GOLD: $1336.90 UP $3.10

Silver: $17.27 UP 17 cents

Closing access prices:

Gold $1344.20

silver: $17.34

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1347.22 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1339.70

PREMIUM FIRST FIX: $8.52

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1353.55

NY GOLD PRICE AT THE EXACT SAME TIME: $1342.85

Premium of Shanghai 2nd fix/NY:$10.70

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1343.35

NY PRICING AT THE EXACT SAME TIME: $1343.10

LONDON SECOND GOLD FIX 10 AM: $1345.35

NY PRICING AT THE EXACT SAME TIME. $1344.40???

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 452 NOTICE(S) FOR 45200 OZ.

TOTAL NOTICES SO FAR: 452 FOR 45200 OZ (1.4059 TONNES),

For silver:

jANUARY

116 NOTICE(S) FILED TODAY FOR

580,000 OZ/

Total number of notices filed so far this month: 116 for 580,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,203/OFFER $10,080 UP $176 (morning)

Bitcoin: BID/ $9984/ $10,200 offer down 51 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY CONSIDERABLE 2830 contracts from 201,188 FALLING TO 198,358 DESPITE YESTERDAY’S TINY 6 CENT FALL IN SILVER PRICING. WE HAD CONSIDERABLE COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 2467 EFP’S FOR MARCH AND AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2467 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 2467 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

2467 CONTRACTS (FOR 1 TRADING DAYS TOTAL 2467 CONTRACTS OR 12.335 MILLION OZ: AVERAGE PER DAY: 2467 CONTRACTS OR 12.335 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 12.335 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.17% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 248.205 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236,879 MILLION OZ

RESULT: A CONSIDERABLE SIZED LOSS IN OI COMEX DESPITE THE 6 CENT FALL IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 2467 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2467 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY LOST 363 OI CONTRACTS i.e. 2467 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 2830 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 6 CENTS AND A CLOSING PRICE OF $17.10 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.9915 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 116 NOTICE(S) FOR 580,000 OZ OF SILVER

In gold, the open interest ROSE BY A LARGE 2891 CONTRACTS UP TO 559,332 DESPITE THE GOOD SIZED FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($4.85). IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED A GOOD SIZED 14,404 CONTRACTS OF WHICH FEBRUARY SAW 14,404 CONTRACTS ISSUED AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS. The new OI for the gold complex rests at 561,437. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DUE TO THE DELAY IN THE RELEASE OF YESTERDAY’S DATA YOU CAN BET THE FARM THAT THEY HAVE DELAYED THE RELEASE OF MANY EFPS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY WE HAVE A GAIN OF 17,295 CONTRACTS: 2891 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 14,404 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 11909 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 14,404 CONTRACTS OR 1,440,400 OZ OR 44.803 TONNES (1 TRADING DAYS AND THUS AVERAGING: 14,404 EFP CONTRACTS PER TRADING DAY OR 1,440,400 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 1 TRADING DAYS: IN TONNES: 44.8 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 44.8/2200 TONNES = 2.03% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 697.02 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX WITH THE LARGE SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($4.85). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS ARE WAITING TO RECEIVE A PRIVATE EFP CONTRACT FOR EITHER FEBRUARY OR APRIL AND THESE GUYS ARE STILL NEGOTIATING THEIR DEAL. WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,404 AS THESE HAVE ALREADY BEEN NEGOTIATED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,404 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 17,295 contracts ON THE TWO EXCHANGES:

14,404 CONTRACTS MOVE TO LONDON AND 2891 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 53.79 TONNES).

we had: 452 notice(s) filed upon for 452,200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

With gold UP $3.10, the crooks orchestrated another big change in gold inventory at the GLD/a withdrawal of 5.32 tonnes of gold/

Inventory rests tonight: 841.35 tonnes.

SLV/

A NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY RESTS AT 313.896 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A CONSIDERABLE 2830 contracts from 201,188 DOWN TO 198,358 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE SMALL SIZED LOSS IN PRICE OF SILVER (6 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 2467 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD MINIMAL COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 2830 CONTRACTS TO THE 2467 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A LOSS OF 363 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET LOSS TODAY IN OZ ON THE TWO EXCHANGES: 1.815 MILLION OZ!!!

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE SMALL SIZED LOSS OF 6 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER GOOD 2467 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 7.17 points or 0.21% /Hang Sang CLOSED UP 193.68 pts or 0.86% / The Nikkei closed DOWN 193.68 POINTS OR 0.83%/Australia’s all ordinaires CLOSED UP 0.18%/Chinese yuan (ONSHORE) closed UP at 6.28897/Oil DOWN to 64.09 dollars per barrel for WTI and 68.03 for Brent. Stocks in Europe OPENED IN THE GREEN . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.2887. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.2887//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE MUCH STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS HAPPY TODAY.(STRONGER CURRENCY BUT STILL WEAK MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

The Bank of Japan intervenes by boosting bond buying to halt the rise in Japanese bond yields as it hit 0.10%

( zerohedge)

3 c CHINA

We have been reporting to you on the financial difficulty of NHA, Today it was revealed that they have a shortfall of almost 15 billion yuan that is owed by June. It seems that they are on the verge of bankruptcy and that will probably start the house of cards collapsing.

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

i)An excellent commentary from Tom Luongo as he outlines the problems facing the EU now. Bond yields are rising because of perceived lack of confidence in Europe’s economy. Investors are cashing out of European bonds which causes the the Euro to rise. The higher Euro value will completely destroy the economies of the southern periphery.

a great commentary

(COURTESY TOM LUONGO)

ii)GERMANY

Germany stops taking migrants from Italy and Greece

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

The algos got totally confused with morning. Oil rose this morning despite API’s surprise crude build but when the DOE reported a massive crude build, oil prices began to drop. However gasoline rose as inventories drew down.

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The use of digital gold from the Perth Mint may threaten the 122 billion in gold ETF’s

( Tony Boyd/Australian Financial Review/GATA)

ii)Mnuchin states that his dollar policy is not aimed at jawboning it lower. He still affirms his strong dollar policy. The question is what does a strong dollar policy mean especially with respect to gold/silver

( Bloomberg/GATA)

iii)South Korea now states that it has no intention to ban Bitcoin or other cryptocurrencies

( zerohedge)

10. USA stories which will influence the price of gold/silver

we have brought this to your attention on many occasions: once the 10 yr bond yield rises above 2.70%, the stock market will tank. Yields rose above 2.70% this morning to 2.74% and that spooked stocks again

( zerohedge

( ADP/zerohedge)

iii)Yellen’s final FOMC: the hawkish fed sees “solid” inflation spending and investment signals

so gold falls on inflation expectations???..

( zerohedge)

iv) reaction to the Fed

(courtesy zerohedge)

v)To which Greenspan warns that we have a stock market bubble

vi)THEN 20 MINUTES LATER, THE YIELD CURVE STARTED TO CRASH WITH THE 10 YR YIELD FALLING FORM 2.75% DOWN TO 2.71%/ WITH THE TWO YR/OVER 30 YR COLLAPSING TO ONLY 79 BASIS POINTS DIFFERENCE…SIGNIFIES RECESSION APPROACHING

iii))SWAMP STORIES

a)Trump tells Republicans that he will release the 4 page memo ” 100 percent”( zerohedge)

b)The Dept. of Justice has now given documents pertaining to Jeff Sessions’ near resignation

( zerohedge)

d)Now the Wall Street Journal has given an editorial demanding the release of the 4 page FISA memo( zero hedge)

e)Reuters is reporting (and not yet collaborated) that the FISA warrant could lead to the firing of both Mueller and Rosenstein or just Rosenstein

( zerohedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY ROSE BY A CONSIDERABLE 2891 CONTRACTS UP to an OI level 559,332 DESPITE THE GOOD SIZED DROP IN THE PRICE OF GOLD ($4.85 FALL WITH RESPECT TO YESTERDAY’S TRADING). WE HAD ZERO COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A GOOD SIZED 14,404 EFP’S ISSUED FOR FEBRUARY AND 0 EFP’s FOR APRIL: TOTAL 14,404 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 17,295 OI CONTRACTS IN THAT 14,404 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 2891 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES: 17295 contracts OR 1,729,500 OZ OR 53.794 TONNES,

Result: A STRONG INCREASE IN COMEX OPEN INTEREST DESPITE THE FAIR SIZED LOSS IN YESTERDAY’S GOLD TRADING ($4.85.) WE HAD ZERO COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 17,295 OI CONTRACTS..

We have now entered the active contract month of FEBRUARY where we lost 25,822 contracts and thus 6455 contracts are standing and by definition the amount of gold initially standing in this active contract month of February is as follows:

6455 CONTRACTS x 100 oz per contract = 645500 oz or 20.07 tonnes. Many transferred over to London February EFP’s and will try and obtain metal through London forwards.

March saw a loss of 148 contracts DOWN to 2049. April saw a GAIN of 25,240 contracts UP to 403,213.

We had 452 notice(s) filed upon today for 452200 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 305,005

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 479,889

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE 2830 CONTRACTS FROM 201,188 DOWN TO 198,358 DESPITE YESTERDAY’S SMALL SIZED 6 CENT LOSS. WE WERE ALSO INFORMED THAT WE HAD ANOTHER FAIR SIZED 2467 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR FEBRUARY TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2467. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE HAD CONSIDERABLE LONG COMEX SILVER LIQUIDATION AND A SMALL SIZED LOSS IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE LOST 363 SILVER OPEN INTEREST CONTRACTS:

2830 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 2467 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS TWO EXCHANGES: 363 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month lost only 2 contracts to stand at 134 contracts. Therefore by definition the amount of silver standing in this non active month of February is as follows:

134 contracts x 5000 oz per contract = 670,000 oz

which is not bad for a relatively poor delivery month.

The March contract LOST 4151 contracts DOWN to 128,809.

We had 116 notice(s) filed for NIL 580,000 for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Jan 31/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

14,518.608

oz Scotia

|

| No of oz served (contracts) today |

452 notice(s)

45200 OZ

|

| No of oz to be served (notices) |

6003 contracts

(600,300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

452 notices

45200 oz

1.4059 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 326 notices were issued from their client or customer account. The total of all issuance by all participants equates to 452 contract(s) of which 182 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (452) x 100 oz or 45200 oz, to which we add the difference between the open interest for the front month of FEB. (6455 contracts) minus the number of notices served upon today (452 x 100 oz per contract) equals 645,500 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (452 x 100 oz or ounces + {(6455)OI for the front month minus the number of notices served upon today (452 x 100 oz which equals 645,500 oz standing in this active delivery month of February (20.07 tonnes). THERE IS 15.198 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR. THIS MAY TURN OUT TO BE VERY PROBLEMATIC FOR OUR BANKERS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 67 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

384,530.572 oz

HSBC

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

5925.000 OZ

???

DELAWARE

|

| No of oz served today (contracts) |

116

CONTRACT(S)

(580,000 OZ)

|

| No of oz to be served (notices) |

18 contracts

(90,000 oz)

|

| Total monthly oz silver served (contracts) | 116 contracts

(580,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into Delaware: 5925.000 oz???

total inventory deposits: 5925.000 oz

we had 1 withdrawals from the customer account;

i) Out of HSBC: 384,530.572 oz

total withdrawals; 384,530.572 oz

we had 1 adjustment

i) Out of CNT: 420,015.734 oz was adjusted out of the dealer and this landed into the customer account of CNT

total dealer silver: 45.041 million

total dealer + customer silver: 246.976 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 116 contract(s) FOR 580,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 116 x 5,000 oz = 580,000 oz to which we add the difference between the open interest for the front month of FEB. (134) and the number of notices served upon today (116 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 116(notices served so far)x 5000 oz + OI for front month of FEBRUARY(134) -number of notices served upon today (116)x 5000 oz equals 670,000 oz of silver standing for the FEBRUARY contract month.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 92,361

CONFIRMED VOLUME FOR YESTERDAY: 88,179 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 88,179 CONTRACTS EQUATES TO 440 MILLION OZ OR 70% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.33% (Jan 30/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.46% to NAV (Jan 30/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.71%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.20%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO 4.04%: NAV 13.96/TRADING 13.38//DISCOUNT 4.04%

END

And now the Gold inventory at the GLD/

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 31/2018/ Inventory rests tonight at 841.35 tonnes

*IN LAST 316 TRADING DAYS: 99.80 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 250 TRADING DAYS: A NET 57.51 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Jan 31no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Jan 31/2017:

Inventory 313.896 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.71%

12 Month MM GOFO

+ 2.11%

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

ATMs Hit By Malware “Jackpotting” Attacks That Dispense All Cash In Minutes

– ATMs in US hit by “jackpotting” attacks that empty ATMs in minutes

– FBI warns of attacks in US after similar crimes in Taiwan, Thailand and Europe

– Hackers have stolen c.$1 million from ATMs across the US warns U.S. Secret Service

– Target Diebold Nixdorf machines – #1 global ATM provider, 35% of ATMs worldwide

– Digital deposits increasingly vulnerable – Time to save in physical gold

Editor: Mark O’Byrne

Source: TechViral.net

Source: TechViral.net

$1 million has been stolen from ATMs across the United States by hackers in a new hacking approach known as ‘jackpotting’. Using malware and an endoscope hackers are able to force cash machines to spew out their entire holding of cash.

Once the machine has been emptied the malware, known as Plotus. D, has handed over complete control to the hackers and displays an ‘Out of Service’ message.

This week a memo was leaked from the US Secret Service regarding this discovery. It stated that it was only a matter of time that the US became a target for this type of hacking, given it has already been seen in both Europe and Asia.

According to Russian cybersecurity firm Group IB, dozens of remote attacks were reported in 2016 within Europe.

Plotus.D is not a new discovery for security services, background reading suggests that they have been aware of it for a while now. An alert issued by the US Secret Service, states:

“In previous Ploutus.D attacks, the ATM continuously dispensed at a rate of 40 bills every 23 seconds…Once the dispense cycle starts, the only way to stop it is to press cancel on the keypad. Otherwise, the machine is completely emptied of cash.”

In fact, it was first seen in Mexico in 2013, as described by security firm FireEye in 2017. They concluded that it was “one of the most advanced ATM malware families we’ve seen in the last few years…

“Once deployed to an ATM, Ploutus-D makes it possible for a money mule to obtain thousands of dollars in minutes,” They believe the malware can be modified to use against 40 different ATM vendors in 80 countries.

No longer need to ‘blow the bl**dy doors off’

As Wired magazine pointed out last year, it used to be that robbers needed to either blow up or physically steal an entire ATM in order to steal its contents. Now there are two, far more subtle routes. A simple physical hack or one which goes through the bank’s own software system.

Due to the nature of cybersecurity threats these days, it is getting harder for hackers to access a bank’s back-end network as it requires a far more sophisticated network intrusion skills. Conversely, hacking physically through the front of a machine does not trigger any alarms and can be done relatively cheaply and easily.

Even more convenient for the hackers, physical attacks on machines means the banks or ATM issuers cannot do a remote fix across all machines, each one has to be repaired individually. Giving the hackers more time to access as many ATMs as they can.

How can this be managed? Wired magazine believe this may be an unsolvable problem:

Physical attacks on ATMs are, in some sense, an unsolvable problem. Computer security experts have long warned that no computer should be considered secure if an attacker takes physical control of it. But weak encryption and a lack of authentication between components leaves ATMs particularly vulnerable to physical attacks—access to any part of the insecure machine Kaspersky describes means access to its most sensitive core. And for computers that are left standing unprotected on a dark street in the middle of the night, stuffed full of money, a little more thought to digital security might be a worthwhile investment.

ATMs are not alone

As we discussed last week, anything is hackable today. Very little with an internet connection is safe from the malicious intent of hackers.

Sadly we’re exposed on all sides to hacking. From the security of our cash machines to the heating in our homes right down to our iphones and the many sensitive apps and data on them.

Hackers are no longer just individuals who have progressed from gaming in their mothers’ basements to hacking for jokes. Nowadays many of the hacks that we see are backed by international crime syndicates who themselves are supported by foreign governments.

Whilst companies are distracted with laying down the best security money can buy, individuals are left somewhat in the dark wondering how best to protect themselves. The idea of ATM attacks is particularly concerning when one realises the ultimate impact on consumer and citizens.

ATM attacks are another excuse to go cashless

Ultimately we will end up paying, either for the privilege of withdrawing our own money or (worse) being forced to go to a bank (of which there are fewer physical branches).

The attack on ATMs will likely be used as an excuse to further outlaw cash in the ongoing war on cash, by both governments and banks.

We have written previously of both governments’ and banks’ missions to prevent us from using cash. Very often reasons for banning large bills or preventing the carrying of certain amounts across borders has been justified under money laundering prevention, terrorism and even for the efficiencies and profitability for banks.

In truth, we know that cash is disliked by less liberal governments. They can’t track it and it’s certainly of no use to them when bail-ins and negative interest rates are on the table. What is the incentive, therefore, for ATM hacking to be resolved?

As we wrote in a previous piece on the cashless society:

Going cashless will not rid us of people and organisations who wish to commit horrific and illegal acts. Instead it will encourage them to find additional ways to run their gangs and terrorist cells. For the rest of us it will remind us of the importance of liberty, safe-havens, security and the need to protect our wealth from negative interest rates, bail-ins and currency devaluations.

We can protect our wealth from hackers, cyber fraud and cyber war by investing in physical gold and silver. When allocated and segregated they cannot be hacked by cyber criminals or terrorists, they cannot be confiscated by bankrupt and desperate governments or banks.

Deposits today are no longer the safe conservative savings option they once were. This further underlines the importance of owning physical gold and indeed saving in physical gold as many of our clients have been doing since 2010.

Related reading

The Alternative Fact of the Cashless Society

Cashless Society – Risks Posed By The War On Cash

News and Commentary

Gold inches up as dollar eases ahead of Fed decision (Reuters.com)

Global stocks tumble anew amid bond yield pressure (Reuters.com)

Gold gives up early gains to end lower as dollar pares decline (MarketWatch.com)

Perth Mint Gold and Silver Bullion Sales Slow in 2017 (CoinNews.net)

London is officially a buyers’ market (CityAM.com)

Gold could smash $10,000 on crashing dollar & other factors – Rickards (RT.com)

The end of the Clinton-Bush era (CapitalAndConflict.com)

Prevent “buyer’s remorse” like this (StansBerryChurcHouse.com)

Vested Interests Pushing House Prices Higher Again (DavidMCWilliams.ie)

Gold Prices (LBMA AM)

31 Jan: USD 1,343.35, GBP 950.29 & EUR 1,078.98 per ounce

30 Jan: USD 1,345.70, GBP 954.37 & EUR 1,083.56 per ounce

29 Jan: USD 1,348.40, GBP 955.07 & EUR 1,085.46 per ounce

26 Jan: USD 1,354.35, GBP 950.21 & EUR 1,087.41 per ounce

25 Jan: USD 1,360.25, GBP 954.35 & EUR 1,095.27 per ounce

24 Jan: USD 1,350.50, GBP 957.50 & EUR 1,093.77 per ounce

23 Jan: USD 1,337.10, GBP 959.10 & EUR 1,091.74 per ounce

Silver Prices (LBMA)

31 Jan: USD 17.23, GBP 12.17 & EUR 13.84 per ounce

30 Jan: USD 17.30, GBP 12.24 & EUR 13.91 per ounce

29 Jan: USD 17.34, GBP 12.33 & EUR 13.99 per ounce

26 Jan: USD 17.40, GBP 12.21 & EUR 13.99 per ounce

25 Jan: USD 17.52, GBP 12.29 & EUR 14.12 per ounce

24 Jan: USD 17.19, GBP 12.16 & EUR 13.93 per ounce

23 Jan: USD 16.98, GBP 12.19 & EUR 13.87 per ounce

Recent Market Updates

– London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

– Silver Bullion: Once and Future Money

– Greatest Stock Bubble In History? GoldNomics Podcast Transcript

– Davos – My Personal Experience of the $100,000 Event, $60 Burgers, Massive Inequality and the Blockchain Revolution

– Is This The Greatest Stock Market Bubble In History? Goldnomics Podcast

– Cyber War Coming In 2018?

– Government Shutdown Ends – Markets Ignore Looming Debt and Bond Market Threat

– Global Pension Ponzi – Carillion Collapse One Of Many To Come

– The Next Great Bull Market in Gold Has Begun – Rickards

– Gold Bullion May Have Room to Run As Chinese New Year Looms

– Digital Gold Flight To Physical Gold Coins and Bars

– Gold and Silver Bullion Are Only “Safe Investments Left” – Stockman

– Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

END

The use of digital gold from the Perth Mint may threaten the 122 billion in gold ETF’s

(courtesy Tony Boyd/Australian Financial Review/GATA)

Digital gold from Perth Mint threatens $122 billion in gold-backed ETFs

Submitted by cpowell on Tue, 2018-01-30 17:37. Section: Daily Dispatches

By Tony Boyd

Australian Financial Review, Sydney

Tuesday, January 30, 2018

The Perth Mint’s release of digital gold certificates for trading, holding, and transferring physical gold could have profound consequences for the $US98 billion ($122.5 billion) in gold-backed exchange traded funds.

The technology underpinning the digital gold certificates could have other uses such as the clearing and settlement of equities.

At this stage the digitisation of gold ownership by the Perth Mint is available only to institutional investors, such as banks, which can then offer it to retail customers.

But it is likely that the Perth Mint will overcome the difficult regulatory obstacles to direct retail ownership such as the know-your-customer rules and anti-money laundering regulations.

When that occurs the Perth Mint’s digital certificates could become a genuine challenger to gold-backed ETFs, which now own about 2,362 tonnes of gold, according to the World Gold Council.

Perth Mint is using technology supplied by digi.cash, a Sydney-based company backed by the Capital Markets Research Centre, to create gold certificates that can be traded on a smart phone.

The supplier of the certificates is a company called InfiniGold, a joint venture between digi.cash and Digital Access Australia. Steve Belloti, the former head of global markets at ANZ Banking Group controls Digital Access Australia.

Andreas Furche, who is chief executive of digi.cash, says the Perth Mint’s digital gold certificates will have at least two advantages over gold-backed ETFs.

The first is that they will be cheaper to own.

He said the cost of holding a digital gold certificate issued by Perth Mint will be less than the 30 to 40 basis points charged by ETFs. The world’s largest ETF, the SPDR Gold Shares, charges 40 basis points of the net asset value each year. The fund has a market capitalisation of $US36 billion.

The second advantage is that the digital gold certificates provide direct ownership of the gold held in the vaults at the Perth Mint. While ETFs are backed by physical gold held in vaults and warehouses, they interpose a third party between the investor and the bullion.

This creates the risk that the counterparty, such as a fund manager, will not be able to meet their obligations to supply the physical gold. Another way of looking at a gold-backed ETF is to think of it as a promissory note for the delivery of gold. …

… For the remainder of the report:

http://www.afr.com/brand/chanticleer/perth-mints-digital-gold-threatens-…

END

Mnuchin states that his dollar policy is not aimed at jawboning it lower. He still affirms his strong dollar policy. The question is what does a strong dollar policy mean especially with respect to gold/silver

(courtesy Bloomberg/GATA)

Mnunchin says his dollar policy isn’t aimed at jawboning it lower

Submitted by cpowell on Wed, 2018-01-31 00:52. Section: Daily Dispatches

By Brendan Murray and Randy Woods

Bloomberg News

Tuesday, January 30, 2018

The U.S. currency policy used to be just a few words: A strong dollar is in the country’s best interest. It’s become more of a mouthful under Treasury Secretary Steven Mnuchin, who wonders why he’s misunderstood.

“Let me be very clear: I absolutely support a strong dollar as being in the long-term best interest of the country, and I strongly support — we have a free currency market that we don’t intervene in and have relied upon the most liquid market in the world,” he said in testimony today to the Senate Banking Committee. “So the short term is not a concern of us.”

With that comment Mnuchin tried to resolve an issue that has roiled currency markets in recent days. Today Mnuchin recounted to lawmakers how in Davos, Switzerland, last week he gave a press briefing and delivered a three-part comment “that was extremely balanced and very specific,” adding that it was “not anything new.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-01-30/mnuchin-says-his-doll…

END

South Korea now states that it has no intention to ban Bitcoin or other cryptocurrencies

(courtesy zerohedge)

South Korea Has No Intention To Ban Bitcoin, Finance Minister Confirms

The months-long will-they-won’t-they back-and-forth between South Korea’s various regulatory bodies and the cryptocurrency market is finally nearing its final moment of clarity.

Today, in one of the more concrete indications that South Korean regulators aren’t planning a China-style stampout of the cryptocurrency market, the country’s finance minister assured jittery traders that the country is not planning to ban cryptocurrency trading – a possibility that has been raised several times in recent months, sending bitcoin plunging on every occasion.

According to CoinDesk, Kim Dong-yeon said, “there is no intention to ban or suppress cryptocurrency [market],” in response to a question from a lawmaker about the government’s plans to regulate the industry.

Instead of taking the dramatic step of shutting down all local exchanges – like China did – the minister assured his audience that, just as we reported last month, “regulating exchanges is [the government’s] immediate task.”

Reports that South Korea was considering a cryptocurrency ban hammered the market in December. Officials reportedly believed the market was overheating and required more scrutiny. However, officials quickly backtracked, and South Korea’s presidential office clarified on Jan. 11 that a plan to ban trading cryptocurrencies “is one of the measures prepared by the Ministry of Justice, but it’s not a measure that has been finalized.”

That plan has reportedly now been thrown out.

Instead, yesterday saw the introduction of new rules banning the use of anonymous virtual accounts for trading – from now on, South Koreans will need to use their real names on bank and exchange accounts. Furthermore, authorities said traders who don’t comply will face penalties.

As the above chart shows, South Korea is one of the world’s biggest markets for trading bitcoin and other digital currencies. But as China’s crackdown demonstrated, an outright ban in South Korea probably wouldn’t have a lasting impact on the market; many of the businesses would simply migrate to more open economies, and domestic traders would take their business to foreign exchanges.

Despite the reassurances, bitcoin and the other large cryptocurrencies were extending this week’s weakness Wednesday morning following President Donald Trump’s first State of the Union address.

Chris Powell: Golden Rays and Silver Linings

January 31

By Rory Hall

We firmly believe, and have stated a number of times, that gold and silver are the only assets that have the fortitude to stand up to governments and banks. These two assets, throughout history, have over and over and over again helped the people to gain wealth, to prosper and to truly innovate new technologies. What has happened over the past 100+ years is our wealth, innovation and sovereignty have been slowly stripped away.

Central banks are secretly trading all futures markets to control prices, this simply can not be reported. We would have to give up the pretense of free markets people would have to acknowledge – “No, we don’t have free markets!” we basically have a totalitarian system that is very carefully disguised. ~Chris Powell, The Daily Coin

The good news is it seems to be changing.

Liberty and truth made an appearance over this past week in two different ways. First, we had people arrested for rigging the precious metals markets and then we had the President stand up to a bunch of bullies in Congress attempting to keep the truth hidden from the American people. Truth that some members of Congress insisted did not exist in the first place. Some of what has been hidden is beginning to be revealed.

We have a very long way to go to overturn and correct the damage of more than 100 years of Federal Reserve manipulation, but this past week, those of us fighting the good fight received a much needed ray of sunshine that illuminated a silver lining surrounding the dark cloud that has been hanging over our nation for far too long.

I sat down with Chris Powell, Secretary Treasurer, GATA, to follow up on the arrest of 6 bank employees convicted of rigging the precious metals markets, how GATA see gold and silver returning to the monetary system and what all these new gold backed cryptocurrencies mean for the monetary system. The market rigging criminals were employed by three of the worlds biggest banks, HSBC, Deutsche Bank and UBS. In order for government to get out of market rigging we need not return to a traditional gold standard, but allow gold and silver to return to the monetary system of their own free will. Chris, along with Bill Still, believe this would naturally happen if governments were to get out of the way. The development of new fintech like gold backed cryptocurrencies may help to foster such an environment. Time will tell and we shall see if governments are willing to hand over their true source of power – control of the currency.

Video link to Chris Powell: Golden Rays and Silver Linings

Tsunami of Truth Coming in 2018 – Bill Holter

By Greg Hunter’s USAWatchdog.com

By Greg Hunter’s USAWatchdog.com

Financial writer Bill Holter thinks revelations from the so-called Washington D.C. swamp are going to intensify in 2018. Holter explains, “I would call what’s coming a tsunami of truth. . . . I think it’s going to affect the mood of the country. It is going to enrage some people. I think it will scare some people. It will definitely affect capital flows. There is a debate about arresting people and perp walks, whether that would be good or bad for confidence. It’s my opinion it would initially be bad for confidence because there are so many people (that would be criminally charged) it would blow their minds. It’s beyond anything that they even thought of. So, I think confidence would initially break, but longer term, it is good for confidence because it will be a sign that the rule of law is coming back to the United States.”

Holter contends the politics of crooked Washington D.C. have a negative effect on the U.S. dollar. Holter says, “One reason I think the dollars has been weak since the beginning of 2017 is there were an awful lot of truth bombs that hit last year. There is more truth with this four page memo from Congress that was just voted to be released. Foreigners are looking at the dollar with high skepticism because all of this ‘truth’ points to a very crooked, fraudulent and corrupt nation. Do you really want your assets in that system and denominated in that currency? I think the answer is no, and that’s one of the reasons you are seeing the huge devaluation of the dollar. . . . In 2017, my theme was that was the year of the truth bomb, and in 2018, I believe the theme will end up being the year that truth finally mattered.”

Holter goes on to say, “This country has lost the rule of law. It’s clear, looking at the DOJ and looking at the FBI, and what will come out on that, the rule of law needs to be restored. There needs to be a confidence restoration, if you will, in those agencies. It’s a complete travesty. What has really happened is they got so dirty that they tried a coup attempt. They tried to take over the government. They tried to negate an election. . . . A lot of people are speculating on Hillary going to jail, and I would put out that with all this illegal surveillance, there is absolutely no way that could have been done without Obama’s knowledge.”

Holter, who is also a precious metals broker, says big money is piling into metal, especially silver. Holter says, “Gold should do extremely well, and silver should do four or five times as well as gold if it gets back to the 15 to 1 historical ratio. . . . The lows were put in with gold and silver back in late 2015.”

What could go wrong with all-time high debt levels facing rising interest rates around the world? Holter points out, “There is all kinds of stuff that can go wrong. Cash levels for investors are at all-time lows. Margin debt is at all-time highs. That, in and of itself, is a recipe for disaster. Also, if you look at valuation levels . . . we are at record levels never seen before. . . . There is record risk/reward.”

Join Greg Hunter as he goes One-on-One with financial expert Bill Holter of JSMineset.com.

(To Donate to USAWatchdog.com Click Here)

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.2887 /shanghai bourse CLOSED DOWN AT 7.17 POINTS 0.21% / HANG SANG CLOSED UP 279.98 POINTS OR 0.86%

2. Nikkei closed DOWN 193.68 POINTS OR 0.83% /USA: YEN RISES TO 108.77

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 88.93/Euro RISES TO 1.2453

3b Japan 10 year bond yield: FALLS TO . +.085/ (TROUBLE THIS MORNING) GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.77/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.09 and Brent: 68.03

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

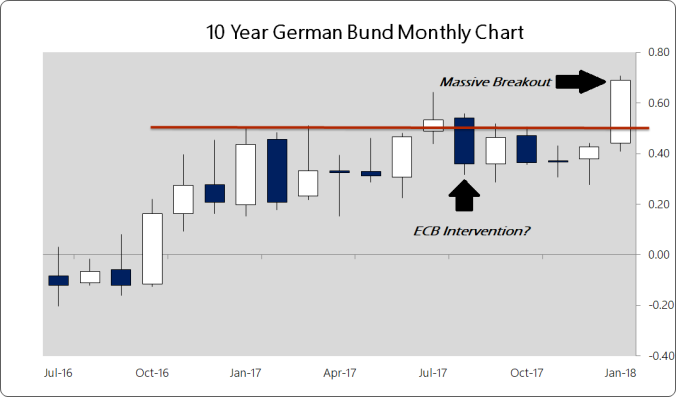

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.671%/Italian 10 yr bond yield DOWN to 2.002`% /SPAIN 10 YR BOND YIELD DOWN TO 1.403%

3j Greek 10 year bond yield RISES TO : 3.716?????????????????

3k Gold at $1343.20 silver at:17.25: 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 17/100 in roubles/dollar) 56.21

3m oil into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.77 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9333 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1620 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.671%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.701% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.9480% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Rebound After Trump’s SOTU Speech; Dollar Slide Resumes Ahead Of Fed

S&P futures rebounded 0.3% from the worst two-day selloff since Sept. 2016, and European and Asian stocks rose modestly from early weakness after Trump’s SOTU address did not deliver any major surprises, while traders were cautious ahead of the Fed’s last rate decision under Janet Yellen’s leadership expected to lean on the hawkish side.

On Tuesday, U.S. stocks tumbled amid concerns about a recent sharp rally in bond yields. Health-care shares slumped after Amazon.com, Berkshire Hathaway and JPMorgan agreed to collaborate on ways to offer health-care services to their employees; drugmakers will be in the spotlight again as Trump says prescription drug prices will come down “substantially.”

Despite the recent drop, it’s been a stellar month for stock markets, with major gains across most major gauges that were followed this week by the MSCI All-Country World Index’s biggest two-day slide since September 2016. Investors will now focus on Wednesday’s Federal Reserve rate decision, the ongoing earnings season and more big economic data points to see if the uptrend can resume.

On Tuesday night, Donald Trump sought to connect his presidency to the nation’s prosperity in his first State of the Union address, arguing the U.S. has arrived at a “new American moment” of wealth and opportunity. Trump vowed the “era of economic surrender is over,” but stopped short of naming the targets of his efforts to narrow the U.S.’s ballooning trade deficit, which prevented a major market reaction.

Trump also stated the US is finally seeing rising wages and that unemployment claims have hit a 45-year low. Trump also called on Congress to produce a bill that generates at least USD 1.5tln for new infrastructure investment and said that they will work to fix bad trade deals.

Overnight, the Dollar weakened again as Trump’s State of the Union speech offers few new details, while EMs rose as Trump failed to emphasize tariffs and trade.

“There was a moment where the dollar was bought on Trump’s infrastructure remarks, but that’s because the topic was in focus and markets reacted to that,” said Koichi Takamatsu, head of G-10 currency trading for Japan at Nomura Securities Co. in Tokyo. “On the other hand, after concerns about protectionism receded at Davos, Trump made clear his stance on ‘America First.’ Overall, the reaction to his speech was limited.”

The yen weakened as the BOJ unexpectedly boosted 3-to-5 year bond purchases in today’s open market operation and Kuroda affirmed stimulus policy, before erasing declines. Aussie grinds lower after inflation data misses, while the Aussie curve bull steepened as 3-year yield drops as much as seven basis points to 2.14% following a benign Australian inflation report. The British pound erased a gain as Prime Minister Theresa May headed to China to talk trade.

U.S. Treasuries were marginally firmer with 10-year yield just above 2.70%, despite Trump unveiling his plan for a $1.5 trillion debt-busting infrastructure plan.

European stocks erased gains of as much as 0.3%, with health-care shares (-0.5%) contributing the most to declines higher, after a two-day selloff as traders assess earnings and eye Federal Reserve Chair Janet Yellen’s final meeting on interest rates before her term ends. The Stoxx Europe 600 Index was flat heading for its best January in three years. Media shares lead gains, while Ericsson drags the tech sector lower after posting sales that missed analysts’ estimates. Capita is the biggest single-stock drag on the index after suspending its dividend and saying it plans to raise more equity, sending the stock for a record slump.

Asian stocks were mostly higher after Trump refrained from any comments that would have unnerved markets. As such, Australia’s ASX 200 (+0.2%) pared early losses and finished positive, although the commodity-related sectors continued their underperformance, while Nikkei 225 (-0.4%) swung between gains and losses with Japanese stock news dominated by earnings. Japan’s Topix index (-1.2%) slid to its lowest this year.

The region also mulled mixed Chinese Official PMI data in which Non-Manufacturing PMI topped estimates but Manufacturing PMI disappointed, which in turn disappointed local markets. The Shanghai Composite fell for a 3rd straight day, down 0.2% to 3480, while the Chinext index, tracking mid and small caps plunged near 2.7%, its biggest drop since January 15, and is now down 1% for year after rising as much as 3.7%. Big-cap blue chips outperformed with the SSE50 index tracking the 50 biggest stocks on Shanghai Stock Exchange climbed over 1.2%. The Koran Kospi index was boosted by Samsung’s stock split announcement, while the won strengthens in line with other Asian currencies. PBOC skips liquidity injections for fifth day; CSI 300 index 0.7% higher.

Of note: China’s onshore yuan climbed for its best month in at least a decade as the greenback drubbing continued. The Onshore yuan jumped 0.62% to 6.2855 per dollar in Shanghai; CNY has gained 3.5% so far in January, biggest monthly advance in CFETS data going back to April 2007 according to Bloomberg. Overnight, the PBOC weakened daily reference rate by 0.04% to 6.3339, matching average estimate in a Bloomberg survey of 25 traders and analysts; the predictions ranged from 6.3250 to 6.3414

Elsewhere, UK PM May said that there was a long-term job to do in Brexit and that she will publish Brexit impact studies during February speech in Munich. Furthermore, PM May said the UK is seeking a free trade deal with China and wants more access in the interim before trade deal. EU officials are to reject the City of London’s intention to strike a post-Brexit free trade deal for financial services, according to financial executives.

In commodities, oil retreated and industrial metals reversed losses. A measure of China’s manufacturing sector came in below expectations, while the services gauge topped estimates. WTI and Brent crude futures trade lower in the wake of last night’s larger than expected build in headline API crude oil inventories with energy newsflow otherwise relatively light ahead of today’s official EIA release. WTI crude slides below $64. In metals markets, gold prices are seen higher amid a lacklustre greenback while copper was marginally supported overnight by the improvement in risk tone. Finally, Chinese steel futures were seen lower overnight as adverse weather conditions capped demand in China. Dalian iron falls two percent.

Expected data include MBA mortgage applications. Anthem, AT&T, Boeing, Facebook, Lilly and Microsoft are among companies reporting earnings.

Bulletin Headline Summary from RanSquawk

- European equities trade broadly higher albeit modestly so, as earnings dictate the state of play for Europe.

- The DXY remains vulnerable under the 89.000 handle as January draws to a close and month end portfolio hedging indices continue to flag sell signals

- Looking ahead, highlights include US ADP, Quarterly Refunding Announcement and FOMC rate decision.

Market Snapshot

- S&P 500 futures up 0.3% to 2,833.00

- STOXX Europe 600 up 0.2% to 396.98

- MSCI Asia Pacific down 0.2% to 184.23

- MSCI Asia Pacific ex Japan up 0.4% to 607.33

- Nikkei down 0.8% to 23,098.29

- Topix down 1.2% to 1,836.71

- Hang Seng Index up 0.9% to 32,887.27

- Shanghai Composite down 0.2% to 3,480.83

- Sensex down 0.1% to 35,993.63

- Australia S&P/ASX 200 up 0.3% to 6,037.68

- Kospi down 0.05% to 2,566.46

- German 10Y yield fell 1.3 bps to 0.67%

- Euro up 0.3% to $1.2444

- Italian 10Y yield rose 0.2 bps to 1.76%

- Spanish 10Y yield rose 1.3 bps to 1.422%

- Brent futures down 0.6% to $68.60/bbl

- Gold spot up 0.3% to $1,343.12

- U.S. Dollar Index down 0.2% to 88.95

Top Overnight News

- Donald Trump sought to connect his presidency to the nation’s prosperity in his first State of the Union address, arguing the U.S. has arrived at a “new American moment” of wealth and opportunity. Trump vowed the “era of economic surrender is over,” but stopped short of naming the targets of his efforts to narrow the U.S.’s ballooning trade deficit

- U.K. Prime Minister May landed in China with a message to rebels back home who want to oust her: she won’t quit. May said she would raise the sensitive topics of China’s human rights record and Hong Kong democracy

- Bank of Japan offered to buy more bonds at a regular operation for the first time since July, helping to bring down yields and weaken the yen as Governor Kuroda reaffirmed a commitment to his ultra-loose monetary policy

- Mark Carney said he can fully focus on tackling inflation as the drag from Brexit on investment and the economy starts to recede

- U.K. banks will have limited access to the European Union’s single market after Brexit if the government refuses to weaken its red lines, the European Commission told diplomats, according to two people familiar with private discussions in Brussels

- The BOJ isn’t at the point where it can change interest rates soon, says Bank of Japan Deputy Governor Kikuo Iwata, in his final press conference before leaving the board

- German jobless rate dropped to a record low of 5.4 percent in January, extending its decline as companies stepped up hiring to meet buoyant demand

- Siemens Reports Strengthening Orders Amid Global Economic Upturn

- H&M’s Biggest Profit Drop in Six Years Puts CEO Under Pressure

- Volvo Sees Rising Global Truck Demand Straining Supply Chain

A mixed tone was gradually seen in Asia, as equity markets somewhat recovered from the initial spill-over selling from Wall St. where the S&P 500 posted its worst 2-day performance since May last year. The overnight rebound in sentiment was alongside President Trump’s first State of the Union Address, which Trump was viewed to have delivered a composed and conventional speech, while he also refrained from any comments that would have unnerved markets. As such, ASX 200 (+0.2%) pared early losses and finished positive, although the commodity-related sectors continued their underperformance, while Nikkei 225 (-0.4%) swung between gains and losses with Japanese stock news dominated by earnings. Furthermore, the region also mulled over mixed Chinese Official PMI data in which Non-Manufacturing PMI topped estimates but Manufacturing PMI disappointed, which in turn clouded over the Shanghai Comp. (-0.6%) and Hang Seng (+0.1%), despite a brief turnaround which momentarily saw most stocks lifted with the tide. Finally, 10yr JGBs are higher, with prices supported from today’s Rinban operation in which the BoJ were in the market for JPY 850bln of JGBs across the curve and upped its purchases of 3yr-5yr maturities.

- Chinese Manufacturing PMI (Jan) 51.3 vs. Exp. 51.6 (Prev. 51.6).

- Non-Manufacturing PMI (Jan) 55.3 vs. Exp. 54.9 (Prev. 55.0)

BoJ Summary of Opinions from January meeting said must continue with powerful easing policy as inflation remains weak. There summary noted the opinion that BoJ must look at effects and costs of BoJ’s ETF and risky asset purchases given stock prices and corporate profits improving sharply, while there also may be a chance for the BoJ to consider adjusting level of yield targets if economy and prices continue improving. BoJ says it plans to keep the current pace of bond purchases in Feb for all maturities.

Top Asian News

- BOJ Lifts Bond Purchases as Kuroda Affirms Loose Policy Path

- Dealmakers Jump Ship as China Tycoon’s $5 Billion M&A Push Ends

- Japan Factory Output Surges in December on Strong Exports

- Sumitomo Mitsui Profit Rises on Fee Income, Share Sale Gains

- Vakrangee Tumbles by 20% Limit Amid Stock-Price Rigging Report

European equities trade broadly higher (Eurostoxx 50 +0.2%) albeit modestly so, as earnings dictate the state of play for Europe. In terms of sector specifics, utility names have seen some support with SSE (+1.6%) sitting near the top of the FTSE after lifting their guidance, while IT names are seen softer with Ericsson (-8%) lower following earnings and Infineon (-0.7%) at the bottom of the DAX after cutting guidance alongside earnings. Elsewhere, stock specifics have been dominated by earnings with reports from the likes of Electrolux (+6.3%), Volvo (+3.4%), H&M (-4.8%), Lonza (-3.6%), Julius Baer (-3.2%) and focus once again on Capita (-35%) with shares slammed following their latest profit warning.

Top European News

- Italy’s Jobless Rate Falls Before Election to Lowest Since 2012

- German Workers Begin Day-Long Strikes as Wage Talks Hit Snag

- EU Softens Push to Keep Clients From Exiting Failing Banks

- European Union’s Biggest Rate Hawks Are Poised to Hike Again

- European Pharma Stocks Drop After Trump Comments, Lonza Results

- VW, Continental Best Placed in Break-Up Scenarios, BofAML Says

In FX, the DXY remains vulnerable under the 89.000 handle as January draws to a close and month end portfolio hedging indices continue to flag sell signals, and strong for several USD/G10 pairs. The Dollar did derive some support from a buoyant from US President Trump’s buoyant SOTU address and clarification by Treasury Secretary Mnuchin that a strong Greenback is in the country’s best interest (long term at least). However, EUR/USD looks solid above 1.2400 and around the 1.2433 level (200 MMA), with decent option expiries between 1.2400-40 (1.5 bn) and 1.2450-55 (1.7 bn) perhaps adding to the aforementioned rebalancing bid tone. Cable briefly reclaimed 1.4200+ status before easing back again amid EUR/GBP month-end demand and news that EU officials are to reject the City of London’s intention to strike a post-Brexit free trade deal for financial services. USD/JPY is back below 109.00, but still within a broad 108.50-109.50 range.

In commodities, WTI and Brent crude futures trade lower in the wake of last night’s larger than expected build in headline API crude oil inventories with energy newsflow otherwise relatively light ahead of today’s official EIA release. In metals markets, gold prices are seen higher amid a lacklustre greenback while copper was marginally supported overnight by the improvement in risk tone. Finally, Chinese steel futures were seen lower overnight as adverse weather conditions capped demand in China.

US Event Calendar

- 7am: U.S. MBA Mortgage Applications, Jan. 26, no est., prior 4.5%

- 8:15am: U.S. ADP Employment Change, Jan., est. 185k, prior 250k

- 8:30am: U.S. Employment Cost Index, 4Q, est. 0.6%, prior 0.7%

- 8:30am: U.S. Treasury’s Quarterly Refunding

- 9:45am: U.S. Chicago Purchasing Manager, Jan., est. 64, prior 67.6, revised prior 67.8

- 10am: U.S. Pending Home Sales MoM, Dec., est. 0.5%, prior 0.2%; NSA YoY, Dec., est. 1.7%, prior 0.6%

- 10:30am: DOE U.S. Crude Oil Inventories, Jan. 26, est. 900k, prior -1.07m

- 2pm: FOMC Rate Decision (Upper Bound), est. 1.5%, prior 1.5%

Looking at the day ahead, the Fed monetary policy meeting outcome will be the highlight today. Flash January CPI reports for the Euro area will be closely watched, as will the January ADP employment print change for the US. The latter will also release the Q4 employment cost index, January Chicago PMI and December pending home sales. Microsoft, Facebook, eBay, AT&T, Boeing and Paypal highlight a busy day for high profile earnings releases. The ECB’s Coeure will also speak.

DB’s Jim Reid Concludes the overnight wrap

If you’re reading this in the Western Hemisphere, stand by today for an event we haven’t seen since 1866. No, not equity markets going down two days in a row but instead a “Super Blue Blood Moon”. To break this down, a blue moon is where there are two new moons in a month. A supermoon is where our satellite’s perigee (its closest approach in its orbit and appearing c.14% larger and is c.30% brighter) coincides with a full moon. A blood moon is a lunar eclipse when the moon passes into the earth’s shadow. The reddish tint that this will bring as the sun’s light is cut off and it’s visible through the filter of our atmosphere provides the blood reference.

As discussed above this astrological event coincides with a bad month end for markets with confidence suddenly sucked into a black hole. Indeed the last couple of days are perhaps a taster of what might actually happen when yields properly normalise rather than simply selling off a bit. However unless something extraordinary happens today, January will still go down as an exceptional month for risk although bond returns will see a lot of negatives in front of the numbers. We’ll do the full review of the month tomorrow.

One of the most impressive parts of the equity sell-off yesterday was that there wasn’t really a flight to quality into bonds. 10yr USTs rose a further 2.6bps and 10yr Bunds only fell 1.1bps even with a weaker than expected German inflation print.

Now reviewing the equity moves. The S&P 500 (-1.09%) saw its worse day since mid-August and worst 2-day fall (-1.76%) since May, while the Dow (-1.37%) and Nasdaq (-0.86%) also retreated. The mini-selloff in the S&P seemed to have a few contributing factors, including ongoing concerns over valuation, rising yields, a lower oil price and weakness in health care stocks (-2.13%). The latter partly reflects potentially higher competitive tensions in view of Amazon, JP Morgan and Berkshire’s plans to launch a new joint company to provide their US staff with tech solutions for simplified healthcare at lower costs. The risk off tone was also evident in Europe with key bourses down 0.9%-1.1% and the Stoxx 600 down the most for c2.5 months (-0.92%). The VIX jumped to an intra-day high of 15.42, before closing 6.9% higher to 14.79 – the highest since mid-August.

Focusing on Apple, Bloomberg reported that according to unnamed sources, the US DOJ and SEC are investigating whether Apple violated securities laws regarding its disclosures about a software update that slowed older iPhones. Notably, the inquiry is in early stages and Apple’s share price fell c1.5% intraday and closed -0.59% lower.

Staying with US equities, since tax reform was signed, banks have written off billions of dollars of deferred tax assets. Yet the effects extend far beyond finance firms. In fact, one in ten companies in the S&P 500 has net deferred tax assets.

Also in the US, President Trump’s first State of the Union address touched on many issues but was short on details on his policy proposals. He highlighted his administration’s progress to building a “safe, strong and proud America” and

noted that “c3m workers have gotten tax cuts…this in fact is our new American moment…there has never been a better time to start living the American dream”. Then he spoke of unity in politics, such as “extending an open hand to work with members of both parties” and “…call upon all of us to set aside our differences… to deliver for the people we were elected to serve”. On trade, he touched on “America has finally turned the page on…unfair trade deals…” Then on the big infrastructure plans, he proposed to allocate $200bn federal funds over the next 10 years on roads and transit projects. Then the expectation is the investments would encourage further spending from the state, local governments and private sector – as least $1.5trn.

Elsewhere the Treasury Secretary Mnuchin sought to clarify his comments last week on the USD. He noted his comments were “not anything new” and “it was no way intended to talk down the dollar whatsoever”. Further he reiterated that “I absolutely support a strong dollar as being in the long term best interest of the country and….we have a free currency market that we don’t intervene in…”. As a reminder, today’s FOMC meeting will serve in part as a farewell to Chair Yellen, but is unlikely to result in any significant new signals for the market. Our US economists expect that the FOMC will want to see some more data and go through another round of forecasts before signalling a more aggressive tightening stance of four hikes this year (DB’s forecast).

This morning in Asia, markets are mixed but UST 10y yields is down c1.5bp. The Nikkei is down 0.47% while the Hang Seng (+0.06%), China’s CSI 300 (+0.14%) and Kospi (+0.44%) are all up, with the latter supported by Samsung, which is up c5% post its 4Q results and announcing a 50 to 1 stock split. Datawise, China’s January manufacturing PMI was a tad softer at 51.3 (vs. 51.6 expected) although the services number was a bit higher. Japan’s December IP was above market at 4.2% yoy (vs. 3.3%). Elsewhere, outgoing deputy BOJ governor Iwata warned against an early turn towards fiscal austerity, in part as “…achievement of the price stability target of 2% will become difficult” Now recapping other markets performance from yesterday. The US dollar index was marginally lower (-0.14%), while the Euro and Sterling gained 0.15% and 0.52%, respectively. Core 10y bond yields traded within a c3bp range intraday and closed little changed (Bunds -1.1bp; OATs -0.7bp; Gilts +0.7bp). In commodities, WTI oil fell 1.62% ahead of the API data, which later showed that US crude inventories rose for the first time since November. Elsewhere, precious metals softened c0.1% (Gold -0.13%; Silver -0.15%) and other base metals also weakened (Copper -0.34%; Zinc -1.06%; Aluminium -0.58%).

Away from markets, the BOE Governor Carney spoke on a range of topics in front of the House of Lords. On inflation, he noted the pass through from Sterling into inflation still has a way to go, but he is happy with the BOE’s inflation target. On Brexit, he denies that the BOE has a bias against it and that a “disorderly Brexit” is not a likely scenario. Elsewhere, he noted business investments is likely 4ppt lower than it would have been if the UK voted to stay in the EU bloc but also noted that investments could also pick up next year when uncertainty from Brexit reduces. On rates, he noted “as slack in the economy has been taken out…. (the focus for monetary policy) is increasingly on returning inflation sustainably to target over an appropriate horizon”. The implied Bloomberg odds of a rate hike in June was little changed, up 2ppt to 49%.

Returning to the UK, BuzzFeed has leaked the UK government’s forecasts of the potential economic impacts from Brexit. The worse scenario suggests the UK economy will be 8% smaller than otherwise in 15 years time and the softest scenario would slow economic growth by 2%. Brexit minister Baker noted the documents “require significant further work” and “its’ not yet anywhere near being approved by the ministers”. DB’s Oliver Harvey has published an update on the state of play with Brexit. He argues that the newsflow in recent days suggests rising risks of a political crisis before agreement can be reached on transitional arrangements in March. Refer to his note for more details.