Feb 9/HUGE VOLATILE DAY: YOUR KEY INDICATORS PREDICTING TROUBLE AHEAD: USA 10 YR TREASURY BOND YIELD: 2.85612/ CLOSING PRICE OF VIX: 28.85 BOTH AT DANGEROUS LEVELS/GOLD DOWN $4.70 TO $1312.60/SILVER DOWN 18 CENTS TO $16.20/USA PASSES A 2 YR BUDGET DEAL WHICH WILL ADD 2 TRILLION DOLLARS TO ITS DEFICIT/MOODY’S WARNS THE USE THAT IT MIGHT DOWNGRADE USA DEBT/CHINA ANNOUNCES THAT IT WILL COMMENCE ITS OIL YUAN CONTRACT SHORTLY AS WELL AS THE FUTURES CONTRACT WHICH WILL BEGIN ON MARCH 23./

In silver, the total open interest FELL BY A HUGE SIZED9371contracts from202,505 FALLING TO 193,135 DESPITE YESTERDAY’S SMALL 8 CENT GAIN INSILVER PRICING. WE HAD CONSIDERABLE COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 3215 EFP’S FOR MARCH AND AND 0 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 3215 CONTRACTS. WITH THE TRANSFER OF 3215 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 3215 CONTRACTS TRANSLATES INTO 16.08 MILLION OZ. WITH THE HUGE DROP IN OPEN INTEREST AT THE COMEX. WE SHOULD EXPECT BIGGER GAINS IN EFP TRANSFERS IN THE NEXT FEW DAYS WITH THE LARGE LOSS AT THE COMEX AS LONGS GAVE UP SEEKING METAL AT THIS EXCHANGE.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

24,531 CONTRACTS (FOR 8 TRADING DAYS TOTAL 24,531 CONTRACTS OR 122.655 MILLION OZ: AVERAGE PER DAY: 3066 CONTRACTS OR 15.331 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 122.655 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.5% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 357.59 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A HUGE SIZED LOSS IN OI SILVER COMEX DESPITE THE SMALL 8 CENT GAIN IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 3215 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 3214 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WITH YESTERDAY’S TRADING WE LOST 6156 OI CONTRACTS i.e. 3215open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 9371 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE SMALLRISEIN PRICE OF SILVER OF 8 CENTS AND A CLOSING PRICE OF $16.38 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.965 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest FELLBY ANOTHER CONSIDERABLE 7,499 CONTRACTS DOWN TO 519,362DESPITE THE GOODSIZED RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($5.20). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED A HUGE SIZED 14,716 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 14,716 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 517,708. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF7217 CONTRACTS:7499 OI CONTRACTSDECREASED AT THE COMEX AND A STRONG SIZED 14,716 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(7219 oi gain in CONTRACTS EQUATES TO 22.45 TONNES)

YESTERDAY, WE HAD 13,622 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 91,370 CONTRACTS OR 9,137,000 OZ OR 284.19 TONNES (8 TRADING DAYS AND THUS AVERAGING: 11,421 EFP CONTRACTS PER TRADING DAY OR 1,142,100 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 8 TRADING DAYS: IN TONNES: 284.19 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 284.19/2200 x 100% TONNES = 12.91% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 917.72 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A HUGE SIZED DECREASE IN OI AT THE COMEX DESPITE THE GOOD SIZED RISE IN PRICE IN GOLD TRADING YESTERDAY ($5.20). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,716 AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,716 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 7217 contracts ON THE TWO EXCHANGES:

14,716 CONTRACTS MOVE TO LONDON AND 7499CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 22.45 TONNES).

we had: 141 notice(s) filed upon for 14100 oz of gold.

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH TODAY’S TURMOIL, THE CROOKS WITHDREW ANOTHER 2 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 826.31

Inventory rests tonight: 826.31 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/ AGAIN WITH TODAY’S TURMOIL NO CHANGE IN INVENTORY

/INVENTORY RESTS AT 314.045 MILLION OZ/

can someone please explain why GLD behaves differently to SLV????

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A GIGANTIC 9371contracts from 202,506 DOWN TO 193,135 (AND now A LITTLE FURTHER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE GOOD SIZED RISE IN PRICE OF SILVER (8 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 3215 PRIVATE EFP’S FOR MARCH AND 0 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 9371 CONTRACTS TO THE 3215 OI TRANSFERRED TO LONDON THROUGH EFP’S, SURPRISINGLY WE OBTAIN A LOSS OF 6156OPEN INTEREST CONTRACTS DESPITE YESTERDAY’S GAIN IN SILVER PRICE. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET LOSS TODAY IN OZ ON THE TWO EXCHANGES: 30.78 MILLION OZ!!!

RESULT: A HUMONGOUS SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THEGOOD SIZED RISE OF 8 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD3215 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 132.19 points or 4.05% /Hang Sang CLOSED DOWN 943.85 or 3.10% / The Nikkei closed DOWN 508,24 POINTS OR 2.32%/Australia’s all ordinaires CLOSED DOWN 0.96%/Chinese yuan (ONSHORE) closed UP at 6.3041/Oil DOWN to 60.47 dollars per barrel for WTI and 64.30 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3040. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.3244//ONSHORE YUAN A LOT STRONGER AGAINST THE DOLLAR/OFF SHORE A LOT STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES EXCEPT CHINA YUAN. CHINA IS NOT TOO HAPPY TODAY.(INTERVENTION STRONGER CURRENCY AND WEAK MARKETS IN CHINA AND THROUGHOUT THE GLOBE

i

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

Asia crashes: China big cap companies crash over 7%/worst week since Lehman

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia slams the illegal USA presence in Syria

( zerohedge)

6 .GLOBAL ISSUES

i)Shiller reports on his 20 City Composite. Landlords are having to offer good incentives to bring in renters.

( Shiller)

ii)Huge spike in Cdn unemployment as part time jobs crash (due to increase in minimum wage in Ontario). This caused the Canadian dollar to falter to 1.2611

( zerohedge)

7. OIL ISSUES

Oil breaks the 60 dollar barrier

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

Banks do not want to risk financing bitcoin as they ban the use of credit cards purchasing Bitcoin

( Surane/Keller)

10. USA stories which will influence the price of gold/silver

i)This morning: suppression of VIX/stocks initially ramped higher

( zerohedge)

i b)Midday dead cat bounce as the Dow turns a 200 point gain into losing territory with the VIX rising to: 32.96 and the 10 yr bond piercing 2.85% again

( zerohedge)

ii)It is now Moody’s turn to sound the alarm bell with respect to the huge increase in the uSA debt. They are threatening the USA with a downgrade. With the new 2 year budget deal passed by both houses, the Debt Ceiling will be reset and the new “Debt to the Penny” will be close to 21 trillion dollars.

( zerohedge)

iii)No shutdown as the Congress passes a two year budget deal. They will fund the government up to March 23.2018

( zerohedge)

iv)Knives come out against Kelly for domestic abuse. Trump looks to Mulvaney to hold the Chief of Staff job along with his two other posts

( zerohedge)

v)UPS and Fed Ex sink badly on news that Amazon will be launching “Shipping with Amazon” where they will pick up parcels at facilities identical to our two major shipping operations

( zerohedge)

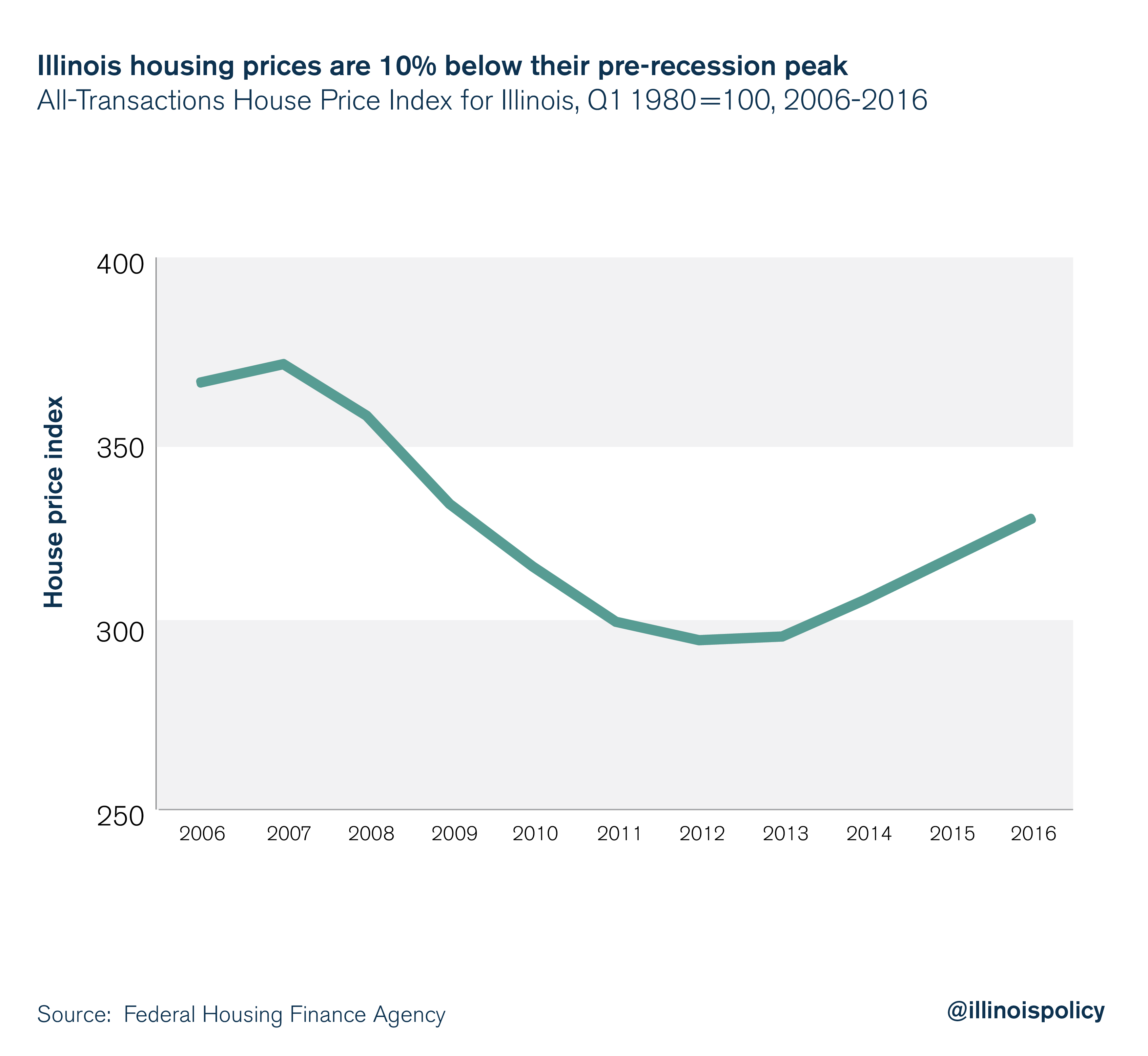

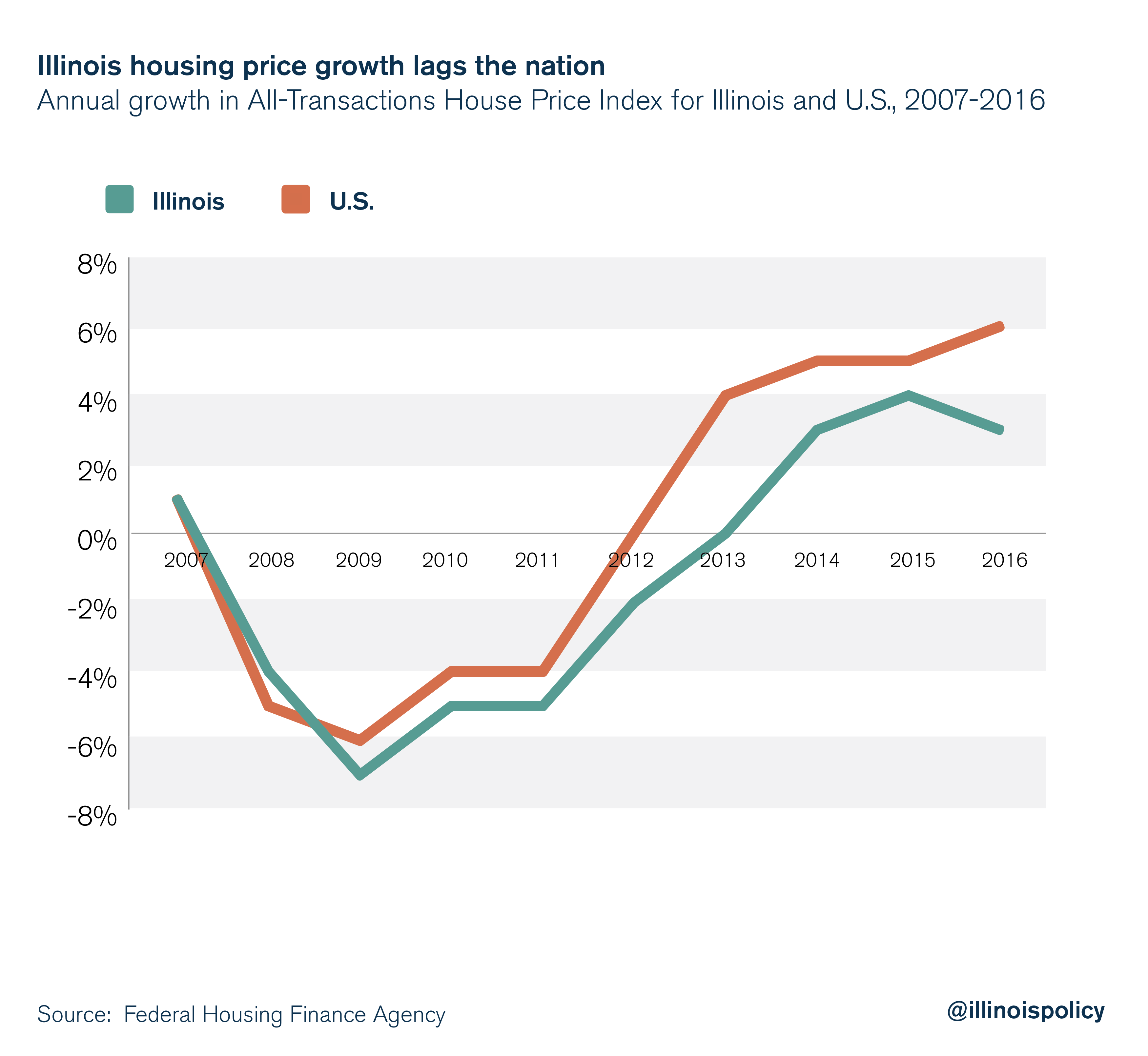

vi)A real problem for real estate companies in Illinois and home owners: Illinois property taxes are going up but prices are lagging( Divounguy,Hill Tabor/Illinois policy)

vii)Wholesale sales and wholesale inventories both slow in December and this will be a further damper to Q4 GDP numbers,

(courtesy zerohedge)

viii)SWAMP STORIES

a)Judicial Watch sues the FBI asking for documents on Comey’s 2 million dollar book deal plus communications between the FBI and Comey prior to his testimony

( zerohedge)

b)The very reliable the Wall Street Journal questions why the media (outside of Fox) is ignoring the real bombshell FISA memo ( the Grassley Memo)(courtesy Benson/Townhall.com)

Let us head over to the comex:

The total gold comex open interest FELL BY A CONSIDERABLE 7499 CONTRACTS DOWN to an OI level 517,708 DESPITETHE GOOD SIZED GAIN IN THE PRICE OF GOLD ($5.20 GAIN WITH RESPECT TOYESTERDAY’S TRADING). WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A HUGE SIZED 14,716 EFP’S ISSUED FOR APRIL AND 0 EFP’s FOR JUNE AND ZERO FOR ALL OTHER MONTHS: TOTAL 14.716 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 7217 OI CONTRACTS IN THAT 14,716 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST7499 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES:7217 contracts OR 721,700 OZ OR 22.91 TONNES, AND THIS WAS ACCOMPLISHED WITH A RISE IN PRICE OF GOLD BUT A SEVERE COMEX LIQUIDATION IN SILVER

Result: A HUGE SIZED DECREASE IN COMEX OPEN INTEREST DESPITE THE GOOD SIZED GAIN IN YESTERDAY’S GOLD TRADING ($5.20.) WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 7217 OI CONTRACTS..

We have now entered the active contract month of FEBRUARY where we lost 117 contracts to 1309 contracts. We had 55 notices filed upon yesterday, so we lost 62 contracts or 6200 oz will not stand in this active contract month of February AND THESE WERE MORPHED INTO LONDON BASED FORWARDS.

March saw a GAIN of 41 contracts UP to 1997. April saw a LOSS of 8230 contracts DOWN to 360,817. MARCH BECOMES THE FRONT MONTH FOR GOLD

We had 141notice(s) filed upon today for 14100 oz

PRELIMINARY COMEX VOLUME FOR TODAY: 384,541 contracts

CONFIRMED COMEX VOLUME FOR YESTERDAY: 362,184 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx And now for the wild silver comex results.

Total silver OI FELL BY A HUMONGOUS SIZED 9371CONTRACTS FROM 202,506 DOWN TO 193,135 DESPITEYESTERDAY’SGOOD SIZED 8 CENT GAIN IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER LARGE SIZED 3215 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3215. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD CONSIDERABLE LONG COMEX SILVER LIQUIDATION AND A GOOD SIZED LOSS IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE LOST 6156 SILVER OPEN INTEREST CONTRACTS:

9371 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 3834 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS TWO EXCHANGES: 6156 CONTRACTS DESPITE THE GAIN IN PRICE YESTERDAY

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 60 contracts DOWN TO 141 contracts. We had 60 notices filed upon yesterday so we GAINED 0 contracts or NIL ADDITIONAL oz will stand for delivery at the comex

The March contract lost 7796 contracts DOWN to 101,101

April gained 31 contracts up to 74 .

.

We had 0 notice(s) filed for NIL OZ for the FEBRUARY 2018 contract for silver

Total monthly oz gold served (contracts) so far this month

1733 notices

173300 oz

4.3902 tonnes

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

we had 0 kilobar transaction/

We had 0 inventory movement at the dealer accounts

total inventory deposit into the dealer accounts: nil oz

we had 2 withdrawals out of the customer account:

i) out of Scotia

we had 1929.0000 oz of gold transferred out of Scotia????

ii) Out of Brinks: 225.057 oz

total withdrawal: 2,225,057 oz

we had 2 customer deposit

i) Into brinks: 1,009.83 oz

ii) Into Scotia; 1929.0000 oz???

total customer deposits: 12,938.838 oz

we had 0 adjustments

total registered or dealer gold: 386,218.559 oz or 12.01 tonnes

total registered and eligible (customer) gold; 9,281457.005 oz 288.69 tones

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 56 notices were issued from their client or customer account. The total of all issuance by all participants equates to 141 contract(s) of which 140 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1733) x 100 oz or 159,200 oz, to which we add the difference between the open interest for the front month of FEB. (1309 contracts) minus the number of notices served upon today (141 x 100 oz per contract) equals 290,100 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1733 x 100 oz or ounces + {(1309)OI for the front month minus the number of notices served upon today (141 x 100 oz )which equals 290,100 ozstanding in this active delivery month of February (9.023 tonnes). THERE IS 12.01 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 62 CONTRACTS OR AN ADDITIONAL 6200 OZ WILL NOT STAND BUT THEY WILL JOIN OTHER LONGS AS THEY HAVE BEEN TRANSFERRED TO A LONDON BASED FORWARD THROUGH THE EFP ROUTE.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES.

IN THE LAST 17 MONTHS 65 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

feb 9 2018

Silver

Ounces

Withdrawals from Dealers Inventory

nil oz

Withdrawals from Customer Inventory

443,771,360 oz

Brinks

Deposits to the Dealer Inventory

nil

oz

Deposits to the Customer Inventory

599,038.290 OZ

JPM

Delaware

No of oz served today (contracts)

0

CONTRACT(S

(NIL OZ)

No of oz to be served (notices)

141 contracts

(705,000 oz)

Total monthly oz silver served (contracts)

199 contracts

(995,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into J.P.MORGAN:598,011.000 oz

ii) into Delaware: 1027.29 oz

total inventory deposits: 599,038.290oz

we had 1 withdrawals from the customer account;

i Out of Brinks: 443,771.360 0z

total withdrawals; 443,771.360 oz

we had 0 adjustment

total dealer silver: 43.384 million

total dealer + customer silver: 250.269 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 199 x 5,000 oz = 995,000 oz to which we add the difference between the open interest for the front month of FEB. (141) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 199(notices served so far)x 5000 oz + OI for front month of FEBRUARY(141) -number of notices served upon today (0)x 5000 oz equals 1,700,000 ozof silver standing for the FEBRUARY contract month.

WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX

YESTERDAY’S CONFIRMED VOLUME OF 137,283 CONTRACTS EQUATES TO 685 MILLION OZ OR 97.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.59% (FEB 9/2018) 2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.41% to NAV (FEB 9/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.59%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.41%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -4.14%: NAV 13.58/TRADING 13.00//DISCOUNT 4.14%

END

And now the Gold inventory at the GLD/

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 9/2018/ Inventory rests tonight at 826.31 tonnes

*IN LAST 323 TRADING DAYS: 114.84 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 257 TRADING DAYS: A NET 42.47 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Feb 8/2017:

Inventory 314.045 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.65%

12 Month MM GOFO

+ 2.09%

end

As many of you know, I find no use for the COT report for the simple reason that a mammoth number of longs leave coupled with the shorts as well.

However for completeness, I will provide the report to you and anything you can glean from it, will be a bonus

First our gold COT

Gold COT Report – Futures

Large Speculators

Commercial

Total

Long

Short

Spreading

Long

Short

Long

Short

273,828

82,951

60,557

158,650

364,101

493,035

507,609

Change from Prior Reporting Period

-24,499

-8,114

2,909

3,960

-15,665

-17,630

-20,870

Traders

170

91

81

48

57

260

192

Small Speculators

Long

Short

Open Interest

42,286

27,712

535,321

-6,381

-3,141

-24,011

non reportable positions

Change from the previous reporting period

COT Gold Report – Positions as of

Tuesday, February 6, 20

our large speculators

those large specs that have been long pitched (transferred to London) a huge 24,499 contracts on a net basis

those large specs that have been short in gold covered 8114 contracts from their short side

our commercials

those commercials who have been long in gold added 3960 contracts to their long side

those commercials who have been short in gold covered (transferred) a net 15,665 contracts their obligation rests in London

our small speculators

those small specs who have been long pitched (transferred) a net 6381 contracts from their long side

those small specs who have been short in silver covered (transferred) a net 3141 contracts from their short side

our silver cot

Silver COT Report: Futures

Large Speculators

Commercial

Long

Short

Spreading

Long

Short

63,729

47,189

38,732

75,255

105,896

-8,416

7,466

8,131

6,977

-9,673

Traders

97

60

48

44

36

Small Speculators

Open Interest

Total

Long

Short

205,470

Long

Short

27,754

13,653

177,716

191,817

420

1,188

7,112

6,692

5,924

non reportable positions

Positions as of:

164

126

our large speculators

those large specs that have been long in silver pitched (transferred) a huge 8416 contracts (net) from their long side

those large specs that have been short in silver added 7466 contracts to their short side

our commercials

those commercials that have been long in silver added 6977 contracts to their long side

those commercials that have been short in silver transferred a net 9673 contracts over to London

our small speculators

those small specs that have been long in silver pitched (transferred) a huge 8988 net contracts from their long side

those small specs that have been short in silver added a huge 7169 contracts to their short side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Brexit Risks Increase – London Property Market and Pound Vulnerable

Brexit Risks Increases – London Property Market and Pound Vulnerable

– Brexit uncertainty deepens as UK government in disarray – BOE warns of earlier and larger rate hikes for Brexit-hit UK – UK property prices fall second month in row, London property under pressure

– No deal Brexit estimated to cost UK £80bn according to government analysis

– Transition period causing major uncertainty for UK and pound

– Pound expected to fall as Brexit fears remain into 2018

Editor: Mark O’Byrne

Source: VoxEU.org

Brexit risks have increased in recent days. A Reuters poll published on 8th February shows the pound is expected to fall this year as uncertainty around Brexit grows. Meanwhile London property prices continue to fall.

The median view of more than 60 foreign exchange specialists asked by Reuters, concluded the pound will struggle as the UK heads towards its exit of from the trading bloc in 2019.

This will come as a shock to many who had thought sterling had seen the worst of times following the 2016 referendum. After all, the currency was one of the world’s best performing currencies in 2017 after the over 30% collapse versus gold in 2016.

Gold in GBP (5 Years) (Click to enlarge)

Much of the 6.5% gain since October 2016 has been thanks to a stable monetary policy expectations. This is likely to remain in the short term but long term the Bank of England will no doubt struggle to handle the fallout of the current bubblicious environment, the immediate impact of Brexit uncertainty and rapidly changing geopolitics.

Also last week a government analysis was published stating that £80 billion would be the cost to the UK should a Brexit result in a ‘no deal’. As well as costs to businesses, food and drink prices are predicted to climb by 21% and 17%, respectively.

The pound has been in a precarious position ever since the referendum result. It will continue to be as more unknowns rear their heads. Savers may be pleased to hear about the prospect of a rate hike as suggested by the MPC this week, but how much difference does it make when the currency is floundering, significantly devalued and the country appears vulnerable until post-Brexit?

Is the EU working against the UK?

Brexit has been a sore point since the referendum but since negotiations began the divisions and wounds have grown deeper and deeper.

Naturally the EU has to be seen working against an event such as Brexit as it questions the trading bloc’s very existence. Last week Michel Barnier managed to behave so anti-UK that he managed to do one thing Theresa May has so far failed to do – unite the British government.

Barnier brought up new demands for a Brexit transition agreement. He suggested that the UK be subject to sanctions if the EU believe laws have been infringed. The country could be fined, suggested Barnier, without the EU having to go through the usually lengthy court process.

In short, Barnier and the EU would like to be able to punish the UK as it deems fit, during the transition period. Sanctions might come about should the country be considered to be operating against the EU’s interests in say, trade deals.

This development further underlines why the most dangerous time for the UK is the 19-month transition period. It is the most dangerous as it is the most unknown. It appears to be negotiations surrounding this that are causing the most damage to the the pound and the future of the UK economy.

Is London ‘dying’?

The financial hub of London has long been revered as one of the most established and most respected in the world.

The City’s power was one of the rallying cries of both the remain and leave campaigners during the referendum. The leavers stating that the financial power of London would only be strengthened by Brexit, the remainers saying it would only be weakened.

Politico’s Capital Markets summit this week gained some interesting insights from EU finance bods.

Olivier Guersent, the director general of the EC’s financial services directorate told the UK’s financial services to be prepared to be treated ‘as a third country’ whilst Claudio Costamagna, chairman of Italy’s Cassa Depositi e Prestiti, said that London’s financial centre is ‘dying’.

This does not bode well for a capital and country which is seeing poor results on various fronts of late, most notably in housing and the property market.

Financial services companies are delaying setting up here, as are other international bodies, because of uncertainty surrounding Brexit. This has had a major impact on demand, which is one of many factors pushing down the capital’s much hyped-up property market.

January’s RICS survey showed London’s house prices remain firmly in the red as more participants reported falling rather than rising prices.

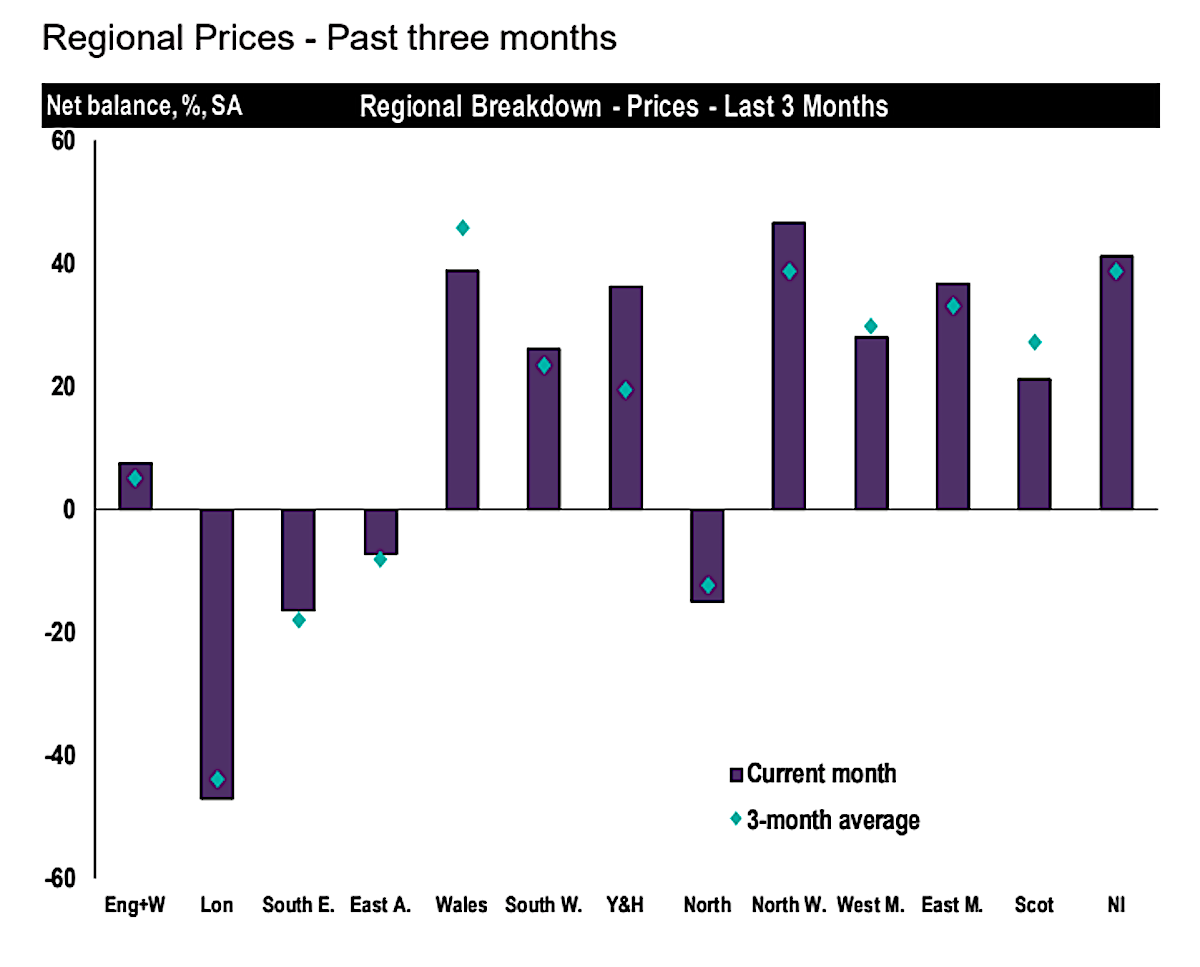

According to Business Insider, the outlook isn’t set to improve much either:

While prices are expected to flatline nationally in the next three months, London is once again the exception, with most respondents expecting prices to fall — although the net balance ticked up from -41% in December to -21%.

This week the MPC decided to keep interest rates on hold but warned hikes may come thicker and faster. Unsurprisingly Mark Carney was questioned at length about the impact of Brexit on the MPC’s decision.

Carney said that should there be no transition deal by the end of March the MPC will be forced to look at the impact on household and business confidence before deciding how this will affect the economy.

The BofE forecast is predicted on the assumption that there will be a smooth transition, which Carney believes will be the case. Secondly, it is based on the view that the MPC has no further information than anyone else does. Carney hopes that we will be better informed by the end of the year and asks markets to consider how ‘nimble’ monetary policy can be.

This does not bode well for a country that has seen a fall in the value of its currency recently. Much of this is thanks to ‘nimble’ monetary policy.

So far, markets have reacted well to the latest announcement that the MPC may hike rates sooner than expected. How will this work out for those who are participating in the London housing market?

Many homeowners are practically mortgaged up-to-the-eyeballs having only ever lived with low-interest rates. Combine this with the uncertainty of jobs due to Brexit, plus increased living costs…the future is not looking bright for the property market and those exposed to it.

Expensive: Uncertainty is the only certainty of Brexit

It certainly seems as though the country and its government are distracted with the transition deal, sticking to the course of the UK’s departure by March 2019.

The problem is that distraction is creating a frothiness in the daily news cycle, surrounding all things Brexit. Rumours are swirling, papers are being leaked and MPs are throwing tantrums at every opportunity.

What does all this mean for the average UK and EU citizen? Major uncertainty. Ultimately nothing has been decided. For now the Brexit negotiations rage on, with very little achieved since they began.

Sadly markets don’t wait to see what the final outcome will be. They operate on news today and expected outcomes. The real news is that British citizens are more in the lurch than ever.

At the moment the expected outcome is unknown and wholly uncertain when it comes to how the UK will fare. Those who diversify away from sterling and other fiat currencies and into gold will be hedged. The price of gold in sterling will rise in the medium and long term, as we saw with the collapse of the pound following the Brexit referendum.

Gold thrives in environments such as these. UK investors would be prudent to pound cost average into gold while prices remain relatively depressed.

Banks do not want to risk financing bitcoin as they ban the use of credit cards purchasing Bitcoin

(courtesy Surane/Keller)

Bitcoin Ban Expands Across Credit Cards as Big U.S. Banks Recoil

By Jennifer Surane and Laura J Keller

Updated on

A growing number of big U.S. credit-card issuers are deciding they don’t want to finance a falling knife.

JPMorgan Chase & Co., Bank of America Corp. and Citigroup Inc. said they’re halting purchases of Bitcoin and other cryptocurrencies on their credit cards. JPMorgan, enacting the ban Saturday, doesn’t want the credit risk associated with the transactions, company spokeswoman Mary Jane Rogers said.

Bank of America started declining credit card transactions with known crypto exchanges on Friday. The policy applies to all personal and business credit cards, according to a memo. It doesn’t affect debit cards, said company spokeswoman Betty Riess.

And late Friday, Citigroup said it too will halt purchases of cryptocurrencies on its credit cards. “We will continue to review our policy as this market evolves,” company spokeswoman Jennifer Bombardier said.

For more on cryptocurrencies, check out the Decrypted podcast:

Allowing purchases of cryptocurrencies can create big headaches for lenders, which can be left on the hook if a borrower bets wrong and can’t repay. There’s also the risk that thieves will abuse cards that were purloined or based on stolen identities, turning them into crypto hoards. Banks also are required by regulators to monitor customer transactions for signs of money laundering — which isn’t as easy once dollars are converted into digital coins.

Bitcoin has lost more than half its value since Dec. 18, falling below $8,000 on Friday for the first time since November. The drop occurred amid escalating regulatory threats around the world, fear of price manipulation and Facebook Inc.’s ban on ads for cryptocurrencies and initial coin offerings.

Now, cutting off card purchases could exacerbate those pressures by making it more difficult for enthusiasts to buy into the market. Capital One Financial Corp. and Discover Financial Services previously said they aren’t supporting the transactions.

Mastercard Inc. said this week that cross-border volumes on its network — a measure of customer spending abroad — have risen 22 percent this year, fueled partly by clients using their cards to buy digital currencies. The firm warned that the trend already was beginning to slow as cryptocurrency prices fell.

Discover Chief Executive Officer David Nelms was dismissive of financing cryptocurrency transactions during an interview last month, noting that could change depending on customer demand. For now, “it’s crooks that are trying to get money out of China or wherever,” he said of those trying to use the currencies.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.3040 /shanghai bourse CLOSED DOWN AT 132.19 POINTS 4.05% / HANG SANG CLOSED DOWN 943.85 POINTS OR 3.10%

2. Nikkei closed DOWN 508.24 POINTS OR 2.32% /USA: YEN RISES TO 108.97

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index RISES TO 90.45/Euro FALLS TO 1.2236

3b Japan 10 year bond yield: FALLS TO . +.066/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.97/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.47 and Brent: 64.30

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.741%/Italian 10 yr bond yield UP to 2.015% /SPAIN 10 YR BOND YIELD UP TO 1.452%

3j Greek 10 year bond yield RISES TO : 4.067?????????????????

3k Gold at $1316.10 silver at:16.36 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 58.29

3m oil into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.97 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9386 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1485 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.741%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8403% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1390% /BOTH DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Asia Crashes, Europe Slides, US Rebounds But Yields Resume Ominous Rise

“$5 trillion was wiped out from global stocks this week.”

After yesterday’s violent last hour plunge in US stocks, which also sent the VIX surging back to the mid-30s, the overnight session was somewhat muted, with European stocks falling further on Friday morning, but at a slower pace than the sharp sell offs in Asia and New York.

Europe’s 600 Index, down -1% as of this moment and back to session lows after a modest rebound earlier, was set for its worst week since 2016 as banks and financial-services stocks led most industry sectors lower. The drop, however, was relatively modest and followed a sheer plunge in Asia, where stocks tumbled across the region, wiping out most of their gains from the previous two sessions. The Shanghai Composite recouped some gains to close down “only” 4.1% – in what has now been a two-week selloff without the Chinese National Team making an appearance and buying stocks – the Hang Seng was down 3.1% with losses across all sectors. Tokyo’s Topix closed down 1.9 per cent.

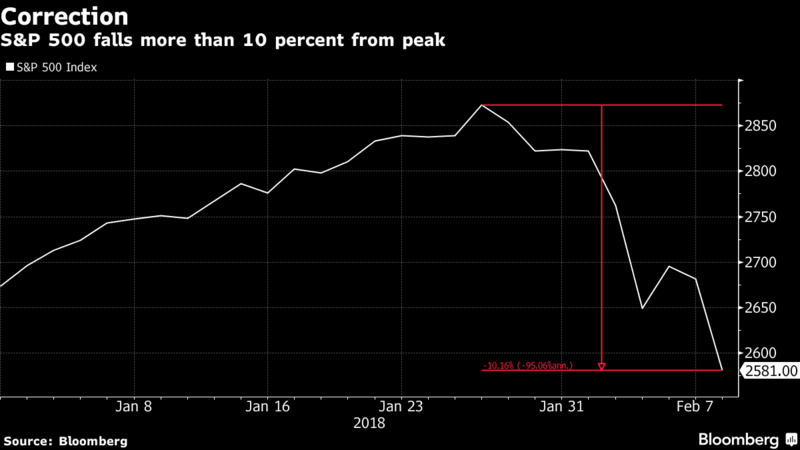

The renewed slide followed Thursday’s drop in the S&P 500, which pushed the index to a 10 per cent decline from its January high – officially, a correction – stirred renewed concerns over the future of the long bull market that followed the 2008 financial crisis, and whether the selloff that was catalyzed by systematic quant funds would spill over to retail investors. And, as we highlighted overnight, that’s precisely what happened following the single biggest weekly outflow from equity funds on record.

And while we look forward to today’s session to see if the retail liquidation continues, S&P 500 futures little changed, after earlier rising as much as 0.9%, while Dow contracts reverse advance to slide 0.3%, even as Congress passed a delayed budget deal, after the government was briefly shut down.

The premarket calm may not last: in what has become a vicious Catch 22, as futures rise, so do 10Y yields, and as the last few days have demonstrated, once the 10Y rises above 2.85%, it leads to an almost immediate selloff.

Some perspective: what was until recently the best start since 1987, has turned into a global selloff that has wiped $5 trillion from global stocks since January while the MSCI World Index is set for its biggest weekly drop since 2011.

Meanwhile over in macro, FX traders have one eye on the stock markets and another on positioning and central bank developments. While in earlier trading the dollar stayed under pressure as U.S. futures pointed to a higher open and Treasuries slipped, the entire move has quickly reversed as futures started to sink as yields rebounded, sending the BBG Dollar index (BBDXY) to session highs.

“A reassessment of the inflation outlook at this point in the cycle is natural and markets are adjusting for this,” Kerry Craig, a Melbourne-based global market strategist at JPMorgan Asset management, said in a note. “But given that U.S. markets are now in correction territory it’s likely that the most severe gyrations will hopefully have passed. Volatility may remain for a while longer, but the strong economic backdrop and sustained earnings outlook means we continue to prefer equities.”

Meanwhile, days after Goldman came out with a glowing endorsement of the commodity sector in general, and crude in particular, oil headed toward its worst week in almost a year as the global risk-asset rout further rankled investors already concerned over growing U.S. supply. Gold declined along with most industrial metals. South Africa’s rand strengthened as speculation intensifies that President Jacob Zuma will soon resign. Russia’s ruble was among the best-performing emerging-market currencies after the country’s central bank cut its policy rate.

Bulletin headline summary from RanSquawk

Partial government shutdown stopped after US Senate and House passes spending bill.

European bourses showing some resilience to the sell-off seen in the US and Asia.

Looking ahead, highlights include Canadian Jobs report and a slew of central bank speakers.

Top Headline News from BBG

Congress passed a two-year budget agreement early Friday that will boost federal spending by almost $300 billion and suspend the debt ceiling for a year, ending a brief partial government shutdown that began at midnight when lawmakers missed a funding deadline

Fed’s Esther George says three rate hikes this year and about the same number next year is a “reasonable baseline unless the outlook changes materially”; she also said that last week’s report of higher wages is a “welcome development” and that she expects inflation to begin to rise as labor markets tighten further and global demand pushes up import prices

Investors pulled $30.6b out of global equity funds, the most on record, analysts at BofAML says in research note citing EPFR Global data for week ending Feb. 7

Hedge funds investing only in Europe received about $6 billion in 2017, reversing a funding exodus in the previous 12 months, according to eVestment data; money pools targeting the U.S. and Asia suffered combined outflows last year of about $24 billion

RBA said in its quarterly policy statement that it will be some time before the economy reaches current estimates of full employment and inflation returns to the midpoint of the target. It left inflation and economic growth forecasts unchanged from three months earlier

U.K. PM Theresa May is adamant that Britain must aim high in its demands for an ambitious free-trade deal, just as she’s determined to make the most of her time in office, however long that lasts, officials said

Market Snapshot

S&P 500 futures up 0.6% to 2,608.50

STOXX Europe 600 down 0.4% to 372.4

MSCI Asia Pacific down 1.9% to 170.20

MSCI Asia Pacific ex Japan down 1.9% to 554.21

Nikkei down 2.3% to 21,382.62

Topix down 1.9% to 1,731.97

Hang Seng Index down 3.1% to 29,507.42

Shanghai Composite down 4.1% to 3,129.85

Sensex down 1.4% to 33,937.75

Australia S&P/ASX 200 down 0.9% to 5,837.97

Kospi down 1.8% to 2,363.77

Brent Futures down 0.5% to $64.48/bbl

Gold spot down 0.3% to $1,315.09

U.S. Dollar Index up 0.02% to 90.25

German 10Y yield unchanged at 0.763%

Euro up 0.2% to $1.2266

Brent Futures down 0.5% to $64.48/bbl

Italian 10Y yield rose 4.3 bps to 1.725%

Spanish 10Y yield fell 1.6 bps to 1.434%

Asia stocks traded negative across the board with global sentiment lambasted after the return of the market turmoil on Wall St, where the major indices closed in correction territory and the DJIA (-4.2%) tumbled over 1000 points on the day with the move accelerating heading into the close. Furthermore, political uncertainty in the US also added to the downbeat tone with the government officially in a shutdown after Senator Rand Paul blocked to fast track the Senate vote on the 2-year budget deal, other commentators have also paid credence to the continued upside in US yields adding pressure to equities. As such, ASX 200 (-0.9%) was weaker with energy names dampened after Brent crude prices fell to a near 2-month low, while losses in the Nikkei 225 (- 2.7%) were magnified by recent JPY strength. Elsewhere, underperformance in China resumed in which Hang Seng (-3.7%) and Shanghai Comp (-5.3%) slumped as the large cap energy and financials dragged, while the PBoC remained steadfast in its efforts to keep interbank liquidity stable and refrained from open market operations for a 12th day. However, the central bank instead announced it released nearly CNY 2tln in temporary liquidity through the Contingent Reserve Allowance which will allow banks to temporarily utilize deposit reserves to satisfy cash demand ahead of the Lunar New Year. Finally, 10yr JGBs were higher on safe-haven bids and with the BoJ also present in the market for JPY 850bln in JGBs across the curve. PBoC skips open market operations, for the 12th consecutive day, while it said it released temporary liquidity valued nearly CNY 2tln as it seeks to satisfy cash demand before the Lunar New Year.

Top Asian News

China Ends 25-Year Wait as Yuan Oil Futures Set to Start Trading

Citic Bank to Offer HNA Group 20B Yuan Credit Line

Bank Indonesia Intervenes to Stabilize Rupiah at 20-Month Low

Shenzhen Stocks Enter Bear Market as New Economy Dreams Fade

European traders were closely watching events in the US on Thursday: The fresh sell-off late yesterday saw US equities (DJIA and S&P 500) move into correction territory amid the surge higher in yields in which the US 10yr yield made a high of 2.88%, matching the post NFP high. This also transpired into a sell-off in the Asia-Pac region with Chinese bourses seeing its largest weekly decline in 2yrs, prompting Chinese authorities to announce a CNY2tln temporary liquidity package. However, despite this, losses in Europe have been somewhat contained, European bourses showing a relatively mixed picture (EuroStoxx 50 -0.4%). On a stock specific basis, M&A talk has been doing the rounds with the L’Oreal CEO hinting that they may acquire a EUR 23bln stake in Nestle. Umicore shares the best performer following their strong trading update.

Top European News

BOE’s Broadbent Says Rate Path Now Slightly Higher Than in Nov.

U.K. PM Is Mulling Trip to Northern Ireland Next Week, BBC Says

Maersk Drops as Company Misses Estimates After an ‘Unusual’ Year

Flow Traders Shares Soar as Volatility Drives 1Q

In FX, Usd/Jpy is now bouncing further from overnight lows (around 108.50 where decent domestic bids were reported) through 109.00 and offers at 109.20 to a 109.30 peak so far. Similarly, Usd/Chf is firmer up towards 0.9400 vs 0.9350 at one stage and the DXY is deriving some underlying support ahead of the 90.000 level despite Greenback losses against other G10 counterparts. Cable has lost grip of the 1.4000 handle and a degree of its bullish/hawkish BoE impetus, but remains firm ahead of 1.3900, as Eur/Gbp continues to trade below 0.8800 and Eur/Usd is capped by 1.2289 resistance (55 DMA) in front of supply at 1.2300. Usd/Cad is still pivoting around 1.2600 and now awaiting Canadian jobs data amidst the ongoing NAFTA impasse, while Aud/Usd stays on the backfoot after the RBA’s dovish SOMP and weaker than forecast mortgage data within a 0.7795-60 range – 200 DMA at 0.7755 providing support and big 0.7800 option expiry (2.75 bn) also exerting some influence. Nzd/Usd is holding just above 0.7200 in wake of this week’s RBNZ meeting, which opened the door to further easing alongside central guidance for tightening in mid-2019, but Usd/Cnh has retreated from its post-capital control related spike highs.

In commodities, across the commodities complex, WTI and Brent crude futures continue to hover near recent lows, however prices have seen a slight pull back amid source reports that the Forties pipeline system is still running at a restricted rate. China plans to launch crude oil futures on March 26th.

Looking at the day ahead, the only data of note is December wholesale trade sales. The Fed’s George is also due to speak early morning.

US event calendar

10am: Wholesale Inventories MoM, est. 0.2%, prior 0.2%; Wholesale Trade Sales MoM, est. 0.4%, prior 1.5%

DB’s Jim Reid concludes the overnight wrap

The Winter Olympics in Pyeongchang starts today and if markets this week were an event I think they’d probably be the Ski Cross. If you haven’t seen this crazy race it consists of wild jumps, fast bends, spectacular crashes, terrifying falls, and jutting elbows. Just like the VIX this week.

The ups and downs continued yesterday with the eventual emphasis on the down with another very poor US close seeing the S&P 500 down -3.75% and 104 points lower than the day’s early highs. Given how sensitive markets were to a slightly hawkish BoE yesterday, one can only imagine the turmoil on Wednesday next week if US CPI comes in ahead of expectations. Obviously a softer/in-line number would be greatly received at the moment. To put the BoE in perspective their forecasts only imply three quarter point hikes over the next three years. So hardly a traditional rate cycle let alone an aggressive one. Initially the sell-off was focused on Government bonds but it spread with a lag of a couple of hours to equities with equity vol spiking again.

Now delving into equities a bit more, US bourses were down c4% yesterday with all sectors in the red and losses led by the financials, tech and discretionary consumer stocks (S&P: -3.75%; Dow -4.15%; Nasdaq -3.90%). Relative to their recent highs two weeks ago, the S&P and Dow are now officially in correction territory with the index down -10.2% and -10.4% respectively, while the Nasdaq is not far behind at -9.7%. European bourses were also lower yesterday, with the Stoxx (-1.60%), DAX (-2.62%) and FTSE (-1.49%) all down.

Over in government bonds, the UST 10 bond yield traded up to 2.882% following a weaker 30y treasury auction but closed -1.2bp lower to 2.825%, in part boosted by the flight to safety that has been absent most of this week. Elsewhere, 10y Bunds yields rose 1.7bp while Gilts rose 6.6bp following the hawkish BOE statements (more below). In credit markets, spreads on IG credit indices widened 4-5bp and the US CDX HY widened 20bp back to December 16 levels. Another focus yesterday was the volatility measures. The VSTOXX jumped c50% to 32.04, now back near the Brexit vote high in 2016 while the VIX traded within a c12pt range before closing c21% higher to 33.46 (+5.7 pt).

This morning in Asia, markets are extending the US sell off. The Nikkei (-2.93%), Hang Seng (-3.56%), Kospi (-1.62%) and China’s CSI 300 (-5.0%) are all down as we type. If these levels hold into close, all indices excluding the Kospi will be down >11% since their recent highs. Datawise, China’s January CPI and PPI both slowed mom but were in line with expectations at 1.5% yoy and 4.3% yoy respectively. In the US, the government may be partially shut down for a few hours. Earlier, Senator Rand argued against the proposed two year spending bill, leaving the Senate to wait till 1am Friday morning (as we go to print) to pass a procedural vote, then the House is expected to pass it sometime between 3am-6am, if not earlier. Elsewhere, the Senate banking committee has narrowly approved (13-12) Trump’s Fed nominee Marvin Goodfriend. His confirmation will now be voted in the full senate where approval may not be certain.

Now recapping other markets performance from yesterday. In currencies, the US dollar index was marginally higher (+0.03%) and rose for the fifth consecutive day, while the Euro dipped 0.14% and Sterling gained 0.23% following the BOE commentaries. In commodities, WTI oil retreated for the fifth straight day to be down 1.04% to $61.15/bbl (-6.6% cumulative). Elsewhere, precious metals strengthened slightly (Gold +0.03%; Silver +0.30%) and other base metals were mixed but little changed (Copper -0.35%; Zinc +0.55%; Aluminium +0.07%).

Turning back to the BOE, as expected the MPC members voted unanimously to keep rates on hold at 0.5%. However the outlook comments seemed more hawkish. The BOE Governor Carney said “it will be likely to be necessary to raise rates to a limited degree in a gradual process but somewhat earlier and…greater extent than what we had thought in November”. A stronger than expected global economy, improving wages and the continuing weak outlook for the UK’s potential supply underpinned the Bank’s more hawkish position. The bank has also upgraded its GDP growth forecasts for 2018 to 1.8% (+0.2ppt) while 2019 was steady at 1.7%. Overall, the meeting was broadly in line with our UK team’s expectations that the MPC would endorse tighter market pricing, without wanting to pre-commit to a May hike. They maintain their view that the BOE will keep rates on hold in May, as they expect demand to slow. For more details, refer to our UK economists’ note. Bloomberg’s implied odds for a May cash rate hike has increased 20ppt to 67%.

Now onto the three Fed speakers overnight. On the recent US equity sell off, similar to their peers, they all seemed to be taking it in their stride. The Fed’s Dudley said “…so far, I’d say this is small potatoes”. The Fed’s Kaplan said “… having a little more volatility, may be a healthy thing”, in part as the recent low volatility was “historically unusual”. Then the Fed’s Harker said “stock market volatility hasn’t changed his economic outlook” and that if you believe the long end of the curve is going up, then “it makes sense that equities would have an adjustment”. That said, he does not think the changes will materially impact business investment and consumer spending.

Moving onto rates and inflation. Mr Dudley noted three rate hikes “still seems like a very reasonable projection” and that “monetary policy around the world is going to become less accommodative”. However, he didn’t put too much weight on the 2.9% yoy wage growth beat last week as it was a single data point and the “question is what’s the trend looking through many months”. Following on, Mr Kaplan noted “my base case right now is the same (3 hikes in 2018)….but it’s a dynamic process”, that is subject to the incoming data and prevailing conditions. He added he “will continue to be vigilant for looking at financial conditions and any spillovers to the economy”, but he is not seeing that at this point. Elsewhere, Mr Harker noted “I’m glad we’re seeing some firming (in inflation)”, but “it’s not obvious that inflation…will absolutely reach our 2% target”, with one of the swing factors being the dollar.

Turning back to the Euro, the ECB’s Weidmann noted “we will monitor closely any impact FX rate movements might have on our primary target of stability”, but should not “allow ourselves to become unsettled by the decline in (the recent) fall in equity prices”. On QE, he reiterated his views that “if the expansion progresses as expected, substantial net purchases beyond the announced amount do not seem to be required”. The ECB’s Praet also noted policy normalisation will be a “long complex” process.

Onto some of the Brexit headlines. Senior EU figures have told Reuters that Britain will not be ready to make a full break from the EU by the end of 2020 and the EU side is bracing for a longer goodbye. Conversely, senior UK officials told Bloomberg that the UK is planning for an instant break from existing EU regulations, such as some rules on financial services to benefit more from Brexit.

Elsewhere, after more talks between the EU and UK counterparts over the past two days, the UK Brexit Secretary Davis said the meeting was “very constructive”, but “…there are still things incomplete”.

Finally, this morning, Michal Jezek in our team published a report “Credit Spread & Vol. Repricing as Equities Go from Melt-Up to Melt-Down”. He reviews the price action in CDS index spreads and their implied volatility during the current market turmoil and shows how their future direction is linked to equity volatility products. The report concludes that the recent vol. shock as a learning event for most market participants is likely to lead to a new, higher regime for both spread levels and their volatility. You can download the report here.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the weekly initial jobless claims (221k vs. 232k expected) and continuing claims (1,923k vs. 1,940k expected) were both moderately lower than expectations – the former is near mid-January’s c44 year low. The January Bank of France industrial sentiment index eased back to a still solid level of 105 (vs. 110 expected). In Germany, the December trade surplus was smaller than expected at €18.2bln (vs. €21bln), with stronger than expected growth in imports (1.4% mom vs. -0.7%) outpacing exports (0.3%). For 2017, Germany’s annual trade surplus fell for the time since 2009, albeit modest (€244.9bln vs. €248.9bln).

Looking at the day ahead, in Europe we get the December industrial production data out of the UK and France, with trade numbers also due in the former, while across the pond in the US the only data of note is December wholesale trade sales. The Fed’s George is also due to speak early morning.

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 132.19 points or 4.05% /Hang Sang CLOSED DOWN 943.85 or 3.10% / The Nikkei closed DOWN 508,24 POINTS OR 2.32%/Australia’s all ordinaires CLOSED DOWN 0.96%/Chinese yuan (ONSHORE) closed UP at 6.3041/Oil DOWN to 60.47 dollars per barrel for WTI and 64.30 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3040. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.3244//ONSHORE YUAN A LOT STRONGER AGAINST THE DOLLAR/OFF SHORE A LOT STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES EXCEPT CHINA YUAN. CHINA IS NOT TOO HAPPY TODAY.(INTERVENTION STRONGER CURRENCY AND WEAK MARKETS IN CHINA AND THROUGHOUT THE GLOBE )

3 a NORTH KOREA/USA

/NORTH KOREA

end

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

Asia crashes: China big cap companies crash over 7%/worst week since Lehman

(courtesy zerohedge)

US Contagion Accelerates – China Big Caps Crash Over 7%, Worst Week Since Lehman

Update 0950ET: Things went from bad to worst very fast…

After an insane winning streak in December and January, the Hang Seng has plummeted in the last few days and along with the rest of the major mainland China equity markets – has entered correction.

2018 started off so well in China…

But after an almost incessant ramp, China and Hong Kong stocks have crashed back to reality in the last few days…

Shanghai Composite is now at 7-month lows…

And Hang Seng is down 12% from its highs, back below 30,000…

The Yuan remains on edge as it tumbles most since the Aug 2015 devaluation…

And across the water, Japanese stocks are down 13% from their highs…

end

4. EUROPEAN AFFAIRS

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia slams the illegal USA presence in Syria

(courtesy zerohedge)

Moscow Slams “Illegal US Presence In Syria” Following Pentagon’s “Defensive” Airstrikes

Moscow lashed out at the US this morning, after the US-led coalition in Syria carried out several “defensive” airstrikes against Syrian forces allied with President Bashar al-Assad on Wednesday in Syria’s Deir al-Zor province – purportedly in retaliation for what the coalition said was an “unprovoked” attack on the US-backed left-wing rebel group.

In response, during a closed door meeting of the UN Security Council in New York, Russian UN ambassador Vasily Nebenzya reminded his colleagues that the US presence in Syria is “actually illegal.” “Nobody invited them there,” Nebenzya stated, emphasizing that the coalition’s actions were jeopardizing the region’s hard-fought stability.

According to the Russian Defense Ministry, the Syrian militia was advancing against a “sleeper cell” of Islamic State terrorists near the former oil processing plant of al-Isba, when the unit was suddenly fired upon by air strikes. At least 25 militiamen were injured in the attack, the Russian Ministry of Defense said, adding that pro-government troops targeted by the coalition did not coordinate their operation with the Russian command.

‘What right does the US have to defend illegal formations in Syria?’ – former US diplomat @JimJatras

The US, however, maintains that the militia attacked the SDF. The Pentagon said Syrian forces moved “in a battalion-sized unit formation, supported by artillery, tanks, multiple-launch rocket systems and mortars.” The battle, which lasted over three hours, according to the US, began after 30 artillery tank rounds landed within 500 meters of the SDF unit’s location, according to RT

“At the start of the unprovoked attack on Syrian Democratic Forces and coalition advisers, coalition aircraft, including F-22A Raptors and MQ-9B Reapers, were overhead providing protective overwatch, defensive counter air and [intelligence, surveillance and reconnaissance] support as they have 24/7 throughout the fight to defeat ISIS,” Air Forces Central Command spokesman Lt. Col. Damien Pickart told Military.com.

“Following a call for support from Air Force Joint Terminal Attack Controllers, a variety of joint aircraft and ground-based artillery responded in defense of our SDF partners, including F-15E Strike Eagles,” he said in a statement Thursday. “These aircraft released multiple precision-fire munitions and conducted strafing runs against the advancing aggressor force, stopping their advance and destroying multiple artillery pieces and tanks.”

As has been the case for years, Damascus called the attack a “war crime,” while Russia’s military asserted that Washington’s true goal is to capture “economic assets” in Syria. The Russian Foreign Ministry spokeswoman Maria Zakharova affirmed that the US military presence in Syria poses a dangerous threat to the political process and territorial integrity of the country, while Foreign Minister Sergey Lavrov called the strike another violation of Syria’s sovereignty by the US.

The US, however, remained unmoved, promising to continue to support the US-allied forces in Syria at any cost.

“We continue to support SDF with respect to defeating ISIS… ISIS is still there, and our mission is still to defeat ISIS,” Pentagon spokeswoman Dana White said Thursday. “We will continue to support them. Our goal is to ensure that our diplomats can negotiate from a position of strength, with respect to the Geneva process.”

“They [US] constantly assert that they are fighting international terrorism there, but we see that they go beyond this framework,” Nebenzya told the UNSC. He warned the US-led coalition members that it is “criminal” to engage the only forces “who actually fight” international terrorism in Syria.

And so the lukewarm proxy war between Syria, Russia and Iran vs the US-coalition and Israel continues apace.

end

6 .GLOBAL ISSUES

Shiller reports on his 20 City Composite. Landlords are having to offer good incentives to bring in renters.

(courtesy Shiller)

Manhattan, London Housing Markets Are Suddenly Reeling

When the latest reading on the Case-Shiller 20-City Composite printed within 1% of its record highs from 2006 a little more than a week ago, we asked a question that’s seemingly on every real-estate investors’ mind: Is this a “top” or a “breakout”?

And with the effects of the Trump tax reform plan – which is expected to hammer real-estate markets, particularly in high-tax blue – having yet to take effect, already states – one early indicator that softness might be entering one of the country’s most iconic (and expensive) real estate markets was reported by Bloombergtoday. To wit, the trend of landlords handing out rental concessions continued to intensify in January, as landlords are increasingly being pressured to hand out incentives like rent-free months or gift cardsto entice potentially renters to sign on the dotted line. Concessions jumped to a record in January, with 49% of newly signed leases coming with some kind of incentive, according to appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate.

That share surpasses the previous peak of 36% set just a month earlier.

All of these concessions have caused the median rent to drop 3.6% from a year earlier to $3,141 – the biggest decline since October 2011 – interrupting six years of near-constant growth.

“Landlords have finally realized, ‘OK, we have to adjust these prices because the concessions aren’t doing as much,'” said Hal Gavzie, who oversees leasing for Douglas Elliman. “Customers are looking past the concessions being offered and just looking for the best deals they can find.”

Rents fell last month in almost every Manhattan neighborhood, including some of the borough’s priciest, Citi Habitats said in its own report. On the Upper West Side, the median was $3,450, down 2.8 percent from a year earlier. Rents in the West Village dropped 4.5 percent to $3,700, while on the Upper East Side, they declined 5.3 percent to $3,185, the brokerage said.

“The dynamic has shifted,” with Brooklyn, Queens and the New Jersey waterfront becoming viable options to many renters,” said Gary Malin, president of Citi Habitats. “Tenants are looking for value, and they’re open to suggestions.”

While these data strictly apply to the rental market, we pointed out last year, the commercial real-estate market is having problems of its own: In September, we noted that sales of commercial real-estate plunged 50%, bringing commercial property purchases to their lowest level since 2012. And that problem isn’t isolated to NYC: Sales of commercial real estate are plunging across the US, and have been since peaking at $262 billion nationally in 2015.

And of course this was before HNA announced this morning that it would be liquidating $4 billion in US commercial real estate across New York City, San Francisco and Chicago and Minneapolis.

* * *

But Manhattan isn’t the only high-end luxury market showing signs of softness. In London, according to the Financial Times, the gap between what sellers are asking and buyers offering for high-end homes is greater than it was in either 2008 or 2009.

But according to one real-estate market analyst, reality is beginning to set in for sellers.

Marcus Dixon, head of research at LonRes, said buyers were becoming more confident in demanding discounts and sellers were ore likely to accept lower offers. “People are going in with relatively cheeky offers, and sellers are accepting them,” said Mr Dixon. “There’s a bit of realism creeping in about what properties are worth.”

LonRes’s data cover London’s most exclusive districts, including Kensington and Chelsea, as well as prime parts of the capital extending from Canary wharf in the east to Richmond in the west and Hampstead in north London.

Outside the most expensive “prime central” areas, discounts to initial asking price stood at just over 9% – the highest level since 2009.

In a phenomenon that’s also manifested in some of America’s toniest zip codes – namely, Greenwich, Connecticut – some sellers are opting to take their homes off the market to wait for another day.