GOLD: $1332.15 DOWN $0.85

Silver: $16.98 DOWN 5 cents

Closing access prices:

Gold $1334.50

silver: $17.01

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1339.90 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1331.55

PREMIUM FIRST FIX: $8.45

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1340.19

NY GOLD PRICE AT THE EXACT SAME TIME: $1329.90

Premium of Shanghai 2nd fix/NY:$10.29

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1335.80

NY PRICING AT THE EXACT SAME TIME: $1336.10

LONDON SECOND GOLD FIX 10 AM: $1332.60

NY PRICING AT THE EXACT SAME TIME. $1331.85

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 50 NOTICE(S) FOR 5000 OZ.

TOTAL NOTICES SO FAR: 522 FOR 52200 OZ (1.6236 TONNES),

For silver:

jANUARY

19 NOTICE(S) FILED TODAY FOR

95,000 OZ/

Total number of notices filed so far this month: 707 for 3,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $11,260/OFFER $11,360 DOWN $72 (morning)

Bitcoin: BID $10,135/OFFER $10,229 DOWN $1200.00 (CLOSING/4 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE 2641 contracts from 194,808 RISING TO 197,449 WITH FRIDAY’S SMALL 9 CENT GAIN IN SILVER PRICING. WE THUS HAVE ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 828 EFP’S FOR MARCH AND ZERO FOR OTHER MONTHS AND THUS TOTAL ISSUANCE OF 828 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 828 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

34,252 CONTRACTS (FOR 15 TRADING DAYS TOTAL 34,252 CONTRACTS OR 171.260 MILLION OZ: AVERAGE PER DAY: 2283 CONTRACTS OR 11.417 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 171.3 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.42% OF ANNUAL GLOBAL PRODUCTION

RESULT: A GOOD SIZED GAIN IN OI COMEX DESPITE THE TINY 9 CENT GAIN IN SILVER PRICE WHICH USUALLY INDICATES ANOTHER FAILED BANKER SHORT-COVERING. WE ALSO HAD A SMALL SIZED EFP ISSUANCE OF 828 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 828 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 3469 OI CONTRACTS i.e. 828 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2641 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE SMALL RISE IN PRICE OF SILVER OF 9 CENTS AND A CLOSING PRICE OF $17.03 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.987 BILLION TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 19 NOTICE(S) FOR 95,000 OZ OF SILVER

In gold, the open interest SHOCKINGLY FELL BY A CONSIDERABLE 8623 CONTRACTS DOWN TO 586,528 DESPITE THE GOOD SIZED RISE IN PRICE OF GOLD WITH FRIDAY’S TRADING ($6.00). IN GOLD THE LONGS STARTED THEIR MOVEMENT FROM COMEX LONGS OVER TO LONDON BASED FORWARDS THROUGH THE EFP ROUTE. WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR MONDAY AND IT TOTALED A GOOD SIZED 5774 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 5774 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS The new OI for the gold complex rests at 586,528. ALSO REMEMBER THAT THERE CAN BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY WE HAVE A SMALL LOSS OF 2849 CONTRACTS: 8623 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 5774 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. EXPECT HUGE NUMBERS OF EFP’S TO BE ISSUED AS WE APPROACH FIRST DAY NOTICE IN THE GOLD FEB COMEX CONTRACT, WEDNESDAY JAN 31.2018

FRIDAY, WE HAD 5867 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 140,491 CONTRACTS OR 1.40491 MILLION OZ OR 436.98 TONNES (15 TRADING DAYS AND THUS AVERAGING: 9366 EFP CONTRACTS PER TRADING DAY OR 9366 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 15 TRADING DAYS: IN TONNES: 437 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 437/2200 TONNES = 19.86% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

Result: A SHOCKINGLY STRONG SIZED DECREASE IN OI AT THE COMEX DESPITE THE GOOD SIZED RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($6.00). WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5774. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5774 EFP CONTRACTS ISSUED, WE HAD A NET LOSS IN OPEN INTEREST OF 2849 contracts ON THE TWO EXCHANGES:

5774 CONTRACTS MOVE TO LONDON AND 8623 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 6.10 TONNES). HOWEVER THE LOSS IN OI IS DUE TO THE DELAY IN THE ISSUANCE OF EFP’S WHICH CAN GENERALLY TAKE UP TO AN ADDITIONAL 48 HRS.

we had: 50 notice(s) filed upon for 5000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

With gold DOWN $0.85, we had a huge change in gold inventory at the GLD/a monstrous deposit of 5.71 tonnes/

Inventory rests tonight: 840.96 tonnes.

SLV/

A BIG CHANGES IN SILVER INVENTORY AT THE SLV/A HUGE WITHDRAWAL OF 1.321 MILLION OZ FROM THE SLV INVENTORY/

INVENTORY RESTS AT 314.179 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 2641 contracts from 194,808 UP TO 197,449 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY SIZED RISE IN PRICE OF SILVER TO THE TUNE OF 9 CENTS WITH RESPECT TO FRIDAY’S TRADING. OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 828 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2641 CONTRACTS TO THE 828 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A BIG GAIN OF 3469 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 17.345 MILLION OZ!!!

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE TINY SIZED RISE OF 9 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 828 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 13.49 points or 0.39% /Hang Sang CLOSED UP 138.52 pts or 0.43% / The Nikkei closed UP 8.27 POINTS OR 0.03%/Australia’s all ordinaires CLOSED DOWN 0.21%/Chinese yuan (ONSHORE) closed UP at 6.4032/Oil DOWN to 63.35 dollars per barrel for WTI and 68.47 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4032. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.4069//ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS VERY HAPPY TODAY.(GOOD MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)/South Korea/North Korea/USA

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

( zerohedge)

( zerohedge)

6 .GLOBAL ISSUES

Trouble in Montego Bay, Jamaica as the military are called in due to a large number of homicides because of gang related issues.

( zerohedge)

ii)Trump initiates a huge trade war as they especially target China as they impose a 30% tariff on solar panel imports. Solar panels utilize considerable amounts of silver per panel

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)SaturdayCrypto currencies attempt a comeback only to falter again

( zerohedge)

ii)Monday morning:

Cryptos are crashing again

(zerohedge)

iii)Chris Powell discusses the worldwide struggle for the control of gold

( ChrisPowell/GATA)

iv)China is now engaging in activities to stop the financing of cryptocurrencies

( South China Morning Post/HongKong)

v)If the UK determines that the bitcoin profits was the result of gambling then it would be tax free

( Morley/London Telegraph)

vi)These guys are pretty good: They are stating that production will fall off the cliff starting this year

( /Daily Economist)

10. USA stories which will influence the price of gold/silver

i)FRIDAY NIGHT:

USA GOVERNMENT HAS SHUT DOWN

( ZEROHEDGE)

ii)MONDAY MORNING:

( zerohedge)

iiib)Although stocks initially rose this morning when there was no deal, stocks and the dollar rose on the 3 week deal to end government shutdown( zerohedge)

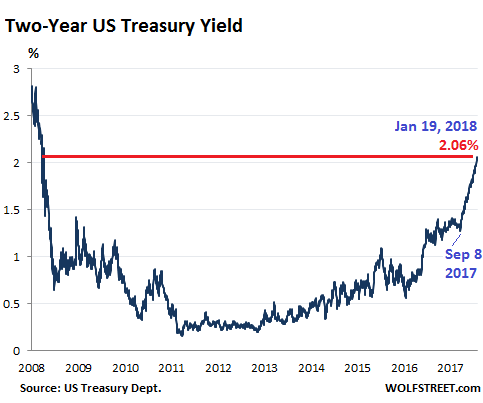

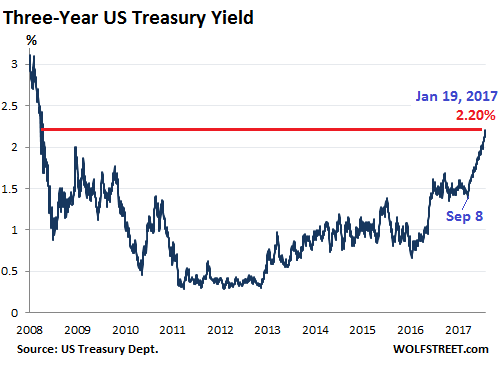

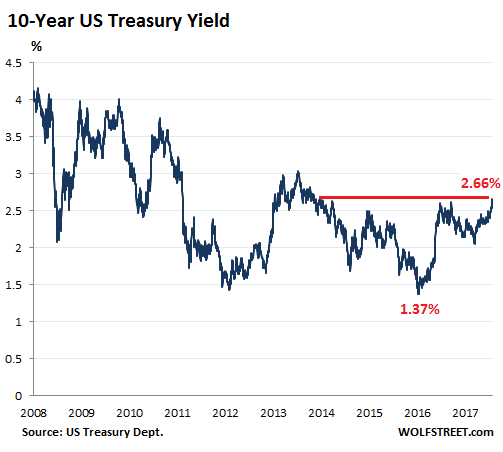

iv) The rise in the 10 yr bond yield to 2.66% on Friday has already had an effect on increasing mortgage rates. Together with the changing tax law on tax deductibility, the entire housing complex could be in for a rough ride.( WolfRichter/WolfStreet)

v)Amazon is now ready to open up its first fully automated grocery store to the public. No need for checkouts as cameras and scanners pick up what shoppers want and put back. They had not figured out children who pick up products and place them back in the wrong spot. Credit cards on file are debited once the customer leaves the store.

( zerohedge)

vi)Trump releases his 1 trillion infrastructure plan and it basically lacks a lot of details

(courtesy zerohedge)

a)Former Fed Prosecutor,Joe Di Genova lays out perfectly the plot to exonerate Hillary Clinton and frame Donald Trump..a must read..

( zerohedge)

go figure..

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SHOCKINGLY FELL BY A CONSIDERABLE 8623 CONTRACTS DOWN to an OI level of 586,528 DESPITE THE RISE IN THE PRICE OF GOLD ($6.00 GAIN WITH RESPECT TO FRIDAY’S TRADING). WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION AS THE LONGS HAVE STARTED ON THE MIGRATION INTO LONDON BASED FORWARDS THROUGH THE EFP ROUTE. THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT A GOOD SIZED 5774 EFP’S WERE ISSUED FOR FEBRUARY , 0 EFP’s FOR APRIL, AND 0 FOR DECEMBER: TOTAL 5774 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE CAN BE A DELAY OF UP TO 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS AS THEY ARE NEGOTIATING A PRIVATE EFP CONTRACT WITH THE BANKS… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE LOST TODAY: 2849 OI CONTRACTS IN THAT 5774 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 8823 COMEX CONTRACTS. NET LOSS ON THE TWO EXCHANGES: 2849 contracts OR 284,900 OZ OR 8.86 TONNES

Result: A SURPRISING AND STRONG DECREASE IN COMEX OPEN INTEREST DESPITE THE RISE IN FRIDAY’S GOLD TRADING ($6.00.) WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST LOSS ON THE TWO EXCHANGES: 2849 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest FALL by 156 contracts FALLING TO 75. We had 19 notices served upon yesterday so we LOST 137 contracts or an additional 13700 oz of gold will NOT stand AT THE COMEX in this non active month of January AS THESE GUYS MORPHED INTO LONDON BASED FORWARDS

FEBRUARY saw a LOSS of 19,542 contacts DOWN to 290,547. March saw a LOSS of 16 contracts DOWN to 616. April saw a GAIN of 10,418 contracts UP to 179,983.

We had 50 notice(s) filed upon today for 5000 oz

a surprise: we receive the comex volumes and on time:

PRELIMINARY VOLUME TODAY ESTIMATED; 397,501

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 321,654

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE 2641 CONTRACTS FROM 194,808 UP TO 197,449 DESPITE YESTERDAY’S TINY 9 CENT RISE. WE WERE ALSO INFORMED THAT WE HAD ANOTHER SMALL SIZED 828 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 828. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE HAD ZERO LONG COMEX SILVER LIQUIDATION AND A GOOD SIZED RISE IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 3469 OPEN INTEREST CONTRACTS:

2641 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 828 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 3469 CONTRACTS

We are now in the poor non active delivery month of January and here the OI GAINED 17 contracts RISING TO 33. We had 5 notices served upon yesterday, so we GAINED 22 contracts or an additional 110,000 oz will stand for delivery AT THE COMEX AND QUEUE JUMPING CONTINUES

February saw a LOSS OF 9 OI contracts FALLING TO 158. The March contract GAINED 878 contracts UP to 138,255.

We had 19 notice(s) filed for NIL 95,000 for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 22/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

7233.75 OZ

SCOTIA

225 KILOBARS

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

NIL

|

| No of oz served (contracts) today |

50 notice(s)

5000 OZ

|

| No of oz to be served (notices) |

25 contracts

(2500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

522 notices

52200 oz

1.6236 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 44 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 50 contract(s) of which 7 notices were stopped (received) by j.P. Morgan dealer and 33 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (522) x 100 oz or 52200 oz, to which we add the difference between the open interest for the front month of JAN. (75 contracts) minus the number of notices served upon today (50 x 100 oz per contract) equals 54700 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (522 x 100 oz or ounces + {(75)OI for the front month minus the number of notices served upon today (50 x 100 oz which equals 54,700 oz standing in this active delivery month of JANUARY (1.701 tonnes). THERE IS 18.245 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 137 CONTRACTS OR AN ADDITIONAL 13700 OZ WILL NOT STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY AS THESE GUYS MORPHED INTO LONDON FORWARDS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 65 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

19,154.319 oz

Scotia

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,225,783.000 oz???

JPMORGAN

|

| No of oz served today (contracts) |

19

CONTRACT(S)

(95,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 707 contracts

(3,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) JPMorgan continues to add silver to its inventory:

Deposit: 1,225,783.000 ??? oz

total inventory deposits: 1,225,783.000 oz

we had 2 withdrawals from the customer account;

i) Out of Scotia: 18,128.100 oz

ii) Out of Delaware: 1026.219 oz

total withdrawals; 19,154.319 oz

we had 0 adjustment

total dealer silver: 45.461 million

total dealer + customer silver: 248.016 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 19 contract(s) FOR 95,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 707 x 5,000 oz = 3,535,000 oz to which we add the difference between the open interest for the front month of JAN. (19) and the number of notices served upon today (19 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 707(notices served so far)x 5000 oz + OI for front month of JANUARY(19) -number of notices served upon today (19)x 5000 oz equals 3,535,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 22 CONTRACTS OR AN ADDITIONAL 110,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY AS QUEUE JUMPING INTENSIFIES AS WE PROCEED TO MONTH’S END.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3.790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

I almost fell from my chair: we received volumes at the comex and they were on time

ESTIMATED VOLUME FOR TODAY: 56,688

CONFIRMED VOLUME FOR FRIDAY: 65,105 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 65105 CONTRACTS EQUATES TO 325 MILLION OZ OR 46.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.96% (Jan 18/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.59% to NAV (Jan 18/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.96%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.70%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO 2.95%: NAV 13.92/TRADING 13.49//DISCOUNT 2.95%

MAKES NO SENSE!!

END

And now the Gold inventory at the GLD/

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 19/2018/ Inventory rests tonight at 846.67 tonnes

*IN LAST 312 TRADING DAYS: 94.48 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 246 TRADING DAYS: A NET 62.83 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 19/2017:

Inventory 314.179 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.76%

12 Month MM GOFO

+ 2.11%

30 day trend

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Global Pension Ponzi – Carillion Collapse One Of Many To Come

Pension Crisis And Deficit of £2.6B At Carillion To Impact UK Pensions

– Carillion collapses leaving a £900 million debt pile and 30,000 pensions at risk

– Carillion PLC share price has collapsed 94% in last twelve months

– Private analysis of Carillion’s pension deficit reveals it to be as high as £2.6 billion

– Figure adds to the UK’s ongoing pension crisis, both private and state are severely underfunded

– UK’s Private Pension Fund already has a levy of £550 million for next twelve months

– UK state pension crisis as state fund to be ‘exhausted by 2033’

– Ensure your pension is funded and properly diversified with gold

Editor: Mark O’Byrne

The looming pension crisis has been signalled in the collapse of Carillion. The deficit of latest private sector dead-on-arrival Carillion is officially £580 million. However, private reports suggest it could be as high as £2.6 BILLION.

According to a Sky News investigation: ‘the £2.6 billion figure relates to the cost to Carillion of paying an insurance company to guarantee all of its pension liabilities, and is significant because it is likely to be the sum claimed on behalf of the pension schemes as part of the liquidation process.’

Nearly 30,000 UK workers’ pensions are at risk thanks to Carillion management’s total mismanagement of a company that has seen its share price collapse 94% in the last 12 months.

Carillion’s 27,500-member pension scheme was placed on an ‘at risk list’ in autumn 2017. Arguably, it like many other pension funds should have been there many months ago.

Sadly, Carillion is just the latest in a very long string of serious company collapses that have highlighted the major pension crisis in the UK and around the Western world. It also likely signals that we may be on the verge of many, many more very large corporate bankruptcies in the UK due to massive debt levels and unfunded liabilities.

This is not a situation unique to the private sector. It will be repeated in the years ahead – both in the public and the private sector.

In November 2017, the OECD warned that the UK’s defined benefit workplace pension plans (final salary schemes) as ‘persistently underfunded’ and the state pension as seriously lacking.

Everyone is exposed by this and it emphasises the importance of saving for retirement and ensuring your pension is both funded and properly diversified.

These ongoing disasters in the UK’s pension pots are also a threat to the efforts of prudent individuals who have worked hard to set aside enough for their hard-earned retirements.

Private Pension Fund Palaver

The UK’s Private Pension Fund estimates that it will cost around £900m to cover the costs of the Carillion pension schemes. The idea of the PPF is that it is funded by liquid private companies who offer private pensions, as a sort of insurance should a Carillion-esque disaster strike.

The PPF rescue of Carillion pensioners is not a full-blown well-equipped life boat rescue, it’s more of a rubber dinghy and a metallic blanket. The rescue fund will pay current Carillion pensioners lower cost-of-living increases than they have been used to, and slash the eventual payments of those who aren’t yet retired.

The Telegraph explains the current state of the PPF:

As of March 2017, the PPF had £28.7bn in invested assets, and cash reserves of £6.1bn. It has a funding ratio – the fund’s assets versus its liabilities – of 121pc. The PPF is the backstop for final salary schemes, which pay guaranteed, inflation-proofed pensions for life.

At the moment (without the Carillion liability) the levy from the PPF is £550m. With this new expense companies who have their own defined-benefit schemes (and therefore must pay into the fund) will see their reviews increase. What damage will this do to the wider economy? How sustainable is a fund that is designed purely to rescue unfunded and bankrupt pension funds?

Why, if you are having to effectively-bailout the pension schemes of your failed contemporaries? Are you at all incentivised to invest in your own company, put up wages or even increase pension contributions yourself? It’s not as though the PPF is filling its contributors with confidence that levies are going to go down any time soon.

The failure of Carillion is a stark reminder that more often than not institutional shareholders, management board members and (in this specific case) politicians act in their own interest, frequently short term, rather than stopping to think what the overall, long term impact of their actions will be.

Reports state that Carillion over 2015 and 2016, £162 million has paid dividends to shareholders, compared with just £94 million to address the pension deficit.

The UK’s pension crisis

Last year we brought you the news that a Pensions and Lifetime Savings Association report found that three million workers with final salary pensions have 50% chance of losing up to fifth of their income because their employers have made unaffordable promises.

We outlined:

The PLSA data finds the most vulnerable employers have a 50:50 chance of not having an insolvency event in the next 30 years:

“More than 11 million people rely on defined benefit pension schemes for some or all of their retirement income but there is a real possibility that without change we will see more high profile company failures such as BHS or Tata Steel.”

Former pensions minister Steve Webb told City A.M. that he agrees:

“It’s not enough money. It’s just brutally not enough money going in,”

Just this week FCA Chief Executive Andrew Bailey made a point of the dangers looming for retirees, in his annual Mansion House speech:

“There is a clear risk that the savings rate for retirement is for many people too low to meet their expectations of retirement.”

The Carillion debacle will just add to this drama. The Private Pension Fund will once again have to step in and cover the expenses of the company’s 13 pension schemes.

Of course, at the moment all of the headlines are all about Carillion’s pension disaster. But what about the hundreds of sub-contracting firms who have their own schemes to cover? And are no longer going to be paid?

The ripple effect of the downfall of this firm will be far and wide. Yet again the mismanagement by the few will end up having an effect on the many. The pension crisis disaster could leave multiple pension pots unfunded and thousands of people bankrupt.

Private pensions are not alone

Many Brits and Europeans have more than one pension and this includes the state pension. For those in the United Kingdom, this is sadly also under threat.

Back in December, we brought you news of a report from the OECD that found those Brits planning to rely solely on their state pension will be left ‘with few resources.’ So bad is the situation that the body felt the need to remind politicians of the importance of long-term planning over short-term policy gains.

Inevitably, it is the tax payer who ends up forking out for government mistakes when it comes to misspending. Earlier this month the Government Actuary Department (GAD) said the rate of National Insurance (the manner in which Brits contribute to state pensions) may have to increase by as much as 5% in order to maintain the stability of the state pension fund.

This is bad news for both worker and employer. Estimates suggest this increase could add an additional £120 and £138, respectively in contributions from each party.

Furthermore, the lack of money means more time is required to have enough for retirees, therefore there is a suggestion that the retirement age is increased once again. This would be a measure to avoid increasing taxes.

GAD warned:

‘There won’t be enough coming in from National Insurance to cover the cost of paying the state pension…

‘To stop that happening, NI contributions have to go up or the government will have to make changes to the state pension or the age it is paid from.’

However, even with this and recently announced changes to minimum pension contributions the Department of Work and Pensions estimate 38% of the UK workforce are under-saving for retirement.

So for those who are saving and working, this is no doubt yet another cost that will come back to bite you no matter how responsible you have been with your own pension pot.

When it comes to your pension, beware who you trust

It is vital that savers and investors begin to take responsibility for their own pensions and ask questions. Most importantly one must ask if you can hold gold as part of your pension.

Gold should be a key part of your pension portfolio. At the moment UK pensions are at threat not just because of Carillion-esque disasters or bad planning by governments, but indirectly due to likely being used to bail-out pension pot implosions. Gold cannot be taken by governments or banks looking to top up their coffers.

The economy shows that whilst stock and bond markets have done well in the short term, they are artificially overvalued. Once again this is with thanks to the easy monetary policies of central banks and governments. So whilst readers may think they are in well-funded pension pots, or have some level of protection, where is the real value coming from?

Gold will protect in coming pension crisis

This is where gold plays a key role.

Dr. Constantin Gurdgiev, formerly an adviser to GoldCore, says the following about the importance of having gold in your pension:

“Gold is a long-term risk management asset, not a speculative one.

As such it should be analysed and treated predominantly in the context of its role as a part of a properly structured, risk-balanced and diversified portfolio spanning the full life-cycle of the investment and pension horizon for individual investors and those with pensions.

Whether they be SIPPs in the UK or IRAs in the USA.”

Investors in the UK and Ireland, the US, the EU can invest in gold bullion in their pension, through self-administered pension funds.

UK investors can invest in gold bullion through their Self-Invested Personal Pensions (SIPPs), Irish investors can invest in gold in Small Self Administered Schemes (SSAS) and US investors can invest in gold in their Individual Retirement Accounts (IRAs).

The pension crisis is a multi-trillion pound crisis. It is not going to go away. Adding physical gold to your pension is a key way to protect your retirement from the pensions time bomb.

As is owning physical gold outside a pension fund and as a hedge and safe haven, store of value.

Pension funds, throughout the West, have a distinct lack of diversification when it comes to assets. This has cost pension holders a huge amount of money and places their future viability at risk.

Gold bullion has an important role to play over the long term in preserving and growing pension wealth. Read our guide about how to own gold in a pension (CGT free) in the UK here.

Recommended reading

UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

Survey shows UK and US Pensions Crisis is Imminent

Pensions and Debt Time Bomb In UK: £1 Trillion Crisis Looms

News and Commentary

Gold steady; U.S. govt shutdown worries investors (Reuters.com)

Stocks Mixed, Dollar Flat With Shutdown in Focus (Bloomberg.com)

Palladium flows from west to east to meet industry demand (Reuters.com)

METALS START THE WEEK ON A STRONG FOOTING (BullionDesk.com)

Gold steady, palladium looks set to stay on the boil (BusinessLive.co.za)

Source: Statista

Risk of US government shut down as US 10 year rises above 2.6% (MoneyWeek.com)

Property Bubbles In Australia, Canada; Flying Blind at 20X as China Chills (MouldinEconomics.com)

Why A Hard Brexit Could Be Inevitable (ZeroHedge.com)

Silver as a Strategic Metal and Why Prices Will Soar (SilverSeek.com)

Futures exchange operator details discounts for secret trading by central banks (CMEGroup.com)

Gold Prices (LBMA AM)

22 Jan: USD 1,334.15, GBP 959.12 & EUR 1,087.87 per ounce

19 Jan: USD 1,335.80, GBP 960.17 & EUR 1,087.74 per ounce

18 Jan: USD 1,329.75, GBP 961.14 & EUR 1,088.40 per ounce

17 Jan: USD 1,337.35, GBP 969.45 & EUR 1,092.48 per ounce

16 Jan: USD 1,334.95, GBP 970.38 & EUR 1,091.32 per ounce

15 Jan: USD 1,343.00, GBP 971.93 & EUR 1,092.93 per ounce

Silver Prices (LBMA)

22 Jan: USD 17.04, GBP 12.25 & EUR 13.90 per ounce

19 Jan: USD 17.04, GBP 12.27 & EUR 13.89 per ounce

18 Jan: USD 17.09, GBP 12.31 & EUR 13.96 per ounce

17 Jan: USD 17.21, GBP 12.49 & EUR 14.10 per ounce

16 Jan: USD 17.10, GBP 12.43 & EUR 13.99 per ounce

15 Jan: USD 17.12, GBP 12.58 & EUR 14.14 per ounce

Recent Market Updates

– The Next Great Bull Market in Gold Has Begun – Rickards

– Gold Bullion May Have Room to Run As Chinese New Year Looms

– Digital Gold Flight To Physical Gold Coins and Bars

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– London Property Crash Looms As Prices Drop To 2 1/2 Year Low

– Gold Bullion Up 1% In Week, Heads For 5th Weekly Gain As Bonds Sell Off

– Gold Prices Rise To $1,326/oz as China U.S. Treasury Buying Report Creates Volatility

– Gold Hits All-Time Highs Priced In Emerging Market Currencies

– World is $233 Trillion In Debt: UK Personal Debt At New Record

– 10 Reasons Why You Should Add To Your Gold Holdings

– Spectre, Meltdown Highlight Online Banking and Digital Gold Risks

– Palladium Prices Surge To New Record High Over $1,100 On Supply Crunch Concerns

END

Crypto currencies attempt a comeback only to falter again

(courtesy zerohedge)

Crypto Comeback Continues; Shiller “Bitcoin Could Be Here 100 Years… Or Collapse Tomorrow”

After the biggest two-week drop since 2011, cryptocurrencies continue their post-futures-expiration comeback with Bitcoin testing $13,000…

And Ripple up 80% off its lows…

Once again some headlines from South Korea were full of contradiction as there are reports that both Bithumb & Korbit, the two largest cryptocurrency exchanges in South Korea, are disabling Kookmin Bank deposits and withdrawals. Instead, they will allow Shinhan Bank (second largest bank) deposits and withdrawals. That means, Shinhan Bank will process payments for traders, and implies there is no ban looming.

For now prices are rising once again but yet another establishment type – though to be fair, he is a little less biased than most – Nobel-prize winning economist Robert Shiller, predicts the cryptocurrency will either implode or drag on, and – as always – compares the rise of Bitcoin to the tulip craze in the 17th century.

“It has no value at all unless there is some common consensus that it has value,”Shiller, who is also Yale professor, told CNBC. The 2013 Nobel laureate in economics says while “other things like gold would at least have some value if people didn’t see it as an investment,” he doesn’t know “what to make of bitcoin ultimately.”

“It reminds me of the Tulip mania in Holland in the 1640s, and so the question is did that collapse? We still pay for tulips even now and sometimes they get expensive,” Shiller went on, referring to an economic bubble in the Netherlands in 1637, when after prices frantically grew the market suddenly fell apart.

“[Bitcoin] might totally collapse and be forgotten and I think that’s a likely outcome but it could linger on for a good long time, it could be here in 100 years,” Shiller said.

The economist has previously spoken of bitcoin on numerous occasions, calling it a “fad” and saying the “story” behind bitcoin drives enthusiasm for it. “A new form of money that… sounds extremely revolutionary and involves a very clever use of cryptography” has inspired interest among people.

Notably, Bitcoin’s slump this week has partially recovered to challenge $13,000, making it worth over 170 percent more than when Shiller made his previous bubble claims in early September, 2017.

Mike Novogratz remains extremely bullish, noting on Twitter that he has just finished 55 investor meetings in 6 days.

“I am very optimistic on the future of the Blockchain/Crypto space. Markets will trade up and down with events and sentiment shifts. regulators are coming which is a good thing. the revolution isn’t turning back. Long term bull.“

END

Monday morning:

Cryptos are crashing again

Cryptos Are Crashing Again…

From South Korean bank blocks to Bulgarian ponzi scheme shutdowns and a Bali bitcoin crackdown, you can take your pick as to what is driving the sudden plunge in cryptocurrencies this morning. Ethereum is back below $1000, Bitcoin is back to a $10k handle, and Ripple is down 30% from the weekend’s highs.

Weakness began around 6amET but really accelerated at around 8am ET…

With Bitcoin and Ethereum breaking key support levels..

The catalyst for the move is uncertain at best with numerous headlines over the weekend:

OneCoin offices were raided and its servers seized in Sofia, Bulgaria, on Jan. 17 and 18, as yet another step in a series of international raids and court cases against the highly-controversial altcoin. Although the servers were shut down, OneCoin currently remains operational.

Bitcoin exchanges are under fire in India, as many of the nation’s top banks have suspended or greatly curtailed functionality on exchange accounts. State Bank of India (SBI), Axis Bank, HDFC Bank, ICICI Bank and Yes Bank have all taken strong action toward crypto exchanges, either closing accounts or severely limiting functionality. The banks cite the risk of dubious transactions, according to local reports.

The biggest Nordic bank sent a memo to all its employees on Monday informing them that they will not be allowed to trade in Bitcoin and other cryptocurrencies. Nordea Bank AB will impose the ban from Feb. 28, after the board agreed to take a stand due to the “unregulated nature” of the market, spokeswoman Afroditi Kellberg said by phone. The bank had about 31,500 employees at the end of the third quarter.

Bitcoin is under heavy surveillance on Bali, an island in the Indonesian archipelago, according to local reports. Central Bank officials are seeking to crack down on the use of the cryptocurrency anywhere in the nation.

But we do note that the most recent plunge occurred as Bitcoin broke below its 100-day moving average at $10951…

As we noted yesterday, the Bitcoin futures short keeps growing…

And with the short overhang growing weekly, one wonders how long before a short squeeze – whether due to some long-overdue bullish catalyst or for some other reason – in unleashed first in bitcoin futures, then quickly cascading into the spot market, potentially unleashing the next move higher in the cryptocurrency space.

Year-to-Date, Ethereum remains the only big winner of the major cryptos…

Finally, as a reminder, this January weakness in Bitcoin is not unusual as it appears a pre-Lunar-New-Year sell-off is prevalent:

Chris Powell discusses the worldwide struggle for the control of gold

(courtesy ChrisPowell/GATA)

GATA secretary discusses worldwide struggle for control of gold

Submitted by cpowell on Sat, 2018-01-20 15:56. Section: Daily Dispatches

10:57a ET Saturday, January 20, 2018

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed yesterday by SD Bullion’s James Anderson for SilverDoctors.com, discussing GATA’s history, the cowardice and vulnerability of the monetary metals mining industry, the refusal of mainstream financial news organizations to address gold market rigging, China’s awareness of and cooperation with gold price suppression as it tries to hedge its foreign-exchange reserves, and the ancient struggle between the productive and financial classes, of which gold price suppression is a major part.

The interview is a half hour long and can be heard at Silver Doctors here:

https://www.silverdoctors.com/gold/gold-news/chris-powell-if-you-can-con…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

China is now engaging in activities to stop the financing of cryptocurrencies

(courtesy South China Morning Post/HongKong)

China orders banks to stop financing cryptocurrencies as noose tightens around disrupter

Submitted by cpowell on Sat, 2018-01-20 17:12. Section: Daily Dispatches

By Xie Yu

South China Morning Post, Hong Kong

Friday, January 19, 2018

The People’s Bank of China has ordered financial institutions to stop providing banking or funding to any activity related to cryptocurrencies, further tightening the noose since its shutdown of crypto exchanges last September sent digital currency enthusiasts fleeing overseas.

“Every bank and branch must carry out self-inspection and rectification, starting from today,” according to a document issued by the central bank on Wednesday. “Service for cryptocurrency trading is strictly prohibited. Effective measures should be adopted to prevent payment channels from being used for cryptocurrency settlement.

The Chinese-language document, as seen by the South China Morning Post, was distributed as an internal document among banks and not published on the central bank’s official website.

“Banks should enhance their daily transaction monitoring, and the timely shutdown of the payment channel once they discover any suspected trading of cryptocurrencies,” the document said, adding that the deadline for disclosing the measures is January 20.

The emphasis was on handling any capital settlement to avoid any financial losses by cryptocurrency investors from escalating into public protests — known as “group events” in China — and preserve social stability, the central bank said. …

… For the remainder of the report:

http://www.scmp.com/business/banking-finance/article/2129645/pboc-orders…

END

If the UK determines that the bitcoin profits was the result of gambling then it would be tax free

(courtesy Morley/London Telegraph)

If buying bitcoin was ‘gambling,’ its profits are tax-free in UK

Submitted by cpowell on Sat, 2018-01-20 17:46. Section: Daily Dispatches

The Tax-Free Bitcoin Loophole that Could Cost UK Treasury Millions

By Katie Morley

The Telegraph, London

Saturday, January 20, 2018

A tax loophole that reduces bitcoin investors’ gains to zero will be exploited by people filling in their returns for this tax year, potentially creating millions in lost revenue for the government, experts have warned.

Her Majesty’s Revenue and Customs is expecting to see a surge in the number of taxpayers declaring gains from cryptocurrencies this year after many investors sold their holdings after values soared, leaving them with huge profits.

However the taxman’s anticipated windfall could be far less than expected thanks to a loophole that lets taxpayers class their investment in cryptocurrency as “gambling,” winnings from which are tax-free. …

… For the remainder of the report:

http://www.telegraph.co.uk/news/2018/01/20/revealed-tax-free-bitcoin-loo…

Gold-backed and convertible cryptocurrency planned by Sprott

Submitted by cpowell on Sun, 2018-01-21 17:55. Section: Daily Dispatches

12:56p ET Sunday, January 21, 2018

Dear Friend of GATA and Gold:

Rick Rule, president of Sprott U.S. Holdings, interviewed this week by the Financial Survival Network’s Kerry Lutz, disclosed that in a few days Sprott plans to introduce a cryptocurrency that is backed by gold and convertible into metal vaulted at the Royal Canadian Mint in Ottawa.

The idea is to slash transaction costs for real metal and challenge the fees charged by exchange-traded funds and similar products.

Lutz’s interview with Rule is 24 minutes long and can be heard at the Financial Survival Network here:

http://financialsurvivalnetwork.com/2018/01/rick-rule-finally-a-gold-bac…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The futures exchange operator details huge discounts to government for secret trading by government. Since all trades go through the CME. , the crooks also receive inside trading on this and thus front run trades.

(courtesy Chris Powell/GATA)

Futures exchange operator details discounts for secret trading by central banks

Submitted by cpowell on Sun, 2018-01-21 18:07. Section: Documentation

1:11p ET Sunday, January 21, 2018

Dear Friend of GATA and Gold:

Central banks and governments that are secretly trading futures contracts in the United States on CME Group exchanges qualify for discounts ranging from 7 percent for two-year U.S. Treasury futures to 15 percent for gold and silver futures to 60 percent for Eurodollar futures.

Central banks and governments receiving these trading discounts cannot trade directly but must use CME Group clearing member firms for their trades, raising the question of whether those clearing members are able to trade for their own accounts on the basis of inside information from central banks, creators of infinite money

These details of the secret futures trading by central banks and governments are contained in a CME Group memorandum describing the discounts and posted at the CME Group’s internet site last month —

https://www.cmegroup.com/company/membership/files/CBIPFAQ.pdf

— and copied to GATA’s internet site just in case:

http://www.gata.org/files/CMEGroupCBIP-Q&A-December2017.pdf

The trading discounts, according to the memorandum, are available to “a non-U.S. central bank, multilateral development bank, multilateral financial institution, sub-regional bank, aid coordination group, or an international organization of central banks.”

These terms apparently would not exclude the U.S. Treasury Department or Federal Reserve if they acted through the U.S. government’s membership in international organizations like the Bank for International Settlements, International Monetary Fund, or the World Bank or through other central banks.

Indeed, last month an official of the Federal Reserve Bank of New York celebrated a century of cooperation by central banks in secretly rigging markets throughout the world:

http://www.gata.org/node/17966

The futures trading discounts extended by CME Group to governments and central banks were disclosed in 2014 by Eric Scott Hunsader of the market data firm Nanex in Winnetka, Illinois, through his research into CME Group’s filings with the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

But last month’s CME Group memorandum discloses details that seem new, starting with the percentage discounts provided and the requirement that central banks conduct their secret trading through intermediary firms associated with CME Group.

The memorandum was called to GATA’s attention by James Anderson of SD Bullion in Ottawa Lake, Michigan, who interviewed your secretary/treasurer for SilverDoctors.com on Friday:

http://www.gata.org/node/17971

Documentation of this secret trading in futures markets by governments and central banks has been provided by GATA to mainstream financial news organizations but they refuse to report it or to question governments and central banks about it.

Since governments and central banks have the power to create infinite money, they easily can become bigger than any market and the ordinary functioning of markets cannot be relied upon to defeat them. Only fearless journalism by large financial news organizations might do that.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

These guys are pretty good: They are stating that production will fall off the cliff starting this year

(courtesy /Daily Economist)

Peak gold mining? 2018 appears to be the year that gold mining output falls off a cliff

11:32 AMgold, gold mining, gold prices, manipulation, peak goldNo Comments

According to a recent presentation given to the Empire Club of Canada regarding market trends for 2018, a portion of the presentation showed what is happening in the gold mining sector and how it has been affected by depressed and manipulated gold prices.

According to Nick Barisheff over at the Market Oracle, gold production is expected to fall off a cliff beginning here in 2018, and will commence declining throughout the next 11 years.

Which begs the question… have we reached the point of Peak Gold?

Annual mine supply is about 2,800 tonnes, and it has been in decline since peaking in 2016. It is projected to decline by 76% by 2029. New mines take about 19.5 years to go into production. No new major discoveries over 3 million ounces have been made since 2009. As a result, the only adjusting factor for increased demand is an adjustment in price. With the global financial system experiencing a condition not seen since 1929 of a simultaneous triple bubble in stocks, bonds and real estate sitting on a historically unprecedented pile of $270 trillion of unpayable government debt, subprime auto debt, student loan debt, margin debt and consumer debt, in addition to a very dangerous mountain of over $600 trillion of derivatives, conditions are set for a major market correction. This will result in a massive increase in the price of gold as investors flee to the safety of gold. – Market Oracle

http://www.thedailyeconomist.com/2018/01/peak-gold- mining-2018-appears-to-be.html

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.4032 /shanghai bourse CLOSED UP AT 13.49 POINTS 0.39% / HANG SANG CLOSED UP 132.52 POINTS OR 0.43%

2. Nikkei closed UP 8.27 POINTS OR 0.03% /USA: YEN RISES TO 110.73

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 90.44/Euro RISES TO 1.2255

3b Japan 10 year bond yield: FALLS TO . +.079/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.73/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 63.35 and Brent: 68.47

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.583%/Italian 10 yr bond yield DOWN to 1.961% /SPAIN 10 YR BOND YIELD DOWN TO 1.444%

3j Greek 10 year bond yield RISES TO : 3.85?????????????????

3k Gold at $1332.65 silver at:17.03: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 16/100 in roubles/dollar) 56.56

3m oil into the 63 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.73 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9604 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1770 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.583%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.648% early this morning. Thirty year rate at 2.921% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets Shrug As US Government Shutdown Enters Day 3

Global stocks and U.S. bond markets on Monday shrugged off day three of the US government shutdown in Washington, although the dollar pulled back as the euro continued its strong start to the year, while U.S. stock index futures dipped less than 0.1% on expectations that the political impasse will not hurt the U.S. economy and that it will be resolved shortly, which may prove to be an overly optimistic outlook.

Here is Bloomberg’s quick on what has been a particularly quiet overnight session:

Exceptionally quiet European session due to lack of pertinent economic data or macro events, focus remains on U.S. government shutdown. USD is offered against G-10, DXY remains firmly within 90-91 range established last week. ZAR outperforms after reports that ANC leadership decided Zuma must leave office, albeit without a deadline. Core European equity markets trade flat, energy sector leads gains despite crude futures also trading unchanged, OPEC+ weekend meeting ended with recommendation to keep cuts for whole of 2018. UST curve holds overnight flattening, focus on long-end swap spreads which tighten back from blowout on Friday; Spain outperforms other EGBs after Fitch upgrade. Metals markets grind marginally higher across the board due to move in USD

U.S. Treasury yields, which fell during previous government shutdowns, rose as investors saw limited economic fallout from the standoff in the U.S. capital and instead focused on a global economy motoring ahead. The 10Y yield rose to to its highest level in more than three years on Monday, although it since faded some of the move.

Bunds were steady after weakening with Treasuries on Friday as USD swap spreads snapped wider. Spanish bonds jumped after Fitch upgraded Spain late on Friday: Spanish 10y bond yields open lower by 5bps at 1.39% after Fitch upgrades Spain to A- from BBB+; though flows have been very low so far, traders told Bloomberg. Strategists were split on the timing of the upgrade with many looking for the move later in the year. While there are no direct index implications, there was some expectation that an upgrade to A status would prompt fresh demand for Spanish bonds from more conservative funds. Most other euro zone bond yields were little changed – analysts said investors were probably moving to the sidelines before the European Central Bank’s first meeting of 2018 this Thursday.

Back to the US shutdown, where analysts appeared unimpressed: “These things have no near-term or midterm economic impact whatsoever,” said Michael Purves, chief global strategist and head of derivatives strategy for Weeden & Co in New York. “They are kind of embarrassing for the United States, but it’s not really going to alter business or consumer confidence,” he said.

“We’re not worried as we have been here before. Perhaps this is more fractious and may take longer to resolve, but it shouldn’t have a massive economic impact,” said Patrick O‘Donnell, investment manager at Aberdeen Asset Management.

And yet, as we explained on Saturday , the biggest reason why the market’s optimism may prove problematic, is should the shutdown stretch into late February or early March when the “X-date” for the US debt ceiling approaches, and put the US in danger of a technical default. This is how Pantehon’s Ian Shepherdson put it this morning:

In the worst case scenario, the budget impasse could drag on, via a series of stopgap measures, until March, perilously close to the point where the debt ceiling has to raised or suspended, as was the case from November 2016 through March last year. We would be astonished if Congress could not cobble together a majority of the sane in order to prevent a default. But astonishment has been quite common in response to events over the past couple of years, so investors would be well-advised to rule out nothing, however outlandish

For now, however, there is hope that a deal may be cobbled as soon as non on Monday: late on Sunday US Senate Majority Leader McConnell said the intention is to resolve immigration as quick as possible and declared the next Senate procedural vote will be held Monday at 12 ET vs. initial expectations of a 0100EST vote, while US Senate Minority Leader Schumer said they have yet to reach an agreement on a path forward. In related news, US Republican Senator Flake noted that a bipartisan meeting is to be held 1000EST to discuss continuing resolution, while US Senator Cornyn had earlier stated he was now more optimistic after leaving a GOP leaders’ meeting.

All of this remains lost on US equity futures however, which as noted above are barely in the red this morning, while major markets around the globe are mixed, with some happy to peek in the green. Wall Street, which had been resilient to the threat of a shutdown, rose on Friday, with the S&P 500 and Nasdaq notching record closing highs despite the imminent shutdown. Investors shrugged off the threat last week, saying they were not worried about a major pullback in shares if U.S. lawmakers failed to strike a deal. Eventually, stocks may have no choice but to sell if a compromise deal is to be “pushed” upon Congress.

Around the world, trader apathy was tangible. European shares traded with little clear direction as markets focused on a flurry of mergers and acquisitions and progress towards an end to political deadlock in Germany. Europe’s STOXX 600 index was largely flat while Germany’s DAX was down 0.1%, France’s CAC-40 was down 0.2% and the UK’s FTSE was unchanged. The MSCI world equity index was also flat. U.S. stock futures were down marginally after Wall Street set record highs on Friday.

In Asia, Australia’s ASX 200 (-0.2%) and Nikkei 225 (flat) were subdued as the US shutdown sapped investor sentiment, although downside was limited amid some hopes on resolving the impasse. Chinese markets were choppy in which the Shanghai Comp (Unch.) was flat and Hang Seng (-0.1%) initially stalled after it recently hit record levels, but was later underpinned amid outperformance in Shenzhen stocks. China’s ChiNext Index of small-cap and tech shares climbed as investors went bargain-hunting following gauge’s drop to a five-month low last week.

Finally, 10yr JGBs were flat despite a cautious tone in stocks, as participants were sidelined amid an enhanced liquidity auction for longer dated JGBs and as the BoJ kick-starts its 2-day policy meeting.

Of note, the People’s Bank of China injected cash into financial system via open-market operations for the eighth straight session, the longest run since November 2016. Onshore market. PBOC pumps in net 20b yuan through reverse-repurchase operations, taking total injections since Jan. 11 to 820b yuan. The onshore yuan little changed at 6.4030 per dollar as of 6:08pm in Shanghai, while the PBOC strengthens daily reference rate by 0.09% to 6.4112.

In macro, the Bloomberg Dollar Spot Index remained in defensive mode amid a government shutdown and a rebound in Treasuries. The euro held modest gains and bunds steadied as Germany took a step toward a coalition government. The pound found leveraged demand after the London open while EMFX and equities traded mixed. The EURUSD gained 0.2 percent and was trading at $1.2253, although volatility in the euro-dollar exchange rate was more muted than would have been expected, given flare-ups during previous U.S. government shutdowns.

“The market is accustomed with what is taking place in U.S. politics. It is not reading too far into the shutdown, which is more like a political show,” said Koji Fukaya, president of FPG Securities in Tokyo.

As reported yesterday, on Sunday Germany’s SPD voted in favor (362 for, 279 against) of formal coalition discussions with German Chancellor Merkel’s conservatives. There were also comments from SPD leader Schulz who said that coalition talks are going to be just as hard as the exploratory talks and that he hopes negotiations will start soon. As a reminder, the Euro Area will today begin their search for Vitor Constancio’s successor as ECB Vice President; Spain’s economy minister de Guindos has been touted as a likely successor.

Elsewhere, reports stated that US President Trump’s anger towards UK PM May puts a post-Brexit trade deal between the 2 nations at risk, and that the relationship is said to have soured. Meanwhile, cable got a boost after French President Macron said UK could get a special trade deal with EU post-Brexit, but will not have full access to the single market without accepting its rules, while he added the UK cannot cherry-pick the elements it liked.

Oil prices climbed higher after comments from Saudi Arabia that cooperation between oil producers who are withholding supplies would continue beyond 2018. Brent crude futures were at $68.67 a barrel at 0930 GMT, not far from the $70.37 level hit on Jan. 15. That was oil’s highest level since December 2014.

Bulletin Headline Summary from RanSquawk

- USD softens in reaction to US government shutdown, while EUR finds support from German politics.

- Equity failing to find any firm direction, with major indices somewhat mixed.

- Today’s calendar sees a lack of tier 1 highlights.

Market Snapshot

- S&P 500 futures down 0.09% to 2,808.50

- STOXX Europe 600 unchanged at 400.87

- MSCI Asia Pacific up 0.2% to 183.98

- MSCI Asia Pacific ex Japan up 0.3% to 600.48

- Nikkei up 0.03% to 23,816.33

- Topix up 0.1% to 1,891.92

- Hang Seng Index up 0.4% to 32,393.41

- Shanghai Composite up 0.4% to 3,501.36

- Sensex up 0.8% to 35,799.18

- Australia S&P/ASX 200 down 0.2% to 5,991.91

- Kospi down 0.7% to 2,502.11

- Brent Futures up 0.2% to $68.71/bbl

- Gold spot up 0.1% to $1,332.70

- U.S. Dollar Index down 0.1% to 90.47

- German 10Y yield rose 0.6 bps to 0.574%

- Euro up 0.2% to $1.2251

- Italian 10Y yield fell 2.7 bps to 1.694%

- Spanish 10Y yield fell 2.2 bps to 1.421%

Top Overnight News

- Lawmakers failed to negotiate an end to the government shutdown Sunday despite a bipartisan effort to broker a deal, raising the political stakes as federal agencies begin closing at the start of their normal workweek

- German Chancellor Angela Merkel moved forward in her bid to form a fourth-term government after her prospective coalition partner agreed to shelve its misgivings and enter negotiations on a common policy platform for Germany

- OPEC and Russia reaffirmed that they’ll persevere with oil-production cuts until the end of the year to clear a global glut and signaled their readiness to cooperate beyond that

- Greece is nearing a key milestone in its financial-crisis history, as it moves a step closer toward the exit from its rescue program; its creditors are set to start discussing better repayment terms for its bailout loans as euro-area finance ministers meet in Brussels today

Asia markets traded with a cautious tone as the region reacted to the US government shutdown, which heads into a 3rd day after the Senate failed to pass the spending bill through procedural vote on Friday, but are currently working on a shorter 3-week continuing resolution. ASX 200 (-0.2%) and Nikkei 225 (flat) were subdued as the US shutdown sapped investor sentiment, although downside was limited amid some hopes on resolving the impasse. Chinese markets were choppy in which the Shanghai Comp (Unch.) was flat and Hang Seng (-0.1%) initially stalled after it recently hit record levels, but was later underpinned amid outperformance in Shenzhen stocks. Finally, 10yr JGBs were flat despite a cautious tone in stocks, as participants were sidelined amid an enhanced liquidity auction for longer dated JGBs and as the BoJ kick-starts its 2-day policy meeting. PBoC injected CNY 60bln via 7-day, CNY 40bln via 14-day and CNY 10bln via 63-day reverse repos. PBoC set CNY mid-point at 6.4112 (Prev. 6.4169)

Top Asian News

- Hedge Fund Startups in Asia See Signs of Revival After Slow 2017

- Fresh Doubts Raised on China’s Bad-Loan Data as Fraud Uncovered

- Templeton’s $38b Bond Fund Builds U.S. Stake in Tilt From EM

- India’s Nifty 50 Futures Roll Is Cheap Days Before Expiration

- Cedar Who? When Obscure Chinese Buyers Pounce on Famous Targets

European equities have kicked the week off with little in the way of firm direction (Eurostoxx 50 -0.1%) with traders awaiting today’s procedural vote in the Senate at 1700GMT as the government shutdown continues. In terms of sector specifics, energy names outperform given the moves seen in oil markets, telecoms are also seen higher following positive comments from the Deutsche Telekom CEO (+1.6%). Elsewhere, other notable movers include, UBS (-2.5%) who trade lower in the wake of their earnings with markets overlooking their buyback and restructuring efforts. Further to this, Ocado (+12.7%) tops the Stoxx 600 after striking an international deal with Sobeys of Canada, William Hill (-12.9%) lags the Stoxx 600 after stake reductions on UK gambling machines. Finally, YOOX Net-a-Porter (+25%) are seen markedly higher after reports that Richemont are to offer EUR 38/shr for the Co.

Top European News

- Battle to Save United Europe Looms and Line Is Drawn at The Alps

- Italy’s Election Promises Heap Strain on Debt-Loaded Nation

- Greece Set to Enter Next Bailout Phase as Day-After Talks Near

- OPEC, Russia Signal Global Oil Alliance May Endure Past 2018

- Dixons Carphone Names Alex Baldock CEO to Replace James