GOLD: $1333.15 UP $6.00

Silver: $17.03 UP 9 cents

Closing access prices:

Gold $1331.70

silver: $17.03

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1338.44 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1331.40

PREMIUM FIRST FIX: $7.04

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1339.81

NY GOLD PRICE AT THE EXACT SAME TIME: $1331.60

Premium of Shanghai 2nd fix/NY:$8.21

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1335.80

NY PRICING AT THE EXACT SAME TIME: $1336.10

LONDON SECOND GOLD FIX 10 AM: $1334.95

NY PRICING AT THE EXACT SAME TIME. $1334.00

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 4 NOTICE(S) FOR 400 OZ.

TOTAL NOTICES SO FAR: 472 FOR 47200 OZ (1.4681 TONNES),

For silver:

jANUARY

5 NOTICE(S) FILED TODAY FOR

25,000 OZ/

Total number of notices filed so far this month: 688 for 3,440,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $11,227/OFFER $11,327 UP 27 (morning)

Bitcoin: BID 11,327/OFFER $11,427 UP $120(CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A SMALL 1615 contracts from 196,423 FALLING TO 194,808 WITH YESTERDAY’S DEEP 23 CENT FALL IN SILVER PRICING. WE THUS HAVE SOME COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1597 EFP’S FOR MARCH AND ZERO FOR OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1597 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1597 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

33,424 CONTRACTS (FOR 14 TRADING DAYS TOTAL 33,424 CONTRACTS OR 167.120 MILLION OZ: AVERAGE PER DAY: 2387 CONTRACTS OR 11.937 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 167.120 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.8% OF ANNUAL GLOBAL PRODUCTION

RESULT: A SMALL SIZED LOSS IN OI COMEX DESPITE THE 23 CENT FALL IN SILVER PRICE WHICH USUALLY INDICATES ANOTHER FAILED BANKER SHORT-COVERING. WE ALSO HAD A HUGE SIZED EFP ISSUANCE OF 1597 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX . FROM THE CME DATA 1573 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY LOST ONLY 42 OI CONTRACTS i.e. 1573 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1615 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 23 CENTS AND A CLOSING PRICE OF $16.94 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.974 BILLION TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 5 NOTICE(S) FOR 25,000 OZ OF SILVER

In gold, the open interest SHOCKINGLY ROSE BY A CONSIDERABLE 3953 CONTRACTS UP TO 595,151 DESPITE THE LARGE FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($11.85). THUS ANOTHER FAILED BANKER SHORT COVERING. IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED A GOOD SIZED 5867 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 5867 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS The new OI for the gold complex rests at 595,151. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE ANOTHER MONSTROUS GAIN OF 9820 OI CONTRACTS: 3953 OI CONTRACTS INCREASED AT THE COMEX AND AN GOOD SIZED 5867 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 6902 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 134,717 CONTRACTS OR 13.4717 MILLION OZ OR 419.02 TONNES (14 TRADING DAYS AND THUS AVERAGING: 9622 EFP CONTRACTS PER TRADING DAY OR 962,200 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 14 TRADING DAYS: IN TONNES: 419 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 419/2200 TONNES = 19.04% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

Result: A SHOCKINGLY STRONG SIZED INCREASE IN OI AT THE COMEX DESPITE THE LARGE FALL IN PRICE IN GOLD TRADING ON YESTERDAY ($11.85). WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5867. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5867 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 9820 contracts ON THE TWO EXCHANGES:

5867 CONTRACTS MOVE TO LONDON AND 3953 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 33.85 TONNES)

we had: 4 notice(s) filed upon for 400 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

With gold up $6.00, we had no change in gold inventory at the GLD/

Inventory rests tonight: 840.96 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

INVENTORY RESTS AT 315.500 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A SMALL 1615 contracts from 196,423 DOWN TO 194,808 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE HUGE FALL IN PRICE OF SILVER TO THE TUNE OF 23 CENTS WITH RESPECT TO YESTERDAY’S TRADING. OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1597 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 1615 CONTRACTS TO THE 1597 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A SMALL LOSS OF 42 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET LOSS TODAY IN OZ ON THE TWO EXCHANGES: 0.210 MILLION OZ!!!

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE GOOD SIZED FALL OF 23 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 1597 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 13.11 points or 0.38% /Hang Sang CLOSED UP 132.95 pts or 0.41% / The Nikkei closed UP 44.69 POINTS OR 0.19%/Australia’s all ordinaires CLOSED DOWN 0.18%/Chinese yuan (ONSHORE) closed WELL UP at 6.4035/Oil DOWN to 63.54 dollars per barrel for WTI and 68.69 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4035. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4003//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(GOOD MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)/South Korea/North Korea/USA

The Pentagon temporarily deploys 3 types of strategic bombers to Guam in anticipation of problems in North Korea( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

China’s housing market is again blowing up and yes we should be worried this time

( zerohedge)

4. EUROPEAN AFFAIRS

i)A must read..with bond yields rising (and bond prices falling) Bill Blain list 3 things that could trigger a bond price avalanche. His solution purchase only real assets

( Bill Blain/Mint Partners)

(courtesy GEFIRA)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

a must view

( Oliver Stone)

6 .GLOBAL ISSUES

7. OIL ISSUES

The IEA now predicts an explosive growth in USA shale production due to the higher oil prices

( IEA/zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The gold industry has seen some “disastrous deals” and no doubt the low gold price has had a serious effect. Almost 85 billion in write downs. The guys who escaped bad deals have been Agnico Eagle and Randgold

( Bloomberg/GATA)

ii)This is why you do not invest in crypto currencies: 14% of all digital currencies have been stolen

( Kharif/Bloomberg/GATA)

iii)New York Fed official celebrates 100 years plus of market rigging

( GATA/Chris Powell)

iv)Another bank pleads guilty to currency rigging and pays a 100 million dollar fine

( Reuters/GATA)

v)for those of you who are intending the Vancouver conference on Monday are invited to a GAR|TA reception

( Chris Powell/GATA)

vi)Copper has been sliding for the 3rd straight week and this is signalling a sure slowdown in the global economy

(courtesy zerohedge)

10. USA stories which will influence the price of gold/silver

i)Early trading N.Y. last night;

10 yr yield touches 2.63..will this lead to a sell off on Friday morning?

(zerohedge)

ii)Friday morning: 10 yr touches 2.64% and crossing Jeff Gundlach’s red line for stock damage. Looks like the yield curve will begin to trade on a flattening basis

iii)Soft data, U of Michigan Confidence index falters badly last month:

iv)SWAMP NEWS

b)Friday morning:still no deal as a shutdown looms

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SHOCKINGLY ROSE BY A CONSIDERABLE 3953 CONTRACTS UP to an OI level of 595,151 DESPITE THE FALL IN THE PRICE OF GOLD ($11.85 LOSS WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ZERO COMEX GOLD LIQUIDATION. WE ALSO WITNESSED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE. THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT A GOOD SIZED 5867 EFP’S WERE ISSUED FOR FEBRUARY , 0 EFP’s FOR APRIL, AND 0 FOR DECEMBER: TOTAL 5867 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 9820 OI CONTRACTS IN THAT 5867 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 3953 COMEX CONTRACTS. NET GAIN ON THE TWO EXCHANGES: 9820 contracts OR 0.9820 MILLION OZ OR 30.54 TONNES

Result: A SURPRISING AND STRONG INCREASE IN COMEX OPEN INTEREST DESPITE THE FALL IN THE PRICE YESTERDAY’S GOLD TRADING ($11.85.) WE HAD NO GOLD LIQUIDATION AT THE COMEX. HOWEVER WE, NO DOUBT WE HAD ANOTHER FAILED BANKER SHORT COVERING .. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 9820 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest RISE by 185 contracts RISING AT 231. We had 19 notices served upon yesterday so we gained 204 contracts or an additional 2400 oz of gold will stand AT THE COMEX in this non active month of January AND QUEUE JUMPING INTENSIFIES.

FEBRUARY saw a LOSS of 2717 contacts DOWN to 310,089. March saw a GAIN of 79 contracts UP to 632. April saw a GAIN of 5,344 contracts UP to 169,565.

We had 4 notice(s) filed upon today for 400 oz

PRELIMINARY VOLUME TODAY ESTIMATED; not available

FINAL NUMBERS CONFIRMED FOR YESTERDAY: not available

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A SMALL 1615 CONTRACTS FROM 196,423 DOWN TO 194,808 WITH YESTERDAY’S 23 CENT FALL. WE WERE ALSO INFORMED THAT WE HAD ANOTHER GOOD SIZED 1597 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1597. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD A SMALL LONG COMEX SILVER LIQUIDATION BUT A RISE IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE LOST 42 OPEN INTEREST CONTRACTS:

1615 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1597 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS TWO EXCHANGES: 42 CONTRACTS

We are now in the poor non active delivery month of January and here the OI LOST 53 contracts FALLING TO 16. We had 58 notices served upon yesterday, so we GAINED 5 contracts or an additional 5,000 oz will stand for delivery AT THE COMEX AND QUEUE JUMPING CONTINUES

February saw a LOSS OF 55 OI contracts FALLING TO 167. The March contract LOST 2119 contracts DOWN to 137,377.

We had 5 notice(s) filed for NIL 25,000 for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 19/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

281,803.687 OZ

HSBC

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

125,848.015 oz

JPMORGAN

|

| No of oz served (contracts) today |

4 notice(s)

400 OZ

|

| No of oz to be served (notices) |

227 contracts

(22700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

472 notices

47200 oz

1.4681 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (472) x 100 oz or 46800 oz, to which we add the difference between the open interest for the front month of JAN. (231 contracts) minus the number of notices served upon today (4 x 100 oz per contract) equals 69,900 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (472 x 100 oz or ounces + {(231)OI for the front month minus the number of notices served upon today (4 x 100 oz which equals 69,900 oz standing in this active delivery month of JANUARY (2.174 tonnes). THERE IS 18.245 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 204 CONTRACTS OR AN ADDITIONAL 2400 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY AS SOMEBODY WAS IN GREAT NEED OF PHYSICAL GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 65 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

5942.600 oz

CNT

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

503,791.730 oz

JPMORGAN

|

| No of oz served today (contracts) |

5

CONTRACT(S)

(25,000 OZ)

|

| No of oz to be served (notices) |

11 contracts

(55,000 oz)

|

| Total monthly oz silver served (contracts) | 688 contracts

(3,440,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) JPMorgan continues to add silver to its inventory:

Deposit: 503,791.730 oz

total inventory deposits: 503,791.730 oz

we had 2 withdrawals from the customer account;

i) Out of CNT: 4958.90 oz

ii) Out of Delaware: 983.700 oz

total withdrawals; 5,942.600 oz

we had 1 adjustment

i) out of CNT: 4973.310 oz was adjusted out of the customer account and this landed into the dealer account of CNT

total dealer silver: 45.461 million

total dealer + customer silver: 246.809 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 5 contract(s) FOR 25,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 688 x 5,000 oz = 3,440,000 oz to which we add the difference between the open interest for the front month of JAN. (16) and the number of notices served upon today (5 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 688(notices served so far)x 5000 oz + OI for front month of JANUARY(16) -number of notices served upon today (5)x 5000 oz equals 3,495,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 5 CONTRACTS OR AN ADDITIONAL 25,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3.790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: not available

CONFIRMED VOLUME FOR FRIDAY: xxx CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF xxx CONTRACTS EQUATES TO xx MILLION OZ OR 75.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.50% (Jan 18/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.70% to NAV (Jan 18/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.50%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.70%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 19/2018/ Inventory rests tonight at 840.76 tonnes

*IN LAST 311 TRADING DAYS: 100.19 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 246 TRADING DAYS: A NET 57.12 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 19/2017:

Inventory 315.500 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.76%

12 Month MM GOFO

+ 2.10%

30 day trend

end

At 3:30 pm we receive the COT report which I feel is totally useless due to the huge EFP transfers.

However for completeness I will provide it for you:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 301,863 | 90,152 | 73,170 | 158,202 | 390,709 | 533,235 | 554,031 |

| Change from Prior Reporting Period | ||||||

| 12,702 | 4,279 | 3,900 | 8,103 | 20,339 | 24,705 | 28,518 |

| Traders | ||||||

| 190 | 91 | 90 | 44 | 57 | 270 | 206 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 49,098 | 28,302 | 582,333 | ||||

| 2,173 | -1,640 | 26,878 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, January 16, 2018 | |||||

Our large specs

our large specs that have been long in gold added 12,702 contracts to their long side and this does not include specs who transferred contracts to London

our large specs that have been short in gold added 4279 contracts to their short side

Our commercials

those commercials that have been long in gold added 8103 contracts to their long side

those commercials that have been short in gold added a whopping 20,339 contracts to their short side and this does not include any of the EFP’s that were transferred to London. the commercials are still has an obligation to deliver upon those contracts transferred.

Our small specs

those small specs that have been long in gold added 2173 contracts to their long side

those small specs that have been short in gold covered 1640 contracts from their short side

the comex is one big fraud!!

AND NOW SILVER

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 79,866 | 42,654 | 21,702 | 68,356 | 118,499 | |

| -4,447 | -3,624 | 4,048 | 383 | 584 | |

| Traders | |||||

| 100 | 47 | 39 | 42 | 39 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 196,511 | Long | Short | |

| 26,587 | 13,656 | 169,924 | 182,855 | ||

| 1,518 | 494 | 1,502 | -16 | 1,008 | |

| non reportable positions | Positions as of: | 156 | |||

Our large specs

On a net basis, those large specs that have been long in silver pitched 4447 contracts from their long side and many of these morphed into London based forwards.

On a net basis, those large specs that have been short in silver covered a huge 3624 contracts from their short side.

Our commercials

on a net basis: those commercials that have been long in silver added a tiny 383 contracts to their long side.

on a net basis: those commercials that have been short in silver added a tiny 584 contracts to their short side.

Our small specs

those small specs that have been long in silver added 1518 contracts to their long side

those small specs that have been short in silver added 494 contracts to their short side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Bullion May Have Room to Run As Chinese New Year Looms

-

Gold bullion tends to rise January and February before Chinese New Year (see table)

-

Gold is nearly 8% and $100 higher since Fed raised rates one month ago

- Options traders are bullish and suggest gold has room to run (see chart)

- Nervous in short term, positive in medium term – gold at $1,500 in 2018

From Bloomberg:

Gold’s breakneck rally eased this week, but tailwinds in both physical and paper markets suggest it’s got room to run.

Chinese New Year buying and option prices suggest the stars are aligning for the metal to extend its 6 percent gain over the past month.

“I’m always a bit nervous when gold prices rise this much, this fast,” said Mark O’Byrne, director of bullion dealer GoldCore Ltd. “But there certainly is healthy demand from China and the futures market — I think we should break highs above $1,400 later in the year.”

Options traders are betting on at least another month of rising prices. They’re charging more for benchmark call contracts than for similar puts, and by the biggest premium since November. The bias, measured in implied volatility, has increased to about 0.6 percentage points.

Gold tends to do well in January and February. That’s when demand spikes in the biggest consuming nation, China. Over the past decade, the metal advanced by about 6 percent on average in the first two months combined. The Lunar New Year, which is often celebrated with gifts of gold in much of Asia, falls on Feb. 16 in 2018.

January has historically been gold’s strongest Still, a technical indicator points to a rally that may have grown tired.

Still, a technical indicator points to a rally that may have grown tired.

The metal, which reached a four-month high this week, crossed into 2018 with an eight-day rally, the longest string of increases since 2011. Now, it’s considered overbought, according to the relative-strength index, a gauge of momentum.

As gold futures are quoted in the U.S. currency, its upswing somewhat depends on whether the greenback’s losing streak continues.

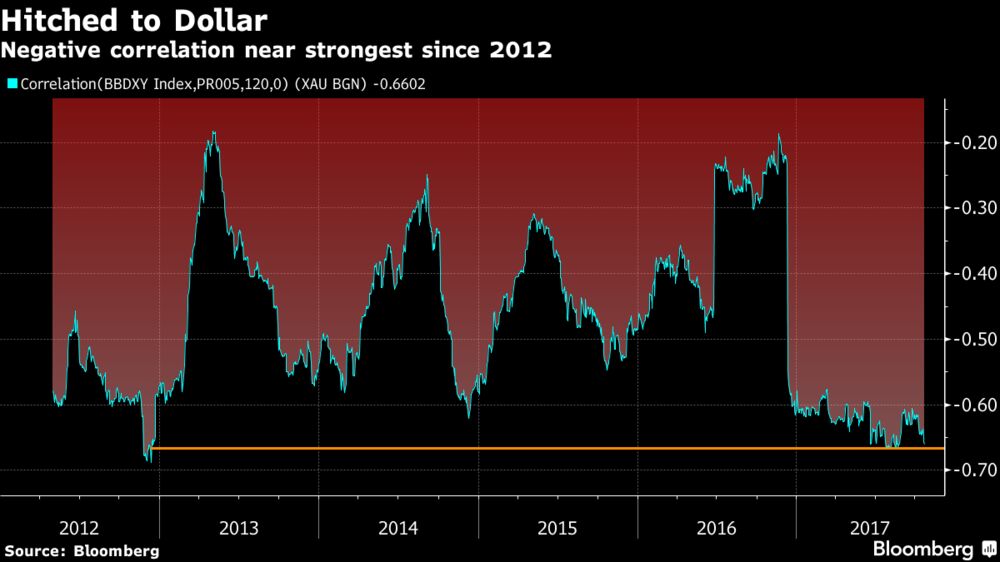

Option prices signal that traders foresee the dollar falling over the next month against the euro, yen and pound. That’s good news for bullion: The 120-day price pattern is close to its strongest negative correlation since late 2012.

GoldCore Note

Gold is due a correction after its $100 rally since the Fed raised rates. A near 8% gain in a month is quite a move up in a short period of time and ordinarily one would expect a correction. Frequently a 50% retracement of the gains takes place. This could take us back to the $1,300 level which acted as resistance before. Previous resistance frequently becomes support.

We are always a bit nervous when gold prices rise this much, this fast. At the same time the sharp fall in bitcoin and crypto-currencies is leading to an increase in demand for physical gold and there is robust demand from China ahead of the Chinese New Year.

We are a little cautious in the very short term but very positive in the medium term and see gold over $1,500 in 2018.

Fed Increases Rates 0.25% – Rising Interest Rates Positive For Gold

Gold’s Positives – Rising Interest Rates and Negative Rates

News and Commentary

Gold flat as U.S. Treasury yields rise (Reuters.com)

Gold inches up, but heads for first weekly loss in six (Reuters.com)

Asian Stocks Rise, Even in Face of Climb in Yields (Bloomberg.com)

Gold suffers biggest one-day decline in more than a month | January 18, 2018 (MorningStar.com)

U.S. Stocks Mixed Following Wednesday’s Records (Bloomberg.com)

U.S. Stocks Mixed Following Wednesday’s Records (Bloomberg.com)

Source: Bloomberg

Gold ETF Holdings Surge as Cryptocurrencies Collapse (Bloomberg.com)

Don’t pile into property in 2018 (MoneyWeek.com)

Global housing markets are warning that the cheap money is running out (MoneyWeek.com)

Investors Turning To Gold As Inflation Risks Resurface: Rhind (Bloomberg.com)

2018 to be Good Year For Gold And Precious Metals (Bloomberg.com)

Weak Dollar Poses a $3.4 Trillion Question for U.S. Credit Markets (Bloomberg.com)

Gold Prices (LBMA AM)

18 Jan: USD 1,329.75, GBP 961.14 & EUR 1,088.40 per ounce

17 Jan: USD 1,337.35, GBP 969.45 & EUR 1,092.48 per ounce

16 Jan: USD 1,334.95, GBP 970.38 & EUR 1,091.32 per ounce

15 Jan: USD 1,343.00, GBP 971.93 & EUR 1,092.93 per ounce

12 Jan: USD 1,332.90, GBP 978.75 & EUR 1,099.78 per ounce

11 Jan: USD 1,319.85, GBP 978.14 & EUR 1,104.45 per ounce

10 Jan: USD 1,321.65, GBP 976.96 & EUR 1,103.31 per ounce

Silver Prices (LBMA)

18 Jan: USD 17.09, GBP 12.31 & EUR 13.96 per ounce

17 Jan: USD 17.21, GBP 12.49 & EUR 14.10 per ounce

16 Jan: USD 17.10, GBP 12.43 & EUR 13.99 per ounce

15 Jan: USD 17.12, GBP 12.58 & EUR 14.14 per ounce

12 Jan: USD 17.12, GBP 12.56 & EUR 14.12 per ounce

11 Jan: USD 17.01, GBP 12.64 & EUR 14.24 per ounce

10 Jan: USD 17.13, GBP 12.64 & EUR 14.27 per ounce

Recent Market Updates

– Digital Gold Flight To Physical Gold Coins and Bars

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– London Property Crash Looms As Prices Drop To 2 1/2 Year Low

– Gold Bullion Up 1% In Week, Heads For 5th Weekly Gain As Bonds Sell Off

– Gold Prices Rise To $1,326/oz as China U.S. Treasury Buying Report Creates Volatility

– Gold Hits All-Time Highs Priced In Emerging Market Currencies

– World is $233 Trillion In Debt: UK Personal Debt At New Record

– 10 Reasons Why You Should Add To Your Gold Holdings

– Spectre, Meltdown Highlight Online Banking and Digital Gold Risks

– Palladium Prices Surge To New Record High Over $1,100 On Supply Crunch Concerns

– Gold Has Best Year Since 2010 With Near 14% Gain In 2017

– Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

END

The gold industry has seen some “disastrous deals” and no doubt the low gold price has had a serious effect. Almost 85 billion in write downs. The guys who escaped bad deals have been Agnico Eagle and Randgold

(courtesy Bloomberg/GATA)

‘Disastrous’ deals sideline gold-mining M&A as metal rises

Submitted by cpowell on Thu, 2018-01-18 18:18. Section: Daily Dispatches

By Luzi-Ann Javier

Bloomberg News

Wednesday, January 17, 2018

Stung by some lousy investments that led to billions of dollars in losses a few years ago, the world’s major gold producers have cut way back on mining deals — even as metal prices posted their biggest rally since 2010.

The value of the industry’s transactions, from acquisitions to venture-capital financing, tumbled by more than a third in 2017 to $8.95 billion, the lowest in at least a dozen years of data compiled by Bloomberg. The decline reflects the skittishness of an industry that went on a buying spree in 2010 and 2011, when prices surged to records, and then got stuck with too much debt and huge writedowns after bullion tumbled.

While prices are up over the past two years, executives are reluctant to start buying again. Shareholders harshly criticized past deals, which billionaire hedge-fund manager John Paulson estimates led to $85 billion of writedowns since 2010. Bullion remains about 30 percent cheaper than its record in September 2011, but over the same period, shares of major mining companies tracked by Bloomberg Intelligence fell even more, by more than half.

“There were some disastrous M&A deals done in the past, which destroyed a lot of shareholder value,” Thomas Kaplan, chairman of Electrum Group Ltd., a mining-focused investment firm that’s the largest shareholder in NovaGold Resources Inc. “We’re still in the phase where investors have been turned off by low returns.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-01-17/gold-losses-in-years-…

END

This is why you do not invest in crypto currencies: 14% of all digital currencies have been stolen

(courtesy Kharif/Bloomberg/GATA)

Hackers have stolen about 14% of digital currencies

Submitted by cpowell on Thu, 2018-01-18 18:34. Section: Daily Dispatches

By Olga Kharif

Bloomberg News

January 18, 2018

Digital currencies and the software developed to track them have become attractive targets for cybercriminals while creating a lucrative new market for computer-security firms.

In less than a decade hackers have stolen $1.2 billion worth of Bitcoin and rival currency Ether, according to Lex Sokolin, global director of fintech strategy at Autonomous Research LLP. Given the currencies’ explosive surge at the end of 2017, the cost in today’s money is much higher.

“It looks like crypto hacking is a $200 million annual revenue industry,” Sokolin said. Hackers have compromised more than 14 percent of the Bitcoin and Ether supply, he said.

All told, hacks involving cryptocurrencies like Bitcoin have cost companies and governments $11.3 billion through lost potential tax revenue from coin sales and illegitimate transactions, according to Susan Eustis, chief executive officer of WinterGreen Research. The blockchain ecosystem — the decentralized “distributed ledgers” that track crypto transactions — is also vulnerable. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-01-18/hackers-have-walked-o…

END

New York Fed official celebrates 100 years plus of market rigging

(courtesy GATA/Chris Powell)

New York Fed official celebrates a century of market rigging

Submitted by cpowell on Thu, 2018-01-18 19:20. Section: Documentation

2:32p ET Thursday, January 20, 2018

Dear Friend of GATA and Gold:

Last month an official of the Federal Reserve Bank of New York celebrated a century of cooperation by central banks in secret interventions in the markets. His address was posted on the internet sites of the New York Fed and the Bank for International Settlements, but mainstream financial news organizations have yet to take note of it.

The official, Simon M. Potter, executive vice president of what the New York Fed calls its Markets Group, spoke December 20 at the bank’s “Commemoration of the Centennial of the Federal Reserve’s U.S. Dollar Account Services to the Global Official Sector”:

https://www.newyorkfed.org/newsevents/speeches/2017/pot171220

https://www.bis.org/review/r180112a.htm

Central banks, Potter said, often prefer and sometimes require their foreign exchange reserve managers to use the account services of other central banks.

This is especially true,” Potter explained — with GATA’s emphasis added below — “for liquidity tranches of reserve portfolios where safety and accessibility are critical for the execution of core central banking functions, including foreign-exchange reserve management, foreign-exchange intervention, time-sensitive official payments, macro-prudential policy, lender-of-last-resort responsibilities, and other central bank operations that may require the use of foreign assets and currencies.” …

Do the “assets and currencies” used in those interventions ever include gold? A PowerPoint presentation made by the Bank for International Settlements in 2008 said they do:

http://www.gata.org/node/11012

“For the world’s major central banks, the maintenance of operational links through reciprocal account relationships is integral to their ability to engage in global financial stability operations. Having accounts, settlement instructions, tested and secure lines of communication, and business processes already in place at the time of or leading up to a crisis enhances major central banks’ ability to respond to crises efficiently and flexibly.

“There are numerous historical examples, both known and unknown to the public, of these account relationships being used to support the stability of the global financial system, perhaps best exemplified historically by the Bretton Woods network of central bank swap lines.

“More recently, in nearly every major international incident over the past 20 years that has prompted a coordinated response by the world’s major central banks — be it coordinated foreign-exchange interventions by the major central banks in the wake of the 2011 Fukushima disaster, the swap lines established during the 2008 financial crisis, or swap lines in the wake of 9/11 — the reciprocal accounts among major central banks formed the backbone for the actual or potential execution of stabilization policies. Without these accounts, coordinated central bank action in pursuit of financial stability objectives would be either severely handicapped or entail high risks in terms of the safety, confidentiality, and reliability of these operations.”

Ah, yes, the heroism of central bankers intervening in markets in cases “both known and unknown to the public.” How romantic — and how profitable!

After all, were those interventions, while unknown to the public, known to certain parties associated with central banks, parties facilitating or helping to implement those interventions? Were those intermediaries able to trade on their knowledge of those central bank interventions? Why were some of those interventions never made public?

All this might be a good subject for financial journalism, if there still was such a thing.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Another bank pleads guilty to currency rigging and pays a 100 million dollar fine

(courtesy Reuters/GATA)

HSBC agrees to pay $100 million to settle U.S. probe into currency rigging

Submitted by cpowell on Thu, 2018-01-18 23:29. Section: Daily Dispatches

By Jonathan Stempel and Sangameswaran S

Reuters

Thursday, January 18, 2018

HSBC Holdings today agreed to pay $101.5 million to settle a U.S. criminal probe into the rigging of currency transactions, which has already led the conviction of one of its former bankers.

The payment includes a $63.1 million fine plus $38.4 million in restitution to a corporate client, according to a deferred prosecution agreement filed today with the U.S. District Court in Brooklyn, New York.

In the settlement with the U.S. Department of Justice, HSBC also agreed to bolster its internal controls, and admitted and accepted responsibility for wrongdoing underlying two criminal wire fraud charges filed today against the bank, according to the agreement.

Deferred prosecution agreements let companies avoid criminal charges so long as they comply with the terms. …

… For the remainder of the report:

https://www.reuters.com/article/us-hsbc-settlement/hsbc-to-pay-100-milli…

END

for those of you who are intending the Vancouver conference on Monday are invited to a GAR|TA reception

(courtesy Chris Powell/GATA)

You’re invited to GATA’s reception following the Vancouver conference Monday

Submitted by cpowell on Fri, 2018-01-19 00:46. Section: Daily Dispatches

7:47p ET Thursday, January 18, 2018

Dear Friend of GATA and Gold:

If you’re attending the Vancouver Resource Investment Conference this coming Sunday and Monday, please consider greeting GATA Chairman Bill Murphy and board member Ed Steer at GATA’s reception from 5-7 p.m. Monday at the Lions Pub at 888 West Cordova St., just around the corner from the conference hall.

The reception will have free snacks for a while and a cash bar until closing time.

There’s still time to arrange free admission to the conference itself. Just register here:

https://cambridgehouse.com/e/vancouver-resource-investment-conference-20…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Copper has been sliding for the 3rd straight week and this is signalling a sure slowdown in the global economy

(courtesy zerohedge)

Dr.Copper Slides For 3rd Straight Week, Options Signal More To Come

Dr.Copper is down for the three straight weeks after trading up to four-year highs, providing cover for the bullish global reflation bet.

As we noted previously, there’s just one little problem with all this copper-futures-price-based exuberance and extrapolation.

The one thing that’s missing is buyers of the actual metal.

As Bloomberg reports, evidence of the anomaly can be seen in the premiums that purchasers of physical copper pay over futures prices to cover shipping and other costs.

Typically these rise as demand grows and buyers are willing to pay extra to access supply that’s being used up at a quicker rate.

Yet, even with factories running at the fastest in years, premiums have been stuck at a low level.

That’s a disconnect with the optimism in futures markets, where hedge funds have been adding to their bullish bets since the middle of December.

But as hedgies have been piling long into futures, the options markets are suggesting resurgent Dr.Copper is about to relapse…

If one looks at the price of copper (Figure 1) and the implied volatility on its options (Figure 2), one might think that the metal – often referred to as Dr. Copper for its reputation as a leading prognosticator of economic health because of its widespread applications — has returned to robust health after a bad spell from 2011 to 2015. Recently, the price has been soaring, and the implied volatility low. Fundamentally, copper looks good. The global economy is expanding robustly and growth in China, copper’s single-most important market, stopped slowing two years ago. A peek below the surface, however, shows that traders have concerns that this benign situation may not last, and 2018 could prove those concerns to be valid.

A deeper look at the copper options market, however, shows a high degree of downside skewness as one moves away from at-the-money (ATM) options. Out-of-the-money (OTM) put options on copper command much higher implied volatility premiums than similar OTM call options (Figure 3). Moreover, in Q4 2017, copper’s implied volatility rose relative to its Q3 levels while implied volatility on options fell sharply for most other futures contracts (Figure 4).

What is the downside risk that copper traders are so worried about? We think it can be summed up in two words: China and equities. China’s economic stabilization in 2016 and 2017 after years of slowing growth was an unexpected and beneficial surprise for copper producers (Figure 5).

Rather than cratering as many feared that it would in 2015, China’s growth rate improved in 2016 and 2017 as the Xi Jinping Administration stimulated the economy ahead of his successful bid to secure a second mandate. Now, with the mandate in hand, the risk is that China’s economy will begin to slow under the pressure of a mountain of debt (Figure 6), a crackdown on lending growth and a broadening of the focus to include environmental concerns at the possible expense of growth.

If China’s growth slows in 2018, as its yield curve suggests (Figures 7 and 8), copper prices have the potential to fall a long way, perhaps even retesting or breaking through their 2015 and 2016 lows.

Equity markets pose another risk. For the moment, global equity markets remain robust. Some of the markets, however, have become quite pricey and as the world economy moves into a more advanced stage of recovery, the easy monetary policy that has supported the markets will probably come to an end. (See our papers on the VIX-Yield Curve, Credit Spread-Yield Curve and Unemployment-Yield Curve).

That said, late stage equity bull markets can be quite powerful. Stocks soared in 1988 and 1989, at end of the 1980s expansion. They did they did even better during the late 1990s and also did well in the later stages of the 2003-2007 expansion. As such, equities could continue to pull copper prices higher despite somewhat stretched valuation levels.

The good news for investors who might be concerned about how copper will perform in the event of an equity bear market is that the day-to-day correlation between copper and equity prices has been relatively low for the past few years; and were also not too high during the bear markets from 2000 to 2002 and 2007 to 2009. (Figure 9). As such, even if U.S. equities sell off, they might not, to a large extent, negatively influence copper prices. That said, if stocks continue to rally, they might also not be particularly supportive, especially if copper looks more to China than to the U.S. and Europe as a source of price support.

If copper does sell off, watch for currencies such as the Australian dollar, the Brazilian real and the Chilean peso which in the past have correlated highly with copper, to find themselves under downward pressure. Weaker emerging market currencies could also increase the downward pressure on China’s forex reserves and could eventually spark a devaluation of the renminbi. This wouldn’t be due to lower copper prices but rather to lower Chinese economic growth which could send commodity prices downward and put emerging market currencies under pressure.

- Copper prices and ATM options prices behave as if the global economy will continue to perform well.

- The skew on options betrays nervousness about downside potential in copper.

- If China slows in response to monetary tightening and high debt levels, copper prices could come under downward pressure.

- Equities pose some risk to copper but they aren’t always as highly correlated as one might expect.

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.4035 /shanghai bourse CLOSED UP AT 13.11 POINTS 0.38% / HANG SANG CLOSED UP 132.95 POINTS OR 0.41%

2. Nikkei closed UP 44.69 POINTS OR 0.19% /USA: YEN FALLS TO 110.76

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 90.41/Euro RISES TO 1.2259

3b Japan 10 year bond yield: RISES TO . +.085/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.76/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.54 and Brent: 68.69

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.584%/Italian 10 yr bond yield DOWN to 1.973% /SPAIN 10 YR BOND YIELD DOWN TO 1.458%

3j Greek 10 year bond yield FALLS TO : 3.733?????????????????

3k Gold at $1334.70 silver at:17.06: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 9/100 in roubles/dollar) 56.61

3m oil into the 63 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.76 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9586 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1754 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.584%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.627% early this morning. Thirty year rate at 2.910% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Jump Despite Threat Of Imminent Government Shutdown; Dollar Slide Accelerates

If US and global stocks sold off yesterday on fears of a government shutdown, coupled with a spike in US Treasury yields to the highest level since March and approaching Gundlach’s “equity selloff redline“…

… then it is unclear what has precipitated their rebound this morning when the threat of a US government shutdown is even more pressing – with not enough votes in the Senate as of this moment (despite it having passed the House late on Thursday) to keep government running reflected in the latest plunge in the dollar which dropped to a fresh 3 year low – while the 10Y jumped even more overnight, breaking above the crucial 2.63% level and rising as high as 2.6407, the highest since September 2016.

While not a rout just yet, the Treasury selloff – arguably on concerns of rising inflation although we have seen many false starts in the past – spilled over across the globe, although Spanish bonds outperform in expectation of sovereign rating upgrade. Bunds underperformed despite a decent bounce off the 160.31 low to 160.56 (-2 ticks vs -27 ticks at worst), with chart support respected again.

Meanwhile, equities again ignore all risks, and overnight Japan’s Topix rose first time in three days, while Europe’s Stoxx 600 rose 0.5%, and was poised to close at the highest level since August 2015, and S&P futures have rebounded, wiping out all of yesterday’s losses.

Predictably, Chinese stocks extended the 2018 rally, while the Nikkei 225 (+0.2%) saw initial upside pared as participants awaited developments in Washington where the stop gap bill to fund government through to February 16th was passed by the House, but faces less certainty at the Senate. Elsewhere, Hang Seng (+0.2%) somewhat took a breather from its recent ascent to all-time highs and Shanghai Comp. (+0.4%) was positive after yesterday’s GDP numbers and firm liquidity efforts by the PBoC. In Europe, the Dax is outperforming, led by ThyssenKrupp after they confirmed their targets and BASF who continue to rally after their positive trading update late yesterday.

Meanwhile, in macro, the dollar selloff accelerated, with the Bloomberg Dollar Spot Index hitting a fresh three-year low and headed for its sixth week of losses – its longest weekly losing streak in almost a year – amid concerns over a potential U.S. government shutdown that outweighed any benefit the greenback normally gets from higher yields. Some thoughts from Bloomberg:

- BBDXY declines 0.3% Friday and is down 0.9% this week; it reached 1,130.91, lowest since January 2015

- Temporary funding for the U.S. government is due to run out midnight Friday

- 10-year U.S. Treasury yield was little changed at 2.63%; reached 2.6407%, highest since September 2014

The pound was among the beneficiaries of greenback weakness and extended its recent run to hit a fresh high since the June 2016 Brexit. According to Bloomberg, given it’s unlikely to get dovish headlines on the Brexit front, at least until the EU March summit gets into play, sterling finds a bid from short-term and momentum accounts.

The moves in American assets however dominated global markets, with the euro, yen, gold and base metals among the beneficiaries of the weaker dollar. The risk-on mood that helped drive up Treasury yields was still in evidence, with European stocks following Asian peers higher, U.S. futures pointing to gains and emerging-market equities climbing for a sixth day. Over in Asia, the Yuan briefly gained beyond 6.40 per dollar for first time since 2015 as the PBOC again strengthened the daily fixing and injected a net 80BN of liquidity.

In commodities, WTI and Brent and crude futures trade lower with markets keeping a close eye on US production after the DoE inventory data on Thursday and following monthly oil market reports from OPEC and the IEA. The DoE data showed US production rebounded over 2% in the latest week to 9.75mln bpd, while the IEA today said that US production could soon top 10mln bpd, and overtake Saudi Arabia and Russia. Precious metals are benefitting from the weak USD and as markets fear a potential US federal government shut down. IEA says global oil supply in December fell by 405k bpd to 97.7mln bpd due to lower North Sea and Venezuelan output. The IEA also saw US crude supply is set to push past 10mln bpd, overtaking Saudi Arabia and rivalling Russia

Bulletin headline Summary from RanSquawk

- Stop gap bill to fund government through to mid-Feb was passed by the House, however faces dim chances of passing a Senate vote.

- GBP back towards 1.39 following soft retail sales which had been distort by Black Friday sales in Novembers reading.

- Looking ahead, highlights include US U. of Michigan Sentiment data and comments from Fed’s Quarles, Bostic and Williams.

Market Snapshot

- S&P 500 futures up 0.3% to 2,805.25

- STOXX Europe 600 up 0.4% to 400.34

- MSCi Asia Pacific up 0.7% to 183.69

- MSCI Asia Pacific ex Japan up 0.6% to 599.11

- Nikkei up 0.2% to 23,808.06

- Topix up 0.7% to 1,889.74

- Hang Seng Index up 0.4% to 32,254.89

- Shanghai Composite up 0.4% to 3,487.86

- Sensex up 0.6% to 35,468.93

- Australia S&P/ASX 200 down 0.2% to 6,005.81

- Kospi up 0.2% to 2,520.26

- German 10Y yield rose 0.8 bps to 0.581%

- Euro up 0.3% to $1.2277

- Italian 10Y yield fell 1.1 bps to 1.721%

- Spanish 10Y yield fell 3.5 bps to 1.458%

- Brent Futures down 0.9% to $68.68/bbl

- Gold spot up 0.7% to $1,335.99

- U.S. Dollar Index down 0.3% to 90.27

Overnight Top Headlines from Bloomebrg

- The Federal Reserve is working to relax a key part of post- crisis demands for drastically increased capital levels at the biggest banks, according to people familiar with the work, a move that could free up billions of dollars for some Wall Street’s giants

- U.S. House passes stopgap govt funding bill, Senate reconvenes at 11 a.m. Eastern today; click here for the latest on the shutdown saga

- White House is said to consider John Williams as Fed vice chair: WSJ

- Fed’s Mester backs three to four rate hikes this year and next; Dudley repeats concern fiscal stimulus may cause overheating

- NAFTA: U.S. is losing patience with slow pace of talks, wants concrete progress next week; threat to withdraw is serious, according to people familiar

- Germany’s Social Democratic Party is looking for ways to sweeten another stint in government with Angela Merkel as the political impasse in Europe’s biggest economy comes to a head

- The Bank of Japan is optimistic about hitting its 2% inflation target within two years and is considering how best to communicate any possible policy changes, WSJ reports, citing unidentified people familiar with its thinking

- Global equity funds see “massive” weekly inflows of $24b, with the four-week inflow to stocks the biggest ever at $58b, signaling investors’ “fear of missing out”, BofAML strategists write in note, citing EPFR Global data

Asia equity markets mostly traded in the green after a subdued performance on Wall St and with focus on whether Congress can avert a government shutdown. ASX 200 (-0.2%) was weighed by continued weakness in commodity-related stocks as well as a lacklustre financial sector, while Nikkei 225 (+0.2%) saw initial upside pared as participants awaited developments in Washington where the stop gap bill to fund government through to February 16th was passed by the House, but faces less certainty at the Senate. Elsewhere, Hang Seng (+0.2%) somewhat took a breather from its recent ascent to all-time highs and Shanghai Comp. (+0.4%) was positive after yesterday’s GDP numbers and firm liquidity efforts by the PBoC. Finally, 10yr JGBs were marginally lower as Japanese yields increased in tandem with global peers including the US 10yr yield which rose above 2.63% and its highest since 2016.

PBoC injected CNY 130bln via 7-day reverse repos, CNY 90bln via 14-day reverse repos and CNY 10bln via 63-day reverse repos for a weekly net injection of CNY 590bln vs. last week’s CNY 40bln net injection. BoJ is said to be optimistic in achieving their 2% inflation target withing two years but are cautious on the next move. People close to the BoJ say the market overreacted to the change in Rinban operations, which they say wasn’t meant to signal any roader policy shift. As a guide, this is relatively the same as recent source reports from the BoJ.

Top Asian News

- China’s State-Backed Firms Are World Beaters Early in 2018

- This Is How China’s Regions Fare in the Fake GDP Data Stakes

- Japan Governor Witholding Reactor Decision During 3-Year Study

- Bunds On Back-Foot Again as Treasuries Slide Continues to Weigh

- Demand for Euro Calls Outweighs Puts This Week Ahead of ECB Meet

- BOJ Is Said Optimistic to Hit 2% Inflation Target in 2 Yrs: WSJ

Equity markets are higher across the board, appearing to shrug off concerns over the potential government shutdown. The Dax is outperforming, led by ThyssenKrupp after they confirmed their targets and BASF who continue to rally after their positive trading update late yesterday. The FTSE underperforms slightly with a number of smaller companies issuing profit warnings, including: Carpetright, Dignity and Bonmarche whose shares all plummeted between 20% and 50%. Although none of these companies are in the FTSE 100, the knock on effect is clear to see with Kingfisher, a competitor to Carpetright, propping up the index. US equity futures pushed higher after reports that the Fed is said to be working on plans to relax bank leverage ratio which could free up billions in bank capital.

Top European News

- U.K. Retailers See Black Friday Hangover as Sales Plunge 1.5%

- BASF Aims to Muscle Itself Onto Battery Materials’ Top Table

- Britain’s Black Belt in EU Law Says She Can’t Fight Brexit

- GOP Conservatives Brought Russia Probe Demand to Shutdown Talks

- Ceconomy Shares Plummet as Black Friday Discounts Erode Profit

In commodities, WTI and Brent and crude futures trade lower with markets keeping a close eye on US production after the DoE inventory data on Thursday and following monthly oil market reports from OPEC and the IEA. The DoE data showed US production rebounded over 2% in the latest week to 9.75mln bpd, while the IEA today said that US production could soon top 10mln bpd, and overtake Saudi Arabia and Russia. Precious metals are benefitting from the weak USD and as markets fear a potential US federal government shut down. IEA says global oil supply in December fell by 405k bpd to 97.7mln bpd due to lower North Sea and Venezuelan output. It maintained its 2018 global oil demand forecast at 1.3mln bpd, down from 2017 growth of 1.6mln bpd. US crude supply is set to push past 10mln bpd, overtaking Saudi Arabia and rivalling Russia.

In FX, the USD remained on the back foot in European trade as the threat of a government shutdown in the US becomes a reality ahead of the Senate vote. 60 votes in the Senate are needed to fund the government but it appears that the Republicans don’t even have the full support of everyone in their own party so getting an additional 10-15 from the Democrats seems unlikely. The JPY remained strong as sources in the WSJ said that the BoJ is optimistic of reaching its 2% inflation target within two years. UK retail sales disappointed, falling 1.5% M/M vs. expectations of a smaller 0.6% decline. Nevertheless, despite a brief dip in GBP on the back of the figures, GBP/USD reversed course as the ONS stated that shoppers are just moving their shopping earlier (NB: November data was much better than expected).

Looking at the day ahead, the December retail sales in the UK and the preliminary University of Michigan consumer sentiment print in the US are the only data of note due. Friday also marks the deadline for the US government shutdown. Oil giant Schlumberger is due to report earnings

US Event Calendar

- 10am: U. of Mich. Sentiment, est. 97, prior 95.9; Current Conditions, est. 114.4, prior 113.8; Expectations, est. 85.3, prior 84.3

- 8:45am: Fed’s Bostic Speaks on U.S. Economy in Nashville

- 8:45am: Fed’s Bostic Speaks on the Economy

- 1pm: Fed’s Quarles Speaks on Bank Regulation

DB’s Jim Reid concludes the overnight wrap

It’s still unclear whether we’ll get some political turbulence in the US as the shutdown vote gets passed to the Senate this morning. Overnight the House has voted 230-197 to pass a spending bill to avoid the US government shutdown and extend funding till 16 February. This was the easy part given the Republican’s majority in the lower House. Looking ahead, the Senate has taken an initial vote, but needs an additional procedural step that requires 60 votes, which means the Republicans need the help of at least nine Democrat votes to pass the bill. Bloomberg noted Senate Democrats say they have the votes to block the bill, in part to force Republicans to discuss other matters such as the protection for young immigrants. So an evolving situation until Friday morning when the Senate reconvenes (US time).

Staying in the US, the Fed’s Dudley has warned that the longer term risks from US tax cuts may be “that the economy could actually overheat, that inflation might not stop at 2%….or 2.2%…and then the Fed would have to step on the brakes a bit harder”. As a reminder, our US team noted that if fiscal changes only provide demand-side stimulus, they could quicken the arrival of the next recession by pulling forward demand and causing the Fed to move more aggressively on rate hikes. Refer to their note for details. Elsewhere, the WSJ reported that the White House is considering the Fed’s John Williams for the role of Fed Vice Chairman

This morning in Asia, markets are trading modestly higher. The Hang Seng (+0.24%), Kospi (+0.09%), China’s CSI300 (+0.75%) and Nikkei (+0.1%) are all modestly up. After the bell in the US, AMEX’s 4Q result was above market but guidance for next year was lower than consensus expectations (adj. EPS of $6.90ps-$7.30ps vs. $7.38ps) – its shares are trading c2.7% lower.

Now recapping performance from yesterday. After the record close on Wednesday, US equities bounced around for most of the day to close modestly lower, with the S&P (-0.16%), Dow (-0.37%) and Nasdaq (-0.03%) all down. Within the S&P, most sectors weakened with losses led by the real estate and energy sectors, while telco and tech stocks were slightly up. European equities were firmer, in part driven by the beat on Chinese GDP. Across the region, the Stoxx 600 nudged 0.19% higher, with the DAX leading the gains (+0.74%) following its underperformance back on Wednesday, while Spain’s IBEX 35 fell 0.40%. The VIX was up for the fifth consecutive day to 12.22 (+2.6%) and to the highest since mid-November.

Over in government bonds, UST 10y bond yields rose 3.5bp to 2.627%, marking a fresh ten month high, and approaching 3 and a half year highs, in part weighed down by concerns of a potential government shutdown. Notably, yesterday’s auction of $13bn 10y TIPS went smoothly and attracted a bid-to-cover ratio of 2.69 – the highest since May 2014. Elsewhere, core European 10y bond yields were up 1-2bp (Bunds +1bp; Gilts +2.2bp) while peripherals outperformed with yields down c1bp.

Turning to currencies, the US dollar index was marginally lower (-0.05%), while the Euro and Sterling both gained c0.4%, with the latter rising to another post Brexit high. In commodities, both WTI oil and Gold were broadly flat, while other base metals were mixed but little changed (Zinc -0.12%; Copper +0.09%; Aluminium +0.72%).

Away from the markets and onto ECB central bankers speak. The ECB’s Coeure seemed relatively upbeat on the Euro economy, he noted “we ourselves at the ECB have stopped saying we want to strengthen the recovery, it’s not a recovery anymore, it’s an expansion”.

Elsewhere, the Bundesbank’s Weidmann noted Germany needs better fiscal spending, but not necessarily more. He said “raising public spending…to reduce Germany’s current account surplus would likely be a futile undertaking”, while this does not mean no action on fiscal policy, particularly to counteract the demographic drag on growth, but “action (is) not with regard to the overall stance, but with regards to how the money is spent”. On the issue of low wage growth despite tight labour market conditions, he noted Germany is not unique here, which suggests “that the factors responsible for holding back wage growth are not only idiosyncratic, but at least partly international as well”.

Staying in Germany, the former head of the SPD Kurt Beck predicts the c600 party delegates will vote “about 60-40” in favour of coalition talks with Ms Merkel’s bloc at this Sunday’s party convention. Elsewhere, Ms Merkel’s caucus chief noted that post a potential yes vote from the SPD, there is unlikely to be major changes to the preliminary accord already agreed upon. He said “what has been negotiated in the exploratory negotiations has been negotiated and can’t be revisited”.

Back onto Brexit, there seems to be a softening in the EU’s stance on whether to include UK based financial services firms in a trade deal post Brexit, provided the UK pays for it. The French President Macron noted “you want to accept a single market with finance being part of it? Be my guest, but that means financial contributions and accepting European jurisdiction”. Elsewhere, he said his overriding goal is to ensure the “single market is preserved”, but it’s “very much” up to the UK to decide what it wants.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the January Philly Fed index fell 7.7pt to a still solid level of 22.2 (vs. 25 expected). In the details, the new orders index dropped 18.1pts to 10.1 (a 16-month low) but the shipments index rose 6.4pts to 30.3 and the prices paid index rose 5.1pts to 32.9. Elsewhere, December housing starts were lower than expected (-8.2% mom vs. -1.7%), largely due to a decline in starts from elevated November levels in the South, while building permits fell less than expected (-0.1% mom vs. -0.6%). Finally, the weekly initial jobless claims fell to the lowest since 1973 (220k vs. 250k expected), while continuing claims was slightly higher than expectations (1,952k vs. 1,900k). This week corresponds to survey week for payrolls so we could get a bump to estimates.

In China, 4Q GDP was above market expectations at 6.8% yoy (vs. 6.7%) which has led to the first annual growth since 2010 (2017: 6.9%; 2016: 6.7%). Factoring in the latest readings, our economists have upgraded their Q1 and Q2 growth forecast to 6.5% and 6.3% (from 6.3% and 6.1%), but have kept their full year forecast for 2018 unchanged at 6.3%. Overall, they expect a tightening of fiscal policy and financial regulation to gradually slow the economy. Indeed, they argue that the resilient economic data will likely encourage the policy makers to maintain a tightening policy stance in the next few months.

Looking at the day ahead, the December retail sales in the UK and the preliminary University of Michigan consumer sentiment print in the US are the only data of note due. Friday also marks the deadline for the US government shutdown. Oil giant Schlumberger is due to report earnings and I’m on a train back home so hopefully I’ll avoid a repeat of the outbound journey.

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 13.11 points or 0.38% /Hang Sang CLOSED UP 132.95 pts or 0.41% / The Nikkei closed UP 44.69 POINTS OR 0.19%/Australia’s all ordinaires CLOSED DOWN 0.18%/Chinese yuan (ONSHORE) closed WELL UP at 6.4035/Oil DOWN to 63.54 dollars per barrel for WTI and 68.69 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4035. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4003//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(GOOD MARKETS )

3 a NORTH KOREA/USA

NORTH KOREA/SOUTH KOREA/USA

The Pentagon temporarily deploys 3 types of strategic bombers to Guam in anticipation of problems in North Korea

(courtesy zerohedge)

Pentagon Temporarily Deploys 3 Types Of Strategic Bombers To Guam

Amid soaring tensions between Washington and Pyongyang, the Pentagon has deployed nearly every type of strategic and nuclear-capable bomber to the island of Guam, an American territory in Micronesia, in the Western Pacific.