GOLD: $1254.90 UP $8.60

Silver: $15.92 UP 7 cents

Closing access prices:

Gold $1253.20

silver: $15.91

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1254.20 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1243.80

PREMIUM FIRST FIX: $10.40

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1268.54

NY GOLD PRICE AT THE EXACT SAME TIME: $1256.90

Premium of Shanghai 2nd fix/NY:$11.64

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1255.60

NY PRICING AT THE EXACT SAME TIME: $1255.10

LONDON SECOND GOLD FIX 10 AM: $1251.00

NY PRICING AT THE EXACT SAME TIME. 1255.10 ???

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECEMBER CONTRACT: 288 NOTICE(S) FOR 28,800 OZ.

TOTAL NOTICES SO FAR: 7010 FOR 701,000 OZ (21.804 TONNES),

For silver:

DECEMBER

270 NOTICE(S) FILED TODAY FOR

1,350,000 OZ/

Total number of notices filed so far this month: 5798 for 28,990,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $16,138/OFFER $16,500, UP $86 (morning)

BITCOIN : BID $16,397 : OFFER 16,571 UP $91 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY ROSE BY A GOOD SIZED 3313 contracts from 202,797 RISING TO 206,110 WITH YESTERDAY’S FAIR SIZED 20 CENT RISE IN SILVER PRICING. WE HAD NO COMEX LIQUIDATION AND ON TOP OF THIS, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1492 EFP’S FOR MARCH (AND ZERO FOR DEC AND OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 1492 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1492 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 2503 EFP’S FOR SILVER ISSUED.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DECEMBER:

31,337 CONTRACTS (FOR 10 TRADING DAYS TOTAL 31,337 CONTRACTS OR 156.68 MILLION OZ: AVERAGE PER DAY: 3,133 CONTRACTS OR 15.665 MILLION OZ/DAY)

RESULT: A GOOD SIZED RISE IN OI COMEX WITH THE 20 CENT RISE IN SILVER PRICE. HOWEVER WE HAD NO SILVER LIQUIDATION AT THE COMEX PLUS A FAIR SIZED 1492 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON THROUGH THE EFP ROUTE: FROM THE CME DATA 1492 EFP’S WERE ISSUED TODAY (FOR MARCH EFP’S) FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. IN ESSENCE THE DEMAND FOR SILVER PHYSICAL INTENSIFIES GREATLY. WE REALLY GAINED 4805 OI CONTRACTS i.e. 1492 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3313 OI COMEX CONTRACTS. AND ALL OF THIS INCREASED DEMAND HAPPENED WITH THE FAIR SIZED RISE IN PRICE OF SILVER BY 20 CENTS AND A CLOSING PRICE OF $15.85 YESTERDAY. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.032 BILLION TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DECEMBER MONTH/ THEY FILED: 270 NOTICE(S) FOR 1,350,000 OZ OF SILVER

In gold, the open interest ROSE BY WHOPPING 9533 CONTRACTS UP TO 456,151 WITH THE FAIR SIZED GAIN IN PRICE OF GOLD YESTERDAY ($6.40). HOWEVER, THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED AN UNBELIEVABLE 17,961 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 17,961 CONTRACTS. The new OI for the gold complex rests at 456,151. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE WITNESS THE HUMONGOUS NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUGE GAIN OF 27,494 OI CONTRACTS: 9,533 OI CONTRACTS INCREASED AT THE COMEX AND THE MONSTROUS 17,961 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 11,317 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DECEMBER STARTING WITH FIRST DAY NOTICE: 137,203 CONTRACTS OR 13.720 MILLION OZ OR 426.74 TONNES (10 TRADING DAYS AND THUS AVERAGING: 13,720 EFP CONTRACTS PER TRADING DAY OR 1.3720 MILLION OZ/DAY)

Result: A GOOD SIZED INCREASE IN OI WITH THE RISE IN PRICE IN GOLD TRADING YESTERDAY ($6.40). WE HAD A HUMONGOUS NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 17,961. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 17,961 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 27,494 contracts:

17,961 CONTRACTS MOVE TO LONDON AND 9533 CONTRACTS INCREASED THE COMEX. (in tonnes, the gain yesterday equates to 85.51 which is unbelievable)

we had: 288 notice(s) filed upon for 28,800 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, A HUGE CHANGES in gold inventory at the GLD/ a deposit of 1.48 tonnes of gold into the GLD>

Inventory rests tonight: 844.29 tonnes.

SLV

A small withdrawal of 377,000 oz and that usually means to pay for fees.

INVENTORY RESTS AT 326.337 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A GOOD SIZED 3313 contracts from 202,497 UP TO 206,110 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE RISE IN PRICE OF SILVER OF 20 CENTS YESTERDAY . HOWEVER,OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1492 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. ON TOP OF THIS, IF WE TAKE THE OI GAIN AT THE COMEX 3,313 CONTRACTS TO THE 1492 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A NET GAIN OF 4805 OPEN INTEREST CONTRACTS, AND YET WE STILL HAVE A HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW). THE NET GAIN TODAY IN OZ: 24.02 MILLION OZ!!!

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 20 CENT RISE IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1492 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER INTENSIFIES DESPITE THE CONSTANT RAIDS. WHAT REALLY STANDS OUT IS THE FACT THAT ON A PERCENTAGE BASIS MORE GOLD EFP’S ARE ISSUED FOR GOLD THAN IN SILVER. SOMEBODY IS TAKING ON THE COMEX TO REMOVE WHATEVER SILVER THEY HAVE.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 10.59 points or 0.32% /Hang Sang CLOSED DOWN 55.72 pts or 0.19% / The Nikkei closed DOWN 63.62 POINTS OR 0.28%/Australia’s all ordinaires CLOSED DOWN 0.11%/Chinese yuan (ONSHORE) closed UP at 6.6080/Oil DOWN to 56.34 dollars per barrel for WTI and 62.05 for Brent. Stocks in Europe OPENED ALL RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6080. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6125 //ONSHORE YUAN SLIGHTLY STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT VERY HAPPY TODAY.(WEAK MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

i)This will be the ultimate dagger into the heart of USA hegemony: the final drill in preparation for the Petro-Yuan for gold futures trading as begun:

( zero hedge)

4. EUROPEAN AFFAIRS

i)The pound got hit after the Bank of England held its interest rate constant. They state that 4th quarter economy is softer and that they see limited rate hikes in the future, in total contrast to the USA Fed

( zerohedge)

ii)the Bank of England sounds the alarm bell as it warns the Government to refrain form borrowing money

iv)As we have been stating to you for the past several years, Germany owes Greece at least 185 billion euros for World War ii reparations which have never been paid except for a tiny 115 million marks in 1953. A good start would be forgiveness of Greece’s Target 2 imbalances

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

i)In my industry, Teva soars over 17% but the reason is very fuzzy:

1.they are suspending their dividend

2 they are laying off workers

3.warns of downward pressure on the top line

( zerohedge)

ii)A must read..eloquently stated: Warning signs that “Everything Bubble” will burst

7. OIL ISSUES

The explosion at a European pipeline bringing natural gas to customers is causing huge problems. Now England is forced to import Russian gas as supplies are limited

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)A terrific commentary from Chris Powell outlining the massive manipulation we have experienced in gold and silver these past 18 years. He says it beautifully:( Chris Powell/GATA)

10. USA stories which will influence the price of gold/silver

i)Despite lower earnings our consumer is doing just great as retail sales surge the fastest since 2012:

( zero hedge)

ii)Markit’s USA service PMI slumps despite higher Manufacturing PMI. These are both soft data entries and as such do not pay attention to them:

( zerohedge)

iii)Ed Yardeni is calculated that the effective USA tax rate is already at 13% so the tax cut to 20% will not help our corporates at all. Even though on the balance sheet money is parked overseas, in reality it is lent back to USA operations. Thus no real gain.

( zerohedge)

iv)SWAMP NEWS:

You must see the latest Trey Gowdy diatribe on the farcical Mueller probe:

( zerohedge)

iv b)Another dandy as Chuck Grassley fires off a scorching letter to the Dept. of Justice after Anti-Trump texts reveal a burner phone..that is correct ,our two FBI clowns, Strzok and Page had burner phones in case their texts would be discovered…and this is not prima facia evidence???????. Also our hero Strozok states that “we must have an insurance policy” against Trump.

we are not making this up

( zerohedge)

iv c)Judicial watch President Fitton is correct: The real question is: Do we need to shut down the FBI?”

( zerohedge)

v)Let us close with this dandy history lesson on what happened in 2008 and how it will repeat shortly

(courtesy David Stockman/ContraCorner)

Let us head over to the comex:

The total gold comex open interest ROSE BY A GOOD SIZED 9,533 CONTRACTS UP to an OI level of 456,151 WITH THE RISE IN THE PRICE OF GOLD ($6.40 GAIN WITH RESPECT TO YESTERDAY’S TRADING). WE DID NOT HAVE ANY GOLD LIQUIDATION ANYWHERE. WE HAD A HUMONGOUS COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 17,961 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 17,961 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 27,494 OI CONTRACTS IN THAT 17,961 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 9,533 COMEX CONTRACTS. NET GAIN: 27,494 contracts OR 2,749,400 OZ OR 85.51 TONNES

Result: AN FAIR SIZED INCREASE IN COMEX OPEN INTEREST WITH THE RISE IN THE PRICE OF GOLD YESTERDAY ($6.40.) WE HAD NO REAL GOLD LIQUIDATION ANYWHERE. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 27,494 OI CONTRACTS…

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest fell by 254 contracts down to 2173. We had 416 notices filed upon yesterday so we gained a whopping 162 COMEX contracts or an additional 16,200 oz will stand for delivery AT THE COMEX in this active delivery month of December. YESTERDAY I REPORTED: “THIS IS THE FIRST TIME THAT WE HAVE EVER SEEN A HUGE AMOUNT IN OZ OF QUEUE JUMPING IN GOLD.” IT CONTINUED ON IN EARNEST TODAY AS BANKERS ARE DESPERATE TO GET THEIR HANDS ON PHYSICAL GOLD.

January saw its open interest LOSS OF 161 contracts DOWN to 1820. FEBRUARY saw a GAIN of 1169 contacts down to 338,877.

We had 288 notice(s) filed upon today for 28800 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 263,776

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 342,936

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE 3,313 CONTRACTS FROM 202,979 UP TO 206,151 WITH YESTERDAY’S 20 CENT GAIN IN PRICE . HOWEVER WE DID HAVE ANOTHER 1492 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 1492. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD NO LONG SILVER LIQUIDATION AS DEMAND FOR PHYSICAL SILVER INTENSIFIES ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE GAINED 4805 OPEN INTEREST CONTRACTS:

3589 CONTRACTS GAIN AT THE COMEX WITH THE ADDITION OF 1492 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN: 4805 CONTRACTS

We are now in the big active delivery month of December and here the OI ROSE by 63 contracts UP to 851. We had 44 notice filed upon yesterday so we GAINED 107 contract or an additional 505,000 oz will stand in this active delivery month of December.

The January contract month FELL by 8 contracts DOWN to 1344. February saw a LOSS OF 3 OI contract FALLING TO 32. The March contract GAINED 3126 contracts UP to 166,701.

We had 270 notice(s) filed for 1,350,000 oz for the DECEMBER 2017 contract

INITIAL standings for DECEMBER

Dec 14/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

10,293.05 oz

brinks

Delaware

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

128,131.716 oz

|

| No of oz served (contracts) today |

416 notice(s)

41600 OZ

|

| No of oz to be served (notices) |

2011 contracts

(201,100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6722 notices

672,200 oz

20.908 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer deposit(s):

i) Into HSBC: 128,131.716 oz

total customer deposits 128,131.716 oz

We had 2 customer withdrawal(s)

i) Out of brinks: 7399.55 oz

ii) Out of Delaware: 2893.500

Total customer withdrawals: 10,293.05 oz

we had 0 adjustment(s)

*December is the biggest delivery month of the year for gold and the fact that no gold has entered the vaults these past three trading days speaks volumes that there is no appreciable gold at the comex to deliver upon our longs and thus the reason for the migration to London

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 288 contract(s) of which 183 notices were stopped (received) by j.P. Morgan dealer and 54 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (7010) x 100 oz or 701,000 oz, to which we add the difference between the open interest for the front month of DEC. (2173 contracts) minus the number of notices served upon today (288 x 100 oz per contract) equals 886,500 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (7010) x 100 oz or ounces + {(2173)OI for the front month minus the number of notices served upon today (288) x 100 oz which equals 886,500 oz standing in this active delivery month of DECEMBER (27.57 tonnes). THERE IS 28 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 162 COMEX CONTRACTS STANDING OR 16,200 OZ WILL STAND AT THE COMEX AND QUEUE JUMPING INTENSIFIES IN GOLD.

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER 2016, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 879,623.576 or 27.35 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,083.905.974 or 282.54 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 71 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,209,115.53 oz

CNT

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

270

CONTRACT(S)

(1,350,000 OZ)

|

| No of oz to be served (notices) |

581 contract

(2,905,000 oz)

|

| Total monthly oz silver served (contracts) | 5798 contracts

(28,990,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

we had 1 customer withdrawal(s):

i) Out of CNT: 1,209,115.53 oz

TOTAL CUSTOMER WITHDRAWAL 1,209,115.53 oz

We had 0 Customer deposit(s):

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: nil oz

we had 0 adjustment(s)

The total number of notices filed today for the DECEMBER. contract month is represented by 270 contract(s) FOR 1,350,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 5798 x 5,000 oz = 28,990,0000 oz to which we add the difference between the open interest for the front month of DEC. (851) and the number of notices served upon today (270 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 5798 (notices served so far)x 5000 oz + OI for front month of DECEMBER(851) -number of notices served upon today (270)x 5000 oz equals 31,895,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE GAINED AN ADDITIONAL 107 CONTRACTS OR 535,000 OZ THAT WILL STAND AT THE COMEX AS QUEUE JUMPING ACCELERATES WITH RESPECT TO SILVER. BOTH GOLD AND SILVER ARE NOW EXPERIENCING QUEUE JUMPING.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 74,895

CONFIRMED VOLUME FOR FRIDAY: 89,468 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 89,468 CONTRACTS EQUATES TO 447 MILLION OZ OR 63.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 56.846 million

Total number of dealer and customer silver: 239.752 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.3 percent to NAV usa funds and Negative 2.6% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.2%

Percentage of fund in silver:36.5%

cash .+.3%( Dec 14/2017)

sprott is updating his website on NAV/will provide it as soon as they execute

2. Sprott silver fund (PSLV): NAV FALLS TO -0.68% (Dec 13 /2017)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.55% to NAV (Dec13/2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.68%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.24%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 21/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

NOV 20/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

Nov 17/no change in gold inventory at the GLD/inventory rests at 843.39 tonnes

Nov 16./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.39 TONNES

Nov 15./no change in gold inventory at the GLD/inventory rests at 843.09 tonnes

NOV 14/a small deposit of .300 tonnes into the GLD inventory/Inventory rests at 843.39 tonnes

Nov 13/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 843.09 TONNES

Nov 10/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 9/no changes in inventory at the GLD/Inventory rests at 843.09 tonnes

NOV 8/ANOTHER HUGE WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD DESPITE GOLD’S RISE TODAY. INVENTORY RESTS AT 843.09

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 14/2017/ Inventory rests tonight at 844.29 tonnes

*IN LAST 292 TRADING DAYS: 96/66 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 227 TRADING DAYS: A NET 60.62 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 29.51 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Nov 21/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

NOV 20/no change in silver inventory at the SLV/inventory rests at 318.074 million oz

Nov 17/no change in silver inventory at the SLV/inventory rests at 318.074 million oz/

Nov 16./NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ/

Nov 15./no change in silver inventory at the SLV/inventory rests at 318.074 tones

NOV 14/no change in silver inventory at the SLV/Inventory rests at 318.074 tonnes

Nov 13/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 10/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz/

Nov 9/no change in silver inventory at the SLV/inventory rests at 318.074 million oz.

NOV 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.074 MILLION OZ

Nov 7/a huge withdrawal of 944,000 oz from the SLV/inventory rests at 318.074 million oz/

Dec 14/2017:

Inventory 326.337 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.56%

12 Month MM GOFO

+ 1.85%

30 day trend

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

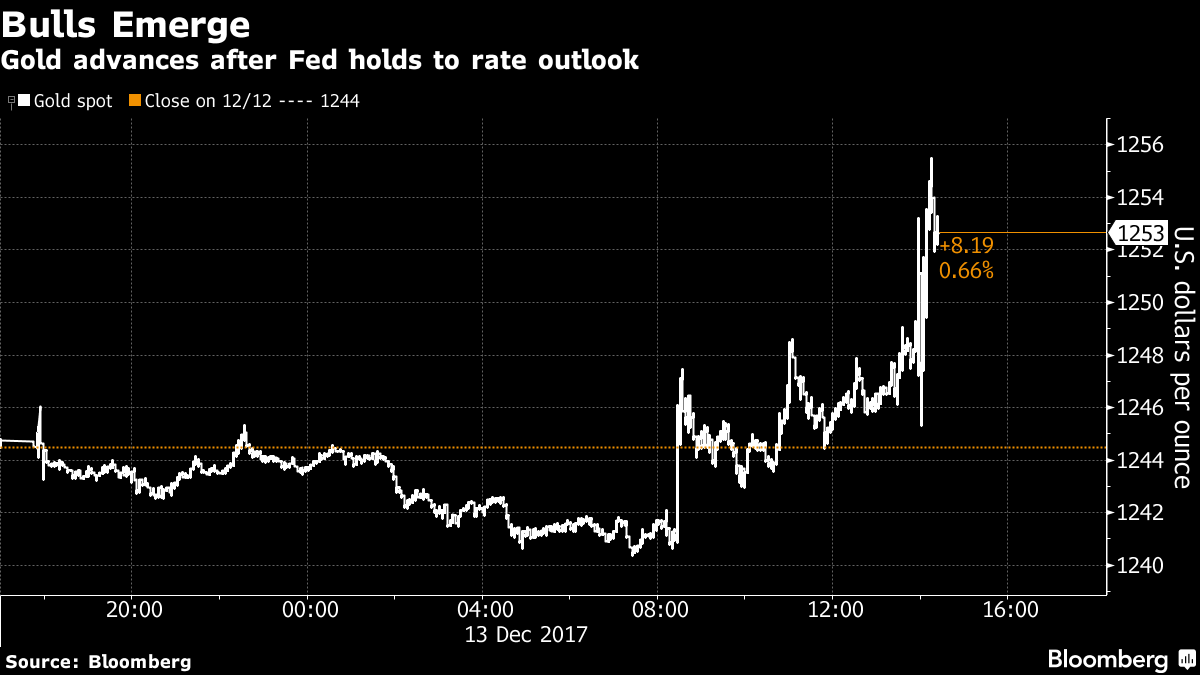

Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

Year-end rate hike once again proves to be launchpad for gold price

– FOMC follows through on much anticipated rate-hike of 0.25%

– Spot gold responds by heading for biggest gain in three weeks, rising by over 1%

– Final meeting for Federal Reserve Chair Janet Yellen

– Yellen does not expect Trump’s tax-cut package to result in significant, strong growth for US economy

– No concern for bitcoin which ‘plays a very small role in the payment system’

There were few surprises yesterday when the Federal Reserve decided to hike rates for the third time this year, by 0.25% to 1.5%. Gold responded with a climb of over 1%.

The statement accompanying the announcement was cautiously optimistic. Two FOMC members dissented whilst Yellen gave comments on Trump’s much lauded tax package and bitcoin.

This was Yellen’s last FOMC announcement as Federal Reserve Chair. As has become her style she was communicative of the Fed’s upcoming plans in terms of normalising monetary policy and the three rate hikes intended for 2018.

Overall Yellen and co are feeling good about how the current Chair is leaving things:

“…the committee expects the labor market to remain strong, with sustained job creation, ample opportunities for workers and rising wages,”

However concern and perhaps surprise was expressed when inflation data came in lower than expected. The reading of 1.7% in the year to November did not hold back the FOMC from increasing their growth projection from 2.1% to 2.5% for 2018.

Gold, defying expectations?

Gold is generally expected to stumble when a rate-hike is announced, or at least do nothing at all given how far in advance these things are telegraphed to the market these days. Once again however gold went against conventional opinion and popped up.

In the aftermath of the announcement gold was the biggest gainer whilst dollar stopped its longest winning streak since 2016. Meanwhile bitcoin tumbled as gold surged on ahead.

Gold’s performance shouldn’t really come as much surprise. In the last two years a Federal Reserve rate hike has proven to be something of a launchpad for the price of gold. We have frequently seen double-digit percentage increases in gold prices following an increase in interest rates.

This may well be down not to the decision to hike up rates but the language that surrounded it. Often rate hikes come with a hawkish tone, warning of risks to the economy. Instead this latest one was optimistic with some caution. The FOMC, despite boosting economic growth forecasts, has expressed confusion over the stubbornly low inflation rates and therefore, given itself plenty of room for manoeuvring around rate hikes.

Gold investors be warned, a rate hike is not likely to be bad news for the yellow metal for some time to come.

Naive to ignore bitcoin bubble?

Bitcoin’s rise this year (currently at around $17,000) has grabbed the attention of many. It has almost been promoted to ‘acceptable’ status thanks to the launch of bitcoin futures and Wall Street’s apparent enthusiasm for it.

One area where it is hoped that it will quietly go away is at the Federal Reserve. When Powell was questioned about the impact of bitcoin, at his confirmation hearing, he responded that it just wasn’t big enough right now.

Yellen was asked about it once again yesterday. She called the cryptocurrency (which has a market cap of $300 billion) a “highly speculative asset” and “not a stable store of value.”

What both Yellen and Powell seem to be missing is that bitcoin, like gold, is proving to be a measure for how people feel about the state of fiat currencies and the economy. For sure it is mainly a speculative asset at present, but it still making a significant contribution to the commentary regarding the sentiment in the economy.

One of the biggest debates about bitcoin at the moment is whether or not it is the finest example of a bubble. This might be the reason Yellen doesn’t want to draw too much attention to it, after all it is not the only asset experiencing bubblenomics.

Currently global asset prices are rising rapidly above their underlying value. Looking at today and ten years ago bubbles are more pervasive now than we saw then. But they have one thing in common – the economists and decision makers are keeping shtum. Even former Fed Chair Alan Greenspan has felt the need to point and shout ‘they’re behind you’. He recently warned that years of unconventional monetary policy by major central banks a global government bond bubble has formed.

It’s not just in the sovereign bond market, one just needs to glance at the stock market or housing markets in various leading economies to see that we are one pin prick away from a big ‘pop’.

What will be the pin prick? The winding down of money printing and upping of interest rates could well be it, all whilst fault lines are appearing in major economies of the world.

This is something Yellen’s successor will have to manage on a fine tightrope, but needless to say he cannot ignore bitcoin or other bubbles for much longer.

Yellen, over and out

Yesterday was most likely Janet Yellen’s final press conference. She was sent off with a standing ovation, so impressed are Wall Street by her record at navigating America out of the financial crisis.

Yellen’s situation is a rare one. She is the first Fed chair not to be reappointed after serving a first full term. President Trump has instead chosen Jeremy Powell. Powell is thought by many to be similar to Janet Yellen and is even known in some circles as Janet-lite.

How Wall Street reacts to Powell (or any Yellen-predecessor) will be interesting to see. Whilst he is known to be light on banking regulation (yay, for the swamp) he is also expected to be more tight-lipped about his plans for the Fed. Yellen has made it a hallmark of her tenure to communicate with the markets.

Yellen’s departure will also be met with some apprehension given no other recent Fed chair has seen the market climb as far as fast as it did under the first female Chair of the central bank.

Of course Powell won’t be able to just pick up Yellen’s baton and run with it. There’s a fairly large elephant in the room which cannot be ignored for much longer – inflation. The FOMC tracks various signals for inflation and currently they just aren’t picking up on any strong ones.

Unemployment is at barely 4 percent this plus strong job-growth numbers should arguably be pushing up wages and prices. Yet there is very little inflation…yet. Yesterday’s FOMC statement acknowledged this.

It will be interesting to see how Powell approaches this issue. He may be forced to face it sooner rather than later when Trump’s new tax package might bring an unexpected stimulus to the economy. Whilst the Fed doesn’t expect much benefit from the tax package past 2018, it may well be the catalyst inflation needs in order to start showing its face on FOMC statistics.

Nothing to see here: keep buying gold and carry on

Ultimately what is this post all about? Nothing has changed. As expected, the FOMC has increased interest rates. As expected, gold was pleased and posted gains well above other asset classes. As expected, Yellen’s successor agree with the decision. As expected, little concern was shown for the looking bubble rapidly darkening all four corners of the earth.

So if little has changed, what can be done? Quite simply do not change your approach to keeping a diversified portfolio that is well protected from fumbling central bankers and questionable economic statistics. By all accounts we appear to be heading for the main course of the global financial crisis with 2008 a mere starter by comparison.

Physical gold that is allocated and segregated in your name is the most obvious and historically proven way to insure your personal wealth. The best way to protect yourself from fiat currency debasement and damaging interest rates is to invest in gold. This is exactly the approach taken by a number of central banks. They know that gold cannot be devalued by the US Federal Reserve and will only benefit from Trump’s dangerous, Wall St approach to economic and monetary management.

Recommended reading

Is New Fed Chief A “Swamp Critter Extraordinaire”?

Gold Price Reacts as Central Banks Start Major Change

Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

News and Commentary

Gold edges up as dollar holds steady (Reuters.com)

Fed Spells Relief for Gold Traders Worried Over Rate-Hike Pace (Bloomberg.com)

Bitcoin is still a good bet as long as greater fools are buying (MarketWatch.com)

Fed Raises Rates While Sticking to Three-Hike Outlook for 2018 (MarketWatch.com)

Source: Bloomberg

Yellen Isn’t Buying Trump’s Tax Cut Talk of an Economic Miracle (Bloomberg.com)

Fed Raises Rates, Eyes Three 2018 Hikes as Yellen Era Nears End (Bloomberg.com)

Gold Will Soar… As China Kneecaps the Dollar (InternationalMan.com)

Global Negative Yielding Debt Surges To $9.7 Trillion Despite ECB’s QE Taper (ZeroHedge.com)

Gold Prices (LBMA AM)

14 Dec: USD 1,255.60, GBP 935.67 & EUR 1,062.49 per ounce

13 Dec: USD 1,241.60, GBP 929.96 & EUR 1,056.97 per ounce

12 Dec: USD 1,243.40, GBP 933.92 & EUR 1,056.27 per ounce

11 Dec: USD 1,251.40, GBP 935.80 & EUR 1,061.19 per ounce

08 Dec: USD 1,245.85, GBP 924.42 & EUR 1,061.09 per ounce

07 Dec: USD 1,256.80, GBP 937.57 & EUR 1,066.77 per ounce

06 Dec: USD 1,268.55, GBP 948.37 & EUR 1,072.31 per ounce

Silver Prices (LBMA)

14 Dec: USD 16.01, GBP 11.92 & EUR 13.54 per ounce

13 Dec: USD 15.71, GBP 11.76 & EUR 13.38 per ounce

12 Dec: USD 15.78, GBP 11.82 & EUR 13.40 per ounce

11 Dec: USD 15.84, GBP 11.84 & EUR 13.43 per ounce

08 Dec: USD 15.83, GBP 11.76 & EUR 13.48 per ounce

07 Dec: USD 15.91, GBP 11.94 & EUR 13.49 per ounce

06 Dec: USD 16.12, GBP 12.06 & EUR 13.64 per ounce

Recent Market Updates

– UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

– An Interview with GoldCore Founder, Mark O’Byrne

– Risk Of Online Accounts Seen As One of Largest Brokerages In World Halts Online Trading After “Glitch”

– Low Cost Gold In The Age Of QE, AI, Trump and War

– Own Gold Bullion To “Support National Security” – Russian Central Bank

– Bitcoin $10,000 – Huge Volatility of Cryptocurrencies and Risky Fiat Making Gold Attractive

– Financial Advice from Dr Wayne Dyer

– Buy Gold As Fed Shows Uncertainty And Concern Over Financial ‘Imbalances’

– Brexit Budget – Grim Outlook As UK Economy Downgraded

Eric Sprott interviewed by Bullion Star at Australia’s Precious Metals Investment Symposium

Submitted by cpowell on Wed, 2017-12-13 15:59. Section: Daily Dispatches

11a ET Wednesday, December 13, 2017

Dear Friend of GATA and Gold:

Sprott Asset Management’s chairman, Eric Sprott, interviewed by Bullion Star’s Luke Chua at the Precious Metals Investment Symposium in Melbourne, Australia, last month, wonders whether shortages in the minor precious metals eventually will indicate shortages in gold and silver and lead to the liberation of the prices of the latter.

Sprott scoffs at central banks for having tried to solve the world’s debt problems with more debt. He says the trading data reported by the London Bullion Market Association and the New York Commodities Exchange are so huge compared to actual world mine production as to be hard to believe.

Sprott says that he has been avoiding cryptocurrencies, and he believes that the metal held by the exchange-traded gold fund GLD has been used for knocking the metal’s price down.

The interview is 17 minutes long and it’s posted at YouTube here:

https://www.youtube.com/watch?v=f3ryaWuU4Ao&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A terrific commentary from Chris Powell outlining the massive manipulation we have experienced in gold and silver these past 18 years. He says it beautifully:

(courtesy Chris Powell/GATA)

Hope for the day of deliverance but avoid predicting it

Submitted by cpowell on Wed, 2017-12-13 16:38. Section: Daily Dispatches

11:46a ET Wednesday, December 13, 2017

Dear Friend of GATA and Gold:

Some of you are inquiring about GATA consultant Harvey Organ’s excellent work calling attention to the huge increase in the use of the New York Commodities Exchange’s “exchange for physicals” procedure for fulfilling long contracts for gold and silver:

http://www.gata.org/node/17873

It seems that most gold and silver bought through futures contracts on the Comex in New York and claimed for delivery now is being delivered in London through what long had been described as an “emergency” mechanism. Since the metals are reported to be in backwardation in London — prices for immediate delivery being higher than prices for future delivery — all this suggests an extreme shortage.

Even so, your secretary/treasurer suspects that the monetary metals issue still comes down to how much metal central banks are willing to disgorge for price control.

From the EFP data at the Comex and the explosion of gold swaps arranged by the Bank for International Settlements this year, as reported by GATA consultant Robert Lambourne —

http://www.gata.org/node/17790

— which the BIS refuses to discuss —

http://www.gata.org/node/17793

— it does seem as if metal offtake has sharply increased lately, and as it long has been, London remains the center of the price-suppression mechanism because that’s where governments keep so much of their metal. As many governments were part of the price-suppression scheme during the London Gold Pool of the 1960s, most of those and many more are probably part of it now, as all major central banks are BIS members.

But we don’t know how much metal is really being delivered in London, nor how much cash is being paid in London to the former Comex longs for their agreeing to delay delivery or not to claim delivery at all. This could be a very nice racket for insiders, providing a regular income for traders not going public about what’s happening.

In any case as GATA been pursuing gold market rigging for 18 years now, so we’re learning not to predict the day of deliverance even as no one disputes the documentation we have compiled about the rigging:

http://www.gata.org/taxonomy/term/21

Since the rigging can’t be disputed, the big challenge is simply to get the mining industry, investors, and good citizens everywhere to care rather than be bought off.

As much as we hope for the day of deliverance, predictions about it don’t help. In regard to predictions your secretary/treasurer, being of a certain age, is often reminded of the “End of the World” skit from Dudley Moore’s “Beyond the Fringe” stage show back in 1962. It’s about a doomsday cult that goes up to the top of a mountain to count down to the moment of the prophesied apocalypse. Audio of the original Broadway version is at YouTube here:

https://www.youtube.com/watch?v=tjEtB3rJB9o

A video of a 1979 performance, which may be more fun, is at YouTube here:

https://www.youtube.com/watch?v=-hJQ18S6aag

After 18 years all GATA can do is endorse the advice the cult leader gives at the end.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.6180 /shanghai bourse CLOSED DOWN AT 10.59 POINTS 0.32% / HANG SANG CLOSED DOWN 55.72 POINTS OR 0.19%

2. Nikkei closed DOWN 63.62 POINTS OR 0.24% /USA: YEN FALLS TO 112.71

3. Europe stocks OPENED ALL RED /USA dollar index RISES TO 93.44/Euro FALLS TO 1.1825

3b Japan 10 year bond yield: RISES TO . +.050/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.34 and Brent: 62.05

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.324%/Italian 10 yr bond yield UP to 1.794% /SPAIN 10 YR BOND YIELD DOWN TO 1.475%

3j Greek 10 year bond yield FALLS TO : 4.165?????????????????

3k Gold at $1257.85 silver at:16.06: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 6/100 in roubles/dollar) 58.65

3m oil into the 56 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.71 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9867 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1683 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.324%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.369% early this morning. Thirty year rate at 2.744% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

It’s Central Bank Bonanza Day: European Stocks Slide Ahead Of ECB; S&P Futs Hit Record High

One day after the Fed hiked rates by 25 bps as part of Janet Yellen’s final news conference, it is central bank bonanza day, with rate decisions coming from the rest of the world’s most important central banks, including the ECB, BOE, SNB, Norges Bank, HKMA, Turkey and others.

And while US equity futures are once again in record territory, stocks in Europe dropped amid a weaker dollar as investors awaited the outcome of the last ECB meeting of the year: the Stoxx 600 falls 0.4% as market shows signs of caution before the Bank of England and the European Central Bank are due to make monetary policy decisions as technology, industrial goods and chemicals among biggest sector decliners, while miners outperform, heading for a 5th consecutive day of gains. “The Federal Reserve raised interest rates last night, but they weren’t overly hawkish in their outlook. This has led to traders being subdued this morning,” CMC Markets analyst David Madden writes in note.

The stronger euro pressured exporters on Thursday although overnight the dollar halted a decline sparked by the Fed’s unchanged outlook for rate increases in 2018, suggesting “Yellen Isn’t Buying Trump’s Tax Cut Talk of an Economic Miracle.”

That said, it has been a very busy European session due to large amount of economic data and central bank meetings, with the NOK spiking higher after the Norges Bank lifted its rate path, while the EURCHF jumped to session highs after SNB comments on CHF depreciation over last few months. The AUD holds strong overnight performance after a monster jobs report which will almost certainly be confirmed to be a statistical error in the coming weeks, while the Turkish Lira plummets as the central bank delivers less tightening than expected. Meanwhile, the USD attempts a slow grind away from post-FOMC lows.

In tates, bunds sell off from the open, with the 2s5s10s butterfly again highlights pressure in 5y sector, strong European PMI prints and possible bearish ECB set-up drive the move. USTs lower in tandem, steepening noted in Eurodollar curve. Divergence seen in equity markets as U.S. equity futures are supported from overnight levels whereas European indices sell-off across the board, move higher in EUR/USD after fed decision weighs on some exporters.

Some of the most notable developments via BBG:

- China: PBOC raises rates on reverse repo and MLF operations by 5bps; Reuters later reports SLF rate is also raised by 5bps

- Norges Bank: holds rates at 0.5% as expected; rate path changed to imply first hike in autumn 2018 from summer 2019

- U.K Nov. Retail Sales m/m: 1.1% vs 0.4% est; ONS says seasonal adjustments capture only an element of the Black Friday effect, with retailers now offering discounts over a two-week period rather than a single day

- SNB holds rates at -0.75% as expected with 3M Target LIBOR Rate at -0.75% vs. Exp. -0.75%. SNB says swiss franc overvaluation has thus continued to decrease, yet the franc remains highly valued.

- HKMA increased its base rate by 25bps to 1.75% in response to the Fed hike. (Newswires)

- Turkey holds benchmark rates at 8.00% as expected; late liquidity rate hiked by 50bps vs 100bps est.

Adding to the optimistic mood were PMIs across the major European economies, with German and French composite PMI indexes smashing estimates. The December flash aggregate euro-zone PMI rose to an almost seven-year high of 58 vs 57.2 median forecast and 57.5 in Nov.

In the ongoing Brexit daram, on Wednesday the UK government was defeated in parliament in a 309-305 vote, meaning MP’s will get a meaningful vote on the final Brexit deal. PM May now heads to Brussels to the European Summit, where she is expected to stall for time to find unity on the exact trade deal Britain wants from Brussels.

Looking at stocks, a slide in technology stocks led the decline in Europe’s Stoxx 600 Index, with most industry sectors in the red. U.S. equity-index futures inched higher. In Asia earlier, China’s domestic equity markets were lower and Hong Kong’s Hang Seng Index fell, while Japanese and South Korean equities were also down. Core European bond yields ticked higher and the euro pared a drop after manufacturing data from Germany and France underscored the resilience of the region’s economy. Sterling was steady before the Bank of England’s policy decision. Brent crude held above $60 a barrel.

As a reminder, the ECB and BOE’s rate meeting are also set for today. Firstly on the ECB, the likely focus will be for more clues about plans to start weaning investors off its monthly bond purchases next year as well as on the latest staff macroeconomic forecasts, with the first outlook for 2020 due to be revealed. DB expects the core inflation 2020 forecast to be 1.6%/1/7% – consistent with previous 3-year ahead staff views. It’s also worth keeping an eye on Draghi’s press conference and particularly if he addresses some of the internal divisions which have been hinted at on forward guidance.

“The ECB is the next big point of focus in the process of moving from quantitative easing to tapering,” Ole Hansen, head of commodity strategy at Saxo Bank A/S in Hellerup, Denmark said via email. “That could have an impact on currencies, bond yields and stocks.”

The BoE meeting could be a non event as recent inflation prints and macro data were broadly in line with consensus. Notably, any discussion on what the Brexit breakthrough on Friday might mean for policy could be the most interesting feature.

Meanwhile, as reported yesterday, the Fed stuck with a projection for three rate hikes in the coming year after raising its benchmark rate by a quarter percentage point. While the U.S. central bank lifted its estimate for growth in 2018 to 2.5 percent from 2.1 percent, it still didn’t see inflation accelerating.

Also reported overnight was that in response to the Fed’s rate hike, the People’s Bank of China unveiled a five basis-point boost to some reverse-repurchase rates, minutes before the country’s release of its main economic data for November. While most economists had anticipated the PBOC to hold off on any move in the wake of the Fed, as they did when the U.S. lifted borrowing costs in June, we disagreed, and we were right when the PBOC instead moved in tandem, as it did March. The yuan was slightly higher against the dollar in Thursday trading, though it advanced less than the won and other Asian currencies.

Bulletin Headline Summary from RanSquawk

- Central Bank Christmas party: Norges Bank brings forward rate hike exp., SNB unchanged with focus now on ECB and BoE

- UK Retail Sales boosted by Black Friday with readings above analyst estimates.

- Looking ahead, rate decisions from ECB and BoE.

Market Snapshot

- S&P 500 futures up 0.2% to 2,673.00

- STOXX Europe 600 down 0.2% to 389.92

- MSCI Asia up 0.1% to 171.01

- MSCi Asia Ex Japan up 0.2% to 556.56

- Nikkei down 0.3% to 22,694.45

- Topix down 0.2% to 1,808.14

- Hang Seng Index down 0.2% to 29,166.38

- Shanghai Composite down 0.3% to 3,292.44

- Sensex up 0.4% to 33,168.14

- Australia S&P/ASX 200 down 0.2% to 6,011.26

- Kospi down 0.5% to 2,469.48

- German 10Y yield rose 1.6 bps to 0.33%

- Euro up 0.01% to $1.1827

- Italian 10Y yield rose 8.9 bps to 1.532%

- Spanish 10Y yield rose 2.0 bps to 1.517%

- Brent futures up 0.2% to $62.58/bbl

- Gold spot down 0.03% to $1,255.14

- U.S. Dollar Index unchanged at 93.43

Top Overnight News

- China’s central bank unexpectedly raised borrowing costs following the Fed’s decision to tighten monetary policy

- Yellen Isn’t Buying Trump’s Tax Cut Talk of an Economic Miracle

- Shell Is Said to Sell Argentine Fuel Assets to Brazil’s Raizen

- China Tightens After Fed as Policy Makers Seek to Soothe Markets

- UBS Wealth Chief Zeltner Replaced by Blessing in Revamp

- Fox’s Workaround for Troubled Sky Takeover? Get Disney to Buy It

- YPF Is Said to Be Near to Selling Unit Stake to GE, Blackstone

- Atos Pushes On With $5.1 Billion Gemalto Bid After Rebuff

- Traders Brace for ‘Explosive’ Rand Moves After ANC Election

Asia equity markets were mostly subdued as the regional bourses and central banks reacted to a hike from the Fed in Yellen’s last meeting. ASX 200 (-0.2%) was indecisive and pared the early mining-led gains, while Nikkei 225 (-0.3%) was hampered by USD/JPY woes post-FOMC. Hang Seng (-0.5%) and Shanghai Comp. (-0.4%) traded subdued as participants mulled over Chinese Industrial Production and Retail Sales figures which either printed inline or below estimates. Furthermore, the HKMA and PBoC responded to the FOMC with the base rate in Hong Kong raised by 25bps in lockstep with the Fed, while the PBoC increased rates by 5bps on 1-year MLF loans and on its Reverse Repo operations. Finally, 10yr JGBs were rangebound despite the subdued risk tone in Japan, while the 20yr auction also failed to spur demand with most metrics inline with the previous month. After three days of injections, the PBoC drained a net 190BN yuan in liquidity via reverse repos, while it also announced to lend CNY 288bln through MLF 1yr loans. PBoC raised rates on reverse repos and its MLF by 5bps each following the Fed rate hike with 7-day reverse repo at yield of 2.50% (Prev. 2.45%), 28-day at 2.80% (Prev. 2.75%) and 1yr MLF loan at 3.25% (Prev. 3.20%). Source reports also stated that SLF loan will be raised 3.35% (Prev. 3.30%)

In other data, Chinese Industrial Output (Nov) Y/Y 6.1% vs. Exp. 6.2% (Prev. 6.2%); YTD 6.6% vs. Exp. 6.6% (Prev. 6.7%), Chinese Retail Sales (Nov) Y/Y 10.2% vs. Exp. 10.3% (Prev. 10.0%); Y/Y 10.3% vs. Exp. 10.3% (Prev. 10.3%). The Australian dollar soared after the Australian Employment Change printed at 61.6k for November vs. Exp. 19.0k (Prev. 3.7k, Rev. 7.8K), while the New Zealand Treasury lowered GDP forecasts for 2017/18 to 3.3% from 3.5% and cuts 2018/19 forecast to 3.4% from 3.5%.

Top Asian News

- China Factory Output, Investment Slow While Consumption Firms

- China Shares Drop as PBOC Raises Borrowing Costs After Fed Hike

- Teva Braces for Nationwide Strikes by Israeli Union on Job Cuts

- Japan Plans Carrot-and-Stick Tax Changes to Drive Wage Gains

- MUFG Brokerage Sued by Manager as Harassment Dispute Escalates

- Philippines Holds Rate With Economists Predicting Hike in 2018

- Russia Dreams Big as U.S. Fails to Kill $27 Billion Gas Project

European equities have seen little in the way of firm direction in what is set to be a busy day for markets ahead of tier 1 data and a slew of central bank activity; most notably the ECB rate decision and press conference for European traders. Focus for the event will centre around the ongoing debate at the Bank on whether to impose an end date on asset purchases with the release also due to be accompanied by the latest staff economic projections. In terms of sector specifics, utilities have posted some modest outperformance with E.ON (+2.4%) top of the DAX leaderboard amid a positive broker upgrade at Exane. Other individual movers include Peugeot (+1.5%) amid a broker upgrade at HSBC and encouraging Eurozone car registration figures.

Top European News

- Euro-Area Activity Surges as Manufacturing Posts Record Growth

- Housing Slump Gathers Pace in Sweden After Buyers Lose Faith

- Draghi’s 2020 Vision for Euro-Area Economy Is Key to QE Exit

- Norway Signals an Earlier Exit From Extreme Monetary Stimulus

- World Record in Negative Rates Transforms a Whole Generation

- May Heads Back to Brussels After Brexit Defeat by Her Own Party

In fixed income, the initial Fed/US Treasury inspired bid always looked tentative and the cautious buying has proved prudent in wake of some strong EU fundamentals ahead of the BoE and ECB policy announcements etc. Bunds and Gilts were already on the turn in truth, but have recoiled further to lows of 162.98 and 124.77 respectively following flash PMIs that lived up to their name in the main, and a significant UK retail sales beat vs consensus, albeit in large part due to Black Friday. So, the 10 year debt futures have been 29 and 15 ticks adrift vs +10 and +13 ticks at one stage and Gilts saw a 2k lot clip sale at 124.90 on the way down. Technically, Bunds will now be wary of Wednesday’s 162.91 Eurex base, and if that yields then bears will target 162.79-74. Meanwhile, USTs have declined in sympathy to unwind more of their post-FOMC gains and the curve continues to re-steepen as the 2 year yield derives more comfort (relief) from no hawkish change to the 2018 tightening profile.

In FX, it’s been a busy morning for markets with European participants arriving at their desks to a softer USD post-FOMC with Yellen failing to deliver any hawkish surprises while the rate path trajectory was kept broadly the same despite fiscal stimulus being incorporated into forecasts. First up in terms of major European central bank decisions was the SNB which prompted a little traction in the CHF after the Bank stood pat on rates and reiterated that the CHF remains ‘highly valued’. Thereafter, the Norges Bank dealt NOK a big helping hand after keeping rates unchanged this time round, but bringing forward expectations for a hike to autumn 2018 from summer 2019; subsequently knocking EUR/NOK firmly back below 9.80. GBP remains a key focus for markets with initial modest strength following PM May’s Parliamentary failure yesterday which will give Parliament a ‘meaningful’ vote on the terms of the UK’s departure from the EU. Thereafter, UK retail sales painted a more upbeat picture for the economy with all readings exceeding expectations and some upward revisions to the previous’. However, limited reaction seen in GBP amid seasonal factors and ongoing Brexit focus.

In commodities, gold prices have retreated from their post-FOMC gains during European trade, while Chinese primary aluminium production showed declines for the 5th consecutive month with domestic crude steel output slipping to a 9-month low amid curbing efforts. WTI crude futures were lacklustre and failed to make any meaningful recovery from the prior day’s losses which were partly triggered by the DOE report which showed increased US production and a large build in gasoline inventories. IEA Monthly Report:

- Our forecast for global demand growth remains unchanged at 1.5 mb/d in 2017 (or 1.6%) and 1.3 mb/d in 2018 (or 1.3%).

- Global oil supply rose 0.2 mb/d in November to 97.8 mb/d, the highest in a year, on the back of rising US production.

- OPEC crude supply fell in November for the fourth consecutive month to 32.36 mb/d, down 1.3 mb/d on a year ago.

- OECD commercial stocks fell 40.3 mb in October to 2 940 mb, their lowest level since July 2015.

- Benchmark crude prices rose by $4-5/bbl on average in November and traded at their highest level in more than two years in early December.

- Global refinery throughput in 3Q17 reached a record high at 81.2 mb/d, even including the impact of Hurricane Harvey, but has fallen back in 4Q17 due to maintenance.

Looking at the day ahead, there is the European Council meeting in Brussels which continues into Friday with Brexit high on the agenda with Mrs May arriving after her voting loss last night. We’ve also got two central bank meetings due with both the BoE and ECB set to hold their last monetary policy meetings of the year. Datawise we’ll get the flash December PMIs in both Europe and the US, as well as the November retail sales data for the UK and US (0.6% mom expected for ex-auto). Other notable data prints include the final November CPI revisions in France, November import price index reading and weekly initial jobless claims data in the US.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 236,000, prior 236,000; Continuing Claims, est. 1.9m, prior 1.91m

- 8:30am: Retail Sales Advance MoM, est. 0.3%, prior 0.2%; Retail Sales Ex Auto MoM, est. 0.6%, prior 0.1%; Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.3%

- 8:30am: Import Price Index MoM, est. 0.7%, prior 0.2%; Import Price Index YoY, est. 3.24%, prior 2.5%

- 8:30am: Export Price Index MoM, est. 0.3%, prior 0.0%; Export Price Index YoY, prior 2.7%

- 9:45am: Markit US Manufacturing PMI, est. 53.9, prior 53.9; Services PMI, est. 54.7, prior 54.5; Composite PMI, prior 54.5

- 9:45am: Bloomberg Consumer Comfort, prior 52.3

- 10am: Business Inventories, est. -0.1%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

A busy evening last night with the Fed rate hike and the UK Government losing a vote (305-309) in the Commons that makes it more likely that the final Brexit deal will have to get approved by Parliament and thus decreases the possibility of a hard Brexit but complicates the negotiation process. Before all this, the highlight of the day was yet another slightly weaker than expected CPI print. The 7th miss in 9 months. 10 year Treasuries traded as high as 2.425% before the number, then dropped to 2.367%, before ending the day at 2.342% after the dovish FOMC. To be honest this suits our short-term belief in carry and tighter spreads (through Q1) but we do expect inflation to start to misbehave more from Q2 onwards. However every inflation miss in the interim makes us more nervous as to whether we get the expected turn around. We still think we do by the time we get to the Spring but it’s fair to say that for us to be correct inflation now has to be sitting in the departure lounge waiting to board a flight taking off pretty soon.

Turning to the FOMC, the Fed raised rates by 25bp as expected, on a 7-2 vote with both the Fed’s Kashkari and Evans dissenting. The market seems to have taken a slightly dovish take on the FOMC with 10y treasury yields lower (see above) and the US dollar index down 0.71% for the day. In the details, the Fed now projects the labour market to remain strong with a lower unemployment rate of 3.9% and stronger GDP growth across the forecast horizon, particularly next year where growth is expected to be 2.5% (vs. 2.1% previous), in part due to the expected tax plans. Despite these positive revisions, the Fed’s forecast for core inflation and the dot plots are unchanged, with median expectations of three more hikes in 2018 and CPI of 1.9% in 2018 and 2.0% in 2019 & 2020.

Moving onto Ms Yellen’s last press conference as the Fed Chair where she was fairly positive on a range of topics. On the economy, she said “I feel good about the economic outlook…risks are balanced and there’s less to lose sleep about now…” On US equities, she noted “the fact that those valuations are high doesn’t mean that they are necessarily overvalued” and on broader financial stability risks, no indicators she monitors “are flashing red or possibly even orange”. On the flatter yield curve, she noted “the yield curve is likely to be flatter than it’s been in the past” and that “it could more easily invert if the Fed were to even move to a slightly restrictive policy stance”. This is important as it indicates that the Fed aren’t as concerned as we would be about an inverted yield curve and could carry on hiking even if longer end yields stay low. Finally on tax, she noted FOMC members “generally identified changes in tax policy as a factor supporting modestly stronger (economic) outlook, although many noted much uncertainty remains about the macro-economic effects of the specific measures”. Further, she added that the economic uplift from tax cuts “it’s not a gigantic increase in growth” and could be mostly short term.

Talking of tax reform, the plans are tracking well and could still become law by Christmas. President Trump noted the Senate and House negotiators have reached a tentative agreement and he hopes to sign the tax bill “in a very short period of time”. Some of the compromises noted by Bloomberg include: i) corporate tax rate of 21%, but begins from 2018, ii) mortgage deduction limit of $750k, iii) top individual tax rate of 37%, iv) 20% deduction on pass through business income, and v) repeal the alternative minimum tax. Earlier yesterday, the Senate Democratic leader Schumer called on Republicans to delay their tax bill vote until Doug Jones (winner of the Alabama election) can vote on the legislation. However, the earliest that Mr Jones can be seated is sometime between 26 December to 3 January, but the Republicans expect a full House and Senate vote on the final bill around next Tuesday (19 December), with the President expected to sign the “Tax Cut and Jobs Act” into law shortly after. Notably, Republican Senator McCain is currently away as he undergoes medical treatment, so things can still change given his crucial vote.

In China, the November macro data just released was broadly in line but slightly lower than the prior month. Both the IP and fixed assets investments matched expectations at 6.1% yoy and 7.2% respectively, but were 0.1ppt lower than the prior month. Retail sales were softer than expectations at 10.2% yoy (vs. 10.3%). Elsewhere, China’s central bank has slightly increased the borrowing costs it charges in open market operations following the Fed’s move, lifting the cost of the 7 and 28 day reverse repo agreement by 5bp. This morning in Asia, markets are trading broadly weaker. The Nikkei (-0.31%), Hang Seng (-0.45%), and China’s CSI 300 (-0.64%) are modestly down but the Kospi is up 0.51% as we type. Treasuries have partly reversed yesterday’s gains and are up 2bps this morning.

As a reminder, the ECB and BOE’s rate meeting are set for today. Firstly on the ECB, the likely focus will be on the latest staff macroeconomic forecasts, with the first outlook for 2020 due to be revealed. DB’s Mark Wall expects the core inflation 2020 forecast to be 1.6%/1/7% – consistent with previous 3-year ahead staff views. It’s also worth keeping an eye on Draghi’s press conference and particularly if he addresses some of the internal divisions which have been hinted at on forward guidance. The BoE meeting could be a non event as recent inflation prints and macro data were broadly in line with consensus. Notably, any discussion on what the Brexit breakthrough on Friday might mean for policy could be the most interesting feature.

Now recapping other market performance from yesterday. US equities were mixed but little changed after bouncing around following the mix of news from the softer CPI, the FOMC meeting and progress on the tax plans. The S&P ended 0.05% lower while the Nasdaq and Dow rose 0.20% and 0.33% respectively. Within the S&P, financials led the losses (-1.27%), partly impacted by the dovish FOMC, while modest gains came from consumer staples and industrials stocks. European markets were all lower, with key bourses down 0.1%-0.4% as losses in utilities offset gains from tech stocks. Across the region, the Stoxx 600 (-0.24%), DAX (-0.44%) and FTSE (-0.05%) all fell modestly while Italy’s FTSE MIB led the losses, ending the day 1.44% lower. The VIX rose for the secondconsecutive day to 10.18 (+2.6%).

Over in government bonds, treasuries firmed with UST 10y yields down 5.7bp while other core bond yields were little changed (Bunds flat; Gilts -0.7bp). Italy’s 10y BTP yields jumped 9bp after newspapers including Corriere della Sera and Messaggero reported that Italian elections could be held earlier at 4 March next year, with President Mattarella expected to dissolve the Parliament on 28 or 29 December to clear the way for elections. Notably, the potential for earlier elections is not new, but perhaps the increased support for the Five Star Movement party may have focused the mind. We note a recent Ipsos opinion poll showed the 5SM leading with 29.1% support versus 24.4% for the ruling Democratic party. Having said that it’s still very difficult for them to be a power broker given the new electoral law so it’s not altogether clear why Italy underperformed so much yesterday.

Turning to currencies, the US dollar index dropped 0.71% following the dovish FOMC, while the Euro and Sterling gained 0.72% and 0.73% respectively. In commodities, WTI oil fell 0.82% following a rise in gasoline stockpiles and OPEC raised its outlook for non-OPEC supply in 2018. Elsewhere, precious metals increased modestly (Gold +0.88%; Silver +2.16%) while other base metals also edged higher (Aluminium flat; Zinc +0.08%; Copper +0.67%).

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the November core CPI (ex food and energy) was weaker than expectations at 0.12% mom (vs. 0.2%) and 1.7% yoy (vs. 1.8%), partly impacted by a 1.3% mom decline in the price of apparel (the biggest monthly decline in 19 years). Notably, inflation on a three month and six month annualised basis was a tad firmer at 1.9%, but at this point there is limited evidence that the trend in core CPI is reaching the Fed’s target of 2%. Looking ahead, our US economists expect core CPI to be slightly softer near term, but should remain near recent levels in yoy terms. Longer term, they expect core inflation to normalise next year. Refer to their note for more details. Elsewhere, the November real average hourly earnings growth was in line with the prior month’s reading of 0.2% yoy.

In the UK, the October unemployment print was slightly higher than expectations at 4.3% (vs. 4.2% expected) with the number of people in work down 56k (vs. -40k expected) – the fastest pace in almost 2.5 years. Elsewhere, wage growth rose the most since January but was in line with expectations at 2.5% yoy, while the claimant count rate was steady mom at 2.3%. In Europe, the October Industrial Production was above market at 0.2% mom (vs. 0% expected) and 3.7% yoy (vs. 3.2% expected), but Italy’s IP was below consensus at 3.1% yoy (vs. 3.4%). Finally, the final reading of Germany’s November CPI was unrevised at 0.3% mom and 1.8% yoy.

Looking at the day ahead, there is the European Council meeting in Brussels which continues into Friday with Brexit high on the agenda with Mrs May arriving after her voting loss last night. We’ve also got two central bank meetings due with both the BoE and ECB set to hold their last monetary policy meetings of the year. Datawise we’ll get the flash December PMIs in both Europe and the US, as well as the November retail sales data for the UK and US (0.6% mom expected for ex-auto). Other notable data prints include the final November CPI revisions in France, November import price index reading and weekly initial jobless claims data in the US.

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 10.59 points or 0.32% /Hang Sang CLOSED DOWN 55.72 pts or 0.19% / The Nikkei closed DOWN 63.62 POINTS OR 0.28%/Australia’s all ordinaires CLOSED DOWN 0.11%/Chinese yuan (ONSHORE) closed UP at 6.6080/Oil DOWN to 56.34 dollars per barrel for WTI and 62.05 for Brent. Stocks in Europe OPENED ALL RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6080. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.6125 //ONSHORE YUAN SLIGHTLY STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT VERY HAPPY TODAY.(WEAK MARKETS)

3 a NORTH KOREA/USA

NORTH KOREA/

3 b JAPAN

c) REPORT ON CHINA

This will be the ultimate dagger into the heart of USA hegemony: the final drill in preparation for the Petro-Yuan for gold futures trading as begun:

(courtesy zero hedge)

China Regulators Complete Final ‘Drill’ In Preparation For Petro-Yuan Futures Trading

Amid all the chatter of Venezuela and Russia potentially creating oil-backed cryptocurrencies, the “huge news” of China’s launch of the Petro-Yuan has fallen off the front page… until now.

This week saw the Shanghai Futures Exchange complete its fifth yuan-back oil futures contract trading drill successfully…