industrial metals headed for the best weekly gain in six. Crude oil surged as OPEC and Russia were said to have agreed on a framework to extend supply cuts.

Expected economic data include November PMIs. Canada’s Valener is reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 2,597.25

- STOXX Europe 600 up 0.2% to 387.68

- MSCI Asia up 0.1% to 173.08

- MSCI Asia ex Japan up 0.2% to 568.34

- Nikkei up 0.1% to 22,550.85

- Topix up 0.2% to 1,780.56

- Hang Seng Index up 0.5% to 29,866.32

- Shanghai Composite up 0.06% to 3,353.82

- Sensex up 0.3% to 33,682.74

- Australia S&P/ASX 200 down 0.06% to 5,982.55

- Kospi up 0.3% to 2,544.33

- German 10Y yield rose 2.3 bps to 0.37%

- Euro up 0.1% to $1.1864

- Italian 10Y yield rose 1.9 bps to 1.518%

- Spanish 10Y yield rose 1.8 bps to 1.481%

- Brent futures down 0.1% to $63.62/bbl

- Gold spot down 0.1% to $1,290.27

- U.S. Dollar Index down 0.1% to 93.10

Top Overnight News

- Former national security adviser Michael Flynn’s lawyers have notified President Trump’s legal team in recent days they can no longer discuss special counsel’s investigation, NYT reports, adding it’s an indication that Flynn is cooperating with prosecutors or negotiating such a deal

- China said it will further cut import taxes for a wide range of consumer goods in a bid to boost consumption

- Germany’s biggest opposition party said it’s open to talks on backing a government led by Chancellor Angela Merkel. The move came after the Green party urged Merkel to forge a coalition with the SPD, while ruling out further attempts to gain a place in any alliance.

- German Ifo business confidence rose to a record high of 117.5 in November vs estimate of 116.7 and 116.8 in October

- BOE official Silvana Tenreyro said two more rate increases will probably be needed to get inflation back to target, but Brexit will be the real determinant of where policy goes next

- The U.K. financial services regulator confirmed all 20 banks have agreed to support the London interbank offered rate until 2021 and will work toward developing an alternative benchmark

- ECB executive board member Benoit Coeure said ECB deposit rate will stay at minus 0.4% for a long time

- U.K. consumer confidence tumbled to 106.6 in November, the lowest level since the aftermath of the Brexit vote, according to a poll by YouGov and the Centre for Economics and Business Research

- Ireland’s deputy PM is pressured to resign by opposition due to historical conduct; potential for fresh elections as PM support for deputy leads to standoff

- In a Thanksgiving address to troops, Trump credited his policies for allowing progress in Afghanistan and against Islamic State, and warned about sending sophisticated weapons to American allies that one day could become the enemy.

- U.K. Prime Minister Theresa May will meet European Union President Donald Tusk Friday as the country seeks guarantees that the bloc will allow stalled Brexit talks to make progress in exchange for new assurances over money.

- Dalian Exchange cuts trading fees for some iron ore futures contracts

- Noble Group Risks Equity Wipeout as Shares Retreat Yet Again

- Credit Suisse-Backed WeLab Is Said to Plan $500 Million IPO

- Temer Said to Agree on Brazil Pension Vote With House Chief

Asia equity markets traded higher albeit with an indecisive tone as markets lacked impetus with US away from market and mainland Chinese markets reeling from yesterday’ s late sell-off. ASX 200 (-0.1%) and Nikkei 225 (+0.1%) were negative at the open with the latter dampened by a firmer currency on return from holiday, while Mitsubishi Materials underperformed as its shares dropped nearly 10% after the Co. disclosed it had falsified product data. However, Japanese stocks then reversed losses in late trade underpinned by a mild rebound in USD/JPY. Hang Seng (+0.5%) and Shanghai Comp. (-0.1%) were mixed with the mainland index jittery after its 2.3% decline on Thursday which was attributed to tighter regulations and deleveraging concerns, as well as a slump in the bond market. 10yr JGBs were subdued with demand weighed by a reserved BoJ Rinban announcement for only JPY 390bln and in which the central bank reduced the amount of buying in 25yr+ maturities. This also coincided with overnight weakness in USTs which tripped through stops at 125.00 to the downside. PBoC injected CNY 30bln via 7-day reverse repos, CNY 10bln via 14-day reverse repos and CNY 10bln via 63-day reverse repos, for a net weekly injection of CNY 150bln vs. Prev. CNY 810bln net injection last week. PBoC set CNY mid-point at 6.5810. China Finance Ministry said it will lower import tariffs on some consumer products from December, with import duties to be cut to an average 7.7% from 17.3%.

Top Asian News

- After Sudden Rout, China Stock Traders Question Beijing Put

- China Approves Taiwan ASE-Siliconware Merger with Conditions

- Hong Kong Finance Elite’s Gym of Choice Is Said to Near Sale

- HNA Is Said to Get Nod From Malaysia for Deutsche Bank Stake

- Banks Squeeze India Firms Harder in $207 Billion Bad Loan Fight

In European trading, it is a somewhat calmer end to the week, with the Euro Stoxx rising 0.3% thus far. The growing prospect of a grand coalition in Germany has helped lift the DAX above 13,000. Move higher in European consumer staples has been aided by the announcement from China that they are to cut tariffs on imported consumer goods. As such, Nestle, Danone and Diageo have been leading the charge, with products including baby formula to be impacted. Bunds holding just edging new and deeper sub-163.00 lows in wake of the stronger than expected German Ifo survey overall, with only current conditions unable to match consensus, albeit still robust. The 10 year benchmark has now recoiled to 162.72 from 163.03 at best, with near term or intraday supports at 162.61 looking attractive. Note, Eur/Usd has now moved a tad higher towards 1.1880 having eclipsed its previous MTD best (1.1761) pre-9.00GMT in what appeared to be a bit of front-running and buy the rumour/sell the fact initially. Back to debt futures, Gilts are largely tracking Bunds and have fallen in sympathy to 125.10 from 125.28 at one stage and from Thursday’s 125.31 close. BBA mortgage data up next in the UK.

Top European News

- U.K. Consumer Confidence Hits Level Last Seen After Brexit Vote

- Man Utd.’s Fellaini Sues New Balance Over Foot-Damaging Cleats

- Clariant to Revise Strategy Yet Won’t Bow to Breakup Demands

- Putin Peace Plan Gets Boost as Syria Opposition Unites for Talks

In FX, the the Dollar showing some signs of stabilisation, if not recovery across the board, as the Index holds in above 93.000 after Thanksgiving and ahead of another shortened US session, which will keep trading conditions thin and choppy. The pound was an early gainer and outerperformer (albeit marginal) on more Brexit headlines, as UK PM May and the EU’ s Juncker both claim progress made in negotiations ahead of more ‘crucial’talks. Cable back above 1.3300 as a result, and Eur/Gbp sub-0.8900. The Euro is still firm vs he Greenback, with the headline pair breaching its November peak (1.1861), while the next key chart resistance resides at 1.1880. EUR had been further bolstered by firm German IFO data, in which the Business Climate figure rose to a record high. The yen was off best levels vs the Usd, as strong technical support just above 111.00 is respected (for now), but 112.10 widely seen capping the upside within a new lower range

In commodities, iron ore prices continued its recent upward trajectory, with the spot price hitting its highest level since September 20th amid stronger steel prices. Copper also edging higher with support from the softer USD. The price of the red metal likely helped by a 24hr strike announced yesterday’ s at Chile’ s Escondida copper mine, the worlds largest mine. WTI and Brent crude futures up 0.9% and 0.1% respectively, with focus on next weeks OPEC and Non-OPEC meeting where expectations are for a 9-month extension

Looking at the day ahead, in Germany we received the November IFO survey, which printed at a new record high of 117.5. In the US, we get the flash November PMIs. Black Friday also marks the traditional start of the US holiday shopping season and any clues to footfall and overall sales will be closely watched. One other event potentially keeping an eye on is S&P and Moody’s scheduled sovereign rating reviews of South Africa, with the country at risk of losing its investment grade status. The ECB’s Supervisory chair Ms Nouy will also speak today.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 55, prior 54.6

- Markit US Services PMI, est. 55.3, prior 55.3

- Markit US Composite PMI, prior 55.2

DB’s Jim Reid concludes the overnight wrap

Welcome to Boxing Thanksgiving Day or Black Friday as it’s commonly known these days. I must have about 10 emails in my inbox already this morning informing me of must have bargains. On the quiet holiday inspired session yesterday the most interesting story occurred after we went to print but before you read it. Chinese bourses weakened very late in the session and ended the day 2-3% lower. The CSI 300 index fell 2.96% – the biggest daily drop since June 2016. The exact cause of the sharp drop is still a bit unclear, but candidates included: the recent domestic govt. bond market sell-off and volatility, rising corporate yields, profit taking, concerns that the government may step up initiatives to cool down the strong gains in certain stocks and further reactions from the recent regulatory tightening in the asset management sector. This aside, we note that despite yesterday’s drop, the CSI index is still up c24% YTD.

This morning in Asia, markets are trading a bit mixed. Chinese bourses are down 0.4-0.5% but then again they were down a similar amount this time yesterday before the late sell-off. The Nikkei is up 0.13% after trading resumed from a holiday. Elsewhere, the Hang Seng (+0.25%) and Kospi (+0.09%) are slightly up as we type. The US markets will be open for half day trading today, with the UST 10y yields up c2bp this morning.

Staying with China, DB’s Zhiwei Zhang takes a closer look at potential macro risks from China . In his note, he tries to gauge the impact of tightening policies on tier 3 cities and finds policy tightening to be effective with a time lag of c3 months. Hence, the impact of the 1st round of tightening should have been reflected in today’s property prices, while the impact of the 2nd round is likely to be seen over the next few months. Overall, he reiterates his view that economic growth in China will slow in 4Q17 and 1H18, and that the government may have to loosen property market policy in 2Q18 to stabilise it.

Moving to Europe, the November Markit PMIs were strong and beat consensus which had anticipated a small pullback. The Eurozone’s flash composite PMI rose to a 6.5 year high (57.5 vs. 56 expected) and is at a level that is broadly consistent with c3.5% yoy GDP growth. A stunning figure for the continent. The strength was led by the manufacturing PMI, which rose 1.5pt to 60 (vs. 58.2 expected) – the highest in 17 years, while the Services PMI also slightly beat (56.2 vs. 55.2 expected). Across the region, the improvements in PMIs were broad based and driven by both core and peripherals (more later). So far, subdued core inflation has kept the pressure off the ECB to move more quickly towards tighter policy. With growth so above trend and the level of slack narrowing, the ECB may struggle to maintain expectations of a very gradual removal of easy policy. Overall, DB’s Peter Sidorov see the timing of the first rate hike at around 2020, as too far out.

Turning to Germany, there seems to be a glimmer of hope in the coalition talks to form the next government after a softening in the SPD’s position. Bloomberg reported that the Head of Germany’s biggest opposition party (SPD) Mr Schulz is now ready to hold talks with Merkel and is prepared to back her, but only for a minority led government at this stage. Notably, Ms Merkel has signalled she prefers a new election rather than a minority government. Elsewhere, other SPD members seem to be more accommodating, with SPD lawmaker Mr Lauterbach noting “…we want to help Germany and have not ruled out anything”, which includes the option of a renewed “grand coalition” with Merkel’s party, although did add this is a last resort.