Glad to be back as I was in Israel over the holidays.

I will resume my normal detailed commentary

GOLD: $1319.50 DOWN $1.40

Silver: $17.12 DOWN 11 cents

Closing access prices:

Gold $1320.50

silver: $17.11

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1323.92 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1320.00

PREMIUM FIRST FIX: $3.92

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1323.92

NY GOLD PRICE AT THE EXACT SAME TIME: $1318.25

Premium of Shanghai 2nd fix/NY:$5.67

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1380.80

NY PRICING AT THE EXACT SAME TIME: $1318.75

LONDON SECOND GOLD FIX 10 AM: $1268.85

NY PRICING AT THE EXACT SAME TIME. 1268.50??

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR: 242 FOR 24200 OZ (0.7527 TONNES),

For silver:

jANUARY

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 507 for 2,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $15,392/OFFER $15,512 DOWN $1155 (morning)

Bitcoin: BID 14,763/OFFER $14,871 DOWN $1800(CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY TINY 165 contracts from 194,264 RISING TO 194,429 WITH FRIDAY’S TINY 4 CENT RISE IN SILVER PRICING. WE HAD ZERO COMEX LIQUIDATION BUT WITHOUT A DOUBT WE WITNESSED ANOTHER MAJOR BANK SHORT- COVERING OPERATION. NOT ONLY THAT , WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: A CONSIDERABLE 1721 EFP’S FOR MARCH (AND ZERO FOR OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 1721 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1721 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED EFP’S FOR SILVER ISSUED. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. I BELIEVE THAT WE MUST HAVE HAD SOME MAJOR BANKER SHORT COVERING AGAIN TODAY.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

17,931 CONTRACTS (FOR 6 TRADING DAYS TOTAL 17,931 CONTRACTS OR 89.66 MILLION OZ: AVERAGE PER DAY: 2988 CONTRACTS OR 14.94 MILLION OZ/DAY)

RESULT: A SMALL SIZED GAIN IN OI COMEX DESPITE THE TINY 4 CENT RISE IN SILVER PRICE WHICH USUALLY INDICATES HUGE BANKER SHORT-COVERING. WE ALSO HAD A FAIR SIZED EFP ISSUANCE OF 1721 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. FROM THE CME DATA 1721 EFP’S WERE ISSUED FOR TODAY (FOR MARCH EFP’S AND NONE FOR ALL OTHER MONTHS) FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 1886 OI CONTRACTS i.e. 1721 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 165 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE TINY RISE IN PRICE OF SILVER BY 4 CENTS AND A CLOSING PRICE OF $17.23 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.9720 BILLION TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest ROSE BY AN HUGE SIZED 9,128 CONTRACTS UP TO 551,441 WITH THE SMALL RISE IN PRICE OF GOLD WITH FRIDAY’S TRADING ($1.40). IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY AND IT TOTALED A GOOD SIZED 6115 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 6115 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS. The new OI for the gold complex rests at 551,441. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE ANOTHER HUMONGOUS GAIN OF 15,243 OI CONTRACTS: 9.128 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 6115 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

FRIDAY, WE HAD 17,213 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 57,605 CONTRACTS OR 5.760 MILLION OZ OR 179.16 TONNES (6 TRADING DAYS AND THUS AVERAGING: 9,600.8 EFP CONTRACTS PER TRADING DAY OR 960,000 OZ/DAY)

Result: A STRONG SIZED INCREASE IN OI WITH THE SMALL SIZED RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($1.40). WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6115. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6115 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 15,243 contracts:

6115 CONTRACTS MOVE TO LONDON AND 9128 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 47.40 TONNES)

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD: with gold up for 11 consecutive days, we still have no changes in gold inventory

Today, with gold down a tiny $1.40 after rising for 12 straight days, gold inventory declines by a huge 1.44 tonnes today/

Inventory rests tonight: 834.86 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

INVENTORY RESTS AT 318.423 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A SMALL 165 contracts from 194,264 UP TO 194,429 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY RISE IN PRICE OF SILVER TO THE TUNE OF 4 CENTS ON FRIDAY. WE HAD WITHOUT A DOUBT ANOTHER MAJOR SHORT COVERING FROM OUR BANKERS AS THEY HAVE CAPITULATED. NOT ONLY THAT BUT OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1721 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD NO COMEX SILVER COMEX LIQUIDATION. BUT, IF WE TAKE THE SMALL OI GAIN AT THE COMEX OF 165 CONTRACTS TO THE 1721 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 1886 OPEN INTEREST CONTRACTS DESPITE THE MAJOR BANKER SHORT COVERING. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ: 9.43 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE TINY SIZED RISE OF 4 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1721 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 17.73 points or 0.53% /Hang Sang CLOSED UP 84.89 pts or 0.28% / The Nikkei closed UP 208.20 POINTS OR 0.89%/Australia’s all ordinaires CLOSED UP 0.11%/Chinese yuan (ONSHORE) closed UP at 6.4974/Oil UP to 61.90 dollars per barrel for WTI and 67.85 for Brent. Stocks in Europe OPENED MOSTLY GREEN. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4974. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4943 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS HAPPY TODAY.(GOOD MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

Huge crypto carnage as the South Korean government launches a probe into their use

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

The end of QE in Europe will cause peripheral bonds to collapse in price (rise in yield)

( zerohedge)

ii)UK

UK Political cabinet shuffle:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Eleven more Saudi royals have been arrested for protesting against MBS’s austerity measures

( zerohedge)

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

Venezuela

Chaos in Caracas as mobs surround shops after a government mandated price cuts,

( zerohedge)

9. PHYSICAL MARKETS

i)Eric Sprott comments on my work (and Ronan Manly/Koos Jansen) in the extra-ordinary use of ERFP’s (exchange for physicals). Sprott suggests (as do I) that there is little metal available for delivery in New York. His final comment is worth noting: “Maybe the whole fraud at the comex is unwinding”

( Eric Sprott/Craig Hemke/Harvey Organ/Koos Jansen/Ron Manly)

ii)Ed Steer comments on the latest COT report. However he does not address the huge EFP transfers which distorts this report greatly

( Ed Steer/GATA)

iii)GATA is hosting another conference in March and a Hong Kong conference in April

( Chris Powell/GATA)

iv)This is how the major banks are going to cause a massive fall in Bitcoin pricing: they are already building up a huge short position in the futures markets

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)the White House is now asking for a down payment on the wall: 18 billion dollars to rebuild 700 miles

( zerohedge)

ii)It looks like it will be a battle in Congress over the next 2 weeks. The Democrats wants a permanent DACA ie. permanent status for illegal immigrants that were children when they arrived years ago vs the Republican wall

( zerohedge)

iii)SWAMP STORIES

a)The SEC is now probing Jared Kushner companies over the use of immigrant visa programs i.e. E. B. -5

( zerohedge)

b)As we reported to you on Friday, Fusion GPS did hand over all bank records after a Federal judge struck down the firm’s attempt to conceal the records form the Intelligence Committee. We will now learn first hand who financed the report

( zerohedge)

c)Wikileaks publishes the entire Michael Wolff book Fire and Fury as a PDF

( zerohedge)

iv) Stockman takes on Wall Street and the false narrative of a growing economy

( David Stockman/ContraCorner)

v)We have been harping on this for quite a while: the death spiral for shopping malls. The following suggests that many of the malls are in worse shape than many think

( zerohedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY HUGE 9128 CONTRACTS UP to an OI level of 553,240 WITH THE SMALL SIZED RISE IN THE PRICE OF GOLD ($1.40 GAIN WITH RESPECT TO FRIDAY’S TRADING). OBVIOUSLY WE HAD ZERO COMEX GOLD LIQUIDATION WITH ANOTHER STRONG GAIN IN TOTAL OPEN INTEREST AS WE WITNESSED ANOTHER HUMONGOUS COMEX TRANSFER THROUGH THE EFP ROUTE. THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 6115 EFP’S WERE ISSUED FOR FEBRUARY AND 0 EFP’s FOR APRIL: TOTAL 6115 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 15,243 OI CONTRACTS IN THAT 6115 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 9,128 COMEX CONTRACTS. NET GAIN: 15,243 contracts OR 1,524,300 OZ OR 47.409 TONNES

Result: A STRONG SIZED INCREASE IN COMEX OPEN INTEREST WITH THE SMALL RISE IN THE PRICE OF FRIDAY’S GOLD TRADING (1.40.) WE HAD NO GOLD LIQUIDATION ANYWHERE. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 15,243 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest FALL by 4 contracts DOWN to 179. We had 4 notices served on Friday so we GAINED 0 contracts or NIL additional oz of gold will stand in this non active month

FEBRUARY saw a GAIN of 869 contacts UP to 371,302. March saw a gain of 34 contracts up to 101. April saw a GAIN of 7,257 contracts UP to 83,725.

We had 0 notice(s) filed upon today for NIL oz

PRELIMINARY VOLUME TODAY ESTIMATED; 329,333

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 412,858

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY 165 CONTRACTS FROM 194,264 UP TO 194,429 DESPITE YESTERDAY’S TINY 4 CENT RISE AGAIN WE MUST HAVE HAD SOME BANKER SHORT COVERING. NOT ONLY THAT, WE HAD ANOTHER GOOD SIZED 1721 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1721. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD ZERO LONG COMEX SILVER LIQUIDATION BUT A RISE IN TOTAL SILVER OI AS IT SEEMS THAT WE ARE WITNESSING SOME MAJOR BANKER SHORT-COVERING. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE GAINED 1886 OPEN INTEREST CONTRACTS:

165 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1721 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN: 1886 CONTRACTS

We are now in the poor non active delivery month of January and here the OI LOSS by 2 contracts DOWN to 39. We had 2 notices served upon yesterday, so we GAINED 0 contracts or an additional NIL oz will stand for delivery

February saw a GAIN OF 0 OI contracts REMAINING AT 182. The March contract LOST 1424 contracts DOWN to 149,964.

We had 0 notice(s) filed for NIL oz for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 8/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

179 contracts

(17,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

242 notices

24200 oz

0.7527 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (242) x 100 oz or 24200 oz, to which we add the difference between the open interest for the front month of JAN. (179 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 42,100 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (242 x 100 oz or ounces + {(179)OI for the front month minus the number of notices served upon today (0 x 100 oz which equals 42,100 oz standing in this active delivery month of JANUARY (1.303 tonnes). THERE IS 33.29 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 568,449.373 oz or 17.681 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,243,329.256 or 287/22 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 67 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(10,000 OZ)

|

| No of oz to be served (notices) |

39 contract

(195,000 oz)

|

| Total monthly oz silver served (contracts) | 509 contracts

(2,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement: nil oz

we had no inventory movement at the customer side of things

total inventory movement; nil

total dealer silver: 45.466 million

total dealer + customer silver: 245.527 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 0 contract(s) FOR 10,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 507 x 5,000 oz = 2,535,000 oz to which we add the difference between the open interest for the front month of JAN. (39) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 507(notices served so far)x 5000 oz + OI for front month of JANUARY(39) -number of notices served upon today (0)x 5000 oz equals 2,730,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3,790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 81.496

CONFIRMED VOLUME FOR FRIDAY: 92.059 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 92,059 CONTRACTS EQUATES TO 460 MILLION OZ OR 65.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 59.182 million

Total number of dealer and customer silver: 240.232 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.5 percent to NAV usa funds and Negative 2.5% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.8%

Percentage of fund in silver:37.0%

cash .+.2%( Jan 8/2018)

2. Sprott silver fund (PSLV): NAV RISES TO -1.15% (Jan 5/2018)??????????????????????????????

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.58% to NAV (Jan 45/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.15%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.58%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 8/2018/ Inventory rests tonight at 836.32 tonnes

*IN LAST 306 TRADING DAYS: 106.09 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 241 TRADING DAYS: A NET 51.22 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 210.31TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 8/2017:

Inventory 318,423 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.69%

12 Month MM GOFO

+ 1.95%

30 day trend

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

10 Reasons Why You Should Add To Your Gold Holdings

10 Reasons Why You Should Add To Your Gold Holdings

– Gold currently undervalued

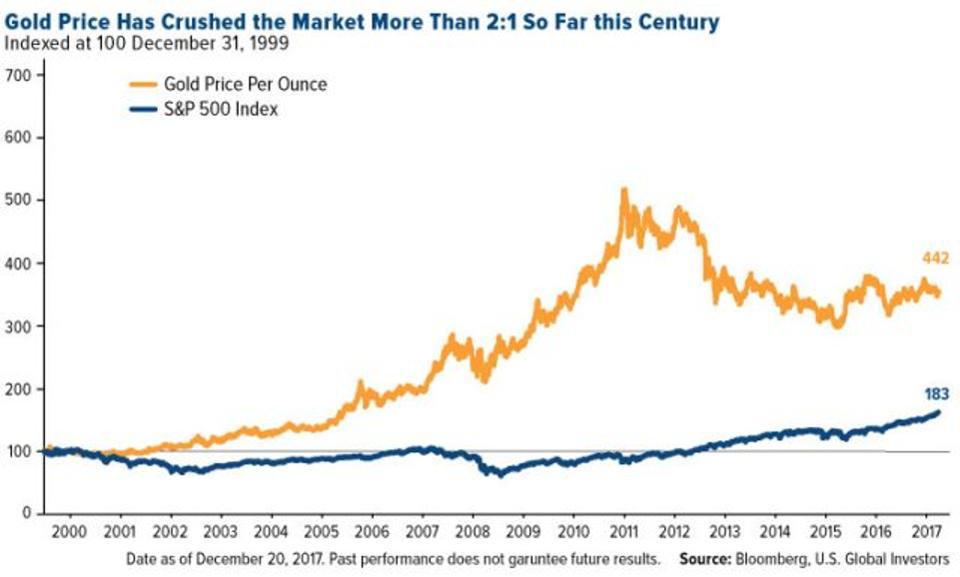

– Since 2000, the gold price has beaten the S&P 500 Index

– A ‘a once-in-a-decade opportunity’ as gold-to-S&P 500 ratio is at its lowest point in 10 years.

– Reached ‘peak gold’ as exploration budgets continue to tighten

– $80 trillion sits in global equities, a ‘ticking time bomb’

– Gold remains an appealing diversifier in the current environment of high valuations and uncertainties

by Frank Holmes via Forbes.com

It’s important to remember that the precious metal has historically shared a low-to-negative correlation with many traditional assets such as cash, Treasuries and stocks, both domestic and international. This makes it, I believe, an appealing diversifier in the event of a correction in the capital and forex markets.

Need more reasons to add to your gold holdings? Below are 10 charts that show why the yellow metal is undervalued right now:1. The gold price has crushed the market so far this century.Investors are invariably surprised to see the top chart whenever I show it at conferences. Believe it or not, since 2000, the gold price has beaten the S&P 500 Index, which has undergone two 40 percent corrections so far this century.2. Compared to stocks, gold looks like a bargain.

As of this month, the gold-to-S&P 500 ratio is at its lowest point in 10 years. For mean reversion to occur, either the gold price needs to appreciate or share prices need to fall. Either way, consider this a once-in-a-decade opportunity.

3. Exploration budgets keep getting slashed.

One of the reasons why gold is so highly valued is for its scarcity. There’s a possibility it could get even scarcer as explorers continue to trim exploration budgets and uncover fewer and fewer large deposits. The time between initial discovery and day one of production is also expanding. This has led many experts in the field to wonder if we’ve finally reached “peak gold.”

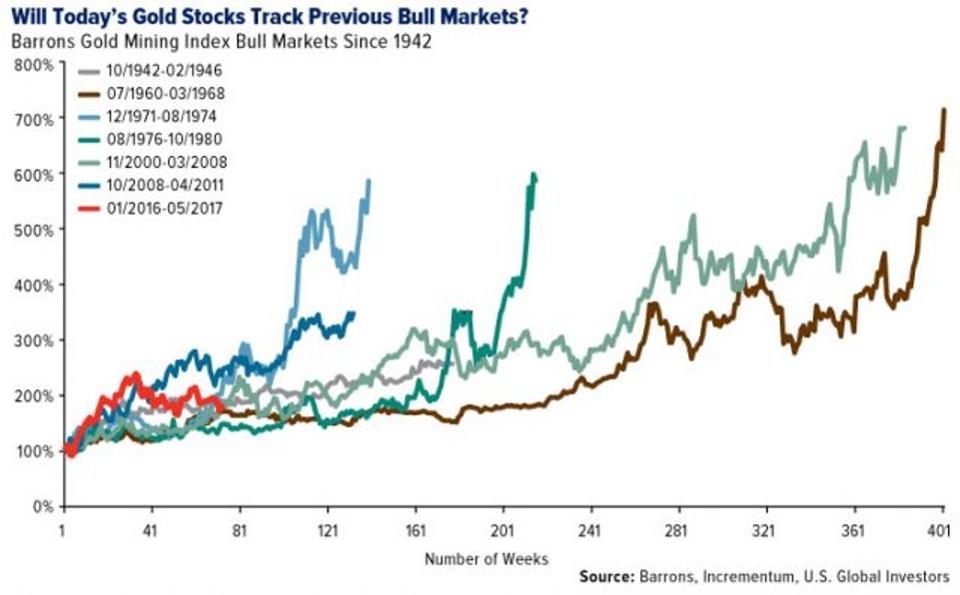

4. Gold stocks could be just getting started.

Last year marked a turnaround in gold prices and gold stocks, and according to analysts at Incrementum Capital Partners, a Swiss financial management firm, they’re just getting warmed up.When charted against past gold bull markets, the present one looks as if it still has a lot of room to run.

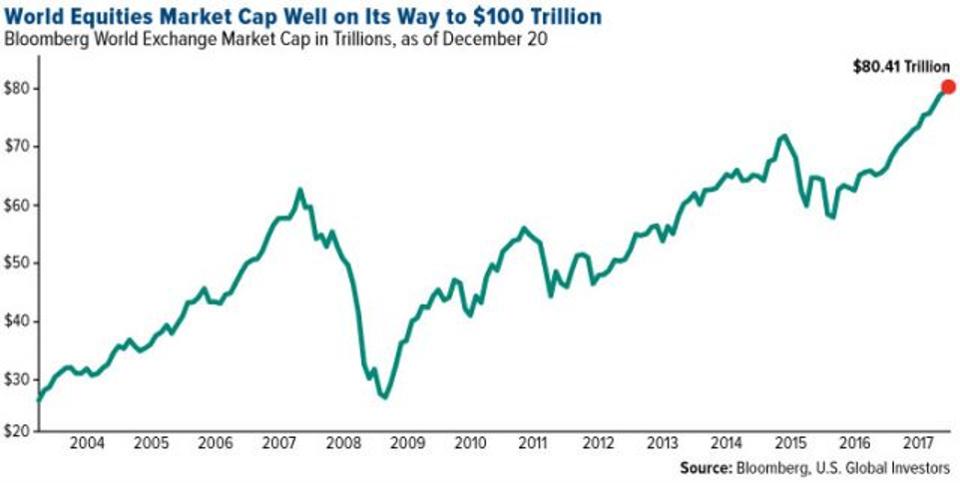

5. Is too much money going into equities?

More than $80 trillion sits in global equities right now, a monumental sum that’s likely to surge even more as we venture further into the bull market. Some worry this is a ticking time bomb just waiting to go off. Another correction similar to the one 10 years ago would wipe out trillions of dollars around the world, and it’s then that the investment case for gold would become strongest.

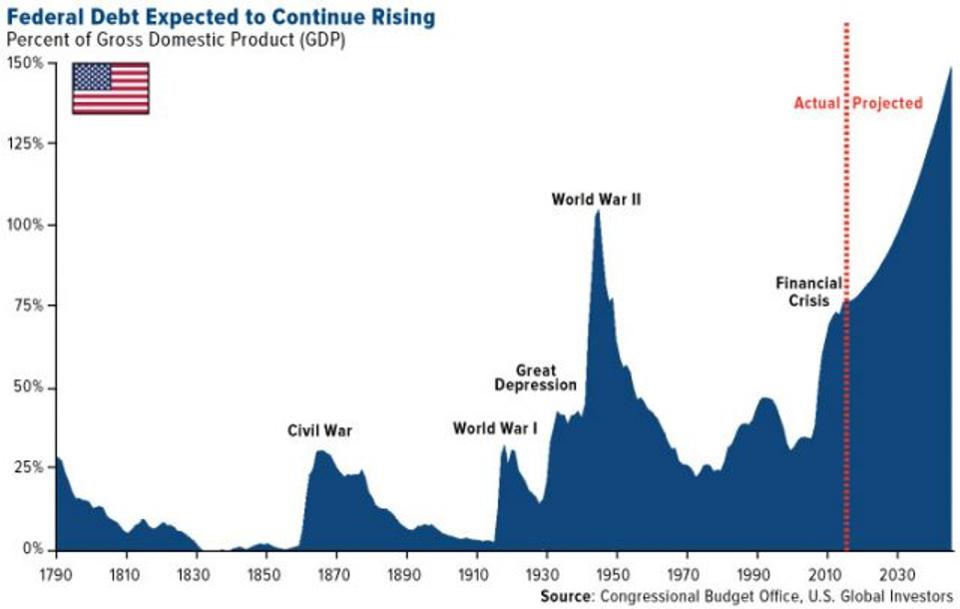

6. Higher debt could mean higher gold prices.

The yellow metal has historically tracked global debt, which stood at $217 trillion as of the first quarter of this year. Looking just at the U.S., debt is expected to continue on an upward trend, driven not just by new, and largely unfunded, spending but also underlying interest. By most estimates, President Donald Trump’s historic tax cuts, although welcome, will contribute to even higher debt as a percent of gross domestic product (GDP).

7. The Fed’s about to take away the punch bowl.

“My opinion is that business cycles don’t just end accidentally. They end by the Fed. If the Fed tightens enough to induce a recession, that’s the end of the business cycle.” That’s according to MKM Partners’ chief economist Mike Darda, who was referring to the Federal Reserve’s efforts to unwind its $4.5 trillion balance sheet after it bought vast quantities of government bonds and mortgage-backed securities to mitigate the effects of the Great Recession. There’s definitely a huge amount of risk here: Five of the previous six times the Fed has similarly reduced its balance sheet, between 1921 and 2000, ended in recession.

8. Rate hike cycles have rarely ended well.

Rate hike cycles also have a mixed record. According to Incrementum research, only three such cycles in the past 100 years have not ended in a recession. Obviously there’s no guarantee that this particular round of tightening will have the same outcome, but if you recognize the risk here, it might be prudent to have as much as 10 percent of your wealth in gold bullion and gold stocks.

9. Trillions of dollars of global bonds are guaranteed to lose money right now.

As of May of this year, nearly $10 trillion of bonds around the world were guaranteed to cost investors money, as more and more central banks instituted negative interest rate policies (NIRPs) to spur consumer spending. Instead, it encouraged many savers to yank their cash out of banks and convert it into gold. That’s precisely what households in Germany did, and by 2016, the European country became the world’s biggest investor in the yellow metal.

10. The Love Trade is still driving gold demand.

The chart above, based on data provided by Moore Research, shows gold’s 30-year seasonal trading pattern. Although it’s changed over the past few years, the pattern reflects the Love Trade in practice. According to the data, the gold price rallies early in the year as we approach the Chinese New Year, then dips in the summer. After that it surges on massive gold-buying in India during Diwali, in late October and early November. Finally, it ends the year at its highest point during the Indian wedding season, when demand is high. The pattern isn’t always observed exactly how I described, but it happens frequently enough for us to make educated, informed decisions on when to trade the precious metal.

This post was published here.

Related reading

Gold Has Longest Winning Streak Since 2011

Gold Has Best Year Since 2010 With Near 14% Gain In 2017

98,750,067,000,000 Reasons to Buy Gold in 2018

LISTEN: What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

News and Commentary

Gold prices firm amid higher U.S. rate hike environment (Reuters.com)

Asia Stocks Rise as Earnings Awaited, Won Weakens (Bloomberg.com)

Will 2018 mirror 2011 as a landmark year for precious metals? (TheNational.ae)

7 reasons why investors should go for gold in 2018 (MarketWatch.com)

Japan’s Abe urges central bank’s Kuroda to keep up efforts on economy (Reuters.com)

Source: Frank Holmes

Bombay Stock Exchange plans oil and gold futures (IndiaTimes.com)

Eric Sprott: Maybe the whole fraud of the Comex is unwinding (SprottMoney.com)

Why Trump Is Probably to Blame for the Weak Dollar (Bloomberg.com)

U.K. Consumer Pullback Sees Worst Year for Spending Since 2012 (Bloomberg.com)

Ghost of Weimar Looms Over German Politics (Bloomberg.com)

Gold Prices (LBMA AM)

08 Jan: USD 1,318.80, GBP 974.33 & EUR 1,099.09 per ounce

05 Jan: USD 1,317.90, GBP 973.40 & EUR 1,094.25 per ounce

04 Jan: USD 1,313.70, GBP 969.77 & EUR 1,090.24 per ounce

03 Jan: USD 1,314.60, GBP 968.20 & EUR 1,092.96 per ounce

02 Jan: USD 1,312.80, GBP 968.85 & EUR 1,087.52 per ounce

29 Dec: USD 1,296.50, GBP 960.84 & EUR 1,082.45 per ounce

28 Dec: USD 1,291.60, GBP 960.43 & EUR 1,082.75 per ounce

Silver Prices (LBMA)

08 Jan: USD 17.17, GBP 12.68 & EUR 14.33 per ounce

05 Jan: USD 17.15, GBP 12.66 & EUR 14.24 per ounce

04 Jan: USD 17.13, GBP 12.64 & EUR 14.20 per ounce

03 Jan: USD 17.12, GBP 12.63 & EUR 14.25 per ounce

02 Jan: USD 17.06, GBP 12.59 & EUR 14.15 per ounce

29 Dec: USD 16.87, GBP 12.48 & EUR 14.07 per ounce

28 Dec: USD 16.74, GBP 12.46 & EUR 14.02 per ounce

Recent Market Updates

– Spectre, Meltdown Highlight Online Banking and Digital Gold Risks

– Palladium Prices Surge To New Record High Over $1,100 On Supply Crunch Concerns

– Gold Has Best Year Since 2010 With Near 14% Gain In 2017

– Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

– 98,750,067,000,000 Reasons to Buy Gold in 2018

– Gold, Bitcoin and the Blockchain Replaces the Banks – Realists Guide To The Future

– It’s A Wonderful Life Is A Wonderful Lesson To Hold Gold Outside of The Banking System

– Goldnomics Podcast – Gold, Stocks, Bitcoin in 2018. Everything Bubble Bursts?

– What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

– New Rules For Cross-Border Cash and Gold Bullion Movements

– ‘Gold Strengthens Public Confidence In The Central Bank’ – Bundesbank

– WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors

– Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

end

Eric Sprott comments on my work (and Ronan Manly/Koos Jansen) in the extra-ordinary use of ERFP’s (exchange for physicals). Sprott suggests (as do I) that there is little metal available for delivery in New York. His final comment is worth noting: “Maybe the whole fraud at the comex is unwinding”

(courtesy Eric Sprott/Craig Hemke/Harvey Organ/Koos Jansen/Ron Manly)

Eric Sprott: Maybe the whole fraud of the Comex is unwinding

Submitted by cpowell on Fri, 2018-01-05 20:11. Section: Daily Dispatches

3:12p ET Friday, January 5, 2018

Dear Friend of GATA and Gold:

Weakness in the U.S. dollar is pushing gold and silver up along with commodities generally, mining entrepreneur Eric Sprott tells interviewer Craig Hemke in the weekly wrapup for Sprott Money News.

Citing the work of gold researchers Harvey Organ and Ronan Manly, Sprott and Hemke also discuss the extraordinary increase in the use of the “exchange for physicals” procedure for clearing gold and silver contracts on the New York Commodities Exchange, which suggests that little metal is available for delivery in New York. “Maybe the whole fraud of the Comex is unwinding,” Sprott says.

We can only hope.

The interview is 12 minutes long and can be heard at the Sprott Money internet site here:

https://www.sprottmoney.com/Blog/maybe-the-whole-fraud-of-the-comex-is-u…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Ed Steer comments on the latest COT report. However he does not address the huge EFP transfers which distorts this report greatly

(courtesy Ed Steer/GATA)

Ed Steer’s Gold & Silver Digest: Another unhappy COT report

Submitted by cpowell on Sun, 2018-01-07 23:50. Section: Daily Dispatches

8p ET Sunday, January 7, 2018

Dear Friend of GATA and Gold:

GATA board member Ed Steer’s Gold & Silver Digest letter for Saturday, headlined “Another Unhappy COT Report,” is posted in the clear at GoldSeek here:

http://news.goldseek.com/GoldSeek/1515360227.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

GATA is hosting another conference in March and a Hong Kong conference in April

(courtesy Chris Powell/GATA)

Join GATA at Singapore conference in March and Hong Kong conference in April

Submitted by cpowell on Mon, 2018-01-08 01:37. Section: Daily Dispatches

8:40p ET Sunday, January 7, 2018

Dear Friend of GATA and Gold:

Your secretary/treasurer will make presentations again at this year’s Mining Investment Asia conference in Singapore, to be held Monday through Wednesday, March 26-28, and the Mines and Money Asia conference in Hong Kong, to be held Tuesday through Friday, April 3-6.

Among the speakers at the Mining Investment Asia conference in Singapore will be:

— Ronald-Peter Stoferle, managing partner of Incrementum AG in Liechtenstein, co-author of the annual “In Gold We Trust Report.”

— Thomas Puppendahl, managing partner of Cartesian Royalty Holdings in Singapore

Jayant Bhandari, mining and minerals expert for Anarcho Capital.

— And mining industry leaders, investment company representatives, and government officials from around the world.

Mining Investment Asia will be held at the Marina Bay Sands hotel and conference center. To learn more about the conference and to register, visit:

https://www.mininginvestmentasia.com/

Speakers at the Mines and Money Asia conference will include:

— Frank Holmes, chief executive officer of U.S. Global Investors.

— Grant Williams of the Things That Makes You Go Hmmm letter and Real Vision.

— Jayant Bhandari, mining and minerals expert for Anarcho Capital.

— Juerg Kiener of Swiss Asia Capital in Singapore.

— Mining entrepreneur and geologist Keith Barron.

— Rick Rule of Sprott U.S. Holdings.

— Mining entrepreneur Robert Friedland.

— Thomas Puppendahl, managing partner of Cartesian Royalty Holdings in Singapore.

— And mining industry leaders, investment company representatives, and government officials from around the world.

The Mines and Money Asia conference will be held at the Hong Kong Convention and Exhibition Centre. To learn more about the conference and to register, visit:

https://asia.minesandmoney.com/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This is how the major banks are going to cause a massive fall in Bitcoin pricing: they are already building up a huge short position in the futures markets

(courtesy zerohedge)

Bitcoin Futures Traders Are Quietly Building A Big Short Position

In retrospect, the launch of bitcoin futures one month ago has proven to be a modestly disappointing event: while it helped send the price of bitcoin soaring as traders braced for the institutionalization of bitcoin, the world’s most popular cryptocurrency has stagnated since the beginning of December when first the Cboe then CME started trading bitcoin futures, trading in a range between $12,000 and $17,000.

And while bitcoin futures markets volumes have been lower than most had expected, the past 4 weeks have provided enough data to observe how volumes and open interest have evolved.

We discussed previously that Bitcoin futures were off to a slow start in the first week of trading, with volumes of CBOE Bitcoin futures averaging just around $40MM per day, despite intense media hype helping fuel heavy trading when both contracts launched, at least in the first hours of trading.

Since then, volumes spike briefly in the following week coinciding with the launch of the CME futures, with volumes of on both exchanges at relatively similar levels.

Then, as JPM’s Nikolaos Panagirtzoglou shows, after a spike in volumes to around $200mn on 22 December, which saw sharp swings in underlying Bitcoin prices, volumes have averaged around $50mn and $60mn per day on the CBOE and CME futures, respectively.

One month after their launch, futures trading volumes remain very modest compared to average Bitcoin trading volumes of around $15bn per day since futures contracts were launched according to coinmarketcap.com data. While open interest in both the CBOE and CME contracts has risen steadily, it too remains rather modest at around $60mn and $70mn, respectively.

Putting futures volumes in context, on Friday, the combined size of the bitcoin-futures markets at the two exchanges was roughly $150 million, measured in terms of the value of outstanding contracts, while the total value of all bitcoins in existence was around $290 billion.

Another factor behind the slow volume growth may be the reluctance of many Wall Street banks to touch bitcoin futures. Firms such as JPMorgan Chase & Co. and Bank of America Merrill Lynch haven’t offered their clients access to bitcoin futures.

Another notable observation: with both volumes and open interest between the two sets of futures contracts converging, it suggests that a large degree of arbitraging of price differentials has taken place between the contracts which initially showed significant divergence. As JPM further notes, when trading in the CBOE futures initially started, a striking feature was the wide basis between the futures contract and the underlying bitcoin prices, which intraday exceeded $2000 or more than 12% of the underlying price at the time. While traders provided numerous explanation for the spread, since then the difference between futures prices on both the CBOE and CME contracts and underlying bitcoin prices has narrowed significantly (chart below), and even turned negative briefly last week.

That covers bitcoin futures volumes, but what about positioning? Well, as many traders expected, it appears that institutions are using the futures product to slowly but surely build a short position in bitcoin. According to the CFTC Commitment of Traders report (available CBOE futures), non-commercial traders held a net short position of around $30mn as of Tuesday Dec 26, or around half of the total open interest.

Separately, the Traders in Financial Futures breakdown provided by the CFTC show that the leveraged funds category that consists largely of hedge funds and various money managers had a short of around $14mn, or around a quarter of the total open interest.

In other words, spec investors have used the futures contracts to establish Bitcoin shorts.

How does this compare with other asset classes typically used as a store of wealth such as gold and silver? As JPMorgan explains, for gold futures, non-commercial investors held as of Dec 26 a net long position of around 30% of open interest, of which the managed money category held around 80%, while in silver futures both the non-commercial and managed money categories were close to zero.

* * *

An analysis by the Wall Street Journal confirms that while hedge funds and other large traders are betting that bitcoin will fall, small investors remain convinced that bitcoin prices will keep on rising.

As the WSJ reports, for traders who hold fewer than 25 of Cboe’s bitcoin futures contracts—a category that likely encompasses many retail investors—bullish bets are 3.6 times more common than bearish ones, according to the latest Commodity Futures Trading Commission data that cover trading through Tuesday.

Meanwhile, the big CBOE players in bitcoin futures tend to be short. For instance, among “other reportables”—large trading firms that don’t necessarily manage money for outside investors—short bets outweighed bullish “long” bets by a factor of 2.6 last week.

The historical data will probably not come as a big surprise: many skeptics on Wall Street have called bitcoin a bubble and would be more apt to bet on its decline. In a sign of how more conservative firms are keeping their distance, the CFTC data show near-zero trading in Cboe’s bitcoin futures by banks and asset managers.

“There is probably more optimism in the retail segment than there is in the institutional segment,” said Steven Sanders, an executive vice president at Interactive Brokers Group Inc., an electronic brokerage firm that offers its customers access to bitcoin futures.

And sure enough, presenting JPM’s data in a slightly different context, COT data shows that hedge funds and other money managers had placed almost 40% more short bets than long bets last week.

Curiously, it is worth noting that that represented a less bearish outlook than they had in late December, when such funds had more than four times as many short bets as long bets.

To be sure, shorting bitcoin futures doesn’t necessarily mean a trader expects bitcoin to crash. In a natural hedge, a cryptocurrency trading firm with significant holdings of bitcoin might go short to hedge those inventories against a price fall. That would make the firm indifferent as to whether bitcoin goes up or down.

As the WSJ further notes, shorting futs could also be part of certain sophisticated trading strategies, such as betting that rival cryptocurrencies will outperform bitcoin. One such rival, Ethereum, rose above $1,000 for the first time last week, more than double its value from the beginning of December.

With the CFTC data, “you’re not seeing the full picture,” said James Koutoulas, chief executive of hedge-fund firm Typhon Capital Management, which trades futures in bitcoin as well as commodities. Typhon has swung back and forth, being long and short bitcoin futures at various times, Mr. Koutoulas said.

Of course, it’s not just bitcoin.

As JPM writes, any given cryptocurrency faces competition from other cryptocurrencies, posing risks to their individual valuations. Indeed, the market capitalisation of Bitcoin has risen by around $100bn to around $270bn since late November, while other cryptocurrencies have seen a significant increase in market cap from around $130bn to nearly $500bn currently.

Other cryptocurrencies – mostly ethereum and ripple – have benefited from the increased interest in Bitcoin amid the listing of exchange traded futures, as well as the sharp rise in Bitcoin average transaction costs from around $6 per transaction in early December to nearly $60 per transaction on Dec 22, before settling in a $25-$30 range in recent days.

By contrast, average transaction fees in Ethereum reached a high of $1.50 in early December and were around $1 on Jan 4, while average transaction fees in Ripple measure a few cents according to bitinfocharts.com. The one-third share of Bitcoin of the total cryptocurrency market cap of around $770bn represents a new low. In contrast, the market of $770bn for the total cryptocurrency market represents a new high.

* * *

And while we await futures contracts to be announced on other cryptos, most likely ethereum and ripple next, events which we believe will be catalysts for substantial price upside in both cryptocurrencies, the question for bitcoin is who will be right: institutions, who are short, or retail investors (especially those in Japan and South Korea) who remain fervently long. If the past 7 years – in which retail has consistently trounced “smart money” returns are any indication, bitcoin is about to soar as yet another major short squeeze develops in the coming weeks and months.

Cryptocurrencies Stage Dramatic Comeback After Flash Crash

Update (1050ET): Ripple crashed down over 30% after the initial headlines then exploded back higher… and Ethereum is now unchanged on the day…

* * *

Amid headlines that South Korean regulators are inspecting 6 banks, including Industrial Bank of Korea, that provide virtual accounts to companies related to cryptocurrency, has sparked selling pressure across the entire space with Ripple down almost 20% today.

Bloomberg reports that South Korea’s Financial Services Commission Chairman Choi Jong-ku said in a speech text:

- There’s high possibility cryptocurrency transactions could be used in money laundering.

- South Korea to suspend virtual account– related operations of banks if they are found to have broken laws related to cryptocurrency.

- Regulator also strengthen probe into cryptocurrency exchanges over price manipulation, money laundering, pyramid scheme.

- Side effects of cryptocurrency “serious”; regulator will consider all measures including shutdown of cryptocurrency exchanges.

- Cryptocurrency fever in S. Korea is much stronger than other countries; regulator won’t let S. Korea take the lead in abnormal cryptocurrency trading.

And the last few days have seen that Korean exuberance being smashed out of cryptos.

Ethereum remains the YTD winner for now, but as is clear Ripple quickly went from hero to zero as the volatile trading continues.

Bitcoin is back below $15,000…

Ethereum is holding above $1000 for now…

and Ripple is testing significant support…

As CoinTelegraph reports, as speculative investments into Bitcoin and altcoins continue to trouble regulators worldwide, Korea has taken a hardline stance in recent months.

New legislation will seek to place heavy restrictions on how cryptocurrency exchanges can operate in the country, as well as who can use them and to what extent.

South Koreans will likely only be able to hold one exchange account linked to their real name, while tax obligations are also being overhauled regarding profits.

Reporting on the inspection, Yonhap News Agency appeared to forecast a predatory climate for exchanges.

“They (the FIU and FSS) are seeking to cut off fund inflows into cryptocurrency exchanges and shutter cryptocurrency exchanges that have loopholes in their system,” it claims.

What these “loopholes” might entail remains vague, yet the security setup of principal exchanges has come into the spotlight following an organized hacking attempt by a Korean news agency.

Using private white-hat hackers, the agency successfully gained entry into exchange accounts it set up maliciously, bypassing even two-factor authentication, it reported last month.

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.4975 /shanghai bourse CLOSED UP AT 17.73 POINTS 0.53% / HANG SANG CLOSED UP 84.89 POINTS OR 0.28%

2. Nikkei closed UP 208.20 POINTS OR 0.89% /USA: YEN RISES TO 113.11

3. Europe stocks OPENED MOSTLY GREEN /USA dollar index RISES TO 92.27/Euro FALLS TO 1.1988

3b Japan 10 year bond yield: FALLS TO . +.060/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.90 and Brent: 67.85

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.414%/Italian 10 yr bond yield UP to 1.977% /SPAIN 10 YR BOND YIELD UP TO 1.487%

3j Greek 10 year bond yield FALLS TO : 3.747?????????????????

3k Gold at $1320.20 silver at:17.19: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 17/100 in roubles/dollar) 57.09

3m oil into the 61 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A HUGE SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.35 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9772 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1717 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.414%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.467% early this morning. Thirty year rate at 2.801% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Euphoria Sends Global Stocks To New Record Highs, Korean Won Boosts Dollar With Overnight Fireworks

Every day is “deja vu all over again” for global stock markets which hovered close to all-time highs on Monday as the best start to a year in eight years showed little sign of running out of steam, thanks to “goldilocks” – the combination of global growth and low inflation – which has sent risk appetites into overdrive

For traders returning from holiday, Wall Street last week posted its best start to a year in more than a decade; In yet another case of “bad news is again good news”, Friday’s disappointing jobs report, while weaker than expected, encouraged hopes that “brisk growth and low inflation can be sustained this year.” The MSCI world index was flat, just below record highs. It has gained 2.5% in the first five trading sessions of the year, its best start since 2010, according to Thomson Reuters data.

After surging every day last week, U.S. equity futures are little changed while European stocks followed Asian markets higher before the start of another earnings season that’s expected to produce strong profit outlooks. The euro and the pound retreated against the dollar which snapped a two-day drop as traders unwound stale short positions, while the euro slid under 1.20 after it failed to find support from data showing speculative long positioning on the common currency reached a record even as Euro-area economic confidence rose to a two-decade high; euro-area bonds and Treasuries were steady, with U.S. two-year yields within sight of psychological 2% level

European stocks climbed for a fourth day, rising to the highest levels since August 2015 and poised for their longest winning streak in two months. Europe’s Stoxx Europe 600 Index added 0.2%, following a weekly gain of 2.1%, the best start to a year since 2013 and its biggest weekly advance since April. Miners and carmakers lead gains, with the latter poised for the highest level since May 2015. Novo Nordisk shares pushed marginally higher after they said they had made a bid for Belgian rival Ablynx, whose shares are yet to open but were indicated higher by as much as 45%. Commerzbank and Deutsche Bank are propping up the DAX after Cerberus said they oppose a merger between the two lenders.

Earlier, Asian markets inched towards all-time peaks. Australia’s ASX 200 (+0.1%) and KOSPI (+0.4%) were positive ahead of inter-Korean talks which begin tomorrow. The tone for the rest of the Asia-Pac region was mostly reserved throughout the day amid the absence of Japanese participants due to public holiday. Chinese shares continued their strong start to the year, with property developers and energy stocks among the top gainers amid optimism over real estate sales and after the government said it would support mergers in the coal sector. The MSCI China Index climbed 0.7%, taking its advance this year to 6.3%; the gauge is at its highest in 10 years. The Hang Seng Index rises 0.3% for 10th straight gain, its best run since October 2012, while the Hang Seng China Enterprises Index rose +0.2%. The Shanghai Composite Index rose +0.5%; its seventh day of gains and the longest streak since March 2016. Real estate companies accounted for five of top 10 advancers on Hang Seng Index, as China developers listed in H.K. build on their best week since January 2015, while property subgauge outperforms in Shanghai. Of note: the PBoC refrained from liquidity operations for the 11th consecutive day, draining a net 40bn yuan in liquidity, amid reports of tighter shadow banking regulations, as well as PBoC researcher comments regarding scope for higher rates.

In an otherwise quiet FX session, South Korea’s won sharply dropped after the government warned it would take action to stem one-sided moves in the currency, which spurred speculation of central bank intervention.

The KRW climbed against the dollar early Monday before sharply reversing to sink as much as 0.7% as traders speculated that the government was in the market. In response to a request for comment from Bloomberg News on the move, an official at the nation’s FX authority said that South Korea will take steps “sternly” in the case of one-sided moves in the won as the dollar weakens globally. The currency had dropped to an intraday low of 1,069.80 per dollar, reversing an earlier gain to 1,058.80, with traders speculating that the swing was due to central bank intervention.

The won was Asia’s best-performing currency last year, climbing almost 13 percent, as its economy benefited from thriving exports and the central bank raised interest rates for the first time since 2011. The Korean government may find that room to act against further advances will increasingly be limited as talks to revise a free-trade agreement with the U.S. proceeds, according to Schroder Investment Management.

Losses in most other emerging Asian currencies accelerated through the trading day.

As emerging market assets advanced this year, other Asian governments including Thailand and the Philippines have also flagged that they would act to smooth volatility if needed. “Since the start of the year, Asian currencies backed by strong trade and current account surpluses, particularly the TWD, THB and KRW have continued to strengthen,” said Heng Koon How, head of markets strategy, global economics and markets research at United Overseas Bank Ltd. “It’s not surprising that local authorities may act to stabilize FX markets in the interim and prevent excessive strength.”

The dollar index rose for the first time in three days as the rally in the euro faded and options signaled bets on a weaker common currency according to Bloomberg; support also came from the Fed’s Williams who said in Reuters interview that three rate hikes in 2018 “makes sense”. The dollar rose against all G10 peers on Monday, even as gains failed to push the Bloomberg Dollar Spot Index markedly away from a three-month low reached during Asian hours.

The greenback has been pressured since the start of the year amid doubts on the strength of the U.S. economic recovery and its impact on the pace of Federal Reserve policy tightening. Market players are focusing on riskier assets such as stocks, while persistent political worries in the U.S. have also weighed on the greenback.

“The dollar may recover in the short-term due to stale short positions and lack of any meaningful catalysts in other currencies to take the dollar another leg lower,” said Viraj Patel, a currency strategist at ING Bank NV. “But this doesn’t mask the structural problems — we think these political and protectionist risks for the dollar could be more evident ahead of President Trump’s State of the Union speech on Jan. 30.” Elsewhere, the Australian dollar reverses gains made since Friday’s U.S. non-farm payroll miss as macro accounts short spot against both kiwi and dollar. The MSCI EM Asia Index gained for a fifth day.

In commodity markets, many commodities paused after the recent run-up in prices, supported by a broadly weak U.S. dollar and the rise in global growth expectations. WTI and Brent crude futures both modestly in the green near 3-year highs that were hit late last week as the rig count last week showed that drillers lowered the number of rigs by 5 in the latest week. Precious metals were slightly lower with silver falling from 6-week highs and gold pulled back 0.1% after rising for its fourth straight week last week.

Attention in the U.S. will turn to the quarterly earnings season, which kicks off this week with the Street expecting solid growth of around 10 percent. Analysts at Bank of America Merrill Lynch said that the global economy had entered 2018 “firing on all cylinders”. “This growth is keeping our quant models bullish and driving earnings revisions to new highs,” they added. “We stay long outside the U.S., with Asia ex-Japan and Nikkei our growth plays, Europe still for yield.”

Meanwhile, in Europe attention is returning to Germany’s struggle to form a government, restraining the single currency. The pound fell and U.K. stocks were flat following weak economic data and reports that Prime Minister Theresa May is considering creating a position for a minister in charge of contingency planning for a no-deal Brexit.

Expected data today includes only US consumer credit. Other things to watch this week include U.S. inflation data; Fed spearkers including San Francisco Fed President John Williams and head of the New York Fed Bill Dudley; China producer and consumer prices data are due Wednesday, while a reading on the country’s money supply is expected in coming days; U.S. firms announcing earnings this week include JPMorgan Chase & Co., Wells Fargo & Co. and BlackRock Inc.

Market Snapshot

- S&P 500 futures little changed at 2,742.75

- STOXX Europe 600 up 0.2% to 398.28

- MSCI Asia Pacific up 0.2% to 179.67

- MSCi Asia Pacific ex Japan up 0.3% to 589.26

- Nikkei up 0.9% to 23,714.53

- Topix up 0.9% to 1,880.34

- Hang Seng Index up 0.3% to 30,899.53

- Shanghai Composite up 0.5% to 3,409.48

- Sensex up 0.6% to 34,370.28

- Australia S&P/ASX 200 up 0.1% to 6,130.37

- Kospi up 0.6% to 2,513.28

- German 10Y yield fell 1.1 bps to 0.428%

- Euro down 0.3% to $1.1989

- Italian 10Y yield fell 0.9 bps to 1.737%

- Spanish 10Y yield fell 2.0 bps to 1.502%

- Brent futures up 0.3% to $67.80/bbl

- Gold spot down 0.2% to $1,317.11

- U.S. Dollar Index up 0.4% to 92.27

Top Overnight News

- Stephen Bannon’s apology for his comments trashing Donald Trump’s family did little to tamp down the president’s anger at his former chief strategist, as aides describe the president demanding a stark choice from supporters of both men: you are either with Bannon, or with me

- Angela Merkel’s own party bloc is making her life more difficult as hard-liners seek to force the German chancellor to shift to the right in talks on setting up a government, while she is also seeking a commitment this week from the rival Social Democrats to start formal negotiations on extending their governing alliance

- U.K. PM Theresa May is starting the new year with a Cabinet reshuffle which will see her move her education and health ministers and create a post for a no-deal Brexit minister, according to newspaper reports

- Berlusconi could end up holding the aces after Italy’s election

- Merkel calls for deal as make-or-break government talks begin

- China’s foreign-currency holdings rose $129 billion in 2017, posting the first annual gain since 2014 amid tighter capital controls, a stronger yuan and resilient economic growth

- Euro-area January Sentix investor confidence at 32.9 vs 31.1 in December

- Germany November factory orders fall 0.4% m/m; estimate unchanged m/m

Asia equity markets traded mostly higher as the positive tone seeped through from last Friday’s record performance on Wall Street where all major indexes printed at all time high levels despite the NFP miss, while the DJIA extended above the 25,000 level and posted its best start to the year in over a decade. As such, ASX 200 (+0.1%) and KOSPI (+0.4%) were positive in which with the latter outperformed ahead of inter-Korean talks which begin tomorrow. The tone for the rest of the Asia-Pac region was mostly reserved throughout the day amid the absence of Japanese participants due to public holiday, while Shanghai Comp. (+0.4%) and Hang Seng (-0.1%) were choppy after the PBoC refrained from liquidity operations and amid reports of tighter shadow banking regulations, as well as PBoC researcher comments regarding scope for higher rates. Opining in the China Daily, PBoC Deputy Head of Research Ji Min stated that there is room for a rate increase in the short-term, although he later reversed himself. On Monday, the PBoC skipped open market operations again today citing relatively high bank liquidity.

Top Asian News

- China’s Currency Reserves Bounced Back Last Year Amid Cash Curbs

- China Insurer Up $101 Billion Trades Like a Technology Stock

- Aramco Joins Saudi Companies Boosting Pay After Royal Orders

- Won Swings to Loss as Korean Government Warns of Stern Steps

- Won’s Whipsaw May Be a Warning to Emerging-Market Currency Bulls

- Asia Stocks Extend Rally on Earnings, Korea Talks Outlook

- Macron Calls for China-EU Relationship to ‘Enter 21st Century’

- China’s Richest Woman’s Wealth Rose by $2 Billion in 4 Days

European equity markets continued their march higher on Monday with all the major indices trading in positive territory. With little major macro news over the weekend, equity markets continued where they left off in the US where all the major indices closed at record highs. In individual equity news, Novo Nordisk shares pushed marginally higher after they said they had made a bid for Belgian rival Ablynx, whose shares are yet to open but were indicated higher by as much as 45%. Commerzbank and Deutsche Bank are propping up the DAX after Cerberus said they oppose a merger between the two lenders. A firm rebound in core bonds, and the recovery started on Eurex where Germany’s 10 year debt future caught a bid ahead of nearest chart support below 161.50. Market contacts noted light buying amidst a paring of Dax gains and then more of an intraday short squeeze once the opening peak was breached. Bunds have now been up to 161.80 (+21 ticks vs -20 ticks at worst), and last

Friday’s 161.87 session high is next on the radar, although firmer than forecast Eurozone retail sales may stall further upside. Gilts have also reversed early Liffe losses to trade at 124.82 (+17 ticks vs -24 ticks at one stage), awaiting news from UK PM May on her new Cabinet Ministers/posts.

Top European News

- German Factory Orders Dip But Economy Continues Upward Trend

- May Emerges Stronger in 2018, Ready to Finally Reshuffle Cabinet

In FX markets, the USD is higher against most of its major counterparts after initially trading lower at the beginning of Asia-Pac trade. The turnaround appeared to be intervention from South Korea who were said to buying dollars to weaken the KRW. GBP/USD trades lower as markets await a cabinet reshuffle from UK PM Theresa May although no major changes are expected. AUD/USD is back down below 0.7850, with the AUD undermined by a marked slowdown in Australia’s construction index and Government forecasts for a sharp 20% decline in iron ore prices this year.

In commodities, WTI and Brent crude futures both trade relatively flat and near 3-year highs that were hit late last week as the rig count last week showed that drillers lowered the number of rigs by 5 in the latest week. Precious metals were slightly lower with silver falling from 6-week highs and gold pulling back after rising for its fourth straight week last week. Markets will be looking out for comments from Fed speakers later in the session on the future path of Fed policy given the its sensitivity to rate hikes. Australia’s government sees iron ore prices dropping 20% this year to an average USD 51.50/ton, due to increasing global supply and moderating Chinese demand.

Looking at the day ahead, the November consumer credit numbers are due. The Fed’s Williams and Rosengren speak at an Inflation targeting conference, while the Fed’s Bostic will also speak on monetary policy and the US economic outlook. Elsewhere, France’s President Macron arrives in China today for a three day state visit.

US Event Calendar

- 3pm: Consumer Credit, est. $18.0b, prior $20.5b

- 12:40pm: Fed’s Bostic Speaks on Economic Outlook in Atlanta

- 1:35pm: Fed’s Williams Speaks at Inflation Targeting Conference

- 4pm: Fed’s Rosengren Speaks at Inflation Targeting Conference

DB’s Jim Reid concludes the overnight wrap

If you’ve just come back to work from holidays today, you’ve missed a bit of a melt up in risk assets so far in 2018 with US equities climbing every day this year (S&P500 +2.60% so far) and Europe increasingly getting in on the act (Stoxx +2.10% YTD) after a hesitant start on an initially surging Euro. Basically the year has started as a turbo charged version of 2017 with many of the same themes still present. Data on both sides of the Atlantic has generally been strong but we’re yet to see signs of elevated inflation pressures with Friday’s US average hourly earnings ‘only’ in-line and with a 0.1ppt downward revision to the prior month.

In a relatively quiet week for data the main highlight has to wait until Friday with the latest US CPI report due. Last month’s release was another miss (the 7th in 9 months) with one of the standout contributors a 1.3% fall in apparel prices, the third largest drop in history and the largest since 1998. Our economists expect the change in apparel prices to largely unwind and, as such, core CPI (+0.2% forecast, +0.2% consensus vs. +0.1% previously) should come in relatively healthy as a result. A print in line with DB’s expectation would see YoY core CPI slip two basis points to 1.69% but the six-month annualised change would rise about 17 basis points to 2.08% and the three month annualised change would rise almost twice that to 2.19%, providing some evidence of core inflation firming. With the price of most refined energy products falling in December, headline CPI (+0.1% vs. +0.4% previous) should moderate correspondingly.

A reminder that our credit view is positive in Q1 based on assumption of still subdued inflation and still contained government yields in the early part of the year. However we think both will move higher from around Q2 and exhibit more volatility and will thus create more headwinds for credit from then, albeit at tighter spreads than today’s levels. If we’re wrong on inflation though the carry trade will likely last longer as growth looks very solid at the moment.

Staying with inflation, we also see US PPI data on Thursday and China CPI and PPI on Wednesday. Outside of the data, US Q4 earnings kicks off from Tuesday, with Friday seeing results from Wells Fargo, JP Morgan and Blackrock.

Back to credit, as mentioned at the top, on Friday my team produced the review of 2017 in Euro HY (link) and a report “Capitalising on the CDS-Bond Basis and Term Structure of Credit Spreads” which analyses the CDS-bond basis and curve steepness in EUR and USD corporate credit. Cash bonds have richened to CDS meaningfully since the ECB announced corporate bond purchases in early 2016. Michal Jezek expects this to reverse as they prepare for exit in 2018. At the same time credit curves are too steep and are expected to flatten, particularly in the CDS space as structured credit activity intensifies. The report provides macro credit trade ideas to take advantage of these dislocations and discusses the implications for hedging bond portfolios.

Over in China, December foreign exchange reserves rose for the 11th consecutive month to US$3.14trn (vs. $3.13 trn expected) amid tighter capital controls and resilient economic growth. This morning in Asia, markets are trading modestly higher. The Kospi and China’s CSI 300 are up 0.47% and 0.65% respectively, while the Nikkei is closed for a national holiday. The Hang Seng and China’s RMBUSD are marginally lower as we type with the former looking to extend a winning run to a tenth day.

Moving on now to the various central bankers speak from Friday and over the weekend. On rates, the Fed’s Williams expects unemployment to fall to 3.7% this year, but he is “not worried about inflation suddenly taking off” and suggested that “something like three rate hikes makes sense to me”. Conversely, the Fed’s Harker who is not a FOMC voter this year, believes two rate hikes will be appropriate in 2018 and “want to be slow and steady with any additional rate increases”. Although he sees the flat yield curve “worries so far have been a little inflated and don’t think the situation we’re in now is analogous to the inversion…. (seen) in the 70’s and ‘80’s”.

On potential impacts from the tax cuts, Mr Williams expect it to have a “modest, positive effect” on GDP growth and that the US economy will be in a very positive place two years from now, with “inflation at 2% and around 4% unemployment”.

Similarly, Mr Harker didn’t expect tax cuts to have a large impact on US economic growth. Elsewhere,the White House Chief economist Kevin Hassett noted the administration’s own analysis suggests the tax cuts should not alter the Fed’s projection of three rate hikes in 2018, in part as “if you have supply side stimulus, then it doesn’t put upward pressure on prices”. Finally, the Fed’s Bullard was more optimistic, he noted “there is some possibility that (tax cuts) could light a fire under investment and really drive growth higher…I have some sympathy for this idea…”

Following on, the Bundesbank’s Weidmann reiterated his views that setting a clear end for ECB’s QE bond buying program is justifiable and that “even after the end of net purchases, monetary policy will remain very expansive”. Elsewhere, the Fed’s Mester said US monetary policy should remain focused on price stability and maximum employment and “not be given a third objective of financial stability”.

Now recapping other markets performance from Friday. The S&P rose 0.70% to fresh highs with only two sectors marginally in the red (energy and utilities). European markets were all higher, with the Stoxx 600 up 0.93% back near its 2.5 year high and all sectors in the green. Across the region, gains were by led the DAX (+1.15%) and CAC (+1.05%), while the FTSE was the relative laggard (+0.37%).