A

GOLD: $1303.00 up $8.50

Silver: $16.44 up 10 cents

Closing access prices:

Gold $1393.00

silver: $16.94

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 137 NOTICE(S) FOR 13700 OZ.

TOTAL NOTICES SO FAR: 137 FOR 13700 OZ (0.4261 TONNES),

For silver:

jANUARY

321 NOTICE(S) FILED TODAY FOR

1,605,000 OZ/

Total number of notices filed so far this month: 321 for 1,605,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $14,555/OFFER $14,670 UP $164 (morning)

BITCOIN : BID $14,323/OFFER $14,443 /down $50 CLOSING

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY A CONSIDERABLE 2763 contracts from 196,966 FALLING TO 194,459 DESPITE YESTERDAY’S GOOD 13 CENT RISE IN SILVER PRICING. WE HAD SOME CONSIDERABLE COMEX LIQUIDATION AND WITHOUT A DOUBT WE WITNESSED ANOTHER MAJOR BANK SHORT- COVERING OPERATION. NOT ONLY THAT , WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: A HUGE 1944 EFP’S FOR MARCH (AND ZERO FOR OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 1944 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1944 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED EFP’S FOR SILVER ISSUED. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. I BELIEVE THAT WE MUST HAVE HAD SOME MAJOR BANKER SHORT COVERING AGAIN TODAY.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

1944 CONTRACTS (FOR 1 TRADING DAY TOTAL 1944 CONTRACTS OR 9.720 MILLION OZ: AVERAGE PER DAY: 1944 CONTRACTS OR 9.720 MILLION OZ/DAY)

RESULT: A CONSIDERABLE SIZED LOSS IN OI COMEX DESPITE THE STRONG 13 CENT RISE IN SILVER PRICE WHICH USUALLY INDICATES HUGE BANKER SHORT-COVERING. WE ALSO HAD A HUGE SIZED SIZED EFP ISSUANCE OF 1944 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. FROM THE CME DATA 1944 EFP’S WERE ISSUED TODAY (FOR MARCH EFP’S AND NONE FOR ALL OTHER MONTHS) FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY LOST 819 OI CONTRACTS i.e. 1944 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 2763 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER BY 13 CENTS AND A CLOSING PRICE OF $16.84 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.973 BILLION TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 321 NOTICE(S) FOR 1,605,000 OZ OF SILVER

In gold, the open interest ROSE BY A HUMONGOUS SIZED 13,167 CONTRACTS UP TO 471,653 WITH THE STRONG RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($6.50). IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY AND IT TOTALED A HUMONGOUS 11,118 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 10,788 CONTRACTS AND APRIL SAW THE ISSUANCE OF 400 CONTRACTS. The new OI for the gold complex rests at 471,653. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR JANUARY. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE AN ATMOSPHERIC GAIN OF 24,285 OI CONTRACTS: 13,167 OI CONTRACTS INCREASED AT THE COMEX AND A MONSTROUS SIZED 11,118 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 11,125 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE TODAY: 11,118 CONTRACTS OR 1,1118 MILLION OZ OR 34.77 TONNES (1 TRADING DAY AND THUS AVERAGING: 11,118 EFP CONTRACTS PER TRADING DAY OR 1.118 MILLION OZ/DAY)

Result: A HUGE SIZED INCREASE IN OI WITH THE GOOD SIZED RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($6.50). WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,125. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,118 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 24,285 contracts:

11,118 CONTRACTS MOVE TO LONDON AND 13,285 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 75.53 TONNES)

we had: 137 notice(s) filed upon for 13700 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, NO CHANGES IN GOLD INVENTORY AT THE GLD

Inventory rests tonight: 837.50 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 323.459 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A CONSIDERABLE SIZED 2763 contracts from 196,966 DOWN TO 194,459 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE GOOD SIZED RISE IN PRICE OF SILVER TO THE TUNE OF 13 CENTS YESTERDAY. WE HAD WITHOUT A DOUBT A MAJOR SHORT COVERING FROM OUR BANKERS AS THEY HAVE CAPITULATED. NOT ONLY THAT BUT OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1944 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD CONSIDERABLE COMEX SILVER COMEX LIQUIDATION. BUT, IF WE TAKE THE OI LOSS AT THE COMEX OF 2763 CONTRACTS TO THE 1944 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A LOSS OF ONLY 819 OPEN INTEREST CONTRACTS DESPITE THE MAJOR BANKER SHORT COVERING. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET LOSS TODAY IN OZ: 4.095 MILLION OZ!!!

RESULT: A GOOD SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE GOOD SIZED RISE OF 13 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1944 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver

Let us head over to the comex:

The total gold comex open interest ROSE BY A HUMONGOUS 13,167 CONTRACTS UP to an OI level of 472,048 WITH THE GOOD SIZED RISE IN THE PRICE OF GOLD ($6.50 GAIN WITH RESPECT TO YESTERDAY’S TRADING). WE NOT ONLY HAD ZERO COMEX GOLD LIQUIDATION BUT WE ALSO HAD ANOTHER STRONG GAIN IN TOTAL OPEN INTEREST AS WE WITNESSED ANOTHER HUMONGOUS COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 10,788 EFP’S WERE ISSUED FOR FEBRUARY AND 400 EFP’s FOR APRIL: TOTAL OF 11125 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 24,680 OI CONTRACTS IN THAT 11,118 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 13,167 COMEX CONTRACTS. NET GAIN: 24,285 contracts OR 2,428,500 OZ OR 75.53 TONNES

Result: A HUGE SIZED INCREASE IN COMEX OPEN INTEREST WITH THE GOOD RISE IN THE PRICE OF YESTERDAY’S GOLD TRADING (6.50.) WE HAD NO GOLD LIQUIDATION ANYWHERE. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 24,285 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest FALL by 119 contracts DOWN to 417. THUS BY DEFINITION THE TOTAL NUMBER OF OUNCES THAT INITIALLY STAND IN THIS NON ACTIVE MONTH IS 417 CONTRACTS X 100 OZ = 41700 OZ OR 1.2970 TONNES WHICH IS VERY GOOD.

FEBRUARY saw a gain of 8039 contacts up to 340,699. April saw a GAIN of 2813 contracts UP to 40,222

We had 137 notice(s) filed upon today for 13700 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 243,862

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 215,566

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FALL BY A CONSIDERABLE 2763 CONTRACTS FROM 196,966 DOWN TO 194,459 DESPITE YESTERDAY’S GOOD 13 CENT RISE IN PRICE WHICH SEEMS TO INDICATE WE HAD ANOTHER MAJOR ROUND OF BANKER SHORT-COVERING. NOT ONLY THAT, WE HAD ANOTHER HUMONGOUS SIZED 1944 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 1944. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD CONSIDERABLE LONG COMEX SILVER LIQUIDATION AS WELL AS TOTAL SILVER OI LIQUIDATION AS IT SEEMS THAT WE ARE HAVING SOME MAJOR BANKER SHORT-COVERING. WE ARE ALSO WITNESSING A HUGE AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE LOST 819 OPEN INTEREST CONTRACTS:

2763 CONTRACTS LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1944 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS: 819 CONTRACTS

We are now in the big active delivery month of January and here the OI loss by 27 contracts down to 539. THUS BY DEFINITION WE HAVE 539 X 5,000 OZ PER CONTRACT EQUALS 2,695,000 OZ STANDING IN THIS NON ACTIVE MONTH OF JANUARY WHICH IS EXCELLENT FOR THIS GENERALLY POOR DELIVERY MONTH.

February saw a gain OF 39 OI contract RISING TO 186. The March contract LOST 2877 contracts DOWN to 153,585.

We had 321 notice(s) filed for 1,605,000 oz for the DECEMBER 2017 contracts

INITIAL standings for JANUARY

Dec 29/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

N/A oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

137 notice(s)

13700 OZ

|

| No of oz to be served (notices) |

280 contracts

(28,000oz)

|

| Total monthly oz gold served (contracts) so far this month |

137 notices

13700 oz

0.4261 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 26 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 137 contract(s) of which 130 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (137) x 100 oz or 13700 oz, to which we add the difference between the open interest for the front month of JAN. (417 contracts) minus the number of notices served upon today (137 x 100 oz per contract) equals 41,700 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (137 x 100 oz or ounces + {(417)OI for the front month minus the number of notices served upon today (137) x 100 oz which equals 41,700 oz standing in this active delivery month of JANUARY (1.297 tonnes). THERE IS 33.29 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 1,070,309.229 or 33.29 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,143,181.135 or 284.39 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

N/A oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

N/A oz

Scotia

|

| No of oz served today (contracts) |

321

CONTRACT(S)

(1,605,000 OZ)

|

| No of oz to be served (notices) |

218contract

(1,090,000 oz)

|

| Total monthly oz silver served (contracts) | 321 contracts

(1,605,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

CANNOT RETRIEVE COMEX INVENTORY DATA

The total number of notices filed today for the JANUARY. contract month is represented by 321 contract(s) FOR 1,605,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 321 x 5,000 oz = 1,605,000 oz to which we add the difference between the open interest for the front month of JAN. (539) and the number of notices served upon today (321 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 321(notices served so far)x 5000 oz + OI for front month of JANUARY(539) -number of notices served upon today (321)x 5000 oz equals 2,695,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3,790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 65,836

CONFIRMED VOLUME FOR FRIDAY: 60,489 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 60,489 CONTRACTS EQUATES TO 302 MILLION OZ OR 43.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 59.182 million

Total number of dealer and customer silver: 240.232 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.6 percent to NAV usa funds and Negative 1.3% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.8%

Percentage of fund in silver:37.0%

cash .+.2%( Dec 28/2017)

2. Sprott silver fund (PSLV): NAV RISES TO -1.30% (Dec 29 /2017)??????????????????????????????

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.91% to NAV (Dec 29 /2017 )

Note: Sprott silver trust back into NEGATIVE territory at -1.30%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.66%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 28/2017/ Inventory rests tonight at 837.50 tonnes

*IN LAST 301 TRADING DAYS: 103.45 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 236 TRADING DAYS: A NET 53.83 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 212.72 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 29/no changes in silver inventory at the SLV/Inventory rests at 323.459 million oz

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Dec 2892017:

Inventory 323.459 million oz

end

WOW!!!

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.85%

12 Month MM GOFO

+ 1.95%

30 day trend

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

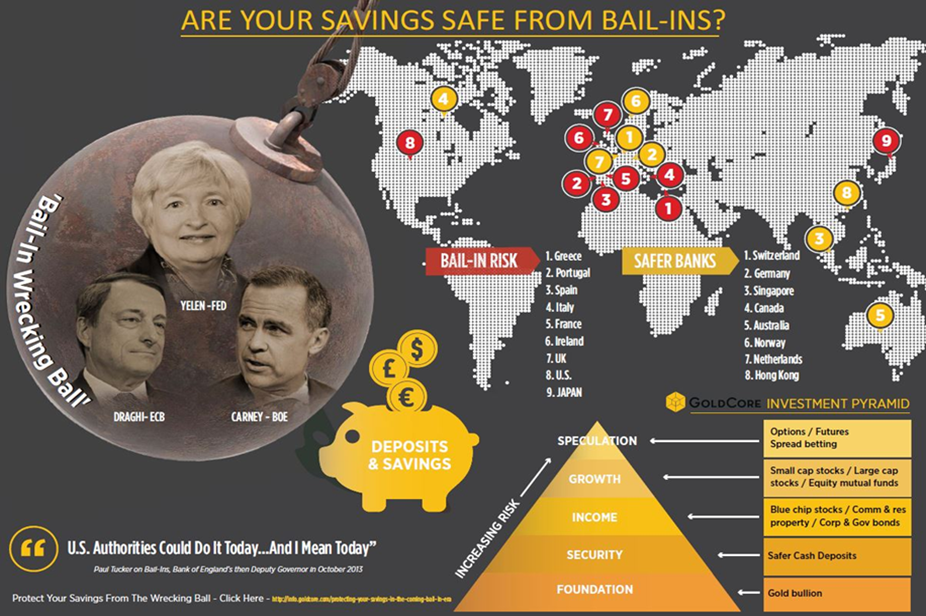

Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

– Two years since bail-in rules officially entered EU regulations

– EU bail-in rules have wiped out billions for savers and and businesses, with more at risk

– Future of many failing banks now rests on depositors who may no longer be protected by deposit insurance

– Physical gold enables savers to stay out of banking system and reduce exposure to bail-ins

– For more listen to our Goldnomics Podcast: What does 2018 have in store for financial markets?

Ah, New Year’s resolutions, what fun. For some reason we opt to commit to fairly big life changes at some point between Christmas and New Year. This is a time when the real world seems a lifetime away from the cosiness of the holiday season. We often make a resolution when we have had too much of something, perhaps booze, perhaps food or perhaps it is based on regrets from the previous year. Despite best intentions, rarely do we stick to them.

May we make a suggestion? If you’re going to make any resolutions this year make one that is pretty easy to stick to and that won’t make too much of a short-term impact on your life: resolve to pay attention to and to protect yourself from the threat that is ECB bail-in tools. In the long-term you’ll be more grateful you did this than if you had given up cursing or drinking for a month.

On the 1st January 2018 the ECB bail-in tool will be two years old. That’s right just over two years ago the ECB decided that it was better to force the financial burden of banks’ failures away from the state and instead onto bondholders and creditors i.e. those with money in the bank.

The ECB was following in the footsteps of the US where bail-ins have been part and parcel of financial legislation since the crisis of 2007-08. Canada has more recently joined the party.

We have relentlessly covered the threat of and developments in bail-in legislation over the last two years. It is perhaps the most shocking decision to come out of regulators and central banks since the financial crisis. It is even more shocking when one considers the lack of uproar from the financial media who continue to peddle the myth that the financial system is more secure than pre-financial crisis.

The bail-in legislation has been put in place because the EU, along with the rest of the world, has been through a horrendous financial crisis. It exposed such dangers in the banking system that it has taken nearly a decade for global regulators to agree to post-banking crisis rules. Just this month Basel III was agreed. The whole aim of the agreement is to protect governments by having private investors suffer losses first during banking crises.

One has to ask, if politicians are so keen for us to believe in the stability of the financial system in those problem areas why the need for legislation that not only places depositors at risk but has been updated continuously to put them at even more of a disadvantage?

2018 should be a time when investors and savers resolve to take charge of their wealth and hold it outside of the banking system. Physical gold that is allocated and segregated is able to offer this, as well as zero exposure to the bail-in regime. You can hear more about our expectations for 2018 in our new Goldnomics podcast.

What is a bail-in?

A quick refresher from our free guide to bail-ins:

A bail-in is when regulators or governments have statutory powers to restructure the liabilities of

distressed banks and nancial institutions, and impose losses on both bondholders and depositors.

Simply stated, a bank bail-in is an attempt to resolve and restructure a bank as a going concern, by creating additional bank capital (recapitalisation) via forced conversion of the bank’s creditors’ claims (potentially bonds and deposits) into newly created share capital (common shares of the bank).

This is really the crux of the Cyprus template – depositors internationally now have to think of their uninsured deposits as liable to potentially being con scated and transformed into bank shares.

Bank depositors have traditionally viewed their bank deposits as one hundred percent secure, with an inalienable right to have their deposits returned in full. However, this has never been the case in legal terms, as a bank depositor is just an unsecured creditor of the bank.

The original bail-in legislation stated that a bail-out using public funds was not an option until creditors accounting for at least 8% of the lender’s liabilities had paid up (the bail-in). At the moment €100,000 or £75,000 is protected per depositor, this amount is known as a ‘covered deposit’.

Deposits soon to be more exposed, as decided by bureaucrats

In terms of who pays what it is no longer down to the sovereign government, the introduction of bail-in legislation made clear that that responsibility now lies with the Single Resolution Mechanism.

So not only are your government unable to act in your best interests when it comes to a bail-in but you are now at the mercy of the ECB who will decide on a bail-in based on the Union’s best interests.

This was most recently reminded to us when the ECB proposed that ‘covered deposits’ should be replaced to allow for more flexibility. Essentially under the new proposals depositors and savers will no longer be guaranteed any amount of money should a bank go under.

“covered deposits and claims under investor compensation schemes should be replaced by limited discretionary exemptions to be granted by the competent authority in order to retain a degree of flexibility.”

To translate the legalese jargon of the ECB bureaucrats this could mean that the current €100,000 (£85,000) deposit level currently protected in the event of a bail-in may soon be no more.

But worry not fellow savers as the ECB is fully aware of the uproar this may cause so they have been kind enough to propose that:

“…during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.”

So that’s a relief, you’ll only need to wait five days for some ‘competent authority’ to deem what is an ‘appropriate amount’ of your own money for you to have access to in order eat, pay bills and get to work.

Quick and dangerous fixes to cover loopholes and prevent further insubordination

Unsurprisingly bailing-in has been politically tricky, to say the least.

Efforts of governments to avoid any awkwardness when it comes to bail-ins has most prominently been seen in Italy.

Earlier this year the country’s clean-up of the two largest lenders, Banca Popolare di Vicenza SpA and Veneto Banca SpA, saw the government enact a loophole. Rather than use the EU’s Bank Recovery and Resolution Directive (which would have put the EU in control of the rescue attempt and forced even more losses on more bondholders) domestic insolvency laws were used.

The EU had been hoping for a ‘success’ story as seen with Banco Popular Espanol SA. This saw the bank sold to a bigger competitor in June 2017. The sale promptly wiped out shareholders and about 2 billion euros ($2.3 billion) owed to bondholders (who are often Joe Bloggs depositors).

Needless to say the EU were not happy when the Italian bank rescues did not go the same route. They have no doubt since been working on amendments to ensure that such insubordination cannot happen again. Italy’s moves did not stop savers from being hurt, the banking meltdown in Veneto Italy destroyed 200,000 savers and 40,000 businesses.

Meanwhile, since the financial crisis regulators have been so busy putting in place rescue agendas and items like Basel III they have lost control of what now puts the financial market at risk.

As GoldCore CEO Stephen Flood reminds us:

The actual cause for a banking collapse is reckless lending policies of banks, the build up of leverage and beckoning inflation rates. The central banks should be focused on stability and not economic growth at all costs and the wholesale confiscation of assets.

There are two key issues that place the bail-in agenda at even greater likelihood of being enforced in a more extreme way, across the EU. These are so great that last month the removal of covered deposits was suggested (see above and read more here) as a means to prevent a run on the banks should depositors get wind of how dangerous a situation many banks find themselves in.

These two issues are thanks to sovereign government debt and the rapid growth of the shadow banking system.

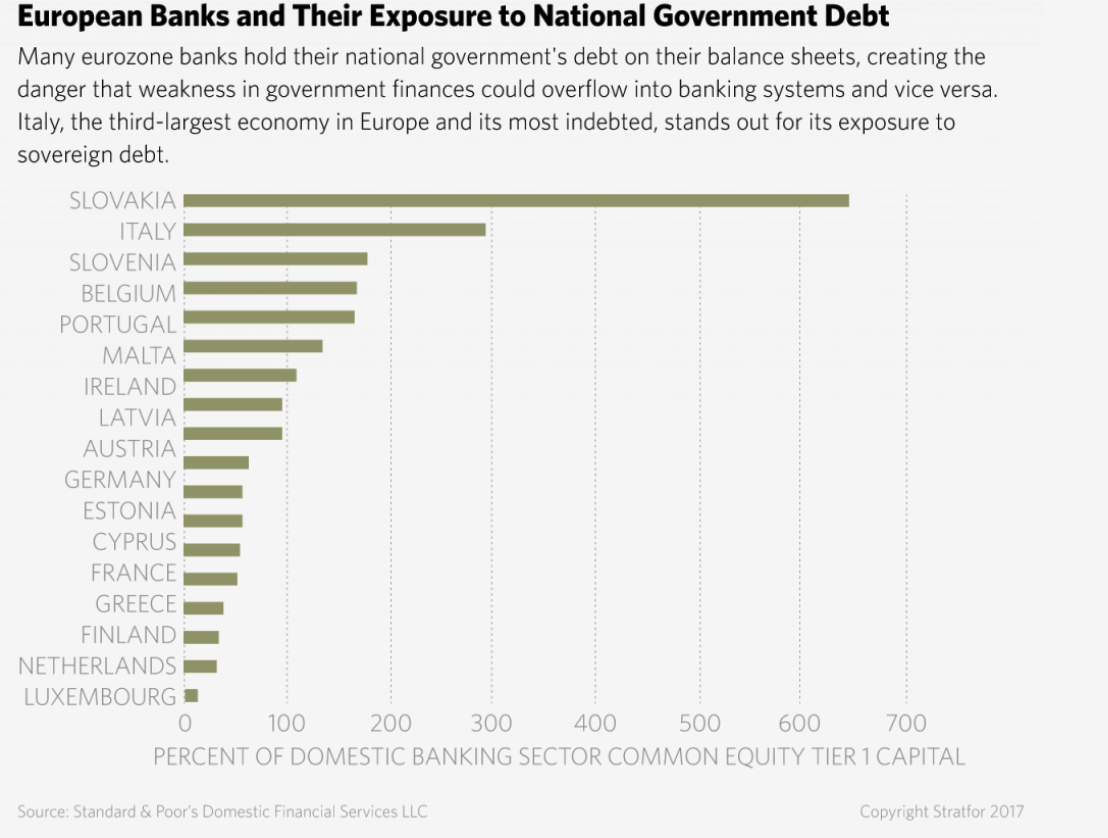

What lies in the shadows

There is a ‘doom-loop’ in existence. In need of safe assets, banks often hold lots of government debt, which is generally deemed risk free. Risk-free? As my 14 year old cousin would say ‘Mega-lolz’.

Stratfor explains the doom-loop as follows:

This refers to the danger that if financial or economic crisis hit a country whose banks owned large amounts of sovereign debt, solvency problems would be transmitted from the banks to the government and back, leading to an insoluble self-reinforcing death spiral.

It was actually the doom-loop which originally inspired the bail-in legislation, launched to prevent such a scenario. The concern now is that it might be too little too late or just the wrong tool for the job.

The second issue is the shadow banking system. Despite the heralding in of Basel III it has done little to restrict the growth of the lesser regulated shadow banking system. The system involved financial intermediaries ranging from hedge funds to special purpose vehicles. Generally they have to abide by by less regulation and lower liquidity requirements than their banking contemporaries.

As a result of this relaxed stance on the shadow banking system, outpaced regular lenders in international credit growth for most of the past decade. Here in the EU they are estimated to hold more than €40 trn on assets.

So far, no one has asked what will happen when this bubble bursts. The loop will no doubt tie-in with the banking system, putting depositors once again at risk. However, as with government debt, we are more likely to see greater restrictions on savers and depositors than we will on additional controls on the shadow banking system.

There is no short-term panacea, prepare for the long-term

Sadly the EU seems to believe that a banking system can be propped up by control of and reduction in the rights of hardworking savers when it comes to their money. This is instead of actually dealing with the crux of the matter – too much debt in the system.

For a long time we have explained to readers about how it is not worth trusting that the ECB and governments have our best interests at heart. Whether you are a saver, a business or a pensioner with limited funds government institutions have shown blatant disregard for your wealth.

Whilst the ECB works shamelessly to protect the bigger picture, you must make a few changes to prepare for the realistic picture.

By way of reminder the ECB is proposing that in the event of a bail-in it will give you an allowance from your own savings. An allowance it will control:

“…during a transitional period, depositors should have access to an appropriate amount of their covered deposits to cover the cost of living within five working days of a request.”

i.e. no-one is saying if you will ever get that £10,000, £75,000 or €100,000 back.

Savers should be looking for means in which they can keep their money within instant reach and their reach only. At this point gold and silver is the clear option.

Physical, allocated and segregated gives you outright legal ownership. There are no counterparties who can claim it is legally theirs (unlike with cash in the bank or shares) or legislation that rules they get first dibs on it.

Gold and silver are the financial insurance against bail-ins, political mismanagement, and overreaching government bodies. As each year goes by it becomes more pertinent than ever to protect yourself from such risks.

This year make sure you’re not ignoring the birthday of the bail-in era, instead you are resolving to fight against it by buying gold to celebrate.

To read more about how you can protect your savings in the bail-in era then read our free guide here.

Recommended reading

Protect Your Savings With Gold: ECB Propose End To Deposit Protection

Invest In Gold To Defend Against Bail-ins

Precious Metals Are “Best Defence” Against Bail-ins In Economic Crisis

Bail-Ins In Italy? World’s Oldest Bank “Survival Rests On Savers”

New EU Rules For Cross-Border Cash and Gold Bullion Movements

News and Commentary

Gold set for best year since 2010 (Reuters.com)

Gold advances to fresh monthly tops above $1290 (FXStreet.com)

Six Charts Show Gold’s Bulls and Bears Have Plenty to Chew Over (Bloomberg.com)

US Treasury yields higher after PMI data beats, jobless claims hold steady (CNBC.com)

Mortgage rates end 2017 with a whimper not a bang (MarketWatch.com)

Source: FT

Citigroup fined for telling clients to buy when it meant sell (Bloomberg.com)

The U.S. Inflation Mystery Made Economists Look Bad in 2017 (Bloomberg.com)

Bitcoin Rebounds to $15,000 as Investors Find a Bottom, For Now (Bloomberg.com)

Russia And China Lay Economic Foundation Based On Golden Rule (ZeroHedge.com)

From Bitcoin to Belize, Here Are Best and Worst Assets of 2017 (Bloomberg.com)

Gold Prices (LBMA AM)

29 Dec: USD 1,296.50, GBP 960.84 & EUR 1,082.45 per ounce

28 Dec: USD 1,291.60, GBP 960.43 & EUR 1,082.75 per ounce

27 Dec: USD 1,285.40, GBP 958.78 & EUR 1,081.54 per ounce

22 Dec: USD 1,268.05, GBP 947.74 & EUR 1,069.85 per ounce

21 Dec: USD 1,265.85, GBP 945.97 & EUR 1,065.09 per ounce

20 Dec: USD 1,265.95, GBP 944.27 & EUR 1,068.21 per ounce

19 Dec: USD 1,263.10, GBP 944.93 & EUR 1,070.10 per ounce

Silver Prices (LBMA)

29 Dec: USD 16.87, GBP 12.48 & EUR 14.07 per ounce

28 Dec: USD 16.74, GBP 12.46 & EUR 14.02 per ounce

27 Dec: USD 16.50, GBP 12.30 & EUR 13.87 per ounce

22 Dec: USD 16.18, GBP 12.08 & EUR 13.65 per ounce

21 Dec: USD 16.15, GBP 12.08 & EUR 13.61 per ounce

20 Dec: USD 16.19, GBP 12.09 & EUR 13.67 per ounce

19 Dec: USD 16.16, GBP 12.08 & EUR 13.68 per ounce

Recent Market Updates

– 98,750,067,000,000 Reasons to Buy Gold in 2018

– Gold, Bitcoin and the Blockchain Replaces the Banks – Realists Guide To The Future

– It’s A Wonderful Life Is A Wonderful Lesson To Hold Gold Outside of The Banking System

– Goldnomics Podcast – Gold, Stocks, Bitcoin in 2018. Everything Bubble Bursts?

– What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

– New Rules For Cross-Border Cash and Gold Bullion Movements

– ‘Gold Strengthens Public Confidence In The Central Bank’ – Bundesbank

– WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors

– Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

– UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

END

Cryptos falling again last night

(courtesy zerohedge)

Cryptos Are Tumbling Again As Bitcoin2x Fork Looms

Having rebounded well off the overnight lows after South Korean regulators headlines, cryptocurrencies are crashing lower once again here with Litecoin and Bitcoin leading the drop…

Volume is considerably lower on this drop…

No immediate catalyst for this latest move yet, but after some earlier disruptions, BitStamp and Gemini have confirmed that withdrawals are once again enabled.

Additionally, as Coinivore reports, the new Segwit2x lead developer Jaap Terlouw has confirmed on the project’s website that the team will finally execute the Bitcoin hardfork on December 28th or block 501451.

Originally scheduled for November, the original B2X development team canceled the fork amidst controversy in the community. In an official statement, the team recognized that they had “not built sufficient consensus for a clean blocksize upgrade at this time,” foregoing the fork in an effort to “keep the community together.”

The project’s now updated roadmap now lists December 28th as the set date for the fork, and in the recent announcement, Terlouw confirmed these ongoing developments:

“Our team will carry out the Bitcoin hard fork, which was planned for mid-November.”

The team argues the reasoning behind the fork is due to “commission and transaction speed within the Bitcoin network has reached extraordinary values.” Terlouw believes that “it is almost impossible to use Bitcoin as a means of payment.”

In hopes of fixing these issues, the Segwit 2x fork will reduce block times to 2.5 minutes and increase block size to 4MB.

For months now only the “trading of B2X futures has been carried out on some exchanges,” according to Terlouw, the most notable being HitBTC. Other exchanges that have confirmed support for the fork include – Binance, GDax, and BTCC.

Jaap Terlouw promises that all “BTC holders will receive not only B2X in the ratio of 1 to 1, but also a proportional number of Satoshi Nakamoto’s Bitcoins as a reward for their commitment to progress.”

It is worth noting that this B2x is not the original hardfork that was scheduled for last month as such it doesn’t have community consensus and has nothing to do with the New York Agreement.

The original B2X was lead by former SegWit2x lead developer Jeff Garzik who announced the cancelation after the agreement caused chaos within the cryptosphere spurring the No2X v.s. 2x argument on many popular forums.

“Although we strongly believe in the need for a larger block size, there is something we believe is even more important; keeping the community together. Unfortunately, it is clear that we have not built sufficient consensus for a clean blocksize upgrade at this time. Continuing on the current path could divide the community and be a setback to Bitcoin’s growth. This was never the goal of SegWit2x.”

Belshe further stated:

“We want to thank everyone that contributed constructively to Segwit2x, whether you were in favor or against. Your efforts are what makes Bitcoin great. Bitcoin remains the greatest form of money mankind has ever seen, and we remain dedicated to protecting and fostering its growth worldwide.”

The newly revived Bitcoin2x will provide the following features:

- Estimated fork date: 12.28.2017

- Total issue: 21 million

- Protection against repeated transactions: Yes

- Block extraction speed: 2.5 minutes

- Mining: X11

- Block size: increased to 4 mb

- Recalculation of complexity: after each block

- Unique address format: Yes

In addition, the Roadmap promises the following within the future:

- Offline codes

- Support for Lightning Network, instant transactions

- ZkSnark

- Smart contracts

- Anonymous transactions

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

Global Stocks Set To Close 2017 At All Time Highs, Best Year For The Euro Since 2003

With just a few hours left until the close of the last US trading session of 2017, and most of Asia already in the books, S&P futures are trading just shy of a new all time high as the dollar continued its decline ahead of the New Year holidays.

Indeed, markets were set to end 2017 in a party mood on Friday after a year in which a concerted pick-up in global growth boosted corporate profits and commodity prices, while benign inflation kept central banks from snatching away the monetary punch bowl. As a result, the MSCI world equity index rose another 0.15% as six straight weeks and now 13 straight months of gains left it at yet another all time high.

In total, world stocks haven’t had a down month in 2017, with the index rising 22% in the year adding almost $9 trillion in market cap for the year.

Putting the year in context, emerging markets led the charge with gains of 34%. Hong Kong surged 36%, South Korea was up 22% and India and Poland both rose 27% in local currency terms. Japan’s Nikkei and the S&P 500 are both ahead by almost 20%, while the Dow has risen by a quarter. In Europe, the German DAX gained nearly 14% though the UK FTSE lagged a little with a rise of 7 percent.

Craig James, chief economist at fund manager CommSec, told Reuters that of the 73 bourses it tracks globally, all but nine have recorded gains in local currency terms this year.

“For the outlook, the key issue is whether the low growth rates of prices and wages will continue, thus prompting central banks to remain on the monetary policy sidelines,” said James. “Globalization and technological change have been influential in keeping inflation low. In short, consumers can buy goods whenever they want and wherever they are.”

Still, the good times may not last: an State Street index that gauges investor risk appetite by what they actually buy and sell, suffered its six straight monthly fall in December, Reuters reported.

“While the broader economic outlook appears increasingly rosy, as captured by measures of consumer and business confidence, the more cautious nature of investors hints at a concern that markets may have already discounted much of the good news,” said Michael Metcalfe, State Street’s head of global macro strategy.

* * *

Now summarizing the overnight action, Europe’s Stoxx 600 Index was little changed on the last trading day of 2017, while U.S. index futures edged higher, with the E-mini trading higher by 0.3% and just 5 points away from 2,700. European stocks hold steady, set for their best year since 2013, while the MSCI Asia Pacific Index closed the year with an annual gain of almost 29%, its biggest advance since 2009.

Bonds in Europe ticked lower as Treasuries steadied. The Bloomberg Dollar Index fell for a third day, heading for its worst annual performance in more than a decade. The Bloomberg Commodity Index gained for 12th day, set for the longest streak on record, as WTI crude advanced above $60 a barrel.

European stocks held steady on the last trading day of 2017, headed for the biggest annual gain in four years. The Stoxx Europe 600 Index was effectively unchanged, on volume that was about half the 30-day average, with miners leading gains. Europe’s benchmark index has risen 7.8% this year. Stock markets including the U.K., Ireland and Germany close early today. 9 out of 19 Stoxx 600 sectors rise; technology sector has the biggest volume at 63% of its 30-day average; 249 Stoxx 600 members gain, 299 decline. Top Stoxx 600 outperformers include: AstraZeneca +1.5%, TGS NOPEC Geophysical +1.1%, Just Eat +1.1%, Old Mutual +1.0%, AP Moller – Maersk +0.9%.

Developing-nation stocks and currencies headed for a third week of gains, extending their biggest annual rallies since 2009 as trading wound down for the year. The Czech koruna posted the strongest advance among peers for 2017 after the central bank lifted its cap on the currency’s gains earlier in the year. MSCI’s currencies gauge rallies for 6th day, adding 0.4% and poised for best week since July; its 2% gain in month is biggest since Jan. Equity benchmark climbs 0.5%, rising 3rd day, set for third weekly advance, best monthly increase since July.

In Asia, the MSCI Asia Pacific Index rose 0.2%, heading for a record close. The MSCI Emerging Markets Index headed for a third straight weekly gain and its highest close since 2011. Japan’s Topix Index fell 0.1 percent as of the close in Tokyo, still near its highest level since 1991. Hong Kong stocks rose in the last week of 2017, the third straight week of gains, as some of this year’s best performers added to their rallies. China’s benchmark gauge capped a relatively muted annual advance. Hang Seng Index adds 0.2% on Friday; the measure jumped 36% this year, while the Hang Seng China Enterprises Index climbed 0.2%, taking YTD gain to 25%. China’s Shanghai Composite climbed 0.33% to 3307 on the last trading day of 2017, making it 6.56% higher for the whole year, while China’s Nasdaq-equivalent, Chinext, was down 10% compared to one year earlier.

In macro, the dollar continued its slide against all G-10 peers, in line with its year-to-date performance. Losses extended as London came into the market, with the greenback reaching multi-week lows against most peers, with the thin liquidity in year-end markets exacerbating the size of the moves. The dollar drop was catalyzed by a fresh decade-low spread between the 2 and 10Y Treasuries, with the relentless flattening fueling concern the U.S. economy will weaken.

China’s onshore yuan rallied 0.4% and Malaysia’s ringgit climbs 0.5%, advancing for third day and leading the rally as the dollar edged lower in subdued trading before the new-year holiday. Taiwan’s currency climbed to the strongest in four years before erasing its advance as its central bank asked banks to purchase dollars. South Korea’s won was the best-performing Asian currency this year, rising 13 percent.

And as the Bloomberg Dollar Spot Index was headed for its worst annual decline since data began in 2005, the euro was set for its best year against the greenback since 2003, while the yen and Aussie are headed for their biggest annual advance since 2010, and the Kiwi since 2012.

The euro touched a fresh three-month high against the dollar amid a broad-based selloff in the U.S. currency as year-end portfolio rebalancing extended the greenback’s 2017 decline. “The market is probably getting too complacent about a shortage of dollar liquidity right now,” said Andreas Steno Larsen, a global currency strategist at Nordea Markets. While the story of a year-end liquidity squeeze in the dollar was “blown out of proportion,” the dynamic is likely to extend into 2018, he said.

Similarly, the yen was poised for its biggest annual gain versus the dollar in six years as a flatter U.S. yield curve weighed on the greenback. “With no policy surprises from Japan and the U.S., dollar-yen was weighed down by the dollar’s general weakness, which was the main theme for 2017,” said Daisuke Karakama, chief market economist at Mizuho Bank in Tokyo. “The flatness of the U.S. yield curve poses a challenge for next year as an inversion of short- and long-term yields comes into sight. That makes it difficult to forecast long-term yields rising, and this will weigh on dollar-yen.” A rally in commodity prices bolstered the currencies of countries that rely on raw material exports, such as Australia and New Zealand. The Aussie headed for its best year since 2010, while the kiwi was set for its biggest annual advance since 2012.

As the chart below shows, in a year in which the dollar was supposed to be the world’s best performer, with many talking about parity with the euro in January, the USD ended up being the worst performer, losing a whopping 13.6% against the Euro. Meanwhile, the Bloomberg Dollar Spot Index is on track for its first annual decline since 2012, sliding 8.5% in 2017.

Meanwhile, boosted by the ongoing dollar weakness, oil prices rose, with WTI crude climbing above $60 per barrel to hit a new two and a half year high. Oil prices rose, with WTI crude climbing above $60 per barrel to hit a 2-1/2 year high. Treasury yields edged lower, while gold climbed. 10Y TSY yields fell 1bp to 2.42%; German 10Y Bunds gained less than 1 bp to 0.43%, while Britain’s 10Y gilt climbed 1 basis point to 1.199%.

The dollar’s loss has been a boon for commodities priced in the currency, which have also benefited from a synchronized pick up in global trade and surprisingly strong demand from China. Everything from coal to iron ore has reaped gains, with copper a stand-out performer in part due to expectations of rising demand for the mass production of electric vehicles. The metal was near a four-year peak on Friday at $7,284 a tonne. It is up more than 30 percent this year and on course for its largest annual rise since 2009.

Gold struggled somewhat this year against a background of subdued global inflation, but at $1,295.18 an ounce was still on track to end 2017 with gains of more than 12 percent.

Oil prices were near their highest in 2-1/2 years after data showed strong demand for crude imports in China and a surprise fall in U.S. production. Brent crude futures added 45 cents to reach $66.61 a barrel, up more than 16 percent on the year so far, while U.S. crude futures climbed 46 cents to $60.30 a barrel.

Market Snapshot

- S&P 500 futures up 0.34% to 2,694.5

- STOXX Europe 600 down 0.03% to 389.43

- MSCI Asia Pacific up 0.3% to 174.00

- MSCI Asia Pacific ex Japan up 0.5% to 570.34

- Nikkei down 0.08% to 22,764.94

- Topix down 0.08% to 1,817.56

- Hang Seng Index up 0.2% to 29,919.15

- Shanghai Composite up 0.3% to 3,307.17

- Sensex up 0.6% to 34,056.87

- Australia S&P/ASX 200 down 0.4% to 6,065.13

- Kospi up 1.3% to 2,467.49

- German 10Y yield rose 0.4 bps to 0.428%

- Euro up 0.3% to $1.1982

- Italian 10Y yield rose 3.5 bps to 1.688%

- Spanish 10Y yield rose 1.6 bps to 1.536%

- Brent Futures up 0.4% to $66.39/bbl

- Gold spot up 0.1% to $1,296.69

- U.S. Dollar Index down 0.3% to 92.34

Top overnight news from BBG

- Donald Trump believes Robert Mueller, special counsel in the Russia probe, will treat him fairly, the U.S. president said in an interview with the New York Times

- Speculation is rising that American drillers will put more rigs to work as oil strengthens, with shale growth driving forecasts of record U.S. supply in 2018; that could act counter to plans by producers including Saudi Arabia, who have pledged to extend production curbs through 2018 to wipe out a global glut

- Euro-area banks were net sellers of EU9.8b public securities in November

- Consumer-price inflation accelerated on the month in December in the German states Saxony, Hesse and Bavaria; inflation slowed y/y

- Spain flash harmonized CPI rose 1.3% y/y in December, vs estimate +1.5%

- Trump’s Tax Overhaul May ‘Punish’ Foreign Banks With U.S. Units

- Florida’s Real Estate Reckoning Could Be Closer Than You Think

- Icahn Wins Tussle With SandRidge as Bonanza Deal Is Scrapped

- Apple Apologizes for IPhone Speed Cuts to Prevent Crashing

- As MiFID Nears, This Risk Officer Is Looking Forward to February

In Asian markets,, the MSCI Asia Pacific Index rose 0.2%, heading for a record close. The MSCI Emerging Markets Index headed for a third straight weekly gain and its highest close since 2011. Japan’s Topix Index fell 0.1 percent as of the close in Tokyo, still near its highest level since 1991. Hong Kong stocks rose in the last week of 2017, the third straight week of gains, as some of this year’s best performers added to their rallies. China’s benchmark gauge capped a relatively muted annual advance. Hang Seng Index adds 0.2% on Friday; the measure jumped 36% this year, while the Hang Seng China Enterprises Index climbed 0.2%, taking YTD gain to 25%. China’s Shanghai Composite climbed 0.33% to 3307 on the last trading day of 2017, making it 6.56% higher for the whole year, while China’s Nasdaq-equivalent, Chinext, was down 10% compared to one year earlier.

Top Asian News

- China Shadow Banks Pay Record Premium for Cash as Squeeze Bites

- Japanese Stocks Have Best Year Since 2013 on Corporate Profits

- India Planning to Cut Oil Import Bill With Methanol Blending

- Taiwan Central Bank Is Said to Ask Banks to Buy U.S. Dollars

- China Says It Created a France-Sized Pile of New Jobs Since 2012

In European bourses, stocks held steady on the last trading day of 2017, headed for the biggest annual gain in four years. The Stoxx Europe 600 Index was effectively unchanged, on volume that was about half the 30-day average, with miners leading gains. Europe’s benchmark index has risen 7.8% this year. Stock markets including the U.K., Ireland and Germany close early today. 9 out of 19 Stoxx 600 sectors rise; technology sector has the biggest volume at 63% of its 30-day average; 249 Stoxx 600 members gain, 299 decline. Top Stoxx 600 outperformers include: AstraZeneca +1.5%, TGS NOPEC Geophysical +1.1%, Just Eat +1.1%, Old Mutual +1.0%, AP Moller – Maersk +0.9%.

Top European News

- Vectura Gains on Final Trading Day of 2017, Up ~30% in December

- Bitcoin is Like Trading in Pearls, ECB’s Rimsevics Tells Tvnet

In commodities, WTI crude increased 0.4% to $60.09 a barrel, the highest in more than two years. Gold advanced 0.2 percent to $1,296.95 an ounce, hitting the highest in 11 weeks with its eighth consecutive advance. Copper dipped 0.4 percent to $3.29 a pound, the first retreat in more than three weeks. The Bloomberg Commodity Index gained less than 0.05 percent to 87.73, hitting the highest in more than seven weeks with its 12th straight advance.

In FX, EUR/USD up as much as 0.4% to $1.1988, highest since Sept. 22. The euro is up ~14% YTD versus the U.S. currency, set for its biggest annual gain since 2003. GBP/USD rises 0.5% to $1.3507, with the pound on track for an annual gain of ~9.5% versus the dollar. Sterling has been supported by better-than-forecast U.K. data in the wake of Brexit and progress in talks with the EU. USD/JPY falls 0.2% to 112.60; yen heads for its biggest annual gain versus the greenback in six years. The yen is set to weaken in 2018 on widening of real yields between Japan and the U.S., according to Eddie Cheung, Asia FX strategist at Standard Chartered Bank in Hong Kong. NZD/USD advances 0.4% to 0.7115, benefiting from a rally in commodity prices as well as quarter- and year-end rebalancing, according to a Credit Agricole note. AUD/USD rises 0.2% to 0.7810, gaining as commodities strength boosts the economic outlook and makes higher interest rates next year more likely.

US Event Calendar: Nothing major scheduled

end

3. ASIAN AFFAIRS

3 a NORTH KOREA/USA

NORTH KOREA/

A Hong Kong ship has just been seized after transferring oil to North Korea

(courtesy zerohedge)

Hong Kong Ship Seized After Transferring Oil To North Korea

Just days after we showed satellite images which indicated that Chinese ships were trading oil with North Korean ships in a blatant violation of UN Security Council sanctions, South Korea said Friday that it was holding a Hong Kong flagged ship suspected of doing just that.

The Lighthouse Winmore is believed to have “secretly transferred” about 600 tons of refined petroleum products to the North Korean ship, the Sam Jong 2, in international waters in the East China Sea on Oct. 19, according to Bloomberg and the Associated Press.

The Hong Kong vessel had previously visited Yeosu port on Oct. 11 to load up on Japanese oil products and departed the port while claiming its destination was Taiwan. Instead, it transferred the oil to the Sam Jong 2 and three other non-North Korean vessels in international waters

The vessel was chartered by Taiwanese company Billions Bunker Group, which is incorporated in the Marshall Islands. According to Bloomberg, Taiwanese investigators are looking into whether any Taiwanese nationals have ties to the ship that was seized on Friday, Taiwan’s Maritime and Port Bureau says in statement on its website.

Photos from US recon satellites released earlier this week showed at least 30 illegal transactions involving Chinese vessels selling oil to North Korea on the West Sea in October. The images allegedly showed large Chinese and North Korean ships transacting in oil in a part of the West Sea closer to China than South Korea. The satellite pictures were so clear, they even showed the names of the ships.

Amusingly, Beijing on Thursday said there was no illicit trade, with defense ministry spokesman Ren Guoqiang denying everything and claiming that China and its military strictly enforced the UN resolutions on North Korea.

“The situation you have mentioned absolutely does not exist,” Ren said at a regular media briefing, without elaborating.

According to Chinese customs data, the country did not export any oil products to North Korea in November.

South Korean customs authorities boarded the ship and interviewed crew members after they returned to Yeosu on Nov. 24. South Korea formally seized the ship after the UN Security Council on Dec. 22 imposed new sanctions on North Korea that allow member states to seize, inspect and freeze vessels that are suspected of transferring banned goods to or from North Korea, the official said. He spoke on condition of anonymity, citing office rules.

The ship’s 25 crew members – 23 of them Chinese nationals and two from Myanmar – are being held at Yeosu but will be allowed to leave South Korea after authorities are finished investigating them, the official said. South Korea plans to report the results of its inspection to the UN Security Council’s sanctions committee.

Whether the Sam Jong 2 returned to North Korea after receiving the oil could not be confirmed.

* * *

The Treasury Department last month sanctioned six North Korean shipping and trading companies and 20 of their vessels. The North Korean ship seen accepting oil transfers in the photos released by the Treasury Department was identified as the Rye Song Gang 1.

Ship-to-ship trade with North Korea at sea is prohibited under the round of UN sanctions adopted on Sept. 11. A subsequent round of sanctions aimed at restricting the North Korean energy trade was passed earlier this month.

President Donald Trump criticized China in a tweet published last night:

Caught RED HANDED – very disappointed that China is allowing oil to go into North Korea. There will never be a friendly solution to the North Korea problem if this continues to happen!

China is responsible for more than 90% of North Korea’s foreign trade and oil supplies.

end

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

China tests its new hypersonic weapon which will render the USA THAAD system powerless

(courtesy zerohedge)

China Tests Hypersonic Weapon, Rendering US THAAD Powerless

The art of (future) war is rapidly evolving with Beijing spearheading the push into the first modern operational hypersonic glide vehicle (HGV). According to The Diplomat, the weapon, known as the Dong Feng (“East Wind”), DF-17 for short, is designed to challenge existing missile defense systems, such as America’s anti-ballistic missile defense system called: Terminal High Altitude Area Defense (THAAD).

An unnamed U.S. government source, who has studied recent intelligence reports on the People’s Liberation Army Rocket Force (PLARF), said China conducted two separate tests of the hypersonic missile back in November. The first test was conducted on November 01 and the second test took place on November 15. The Diplomat signals, that the November 01 test was the first Chinese ballistic missile launch to take place after the Communist Party of China’s 19th Party Congress in October.

Following half-dozen development tests between 2014-2016, the most recent tests were launched from the Jiuquan Space Launcher Center in Inner Mongolia. The Diplomat then explains that the November 01 test was widely viewed as successful after the hypersonic weapon hit its intended target “within meters.”

During the November 1 test flight, which took place from the Jiuquan Space Launcher Center in Inner Mongolia, the missile’s payload flew to a range of approximately 1,400 kilometers with the HGV flying at a depressed altitude of around 60 kilometers following the completion of the DF-17’s ballistic and reentry phases.

HGVs begin flight after separating from their ballistic missile boosters, which follow a standard ballistic trajectory to give the payload vehicle sufficient altitude.

Parts of the U.S. intelligence community assess that the DF-17 is a medium-range system, with a range capability between 1,800 and 2,500 kilometers. The missile is expected to be capable of delivering both nuclear and conventional payloads and may be capable of being configured to deliver a maneuverable reentry vehicle instead of an HGV.

Most of the missile’s flight time during the November 1 flight test was powered by the HGV during the glide phase, the source said. The missile successfully made impact at a site in Xinjiang Province, outside Qiemo, “within meters” of the intended target, the source added. The duration of the HGV’s flight was nearly 11 minutes during that test.

The source told The Diplomat, this was “the first HGV test in the world using a system intended to be fielded operationally.” U.S. intelligence assessments indicate the DF-17 could be operational as soon as 2020.

China just showed its hypersonic-BGV in a vid on 08 Oct. Probably a test design model, but AFAIK this is first pics of an actual object 1/

“Although hypersonic glide vehicles and missiles flying non-ballistic trajectories were first proposed as far back as World War II, technological advances are only now making these systems practicable,” Vice Admiral James Syring, director of the U.S. Missile Defense Agency, said in June, during a testimony before the U.S. House Armed Services Committee.

In 2015, Lockheed Martin, well aware of China’s HGV threat, dusted off their plans to upgrade its THAAD missile system to counter hypersonic weapons.

Lockheed Martin is hoping the maturing threat of hypersonic boost glide vehicles from ambitious adversaries will spark interest in the company’s dormant plan to design a more capable interceptor for the Terminal High-Altitude Area Defense (Thaad) air defense system.

Chinese officials confirmed they conducted a test last month of what they are calling a hypersonic strike vehicle. U.S. officials worry this missile could outsmart their defenses.

That said, China is not the only superpower in the HGV game, the United States and Russia are developing hypersonic weapons, as well.

And lastly, the Rand Corporation warns, “the trajectory and capabilities of HGVs provide them with some unprecedented attributes that may be disruptive to current military doctrines of advanced nations.”

4. EUROPEAN AFFAIRS

Italy’s President Dissolves Parliament: “The Current Situation Is One That Fuels Populism”

Authored by Mike Shedlock via www.themaven.net/mishtalk,

The Wall Street Journal reports Italy’s President Calls National Elections as Country Grapples With Economic Pain.

The Wall Street Journal reports Italy’s President Calls National Elections as Country Grapples With Economic Pain.Italy’s President Sergio Mattarella dissolved parliament Thursday and called elections for early March, a vote that will highlight the economic and political problems still stalking Europe and the country’s role as the weakest flank in the currency union.

The vote—the latest in a series of momentous elections in Europe—will be in line with the overwhelming trends of 2017, featuring a fractured electorate, continued pressure from populist movements and predictions of a struggle to form a cohesive government.

Its economy is 6% smaller than at the start of 2008, making it the only G-7 economy not to have returned to its pre-crisis size.

In a speech a decade ago as head of Italy’s industry association, Luca di Montezemolo, former chairman of Fiat SpA, listed 10 urgent reforms Italian businesses wanted from the government, including a leaner bureaucracy and lower taxes. “I could give that same speech today,” he said in an interview.

The downturn has left deep scars in Italy’s social fabric. More than 4.7 million Italians live in absolute poverty, nearly double the number a decade ago, according to Italian statistical agency Istat.

With youth unemployment at 35%, an entire generation of young people remains jobless or subsists on poorly paid, short-term contracts. Even as the brain drain that has afflicted much of southern Europe begins to ebb, thousands of Italian university graduates continue to emigrate each year.

With no group likely to reach a majority, a hung parliament is highly probable. Lorenzo Codogno, former director general of the Italian Treasury Ministry, assigns a 75% probability to such an outcome.

Return of Silvio Berlusconi

The current situation is one that fuels populism. Support for Matteo Renzi’s party has collapsed.

However, Renzi and former prime minister Silvio Berlusconi conspired to change the rules for the specific purpose of blocking Beppe Grillo’s Five Star movement.

The elections could have been called earlier but they were purposely delayed to benefit Berlusconialthough the 4-time prime minister still cannot become prime minister again himself due to a tax fraud conviction.

Eurosceptic?

Previously, Berlusconi was viewed as a Eurosceptic, but his tune comes and goes with the wind. Currently, the Five Star movement is the only party pushing hard to have a decisive vote on Eurozone membership.

Regardless, Italy has had corrupt governments after corrupt governments. It’s rules and regulations are hugely problematic.

Economic Freedoms

Italy and France are not ranked highly in terms of economic freedom. For details, please see Economic Freedom: Best and Worst Countries, US Timeline History .

Don’t expect the next election to solve any economic problems.

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

The USA and Israel reach a “secret plan” on how to contain Iran

(courtesy zerohedge)

US And Israel Reach “Secret Plan” To Counter Iran

One month after we reported that Israel would take the unprecedented step of sharing intelligence with Saudi Arabia as the two countries ramped up efforts to curb what they perceive as “Iranian expansion” in the region, on Thursday Israel’s Channel 10 reported that Israel has also pivoted to the US and reached a similar plan to counter Iranian activity in the Middle East. As Axios adds, U.S. and Israeli officials said the joint understandings were reached in “a secret meeting” between senior Israeli and U.S. delegations at the White House on December 12th.

Speaking to Axios, a senior U.S. official said that after two days of talks the U.S. and Israel “reached at a joint document which included understandings on countering Iranian actions in the region.”

The U.S. official said the document goal’s was to translate President Trump’s Iran speech to joint U.S.-Israeli strategic goals regarding Iran and to set up a joint work plan.

On the Israeli side, the team was headed by national security adviser Meir Ben-Shabbat and included senior representatives of the Israeli military, including the Ministry of Defense, Foreign Ministry and intelligence community. The U.S. side was headed by national security adviser H.R. McMaster and included senior representatives from the National Security Council, State Department, Department of Defense and the intelligence community.

- Covert and diplomatic action to block Iran’s path to nuclear weapons – according to the U.S. official this working group will deal with diplomatic steps that can be taken as part of the Iran nuclear deal to further monitor and verify that Iran is not violating the deal. It also includes diplomatic steps outside of the nuclear deal to put more pressure on Iran. The working group will deal with possible covert steps against the Iranian nuclear program.

- Countering Iranian activity in the region, especially the Iranian entrenchment efforts in Syria and the Iranian support for Hezbollah and other terror groups. This working group will also deal with drafting U.S.-Israeli policy regarding the “day after” in the Syrian civil war.

- Countering Iranian ballistic missiles development and the Iranian “precision project” aimed at manufacturing precision guided missiles in Syria and Lebanon for Hezbollah to be used against Israel in a future war.

- Joint U.S.-Israeli preparation for different escalation scenarios in the region concerning Iran, Syria, Hezbollah in Lebanon and Hamas in Gaza.

After the (not so) “secret” meetings, senior Israeli officials confirmed the U.S. and Israel have arrived at strategic understandings regarding Iran that would strengthen the cooperation in countering regional challenges. The Israeli official added that “[T]he U.S. and Israel see eye to eye the different developments in the region and especially those that are connected to Iran. We reached at understandings regarding the strategy and the policy needed to counter Iran. Our understandings deal with the overall strategy but also with concrete goals, way of action and the means which need to be used to get obtain those goals.”

Meanwhile, apparently unconcerned by the Saudi-Israeli-US axis that has formed to contain his nation, Iranian Supreme Leader Ayatollah Ali Khamenei said on Wednesday that US President Donald Trump would fail in his hardened stance towards Iran, saying Tehran is stronger than during the time of Ronald Reagan.

“Reagan was more powerful and smarter than Trump, and he was a better actor in making threats, and he also moved against us and they shot down our plane,” Khamenei said in a speech carried on state television.

For now, the Iranian’s Trump-tautning has remained unanswered. The problem is that if Iran continues to dare the US, and its new regional allies Israel and Saudi Arabia, now that there is a regional axis meant to “contain” Iran by any means necessary, it won’t take much for the US, and especially Israel, to respond accordingly.

Rare Anti-Government Protests Grow In Iran, Reports Of Jammed Satellite TV Networks

Rare protests in multiple cities across Iran, especially in the country’s second largest city of Mashhad, gained momentum on Thursday and Western media and pundits are beginning to take note. Though it appears the main protest locations have been consistently described as being in the hundreds and not yet reaching mass numbers, observers say they are likely to grow in size and in intensity as economic grievances over high prices, corruption, and mismanagement have reached a boiling point.

The largest and most covered protests were held in Mashhad on Thursday. Map via World Atlas

Notably, dozens of videos were uploaded to social media channels Thursday showing demonstrators primarily in Mashhad in northwest Iran chanting “death to [President] Rouhani” and “death to the dictator”. Mashhad is considered one of the holiest and most conservative places in Shia Islam, causing some pundits to conclude that if such aggressive anti-government demonstrations can take place there, they could take place anywhere throughout Iran. Other places named by the semi-official ILNA news agency and social media reports where demonstrations have occurred are in Razavi Khorasan Province, including Neyshabour and Kashmar.

And there are some indications that authorities in Tehran are preparing for a broader crackdown to prevent protests from spreading. Though unconfirmed, Carl Bildt, the co-chair for the European Council on Foreign Relations cited on Thursday afternoon “Reports of signals of international satellite TV networks jammed in large cities of Iran. Would be sign of regime fear of today’s protests spreading.” And well-known opposition outlets further reported that over 100 protesters were arrested in Mashhad.

این ویدئو را یکی از مخاطبان از تجمع اعتراضی امروز مردم در #مشهد فرستاده. فرماندار مشهد تظاهرات و تجمع اعتراضی امروز در این شهر را غیرقانونی خوانده و گفته است که نیروی انتظامی با تجمعکنندگان “بسیار با مدارا” برخورد کرده است.

Ground footage of Thursday’s protests in Mashad, northeast Iran.

Incredible! Huge anti-regime protest in #Mashad#Iranhttps://www.youtube.com/watch?v=K4xOG5tpd3w&sns=tw … via @youtube

Mass protest in #Mashad#Iran calling for the death of the dictator Rouhani https://www.youtube.com/watch?v=RzUpuzuX1C0&sns=tw … via @youtube

Though Iranian president Rouhani’s signature achievement – the 2015 nuclear deal brokered with the United States and other world powers – resulted in the lifting of most international sanctions in early 2016, this has yet to bring the broad economic benefits the government had promised was coming.

A Reuters summary of the dire economic situation nationwide is as follows:

Unemployment stood at 12.4 percent in this fiscal year, according to the Statistical Centre of Iran, up 1.4 percent from the previous year. About 3.2 million Iranians are jobless, out of a total population of 80 million. Mashad governor Mohammad Rahim Norouzian was quoted by the semi-official ISNA news agency as saying that “the demonstration was illegal but the police dealt with people with tolerance”.

He said a number of protesters were arrested for “trying to damage public property”. Videos posted on social media showed riot police used water cannon and tear gas to disperse crowds.

Norouzian was quoted as saying by state news agency IRNA that the protests were organized by “enemies of the Islamic Republic” and “counter-revolutionaries”.