GOLD: $1329.05 DOWN $24.15

Silver: $16.48 DOWN 29 cents

Closing access prices:

Gold $1330.20

silver: $16.46

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $XXXX DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $XXXX

PREMIUM FIRST FIX: $xxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $XXXX

NY GOLD PRICE AT THE EXACT SAME TIME: $xxx

discount of Shanghai 2nd fix/NY:$

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1337.40

NY PRICING AT THE EXACT SAME TIME: $1337.65

LONDON SECOND GOLD FIX 10 AM: $1339.85

NY PRICING AT THE EXACT SAME TIME. $1340.30

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:1784 FOR 178400 OZ (5.5489 TONNES),

For silver:

FEBRUARY

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 310 for 1,550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $11,443/OFFER $11,514: UP $319(morning)

Bitcoin: BID/ $11,651/offer $11,722: UP $526 (CLOSING/5 PM)

end

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY SIZED 122 contracts from 199,730 RISING TO 199,852 DESPITE FRIDAY’S 7 CENT LOSS IN SILVER PRICING. WE HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 849 EFP’S FOR MARCH AND AND 0 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 849 CONTRACTS. WITH THE TRANSFER OF 849 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 849 CONTRACTS TRANSLATES INTO 4.245 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

38,948 CONTRACTS (FOR 14 TRADING DAYS TOTAL 38,948 CONTRACTS OR 194.740 MILLION OZ: AVERAGE PER DAY: 2782 CONTRACTS OR 13.910 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 194.74 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 27.81% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 443.08 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A TINY SIZED GAIN IN OI SILVER COMEX DESPITE THE 7 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1247 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 849 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 971 OI CONTRACTS i.e. 849 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 122 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 7 CENTS AND A CLOSING PRICE OF $16.77 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0001 BILLION TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest ROSE BY A GOOD 4,015 CONTRACTS UP TO 536,075 DESPITE THE SLIGHT RISE IN PRICE OF GOLD WITH FRIDAY’S TRADING ($0.25). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TUESDAY AND IT TOTALED AN GOOD SIZED 6,334 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 6334 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 536,075. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 10,349 CONTRACTS: 4015 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 6334 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(10,349 oi gain in CONTRACTS EQUATES TO 32.18 TONNES)

FRIDAY, WE HAD 21,324 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 159,088 CONTRACTS OR 15,908,800 OZ OR 494.83 TONNES (14 TRADING DAYS AND THUS AVERAGING: 11,363 EFP CONTRACTS PER TRADING DAY OR 1,136,300 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 14 TRADING DAYS: IN TONNES: 494.83 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 494.83/2200 x 100% TONNES = 22.49% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1128.23 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX WITH THE SLIGHT RISE IN PRICE IN GOLD TRADING FRIDAY ($0.25). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6334 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6334 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 10,349 contracts ON THE TWO EXCHANGES:

6334 CONTRACTS MOVE TO LONDON AND 4015 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 32.18 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $24.15 TODAY, THE CROOKS DECIDED TO DEPOSIT 3.34 TONNES OF GOLD INTO THE GLD

Inventory rests tonight: 824.64 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 314.045 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A TINY 122 contracts from 199,730 UP TO 199,852 (AND now A LITTLE FURTHER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FAIR SIZED FALL IN PRICE OF SILVER (7 CENTS WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 849 PRIVATE EFP’S FOR MARCH AND 0 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 122 CONTRACTS TO THE 849 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 971 OPEN INTEREST CONTRACTS . WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 4.855 MILLION OZ!!!

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FAIR SIZED FALL OF 7 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 849 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed /Hang Sang CLOSED / The Nikkei closed DOWN 224.11 POINTS OR 1.01%/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed UP at 6.3415/Oil DOWN to 62.03 dollars per barrel for WTI and 65.23 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED XXX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED XXX AGAINST THE ONSHORE YUAN AT XXX//ONSHORE YUAN /OFFSHORE YUAN NOT TRADING

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

i)Deutsche bank/Germany

More trouble on the horizon for the world’s biggest derivative player. They seem to be leaning on firing 500 of their workers due to tumbling trading revenues

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SaturdayTurkish forces hit the Kurds with toxic gas after crossing into Syria

( zerohedge)

ii)The Gatestone’s Institute , Bulut comments that relations between Greece and Turkey have soured. Emboldened by its attack on Afrin, it seems that Turkey may wish to attack many Greek islands. Turkey is trying to reassert itself to its former glory days of its powerhouse Ottoman Empire.

( Bulut/Gatestone Institute()

iii)Sunday

( zerohedge)

iv)Monday/ Kurds/Turkey/Syria/Israel/Iran

v)Russia to the USA: stop playing with fire…leave the area in Syria immediately that which the USA controls( zerohedge)

vi)Tuesday

The situation in Syria has now escalated greatly as Syrian fighters loyal to Assad has joined the Kurds in attacking the invading Turks. This has sent the Turkish lira southbound as well as their stock market

( zerohedge)

6 .GLOBAL ISSUES

NATO is to allow free movement of troops across Europe (same as Schengen treaty). Not only that but NATO is going to augment USA troops in Syria and in Iraq as well as in Eastern Europe much to the chagrin of Russia who will not be very happy with this

( Gorka/Strategic Culture Foundation)

7. OIL ISSUES

Rig counts continue to rise in the USA and along with that, huge increase in production. USA production will exceed that of Saudi Arabia which puts OPEC’s future in doubt.

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)Not sure if foul play is here, but this South Korean regulator who tried to rein in crypto trading was found dead this morning

( zerohedge)

(courtesy Lawrie Williams/Sharp Pixley)

10. USA stories which will influence the price of gold/silver

i)Trading today/big news to be cognizant of:

(zerohedge)

ii)Perennial basket case Winn Dixie after shutting down more than 5,000 stories in 2017, are planning another 200 stories with news that parent Bi Lo LLC is preparing for a potential bankruptcy filing maybe as soon as next month.

( zero hedge)

iii)The Amazon effect is certainly causing troubles for Wal-Mart. It’s shares tumbles after missing earnings, its guidance disappoints and its on line sales slow

( zerohedge)

iv)We close out today’s commentary with Part 4 and Part 5 of David Stockman’s reporting that the USA economy’s reporting is not what it seems

(courtesy David Stockman)

v)SWAMP STORIES

a)Presented with no comment… (but a big eyebrow raise)…

b)The indictment certainly does not end the Mueller probe and it may continue for months

( zerohedge)

c)Manafort is now hit with new bank fraud over claims he “doctored” paperwork to secure a mortgage on one of his properties. He has pledged that property for bail and that may complicate things

( zerohedge)

d)Rick Gates, Manafort’s partner has now plead guilty and will testify against his former partner as part of a plea Mueller deal

( zerohedge)

e)Now Kushner is being probed for his Chinese contacts Anbang along with Russian contacts who were trying to rescue 666 5th Avenue

( zerohedge)

(courtesy zerohedge)

PRELIMINARY COMEX VOLUME FOR TODAY: 365,157 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 258,753 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY SIZED 122 CONTRACTS FROM 197,126 UP TO 199,752 DESPITE FRIDAY’S SMALL SIZED 7 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER GOOD SIZED 849 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 849. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD NO LONG COMEX SILVER LIQUIDATION BUT A HUGE SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 971 SILVER OPEN INTEREST CONTRACTS:

122 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 849 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 971 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 0 contracts REMAINING AT 77 contracts. We had 1 notices filed upon yesterday so we GAINED 1 contract or 5,000 ADDITIONAL oz will stand for delivery at the comex

The March contract lost 12,565 contracts DOWN to 72,018

April LOST 8 contracts DOWN to 150 .

.

We had 1 notice(s) filed for 5,000 OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 20/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1157 contracts

(115700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1784 notices

178400 oz

5.5489 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1784) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1157 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 294,100 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1784 x 100 oz or ounces + {(1157)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 294,100 oz standing in this active delivery month of February (9.147 tonnes). THERE IS 12.52 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 4 CONTRACTS OR AN ADDITIONAL 400 OZ WILL STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 71 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,414,916.610 oz

Brinks

HSBC

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,187,188.710 oz

JPM

|

| No of oz served today (contracts) |

1

CONTRACT(S

(5,000 OZ)

|

| No of oz to be served (notices) |

77 contracts

(385,000 oz)

|

| Total monthly oz silver served (contracts) | 310 contracts

(1,550,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had zero inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into J.P.MORGAN:1,187,188.710 oz ***

total inventory deposits: 1,187,188.710 oz

*** JPMorgan is continually adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 55% of all official comex silver.

we had 2 withdrawals from the customer account;

iii) Out of Brinks:: 416,190.3200 oz

ii) Out of HSBC: 998,726.310 oz

total withdrawals; 1,414,916.610 oz

we had 1 adjustment and it was a doozy!

i) Out of HSBC: 6,604,821.240 was removed from the customer account and out of the comex altogether.

total dealer silver: 43.827 million

total dealer + customer silver: 246.403 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 1 contract(s) FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 310 x 5,000 oz = 1,545,000 oz to which we add the difference between the open interest for the front month of FEB. (77) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 310(notices served so far)x 5000 oz + OI for front month of FEBRUARY(77) -number of notices served upon today (1)x 5000 oz equals 1,935,000 oz of silver standing for the FEBRUARY contract month.

WE GAINED 1 CONTRACT OR AN ADDITIONAL 5,000 OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 144,047 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 111,686 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 111,686 CONTRACTS EQUATES TO 458 MILLION OZ OR 80% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.29% (FEB 20/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.44% to NAV (FEB 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.29%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.44%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.94%: NAV 13.69/TRADING 13.30//DISCOUNT 2.94%.

END

And now the Gold inventory at the GLD/

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824.64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 20/2018/ Inventory rests tonight at 824.64 tonnes

*IN LAST 327 TRADING DAYS: 116.51 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 257 TRADING DAYS: A NET 40.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Feb 14/2017:

Inventory 314.045 million oz

end

HUGE SCARCITY OF GOLD IN LONDON AS THE GOLD LENDING RATE SURPASSES 2.23%

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.86%

12 Month MM GOLD LENDING RATE

+ 2.23%

GOFO = LIBOR – GOLD LENDING RATE

GOFO = 2.39 – 2.23 = .16

GOLD IS SCARCE.

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

GoldCore

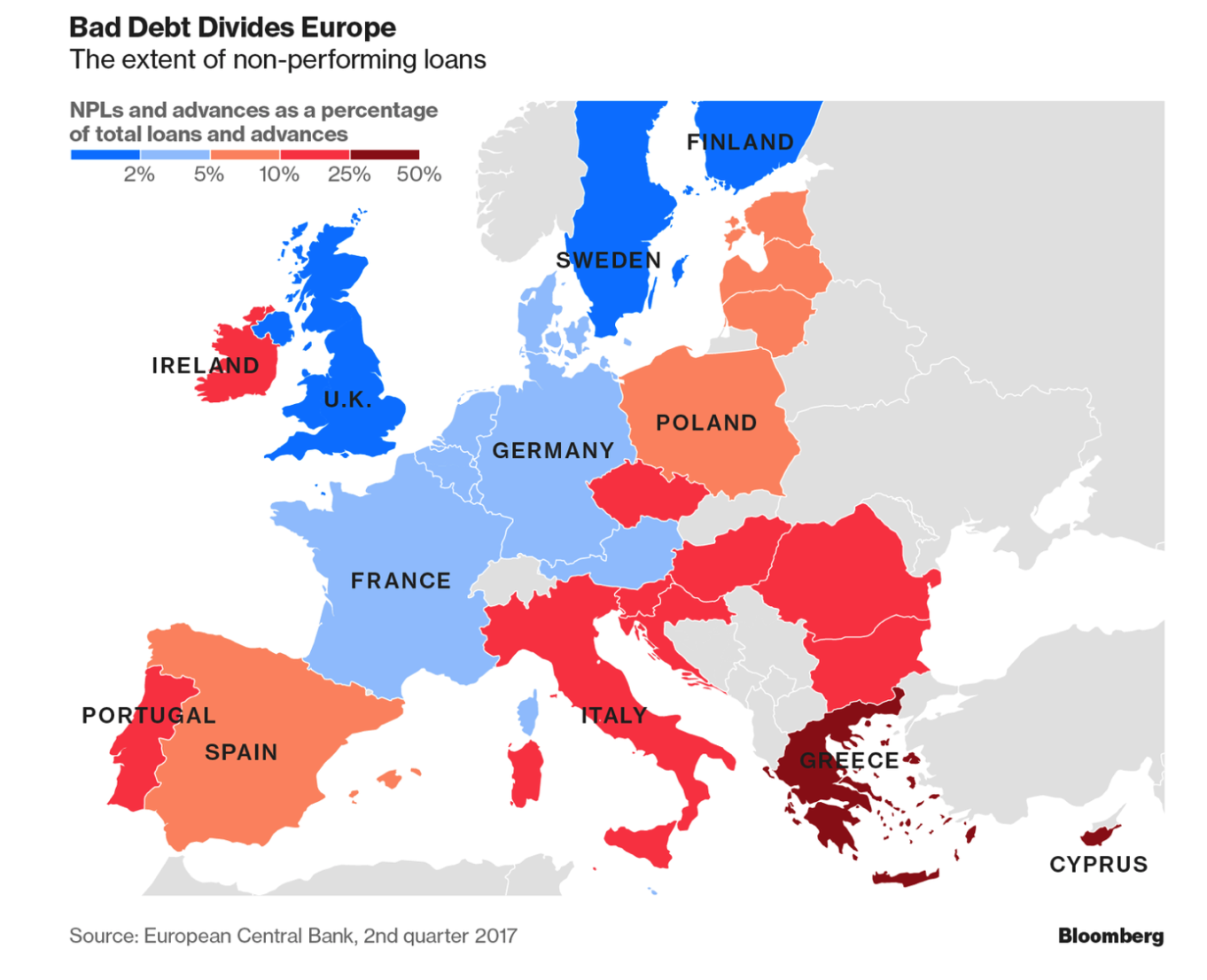

Bank Bail-In Risk In European Countries Seen In 5 Key Charts

Bank Bail-In Risk In Europe Seen In 5 Charts

– Nearly €1 trillion in non-performing loans poses risks to European banks’

– Greece has highest non-performing loans as a share of total credit

– Italy has the biggest pile of bad debt in absolute terms

– Bad debt in Italy is still “a major problem” which has to be addressed – ECB

– Level of bad loans in Italy remains above that seen before the financial crisis

– Deposits in banks in Greece, Cyprus, Italy, Ireland, Czech Republic and Portugal most at risk from bank bail-in

Editor: Mark O’Byrne

As reported by Bloomberg this week in an important article entitled ‘Five Charts That Explain How European Banks Are Dealing With Their Bad-Loan Problem’:

For European banks, it’s a headache that just won’t go away: the 944 billion euros ($1.17 trillion) of non-performing loans that’s weighing down their balance sheets.

Economists say the pile of past-due and delinquent debt makes it harder for banks to lend more money, hurting their earnings. European authorities are prodding lenders to sell or wind down non-performing credit, but they’re split on how to tackle the issue, and some investors are disappointed by the pace of progress.

There are various ways of calculating soured loans. The European Central Bank advises that non-performing asset indicators should be interpreted with caution because the definition of impaired assets and loss provision differ between countries. The data used below refers to domestic banking groups and standalone banks only, and excludes foreign subsidiaries and controlled branches.

“The data for the Czech banking sector consist of the banks that represent only 6 percent of credit extended by the banks operating in the Czech Republic,” the central bank said by email.Here are five charts (above and below) using the ECB data that help explain the non-performing loan issue and how banks are tackling it.

The problem is particularly acute in the countries that were hit hardest by the sovereign debt crisis. Greece, which has yet to exit its bailout program, tops the list of non-performing loans as a share of total credit, while Italy has the biggest pile of bad debt in absolute terms.

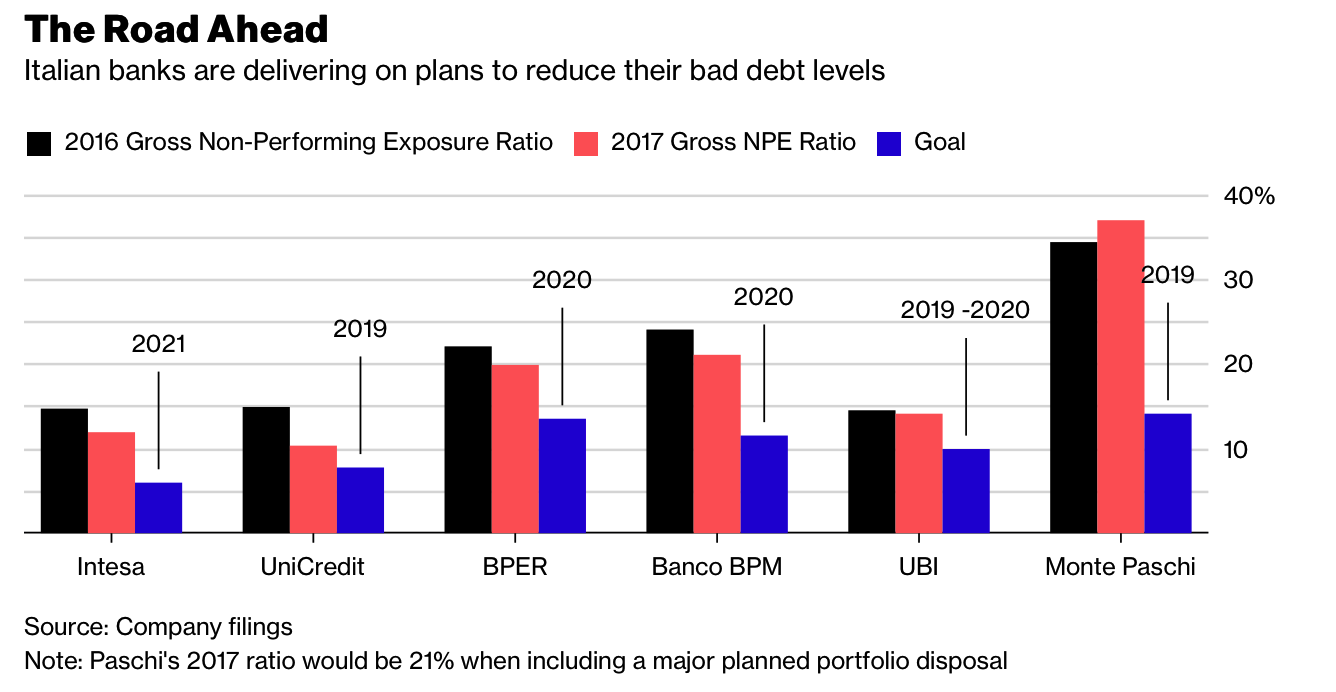

Italian banks have fixed goals for shrinking their bad credit levels by selling portfolios or winding down loans. Intesa Sanpaolo SpA, the country’s biggest bank by market value, got a head start on its rivals two years ago and plans to accelerate the reduction of non-performing loans, Chief Executive Officer Carlo Messina said last month. He says other Italian banks “are doing the right job” and should make further progress this year.

Italy amassed its pile of non-performing loans during years of little or no economic growth. The problem is compounded by the country’s legal system, where it takes lenders longer to liquidate collateral than in many other countries. Italy overhauled its bankruptcy rules in October to make them quicker and more efficient.

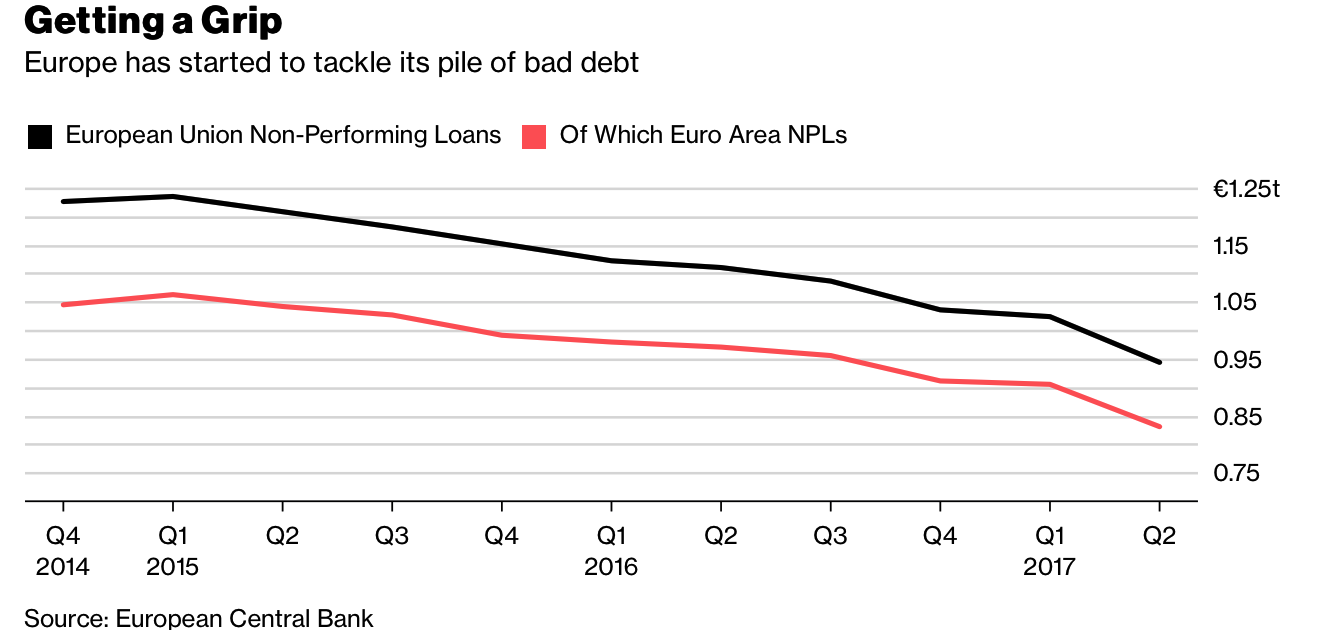

European banks overall have cut their non-performing loans by more than 280 billion euros since the end of 2014. The European Central Bank, which supervises most of the bloc’s big lenders, says bad debt is still “a major problem” which has to be addressed lenders while the economy performs well.

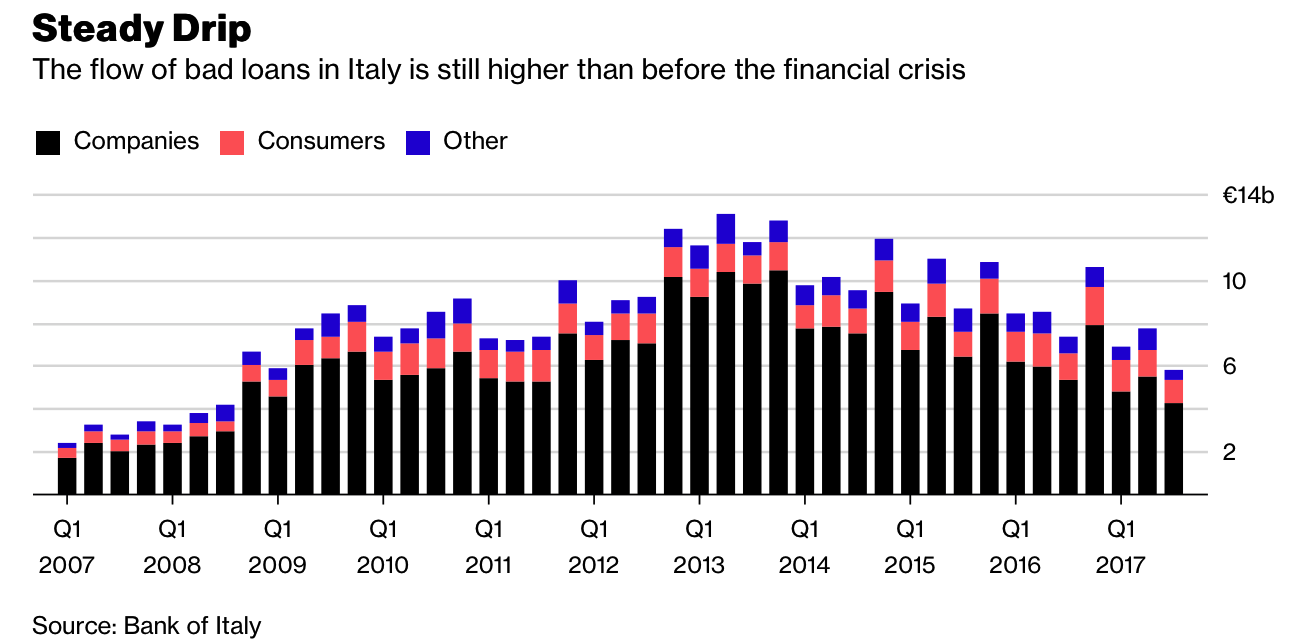

The flow of new bad loans is declining in Italy, but the level remains above that seen before the financial crisis. The Bank of Italy says an improvement in the country’s real estate market is helping to reduce the risks for banks. According to the central bank’s most recent financial-stability report, key vulnerability indicators for lenders should continue to decrease over the next few quarters.

What the five charts don’t show you is how much at risk are the deposits of savers and the capital of small to medium size enterprises (SMEs) who are the backbone of our respective economies. Bank bail-in and bail-in tools are now the preferred option for the ECB when it comes to dealing with failing banks. As you can see from the five charts, failing banks in Europe remain a very real risk.

In the EU it has been two years since the ECB decided it was better to force the financial burden of banks’ failures away from ordinary tax payers and instead onto bondholders and creditors i.e. those with deposits in a bank. Since then there has been very little information from the banks or mainstream media to warn individuals and businesses about the risk their deposits are exposed to and depositors have been lulled into a false sense of security regarding bank bail-ins.

Depositors, including savers, should consider diversifying some of their capital and not having all their eggs in the bank deposit basket. An allocation to physical gold and silver is prudent in this regard.

Gold and silver are financial insurance against bank bail-in, political mismanagement, and insolvent banks and governments. Allocated and segregated coins and bars confers outright legal ownership that is difficult to be appropriated, confiscated or subject to “haircuts”.

If bullion is owned in the safest ways possible, your precious metal intermediary or counter party cannot claim it is legally theirs and jeopardise your ownership of the asset. Nor can they hamper or remove that all important liquidity and the ability to use your precious metal assets as and when you need to.

It has been more than 10 years since the start of the financial crisis and yet banking risks, particularly in Europe, remain very high. The root cause of the problem – too much debt – was not dealt with and as each year goes by it becomes more important than ever to protect yourself from bail-in risks.

Related reading

How To Protect Your Savings From Bank Bail-Ins

Invest In Gold To Defend Against Bail-ins

Precious Metals Are “Best Defence” Against Bail-ins In Economic Crisis

News and Commentary

Gold prices inch down as dollar strengthens (Reuters.com)

Asia Stocks Track U.S. Futures Down; Dollar Steady (Bloomberg.com)

Zimbabwe Plans Gold, Tobacco Diaspora Bonds as Bank Rules Change (Bloomberg.com)

Congress sets sights on federal cryptocurrency rules (Reuters.com)

Morgan Stanley Says Stock Slide Was Appetizer for Real Deal (Bloomberg.com)

London’s Housing Boom Is Over, Rightmove Says (Bloomberg.com)

How One of the Most Profitable Trades of the Last Few Years Blew Up in a Single Day (Bloomberg.com)

World Embraces Debt At Exactly The Wrong Time (DollarCollapse)

Gold: Another Month, Another Test Of Key Resistance – But This Time With A Difference (GoldSeek.com)

Gold Prices (LBMA AM)

20 Feb: USD 1,337.40, GBP 955.97 & EUR 1,083.83 per ounce

19 Feb: USD 1,347.40, GBP 961.10 & EUR 1,085.47 per ounce

16 Feb: USD 1,358.60, GBP 964.61 & EUR 1,086.47 per ounce

15 Feb: USD 1,353.70, GBP 962.21 & EUR 1,084.45 per ounce

14 Feb: USD 1,330.75, GBP 959.74 & EUR 1,077.77 per ounce

13 Feb: USD 1,329.40, GBP 955.04 & EUR 1,077.61 per ounce

12 Feb: USD 1,321.70, GBP 955.19 & EUR 1,077.45 per ounce

Silver Prices (LBMA)

20 Feb: USD 16.57, GBP 11.85 & EUR 13.42 per ounce

19 Feb: USD 16.72, GBP 11.92 & EUR 13.46 per ounce

16 Feb: USD 16.84, GBP 11.97 & EUR 13.49 per ounce

15 Feb: USD 16.83, GBP 11.98 & EUR 13.49 per ounce

14 Feb: USD 16.58, GBP 11.97 & EUR 13.43 per ounce

13 Feb: USD 16.61, GBP 11.94 & EUR 13.46 per ounce

12 Feb: USD 16.43, GBP 11.86 & EUR 13.39 per ounce

Recent Market Updates

– US-China Trade War Escalates As Further Measures Are Taken

– Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

– Is The Gold Price Heading Higher? IG TV Interview GoldCore

– Global Debt Crisis II Cometh

– Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC

– Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

– “This Is Where They Completely Lost Their Minds” – Hussman

– Brexit Risks Increase – London Property Market and Pound Vulnerable

– Peak Gold: Global Gold Supply Flat In 2017 As China Output Falls By 9%

– Crypto Currency Backlash Sees Flight From Cryptos and Bitcoin

– Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

– Shrinkflation Intensifies – Stealth Inflation As Thousands of Food Products Shrink In Size, Not Price

– U.S. Debt Is “Extraordinarily High” and Are Stock And Bond Bubbles – Greenspan

Clive Maund still can’t admit that central banks diddle the gold market

Submitted by cpowell on Mon, 2018-02-19 18:19. Section: Daily Dispatches

1:16p ET Monday, February 19, 2018

Dear Friend of GATA and Gold:

Financial letter writer Clive Maund still can’t bear the thought that central banks might be interfering with his technical analysis of the gold market.

In his “Gold Market Update” posted at GoldSeek today —

http://news.goldseek.com/CliveMaund/1519050780.php

— Maund writes: “There has been much grumbling and muttering within the gold community about how ‘The Cartel’ and the Comex, etc., are holding the gold price in restraint by means of naked short-selling, hitting the market with supply when trading is thin during public holidays and overnight, and so on, but the fact of the matter is that the reason the precious metals sector has taken a back seat for years now is that there have been hotter games in town, like biotech, bitcoin, cannabis, the FANGS, tech generally, etc., and endless quantities of cheap money to bid them up into the stratosphere.”

Yes, all investment opportunities compete against each other, but not all of them have to compete against central banks, creators and dispensers of infinite money. After all, might not gold trade more positively if it was not constantly being jostled by a gold derivatives position of nearly 600 tonnes being managed aggressively every day by the Bank for International Settlements on behalf of its member central banks?:

http://www.gata.org/node/18041

If Maund thinks that central banks are not terribly important to the gold market, they plainly disagree with him. Will he not admit that they meddle in that market every day and that the longstanding public policy of Western central banks has been to suppress the price to defend their own currencies and government bonds? That policy is all over the archives that Maund strives to ignore.

Another financial letter writer, Michael Ballanger, in commentary also posted at GoldSeek today, “What the Markets Have in Common with the Film ‘Casablanca'” –

http://news.goldseek.com/GoldSeek/1519048800.php

— delivers a telling chart showing that the gold price was closely tracking the growth in the Federal Reserve’s asset book until 2013, when Fed asset purchases went vertical even as the gold price strangely collapsed. “Try to pick the spot where the interventionalists targeted gold,” Ballanger’s chart says. Even Maund might be able to identify the spot.

“Why,” Ballanger asks, “can the Fed buy, sell, and short (think volatility and gold) infinite amounts of anything and everything without ever getting a margin call? Are you not shocked — shocked — that the Captain Renault of bond vigilante-ism isn’t closing down that casino?”

Close down that casino? Ha! Like Maund, most financial letter writers and nearly all mainstream financial news organizations can’t even acknowledge that central banks have essentially commandeered all markets.

Such an acknowledgment would put most technical analysis and financial journalism out of business.

end

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

For your interest…

(courtesy Chris Powell/GATA)

Incredible 19th-century daguerrotypes show the faces of the Gold Rush

Submitted by cpowell on Mon, 2018-02-19 18:30. Section: Daily Dispatches

By Alyssa Pereira

San Francisco Chronicle

Sunday, February 18, 2018

After 1848 the prospectors came from all over to California for gold. The lot of them were hopeful, desperate, and ambitious — “the Forty-Niners” they were called. At a new museum exhibit at the National Gallery of Canada in Ottawa (and in a new book), you can come face to face with them.

As these fortune-seekers arrived in the West — 200,000 or so of them between 1849 and 1851 — so did those hoping to chronicle their efforts. Aiming to make a few bucks by providing portraits to those who were making new money, photographers utilized a method created only 10 years earlier by a Frenchman named Louis Daguerre. It was called daguerreotyping.

Photographers set up their studios in wagons and created these daguerreotypes from silver and copper plates. As the story goes, the photographers would manipulate the images after printing them, “adding gold dust onto streams or gold nuggets onto the sieves of the pioneers.” …

… For the remainder of the report:

https://www.sfgate.com/bayarea/article/Gold-Rush-daguerrotypes-photos-Fo..

END

Not sure if foul play is here, but this South Korean regulator who tried to rein in crypto trading was found dead this morning

(courtesy zerohedge)

Top South Korean Crypto Regulator Found Dead “From Unknown Cause”

The struggle between the South Korean Ministry of Finance and Ministry of Justice over the future of cryptocurrency regulation – a debate that mostly played out during December and January – terrified crypto traders who feared the South Korean government was on the verge of – wittingly or unwittingly – devastating the market.

Headlines about a pending ban in South Korea helped drive the bitcoin price more than 60% lower in January – its largest monthly drop in years – but now that the debate has been settled, the price has been steadily climbing again, breaking above $11,500 earlier today…

…having nearly doubled off the mystery dip-buyer lows…

But in a shocking development that’s almost guaranteed to contribute to speculation about whether any foul play was involved, the Wall Street Journal reports that one of the country’s top crypto regulators was found dead Tuesday.

While some speculated that the cause of death was a heart attack, the official statement – so far – is that the cause of death remains”unknown.”

Semiofficial news agency Yonhap reported that Mr. Jung was presumed to have suffered a heart attack and police had opened an investigation into the cause of death. Yonhap also reported that Mr. Jung was found at home. The government spokesman said later that “he died from some unknown cause. He passed away while he was sleeping and [his] heart [had] already stopped beating when he was found dead.”

His death comes barely a month after the country’s regulators appeared to settle on a suitable regulatory framework: Crypto exchanges and banks will soon be required to collect customers’ names and information.

The meteoric rise in bitcoin concerned South Korean Prime Minister Lee Nak-yon, who warned late last year that rising interest in cryptocurrencies could “lead to some serious distorted or pathological phenomenon.”

The dead regulator ran a government economics office that was responsible for South Korea’s legislative framework for bitcoin:

A South Korean official who guided Seoul’s regulatory clampdown on cryptocurrencies was found dead on Sunday, according to a government spokesman.

Jung Ki-joon, 52, was head of economic policy at the Office for Government Policy Coordination. He helped coordinate efforts to create new legislation aimed at suppressing cryptocurrency speculation and illicit activity, the spokesman said.

Semiofficial news agency Yonhap reported that Mr. Jung was presumed to have suffered a heart attack and police had opened an investigation into the cause of death. Yonhap also reported that Mr. Jung was found at home. The government spokesman said later that “he died from some unknown cause. He passed away while he was sleeping and [his] heart [had] already stopped beating when he was found dead.”

Coincidentally, a different regulator, Choe Heungsik, governor of Financial Supervisory Service, said Tuesday that he wants to see “normal” trading in cryptocurrencies and FSS will “actively” support it. In addition to registering accounts, the country is also seeking to develop a suitable anti-money laundering framework.

Jung’s colleagues said he had been under heavy stress in recent months as South Korea worked to tackle cryptocurrency speculation. There’s no indication that foul play was involved.

According to CryptoCompare, about 4.5% of all bitcoin transactions world-wide last year used the South Korean won, making it the most widely used fiat currency in bitcoin trading after the dollar, the yen and the euro. Bitcoin prices in South Korea are sometimes up to 50% higher than on other exchanges – a phenomenon bitcoin traders have termed “the kimchi premium”.

end

With China away from the gold market celebrating their lunar New Year, generally you can expect the crooks to raid the paper price as we have one less physical zone.

(courtesy Lawrie Williams/Sharp Pixley)

We would advise against backing equities and bitcoin again – at least for the time being. Their recent huge falls will have destroyed a degree of confidence in them and it won’t take much in the way of perceived bad news to bring them crashing back down again. They may recover, but both appeared to be in bubble territory and there is certainly the possibility that the real falls have not fully occurred yet.

Precious metals may have their ups and downs, but they do tend to be less volatile than equities and bitcoin so are probably safer bets in terms of wealth preservation. They may not see the levels of gains that bitcoin and equities have the potential for, but don’t have the massive loss potential either. Gold has, over time, been the most reliable wealth protector and while we may not subscribe to the massive gain predictions seen by some other commentators we do see steady overall growth ahead. Good advice is keep some of your wealth in gold – perhaps 10-12.5% – and it will help iron out the downturns. Because equities have seen big rises over the past few years don’t rely on these continuing ad infinitum.

https://www.sharpspixley.com/articles/lawrie-williams- gold-bears-play-while-chinese-away_276952.html

20 Feb 2018

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED /shanghai bourse CLOSED / HANG SANG CLOSED

2. Nikkei closed DOWN 224.11 POINTS OR 1.01% /USA: YEN RISES TO 107.15/DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 89.64/Euro FALLS TO 1.2340

3b Japan 10 year bond yield: RISES TO . +.066/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.15/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.23 and Brent: 65.03

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.742%/Italian 10 yr bond yield UP to 2.056% /SPAIN 10 YR BOND YIELD UP TO 1.524%

3j Greek 10 year bond yield RISES TO : 4.426?????????????????

3k Gold at $1339.05 silver at:16.53 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 16/100 in roubles/dollar) 56.64

3m oil into the 62 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.16 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9341 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1534 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.742%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.909% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.162% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Slide As Dollar, Rates Jump Ahead Of “Monster” Treasury Issuance

After a week in which stock-trading abruptly algos decided that rising yields are irrelevant at worst, and at best positive for equities, the correlation has again flipped overnight sending Asian shares lower and European share erasing earlier gains as bonds fell around the globe, with the 2Y Treasury yield rising 3bps to 2.23% – highest since September 2008 – and the 10Y briefly as high as 2.93%…

… ahead of this week’s “monster issuance” of $258 billion in TSY bills and notes…

… which in turn has sent the recently beaten down dollar higher for the third day in a row...

… and pushed S&P futures sharply lower for the second consecutive day, as the VIX is above over 21 as of 6am ET.

Europe’s main bourses saw a steady start as lower domestic currencies helped their cause, although early gains were quickly faded amid declines in auto and banking, but weakness across Asia where Tokyo and South Korea saw drops more than 1%, meant MSCI’s 47-country world share index was 0.2 percent in the red.

European equities trimmed initial gains (Eurostoxx 50 flat) to trade with little in the way of firm direction ahead of the US return to market. The FSTE 100 lagged peers (-0.4%) after disappointing earnings from index heavyweights HSBC (-4%) and BHP Billiton (-4%), dampening sentiment for UK stocks and the former leading to underperformance in the financial sector. Other individual movers include Hikma Pharmaceuticals (+9%) after appointing their new CEO, Fidessa (+21.4%) are also seen higher after reports that Swiss-listed Temenos (-6.8%) are to make an offer for the Co., while Intercontinental Hotels (-3.9%) have faced selling pressure this morning following a lacklustre earnings update.

MSCI Asia Pacific index declines for first time in seven days. The Hang Seng index slipped after HSBC profits missed; H-shares erase most losses after falling as much as 1.9%. n. In Australia, the ASX 200 came under pressure from material and financial names, with many of the large banks reversing the prior days gains. Over in Japan, the Nikkei (-1.0%) had tripped through 22,000 amid softness in tech names. The Hang Seng (-0.8%) reopened for the first time since last week, however initial gains had been short-lived.

But all attention today will be on the bond market, where as Bloomberg notes, debt investors are trading with caution as Treasury markets reopened after the Presidents’ Day break as the VIX jumped to its highest level in five sessions. As reported yesterday, Treasuries are under pressure ahead of what Bloomberg has dubbed “monster debt supply” in which the U.S. gets set to sale a record amount of debt with three days of auctions today totaling $258 billion. And while speculators are turning bearish – rapidly covering net short bets across the curve but mostly in the 2Y…

… money managers are looking at the highest U.S. yields in years as a buying opportunity in a world where shorter-term Japanese and German notes still carry negative yields.

“I just advise caution,” said Principal Global Investors’ chief global economist Bob Baur said about stocks as Wall Street futures also pointed lower. “I‘m not sure whether this (early February sell-off) was the dip to buy, there will probably be a relapse and then another relapse, before maybe around mid-summer stocks make another run up.”

European bond yields pushed up too, with traders also working through the options of who could succeed Mario Draghi as European Central Bank chief next year after Spain’s economy minister was nominated for the bank’s number two job.

In other news, BOJ governor Haruhiko Kuroda didn’t discuss monetary policy during an appearance in parliament today. Speculation has been swirling about the possibility the BOJ is scaling back its stimulus since the central bank reduced its purchases of government bonds in January.

The UK is said to have a secret plan to withhold Brexit payments if the EU refuses to provide the UK with a desirable trade deal. Elsewhere, according to a letter seen last week, Netherlands government has linked its decision to activate hard Brexit plan amid a lack of clarity from the UK.

Echoing China, the German Economy Minister says the EU will respond appropriately if the US puts a tariff on European steel imports.

Speaking of Germany, it reported mixed February ZEw numbers: German ZEW Economic Sentiment (Feb) 17.8 vs. Exp. 16.5 (Prev. 20.4); German ZEW Current Conditions (Feb) 92.3 vs. Exp. 93.9 (Prev. 95.2)

South Africa’s rand and Turkey’s lira both gave back more of their recent gains, while growing concerns about the previously reported alleged fraud at India’s second-largest state-run bank sent the rupee skidding to a near three-month low: “Punjab National Bank will need to provide for at least a substantial portion of the exposure. As a result, the bank’s profitability will likely come under pressure,” rating agency Moody’s said as it put it on a downgrade warning.

In commodity markets, Oil prices were mixed, with reduced flows from Canada pushing up U.S. crude while Brent sagged $65.45 per barrel on the back of weaker Asian stocks and the dollar’s bounce. Spot gold slipped 0.4 percent to 1,341.06 an ounce, also corseted by the dollar’s bounce, while industrial metals including copper drifted lower for a second day in a thinner-than-usual trading due to new year holidays in China.

Bitcoin broke above $11,500, almost double its intraday low from just two weeks ago.

Bulletin Headline Summary from RanSquawk

- European equities have trimmed initial gains (Eurostoxx 50 flat) to trade with little in the way of firm direction ahead of the US return to market

- EU Parliament is to call for Britain to have privileged single market access after Brexit, according to Business

- Insider

- Looking ahead, highlights include US supply, WalMart earnings

Market Snapshot

- S&P 500 futures down 0.6% to 2,719.50

- STOXX Europe 600 up 0.1% to 378.63

- MSCI Asia Pacific down 0.9% to 176.50

- MSCI Asia Pacific ex Japan down 0.5% to 575.76

- Nikkei down 1% to 21,925.10

- Topix down 0.7% to 1,762.45

- Hang Seng Index down 0.8% to 30,873.63

- Shanghai Composite up 0.5% to 3,199.16

- Sensex down 0.09% to 33,745.75

- Australia S&P/ASX 200 down 0.01% to 5,940.85

- Kospi down 1.1% to 2,415.12

- German 10Y yield rose 2.0 bps to 0.755%

- Euro down 0.4% to $1.2355

- Brent Futures down 0.6% to $65.28/bbl

- Italian 10Y yield rose 5.6 bps to 1.773%

- Spanish 10Y yield fell 0.3 bps to 1.508%

- Brent Futures down 0.6% to $65.28/bbl

- Gold spot down 0.7% to $1,337.27

- U.S. Dollar Index up 0.6% to 89.60

Top Overnight News

- Latvia will seek to prevent ECB Governing Council member Ilmars Rimsevics from returning to his post after he was caught up in a bribery probe that’s rocked the Baltic nation, the country’s prime minister said in an interview

- Treasuries are about to reach a turning point, with the trend toward a flatter yield curve poised to end in the next few months, says Akira Takei, a fund manager at Asset Management One

- Chancellor Angela Merkel sent a strong signal in the debate over her preferred successor as German leader by appointing close ally Annegret Kramp-Karrenbauer as general secretary of her Christian Democratic Union party

- Prime Minister Theresa May’s team is eyeing up a contingency plan to hold back billions of pounds in Brexit payments, if the European Union refuses to give the U.K. the trade deal it wants

- Brexit Secretary David Davis will reassure the European Union that the U.K. won’t try to undercut the bloc by tearing up regulations after the split, making the case for mutual trust between regulators on each side

- Spain’s Economy Minister Luis de Guindos won the backing of euro-area finance ministers late Monday to replace ECB Vice President Vitor Constancio; some economists reckon he may side with the more optimistic governors on the council, who have long been pushing for an end to quantitative easing, while at the same time being mostly consensus-oriented

- Australia’s central bank reiterated that inflation is expected to “only gradually” accelerate as the economy strengthens and wage pressures increase, in minutes of this month’s policy meeting

Asian equity markets are somewhat fragile, with major Asian bourses off to a weaker start. US markets were closed for President’s day and as such, Asian participants took the cue from European equities which slipped in yesterday’s session. In Australia, the ASX 200 (flat) has come under pressure from material and financial names, with many of the large banks reversing the prior days gains. Over in Japan, the Nikkei (-1.0%) had tripped through 22,000 amid softness in tech names. The Hang Seng (-0.8%) reopened for the first time since last week, however initial gains had been short-lived, with the index conforming to the sombre tone. JGBs are flat in thin-trade, March futures contract down 2 ticks and hovering near yesterday’s levels. USTs off by 6+ ticks with yields continuing to pick up, 2yr yields now at the highest since Sep’08 after hitting 2.22%, while the US curve is also flattening this morning. The RBA meeting minutes failed to provide any fireworks with the central bank sticking with its neutral tone. As such, AUD had been largely unmoved post the release of the minutes and instead focus will fall on the wage price index due out tomorrow. RBA February minutes states that low rates are helping reduce unemployment and lift inflation, additionally rising AUD would impede pickup in economic growth and inflation, however AUD TWI is still within narrow range of past couple of years.

Top Asian News

- Espenilla Says Philippine Rate Hike on Table But Data Dependent

- India Is Said to Tighten Approvals for Offshore Borrowing

- Bitcoin Rises as South Korea Talks ‘Active’ Support for Trading

- BHP Falls as Much as 3.8% in London After Adj Profit Misses Ests

- Toyota Readies Cheaper Electric Motor by Halving Rare Earth Use

European equities have trimmed initial gains (Eurostoxx 50 flat) to trade with little in the way of firm direction ahead of the US return to market. The FSTE 100 modestly lags its peers (-0.4%) after disappointing earnings from index heavyweights HSBC (-4%) and BHP Billiton (-4%), dampening sentiment for UK stocks and the former leading to underperformance in the financial sector. Other individual movers include Hikma Pharmaceuticals (+9%) after appointing their new CEO, Fidessa (+21.4%) are also seen higher after reports that Swiss-listed Temenos (-6.8%) are to make an offer for the Co., while Intercontinental Hotels (-3.9%) have faced selling pressure this morning following a lacklustre earnings update.

Top European News

- Gulliver Ends HSBC Tenure With Rare Profit Miss on Margins

- U.K. Has Plan to Halt Brexit Cash If EU Backslides on Trade Deal

- Morgan Stanley Says Stock Slide Was Just Appetizer for Real Deal

- Oil Holds Momentum That’s Driven by OPEC’s Promise to Re- Balance

- A Diversified Portfolio May Not Help Investors Much This Year

In FX, the DXY has now rebounded above 89.500, and on broad-based gains vs G10 rivals, albeit mainly inspired by another round of short covering. A major French bank notes that the market remains very short of Dollars (in line with latest weekly CFTC spec positioning data) and modestly long Jpy and moves in the headline pairing off last week’s circa 105.55 low support the rebalancing theory as spot trades back over 107.00. 107.32 offers eyed next, and as a recap this level now forms resistance rather than support on the way down as the 2017 low. Similar price moves elsewhere, as Eur/Usd recoils further from recent peaks and briefly testing bids at 1.2350 with small stops just below, but not challenging key Fib support at 1.2319. Cable briefly reclaimed the 1.4000 handle after reports in Business Insider suggested that the EU Parliament is to call for Britain to have privileged single market access after Brexit. Usd/Chf now inching closer to 0.9350 and Usd/Cad just shy of 1.2600 amidst the ongoing Greenback recovery, while Aud/Usd is retesting 0.7900 on the downside with little direction gleaned from RBA minutes overnight, but key data to come

tomorrow (wage growth). Nzd/Usd straddling 0.7350, with strong chart support around 0.7338.

In commodities, WTI and Brent crude futures are seen higher albeit off best levels as the firmer USD caps gains; WTI holds above the USD 62.00bbl level (note the weekly API inventories will be released tomorrow, not today due to yesterday’s US market holiday). In terms of energy news flow, the Joint OPEC/non-OPEC Technical Committee concluded that the oil glut is dissipating at a faster pace than anticipated, according to sources. Additionally, UAE energy minister claims OPEC and allies are to continue oil cooperation beyond 2018 and notes UAE, Saudi Arabia and Russia all support an extension cut beyond 2018. In metals markets, spot gold trades lower alongside the aforementioned firmer USD while copper prices have seen little in the way of firm direction as Chinese participants remain away from market. UAE Energy Minister says the UAE is expected to over-deliver on production cuts in Q1 due to maintenance commitment with OPEC-led pact.

Global Event Calendar

- Mexico Citibanamex Survey of Economists

- 8:30am: Canada Wholesale Trade Sales MoM, Dec., est. 0.4%, prior 0.7%

- 10am: Mexico International Reserves Weekly, Feb. 16, no est., prior 173b

Bond Auctions:

- 11:30am: U.S. to Sell USD51 Bln 3-Month Bills

- 11:30am: U.S. to Sell USD45 Bln 6-Month Bills

- 1pm: U.S. to Sell USD55 Bln 4-Week Bills

- 1pm: U.S. to Sell USD28 Bln 2-Year Notes

DB’s Jim Reid concludes the overnight wrap

With Chinese New Year holidays and President’s Day in the US, yesterday was always going to be quiet and we weren’t disappointed on this. It was a far cry from two weeks ago last night when we saw the largest single day spike in the VIX on record and a 1000 point move on the DOW in c20 minutes towards the end of the session. In reality the market has regained its poise very impressively since. For the markets that were open yesterday, it was generally a down day though. The Stoxx 600 fell for the first time in four days (-0.63%), but trading volume was thin and at roughly half the 30 day average. Within the Stoxx, losses were led by the health care, consumer and real estate sector, with Reckitt Benckiser down 7.5% after warning pricing pressures would continue to hit margins. Across the region, the DAX (-0.53%) and FTSE (-0.64%) also fell modestly while Italy’s FTSE MIB was the relative laggard at -1.0%. The Vstoxx rose for the first time in six days, up 7.7% to 19.13.

Government bonds weakened with core 10y bond yields up 2-4bp (Bunds +2.8bp; Gilts +2bp), in part reversing Friday’s gains in the absence of material macro data. Key peripherals yields were also up 2-5bp, while Greek bonds outperformed with its 10y yields down 1.9bp after Fitch upgraded the country’s long term issuer rating from B- to B with a positive outlook retained. Post the change, Fitch’s rating is now in line with S&P’s. In FX, the US dollar index was marginally higher (+0.13%) while the Euro was broadly flat and Sterling fell 0.19%. In commodities, WTI oil was up 1.33% to $62.50/bbl while precious metals were little changed (Gold -0.04%; Silver +0.18%).

This morning in Asia, markets are broadly lower with the Nikkei down for the first time in four days (-1.06%), while the Kospi (-1.27%) and Hang Seng (-0.37%) are also lower, as the latter pared back earlier gains as trading resumed post the New Year holidays. The UST 10y yield is up 2bp and S&P index futures are down c0.3% this morning.

Back in Europe, finance ministers have nominated the Spanish Economy Minister Luis de Guindos to be the next Vice President of the ECB to replace Mr Constancio. The decision puts Spain back on the ECB’s executive board after a six year absence. Mr de Guindos will resign from his existing post within days and said he is “pragmatic” rather than a dove / hawk when it comes to monetary policy and will always defend the ECB’s independence. Looking ahead, he will face a hearing at the EU Parliament and then EU leaders will ratify his appointment at their summit on March 22. Elsewhere, Germany’s acting Finance Minister Peter Altmaier said Mr de Guindos would be an “excellent choice” for the role.

Staying with the ECB, the latest QE purchases data was released yesterday. It was yet another very strong week for CSPP relative to PSPP which now leaves little doubt about the ECB’s intentions to keep the former elevated relative to the latter, given that we now have 6 full weeks of data since they halved the net flow of QE. The CSPP/PSPP ratio was 29.4% (27.3% over last 4 weeks). As a reminder, before Apr 2017 when QE was still €80bn/m the ratio was 11.5%.

Between Apr-Dec 2017 (QE €60bn/m) the ratio edged up to 12.7% but since Jan 2018 (QE €30bn/m) the ratio is now 25.5%. Indeed the strength of corporate vs. government purchases as proxied by the CSPP/PSPP ratio has so far surpassed our expectations of “roughly 20%”.

Staying in Europe, an interesting story yesterday as SPD members now start voting as to whether to enter a coalition with Mrs Merkel, was the one that suggested that the far right AfD party has overtaken the SPD in the polls for the first time. The Bild/INSA poll put them at 16% and 15.5% respectively against 12.6% and 20.5% at the election back in September. The fear from the SPD was always that a renewed collation agreement would lead to them seeing their popularity drop further but with stalemate elsewhere they were left with limited choice but to negotiate in the end. Are the electorate punishing them for their decision to enter talks or the fact that it took so long to do so? Either way, in our view the fact that far right in Germany are now second in the polls is fairly remarkable really.

Continuing with politics, ahead of the 4th March national election in Italy, DB’s Clemente De lucia noted that the risk of a hung parliament remains high, but it is a close call as the centre-right coalition is closing the gap to get an outright majority. If the elections prove to be inconclusive, Clemente expect the parties and institutions to work hard to form a grand coalition. Whatever the result of the elections, the fiscal stance will be in the spotlight after the vote. All parties are pledging significant expansionary policies. As things stands, Italy does not comply with EU fiscal rules and without some adjustments, Rome could be on a collision course with Brussels. With the gap between Rome and Brussels not significantly large, we expect a compromise to be reached. Refer to the note for more details.

Now turning to some of the Brexit headlines. The BOE governor Carney noted the transitional deal to be reached before the end of March “obviously won’t be a hard, legally binding agreement, but….something that has legal text associated with it, which will be part of the separation agreement, (then) that should be good enough”. Elsewhere, three unnamed senior British officials have told Bloomberg that the UK have a fall back option of withholding the £40bn divorce Brexit payments to ensure the EU agrees to the trade deal it wants. The former leader of PM May’s conservative party Iain Duncan Smith said “either the EU gives us a trade deal or they won’t get any money at all”. Finally, DB’s Oliver Harvey has assessed the suitability of a CETA (comprehensive economic and trade agreement) type deal between the UK and the EU and the implications for growth and markets. Overall, the team believes there are no workable alternatives for the UK to maintain close to present levels of trade with the EU27 in the current time frame outside of the EEA and a separate customs agreement. They expect this to be the ultimate destination of Brexit, but not before a political crisis. Refer to their note for more details.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. The February Rightmove index on asking prices for UK homes was above the prior month’s reading at 0.8% mom (vs. 0.7% previous) and 1.5% yoy (vs 1.1% previous). The Euro area’s current account surplus in December was below last month’s reading at €29.9bln (vs. €32.5bln previous) but the fullyear surplus rose to a new high of €392bn. In Asia, Japan’s Reuters’ Tankan manufacturers’ index fell 6pts to +29 in February (vs. the prior reading at an 11- year high), while the non-manufacturers index was steady at a solid level of +33.

Looking at the day ahead, the January PPI and the February ZEW survey are due in Germany. The February CBI selling prices data in the UK and the February consumer confidence print for the Euro area are also due in the afternoon. In terms of politics, the Social Democrats party in Germany will begin a two-week period for members to vote on the proposed coalition pact.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed /Hang Sang CLOSED / The Nikkei closed DOWN 224.11 POINTS OR 1.01%/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed UP at 6.3415/Oil DOWN to 62.03 dollars per barrel for WTI and 65.23 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED XXX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED XXX AGAINST THE ONSHORE YUAN AT XXX//ONSHORE YUAN /OFFSHORE YUAN NOT TRADING

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

end

4. EUROPEAN AFFAIRS

Deutsche bank/Germany

More trouble on the horizon for the world’s biggest derivative player. They seem to be leaning on firing 500 of their workers due to tumbling trading revenues

(courtesy zero hedge)

Deutsche Bank To Fire Up To 500 Amid Tumbling Trading Revenues

The drip-drip-drip death spiral of what was once the world’s most systemically dangerous bank continues as Bloomberg reports Deutsche Bank has started cutting at least another 250 jobs at its corporate and investment bank units.

These new firings, which could widen to more than 500, according to Bloomberg‘s sources, comes after bonus payments that Chief Executive Officer John Cryan said were on the “generous” side, helped push the business in the red.

Cryan is trying to motivate and retain top investment banking staff, while keeping a lid on costs following three straight years of losses.

But with revenue at a seven-year low, even a relatively small increase in compensation can cause losses at the securities unit.

Chief Financial Officer James von Moltke has urged a return to more disciplined cost management after the lender scrapped a target for this year.

And these “generous” bonuses follow a 27% collapse in trading revenues and the disastrous debacle surrounding China’s HNA liquidating its holdings of the giant German bank.

Imagine how “generous” these bonuses would have been if things were really bad?

As Michael Huenseler at Assenagon noted previously:

“The results are disappointing again and we don’t see anything encouraging in them, reinforcing our doubts in the bank’s strategy and management…There’s no silver lining.“

Bloomberg notes that bank officials declined to comment.

For context, Deutsche Bank’s corporate and investment bank employed 17,251 front office full-time staff at the end of last year.

While Deutsche’s share price continues to languish, the last week or so has seen a more concerning re-ignition of short-term counterparty risks as Deutsch Bank’s 1Y Sub CDS spreads have blown out…

Or does someone know something about a short-vol position that DB may be holding?

And even more worrying for the bank itself is the total decoupling of short-term default risk from Germany’s systemic risk…

In other words – you’re on your own Mr. Cryan.

Latvia Bank Crisis: Central Bank In Chaos As ECB Blocks Payments By Third Largest Bank

One day after we reported that Latvia’s central bank governor – and ECB Governing Council member – Ilmars Rimsevics was detained by Latvia’s anti-corruption authority on Saturday on suspicion of accepting a bribe of more than €100,000, prompting both Latvia’s Prime Minister and the president to call on Rimsevics to resign, Latvia now appears to have a full-blown banking crisis on its hands, after the European Central Bank froze all payments by Latvia’s third largest bank, ABLV, following U.S. accusations the bank laundered billions in illicit funds, including for companies connected to North Korea’s banned ballistic-missile program.

The troubles started on February 14, when Latvia began investigating ABLV over suspicions of illegal trading related to North Korea’s weapons system. The investigation was launched after the Treasury Department charged the bank on Feb. 13 with having “institutionalized money laundering as a pillar of the bank’s business practices,” which proposed preventing the bank from opening an account in the U.S.

That decision immediately made ABLV a pariah to other financial institutions, effectively cutting its access to the dollar and funding flows from the world’s most important market, and forcing it to rely exclusively on the ECB as it sole-source of funds.

As the WSJ reported, in proposing the ban on ABLV, Treasury said the bank managed transactions for clients connected to several long-sanctioned North Korean firms.

These include North Korea’s Foreign Trade Bank, the institution that manages Pyongyang’s foreign-currency earnings, revenue that U.S. and United Nations officials say go directly to North Korea’s nuclear and missile programs.

According to the Treasury, ABLV’s alleged illegal activity also included funneling billions of dollars in public corruption proceeds from Azerbaijan, Russia and Ukraine through shell company accounts.

ABLV, Latvia’s third-largest lender by assets, is based in Riga but has an office in Luxembourg and a subsidiary in the U.S. It is also supervised directly by the ECB under a new system of eurozone bank supervision introduced during the region’s recent financial crisis, under which national authorities remain responsible for enforcing money-laundering laws.

On Monday morning, the troubles for ABLV cascaded when the ECBsaid that it had instructed Latvia’s banking supervisor to impose a moratorium on the country’s third-largest bank, which freezes all payments by the bank on its liabilities.

“In recent days, there has been a sharp deterioration of the bank’s financial position. This follows an announcement on 13 February by the US Department of the Treasury’s Financial Crimes Enforcement Network from February to propose a measure naming ABLV bank an institution of primary money laundering concern pursuant to Section 311 of the USA Patriot Act,” the ECB said in a statement.

“A moratorium was considered necessary given that the bank is working with the Latvian central bank and authorities to address the current situation.”