GOLD: $1329.95 UP $0.90

Silver: $16.63 UP 15 cents

Closing access prices:

Gold $1324.50

silver: $16.50

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $XXXX DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $XXXX

PREMIUM FIRST FIX: $xxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $XXXX

NY GOLD PRICE AT THE EXACT SAME TIME: $xxx

discount of Shanghai 2nd fix/NY:$

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1328.60

NY PRICING AT THE EXACT SAME TIME: $1328.75

LONDON SECOND GOLD FIX 10 AM: $1339.85

NY PRICING AT THE EXACT SAME TIME. $1340.30

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:1784 FOR 178400 OZ (5.5489 TONNES),

For silver:

FEBRUARY

76 NOTICE(S) FILED TODAY FOR

380,000 OZ/

Total number of notices filed so far this month: 386 for 1,930,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,971/OFFER $11,050: DOWN $203(morning)

Bitcoin: BID/ $10,379/offer $10,499: DOWN $811 (CLOSING/5 PM)

end

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUGE SIZED 3777 contracts from 199,852 RISING TO 203,629 DESPITE YESTERDAY’S 29 CENT LOSS IN SILVER PRICING. SHOCKINGLY WE HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1293 EFP’S FOR MARCH AND AND 28 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1321 CONTRACTS. WITH THE TRANSFER OF 1321 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 1321 CONTRACTS TRANSLATES INTO 6.605 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

40,269 CONTRACTS (FOR 15 TRADING DAYS TOTAL 40,269 CONTRACTS OR 201.345 MILLION OZ: AVERAGE PER DAY: 2685 CONTRACTS OR 13.423 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 201.345 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 28.77% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 449.88 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A HUGE SIZED GAIN IN OI SILVER COMEX DESPITE THE 29 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1321 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1321 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 5098 OI CONTRACTS i.e. 1321 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3777 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 29 CENTS AND A CLOSING PRICE OF $16.48 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0195 BILLION TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 386 NOTICE(S) FOR 380,000 OZ OF SILVER

In gold, the open interest FELL BY AN SURPRISINGLY SMALL 7921 CONTRACTS DOWN TO 528,154 DESPITE THE HUGE FALL IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($24.15). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR WEDNESDAY AND IT TOTALED AN HUGE SIZED 13,134 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 13,134 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 530,573. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 5213 CONTRACTS: 7921 OI CONTRACTS DECREASED AT THE COMEX AND A HUGE SIZED 13,134 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(5131 oi gain in CONTRACTS EQUATES TO 15.95 TONNES) AND ALL OF THIS GAIN HAPPENED WITH A MONSTROUS RAID AND A FALL IN PRICE OF $24.15

YESTERDAY, WE HAD 6434 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 172,222 CONTRACTS OR 17,222,000 OZ OR 535.67 TONNES (15 TRADING DAYS AND THUS AVERAGING: 11,481 EFP CONTRACTS PER TRADING DAY OR 1,148,100 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 15 TRADING DAYS: IN TONNES: 535.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 535.67/2200 x 100% TONNES = 24.34% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1169.08 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX WITH THE HUGE FALL IN PRICE IN GOLD TRADING YESTERDAY ($24.15). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 13,134 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 13,134 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 5213 contracts ON THE TWO EXCHANGES:

13134 CONTRACTS MOVE TO LONDON AND 7921 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 16.21 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $0.90 /NO CHANGE IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 827.79 tonnes.

SLV/

WITH SILVER UP 15 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF:1.226 MILLION OZ OF SILVER

/INVENTORY RESTS AT 315.271 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 3777 contracts from 199,730 UP TO 203,629 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE HUGE SIZED FALL IN PRICE OF SILVER (29 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1293 PRIVATE EFP’S FOR MARCH AND 28 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 4092 CONTRACTS TO THE 1321 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 5098 OPEN INTEREST CONTRACTS . WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 25.49 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE HUGE SIZED FALL OF 29 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 1321 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed /Hang Sang CLOSED UP 558.26 POINTS OR 1.81% / The Nikkei closed UP 45.71 POINTS OR 0.21%/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed UP at 6.3415/Oil DOWN to 61.48 dollars per barrel for WTI and 65.14 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED XXX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED XXX AGAINST THE ONSHORE YUAN AT XXX//ONSHORE YUAN /OFFSHORE YUAN NOT TRADIN

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

i)Italy

In Italy, Tax evasion is considered a sport. Now the Italian government has introduced a new automated tax snitch program trying to get at tax cheats. Originally they had a program which highlighted if you spent too much one expenses that you had evaded taxes. Now a new program: if you do not access your bank account often enough, or save too much, you are targeted

a good one…

( Simon Black/SovereignMan)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

Interesting: Sweden is the world’s biggest nation to go cashless. Now they are worried that the cashless part is going too fast

( zerohedge)

7. OIL ISSUES

i)There is a huge shortage of Frac sand which is in integral part of the shale production. It is hard and made up of round particles and is very porous..ideal for fracing

so we now have two fold problems

1. shortage of rail cars to transport shale

2. shortage of frac sand.

( Nick Cunningham/OilPrice.com)

ii)THIS HAS NO CHANCE OF SURVIVING: Maduro launches his oil backed crypto currency

( zerohedge)

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

( Harris/Bloomberg/GATA)

ii)Russia adds a considerable 19.7 tonnes to its official reserves which now stand at 1857. tonnes.

( Lawrie Williams/Sharp’s Pixley)

10. USA stories which will influence the price of gold/silver

i)Early trading this morning;

VIX crushed and that propelled the Dow northbound:

( zerohedge)

ii)Even though European PMI’s slump, soft data USA manufacturing and service pMI signals USA growth at 3%

( zerohedge)

iii)However this did not help the narrative: existing home sales extend their plunge from last month. It is the biggest annual drop since 2014:

iv)Mortgage applications plunge the most since 2015 as interest rates on the long end soar( zerohedge)

v)More volcanic activity underneath Yellowstone. They have experienced 200 earthquakes in the past 10 days as the ring of fire awakens

( zero hedge)

vi)Brandon Smith is another smart cookie. The following is a very important read as he states that the Fed Chairman wants to trigger a historic stock market crash as he unloads his $4.5 trillion of bonds on its balance sheet

( Brandon Smith/Alt-Market.com)

a)In an unexpected twist, the Judge in the Flynn case has demanded Mueller turn over ‘exculpatory evidence’ which would exonerate Flynn. It seems that the Judge has caught onto the fact that the FBI changed many 302’s which are interview notes. It looks like the Judge has enough evidence that McCabe altered 302’s enough to state that Flynn lied.

( zerohedge)

b)Tom Fitton is President of Judicial Watch and he has been tenacious in getting documents via Freedom of Information. He has penned an op-ed: what is the FBI hiding in its war to protect James Comey

a must read..

( Tom Fitton)

c)Trump’s 3 logical questions for Jeff Sessions

( zerohedge)

PRELIMINARY COMEX VOLUME FOR TODAY: 193,506 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 400,031 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE SIZED 3777 CONTRACTS FROM 199,752 UP TO 203,629 DESPITE YESTERDAY’S HUGE SIZED 29 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER GOOD SIZED 1293 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 28 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1321. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD NO LONG COMEX SILVER LIQUIDATION BUT A HUGE SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 5098 SILVER OPEN INTEREST CONTRACTS:

3777 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1321 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 5098 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 1 contracts LOWERING TO 76 contracts. We had 1 notices filed upon yesterday so we GAINED 0 contract or NIL ADDITIONAL oz will stand for delivery at the comex

The March contract lost 8769 contracts DOWN to 63,249

April GAINED 15 contracts UP to 165 .

.

We had 76 notice(s) filed for 380,000 OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 21/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

321.50 oz

10 kilobars

Scotia

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 32,150.000 oz

1000 kilobars Scotia |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1131 contracts

(113,100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1784 notices

178400 oz

5.5489 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

1000 kilobars

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1784) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1131 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 291,500 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1784 x 100 oz or ounces + {(1157)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 291,500 oz standing in this active delivery month of February (9.066 tonnes). THERE IS 12.52 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 26 CONTRACTS OR AN ADDITIONAL 2600 OZ WILL NOT STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,414,916.610 oz

Brinks

HSBC

|

| Deposits to the Dealer Inventory |

505,458.01

oz

Brinks

|

| Deposits to the Customer Inventory |

410,685.140 oz

JPM

Delaware

|

| No of oz served today (contracts) |

76

CONTRACT(S

(380,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(385,000 oz)

|

| Total monthly oz silver served (contracts) | 386 contracts

(1,930,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had one inventory movement at the dealer side of things

i) Into dealer Brinks: 505,458.01 oz

total inventory movement dealer: 505,458.01 oz

we had 2 inventory deposits into the customer account

i) into J.P.MORGAN:409,630.740 oz ***

ii) Into Delaware: 1054.400 oz

total inventory deposits: 410,685.140 oz

*** JPMorgan is continually adding to its inventory almost every single day.

JPMorgan now has 136 million oz of total silver inventory or 55% of all official comex silver.

we had 2 withdrawals from the customer account;

iii) Out of Brinks:: 75,670.470 oz

ii) Out of CNT:: 81,142.525 oz

total withdrawals; 290,227.110 oz

we had 1 adjustment

i) Out of Scotia: 996,251.200 was removed from the customer account and this lands into the dealer account of Scotia

total dealer silver: 45.329 million

total dealer + customer silver: 246.872 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 76 contract(s) FOR 380,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 386 x 5,000 oz = 1,930,000 oz to which we add the difference between the open interest for the front month of FEB. (76) and the number of notices served upon today (76 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 386(notices served so far)x 5000 oz + OI for front month of FEBRUARY(76) -number of notices served upon today (76)x 5000 oz equals 1,930,000 oz of silver standing for the FEBRUARY contract month.

WE GAINED 0 CONTRACT OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 110,101 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 152,370 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 152,370 CONTRACTS EQUATES TO 761 MILLION OZ OR 108% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.35% (FEB 21/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.64% to NAV (FEB 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.35%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.64%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.00%: NAV 13.68/TRADING 13.24//DISCOUNT 3.00.

END

And now the Gold inventory at the GLD/

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 21/2018/ Inventory rests tonight at 827,79 tonnes

*IN LAST 328 TRADING DAYS: 113.36 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 258 TRADING DAYS: A NET 43.95 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 215.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Feb 14/2017:

Inventory 315.271 million oz

end

HUGE SCARCITY OF GOLD IN LONDON AS THE GOLD LENDING RATE SURPASSES 2.23%

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.86%

12 Month MM GOLD LENDING RATE

+ 2.23%

GOFO = LIBOR – GOLD LENDING RATE

GOFO = 2.408 – 2.23 = .178

GOLD IS SCARCE.

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

GoldCore

Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bitcoin has ‘pretty much failed’ as a currency says Bank of England Carney

– Bitcoin is neither a store of value nor a useful way to buy things – BOE’s Carney

– Project fear against crypto-currencies or an out of control investing bubble?

– Bitcoin will likely recover in value but is speculative and not for widows and orphans

– British pound has been a terrible store of value – unlike gold

– Pound collapsed 30% in 2016 and down 11.5% per annum versus gold in last 15 years

– Fiat currency experiment may fail and dollar set to lose reserve currency status

Gold in GBP 10 Years

Sputniknews.com interview GoldCore

Sputnik: After a significant fall in the currency during December and January, Bitcoin is showing signs of a recovery in value. Could we see the coin regain value pre-2018 levels?

Mark: Yes, it’s quite possible, given the state of markets these days with the amount of liquidity that’s sloshing around the financial system due to QE and ultra loose monetary policies.

So the short answer is yes we could. But nobody has a crystal ball and nobody knows for definite. I think it’s quite interesting from a speculation point of view and I think that’s how some of the smart money around the world is seeing it — as an interesting speculation. However, it is very high risk, people need to be aware of that and it’s not for ‘widows and orphans’.

Given the degree of volatility we’ve seen in recent weeks and the massive 60% collapse we saw and also the huge risks we see with the various crypto exchanges around the world. The risk is Bitcoin’s volatility itself but also the intermediate risk and the counterpart risk behind how you own that bitcoin with exchanges having been hacked and subject to fraud.

Sputnik: Are these recent comments from Carney another attempt of asserting elements of ‘project fear’ against potential crypto-investors or a stark statement of an out of control investing bubble?

Mark: I think it’s a bit of both. I think there is a bit of an element of project fear and a lot of the central banks seem to feel threatened by Bitcoin but at the same time I think the wider cryptocurrency marketplace has been showing signs of an out of control bubble.

The cryptocurrencies – most of them, and there’s hundreds of them, were surging in value going up ten, fifty, a hundred times in value … some of them. Bitcoin, Ethereum and one or two others have real world applications, but who’s to know which cryptos will survive?

Mark Carney, Governor of the Bank of England, said they have not been a medium exchange and that’s true for a period of time now. And that’s the real vision of Satoshi Nakamoto, the Founder of Bitcoin, so it’s not a medium exchange now and it’s not showing the characteristics of storing value in recent weeks, but who’s to know? History will tell us in time whether Bitcoin does become a store for value … and it possibly could. It’s hard to know – at this stage as there is a degree of volatility that suggests that it won’t be but who knows … there are so many variables and this may change over time.

Sputnik: Back in January, we were seeing a lot people who invested in Bitcoin and other crypto-currencies actually sell and re-invest in fiat depressed currencies like Gold and Silver. Are we seeing a return of traditional assets?

Mark: There definitely was a move and we saw that ourselves, I think the smarter people in the cryptocurrency space realized the gains we were seeing were oversized and we were therefore due a sharp correction. Some of those guys were diversifying into Gold and Silver, the two primary precious metals which have a proven store of value over time with a huge amount of research behind them, showing that they are hedges and a store of value.

I think this trend will continue due to the degree of volatility we’re seeing in markets and also the big risks that are out there in terms of things like Brexit and the Trump presidency. There is a lot of political and economic uncertainty out there which will lead to an increased demand for gold.

Ultimately, Gold is a reliable store of value as fiat currencies haven’t been a store of value for some time.

Mark Carney is now presiding over The Bank of England and sterling itself has been a terrible store of value. Sterling fell 30.2% in 2016 alone after the Brexit vote and that’s a massive fall in the value of sterling in one year. Over the last 15 years sterling was down 11.4% per annum against gold (see table above).

Gold has clearly shown its characteristics as a way to protect yourself as a true store of value against devaluation of fiat currencies. Fiat currencies lose their value over time.

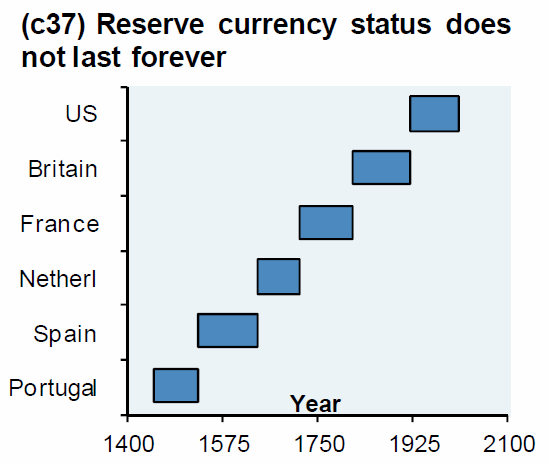

There have been many reserve currencies throughout history. If you go back to 1450, it was the Portuguese who had the reserve currency of the world. It was then the Spanish, then the Dutch, then the French, then England during the British Empire and finally, more recently we have the American Dollar as the reserve currency of the world.

The dollar and the degree of debt that Trump is running up is out of control. Trump is running up a 1 trillion-dollar plus deficits now so I think there is a real risk that the dollar and other fiat currencies are going to be further debased in the coming years.

It’s for this reason that so many techies and investors believe in Bitcoin, because they think it will act as a hedge against this risk in the same way that gold does. I think that this has yet to be seen. It may well do, but there is no guarantee because there are so many variables.

Sputnik.com interview transcript here

News and Commentary

Gold prices inch down as dollar strengthens (Reuters.com)

Asia Stocks Track U.S. Futures Down; Dollar Steady (Bloomberg.com)

Zimbabwe Plans Gold, Tobacco Diaspora Bonds as Bank Rules Change (Bloomberg.com)

Congress sets sights on federal cryptocurrency rules (Reuters.com)

Morgan Stanley Says Stock Slide Was Appetizer for Real Deal (Bloomberg.com)

Source: MarketWatch

London’s Housing Boom Is Over, Rightmove Says (Bloomberg.com)

How One of the Most Profitable Trades of the Last Few Years Blew Up in a Single Day (Bloomberg.com)

World Embraces Debt At Exactly The Wrong Time (DollarCollapse)

Gold: Another Month, Another Test Of Key Resistance – But This Time With A Difference (GoldSeek.com)

Gold Prices (LBMA AM)

20 Feb: USD 1,337.40, GBP 955.97 & EUR 1,083.83 per ounce

19 Feb: USD 1,347.40, GBP 961.10 & EUR 1,085.47 per ounce

16 Feb: USD 1,358.60, GBP 964.61 & EUR 1,086.47 per ounce

15 Feb: USD 1,353.70, GBP 962.21 & EUR 1,084.45 per ounce

14 Feb: USD 1,330.75, GBP 959.74 & EUR 1,077.77 per ounce

13 Feb: USD 1,329.40, GBP 955.04 & EUR 1,077.61 per ounce

12 Feb: USD 1,321.70, GBP 955.19 & EUR 1,077.45 per ounce

Silver Prices (LBMA)

20 Feb: USD 16.57, GBP 11.85 & EUR 13.42 per ounce

19 Feb: USD 16.72, GBP 11.92 & EUR 13.46 per ounce

16 Feb: USD 16.84, GBP 11.97 & EUR 13.49 per ounce

15 Feb: USD 16.83, GBP 11.98 & EUR 13.49 per ounce

14 Feb: USD 16.58, GBP 11.97 & EUR 13.43 per ounce

13 Feb: USD 16.61, GBP 11.94 & EUR 13.46 per ounce

12 Feb: USD 16.43, GBP 11.86 & EUR 13.39 per ounce

Recent Market Updates

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

– US-China Trade War Escalates As Further Measures Are Taken

– Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

– Is The Gold Price Heading Higher? IG TV Interview GoldCore

– Global Debt Crisis II Cometh

– Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC

– Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

– “This Is Where They Completely Lost Their Minds” – Hussman

– Brexit Risks Increase – London Property Market and Pound Vulnerable

– Peak Gold: Global Gold Supply Flat In 2017 As China Output Falls By 9%

– Crypto Currency Backlash Sees Flight From Cryptos and Bitcoin

– Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

– Shrinkflation Intensifies – Stealth Inflation As Thousands of Food Products Shrink In Size, Not Price

END

The reason gold had to be smashed yesterday: the USA (as I indicated to you yesterday) sold a massive 179 billion dollars worth of treasuries

(courtesy Harris/Bloomberg/GATA)

No wonder gold had to be smashed today

Submitted by cpowell on Wed, 2018-02-21 00:17. Section: Daily Dispatches

U.S. Floods the Market with $179 Billion of Debt in Just One Day

By Alex Harris

Bloomberg News

Tuesday, February 20, 2018

The U.S. Treasury on Tuesday sold $179 billion of securities as it works to rebuild its cash balance, with yields at its auctions of three- and six-month debt rising to levels unseen since 2008.

The government began at 11:30 a.m. New York time by auctioning $51 billion of three-month bills at a yield of 1.64 percent, 6 basis points more than similar-tenor debt sold on Feb. 12, and $45 billion of six-month bills at 1.82 percent.

Its $55 billion sale of four-week notes at 1 p.m. had a yield of 1.38 percent, with a gauge of demand known as the bid-to-cover ratio falling to 2.48, the lowest level since 2008. The first coupon offering of the week, a $28 billion auction of two-year notes, yielded 2.255 percent, the highest in almost a decade. …

The $258 billion slate of U.S. auctions set for this week is helping to push up the rates investors demand. Concerns about the U.S. borrowing cap had forced the Treasury to trim the total amount of bills it had outstanding, but with the latest debt-ceiling drama over, the government is now busy ramping up issuance. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-02-20/u-s-sells-bills-at-hi…

end

LAWRIE WILLIAMS: Russia now World no. 5 national gold holder – but is it?

Russia adds a considerable 19.7 tonnes to its official reserves which now stand at 1857. tonnes.

(courtesy Lawrie Williams/Sharp’s Pixley)

The day has come. Russia, which added 19.7 tonnes of gold to its forex reserves in January is now officially the world’s fifth largest national holder of gold as reported to the IMF. This latest figure moves it ahead of China, which has not reported any increases in its gold reserves since October 2016, in terms of reported official gold holdings.

The Russian reported total is now 1,857 tonnes as against China’s 1,842.6 tonnes, still well short of the U.S., German, Italian and French totals, but closing the gap as neither the USA, or big European gold holders have changed their reported holdings for a number of years now. It should be recognised that none of these are audited figures and the IMF relies on the levels of gold holdings as reported to it as being genuine. We have often stated that we do not believe the Chinese figures as reported, but then, in reality, one should perhaps also cast doubts on the veracity of other reported figures too – especially in relation to available gold given that, under the IMF’s reporting rules, gold which has been leased, or swapped, is allowed to remain in the official holding figure. It is known that some central banks have participated in gold leasing, or gold swap arrangements, but do not tend to report the amounts involved. The sizes of individual countries’ gold holdings have an overtly political agenda.

Regardless, we suspect the real Chinese gold reserve is considerably larger than stated and thus Russia’s position as the World No. 5 national holder of gold is perhaps unlikely with China, in reality, actually still in 5th place – or possibly even higher up the table!

Table: World Top 10 National Gold Holders*

| Rank | Country | Tonnes |

|

1 |

United States |

8,133.5 |

|

2 |

Germany |

3,373.6 |

|

3 |

Italy |

2,451.8 |

|

4 |

France |

2,436.0 |

|

5 |

Russia |

1,857.0 |

|

6 |

China |

1,838.8 |

|

7 |

Switzerland |

1,040.0 |

|

8 |

Japan |

765.2 |

|

9 |

Netherlands |

612.5 |

|

10 |

Turkey |

564.8 |

Source: IMF, Lawrieongold.com

*As reported to IMF. Russian figure as reported by central bank

As can be seen from the above table, Russia still has a long way to go before catching France and Italy in the size of its gold reserve, but at the current rate of reserve growth could be there in a little over 2 years. Given the growth in its domestic gold production, from which it is believed to source most of its reserve gold, that is not an unrealistic target.

But the enigma is China. Apart from a 15-month period leading up to the yuan’s (renminbi’s) acceptance as a constituent of the IMF’s Special Drawing Right basket of currencies, China resolutely insisted on non-reporting of monthly increases in its gold reserve figure. Instead it would announce big increases in its holdings at five or six year intervals. It very much looks as if it is returning to this policy having not announced any increase in its gold reserve for 15 straight months – yet is understood to be a firm believer in the size and value of its gold holdings in any future global economic re- alignment, as is Russia.

In both China’s and Russia’s cases, building gold reserves as an integral, and growing, part of their forex reserves may also be in order to reduce their reliance on the U.S. dollar and dollar related financial instruments in their reserves. There certainly seems to be a degree of growing U.S. economic hostility towards both nations and should this lead to a cutting off of some key financial dollar-related elements – such as access to the SWIFT global interbank system, controlled by the U.S. and its allies – then this diversification of reserves makes a lot of sense. Both Russia and China have been setting up an alternative to SWIFT which is just about ready to go live if needed.

https://www.sharpspixley.com/articles/lawrie-williams- russia-now-world-no-5-national-gold-holder-but-is- it_277004.html

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED /shanghai bourse CLOSED / HANG SANG CLOSED UP 558.26 POINTS OR 1.81%

2. Nikkei closed UP 45.71 POINTS OR 0.21% /USA: YEN RISES TO 107.48/ STILL DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index RISES TO 89.64/Euro FALLS TO 1.2340

3b Japan 10 year bond yield: FALLS TO . +.056/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.48/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.48 and Brent: 65.14

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.706%/Italian 10 yr bond yield UP to 2.056% /SPAIN 10 YR BOND YIELD UP TO 1.511%

3j Greek 10 year bond yield RISES TO : 4.481?????????????????

3k Gold at $1328.05 silver at:16.43 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 8/100 in roubles/dollar) 56.64

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.48 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9385 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1546 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.706%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.893% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.155% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures, European Stocks Slide After Poor PMIs; Dollar Gains Ahead Of Fed Minutes

The dollar rose to its highest level in a week against its G10 peers on Wednesday, rising for the 4th day against the yen and most pairs as investor focus shifted to the minutes of the Federal Reserve’s last policy meeting.

The dollar hasn’t had it this good this year, bouncing 1% so far this week after slumping 1.5% last week to the lowest level in 3 years, as traders unwound short positions ahead of today’s January FOMC minutes (where the most likely surprise would be the Fed‘s endorsement of 4 rate hikes in 2018), with investors looking for clues on just what policy makers had in mind when they added “further” twice to their guidance on interest rates.

After yesterday’s bond supply deluge, Treasury yields in the belly were steady ahead of the continued glut of supply this week, and the 10Y traded virtually unchanged and just shy of 2.89%. The Treasury’s $258 billion of auctions slated for this week comes amid a rapid jump in rates that gave impetus to one of the steepest equity sell-offs in years two weeks ago. And while investors seem to have adjusted to 10-year yields at a four-year high for now, the deluge of supply could push them even higher, above 3%, weakening the case for owning stocks at elevated valuations.

Meanwhile, US futures and world stocks looked set to fall for a third straight day: MSCI’s world stock index down 0.1%, declining for the 3rd day, as a down day in Europe offset earlier gains in Asia.

Investor attention will be on the minutes of the Fed’s last policy meeting in late January. The last readings of U.S. wages and inflation came in higher than expected, with some blaming the numbers for prompting a violent selloff in stocks earlier this month.

“Markets are particularly sensitive to inflation, and we think the odds that the minutes reinforce the narrative of firming inflation are high,” said Elsa Lignos, RBC’s global head of FX strategy. “We think there is a high probability that the Fed moves the dots to four hikes in 2018 (from three) near-term and that the minutes could be another step in that direction.”

* * *

In Europe, almost every sector of the Stoxx 600 Index fell, with the gauge tracking losses in the U.S. on Tuesday rather than a more positive mood in Asia after Markit data showed a fading outlook for manufacturing and services in the region, prompting some to ask if the recovery momentum has now peaked. The risk-off tone permeating European trading came as PMI data missed estimates across the board, first in France, then Germany and finally for the whole EU:

- Euroarea PMI Manufacturing 58.5 vs. Exp. 59.2 (Prev. 59.6)

- Euro-area PMI Services 56.7 vs. Exp. 57.6 (Prev. 58.0)

- Euro-area PMI Composite 57.5 vs. Exp. 58.5 (Prev. 58.8)

European equities led lower by technology, while FTSE 100 outperforms slightly after earnings from Lloyds and Glencore. In terms of sector specifics, telecoms outperform their peers amid strong earnings from Orange (+2%), to the downside, energy names lag their peers amid price action seen across the commodities complex. Other individual movers include Glencore (+4.1%), Lloyds (+1.6%) and who sit near the top of the FTSE 100 following their respective earnings. Elsewhere, other notable movers include Accor (+2.4%), Atos (-3.7%) and Iberdrola (-3.4%) post-earnings, whilst AA (-22.1%) lag the Stoxx 600 after a disappointing strategy update.

Lower than expected readings of purchasing manager surveys in France, Germany and the euro zone all came in lower than expected, stabilizing euro zone bond markets. Bunds rallied from the open across the curve; UST/bund 10-year spread widens toward key 220bps level, which was last seen in January 2017.

* * *

Earlier during the Asian session, MSCI’s index of Asia-Pacific shares outside Japan rose 0.7 percent after slipping earlier in the session following the U.S. market losses, which snapped a six-session winning streak. Stocks climbed in Hong Kong ahead of China’s return from the week-long Lunar new year holiday on Thursday, cementing a rebound from one of the worst sell-offs in years at the start of the month. As the Asian session progressed a combination of the fall in US equity futures and 1% declines in crude prices, the Nikkei had briefly dipped into negative territory. Elsewhere, the ASX 200 (+0.1%) had opened lower in response to the falls on Wall Street but has recovered into positive territory. Mining names the largest drag on the index with BHP and Fortescue both losing ground following soft earnings. Hang Seng (+1.8%) traded higher amid HSBC shares recovering from yesterday’s declines.

In FX, after soft U.K. domestic employment report, GBP/USD extends losses through yesterday’s low while gilt futures hit two-week high. The euro traded in a narrow range that was yawn-inducing for traders even though euro-area PMI missed estimates, while the pound was buffeted by weak jobs data out of the U.K. EUR/USD edges lower to approach 1.2300 as USD continues strength seen from last three sessions. However, not even the weaker Euro could push European stocks higher.

Asia’s emerging currencies were mostly lower amid a rising dollar and elevated Treasury yields. The Taiwan dollar the main exception as it reopened after the Lunar New Year holidays. Sovereign bonds advanced and Taiwan led regional stock gains. A deluge of new supply is pushing down Treasuries and spurring speculation the U.S. 10-year yield could breach the watershed 3 percent level as early as this week, which would reduce the attractiveness of developing-nation assets. The Federal Reserve will release minutes of its latest meeting later on Wednesday.

“The ongoing USD rebound alongside higher UST yields is likely to pressure Asian currencies,” said Mizuho’s FX strategist, Ken Cheung. “With a light calendar, the USD movement will remain the main driver for the Asian FX. The CNY fixing after the long holiday will be the focus,” with recent developments suggesting no big changes, he said.

In the neverending drama surrounding Brexit, a UK Official said they are in a broad alignment with the EU on the transition period. Meanwhile, PM May is facing pressure after 62 Tory hardliners demand clean Brexit, with lawmakers challenging May to take a harder approach on how far UK rules should move away from the EU after Brexit and the nature of the transition period.

The stronger dollar weighed on commodities, with Brent crude futures losing 1 percent to $64.61 per barrel and U.S. crude oil futures also slipping 1 percent to $61.16. U.S. crude hit a near two-week high the previous day on news of inventory declines at a key storage hub and from expectations that top OPEC producers could extend cooperation beyond 2018. Spot gold touched a one-week low of $1,329.42 an ounce due to the resurgent dollar, having declined 1.4 percent so far this week.

On today’s economic data calendar, we have Markit PMI data and home sales. Scheduled earnings include Dish and The Southern Company.

Bulletin headline Summary from RanSquawk

- European equities (Eurostoxx 50 -0.7%) trade lower across the board amid lacklustre Eurozone PMIs and a dip in US equity futures

- USDJPY has built on gains above the 2017 low (107.32), but stalled just before 108.00 amidst another bout of global stock market weakness

- Looking ahead, highlights include Eurozone and US PMIs, US existing home sales, FOMC minutes and a slew of speakers

Market Snapshot

- S&P 500 futures down 0.07% to 2,712.00

- STOXX Europe 600 down 0.5% to 378.62

- MSCI Asia Pacific up 0.3% to 177.20

- MSCI Asia Pacific ex Japan up 0.9% to 581.18

- Nikkei up 0.2% to 21,970.81

- Topix down 0.05% to 1,761.61

- Hang Seng Index up 1.8% to 31,431.89

- Shanghai Composite up 0.5% to 3,199.16

- Sensex up 0.4% to 33,821.09

- Australia S&P/ASX 200 up 0.05% to 5,943.72

- Kospi up 0.6% to 2,429.65

- German 10Y yield fell 3.0 bps to 0.705%

- Euro down 0.1% to $1.2321

- Brent Futures down 0.9% to $64.67/bbl

- Gold spot unchanged at $1,329.24

- U.S. Dollar Index up 0.2% to 89.86

- Italian 10Y yield rose 2.6 bps to 1.8%

- Spanish 10Y yield fell 0.6 bps to 1.525%

Top Overnight News from Bloomberg

- Lloyds to Invest $4.2 Billion in Technology, Plans Share Buyback

- Glencore M&A Firepower Undiminished After $2.9 Billion Dividend

- Prime Minister Theresa May is facing a potentially dangerous outcry from 62 members of her own party who are demanding a quick, clean break from the European Union, just as she tries to finalize her Brexit plans

- Japanese Lifers: Meiji Yasuda Life (AUM $353b): increasing holdings of unhedged U.S. debt; investing mostly in Ginnie Mae, some in credit and Treasuries

- ECB’s Vasiliauskas: we have not seen an unwarranted tightening in conditions; appropriate to rephrase guidance to focus on all instruments, not just QE: Reuters

- U.K. Dec. Unemployment Rate: 4.4% vs 4.3% est; Avg. Weekly Earnings 2.5% vs 2.5% est.

- Apple Is Said to Negotiate Buying Cobalt Direct From Miners

- Democrats Counter GOP Tax-Cut Pitch by Warning of Long-Term Pain

- Unibail Says Malls Will Evolve to Counter the Threat of Amazon

- Gibson Creditors Are Said to Want New CEO Before Rescue Deal

- Brexit Secretary David Davis will set out U.K.’s official response to EU’s transition proposals before the U.K. parliament in a written statement on Wednesday, Politico reports; Davis to demand mechanism to protect U.K. from any “harm” caused by new EU rules and regulations introduced during transition period

- Merck to Purchase Viralytics in Deal Valued at A$502m

- Takeover Target Fidessa Gains as Activist Elliott Reveals Stake

- AA Shares Plunge Most Since Debut After Predicting Profit Drop

- Output of Faulty Airbus Engine to Double, Suggesting Likely Fix

- A preliminary composite purchasing managers’ index for the euro-zone retreated in February to 57.5, from 58.8, and missing the median estimate of 58.4

Asian equities are trading with modest gains this morning, in what has been a relatively quiet session. Nikkei 225 (+0.2%) had been up as much as 1.2% with the JPY continuing to weaken across the board in which USD/JPY hovering around 1.08. Although, as the session progressed a combination of the fall in US equity futures and 1% declines in crude prices, the Nikkei had briefly dipped into negative territory. Elsewhere, the ASX 200 (+0.1%) had opened lower in response to the falls on Wall Street but has recovered into positive territory. Mining names the largest drag on the index with BHP and Fortescue both losing ground following soft earnings. Hang Seng (+1.8%) traded higher amid HSBC shares recovering from yesterday’s declines. In credit markets, the US Treasury curve is modestly flatter in the Asia-Pacific session, with the 10-Year yield last 0.4bp higher at 2.89%. JGBs trading in a tight range, with the 10yr up by 3 ticks.

Top Asian News

- Yen Surge Ends $353 Billion Insurer’s Wait to Buy U.S. Bonds

- Hong Kong Shares Soar Ahead of China’s Return From Holiday

- At Last, a Woman Takes Center Stage for India’s Tech Industry

- How a $1.8 Billion Indian Bank Fraud Lasted Seven Years

- Hong Kong Traders Return to Recent Listings as Razer Surges 24%

European equities (Eurostoxx 50 -0.7%) trade lower across the board amid lacklustre Eurozone PMIs and a dip in US equity futures overnight. In terms of sector specifics, telecoms outperform their peers amid strong earnings from Orange (+2%), to the downside, energy names lag their peers amid price action seen across the commodities complex. Other individual movers include Glencore (+4.1%), Lloyds (+1.6%) and who sit near the top of the FTSE 100 following their respective earnings. Elsewhere, other notable movers include Accor (+2.4%), Atos (-3.7%) and Iberdrola (-3.4%) post-earnings, whilst AA (-22.1%) lag the Stoxx 600 after a disappointing strategy update.

Top European News

- U.K. Wages Pick Up as Fewer Foreign Workers Take Jobs

- Berlusconi Poaching Among Five Star Ranks: Italy Campaign Trail

- Euro Area Hits Speed Bump on Road to Faster Economic Growth

- German Economy on Track for Fastest Quarterly Growth Since 2011

- Black Sea Gas to Flood Nation That Can’t Decide on a Use for It

In currencies, Asian contacts are said to have attributed the latest Dollar leg-up to a further ‘technical correction’, and for the DXY 90.000 will be next on the radar given its psychological significance, but chart-wise nearest resistance resides between 90.500-600 as the index trades within a 89.935-700 range. Looking at basket components, Usd/Jpy has built on gains above the 2017 low (107.32), but stalled just before 108.00 amidst another bout of global stock market weakness. However, Jpy puts at the big figure have reportedly been in demand as the headline pair hovers around 107.50, with bids seen at 107.20. Eur/Usd is testing key Fib support at 1.2319 and buying interest into 1.2300 in wake of French, German and pan-EZ flash PMIs that missed consensus across the board. A downside break of 1.2300 exposes recent lows circa 1.2275 and stops below, but on the upside 1 bn option expiries run-off today between 1.2300-20. GBP initially faced selling pressure in the wake of the latest UK jobs figures despite the firmer than expected earnings ex-bonus release (prev. revised lower), with the report met by an unexpected uptick in the UK unemployment rate, slowdown in employment growth and the earnings release perhaps not enough to change the narrative at the BoE and nail on a May hike. However losses were then pared as it appears that the UK are now in a broad agreement with the EU on a transition period. Aud/Usd another notable mover, and retreating some distance from 0.7900 towards 0.7842 interim support despite former than forecast Aussie wages overnight as the breakdown was not as encouraging as the headline numbers appeared.

In the commodities complex, WTI and Brent crude futures are seen lower alongside the firmer USD after taking a tumble during Asia-Pac trade. In terms of energy specific newsflow, things remain light ahead of tonight’s rescheduled API release with traders wary over any further climbs in US production. In metals markets, spot gold has recovered from modest overnight losses to trade relatively unchanged as markets await today’s FOMC minutes release. Elsewhere, price action across the rest of the complex remains light as Chinese participants away are still away from market.

Looking at the day ahead, the flash February PMIs on manufacturing, services and composite are due in the US. Other data due includes January existing home sales data in the US. Away from this, the FOMC minutes from the January meeting are due late in the evening, while the Fed’s Harker is scheduled to speak on the economic outlook in the afternoon.

US Event Calendar:

- 7am: MBA Mortgage Applications, prior -4.1%

- 9:45am: Markit US Manufacturing PMI, est. 55.5, prior 55.5; Services PMI, est. 53.7, prior 53.3; Composite PMI, prior 53.8

- 10am: Existing Home Sales, est. 5.6m, prior 5.57m; MoM, est. 0.54%, prior -3.6%

- 2pm: FOMC Meeting Minutes

Central Bank Speakers

- 9am: Fed’s Harker Speaks on the Economic Outlook

- 10am: Kashkari speaks in Minneapolis on Bloomberg Television

- 2pm: FOMC Meeting Minutes

- 8:20pm: Kashkari speaks at Bloomberg event in Minneapolis

DB’s Jim Reid concludes the overnight wrap

Today is the biggest day in a quiet week for data. The highlight will be the flash February PMIs with manufacturing, services and composite readings due in Europe and the US. As a reminder, the January manufacturing reading for the Euro area came in at an impressive 59.6, albeit slightly down from the highs above 60 in December and November last year. The consensus is for another small pullback to 59.2, while the composite is expected to edge down to a still solid 58.4 from 58.8. Outside of this, we also see the monthly UK employment release with eyes on wages as the BoE gets closer to their next hike. UK data and/or BoE hawkishness has caused global yields to sell off sharply a couple of times in recent months so the release will be important. Finally FOMC minutes from the January meeting (Yellen’s last) will be out tonight but it will be outdated news given it occurred before the higher AHE’s and CPI/ PPI prints and before the market sell-off.

Staying with yields, the big focus over the last 24 hours has been this week’s large Treasury supply. Overnight the US treasury has sold US$179bn of debt securities with yields at its auctions of three / six month bills and two year notes

($28bn at 2.255%) reaching the highest in c10 years. Notably, demand for the securities were reasonably sound with bid-to-cover ratio of 2.74x, 3.11x and 2.72x (vs. 3.22x previous) respectively. Looking ahead, auctions for 5 and 7 year notes will occur in the next two days. Elsewhere, core 10y bonds yields were little changed, with the UST 10y up 1.5bp to 2.89% while Bunds were flat and Gilts fell 1.7bp. The UST 2y was up 2.9bp to 2.221% and is higher again this morning.

In US equities, the S&P fell for the first time in seven days (-0.58%) with all sectors but tech stocks modestly up. The index was weighted down by the consumer staples sector, in particular Walmart as it fell the most in c30 years (-10.2% vs. -10.3% in Jan. 1988) after guiding to a lower than expected earnings outlook and a slower push into online sales. The Dow (-1.01%) and Nasdaq (-0.07%) also retreated. Conversely, European bourses were broadly higher as the Euro weakened and largely reversed Monday’s decline. Across the region, the Stoxx (+0.60%) and DAX (+0.83%) both rebounded while the FTSE was marginally lower. Elsewhere, the VIX is up for the second straight day and now back up above 20 (+5.9% to 20.60).

This morning in Asia, markets are modestly higher, with the Nikkei (+0.05%), Hang Seng (+0.98%) and Kospi (+0.47%) all up as we type. Elsewhere, the February Nikkei manufacturing PMI eased mom to 54 (vs. 54.8 previous). Recapping other markets performance from yesterday, in FX, the US dollar index jumped 0.69% while the Euro and Sterling fell 0.56% and 0.03% respectively. In commodities, WTI oil rose for the fourth consecutive day (+0.39%). Precious metals weakened c1.3% (Gold -1.28%; Silver -1.34%) and other LME base metals also retreated modestly (Copper -0.39%; Zinc -0.14%; Aluminium -1.31%).

Away from markets, the Handelsblatt reported that given Germany’s strong support for Spain’s Economy Minister Luis de Guindos to be the next Vice President of the ECB, unnamed German officials now hope this would set the stage for Bundesbank’s Weidmann to be first ECB President from Germany after Mr Draghi’s terms ends in October 2019. According to these officials, the swing factor may depend on the relative support of French President Macron. Staying in Europe, the EC spokesman Ms Schinas said the EU is “deeply concerned” by any US trade sanctions impacting EU businesses. She added “we would be taking appropriate measures to defend EU industry, and we stand ready to react swiftly….in case our exports are affected by restrictive trade measures from the US”.

Now onto some of the Brexit headlines. When asked if the UK will withhold the divorce Brexit payment to achieve the trade deal that it wants with the EU, the Brexit Secretary Davis said the “withdrawal agreement and the future relationship (between the UK and EU) are intertwined….and not separate issues”. He also noted trade must be as open and “frictionless” as possible between the two sides and that the UK and the EU will continue to work together as partners on regulations, where the UK is determined “to lead a race to the top in global standards”. Elsewhere, Foreign Secretary Johnson has said “there is no reason” why the UK and EU can’t have frictionless trade if Britain leaves both the customer union and single market. Conversely, the opposition leader Mr Corbyn has confirmed the Labour Party will support Britain remaining inside a customs union. He noted “we have to have a customs union that makes sure we can continue to trade, particularly between Northern Ireland and the Republic of Ireland…” Looking ahead, we should have more clarity next week when PM May is expected to set out her vision for the post Brexit trade deal after extensive cabinet discussions this week. Her task has been made more difficult by an open letter from 62 Eurosceptic Tory MPs insisting on elements of a hard Brexit just as hope was emerging that she could find a united cabinet position.

Finally onto some central bankers commentaries. The Riksbank Deputy Governor Floden said “we have to be cautious moving forward not to surprise markets too much (on rates) and generate negative market reactions….for example…too rapid appreciation of the Krona”. He added, “most likely” we will raise repo rates in 2HCY18 and then “roughly 50bp per year under the forecast horizon”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In Germany, the January PPI was above market at 0.5% mom (vs. 0.3%) and 2.1% yoy (vs 1.8% expected). The February ZEW survey on the current situation was lower than expected at 92.3 (vs. 93.9) with the expectations index beating at 17.8 (vs. 16 expected). For the Euro area, the February ZEW survey on expectations eased to 29.3 (vs. 31.8 previous) while consumer confidence was also below expectations at 0.1 (vs. 1.0) following a fresh 17 year high back in January. Finally, in the UK, the February CBI trend total orders were a tad softer at 10 (vs. 11 expected).

Looking at the day ahead, the flash February PMIs on manufacturing, services and composite are due in Germany, France and the Euro area. Later on we’ll then get the same data in the US. Other data due includes December and January employment indicators in the UK, and January existing home sales data in the US. Away from this, the FOMC minutes from the January meeting are due late in the evening, while the Fed’s Harker is scheduled to speak on the economic outlook in the afternoon. The BoE’s Carney, Broadbent, Haldane and Tenreyro are also due to testify to Parliament’s Treasury Committee on the Inflation Report.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed /Hang Sang CLOSED UP 558.26 POINTS OR 1.81% / The Nikkei closed UP 45.71 POINTS OR 0.21%/Australia’s all ordinaires CLOSED UP 0.03%/Chinese yuan (ONSHORE) closed UP at 6.3415/Oil DOWN to 61.48 dollars per barrel for WTI and 65.14 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED XXX AGAINST THE DOLLAR AT XXX. OFFSHORE YUAN CLOSED XXX AGAINST THE ONSHORE YUAN AT XXX//ONSHORE YUAN /OFFSHORE YUAN NOT TRADING

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

end

4. EUROPEAN AFFAIRS

Italy

In Italy, Tax evasion is considered a sport. Now the Italian government has introduced a new automated tax snitch program trying to get at tax cheats. Originally they had a program which highlighted if you spent too much one expenses that you had evaded taxes. Now a new program: if you do not access your bank account often enough, or save too much, you are targeted

a good one…

(courtesy Simon Black/SovereignMan)

Meet The Italian Government’s Orwellian New Automated Tax Snitch

Authored by Simon Black via SovereignMan.com,

By the end of the 3rd century AD, the finances of ancient Rome were in terminal crisis.

Years and years of debasing the currency had resulted in severe hyperinflation– a period of Roman history known as the Crisis of the Third Century (from AD 235 through AD 284).

During the time of Julius Caesar, for example, the Roman silver denarius coin was nearly 98% pure silver.

Two centuries later in the mid-100s AD, the silver content had fallen to 83.5%.

And by the late 200s AD, the silver content in the denarius was just 5%.

As the money continued to be devalued, prices across the Empire skyrocketed.

Wheat, for example, rose in price by over 4,000% during the first three decades of the third century.

Rome was on the brink of collapse. And when Emperor Diocletian came to power at the end of the third century, he tried to stabilize the economy with his ill-fated Edict on Wages and Prices.

Diocletian’s infamous decree fixed the price of everything in the Empire. Food. Lumber. Salaries. Everything.

And anyone caught violating the prices set forth in his edict would be put to death.

Another one of Diocletian’s major policies was reforming the Roman tax system.

He mandated widespread census reports to determine precisely how much wealth and property each citizen had.

They counted every parcel of land, every piece of livestock, every bushel of wheat, and demanded from the population increasing amounts of tribute.

And anyone found violating this debilitating tax policy was punished with– you guessed it– the death penalty.

Needless to say, Diocletian’s reforms didn’t work.

Every high school economics student knows that wage and price controls don’t work… and that excessive taxation bankrupts the population.

But that doesn’t stop governments from trying the same tactics over and over again.

Fast forward about seventeen centuries and Italy is once again in the same boat.

The Italian government is one of the most bankrupt in the world; its debt level is an unbelievable 132% of GDP– and rising.

In other words, the Italian government’s debt is substantially larger than the value of the entire Italian economy.

It’s almost as bad as Greece, and it grows worse each year as the national government routinely runs budget deficits.

Their only solution, of course, is hiking taxes and increasing regulation… exactly the opposite of what they should be doing.

And, just like the ancient Romans, the government is on a witch hunt for anyone they think (in their sole discretion) might be dodging taxes.

They already have a system in place called the redditometro, an automated tool for the tax authorities to comb through income and expense records of Italian residents.

The algorithm finds anyone whose expenses were higher than his/her income and presumes that s/he has been evading taxes.

The irony here is pretty profound given that the Italian government itself has expenses that are higher than its income.

After all, that’s how it ended up with such a prodigious debt level.

Earlier this month, however, the Italian tax authorities rolled out a brand new tool called risparmiometro. And this one is really insidious.

Risparmiometro goes through ALL financial records – credit card transactions, bank accounts, investment accounts, etc. to determine whether or not someone has too much savings relative to his/her occupation.

Think of the implication.

Under the redditometro system, if you spend too much money, they think you’re evading taxes.

But under the risparmiometro system, if you save too much money, they think you’re evading taxes.

Unbelievable.

But it gets better.

Risparmiometro (the new tool) also looks at bank activity to see how frequently you’re using the account.

And if you’re not using the account frequently enough, the government assumes that it’s because you’re dealing in cash… and evading taxes.

I have no doubt that there’s a substantial amount of tax evasion in Italy.

I spend several weeks in the country every summer, and I see how much people and businesses are suffering.

And they’re definitely coming up with creative ways to survive.

But rather than take the necessary steps to liberate the economy, the government continues to double down on more taxes and more regulation… and then invest their remaining energy to develop new tools to spy on their citizens.

Two key points here:

1) Nearly ALL bankrupt governments invariably resort to this tactic at some point.

2) It’s also a great way to engineer a banking crisis.

Think about it– Italy’s banks are already teetering on collapse. Some have already failed, others are almost there.

If Italians know that the government is spying on every transaction they make (or don’t make), who in his/her right mind would want to keep money in an Italian bank?

Anyone with half a brain will be moving funds to Switzerland or Austria.

Italy’s banks are so fragile, though, that they won’t be able to survive if even a small percentage of their depositors flee.

So as the Italian government rolls out this new tool in the latest campaign of its tax jihad, they’re all but guaranteeing widespread bank failure.

It’s genius.

To continue learning how to legitimately reduce your taxes, I encourage you to download our free Perfect Plan B Guide.

Merkel Is Forming A Coalition With The Wrong Party

The last time I looked at the miasma of German coalition talks the big takeaway was the mood turning against the Social Democrats (SPD).

Today the latest polling confirms that the more Merkel tries to form a coalition with Martin Schultz and the SPD the more support the coalition loses.

There have been two polls recently, one which grabbed headlines showing that anti-immigration, Eurosceptic Alternative for Germany (AfD) is now ahead of the SPD nationally, 16% to 15.5%. Another has AfD rising two points to 14%, though still four points behind the SPD.

The takeaway from these polls is not whether AfD is or is not more popular than the SPD at this point. Coupling those results with the surprising rise of Angela Merkel’s Union party by two points in both polls a clear message from the German electorate emerges.

They want a government formed because they are unaccustomed to being without one, but they don’t want another grand collation between Merkel and the SPD.

That is the kind of formless, opinion-allergic government the German people are sick of. They had that for the past four years and all it got them was more subservience to both Brussels and Washington D.C.

No, since Merkel has staunched the flow of immigrants into Germany – to help her re-election campaign – her leadership is, for now, acceptable to get things done. But, what the German people are telling everyone is that they want her to shift farther ‘right’ rather than left in order to appease the SPD.

And that means a coalition with AfD, which, of course, is not possible with the current political leadership in Germany. And that’s why AfD continues to take a larger bite out of the electoral pie.

Don’t Believe the Numbers

A new article over at the American Conservative by Doug Bandow goes into some great detail on the dynamics at play here. He rightly points out that Germans are unhappy with the current status quo.