GOLD: $1326.60 DOWN $8.00

Silver: $16.50 DOWN 27 CENTS

Closing access prices:

Gold $1325.40

silver: $16.50

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1341.05 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1335.00

PREMIUM FIRST FIX: $6.05

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1340.26

NY GOLD PRICE AT THE EXACT SAME TIME: $1333.75

PREMIUM SECOND FIX /NY:$6.51

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1332.50

NY PRICING AT THE EXACT SAME TIME: $1333.10

LONDON SECOND GOLD FIX 10 AM: $1329.40

NY PRICING AT THE EXACT SAME TIME. $1330.44???

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR NIL OZ.

TOTAL NOTICES SO FAR:2749 FOR 274900 OZ (8.5505 TONNES),

For silver:

MARCH

302 NOTICE(S) FILED TODAY FOR

1510,000 OZ/

Total number of notices filed so far this month: 4524 for 22,620,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,557/OFFER $10,627: DOWN $129(morning)

Bitcoin: BID/ $9907/offer $9978: DOWN $777 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE SIZED 3100 contracts from 193,489 RISING TO 196,590 WITH YESTERDAY’S HUGE 38 CENT RISE IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 4470 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 4470 CONTRACTS. WITH THE TRANSFER OF 4470 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4440 CONTRACTS TRANSLATES INTO 22.35 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

12,977 CONTRACTS (FOR 5 TRADING DAYS TOTAL 12,977 CONTRACTS OR 64.89 MILLION OZ: AVERAGE PER DAY: 2595 CONTRACTS OR 12.977 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 64.89 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.27% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 557.36 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD ZERO LOSS IN COMEX OI SILVER COMEX WITH THE 18 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 4470 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 4470 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 7570 OI CONTRACTS i.e. 4470 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3100 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 38 CENTS AND A CLOSING PRICE OF $16.77 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.968 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 17 NOTICE(S) FOR 85,000 OZ OF SILVER

In gold, the open interest ROSE BY A STRONG 8,498 CONTRACTS RISING TO 508,100 . WITH THE CONSIDERABLE RISE IN PRICE YESTERDAY ($15.60) HOWEVER FOR TUESDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN HUGE SIZED 14,232 CONTRACTS THE ISSUANCE OF, APRIL SAW THE ISSUANCE OF 14,232 CONTRACTS , JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 508,100. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUGE GAIN CONTRACTS: 8498 OI CONTRACTS INCREASED AT THE COMEX AND A HUGE SIZED 14232 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(22,730 oi GAIN in CONTRACTS EQUATES TO 37.85 TONNES)

YESTERDAY, WE HAD 4962 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 54,267 CONTRACTS OR 5,426,700 OZ OR 168.79 TONNES (5 TRADING DAYS AND THUS AVERAGING: 10,855 EFP CONTRACTS PER TRADING DAY OR 1,085,500 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 5 TRADING DAYS IN TONNES: 168.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 168.79/2550 x 100% TONNES = 6.59% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1420.99 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX WITH THE CONSIDERABLE RISE IN PRICE IN GOLD TRADING YESTERDAY ($15.60). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,232 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14232 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 22,730 contracts ON THE TWO EXCHANGES:

14232 CONTRACTS MOVE TO LONDON AND 8,498 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 37.85 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $8.00 : A SLIGHT CHANGES IN GOLD INVENTORY AT THE GLD /A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES.

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER DOWN 27 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 3100 contracts from 193,489 UP TO 196,590 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE CONSIDERABLE PRISE IN PRICE OF SILVER (38 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 4470 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 3100 CONTRACTS TO THE 4470 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE GAIN OF 7570 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 37.85 MILLION OZ!!!

RESULT: A CONSIDERABLE INCREASE IN SILVER OI AT THE COMEX WITH THE STRONG RISE OF 38 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD SIZED 4470 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/LATE TUESDAY NIGHT: Shanghai closed DOWN 17.97 POINTS OR 0.55% /Hang Sang CLOSED DOWN 313.81 POINTS OR 1.03% / The Nikkei closed DOWN 165.04 POINTS OR 0.77%/Australia’s all ordinaires CLOSED DOWN 0.93%/Chinese yuan (ONSHORE) closed UP at 6.3196/Oil DOWN to 62.18 dollars per barrel for WTI and 65.22 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AT 6.3196 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3175 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY BUT LOUSY CHINESE MARKETS AND GLOBAL MARKETS/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

ItalySnyder writes that Italy is doomed due to the advance in the euroskeptic parties.

( Jeffrey Snyder/Alhambra Investment Partners)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The following is an extremely important paper by Stewart Dougherty and the subject is very dear to my heart…the fact that the USA does not have beneficial official gold and thus the reasons for the constant raids

it is long but well worth it…

( Stewart Dougherty)

ii)Real Vision’s Grant William confirms market rigging by governments:

( Grant Williams/GATA)

iii)

Gold expert Labourne states that the use og gold derivatives by the BIS declines by 55 tonnes and that helped gold rebound.

( Labourne/GATA)

10. USA stories which will influence the price of gold/silver

i)Gary Cohn resigns!!

iii)Early trading: why the Cohn resignation is far worse than markets think!!

( Mark Cudmore)

iv)Wall Street reacts to the departure of Cohen:

( zerohedge)

v)It begins; Trump to sign the import tariffs tomorrow. We will see any country exclusions, if any, tomorrow

(courtesy zero hedge)

vi)Atlanta Fed President Bostic warns that trade wars may delay the implementation of rate hikes

(courtesy zerohedge)

vii)Morning data/trade data

( zerohedge)

viii)The following is the key data point that the Fed is looking for: wage growth and it is at its lowest level in 9 years:

( zerohedge)

(courtesy Jay Syrmopolous/TruthinMedia.com)

x)Navarro not on the list to replace Cohn: probable choice Larry Kudlow, a doorknob, but an anti tariff person. Should be interesting

( zerohedge)

xi)Finally we see USA credit card usage slow down a bit: an increase of only $ 0.700 billion. The drop in January of credit card debt (probably to pay for December purchases) is probably another signal of problems in the economy that which we are witnessing.

( zerohedge)

a)Peter Strzok ignored evidence of the Clinton hack and changed the wording of that a foreign hack actors from “reasonably likely” to “probable” so they could say that Clinton’s misuse of her server as extremely careless but not grossly negligent.

( zerohedge)

b)Have fun with this: Our porn star sues Trump who forgot to sign his non disclosure

( zerohedge)

c)The USA now sues sanctuary California:

( zerohedge)

( zerohedge)

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: N/A contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: N/A CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE 3100 CONTRACTS FROM 190,630 UP TO 196,590 DESPITE YESTERDAY’S 38 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 4470 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 4470. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD NO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 7570 SILVER OPEN INTEREST CONTRACTS

3100 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 4470 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:7570 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month GAINED 3 contracts RISING TO 957 contracts. We had 17 contracts filed upon yesterday, so we GAINED 20 contracts or an additional 100,000 will stand in this active delivery month of March.(AS SOMEBODY IS IN GREAT NEED OF PHYSICAL SILVER)

April GAINED 30 contracts RISING TO 440 .

The next big active delivery month for silver will be May and here the OI GAINED 89 contracts UP to 148,382

We had 302 notice(s) filed for 1,520,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 7/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

160,871.779 oz

DELAWARE

Scotia

I-D

MALCA

HSBC

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | 178,176.636 OZ

JPM |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

608 contracts

(60800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

0 notices

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (0) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (608 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 60800 oz, the number of ounces standing in this nonactive month of MARCH (1.8912 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (0 x 100 oz or ounces + {(608)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 60800 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 71 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

2.005.100 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

10,786.724 oz

Delaware

CNT

|

| No of oz served today (contracts) |

302

CONTRACT(S

(1,520,000 OZ)

|

| No of oz to be served (notices) |

655 contracts

(3,275,000 oz)

|

| Total monthly oz silver served (contracts) | 4524 contracts

(22,620,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 2 deposits into the customer account

i) Into Delaware: 7856.724 oz

ii) Into CNT: 2940.190 oz

ii) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

total deposits customer account: 8973.527 oz

JPMorgan did not add any silver into its warehouses (official) today.

total deposits today: 10,796.224 oz

we had 1 withdrawals from the customer account;

i) Out of Delaware 2005.100 oz

total withdrawals; 2005.100 oz

we had 1 adjustments

i) out of CNT: 1,137,558.990 oz was adjusted out of the customer is this landed into the dealer account of CNT

total dealer silver: 58.592 million

total dealer + customer silver: 251.724 million oz

The total number of notices filed today for the March. contract month is represented by 302 contract(s) FOR 1,510,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4524 x 5,000 oz = 22,620,000 oz to which we add the difference between the open interest for the front month of Mar. (957) and the number of notices served upon today (302 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4524(notices served so far)x 5000 oz + OI for front month of March(957) -number of notices served upon today (302)x 5000 oz equals 25,895,000 oz of silver standing for the March contract month.

We GAINED an additional 20 contracts or 100,000 additional silver oz will stand for delivery at the comex as somebody ws in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: N/A CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: N/A CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF N/A CONTRACTS EQUATES TO N/A MILLION OZ OR N/A% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.76% (MARCH 7/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.50% to NAV (March 7/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.76%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.50%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2/91%: NAV 13.68/TRADING 13.28//DISCOUNT 2/91.

END

And now the Gold inventory at the GLD/

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 7/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 337 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 267 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

MARCH 7/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 318.069 million oz

end

6 Month MM GOFO 2.00/ and libor 6 month duration 2.24

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.00%

libor 2.24 FOR 6 MONTHS/

GOLD LENDING RATE: .24%

XXXXXXXX

12 Month MM GOFO

+ 2.40%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.10

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Does Not Fear Interest Rate Hikes

Gold Does Not Fear Interest Rate Hikes

– Gold no longer fears or pays attention to Fed announcements regarding interest rates

– Renewed interest in gold due to inflation fears and concern Fed won’t do enough to control it

– Higher interest rates on horizon will make debt levels unsustainable

– New Fed Chair warns “the US is not on a sustainable fiscal path” and could lead to an “unsustainable” debt load

– Higher interest rates are good for gold as seen in the 1970s and 2000s

– Gold markets aware that central banks are running out of financial weapons to deal with crises

You wouldn’t believe it by looking in the financial news but the price of gold has had a stellar run over the last few years. Since the beginning of the year it is up nearly 10%, contributing to the near 30% rise since early 2016. Most recently it has been thanks to a weaker dollar, but longer-term it is due to the disbelief gold has in central banks.

Many commentators and market observers did not expect gold to rise as it has: the same period included interest rate rises from the Federal Reserve, something once considered to be the gold market’s kryptonite.

But instead of driving the gold price down, US interest rate hikes have had little impact. One of the key factors supporting the gold price is the very same factor that has central bankers spooked – inflation.

Gold investors have realised that whilst interest rate hikes are likely to continue, the factors they are trying to combat (namely inflation) are now so far beyond central bankers’ control that gold remains an attractive safe haven and asset class.

Interest rate hikes are inevitable but gold sees past them

Inflation in the US is on the move — the PPI measured 2.2% in February. That might not seem like much but don’t forget that the markets are not prepared for higher inflation. Consider reactions back in January when it dawned on market participants that inflation could not stay this low forever.

Higher inflation will inevitably mean even more interest rate hikes. Surely this is a good thing? Perhaps, but is it too little too late?

Sadly central bankers seem to one step behind, rather than one step ahead when it comes to monetary policy. As we have seen since the financial crisis struck, central banks are reactors rather than actors when it comes to preventing seismic events.

Those investing in gold recognise that central banks can increase rates as much as they like. But a rapid reaction such as this can lead to dangerous problems for the debt-laden side of the market.

Interest rate increased will see unsustainable levels of debt

“Everything is just very burdened with debt, and there’s no stopping it.” Ron Paul told CNBC this week. He’s not wrong. At the moment there are zero plans in place to reduce the debt burden across the financial world.

What makes the debt so unsustainable? Interest rate hikes.

“We’re gonna see higher interest rates and when that happens then that debt becomes very much unsustainable” Stephen Flood, The Goldnomics Podcast

“the scene is set for higher interest rates, debt burden is going to become difficult to manage and we think that there’s going to be market events that these Treasury officials are going to have to answer for.”Stephen Flood, The Goldnomics Podcast

If central bankers react by increasing rates then it could make interest payments the US government’s largest single expenditure — bigger than Social Security ($916 billion in 2016), defense ($605 billion) or Medicare ($594 billion).

One could argue that the world did not end the last time the yield on the 10-year U.S. Treasury note was at levels we have seen recently. That was back in 1996. But think back to that year. The US national debt was under $5 trillion, today it is $20 trillion and counting. If the cost of servicing this debt increases then the impact on financial markets could well be astronomical.

This year it is set to get worse thanks to Trump’s tax plans. They are expected to push the annual budget deficit above $1 trillion and expand the $20 trillion national debt.

Its not just unsustainable levels of government debt that interest rates will trigger. Consider the huge levels of indebtedness we see for individuals across the Western world. For example, US consumer non-mortgage debt has never been higher. At the end of 2017 US households had a record $1.0 trillion of credit card/revolving loans, $1.3 trillion of auto loans, and $1.5 trillion of student loans.

Just a brief look at the US economy alone and one can see why an uptick in inflation and higher interest rates could easily flip us into the next recession. Gold remains an attractive asset as rate setters are running out of tools to control the markets with.

Central bankers have no more tools in the armoury

Back when the last recession took hold central banks could get (somewhat of) a grasp on the situation thanks to monetary policy. They slashed rates and the markets responded accordingly.

Today, interest rates remain very low but another recession is on the horizon. This is something that keeps many Fed bods awake at night.

As Reuters reports:

Federal Reserve policymakers are fretting that they could face the next U.S. recession with an arsenal of policies little different from that used in the last downturn but robbed of much of their punch because interest rates are still low.

“The thing that keeps me up at night is that when that next recession happens, and hopefully not for a long time, I don’t think we have as strong a toolkit as we would like to have to respond to that,” San Francisco Federal Reserve Bank President John Williams said Friday at a Town Hall Los Angeles event.

To pull out of the 2007-2009 recession, the Fed slashed short-term interest rates to near zero and bought $3.5 trillion in bonds to push down longer-term borrowing costs.

Since late 2015 it has gradually reversed course. Its key rate is now in the range of 1.25 to 1.5 percent, and the Fed expects to end this year with rates between 2 percent and 2.25 percent.

With an aging population slowing the economy’s growth potential, the Fed projects it can raise rates only to about 2.75 percent before borrowing costs will really start to brake the economy.

Are higher interest rates bad for gold?

Even with the dire consequences for the financial markets, one could think that there would be an opportunity cost to holding gold over keeping cash in the bank as interest rates are rising.

Not so, rapidly rising rates against a backdrop of struggling financial markets make gold an even more attractive prospect. As Mark O’Byrne explains:

“…You see the media saying rising interest rates is bearish for gold. But if you look at the history and look at the data, interest rates rose continuously throughout the 1970s from below at the 10-year US Treasury, 10-year bonds below 5% in 1970, to up above 15% in 79-80 and gold prices went up from $35 to $ 850 in those nine years. So, rising interest rates weren’t a negative for gold whatsoever.

“Same thing happened again more recently. Obviously some people might say; “Oh well that’s ancient history and we’re a long way from the 1970s.

“Okay, fair enough well let’s look from 2003 to 2007. I think interest rates went from roughly 3/3½% to 5/5½ %and the gold price went up from $ 400 to $700/800. So, the narrative is incorrect. Rising interest rates are actually bearish as you can imagine for assets that are bought with debt and with leverage.” Mark O’Byrne, The Goldnomics Podcast

As Mark explains on the podcast, raising interest rates are bad news for those assets ‘bought with debt and with leverage’. Within this consider the scenario if both the Federal Reserve and the ECB respond to runaway inflation with accelerated large interest rate increases. This (combined with removal of monetary stimulus) it could very easily turn current ‘all-time-highs’ in the stock market to years of lows in a very short period of time.

You can hear more of Mark’s thoughts on this in our podcast.

Gold looks beyond the short-term

Unlike the financial media, gold looks beyond the short-term moves and commentary. Whilst gold is often dismissed in a higher interest rate environment those investing in it realise that monetary policy changes are not a sign of a healthier economy.

This explains why they have failed to react negatively to past-hikes and declarations by banks that more are on the horizon.

As briefly demonstrated above, one can see that interest rate hikes are unlikely to come at a time with either the US or global economy can handle them. The problem is, the central banks just don’t know what else to do.

Once higher hikes take hold the Federal Reserve will be back to their old game of catch-up and there is little indication that that will bode well for the financial system.

Gold has held its own in this financial crisis and particularly in the face of bearish central bank policies. Combine the likely outcome of these policies with flashpoints in the geopolitical system. This provides you with an even stronger case for gold bullion and bars as a safe haven.

News and Commentary

Gold gains as trade war fears weigh on dollar, equities (Reuters.com)

Asian markets dragged down after Gary Cohn’s resignation (MarketWatch.com)

Asian gold-backed ETFs grow by nearly 10 pct in February -WGC (Reuters.com)

Gold climbs to a more than two-week high as dollar slumps (MarketWatch.com)

Gold rallies 1.4 pct as potential North Korea talks hurt dollar (Reuters.com)

Source: Zerohedge

How about just conducting government business — and trading — in public? (Bloomberg.com)

Gold documentary confirms market rigging by governments (Youtube.com)

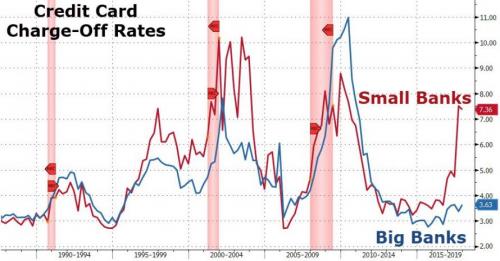

The WSJ Also Uncovered The Source Of The Next Consumer Debt Crisis (ZeroHedge.com)

‘There’s no stopping it,’ warns Ron Paul (MarketWatch.com)

Rand Paul Adds ‘Audit The Fed’ Amendment To Senate Banking Bill (ZeroHedge.com)

Gold Prices (LBMA AM)

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

28 Feb: USD 1,320.30, GBP 951.14 & EUR 1,080.53 per ounce

27 Feb: USD 1,332.75, GBP 954.78 & EUR 1,081.26 per ounce

Silver Prices (LBMA)

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

28 Feb: USD 16.44, GBP 11.88 & EUR 13.45 per ounce

27 Feb: USD 16.61, GBP 11.91 & EUR 13.48 per ounce

Recent Market Updates

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

– US-China Trade War Escalates As Further Measures Are Taken

– Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

THE FOLLOWING CAME FROM KOOS JANSEN:

YOU WILL NOTE THAT FOR THE FIRST TIME EVER CHINA EXPORTED GOLD TO LONDON.

THE QUESTION IS WHY?

I ASKED MY GOOD FRIEND REG HOWE FOR HIS THOUGHTS ON THIS AND WE AGREE THAT THERE ARE TWO POSSIBILITIES: 1) THAT THERE IS EXTREME SHORTAGE IN LONDON AND A MAJOR BANK COULD NOT DELIVER UPON ALONG OVER THERE.. CHINA WOULD BE ASKING FOR A BIG QUID PRO QUO FOR PROVIDING THE NECESSARY PHYSICAL. (IT MAKES SENSE IN THE FACT THAT GOLD IS IN BACKWARDATION IN LONDON)

2. TO HELP IN THE FACILITATION OF THE NEW OIL FOR YUAN FOR GOLD NEW FORMAT OR SOME FUTURE MEASURE THAT CHINA WILL REQUIRE OR AT LEAST BENEFIT FROM ADDITION PHYSICAL LIQUIDITY IN LONODN..

REGARDLESS, IT SHOWS SCARCITY OVER THERE.

FROM REG HOWE TO ME:

“Have read speculation that it may have to do with the mechanics of settling the new oil and gold contracts in physical. More generally, I would guess it’s one of two things: (1) Chinese help in containing some serious stress in the gold market due to lack of physical, e.g., some central bank or major bullion bank unable to deliver, in which case there is likely a big quid pro quo; or (2) a positioning to facilitate some (other) future measure by China that will require or at least benefit from additional physical liquidity in London. In any event, seems to be more evidence of severe shortage of physical in London, otherwise they would just buy it there at today’s suppressed prices.”

END

The following is an extremely important paper by Stewart Dougherty and the subject is very dear to my heart…the fact that the USA does not have beneficial official gold and thus the reasons for the constant raids

it is long but well worth it…

(courtesy Stewart Dougherty)

Mr. President, If We Don’t Have Gold, We Don’t Have a Country

The consequences of Gold Truth, such as it is but has not yet been revealed, are beyond sobering. If the Gold Truth is that USG, Inc. does not possess and own the gold it has promised the world that it owns and possesses, every last shred of monetary, fiscal, financial, economic and moral authority that USG, Inc. still possesses would be destroyed in a matter of seconds. And it is virtually impossible to see how the U.S. dollar could survive such a revelation without plummeting. – Stewart Dougherty

Stewart Dougherty has written another compelling, thought-provoking essay about gold and the United States Government’s intentional omission of gold as the foundation of monetary and fiscal policy. Please note that Mr. Doughtery’s view of Trump does not represent IRD’s view of Trump or his efforts as President.

“Passivity is fatal to us. Our goal is to make the enemy passive. … Communism is notlove. Communism is a hammer which we use to crush the enemy.” Mao Tse-tung, proclaiming the founding of the People’s Republic of China, 1949

Circumstantial evidence is mounting high that there is something seriously wrong with the amount of gold reportedly owned by the United States government, or more precisely, the American people.

After nearly two generations of being brainwashed into believing that gold is a meaningless relic, western citizens have lost all concept of gold’s crucial monetary importance. If it turns out that the United States does not, in fact, possess and own the gold it claims to, the monetary, fiscal, economic, and humanitarian fallout will be unprecedented in its destructiveness. Unfortunately, the people have no idea what is at stake.

The largest corporation in the world, by far, is the United States government. No other corporation has anything even close to its $3.4 trillion in annual revenues, and $4.4 trillion in annual expenses. And no other corporation has ever suffered multiple annual losses exceeding $1 trillion dollars, nor could it have, as such losses would have financially annihilated it. To be able to print money at will and without limit, as USG, Inc. can do, has blinded it to the powerful beast called Consequences that is slowly and methodically hunting it down.

USG, Inc. employs thousands of accountants, many of whom work at the Congressional Budget Office. The CBO prepares detailed budgets, one of which looks forward thirty years, and then extrapolates the numerical trends for an additional forty-five years, for a total forward horizon of 75 years. The 2015 report examines USG, Inc.’s projected performance until the year 2090. According to that report, not only will USG, Inc. lose money every single year for the next 75 years, the losses will actually accelerate each year and total more than $300 trillion. In 2047 alone, the deficit is estimated to be $5.3 trillion, on a cash accounting basis. On an accrual accounting basis, it will be far worse, if USG, Inc. even makes it to that point in its current state, something we find it difficult to envision. It is arithmetically impossible for the dollar to avoid destruction in such a scenario.

It should be no surprise that USG, Inc.’s finances are such a disaster, because for the past generation and longer, the CEOs of USG, Inc. have never in their lives held real jobs in the productive economy, other than GW Bush’s brief stints as a member of an oil and then a baseball investor group, which is not the kind of real job we mean. Instead, these CEOs have all been professional politicians, who by definition do not contribute to the real economy, but rather, feed upon it.

This pattern was about to repeat itself in 2016, with the Deep State’s planned installation of Hillary Clinton into the CEO role at USG, Inc. Clinton, too, has never in her life had a real job in the productive economy, and has precisely zero experience managing anything even beginning to resemble a massive corporation with millions of employees and projected $1+ trillion, accelerating annual losses extending as far as eyes can see. This is exactly what the Deep State wanted: a corrupt, financially clueless, ideological figurehead, who would be oblivious as they ramped up the looting of USG, Inc. to a new level of rapaciousness while she was busy hectoring the nation’s producers and taxpayers about their deplorable selves. It is this looting that is the precise reason why USG, Inc. is now drowning in losses and debt, and is strategically paralyzed.

While anyone with any common sense would immediately understand that it would be ridiculous to expect that someone with zero education, training or experience in engineering could oversee the design of a spacecraft capable of landing on Mars, or that someone with zero medical education, training or experience could successfully conduct brain surgery, for some unfathomable reason, people think that someone with zero business education, training or experience can successfully manage the world’s largest corporation. USG, Inc.’s catastrophic financial results demonstrate the regrettable stupidity of that thought.

We previously termed the current United States operating system as one of “crony communism,” whereby the cronies have free rein to steal the nation’s current and retained earnings (the private wealth), while the people are progressively immiserated in communistic helplessness and squalor. The election of HRC would have finalized the crony communist revolution that Obama unleashed with all his might.

During the campaign, Trump claimed that the 2016 election provided the American people their “last chance” to turn the nation around. The key word was “chance;” he offered no guarantees, because he knew that the situation hung on a thread. In an upset, Trump won, and for the first time in decades, an actual businessman is now the CEO of the world’s largest corporation. Imagine that. Unfortunately, he inherited a situation so fractured and poisoned fiscally, monetarily, politically and societally that his turnaround task is virtually impossible, no matter how genuine his efforts might be.

Whether or not one agrees with Trump’s policies or style, he is now talking to the American people and the world about business topics that previous, politician USG, Inc. CEOs totally avoided, given their desire and incentive to preserve the status quo: the astronomical trade deficit; the need to bring back offshored jobs; the critical importance of reviving manufacturing; the staggering national debt; NATO’s getting a free defense ride at U.S. taxpayers’ expense; the need to slash strangulating regulations; skewed, unfair trade deals; the urgent need for GDP growth; the untenable condition of the nation’s infrastructure; the need to get massive illegal immigration, which comes at an exorbitant cost to taxpayers, under control; and all the rest.

Beyond those issues, Trump’s most important job responsibility is to restore the American spirit. Under Obama’s crony communist revolution, euphemized as his so-called “fundamental transformation of America,” a fraud he dared not call by its true name given that it was such an overt and pernicious attack on everything the vast majority of the people of this nation stand for, believe in and want, the citizens started to do, in droves, what they always do when subjected to totalitarian control: check out and shut down.

GDP and retail sales stagnated, and the economy progressively ground down. Stores closed and business owners gave up. And by the millions, the people retreated into the dead-end dependency of welfare, Food Stamps and Medicaid, while homelessness, tent city and under-bridge community numbers skyrocketed. Not coincidentally, opioid addiction, the ultimate surrender to despair and suicide, became a national epidemic. Which is exactly what the crony communist profiteers wanted: an increasingly helpless, hopeless, addicted and compliant populace that could be controlled by the actual “crumbs,” Ms. Pelosi, of subsistence government pigeon feed scattered upon the ground for the citizens to peck at.

As the Dutch thinker, Ronald Bernard, so incisively realized: “All the misery in the world is a business plan.”

Trump has said that his proposed tariffs on steel and aluminum are more than a matter of financials; they are also a matter of national security, because “if you don’t have steel, you don’t have a country.” This is thematically identical to the statement he has repeatedly made about illegal immigration: “If you don’t have borders, you don’t have a country.” This notion of “country” is vital, and particularly so when it comes to a nation’s monetary reserves. To steel and borders, we would add that, “if don’t have gold, you don’t have country.”

Mr. Trump is knowledgeable about gold. In fact, on January 29, 2016, he sealed a deal with Apmex, one of the nation’s largest gold dealers, for a 10 year lease of the 50th floor of “The Trump Building” located at 40 Wall Street in New York City. Significantly, at the signing ceremony, Apmex CEO Michael Haynes paid Mr. Trump the $200,000 lease deposit in gold bars.

In a statement, Mr. Trump said: “It’s a sad day when a large property owner starts accepting gold instead of the dollar. The economy is bad, and Obama’s not protecting the dollar at all. … If I do this, other people are going to start doing it, and maybe we’ll see some changes.”

Later, Trump’s press office amplified his statement by saying that “Mr. Trump has been bullish on gold due to his concerns about the value of the dollar.”

These statements demonstrate that Mr. Trump has more than a casual understanding of gold.

It is well-known that China, Russia and Turkey, among many other smaller nations, are steadily, and in the case of China, massively adding to their gold reserves. In fact, the governments of China and Turkey publicly encourage their citizens to buy gold, while Russia leads by example with its steady and well-publicized sovereign purchases. Gold is important to these nations for reasons that are well thought-out, forward-thinking and strategic.

On August 21, 2017, Treasury Secretary Mnuchin breezed into Kentucky for a visit. That morning, he spoke to members of the Louisville Chamber of Commerce, and announced, with no advance warning to the press, that after his speech, he was headed to the Fort Knox Gold Bullion Depository to check things out. Laughingly, he said to the audience, “I assume the gold is still there. It would be quite a movie if we walked in and there was no gold.”

After a short visit and cursory inspection, during which only one of the numerous Fort Knox lockers said to hold the American people’s gold was opened and eyeballed, and a few bars were handled,” Mnuchin concluded his visit and then tweeted to America and the world, “Glad gold is safe.” The insouciance of his tweet was stunning. [IRD Note: the gold remaining in Ft. Knox is largely for ceremonial display; most of the gold has been moved to what is dubiously called “deep storage” at West Point. It’s never been independently confirmed that gold actually exists or, if it does, to what extent the Fed has leased or hypothecated the gold to be used in support of the use of futures and LMBA forwards by Fed-member banks to help suppress the market clearing price of gold].

The supposed U.S. gold hoard was last audited in 1953, sixty-five years ago. The nation’s debt at that time was $266 billion, inflation adjusted. Today, it is nearly $21 trillion, or seventy-nine times greater. In 1953, the nation owned 20,000 tonnes of gold, an amount that plunged to 8,133 tonnes by 1974 [at least according to the numbers reported by the Fed]. From 1974 until now, the hoard has supposedly remained unchanged at 8,133 tonnes, despite the fact that the country’s fiscal situation has disintegrated with, in addition to the rapidly approaching $21 trillion in debt, more than $180 trillion in federal unfunded contingent liabilities; additional trillions in unfunded corporate and municipal, county and state government pensions; and annual trillion dollar plus deficits on a hockey stick trajectory projected for the next 75 years.

And yet, we are asked to believe that despite the fact that 11,867 tonnes of gold were sold and shipped between 1953 and 1974, generally strong economic years for the United States, not one ounce has been sold in the 44 year period from 1974 until now. Not one ounce has been used, for example, to guarantee China, Japan and other sovereign nations’ multi-trillion dollar investments in U.S. Treasury securities; not one ounce has been used to even fractionally settle the nation’s massive, persistent, multi-trillion dollar trade deficit that now measures $800+ billion per year; not one ounce has been used to sway foreign politicians who consistently and curiously pursue an American-dictated agenda at odds with their own national interests; and that not one ounce has been required to facilitate the largest national bailout in history, in the wake of the Great Financial Crisis. In fact, not one ounce has been needed for anything, despite the fact that USG, Inc.’s financial fortunes have collapsed since 1974. While we suppose that anything is possible, this does not appear plausible.

Mr. Trump was rightfully excited when Apple Computer announced a multi-year $350 billion investment in its U.S. facilities and operations. He has been similarly pleased by far smaller U.S. investment commitments made by other corporations. To him, every investment in America is important, no matter how big or small, and rightly so, as each has the potential to create jobs and needed tax revenues.

USG, Inc. is said to own 261.5 million ounces (8,133 tonnes) of gold. Mr. Trump could increase the price of gold by at least $1,000.00 per ounce in 10 seconds if he simply announced that USG, Inc. believes in gold, and that, similarly to Russia, China, Turkey and numerous other nations, plans to buy it on a regular basis. He could boost the price even more if he simultaneously announced that USG, Inc. would no longer tolerate the illegal rigging of gold’s price by the Wall Street profiteers and swindlers who have corrupted and criminalized the gold market for the past 40 years.

As the supposed largest sovereign holder of gold, by far, why on earth would USG, Inc. not support its price, when it would so obviously be in its direct financial interests to do so? If gold’s price increased by $1,000 per ounce, it would result in a $261.5 billion instantaneous windfall for USG, Inc. and the American citizen shareholders who supposedly own it. This would come at no cost whatsoever to USG, Inc. or to the shareholders, other than the trivial expense of setting up the press conference. And there would be no reason for the dollar to decline simply because USG, Inc. announced that as one of its many investment initiatives, from education to infrastructure to armaments, it was also going to put money into gold, in the expectation of making a profit from it. Just has China has been doing for the past twenty years, with great financial success.

$261.5 billion in profits, in 10 seconds, would be many times greater than what USG, Inc. will realize from Apple Computer’s multi-year $350 billion investment, only a small portion of which will actually trickle down to the U.S. Treasury in the form of tax revenues. So one would think there would be even more excitement about the opportunity in gold than in Apple’s planned spending. And we have not even included the significant capital gains tax revenue that would pour into USG, Inc. as a cohort of current gold investors traded their positions at a large, tax-generating profit.

USG, Inc.’s persistent silence, aside from the frivolous comments and jokes made about gold by Mr. Mnuchin in Kentucky, make no common sense. But the situation is actually deeper, and worse.

As those who study the gold market now know to be an undeniable, categorical fact, the price of gold has been illegally manipulated for decades by Wall Street profiteers who appear to operate with the full agreement and protection of USG, Inc. given that the manipulators are never prosecuted and that their criminal rigging operations continue unabated to this day.

Therefore, while foreign nations have dumped state-subsidized, underpriced steel, aluminum and other products into the United States, which we are told is terrible for our nation, Wall Street and its City of London collaborators have facilitated the dumping of tonnes of illegally manipulated, underpriced western gold into numerous countries including Russia, China and Turkey and many others. And yet western citizens are supposed to believe that the dumping of underpriced gold, including sovereign gold, which is supposed to be the people’s gold, is somehow a brilliant gambit that should be allowed to continue. In other words, the equivalent of western government cargo planes dumping gold out of their holds onto Moscow, Beijing, Ankara and other foreign capitals is presented as a smart thing for western nations to do, and of benefit to the increasingly impoverished, crony-communized citizens of the west, whose gold it is that is being dumped offshore.

Perhaps the same level of outrage that is expressed about jobs offshoring should also be expressed about gold offshoring, whose financial damage will compound over time and end up costing the nation more than the lost jobs.

It is virtually impossible to fathom the idiocy of this ongoing process of foreign gold dumping. On one hand, certain foreign nations promote their strategically important industries, such as steel and aluminum, by selling their products to the United States at low prices. On the other hand, the United States and its western counterparts facilitate the sale of their sole monetary bedrock, gold, to arch foreign competitors, for a fraction of the gold’s true price given that it is illegally manipulated by the western financial elite for their own private profit. Even if a country, say China for example, loses some money selling low-priced steel to the United States, by using the revenue they generate from such sales to buy western gold at a fraction of its true price is a no-brainer deal the artistry of which even Trump would have to admire. While they might lose a few pennies per pound on the steel, they stand to earn thousands of dollars per ounce on the gold.

If USG, Inc. actually owned and possessed 261.5 million ounces of gold, why would it allow Wall Street profiteers to wantonly crush its price, and directly facilitate its outflow to and enrichment of foreign countries with which it competes, and by which it is systematically being destroyed in trade wars it has been losing for decades?

We can understand Clinton, Bush and Obama not knowing the first thing about the strategic national importance of gold, and being clueless about how Wall Street has manipulated the gold market for nearly 40 years, at a profit to themselves that we have estimated exceeds $1+ trillion dollars to date. As mentioned previously, none of those persons has ever had a real job in the productive economy, or understands the first thing about competitive business tactics, capital markets, or national financial strategy. But Trump is a businessman and, as we have shown, is knowledgeable about gold. Yet while he has focused on far smaller opportunities than the enormous USG, Inc. balance sheet windfall he could engineer by simply talking up the price of gold, he does the exact opposite: he allows its price trashing and foreign dumping to continue.

We can reach only one possible, logical explanation for this stance: USG, Inc. stays silent about gold, because its gold is gone, either in large part, or altogether. And even if a portion of it is still housed at Fort Knox, West Point and Denver, it is pledged to and owned by others. Therefore, if USG, Inc. were to talk up the price of gold, the financial benefits would accrue not to USG, Inc., but to its national competitors such as China, Russia, Turkey and the other governments that have strategically purchased gold in large quantities at the bargain basement prices extended to them by the private Wall Street and London City manipulators and profiteers.

USG, Inc. will lose more than $1 trillion this fiscal year. To fully offset that loss, the price of USG, Inc.’s reported gold reserve would have to rise by $3,842.00 per ounce. Keep in mind, this price increase would be required to offset just one year of USG, Inc.’s deficit (aka, loss), namely that of Fiscal Year 2018. This price increase would do absolutely nothing to neutralize or ameliorate the roughly $20 trillion of pre-Fiscal Year 2018 debt, or the upcoming 75 years’ worth of $1+ trillion, steadily increasing annual deficits. The price of gold would have to increase by $4,000 and progressively more each and every year from now on just to offset USG, Inc.’s upcoming annual losses, which are currently projected to extend into perpetuity.

The consequences of Gold Truth, such as it is but has not yet been revealed, are beyond sobering. If the Gold Truth is that USG, Inc. does not possess and own the gold it has promised the world it does, every last shred of monetary, fiscal, financial, economic and moral authority that USG, Inc. still possesses would be destroyed in a matter of seconds. And it is impossible to see how the U.S. dollar could survive such a revelation without plummeting. A sudden, sharp dollar revaluation would wreak havoc on the global monetary system, financial markets, and economy, and let us all hope it never happens, even though the epic mismanagement of USG, Inc. indicates that it could happen.

The consequences of fiat currency destruction are currently on disturbing and heart-wrenching display in Venezuela. Many westerners look down their noses at Venezuela, as if it is some kind of freak, outlier nation whose suffering people are on a different planet from ours. But those people are not; they are here on earth, just like the rest of us. And if we are correct about our concerns that the actual gold balances at USG, Inc. are not what is being reported, the Venezuelization of the United States would become a likely, if not a guaranteed outcome.

President Trump is doing his best to be the agent of change so desperately needed in the United States. [IRD Note: whether or not you agree with the way Trump is going about effecting change is another matter]. At the same time, Truth is doing its best, as it always does, to be the same: an agent of revelation and change. History conclusively proves that Truth always wins in the end. When people are ahead of a dangerous truth, they can work with and even tame it by honoring and respecting its righteousness and force. But when a dangerous truth is ahead of the people, and expresses itself on its terms and schedule, it almost always cloaks itself in fury, and metes out destruction to those who have stood in its way and dishonored it.

We believe that it is vital for President Trump to now get ahead of and tell the people the truth about USG, Inc.’s gold situation, while there is still time to do so constructively. If the gold is gone, then as a national priority, USG, Inc. must figure out how to buy it back, at least to some degree. A monetary world in which China, Russia, Turkey and other nations own gold, but the west does not would yield invincible monetary and financial superiority to the west’s competitors. If the gold is there, then USG, Inc. should revel in and leverage the enormous fortune and financial opportunity it represents.

Mr. President, as someone who respects and supports the work you are doing to try to turn this country around, might I, with all due respect, paraphrase and echo your own words: “If we don’t have gold, we don’t have a country either.”

end

Stewart Dougherty is the creator of Inferential Analytics, a forecasting method that applies to events proprietary, time-tested principles of human instinct, desire and action. In his view, forecasting methods not fundamentally based upon principles of human action are unlikely to be reliable over time. He is a graduate of Tufts University (BA) and Harvard Business School (MBA). He developed expertise in strategic analysis and planning during a 35+ year business career, has traveled to and conducted research in over 25 countries and has refined Inferential Analytics into a reliable predictive instrument over a period of 17+ years

end

Real Vision’s Grant William confirms market rigging by governments:

(courtesy Grant Williams/GATA)

Real Vision’s gold documentary confirms market rigging by governments

Submitted by cpowell on Tue, 2018-03-06 14:36. Section: Daily Dispatches

9:40a Tuesday, March 6, 2018

Dear Friend of GATA and Gold:

Grant Williams of Real Vision has posted in the clear at You Tube a trailer for his new two-part documentary on gold, the second part examining gold market manipulation.

The trailer, quoting Ned Naylor-Leyland of Old Mutual Investors, fund manager and author James Rickards, and Ross Norman of London bullion dealer Sharps Pixley, maintains that to defend their own currencies governments always have had a powerful interest in controlling the gold price, long have intervened against it, and most likely are continuing to do so.

.Indeed, an expert unidentified in the trailer notes that the modern gold derivatives system was created precisely to divert demand away from real metal and thus help keep the price down.

The trailer is a little less than five minutes long and can be viewed here:

https://www.youtube.com/watch?v=gjw1lduO6xw

Meanwhile over at Kitco News correspondent Daniela Cambone, covering the annual conference in Toronto of the Prospectors and Developers Association of Canada, interviews gold and silver mining executives and analysts who marvel at what they consider the underpricing of the monetary metals and their miners.

See:

http://www.kitco.com/news/video/show/PDAC-2018/1880/2018-03-05/Gold-Is-C…

And:

http://www.kitco.com/news/video/show/PDAC-2018/1881/2018-03-05/Gold-Equi…

And:

http://www.kitco.com/news/video/show/PDAC-2018/1879/2018-03-05/The-Best-…

But gold price suppression by governments and central banks cannot be discussed at PDAC, and Kitco is always too polite to ask mining company executives about it. While such discussion might help expose and agitate against market rigging and thus benefit mining company shareholders, it also might complicate PDAC’s main business, stock touting.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Gold expert Labourne states that the use og gold derivatives by the BIS declines by 55 tonnes and that helped gold rebound.

(courtesy Labourne/GATA)

Robert Lambourne: Use of gold derivatives by BIS declines by 55 tonnes in February

Submitted by cpowell on Tue, 2018-03-06 21:57. Section: Documentation

By Robert Lambourne

Tuesday, March 6, 2018

The Bank for International Settlements reduced its use of gold swaps and other gold-related derivatives during February, according to the bank’s statement of account for the month:

https://www.bis.org/banking/balsheet/statofacc280218.pdf

This decrease follows a large increase in the bank’s gold swaps in January.

In recent months the BIS has been actively trading gold derivatives and the amounts disclosed each month have been variable.

The information provided in the BIS monthly statement of account is not sufficient to calculate a precise amount of gold-related derivatives, including swaps, but it appears that the bank’s total exposure as of February 28, 2018, was 525 tonnes of gold.

This compares to estimates of 580 tonnes, 450 tonnes, 600 tonnes, and 570 tonnes, respectively, at the January, December, November, and October month-ends and an audited swaps figure of 438 tonnes as of March 31, 2017.

The BIS is an association of central banks and provides little information about what it is doing in the gold market and for whom. This lack of transparency fuels suspicion that the bank’s activity is related to official efforts to suppress the gold price.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3196 /shanghai bourse CLOSED DOWN 17.97 POINTS OR 0.55% / HANG SANG CLOSED DOWN 313.81 POINTS OR 1.03%

2. Nikkei closed DOWN 165.04 POINTS OR 0.77% /USA: YEN RISES TO 105.68/ DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index FALLS TO 89.51/Euro RISES TO 1.2420

3b Japan 10 year bond yield: FALLS TO . +.050/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.68/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.18 and Brent: 65.22

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.653%/Italian 10 yr bond yield DOWN to 1.956% /SPAIN 10 YR BOND YIELD DOWN TO 1.440%

3j Greek 10 year bond yield RISES TO : 4.317?????????????????

3k Gold at $1330.45 silver at:16.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 30/100 in roubles/dollar) 56.95

3m oil into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.68 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9405 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1666 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.653%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.844% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.122% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

World Stocks, US Futures Tumble Amid Surge In Trade War Fears

If yesterday world markets were a sea of green as traders bought risk on news that threats of both a nuclear and trade war had sharply receded, today it’s the opposite, and while North Korea has yet to “unexpectedly” test fire an ICBM, Tuesday’s departure of Gary Cohn has all but assured market that a trade war is, after all, just a matter of time.

To be sure, Cohn’s departure – which is widely seen as a victory for the protectionists led by Peter Navarro and immigration hawks – is the only thing analysts and traders are writing about this morning, and while some thing the market’s overnight response, which has seen S&P futures slide over 20 points and the DJIA is set to open 330 points lower, has been exaggerated…

… others disagree, and fear that much more pain is in store, especially if Cohn’s departure is indicative of an imminent trade bombardment by the Trump administration.

The litany is summarized best by Bloomberg which notes that Cohn’s resignation “is a victory for figures who have sought to expunge the Trump administration of advocates for free trade and globalization, principles that have long been a hallmark of the Washington establishment. A registered Democrat, Cohn was regarded as one of the few political moderates close to the president. His absence will amplify voices like Commerce Secretary Wilbur Ross and trade adviser Peter Navarro who back the president’s impulses to buck convention and pick trade fights on a global stage.”

Citi went further, going so far as to compare Gary Cohn to Luke Skywalker:

While heavily-trailed in the press, the market is still mourning the sudden departure of Gary Cohn, the White House’s ‘lonely democrat’ – seen by some as the final bastion of tariff-free international trade. Alas, now the last Jedi has fallen, Trade Wars and a galaxy far, far away now all seems an awful lot closer than before. USD is caught between a more hawkish Fed (Kaplan, Brainard overnight) and an administration that appears ready to shoot from the hip with regards to trade wars.

Echoing what we said 2 weeks ago, when we correctly predicted the coming trade wars when we highlighted the little noticed Peter Navarro promotion, Bank of Singapore’s James Cheo said that “Cohn’s resignation shows that within the Trump administration the pendulum is swinging toward anti-trade,” adding that “what we should be watching out for is how other countries react in response to the tariffs.”