GOLD: $1327.15 DOWN $11.85

Silver: $16.94 DOWN 23 cents

Closing access prices:

Gold $1327.25

silver: $16.94

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1334.02 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1326.00

PREMIUM FIRST FIX: $8.02

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1337.38

NY GOLD PRICE AT THE EXACT SAME TIME: $1326.50

Premium of Shanghai 2nd fix/NY:$10.88

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1329.75

NY PRICING AT THE EXACT SAME TIME: $1329.00

LONDON SECOND GOLD FIX 10 AM: $1332.20

NY PRICING AT THE EXACT SAME TIME. $1330.85??

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 19 NOTICE(S) FOR 1900 OZ.

TOTAL NOTICES SO FAR: 468 FOR 46800 OZ (1.4556 TONNES),

For silver:

jANUARY

58 NOTICE(S) FILED TODAY FOR

290,000 OZ/

Total number of notices filed so far this month: 625 for 3,125,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $11,712/OFFER $11,812 UP 609 (morning)

Bitcoin: BID 11,490/OFFER $11,590 UP $364(CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A SMALL 88 contracts TO 196,511 FALLING TO 196,423 WITH YESTERDAY’S 3 CENT FALL IN SILVER PRICING. WE HAD TINY COMEX LIQUIDATION. WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1273 EFP’S FOR MARCH AND ZERO FOR OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1273 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1273 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

32,827 CONTRACTS (FOR 13 TRADING DAYS TOTAL 32,827 CONTRACTS OR 164.135 MILLION OZ: AVERAGE PER DAY: 2525 CONTRACTS OR 12.625 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 164.135 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.4% OF ANNUAL GLOBAL PRODUCTION

RESULT: A SMALL SIZED LOSS IN OI COMEX DESPITE THE 3 CENT FALL IN SILVER PRICE WHICH USUALLY INDICATES ANOTHER FAILED BANKER SHORT-COVERING. WE ALSO HAD A HUGE SIZED EFP ISSUANCE OF 7310 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX . FROM THE CME DATA 1273 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 1185 OI CONTRACTS i.e. 1273 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 88 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 3 CENTS AND A CLOSING PRICE OF $17.17 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.9820 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 58 NOTICE(S) FOR 290,000 OZ OF SILVER

In gold, the open interest ROSE BY A CONSIDERABLE 8865 CONTRACTS UP TO 591,198 WITH THE SMALL RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($2.20). IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED TUESDAY FOR WEDNESDAY AND IT TOTALED A GOOD SIZED 6902 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 6902 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS The new OI for the gold complex rests at 591,198. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE ANOTHER MONSTROUS GAIN OF 15,767 OI CONTRACTS: 8865 OI CONTRACTS INCREASED AT THE COMEX AND AN GOOD SIZED 6902 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 23,183 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 128,850 CONTRACTS OR 12.885 MILLION OZ OR 409.04 TONNES (13 TRADING DAYS AND THUS AVERAGING: 9911 EFP CONTRACTS PER TRADING DAY OR 991,100 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 13 TRADING DAYS: IN TONNES: 409 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 409/2200 TONNES = 18.59% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX WITH THE SMALL RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($2.20). WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6902. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6902 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 15,767 contracts ON THE TWO EXCHANGES:

6902 CONTRACTS MOVE TO LONDON AND 8865 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 49.04 TONNES)

we had: 19 notice(s) filed upon for 1900 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WOW!!, with gold down $11.85, the GLD people added a whopping 11.80 paper tonnes/ there is absolutely no way that they were going to obtain almost 12 tonnes of physical gold overnight.

Inventory rests tonight: 840.96 tonnes.

SLV/

a BIG CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 848,000 OZ FROM THE SLV/

INVENTORY RESTS AT 315.500 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A SMALL 88 contracts from 196,511 UP TO 196,423 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN PRICE OF SILVER TO THE TUNE OF 3 CENTS WITH RESPECT TO YESTERDAY’S TRADING. OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1273 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 88 CONTRACTS TO THE 1273 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 1185 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 5.925 MILLION OZ!!!

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE SMALL FALL OF 3 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1273 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 30.08 points or 0.87% /Hang Sang CLOSED UP 138.53 pts or 0.43% / The Nikkei closed DOWN 104.94 POINTS OR 0.44%/Australia’s all ordinaires CLOSED DOWN 0.06%/Chinese yuan (ONSHORE) closed WELL UP at 6.4227/Oil UP to 64.05 dollars per barrel for WTI and 69.33 for Brent. Stocks in Europe OPENED ALL RED. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4227. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4201//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(GOOD MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)/South Korea/North Korea/USA

b) REPORT ON JAPAN

3 c CHINA

China’s latest GDP numbers beat the street but retail sales are slumping. There is renewed fears that much of the data is fake

( zero hedge)

4. EUROPEAN AFFAIRS

i)Germany

We have discussed at length Japan’s demographic problems of an aging population and low fertility rates. Germany will be the second nation to have a demographic aging population

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

iii)USA will not like this: Syria vows to shoot down Turkish jets as Erdogan orders Putin not to engage.

6 .GLOBAL ISSUES

i SWEDEN

Sweden has had enough as they are preparing for a civil war as they are now going to enter the “no go zones”

( zerohedge)

ii)Horseman Capital are really smart guys. It;s chairman Russell Clark has a stunning theory as to what is going to happen next to the USA dollar and it is not pretty.

a must read…

(Russell Clark/Horseman Capital)

7. OIL ISSUES

Opec oil production rose in December despite a huge plunge in Venezuelan production

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The dollar weakness is unsettling many central banks

( Roger Blitz/London’s financial times)

ii)Dave Kranzler highlights reasons why 2018 will be a good year for both gold/silver

( Kranzler/IRD/GATA)

10. USA stories which will influence the price of gold/silver

i)Soft data Fed Philly Manufacturing index slumps to its weakest level in over a year. The hope category tumbles

( zerohedge)

( zerohedge)

iii)Trump backtracks again: the USA will not be moving its embassy to Jerusalem this year

( zerohedge)

iv)it does not look good as the Republicans are running out of options even with the Continuing Resolution Bill as the Democrats are holding out for a immigration deal e.g. DACA

(courtesy zerohedge)

v)Is American Express suspending its buyback because they are worried about defaulting consumers?

(courtesy zerohedge)

vi)SWAMP STORIES

a)Now the FBI is investigation millions of dollars funneled from the Australian government to the Clinton foundation

( zerohedge)

vii)ICE plans the largest raid on Northern California illegals immediately after the state passed sanctuary legislation. The next few weeks should be interesting( zerohedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY A CONSIDERABLE 8865 CONTRACTS UP to an OI level of 591,198 WITH THE RISE IN THE PRICE OF GOLD ($2.20 GAIN WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ZERO COMEX GOLD LIQUIDATION. WE ALSO WITNESSED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE. THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT A GOOD SIZED 6902 EFP’S WERE ISSUED FOR FEBRUARY , 0 EFP’s FOR APRIL, AND 0 FOR DECEMBER: TOTAL 6902 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 15,767 OI CONTRACTS IN THAT 6902 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 8865 COMEX CONTRACTS. NET GAIN ON THE TWO EXCHANGES: 15,767 contracts OR 1.5767 MILLION OZ OR 49.04 TONNES

Result: A CONSIDERABLE INCREASE IN COMEX OPEN INTEREST WITH THE RISE IN THE PRICE YESTERDAY’S GOLD TRADING ($2.20.) WE HAD NO GOLD LIQUIDATION AT THE COMEX. HOWEVER WE, NO DOUBT WE HAD ANOTHER FAILED BANKER SHORT COVERING .. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 15,767 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest RISE by 6 contracts RISING AT 46. We had 0 notices served upon yesterday so we gained 6 contracts or an additional 600 oz of gold will stand AT THE COMEX in this non active month of January AND QUEUE JUMPING INTENSIFIES.

FEBRUARY saw a LOSS of 7083 contacts DOWN to 312,806. March saw a GAIN of 68 contracts UP to 553. April saw a GAIN of 13,615 contracts UP to 164,221.

We had 19 notice(s) filed upon today for 1900 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 332,362

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 437,065

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY 88 CONTRACTS FROM 196,511 UP TO 196,423 WITH YESTERDAY’S 3 CENT FALL. NOT ONLY THAT, WE HAD ANOTHER GOOD SIZED 1273 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1273. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD TINY LONG COMEX SILVER LIQUIDATION BUT A RISE IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1185 OPEN INTEREST CONTRACTS:

88 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1273 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 1185 CONTRACTS

We are now in the poor non active delivery month of January and here the OI GAINED 6 contracts RISING TO 68. We had 52 notices served upon yesterday, so we GAINED 58 contracts or an additional 290,000 oz will stand for delivery

February saw a GAIN OF 39 OI contracts RISING TO 222. The March contract LOST 673 contracts DOWN to 139,496.

We had 58 notice(s) filed for NIL 290,000 for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 18/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

324,357.372 oz

JPMORGAN

(10 TONNES)

|

| No of oz served (contracts) today |

19 notice(s)

1900 OZ

|

| No of oz to be served (notices) |

27 contracts

(2700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

468 notices

46800 oz

1.4556 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 19 contract(s) of which 8 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (468) x 100 oz or 46800 oz, to which we add the difference between the open interest for the front month of JAN. (46 contracts) minus the number of notices served upon today (19 x 100 oz per contract) equals 49,500 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (468 x 100 oz or ounces + {(46)OI for the front month minus the number of notices served upon today (19 x 100 oz which equals 49,500 oz standing in this active delivery month of JANUARY (1.5396 tonnes). THERE IS 18.245 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 6 CONTRACTS OR AN ADDITIONAL 600 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 60 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

676,194.099 oz

Brinks

CNT

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

635,396.900 oz

JPMORGAN

|

| No of oz served today (contracts) |

58

CONTRACT(S)

(290,000 OZ)

|

| No of oz to be served (notices) |

11 contracts

(55,000 oz)

|

| Total monthly oz silver served (contracts) | 683 contracts

(3,415,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) JPMorgan continues to add silver to its inventory:

Deposit: 635,396.900 oz

total inventory deposits: 635,396.900 oz

we had 3 withdrawals from the customer account;

i) out of Brinks; 1989.100 oz

ii) Out of CNT: 669,015.527 oz

iii) Out of Delaware: 5188.972 oz

total withdrawals; 676,194.099 oz

we had 0 adjustments

total dealer silver: 45.456 million

total dealer + customer silver: 246.311 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 58 contract(s) FOR 290,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 683 x 5,000 oz = 3,415,000 oz to which we add the difference between the open interest for the front month of JAN. (69) and the number of notices served upon today (58 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 683(notices served so far)x 5000 oz + OI for front month of JANUARY(69) -number of notices served upon today (58)x 5000 oz equals 3,470,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 58 CONTRACTS OR AN ADDITIONAL 290,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3.790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 92,605

CONFIRMED VOLUME FOR FRIDAY: 105,638 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 105,638 CONTRACTS EQUATES TO 528 MILLION OZ OR 75.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -0.95% (Jan 17/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.51% to NAV (Jan 17/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -0.95%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.51%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

3. SPROTT CEF.A FUND (PURCHASED FROM CENTRAL FUND OF CANADA

NAV $13,85 CDN/TRADING: $13.45 : DISCOUNT TO NAV 2.02%

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 18/2018/ Inventory rests tonight at 840.76 tonnes

*IN LAST 311 TRADING DAYS: 100.19 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 246 TRADING DAYS: A NET 57.12 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 18/2017:

Inventory 315.500 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.78%

12 Month MM GOFO

+ 2.08%

30 day trend

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

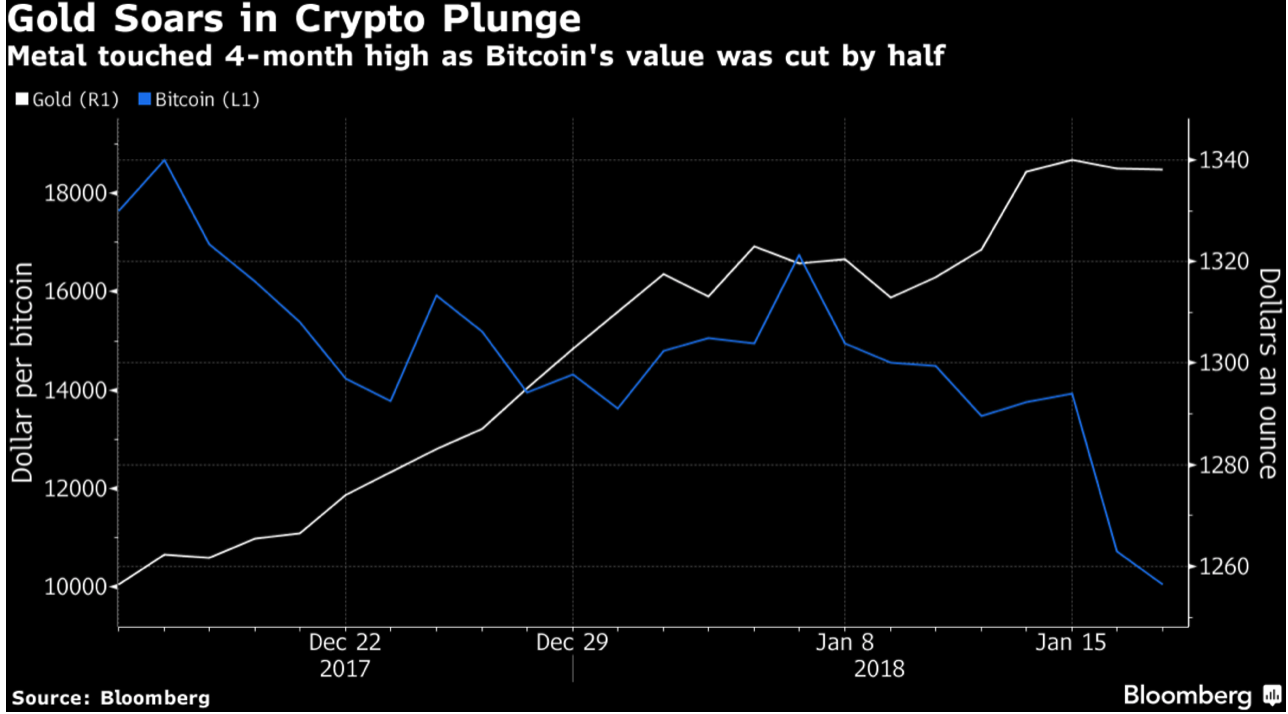

Digital Gold Flight To Physical Gold Coins and Bars

‘Digital Gold’ Bitcoin Flight To Safe Haven Physical Gold

– Latest bitcoin, crypto crash causes gold coin and bar demand to surge

– Bitcoin down 40% from high, Ripple down 50% and Ethereum down 30%

– Ripple and ‘Digital gold’ Bitcoin fall past key psychological price levels

– $300bn wiped from cryptocurrency fortunes in just 36 hours

– New research says that there is ‘Price Manipulation in the Bitcoin Ecosystem’

– Savvy crypto buyers converted their short term gains into physical gold bars, coins

– Bitcoin and Ripple sellers bought gold both for delivery and storage from GoldCore

– Gold ETF holdings rise – Assets in iShares Gold soar to $10.7 b, highest in 5 years

– 95% of cryptocurrencies will go to zero …

Editor: Mark O’Byrne

30% to 50% price drops in a matter of days and the loss of $300 billion in value is quite a knock for a market that was not meant to be in a speculative bubble.

In just 36 hours the cryptocurrency market has managed to make a fair few people feel very nervous as they watched crypto currency prices fall very sharply.

The two most popular cryptocurrencies (as measured by market cap) saw the biggest losses over Tuesday and Wednesday, this week. Digital gold bitcoin dropped below it’s key psychological level of $10,000, whilst ether also made a drop below the all-important level of $1,000.

The crypto market has been on a tear for the last few months. We are frequently asked by people about bitcoin and whether or not they ‘should’ be getting into it.

Gold is the best way to secure value from crypto volatility

Unsurprisingly many cryptocurrency buyers or investors have been looking at how they can secure their gains. Since early December and continuing in recent days, we are seeing numerous existing and new clients who had seen massive gains in bitcoin, ripple etc diversifying into physical gold. They have been buying both gold coins and bars, for both delivery and storage.

One high net worth British entrepreneur involved in tourism sold a substantial amount of bitcoin and bought kilo bars (gold) for storage in Zurich. Another tech entrepreneur told us he was selling Ripple after having very large profits and a “nine bagger” meaning his initial punt on Ripple had surged nine times. He bought a substantial amount , over 100, of gold maple leaf coins for insured delivery.

Ripple lost 50% of value in one day

It’s not just digital gold bitcoin gains that have people diversifying into gold. In the last two weeks, we have had a few clients who had seen huge short term gains in Ripple diversify back into gold.

They told us they were concerned that the massive price appreciation was unsustainable and they got nervous about it and decided it was a good time to sell and take some profits. This was a fortuitous move given XRP (the Ripple currency) lost 50% of its value on Tuesday alone.

Source: Coinmarketcap.com

This price action (along with the other major cryptocurrencies) has got many asking as to where the value in a cryptocurrency really is. Some in the newly rich crypto community are recognising that it is about realising real value when you cash out and place it into real assets such as gold and silver.

Those we have spoken to and have assisted in recent weeks are selling a very overvalued asset and putting it into a still undervalued asset. Gold prices remain quite depressed, especially from where they were compared to six or seven years ago, and sentiment is still quite poor.

There is a definitely a trend there and we think that trend is likely to continue given the overvaluation of crypto currencies and the undervaluation of precious metals.

This trend is already playing through the price of gold which has been on a winning streak just as cryptos begin to fall out of favour (see chart above).

It is also being seen in a sharp increase for gold coins and bars as reported by Bloomberg overnight.

There are people in the cryptocurrency industry that have been trying to position cryptocurrencies as alternatives to gold and indeed as “digital gold.” We think increasingly people are realizing that these digital assets have much higher risk levels than the traditional safe haven asset – gold.

Risk of manipulation

As we explained earlier this week, there are some dodgy dealings and market manipulation going on in the world of precious metals namely silver but also gold. Whilst it is a disconcerting prospect, the beauty of it is that precious metal investors can take advantage of it and secure physical silver and gold at relatively low prices, in preparation for the coming bull markets.

However, when it comes to the manipulation of digital or ‘paper’ assets then it doesn’t work out so well for the average investor. One of the reasons so many of the early adopters took to bitcoin wasn’t just because it was a cheap punt but also because it was supposedly more secure and offered a more honest form of exchange than those currently seen in the wider financial world.

Yet it has been victim to a number of security breaches and even price manipulation scandals. A new paper by researchers at Tel Aviv University and the University of Tulsa finds that bitcoin has been victim to price manipulation.

In a paper entitled ‘Price Manipulation in the Bitcoin Ecosystem’ , they find that ‘Suspicious trades on a Bitcoin currency exchange are linked to rises in the exchange rate.’

Making particular reference to the infamous Mt Gox debacle they analyse:

the impact of suspicious trading activity on the Mt. Gox Bitcoin currency exchange, in which approximately 600,000 bitcoins (BTC) valued at $188 million were fraudulently acquired. During both periods, the USD-BTC exchange rate rose by an average of four percent on days when suspicious trades took place, compared to a slight decline on days without suspicious activity. Based on rigorous analysis with extensive robustness checks, the paper demonstrates that the suspicious trading activity likely caused the unprecedented spike in the USD-BTC exchange rate in late 2013, when the rate jumped from around $150 to more than $1,000 in two months.

So bitcoin might be vulnerable to manipulation and not be as unbreakable after all.

From digital gold to real physical gold

As we have explained repeatedly, bitcoin (or any other crypto) is not a substitute for gold or silver. But, they can have a complementary relationship as we are seeing today.

Bitcoin and crypto currencies are digital assets. Most are no more secure in terms of value or pricing than any other form of digital gold, stock or ETF. However, many of those who choose to hold cryptocurrencies do so for the same reason many choose precious metals – because they wish to diversify outside of the global monetary and financial system.

Physical gold and silver bullion that is allocated and segregated in your name is the best way to guarantee the securing of the profits achieved from and wealth created by cryptocurrencies.

Most crypto currencies have little real value whatsoever other than to make hard and fast profits from – or indeed hard and very large losses.

The lesson here is to take profits on overvalued assets – be they cryptos, stocks, bonds or property. Sell over valued assets and buy undervalued assets. Rebalance investments and diversify into undervalued assets such as gold bullion – the proven safe haven.

Related Reading

Here’s Why Bitcoin Won’t Replace Gold So Easily

Up to 95 Percent of Cryptocurrencies ‘Will Drop to Zero’ – GoldCore

Goldnomics Podcast – Gold, Stocks, Bitcoin in 2018. Everything Bubble Bursts?

Gold On The Blockchain – For Now Caveat Emptor

News and Commentary

Gold Rally May Have More Room to Run – GoldCore (Bloomberg.com)

Bitcoin’s Nouveau Riche Run to Gold as Cryptocurrency Crashes (Bloomberg.com)

Gold treads lower as dollar gains on stronger U.S. data (Reuters.com)

Fed’s Beige Book finds muted reaction to Republican tax plan (MarketWatch.com)

Homebuilder Sentiment in U.S. Cools in January From 18-Year High (Bloomberg.com)

Source: Sputnik

Did Bitcoin Just Burst? How It Compares to History’s Big Bubbles (Bloomberg.com)

Wall Street Has a $1.7 Billion Bet on the Rising Risk of Grid Attacks (Bloomberg.com)

VIX Surges To Highest Since 2015’s Flash-Crash Versus Europe (ZeroHedge.com)

Gold Prices (LBMA AM)

18 Jan: USD 1,329.75, GBP 961.14 & EUR 1,088.40 per ounce

17 Jan: USD 1,337.35, GBP 969.45 & EUR 1,092.48 per ounce

16 Jan: USD 1,334.95, GBP 970.38 & EUR 1,091.32 per ounce

15 Jan: USD 1,343.00, GBP 971.93 & EUR 1,092.93 per ounce

12 Jan: USD 1,332.90, GBP 978.75 & EUR 1,099.78 per ounce

11 Jan: USD 1,319.85, GBP 978.14 & EUR 1,104.45 per ounce

10 Jan: USD 1,321.65, GBP 976.96 & EUR 1,103.31 per ounce

Silver Prices (LBMA)

18 Jan: USD 17.09, GBP 12.31 & EUR 13.96 per ounce

17 Jan: USD 17.21, GBP 12.49 & EUR 14.10 per ounce

16 Jan: USD 17.10, GBP 12.43 & EUR 13.99 per ounce

15 Jan: USD 17.12, GBP 12.58 & EUR 14.14 per ounce

12 Jan: USD 17.12, GBP 12.56 & EUR 14.12 per ounce

11 Jan: USD 17.01, GBP 12.64 & EUR 14.24 per ounce

10 Jan: USD 17.13, GBP 12.64 & EUR 14.27 per ounce

Recent Market Updates

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– London Property Crash Looms As Prices Drop To 2 1/2 Year Low

– Gold Bullion Up 1% In Week, Heads For 5th Weekly Gain As Bonds Sell Off

– Gold Prices Rise To $1,326/oz as China U.S. Treasury Buying Report Creates Volatility

– Gold Hits All-Time Highs Priced In Emerging Market Currencies

– World is $233 Trillion In Debt: UK Personal Debt At New Record

– 10 Reasons Why You Should Add To Your Gold Holdings

– Spectre, Meltdown Highlight Online Banking and Digital Gold Risks

– Palladium Prices Surge To New Record High Over $1,100 On Supply Crunch Concerns

– Gold Has Best Year Since 2010 With Near 14% Gain In 2017

– Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

– 98,750,067,000,000 Reasons to Buy Gold in 2018

– Gold, Bitcoin and the Blockchain Replaces the Banks – Realists Guide To The Future

END

The dollar weakness is unsettling many central banks

(courtesy Roger Blitz/London’s financial times)

Dollar’s weakness unsettles central bankers

Submitted by cpowell on Wed, 2018-01-17 14:21. Section: Daily Dispatches

All they have to do is rig gold down some more.

* * *

By Roger Blitz

Financial Times

Wednesday, January 17, 2018

The persistent weakness of the U.S. dollar is forcing global central bankers to step up their efforts in warning about the cost of currency appreciation on their economies.

The dollar’s decline has extended into 2018, with the index measuring the currency against its leading peers touching a three-year low. The decline in the global reserve currency matters greatly for other economies that have rebounded thanks to stronger exports, such as Europe and Japan.

The euro, which rose by as much as 2.7 percent since the start of the year, dropped sharply from an intraday high of $1.2322 today after Vitor Constancio, European Central Bank vice president, became the latest policymaker to take issue with the single currency’s sharp rise against the dollar.

“I am concerned about sudden movements [in the euro] which don’t reflect changes in fundamentals,” he said.

Ewald Nowotny, fellow ECB member, added that the euro’s rise was “not helpful.” The euro was trading 0.4 percent lower today. …

… For the remainder of the report:

https://www.ft.com/content/23dbe094-fb79-11e7-9b32-d7d59aace167

END

Dave Kranzler highlights reasons why 2018 will be a good year for both gold/silver

(courtesy Kranzler/IRD/GATA)

Dave Kranzler: 2018 should be bullish for the precious metals sector

Submitted by cpowell on Wed, 2018-01-17 18:27. Section: Daily Dispatches

By Dave Kranzler

Investment Research Dynamics, Denver

Wednesday, January 17, 2018

Usually I’m loathe to stick out price targets on the markets, especially gold and silver, because of the undeniable market intervention of the central banks — market manipulation that is so blatant now that it is denied only by card-carrying idiots.

Gold and silver had a sharp run-up in the last two weeks of 2017. But the abrupt move in gold was accompanied by a rapid rise in the gold futures open interest on the Comex. The “commercial” net short position in Comex gold futures — that is, the position of “the banks — has increased by 100,000 contracts (from 120,000 net short to 220,000 net short) in just four weeks through the most recent commitment-of-traders report. That’s a net paper gold short of 22 million ounces, or 623 tonnes of paper sold short.

As of yesterday the open interest in gold futures increased another 27,000 contracts, most of which, based on the trend in the COT positions, can be attributed to a continued increase in bank short interest.

To put this paper gold short position in perspective, the Comex reports that its warehouses “safekeep” 9.2 million ounces of gold. (This number is unaudited.) That’s 11 million ounces less than the bank net short position. However, only 586,000 ounces of gold are reported to be “registered,” or available for delivery. The ratio of the paper gold short to deliverable gold is 37:1.

In other words, each ounce of deliverable gold has been “hypothecated” and resold 37 times. …

… For the remainder of the commentary:

http://investmentresearchdynamics.com/2018-should-be-bullish-for-the-pre…

END

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.4227 /shanghai bourse CLOSED UP AT 30.08 POINTS 0.87% / HANG SANG CLOSED UP 138.53 POINTS OR 0.43%

2. Nikkei closed DOWN 104.94 POINTS OR 0.44% /USA: YEN FALLS TO 110.73

3. Europe stocks OPENED MIXED /USA dollar index FALLS TO 90.54/Euro RISES TO 1.2235

3b Japan 10 year bond yield: FALLS TO . +.084/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.73/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.05 and Brent: 69.33

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.577%/Italian 10 yr bond yield UP to 1.983% /SPAIN 10 YR BOND YIELD DOWN TO 1.483%

3j Greek 10 year bond yield FALLS TO : 3.781?????????????????

3k Gold at $1328.75 silver at:17.06: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 22/100 in roubles/dollar) 56.63

3m oil into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.22 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9601 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1746 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.577%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.607% early this morning. Thirty year rate at 2.8830% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

All Eyes On The 10Y Treasury Which Is Blowing Above 2.60%, Nears Gundlach’s ‘Redline’

The meltup continues: European stocks edged higher as Asian shares traded mixed, while U.S. equity futures point to another open in record territory. However, today’s story may not be stocks, but rather rates as U.S. bonds extended the Wednesday selloff with the 10-year Treasury yield climbing above 2.6% for the first time since March to help the dollar hold Wednesday’s gain.

The catalyst for the ongoing selling in the rates complex was China, and specifically the barrage of Chinese data reported overnight.

For the better part of the past decade, “bad news was good news” for stocks as it meant more central bank support. Now, good news is even better news – at least until central banks realize they can’t withdraw – and the push into new record highs across global risk assets overnight is being attributed to the latest set of stronger than expected Chinese economic data released overnight, which beat across the board with the exception of retail sales.

China GDP YoY BEAT: +6.8% vs +6.7% exp (+6.8% prior)

China Industrial Production YoY BEAT: +6.2% vs +6.1% exp (+6.1% prior)

China Retail Sales YoY MISS: +9.4% vs +10.2%% exp (+10.2% prior) – lowest since Feb 04

China Fixed Assets Investment YoY BEAT +7.2% vs +7.1% exp (+7.2% prior)

However, as we said yesterday, despite the occasional blip the trend remains all too clear.

As a result, and as Bloomberg confirms, the Treasury curve is in focus as 10Y yield breaks above the key 260bps level – which Jeff Gundlach last week dubbed as a red line for not only an accelerated selloff but the level above which it will start hurting equities – leading curve steeper as Apple repatriation announcement remains in focus with speculation the firm may have to sell some Treasuries to pay the tax liability.

Treasuries also retreated amid hopes that U.S. lawmakers will strike a deal to avert a government shutdown before temporary funding runs out on Friday, after Chief of Staff Kelly said the GOP has the needed votes to pass the stopgap bill. China’s better-than-expected data only added to the narrative of synchronized expansion, which – alongside upbeat profit expectations – could mean the bull run in stocks going until 2019 or beyond, according to a Bank of America survey of fund managers.

In response to the push higher in US yields, Germany’s 10-year bond yield, the benchmark for the region, was near a 5-1/2 month top at 0.52%.

Away from the bond reaction, most Asian equity bourses were closing when the Chinese data landed but had briefly set a new an all-time record after the U.S. bluechip Dow Jones Industrial index had closed above 26,000 points for the first time.Australia’s ASX 200 (Unch.) and Nikkei 225 (-0.7%) both gained at the open in which the Japanese benchmark briefly rose above the 24000 level for the first time in around 27 years, although both then pared gains with Japanese stocks sliding into the close, while commodity-related stocks in Australia were dampened by disappointing production updates from Whitehaven Coal and Woodside Petroleum. Elsewhere, Hang Seng (-0.1%) and Shanghai Comp. (+0.5%) were varied in anticipation of tier-1 China data releases including GDP in which officials including Premier Li had suggested the economy grew 6.9% for 2017. China’s yuan finished at its highest since December 2015.

Europe’s main FTSE, Dax and CAC40 stock markets then ticked higher though moves were choppy in the cross currents of rising euro and bond yields. The euro strengthened while European stocks were mixed, with the technology sector lifted by Infineon (+4.5%) after upgrade by Goldman. The FTSE 100 was struggling thus with the index dragged down by the likes of Whitbread after a soft earnings report

“The likelihood we have higher inflation data in the big economies is well over 50 percent so that is the next turning point for the markets,” SEB investment management’s global head of asset allocation Hans Peterson told Reuters. He added there were now two big questions. How will central banks respond and will the rise in bond yields happen at such a pace that it impacts optimism around assets like equities?

“We are going to change the regime probably within the next 2-3 months,” he said. “Will it be accompanied by rising producer prices then we can live with higher bond yields, otherwise it is a problem for us.”

In FX, the break higher in U.S. yields, supposedly launched by news of Apple’s cash repatriation even if as Morgan Stanley explained the market reaction was wrong, helped the dollar rise from a three-year low hit earlier in the day in Asia. The euro last stood nearly 1.225 but below a peak of $1.2323 set on Wednesday, the euro’s strongest level since December 2014.

A number of top ECB policymakers were due to speak in Frankfurt. Some may have been caught off guard by the speed of the euro’s appreciation, said Lee Jin Yang, macro research analyst for Aberdeen Standard Investments in Singapore. “Maybe they are trying to manage volatility or slow down the rise,” Lee said referring to Austria’s Ewald Nowotny who told reporters on Wednesday that the euro’s recent strength against the dollar was “not helpful.”

Emerging markets were gearing up meanwhile for a number of key interest rate meetings including in Turkey where last year’s 18 percent slump in the lira versus the euro has got inflation back in double digits. South Africa’s central bank also meets. After being sickly for much of 2017, a sounder political backdrop has seen the rand surge. ZAR is one of the best performing currencies in the world so far this year, fuelling talk of a possible rate cut.

“The South Africa meeting is the big show today. People are in it, they want to like it they want to own it,” said UBP’s EM macro and FX strategist Koon Chow. “So any dovishness or a cut would be another trigger for another leg higher.”

The rising U.S. bond could cause turbulence for EM debt markets, however. As well as the gains for benchmark Treasuries, The two-year yield US2YT=RR hovered at a nine-year high of just over 2 percent. “In emerging markets we are trained like dogs,” Chow said about the rising yields. “When we hear that bell ring we want to just run,”

In commodities, crude oil prices rose earlier on data showing a decline in U.S. crude inventories and as rebels in Nigeria threatened to attack the country’s petroleum infrastructure, before trimming their gains. U.S. crude futures were 2 cents higher at $63.99 a barrel have hit a three-year high of $64.89 on Tuesday. Spot gold was down 0.1 percent at $1,327.56 an ounce, with the dollar’s bounce pulling it back from a four-month high of $1,344.43 set on Monday.

IBM, Morgan Stanley and American Express are among companies scheduled to publish earnings. Economic data due include housing starts and jobless claims.

Top overnight news from BBG

- A small shift is taking place in internal discussions among Bank of Japan policy makers, with a minority raising the need to eventually start discussing policy normalization, even though they agree the current stimulus program must continue unchanged for some time, according to people familiar

- Republicans are betting Democrats won’t risk forcing the government to shutter during an election year to press their demand for a deal on immigration by Friday’s funding deadline.

- Theresa May’s hopes of thawing frosty relations with Donald Trump at a meeting on the slopes of Davos next week look to be fading, according to people familiar with the matter.

- China’s holdings of Treasuries fell to a four-month low even as its foreign-exchange holdings increased in November, in a potential sign the world’s second-largest economy is curbing its appetite for U.S. government debt

- Barclays Plc is eliminating as many as 100 senior staff at its underperforming investment bank division; cutbacks will fall mainly at the managing director and director levels and are evenly split between Europe and the U.S., according to people familiar with the decision

Market Snapshot

- S&P 500 futures down 0.09% to 2,801.25

- Brent Futures down 0.09% to $69.32/bbl

- Gold spot up 0.1% to $1,328.76

- U.S. Dollar Index up 0.2% to 90.71

- STOXX Europe 600 up 0.07% to 398.25

- MSCI Asia Pacific down 0.3% to 182.18

- MSCI Asia Pacific ex Japan up 0.2% to 595.48

- Nikkei down 0.4% to 23,763.37

- Topix down 0.7% to 1,876.86

- Hang Seng Index up 0.4% to 32,121.94

- Shanghai Composite up 0.9% to 3,474.75

- Sensex up 0.5% to 35,258.78

- Australia S&P/ASX 200 down 0.02% to 6,014.57

- Kospi up 0.02% to 2,515.81

- German 10Y yield rose 2.2 bps to 0.584%

- Euro up 0.3% to $1.2218

- Brent Futures down 0.09% to $69.32/bbl

- Italian 10Y yield rose 2.9 bps to 1.732%

- Spanish 10Y yield rose 0.5 bps to 1.507%

Asia stocks were mixed as the region faltered in late trade and gave up the momentum from Wall St. where the S&P 500 and DJIA closed above 2800 and 26000 respectively amid earnings optimism, as well as reports that Apple is to repatriate some of its cash holdings and invest in the US. ASX 200 (Unch.) and Nikkei 225 (-0.7%) both gained at the open in which the Japanese benchmark briefly rose above the 24000 level for the first time in around 27 years, although both then pared gains with Japanese stocks sliding into the close, while commodity-related stocks in Australia were dampened by disappointing production updates from Whitehaven Coal and Woodside Petroleum. Elsewhere, Hang Seng (-0.1%) and Shanghai Comp. (+0.5%) were varied in anticipation of tier-1 China data releases including GDP in which officials including Premier Li had suggested the economy grew 6.9% for 2017. Finally, 10yr JGBs were flat uneventful with early short-covering seen in prices after yields rose to a 6-month high of above 0.08%. Furthermore, mixed 30yr auction results and source reports that some at the BoJ were said to see a need for future normalization talks, failed to garner a reaction, as they also agreed that current stimulus was needed for the time-being.

Top Asian News

- Some at BOJ Are Said to Flag Need for Future Normalization Talks

- Pimco, Goldman Asset See China as Threat to Emerging Bonds

- Celebrity Eye Clinic Quintuples in Four Days After Hong Kong IPO

- Battle of K-Pop Stocks: ‘Twice’ Girl Group Agency Now No. 2

- India Steel Ministry Seeks Abolition of Met Coal Import Tax

- ‘Terminator’ Lourenco Proves He’s No One’s Puppet in Angola

- China Banks Boost H-Share Gains as GDP Growth Comes in Strong

European equities are inching higher this morning following on from the bounce back seen on Wall Street, which had stemmed from reports that Apple are to pledge a USD 350bln contribution to the US economy. Additionally, optimism over a potential passing of a stop-gap funding bill to prevent a government shutdown also buoyed demand for equities. Elsewhere, encouraging Chinese GDP data helped aid sentiment with China reporting the fastest growth in 2yrs. IT names outperforming in Europe with Infineon shares rising some 4% after a positive note out from Goldman Sachs. FTSE 100 struggling thus with the index dragged down by the likes of Whitbread after a soft earnings report. Meanwhile, more downside pressure in the debt markets, and US Treasury led as the 10 year benchmark yield inches another basis point closer to the 2.63-64% area that many chartists and cash traders have been flagging if not targeting. Bunds have now been down to 160.32, -1/2 point on the day and just 2 ticks shy of tech support that stands in front of the January low so far at 160.11. Accordingly, 10 year German yields are within a whisker of 0.6%, albeit on the relatively new 2028 bond.

Top European News

- BP Signs Iraq Deal to Help Increase Oil Output at Kirkuk Fields

- Weidmann’s Fiscal Ideas May Cap German Yields

- Countrywide Tumbles on Warning; Foxtons, Rightmove Also Drop

- UBS Rises; Credit Suisse Sees UHNW Boost, Says Buyback Likely

In FX, the USD Index extended recovery gains to just over 91.000 overnight, but quickly backed off again despite supportive impulses via data, rising Treasury yields and another solid Fed Beige Book. The Greenback is now relatively mixed within ranges vs G10 counterparts, around 1.2200 against the Eur, 111.25 vs the Jpy and with Cable back down between 1.3800-50 after a spike to 1.3942 (new peak since the Brexit vote). Back to Usd/Jpy, and some large option expiries could well provide some direction today, with 1.4 bn at the 111.00 strike and 1.5 bn at 110.80, while on the upside there is key chart resistance at 111.74 (200 DMA) and 111.97 (50% Fib). For Eur/Usd, if 1.2200 is breached again on the downside then stops are reportedly seen below 1.2150, while 1.2119 is tech support ahead of the next big figure. Aud and Nzd both firming up again vs their US counterpart towards 0.8000 and 0.7300 after the former traded in a volatile fashion on mixed jobs data. In terms of crosses, Eur/Gbp has seen offers around 0.8830 filled, but bids at 0.8800 and strong chart support around 0.8792 are forming a base.

In commodities, WTI and Brent crude futures marginally lower despite last nights wider than expected drawdown in the latest API crude report. Price action in oil largely dictated by the mild recovery seen in the USD-index. Saudi Aramco is to boost refining capacity to 8mln-10mln bpd from 5mln bpd. US API weekly crude stocks (12 Jan, w/e) -5.120M vs. Exp. -3.500M (Prev. -11.190M).

Looking at the day ahead, there’s no data due in Europe, however the Bundesbank’s Weidmann and ECB’s Coeure are due to speak at a joint conference with the IMF in Frankfurt. In the US, December housing starts and building permits are due along with the January Philly Fed business outlook and latest weekly initial jobless claims numbers. Morgan Stanley is due to report Q4 earnings, along with IBM and American Express.

US Event Calendar

- 8:30am: Housing Starts, est. 1.27m, prior 1.3m;

- 8:30am: Building Permits, est. 1.3m, prior 1.3m

- 8:30am: Philadelphia Fed Business Outlook, est. 25, prior 26.2

- 8:30am: Initial Jobless Claims, est. 249,000, prior 261,000; Continuing Claims, est. 1.9m, prior 1.87m

- 9:45am: Bloomberg Economic Expectations, prior 47; Consumer Comfort, prior 53.5

DB’s Jim Reid concludes the overnight wrap

The only train running last night was the bulled up express with the S&P 500, Dow and Nasdaq up +0.94%, +1.25% and 1.03% respectively – their best day since late November for the first two and 2nd January for the Nasdaq. Within the S&P, all sectors were up with gains led by the tech, energy and consumer staples stocks. Apple’s share price rose 1.65% after announcing it will repatriate some of its offshore cash reserves, with plans to spend $30bn on capex in the US over the next five years, even after paying $38bn of taxes. Elsewhere, reactions to corporate earnings were a little mixed, Bank of America’s 4Q result was above market but the share price dipped 0.19%, following a c36% rally since mid-September, while Goldman Sachs fell 1.86% after its annual fixed income trading revenue fell to the lowest since the GFC.

Staying with US tax cuts and economic growth, the Fed’s Mester noted the risks are still balanced, but in terms of her estimates for the impact from fiscal policy, she thinks “there are some salient upside risks”, although this will be guided by how firms and households react in their spending. Elsewhere, the Fed’s Evans noted the US economy is strong and tax cuts “should add to business investments”. Our US team noted that if these fiscal changes only provide demand-side stimulus, they could quicken the arrival of the next recession by pulling forward demand and causing the Fed to move more aggressively on rate hikes. Refer to their note for a detailed assessment of how tax reform will impact the economy in 2018 and beyond.

Turning to Fed speak on inflation, the Fed’s Evans said “I’m confident we are going to be on a path” to the 2% target, although the Fed’s Kaplan believes that while “inflation pressures are building…they are being offset to a great degree by technology enabled disruption”. On the rates outlook, Ms Mester noted “a gradual pace of interest increase over the course of this year will be appropriate” and that she is “not concerned” the US is nearing a recession. Mr Evans reiterated his dovish view and noted that “something less than three (hikes) is probably appropriate” and it’s better to wait till June where if growth and inflation readings are robust, then “we would have time for three hikes in the year”. Conversely, the Fed’s Kaplan doesn’t want to get in a situation where the cyclical inflationary forces are getting stronger “….to the point where the Fed feels it needs to move much more rapidly to address it”, so the Fed should be “acting sooner rather than later” on rates.

In China, its 4Q17 GDP stats (6.7% expected), retail sales and IP are expected to be out just after we go to print at 7am UK time. Ahead of the data dump, our China economists have published a timely presentation outlining their views on China’s opportunities and risks in 2018-2020. Amongst the key messages, they believe the tightening of fiscal policy is the most underestimated risk in 2018, in part as fiscal spending was a key driving force behind the economic cycle in 2014-17. So growth is set to slow in 2018. Further, the team is more worried about inflation than consensus. Refer to their report for more details.

This morning in Asia, markets pared gains to be modestly lower, with the Nikkei (-0.1%), Kospi (-0.05%) and Hang Seng (-0.02%) all modestly down. Elsewhere, Bloomberg reported a minority within the BOJ are raising the need to eventually start to discuss policy normalisation – as per unnamed sources.

Now recapping other markets performance from yesterday. European equities weakened with the Stoxx 600 down 0.10%, weighed down by telco and health care stocks. Across the region, key bourses fell c0.4% (CAC -0.36%; FTSE -0.39%; DAX -0.47%) while Italy’s FTSEMIB rose marginally. Core European 10y bond yields were little changed (Bunds +0.1bp; Gilts +0.4bp) but UST 10y rose 5.2bp, partly weighed down by concerns of a potential government shutdown, increasing US bond supply (partly on concessions to get a deal done) and US Treasury Department’s data showing China’s holding of Treasuries fell to a four month low in November (-1.1% mom to $1.18trn). This morning, UST 10y is c0.6bp lower.

Turning to currencies, the US dollar index rebounded slightly (+0.16%) from its three year low, while Euro dropped 0.60% post the various ECB speak (more below). Sterling jumped to an intraday high of 1.394 before stabilising to end the day 0.28% higher – a fresh post Brexit high. In commodities, WTI oil rose 0.38%, partly reflecting solid compliance to OPEC production cuts, which was 125% in December. Elsewhere, precious metals weakened (Gold -0.86%; Silver -1.12%) and other base metals also fell, but losses are moderating (Copper -0.54%; Zinc -0.36%; Aluminium -0.17%).

Away from the markets and onto other central bankers commentaries. There appears to be more jawboning on the stronger Euro, with the ECB’s Nowotny noting the recent strength is “not helping” and must be observed. Further, the ECB’s Constancio noted “I’m concerned about sudden movements” in the exchange rate “which don’t reflect changes in fundamentals” and that looking at the fundamentals “inflation declined slightly in December”. Elsewhere on policy guidance, he noted that while we see the need for a gradual adjustment of all the elements of our forward guidance, “this does not mean that changes will be immediate”.

Continuing with the theme of ECB’s guidance, DB’s Mark Wall argues that given the strength of the Euro economy, relatively easy and stable financial conditions (despite recent market moves), he expects a change to forward guidance within the next few months. The team has set out a base time line for this change, including: i) At the press conference on 25 January, they expect Mr Draghi to prepare the ground for changes to forward guidance. ii) In March/April, they expect the ECB to redefine the reaction function within forward guidance, weakening the direct link between economic/financial shocks and QE. iii) In June, they expect the ECB to announce a tapering of QE net purchases to zero over the course of Q4 and finally iv) In Q4 they expect the ECB to adjust rates guidance to manage expectations for the timing and pace of policy rate hikes in 2019. Overall, we see the less hawkish strategy as being more likely, but one way or another, exit is in train.

Back in the UK, the BOE’s Saunders reiterated his slightly hawkish stance, noting that the unemployment rate could drop below 4% in 2018 and that with “….labour market tightness and signs of higher growth…(then) I consider it likely that interest rates will need to rise further over time”. Elsewhere, on Brexit, the EU side have continued to offer reassuring rhetoric if the UK changes its mind on Brexit. Yesterday, the Head of the EU executive arm noted the UK can always re-apply for EU membership after departing. Conversely, PM May’s spokesman responded “we have been absolutely clear…that we are leaving the EU….I’m not sure how much clearer we can be”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the December IP was above market expectations at 0.9% mom (vs. 0.5%), although the prior month was revised down by 0.3ppt. In the details, most of the growth in December was due to a 5.7% mom increase in utility production and a 1.6% mom increase in mining production. Elsewhere, capacity utilisation also beat at 77.9% (vs. 77.3%) while the January NAHB housing market index was in line at 72, following a 5pt improvement to a 17- year high back in December. Finally, the Fed’s latest Beige book painted an upbeat picture. It noted 11 Districts reported “modest to moderate gains” in activity and Dallas reported a “robust” increase. Further, the outlook for this year remains optimistic for a majority of the Fed’s contacts across the country.

Most Districts cited on-going labour market tightness and most Districts said that wages increased at a “modest” pace.

In Europe, the final December reading for the Euro area CPI was unrevised, with headline CPI at 1.4% yoy and core CPI at 0.9% yoy, which was steady for the third consecutive month.

In Canada, the central bank lifted the cash rate by 25bp to 1.25% as widely expected. Looking ahead, the BOC seems a bit dovish and noted that “while the economic outlook is expected to warrant higher interest rates over time…… some continued monetary policy accommodation will likely be needed…. (and) the Governing Council will remain cautious in considering future policy adjustments”. The Bank also pointed to uncertainty surrounding the future of the North American Free Trade Agreement (NAFTA).

Looking at the day ahead, there’s no data due in Europe, however the Bundesbank’s Weidmann and ECB’s Coeure are due to speak at a joint conference with the IMF in Frankfurt. In the US, December housing starts and building permits are due along with the January Philly Fed business outlook and latest weekly initial jobless claims numbers. Morgan Stanley is due to report Q4 earnings, along with IBM and American Express.

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 30.08 points or 0.87% /Hang Sang CLOSED UP 138.53 pts or 0.43% / The Nikkei closed DOWN 104.94 POINTS OR 0.44%/Australia’s all ordinaires CLOSED DOWN 0.06%/Chinese yuan (ONSHORE) closed WELL UP at 6.4227/Oil UP to 64.05 dollars per barrel for WTI and 69.33 for Brent. Stocks in Europe OPENED ALL RED. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4227. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4201//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(GOOD MARKETS )

3 a NORTH KOREA/USA

NORTH KOREA/SOUTH KOREA/USA

Six Chinese ships have been secretly breaking North Korean sanctions

(courtesy zerohedge)

Despite Beijing’s Denials, 6 Chinese Ships Are Observed “Secretly” Breaking N.Korean Sanctions

China officials denied reality in December despite being “caught red handed” selling sanctions-defying oil to North Korea.However, the denials might be harder to justify, as WSJ reports citing satellite photographs and intelligence gathered by U.S. officials, at least six Chinese-owned or operated cargo ships violated UN sanctions against North Korea.

The Wall Street Journal reports that the U.S. compiled the information from Asian waters as part of the Trump administration’s strategy to pressure North Korea into giving up its nuclear weapons and long-range missiles.

The effort identified the ships by name and tracked their movements.

The ships entered ports in North Korea and transported what U.S. officials said was illicit cargo to Russia and Vietnam or made ship-to-ship transfers at sea.

Additionally, U.S. evidence shows the ships made extensive maneuvers designed to disguise the violations.

WSJ reports that declassified intelligence reports, photos and maps shared with the U.N. by American officials asserted multiple instances of Chinese ships violating Security Council resolutions banning North Korean coal exports and ship-to-ship transfers of refined petroleum bound for North Korea. The Journal reviewed much of that evidence.

Within days after the complete U.N. ban was passed, the Glory Hope 1, a Chinese-owned vessel, entered the Yellow Sea near North Korea under a Panamanian flag. The ship crossed the Yellow Sea, entered North Korea’s Taedong River and then turned into the North Korean port of Songnim, according to the information presented to the U.N.

The vessel turned off its Automatic Identification System, or AIS, a transmission device that discloses a ship’s position to other ships, satellites, and land-based tracking systems.

“When AIS is off in a vast sea, you are basically invisible,” said Ioannis Sgouras, a veteran Greek captain of crude-oil carriers. “You can still be picked up by other ships on radar if you are in range, but they can’t tell the ship’s name, cargo or destination.”

U.S. intelligence officials used satellite photos to monitor the Glory Hope 1 as it took on a load of North Korean coal Aug. 7. The ship then proceeded toward the coast of China, with its AIS still turned off.

China’s foreign ministry said in a statement to the WSJ that it abides fully with Security Council resolutions and deals with violations in accordance with the law

In December, The Chinese delegation to The UN provided the sanctions committee with no formal explanation of why China was willing to allow some ships to go on the list but not others. Some U.S. officials believe the goal was to avoid the embarrassment of ships with Chinese ties being found in breach of U.N. sanctions.

Ironically, President Trump was bashing Russia yesterday for its ship-to-ship sanctions violations, and praising China for its help on North Korea.

Today’s intel release may make that a little harder to defend.

Can you get caught red-handed-er?

Caught RED HANDED – very disappointed that China is allowing oil to go into North Korea. There will never be a friendly solution to the North Korea problem if this continues to happen!

The U.S. is likely to keep pressuring for tough enforcement of the sanctions. H.R. McMaster, President Donald Trump’s national security adviser, warned in December that owners of ships that violate sanctions risk severe reprisals.

At a conference hosted by the Policy Exchange, a British think tank, Mr. McMaster said:

“A company whose ships would engage in that activity ought to be on notice that that might be the last delivery of anything they do for a long time, anywhere.”

That seems to sum things up pretty well!

end

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

China’s latest GDP numbers beat the street but retail sales are slumping. There is renewed fears that much of the data is fake

(courtesy zero hedge)

China GDP Beats, Retail Sales Slump (Amid Renewed Fake Data Fears)

China bond yields rose ahead of the macro data avalanche tonight (following a leaked upside surprise print for GDP). GDP, Industrial Production, and Fixed Asset Investment all beat expectations but Retail Sales missed dramatically – growing at its slowest since Feb 2004.

As a reminder, these numbers are landing amid some renewed concern over the integrity of Chinese data, with a nationwide audit of city and county governments last year finding a slew inflated fiscal revenues.

The last couple of months have seen upside surprises for Chinese data…

Before the data release, an official at the National Development and Reform Commission, China’s top economic planner, said GDP rose 6.9% in 2017, according to financial information website Hexun.com.

And the data deluge tonight printed as follows…

- China GDP YoY BEAT: +6.8% vs +6.7% exp (+6.8% prior)

- China Industrial Production YoY BEAT: +6.2% vs +6.1% exp (+6.1% prior)

- China Retail Sales YoY MISS: +9.4% vs +10.2%% exp (+10.2% prior) – lowest since Feb 04

- China Fixed Assets Investment YoY BEAT +7.2% vs +7.1% exp (+7.2% prior)

Visually…the trend is clear…

Offshore Yuan has trod water for the last 3 days, albeit with some volatility within that range…

Chinese stocks have been divergent in the last few days but overnight saw a panic bid rip through CHINEXT (China’s small caps and tech index) as crypto-carnage sent many stocks limit down but The National Team appeared to have other ideas…

Stocks in Hong Kong, which have been strong all day, are taking a bit of a leg up after the dat, led by banks.

Notably, PBOC pumps in net 90b yuan through reverse-repurchase operations, taking total injections since Jan. 11 to 720b yuan.. which might help explain the rebound.

Finally, now that we have all the data in from 2017, Bloomberg’s Chris Anstey reminds us that the consensus forecast of economists surveyed by Bloomberg is for a 2018 growth rate of 6.4%. To get there, it means we’ll need to see a step down in the monthly data for China to decelerate somewhat. Assuming that exports and consumption continue to expand rapidly, that puts the onus on the slowdown potentially on production and investment.

end

4. EUROPEAN AFFAIRS

Germany

We have discussed at length Japan’s demographic problems of an aging population and low fertility rates. Germany will be the second nation to have a demographic aging population

(courtesy zerohedge)

Over The Next Year, Germany Will Hit A Scary Demographic Milestone

In Europe, the economy is humming along at its fastest pace in 10 years.

According to the European Central Bank, the most recent forecast for the eurozone pegs growth at 2.3% for the year ahead, a significant upgrade from the central bank’s previous estimate of 1.8%.

But as Europe regains its economic mojo, Visual Capitalist’s Jeff Desjardins notes, a key part of the machine is seeing demographic reality take shape.

A Scary Milestone