GOLD: $1353.20 UP $0.25

Silver: $16.77 DOWN 7 cents

Closing access prices:

Gold $1348.20

silver: $16.67

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $XXXX DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $XXXX

PREMIUM FIRST FIX: $3.78

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $XXXX

NY GOLD PRICE AT THE EXACT SAME TIME: $1333.50

discount of Shanghai 2nd fix/NY:$1.20

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1358.60

NY PRICING AT THE EXACT SAME TIME: $1359.10

LONDON SECOND GOLD FIX 10 AM: $1352.10

NY PRICING AT THE EXACT SAME TIME. $1352.00

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:1784 FOR 178400 OZ (5.5489 TONNES),

For silver:

FEBRUARY

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 309 for 1,5455,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9768/OFFER $9,838: down $213(morning)

Bitcoin: BID/ $9,974/offer $10,044: DOWN $7 (CLOSING/5 PM)

end

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A GOOD SIZED 2604 contracts from 197,126 RISING TO 199,730 DESPITE YESTERDAY’S 8 CENT LOSS IN SILVER PRICING. WE HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1247 EFP’S FOR MARCH AND AND 0 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1731 CONTRACTS. WITH THE TRANSFER OF 1247 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 1247 CONTRACTS TRANSLATES INTO 6.23 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

38,099 CONTRACTS (FOR 13 TRADING DAYS TOTAL 38,099 CONTRACTS OR 190.495 MILLION OZ: AVERAGE PER DAY: 2930 CONTRACTS OR 14.653 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 190.495 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 27.14% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 438.83 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A GOOD SIZED GAIN IN OI SILVER COMEX WITH THE 8 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1247 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1247 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 3851 OI CONTRACTS i.e. 1247 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2604 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 8 CENTS AND A CLOSING PRICE OF $16.84 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.998 BILLION TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest ROSE BY A GOOD 3,678 CONTRACTS UP TO 532,060 DESPITE THE FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($2.45). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED AN ATMOSPHERIC SIZED 21,324 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 21,324 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 528,382. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 25,002 CONTRACTS: 3,678 OI CONTRACTS INCREASED AT THE COMEX AND A GIGANTIC SIZED 21,324 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(25002 oi gain in CONTRACTS EQUATES TO 77.76 TONNES)

YESTERDAY, WE HAD 22,672 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 152,754 CONTRACTS OR 15,275,400 OZ OR 475.12 TONNES (13 TRADING DAYS AND THUS AVERAGING: 11,750 EFP CONTRACTS PER TRADING DAY OR 1,175,000 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 13 TRADING DAYS: IN TONNES: 475.12 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 475.12/2200 x 100% TONNES = 21.59% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1108.53 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX WITH THE FALL IN PRICE IN GOLD TRADING YESTERDAY ($2.45). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 21,324 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 21,324 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 25,002 contracts ON THE TWO EXCHANGES:

21,324 CONTRACTS MOVE TO LONDON AND 3,678 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 77.76 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $0.25 TODAY, THE CROOKS DECIDED TO RAID THE COOKIE JAR (WITHDREW) 2.36 TONNES OF GOLD FROM THE GLD

Inventory rests tonight: 821.30 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 314.045 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 2604 contracts from 197,126 UP TO 199,730 (AND now A LITTLE FURTHER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FAIR SIZED FALL IN PRICE OF SILVER (8 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1731 PRIVATE EFP’S FOR MARCH AND 0 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2604 CONTRACTS TO THE 1247 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 3851 OPEN INTEREST CONTRACTS . WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 19.255 MILLION OZ!!!

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE FAIR SIZED FALL OF 8 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 1247 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed /Hang Sang CLOSED / The Nikkei closed UP 255.27 POINTS OR 1.19%/Australia’s all ordinaires CLOSED DOWN 0.07%/Chinese yuan (ONSHORE) closed UP at 6.3415/Oil DOWN to 61.36 dollars per barrel for WTI and 64.45 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3415. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.2980//ONSHORE YUAN /OFFSHORE YUAN NOT TRADING

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

i)Troubled HNA has now cut its stake in Deutsche bank. There seems to be a liquidation panic by the company. Their bankruptcy will have far reaching effects throughout the globe.

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

This will no doubt be the end of the Petrodollar scheme. The futures market in Shanghai is set to begin on March 26.2018 where future traders can settle in yuan. There also seems to be an element that if the owners of newbie yuan wish they can convert to gold. This will be watched closely

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The following two commentaries are essential for you to read. Chris Powell comments on Ted Butler’s latest offering discussing the massive buildup of physical silver by JPMorgan. Butler states that it is illegal and manipulative for JPMorgan while being the world’s largest short in silver at the Comex and probably also at the LBMA has accumulated such a hoard of physical silver of which he estimates to be north of 700 million oz.

Chris Powell states that it may be legal if the USA government is behind the acquisition

I believe that JPMorgan is acquiring the metal for sovereign China and that is why the regulators are mum.

I would like to state that even if the government is behind the acquisition they will never admit to their nefarious activities on this front

a must read..

( Ted Butler/ChrisPowell/GATA)

ii)Dave Kranzler thinks that the Fed by adding 18 billion to the system is back to QE. If so the dollar will tank

(courtesy Dave Kranzler/IRD)

iii)Gold rose this week on the dollar collapse coupled with higher inflation

( James Turk/Kingworldnews)

iv)You must hear this interview of Chris Powell explain the cowardice of all our precious metals mining industry save a few

( Chris Powell/Mike Gleason/MME/GATA)

v) This seeking alpha author correctly read the tea leaves on Agnico Eagle while others have not figured it out yet.

(courtesy Peter Arendas/Seeking Alpha)

vi)A first ever fraud charge against a crypto trader

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)Trading early this morning: Inflation is gripping the uSA; it jumped a whopping 1% month over month

( zerohedge)

ii)Another indicator of the economy (inflation) heating up: both housing starts and permits spike and it all came on rental or multi family units

(courtesy zerohedge)

iib)Futures slide badly, the 10 yr bond yield rises as the dollar rebounds

iii)USA consumer confidence (U. of Michigan Consumer Confidence) surges due to tax reform

a)Schiff claims that there is ample evidence of collusion as Bannon was interviewed by Mueller and his team. If so can he show us some specifics

( zerohedge)

b)A good one: Why are Comey’s memos dealing with Trump on supposed obstruction still secret

( Bryon York/Washington Examiner)

( zerohedge)

f)After gaining some composure from laughing so far, Russia finally responds to this absurd election meddling:

( zerohedge)

g)Trump responds: Campaign did nothing wrong..no collusion!!

( zerohedge)

PRELIMINARY COMEX VOLUME FOR TODAY: 141,530 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 299,115 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A GOOD SIZED 2604 CONTRACTS FROM 197,126 UP TO 199,730 DESPITE YESTERDAY’S SMALL SIZED 8 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER GOOD SIZED 1247 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1247. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD NO LONG COMEX SILVER LIQUIDATION BUT A HUGE SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 3851 SILVER OPEN INTEREST CONTRACTS:

2604 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1247 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 3851 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 177 contracts DOWN TO 77 contracts. We had 3 notices filed upon yesterday so we LOST 174 contracts or 870,000 ADDITIONAL oz will NOT stand for delivery at the comex AND THESE LONGS EXITED OUT OF THE COMEX THROUGH THE EFP ROUTE AND RECEIVED A LONDON BASED FORWARD.

The March contract lost 2720 contracts DOWN to 84,583

April GAINED 3 contracts UP to 158 .

.

We had 1 notice(s) filed for 5,000 OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 16/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

6,076.215 oz

Brinks

Scotia

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1153 contracts

(115300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1784 notices

178400 oz

5.5489 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1784) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1153 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 293,700 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1784 x 100 oz or ounces + {(1153)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 293,700 oz standing in this active delivery month of February (9.135 tonnes). THERE IS 12.52 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 13 CONTRACTS OR AN ADDITIONAL 1300 OZ WILL STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 71 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

3922.200 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

742,545.040 oz

JPM

HSBC

|

| No of oz served today (contracts) |

1

CONTRACT(S

(5,000 OZ)

|

| No of oz to be served (notices) |

76 contracts

(380,000 oz)

|

| Total monthly oz silver served (contracts) | 309 contracts

(1,545,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had zero inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 2 inventory deposits into the customer account

i) into J.P.MORGAN:598,412.100 oz ***

ii) Into HSBC: 144,132.940 oz

total inventory deposits: 742,545.040 oz

*** JPMorgan is continually adding to its inventory almost every single day.

JPMorgan now has 134 million oz of total silver inventory or 53% of all official comex silver.

we had 1 withdrawals from the customer account;

iii) Out of Delaware:: 3922.200 oz

total withdrawals; 3922.200 oz

we had 0 adjustment

total dealer silver: 43.827 million

total dealer + customer silver: 253.236 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 1 contract(s) FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 309 x 5,000 oz = 1,545,000 oz to which we add the difference between the open interest for the front month of FEB. (77) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 309(notices served so far)x 5000 oz + OI for front month of FEBRUARY(77) -number of notices served upon today (1)x 5000 oz equals 1,925,000 oz of silver standing for the FEBRUARY contract month.

WE LOST 174 CONTRACTS OR AN ADDITIONAL 870,000 OZ WILL NOT STAND AT THE COMEX AND THEY MORPHED INTO LONDON BASED FORWARDS..THE COMEX IS ONE BIG FARCE!!.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 109,674 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 99,691 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 99,691 CONTRACTS EQUATES TO 498 MILLION OZ OR 71.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.16% (FEB 14/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.34% to NAV (FEB 14/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.16%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.34%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2/99%: NAV 13.98/TRADING 13.51//DISCOUNT 2.99.

END

And now the Gold inventory at the GLD/

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 16/2018/ Inventory rests tonight at 821.30 tonnes

*IN LAST 327 TRADING DAYS: 119.85 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 257 TRADING DAYS: A NET 37.46 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Feb 14/2017:

Inventory 314.045 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.79%

12 Month MM GOFO

+ 2.17%

end

At 3:30 pm est we receive the phony COT report. Since it does not disclose the EFP transfers it is basically a useless report:

but for completeness sake, I will include it:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 251,860 | 76,254 | 64,242 | 150,847 | 345,383 | 466,949 | 485,879 |

| Change from Prior Reporting Period | ||||||

| -21,968 | -6,697 | 3,685 | -7,803 | -18,718 | -26,086 | -21,730 |

| Traders | ||||||

| 172 | 79 | 74 | 44 | 61 | 251 | 183 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 44,796 | 25,866 | 511,745 | ||||

| 2,510 | -1,846 | -23,576 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, February 13, 2018 | |||||

our large speculators

those large specs who are long gold pitched (transferred through EFP’s) a net 21,968 contracts

those large specs who have been short in gold covered (transferred) 6697 contracts from their short side

our commercials

those commercials who have been long in gold pitched (transferred ) a huge 7803 contracts from their long side

those commercials who have been short in gold transferred a huge and net 18,718 contracts from their short side

our small speculators

those small specs who have been long in gold added 2510 contracts to their long side

(they do not participate in the EFP’s)

those small specs who have been short in gold covered 1846 contracts from their short side.

Conclusions;

please do not read the above/the data is totally compromised.

And now for our silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 64,816 | 56,105 | 20,939 | 80,026 | 101,974 | |

| 1,087 | 8,916 | -17,793 | 4,771 | -3,922 | |

| Traders | |||||

| 98 | 60 | 50 | 45 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 194,056 | Long | Short | |

| 28,275 | 15,038 | 165,781 | 179,018 | ||

| 521 | 1,385 | -11,414 | -11,935 | -12,799 | |

| non reportable positions | Positions as of: | 168 | |||

our large speculators

those large specs that have been long in silver added 1087 contracts on a net basis to their long side

those large specs that have been short in silver added 8916 contracts to their short side.

our commercials

those commercials that have been long in silver added 4771 contract to their short side

those commercials that have been short in silver transferred a net 3922 contracts from their short side to London

our small speculators

those small specs that have been long in silver added 521 contracts to their long side

those small specs that have been short in silver added 1385 contracts from their short side

Conclusions

please do not read the above crap!

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

GoldCore

Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

Gold rose as the dollar fell to near a three-year low against a basket of currencies on Friday, heading for its biggest weekly loss in nine months, as a slew of bearish factors including firming inflation and a fall in retail sales and industrial production hit the dollar.

Gold in USD – 10 Years – (GoldCore)

U.S. producer prices accelerated in January, boosted by strong rises in the cost of gasoline and healthcare, offering more evidence that inflation pressures are building. The U.S. producer price index for final demand rose 0.4% last month after being unchanged in December.

In a second U.S. report yesterday, initial claims for state unemployment benefits increased by 7,000 to a seasonally adjusted 230,000 for the week ended February 10. U.S. President Donald Trump’s tax reform may help boost U.S. growth in the short term but could have negative consequences for the U.S. deficit and debt in the medium term, warned International Monetary Fund chief Christine Lagarde yesterday.

Inflation was also surprisingly high in this week’s regional Fed reports, which saw a surge in the Prices Paid index, the clearest indicator of input cost inflation, which in both the Philly and New York reports jumped to 6 year highs.

U.S. industrial production and retail sales were also weaker than expected this week. U.S. retail sales unexpectedly fell sharply in January, recording their biggest drop in nearly a year. Households cut back on purchases of motor vehicles and building materials.

This in conjunction with the high inflation numbers suggests that there is an increasing risk of stagflation taking hold in the U.S.

News and Commentary

Gold set for 4% gain – biggest weekly gain in nearly 2 years (Reuters.com)

Gold holds above $1350 level, closer to 3-week tops (FXStreet.com)

Bitcoin Chops Near $10,000 After Falling From New All-Time Near $20,000 (GoldSeek.com)

U.S. factory output fails to grow for second straight month (Reuters.com)

Wall Street eyes gold as inflation stirs, futures near multi-year highs (CNBC.com)

Barrick Cuts Gold Output Forecast for Eighth Potential Drop (Bloomberg.com)

Inflation Is Picking Up In The US – and There’s More To Come (MoneyWeek.com)

Is the Fed back to ‘quantitative easing’? (InvestmentResearchDynamics.com)

Is the Silver Market Not Manipulated After All? (SilverSeek.com)

The World Embraces Debt At Exactly The Wrong Time (ZeroHedge.com)

Go for gold! Vintage portraits of California prospectors – in pictures (TheGuardian.com)

Gold Prices (LBMA AM)

15 Feb: USD 1,353.70, GBP 962.21 & EUR 1,084.45 per ounce

14 Feb: USD 1,330.75, GBP 959.74 & EUR 1,077.77 per ounce

13 Feb: USD 1,329.40, GBP 955.04 & EUR 1,077.61 per ounce

12 Feb: USD 1,321.70, GBP 955.19 & EUR 1,077.45 per ounce

09 Feb: USD 1,316.05, GBP 945.58 & EUR 1,072.84 per ounce

08 Feb: USD 1,311.05, GBP 944.87 & EUR 1,071.13 per ounce

07 Feb: USD 1,328.50, GBP 956.12 & EUR 1,075.95 per ounce

Silver Prices (LBMA)

15 Feb: USD 16.83, GBP 11.98 & EUR 13.49 per ounce

14 Feb: USD 16.58, GBP 11.97 & EUR 13.43 per ounce

13 Feb: USD 16.61, GBP 11.94 & EUR 13.46 per ounce

12 Feb: USD 16.43, GBP 11.86 & EUR 13.39 per ounce

09 Feb: USD 16.36, GBP 11.83 & EUR 13.37 per ounce

08 Feb: USD 16.35, GBP 11.70 & EUR 13.36 per ounce

07 Feb: USD 16.69, GBP 12.02 & EUR 13.52 per ounce

Recent Market Updates

– Is The Gold Price Heading Higher? IG TV Interview GoldCore

– Global Debt Crisis II Cometh

– Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC

– Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

– “This Is Where They Completely Lost Their Minds” – Hussman

– Brexit Risks Increase – London Property Market and Pound Vulnerable

– Peak Gold: Global Gold Supply Flat In 2017 As China Output Falls By 9%

– Crypto Currency Backlash Sees Flight From Cryptos and Bitcoin

– Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

– Shrinkflation Intensifies – Stealth Inflation As Thousands of Food Products Shrink In Size, Not Price

– U.S. Debt Is “Extraordinarily High” and Are Stock And Bond Bubbles – Greenspan

– Gold Bullion Price Suppression To End? Bullion Bank Traders Arrested For Manipulating Market

– ATMs Hit By Malware “Jackpotting” Attacks That Dispense All Cash In Minutes

END

The following two commentaries are essential for you to read. Chris Powell comments on Ted Butler’s latest offering discussing the massive buildup of physical silver by JPMorgan. Butler states that it is illegal and manipulative for JPMorgan while being the world’s largest short in silver at the Comex and probably also at the LBMA has accumulated such a hoard of physical silver of which he estimates to be north of 700 million oz.

Chris Powell states that it may be legal if the USA government is behind the acquisition

I believe that JPMorgan is acquiring the metal for sovereign China and that is why the regulators are mum.

I would like to state that even if the government is behind the acquisition they will never admit to their nefarious activities on this front

a must read..

(courtesy Ted Butler/ChrisPowell/GATA)

Ted Butler: No manipulation after all?

Submitted by cpowell on Thu, 2018-02-15 15:42. Section: Daily Dispatches

10:46a ET Thursday, February 15, 2018

Dear Friend of GATA and Gold:

Silver market rigging whistleblower Ted Butler today lays out the overwhelming evidence that a single entity long has been rigging the silver market, and then raises the question of why the market regulatory agencies do nothing about it.

Here’s a possible answer: Regulators ignore the market rigging because the entity doing it is acting as agent for the U.S. government, which is fully authorized by federal law, the Gold Reserve Act of 1934 as amended in the 1970s, to intervene secretly in and to rig any market in the world:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

Indeed, at a hearing in November 2001 in U.S. District Court in Boston in GATA’s federal lawsuit against the U.S. government and the Bank for International Settlements, a lawyer for the government essentially conceded as much:

Butler’s commentary is headlined “No Manipulation After All?” and it’s posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/no-manipulation-after-all-17103

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-no-manipulation-after-al…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

No Manipulation, After All?

|

February 15, 2018 – 9:08am

In the never-ending search to either verify or rebut one’s own findings, I’d like you to consider something different today. I’m going to ask you to set aside my highly specific allegations of wrong-doing in the silver and gold markets, mostly centering on JPMorgan, and focus instead on whether if what I allege is really wrong or even matters much. Even though my allegations are based upon data published by the CFTC and CME Group, I would ask you to put that aside and consider that I may have been making a mountain out of a molehill about silver (and gold) price manipulation.

The best way of determining whether there is anything wrong in silver is to do a controlled experiment, namely, by removing it from the equation (along with any mention of JPMorgan) and substitute any other world commodity or entity in its place. In other words, would it be patently and outrageously illegal or no big deal at all if what is transpiring in silver occurred in any other commodity? I’ll present the facts and leave you to be the judge.

Pick any and every commodity with an active futures derivatives market that comes to mind and plugin the facts that are known to have existed in COMEX silver over the past ten years. Any and every commodity – corn, copper, crude oil, no exceptions. Now let’s plug in what we know in terms of facts that exist in silver.

First, we know from COT report data that a single entity has held a consistently large concentrated short position in COMEX silver, larger in terms of actual world production than in any other commodity. We further know that this large entity has always been the largest futures market short in COMEX silver over the entire decade; never flipping to net long. Next we know from COT data that while this uniquely large concentrated short seller has always been net short, its short position has both expanded and contracted regularly over the years and – get this – it has never lost money as it added or bought back short COMEX futures contracts. Never a loss, always only gains, a stunningly perfect trading record. This is determined in silver from observing changes in the concentrated short position of the largest short entity.

Finally we know, from the same source data used in the COT report but published separately in the Bank Participation report, that the dominant short seller in COMEX silver is a large US bank. Although this fact, by itself, wouldn’t be necessarily germane to the question if a manipulation exists or not, it does help tie in other facts.

You should now be envisioning any world commodity that comes to mind having had a single dedicated and dominant futures market short seller who has been consistently short for a decade and who has a perfect trading record – never suffering a loss and only having made profits from the short side. Wouldn’t you be at least a little suspicious that something was wrong or that the market was rigged? Or would the existence of a single large trader, always short and never long or wrong for ten years running in corn, copper or crude oil or any other commodity not bother you at all?

Before you make up your mind, let me add in a few related facts. What if I told you that the same single dominate futures market short seller had spent the last seven years, in addition to maintaining its perfect paper trading as the largest short seller of all, also acquiring a massive physical hoard of the same commodity? And get this – this same paper market dominator had managed to acquire the largest physical stock pile in history of this same commodity.

Wouldn’t the thought cross your mind that maybe this big entity was milking this particular commodity in an underhanded manner, not only achieving the first perfect trading record ever and then taking advantage of the overall lower prices its massive short selling caused by buying all it could of the same commodity in a different form? Wouldn’t this sound like the perfect commodity price manipulation, namely, the manipulator making on both sides, milking the paper side and then using its price influence to buy the physical side in massive quantities and at depressed prices?

But wait, there’s more. What if I told you that there was a federal regulator, as well as a self-regulating entity in existence, in the form of the CFTC and the CME Group, who were specifically mandated with preventing such a scheme as I just outlined as their primary mission? Neither regulator has said anything about any of this for ten years, although the CFTC closed a formal five-year investigation into silver manipulation in 2013, which was inconclusive to say the least. Oh, and the financial institution identified as the big silver manipulator, JPMorgan, hasn’t said a peep about being publicly accused of criminal wrongdoing. Most usually, financial institutions are interested in maintaining the highest reputation possible and immediately address any issues contrary to their best interest. Not so with JPMorgan and silver.

So, you make the call. If the facts that are known to exist in silver were present in any other commodity, would this constitute manipulation in your opinion? Or if the facts were sufficient enough so as to require the CFTC, the CME, and JPMorgan to at least try to explain why manipulation wouldn’t exist in silver, given the verifiable facts? You might want to remember this the next time someone declares that no manipulation exists in silver or even better, that all markets are manipulated, so who cares? Just ask them which market features the largest paper short who also happens to be the largest physical buyer of that same commodity?

Ted Butler

February 15, 201

END

Finally, we hear from Bart: The Whistleblower’s allegation of VIX manipulation rings true.

Strange,we have been harping on the commission for years on this issue

(courtesy http://www.hitc.com/GATA)

Former CFTC commissioner: Whistleblower allegation about volatility index manipulation ‘rings true’

The VIX, often called the market’s fear index, has been “suspect for at least seven years,” says Bart Chilton, former CFTC commissioner.

The allegation by a whistleblower , in a letter to the Securities and Exchange Commission , of potential manipulation of the VIX, a key gauge of market fear and volatility, “rings true,” a former market regulator told CNBC on Wednesday.

Formally called the CBOE Volatility Index, the VIX measures market expectations of near-term volatility conveyed by S&P 500 stock index option prices.

“The VIX has been suspect for at least seven years,” said Bart Chilton, former commissioner of the Commodities Futures Trading Commission. The CFTC aims to protect market participants from fraud, manipulation, and abusive practices related to financial derivatives such as futures and options. “People have been concerned about prices being pushed around. Although, there’s never been any hard evidence,” he said.

-END-

You must hear this interview of Chris Powell explain the cowardice of all our precious metals mining industry save a few

(courtesy Chris Powell/Mike Gleason/MME/GATA)

(GATA)GATA secretary explains cowardice of gold mining industry, financial news media

Submitted by cpowell on 05:52PM ET Friday, February 16, 2018. Section: Daily Dispatches

12:50p ET Friday, February 16, 2018

Dear Friend of GATA and Gold:

Interviewed this week by Mike Gleason of Money Metals Exchange, your secretary/treasurer explained why most monetary metals mining companies are too scared to protest government’s suppression of the price of their products. That is, the industry is too vulnerable to government regulation and utterly dependent for financing by the major investment banks that are formally government agents.

Mainstream financial news organizations, your secretary/treasurer adds, won’t report the market rigging because governments consider it a national security issue.

But, he continues, the documentation of this market rigging is all over the place, including the internet site of the Bank for International Settlements, the broker for central bank intervention in the gold market.

The interview is 20 minutes long and can be heard and read at the Money Metals Exchange internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Dave Kranzler thinks that the Fed by adding 18 billion to the system is back to QE. If so the dollar will tank

(courtesy Dave Kranzler/IRD)

Dave Kranzler: Is the Fed back to ‘quantitative easing’?

Submitted by cpowell on Thu, 2018-02-15 23:13. Section: Daily Dispatches

By Dave Kranzler

Investment Research Dynamics, Denver

Thursday, February 15, 2018

The Federal Reserve added $11 billion to its System Open Market Account account for the week ending yesterday. It purchased $11 billion in mortgage securities directly from banks.

This injects $11 billion into the banking system. Cash is “high-powered” money — it can be leveraged 10 times (banks need to hold 10 percent in reserves against “high-powered” money. Eleven billion dollars is $110 billion of leverage for the banks to use for activities such as propping up the stock market.

This certainly explains why there appears to be another “V” recovery in the stock market after a near-10-percent drawdown in the Dow and the SPX. This is very similar to the 10-percent market plunges in August 2015 and January 2016, both of which were followed with highly unusual “V” recoveries. …

… For the remainder of the report:

http://investmentresearchdynamics.com/is-the-fed-back-to-quantitative-ea…

END

Gold rose this week on the dollar collapse coupled with higher inflation

(courtesy James Turk/Kingworldnews)

Gold defied expectations to rise on inflation report, Turk says

Submitted by cpowell on Fri, 2018-02-16 00:14. Section: Daily Dispatches

7:14p ET Thursday, February 15, 2018

Dear Friend of GATA and Gold:

Interviewed by King World News, GoldMoney founder and GATA consultant James Turk says gold’s sharp increase Tuesday on a day when it was supposed to lose no matter which way the government’s inflation report went suggests that the shorts are in serious trouble. Turk’s interview is posted at KWN here:

https://kingworldnews.com/james-turk-this-is-what-really-triggered-the-m…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A first ever fraud charge against a crypto trader

(courtesy zerohedge)

Federal Prosecutors File First-Ever Fraud Charges Against Crypto Trader

The nearly 10-year-old cryptocurrency space has reached one of the more ignominious milestones to date.

Several months after the SEC filed the first civil fraud action against an ICO founder who was believed to have stolen money from investors, US prosecutors are sending a message to the community by filing the first case of a criminal fraud prosecution in blockchain history, according to federal prosecutors in Chicago.

Prosecutors are expected to outline the charge that “from September through November 2017, Kim transferred more than $2 million of the trading firm’s Bitcoin and Litecoin to personal accounts to cover his own trading losses, which had been incurred while trading cryptocurrency futures on foreign exchanges.”

But unlike the previous civil actions, the criminal case involves an employee at a blockchain startup who stole from his employer to fund a severe gambling problem, according to ABC 7.

According to a local Chicago television station, a 24-year-old trader named Joseph Kim considered himself “invincible” according to federal investigators. The trader was charged after allegedly siphoning $2 million in bitcoin and litecoin away from his Chicago-based employer.

Kim, who’s biography identifies him as a 2016 graduate of University of Chicago, is charged with fraud against Consolidated Trading LLC. Kim illegally transferred the firm’s cryptocurrency to his own personal accounts, according to federal investigators, to cover trading losses.

The Korean-American then lied about the transfers and tried to cover up the illegal trades by repaying some of the funds, prosecutors claim.

According to a federal complaint, Kim referred to himself as “DEGEN”, short for “degenerative gambler.”

In an email to his bosses last November, Kim allegedly admitted to the scheme. “It was not my intention to steal for myself” he is quoted as writing. “Until the end I was perversely trying to fix what I had already done.”

“I can’t believe I did not stop myself when I had the money to give back, and I will live with that for the rest of my life,” he said, according to prosecutors.

Kim was hired as a trader in July 2016. In an email last November to the firm’s top executives authorities say Kim apologized and said he was “sorry to betray you all like this.”

Yet it was Consolidated’s management team that discovered the misappropriation.

Kim made his initial court appearance on Friday at 10:30 am before Magistrate Judge Daniel G. Martin at the Dirksen Federal Building.

end

This seeking alpha author correctly read the tea leaves on Agnico Eagle while others have not figured it out yet.

(courtesy Peter Arendas/Seeking Alpha)

Agnico Eagle Is Flying High

Summary

Agnico Eagle Mines set a new gold production record in 2017.

The 2018 and 2019 production guidance was improved slightly.

In 2020, Agnico should produce more than 2 million toz gold.

The debt is well under control and the company expects to raise dividends after the Amaruq and Meliadine mines are completed.

If everything goes well, the $60 share price level may be crossed over the next two years.

Agnico Eagle Mines (AEM) recorded great results in 2017. It confirmed its ability to grow production while keeping the costs low, especially when compared to the other major gold miners. It was also Agnico’s 6th consecutive year when it was able to beat its production guidance. Agnico is up by more than 50% over the last 2 years and although it has been moving sideways over the last 12 months, the company is in a good shape and it’s primed for a significant growth over the next two years.

AEM data by YCharts

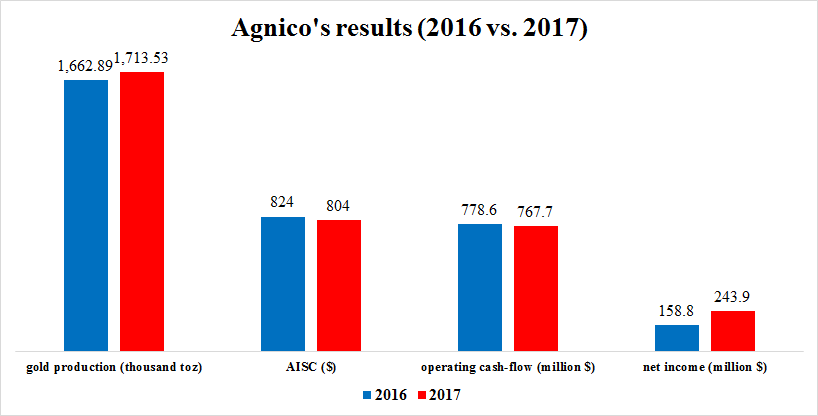

AEM data by YChartsIn 2017, Agnico Eagle Mines produced 1,713,533 toz. gold, at an AISC of $804/toz. It compares favorably to the recent guidance of 1.68 million toz. gold at an AISC of $845/toz. Compared to 2016, the gold production increased by 3.05%. The operating cash-flow climbed to $767.6 million, which is in line with 2016. The development capital expenses equaled $575 million and the free-cash-flow remained positive despite the extensive development activities. However, as the management has stated, in 2018 and H1 2019, the free-cash-flow will be negative, as the development CAPEX should climb to $1.08 billion in 2018 alone. The 2017 net income equaled $243.9 million, or $1.06 per share. It represents a 53.6% growth compared to 2016. The total cash costs declined to $558/toz., which is 2.6% better than in 2016. The AISC declined by 2.4%, to $804/toz.

Source: own processing, using data of Agnico Eagle Mines

Source: own processing, using data of Agnico Eagle Mines

As of December 31, Agnico Eagle Mines held cash & cash equivalents worth $643.9 million. Moreover, it had also credit lines of approximately $1.2 billion at its disposal. The news release also announced that in Q1 2018, notes worth $350 million, bearing an average interest of 4.75%, should be issued. Together with the cash-flow, Agnico should be more than sufficiently financed for the projected near-term growth.

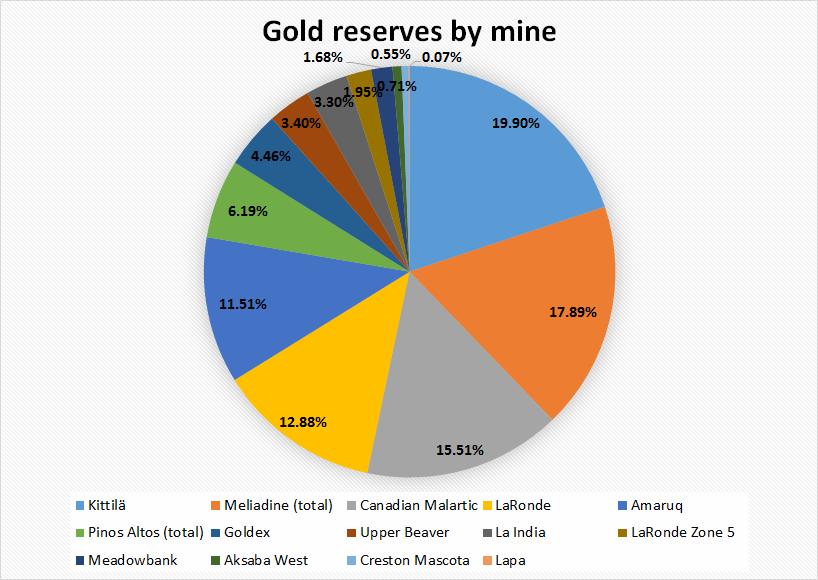

Another very positive news is, that although Agnico Eagle set a new gold production record, it was able to grow its gold reserves by 3.1%, to 20.6 million toz. The biggest reserves are at Kittilä (4.09 million toz. gold, 4.74 g/t), Meliadine (3.677 million toz. gold, 7.12 g/t) and Canadian Malartic (3.189 million toz. gold, 1.1 g/t).

Source: own processing, using data of Agnico Eagle Mines

Source: own processing, using data of Agnico Eagle Mines

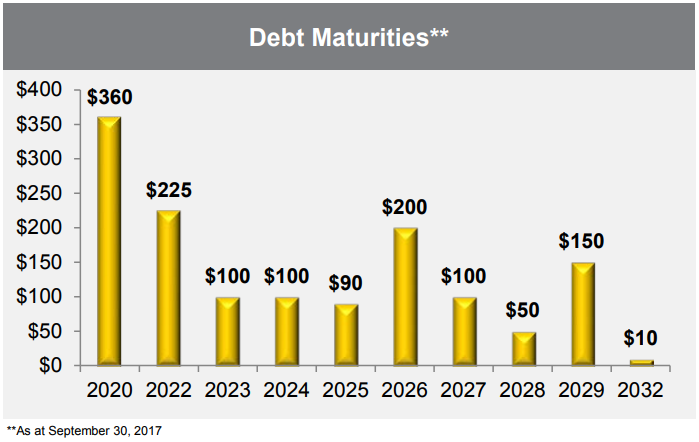

Also Agnico’s debt situation is well under control. As of the end of 2017, the long-term debt equaled $1.37 billion. It means that the long-term debt to operating cash-flow ratio stands only at 1.78. Moreover, the maturities are well manageable. The first portion of the debt ($360 million) matures in 2020. Another $225 million is due in 2022. The rest of maturities is spread over the 2023-2032 period and it is never more than $200 million per year. Source: Agnico Eagle Mines

Source: Agnico Eagle Mines

The near-term growth prospects

The near-term prospects of Agnico Eagle Mines are very good. Although a slight decline in the production volumes is expected in 2018 (from 1.71 million toz. in 2017 to 1.53 million toz, or by 10.5%), in 2019 it should grow back to 1.7 million toz. and in 2020, the 2 million toz. per year level should be reached. The production growth should be fueled especially by the Amaruq and Meliadine projects, which should start gold production in 2019.

The Amaruq project is located in Canadian Nunavut territory. According to Agnico Eagle Mines, the deposit consists of multiple gold-bearing sulphide-rich lenses. It was discovered in 2013 and according to the December 2017 resource estimate, the proposed open pit contains reserves of 2.366 million toz. gold, at a gold grade of 3.67 g/t. It contains also measured & indicated resources of 720,000 toz. gold, at a gold grade of 3.15 g/t and inferred resources of 135,000 toz. gold at a gold grade of 4.3 g/t. Moreover, besides the open pit, there is potential also for an underground operation. The underground part of the deposit contains measured & indicated resources of 301,000 toz. gold at a gold grade of 5.64 g/t and inferred resources of 1.609 million toz. gold, at a gold grade of 6.5 g/t. Ore from Amaruq should be processed at the Meadowbank mill. The development of the open pit is underway and the final permits are expected by the end of Q3. According to Agnico’s corporate presentation, Amaruq should produce 162,500 toz. gold in 2019 and 265,000 toz. gold in 2020. The AISC is estimated at $850/toz, over the mine life.

Just like Amaruq, also the Meliadine project is located in Nunavut. The open pit portion of the deposit contains reserves of 628,000 toz. gold at a gold grade of 5.22 g/t and the underground portion of the deposit contains reserves of 3.05 million toz. gold at a gold grade of 7.7 g/t. The open pit contains also measured & indicated resources of 1.166 million toz. gold, at a gold grade of 3.46 g/t and inferred resources of 133,000 toz. gold at a gold grade of 4.56 g/t. The underground portion of the deposit contains measured & indicated resources of 1.901 million toz. gold, at a gold grade of 4 g/t and inferred resources of 2.533 million toz. gold at a gold grade of 6.14 g/t. The development of the underground operation and facilities is underway, with a production start-up projected for 2019. The gold production should reach the 170,000 toz. gold level in 2019 and 385,000 toz. gold level in 2020. In years 2 through 12, the average annual production should equal approximately 400,000 toz. gold. The life of mine AISC is estimated at $720/toz.

Conclusion

Agnico Eagle Mines is in a good shape which was confirmed also by the 2017 results. The company is able to generate a lot of cash at the current gold prices and its cash-generating ability is poised to grow further, as its gold production should increase to 2 million toz. gold per year by 2020. As stated in the recent news release, after the Amaruq and Meliadine projects are completed (in the middle of 2019), the free-cash-flow should grow notably, which should be reflected also by higher dividend payments. Right now, the dividend stands at $0.11 per quarter and at the current share price of $45.1, the dividend yield equals slightly less than 1%. If there are no negative surprises and the gold price stays at least at the current levels, it is reasonable to expect Agnico Eagle’s shares to retest the summer 2016 highs at $60 over the next two years.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED /shanghai bourse CLOSED / HANG SANG CLOSED

2. Nikkei closed UP 255.27 POINTS OR 1.19% /USA: YEN RISES TO 106.29/DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 88.73/Euro FALLS TO 1.2466

3b Japan 10 year bond yield: FALLS TO . +.059/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.29/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.36 and Brent: 64.45

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.740%/Italian 10 yr bond yield DOWN to 2.016% /SPAIN 10 YR BOND YIELD DOWN TO 1.479%

3j Greek 10 year bond yield FALLS TO : 4.27?????????????????

3k Gold at $1355.80 silver at:16.82 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 6/100 in roubles/dollar) 56.46

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.29 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9243 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1527 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.740%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.889% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.141% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Violent Dollar Swings Fail To Stop Futures Levitation, Best Week For Stocks Since 2011

Global stocks were set to post their best week of gains in six years on Friday after two consecutive weeks spent in the red, shrugging off a rise in global borrowing costs while the dollar hit its lowest level since 2014. The MSCI world index rose 0.4% after European bourses opened. .After suffering its biggest weekly drop since August 2015 last week, this week’s recovery puts the index on track for its best weekly showing since early December 2011.

As Deutsche Bank notes, “The S&P 500 (+1.21%) rose for the 5th day and is now up +2.15% YTD which on a compounded annualised basis is c18.5%!! On this basis the NASDAQ (+1.58% yesterday, +5.11% YTD) is up c49.5% on an annualised basis.“

As Reuters notes, investors remain puzzled at this week’s quick rebound in stock markets, which has also coincided with a rise in bond yields on evidence that inflation is starting to creep up globally. The most frequent argument offered by economists has been that historically, it’s not unusual for stocks and bond market borrowing costs to rise in tandem with a rapidly expanding economy.

“For me it’s really a question of maybe. Markets are taking a look at the inflationary outlook and saying OK, maybe rates are going up and maybe the economy will compensate for that,” said Michael Hewson, chief markets analyst at CMC Markets. “That might change if we move to 3 percent on the 10-year (Treasury).”

In an especially quiet and illiquid overnight session, with most of Asia on holiday celebrating the Lunar New Year, FX traders saw fireworks in the latest violent lunges of the dollar, and especially the USDJPY, which tumbled as low as 105.55, taking out perimeter stops, and sending the pair to a fresh 15 month low, as the market shrugged off the widely-expected nomination of Haruhiko Kuroda (translation: no change to the BOJ’s policy) for another term as the BOJ governor, while Japanese stocks closed 1.2% higher, ignoring the spike in the yen.

While Japan closed higher, and Australia slightly lower, most major markets across Asia Pacific shut for Lunar New Year holidays, volumes in the region were light. What markets were open, were broadly in the green this morning…

… with European stocks emerging from the shadow of a global selloff rose further on Friday, extending their biggest weekly gain in more than a year. The Stoxx Europe 600 Index rises 0.8%, with energy shares leading a broad rebound. This morning’s equity newsflow has been largely dominated by a busy slate of earnings from the likes

of Renault (+3.1%), Eni (+1.5%), Allianz (-0.7%) and Vivendi (-5.8%) which have provided a bulk of the focus for traders thus far. Elsewhere, Vopak jumped after saying it has the potential to “significantly improve” its 2019 Ebitda, while Vivendi tumbled after posting earnings and confirming trends previously reported in January.

Over in the US, U.S. stock index futures rose, although were off session highs, signaling further gains on Wall Street as global equities continue to recover and bond yields fall back from recent peaks. So far in the rebound, the S&P 500 has recouped more than 50% of the losses suffered in the latest correction, the index is back above its 50-DMA and technical breadth is rising.

Bit the biggest mover so far was the dollar came under early pressure as the Lunar New Year kept liquidity below average, as greenback sellers found limited resistance in pushing the currency lower before a long weekend in the U.S. In the process, the euro hit a fresh three-year high, while the yen seems determined to check barrier defense at 105.00. However shortly after the European open, the mood reversed completely, and the dollar saw a strong bid amid what some speculated was a broad round of dollar short covering, sending the BBG dollar index to session highs.

There is no strong consensus yet on what is driving the dollar’s persistent weakness, especially in light of rising yields. Some say it simply reflects a return of risk appetite and a shift to higher-yielding currencies, including many emerging market ones. But others cite concerns that Washington might pursue a weak dollar strategy as well as talk that foreign central banks may be reallocating their reserves out of the dollar. There are also worries President Donald Trump’s tax cuts and fiscal spending could stoke inflation and erode the value of the dollar.

“His protectionist policies could also fan inflation. Markets appear to have calmed down for now but fundamentally it is different from last year,” said Yoshinori Shigemi, global market strategist at JPMorgan Asset Management. “You could say that right now, rather than stocks rising around the world, it is the dollar falling against almost everything,” he added.

Benchmark Treasury yields halted their surge at around 2.9% and the dollar paused after falling to a three-year low against major peers. Failing to break above 2.90%, the yield on the 10Y Treasury has instead tested the downside, and was currently trading just north of 2.88%, which has proven a support level over the past 48 hours.

Even with borrowing costs on the rise, investors seem once again unconvinced they’re not yet at levels that would hinder equities as economic growth accelerates. While a larger number of economists forecast the Federal Reserve to step up its pace of interest-rate increases, that’s not helping the greenback, and as Bloomberg again highlights, the U.S.’s twin deficits have become a likely catalyst for a renewed wave of dollar-selling after February’s brief rally.

In other news, the White House urged the House to advance the Goodlatte immigration proposal after 4 bills were defeated in the Senate. Former Trump campaign adviser Gates is said to be nearing a plea deal with Special Counsel Mueller with negotiations having taken around a month already. The UK’s IOD has put forward a bespoke Brexit solution which it believes will protect manufacturers from customs chaos but also allow the UK to strike independent trade deals. UK Retail Sales disappointed, rising on 0.1 M/M% vs. Exp. 0.5%.

Elsewhere, crude oil rose to a one-week high as the greenback’s slump increased the appeal of dollar-priced commodities. Bitcoin pared earlier gains, failing to hold above $10,000, while South Africa’s rand held near a three-year high as newly elected President Cyril Ramaphosa prepares to deliver his state-of-the-nation speech Friday.

On today’s calendar, expected data include housing starts, building permits and University of Michigan Consumer Sentiment Index. Coca-Cola, Deere, Kraft Heinz and Air Canada are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.4% to 2,745.50

- STOXX Europe 600 up 0.8% to 379.55

- MXAP up 0.7% to 177.20

- MXAPJ up 0.4% to 579.63

- Nikkei up 1.2% to 21,720.25

- Topix up 1.1% to 1,737.37

- Sensex down 0.9% to 34,001.42

- Australia S&P/ASX 200 down 0.08% to 5,904.04

- Kospi up 1.1% to 2,421.83

- German 10Y yield fell 2.0 bps to 0.744%

- Euro up 0.2% to $1.2531

- Italian 10Y yield unchanged at 1.796%

- Spanish 10Y yield fell 2.8 bps to 1.479%

- Brent futures up 0.5% to $64.62/bbl

- Gold spot up 0.5% to $1,360.00

- U.S. Dollar Index down 0.1% to 88.47

Top overnight news

- Prime Minister Shinzo Abe nominated Haruhiko Kuroda to lead the Bank of Japan for another five-year term, with the Cabinet forwarding the nomination to parliament on Friday

- The U.S. Senate blocked four immigration proposals Thursday, deepening a bitter impasse over how to protect 1.8 million young undocumented immigrants from deportation

- U.K. is ready to set out its vision of how it wants financial services to operate after Brexit and favors “mutual recognition” of regulations to preserve the City of London’s access to the EU, FT reports, citing three unidentified senior figures briefed on Brexit discussions in the cabinet

- Brexit talks are currently not headed to a disorderly exit, EU’s Chief Brexit negotiator Michel Barnier says at Munich Security Conference

- Britain should aim for a partial customs union with the EU once it quits the bloc, according to the Institute of Directors

- PIMCO had about $15 billion of third-party inflows in January as the bond manager owned by Allianz SE was allocated money by retail and institutional investors in Asia and the U.S., Chief Financial Officer Giulio Terzariol said in a Bloomberg TV interview on Friday

Stock markets were quiet in Asia with most the region away for Lunar New Year holiday, while the few bourses which were open seemed to have joined in on the celebratory tone and initially took impetus from a 5th consecutive win streak on Wall St. As such, ASX 200 (-0.1%) was positive for most the day with earnings in focus, although upside was capped and later reversed amid profit taking in mining-related sectors. Nikkei 225 (+1.2%) continued to defy the recent JPY strength and outperformed as participants widely anticipated the Japanese government nominations for Kuroda to serve a 2nd term and 2 more doves for the Deputy Governor roles, while markets in China, Hong Kong, Taiwan and Singapore were among the mass holiday closures. Finally, 10yr JGBs were higher as Japanese yields retreated across the curve and which also followed the gains in USTs during the prior session, while the enhanced liquidity auction for longer-dated bonds failed to impact prices with the results broadly in line with the prior.

Japan submitted nomination for BoJ Governor Kuroda to stay on for another term, while it also nominated reflationist academic Wakatabe and BoJ’s Amamiya as Deputy Governors.

Top Asian News

- Kuroda Nominated for Another Term as BOJ Governor

- One of India’s Richest Men Allegedly Executed a $2 Billion Fraud

- Ex-Lehman Banker Sees Gold Mine in India Bankruptcy Overhaul

- India Stocks Fall as Deficit, Bank Fraud Weigh on Sentiment

- Top China Lithium Producer to Extend Deal Spree with Listing

European equities (Eurostoxx 50 +0.9%) trade higher across the board after what was another firm close on Wall Street (S&P 500 +1.2%). All ten sectors trade in positive territory with outperformance in utility names following stellar earnings from EDF (+6.2%), subsequently dragging other names in the space higher. Elsewhere, energy names are performing well as prices remain supported by the softer USD. This morning’s equity newsflow has been largely dominated by a busy slate of earnings from the likes of Renault (+3.1%), Eni (+1.5%), Allianz (-0.7%) and Vivendi (-5.8%) which have provided a bulk of the focus for traders thus far.

Top European News

- EDF Sees Profit Rebounding This Year as Power Prices Recover

- U.K. Retail Sales Barely Grow as Consumers Subdued by Inflation

- Saab Plunges After Failing to Live Up to Lowest Profit Estimates

- Eni Boosts Production to Record as Profit Beats Estimates

- Renault’s Ghosn Pledges ‘Irreversible’ Alliance With Nissan

- Africa’s Richest Man Is Said to Revive Dangote Cement London IPO

In currencies, the Yen’s flight continues to compound the Dollar’s plight amongst G10 majors, but the Greenback remains a broader loser as EM currencies and commodities also prosper amidst the latest Usd sell-off. The DXY only just held above major Fib support at 88.250 overnight as Usd/Jpy selling eased up ahead of 105.50. However, only mild verbal acknowledgment of the largely one-way tide from Japanese officials, and no mention of intervention inspired a tame or token rebound to around 106.00 before the slide resumed. The Aud and Nzd are now looking at 0.8000 and 0.7450 vs their US counterpart, while the Eur has eclipsed its previous 2018 peak to trade just above 1.2550 and a few pips over the 1.2551 100 MMA having surpassed the 200 version (1.2453) on the way. Stops are said to waiting on a break of 1.2570, ahead of the next upside tech target at 1.2598, but a decent 1.2550 option expiry (1 bn) may keep the pair in check. Cable has now advanced through 1.4100 and almost hit 1.4144, with price action relatively contained following this morning’s below-expectation UK retail sales release. Usd/Chf is seriously testing the 0.9200 handle, with 0.9175 in sight. Japan’s Chief Govt. spokesman said the FX market has shown one-sided moves recently. He added no need to change government stance on FX however no comments were added on whether appropriate measures include FX intervention.

In commodities, WTI and Brent crude futures continue to benefit from the softer USD with prices eyeing USD 62.00bbl and USD 65.00bbl to the upside respectively despite forecasts for a continuation of surging US production and a slew of markets currently shut in Asia; Baker Hughes set to take focus in the latter stages of the session. In metals markets, gold is on course for its largest percentage rise in two years as the softer USD and buying ahead of the Chinese Lunar New year dictated a bulk of the price action. Elsewhere, copper has also benefited from the aforementioned currency swings and global manufacturing picture with prices on track for their largest gain in over a year.

Looking at the day ahead, there is January retail sales data in the UK this morning. In the US, the January import price index, housing starts and building permits along with the preliminary February University of Michigan consumer sentiment reading are also due. Elsewhere, the ECB’s Coeure will speak and Coca- Cola and Kraft Heinz will report their earnings.

US Event Calendar

- 8:30am: Import Price Index MoM, est. 0.6%, prior 0.1%; YoY, est. 2.95%, prior 3.0%

- 8:30am: Export Price Index MoM, est. 0.3%, prior -0.1%; YoY, prior 2.6%

- 8:30am: Housing Starts, est. 1.23m, prior 1.19m; MoM, est. 3.52%, prior -8.2%

- 8:30am: Building Permits, est. 1.3m, prior 1.3m; MoM, est. 0.0%, prior -0.1%

- 10am: U. of Mich. Sentiment, est. 95.4, prior 95.7; Conditions, est. 111.1, prior 110.5; Expectations, est. 87.2, prior 86.3

DB’s Jim Reid concludes the overnight wrap

Another day, another higher inflation print largely ignored by the market. This time it was US core PPI that beat (0.4% mom vs 0.2% expected). As DB’s Matt Luzzetti highlighted the standout in the report was an incredibly strong reading for health care PPI, which is used to estimate the health care component of the PCE price index – the Fed’s favoured gauge. Health care PPI was up 0.68% m/m on a seasonally adjusted basis, the strongest print since the first reading of this series in Jan 2007. The data implies a sharp jump in the yoy rate for health care PCE inflation from about 1.5% to 2.2%. Matt went onto say that Wednesday’s CPI data and yesterday’s health care PPI data are consistent with a very strong core PCE print for January (+0.3% m/m), which would lift the 3m and 6m annualized inflation rate above 2%. So the inflation narrative builds and builds. This story and its’ impact on markets won’t go away in our opinion and we might just be ignoring it as we normalise from last week’s shock.

The S&P 500 (+1.21%) rose for the 5th day and is now up +2.15% YTD which on a compounded annualised basis is c18.5%!! On this basis the NASDAQ (+1.58% yesterday, +5.11% YTD) is up c49.5% on an annualised basis. Within the S&P, all sectors but energy rose, with gains led by the utilities and tech stocks. The VIX (-0.67%) fell for the 5th day and closed at 19.13.