GOLD: $1336.90 DOWN $4.85

Silver: $17.10 DOWN 6 cents

Closing access prices:

Gold $1338.50

silver: $17.13

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1345.27 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1335.75

PREMIUM FIRST FIX: $7.79

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1362.55

NY GOLD PRICE AT THE EXACT SAME TIME: $1335.55

Premium of Shanghai 2nd fix/NY:$27.00

SHANGHAI REJECTS FULLY NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1345.70

NY PRICING AT THE EXACT SAME TIME: $1343.45

LONDON SECOND GOLD FIX 10 AM: $1344.90

NY PRICING AT THE EXACT SAME TIME. $1346.00???

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 2 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR: 698 FOR 69800 OZ (2.1710 TONNES),

For silver:

jANUARY

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 730 for 3,650,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,959/OFFER $11,059 DOWN $183 (morning)

Bitcoin: BID/ $10,101/ $10,200 offer down 1035 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY SIZED 361 contracts from 200,827 RISING TO 201,188 DESPITE YESTERDAY’S BIG 26 CENT FALL IN SILVER PRICING. WE HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1460 EFP’S FOR MARCH AND AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1460 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1460 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

47,174 CONTRACTS (FOR 21 TRADING DAYS TOTAL 47,174 CONTRACTS OR 235.870 MILLION OZ: AVERAGE PER DAY: 2246 CONTRACTS OR 11.231 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 235.8 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 33.6% OF ANNUAL GLOBAL PRODUCTION

RESULT: A TINY SIZED LOSS IN OI COMEX DESPITE THE BIG 26 CENT FALL IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 1460 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1460 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 1333 OI CONTRACTS i.e. 1460 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 361 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 26 CENTS AND A CLOSING PRICE OF $17.16 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0060 BILLION TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest FELL BY A LARGE 8799 CONTRACTS DOWN TO 566,441 WITH THE GOOD SIZED FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($11.25). IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED A GOOD SIZED 11,909 CONTRACTS OF WHICH FEBRUARY SAW 3284 CONTRACTS ISSUED AND APRIL SAW THE ISSUANCE OF 8625 CONTRACTS. The new OI for the gold complex rests at 558,239. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DUE TO THE DELAY IN THE RELEASE OF YESTERDAY’S DATA YOU CAN BET THE FARM THAT THEY HAVE DELAYED THE RELEASE OF MANY EFPS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY WE HAVE A GAIN OF 3110 CONTRACTS: 8799 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 11,909 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. EXPECT HUGE NUMBERS OF EFP’S TO BE ISSUED AS WE APPROACH FIRST DAY NOTICE IN THE GOLD FEB COMEX CONTRACT, WEDNESDAY JAN 31.2018

YESTERDAY, WE HAD 4123 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 209,695 CONTRACTS OR 20.9695 MILLION OZ OR 652.22 TONNES (21 TRADING DAYS AND THUS AVERAGING: 9,985 EFP CONTRACTS PER TRADING DAY OR 998,500 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 21 TRADING DAYS: IN TONNES: 652 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 652/2200 TONNES = 29.63% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX WITH THE LARGE SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($11.25). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS ARE WAITING TO RECEIVE A PRIVATE EFP CONTRACT FOR EITHER FEBRUARY OR APRIL AND THESE GUYS ARE STILL NEGOTIATING THEIR DEAL. WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,909 AS THESE HAVE ALREADY BEEN NEGOTIATED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,909 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 3110 contracts ON THE TWO EXCHANGES:

11909 CONTRACTS MOVE TO LONDON AND 8799 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 9.67 TONNES).

we had: 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

With gold down another $4.85, we had a big changes in gold inventory at the GLD/a withdrawal of 1.47 tonnes of gold/

Inventory rests tonight: 846.67 tonnes.

SLV/

A NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 313.896 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A TINY 361 contracts from 200,827 DOWN TO 201,188 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE FAIR SIZED LOSS IN PRICE OF SILVER (26 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1460 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD MINIMAL COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 361 CONTRACTS TO THE 1460 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 1821 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 9.105 MILLION OZ!!!

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE FAIR SIZED LOSS OF 26 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER GOOD 1460 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 34.99 points or 0.99% /Hang Sang CLOSED DOWN 359.60 pts or 1.09% / The Nikkei closed DOWN 337.37 POINTS OR 1.43%/Australia’s all ordinaires CLOSED DOWN 0.895%/Chinese yuan (ONSHORE) closed UP at 6.3235/Oil DOWN to 64.92 dollars per barrel for WTI and 69.06 for Brent. Stocks in Europe OPENED IN THE RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3235. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.3279//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE MUCH STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT HAPPY TODAY.(STRONGER CURRENCY BUT WEAK MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

you knew that this was coming: a military showdown in Syria

( zerohedge)

( zerohedge)

6 .GLOBAL ISSUES

( London’s Financial times/)

7. OIL ISSUES

Oil and gasoline drop after a surprise crude oil build

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Our banker friends are doing a great job crushing cryptos again

( zerohedge)

ii)How will the deniers of gold market rigging explain the fines and convictions

( TFMetals/Craig Hemke/gATA)

iii)In case you missed yesterday’s big story: 3 banks and 8 individuals charged in gold/silver spoofing

( Reuters/GATA)

iv)Bill Murphy explains why our precious metals will rise in price

( Kitco/Bill Murphy/GATA)

10. USA stories which will influence the price of gold/silver

i)it seems that Met Life owes a lot of pensioners money that it had failed to pay and this may add up to tens of thousands of workers for the past years. The stock tumbled 10% in after hours. The big question is this a “lone wolf” with respect to MetLife or does this extend to other insurers who engaged in this type of deal

( zerohedge)

ii)A housing bust may be just around the corner: rates have now hit their highest level since 2014

( Mish Shedlock/Mishtalk)

iii)Home prices are rising faster than incomes:

( zerohedge)

iv)SWAMP STORIES

a)It looks like we have some text messages referring to destroying evidence etc The FBI is still withholding 85% if the texts and redacting many items that they refer to as personal.

The FBI is doing a good job of preventing the swamp from being drained

( zerohedge)

b)The house Intel committee votes to make the FISA memo public. The fun begins

( zerohedge)

c)FBI director Wray supposedly was shocked by the FISA warrant and more importantly there is talk that McCabe asked agents to change with 302’s which is without a doubt an obstruction of justice

d)Seems the noose is getting tighter and tighter around McCabe’s neck. The House Judiciary tells the FBI to preserve all emails of McCabe especially around the Trump election and afterwards.

Let us head over to the comex:

The total gold comex open interest FELL BY A CONSIDERABLE 8799 CONTRACTS DOWN to an OI level 556,441 of WITH THE GOOD SIZED FALL IN THE PRICE OF GOLD ($11.25 FALL WITH RESPECT TO YESTERDAY’S TRADING). WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A GOOD SIZED 3284 EFP’S ISSUED FOR FEBRUARY AND A HUGE 8625 EFP’s FOR APRIL: TOTAL 11,909 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 3110 OI CONTRACTS IN THAT 11,909 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 8799 COMEX CONTRACTS. NET GAIN ON THE TWO EXCHANGES: 3110 contracts OR 311,000 OZ OR 9.67 TONNES,

Result: A STRONG DECREASE IN COMEX OPEN INTEREST WITH THE FAIR SIZED LOSS IN YESTERDAY’S GOLD TRADING ($11.25.) WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 3110 OI CONTRACTS..

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest FALL by 0 contracts REMAINING AT 2. We had 0 notices served upon yesterday so we GAINED 0 contract or an additional NIL oz of gold will stand AT THE COMEX in this non active month of January as these guys joined others in obtaining a London based forward contract.

FEBRUARY saw a LOSS of 44,722 contacts DOWN to 32,327. March saw a GAIN of 59 contracts UP to 2197. April saw a GAIN of 31,373 contracts UP to 377,973. WE HAVE ONE MORE READING DAY BEFORE FIRST DAY NOTICE ON WEDNESDAY JAN 31. THE AMOUNT STANDING FOR FEBRUARY DELIVERY WILL BE A DILLY!!

We had 2 notice(s) filed upon today for 200 oz

PRELIMINARY VOLUME TODAY ESTIMATED; not available

FINAL NUMBERS CONFIRMED FOR YESTERDAY: not available

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY 361 CONTRACTS FROM 200,700 DOWN TO 201,188 DESPITE YESTERDAY’S GOOD SIZED 26 CENT LOSS. WE WERE ALSO INFORMED THAT WE HAD ANOTHER FAIR SIZED 1460 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR FEBRUARY..AS SOMEBODY WAS IN URGENT NEED OF METAL AND NEEDED TO GO TO LONDON TO GET IT AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1460. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE HAD ZERO LONG COMEX SILVER LIQUIDATION AND A SMALL SIZED RISE IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1821 SILVER OPEN INTEREST CONTRACTS:

361 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1460 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 1821 CONTRACTS

We are now in the poor non active delivery month of January and here the OI LOST 1 contract FALLING TO 1. We had 1 notice served upon yesterday, so we GAINED 0 contract or an additional NIL oz will stand for delivery AT THE COMEX

February saw a LOSS OF 12 OI contracts FALLING TO 136. The March contract LOST 1381 contracts DOWN to 132,920.

We had 1 notice(s) filed for NIL 5,000 for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 30/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

47,842.227 oz

SCOTIA

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil OZ

|

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

2 contracts

(200 oz)

|

| Total monthly oz gold served (contracts) so far this month |

698 notices

69800 oz

2,1710 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (698) x 100 oz or 69,800 oz, to which we add the difference between the open interest for the front month of JAN. (2 contracts) minus the number of notices served upon today (2 x 100 oz per contract) equals 69,800 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (696 x 100 oz or ounces + {(2)OI for the front month minus the number of notices served upon today (2 x 100 oz which equals 69,800 oz standing in this active delivery month of JANUARY (2.1710 tonnes). THERE IS 17.629 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY(CME correction from Friday

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 17 MONTHS 67 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,258,843.95 oz

CNT

HSBC

Malca

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

606,295.500 OZ

scotia

|

| No of oz served today (contracts) |

1

CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 730 contracts

(3,650,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into Brinks: 606,295.500

total inventory deposits: 606,295.500 oz

we had 3 withdrawals from the customer account;

i) out of CNT: 623,340.04 oz

ii) Out of HSBC: 600,811.04

iii) Out of Malca: 34,692.870

total withdrawals; 1,258,843.95 oz

we had 0 adjustment

total dealer silver: 45.461 million

total dealer + customer silver: 247.355 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 1 contract(s) FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 730 x 5,000 oz = 3,650,000 oz to which we add the difference between the open interest for the front month of JAN. (1) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 730(notices served so far)x 5000 oz + OI for front month of JANUARY(1) -number of notices served upon today (1)x 5000 oz equals 3,650,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY AS QUEUE JUMPING CONTINUES AS WE PROCEED TO MONTH’S END.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3.790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: n/a

CONFIRMED VOLUME FOR YESTERDAY: n/a CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF n/a CONTRACTS EQUATES TO n/a MILLION OZ OR n/a% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.71% (Jan 29/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.20% to NAV (Jan 29/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.71%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.20%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO 3.46%: NAV 13.98/TRADING 13.50//DISCOUNT 3.46%

END

And now the Gold inventory at the GLD/

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 30/2018/ Inventory rests tonight at 846.67 tonnes

*IN LAST 316 TRADING DAYS: 94.48 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 250 TRADING DAYS: A NET 62.83 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Jan 30/2017:

Inventory 313.896 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.74%

12 Month MM GOFO

+ 2.11%

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

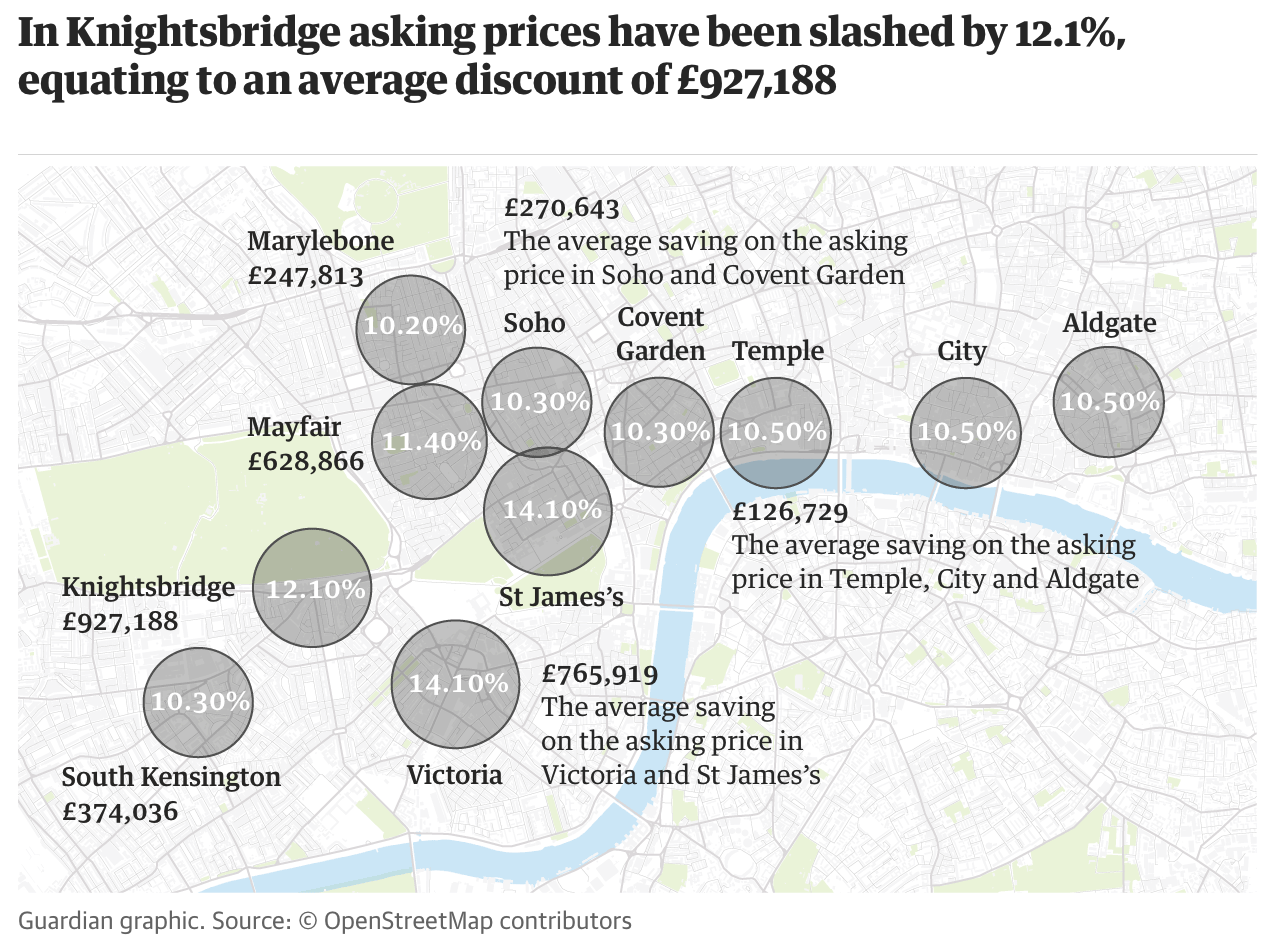

London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

– London property market tumbles as glut of luxury apartments grows to 3,000

– Property crisis in London as over half of 1,900 luxury apartments built 2017 fail to sell

– London’s still high priced property causes companies to locate offices elsewhere

– At current rates, glut of London properties will take three years to sell

– Leading London-based estate agents Foxtons’ sees 42% drop in earnings, yoy

– UK’s largest estate agent issues second profit warning in three months

– Number of homes sold in December fell to 99,100, lowest level since Nov 2016

– The ‘Shard disaster’ – Ten apartments at top of London’s largest skyscraper, all priced over £50m and in five years not a single one has sold

– Property gold? Diversify and own the physical property of real gold

Editor: Mark O’Byrne

There is much talk of bubbles bursting of late. Bitcoin, bonds have been considered in this regard but so far very little consideration of the property bubbles in London, Sydney, Toronto, Vancouver, Hong Long and other major cities.

London’s property market is another market to consider when looking for evidence that the party is over when it comes to frothy, record-high asset prices.

On average, UK properties take around six weeks to sell. London properties have been consistently below average, with many taking less than a day to go from ‘For Sale’ to ‘Under Offer’. However, in recent months, three London regions – West, North-West and South-West – appeared in the slowest 10 postcode areas for property sales.

According to this research by the Homeowners Alliance, West London has taken the very bottom spot after properties spent an average of 107.9 days on the market as of last month.

This is in line with other data that shows property prices in the capital have fallen for the first time since 2009.

Delicate buyers: London becomes price-sensitive

One of the first things someone outside of London says about the city is how expensive it is. They often say it as if those of us who are from there have never noticed.

Arguably, this has been the case for the last eight years or so when it comes to London’s luxury properties. But it seems many buyers are waking up to the sheer madness of paying millions for a tiny shoe box small apartment, that is in the no man’s land of Brexit and majorly exposed to the vulnerable indebted UK economy and a further devaluation of the pound.

The Guardian reports that more than half of the 1,900 ultra-luxury apartments built in London last year failed to shift. There are now an estimated 3,000 unsold luxury properties, such as these, in the capital. These are the apartments that are priced above £1,500 per square-foot.

For the slightly cheaper apartments, priced at between £1,000-£1,500 per sq ft, there are 14,000 unsold properties. The average price per sq ft across the country is £211.

In the West of London (the worst performing area in the UK in terms of days sold) Savills is marketing a two-bedroom duplex penthouse for £7.25m, a ridiculous amount. But, this is not as eye watering when you consider it has already had a discount of 39.6 per cent off its original launch price of £12m.

The FT reports:

“76 per cent of properties have been on the market for more than six months [In St. James’s]” says Tim Macpherson, head of London residential sales at Carter Jonas, and “almost half — 45.7 per cent — have been reduced in price”.

The problem really is very serious in the West of London. The Guardian reports:

The steepest discounts are currently to be found in St James’s and Victoria, where the average prime property price has been reduced by 14.1% (£766,000) and where more than three-quarters of homes have been on the market for more than six months. In Knightsbridge, prices have been reduced by 12.1% on average, followed by Mayfair (11.4%) and Temple and the City (10.5%).

Gluttonous property developers of London

In any other industry a glut of supply would require the manufacturers to take stock of what was going on and likely hold off on producing any more goods until the glut had shifted or a new strategy had been taken. This would be forced to happen in any industry where the environmental and social disruption was so great, thanks to the production process.

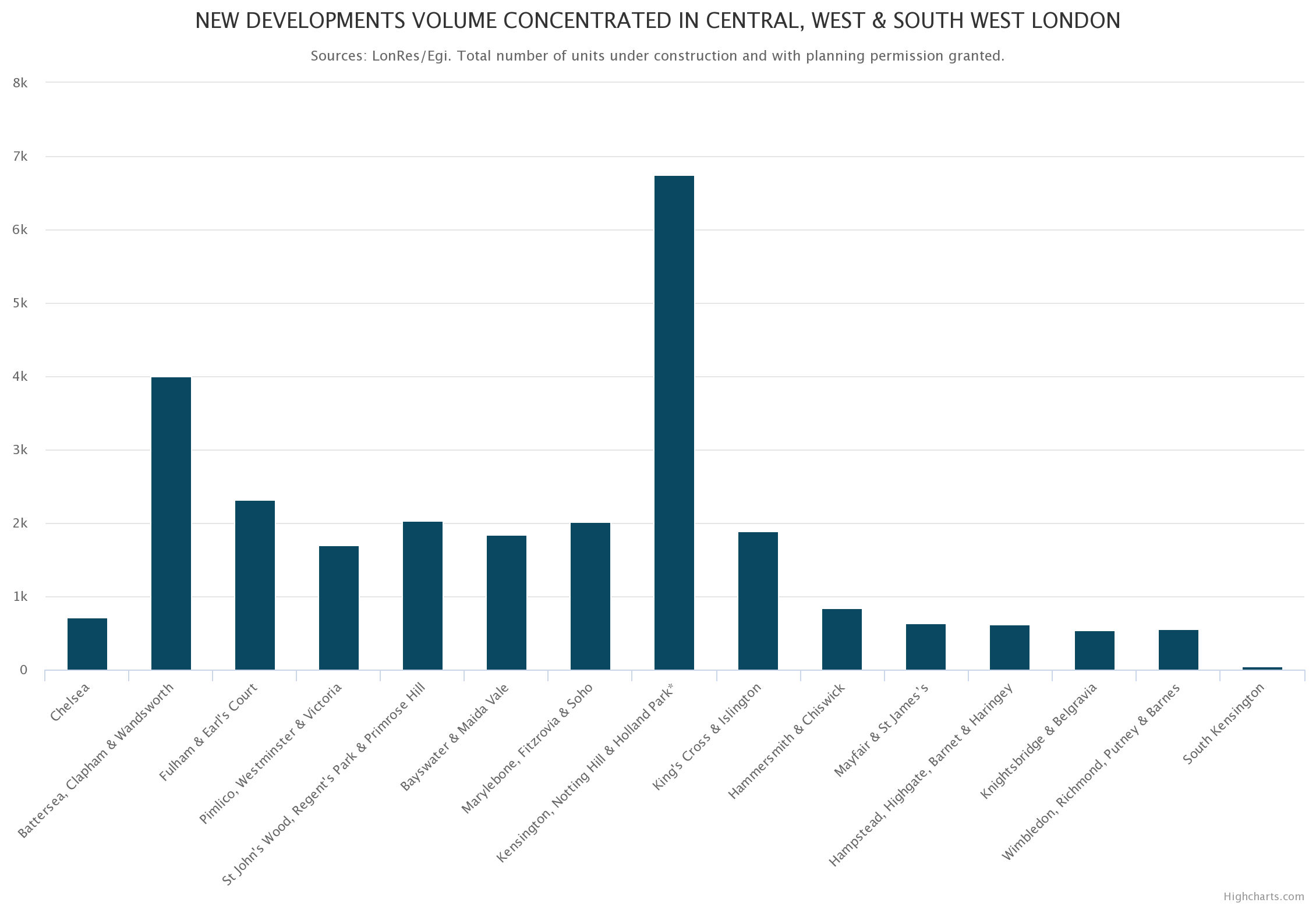

But not in London. No authority has stepped in and demanded building firms halt works. Instead, there are a further 420 residential towers (each at least 20 storeys high) in the pipeline, according to New London Architecture and GL Hearn.

The Coutts London Prime Property Index Q4 2017, warns of the risk of ‘over supply’:

Londoners have grown used to the sight of cranes and construction sites dotted across the capital. More than 26,000 new units are currently under construction or have received permission to start building in post codes covered by the Coutts London Prime Property Index as at December 2017.

New developments are cropping up throughout the 15 areas we cover, but it’s Central and West & South West London that are leading the charge. While this reflects the degree of demand in these sought-after areas, there is a risk of a potential over-supply of luxury new builds leading to an increase in listing times for them and higher discounts than on existing homes.

The government love this. They believe that this promotes confidence in the capital. They are happy with this – especially at a time when financial companies are threatening to pull out jobs and offices in the City, in the face of Brexit. For some reason, building more residential apartments means we don’t need to worry about it. But who is going to buy them?

Not the foreigners we have so long relied on, it seems. Property buying agent Henry Pryor told the Guardian:

“We’re going to have loads of empty and part-built posh ghost towers,” he says. “They were built as gambling chips for rich overseas investors, but they are no longer interested in the London casino and have moved on.”

So the London Casino’s chips are down, the house has folded. But the owners keep building more roulette tables and penthouses, desperate to try and entice the gamblers. Where was the tipping point? Most likely London’s very own phallic-symbol of arrogance, the Shard.

There are ten apartments at the top of the capital’s largest skyscraper. All are priced over £50m each. In five years not a single one has sold.

A ‘Shard-shaped disaster’

The key problem with London’s property market is that the developers and government are keen only to serve the tip of the triangle – the wealthiest Brits and international buyers.

But this is no longer where the demand is. Many of those investors from the likes of China and Russia are keen to shift properties they bought a few years ago. Illusions of making quick profit shattered in the wake of the slowing property market and massive currency devaluation of Brexit.

International investors really don’t care where they buy. London is most likely not their home, or where they plan to spend a significant amount of time. They will find the next property bubble or asset class that will serve their millions far better. Where Brexit isn’t a ‘thing’ and stamp duty cannot touch them.

It is the bottom of the Shard that is struggling. The foundations of London’s society. There are no affordable properties being built for those who have to work in London, or at least want to work in London. Estate agent Savills estimates that 58% of demand in London is for homes priced below £450k, but only 25% of homes being built are at this price.

This does not bode well long-term for the UK’s capital. At a time when the Prime Minister and members of the Royal Family are traveling the world in an effort to show the country is open for business, why would a foreign company move to or expand it’s presence? Brexit aside, if employees are unable to find somewhere affordable to live in the capital, businesses will not be tempted to come to an area where they are unable to attract key talent and core workers.

Salesmen begin to suffer

Foxtons is one of the capital’s largest estate agents. Their offices alone have been an excellent marker for the size of the London bubble.

From personal experience I realised we were in full bubble mode when I organised to see a property in South-East London five years ago. I caught the bus there. The estate agent turned up in a brand new Porsche Cayenne.

Source: Guardian

Since then Foxtons capital offices have been transformed into large glass-fronted show spaces, akin to a Scandinavian concept furniture store. They display no properties in the window. Instead there are low coffee tables and armchairs for you to place yourself in as someone greets you and gets you a drink from the moodily lit fridges in the middle of the space.

Eventually someone called Darren in a shiny suit swaggers around and asks you lots of invasive questions about your finances. In no other industry would someone get away with interviewing you like this.

For a long-time Foxtons have survived on the premise that the customer needs them more than they need the customer. Now the tap has run dry and so have their profits.

Last week announced expectations that its earnings before interest, taxes, depreciation and amortisation for the last twelve months to come in at just £15m, a 42% drop from its £26m earnings in 2016. This followed a year of dire financial statements from the company.

It’s not just London estate agents that are suffering. Countrywide, the UK’s largest estate agents have seen their share price fall by nearly a fifth after the group issued its second profit warning in three months.

Much of the group’s disappointing results were thanks to sales in London and the South-East, but data from elsewhere suggests the London-curse is set to spread across the country.

Country-wide properties and buyers are slumping

The Royal Institution of Chartered Surveyors found that 86% of its members surveyed had not seen any increase in inquiries from first-time buyers in December. The same survey found that the number of new buyer inquiries fell last month by 15%. Agreed sales also dropped across the country, with a balance of 13% reporting a decline in volumes.

Investment house, Goodbody took this information and concluded that we are now in ‘the first stage of a housing downturn’.

Data published by HMRC found that the number of homes changing hands in December fell to 99,100, the lowest level since November 2016.

It is clear that the UK property market is stumbling, it is only stumbling now partly thanks to the strong gusts that are coming from the bursting bubble that is London’s property market as people seek alternatives.

The bitter cold of London’s prices will soon sweep around the country and bitcoin mania will no longer be the dinner-party conversation of choice.

Property gold? London property bubble should be a warning to all speculators

For too long the capital has encouraged speculators that prices will continue to rise for ever. As with bitcoin, the capital’s properties became these extreme financial assets that delivered capital gains far in excess of people’s ability to earn income from work, or from investment in the real economy.

For so many government ministers, questioned about the unaffordable London property market they had a two part response. The first was that it was a positive sign for the whole country. The second was that high prices were thanks to too little supply.

Gold in GBP – 10 years (GoldCore)

Really it has nothing to do with a shortage of supply, it has had everything to do with encouraging speculation.

Speculation has been fuelled by governments encouraging home ownership by UK residents and speculation by foreign investors. All of this was further fuelled by record-low interest rates, zero-rate mortgages, loans from the bank of Mum and Dad, government subsidies and tax breaks. It has all been kindling on an ever-growing fire.

Time to diversify and own the physical property of real gold.

Related reading

London Property Crash Looms As Prices Drop To 2 1/2 Year Low

London House Prices Are Falling – Time to Buckle Up

London Property Bubble Bursting? UK In Unchartered Territory On Brexit and Election Mess

Follow Us On Facebook, Linkedin and Twitter

News and Commentary

Gold drops on firmer dollar, higher bond yields (Reuters.com)

Asia Stocks Follow U.S. Drop as Bond Slump Extends (Bloomberg.com)

Stocks Fall as Treasury Yields Climb to 2014 Highs (Bloomberg.com)

These Are The 6 Traders Who Were Just Arrested For Manipulating The Gold Market (ZeroHedge.com)

U.S. Releases Sweeping List of Russian Oligarchs and Officials (Bloomberg.com)

Latest Updates on Russia Sanctions List (Bloomberg.com)

Source: US Treasury via Bloomberg

Gold Prices At Their Highest Since August 2016 (Gold-Eagle.com)

Gross Domestic Problems (MauldinEconomics.com)

This is why – and how – to combat consistency (StansBerryChurcHouse.com)

Davos Dumbbells (BonnerAndPartners.com)

The Donald’s Davos Delusions (DavidStockMansContraCorner.com)

London’s Bankers Haven’t Been This Gloomy Since 2008 (Bloomberg.com)

Gold Prices (LBMA AM)

30 Jan: USD 1,345.70, GBP 954.37 & EUR 1,083.56 per ounce

29 Jan: USD 1,348.40, GBP 955.07 & EUR 1,085.46 per ounce

26 Jan: USD 1,354.35, GBP 950.21 & EUR 1,087.41 per ounce

25 Jan: USD 1,360.25, GBP 954.35 & EUR 1,095.27 per ounce

24 Jan: USD 1,350.50, GBP 957.50 & EUR 1,093.77 per ounce

23 Jan: USD 1,337.10, GBP 959.10 & EUR 1,091.74 per ounce

Silver Prices (LBMA)

30 Jan: USD 17.30, GBP 12.24 & EUR 13.91 per ounce

29 Jan: USD 17.34, GBP 12.33 & EUR 13.99 per ounce

26 Jan: USD 17.40, GBP 12.21 & EUR 13.99 per ounce

25 Jan: USD 17.52, GBP 12.29 & EUR 14.12 per ounce

24 Jan: USD 17.19, GBP 12.16 & EUR 13.93 per ounce

23 Jan: USD 16.98, GBP 12.19 & EUR 13.87 per ounce

Recent Market Updates

– Silver Bullion: Once and Future Money

– Greatest Stock Bubble In History? GoldNomics Podcast Transcript

– Davos – My Personal Experience of the $100,000 Event, $60 Burgers, Massive Inequality and the Blockchain Revolution

– Is This The Greatest Stock Market Bubble In History? Goldnomics Podcast

– Cyber War Coming In 2018?

– Government Shutdown Ends – Markets Ignore Looming Debt and Bond Market Threat

– Global Pension Ponzi – Carillion Collapse One Of Many To Come

– The Next Great Bull Market in Gold Has Begun – Rickards

– Gold Bullion May Have Room to Run As Chinese New Year Looms

– Digital Gold Flight To Physical Gold Coins and Bars

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– London Property Crash Looms As Prices Drop To 2 1/2 Year Low

END

Our banker friends are doing a great job crushing cryptos again

(courtesy zerohedge)

Cryptos Are Getting Crushed Again

Having bounced back from the Coincheck-hack crash, cryptocurrencies are extending yesterday’s ugliness today and accelerating to the downside…

Bitcoin is back below the Coincheck crash lows…

There are no clear catalysts for this drop.

Deutsche Bank executives have suggested that “governance” that will legitimize crypto investments could exist in “five to ten years.”

Originally speaking in an interview with Bloomberg on Monday, Jan. 29, Mueller cautioned against current investment in cryptocurrency as only for those “who invest speculatively” while appealing for businesses in the sphere to work together with regulators.

“Once security and the corresponding trust have been created, cryptocurrencies can be assessed and evaluated like established asset classes,” he forecast.

“It’s possible that the required governance will be in existence in five to ten years.”

Deutsche Bank has traditionally taken a bearish view on cryptocurrencies as prices rise, cautioning in December that a major fall in Bitcoin was being “discounted as a small issue” by financial markets.

The lack of volatility in traditional stocks was driving investor interest in more risky assets such as Bitcoin, fellow Deutsche Bank analyst Masao Muraki determined in a note mid-January.

“Now, a growing number of institutional investors are watching cryptocurrencies as the frontier of risk-taking to evaluate the sustainability of asset prices,” he wrote.

Germany continues to fall behind in its treatment of cryptocurrencies at consumer level, providing a stark contrast to initiatives in other countries, such as neighboring Switzerland.

Earlier this month, the country’s central bank director nonetheless precluded comments from UK and US lawmakers at the World Economic Forum 2018 that regulation of cryptocurrency should be a joint international effort.

* * *

As a reminder this early-year weakness in crypto is not unusual…

As CoinTelegraph notes, the lead up to Chinese New Year is one of high spending as people book all sorts of travel and holidays, not to mention buy presents. Thus, just like Christmas and December is a time for spending in the West, January has a similar pattern in the east.

With Bitcoin’s value almost halving from $20,000 in the middle of December to $10,000 at its worst in January, Wallin is both unperturbed or surprised.

“The January drop is a recurring theme in cryptocurrencies as people celebrating the Chinese New Year, aka Lunar New Year, exchange their crypto for fiat currency,” explains Alexander Wallin, CEO of trading social network SprinkleBit, as quoted by Bloomberg.

“The timing is about four to six weeks before the lunar year when most people make their travel arrangements and start buying presents,” he added.

The holiday takes place on Feb. 16; however, the build-up is where people start to spend their money. And with the Chinese population heavily vested in Bitcoin, it has a huge role to play on the movement of the market.

The thoughts are that people have been taking their profits into the build-up of the New Year, turning their Bitcoin into fiat currency to use for gift buying.

end

How will the deniers of gold market rigging explain the fines and convictions

(courtesy TFMetals/Craig Hemke)

TF Metals Report: How will the deniers of gold market rigging explain this?

Submitted by cpowell on Mon, 2018-01-29 19:25. Section: Documentation

2:26p ET Monday, January 29, 2018

Dear Friend of GATA and Gold:

The TF Metals Report today wonders what excuses will be made by deniers of monetary metals market manipulation now that three investment banks — Deutsche Bank, UBS, and HSBC — have been fined millions of dollars by the U.S. Commodity Futures Trading Commission for manipulating the futures markets in the monetary metals.

The TF Metals Report’s commentary is headlined “CFTC Fines Banks for Precious Metal Price Manipulation” and it’s posted here:

https://www.tfmetalsreport.com/blog/8799/cftc-fines-banks-precious-metal…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

In case you missed yesterday’s big story: 3 banks and 8 individuals charged in gold/silver spoofing

(courtesy Reuters/GATA)

U.S. authorities charge three banks, eight individuals in futures ‘spoofing’ probe

Submitted by cpowell on Mon, 2018-01-29 21:29. Section: Documentation

By Michelle Price

Reuters

Monday, January 30, 2018

WASHINGTON — The U.S. Justice Department and the country’s derivatives regulator said on Monday they had filed civil and criminal charges against three European banks, which paid $46.6 million to settle the cases, and eight individuals for alleged manipulation in U.S. futures and commodities markets.

UBS, Deutsche Bank, and HSBC and former traders at the banks, as well as individuals at other firms, were charged following a large-scale multi-agency probe including the Commodity Futures Trading Commission (CFTC) into so-called “spoofing” in metals and equities futures.

Deutsche Bank and UBS have agreed to pay $30 million and $15 million respectively to settle the civil charges in the case, while HSBC will pay $1.6 million to settle the charges, the CFTC said.

All three banks received reduced penalties from the CFTC for providing significant assistance in the investigations. UBS self-reported the alleged misconduct by its traders to the regulator, the CFTC said. …

… For the remainder of the report:

https://www.reuters.com/article/us-usa-cftc-arrests/u-s-authorities-char

END

Bill Murphy explains why our precious metals will rise in price

(courtesy Kitco/Bill Murphy/GATA)

To catch up with other assets, metals will explode, Murphy says in Kitco interview

Submitted by cpowell on Tue, 2018-01-30 00:13. Section: Daily Dispatches

7:14p ET Monday, January 29, 2018

Dear Friend of GATA and Gold:

Daniella Cambone of Kitco News interviewed GATA Chairman Bill Murphy this month at the Vancouver Resource Investment Conference, prompting him to say that if gold and silver are to catch up with the prices of other assets and escape the clutches of the gold cartel, they will explode — and he thinks they will this year. Murphy’s interview is three minutes long and can be seen at Kitco News here:

http://www.kitco.com/news/video/show/VRIC-2018/1831/2018-01-26/Gold-And-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.3235 /shanghai bourse CLOSED DOWN AT 34.99 POINTS 0.99% / HANG SANG CLOSED DOWN 359.60 POINTS OR 1.09%

2. Nikkei closed DOWN 337.37 POINTS OR 1.43% /USA: YEN FALLS TO 108.64

3. Europe stocks OPENED RED /USA dollar index FALLS TO 89.08/Euro RISES TO 1.2418

3b Japan 10 year bond yield: RISES TO . +.094/ (TROUBLE THIS MORNING) GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.64/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.92 and Brent: 69.06

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.687%/Italian 10 yr bond yield UP to 2.031`% /SPAIN 10 YR BOND YIELD DOWN TO 1.415%

3j Greek 10 year bond yield RISES TO : 3.667?????????????????

3k Gold at $1343.40 silver at:17.22: 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 34/100 in roubles/dollar) 55.98

3m oil into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.64 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9334 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1592 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.687%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.701% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.950% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets A Sea Of Red As Dollar Selloff Resumes

The global selloff that started on Monday as traders were spooked by the double whammy of surging interest rates and fears about iPhone X demand, and resulting in the biggest drop in US stocks since September, accelerated overnight and as seen below world stocks and US equity futures are a sea of red this morning:

In an odd reversal, yesterday’s dollar bounce lost steam amid position rebalancing before Trump’s State of the Union address and the Fed’s two-day meeting. So far today, it has been a tale of two halves: Light dollar buying throughout the Asia session, reversing once London opened, with EUR and other G10 pairs bouncing off the lows. Bunds have also come down from the highs. USD is now looking heavy, with perhaps more selling to come according to some desks, even as US yields are dipping. Most pairs remain range-bound for the time being, as we head into the magic of month-end tomorrow, for the first time in 2018. Month-end related selling is expected at some point.

The euro advanced alongside the yen, and the pound erased a drop. The yen advanced against all of its Group-of-10 peers as a stock selloff prompts risk aversion. Tokyo-based funds are selling the Aussie against the yen ahead of Trump’s speech Tuesday night, according to a trader who spoke to Bloomberg. “After last week’s large moves, currency markets are wary of this week’s upcoming events but also of the implications for higher yields,” said Mansoor Mohi-uddin, head of currency strategy at NatWest Markets in Singapore. “The focus in G-10 currencies is whether higher yields cause stocks to weaken, thus supporting safe haven currencies.”

Predictably, volatility across FX continues to rise, with EUR/USD driven back above 1.24, while GBP/USD rallies 100 pips to 1.41 after sliding below 1.40. Actually make that vol across all assets classes.

Treasury yield rose above 2.7% before slipping back, while European government bonds edged higher as traders digested growth data from the region. Rate moves were supported as rebalancing inflows widely flagged over last week, keeping the curve relatively unchanged; bunds initially rally after soft Saxony CPI reading, however other German regions reduce probability of large national German CPI miss. US TSYs tracked the dollar for much of the session, although they have since rebounded from session lows even as the BBDXY continues to decline.

Overnight the US bond selloff spread to Japan, where the benchmark 10-year bond yield briefly rose over 2bps above 0.10%, the highest since July 11, with yields up ~1bp across the curve at last check. Any sustained increase in the 10-year yield to 0.1% would test speculation the BOJ will offer to buy unlimited amount of bonds for fixed rates.

Meanwhile in equities, European stocks opened in the red and drifted lower, mirroring a particularly weak Asian equity session and the drop in U.S. index futures. The Stoxx Europe 600 Index drops 0.5%, declining for the fourth time in five days. Miners are among the biggest decliners as copper and gold prices fall, with banks also sliding. Index losses are tempered by a gain for Swatch after its earnings beat estimates, while Siemens Gamesa also advances after saying it’s on the right path to meet 2018 targets.

Asian markets also traded lower across the board as the selling in US equity futures and retreat from record highs gathered pace overnight. Australia’s ASX 200 (-0.9%) and Japan’s Nikkei 225 (-1.4%) were both negative with Australia led lower by weakness across commodity-related sectors, while Japanese participants digested earnings and a slew of data including a contraction in Household Spending, as well as higher Unemployment. Selling accelerated in late trade amid a slump in US equity futures, in which DJIA futures fell over 200 points after a breakdown of near-term support at 26,400. Hang Seng (-1.1%) and Shanghai Comp. (-1.0%) conformed to the losses after continued PBoC inaction which resulted to a daily net drain of CNY 240bln and amid reports that banks were ordered to curb overnight lending, while tech names and Apple suppliers in the region were also mostly downbeat after the tech giant was said to reduce Q1 iPhone X orders by 50% due to slower than expected sales

At the same time, a wariness is emerging in equity markets as surging rates on government bonds test appetite for stocks at elevated valuations. Investors are weighing whether stronger corporate earnings, a pick-up in economic growth and optimism over U.S. tax cuts can continue driving up prices in markets that recently touched their highest on record; as noted yesterday, Goldman Sachs predicted a correction is imminent, but said any such pullback would be a buying opportunity.

“An acceleration in the selloff of global bond markets appears to be starting to let some of the air out of the recent rally in global equity markets,” said Michael Hewson, chief market analyst at CMC Markets UK. “U.S. markets suffered their worst one day fall this year, though sharp falls in tech stocks also contributed.” Apple Inc. shares dropped as much as 2.6 percent amid renewed concerns about falling demand for the iPhone X.

Looking at today’s key event, expect Trump’s State of the Union address to borrow from Trump’s Davos appearance with respect to detailing the America First approach, Credit Agricole strategists including Valentin Marinov write in a note. Markets will be particularly sensitive to any hints of further trade barriers to protect domestic U.S. producers, probably with negative implications for the USD.

A quick look at the ongoing Brexit chaos, cable initially sold off on news that PM May will reject the EU’s proposed deal on the Brexit transition period and go into battle next week over freedom of movement and so-called “rule taking”, the Telegraph reported. Then, the Times said that May is facing a donors’ revolt and growing pressure to leave Downing Street as soon as the outline of a trade deal is negotiated with the European Union this autumn. Finally, BuzzFeed leaked the UK government’s unreleased Brexit analysis which reportedly showed that UK will be worse off in every scenario outside the EU.

Elsewhere, many metals pared Monday’s gain, though gold reversed a decline to trade higher. Bitcoin fluctuated around $11,000 and emerging-market stocks slumped. Both WTI and Brent crude futures traded lower amid the (early) resurgence in the USD with prices hovering around the USD 65bbl and USD 69bbl levels respectively with energy newsflow otherwise relatively light. In metals markets, gold trades lower amid the global risk environment and the yellow metal’s safe-haven status.

Bulletin Headline Summary from RanSquawk

- European bourses are trading mostly lower (Eurostoxx 50 -0.3%), in-fitting with the global risk sentiment

- Choppy trade for the USD as gains prove to be short-lived with EUR/USD and GBP/USD back above 1.2400 and

- 1.4000 respectively

- Looking ahead, highlights include German national CPIs and a slew of central bank speakers

Market Snapshot

- S&P 500 futures down 0.3% to 2,844.50

- STOXX Europe 600 down 0.3% to 398.53

- MSCI Asia Pacific down 1.1% to 184.84

- MSCI Asia Pacific ex Japan down 1.3% to 605.78

- Nikkei down 1.4% to 23,291.97

- Topix down 1.2% to 1,858.13

- Hang Seng Index down 1.1% to 32,607.29

- Shanghai Composite down 1% to 3,488.01

- Sensex down 0.7% to 36,027.57

- Australia S&P/ASX 200 down 0.9% to 6,022.80

- Kospi down 1.2% to 2,567.74

- German 10Y yield fell 1.9 bps to 0.675%

- Euro down 0.02% to $1.2381

- Italian 10Y yield rose 2.0 bps to 1.758%

- Spanish 10Y yield fell 1.8 bps to 1.401%

- Brent futures down 0.4% to $69.21/bbl

- Gold spot up 0.3% to $1,343.98

- U.S. Dollar Index down 0.1% to 89.20

Top Headline News

- The U.S. identified 96 of Russia’s richest people as “oligarchs” and 104 top government figures in lists mandated under last year’s sanctions law, adding pressure over alleged Kremlin interference in the 2016 presidential vote

- Struggling to find an approach to Brexit that can win the support of her divided cabinet, U.K. PM Theresa May is asking European officials and leaders to come up with ideas on what kind of future relationship might be on offer, according to three people familiar with the situation

- The euro-area economy expanded 0.6% q/q in 4Q, matching the median economist forecast while economic confidence for the region fell to 114.7 from 115.3 in December

- Mnuchin says U.S. debt limit suspension can be extended into February

- Dubai’s Biggest Lender in Talks With Sberbank on Turkey Unit

- Wynn Scrutiny Intensifies as Macau Regulators Voice Concerns

- HNA Crisis Deepens as Group Is Said to Face Liquidity Crunch

- Varian to Buy Sirtex for $1.3 Billion to Add Cancer Drugs

- Trump Agenda Faces Tough Fiscal Reality After State of the Union

- Blackstone in Talks Buy TRI Unit Stake For $17b: Reuters

- Japan December retail sales 0.9% vs -0.4% est; y/y 3.6% vs 2.2% est

- New Zealand December trade balance NZ$640m vs -NZ$125m estimate

Asian markets traded lower across the board as the selling in US equity futures and retreat from record highs gathered pace overnight. ASX 200 (-0.9%) and Nikkei 225 (-1.4%) were both negative with Australia led lower by weakness across commodity-related sectors, while Japanese participants digested earnings and a slew of data including a contraction in Household Spending, as well as higher Unemployment. Furthermore, selling then accelerated in late trade amid a slump in US equity futures, in which DJIA futures fell over 200 points after a breakdown of near-term support at 26,400. Hang Seng (-1.1%) and Shanghai Comp. (-1.0%) conformed to the losses after continued PBoC inaction which resulted to a daily net drain of CNY 240bln and amid reports that banks were ordered to curb overnight lending, while tech names and Apple suppliers in the region were also mostly downbeat after the tech giant was said to reduce Q1 iPhone X orders by 50% due to slower than expected sales. Finally, 10yr JGBs were lower as Japanese yields played catch up to their US counterparts in which the US 10yr yield rose above 2.7% to its highest since April 2014, while firmer demand for the 2yr JGB auction.

Top Asian News

- China Stocks in Hong Kong Sink to Pare World’s Steepest Rally

- PetroChina Says Profit May Triple Amid Cost Cuts, Higher Oil

- Top Noble Group Shareholder Urges SGX Probe of Trader’s Actions

- Apps to Screen Tenants Latest Chinese Startups Battleground

- Asian Suppliers Fall on Report Apple Cut IPhone X Targets

European bourses are trading broadly lower (Eurostoxx 50 -0.3%), in-fitting with the global risk sentiment spurred from equity performance seen in US and Asia-Pac hours. The only index immune to losses this morning is the SMI (+0.3%) with the Swiss bourse supported by the luxury sector after a positive update from Swatch (+2.7%) and the latest Swiss watch exports which have also lifted Richemont (+1.8%) higher in sympathy. Elsewhere, IT names trade higher after chip makers such as Infineon (+0.8%) and STMicroelectronics (+0.5%) are granted some reprieve in the wake of yesterday’s news that Apple could curtail some of their production of the iPhone X. Additionally, material names lag their peers amid the price action seen in the metals complex. Finally, Telecom Italia (+2.8%) top the FSTE MIB after news that the Co. are to unveil their network spin-off proposal on February 7th.

Top European News

- U.K. Mortgage Approvals at 3-Year Low as Housing Market Slows

- Russian Traders Unfazed by U.S. Oligarch List as Bonds Rally

- Top Norway Fund Manager Is Betting on Rigs for 200% Return

In currencies, the USD initially managed to maintain its recovery momentum after recovering above 89.500 on widespread gains vs its G10 rivals (Ex-JPY and CHF), before sentiment reversed and the USD was dragged into negative territory.

- EUR/USD briefly retested overnight lows around 1.2337 on a weak inflation read from German state Saxony, but very mixed data from others ahead of heavyweight NRW, broad USD softness and progress in German coalition negotiations prompted a marked rebound towards 1.2400.

- GBP/USD initially lost the 1.4000 handle with stops triggered on a break to 1.3980, but has recovered to trade around 1.4080 in choppy price action.

- AUD/USD mid-range between 0.8040-0.8100 and undermined by ongoing weakness in metals/commodities, while

- NZD/USD has retreated further towards 0.7300 despite decent NZ trade data as CFTC shorts continue to pare positions.

- USD/CAD nudging higher again between 1.2330-1.2380 as some positive NAFTA discussions are offset by another downturn in oil prices.

Ahead, US President Trump’s State of the Union address kicks off a busy line up of risk events, with the FOMC concluding its 2-day meeting on the last trading day of January and NFP looming on Friday.

In commodities, both WTI and Brent crude futures traded lower amid the (early) resurgence in the USD with prices hovering around the USD 65bbl and USD 69bbl levels respectively with energy newsflow otherwise relatively light. In metals markets, gold trades lower amid the global risk environment and the yellow metal’s safe-haven status. Elsewhere, copper was pressured during Asia-Pac and fell below USD 3.20/lb amid broad declines across the complex and with sentiment spooked as the equity sell-off gathered pace. Additionally, zinc prices have shown losses in London after printing 11 year highs yesterday.

Looking at the day ahead, the highlight is President Trump’s first State of the Union address in front of Congress. Also due to speak is the BoE’s Carney before the UK Parliament’s Economic Affairs Committee. Datawise, in Europe the highlights include a first look at Q4 GDP for the Euro area and France, the flash January CPI report in Germany, UK credit and money aggregates data for December and January confidence indicators for the Euro area. In the US the highlight is the January consumer confidence print, while the November S&P/ Case-Shiller house price index is also due to be released. Away from this, the ECB’s Mersch speaks in Frankfurt and Catalonia’s parliament votes on its regional

president. Pfizer and McDonald’s will release earnings.

US Event Calendar

- 9am: S&P CoreLogic CS 20-City NSA Index, prior 203.8; MoM SA, est. 0.6%, prior 0.7%; YoY NSA, est. 6.3%, prior 6.38%

- 10am: Conf. Board Consumer Confidence, est. 123, prior 122.1;Present Situation, prior 156.6;Expectations, prior 99.1

DB’s Jim Reid concludes the overnight wrap

Bonds continue to be caught in the cross hairs at the moment although a story at the end of the European session on the ECB likely tapering between September and December rather than abruptly ending the program stemmed a little bit of the sell-off yesterday. The global rise in yields did start to cause some damage though with the S&P 500 (-0.67%) seeing its worst day since September and the VIX climbing 24.9% to 13.84 – the highest close since August. More on equities below but the bond sell-off started after we went to print yesterday morning and finished with 10yr USTs +3.5bp and 10yr Bunds +6.5bps. 5yr equivalents sold off 2bps and 3.3bps respectively. The four bonds mentioned above are up +8bps, +12.4bps, +7.9bps and +12.8bps respectively since the intraday lows after the ECB meeting on Thursday afternoon. So a pretty substantial sell-off in these low yield times.

In terms of landmarks, US 10yr hit the highest level since April 2014 (close 2.695% – day’s highs 2.725%) and 10yr Bunds the highest since September 2015 (close 0.691% – day’s highs 0.6995%). 5 year Bunds spent most of the day trading above 0% but closed at -0.006%. We haven’t closed above zero since November 2015.

There was nothing particularly igniting the sell-off. However there’s no doubt that global yields remain too low given strong growth, the likely pick up in US inflation, much less QE going forward, significantly higher upcoming US treasury supply, higher oil and a weaker dollar. Yesterday gives us confidence that the reasoning behind our credit view for 2018 has some basis. To recap we think Q1 will be good for credit but that higher yields and inflation through the year will eventually lead to volatility picking up and spreads reversing. It’s too early for too much damage to be done in credit (especially with CSPP technicals still strong – see below) but recent moves have given us a hint of a slightly higher vol regime if rates continue to climb as we expect.

Despite the notable rise in 10y treasury yields, our US economists believe there is considerable scope for bond yields to rise before they weigh on growth and equities. They note the economy neutral 10-year yield (10yr-star) in nominal terms is currently c3.5% – suggesting that bond yields could rise about 80bp from current levels before we would begin to worry about them materially slowing growth momentum. For more details, refer to their note.

Staying with rates, the Bloomberg story that the ECB will likely taper QE between September and YE 2018 was attributed to officials familiar with the discussions. The main implication is that it probably rules out a rate increase before June 2019 as the perception is that there will be a six month gap between the end of QE and the first rate hike. Staying with the ECB, the latest CSPP/PSPP ratio has exceeded last week’s record and is again way above the long-run average. The net CSPP purchases were €2.3bn last week with net PSPP purchases at €5.8bn. The CSPP/ PSPP ratio was a huge 39.5% (27.2% over last 4 weeks vs. 11.5% before QE was trimmed in April 2017). There may have been another lumpy PSPP redemption just like in the previous week, which could have pushed the ratio up meaningfully. However, with every weekly print, a signal is emerging from the noise that gives us confidence that the role of corporate bonds in QE has indeed risen as we forecast – at least around the 20% mark that we expect on average in H1.

This morning in Asia, equities have followed the negative lead from the US and are down c1%. The Nikkei (-1.46%), Kospi (-1.08%), Hang Seng (-1.05%) and China’s CSI 300 (-0.53%) are all down, while UST 10y yields are up c2bp as we type. Elsewhere, Exxon Mobil is reportedly planning a $50bn capex over the next five years in the US, according to a tweet from Texas Senator Kevin Brady – whose district is home to Exxon’s corporate campus.

Now recapping other markets performance from yesterday. US equities retreated c0.6% from their record highs (S&P & Dow -0.67%; Nasdaq -0.52%). All sectors within the S&P were in the red with losses led by utilities, energy and telco stocks. Apple fell 2.1% after the Nikkei reported that Apple told suppliers it will halve 1Q production targets for the iPhone X. European markets were broadly lower, with the Stoxx 600 (-0.19%) and Dax (-0.12%) modestly lower while the FTSE rose marginally (+0.08%), partly benefiting from a lower Sterling.

Turning to currencies, the US dollar index gained 0.27%, while the Euro and Sterling fell 0.39% and 0.62% respectively, although the latter is still up c4.2% since early January. In commodities, WTI oil retreated -0.88% from its c3 year high. Elsewhere, precious metals weakened c1% (Gold -0.61%; Silver -1.30%) and other base metals were mixed but Zinc edged 0.5% higher to a fresh 10 year high (Copper -0.13%; Zinc +0.50%; Aluminium -0.71%).

Away from the markets and ahead of tomorrow’s official forecasts, unnamed sources told Reuters that the German government has lifted its 2018 GDP growth forecast to 2.4% from 1.9%, while the unemployment rate is expected to fall 0.4ppt yoy to 5.3% in 2018. Elsewhere, ITV reported that Ms Merkel said her behind the scenes Brexit talks with UK’s PM May were going round in circles, with an endless cycle of “what do you want?” (from Ms Merkel) and “make me an offer” (from PM May).

Following on with some more Brexit headlines. On the EU side, Chief negotiator Barnier noted “we very much need the UK to clarify its position” and “we have to make sure we do have time (to complete the Brexit deal)….we’re working towards the end of October”. Conversely, the UK’s Brexit Secretary Davis pushed back on the deadline, noting “…it can be done in the time – (but) the end of this year” and subject to clarity on a future trade deal. Elsewhere, he added “… we think it would be cherry picking the other way around (by the EU) to leave financial services out” and given it’s so big, we’ll have to treat it separately, with a key argument around financial services being regulatory equivalence. Finally, Bloomberg noted the opposition leader Mr Corbyn has told a private group of business executives that his party’s policy on Brexit is wide open, but a second referendum is out of the question.

Over in Canada, the sixth round of NAFTA talks seemed to have ended with a slightly positive tone. The US trade representative Lighthizer noted “…we finally began to discuss core issues…but we’re progressing very slowly”, my hope is that we “start seeing some breakthroughs between now and the next round” of talks scheduled in late February. Elsewhere, the Canadian and Mexican counterparts noted “some progress” and “on the right track to reach a deal” respectively post the talks.

Finally as a reminder, President Trump’s State of Union speech is out just before we go to print in the morning (late evening US time tonight). DB’s Ruskin noted that it’s not normally a market mover but that if there is a potential market sensitive topic its US trade relations with China.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the December PCE core was in line at 0.2% mom and 1.5% yoy. Notably the three and six month annualised rate was firmer at 1.9% yoy and 1.7% yoy respectively. The January Dallas Fed manufacturing activity index was above market at 33.4 (vs. 25.4) and the highest in 12 years. Elsewhere, the December personal income was above expectations at 0.4% mom (vs. 0.3%) while personal spending was in line at 0.4% mom, but the prior month’s reading was upwardly revised by 0.2ppt. In Europe, Germany’s December import price index was in line at 1.1% yoy, while Italy’s December PPI was lower than the prior month’s print at 2.2% yoy (vs. 2.8%).

Looking at the day ahead, the highlight is President Trump’s first State of the Union address in front of Congress. Also due to speak is the BoE’s Carney before the UK Parliament’s Economic Affairs Committee. Datawise, in Europe the highlights include a first look at Q4 GDP for the Euro area and France, the flash January CPI report in Germany, UK credit and money aggregates data for December and January confidence indicators for the Euro area. In the US the highlight is the January consumer confidence print, while the November S&P/ Case-Shiller house price index is also due to be released. Away from this, the ECB’s Mersch speaks in Frankfurt and Catalonia’s parliament votes on its regional

president. Pfizer and McDonald’s will release earnings.

3. ASIAN AFFAIRS