GOLD: $1246.30 UP $6.40

Silver: $15.85 UP 20 cents

Closing access prices:

Gold $1255.50

silver: $16.07

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1254.20 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1243.80

PREMIUM FIRST FIX: $10.40

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1253.58

NY GOLD PRICE AT THE EXACT SAME TIME: $1242.10

Premium of Shanghai 2nd fix/NY:$11.18

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1241.60

NY PRICING AT THE EXACT SAME TIME: $1241.10

LONDON SECOND GOLD FIX 10 AM: $1242.65

NY PRICING AT THE EXACT SAME TIME. 1242.65

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECEMBER CONTRACT: 416 NOTICE(S) FOR 41600 OZ.

TOTAL NOTICES SO FAR: 6722 FOR 672,200 OZ (20.908 TONNES),

For silver:

DECEMBER

44 NOTICE(S) FILED TODAY FOR

220,000 OZ/

Total number of notices filed so far this month: 5528 for 27,640,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $17,120/OFFER $17,240, UP $171 (morning)

BITCOIN : BID $16,600 : OFFER 16,72 DOWN $389 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE BY A GOOD SIZED 2526 contracts from 200,271 RISING TO 202,797 DESPITE YESTERDAY’S FAIR SIZED 11 CENT FALL IN SILVER PRICING. WE HAD SURPRISINGLY NO REAL COMEX LIQUIDATION AND ON TOP OF THIS, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GIGANTIC NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE : 2503 EFP’S FOR MARCH (AND ZERO FOR DEC AND OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 2503 CONTRACTS. I GUESS WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 2940 EFP’S FOR SILVER ISSUED.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DECEMBER:

29,845 CONTRACTS (FOR 9 TRADING DAYS TOTAL 29,845 CONTRACTS OR 149.22 MILLION OZ: AVERAGE PER DAY: 3,316 CONTRACTS OR 16.580 MILLION OZ/DAY)

RESULT: A GOOD SIZED RISE IN OI COMEX DESPITE THE 11 CENT FALL IN SILVER PRICE. HOWEVER WE HAD ALL OF OUR COMEX LONGS WHICH EXITED OUT OF THE SILVER COMEX TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 2503 EFP’S WERE ISSUED TODAY FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY GAINED 5029 OI CONTRACTS i.e. 2503 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2526 OI COMEX CONTRACTS. AND ALL OF THIS INCREASED DEMAND HAPPENED WITH THE FALL IN PRICE OF SILVER BY 11 CENTS AND A LOW CLOSING PRICE OF $15.65 YESTERDAY. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.015 BILLION TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DECEMBER MONTH/ THEY FILED: 44 NOTICE(S) FOR 220,000 OZ OF SILVER

In gold, the open interest FELL BY FAIR SIZED 4577 CONTRACTS DOWN TO 446,618 WITH THE FAIR SIZED FALL IN PRICE OF GOLD YESTERDAY ($5.15). HOWEVER, THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED ANOTHER 11,317 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 11,317 CONTRACTS. The new OI for the gold complex rests at 446,618. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE WITNESS THE HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER. IN ESSENCE WE HAVE A HUGE GAIN OF 6840 OI CONTRACTS: 4577 OI CONTRACTS LEFT THE COMEX BUT 11,317 OI CONTRACTS NAVIGATED OVER TO LONDON. THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP ISSUANCE. THEY ARE IMMEDIATELY REMOVING COMEX OPEN INTEREST NUMBERS BUT DELAYING RELEASE OF EFP’S FOR 24 HOURS OR GREATER AS NO DOUBT THEY ARE NEGOTIATING WITH THE LONGS FOR A FIAT BONUS.

YESTERDAY, WE HAD 7704 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DECEMBER STARTING WITH FIRST DAY NOTICE: 119,242 CONTRACTS OR 11.924 MILLION OZ OR 370.88 TONNES (9 TRADING DAYS AND THUS AVERAGING: 13,249 EFP CONTRACTS PER TRADING DAY OR 1.3249 MILLION OZ/DAY)

Result: A GOOD SIZED DECREASE IN OI WITH THE FALL IN PRICE IN GOLD TRADING YESTERDAY ($1.45). WE HAD A LARGE NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,317. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,317 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 6840 contracts:

11,317 CONTRACTS MOVE TO LONDON AND 4577 CONTRACTS LEFT THE COMEX.

we had: 416 notice(s) filed upon for 41600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, SURPRISINGLY NO CHANGES in gold inventory at the GLD/

Inventory rests tonight: 842.81 tonnes.

SLV

OH OH!!/ WITH SILVER DOWN AGAIN TODAY BY 11 CENTS/WE HAD ANOTHER HUGE INVENTORY GAIN OF 1,415,000 OZ. SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS AND YET SLV INVENTORY RISES??/

INVENTORY RESTS AT 326.714 MILLION OZ/

oh oh!!!TODAY WE HAD ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A ‘DEPOSIT” OF 944,000 OZ DESPITE THE CONSTANT RAID ON SILVER. SILVER HAS BEEN DOWN 9 STRAIGHT TRADING DAYS.

INVENTORY RESTS AT 325.299 MILLION OZ

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A GOOD SIZED 2526 contracts from 200,271 UP TO 202,497 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY FALL IN PRICE OF SILVER AND CONTINUAL BOMBARDMENT (A FALL OF 11 CENTS ). HOWEVER,OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER HUGE 2503 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. ON TOP OF THIS, IF WE TAKE THE OI GAIN AT THE COMEX 2526 CONTRACTS TO THE 2503 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET GAIN OF 5029 OPEN INTEREST CONTRACTS, AND YET WE STILL HAVE A HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW). THE NET GAIN TODAY IN OZ: 25.14 MILLION OZ!!!

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 11 CENT FALL IN PRICE (WITH RESPECT TO FRIDAY’S TRADING). BUT WE ALSO HAD ANOTHER 2503 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER INTENSIFIES DESPITE THE CONSTANT RAIDS.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 22.22 points or 0.68% /Hang Sang CLOSED UP 428.20 pts or 1.49% / The Nikkei closed DOWN 108.10 POINTS OR 0.47%/Australia’s all ordinaires CLOSED UP 0.16%/Chinese yuan (ONSHORE) closed DOWN at 6.6200/Oil DOWN to 57.34 dollars per barrel for WTI and 63.82 for Brent. Stocks in Europe OPENED ALL MIXED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6200. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6250 //ONSHORE YUAN SLIGHTLY WEAKER AGAINST THE DOLLAR/OFF SHORE MUCH WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(STRONG MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

Seems that the long awaited election is to be held on March 4 and that sent Italian bonds and their stock market southbound

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

OPEC certainly saw its output fall to it lowest level in 6 months. However they fear that the shale boys will increase that production to meet demand needs

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)What a riot: the bankruptcy of Mt Gox has now become quite interesting in that the assets (the bitcoins) have risen 40 fold. Now the claimants could be made whole. However the original owners want that asset. The creditors should win

(Lewis/London’s Financial Times)

ii)Gold trading today/early morning: the CPI is probably the most important number released in the month. We had a much weaker CPI (to which Janet is not happy as they need wage inflation), which caused treasury yields to drop, the dollar to drop and gold/silver to rise

(courtesy zerohedge)

10. USA stories which will influence the price of gold/silver

i)Core CPI which is closed watched by the Fed came in with a gain of only 1.7%, a lot lower than expected and this sent the dollar southbound along with bond yields. Gold advanced..

( zerohedge)

ii)Doug Jones wins in Alabama and will take office late in December. This will bring the voting in the senate to 51 Republicans vs 49 democrats and may upset the apple cart a bit.

( zerohedge)

iv)More on the swamp: Nunes is furious over the McCabe now show. He did not issue a subpoena as the FBI stated it was a scheduling snafu. This is getting quite ridiculous( zerohedge)

v)My goodness: the texts between FBI agents Strzok and Lisa Page have been released and it certainly states that the investigation was tainted right from the beginning

( zerohedge)

vi)Deputy Attorney General Rosenstein who is himself deeply conflicted takes the hot seat trying to explain his non actions at setting up another Special Investigation into the corrupt Hillary email scandal, the Uranium 1 scandal and the Fusions debacle

( zerohedge)

vii)As expected Yellen raised her key interest rate. She expects 3 hikes and faster growth. Two dissented

( zerohedge)

viii)Market reaction to FOMC

gold rises, the dollar falls, yields tumble despite the hawkish hiking Fed. Gold, the dollar and falling yields is exactly opposite to what the Fed desired

( zerohedge)

ix)Supposedly the House and Senate Republicans have reached a tax deal but they still need a cost analysis on their deal. I still feel that they have no chance of passing this..but let us see

( zerohedge)

Let us head over to the comex:

The total gold comex open interest FELL BY A FAIR SIZED 4577 CONTRACTS DOWN to an OI level of 446,618 WITH THE FALL IN THE PRICE OF GOLD ($5.15 LOSS WITH RESPECT TO YESTERDAY’S TRADING). IN ACTUAL FACT WE DID NOT HAVE ANY GOLD LIQUIDATION. WE HAD ANOTHER LARGE COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 11,317 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 11,317 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE CONSTANT BANKER RAIDS CONTINUE AS THEY TRY TO GET OUR “MATHEMATICAL PAPER LONGS” IN GOLD TO LIQUIDATE THEIR POSITIONS AT THE COMEX AND NO DOUBT IN LONDON. . THE CME HAS BEEN VERY TARDY IN THEIR REPORTING OF EFP’S CONTRACTS AFTER A COMEX OI MORPHS INTO AN EFP WHICH WAS THE REASON FOR MY 2ND LETTER TO THE CFTC.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 6840 OI CONTRACTS IN THAT 11,317 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 4577 COMEX CONTRACTS. NET GAIN: 6840 contracts OR 648,400 OZ OR 20.16 TONNES

Result: AN FAIR SIZED DECREASE IN COMEX OPEN INTEREST WITH THE FALL IN THE PRICE OF GOLD YESTERDAY ($5.15.) WE HAD NO REAL GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 6840 OI CONTRACTS…

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest surprisingly rise by 233 contracts up to 2427. We had 207 notices filed upon yesterday so we gained a whopping 440 COMEX contracts or an additional 44,000 oz will stand for delivery AT THE COMEX in this active delivery month of December. THIS IS THE FIRST TIME THAT WE HAVE EVER SEEN A HUGE AMOUNT IN OZ OF QUEUE JUMPING IN GOLD.

January saw its open interest GAIN OF 22 contracts UP to 1981. FEBRUARY saw a loss of 6574 contacts down to 338,198.

We had 416 notice(s) filed upon today for 41600 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 247,947

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 199,816

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI SURPRISINGLY ROSE BY A TOTALLY UNEXPECTED 2526 CONTRACTS FROM 200,271 UP TO 202,797 DESPITE YESTERDAY’S 11 CENT LOSS IN PRICE (AND CONTINUAL RAIDING OF OUR PRECIOUS METALS). HOWEVER WE DID HAVE ANOTHER STRONG 2503 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 2503. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WITHOUT A DOUBT WE HAD NO LONG SILVER LIQUIDATION AS DEMAND FOR PHYSICAL SILVER REMAINS STRONG ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER AS WELL AS THAT MASSIVE MIGRATION OF EFPS OVER TO LONDON. IT SEEMS THAT ALL OF OUR LOST SILVER COMEX OI CONTRACTS HAVE MIGRATED OVER TO THE PHYSICAL HUB OF OUR PRECIOUS METALS, LONDON. ON A NET BASIS WE GAINED 5029 OPEN INTEREST CONTRACTS:

2526 CONTRACTS GAIN AT THE COMEX WITH THE ADDITION OF 2503 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN: 5029 CONTRACTS

We are now in the big active delivery month of December and here the OI FELL by 39 contracts DOWN to 788. We had 198 notice filed upon yesterday so we GAINED 159 contract or an additional 795,000 oz will stand in this active delivery month of December.

The January contract month ROSE by 46 contracts UP to 1352. February saw a LOSS OF 1 OI contract FALLING TO 35. The March contract GAINED 2367 contracts UP to 163,823.

We had 44 notice(s) filed for 220,000 oz for the DECEMBER 2017 contract

INITIAL standings for DECEMBER

Dec 13/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

16075 oz

Scotia

500 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

416 notice(s)

41600 OZ

|

| No of oz to be served (notices) |

2011 contracts

(201,100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6722 notices

672,200 oz

20.908 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 1 customer withdrawal(s)

i) Out of Scotia: 1675.000 oz

500 kilobars

Total customer withdrawals: 1675.000 oz

we had 0 adjustment(s)

*December is the biggest delivery month of the year for gold and the fact that no gold has entered the vaults these past three trading days speaks volumes that there is no appreciable gold at the comex to deliver upon our longs and thus the reason for the migration to London

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 416 contract(s) of which 286 notices were stopped (received) by j.P. Morgan dealer and 74 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (6722) x 100 oz or 672,200 oz, to which we add the difference between the open interest for the front month of DEC. (2427 contracts) minus the number of notices served upon today (416 x 100 oz per contract) equals 873,300 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (6722) x 100 oz or ounces + {(2427)OI for the front month minus the number of notices served upon today (416) x 100 oz which equals 873,300 oz standing in this active delivery month of DECEMBER (27.16 tonnes). THERE IS 28 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 440 COMEX CONTRACTS STANDING OR 44,000 OZ WILL STAND AT THE COMEX AND QUEUE JUMPING INTENSIFIES IN GOLD.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER 2016, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 879,623.576 or 27.35 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 8,966,067.308 or 278.88 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 75 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

25,305.130 oz

brinks

|

| Deposits to the Dealer Inventory |

629,513.100 oz

Scotia

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

44

CONTRACT(S)

(220,000 OZ)

|

| No of oz to be served (notices) |

744 contract

(3,720,000 oz)

|

| Total monthly oz silver served (contracts) | 5528 contracts

(27,640,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of Brinks: 25,305.130 oz

TOTAL CUSTOMER WITHDRAWAL 25,305.130 oz

We had 1 Customer deposit(s):

i) into Scotia: 629,513.100 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: nil oz

we had 0 adjustment(s)

The total number of notices filed today for the DECEMBER. contract month is represented by 44 contract(s) FOR 220,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 5528 x 5,000 oz = 27,640,0000 oz to which we add the difference between the open interest for the front month of DEC. (788) and the number of notices served upon today (44 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 5528 (notices served so far)x 5000 oz + OI for front month of DECEMBER(788) -number of notices served upon today (44)x 5000 oz equals 31,360,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE GAINED AN ADDITIONAL 159 CONTRACTS OR 795,000 OZ THAT WILL STAND AT THE COMEX AS QUEUE JUMPING ACCELERATES WITH RESPECT TO SILVER. BOTH GOLD AND SILVER ARE NOW EXPERIENCING QUEUE JUMPING.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 68,763

CONFIRMED VOLUME FOR FRIDAY: 59,555 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 59,555 CONTRACTS EQUATES TO 297 MILLION OZ OR 42.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 56.846 million

Total number of dealer and customer silver: 240.961 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 0.6 percent to NAV usa funds and Negative 0.8% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.4%

Percentage of fund in silver:36.3%

cash .+.3%( Dec 13/2017)

not available tonight

2. Sprott silver fund (PSLV): NAV FALLS TO -0.68% (Dec 13 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.24% to NAV (Dec13/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.68%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.24%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 13/2017/ Inventory rests tonight at 842.81 tonnes

*IN LAST 292 TRADING DAYS: 98.14 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 227 TRADING DAYS: A NET 59.14 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 28.03 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

Dec 13/2017:

Inventory 326.714 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.52%

12 Month MM GOFO

+ 1.82%

30 day trend

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

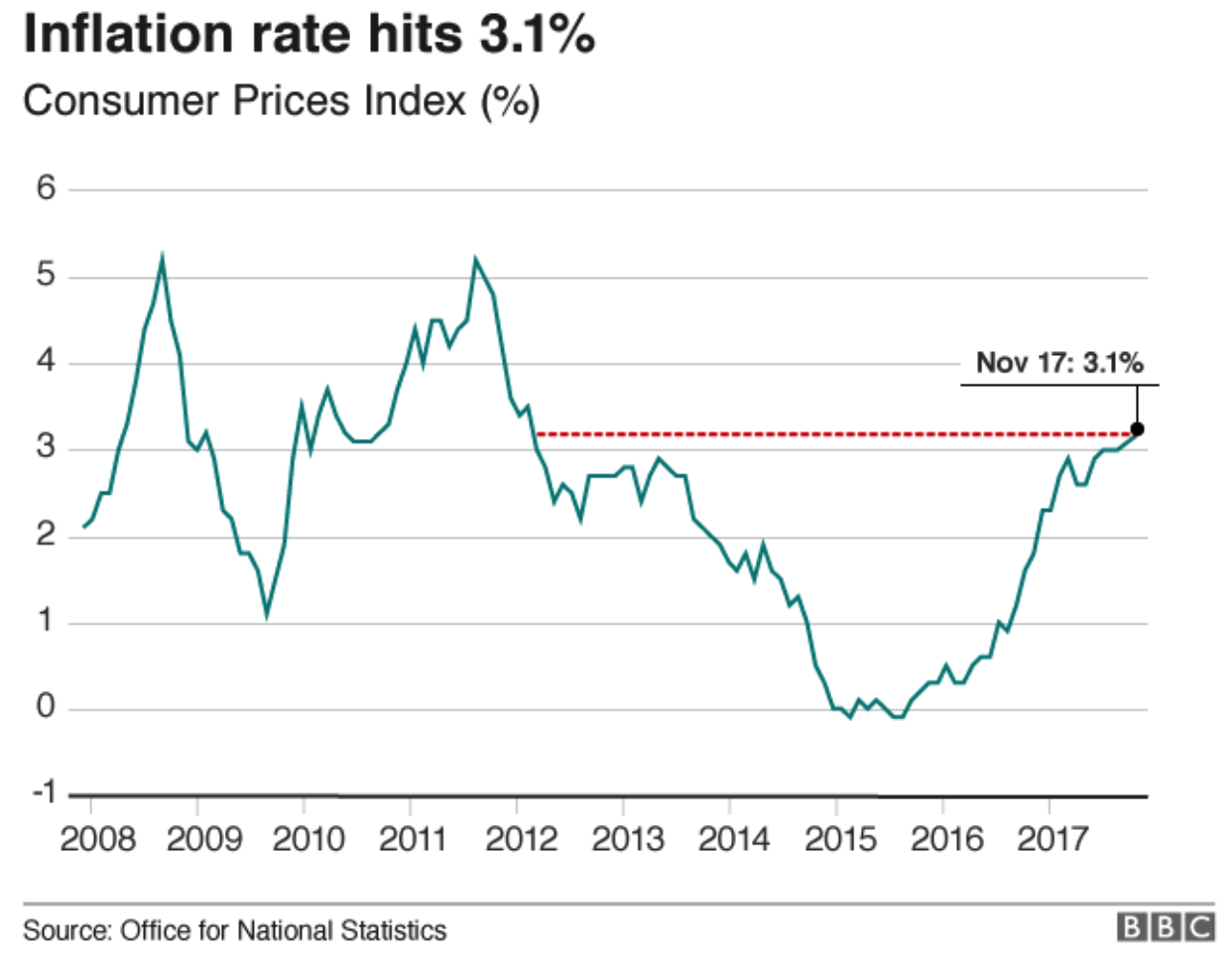

UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– UK inflation hits 3.1%, highest in nearly six years

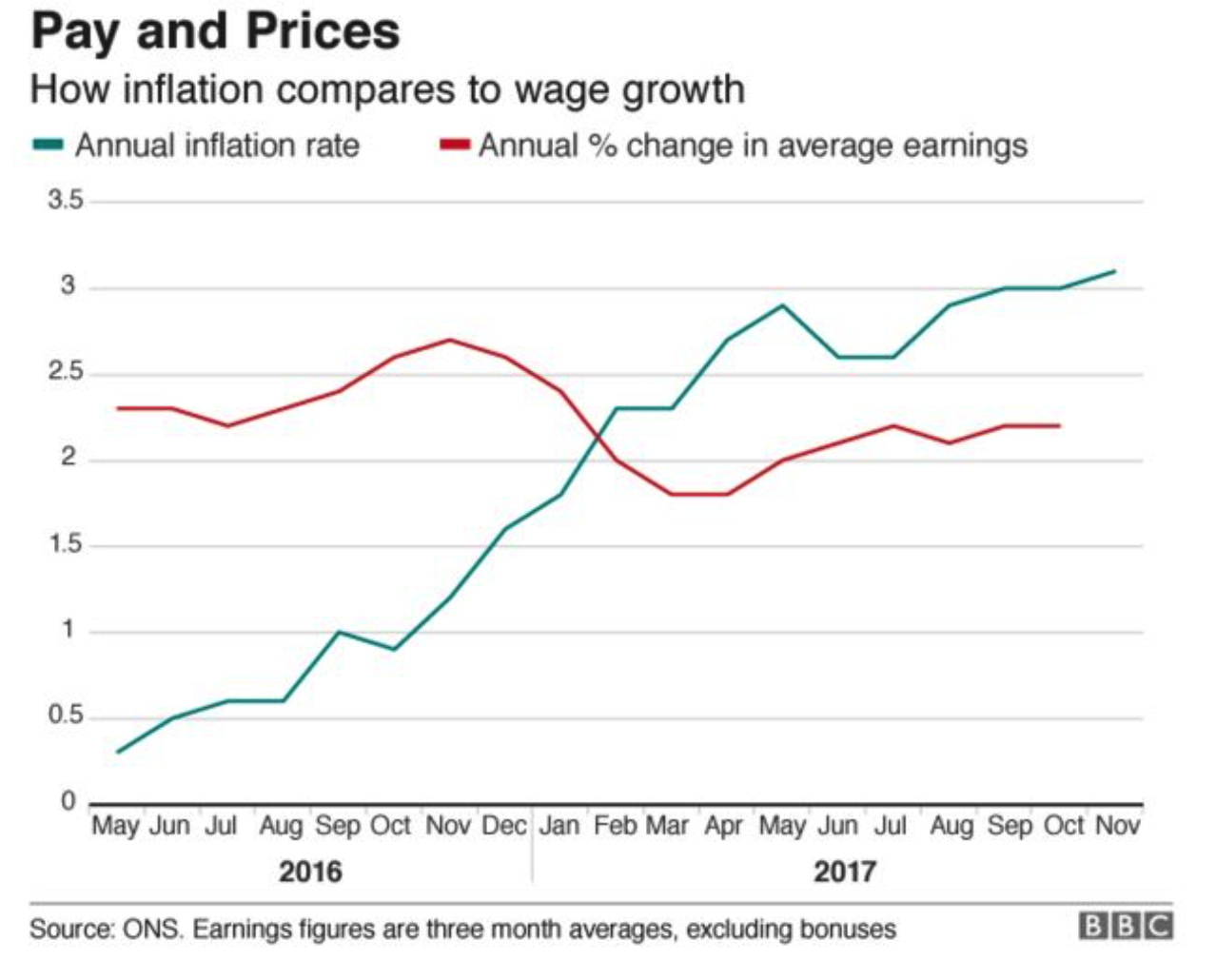

– UK earnings flat – households are still suffering falling real wages

– Stagflation risk as food and drink prices jumped 4.1% in 12 months

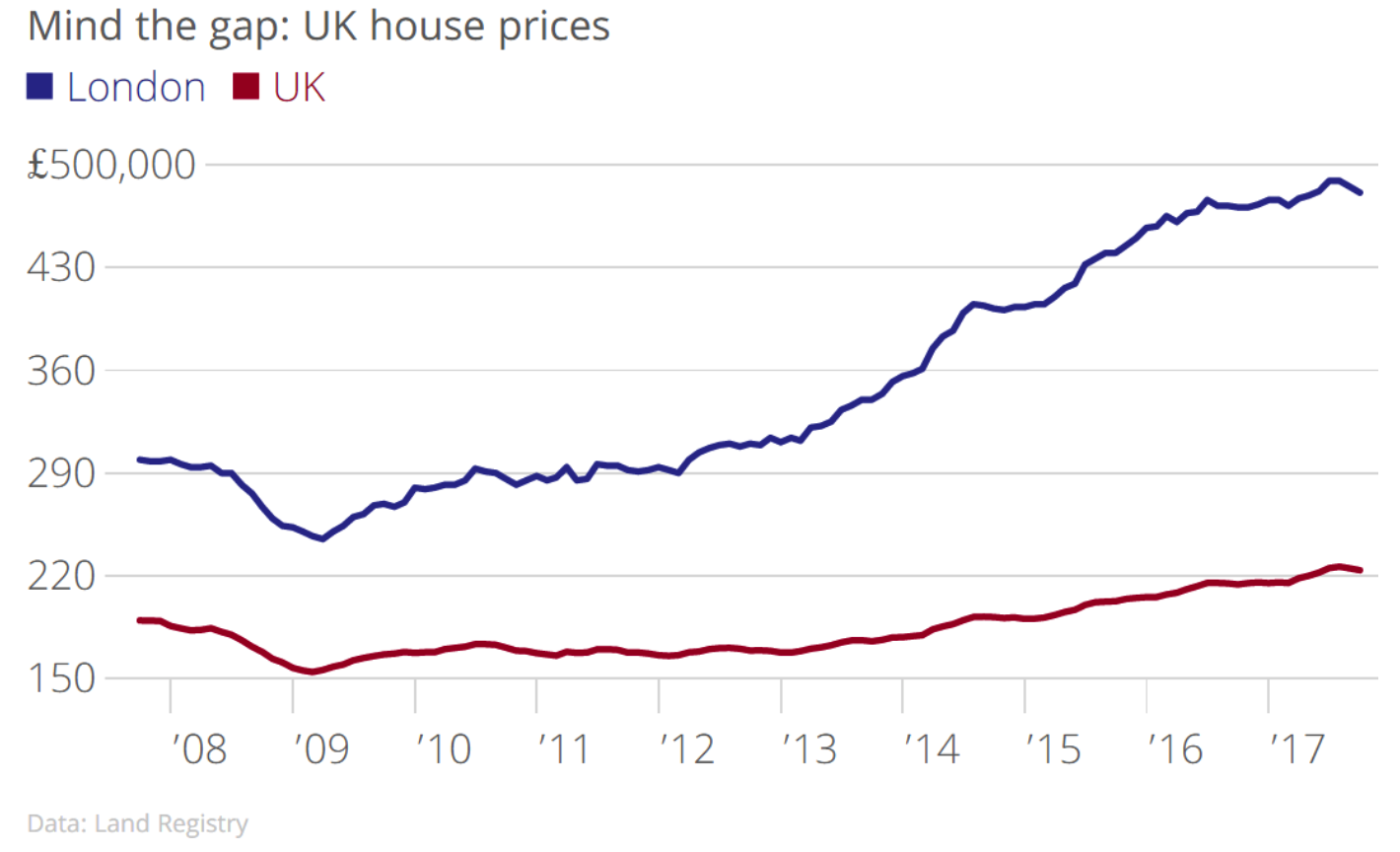

– UK house prices fall two-months in a row, down 0.5% in October

– Real stagflation risk now, inflation high and growth slowing

– Savings continue to be eaten by inflation

It was just two years ago that Mark Carney was writing his fourth letter to the British Chancellor, explaining why the country was in a deflationary slump. Even then households were feeling the pinch, despite what officials reported.

Since then Brits have become increasingly vindicated as inflation figures have begun to show what they have all known for some time – prices and the cost of living is on the rise.

Now Mark Carney is forced to write a different type of letter to the Chancellor, one where he will have to explain why inflation is above target at 3.1%. The jump to over 3% in the year to November is the fastest paced increase seen in nearly six years.

Carney’s dilemma

The Governor of the Bank of England now finds himself in a bit of a quandary.

Usually a central bank would increase interest rates in order to combat inflation. Currently the UK’s stands at the punishingly low 0.5% so one would think that there is plenty of room for manoeuvre.

However, debt levels in the UK are massive – at every strata of society – and increase rate rises will lead to a recession or indeed a depression. There is also the not inconsequential matter of Brexit.

Brexit is now seemingly more important than the spending and saving power of Britain’s households and must be considered when looking at a rate hike. When rates were raised last month (the first time in a decade) it was done with the Bank of England’s acknowledgement that Brexit was likely to hurt the country’s growth prospects. So the MPC erred on the side of caution.

With the Brexit cloud growing ever darker and uncertain, the Committee are aware of the need to keep consumer spending, the engine of the UK economy, pumping along. However, if inflation is not ‘handled’ then too much inflation could threaten the central bank’s grip on the economy. Too much inflation could result in total engine failure.

This is Carney’s dilemma.

No dilemma for households?

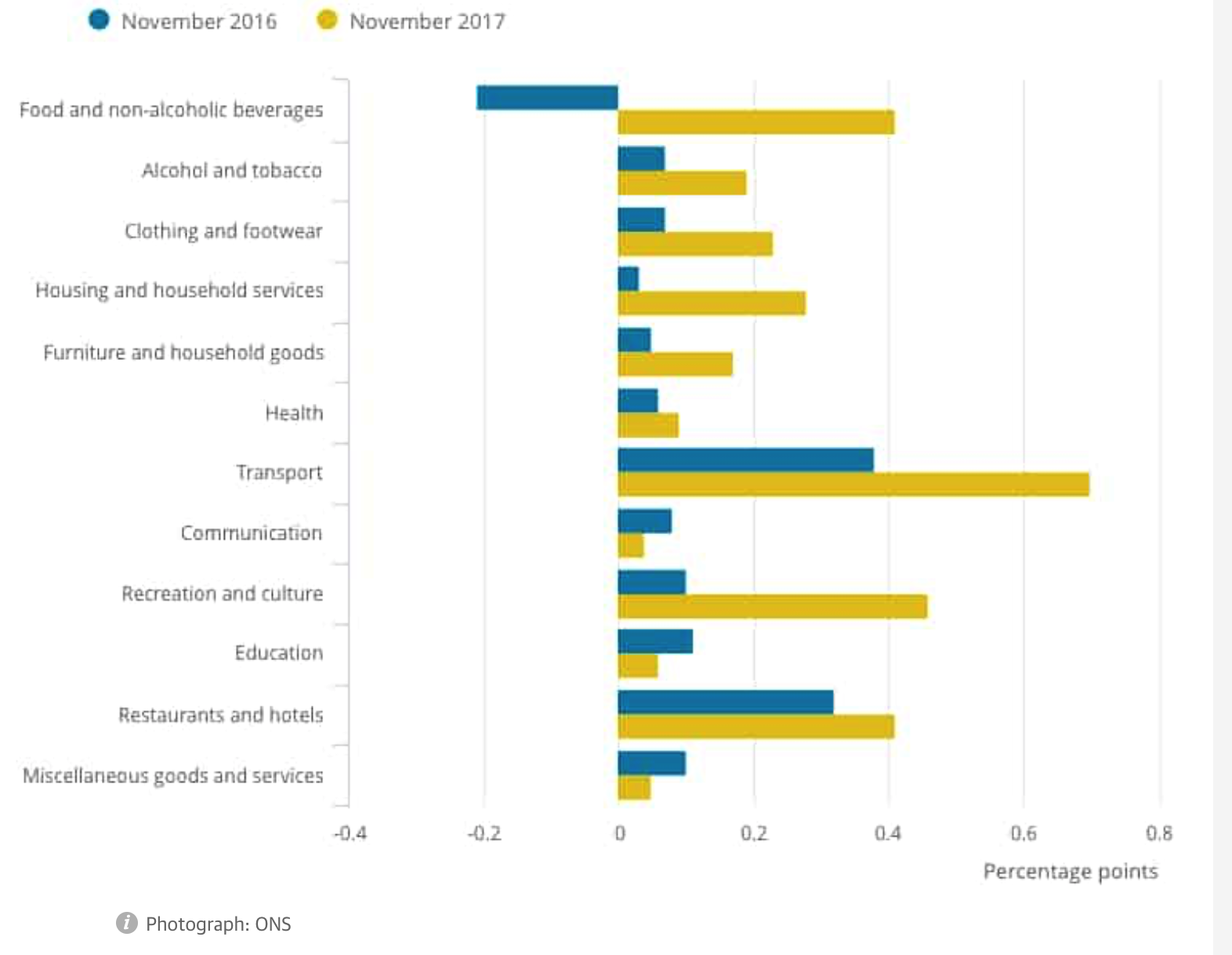

For savers, pensioners, businesses and households the situation should really be a no brainer. Household bills for food and non-alcoholic drinks are now up by a punishing 4.1% in the last year.

And that discounts the stealth inflation that is taking place in the UK and internationally in the form of shrinkflation. Shrinkflation in the UK is very real with real inflation much higher than reported and realised as consumer items, especially food, shrink in size while prices remain the same or go higher.

Savers, pensioners and households are likely tearing their hair out as economists rush to point to airfares and computer games as the main causes of increasing inflation figures. This is of little consequence to a household pushed to its limits when it comes to feeding and clothing a family.

A flight to Malaga or the next Grand Theft auto is likely the last things on parents’ minds.

The squeeze is so tight that many households have been forced into credit card spending and other forms of borrowing. This has been ‘manageable’ so far as deals offered by credit companies often mean no payments for a set period, free transfers and interest rates make little difference to borrowing costs.

The primary way to combat inflation is to hike interest rates. This will be good if it brings down household debt in the long term but painful as it will push up the cost of debt in the short and likely medium term.

UK household debt stands at £1,630.1 billion (£1.63 Trillion)

Currently UK household debt stands at £1,630.1 billion, an increase of 19% in the last five years.

Sadly the latest measure does not include the rise in fuel prices. This is something else households and businesses are feeling the pinch in and must feel frustrated that it is so rarely acknowledged by those deciding the fate of finances.

The RAC have today warned that thanks to the shutdown of a major North Sea pipeline could push fuel prices up by a further 3p. This will be felt acutely in an economy that saw fuel and raw material bills for manufacturers up 7.3% in November, up from 4.8% in October, while factory gate prices rose by 3%, up from 2.8% in October.

Those who actually live, spend and want to live in the black have a terrible dilemma on their hands. Inflation is killing them, debt is helping them to get by but the solution to both is going to be crippling.

No savings and situation set to worsen

Sadly there is currently little incentive to save. Wages are not keeping pace with inflation and the latter just eats away at cash in the bank. UK savings are at their lowest in fifty years.

Latest readings show weekly wage inflation is just at 2.2%. For those recalling inflation levels of the 70s and 80s and are currently scoffing at an inflation reading of 3.1% it would be worth reminding you that back then wage inflation was actually outpacing the CPI.

30-40 years ago the logic that wages would respond to higher prices and outpace them was really happening. Today, this is a fallacy.

The situation is made worse by what is in store for the UK economy. Following the release of the inflation figures many economists were quick to reassure that we were now seeing the peak of inflation.

This is highly doubtful. The Bank of England and ONS are pointing towards the weak post-Brexit pound as argument for inflation levels. In truth, the fall in sterling was just the much needed catalyst inflation needed in order to appear in official readings.

Households, businesses and savers and been feeling inflation long before Brexit was even in our common lexicon.

We have inflation today, as we have for at least the past five years. But along with it we also have shrinkflation and now what appears to be signs of stagflation.

Stagflation occurs when there is persistently high inflation combined with stagnant demand and low employment levels. This is appearing in the UK housing market where prices are down for the second-month in a row and the volume of transactions is falling. Unemployment remains low in the UK but this looks set to change.

Only set to get worse so buy gold

From Brexit to stagflation to debt levels it is tricky to see how Governor Mark Carney can turn this situation around. Whilst he might, just might, be able to pull it out the bag for the sake of appearances the ‘solution’ is unlikely to be one which is beneficial to savers.

The monetary policy we have fallen victim to is wealth ignorant. It does not create or protect wealth. It eats away at it month by month. It shows little regard to how you spend your money and where you hold your cash. This why investors and savers must diversify their portfolios and own real assets which cannot be devalued by monetary and government policies.

Investments such as gold and silver by their very nature are immune to the effects of inflation, stagflation and the dangerous ideas and experiments of central banks.

This year gold is up by nearly 8% and acting as . Wouldn’t it be nice next time the UK inflation figures are released to consider how your portfolio has done in real terms thanks to precious metals?

Related reading

UK Debt Crisis Is Here – Consumer Spending, Employment and Sterling Fall While Inflation Takes Off

Shrinkflation In UK – Real Inflation Much Higher Than Reported

UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

Brexit Budget – Grim Outlook As UK Economy Downgraded

News and Commentary

Gold prices hold steady, focus shifts to Fed meeting outcome (Reuters.com)

Gold Traders Are ‘Jaded’ to Global Fears Ahead of Expected Fed Hike (Bloomberg.com)

U.S. Stocks Mixed After Paring Gains, Dollar Rises (Bloomberg.com)

U.S. government posts $139 billion deficit in November (Reuters.com)

House price growth has fallen for the third month in a row (CityAM.com)

Source: Goldman via Zerohedge

London property prices set to drop in 2018 (Independent.co.uk)

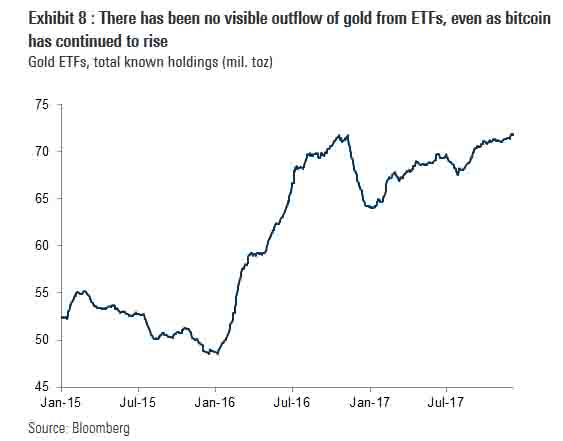

Is Bitcoin Really Stealing Demand For Gold? Here Is Goldman’s Answer (Zerohedge.com)

Rise of bitcoin has all the hallmarks of a disaster waiting to happen (MarketWatchc.com)

How to protect yourself from the “bubble in bubbles” (StansberryChurcHouse.com)

$10,000 Gold – Jim Rickards Makes The Case (BusinessInsider.com)

Gold Prices (LBMA AM)

13 Dec: USD 1,241.60, GBP 929.96 & EUR 1,056.97 per ounce

12 Dec: USD 1,243.40, GBP 933.92 & EUR 1,056.27 per ounce

11 Dec: USD 1,251.40, GBP 935.80 & EUR 1,061.19 per ounce

08 Dec: USD 1,245.85, GBP 924.42 & EUR 1,061.09 per ounce

07 Dec: USD 1,256.80, GBP 937.57 & EUR 1,066.77 per ounce

06 Dec: USD 1,268.55, GBP 948.37 & EUR 1,072.31 per ounce

05 Dec: USD 1,275.90, GBP 950.29 & EUR 1,075.71 per ounce

Silver Prices (LBMA)

13 Dec: USD 15.71, GBP 11.76 & EUR 13.38 per ounce

12 Dec: USD 15.78, GBP 11.82 & EUR 13.40 per ounce

11 Dec: USD 15.84, GBP 11.84 & EUR 13.43 per ounce

08 Dec: USD 15.83, GBP 11.76 & EUR 13.48 per ounce

07 Dec: USD 15.91, GBP 11.94 & EUR 13.49 per ounce

06 Dec: USD 16.12, GBP 12.06 & EUR 13.64 per ounce

05 Dec: USD 16.29, GBP 12.14 & EUR 13.72 per ounce

Recent Market Updates

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

– An Interview with GoldCore Founder, Mark O’Byrne

– Risk Of Online Accounts Seen As One of Largest Brokerages In World Halts Online Trading After “Glitch”

– Low Cost Gold In The Age Of QE, AI, Trump and War

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

– Financial Advice from Dr Wayne Dyer

– Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– Brexit Budget – Grim Outlook As UK Economy Downgraded

END

Gold trading today/early morning: the CPI is probably the most important number released in the month. We had a much weaker CPI (to which Janet is not happy as they need wage inflation), which caused treasury yields to drop, the dollar to drop and gold/silver to rise

(courtesy zerohedge)

Gold Pops, Bond Yields Drop, & Dollar Flops After Weaker-Than-Expected CPI

Hours ahead of today’s “historic” final Yellen FOMC rate hike, CPI disappointed and traders are bidding bonds and bullion while dumping the dollar…

The odds of two rate hikes next year just tumbled…

Gold jumped and the dollar dumped…

And Treasury yields are tumbling…

end

What a riot: the bankruptcy of Mt Gox has now become quite interesting in that the assets (the bitcoins) have risen 40 fold. Now the claimants could be made whole. However the original owners want that asset. The creditors should win

(Lewis/London’s Financial Times)

Bitcoin surge prompts bid to remove Mt Gox from bankruptcy

Submitted by cpowell on Tue, 2017-12-12 15:04. Section: Daily Dispatches

By Leo Lewis

Financial Times, London

Tuesday, December 12, 2017

A group of creditors pursuing a potentially vast bitcoin fortune from the imploded Mt Gox exchange have begun a legal action in Tokyo that would, if successful, remove the company from bankruptcy, disburse more than $3 billion worth of coins among depositors, and stop its former chief executive emerging from the debacle as a multibillionaire.

The move, which breaks largely uncharted legal ground in Japan, is a response by frustrated claimants to the recent stratospheric rise of bitcoin and a liquidation process that began when the cryptocurrency was trading at just a fraction of its current price of 2 million yen ($17,600) per bitcoin.

Creditors involved in launching the legal challenge to the bankruptcy say the 40-fold price surge in bitcoin since Mt Gox’s collapse in February 2014 has fundamentally changed the financial mathematics of the bankruptcy, because the company’s assets now completely dwarf its liabilities.

Mark Karpels, the exchange’s former chief executive currently fighting charges of embezzlement in Tokyo, controls the company that owns almost 90 percent of Mt Gox. At the current bitcoin price, Mt Gox could meet all its liabilities and, under Japanese law, Mr Karpeles would then receive his share of the surplus — a theoretical fortune worth well in excess of $2 billion. …

… For the remainder of the report:

https://www.ft.com/content/e741e792-df16-11e7-a8a4-0a1e63a52f9c

end

Bitcoin trading: the futures are doing their thing as Bitcoin falls below 16,000 per coin

(courtesy zerohedge)

Crypto Is Suddenly Crashing – Bitcoin Back Below $16,000

While Ethereum remains solidly higher on the day, the entire crypto space just took a notable leg lower.

The day’s slide started around 9amET, when a burst of gold buying appears to have reset the correlation between XAU and BTC:

Just a few hours later, Bitcoin is back below $16,000

Litecoin – yesterday’s big winner – is tumbling…

And while Ethereum is up 11% still, it is roling over…

Futures are underperforming spot and collapsing the arbitrage…

While no immediate catalyst for the moves is obvious, we note that Interactive Brokers has allowed clients to short Bitcoin futures (with a massive $40,000 margin) and South Korea said on Wednesday it may tax capital gains from cryptocurrency trading as global regulators worried about a bubble, with Australia’s central bank chief warning of a ‘speculative mania” that has seen the digital asset making rip-roaring gains.

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.6200 /shanghai bourse CLOSED UP AT 22.22 POINTS 0.68% / HANG SANG CLOSED UP 428.22 POINTS OR 1.49%

2. Nikkei closed DOWN 108.10 POINTS OR 0.67% /USA: YEN RISES TO 113.33

3. Europe stocks OPENED ALL MIXED /USA dollar index RISES TO 94.07/Euro FALLS TO 1.1735

3b Japan 10 year bond yield: RISES TO . +.050/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.33/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.34 and Brent: 63.82

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.326%/Italian 10 yr bond yield UP to 1.783% /SPAIN 10 YR BOND YIELD UP TO 1.493%

3j Greek 10 year bond yield FALLS TO : 4.431?????????????????

3k Gold at $1241.10 silver at:15.70: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 28/100 in roubles/dollar) 59.03

3m oil into the 57 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.33 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9921 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1643 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.326%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.415% early this morning. Thirty year rate at 2.786% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Rebound From “Bama Shock”, All Eyes On Yellen’s Last Rate Hike

After an early slide last night following the stunning news that Doug Jones had defeated Republican Roy Moore in the Alabama special election, becoming the first Democratic senator from Alabama in a quarter century and reducing the GOP’s Senate majority to the absolute minimum 51-49, US equity futures have quickly rebounded and are once again in the green with the S&P index set for another record high, as European stocks ease slightly, and Asian stocks gain ahead of today’s Fed rate hike and US CPI print.

“The big issue now is whether Republicans will push through their tax bill before Christmas,” said Sue Trinh, head of Asia foreign-exchange strategy at RBC Capital Markets in Hong Kong. “And more broadly, U.S. dollar bulls will be more worried that this marks a Democratic revival into 2018 mid-term Congressional elections.”

The negative sentiment faded quick, however, because according to Bloomberg, despite the loss of a Senate seat, it probably won’t affect the expected vote on business-friendly tax cuts, however, as the winner won’t be certified until late December.

Yet despite the bullish reversal in equities where the BTFD algos quickly arrived, the Bloomberg Dollar Spot Index fell for the first time in eight days after the Jones victory, ending its longest winning streak since January 2016. That said, the market has largely forgotten Alabama by now, and will focus on the Fed’s forward guidance as the central bank is widely expected to raise interest rates on Wednesday, with Treasuries slipping in the London session. The USD Index is just clinging on to the 94.000 marker and paring broad basket losses made in the wake of Alabama’s election result. However, the next major directional move (towards 94.500 or 93.500) will likely come from the FOMC tonight, notwithstanding CPI data after Tuesday’s firmer than forecast PPI readings

Ironically, the narrative that a Democrat won Alabama for the first time in decades is bullish for stocks did not reach Europe on time, and the continent struggled to match Asian gains as investors awaited policy decisions by central banks on the continent and in America. Most European bonds followed Treasuries lower as the dollar retreated. European stocks were fractionally lower (Stoxx 600 -0.1%) with a gain in retail shares, led by U.K. electronics retailer Dixons Carphone Plc, was offset by a drop in food and beverage companies and household goods names. Zara owner Inditex SA is among the best performers on the European gauge after signaling that sales growth is rebounding this quarter after weakening to the slowest pace in more than three years. An earlier technical problem that delayed the opening of all futures and options trading on Eurex, Europe’s largest derivatives market, has been resolved.

Earlier, solid gains in Asia overnight inched MSCI’s 47-country world index up for a fifth day running and while the pre-Fed anticipation meant Europe’s main bourses were barely budged, there was action elsewhere as stocks in Australia, South Korea and Hong Kong rose, while stocks in Tokyo fell. U.S. equities posted fresh all-time highs overnight after data showed signs of inflation in producer prices. Australia’s ASX closed +0.1%, kept in a tight range while Japan’s Nikkei 225 (-0.5%) was dampened by a firmer JPY, as focus centred on the developments in US which was a blow for President Trump and effectively tightens the passage for tax reforms. Hang Seng (+1.1%) outperformed and Shanghai Comp. (-0.1%) was choppy as liquidity efforts by the PBoC – which injected net funds via reverse repo for a 3rd day – were counterbalanced amid the backdrop of the risk events stateside.

The Alabama vote temporarily seized the spotlight away from the Fed, which will raise rates later by 25bps to between 1.25 and 1.50 percent, its third hike of the year and fifth since the financial crisis. Oppenheimer’s Brian Levitt suspects the Fed will also revise up its growth forecast, adding upside risk to the “dot plot” forecasts on interest rates, though he does not expect as many hikes next year as some economists.

“We are going to see a Fed that continues to attempt to tighten policy next year,” he said. “But fortunately with inflation low in the U.S. the Fed has the cover to go slowly… I know people have hopes for the tax cuts (planned by Trump), but I don’t think they will be able to push ahead with 3-4 rate hikes.”

As a result, comments on the outlook for 2018 will be the focus for investors as they weigh the impact of coming policy normalization on global asset prices, while it’s anticipated that the ECB will reveal details of plans to taper asset purchases on Thursday.

Meanwhile, more Brexit drama as UK PM May is being urged by some of her allies to consider the possibility of a cabinet reshuffle in order to build on her recent Brexit success, the FT reports, with the Times adding that the BoE should leave interest rates unchanged this month following November’s historic increase. Italian PM Gentiloni was on the wires saying that the next Brexit talk phase will be more challenging and called for a tailor-made trade deal between EU and UK. Separately, Labour said it will back Dominic Grieve’s amendment giving Parliament a proper say on the Brexit deal if he pushes it to a vote tonight. The terms of our future are not for the government alone to determine, according to the shadow Brexit secretary

Elsewhere in Europe, La Repubblica reported that Italian parties have agreed to hold elections on March 4th.

With the Fed looming, global rates were largely unchanged: the yield on 10-year Treasuries increased one basis point to 2.41%, reaching the highest in almost seven weeks as 10-year Bund yields gained two basis points to 0.33%, the highest in more than a week; Britain’s 10Y Gilt yield climbed one basis point to 1.202%.

In commodity markets, oil was nudging back towards two-year highs hit in the previous session on an unplanned closure of the pipeline that carries the largest volume of North Sea crude oil. Brent crude added 0.8 percent, or 51 cents, to $63.85 a barrel, after shedding 2 percent on Tuesday. U.S. crude added 0.7 percent, or 38 cents, to $57.52, after slipping 1.4 percent overnight. Gold was near its weakest level in almost five months at $1,242.18 an ounce. It is often seen as a safe-haven play and can perform poorly when central bank’s like the Fed feel confident enough to raise interest rates.

Market Snapshot

- S&P 500 futures up 0.02% to 2,668.25

- STOXX Europe 600 down 0.1% to 391.17

- MSCI Asia up 0.3% to 170.33

- MSCI Asia ex Japan up 0.4% to 553.80

- Nikkei down 0.5% to 22,758.07

- Topix down 0.2% to 1,810.84

- Hang Seng Index up 1.5% to 29,222.10

- Shanghai Composite up 0.7% to 3,303.04

- Sensex down 0.7% to 32,999.64

- Australia S&P/ASX 200 up 0.1% to 6,021.83

- Kospi up 0.8% to 2,480.55

- German 10Y yield rose 0.5 bps to 0.319%

- Euro up 0.08% to $1.1751

- Brent Futures up 1.5% to $64.28/bbl

- Italian 10Y yield rose 5.2 bps to 1.443%

- Spanish 10Y yield rose 2.7 bps to 1.489%

- Brent Futures up 1.5% to $64.28/bbl

- Gold spot down 0.2% to $1,242.18

- U.S. Dollar Index down 0.1% to 93.98

Top News from Bloomberg

- Democrat Doug Jones delivered an upset defeat to Republican Roy Moore in deep-red Alabama. Jones’s victory cuts the GOP’s Senate majority to just 51-49, which will make it harder for the party to enact its agenda; Moore says Alabama senate election ‘not over’; doesn’t concede

- Cutting the top individual income tax rate to 37%, setting the corporate tax rate at 21% and capping the mortgage interest deduction at loans of $750,000 or less are among the issues being considered as congressional Republicans consider last-minute revisions to key provisions in tax-overhaul legislation

- With many believing the a 25 basis point increase in the benchmark federal funds rate is a given, investors will focus on the Fed’s projections for future rate hikes in today’s FOMC meeting

- The EU warned the U.K. against rowing back on the agreements it made last week as leaders prepare to hand Britain its first reward in the Brexit negotiations

- China and the U.K. will assess the feasibility of a bond-trading link that would mark a fresh step in opening up the world’s third-largest debt market, according to people familiar with the matter

- German Social Democrat leader Martin Schulz, who last week secured an endorsement to hold talks with Merkel, has told members the party will explore a “cooperation coalition,” which would include cabinet posts for the SPD but fall short of a traditional government partnership

- Sentiment among chief financial officers in the U.S. advanced to a 13-year high on optimism surrounding proposed corporate-tax cuts, indicating the economy will continue to make strides next year

- President Trump plans to make what his staff members called a “closing argument” for tax- overhaul legislation Wednesday as congressional Republicans consider last-minute revisions to key provisions

- Eurozone industrial output expanded 0.2% m/m in October, beating the estimate for a flat reading

- Despite a recent bounce back, analysts and investors say the dollar could lose more ground against the euro and yen as the prospect of strong economic growth and tighter monetary policy outside the U.S. more than offsets higher interest rates at home

- U.K. Prime Minister Theresa May’s flagship Brexit Bill returns to the House of Commons Wednesday for a seventh day of detailed scrutiny. Conservative pro-Europeans want a line in the bill requiring the government to pass full legislation before it attempts to implement any Brexit deal it reaches with the European Union.

- Secretary of State Rex Tillerson said the U.S. is prepared to negotiate with North Korea without preconditions, but the Trump administration would first want a “quiet period” without nuclear or missile tests for discussions with Kim Jong Un’s regime to begin

Asia equity markets were mostly positive on what was an indecisive trading day with the region cautious throughout most of the session ahead of the looming FOMC and amid the Alabama Senate election results, in which the GOP’s US Senate majority was trimmed to 51-49 seats after Doug Jones won the race to be the state’s first Democratic Senator in 25 years. ASX 200 (+0.1%) was kept in a tight range and Nikkei 225 (-0.5%) was dampened by a firmer JPY, as focus centred on the developments in US which was a blow for President Trump and effectively tightens the passage for tax reforms. Hang Seng (+1.1%) outperformed and Shanghai Comp. (-0.1%) was choppy as liquidity efforts by the PBoC were counterbalanced amid the backdrop of the risk events stateside. Finally, 10yr JGBs were range-bound with early support seen amid weakness in Japanese stocks and after the BoJ Rinban announcement for JPY 960bln in 1yr-10yr JGBs, although this was later pared in 2nd half of trade in which prices returned flat. PBoC injected CNY 70bln via 7-day reverse repos and CNY 60bln via 28-day reverse repos. PBoC set CNY mid-point at 6.6251. CASS official Yin said Chinese interbank liquidity will remain tight until the Lunar New Year due to wealth management business restrictions and expected Fed hikes, while Yin added the solution to liquidity problems is to lower RRR.

Top Asian News

- China Is Said to Plan U.K. Bond-Connect Joint Feasibility Study

- Carlsberg Says It Reaches ‘Understandings’ on Habeco Deal Talks

In Europe, equities trade slightly in the red (Stoxx 600 -0.1%) with little in the way of firm direction with the reduction in the GOP’s Senate majority following Democrat Doug Jones’ victory in Alabama seeing little follow through into European trade. The FSTE MIB (-0.4%) lags its peers amid political concerns after Italian parties have agreed to hold elections on March 4th, subsequently reinvigorating concerns over the rise of anti-establishment sentiment in the nation via the 5Star movement. In terms of sector specific performance, consumer discretionary names are the notable outperformers, bolstered by Spanish heavyweight Inditex which had been up as much as 4% in the wake of their latest earning release. Another relatively tame reaction to UK data, and this time for good (fundamental) reason as the latest labour and wage update is somewhat contradictory. Gilts have slipped to a marginal new Liffe low at 124.63 (13 ticks under yesterday’s close, albeit 23 ticks below best levels seen so far) and the Short Sterling strip has reversed earlier gains of 1 tick and a tad more. However, these losses are far more contained compared to the downside seen in the Eurozone where Bunds appear to have been dragged down by more pronounced selling in peripheral bonds, and especially Italian BTPs on political jitters – president to dissolve Government at the end of the month and elections to be held in early March 2018. The 10 year German benchmark has been down to 162.91 (-36 ticks vs +13 ticks at best), while its Italian peer traded at 138.90 (-85 ticks) and the yield 5+ bp higher pushing the spread to Germany over 4 bp wider. From a tech perspective, Bunds may look towards 162.79-74 next. Elsewhere, US Treasuries are inching lower (through Tuesday’s lows) and the curve is fractionally steeper in typically defensive pre-FOMC fashion.

Top European News

- U.K. Loses Most Jobs Since 2015 as Labor Market Shows Strain

- U.K. Minister Hints at Concessions to Tory Rebels: Brexit Update

- German Social Democrats Weigh Coalition-Lite Tie-Up With Merkel

- Investec Provides U.K. Fintech With $67 Million for Online Loans

In FX markets, the USD Index is just clinging on to the 94.000 marker and paring broad basket losses made in the wake of Alabama’s election result. However, the next major directional move (towards 94.500 or 93.500) will likely come from the FOMC tonight, notwithstanding CPI data after Tuesday’s firmer than forecast PPI readings. GBP is Holding above lows vs the USD and EUR with GBP not swayed too much by the latest UK jobs report which saw a slightly higher unemployment rate and an unexpected uptick in ex-bonus earnings. Focus for GBP will likely continue to centre on politics with today’s parliamentary vote on the Brexit bill, with the opposition Labour Party affirming that it will side with Tory rebels wanting a say on the divorce deal. AUD continues to outperform (just) after upbeat survey news overnight (Westpac consumer index at 100+ multi-year high and sentiment rebounding to positive territory).

In commodities , energy prices trade modestly higher in the wake of yesterday’s API report which showed a larger than expected drawdown in headline crude stockpiles (-7.382mln vs. Exp. -3.8mln). Elsewhere, spot gold trades with little in the way of notable direction, whilst copper has seen some support from the broadly softer USD during London trade in what was otherwise a relatively subdued session overnight for the complex.

Looking at the day ahead, all eyes will be on the US with the November CPI report due out, and also the conclusion of the two-day FOMC meeting. Fed Chair Yellen will follow with her last press conference. Also of significance is a scheduled discussion between European parliamentarians and European Commission President Juncker and European Council President Tusk around the state of Brexit negotiations. Other data releases include the final November CPI revisions in Germany, October and November employment data in the UK, and October industrial production data for the Euro area. Finally, President Trump may speak on tax reforms today and Germany’s Merkel and SPD will also start formal coalition talks.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 4.7%

- 8:30am: US CPI MoM, est. 0.4%, prior 0.1%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- 8:30am: US CPI YoY, est. 2.2%, prior 2.0%; Ex Food and Energy YoY, est. 1.8%, prior 1.8%

- 8:30am: Real Avg Weekly Earnings YoY, prior 0.38%;

- 2pm: FOMC Rate Decision

- 2:30pm: Yellen Holds Her Final Press Conference Following FOMC Meeting

- 6pm: Fed’s Brainard Makes Opening Remarks at Awards Ceremony

DB’s Jim Reid concludes the overnight wrap

A pretty big day ahead with US CPI and Yellen’s last press conference and the associated latest Fed economic projections (including the dots) overshadowing what is now a near slam dunk US rate hike.

With regards to inflation, the house view is that inflation trends are beginning to firm and should continue in today’s CPI for both headline (0.4% mom vs. 0.1% previously) as well as core (0.2% mom vs. 0.2%). Watch out for those three decimal place numbers which are all in vogue at the moment as inflation holds the key to pretty much everything in 2018. Prints in line with DB forecasts would boost the six-month annualized change in core CPI about 25 bps over October’s number of 1.8%, which would provide further evidence of firming inflation. Staying on inflation the US’s November core PPI (ex food and energy) was above market yesterday at 0.3% mom (vs. 0.2% expected), while the annual increase of 2.4% yoy was in line. Our US economists noted the healthcare component of PPI – which is highly correlated with the healthcare component of the core PCE deflator – rose a solid 0.15% mom. In the UK, the headline November CPI was above expectations at 0.3% mom (vs. 0.2% expected), but the core annual CPI was in line and steady at 2.7% yoy – the highest since 2012. The core PPI was also in line at 2.2% yoy while the closely watched Sweden’s CPI was above market at 1.9% yoy (vs. 1.7% expected).

All this came on a day where Brent futures initially rallied to $65.83 on the previous day’s news of the crack shutting down a North Sea oil pipeline, but then reversed those gains to close 1.31% lower to $63.84/bbl. Elsewhere, the Jan 18 futures on UK natural gas prices jumped as much as 20% following an explosion at an Austrian hub, but closed c11% higher after news that natural gas flows in Europe are expected to resume soon. So it’s been a big 24 hours for all things price related and with today’s US inflation report, this is set to continue.

As for the FOMC meeting, the main focus will be on the messaging around the outlook for rate increases in 2018 and beyond. Although our economists recently shifted to expecting four rate increases next year, they think it is likely too early for this message to be solidified in a higher median “dot” for 2018. However, they still expect the signal from the meeting to be that with growth

well above potential, the labour market at full employment, record easy financial conditions, rising odds of fiscal stimulus, and early evidence that inflation is recovering, a gradual pace of rate hikes is warranted, and indeed risks have risen somewhat that the Fed could need to move more aggressively. They think this could be reflected in some upward migration in the dots, revisions to growth and unemployment forecasts, and the overall tone from the statement and press conference. The interpretation should be that if the economy remains broadly in line with the Fed’s and DB’s forecasts, tightening once per quarter should continue, with the next rate increase likely in March. Given Mrs Yellen’s history of being a team player and a consensus builder one would imagine her last press conference will not see any surprises left for her successor though.

In the US, momentum on the tax plans appears to be going reasonably well. The House Ways and Means Chairman Brady noted the conference panel could deliver the written agreement on the final tax legislations by Friday, noting “we’re on track for this week”. Looking ahead, the House Majority leader McCarthy told GOP members that the goal is for the House to vote on the reconciled tax bill next Tuesday (19th December), which is also confirmed by Senator Reed of NY, who noted “the time frame of a vote next week is very realistic”. Elsewhere, the final bill is evolving but some of the compromises noted by Washington Post include: i) mortgage deduction limit of $750k, ii) corporate tax rate of 21% and iii) top individual tax rate of 37%. We shall find out the details soon.

Staying in the US, Doug Jones will be the first Democrat to win a Senate seat in Alabama in almost 25 years. With c98% of precincts reporting, the Associated Press projects Jones as the winner with 49.5% of the votes versus 48.8% for the Republican candidate Mr Moore. Mr Jones is scheduled to take office before 3 January, so should not scuttle the tax votes too much if they proceed to plan but it could if delayed to 2018. Once the potential win is confirmed, it will reduce the Republican’s Senate majority to a thin margin of 51-49 (from 52-48) and could impact the prospects of future bills being passed. CNN noted that one in every 20 votes so far this year in the Senate would have had a different outcome if just one vote had flipped to the opposite side.

This morning in Asia, markets are mixed ahead of the upcoming central bank meetings. The Kospi (+0.50%), China’s CSI 300 (+0.41%) and Hang Seng (+1.08%) is up modestly, while the Nikkei (-0.55%) is down as we type. Elsewhere, the US dollar index is down 0.2% following the Alabama voting developments while WTI oil is trading c0.7% higher after API data showed US crude stockpiles

dropped for the fourth week.

Now recapping other markets performance from yesterday. US equities broadly rose to fresh highs following further progress on the tax bill, although gains were pared back after Senator Paul tweeted “I cannot in good conscience vote to add more to the already massive $20trn debt”. The S&P (+0.15%) and Dow (+0.49%) both rose modestly while Nasdaq dipped -0.19%. Within the S&P, gains in the telco and financials sector were partly offset by losses from utilities and energy stocks. European markets also trended higher, with Stoxx 600 up +0.66% to the highest in three months – supported by energy and tech stocks. Across the region, key bourses rose c0.5% (DAX +0.46%; FTSE +0.63%) while Spain’s IBEX fell 0.18%. The VIX rose for the first time in six days to 9.92 (+6.2%).

Following the aforementioned UK CPI and US PPI stats, government bonds weakened with core yields up 1-2bp (UST 10yr +1.3bp; Bunds & Gilts +2.1bp), while peripherals underperformed with yields up 4-5bp. Turning to currencies, the US dollar index firmed 0.23%, while Euro and Sterling fell 0.23% and 0.17% respectively. In commodities, precious metals edged c0.2% higher (Gold +0.20%; Silver +0.13%) while other base metals were mixed but also little changed (Copper +0.56%; Zinc +1.11%; Aluminium -0.70%).

Away from the markets and onto Brexit where the rhetoric continues. The EU Chief negotiator Barnier cautioned the UK against reneging on the agreements made last Friday, noting “we will not accept any backtracking from the UK”. Elsewhere, the EU Parliament lawmaker Guy Verhofstadt tweeted that it was time for the UK government to “restore trust” after the “unacceptable remarks” by Brexit Secretary Davis who noted the Brexit deal last week was more of a “statement of intent”. Nonetheless, the draft European Council guidelines seems to suggests trade talks between UK and EU could formally start in March 2018 as it noted “….the EC will continue to follow the (Brexit) negotiations closely and adopt additional guidelines in March 2018, in particular as regards the framework for the future relationship”.

Finally, Australia’s central bank governor Lowe has also added to the debate on Bitcoin. He noted “the current fascination with these currencies feels more like a speculative mania than it has to with their use as an efficient and convenient form of electronic payment”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the November NFIB small business optimism index was above market at 107.5 (vs. 104 expected) – the highest reading since 1983. In the UK, the RPI was slightly below expectations at 0.2% mom (vs. 0.3%) and 3.9% yoy (vs. 4.0%). In Europe, the December ZEW survey on expectations was slightly below the prior month’s reading at 29 (vs. 30.9 previous). In Germany, the ZEW survey on current situations was above market at 89.3 (vs. 88.7 expected) but expectations were a tad below market at 17.4 (vs. 18 expected).

Looking at the day ahead, all eyes will be on the US with the November CPI report due out, and also the conclusion of the two-day FOMC meeting. Fed Chair Yellen will follow with her last press conference. Also of significance is a scheduled discussion between European parliamentarians and European Commission President Juncker and European Council President Tusk around the state of Brexit negotiations. Other data releases include the final November CPI revisions in Germany, October and November employment data in the UK, and October industrial production data for the Euro area. Finally, President Trump may speak on tax reforms today and Germany’s Merkel and SPD will also start formal coalition talks.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 22.22 points or 0.68% /Hang Sang CLOSED UP 428.20 pts or 1.49% / The Nikkei closed DOWN 108.10 POINTS OR 0.47%/Australia’s all ordinaires CLOSED UP 0.16%/Chinese yuan (ONSHORE) closed DOWN at 6.6200/Oil DOWN to 57.34 dollars per barrel for WTI and 63.82 for Brent. Stocks in Europe OPENED ALL MIXED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6200. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6250 //ONSHORE YUAN SLIGHTLY WEAKER AGAINST THE DOLLAR/OFF SHORE MUCH WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(STRONG MARKETS)

3 a NORTH KOREA/USA

NORTH KOREA/

3 b JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

Italy:

Seems that the long awaited election is to be held on March 4 and that sent Italian bonds and their stock market southbound

(courtesy zerohedge)

Italian Bonds, Stocks Tumble On March Election Report

Two days after Prime Minister Paolo Gentiloni’s one-year anniversary of taking the country’s top job, Italy’s political parties have reached an agreement on when next year’s election will be held, according to Italian media reports, with the news prompting a selloff across Italian assets. According to local press, President Sergio Mattarella will dissolve parliament this month and set a March 4 election date.

The date has not yet been formally confirmed, but according to Repubblica, Italian President Sergio Mattarella – the only person who can call an election – and Italy’s main political parties have agreed on the date for Italy’s next general election. The vote has to be held before May 20th, 2018, The Local notes.

The news comes just a day after Paolo Gentiloni marked his one year anniversary as Italy’s Prime Minister, an office he took after Matteo Renzi resigned following a humiliating defeat in a national referendum. The failure of Renzi’s proposed constitutional reforms also meant Italy was left without a workable electoral law, as the upper and lower houses of parliament had two different electoral systems.

After months of debate, a new election law named ‘Rosatellum’ was finally passed in late October, despite fierce opposition from the Five Star Movement (M5S), which describes itself as ‘anti-establishment’. One crucial feature of the new law is that it favours parties which build alliances, something the M5S has ruled out doing. Speaking to La Stampa about his year in the top job, Gentiloni described it as a “roller coaster” and said that he would leave his successor “a more stable Italy”, which he said “has overcome its most serious crisis”.

It’s far from clear who that successor is likely to be. Under the Rosatellum law, there will only be a clear-cut winner if one party or bloc receives over 40 percent of the vote. Recent opinion polls show a centre-right coalition ahead, followed by the M5S and Gentiloni’s Democratic Party, but all of them several points away from the 40 percent bar.

One thing that is very clear, is that with Italian politics again in the spotlight, the market is getting nervous, and the news sent Italy’s MIB index lower by 1% while Italian 10-year yields shot up more than 10bps to 1.77%. So far, other Eurozone non-core bonds have been spared the selling as the catalyst is seen as Italy specific; meanwhile core bonds remain well bid. As RanSquawk summarizes, “Italian bonds are prone to every headline report about the impending election and dissolution of the incumbent regime.”

end

Theresa May has been humiliated as a vote in parliament has now stated that only Parliament can allow for a Brexit from the EU. This will further hamper the Government’s exit strategy. The pound surges on the news.

(courtesy zerohedge)

Theresa May Humiliated As Tory Rebellion Leads To Key Brexit Vote Loss

Prime Minister Theresa May suffered a humiliating defeat for her key Brexit law on Wednesday after pro-European members of her own party openly defied her orders in a vote in Parliament. The vote in the UK Parliament was described as being “knife-edge” with the BBC’s chief political correspondent, Norman Smith, called it a “Big Bananas moment” for May. In the end, May lost by a narrow margin, with 309 voting for and 305 against, and as a result, UK members of parliament – not Theresa May and her Cabinet – will have the final say on Brexit.

MPs had been asked to vote on the following amendment:

The final deal with the EU must be approved by a law passed by Parliament.

The results of the vote were as follows: Yes: 309 No: 305 Majority: 4

According to Sky News, 12-13 Conservative MPs voted against the government with 2 Labour MPs voted with the government, and “while this won’t derail the Brexit deal it is a sign of UK Prime Minister May’s increasingly strained position” Citi explained after the vote.

Some more media reactions, first the Telegraph: