GOLD: $1239.90 DOWN $5.15

Silver: $15.65 DOWN 11 cents

Closing access prices:

Gold $1243.70

silver: $15.72

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1254.21 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1244.60

PREMIUM FIRST FIX: $9.61

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1258.35

NY GOLD PRICE AT THE EXACT SAME TIME: $1251.00

Premium of Shanghai 2nd fix/NY:$8.35

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1251.40

NY PRICING AT THE EXACT SAME TIME: $1250.40

LONDON SECOND GOLD FIX 10 AM: $1240.90

NY PRICING AT THE EXACT SAME TIME. 1240.50

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECBER CONTRACT: 207 NOTICE(S) FOR 20700 OZ.

TOTAL NOTICES SO FAR: 6306 FOR 630600 OZ (19.614 TONNES),

For silver:

DECEMBER

198 NOTICE(S) FILED TODAY FOR

990,000 OZ/

Total number of notices filed so far this month: 5484 for 27,420,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $17,177/OFFER $17,299, UP $571 (morning)

BITCOIN : BID $17,191 OFFER: $17,307 // UP $572 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

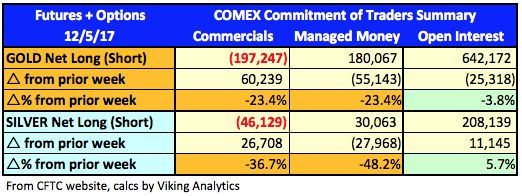

In silver, the total open interest SURPRISINGLY ROSE BY A WHOPPING 3715 contracts from 196,556 RISING TO 200,271 DESPITE YESTERDAY’S SMALL SIZED 4 CENT FALL IN SILVER PRICING. WE HAD SURPRISINGLY NO REAL COMEX LIQUIDATION AND ON TOP OF THIS, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GIGANTIC NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 2940 EFP’S FOR MARCH (AND ZERO FOR DEC AND OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 2940 CONTRACTS. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 2094 EFP’S FOR SILVER ISSUED.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DECEMBER:

27,342 CONTRACTS (FOR 8 TRADING DAYS TOTAL 27,342 CONTRACTS OR 136.71 MILLION OZ: AVERAGE PER DAY: 3,417 CONTRACTS OR 17.088 MILLION OZ/DAY)

RESULT: A HUGE SIZED RISE IN OI COMEX DESPITE THE 4 CENT FALL IN SILVER PRICE. HOWEVER WE HAD ALL OF OUR COMEX LONGS WHICH EXITED OUT OF THE SILVER COMEX TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 2940 EFP’S WERE ISSUED TODAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY GAINED 6655 OI CONTRACTS i.e. 2940 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3715 OI COMEX CONTRACTS. AND ALL OF THIS INCREASED DEMAND HAPPENED WITH THE TINY FALL IN PRICE OF SILVER BY 4 CENTS AND A LOW CLOSING PRICE OF $15.76 YESTERDAY. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.001 BILLION TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DECEMBER MONTH/ THEY FILED: 198 NOTICE(S) FOR 990,000 OZ OF SILVER

In gold, the open interest FELL BY FAIR SIZED 1842 CONTRACTS DOWN TO 451,195 WITH THE TINY SIZED FALL IN PRICE OF GOLD YESTERDAY ($1.45). HOWEVER, THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED ANOTHER 7,704 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 7704 CONTRACTS. The new OI for the gold complex rests at 451,195. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE WITNESS THE HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND ON TOP OF THAT IT IS TAKING A FURTHER 13 WEEKS TO OBTAIN PHYSICAL FROM THE POINT WHEN FORWARDS BECOME DUE. IN ESSENCE WE HAVE A HUGE GAIN OF 7411 OI CONTRACTS: 1842 OI CONTRACTS LEFT THE COMEX BUT 7704 OI CONTRACTS NAVIGATED OVER TO LONDON. THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP ISSUANCE. THEY ARE IMMEDIATELY REMOVING COMEX OPEN INTEREST NUMBERS BUT DELAYING RELEASE OF EFP’S FOR 24 HOURS OR GREATER AS NO DOUBT THEY ARE NEGOTIATING WITH THE LONGS FOR A FIAT BONUS.

FRIDAY, WE HAD 5,694 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DECEMBER STARTING WITH FIRST DAY NOTICE: 107,825 CONTRACTS OR 10.783 MILLION OZ OR 335.00 TONNES (8 TRADING DAYS AND THUS AVERAGING:13.478 EFP CONTRACTS PER TRADING DAY OR 1.3478 MILLION OZ/DAY)

Result: A TINY SIZED DECREASE IN OI WITH THE FALL IN PRICE IN GOLD TRADING YESTERDAY ($1.45). WE HAD A LARGE NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7704. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7704 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 5862 contracts:

7704 CONTRACTS MOVE TO LONDON AND 1842 CONTRACTS LEFT THE COMEX.

we had: 207 notice(s) filed upon for 20,700 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, SURPRISINGLY NO CHANGES in gold inventory at the GLD/

Inventory rests tonight: 842.81 tonnes.

SLV

OH OH!!/ WITH SILVER DOWN AGAIN TODAY BY 11 CENTS/WE HAD ANOTHER HUGE INVENTORY GAIN OF 1,415,000 OZ. SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS AND YET SLV INVENTORY RISES??/

INVENTORY RESTS AT 326.714 MILLION OZ/

oh oh!!!TODAY WE HAD ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A ‘DEPOSIT” OF 944,000 OZ DESPITE THE CONSTANT RAID ON SILVER. SILVER HAS BEEN DOWN 9 STRAIGHT TRADING DAYS.

INVENTORY RESTS AT 325.299 MILLION OZ

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 3715 contracts from 196,556 UP TO 200,271 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY FALL IN PRICE OF SILVER AND CONTINUAL BOMBARDMENT (A FALL OF 4 CENTS ). HOWEVER,OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER HUGE 2940 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. ON TOP OF THIS, IF WE TAKE THE OI GAIN AT THE COMEX 3715 CONTRACTS TO THE 2940 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET GAIN OF 6655 OPEN INTEREST CONTRACTS, AND YET WE STILL HAVE A HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW). THE NET GAIN TODAY IN OZ: 33.27 MILLION OZ!!!

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT FALL IN PRICE (WITH RESPECT TO FRIDAY’S TRADING). BUT WE ALSO HAD ANOTHER 2940 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER INTENSIFIES DESPITE THE CONSTANT RAIDS.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 41.38 points or 1.25% /Hang Sang CLOSED DOWN 171.41 pts or 0.59% / The Nikkei closed DOWN 72.56 POINTS OR 0.32%/Australia’s all ordinaires CLOSED UP 0.19%/Chinese yuan (ONSHORE) closed DOWN at 6.6187/Oil UP to 58.86 dollars per barrel for WTI and 65.68 for Brent. Stocks in Europe OPENED ALL IN THE GREEN EXCEPT SPAIN. ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6189. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6272 //ONSHORE YUAN SLIGHTLY WEAKER AGAINST THE DOLLAR/OFF SHORE MUCH WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT VERY HAPPY TODAY.(WEAK MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

These guys have nothing else to do so why not try and hack into Bitcoin as steal them. This is why you do not buy bitcoins

(courtesy Mac Slavo/SHTFPlan.)

b) REPORT ON JAPAN

3 c CHINA

The Chinese banks push back on their $4Trillion shadow banking sector. It is really a Ponzi scheme where these lenders are insolvent but too keep paying interest they need new suckers coming in

( zerohedge)

4. EUROPEAN AFFAIRS

Mark Carney is now forced to explain to the Chancellor of the Exchequer why inflation is running 1% above the approved allowance of 2%. Inflation is surging in Great Britain

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

You must may attention to these guys: the world’s largest shipping line, Copenhagen’s Maersk states that global growth is waning

( zerohedge)

7. OIL ISSUES

A huge explosion in Austria sends natural gas surging in the uK which will also not help them in trying to contain inflation

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Ronan Manley discusses why Singapore is great for gold investors

( Ronan Manly/Bullionstar)

ii)As Goldman Sachs discusses, Bitcoin does not steal demand for gold. The author gives 3 reasons for this:

( GoldmanSachs/GATA)

10. USA stories which will influence the price of gold/silver

iv)The walls are closing in on Peter Strozok over involvement in issuing that FISO warrant

vi) the real truth on the USA economy

Let us head over to the comex:

The total gold comex open interest FELL BY A FAIR SIZED 1842 CONTRACTS DOWN to an OI level of 451,195 WITH THE FALL IN THE PRICE OF GOLD ($1.45 LOSS WITH RESPECT TO YESTERDAY’S TRADING). IN ACTUAL FACT WE DID NOT HAVE ANY GOLD LIQUIDATION. WE HAD ANOTHER LARGE COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 7704 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 7704 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE CONSTANT BANKER RAIDS CONTINUE AS THEY TRY TO GET OUR “MATHEMATICAL PAPER LONGS” IN GOLD TO LIQUIDATE THEIR POSITIONS AT THE COMEX. IT LOOKS LIKE IT HAS SUCCEEDED WITH OUR MATHEMATICAL PLAYERS AS THEY CONTINUE TO INCREASE ON THE SHORT SIDE (SEE SATURDAY’S COT REPORT) BUT THE OTHER SMART HEDGE PLAYERS MORPH INTO LONDON FORWARDS AND RECEIVE A FIAT BONUS FOR THEIR EFFORT. THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP’S CONTRACTS AFTER A COMEX OI MORPHS INTO AN EFP WHICH WAS THE REASON FOR MY 2ND LETTER TO THE CFTC.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 5862 OI CONTRACTS IN THAT 7704 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 1842 COMEX CONTRACTS. NET GAIN: 5862 contracts OR 586,200 OZ OR 18.23 TONNES

Result: AN FAIR SIZED DECREASE IN COMEX OPEN INTEREST WITH THE FALL IN THE PRICE OF GOLD YESTERDAY ($1.45.) WE HAD NO REAL GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 5862 OI CONTRACTS…

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest surprisingly rise by 16 contracts up to 2194. We had 4 notices filed upon yesterday so we gained 20 COMEX contracts or an additional 1900 oz will stand for delivery AT THE COMEX in this active delivery month of December

January saw its open interest LOSS OF 25 contracts DOWN to 1959. FEBRUARY saw a loss of 1925 contacts down to 344,282.

We had 207 notice(s) filed upon today for 20700 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 208,302

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 201,009

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY ROSE BY A TOTALLY UNEXPECTED 3715 CONTRACTS FROM 196,556 UP TO 200,271 DESPITE YESTERDAY’S TINY 4 CENT GAIN IN PRICE (AND CONTINUAL RAIDING OF OUR PRECIOUS METALS). HOWEVER WE DID HAVE ANOTHER STRONG 2940 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 2940. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WITHOUT A DOUBT WE HAD NO LONG SILVER LIQUIDATION AS DEMAND FOR PHYSICAL SILVER REMAINS STRONG ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER AS WELL AS THAT MASSIVE MIGRATION OF EFPS OVER TO LONDON. IT SEEMS THAT ALL OF OUR LOST SILVER COMEX OI CONTRACTS HAVE MIGRATED OVER TO THE PHYSICAL HUB OF OUR PRECIOUS METALS, LONDON. ON A NET BASIS WE GAINED 6655 OPEN INTEREST CONTRACTS:

3715 CONTRACTS GAIN AT THE COMEX WITH THE ADDITION OF 2940 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN: 6655 CONTRACTS

We are now in the big active delivery month of December and here the OI ROSE by 22 contracts UP to 827. We had 1 notice filed upon yesterday so we GAINED 23 contract or an additional 115,000 oz will stand in this active delivery month of December.

The January contract month FELL by 72 contracts DOWN to 1306. February saw a LOSS OF 20 OI contract FALLING TO 36. The March contract GAINED 3605 contracts UP to 161,208.

We had 198 notice(s) filed for 990,000 oz for the DECEMBER 2017 contract

INITIAL standings for DECEMBER

Dec 12/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

207 notice(s)

20,700 OZ

|

| No of oz to be served (notices) |

1987 contracts

(198,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6306 notices

630600 oz

19.614 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 0 customer withdrawal(s)

Total customer withdrawals: nil oz

we had 3 adjustment(s)

i) Out of Brinks: 7399.55 oz was removed from the dealer account and placed into the customer account of Brinks

ii) Out of HSBC 23,682.641 oz was removed from the dealer account and placed into the customer account

iii) Out of Manfra:

2893.500 oz was removed from the dealer and placed with the customer account of Manfra.

*December is the biggest delivery month of the year for gold and the fact that no gold has entered the vaults these past three trading days speaks volumes that there is no appreciable gold at the comex to deliver upon our longs and thus the reason for the migration to London

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 207 contract(s) of which 175 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (6306) x 100 oz or 630,600 oz, to which we add the difference between the open interest for the front month of DEC. (2194 contracts) minus the number of notices served upon today (207 x 100 oz per contract) equals 829,300 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (6306) x 100 oz or ounces + {(2194)OI for the front month minus the number of notices served upon today (207) x 100 oz which equals 829,300 oz standing in this active delivery month of DECEMBER (25.79 tonnes). THERE IS 28 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 20 COMEX CONTRACTS STANDING OR 2000 OZ WILL STAND AT THE COMEX AND QUEUE JUMPING RETURNS TO GOLD.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER 2016, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 979,623.576 or 27.35 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,982,142.308 or 279.38 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 75 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

145,881.770 oz

brinks

Delaware

Scotia

|

| Deposits to the Dealer Inventory |

600,396.340

CNT

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

198

CONTRACT(S)

(990,000 OZ)

|

| No of oz to be served (notices) |

629 contract

(4,145,000 oz)

|

| Total monthly oz silver served (contracts) | 5484 contracts

(27,420,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 1 deposit(s) into the dealer account:

i) Into CNT: 600,396.340 oz

total dealer deposit: 600,396.340 oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

we had 3 customer withdrawal(s):

i) Out of Delaware: 1946.800 oz

ii) Out of Brinks: 83,838.870 oz

iii) Out of Scotia: 60,096.100 oz

TOTAL CUSTOMER WITHDRAWAL 145,881.770 oz

We had 0 Customer deposit(s):

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: nil oz

we had 2 adjustment(s)

i) Out of Brinks: 147,596.100 oz was adjusted out of the customer and this landed into the dealer account of Brinks

ii) Out of CNT: 591,944.199 oz was adjusted out of the dealer and this landed into the customer account of CNT

The total number of notices filed today for the DECEMBER. contract month is represented by 198 contract(s) FOR 990,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 5484 x 5,000 oz = 27,420,0000 oz to which we add the difference between the open interest for the front month of DEC. (827) and the number of notices served upon today (198 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 5484 (notices served so far)x 5000 oz + OI for front month of DECEMBER(827) -number of notices served upon today (198)x 5000 oz equals 31,565,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE GAINED AN ADDITIONAL 23 CONTRACTS OR 115,000 OZ THAT WILL STAND AT THE COMEX AS QUEUE JUMPING ACCELERATES WITH RESPECT TO SILVER. BOTH GOLD AND SILVER ARE NOW EXPERIENCING QUEUE JUMPING.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 61,895

CONFIRMED VOLUME FOR FRIDAY: 59,951 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 59,951 CONTRACTS EQUATES TO 299 MILLION OZ OR 42.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 56.846 million

Total number of dealer and customer silver: 240.357 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.9 percent to NAV usa funds and Negative 1.9% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.3%

Percentage of fund in silver:36.4%

cash .+.3%( Dec 12/2017)

2. Sprott silver fund (PSLV): NAV FALLS TO -0.68% (Dec 12 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.24% to NAV (Dec12/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.68%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.24%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 12/2017/ Inventory rests tonight at 842.81 tonnes

*IN LAST 291 TRADING DAYS: 98.14 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 226 TRADING DAYS: A NET 59.14 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.03 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

Dec 12/2017:

Inventory 326.414 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.52%

12 Month MM GOFO

+ 1.82%

30 day trend

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Gold and silver COT suggests bottoming and price rally coming

– Speculators cut way back on long positions and added to short bets

– Commercials/banks significantly reduced short positions

– Commercial net short position saw biggest one-week decline in COMEX history

– ‘Big 4’ commercial traders decreased their short positions by 28,800 contracts

– Seasonally, January is generally a good month to own gold (see table)

– “If history is still reliable, January will be a great month to own precious metals”

Have you found the gold price in the last few months to be particularly boring? Well, fear not as it looks like it might all be about to take a turn upwards. Last Friday’s Commitment of Traders (COT) report signaled we are close to bottoming and suggest that both gold and silver should have a positive January and Q1, 2018.

As John Rubino wrote in his latest note, ‘gold futures traders have finally started behaving “normally.”’ This simply means that speculators are finally beginning to cut back on long bets whilst commercials and large bullion, the “smart money” and the “inside money” have reduced their shorts dramatically.

This was seen in gold and also in silver, the industrial, technological precious metal. Historically when commercial and speculator positions are brought into balance then this has proven to be bullish for the precious metals.

Previously peaks in net commercial short interest have often happened alongside sell-offs, subsequently valleys in commercial short interest have almost always coincided with nearby rises in price. This could be a positive indicator for the next few months in both gold and silver prices.

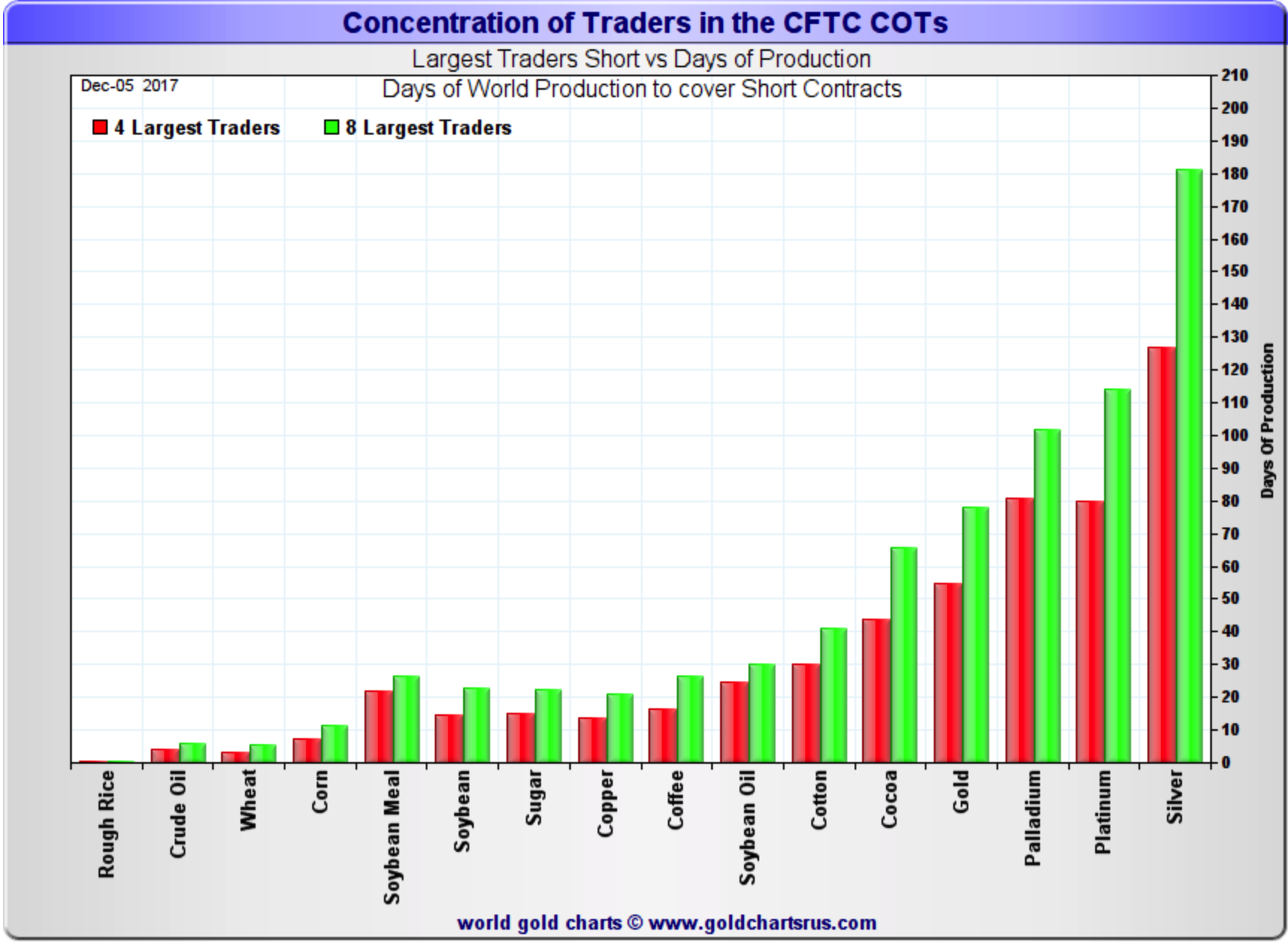

Silver: short 181 days of world silver production

According to Ed Steer:

“In silver, the Commercial net short position cratered by an eye-watering 26,721 contracts, or 133.6 million troy ounces of paper silver. That is, without doubt, the biggest one-week decline in COMEX history. They arrived at that number by adding 9,701 long contracts, plus they reduced their short position by an incredible 17,020 contracts — and the sum of those two numbers is the change for the reporting week…the Big 4 traders reduced their short position by about 6,400 contracts — and the ‘5 through 8’ large traders reduced their short position by around 4,700 contracts… the 36-odd small Commercial traders other than the Big 8, added approximately 15,600 contracts to their long position.”

As you can see from the chart at the top, the Big 8 commercial trader are now net short 439.8 million troy ounces of paper silver. This is equal to 181 days of world silver production or about 439.8 million troy ounces of paper silver held short by the Big 8.

“The two largest silver shorts on Planet Earth—JP Morgan and Canada’s Scotiabank—are short about 92 days of world silver production between the two of them—and that 92 days represents about 72 percent of the length of the red bar in silver in the above chart… about three quarters of it.”

Interestingly these dramatic changes in both short and long positions did not bring with them any dramatic changes in price. This is clearly something to look out for in the coming weeks. For many analysts, this latest COT report suggest we are looking at a bottom in silver as such changes in futures positions ordinarily coincide with a low in gold and silver prices and a good time to buy.

Gold: short 78 days of world gold production

As reported by Ed Steer:

“The commercial net short position crashed by 56,651 contracts, or 5.65 million troy ounces of paper gold. They arrived at that number by adding 15,678 long contracts, plus they decreased their short position by an incredible 40,973 contracts — and the sum of those two numbers is the change for the reporting week.Ted said that the ‘Big 4’ traders decreased their short position by a whopping 28,800 contracts, or thereabouts — and the big ‘5 through 8’ large traders decreased their short position by around 16,900 contracts…the 47-odd small commercial traders other than the Big 8, added 11,000 contract to their long position.”

The big chart at the top show the Big 8 are short nearly 80 days of production.

“In gold, the Big 4 are short 55 days of world gold production, which is down 10 days from what they were short last week — and the ‘5 through 8’ are short another 23 days of world production, which is down 6 days from what they were short the prior week, for a total of 78 days of world gold production held short by the Big 8 — which is down 16 days from the 94 days they were short in last week’s report. These are monster weekly changes. Based on these numbers, the Big 4 in gold hold about 70 percent of the total short position held by the Big 8…which is up 1 percentage point from last week’s COT Report.”

New Year’s resolution: buy gold and silver

Some caution should be exercised when looking at COT reports. When released the data is three days old, published on a Friday with Tuesday’s trading data. However this does not mean that some signal can be taken from them.

Seasonally, January is generally a good month to own precious metals, particularly gold. On average the gold price rises over 3% in the month and generally continues to rise into February.

This latest COT report is unlikely to be a one-off and should be embraced by those looking to allocate funds to own gold and silver.

As John Rubino concluded in his own coverage:

The numbers we’re seeing here are as of Tuesday the 5th, and the final three days of last week were a bloodbath for precious metals, so it’s highly likely that the next COT numbers – due out on Friday the 15th – will show absolute panic among speculators, leading to an even bigger swing in the right direction.

If history is still reliable, January will be a great month to own precious metals and mining stocks.

Investors and savers should keep their heads over the next few months and take solace from the fact that whilst the ‘Big’ players are gambling with paper they can in fact benefit by buying physical, allocated and segregated gold and silver.

We leave you with some wise words from John Hathaway who wrote on how the phenomenon of the paper precious metals market would come to benefit those holding the real thing:

“An acute shortage of readily marketable physical gold is developing that we believe will deepen in years to come. This possibility seems to be unrecognized by those who are short the gold market through paper contracts. The relentless dumping of synthetic or paper gold contracts since 2011 by speculators in Western financial markets has caused the shortage. The steady selling has driven down the price of physical gold, hobbled the gold-mining industry, and drained the stores of gold held in the vaults of Western financial centers …”

Veteran gold market analyst and CFA, Hathaway concludes that:

“Much of what passes for financial wealth is in our opinion imprisoned in a matrix from which there is no easy exit. The return migration of capital to real assets promises to be disruptive. The misdirection of capital could well cause losses for many but opportunity for a few. The list of opportunities is short, limited in capacity, possibly complex, and difficult to access. Among the possible opportunities, gold is accessible and straightforward. Gold has a history of responding inversely to the direction of confidence.

Related reading

Gold Trading COT Report “Means Lower – Then Much Higher – Prices Coming”

Physical Gold Market Will ‘Trump’ Paper Gold

Value of Gold – Unlike Paper Currency Gold Has Maintained Its Value Throughout Ages

Paper Gold: Utopia for Alchemists

News and Commentary

Gold inches up from near five-month low ahead of Fed meeting (Reuters.com)

Gold slightly higher ahead of Fed meeting (Reuters.com)

Asia shares take breather, Brent oil breaks above $65 (Reuters.com)

Asia Stocks Mixed Ahead of Central Bank Meeting (Bloomberg.com)

What bond and currency traders are looking for from Yellen’s Fed decision (MarketWatch.com)

Source: TheMaven.net

Source: TheMaven.net

98,750,067,000,000 Reasons to Be Worried About 2018 (Bloomberg.com)

Six Ways US Stocks Most Overvalued in History (TheMaven.net)

The Biggest Bubble Ever, In Three Charts (DollarCollapse.com)

Perfect Job Storm Coming in Robotic Wipeout (MauldinEconomics.com)

Crypto isn’t the only bubble in town… (StansBerryChurcHouse.com)

Gold and silver have proven durability; Digital currencies have not (Bloomberg.com)

Gold Prices (LBMA AM)

12 Dec: USD 1,243.40, GBP 933.92 & EUR 1,056.27 per ounce

11 Dec: USD 1,251.40, GBP 935.80 & EUR 1,061.19 per ounce

08 Dec: USD 1,245.85, GBP 924.42 & EUR 1,061.09 per ounce

07 Dec: USD 1,256.80, GBP 937.57 & EUR 1,066.77 per ounce

06 Dec: USD 1,268.55, GBP 948.37 & EUR 1,072.31 per ounce

05 Dec: USD 1,275.90, GBP 950.29 & EUR 1,075.71 per ounce

04 Dec: USD 1,279.10, GBP 952.67 & EUR 1,079.43 per ounce

Silver Prices (LBMA)

12 Dec: USD 15.78, GBP 11.82 & EUR 13.40 per ounce

11 Dec: USD 15.84, GBP 11.84 & EUR 13.43 per ounce

08 Dec: USD 15.83, GBP 11.76 & EUR 13.48 per ounce

07 Dec: USD 15.91, GBP 11.94 & EUR 13.49 per ounce

06 Dec: USD 16.12, GBP 12.06 & EUR 13.64 per ounce

05 Dec: USD 16.29, GBP 12.14 & EUR 13.72 per ounce

04 Dec: USD 16.33, GBP 12.09 & EUR 13.77 per ounce

Recent Market Updates

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

– An Interview with GoldCore Founder, Mark O’Byrne

– Risk Of Online Accounts Seen As One of Largest Brokerages In World Halts Online Trading After “Glitch”

– Low Cost Gold In The Age Of QE, AI, Trump and War

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

– Financial Advice from Dr Wayne Dyer

– Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– Brexit Budget – Grim Outlook As UK Economy Downgraded

END

I thought I might never live to see a bubble greater than Tulip Mania. Now Bitcoin surpasses it as the No 1 bubble ever

bitcoin this morning: 17,271

It’s Official: Bitcoin Surpasses “Tulip Mania”, Is Now The Biggest Bubble In World History

One month ago, a chart from Convoy Investments went viral for showing that among all of the world’s most famous asset bubbles, bitcoin was only lagging the infamous 17th century “Tulip Mania.”

One month later, the price of bitcoin has exploded even higher, and so it is time to refresh where in the global bubble race bitcoin now stands, and also whether it has finally surpassed “Tulips.”

Conveniently, overnight the former Bridgewater analysts Howard Wang and Robert Wu who make up Convoy, released the answer in the form of an updated version of their asset bubble chart. In the new commentary, Wang writes that the Bitcoin prices have again more than doubled since the last update, and “its price has now gone up over 17 times this year, 64 times over the last three years and superseded that of the Dutch Tulip’s climb over the same time frame.”

That’s right: as of this moment it is official that bitcoin is now the biggest bubble in history, having surpassed the Tulip Mania of 1634-1637.

And with that we can say that crypto pioneer Mike Novogratz was right once again when he said that “This is going to be the biggest bubble of our lifetimes.” Which, of course, does not stop him from investing hundreds of millions in the space: when conceding that cryptos are the biggest bubble ever, “Novo” also said he expects bitcoin to hit $40,000 and ethereum to triple to $1,500.

“Bitcoin could be at $40,000 at the end of 2018. It easily could,” Novogratz said Monday on CNBC’s “Fast Money.” “Ethereum, which I think just touched $500 or is getting close, could be triple where it is as well.”

As for Wang, here are some additional observations:

I continue this topic and discuss a main driver of bubbles. When we see a dramatic rise in asset prices, there is often an internal struggle between the two types of investors within us. The first is the value investor, “is this investment getting too expensive?” The second is the momentum investor, “am I missing out on a trend?” I believe the balance of these two approaches, both within ourselves and across a market, ultimately determines the propensity for bubble-like behavior. When there is a new or rapidly evolving market, our conviction in the value investor can weaken and the momentum investor can take over. Other markets that structurally lack a basis for valuation are even more susceptible to momentum swings because the main indicator of future value is the market’s perception of recent value.

We will publish the balance of Wang’s full note “What causes asset bubbles?” shortly, but for now we just wanted to experience a moment of true zen serenity, knowing that we now stand in proximity to an asset bubble the magnitude of which has never before been observed by humanity. Thanks central banks!

Ronan Manley discusses why Singapore is great for gold investors

(courtesy Ronan Manly/Bullionstar)

Bullion Star: Why Singapore is so great for gold investors

Submitted by cpowell on Mon, 2017-12-11 19:40. Section: Daily Dispatches

2:39p ET Monday, December 11, 2017

Dear Friend of GATA and Gold:

Bullion Star, headquartered in Singapore, today expounds on the city-state’s great advantages for gold investors.

Bullion Star writes: “Apart from the goods-and-services tax exemption on investment precious metals, there are a number of other jurisdictional advantages that have supported the growth of Singapore as a gold trading and storage hub and that reinforce the logic for buying gold and storing gold in Singapore.

“In Singapore, there are no other taxes when buying gold, silver, or other precious metals. This means no capital gains tax, no other sales tax, no death tax — in short no taxes. There are no reporting requirements when buying or selling gold or silver or other precious metals in Singapore. This means no reporting requirements to any Singaporean authority and no reporting requirements to any international authority.

“There is no goods-and-services tax when importing gold and other precious metals into Singapore, or when exporting gold or other precious metals out of the country.

“Singapore is also famed for its strong rule of law, making the country one of the safest and most secure countries to buy and store gold. In taking delivery or selling precious metals, it is quite safe, apart from the usual precautions, to walk in and out of bullion dealer shops in Singapore carrying your precious metals.

“Furthermore, the Singapore legal system is very protective of private property rights, and the nation of Singapore has strong military capabilities. Both factors are reassuring when storing gold or silver in the city-state.

“Finally, because it’s a thriving gold trading hub, with a buoyant wholesale and retail bullion market, Singapore has a very well-developed gold storage and vaulting infrastructure, and is very well serviced by secure transport companies.”

Bullion Star’s commentary is headlined “Gold Demand in the Singapore Bullion Market” and it’s posted here:

https://www.bullionstar.com/blogs/bullionstar/true-state-singapore-gold-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

As Goldman Sachs discusses, Bitcoin does not steal demand for gold. The author gives 3 reasons for this:

(courtesy GoldmanSachs/GATA)

Is Bitcoin Really Stealing Demand For Gold? Here Is Goldman’s Answer

A few days ago we first showed a chart of a dramatic divergence between the price of gold and bitcoin…

… which together with a recent unscientific poll showing that more Ron Paul followers prefer bitcoin to gold…

…prompted many to wonder if bitcoin – whether it is a commodity, currency, commodity-equity hybrid as some suggest, or simply a bubble as its opponents claim daily – was stealing demand for gold.

In an overnight note, Goldman’s global head of commodities Jeffrey Currie answered this question, arguing that despite bitcoin’s “explosive upward trajectory” the answer to whether “bitcoin is taking demand from gold” is no, and gives three reasons why there is a lack of substitution by investors from gold into bitcoin:

- First, the investor pools are vastly different. Gold investors who use ETFs, futures or commodity indices are automatically covered by anti-money laundering (AML) and counter-terrorist financing (CTF) regulations which are already “baked in” to processes in these markets. Even physical trading in jewellery, bars, coins etc. has seen a huge increase in regulatory scrutiny, globally, over the last few decades. In the US, professional jewellers and dealers must have an AML program implemented, and significant cash purchases or precious metal sales require additional reporting to the IRS on a transaction by transaction basis. In contrast, there is still very little clarity on how trading in cryptocurrencies could be made to comply with AML and CTF regulations, even in theory. This creates huge regulatory hurdles for professional investors wishing to enter these markets.

- Second, as the chart below shows, there has been no discernible outflow of gold from ETFs. Indeed, total known gold ETF holdings recently reached their highest level since mid-2013 (currently up 12% YTD, see Exhibit 8). This is somewhat related to the first point, as mutual funds are the largest holders of gold ETFs, but even accounting for this there is no evidence of a mass exodus from gold.

- Third, and final, the market characteristics of gold and cryptocurrencies are vastly different Currie claims. In this context, th emarket cap of bitcoin is still just under $300 billion, while the total value of gold is a little over $8 trillion. And while bitcoin has a mathematically certain total supply, and gold has a finite (but less certain) supply in the earth’s crust, even a cursory examination shows very different market dynamics according to Currie. As a result, Goldman believes that the composition of demand between bitcoin and gold is the key difference in the recent price action, and specifically, bitcoin is attracting more speculative inflows relative to gold.

Putting all this together, Currie concludes that bitcoin has demonstrated much higher volatility and lower liquidity / price discovery compared to gold.

“The market cap of bitcoin is c.$275 billion versus gold at $8.3 trillion. Even all of the cryptocurrencies combined have a market cap less than $500 billion. While the lack of liquidity and increased volatility may keep bitcoin interesting, it is unlikely to convince investors looking for the kind of diversification and hedging benefits which gold has proven to possess over its long history.”

Unless it is successful, of course, in which case there is a little under 20x upside for the crypto sector.

Currie does make a good point in his conclusion: “to deal with the AML and CTF uncertainties surrounding bitcoin, and attract a wider investor pool, custody issues must first be resolved beginning with identifying it as a commodity, fund or security.” Here Goldman “firmly believes” that bitcoin is commodity, “as bitcoin has no liability that all securities have by definition. Even a dollar bill is ultimately a liability to the US government.”

Which is also why demand for bitcoin is so exponentially greater than demand for a dollar bill.

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.6189 /shanghai bourse CLOSED DOWN AT 41.38 POINTS 1.25% / HANG SANG CLOSED DOWN 171.41 POINTS OR 0.59%

2. Nikkei closed DOWN 72.56 POINTS OR 0.32% /USA: YEN FALLS TO 113.46

3. Europe stocks OPENED ALL GREEN EXCEPT SPAIN /USA dollar index FALLS TO 93.85/Euro FALLS TO 1.1770

3b Japan 10 year bond yield: FALLS TO . +.046/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.46/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 58.46 and Brent: 65.68

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.307%/Italian 10 yr bond yield UP to 1.674% /SPAIN 10 YR BOND YIELD UP TO 1.438%

3j Greek 10 year bond yield FALLS TO : 4.421?????????????????

3k Gold at $1242.80 silver at:15.77: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 58.86

3m oil into the 58 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.46 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9909 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1665 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.307%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.388% early this morning. Thirty year rate at 2.775% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat As FOMC Meeting Begins; Brent Jumps Over $65 For First Time Since 2015

E-mini futures are modestly in the green this morning, though net of fair value the S&P index is poised for another record high open as the FOMC begins its last meeting for 2017 in which it is expected to raise rates by 25bps. European stocks gain while Asian equities slide led by weakness in Chinese airplane stocks. Brent has jumped above $65 for the first time since 2015 as a result of a shutdown in the Forties North Sea pipeline, which carries 40% of UK North Sea oil & gas production while sterling declines amid the ongoing Brexit drama despite the highest UK inflation print since 2012.

The Forties pipeline is important for the global oil market because the crude it carries normally sets the price of dated Brent, a benchmark used to price physical crude around the world and which underpins Brent futures. The shutdown comes as oil supply cuts by OPEC have helped chip away an excess of inventories built up following a global supply glut which began to emerge in late 2014.

“Such a reaction (in prices) indicates that supply disruptions can no longer be ignored in tight markets,” said Hussein Sayed, analyst at FXTM. U.S. crude oil futures were last 0.5 percent higher at $58.30 a barrel.

Across macro, the Aussie 10-year yield fell four basis points while T-note yields were a basis point lower at 2.38%. The Bloomberg Dollar Index steady near three-week high; kiwi outperformed G-10 peers for second day. In China, the PBOC added a net 40bn yuan of liquidity, after injecting 20bn the day before, while keeping the CNY fixing little changed.

Europe’s Stoxx 600 Index gained 0.2% as technology shares rebounded after a tech deal in the sector, in which Atos offered to buy Gemalto for $5 billion, lifting shares of peer Ingenico. Energy shares also rose, helped by firmer oil prices as brent jumped above $65 for the first time since 2015 on a North Sea pipeline closure.

In Asia earlier, MSCI’s broadest index of Asia-Pacific shares outside Japan drifted off 0.3 percent, having bounced 2% in the past three sessions, with markets consolidating in the hope an upswing in global growth could outlast a likely hike in U.S. interest rates this week. The Nikkei 225 retreated from a 26-year high, and Hong Kong and Chinese shares slipped. Australia’s ASX 200 (+0.3%) and Nikkei 225 (-0.3%) were mixed with strength in commodity related stocks keeping the Australian benchmark afloat. This was after copper rose to above USD 3/lb and Brent crude rallied to a 2-year high on reports the Forties pipeline, which carries 40% of UK North Sea oil production, will be shut for weeks due to repairs. Meanwhile the Hang Seng (-0.6%) and Shanghai Comp. (-1.3%) were subdued on plans of further regulatory steps for insurers to help curb risks and reports of possible contingency measures such as higher interest rates and tighter capital controls to combat possible outflows and support CNY from the impact of US tax reform and Fed hikes.

Losses for large-cap Chinese shares accelerated toward the close as A shares of the nation’s big three carriers all posted their worst daily declines since February 2016 amid rising oil prices. China Southern Airlines Co. slumped 6.5% in Shanghai, Air China Ltd. lost 5.5% and China Eastern Airlines Corp. dropped 5.3%. All three rose more than 10% over one month through Monday, led by China Southern with a 23% gain; even after Tuesday’s losses, China Southern and Air China are up more than 40% this year. “Airlines stocks have been rising in defiance of an oil rally because of better performance in ticket prices in what is traditionally a slow season,” said Su Baoliang, an analyst at Sinolink Securities Co. “Today’s decline shows the continued oil rally finally having its toll. Some investors have decided to lock in their gains.” As a result, the CSI 300 Index closed down 1.3%, its biggest loss in two weeks.

Hong Kong stocks fell in tandem with mainland equities Tuesday afternoon, as airlines tumbled amid rising oil prices. Sunny Optical Technology Group Co. led a retreat among technology shares after a recent rally. The Hang Seng Index closed down 0.6% after rising as much as 0.4% in the morning; that ended three days of gains that had added 2.6%. Hang Seng China Enterprises Index drops 1%. Shanghai Composite Index falls 1.3%.

The euro edged higher and most European bonds declined even as German investor confidence slid in December for the first time in four months. The Bloomberg Dollar Spot Index erased overnight losses before the start of the FOMC’s two-day meeting and 10-year Treasury yields edged lower. Sweden’s krona led G-10 gains after inflation beat expectations. Meanwhile, sterling fluctuated as U.K. inflation unexpectedly accelerated to the highest rate in more than five-and-a-half years. Commodity-linked currencies also got a boost from the pick up in oil prices. The Australian dollar and the New Zealand dollar were both over half a percent higher while the Norwegian crown rose 0.7 percent.

The dollar was idling at 113.42 yen just off a one-month top of 113.69, while the index that measures it against a basket of peers was down 0.1 percent. Dealers at Citi noted interbank volumes in the forex market had been 35 percent below average overnight and another thin session was in prospect for Tuesday. There was a little more action in bitcoin, which was last up over half a percent on the day at $16,540 on the Bitstamp exchange BTC=BTSP. The cryptocurrency’s newly launched 1-month futures contract fell 4% to stand at $17,780 on its second day of trading.

The fate of the dollar is now in the hands of the 3-day FOMC meeting which started today, while the European Central Bank and the Bank of England will meet for the last time in 2017 on Thursday.

JPMorgan economist David Hensley suspects the Fed will revise up its growth forecast while trimming the outlook for the unemployment rate, potentially adding upside risk to the “dot plot” forecasts on interest rates. “The dot plot previously called for three hikes in 2018; it is a close call whether this moves to four hikes,” he warned, a shift that would likely boost the dollar but could bludgeon bonds. “For its part, the European Central Bank (ECB)is likely to emphasize its low-for-long stance and continue to distance itself from the Fed,” he added. “The staff is likely to revise up its 2018 growth forecast, while we think the core inflation forecast will reveal an even slower recovery than before.”

The divergence in Fed and ECB policy was supposed to be bullish for the dollar, given it had widened the premium offered by U.S. two-year yields over German yields to 256 basis points from 188 basis points this time last year. The last time the spread was so wide was in 1999 according to Reuters.

In commodities, the big mover was Brent which topped $65 for the first time since 2015 amid reports of an outage in the Forties North Sea pipeline. Subsequently, this saw the WTI/Brent widen to $7.35, the widest since May 2015, while UK gas futures saw its largest rise since 2011 with support also coming from an explosion at OMV’s gas facility in Baumgarten.

In metals markets, gold is currently trading relatively flat whilst base metals in China continued to be supported overnight by domestic supply cuts. Goldman Sachs says on a long term basis expects commodities to outperform other asset classes even as policy makers are forced to hike rates, most bullish copper and most bearish aluminium. Protesters in Nigeria claim they have halted flows from 3 of Eni’s (ENI IM) wells. U.K. natural gas prices surged after a pipeline explosion in Austria threatened to tighten flows.

In rates, the yield on 10Y TSYs dipped less than one basis point to 2.39%, while Germany’s 10Y Bund rose two bps to 0.31%, the highest in a week. Yield on Britain’s 10Y Gilt climbed two basis points to 1.225% as Japan’s 10Y JGB yield declined less than one basis point to 0.047%, the lowest in a week.

VeriFone and MongoDB are among companies reporting earnings. Economic data include PPI readings, monthly budget statement.

Bulletin Headline Summary from RanSquawk

- European equities trade with little in the way of firm direction. Energy names outperform in the wake of yesterday’s Forties pipeline outage

- In FX markets, EUR and JPY are a tad firmer vs the Dollar, as the DXY struggles to stay within touching distance of the 94.000

- Looking ahead, highlights include US PPI and supply from the US

Market Snapshot

- S&P 500 futures up 0.08% to 2,663.50

- STOXX Europe 600 up 0.2% to 389.75

- MSCI Asia down 0.1% to 170.21

- MSCI Asia ex Japan down 0.3% to 552.60

- Nikkei down 0.3% to 22,866.17

- Topix up 0.1% to 1,815.08

- Hang Seng Index down 0.6% to 28,793.88

- Shanghai Composite down 1.3% to 3,280.81

- Sensex down 0.7% to 33,222.70

- Australia S&P/ASX 200 up 0.3% to 6,013.20

- Kospi down 0.4% to 2,461.00

- German 10Y yield rose 0.7 bps to 0.3%

- Euro up 0.1% to $1.1783

- Italian 10Y yield rose 0.3 bps to 1.391%

- Spanish 10Y yield fell 0.5 bps to 1.408%

- Brent Futures up 1.1% to $65.37/bbl

- Gold spot up 0.2% to $1,244.35

- U.S. Dollar Index down 0.08% to 93.79

Top Overnight News via BBG

- Alabama votes in a special general election to fill Senate seat vacated by Attorney General Jeff Sessions

- U.S. and South Korea may delay joint military drills until after Pyeongchang Winter Olympics in February to reduce tensions with North Korea

- International Trade Secretary Liam Fox said the U.K. would like a trading relationship with the EU after it leaves the bloc that’s “virtually identical” to the one it has now

- China will continue its neutral monetary policy with a bias toward tightening next year, according to a front-page commentary in Securities Times; the country may cut RRR for some banks to provide liquidity and increase support for agriculture and small companies

- Britons will see their real wages drop 0.5% next year, lagging behind a global average of a 1.5% gain, according to a salary forecast from Los Angeles-based recruitment firm Korn Ferry

- Unibail Buys Westfield for $16 Billion as Mall Owners Merge

- Disney Said to Near Deal for Fox Assets as Comcast Drops Out

- Edison Sees Its Equipment Being Probed as Possible Cause of Fire

- Atos Bids $5.1 Billion for Security- Software Maker Gemalto

- Passport to Shut Global Hedge Fund After ‘Unacceptable’ Returns

- State Dept. Said to Convene U.S. Airlines for ‘Open Skies’ Talks

- Trump May Actually Be Right About the Trade Deficit With Canada

- ‘Star Wars: Last Jedi’ Could Approach $200m in Domestic Opening

- AMC, Saudi Arabia Fund to Explore Commercial Opportunities

- J&J Says Darzalex Data Show Manageable Safety Profile, 12% IRs

- Billionaire Zara Owner Said to Seek $472 Million for 16 Stores

Asia equity markets traded subdued as momentum from Wall Street where S&P 500 and DJIA posted fresh record closes, was lost on the region. ASX 200 (+0.3%) and Nikkei 225 (-0.3%) were mixed in which strength in commodity related stocks kept the Australian benchmark afloat. This was after copper rose to above USD 3/lb and Brent crude rallied to a 2-year high on reports the Forties pipeline, which carries 40% of UK North Sea oil production, will be shut for weeks due to repairs. Hang Seng (-0.6%) and Shanghai Comp. (-1.3%) were subdued on plans of further regulatory steps for insurers to help curb risks and reports of possible contingency measures such as higher interest rates and tighter capital controls to combat possible outflows and support CNY from the impact of US tax reform and Fed hikes. Finally, 10yr JGBs traded relatively flat, although some mild support was observed following a 5-yr auction in which the b/c and accepted prices were higher than previous. China’s insurance regulator plans to revise certain guarantee fund rules for insurance industry as China seeks to strengthen insurers’ capability to curb risks. PBoC injected CNY 80bln via 7-day reverse repos and CNY 70bln via 28-day reverse repos. PBoC set CNY mid-point at 6.6162 (Prev. 6.6152)

Top Asian News

- Philippines to Approve $2.6 Billion Tax Bill in Win for Duterte

- Big 3 China Airlines Fall Most in 22 Months, Dragging Large Caps

- Reliance Said to Weigh Jio IPO After $31 Billion Wireless Spree

- China to Guide Private Capital into Internet Security Investment

European stocks trade modestly higher in what’s been a relatively choppy session thus far. Shares have seen some support from M/A activity, alongside the strength in energy names. Gemalto shares surged some 30% after Atos’s EUR 4.3bln takeover proposal. Energy names gaining on the back of Brent crude futures rising to the highest level since 2015 amid reports of the outage in the Forties North Sea pipeline, which carries 40% of UK North Sea oil & gas production. It seems the path of least resistance remains south for fixed, with fresh losses made in recent trade, albeit in a gradual and measured manner. Bunds are just off a 163.27 base, and with the 10 year cash yield back above the 0.30% level that has been sticky despite a brief dip below on Monday, and even 2 year Schatz futures are retesting worst levels (112.130) despite a solid auction, but chart support around 112.120 could stall further declines. Elsewhere, Gilts just printed a tick below the initial post-UK inflation data low, at 124.69 before regrouping and USTs have also recovered some composure to sit just off worst levels awaiting the 2nd half and PPI data, plus the long bond offering.

Top European news

- Genmab Drops; Bernstein Expects Near-Term Estimates to Come Down

- Swedish Inflation Surprise Paves Way for Stimulus Retreat

- Gas Explosion at OMV’s Baumgarten Hub Leads to Shutdown

- Poland Triggers Alarm Bells as Judges Tumble in Eastern EU

- Atos Bids $5.1 Billion for Security-Software Maker Gemalto

In FX markets, EUR and JPY are a tad firmer vs the Dollar, as the DXY struggles to stay within touching distance of the 94.000 level into day 1 of the December FOMC. Sterling saw a push higher with inflation rising by 3.1% above analyst estimates which is also against the peak that the BoE had estimated for October. However, the move was short-lived and GBP then proceeded to lose ground against its major counterparts with Brexit still at the forefront after European Parliament’s Verhofstadt stating that David Davis made an own goal with Brexit deal remarks. Elsewhere, we have seen a sharp reversal and retreat in EUR/SEK on the back of Swedish inflation data beats with CPI at 1.9% y/y in November vs 1.7% expected and last, while the Riksbank’s targeted CPIF index came in at 2% against the 1.8% forecast and the same previously. Finally, Kiwi continues to outperform its G10 peers, with NZD/USD forming a firmer base above 0.6900 and the rebound on less dovish RBNZ expectations pushing the pair just over 0.6950 at one stage

In commodities, Brent crude futures are trading at 2015 levels after breaking above USD 65/bbl amid reports of an outage in the Forties North Sea pipeline. Subsequently, this saw the WTI/Brent widen to USD 7, while UK gas futures saw its largest rise since 2011 with support also coming from an explosion at OMV’s gas facility in Baumgarten. In metals markets, gold is currently trading

relatively flat whilst base metals in China continued to be supported overnight by domestic supply cuts. Goldman Sachs says on a long term basis expects commodities to outperform other asset classes even as policy makers are forced to hike rates, most bullish copper and most bearish aluminium. Protesters in Nigeria claim they have halted flows from 3 of Eni’s wells. Ineos who operate the Forties pipeline state that the crack in the pipeline is 5-6 inches and they will know within the coming days

whether the pipeline will be closed for 2 or 3 weeks. Libya’s Waha Oil Co. state that they are producing around 217k bpd.

Looking to the day ahead, the CPI/RPI/PPI prints are due in the UK (CPI 0.2% mom and 2.7% yoy core expected), and November PPI due in the US. The December ZEW survey will also be released in Germany while the November NFIB small business optimism and November monthly budget statement data are also out in the US. Away from the data, ECB President Draghi is scheduled to speak in Frankfurt while in the US a special general election will be held in Alabama to fill the US Senate seat, which has been vacated by Attorney General Jeff Sessions.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 104, prior 103.8

- 8:30am: PPI Final Demand MoM, est. 0.3%, prior 0.4%; Ex Food and Energy MoM, est. 0.2%, prior 0.4%

- PPI Final Demand YoY, est. 2.9%, prior 2.8%; Ex Food and Energy YoY, est. 2.35%, prior 2.4%

- 2pm: Monthly Budget Statement, est. $134.5b deficit, prior $136.7b deficit

DB’s Jim Reid concludes the overnight wrap

In between the snow showers in London yesterday there really wasn’t a lot going on yesterday unless of course you were a Bitcoin trader. Markets are waiting for the central bank and inflation onslaught this week. Indeed this morning see the starts of this with CPI/RPI/PPI prints due in the UK before the PPI is due in the US. Ahead of this there was a big Gilts rally yesterday as 10y yields fell 7.7bp to a 3 month low, while USTs rose 1.2bp and Bunds fell 1.4bp back to levels last seen in late June.

The rally in Gilts partly reflects increased concerns on the Brexit deal from last week. In the UK, PM May told Parliament that the UK’s financial settlement offer is conditional on a successful post-Brexit trade deal and Brexit Secretary Davis noted the agreement was “much more a statement of intent than it was a legally enforceable thing”. Bloomberg also noted Foreign minister Johnson continues to press PM May for a “hard” Brexit. On the other side, the EU Commission called it a “gentlemen’s agreement”, but caveat that if the UK try to unpick what it was agreed, it will halt the next phase of talks. Elsewhere, Bloomberg reported that Ms Merkel told CDU/CSU caucus members that it’s likely the EU Summit this week will confirm Brexit talks can move onto trade, but the mandate will only be provided in February. Along with the Gilts rally, GBPUSD fell 0.37% yesterday.

Over in the US, there is a special general election in Alabama today to fill the US Senate seat which has been vacated by Republican Jeff Sessions. It was initially thought to be an easy win for the Republicans as no Democrat has won an election for the Senate in almost 20 years. However, the race has tightened with polls suggesting it is too close to call or showing conflicting results. For example, a Fox News poll released yesterday showed the Democrat candidate having a 10 point lead, but Politico noted most public surveys conducted last week showed the Republican candidate Roy Moore having a small lead instead.

Notably, a potential win by Democrats would reduce the Republican’s Senate majority to a thin margin of 51-49 (from 52-48). Given that the tax bill has been approved by Congress and is now in the reconciliation stage, it is less likely to scuttle this process, but a Democrat win could impact the prospects of future bills being passed. CNN noted that one in every 20 votes so far this year in the Senate would have had a different outcome if just one vote had flipped to the opposite side.

Over in commodities, Brent rose 2.03% to the highest since August 2015 as a key North Sea pipeline (Forties Pipeline system) was shut down after a crack was discovered. According to the operator, repairs are expected to take weeks. The boost to energy stocks along with a rebound in tech and telco shares helped the S&P edge +0.32% higher to a fresh high, while the Dow (+0.23%) and Nasdaq (+0.51%) also advanced. Back in Europe, equities trended slightly lower with the Stoxx 600 (-0.05%) and DAX (-0.23%) both down, but the FTSE100 bucked the trend to be up 0.80%, partly benefiting from the weaker Sterling and gains in mining stocks.

Moving along, the DB’s House View team published their latest report yesterday, with the title “Happy holidays”, which they think summarises the market mood at the moment. As always they recap the views from our economists and strategists across research. Click the link for our views into 2018 for global macro, central banks, political risk and key markets views by asset class. This morning in Asia, markets are trading modestly weaker. The Nikkei is down -0.28%, while other key bourses are down c0.5% as we type (Kospi -0.54%; Hang Seng -0.46%; China CSI 300 -0.61%). Now briefly recapping other markets performance from yesterday. The US dollar index firmed 0.06% while the Euro and Sterling fell 0.03% and 0.37% respectively. The NZDUSD jumped 0.95% following news that Adrian Orr has been appointed as the next Governor of New Zealand’s central bank. In commodities, precious metals softened (Gold -0.52%; Silver -0.97%) while other base metals advanced modestly (Copper +1.20%; Zinc +1.46%; Aluminium +0.56%). Elsewhere, The VIX fell for the fifth consecutive day to 9.34 and is now down c20% from last Monday.

Away from the markets and onto the ECB’s Nowotny comments. He noted the ECB should be “careful when unwinding low interest rates” but “thanks to the broad base economic expansion…growth prospects are looking up…in particular at the European level”. On Austria more specifically, he noted systemic risks from real estate lending remain subdued, but close supervisory monitoring is required.

Elsewhere, he touched on Bitcoin, noting it is “not a currency. It doesn’t fulfil the criteria” and based on its scope, “one should probably discuss whether regulatory steps are necessary here”.

Over in the US, President Trump’s infrastructure plans may be in focus early next year as the White House noted Trump had “a productive meeting” with Transportation and Infrastructure Committee Chairman Shuster where they discussed plans “for rebuilding America’s infrastructure”. Bloomberg had earlier noted that Trump may be releasing his infrastructure plans in January 2018. Elsewhere, according to a one page analysis by the US Treasury department, the Republican tax proposals would pay for themselves over the next 10 years, with the report expecting GDP to increase an average of 2.9%, which would lead to US$1.8trn in new revenue. The growth number will obviously be questioned.

Back in Germany, Ms Merkel seems to be providing support for France Macron’s proposed reforms for a tighter Europe. She noted “it would be better if Europe spoke with one voice” and that Europe “does not only need a stronger economic and monetary union but we must also have a Europe of security and the rule of law…” Elsewhere, she was confident that Germany would be able to ‘react

in a concrete way” to Macron’s proposed reforms and that reforms must make progress in 2018.

The latest ECB holdings were released yesterday. Net CSPP purchases last week were €1.1bn and Net PSPP purchases €16.2bn. This left the CSPP/PSPP ratio at a lowly 7% last week (12% over last 4 weeks vs. 11.5% before QE was trimmed in April 2017). The reduced CSPP/PSSP ratio partly reflects the seasonal lull and likely noise in these numbers during December. Overall, we believe relevant signals will start trickling in from January after net QE purchases have been halved. That said, we still think the ECB will likely keep CSPP relatively unscathed as part of this process.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the October JOLTS job openings was lower than expectations at 5,996 (vs. 6,135), but the quits rate remained at 2.2%. In France, the November Business industry sentiment index was broadly in line at 106 (vs. 107). Over in Italy, the October retail Sales fell more than expected, at -1% mom (vs. flat expected) and -2.1% yoy (vs. 3.1% previous). In the UK, the November Rightmove measure of home asking prices fell 2.6% mom (vs. -0.8% previous).

Over in Asia, Japan’s 4Q MoF/Cabinet Office Business Outlook Survey was reasonably upbeat. Large and medium sized firms in both the manufacturing and non-manufacturing sectors reported an improvement in business conditions and the survey also pointed to considerable optimism about the outlook for business conditions in 1Q18.

Looking to the day ahead, the CPI/RPI/PPI prints are due in the UK (CPI 0.2% mom and 2.7% yoy core expected), and November PPI due in the US. The December ZEW survey will also be released in Germany while the November NFIB small business optimism and November monthly budget statement data are also out in the US. Away from the data, ECB President Draghi is scheduled to speak in Frankfurt while in the US a special general election will be held in Alabama to fill the US Senate seat, which has been vacated by Attorney General Jeff Sessions.

3. ASIAN AFFAIRS