GOLD: $1312.80 DOWN $6.30

Silver: $16.98 DOWN 14 cents

Closing access prices:

Gold $1311.80

silver: $16.94

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1325.13 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1318.70

PREMIUM FIRST FIX: $6.43

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1321.22

NY GOLD PRICE AT THE EXACT SAME TIME: $1318.15

Premium of Shanghai 2nd fix/NY:$3.77

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1314.05

NY PRICING AT THE EXACT SAME TIME: $1315.00

LONDON SECOND GOLD FIX 10 AM: $1311.00

NY PRICING AT THE EXACT SAME TIME. 1310.75

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 13 NOTICE(S) FOR 1300 OZ.

TOTAL NOTICES SO FAR: 255 FOR 25500 OZ (0.7931 TONNES),

For silver:

jANUARY

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 507 for 2,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $14,727/OFFER $14,847 DOWN $220 (morning)

Bitcoin: BID 14,696/OFFER $14,817 DOWN $240(CLOSING)

end

your humour story of the day:

Wife texts to husband on a cold winter morning:“Windows frozen. Won’t open.”Husband texts back:“Slowly pour warm water over it and then gently tap the edges with a hammer.”Wife texts back 10 minutes later:“Computer really messed up now.”

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY TINY 215 contracts from 194,429 FALLING TO 194,214 WITH YESTERDAY’S 11 CENT FALL IN SILVER PRICING. WE HAD MINIMAL COMEX LIQUIDATION BUT WITHOUT A DOUBT WE WITNESSED ANOTHER MAJOR BANK SHORT- COVERING OPERATION. NOT ONLY THAT , WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: A CONSIDERABLE 1340 EFP’S FOR MARCH (AND ZERO FOR OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 1340 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1340 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED EFP’S FOR SILVER ISSUED. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. I BELIEVE THAT WE MUST HAVE HAD SOME MAJOR BANKER SHORT COVERING AGAIN TODAY.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

19,271 CONTRACTS (FOR 7 TRADING DAYS TOTAL 19,271 CONTRACTS OR 96.355 MILLION OZ: AVERAGE PER DAY: 2753 CONTRACTS OR 13.765 MILLION OZ/DAY)

RESULT: A SMALL SIZED GAIN IN OI COMEX DESPITE THE 11 CENT FALL IN SILVER PRICE WHICH USUALLY INDICATES HUGE BANKER SHORT-COVERING. WE ALSO HAD A FAIR SIZED EFP ISSUANCE OF 1721 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. FROM THE CME DATA 1340 EFP’S WERE ISSUED FOR TODAY (FOR MARCH EFP’S AND NONE FOR ALL OTHER MONTHS) FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 1125 OI CONTRACTS i.e. 1340 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 215 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER BY 11 CENTS AND A CLOSING PRICE OF $17.12 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.9710 BILLION TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest ROSE BY AN SMALL SIZED 631 CONTRACTS UP TO 552,072 DESPITE THE FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($1.40). IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY AND IT TOTALED A GOOD SIZED 5660 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 5660 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS. The new OI for the gold complex rests at 552,072. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE ANOTHER GOOD GAIN OF 6,291 OI CONTRACTS: 631 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 5660 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

FRIDAY, WE HAD 6115 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 63,265 CONTRACTS OR 6.326 MILLION OZ OR 196.76 TONNES (7 TRADING DAYS AND THUS AVERAGING: 9,037 EFP CONTRACTS PER TRADING DAY OR 903,700 OZ/DAY)

Result: A SMALL SIZED INCREASE IN OI DESPITE THE FALL IN PRICE IN GOLD TRADING ON YESTERDAY ($1.40). WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5660. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5660 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 6,291 contracts:

5660 CONTRACTS MOVE TO LONDON AND 631 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 19.56 TONNES)

we had: 13 notice(s) filed upon for 1300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

No changes in gold inventory at the GLD

Inventory rests tonight: 834.86 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

INVENTORY RESTS AT 318.423 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A SMALL 215 contracts from 194,429 UP TO 194,214 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE FALL IN PRICE OF SILVER TO THE TUNE OF 11 CENTS YESTERDAY. WE HAD WITHOUT A DOUBT ANOTHER MAJOR SHORT COVERING FROM OUR BANKERS AS THEY HAVE CAPITULATED. NOT ONLY THAT BUT OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1340 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD NO COMEX SILVER COMEX LIQUIDATION. BUT, IF WE TAKE THE SMALL OI LOSS AT THE COMEX OF 215 CONTRACTS TO THE 1340 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 1125 OPEN INTEREST CONTRACTS DESPITE THE MAJOR BANKER SHORT COVERING. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ: 5.63 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE FALL OF 11 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1340 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 4.42 points or 0.13% /Hang Sang CLOSED UP 111.88 pts or 0.36% / The Nikkei closed UP 135.46 POINTS OR 0.57%/Australia’s all ordinaires CLOSED UP 0.08%/Chinese yuan (ONSHORE) closed DOWN at 6.5280/Oil UP to 61.92 dollars per barrel for WTI and 67.86 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5230. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.5300 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS STILL HAPPY TODAY.(GOOD MARKETS BUT WEAKER YUAN)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea/South Korea

Peace progress. North Korea will be sending a team to the Winter Games much to the chagrin of the uSA. Seoule is also prepared to lift some sanctions against the North.

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

China removes one of the support factors in the yuan fixing and this causes the yuan to fall. It looks like China is ready to have the market determine the value of the yuan.

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

With Washington set to impose more sanctions on Iran, it is likely that Iran will switch from receiving dollars for its oil to yuan.

( Nick Cunningham/OilPrice.com)

6 .GLOBAL ISSUES

Amazing! every time a state or a province raises the minimum wage, companies react by initiating job less plus reducing benefits etc. Just look what Tim Horton did when Ontario raised its minimum wage

( zero hedge)

7. OIL ISSUES

Both oil and gasoline rise after a huge drawdown in crude

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

RT reports that the rise in gold reserves between Russia and China is aimed to shake USA dominance

( RT/GATA)

10. USA stories which will influence the price of gold/silver

i)Early trading:

yields rise in a mini tantrum due to the rise in Japanese bond yields. The 10 yr yield is now over 2.50%

(courtesy zerohedge)

ii) Negative family net worth growth is rising with the latest states that the median net worth is below 1989 levels.

Almost 30.4% of the population have zero or non home wealth.

( Mish Shedlock/Mishtalk)

Let us head over to the comex:

The total gold comex open interest ROSE BY SMALL 631 CONTRACTS UP to an OI level of 552,072 DESPITE THE SMALL SIZED FALL IN THE PRICE OF GOLD ($1.40 LOSS WITH RESPECT TO FRIDAY’S TRADING). OBVIOUSLY WE HAD ZERO COMEX GOLD LIQUIDATION WITH ANOTHER STRONG GAIN IN TOTAL OPEN INTEREST AS WE WITNESSED ANOTHER HUMONGOUS COMEX TRANSFER THROUGH THE EFP ROUTE. THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 5660 EFP’S WERE ISSUED FOR FEBRUARY AND 0 EFP’s FOR APRIL: TOTAL 5660 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 6291 OI CONTRACTS IN THAT 5660 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 631 COMEX CONTRACTS. NET GAIN: 6291 contracts OR 629,100 OZ OR 19.56 TONNES

Result: A SMALL SIZED INCREASE IN COMEX OPEN INTEREST DESPITE THE SMALL FALL IN THE PRICE YESTERDAY’S GOLD TRADING (1.40.) WE HAD NO GOLD LIQUIDATION ANYWHERE. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 6291 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest RISE by 14 contracts UP to 193. We had 0 notices served on Friday so we GAINED 14 contracts or 1400 additional oz of gold will stand in this non active month AND QUEUE JUMPING RETURNS.

FEBRUARY saw a LOSS of 13,425 contacts DOWN to 357 877. March saw a gain of 318 contracts up to 419. April saw a GAIN of 10,734 contracts UP to 94,459.

We had 13 notice(s) filed upon today for 1300 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 329,333

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 412,858

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY 215 CONTRACTS FROM 194,429 DOWN TO 194,214 DESPITE YESTERDAY’S 11 CENT FALL. AGAIN WE MUST HAVE HAD SOME BANKER SHORT COVERING. NOT ONLY THAT, WE HAD ANOTHER GOOD SIZED 1340 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1340. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD MINIMAL LONG COMEX SILVER LIQUIDATION BUT A RISE IN TOTAL SILVER OI AS IT SEEMS THAT WE ARE WITNESSING SOME MAJOR BANKER SHORT-COVERING. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE GAINED 1125 OPEN INTEREST CONTRACTS:

215 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1340 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN: 1125 CONTRACTS

We are now in the poor non active delivery month of January and here the OI LOSS by 0 contracts REMAINING AT 39. We had 0 notices served upon yesterday, so we GAINED 0 contracts or an additional NIL oz will stand for delivery

February saw a GAIN OF 1 OI contracts RISING TO 183. The March contract LOST 1030 contracts DOWN to 148,934.

We had 0 notice(s) filed for NIL oz for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 9/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

24,112.500 oz

Scotia

750 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

13 notice(s)

1300 OZ

|

| No of oz to be served (notices) |

180 contracts

(18,000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

255 notices

25500 oz

0.7931 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 13 contract(s) of which 12 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (255) x 100 oz or 25500 oz, to which we add the difference between the open interest for the front month of JAN. (193 contracts) minus the number of notices served upon today (13 x 100 oz per contract) equals 43,500 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (255 x 100 oz or ounces + {(193)OI for the front month minus the number of notices served upon today (0 x 100 oz which equals 43,500 oz standing in this active delivery month of JANUARY (1.353 tonnes). THERE IS 17.68 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 14 CONTRACTS OR AN ADDITIONAL 1400 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 568,449.373 oz or 17.681 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,210,113.76 or 286.44 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 68 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

502,712.320 oz

Delaware

Scotia

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(10,000 OZ)

|

| No of oz to be served (notices) |

39 contract

(195,000 oz)

|

| Total monthly oz silver served (contracts) | 509 contracts

(2,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had no inventory deposits into the customer account

total inventory deposits: nil

we had 2 withdrawals from the customer account;

i) out of Delaware; 1937.100 oz

ii) Out of Scotia; 500,775.220 oz

total withdrawals; 502,712.320 oz

we had no adjustments.

total dealer silver: 45.466 million

total dealer + customer silver: 244.470 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 0 contract(s) FOR 10,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 507 x 5,000 oz = 2,535,000 oz to which we add the difference between the open interest for the front month of JAN. (39) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 507(notices served so far)x 5000 oz + OI for front month of JANUARY(39) -number of notices served upon today (0)x 5000 oz equals 2,730,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3,790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 81.496

CONFIRMED VOLUME FOR FRIDAY: 92.059 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 92,059 CONTRACTS EQUATES TO 460 MILLION OZ OR 65.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 59.182 million

Total number of dealer and customer silver: 240.232 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.6 percent to NAV usa funds and Negative 2.6% to NAV for Cdn funds!!!!

Percentage of fund in gold 62.8%

Percentage of fund in silver:37.0%

cash .+.2%( Jan 9/2018)

2. Sprott silver fund (PSLV): NAV RISES TO -0.98% (Jan 9/2018)??????????????????????????????

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.37% to NAV (Jan 9/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -0.98%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.37%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnrd

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 9/2018/ Inventory rests tonight at 834.88 tonnes

*IN LAST 307 TRADING DAYS: 106.09 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 242 TRADING DAYS: A NET 51.22 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 210.31TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 9/2017:

Inventory 317.575 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.73%

12 Month MM GOFO

+ 1.97%

30 day trend

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

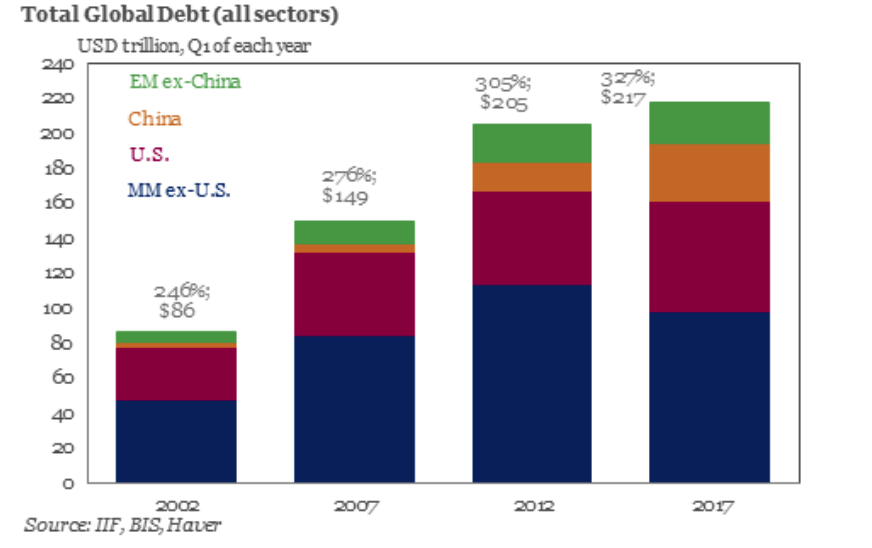

The World is $233 Trillion In Debt: It’s Time to Rebalance To Gold

– Record level global debt level hit $233 trillion in Q3 2017

– World’s per capita debt now more than $30,000

– UK personal debts climbed to the highest level since credit crunch, reaching more than £200bn

– US consumer credit highest jump in 2 years by 8.8% in November to $3.83 trillion

– BofE warn UK banks could incur £30bn of losses if interest rates and unemployment rise sharply

Graph updated September 2017.

Global debt levels have soared to a record high of $233 trillion, according to the Institute of International Finance (IIF).

Since the end of 2016 to the end of Q3 2017, the total debt incurred by the household, government, financial and non-financial corporate sectors increased by $16 trillion. A major increase in just nine months.

The institute reported that the rise was split between $63tn in government debts, $58tn in financial, $68TN in non-financial and $44tn in household sectors.

Just consider for one moment that prior to the financial crisis global debt was “only” around $150 trillion. How have we managed to add over $80 trillion in less than a decade?!

On a country-by- country basis both the UK and US saw worrying data when it came to their own levels of consumer debt.

Here in the UK personal borrowing on credit cards, loans and car finance, is now outpacing the rate of growth in UK pay five-times over.

In the US consumer credit jumped by its highest in two years, by 8.8% in November to $3.83 trillion.

Countries that saw a major increase in non-financial debt were Canada, France, Hong Kong, South Korea, Switzerland and Turkey, all saw all-time highs. Debt is increasing not because low-earners are borrowing more, but data is showing that increasing numbers of middle-class earners are driving up levels of leverage.

Why would those in usually stable jobs and comfortable earning levels be driving themselves into debt?

UK middle-class pushing up borrowing levels

UK personal debt is now rising at almost five times the rate of growth in UK pay. According to debt charities, many families are now living on the colloquially termed ‘never-never’ i.e. they rely on the prayer that they can keep transferring debt and therefore never repay it.

These are not all people who have directly suffered from the financial crisis by losing their jobs or losing their homes. Many are suffering from the repercussions of the ‘solutions’ to the downturn. According to StepChange the majority of those they help are employed, some even have senior roles and one in five are homeowners.

Last year credit card debt levels grew at their fastest rate in 11 years. In April alone £606 million was put on plastic. Previously the Bank of England and other organisations have not expressed too much concern about the ability of households to pay this back. Until now that is.

This week a report by the Bank of England and FCA, stated that British consumers are trapped by credit card debt for longer than previously thought.

The Guard-+ian reports on the study:

Nine out of every £10 of outstanding credit card debt in November 2016 was owed by people who were also in the red two years earlier, according to the study.

The analysis follows the rapid growth in personal borrowing on credit cards, loans and car finance, now rising at almost five times the rate of growth in UK pay. Households are finding themselves increasingly squeezed by meagre earnings growth and rising inflation, as the weak pound after the Brexit vote pushes up the cost of imported goods.

Bank data shows personal debts have risen to the highest level since before the credit crunch, reaching more than £200bn – with credit cards accounting for more than £70bn of the total.

Households are also facing a year of stagnant real earnings growth in 2018, which may push them further into debt should they wish to maintain their living standards.

Writing on the Bank Underground blog – where Threadneedle Street staff can air their views in public – the officials said: “Although a consumer may clear their debt on one credit product, it is not uncommon for them to remain in debt as they transfer balances, take out new credit products or draw down on existing credit lines, such as credit cards.”

US consumers feel confident to borrow more

The US Federal Reserve had a notable 2017 given their actions to both reduce their balance sheet and increase interest rates. One would have thought that an increase in the cost of borrowing would have given consumers pause for thought when it came to taking out loans.

This was not the case. In November 2017 consumer credit grew rapidly by $28.0bn in November. This was the largest gain in 16 years, according to Nomura. In the month previous it had climbed by $20.5bn.

Nomura, reporting on the data, pointed to the figures as if they are a sign of strength in the economy ‘This appears consistent with a strong labor market with low unemployment and elevated consumer confidence, which we expect will continue in the near term.’

In the US consumer spending accounts for roughly 7-0% of the economy’s activity. Last month surveys showed that American shoppers are feeling increasingly confident in the state of the country’s future. Early holiday reports suggest spending did not take a hit. However it was big loans such as student and auto which accounted for the major leap in debt levels.

So, if student loans accounted for a near $16.8 billion leap in the country’s spending, can one really argue that the increase is thanks to confidence levels. To me that sounds like a form of borrowing which is thanks to necessity rather than confidence.

Soon those student loans will need to be paid back, in an economy which is not currently creating that many jobs for graduates.

The student debt bubble is not a new phrase. It is something that has been reported on widely but with the logic that if we talk about it loud enough it might just skulk away and not rear its head. We should be so lucky.

As the FT reported back in April:

It is worth noting that over the past 10 years the amount of student loan debt in the US has grown by 170 per cent, to a whopping $1.4tn — more than car loans, or credit card debt.

In America, 44m people have student debt. Eight million of those borrowers are in default. That’s a default rate which is still higher than pre-crisis levels — unlike the default rate for mortgages, credit cards or even car loans. Rising college education costs will not help shrink those numbers. While the headline consumer price index is 2.7 per cent, between 2016 and 2017 published tuition and fee prices rose by 9 per cent at four-year state institutions, and 13 per cent at posher private colleges.

This is not something that can be magicked away by economic growth. Investors are worrying about their portfolios thanks to a financial crisis caused by rising, unsustainable debt levels. We appear to be in the same, if not worse, position that got us here in the first place.

Rebalance to combat global imbalance

These raging debt levels, whether government or consumer, are clearly unsustainable. These figures should serve as an indicator to investors that now is the time to look at their portfolios and rebalance them for this unbalanced world.

A shift from risk assets to safe haven assets such as gold and silver bullion seems to be a timely move, right now.

The concern with debt-levels such as these is that they end up scuppering the period of accelerated growth in global GDP, that we are currently witnessing. At the moment this high growth is the only way central banks and governments can justify the high levels of debt.

Central banks are obviously keen to start reigning in their balance sheets as well as increase interest rates. Unsustainable levels of debt could force them to park these plans should debtors begin to struggle with repayments.

This is quite the vicious circle. As we all know it was low interest rates which propelled such a highly-leveraged situation in the first place. This is an unsustainable path, something the central banks have become aware of all too late but now it seems they’ve buried themselves in real deep red hole.

Needless to say the future of global growth has been built on the Emperor’s New Clothes of foundations. There is little value really propping up an economy when it relies on its citizens drowning itself in debt in order to keep the charade going.

There’s little we can do to prevent individuals wracking up credit card debts or buying cars on finance. All we can do is prepare our portfolios for when the world realises that it’s standing on thin air.

Gold that is held in a segregated, allocated portfolio is a key way to protect your savings from counter-party risk in the financial system. Gold’s performance in 2017, along with low gold liquidations, increased demand for gold coins and bars and central bank purchases suggests that gold buyers have identified that this really is all a mirage.

It is obvious from both political and economic events that the global economic crisis is not over. Data shows that we are fast approaching circumstances worse than those seen prior to 2008. Sadly no one is acknowledging them and solutions and preparations are not being considered.

-END-

END

RT reports that the rise in gold reserves between Russia and China is aimed to shake USA dominance

(courtesy RT/GATA)

Russia-China gold reserves could shake U.S. economic dominance, expert tells RT

Submitted by cpowell on Mon, 2018-01-08 17:57. Section: Daily Dispatches

From Russia Today, Moscow

Monday, January 8, 2018

The gold accumulated by China and Russia could be seen as part of a strategy to move away from international trade denominated in U.S. dollars, according to Singapore’s Bullion Star precious metals expert Ronan Manly.

Manly exclusively told RT that there is a shift occurring regarding the two countries building up their gold reserves, to perhaps returning to gold-backed currencies in the future and a move away from the global dominance of the U.S. dollar, which is no longer supported by gold.

“China and Russia have both been aggressively accumulating their official gold reserves over the last 10 to 15 years,” Manly said, adding that only a decade ago each of them held around or less than 400 tons. “But now both these nations hold a combined 3,670 tons of gold.”

“Interestingly, both Russia and China publicize and promote their accumulations of gold and publicly refer to gold as a strategic monetary asset. They make no secret of this. But on the flip side, the U.S. does the opposite, and constantly downplays the strategic role of gold.”

According to Manly, for Russia and China gold is the only strategic monetary asset that could provide independence from the U.S. dollar. …

… For the remainder of the report:

First Majestic Silver CEO Keith Neumeyer Talks About The End Of The Silver Manipulation

During a recent interview, First Majestic Silver CEO Keith Neumeyer shared some interesting comments about the silver market. In particular he spoke about a development that could lead to the end of the ongoing manipulation.

For those not familiar, Neumeyer is one of, if not the only mining CEO to speak publicly about the manipulation that has left silver prices suppressed. His interviews always offer insightful commentary, and this latest one covered what could be a game changing event for the price of silver.

For those who have read about or studied the manipulation, you’ve likely heard about how there’s a large disconnect between the physical and paper silver markets. Of course the natural question on the mind of many investors, is when will it end.

In his interview Neumeyer mentioned that “there’s work going on right now to create a system using blockchain to price metals.” When asked directly how he thought the implementation of such an idea could impact the situation in the silver market, here’s how he responded.

“It’s going to remove the whole system of marginal banking where today we have over 300 times margin on silver. Silver trades on a global scale about a billion ounces a day and virtually all of that is paper, or 90% plus is paper.

The miners produce 800 million ounces a year, so we ‘re trading, just using simple math, 365 billion ounces a year on the exchanges worldwide, and we’re only producing 800 million ounces per year.

That ‘s a quite lot of leverage in my view. So if you get a way from the exchanges, that leverage disappears, and you have a much more fair pricing mechanism.“

That whole system that‘s currently pricing our metals is going to end“

Keep in mind that Neumeyer is not the only figure in the market to suggest such a possibility. There was a lot of attention in mid 2017 when well-known analyst Andrew Maguire predicted a gold and silver price reset, based on his involvement with a similar project at the time.

Obviously that didn’t occur on the schedule Maguire predicted. However his forecast was based on the introduction of a blockchain product backed by gold and silver, which was delayed, but is what Neumeyer is talking about now.

Neumeyer also commented on some of the supply and demand fundamentals in the market that have led to the potential development of such a product.

“If you go back to 2015, the mining industry as a whole worldwide produced 850 million ounces of silver. In 2016 that number was 800 million ounces. A reduction of 50 million ounces. We know in 2017 that Chile is down 10%, and Canada and Mexico are also down.

If we add it all up the speculation is that the mining industry as a whole is something in the order of 750 million ounces in 2017. So we ‘re seeing declining world production of silver and increasing demand for the metal. This is a perfect storm.

The market hasn‘t picked up on this yet, but this is a serious issue.

In terms of how that will impact the market, Neumeyer shared the following:

There will be a day, and in my view it‘s going to be in the short term, not in the long term, whereby you have a Tesla, an Apple, or a Toyota that just simply can’t produce their products anymore because they have a lack of silver.

That‘s what going to change the industry, and that’s going to start showing up in the headlines. Naturally we’re going to start see a big change in the current ratio to numbers that are closer to the production ratio of 9:1 (gold to silver) which will put silver at triple digits.

I‘m actually quite positive about blockchain technology because blockchain is going to be a way for mining companies to price their metals on a direct basis so we could sell direct to consumers, bypassing all of the current exchanges.

I believe that the current system with the LBMA and CME/COMEX type system is at the end of its ropes.”

Certainly it’s reasonable for silver investors to be frustrated by the pricing action of past years. I can understand being tired of hearing the reasons why the price should rise, only to see it stay the same or drop lower.

But while the wait has been longer than many might have imagined possible, there are reasons to believe we could be nearing the break point. And perhaps the marriage of precious metals and blockchain technology will be what finally brings free-market pricing back to precious metals.

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.5228 /shanghai bourse CLOSED UP AT 4.42 POINTS 0.13% / HANG SANG CLOSED UP 111.88 POINTS OR 0.36%

2. Nikkei closed UP 135.46 POINTS OR 0.57% /USA: YEN FALLS TO 112.65

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 92.52/Euro FALLS TO 1.1929

3b Japan 10 year bond yield: RISES TO . +.071/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.92 and Brent: 67.86

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.424%/Italian 10 yr bond yield UP to 1.973% /SPAIN 10 YR BOND YIELD DOWN TO 1.465%

3j Greek 10 year bond yield FALLS TO : 3.669?????????????????

3k Gold at $1314.85 silver at:17.02: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 27/100 in roubles/dollar) 56.85

3m oil into the 61 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A HUGE SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.65 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9818 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1717 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.424%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.485% early this morning. Thirty year rate at 2.825% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Smash More Records As Global Melt Up Accelerates; BOJ, PBOC Surprise Traders

The global market melt up continues, with Asian and European stocks rising, sending the MSCI all-country world stocks index to another record high as Europe’s main markets shrugged off a tech wobble in Asia and instead cheered Christmas trading updates and more forecast-beating data from Germany.

The MSCI Asia Pacific Index rose 0.3 percent on optimism earnings and economic growth prospects in the region support the stocks trading near record highs. Japan’s Nikkei closed at its highest since November 1991, catching up to the previous session’s gains as markets reopened after a holiday on Monday. Most equity benchmarks in the region rose except those of South Korea, Malaysia, Indonesia and Pakistan, while Taiwan was little changed. Offsetting Japan’s euphoria, South Korea’s Kospi erased its gains and slipped 0.1 percent, dragged lower by a 3.1% drop in shares of Samsung Electronics Co. Samsung’s guidance fell short of market expectations despite a forecast for a record fourth-quarter profit, as a strong won and one-off staff bonuses offset surging DRAM prices.

European stocks likewise climbed as traders focused on strong economic data in Germany and a chaotic cabinet reshuffle in the U.K. that may bode ill for its government’s ability to navigate the next stage of Brexit talks. The Stoxx Europe 600 Index was up 0.3%, led by miners and telecommunications stocks. The U.K.’s FTSE 100 Index rises 0.4% as sterling weakens after the cabinet reshuffle. Altice NV is the Stoxx 600’s biggest gainer after the company said it will spin off its U.S. cable-television business

While stocks continue their smooth levitation day after day, there were some fireworks in FX, where first the Yen surged after the BOJ trimmed its purchases of long-dated government bonds, reducing buying of 10-to-25 year debt by 10 billion yen to 190 billion, the first cut in the sector since Dec. 28, 2016, and also scaled back purchases of bonds maturing in more than 25 years by 10 billion yen to 80 billion, stoking speculation it could start to wind down its stimulus policy this year, and resulting in a sharp move higher in the Yen against all its G-10 peers.

Investors sold the USDJPY, with bids on bank platforms hit hard by Tokyo-based leveraged accounts following the BOJ operation, according to Bloomberg. The Japanese currency rose against all of its Group-of-10 peers, while yields for government bonds advanced.

“BOJ’s operation was a trigger for yen gain as it came amid a lack of fresh factors and as people were getting cautious about buying in the 113 levels,” said Hiroshi Yanagisawa, chief analyst at FX Prime by GMO in Tokyo. “FX markets had not paid attention to BOJ last year but there may be some expectations that the situation may be changing a bit this year.”

As central banks in the U.S. and Europe start to normalize monetary policies, attention is turning to Japan to see if the BOJ will follow suit, even if inflation has yet to reach its 2 percent target. The

… followed by the PBOC announcing it was suspending its countercyclical buffer, which in turn resulted in the biggest drop in the offshore yuan since September.

Both moves took analysts by Surprise: since it adopted its yield-curve-control policy in 2016, the BoJ has occasionally tweaked its buying, but some market players seemed to take Tuesday’s move as a signal. “It shouldn’t be perceived as a monstrous signal of the end of monetary easing but it shows that even the tiniest announcement on a quiet day can have a reaction,” said Societe Generale’s global head of currency strategy Kit Juckes. “And it shows that when they start turning their ship around from this policy, the yen is going to go miles.”

Commenting on the PBOC’s move, Goldman’s MK Tang said that it would suggest that “the authorities are ready to allow the CNY to be more market-determined… The recent bout of CNY appreciation before today’s move—which had taken the currency’s strength against the CFETS basket close to the Sep ’17 peak—might also have been viewed as too rapid.”

The dollar, meanwhile, rose for the second day against most other major currencies.

The euro – which last week approached three-year highs – slipped further away from $1.20 to a 10-day low of $1.1941. That was despite the biggest increase in German industrial data since September 2009 and suggested investors were becoming more cautious after a rally that has pushed “long” euro positions to records.

“I don’t think right now levels substantially above $1.20 are justified,” Reichelt said. “I know the market is very optimistic about the euro, but if you look at the data and the central bank, the ECB (European Central Bank) is still on an expansionary path.” Nevertheless, euro zone bond yields rose, with traders also making room for new supply from three of the bloc’s best-rated countries at relatively attractive levels. The yield on the region’s benchmark, German 10-year debt, climbed to 0.44 percent, well above the mid-December level of 0.30 percent.

In geopolitical developments, a North Korea delegation head said that inter-Korean talks were expected to go well and that he hoped to achieve precious results. Furthermore, it was later reported after discussions finished, that North Korea is to send a delegation of high-ranking officials, athletes and cheering squad to the Olympics. The news comes as the WSJ reported on Monday that US Secretary of State Tillerson and Secretary of Defense Mattis are reportedly trying to hold President Trump back from striking North Korea, while National Security Adviser McMaster is in favour of a “bloody nose” attack.

In rates, US 10Y Treasuries come under pressure, with the yield curve steepening following decline in Japanese government bonds as focus turns to heavy global bond supply due this week. As a result, 10-year TSY yields rose as much as 2.4bps to 2.504%, the highest level since March.

In commodities, the focus remained on oil. U.S. crude prices hit their highest since 2015 on Tuesday amid OPEC-led production cuts and a dip in American drilling. WTI crude futures were at $62.16 a barrel at 0951 GMT – 43 cents, or 0.7 percent, above their last settlement. They earlier matched a May 2015 high of $62.56 a barrel.

Beyond equaling that 2015 high, which was a short intra-day spike, Tuesday’s high was the strongest for WTI since December, 2014, at the start of the oil market slump. “Speculators continued to increase their net long in ICE Brent … According to exchange data, speculators increased their position by 4,175 lots to leave them with a record net long of 565,459 lots,” ING bank said. Meanwhile, Brent crude futures were at $68.11 a barrel, 33 cents, or 0.5 percent, above their last close. Brent touched $68.27 last week, its highest since May 2015.

Bulletin headline summary from RanSquawk

- USD is extending recent recovery gains to just over 92.500 amid reports that the PBoC is planning to suspend the counter-cyclical factor in CNY fixes

- Global European equities are trading higher across the board (Eurostoxx 50 +0.2%) with all sectors (ex-energy) in

- the green

- Highlights include APIs, Fed’s Kashkari and supply from the Netherlands, Austria, Germany, UK and the US

Market Snapshot

- S&P 500 futures unchanged at 2,747.00

- STOXX Europe 600 up 0.3% to 399.66

- MSCI Asia up 0.2% to 180.15

- MSCi Asia ex Japan down 0.1% to 589.21

- Nikkei up 0.6% to 23,849.99

- Topix up 0.5% to 1,889.29

- Hang Seng Index up 0.4% to 31,011.41

- Shanghai Composite up 0.1% to 3,413.90

- Sensex up 0.4% to 34,479.65

- Australia S&P/ASX 200 up 0.09% to 6,135.81

- Kospi down 0.1% to 2,510.23

- German 10Y yield rose 0.4 bps to 0.435%

- Euro down 0.2% to $1.1940

- Italian 10Y yield fell 2.2 bps to 1.715%

- Spanish 10Y yield fell 1.8 bps to 1.464%

- Brent futures up 0.2% to $67.88/bbl

- Gold spot down 0.4% to $1,314.76

- U.S. Dollar Index up 0.2% to 92.53

Top Overnight News

- Negotiators from North Korea and South Korea met on Tuesday for talks aimed at making the Olympics a success, a move that could lead to broader discussions on Kim Jong Un’s nuclear program

- North Korea to send athletes, officials to Winter Olympics; says wants to resolve Korean peninsula issues through dialogue and negotiations

- Britain should be granted the “Canada plus plus plus” trade deal that Brexit Secretary David Davis has called for, Italian Economic Development Minister Carlo Calenda said in an interview

- The Bank of Japan is considering raising its economic growth forecast for the fiscal year beginning in April at its policy meeting ending on Jan. 23, Kyodo news reported, without citing its source

- European fund managers have cut their 2018 investment research budgets by 20 percent as they scale back the number of providers they use in response to MiFID II, according to a survey by U.S. consulting firm Greenwich Associates

- Fed’s Bostic says ’two to three’ hikes 2018 base case, need higher inflation to justify 3-4 hikes; caution if yield curve inverting

- Fed’s Williams says U.S. economy has fully recovered from recession; Rosengren says worth assessing if 2% inflation goal still warranted

- U.K. December BRC like-for-like retail sales 0.6% vs 0.3% estimate

- Japan November labor cash earnings 0.9% vs 0.6% estimate

- Australia November building approvals 11.7% vs -1.3% estimate

Asian equity markets traded mostly higher as the region mirrored the tone seen in US, where all majors posted fresh record highs but the DJIA still snapped its New Year streak. ASX 200 (+0.1%) and Nikkei 225 (+0.6%) were positive in which commodity names led in Australia and the Japanese benchmark outperformed as it played catch up on return from the extended weekend. However, some of the gains in Japan were later pared on tapering concerns after the BoJ reduced its Rinban announcement for longer dated bonds. Elsewhere, KOSPI (-0.1%) was dampened after index-heavyweight Samsung Electronics missed on Q4 preliminary results, while both Hang Seng (+0.4%) and Shanghai Comp. (+0.1%) also gained despite initial cautiousness on further inaction by the PBoC which resulted to a net daily drain of CNY 130bln. Finally, 10yr JGBs were lower by about 15 ticks on concern of BoJ tapering after the Rinban announcement saw a reduction of buying in 10yr-25yr maturities to JPY 190bln from JPY 200bln, as well as the amount in 25yr+ maturities which was cut to JPY 80bln from JPY 90bln. As reported earlier, the Yuan tumbled after China announced it would suspend the counter-cyclical factor in the CNY fix. Earlier,the PBoC skipped open market operations again for the 12th day.

Top Asian News

• Richest Asian Banker Plans a Family Office But Spurns Crypto

• UBS Says Investors Won’t Make Money on Indian Stocks This Year

• Geely Auto Expects Full-Year Profit to Double as Sales Surge

• Ruyi Is Said to Lead Bidding for Swiss Luxury Brand Bally

Global European equities are trading higher across the board (Eurostoxx 50 +0.2%) with all sectors (ex-energy) in the green. Performance is relatively broad-based with some slight outperformance in material names. Focus has also been on the UK supermarket sector after the latest trading update from Morrisons (+2.6%) sent their shares to the top of the FTSE alongside the latest Kantar and Nielsen reports. Elsewhere, focus has also fallen on UK homebuilders with Persimmon shares initially supported by upbeat guidance before upside momentum then dissipated. British American Tobacco shares have been supported after stating that the impact of new US tax legislation would result in a benefit of 6% to FY 2018 EPS. A somewhat belated and limp uptick in Bunds and Gilts given the well-received German and UK supply offerings with the only slight fly in the ointment perhaps coming via the 2027 DMO average yield. The rather muted price moves suggest more supply related topside pressure looming ahead of the start of US refunding and with plenty of EU issuance still to come this week, not to mention corporate deals. US Treasuries also seem to have supply in mind with a steeper bias across the maturity curve, and the 10 year yield just crossing 2.5% again.

Top European News

- German Industry Output Rebounds on Strong Investment Demand

- Spanish Emblem of Real-Estate Bust Returns to Market With IPO

- Sweden Has ‘Crazy’ Surplus as Soaring Tax Revenue Swells Coffers

- U.K. Scrimps at Department Stores to Fund Holiday Feasts

- World’s Biggest Covered-Bond Market Tests Extreme Rate Territory

In FX, USD is extending recent recovery gains to just over 92.500, with the Greenback getting a boost from reports that the PBoC is planning to suspend the counter-cyclical factor in CNY fixes, which saw USD/CNH spike to 6.51520 from 6.50340 following the earlier 6.4968 USD/CNY mid-point setting. JPY firmer and the G10 outperformer on reduced Rinban activity overnight which alongside monthly BoJ data suggests a concerted slowdown in JGB buying. USD/JPY down to 112.50 from 113.00+ at one stage, but bids around the low held and broader US Dollar gains now nudging the pair back up towards 113.00 again. EUR is still on the back foot across the board as more long positions are trimmed, with EUR/USD now under 1.1950 and eyeing stops said to be in place at 1.1925. AUD/CAD/NZD all off best levels vs their US counterpart, with AUD/USD above 0.7850 on much better than expected Aussie building approvals data overnight, but now back down under 0.7825, USD/CAD looking firmer over 1.2400 after another dip below the figure (another uptick in oil prices and solid BoC business outlook survey supporting the Loonie) and NZD/USD down around 0.7170 having almost touched 0.7200.

In the commodities complex, WTI and Brent crude prices were initially trading in close proximity to recent highs in a continuation of sentiment yesterday after expectations of a draw of 4.1mln bbls for this week’s inventory data. Furthermore, OPEC officials suggested that the Iran situation was being monitored, and output will only be raised in the event that there is a significant and sustained disruption to output. However, prices then began to be dragged lower after comments from the Iranian energy minister who claimed that OPEC does not want oil prices above USD 60/bbl. In metals markets, the recovery in the USD placed some weight on precious metals (Silver tested USD 17.00/oz to the downside) after a relatively uneventful Asia-Pac session. Elsewhere, Chinese iron ore futures were seen higher overnight as production cutbacks in China continues to sway sentiment. Iran oil minister Zanganeh says OPEC does not want oil prices above USD 60/bbl. Indian Trade Ministry official says comprehensive gold policy will likely be prepared by March and that there is also a likelihood for the recommendation of lower import tax on gold.

Looking at the day ahead, the November unemployment rate for the Eurozone came in (8.7%, Exp. 8.7%, Last 8.8%), along with Germany’s IP (3.4%, Exp. 1.9%, last -1.2%). Over in the US, there is the December NFIB small business optimism index and JOLTS job openings. Onto other events, the Fed’s Kashkari speaks at a moderated panel.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 107.8, prior 107.5

- 10am: JOLTS Job Openings, est. 6,025, prior 5,996

- 10am: Fed’s Kashkari Speaks on Moderated Panel

DB’s Jim Reid concludes the overnight wrap

The eyes of the holders of US equities continue to stream tears of joy at the moment, as yesterday marked the 5th up day out of 5 so far this year for the S&P (+2.77% so far). Since 1928 we’ve only seen the first 5 days of the year to be consecutively up 7 times and this is the first occurrence since 2010. When the first 5 days are up, the average price return for the year is +13.44%, with the low of +2.03% and high of 20.09%. Notably, the longest streak was in 1976 and 1987 when the S&P rose for 7 consecutive days at the start of the year.

Staying in the US, in a quiet week for data leading up to Friday’s CPI, Fed speakers grabbed the headlines yesterday. The Fed’s Bostic seemed dovish and noted “I’m comfortable continuing with a slow removal of policy accommodation”, but “I would caution that doesn’t necessarily mean as many as three or four moves per year”. On inflation, his main concern is that inflation expectations risk becoming anchored below 2% and if this happened, “it would be increasingly difficult for the Fed to hit our 2% target”. In terms of impacts from the tax cuts, he is making a “positive, but modest boost” to his near term GDP growth profile for the coming year, but is treating a more substantial breakout of tax reform related growth as a “upside risk” to his outlook.

Elsewhere, at the Inflation targeting conference, the Fed’s Rosengren said his “own view is that we should be focused on inflation range (rather than the 2% target), with flexibility to move within the range as the optimal inflation rate changes”. He added that a range of 1.5%-3% could provide flexibility and “don’t think most people are going to notice”. The former Fed governor Bernanke also noted there will be “some pretty serious discussions” on monetary policy frameworks over the next 18 months under the new Fed leadership.

Turning to the US’s 4Q17 earnings season kicking off today, our equity strategists expect the S&P’s 4Q EPS growth to rise to near a 6-year high of 14.6% (vs. 3Q: 7.8%), with earnings supported by stronger US and foreign economic growth, a weaker USD, higher oil price and a dissipation of hurricane related losses. On a sector basis, median growth is expected to be led by the energy (+138%), tech (+18.6%) and financial (+16.6%) sectors while growth from industrials is the relative laggard at 4.8%, impacted by GE. Looking to 2018, our team expect the aggregate S&P effective tax rate to fall from 27% to 19%, with all sectors to benefit but the bigger relative beneficiaries are energy, retailing and telco sectors, while the laggards are Pharma, insurance and tech companies. The new 2018 S&P target is 3,000 (c9% above current levels).

Over in Europe, our Economists have published a note posing five key questions for the Euro area in 2018. The first question is whether the euro area’s growth will reach new cyclical highs in 2018? Their answer is “possibly”, as their forecast for CY18 of 2.3% is close to the 2.3%-2.4% that they estimate for CY17, and they see the risks around their forecast as broadly balanced but skewed to the upside in early 2018. Moving on, the team expect 2018 to be a year in which market perceptions of inflation improves, albeit that normalisation may be slow, complicated by rigid inflation regimes in some countries, structural changes and the appreciation of the EUR more recently. Notably, the German wage settlements could influence such perceptions as one third of employees are up for renegotiations in 2018 (in metalwork our team expect a settlement clearly above 3%). Elsewhere, our team also pose questions on: iii) will the ECB be able to engineer a soft landing for financial conditions iv) will “integration” or “exit” be the dominant political theme and v) whether the EU27 and the UK will reach a deal in 2018. For more details, please refer to their report.

This morning in Asia, markets continue to be modestly higher. The Nikkei is up 0.53% after trading resumed post yesterday’s holiday, Hang Seng is up 0.24% while Kospi pared early gains to be down 0.51% as we type. Elsewhere, the North and South Korean delegates have started their first high level talks time since 2015, with discussion topics such as North Korea joining next month’s Winter Olympics.

Now recapping market performance from yesterday. The S&P (+0.17%) and Nasdaq (+0.29%) recovered from earlier losses and edged higher for the fifth consecutive day, while the Dow dipped 0.05%. Within the S&P, modest gains in the utilities and real estate sectors were partly offset by losses in healthcare and financials. European markets were broadly higher, with the Stoxx (+0.27%) and DAX (+0.36%) up modestly, while the FTSE (-0.36%) was weighed down by profit downgrades in the tech and healthcare space.

In government bonds, core 10y European bond yields fell c1bp (Bunds & OATs -0.7bp; Gilts -0.8bp) while treasuries were broadly flat. Peripherals outperformed with Portugal’s 10y yields down 6.7bp, in part due to a reversal of weakness back in the end of 2017. Turning to currencies, the US dollar index gained for the second consecutive day (+0.44%), while Sterling and the Euro weakened 0.04% and 0.52% respectively. In commodities, WTI oil rebounded 0.47% to $61.73/bbl.

Elsewhere, precious metals (Gold +0.06%; Silver -0.55%) and other base metals were mixed, but little changed (Copper +0.04%; Zinc +0.79%; Aluminium -0.47%). Away from markets, an unnamed White House official has told Bloomberg that President Trump is close to making a decision on who to nominate to be the next Vice Chairman for the Fed. Elsewhere, Politico has reported that President Trump’s administration is preparing to unveil an aggressive trade crackdown in the coming weeks that is likely to include new tariffs aimed at countering China and other economic competitors’ alleged unfair trade practices.

In the UK, PM May has reshuffled her cabinet with key posts such as Foreign Secretary Johnson, Brexit Secretary Davis and Chancellor Philip unchanged, but the Education Secretary Justine Greening has quit after the PM has offered her an alternative role – the work and pensions portfolio. Health minister Hunt also persuaded her to change her mind about being moved from his position. Mrs May seemed to start the year with a little bit of momentum but most of the British press has seen yesterday’s reshuffle as shambolic and reflective of her weak political position.

Elsewhere the latest ECB holdings were released yesterday, but there was little relevant info as it only contained a few days of secondary purchases data. Net CSPP purchases last week were €0.3bn and Net PSPP purchases €2.5bn. This left the CSPP/PSPP ratio at 12.4% last week (vs. 11.5% before QE was trimmed in April 2017). We expect more meaningful data from next week when we get the first clues to the PSPP/CSPP taper split post January’s QE cut.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the November consumer credit data rose the most in 16 years, with total credit up $28.0bln (vs. $18bln expected), mainly driven by strong credit card spending which rose the most in 12 months. The confidence indicators for the Eurozone were broadly above market. The December economic confidence index was above expectations at 116 (vs. 114.8) and to the highest since October 2000, with the rise due to an improvement in the outlook for industry and services. The January Sentix investor confidence was also above market at 32.9 (vs. 31.3 expected) – slightly below the 10 year high back in November. Elsewhere, the final reading of consumer confidence was in line at 0.5 while the November retail sales print was above expectations at 2.8% yoy (vs 2.4%). Over in Germany, November factor orders fell 0.4% mom (vs. 0% expected), but prior revisions meant the annual growth remained solid at 8.7% yoy (vs 7.8% expected). In the UK, the December Halifax house price index fell for the first time in six months (-0.6% mom vs. +0.2% expected), so annual growth for the past quarter slowed to 2.7% yoy (vs 3.3% expected).

Looking at the day ahead, the November unemployment rate for the Eurozone and Italy are due, along with Germany’s IP. Then the trade and current account balance stats for France and Germany are also due. Over in the US, there is the December NFIB small business optimism index and JOLTS job openings. Onto other events, the Fed’s Kashkari speaks at a moderated panel.

end

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 4.42 points or 0.13% /Hang Sang CLOSED UP 111.88 pts or 0.36% / The Nikkei closed UP 135.46 POINTS OR 0.57%/Australia’s all ordinaires CLOSED UP 0.08%/Chinese yuan (ONSHORE) closed DOWN at 6.5280/Oil UP to 61.92 dollars per barrel for WTI and 67.86 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.5230. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.5300 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS STILL HAPPY TODAY.(GOOD MARKETS BUT WEAKER YUAN)

3 a NORTH KOREA/USA

NORTH KOREA/SOUTH KOREA

Peace progress. North Korea will be sending a team to the Winter Games much to the chagrin of the uSA. Seoule is also prepared to lift some sanctions against the North.

(courtesy zerohedge)

Peace Progress: North Korea Will Send Team To Winter Games As Seoul Prepares To Lift Some Sanctions

A day after the Wall Street Journal reported that the US officials are debating whether it’d be possible to mount a limited military strike against the North without provoking a nuclear response (maybe but who’d want to risk finding out?), the North said on Tuesday that, following a session of talks with its South Korean neighbors, the isolated country would be sending a delegation of athletes, dignitaries and journalists to the Winter Games in Pyeongchang next month.

While the US has yet to issue a response, such a move will probably infuriate South Korea’s American allies. President Donald Trump and North Korean leader Kim Jong Un have been engaged in an escalating war of words since the former took office a year ago.

According to Reuters, South Korea had unilaterally banned several North Korean officials from entering the country in response to Pyongyang’s nuclear and missile tests, Seoul said if it needs to take “prior steps” to help the North Koreans visit for the Olympics, it would consider it, together with the United Nations Security Council and other relevant countries, foreign ministry spokesman Roh Kyu-deok said during a press briefing.

The agreement comes after North Korea and South Korea last week agreed to reopen a cross-border hotline that had been shuttered for two years.

As the Guardian pointed out, the agreement represents a cautious diplomatic breakthrough after months of rising tensions over Pyongyang’s nuclear weapons program.

The five-member North Korean delegation traveled to the border in a motorcade and then walked across the military demarcation line into the southern side of the truce village of Panmunjom at around 9.30 am local time, the Guardian reported. The village straddles the demilitarized zone (DMZ), the heavily armed border that has separated the two Koreas for more than six decades.

As the two sides sat down for their first face-to-face talks since December 2015, North Korean media pushed back against Trump’s claim that his tough stance on North Korea had forced it to the negotiating table. The Rodong Sinmun, the newspaper of the ruling Workers’ party, said Trump’s claim that sanctions and pressure on the regime had brought him “diplomatic success” during his first year in the White House was “ridiculous sophism”.

After a day of meetings, South Korean news agency Yonhap reported that the two delegations said in a joint statement that they would also engage in military talks, as well as talks pertaining to a whole host of inter-Korean issues. Meanwhile, they also agreed to “resolve problems” through dialogue and negotiation.

Discussions have focused on North Korean participation in the Pyeongchang Winter Games, but are also thought to have included other inter-Korean issues such as the resumption of reunions between family members who were separated at the end of the 1950-53 Korean war. South Korea has suggested holding reunions during the Lunar New Year holidays next month.

At Tuesday’s talks, the first since December 2015, Seoul also proposed inter-Korean military discussions to reduce tension on the peninsula and a reunion of family members in time for February’s Lunar New Year holiday, South Korea’s vice unification minister Chun Hae-sung said quoted by Reuters.

In the past, the Olympics have provided rare moments of unity for the two Koreas. They previously made joint entrances to Olympics opening and closing ceremonies in Sydney in 2000, Athens in 2004 and at the 2006 Winter Games in Turin.

end

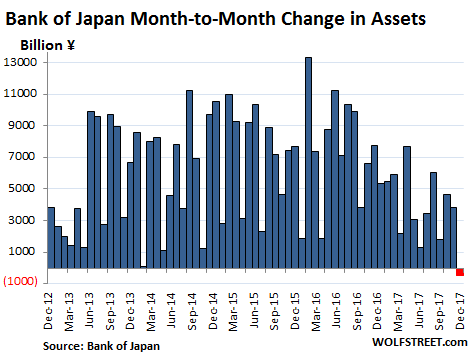

3 b JAPAN AFFAIRS

Oh OH, it started. We have been warning you that Japan is running out of bonds to buy. The Bank of Japan has now begun to taper its bond buying. This sends the yen flying and bond yields rising.

USDJPY, JGBs Tumble After Bank Of Japan ‘Tapers’ Bond-Buying

USDJPY and JGB Futures are tumbling after the Bank of Japan ‘tapers’ its purchasing of longer-dated bonds.

The JPY has strengthened the most since January 2 against the USD:

We previously noted the fact that the QE party was over in Japan as its balance sheet declined for the first time since 2012: under “QQE” – so huge that the BOJ called it Qualitative and Quantitative Easing to distinguish it from mere “QE” as practiced by the Fed at the time – the BOJ has been buying Japanese Government Bonds (JGBs), corporate bonds, Japanese REITs, and equity ETFs, leading to astounding month-end to month-end surges in the balance sheet. But as we showed over the weekend, now the “QQE Unwind” has commenced. Note the trend over the past 12 months and the first dip (red):

And today, the BOJ just announced it trimmed the size of its asset purchases some more, specifically by 10BN yen each in the 10-25 year segment and the more-than-25-years bucket.

Here’s a comparison with previous operations:

- 190b yen of 10-25 year bonds vs 200b on Dec. 28

- 80b yen of bonds maturing in over 25 years vs 90b on Dec. 28

As a result, the JGB yield curve steepened modestly, with the 10-year yield rising 1bp to 0.065% while the 30-year is up 1.5bps to 0.830%.

As Wolf Richter concluded previously, The BOJ has used QQE as an internationally accepted pretext to bring Japan’s public debt under control by effectively removing much of it from the market in order to prevent a Greek-like debt crisis. And so far it has worked.

Japan’s national debt reached 250% of GDP at the end of 2016, by far the highest in the world. Between the JGB holdings by the BOJ and by state-owned institutions, such as the Government Pension and Investment Fund, Japanese authorities now control the majority of Japan’s national debt, and there won’t be a debt crisis – though it could trigger other crises. And it appears that the BOJ decided that this might be enough control. Hence the end of QQE…. at least until the market wakes up and realizes the yet another central bank pillar of support is slowly being pulled out from beneath it and risk assets finally sell off.

c) REPORT ON CHINA

China removes one of the support factors in the yuan fixing and this causes the yuan to fall. It looks like China is ready to have the market determine the value of the yuan.

(courtesy zerohedge)

Yuan Tumbles After China Unexpectedly Suspends “Counter-Cyclical Factor” In FX Fixing

Back on May 26, 2017, shortly after Moody’s downgrade of China, Beijing “moved the goalposts” in its bid to reduce yuan volatility, to punish currency manipulators (read Yuan shorts) and limit capital outflows (the currency had weakened for three straight years, triggering draconian capital controls and the surge of bitcoin) when the PBOC introduced a new “counter-cyclical factor” to reduce exchange-rate volatility while undermining efforts to increase the role of market forces.