GOLD: $1279.50 UP $5.65

Silver: $16.35 DOWN 8 cents

Closing access prices:

Gold $1280.30

silver: $16.45

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1282.27 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1275.30

PREMIUM FIRST FIX: $6.97

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1283.09

NY GOLD PRICE AT THE EXACT SAME TIME: $1275.40

Premium of Shanghai 2nd fix/NY:$7.69

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1277.25

NY PRICING AT THE EXACT SAME TIME: $1276.20

LONDON SECOND GOLD FIX 10 AM: $1275.50

NY PRICING AT THE EXACT SAME TIME. 1275.00

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECBER CONTRACT: 627 NOTICE(S) FOR 62700 OZ.

TOTAL NOTICES SO FAR: 2936 FOR 293,600 OZ (9.131 TONNES)

For silver:

DECEMBER

398 NOTICE(S) FILED TODAY FOR

1,990,000 OZ/

Total number of notices filed so far this month: 4392 for 21,960,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $1016/OFFER $1022, up $278 (morning)

BITCOIN : BID $10814 OFFER: $10881 // UP $881 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY ONLY 2493 contracts from 189,526 FALLING TO 187,033 DESPITE YESTERDAY’S CONTINUAL DRUBBING OF SILVER WHICH SAW OUR METAL FALL 13 CENTS AND NOW WELL BELOW THE HUGE $17.25 SILVER RESISTANCE. WE HAD SURPRISINGLY NO REAL COMEX LIQUIDATION AS WE WERE ALSO NOTIFIED THAT WE HAD ANOTHER LARGE NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 5387 EFP’S FOR MARCH AND THUS TOTAL ISSUANCE OF 5387 CONTRACTS. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 5700 EFP’S FOR SILVER ISSUED.

RESULT: A SMALLER SIZED FALL IN OI COMEX DESPITE THE CONTINUAL DRUBBING IN SILVER PRICE: YESTERDAY IT FELL 13 CENTS. HOWEVER WE HAD ALL OF OUR COMEX LONGS WHICH EXITED OUT OF THE SILVER COMEX TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 5387 EFP’S WERE ISSUED TODAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY GAINED 2894 OI CONTRACTS i.e. 5387 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 2493 OI COMEX CONTRACTS.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.935 BILLION TO BE EXACT or 134% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 398 NOTICE(S) FOR 1,990,000 OZ OF SILVER

In gold, the open interest FELL BY ONLY 3727 CONTRACTS DOWN TO 485,309 DESPITE THE HUGE FALL IN PRICE OF GOLD YESTERDAY ($9.15). HOWEVER THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY TOTALED ANOTHER 15,472 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 15,472 CONTRACTS. The new OI for the gold complex rests at 486,098. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE WITNESS THE HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING A FURTHER 13 WEEKS TO OBTAIN PHYSICAL FROM THE POINT WHEN FORWARDS BECOME DUE. IN ESSENCE WE HAD A NET GAIN OF 11,745 OI CONTRACTS: 3727 OI CONTRACTS LOST AT THE COMEX OI BUT 15,472 OI CONTRACTS NAVIGATED OVER TO LONDON. AS I REPORTED YESTERDAY: “THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP ISSUANCE. THESE GUYS ARE CROOKS. THEY ARE IMMEDIATELY REMOVING OPEN INTEREST NUMBERS BUT DELAYING RELEASE OF EFP’S FOR 24 HOURS OR GREATER.

YESTERDAY, WE HAD 20,559 EFP’S ISSUED.

Result: A HUGE SIZED DECREASE IN OI WITH THE HUGE SIZED FALL IN PRICE IN GOLD YESTERDAY ($9.15). WE HAD AN LARGE NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,472. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,472 EFP CONTRACTS ISSUED, WE HAD A NET GAIN OPEN INTEREST OF 11,745 contracts:

15,472 CONTRACTS MOVE TO LONDON AND 3727 CONTRACTS REMOVED FROM THE COMEX.

we had: 627 notice(s) filed upon for 62,700 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, no changes in gold inventory at the GLD/

Inventory rests tonight: 839.55 tonnes.

SLV

TODAY WE HAD A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: AN DEPOSIT OF 2.076 MILLION OZ WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS????

INVENTORY RESTS AT 319.206 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver SURPRISINGLY FELL BY ONLY 2493 contracts from 189,526 DOWN TO 187,033 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE LOSS IN PRICE OF SILVER PRICE (A FALL OF 13 CENTS ). HOWEVER, OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER HUGE 5387 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. AS I STATED YESTERDAY: “THIS IS THE SCENE WHERE IN THE PAST WE DID SEE MASSIVE COMEX OI CONTRACTION ALTHOUGH IT WAS MORE PRONOUNCED IN GOLD THAN WITH SILVER.” IF YOU COMPARE GOLD TO SILVER ONE CAN SEE THE DIFFERENCE: GOLD HAS A MUCH GREATER TRANSFER IN EFP’S THAN SILVER. TODAY IN REALITY WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE ADD THE OI LOSS AT THE COMEX (2493 CONTRACTS) TO THE 5387 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET GAIN OF A MASSIVE 2894 OPEN INTEREST CONTRACTS, ON TOP OF THE HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW)

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT FALL IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 5387 EFP’S ISSUED.. TRANSFERRING OUR COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER IS STRONG.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 0.43 points or .01% /Hang Sang CLOSED DOWN 103.11 pts or 0.35% / The Nikkei closed UP 04.07 POINTS OR 0.41%/Australia’s all ordinaires CLOSED UP 0.30%/Chinese yuan (ONSHORE) closed UP at 6.6093/Oil DOWN to 57.83 dollars per barrel for WTI and 63.25 for Brent. Stocks in Europe OPENED ALL RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6093. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.6069 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS SLIGHTLY WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT HAPPY TODAY.(MARKETS WEAK)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

This will move the stock market another 300 points up and cause gold to fall again. North Korea is preparing to launch another missile

( zero hedge)

ii)New images show that North Korea now has the capability of carrying multiple warheads

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

UK labour leader: Jeremy Corbyn lashes out at Morgan Stanley and yes: Yes, I am a threat to the big banks

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)RUSSIA

Stands to reason: Russian Parliament bans access to all USA reporters as the USA government yanked their TV station credentials

( zerohedge)

ii)Turkey

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The advantages to hold gold

Bullion Star/Persson/GATA)

ii)This is going to be interesting: Coinbase loses its bid to block a USA tax probe of gains made by individuals

( Rosenblatt/Bloomberg)

iii)Bill Murphy correctly states that the monetary metals camp is demoralized with the constant criminal acts by our bankers. Very shortly gold/silver will be joined by Bitcoin as the bankers flood the system with non backed bitcoin paper

( Bill Murphy/GATA)

iv)Alasdair outlines why the prospects to the dollar are poor. He is always a must read.

( Alasdair Macleod)

10. USA stories which will influence the price of gold/silver

i)Chaos last night as they delay the tax bill to today. It may include 350 billion in new tax hikes.

( zerohedge)

ii)Then late in the morning: Johnson and Daines support the tax proposal and the voting looks close:

( zerohedge)

iii)Interesting: the White House is monitoring the “bitcoin situation”

( zerohedge)

iv)What an absolute joke: Michael Flynn is to plead guilty to lying to the FBI

( zerohedge)

iv b What a riot: gold rises as Flynn is to testify against Trump saying that Donald Trump directed him to make contact with Russians.

iv c what garbage!!

( zerohedge)

iv b) Here are two scenarios, one bad for Trump and the other quite innocuous. I will go with the latter

( zerohedge)

v)Soft data Markit Manufacturing Index falls lead by new orders

( zero hedge)

Let us head over to the comex:

The total gold comex open interest FELL BY A LESS THAN EXPECTED 3,727 CONTRACTS DOWN to an OI level of 485,509 DESPITE THE HUGE SIZED FALL AND CONTINUAL DRUBBING IN THE PRICE OF GOLD ($9.15 LOSS WITH RESPECT TO YESTERDAY’S TRADING). IN ACTUAL FACT WE DID NOT HAVE ANY GOLD LIQUIDATION. WE HAD ANOTHER LARGE COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 15,472 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 15,472 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE CONSTANT BANKER RAIDS CONTINUE AS THEY TRY TO GET OUR “MATHEMATICAL PAPER LONGS” IN GOLD TO LIQUIDATE THEIR POSITIONS AT THE COMEX. SO FAR IT HAS NOT SUCCEEDED (AS THEY MORPH INTO LONDON FORWARDS) AND THUS THE CONTINUAL RAID EVEN TODAY . THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP’S CONTRACTS AFTER A COMEX OI MORPHS INTO AN EFP WHICH WAS THE REASON FOR MY 2ND LETTER TO THE CFTC.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 11,745 OI CONTRACTS IN THAT 15,472 LONGS WERE TRANSFERRED AS LONGS TO LONDON AS A FORWARD AND WE LOST 3727 COMEX CONTRACTS. NET GAIN: 12,334 contracts.

Result: a SMALLER THAN EXPECTED DECREASE IN COMEX OPEN INTEREST WITH THE HUGE SIZED LOSS IN THE PRICE OF GOLD ($12.30.) WE HAD NO REAL GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 11,745 OI CONTRACTS…AS I STATED YESTERDAY: “WITH A PROBABLE FURTHER ADDITION IN EFP TOMORROW” . FROM THE DATA, THAT CERTAINLY WAS THE CASE.

.

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest decline by 3560 contracts down to 8,348. We had 2309 notices filed upon yesterday so we lost 1,251 contracts or an additional 125,100 oz will not stand for delivery in this active delivery month of December but they did migrate over to London as a forward for February…the reason for the move is that there is not any gold for them at the comex.

January saw its open interest GAIN OF 174 contracts UP to 2093. FEBRUARY saw a loss of 733 contacts down to 377,095.

We had 627 notice(s) filed upon today for 62700 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 417,474

FINAL NUMBERS CONFIRMED FOR FRIDAY: 371,115

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY FELL BY ONLY 2,493 CONTRACTS FROM 189,526 DOWN TO 187,033 DESPITE YESTERDAY’S 13 CENT LOSS IN PRICE. HOWEVER WE DID HAVE ANOTHER STRONG 5387 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 5387. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD NO REAL LONG SILVER LIQUIDATION AS DEMAND FOR PHYSICAL SILVER REMAINS STRONG ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER AS WELL AS THAT MASSIVE MIGRATION OF EFPS OVER TO LONDON. IT SEEMS THAT ALL OF OUR LOST SILVER COMEX OI CONTRACTS HAVE MIGRATED OVER TO THE PHYSICAL HUB OF OUR PRECIOUS METALS, LONDON. ON A NET BASIS WE GAINED 2894 OPEN INTEREST CONTRACTS: 2493 CONTRACTS LOST AT THE COMEX WITH THE ADDITION OF 5387 OI CONTRACTS NAVIGATING OVER TO LONDON.

We are now in the big active delivery month of December and here the OI fell by 4390 contracts down to 2188. We had 3994 notices filed upon yesterday so we LOST 396 contracts or an additional 1,980,000 oz will NOT stand in this active delivery month of December BUT THEY DID MIGRATE THEIR LONG POSITION OVER TO LONDON..

The January contract month fell by 276 contracts down to 1395. February saw the first initial 23 oi advance. The March contract gained 2078 contracts up to 148,230.

We had 398 notice(s) filed initially for 1,990,000 oz for the DECEMBER. 2017 contract

INITIAL standings for DECEMBER

Dec 1/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

1484.298 oz

HSBC

Scotia

10 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

oz

|

| No of oz served (contracts) today |

627 notice(s)

62,700 OZ

|

| No of oz to be served (notices) |

7721 contracts

(771,600 oz)

|

| Total monthly oz gold served (contracts) so far this month |

2936 notices

293,600 oz

9.1321 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 2 customer withdrawal(s)

i) Out of HSBC: 1162.798 oz

ii) Out of Scotia: 321.500 oz (10 kilobars)

Total customer withdrawals: 1488.298 oz

we had 0 adjustment(s)

*December is the biggest delivery month of the year for gold and the fact that no gold has entered the vaults these past two days speaks volumes that there is no appreciable gold at the comex to deliver upon our longs and thus the reason for the migration to London

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 328 notices were issued from their client or customer account. The total of all issuance by all participants equates to 627 contract(s) of which 338 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (2936) x 100 oz or 293,600 oz, to which we add the difference between the open interest for the front month of DEC. (8348 contracts) minus the number of notices served upon today (627 x 100 oz per contract) equals 1,065,700 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (2936) x 100 oz or ounces + {(8348)OI for the front month minus the number of notices served upon today (627) x 100 oz which equals 1,065,700 oz standing in this active delivery month of DECEMBER (33.14 tonnes). INTERESTINGLY THERE IS ONLY 28 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

LAST YEAR WE SAW CONSIDERABLE GOLD LEAVE THE COMEX THROUGH EFP’S. TODAY WE SAW 1345 CONTRACTS OR 1,345000 OZ NOT STAND AT THE COMEX BUT THESE GUYS MIGRATED OVER FOR A LONDON FORWARD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 922,639.946 or 28.69 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,913,360.693 or 277.24 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 77 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

23,979.679 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,200,022.23 oz

Scotia

|

| No of oz served today (contracts) |

398 CONTRACT(S)

(1,990,000OZ)

|

| No of oz to be served (notices) |

1,720 contract

(8,600,000 oz)

|

| Total monthly oz silver served (contracts) | 4392 contracts

(21,960,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 2 customer withdrawal(s):

i) Out of Brinks: 21,906.679 oz

ii) Out of Delaware: 2073.000 oz ??exact weight???

TOTAL CUSTOMER WITHDRAWAL 23,979.679 oz

We had 1 Customer deposit(s):

i) Into Scotia: 1,200,022.23 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 1,200,022.23 oz

we had 1 adjustment(s)

i) Out of Brinks:

10,578.420 oz was adjusted out of the customer and this landed into the dealer account of Brinks

The total number of notices filed today for the DECEMBER. contract month is represented by 398 contract(s) FOR 1,990,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 4392 x 5,000 oz = 21,960,0000 oz to which we add the difference between the open interest for the front month of DEC. (2118) and the number of notices served upon today (398 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 4392 (notices served so far)x 5000 oz + OI for front month of DECEMBER(2118) -number of notices served upon today (398)x 5000 oz equals 30,560,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE LOST 396 CONTRACTS OR 1,980,000 OZ WILL NOT STAND AT THE COMEX BUT THESE LONGS MIGRATED OVER TO LONDON AS THERE IS NO APPRECIABLE SILVER AT THE COMEX FOR DELIVERIES.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 97,094

CONFIRMED VOLUME FOR YESTERDAY: 97,575 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 97,575 CONTRACTS EQUATES TO 487 MILLION OZ OR 69.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 55.863 million

Total number of dealer and customer silver: 237.081 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.7 percent to NAV usa funds and Negative 2.0% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.0%

Percentage of fund in silver:36.7%

cash .+.3%( Dec 1/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -0.47% (Dec 1 /2017)

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.40% to NAV (Dec 1/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.47%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.40%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 1/2017/ Inventory rests tonight at 839.55 tonnes

*IN LAST 284 TRADING DAYS: 101.40 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 219 TRADING DAYS: A NET 55.88 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 24.77 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Dec 1/2017:

Inventory 319.207 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.52%

12 Month MM GOFO

+ 1.82%

30 day trend

end

I normally provide the COT which we receive at 3 :30 pm. Since we have discovered massive amounts of long contracts in gold and silver are transferred to London (through EFP’s) with the bankers having the same obligation to deliver but over there, I felt that the data provides nothing to us to aid us in predicting what the crooks are up to. Thus I will not provide it from this day forth, as I do not want you to waste your time reading the crap data.

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Goldcore:

Risk Of Online Accounts Seen As One of Largest Brokerages In World Halts Online Trading After “Glitch”

– ‘Technical issue’ at Fidelity temporarily blocks access to online accounts and halts online trading

– Fidelity is 3rd largest brokerage by client assets: $1.7 trillion at the end of 2016

– NatWest, RBS, Ulster Bank have experienced online banking “issues” in November

– Clients left without access to funds & failed payments & little to no recourse

– Social media exposing the banks’ and online trading platforms’ shortcomings

– Reminder that online accounts can be rendered non-viable and vulnerability of absolute dependence and digital cash, digital gold etc

Editor: Mark O’Byrne

Yesterday, customers of Fidelity, the third largest brokerage in the world, found themselves unable to access their online accounts.

The company is responsible for an estimated 8% of total US wealth management. With such a huge responsibility, Fidelity, like most companies, works hard to ensure clients have access to online accounts at all times.

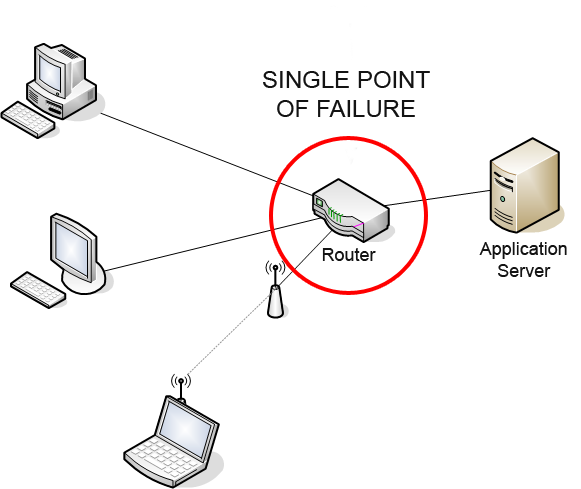

Yet it still happened, reminding investors of the risks posed by digital assets – be they stocks, gold or indeed deposits – held solely through online accounts and platforms – the ‘Single point of failure’.

Fidelity is just one of many online “outages” or “glitches” reported by financial institutions in the last year. In Europe, particularly the United Kingdom, banking customers have found themselves regularly facing bank account ‘glitches’. It is thanks to social media that some of these even come to the fore, with many organisations keen to sweep them under the carpet.

Investors, savers and, in fact, any user of online services needs to be aware of the risks and how to protect themselves in the case of a sudden ‘access denied’ message or worse, a prolonged period of not being able to access, trade and or withdraw funds from an online account.

Not like the old days…

Prior to online accounts it rarely occurred to users that they could suddenly be without access to funds, unable to make transactions or even receive their wages. Sadly, with the dawn of the internet and growing cyber security risks this is something no-one can afford to be without a plan-B for.

Outages can happen for a number of reasons, but many result in customers being unable to transact and being without funds.

In the case of Fidelity, it appears to have been an internal error, which also seems to be the common thread among many banking outages. However, cyber security is a major threat to any account that involves personal data and financial information.

Just this week Uber finally admitted exposing hackers to over 2.7 million customers’ data, putting savings and futures at risk.

We must also consider what happened in Puerto Rico for a lesson in how vulnerable we are should natural disasters impede access to much needed personal funds for days and weeks.

Absolute reliance on online accounts and digital cash and digital gold is not prudent. When such accounts can be rendered non-viable in a matter of seconds, there is little recourse for the digital saver and investor should they not also own some tangible assets.

Social media prevents cover-up

Online account failures are becoming more common. We are increasingly aware of this thanks to social media. Whilst the majority of outages experienced in the West are resolved within a few hours (in the case of Fidelity it was hours) or days, customers are left feeling nervous and frustrated and in some cases they experience real repercussions. Rents are not paid, important direct debits fail and charges are incurred.

This last month Lloyds and Halifax Bank of Scotland experienced major issues with accounts. Some account holders not only found transactions weren’t processed but also logged in to be told they no longer had an account with their bank.

Many customers in the recent Natwest outage were particularly frustrated at the bank’s lack of communication and failure to alert account holders to the problem.

“Not just an online problem, my bank card is not working now as well for online payments! People have bills to pay, how much longer?”

“You were acknowledging this problem over an hour ago but only to those that tweeted you directly. Why has it taken so long for a public tweet?”

Also this week Nationwide customers found themselves embarrassed when their funded accounts suggested they had no money:

Banking outages are becoming so common that we no longer hear reports in the mainstream media of them. Users report to feeling ’embarrassed’ but the reality and severity of the situation and can have far-reaching complications.

One would have thought that banks would have learnt from the 2012 disaster that was seen in the summer of 2012 for customers of RBS, NatWest and Ulster Bank. Users found they could not access funds for a week or more as account balances had to be manually updated. RBS was fined £56m for the inconvenience and risk placed on account holders.

Complacency amongst bank and online account users

I don’t think I am aware of a single person who has not experienced problems with bank or financial account services. Whether access to, payment issues or information failure everyone I know has come up against such issues in the past.

Concern regarding the risks to online customers is so high that the European Banking Authority this week mentioned the growing reliance on online digital platforms as a major risk to customers.

What do the majority of people do? Get a bit annoyed then shrug their shoulders and make some comment about ‘banks today’. The same goes for the likes of Fidelity, Uber and TalkTalk, non-banks who have also exposed their customers with little to no recourse for the end user.

The lethargy regarding customers’ switching banks is astonishing when one considers the problems that have been caused in recent years. This is for two reasons, the first is because there is little knowledge of the alternatives out there and secondly, because there is a belief that this is just what you have to put up with these days.

This is a sad state of affairs. Those who earn and save money have every right to be able to access their funds at all times, for whatever purpose. It is tragic that the digital, online economy has made many feel otherwise. For something that was heralded as giving customers so many more options, it is instead making many feel trapped and without options.

Cyber-attacks, natural disasters and technical errors are all very good reasons for those who wish to hold money and data with an organisation to seek out ways to diversify their investments. This is not just in terms of spreading the risks between digital accounts, but also away from solely digital assets.

Non digital gold cannot be exposed to ‘glitches’

Gold and silver often get a bad rap when it comes to discussions about their role as money. Both are pushed to the bottom of the pile when you consider the convenience of spending on a card, paying out wages or making quick gains when trading stocks and shares.

But one thing that is guaranteed with physical, allocated and segregated gold and coins and bars for delivery as offered by GoldCore, is that you know you will always have access and liquidity due to outright legal ownership of bullion. Either with bullion in your possession or with direct ownership in some of the safest vaults in the world. That is not the case with fiat electrons bank accounts or online trading accounts, whether in times of crisis or technical outages.

In addition many such platforms force you to only buy and sell through their online account and their online platform and website. Such digital platforms are “closed loop systems” where liquidity and pricing are dependent on a single platform, website and large corporation. A buyer can only buy and sell through that one online platform. An investor is in effect “captive” and massively dependent on that one counter party and a single point of failure.

No matter the town, city or country you find yourself in, times such as these pose multiple threats whether military, natural or just digital.

Today we still assume banks, companies and governments are competent and will look after our accounts. We cannot bring ourselves to imagine electricity systems and our banking systems including ATMs going down and not having access to our hard earned savings. This is despite it clearly happening increasingly frequently.

News and Commentary

Gold volatility ‘breakout’ coming soon to ‘eerily quiet’ market – Metals Expert (CNBC.com)

Gold inches up as dollar weakens after U.S. Senate tax bill stalls (Reuters)

Dollar Dips as Tax Bill Hits Snag; Stocks Decline: Markets Wrap (Bloomberg.com)

U.S. Mint American Eagle gold, silver coin sales fall sharply (Reuters)

Turkish gold trader implicates Erdogan in Iran money laundering (Reuters)

Source: City AM

“There will be pain”: Bank of England’s Carney warns against no deal Brexit (City AM)

Chance of US stock market correction now at 70 percent: Vanguard Group (CNBC)

4 habits that will make you poor (SBCH)

How central banks paved the way for bitcoin’s birth (MoneyWeek)

Sharia-compliant gold standard – Response from Muslim investors has been positive (The National )

Gold Prices (LBMA AM)

01 Dec: USD 1,277.25, GBP 946.57 & EUR 1,072.51 per ounce

30 Nov: USD 1,282.15, GBP 952.64 & EUR 1,084.06 per ounce

29 Nov: USD 1,294.85, GBP 965.70 & EUR 1,092.46 per ounce

28 Nov: USD 1,293.90, GBP 972.75 & EUR 1,088.95 per ounce

27 Nov: USD 1,294.70, GBP 969.73 & EUR 1,084.83 per ounce

24 Nov: USD 1,289.15, GBP 967.89 & EUR 1,086.37 per ounce

23 Nov: USD 1,290.15, GBP 969.93 & EUR 1,089.40 per ounce

Silver Prices (LBMA)

01 Dec: USD 16.42, GBP 12.16 & EUR 13.80 per ounce

30 Nov: USD 16.57, GBP 12.32 & EUR 14.00 per ounce

29 Nov: USD 16.90, GBP 12.60 & EUR 14.26 per ounce

28 Nov: USD 17.07, GBP 12.84 & EUR 14.36 per ounce

27 Nov: USD 17.10, GBP 12.81 & EUR 14.32 per ounce

24 Nov: USD 17.05, GBP 12.80 & EUR 14.38 per ounce

23 Nov: USD 17.10, GBP 12.84 & EUR 14.43 per ounce

Recent Market Updates

– Low Cost Gold In The Age Of QE, AI, Trump and War

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

– Financial Advice from Dr Wayne Dyer

– Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– Brexit Budget – Grim Outlook As UK Economy Downgraded

– Geopolitical Risk Highest “In Four Decades” – Gold Demand in Germany and Globally to Remain Robust

– Gold Versus Bitcoin: The Pro-Gold Argument Takes Shape

– Money and Markets Infographic Shows Silver Most Undervalued Asset

– Is New Fed Chief A “Swamp Critter Extraordinaire”?

– Deepening Crisis In Hyper-inflationary Venezuela and Zimbabwe

– UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

– Protect Your Savings With Gold: ECB Propose End To Deposit Protection

END

The advantages to hold gold

Bullion Star/Persson/GATA)

Torgny Persson: Even if you don’t eat it, gold has unique advantages

Submitted by cpowell on Thu, 2017-11-30 18:07. Section: Daily Dispatches

6p GMT Thursday, November 30, 2017

Dear Friend of GATA and Gold:

Bullion Star proprietor Torgny Persson today demolishes the old disparagement about gold’s value in emergencies — that you can’t eat it. In fact you can, Persson notes, even if it provides no nutritional value. But, Persson asks, what financial instrument is edible?

In emergencies, Persson notes, gold has advantages over other financial instruments. “Since gold is a universal money supported by a highly liquid global market, it will always be accepted everywhere at the going gold price,” Persson writes. “Gold can easily be sold. Gold can easily be traded or even bartered with, especially in non-functioning economies where the local paper currency has collapsed or has become worthless. That gold coins are regularly issued to elite military personnel in areas of conflict attests to gold’s critical benefits in times of monetary crisis and localized economic collapse.” And of course unlike other financial instruments gold has no counterparty risk.

Persson’s commentary is headlined “Eat Gold” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/bullionstar/eat-gold/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This is going to be interesting: Coinbase loses its bid to block a USA tax probe of gains made by individuals

(courtesy Rosenblatt/Bloomberg)

Coinbase loses bid to block U.S. tax probe of bitcoin gains

Submitted by cpowell on Thu, 2017-11-30 18:16. Section: Daily Dispatches

By Joel Rosenblatt

Bloomberg News

Wednesday, November 29, 2017

Coinbase Inc. lost a bid to block an Internal Revenue Service investigation into whether some of the company’s customers haven’t reported their cryptocurrency gains.

U.S. Magistrate Judge Jacqueline Scott Corley in San Francisco ruled that the tax agency’s demand for information isn’t overly intrusive. The price of bitcoin has been soaring and crossed $10,000 Tuesday.

With just 800 to 900 taxpayers reporting bitcoin gains from 2013 through 2015 in a period when more than 14,000 Coinbase users have either bought, sold, sent, or received at least $20,000 worth of bitcoin, “many Coinbase users may not be reporting their bitcoin gains,” she wrote. “The IRS has a legitimate interest in investigating these taxpayers.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-11-29/coinbase-loses-bid-to…

END

Bill Murphy correctly states that the monetary metals camp is demoralized with the constant criminal acts by our bankers. Very shortly gold/silver will be joined by Bitcoin as the bankers flood the system with non backed bitcon apper

(courtesy Bill Murphy/GATA)

Sector is demoralized and monetary metals are bargains, GATA chairman says

Submitted by cpowell on Fri, 2017-12-01 09:06. Section: Daily Dispatches

9:05a GMT Friday, December 1, 2017

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy, interviewed by GoldSeek Radio’s Chris Waltzek, says the monetary metals sector is hugely demoralized and gold and silver are the world’s most undervalued assets. The interview is eight minutes long and can be heard at GoldSeek Radio here:

http://radio.goldseek.com/nuggets/murphy.11.30.17.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

As promised to you, here is Part ii of a powerful commentary on the “War on Gold”

you do not want to miss this

(courtesy Stewart Dougherty)

Here is Part 2 of Stewart Dougherty’s “War on Gold” essay. Here’s Part 1

Magicians use distraction, deflection and misdirection to conduct their tricks. They get their audiences to look to the left while they perform their magic undetected on the right. So do con artists and swindlers.

George H. W. Bush, in a speech delivered to a joint session of Congress on 11 September 1990 entitled “Toward a New World Order,” headlined a geopolitical theme that has garnered a great deal of attention ever since. And while Bush was not the first person to use the term, it struck a global nerve when he invoked it.

Bush’s speech about the New World Order deflected and misdirected the people’s attention to the left, and prevented them from seeing the real action that was taking place

to the right: the imposition of a New World Central Banking Order throughout the west. This multi-country, supranational, autonomous, all-powerful, privately-controlled, for profit, non-auditable, monopolized, collusive, monetary leviathan has become what we call the Western Central Banking Dictatorship (WCBD). to the right: the imposition of a New World Central Banking Order throughout the west. This multi-country, supranational, autonomous, all-powerful, privately-controlled, for profit, non-auditable, monopolized, collusive, monetary leviathan has become what we call the Western Central Banking Dictatorship (WCBD).This dictatorship, and we are not being pejorative, we are simply applying the standard definition of the word to what central banking actually is, operates throughout the broadly defined “west,” which includes: the United States, Canada, Mexico, the European Union, the United Kingdom, Japan, India, New Zealand and Australia. Certain African, Asian and South American countries also play lesser parts in the regime. Dictatorially ruled by this private monetary system are the hundreds of millions of citizens who must use Euros, Yen, Rupees, and United States, Canadian, Australian and New Zealand dollars to function in their daily lives, as these fiat currencies are all 100% controlled by the regime, and are subject to whatever actions, no matter how experimental or extreme (such as Quantitative Easing and negative interest rates), the controllers, in their sole discretion, decide to take.

One of the seven core principles of Inferential Analytics, the forecasting method we have developed and use, is that all phenomena represent Life Forces, and that all Life Forces ceaselessly work to expand, evolve, empower themselves, and conquer new terrain.

Some of the most powerful Life Forces on earth are the “isms.” One of today’s most rapidly evolving “isms’ is crony communism, the national operating system now metastasizing throughout western nations to replace its dying predecessor, crony capitalism. In this expanding system of crony communism, the cronies loot the capital that was produced by the dying capitalistic system, while the masses descend into communistic impoverishment, entrapment and despair. Crony communism is a system in which the forces of diabolism, greed and evil usurp and exploit state power for their own enrichment, empowerment and dominance, at the direct expense of the communized masses.

Relentlessly increasing wealth concentration combined with spreading impoverishment and paycheck to paycheck living are two glaring signs among many others that the Life Force of crony communism has entrenched itself throughout the west, and that it is evolving and advancing.

The enabling institution for the spread of crony communism is the WCBD, which is owned and operated by the Deep State crony elite, both of which are Life Forces of plunder and human exploitation.

To those who pay attention to fiscal, monetary, economic and financial realities, it is becoming clear, despite the current frenzy of propaganda to the contrary, that the existing system is failing. In the United States, to focus on one national example, massively underfunded pensions will collapse without equally massive bailouts; every government entitlement program is bankrupt, a fact publicly admitted by the programs’ respective government overseers; structural deficits are uncontrollable under current law and can only be contained if government promises are broken at extreme expense to the economy and people; debt at all levels is exploding and structurally, must continue to explode; mass financial stress is directly observable in such forms as street-level, in one’s face homelessness, fast-spreading tent cities, and teeming under-bridge communities; paycheck to paycheck and government welfare payment to government welfare payment living is now the norm for the vast majority of the population (for example, 78% of full time workers in the United States now live paycheck to paycheck; the financial condition of part time and unemployed persons is even more dire); the savings rate has plunged as people struggle to make ends meet or engage in financially disastrous “Eat, Drink and Be Merry” binge spending programmed into their brains by the MSM, which repeatedly tells them that things have never been better and they should go shopping; overall savings are non-existent or meaningless for the vast majority of the population; among many other signs of fiscal and financial decline.

The WCBD, which includes all western central banks, the World Bank, the IMF, the ESF and their consolidating organization, the intensely secretive, predatory, and frigid BIS, is fully aware that the system is failing. The United States Federal Reserve System alone employs hundreds of Ph. D. economists and statisticians, and it is literally impossible they do not comprehend that trillions more fiat currency units must be created out of nothing to keep the monetary system functioning. Further, it is impossible that these Ph. D.s and their management do not realize that ultimately, the very design of the fiat monetary edifice means that it must erupt into a hyperinflationary bonfire, exactly as it has repeatedly done throughout history. Every “fix” now being implemented, most particularly the new, frenzied fixation on GDP growth, is an urgent attempt deflect attention away from the structural impossibilities of the monetary system, and to buy time.

For years, people have realized that certain vital government statistics, such as employment, inflation, retail sales and GDP are manipulated to tell a comforting narrative that all is well in the land. Confidence is everything in debt-dependent, fiat currency-based, consumer-expenditure-addicted economies. But for some strange reason, very few people question the most important statistic of all: money supply. This is remarkable in light of the fact that long after the emergency measures taken to re-start the system during the Great Financial Crisis (GFC), we learned that the Fed had created, in total secrecy, trillions of dollars’ worth of currency swaps that were extended to foreign central banks in order to bail out the financial system. This was so far outside the Fed’s “Dual Mandate” that it beggared belief they had actually done it, let alone without any public or even intra-governmental disclosure whatsoever.

We believe that such secret GFC money creation is just the tip of the iceberg, and that the revelation of actual, as opposed to deliberately misstated money supply would dumbfound even the most sophisticated of financial observers and require a recalculation of virtually every financial and economic metric. All of which would massively deteriorate. We believe that this is one black swan among dozens that could ignite a broad-based flight into physical gold, as people rushed to monetary high ground for financial and personal safety.

On 27 June 2017, during the British Academy President’s Lecture Q&A Session in London, Janet Yellen made the following, now famous statement in answer to a question:

“Would I say there will never, ever be another financial crisis? You know,

that would probably be going too far, but I do think we are much safer, and I hope that it will not be in our lifetimes, and I don’t believe it will be.” Many observers chalked up this comment to central banker self-congratulation and boastfulness. Or, they assumed that Ms. Yellen was making a campaign statement to land a second term as Fed Chair. We viewed it differently.

We do not believe Yellen ever had any intention of serving a second term as Fed Chair, and that her “candidacy” was theater. Yellen, Fischer and Dudley, all of whom have gotten or are getting out, realize that the monetary and financial systems are rigged to the breaking point, and that when they fail, the fallout will be uncontrollable. They know the systems are rigged, because they rigged them, and don’t want to be anywhere near them when they blow apart. This helps explain the documented elitist fascinations with long range Gulfstream jets and New Zealand, among their numerous other escape vehicles.

If Yellen had said she was not interested in serving a second term, this would have indicated that something is seriously wrong, a message central bankers never send beforehand. Having admitted, as she has, that she and many of her colleagues no longer understand inflation, an appreciation of which is absolutely critical to the entire process of central banking, she also admitted that, like Fukushima, the monetary system is melting down and out of control. Therefore, she played the game of running for a second term, even though it was just an act.

In the second to last paragraph of her 20 November 2017 resignation letter, Yellen wrote:

“I am enormously proud to have worked alongside many dedicated and highly able

women and men, particularly my predecessor as Chair, Ben S. Bernanke, whose leadership during the financial crisis and its aftermath was critical to restoring the soundness of our financial system and prosperity of our country. I am also gratified by the substantial improvement in the economy since the crisis. The economy has produced 17 million jobs, on net, over the past 8 years and, by most metrics, is close to achieving the Federal Reserve’s statutory objective of maximum employment and price stability. Of course, sustaining this progress will require continued monitoring of, and decisive responses to, newly emerging threats to financial and economic stability.” [Our italics.] This statement was an Inferential Analytics trigger, because we noted that she did not say, “if” there are “newly emerging threats to financial and economic stability.” [Cryptocurrencies/Bitcoin are seen as threat per Trump’s statement that Homeland Security was monitoring Thursday’s Bitcoin sell-off]

A second IA trigger was pulled when Jerome Powell, during his opening comments to the U.S. Senate Banking Committee reviewing his Fed Chair nomination, said the following on 28 November 2017:

“We must be prepared to respond decisively and with appropriate force to new and

unexpected threats to our nation’s financial stability and economic prosperity.” Please note two things: 1) Like Yellen, he did not say “if” there are “new and unexpected threats to our nation’s financial stability and economic prosperity;” and, 2) the nearly identical language used by both.

To us, both Yellen and Powell are warning that “newly emerging financial threats to financial and economic stability” and “economic prosperity” are on the horizon. People might comfort themselves by saying, “That is always the case,” which is true. Endogenous and exogenous risks to complicated systems always exist. The problem is that when these threats manifest themselves, what can they do about them at this point, other than print massive quantities of new currency units, a so-called medicine that has become more toxic than the disease it attempts to cure.

Central bankers go to lengths to paint a rosy picture, because belief is everything when people are living in a fantasy, which an economy that is more than $200 trillion in debt all told, is. We therefore find it extraordinary that Yellen, on her way out, and Powell, on his way in are painting a dark picture by talking about “threats to financial and economic stability.” They would not be using these words if they did not know that something serious is on the horizon. They know, because the threats are of the WCBD’s direct making.

Regarding the specific comment Yellen made in London, we believe she was saying that the Fed in particular, and the WCBD in general, have now transferred the mechanisms perfected over the past 40 years to control precious metals prices, to western stock markets, in order to control their prices. The only difference being that while they have used sophisticated, computerized price manipulation techniques to push precious metals prices down, they are using the same techniques to push stock prices up.

Why? For four primary reasons: 1) To prevent the pension system from collapsing, which would bring down the entire economy and banking system with it; 2) To generate badly needed income and capital gains tax revenue; (Please keep in mind that most employee stock option gains are taxed as individual income, and result in top income tax rates being imposed; full, uncapped Medicare taxes being paid by both employee and employer; and, the Obamacare 0.9% Medicare surtax being collected. Therefore, such stock option gains represent a trifecta tax bonanza for the government. Additionally, capital gains over a minor threshold amount, which is not indexed to inflation, are now subject to the Obamacare 3.8% surtax, which the proposed “Repeal and Replace” House and Senate legislation never rescinded, evidence that the government is dependent upon the surtax revenue and will not let it go. As we can see, Republican legislators spoke with a forked tongue; while they said they hated Obamacare, they forgot to mention that they love its tax revenue and have no intention of parting with it); 3) To foster the “Wealth Effect,” and thereby stimulate consumer spending, which is critical to employment, corporate profits, corporate profit taxes and state sales taxes. In deliberately creating a consumer spending, as opposed to a production economy, the government and the citizens have become slaves to a low-to-zero savings, binge spending, consumer impoverishment economy, which is a Castle in the Air and a mirage that will fade; 4) To facilitate a high-intensity, big-dollar insider trading, front running and looting spree, via the dissemination of inside information to the elite regarding upcoming WCBD policy decisions and government economic reports, all of which move markets in predictable, sizable, and enormously profitable ways for those who can exploit them in advance. The surge in wealth inequality is not natural, and not an accident.

In addition to precious metals price controls and the legalization of bail-in banking, numerous other developments, such as the accelerated push to eliminate cash all suggest that the people are being elaborately set up for epic financial slaughter by the Deep State plunderers. The Deep Statists are intent on eliminating financial sanctuaries that are outside their bail-in dragnets. In past situations of this kind, gold has performed admirably in protecting wealth and, far more important, human lives.

We mentioned in Part 1 that there is a clue in the Financial Times article that demonstrates the statists’ fear that they cannot prevent broad scale interest in gold from developing among the people. The FT article argued that due to dealer commissions, physical gold is more expensive than its electronic counterpart. It also stated that physical coin dealers are dangerous because they are “exploitative” and “shady.” The conclusion the author reached for his dear readers to follow was this: “More gold will be traded electronically,” because if one is going to buy gold, electronic products are the better deal.

This is exactly what the increasingly concerned Deep Statists are trying to steer people into doing: buying electronic, not physical gold. They appear to realize that they might not be able to control the gold price for much longer, and that if the price gets away from them, the Cryptocurrency Effect will be activated in gold. If that happens, a price Vesuvius lies ahead. The volcano, they cannot stop. All they can do is misdirect the people’s money into their phony electronic gold products, to sterilize and control those funds. Then, when the price does explode, they will force customers to accept involuntary cash settlements and close out the electronic acounts. The customers will get fiat currency at the precise time when it is plunging in value, and the statists will keep any physical gold they might have purchased with customers’ funds.

As Sun Tzu said, in war, you must know the enemy and yourself if you intend to win. We hope that our article has helped readers know the enemy a bit better. The next task is to know yourself; to ask yourself, “Given what I know, what should I do?” In our opinion, and this is just our personal point of view, not an investment recommendation, which we are not licensed to provide, the fact that the Deep State elitists are stopping at nothing to discourage you from buying physical gold is the precise reason why you should buy it. And if this article has resonated with you, then you probably also believe, as we do, that the time to financially prepare yourself is getting short. The current intensity of price maneuvering and manipulation in a broad variety of markets implies that the center is losing hold, and that something wicked this way comes.

Stewart Dougherty is the creator of Inferential Analytics, a forecasting method that applies to events proprietary, time-tested principles of human instinct, desire and action. In his view, forecasting methods not fundamentally based upon principles of human action are unlikely to be reliable over time. He is a graduate of Tufts University (BA) and Harvard Business School (MBA). He developed expertise in strategic analysis and planning during a 35+ year business career, has traveled to and conducted research in over 25 countries and has refined Inferential Analytics into a reliable predictive instrument over a period of 17+ years

|

end

Alasdair outlines why the prospects to the dollar are poor. He is always a must read.

(courtesy Alasdair Macleod)

Alasdair Macleod: The dollar’s prospects are poor

Submitted by cpowell on Fri, 2017-12-01 09:25. Section: Daily Dispatches

9:24a GMT Friday, December 1, 2017

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod writes this week that the next credit crisis will diminish demand for dollars and that if governments don’t obstruct them, cryptocurrencies will diminish demand for all government currencies. Such developments, Macleod concludes, will support gold prices. Macleod’s analysis is headlined “Monetary Update for the Dollar” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/monetary-update-fo…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Alasdair Macleod…

A dispassionate look at the quantities and flows of fiat dollars tells us much about the current state of the US economy, and therefore prospects for the dollar itself.

This is a starting point for understanding the dynamics likely to affect the dollar’s purchasing power after the next credit-induced crisis, which are now beginning to clarify. That is the purpose of this article, which starts by updating the most recent developments in the quantity of fiat money (FMQ), the greatest of all monetary pictures. [i]

Inflation of the fiat money quantity appears to be stalling, as the above graph attests. It has increased just under 3% over the last year to October, compared with 5.8% the previous year. It seems the monetary punch bowl, while not taken away, is lacking its post-crisis drive.

By far the largest component is deposits and savings held at the banks, which total $11,132bn, and have grown a vigorous 7.4% during the last year. The component that has a significantly lower balance is the US Treasury general account, which has reduced from $348.7bn to $160.4bn, knocking FMQ’s overall growth rate. The fact that it is this account that is holding back FMQ inflation tells us that FMQ inflation in public hands is still very much alive.

In recent months, there has been heated debate about whether the US economy is stalling or not, and that perhaps the widely anticipated increase in the Fed funds rate next month will be the last for some time. However, the continuing growth in depositors’ bank balances suggests consumer demand is reasonably robust and interest rate rises are not over.

We are of course skating over an important consideration, the ownership of these deposits. Long-standing experience tells us that when the banks first increase their loans to their customers after a credit crisis, they tend to favour the lower risk accounts. These are the big corporates capable of bringing not only interest income, but fees as well. Additional loans are drawn down through payments to their suppliers, who tend to be large and medium-sized businesses. Thus, deposits are created, and they filter down from the larger to smaller businesses over time. And as these businesses employ extra staff, their personal bank balances benefit as well.

This trickle-down effect conventionally disperses the ownership of bank balances from the large to the less large, and eventually the general public. But today, life is not so simple. The general public is up to its neck in credit card, auto, student and mortgage debt. The creation of bank deposits is therefore the result of consumer debt, more than business loans. This issue is explored further later in this article.

Business finance

It is also clear that we need to dig deeper to see what is going on with American businesses, and whether they collectively think trading conditions merit further investment. There is no doubt the Fed is keeping interest rates suppressed below the level indicated by time-preference, the condition required to justify increasing business investment.[ii] This can be measured by seeing what proportion of overall monetary expansion is being applied to business investment, and whether it is increasing or decreasing relative to the total, which is represented by the blue line in the following chart.

The blue line represents business loans as a percentage of broad money (M2). An increasing percentage represents periods, when in aggregate, businesses are investing in production. A decline represents periods when businesses decide returns on business investment are less than the cost of financing. Instead, they pay down their loans, or alternatively the banks decide to call them in. Before 1980, investment downturns were driven by both these reasons, while after 1980, central bank interest rate policy increasingly became the overriding factor. The correlation between interest rates and the expansion and contraction of business loans, while readily apparent, should be regarded in this light.

There are other factors to consider. Since the last financial crisis, a substantial portion of business debt taken out has been for share buy-backs, so even less investment has been applied to production than the chart implies. Before the last financial crisis, FMQ had been growing at a reasonably constant annual average of 5.9% (the dashed line in the first chart), after which the quantity of fiat money increased with unprecedented rapidity. The chart shows that lending to businesses as a percentage of money supply has been anaemic at best compared with lending to other categories since the crisis, even though it has increased in absolute terms.

Whichever way you cut it, this chart shows the US’s supply-side is now stalling (circled), particularly following the quarter-point increases in the Fed funds rate from December 2015 onwards (also circled). And with only 15.5% of M2 applied to business loans, the other 74.5% is applied to consumer credit and purely financial activities.

This finding is consistent with business surveys that indicate a mixed picture for US production, and supports concerns in the investment community that the economy faces a low-growth future, with a significant risk of a downturn.

The lacklustre performance of this, the supply side of the US economy, is in contrast with the pick-up in productive activity elsewhere in the world. Driven by China’s voracious appetite for commodities, the outlook for all commodity exporters is improving. Europe is being linked into the Chinese economy through two-way trade, driving the euro up on improving economic prospects. Japan similarly benefits from the expansion of regional trade with China and all the East Asian nations. The only exception to this positive outlook is for the US and therefore its currency, the dollar.

Credit flows have reversed

The decline of US domestic business lending as a proportion of the total is the consequence of decades of monetary and economic meddling with free markets. When money was sound, or relatively so, the bulk of non-financial lending was to commercial businesses, and it was their demands for funds that drove interest rates, in the context of monetary policy. This is no longer so. Consumer credit became an increasingly important economic factor, particularly after 1980. Excluding mortgage debt, it is currently 27.5% of M2, compared with business loans at 15.5%. While business loans are interest-rate sensitive, consumer credit is very much less so, being comprised of credit cards, motor vehicle and student loans.

Mortgages are a far larger and additional element of consumer credit, and the majority of them in America are fixed rate, with only 10% being variable.[iii] As we have seen, the small increases in interest rates have already stalled business loan growth, but it will need further interest rate increases to moderate the expansion of consumer debt. So, if the Fed is forced to raise rates further from here, there will be a disproportionally negative effect on businesses.

The effect of bank credit growth switching to consumers has been to reverse credit flows from their original direction. Instead of credit flowing from the financial sector to finance business expansion, which in turn leads to increased consumption, business is now bypassed and consumption is financed directly. Instead, deposit balances are accumulating in the bank accounts of financial entities as a consequence of debt origination taken up directly by the consumer.

In terms of credit flows, a consumption-driven economy is therefore very different from a production-driven economy. Consequently, production of goods fails to keep pace with demand. This surplus demand is satisfied by imports, which sooner or later leads to a general price adjustment through a decline in the currency.

Not enough attention is paid to these flows and the consequences of reversing the natural order of monetary events. They are an important contributor to the trade deficit, which has little or nothing to do with the current administration’s obsession with supposedly unfair trade practices by foreign manufacturers. Inevitably, the expansion of credit in favour of the consumer while neglecting the supply side creates net selling of the dollar, requiring inward investment or government intervention to counteract its decline.

There are other reasons why the dollar is set to decline anyway. Foreign ownership is already at saturation point, and further portfolio flows into foreign hands appear to be stalling. Additionally, China is pursuing a policy of discouraging use of the dollar for her own trade. The world is therefore awash with dollars that fewer people need or want.

This brings us back to the importance of the fiat money quantity. While the dollar was rising in terms of its purchasing power against both commodities and other currencies, it did not matter that the FMQ was increasing above its long-term trend rate. Those conditions have now changed, and the outlook for the dollar in terms of commodities and other currencies is for it to weaken. And when the next credit crisis comes along, instead of there being a scramble for dollar liquidity, after the initial hiatus we can expect a public desire to hold alternatives to bank deposits. Therefore, the next credit crisis should threaten the dollar with a significant fall in its purchasing power in the years following.

A falling purchasing power for the dollar is obviously beneficial for the gold price. How beneficial can be visualised from the next chart, which shows gold priced in dollars adjusted for the increase in FMQ since the price was first fixed at $35.

Adjusted for the increase in FMQ, the gold price today is in the same territory as it was when the gold pool failed in the late 1960s, and at the turn of the century when gold sank to $260. It is clear from this chart that the gold price is unlikely to go lower and has substantial upside, now that the dollar is poised for further weakness.

There is more on the dollar-gold relationship towards the end of this article.

The impact of cryptocurrencies

The context of our analysis so far has been restricted to the well-established credit cycle. This consists of a period of credit expansion, facilitated by central banks suppressing interest rates, leading to price inflation, and thereby forcing central banks to raise interest rates until credit stops expanding. Inevitably, when bank credit stops expanding, businesses get into difficulty, the economic climate sours, and bank credit begins to implode. The correlation between changes in bank credit applied to business loans and interest rates managed by the central banks is evident in the second chart in this article.

It should be clear that the current period of credit expansion, being unprecedented in its magnitude, will be followed by a credit crisis potentially worse than the last. Furthermore, as posited above, the rapid expansion of base money, which is the traditional central bank response to a credit crisis, will coincide with a surfeit of deposited dollars in the banking system accumulated since the last crisis. Accordingly, instead of a deflationary event being triggered, the next crisis will increase these deposits even further, and is likely to trigger an inflationary event, once the dust settles. Depositors, who are not finance companies, will almost certainly attempt to reduce their swollen bank accounts, in favour of precious metals, and perhaps tangible assets such as art, land and buildings as well.

We now must consider the impact of a new element, cryptocurrencies. Assuming that central banks do not prohibit commercial banks from processing payments to facilitate cryptocurrency settlements, it is likely the cryptocurrency bubble will not only survive the next credit-induced economic crisis, but be fuelled by it. This being the case, increasing public participation becomes an additional destabilising factor for fiat currencies themselves.

Before the next credit crisis, there could be increasing speculation in cryptocurrencies, providing windfall profits for growing numbers of the general public all round the world. This will have two affects. Fiat money will be diverted from other uses into settling cryptocurrency transactions. This will require additional expansion of bank credit, if not for this direct purpose, to satisfy continuing economic activities that benefit indirectly from the bubble’s wealth creation. And secondly, the decline in preference for fiat money in favour of holding cryptocurrencies is could trigger a wider decline in the purchasing power of state-issued money.

It is perhaps time to consolidate our thoughts so far, and summarise the danger to the dollar. Unlike the last credit-induced crisis, which triggered a flight into the dollar, the dynamics building for the next crisis are wholly different, even though it will happen for the same underlying reasons. This time, the world is flooded with dollars, both in the form of investment money and bank deposits.

The Fed’s solution to a credit-induced crisis is always to inject more money into the system. But there is already too much money in circulation, illustrated by the above-trend increase in FMQ since August 2008. Foreign ownership of dollars in portfolios also increased from $9.641 trillion in 2009 to $17.139 trillion in 2016 (according to TIC data from the US Treasury), the unwinding of which will undoubtedly put pressure on the dollar’s exchange rate, in addition to other negative trade-related factors. Furthermore, fiat currency in the banks and at the Fed is now $6.4 trillion above its long-term sustainable growth rate.

There is therefore, already a recipe for a substantial fall in the dollar, adversely affecting all other fiat currencies linked to it. This problem is compounded by the lack of headroom to raise interest rates without aggravating the overall debt situation. The addition of cryptocurrencies as an alternative to holding fiat cash, if the cryptocurrency bubble is still extant at the time of the next credit crisis, can be expected to offer the public an alternative to holding fiat currencies deposits in the banks. This is all bad news for the dollar.

The implications for gold

Some commentators have taken the view that cryptocurrencies are the new gold, sound money compared with unbacked fiat currencies. I have written elsewhere why cryptocurrencies are not money, but if they are going to undermine anything, it is not gold, but fiat currencies.

In the short-term, along with the more credible alternatives, bitcoin has had an incredible run, hitting $11,400 this week. There is perhaps too much bullishness in the price for the short-term, and while it has the potential to go much higher, a period of consolidation would be healthy. If that doesn’t happen, the price could blow off, doing serious damage to cryptocurrencies’ credibility in the longer term. It would also encourage governments to kill the phenomenon.