WORK IN PROGRESS!!

GOLD: $1321.15 DOWN $5.45

Silver: $16.49 DOWN 1 CENT

Closing access prices:

Gold $1322.00

silver: $16.49

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1335.83 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1327.45

PREMIUM FIRST FIX: $8.38

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1340.26

NY GOLD PRICE AT THE EXACT SAME TIME: $1333.75

PREMIUM SECOND FIX /NY:$6.51

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1332.50

NY PRICING AT THE EXACT SAME TIME: $1333.10

LONDON SECOND GOLD FIX 10 AM: $1321.00

NY PRICING AT THE EXACT SAME TIME. $1321.00

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 4 NOTICE(S) FOR 400 OZ.

TOTAL NOTICES SO FAR:4 FOR 400 OZ

For silver:

MARCH

30 NOTICE(S) FILED TODAY FOR

150,000 OZ/

Total number of notices filed so far this month: 4554 for 22,770,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9561/OFFER $9,661: DOWN $129(morning)

Bitcoin: BID/ $9332/offer $9408: DOWN $538 (CLOSING/5 PM)

end

I GUESS THE WORK LOAD OF NEGOTIATING ALL OF THOSE GOLD CONTRACTS IS WEARING OUR CME BOYS DOWN. FOR THE PAST 6 MONTHS THEY HAVE BEEN LATE IN PROVIDING BUT I WAIT AND PATIENTLY I HAVE ENOUGH TIME TO INCORPORATE THEM INTO THE DAY’S COMMENTARY.

I USED TO RECEIVE THE DATA ALWAYS AT 10 PM, THE NIGHT BEFORE. IT THEN MORPHED INTO 12 AM AS I STAYED UP TO RECEIVE THE DATA.

THEN IT ARRIVED AT 2 AM

THEN 6 AM

AND NOW, EVEN AT 6.04 PM EST, I DO NOT HAVE THE GOLD EFP DATA. i RECEIVED THE SILVER EFP DATA AT 5 PM.

THE OPEN INTEREST AT THE COMEX DATA FOR BOTH GOLD AND SILVER IS ACCURATE.

THE ENTIRE SILVER COMEX/EFP DATA IS ACCURATE

I DO NOT HAVE THE DATA FOR GOLD EFP

SO THIS IS WHAT I AM GOING TO DO:

I WILL PUBLISH MY REPORT NOW BUT IT WILL BE WORK IN PROGRESS AND WHEN THE GOLD EFPS ARRIVE LATE TONIGHT , I PROMISE TO UPDATE THE DATA TO FINALIZE THE COMEX DATA FOR YOU.

HARVEY.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A SMALL SIZED 866 contracts from 196,597 FALLING TO 195.724 WITH YESTERDAY’S 27 CENT FALL IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2686 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2686 CONTRACTS. WITH THE TRANSFER OF 4470 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2686 CONTRACTS TRANSLATES INTO 13.43 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

15,663 CONTRACTS (FOR 6 TRADING DAYS TOTAL 15,663 CONTRACTS OR 78.315 MILLION OZ: AVERAGE PER DAY: 2610 CONTRACTS OR 13.052 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 78.315 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.18% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 570.79 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A TINY LOSS IN COMEX OI SILVER COMEX WITH THE 27 CENT FALL IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 2686 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2686 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 1820 OI CONTRACTS i.e. 2686 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 866 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 27 CENTS AND A CLOSING PRICE OF $16.50 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.987 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 30 NOTICE(S) FOR 150,000 OZ OF SILVER

In gold, the open interest FELL BY A TINY 50 CONTRACTS DOWN TO 508,050 DESPITE THE CONSIDERABLE FALL IN PRICE YESTERDAY ($8.00) HOWEVER FOR TUESDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN GOOD SIZED 7473 CONTRACTS THE ISSUANCE OF, APRIL SAW THE ISSUANCE OF 7473 CONTRACTS , JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 508,050. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD GAIN IN OI CONTRACTS I.E. 7423 CONTRACTS: 50 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 7473 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(7423 oi GAIN in CONTRACTS EQUATES TO 23.08 TONNES)

YESTERDAY, WE HAD 14232 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 61,690 CONTRACTS OR 6,169,000 OZ OR 191.88 TONNES (6 TRADING DAYS AND THUS AVERAGING: 10,281 EFP CONTRACTS PER TRADING DAY OR 1,028,100 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 5 TRADING DAYS IN TONNES: 191.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 191.88/2550 x 100% TONNES = 7.52% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1442.23 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A TINY SIZED DECREASE IN OI AT THE COMEX WITH THE CONSIDERABLE FALL IN PRICE IN GOLD TRADING YESTERDAY ($8.00). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7473 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7473 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 7423 contracts ON THE TWO EXCHANGES:

7473 CONTRACTS MOVE TO LONDON AND 50 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 23.08 TONNES).

we had: 4 notice(s) filed upon for 400 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $5.45 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER DOWN 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 866 contracts from 196,590 DOWN TO 195,724 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE CONSIDERABLE FALL IN PRICE OF SILVER (27 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2686 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 886 CONTRACTS TO THE 2686 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1820 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 9.100 MILLION OZ!!!

RESULT: A SMALL DECREASE IN SILVER OI AT THE COMEX DESPITE THE STRONG FALL OF 37 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD SIZED 2686 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/LATE WEDNESDAY NIGHT: Shanghai closed UP 16.74 POINTS OR 0.51% /Hang Sang CLOSED UP 457.60 POINTS OR 1.52% / The Nikkei closed UP 115.35 POINTS OR 0.54%/Australia’s all ordinaires CLOSED UP 0.69%/Chinese yuan (ONSHORE) closed DOWN at 6.3385/Oil DOWN to 60.98 dollars per barrel for WTI and 64.03 for Brent. Stocks in Europe OPENED GREEN EXCEPT GERMAN DAX . ONSHORE YUAN CLOSED DOWN AT 6.3385 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3388 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS TO BE INITIATED/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

i)A nightmare scenario for the Euro: Berlusconi backs Northern League to a form a coalition. Berlusconi’s centre right garnered 14% and northern league got 17%. Together with the 5 star at 31%, they can form a government.

( zerohedge)

ii)The Euro rises along with Bund yields as Draghi drops his pledge to increase QE if needed. It looks like these guys are going to taper in September

( zerohedge)

iii)the Euro then gives up its gain when Draghi states he is worried about the USA tariffs and protectionism

iv)Trial balloon: to Bloomberg: the ECB will tape by 10 billion euros per month starting Oct-December and then stopStarting in 2019 it is only up to Japan’s Kuroda to continue QE

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey is becoming quite belligerent..today they threaten the USA’s Exxon Mobil’s hydrocarbon survey ships and the USA 6th Fleet from participating in a naval exercise . Turkey is the only nation that recognizes Northern Cyprus as a sovereign and this has been going on since 1974. Turkey wants to claim the huge oil/gas discovery for themselves.

(courtesy zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Five banks open up a trillion dollar gold club in London as they are concerned with the perception of manipulation and rigging

( Hobson/ Reuters)

ii)Sound money returns to Wyoming as they pass a bill to end taxation on gold and silver

( Cortez/Sound Money Defense League/GATA)

iii)Japanese regulators crackdown on 7 crypto exchanges and shut down two more

( zerohedge)

iv)I guess the explosion of EFP’s into London is swamping our boys as the now intend to delay gold and silver price fixing auctions

(courtesy Ronan Manly)

10. USA stories which will influence the price of gold/silver

A)Trading:

Fact Vs Fiction: GAAP Earnings Have Yet To Surpass 2013 HIghs

Fact or fiction: GAAP earnings have yet to surpass 2013 highs

Answer: true

B.

i)JPMorgan Co President warns that he sees a 40% correction in stocks due to higher interest rates and the inflationary pressures created by tariffs

( zerohedge)

ii)Trump to sign tariffs today with no curve outs/but hints of exemption for Canada and Mexico

( zerohedge)

iib)Canada and Mexico are exempted indefinitely from tariffs and that causes the collar and the peso to soar

( zerohedge)

iic)And now the full details. Canada and Mexico are off the table for now due to continuing talks on NAFTA. If Canada and Mexico become long term exemptions then Trump will raise the tariffs on the foreign suppliers. Countries can negotiate to remove those tariffs if the uSA gets a favourable deal. It does beg the question as to why Cohn resigned.

( zerohedge)

iii)Brandon Smith: a terrific article. He correctly states that when a country introduces tariffs it must be done on strength and self sufficiency. The USA has neither. Its manufacturing base is at best only 10% of GDP as policies caused many manufacturing sites to travel to other foreign jurisdictions. Trump’s tax cuts will solve nothing as corporations will use the low tax rate to borrow funds and buy back stock instead of investing in the country

a must read.

(Brandon Smith/Alt Market .com)

iv)On the same theme as above David Stockman celebrates the end of the Goldman Sachs regency at the White House

( David Stockman/ContraCorner)

v)Interesting: even though Charles Koch states that Trump tariffs will help his investment in the steel industry it will lose far more jobs in other industries vs the amount of job gains in the steel and aluminum industry.

(courtesy zerohedge)

vi)This is getting Washington absolutely terrified: stocks are spooked by reports that Navarro wants Cohn’s job after all

(courtesy zerohedge)

vii)

(courtesy zerohedge)

viii)SWAMPVILLE

( zerohedge)

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 262,252 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 345,168 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A SMALL 866 CONTRACTS FROM 196,500 UP TO 195,724 DESPITE YESTERDAY’S 27 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 2686 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2686. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD SOME LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1820 SILVER OPEN INTEREST CONTRACTS

886 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 2686 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:1820 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 299 contracts FALLING TO 658 contracts. We had 302 contracts filed upon yesterday, so we GAINED 3 contracts or an additional 15,000 will stand in this active delivery month of March.(AS SOMEBODY IS IN GREAT NEED OF PHYSICAL SILVER)

April LOST 2 contracts FALLING TO 438 .

The next big active delivery month for silver will be May and here the OI LOST 2577 contracts DOWN to 145,885

We had 30 notice(s) filed for 1,50,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 8/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | 20,099.639 OZ

JPM |

| No of oz served (contracts) today |

4 notice(s)

400 OZ

|

| No of oz to be served (notices) |

603 contracts

(60300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

4 notices

400 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (4) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (607 contracts) minus the number of notices served upon today (4 x 100 oz per contract) equals 60,700 oz, the number of ounces standing in this nonactive month of MARCH (1.8912 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (4 x 100 oz or ounces + {(607)OI for the front month minus the number of notices served upon today (4 x 100 oz )which equals 60700 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST ONE CONTRACT OR AN ADDITIONAL 100 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

16,830.052 oz

BRINKS

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

NIL oz

|

| No of oz served today (contracts) |

30

CONTRACT(S

(1,50,000 OZ)

|

| No of oz to be served (notices) |

628 contracts

(3,140,000 oz)

|

| Total monthly oz silver served (contracts) | 4554 contracts

(22,770,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 0 deposits into the customer account

ii) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

JPMorgan did not add any silver into its warehouses (official) today.

total deposits today: NIL oz

we had 1 withdrawals from the customer account;

i) Out of BRINKS 16,830.052 oz

total withdrawals; 16,830.052 oz

we had 0 adjustments

total dealer silver: 58.592 million

total dealer + customer silver: 251.707 million oz

The total number of notices filed today for the March. contract month is represented by 30 contract(s) FOR 1,50,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4554 x 5,000 oz = 22,770,000 oz to which we add the difference between the open interest for the front month of Mar. (658) and the number of notices served upon today (30 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4554(notices served so far)x 5000 oz + OI for front month of March(658) -number of notices served upon today (30)x 5000 oz equals 25,910,000 oz of silver standing for the March contract month.

We GAINED an additional 3 contracts or 15,000 additional silver oz will stand for delivery at the comex as somebody ws in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 64,369 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 101,826 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 101,826 CONTRACTS EQUATES TO 509 MILLION OZ OR 72.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.89% (MARCH 8/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.51% to NAV (March 8/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.89%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.51%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.99%: NAV 13.66/TRADING 13.26//DISCOUNT 2.99.

END

And now the Gold inventory at the GLD/

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 8/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 338 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 268 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

MARCH 8/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 318.069 million oz

end

6 Month MM GOFO 2.00/ and libor 6 month duration 2.24

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.00%

libor 2.24 FOR 6 MONTHS/

GOLD LENDING RATE: .24%

XXXXXXXX

12 Month MM GOFO

+ 2.37%

LIBOR FOR 12 MONTH DURATION: 2.52

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.15

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

– Sales in London property market at ‘historic lows’

– 65% fall in pre-tax profits in 2017 to £6.5m reported by London estate agents Foxtons

– Foxtons warns 2018 will ‘remain challenging’ for London property

– Norway’s sovereign wealth fund is backing London’s property market

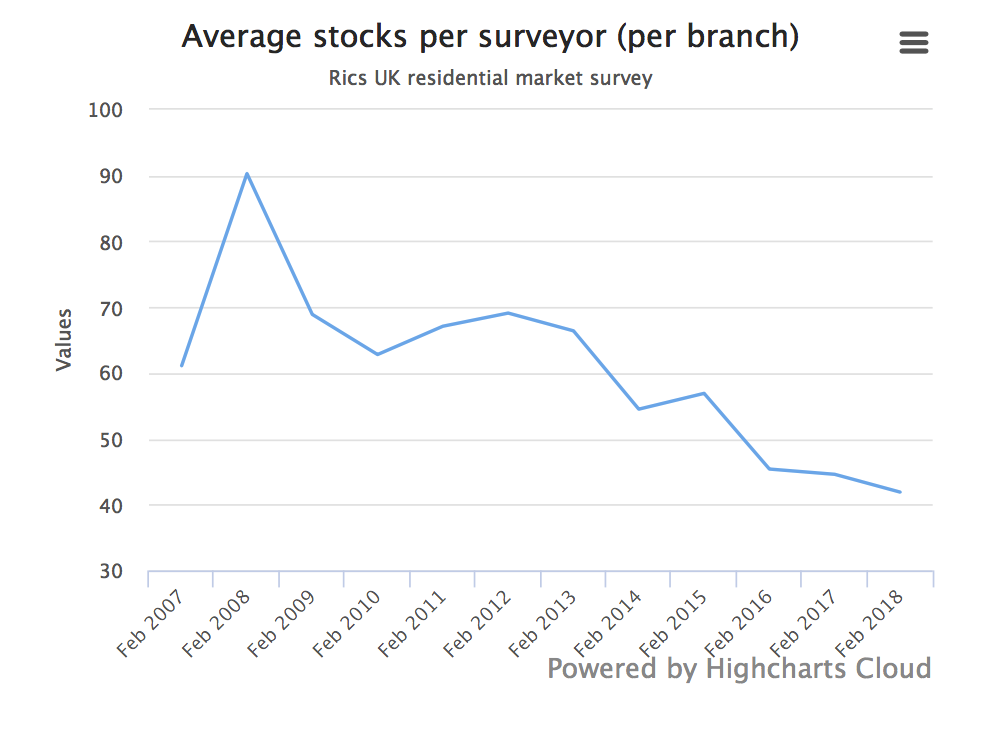

– RICS: UK property stock hits record low as buyer demand falls

– Own physical gold to hedge falls in physical property

The world’s biggest sovereign state fund is backing the London property market. The news comes at a time when the UK capital’s real estate market is reportedly at ‘historic lows’ with conditions expected to remain challenging.

There is a risk that Norway’s investment decision will end up being famous example of buyer’s remorse. Activity in both the London and UK housing market continues to slow, new buyer enquiries are at an 11-month consecutive low and agreed sales are down for the sixth month.

There appears to be little sign of recovery given Brexit-jitters and the resulting damage from years of rampant inflation that has pushed prices out of the reach of many.

Norway is possibly out on its own when it comes to confidence in the London property market. Foxton’s and the Royal Institute of Chartered Surveyors (Rics) are indicating that not only has the last year been tough but that it is set to continue into 2018.

This makes for a tough situation for those who have little option to be involved in the UK property market or not. Many don’t realise that even if they do not own a property, they are still exposed to the risks involved in a housing crash. A downturn or total collapse of the property market would not just affect homeowners and mortgage providers. It would send major waves through the rest of the economy.

London property agent Foxton’s sees ‘historic lows’

Foxton’s profits for 2017 took a 65% hit thanks to a slowdown in the real estate market. Whilst they say that this was in line with expectations, few can have expected it to be this tough and to continue into 2018.

The fall in profits has been blamed on Brexit uncertainty and stamp duty changes. These factors along with highly inflated prices have have driven sales in the capital to near record lows. Overall it is political uncertainty which currently appears to be preventing anyone from making any new moves on the housing ladder.

A new survey of estate agents has shown that in London we are seeing the chronic housing shortage most concentrated. Rics’s monthly residential market survey found that the average number of properties on estate agents’ books has hit a record low and is “unlikely to improve”. In the good times estate agents will have around 42 properties on its books, London branches are now reported to have just 33.

Property website Rightmove says London property owners need to be aware that the capital has moved out of its boom phase. Sellers must be more realistic about the prices they are likely to sell for given they have fallen for the sixth month in a row. In the fourth quarter of 2017 London property prices fell by a sharp 4.3%. This was the worst quarterly performance since the financial crisis.

The boom time was always going to come to an end. The surge in London property was thanks to easy monetary policy by the Bank of England and debt-fuelled spending from across the world. Neither were sustainable sources of income for the capital’s property market.

The problem with London is that the boom has ended prematurely thanks to Brexit. Whilst many could predict the end of a boom created by tightening of lending, increased interest rates and unaffordable housing stock, no one knows how the likes of Brexit and a tricky political climate will really affect things.

For most this is makes for an uncomfortable environment. Many are holding off from making expensive mistakes whilst major companies are getting out whilst they can. One notable exception is the world’s largest sovereign wealth fund.

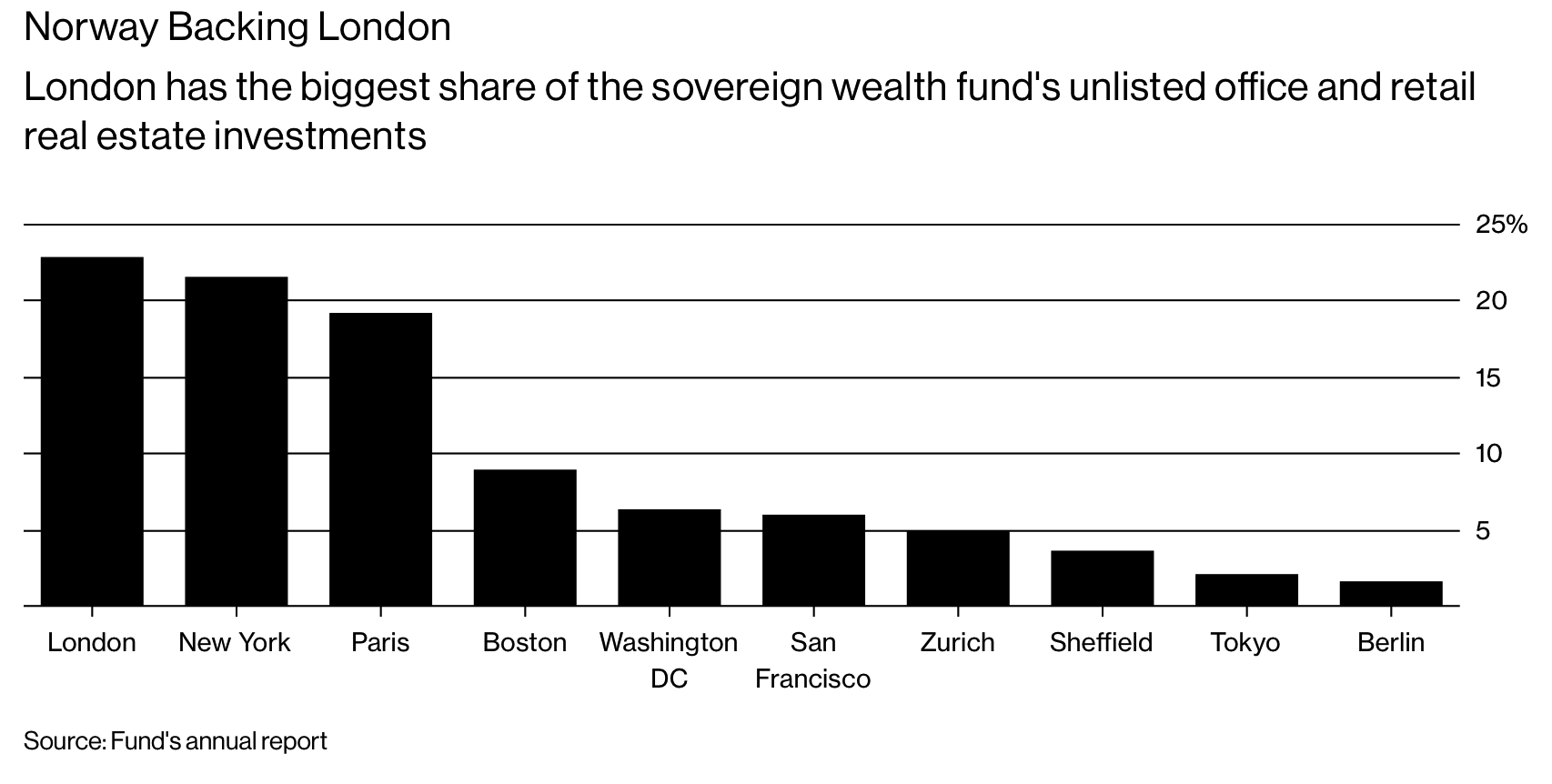

Norway backs London property but is anyone else?

Unlisted real estate makes up 2.6% of Norway’s sovereign wealth fund. Within this London property accounts for over 22%, followed by New York and Paris.

In contrast to many companies’ opinions on London, the fund’s Chief Executive Officer told a press conference that they would continue to be bullish about the London market for the foreseeable future. This positivity will remain “regardless of what the outcome of the political discussion will be” over Brexit.

Not everyone is feeling the love for London. The sovereign fund’s commitment comes at a time when major players in the City are making plans to clear some space in the capital. London, they believe, may no longer be able to hold its own as a financial hub.

Earlier this year both Deutsche Bank AG and Credit Suisse announced plans to move some positions out of London to Frankfurt. Credit Suisse’s Urs Rohner has warned that banks have just a matter of weeks to act on any Brexit contingency plans once the final package has been announced.

Use gold to hedge the London property market

Figuring out how to effectively hedge property investments can be difficult. Luckily physical gold comes into its own. Thanks to its relationship with increasingly correlated interest rates and economic cycles, it may likely act as a good hedge in a downturn or indeed in a full blown London property crash.

As stated at the beginning exposure to a potential property crisis does not just come about if you own or rent a property. All investors, savers and consumers are exposed, as we all have dependencies on the UK banking, financial and economic systems. All of which would be vulnerable in a property crash.

You can take some heart from the fact that the crash will not happen overnight. Investors and savers have time to get their affairs in order. They have time to diversify and decide on a reasonable allocation to gold bullion. When choosing to invest in bullion choose to own physical gold coins and bars held in allocated and segregated storage in safer, less debt laden jurisdictions.

Related reading

Brexit Risks Increase – London Property Market and Pound Vulnerable

London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

London Property Crash Looms As Prices Drop To 2 1/2 Year Low

News and Commentary

Gold settles lower, extends loss after Fed Beige Book (MarketWatch.com)

Gold slips after hitting 1-week high on trade war fears (Reuters.com)

U.S. job market remains tight, inflation seen as moderate: Fed (Reuters.com)

U.S. Stocks End Mixed as Trade War Concerns Ease (Bloomberg.com)

Companies in U.S. Add More Jobs Than Expected, ADP Data Show (Bloomberg.com)

SOURCE: Sharelynx

World’s Oldest Central Bank Has Hit a Dangerous Inflation Wall (Bloomberg.com)

Silver Institute: U.S. investment in silver expected to return in 2018 (CoinWorld.com)

It’s time to buy silver (and sell gold) (MoneyWeek.com)

Trump tariffs risk more than just a new trade war (Reuters.com)

Trade options for UK financial services after Brexit (Reuters.com)

Gold Prices (LBMA AM)

08 Mar: USD 1,325.40, GBP 955.08 & EUR 1,070.39 per ounce

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

Silver Prices (LBMA)

08 Mar: USD 16.48, GBP 11.89 & EUR 13.31 per ounce

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

Recent Market Updates

– Gold Does Not Fear Interest Rate Hikes

– RaboDirect Closing – Gold May Protect From Irish Banks Going “Belly Up Again” – Finuncane

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

THE FOLLOWING CAME FROM KOOS JANSEN:

YOU WILL NOTE THAT FOR THE FIRST TIME EVER CHINA EXPORTED GOLD TO LONDON.

THE QUESTION IS WHY?

I ASKED MY GOOD FRIEND REG HOWE FOR HIS THOUGHTS ON THIS AND WE AGREE THAT THERE ARE TWO POSSIBILITIES: 1) THAT THERE IS EXTREME SHORTAGE IN LONDON AND A MAJOR BANK COULD NOT DELIVER UPON ALONG OVER THERE.. CHINA WOULD BE ASKING FOR A BIG QUID PRO QUO FOR PROVIDING THE NECESSARY PHYSICAL. (IT MAKES SENSE IN THE FACT THAT GOLD IS IN BACKWARDATION IN LONDON)

2. TO HELP IN THE FACILITATION OF THE NEW OIL FOR YUAN FOR GOLD NEW FORMAT OR SOME FUTURE MEASURE THAT CHINA WILL REQUIRE OR AT LEAST BENEFIT FROM ADDITION PHYSICAL LIQUIDITY IN LONODN..

REGARDLESS, IT SHOWS SCARCITY OVER THERE.

FROM REG HOWE TO ME:

“Have read speculation that it may have to do with the mechanics of settling the new oil and gold contracts in physical. More generally, I would guess it’s one of two things: (1) Chinese help in containing some serious stress in the gold market due to lack of physical, e.g., some central bank or major bullion bank unable to deliver, in which case there is likely a big quid pro quo; or (2) a positioning to facilitate some (other) future measure by China that will require or at least benefit from additional physical liquidity in London. In any event, seems to be more evidence of severe shortage of physical in London, otherwise they would just buy it there at today’s suppressed prices.”

END

Five banks open up a trillion dollar gold club in London as they are concerned with the perception of manipulation and rigging

(courtesy Hobson/ Reuters)

Reuters exclusive: Five banks open up trillion-dollar gold club

Submitted by cpowell on Thu, 2018-03-08 01:42. Section: Daily Dispatches

By Peter Hobson

Reuters

Wednesday, March 7, 2018

LONDON — The five banks that settle every transaction in London’s $6.8 trillion (4.9 trillion pounds) a year gold market are changing the rules of their clearing house to make it easier for newcomers to join.

The reform is part of a broad overhaul of institutions that underpin the world’s largest bullion trading centre to make them more transparent after accusations of price manipulation by banks and traders and pressure from regulators.

As that pressure increased, the number of banks clearing gold transactions through a company they own called the London Precious Metals Clearing Limited (LPMCL) has dwindled from seven to five. They are HSBC, JPMorgan, Scotiabank, UBS, and ICBC Standard.

Several banks have attempted to join the group in recent years. ICBC Standard joined in 2016 after months of wrangling over conditions and an application from at least one other, Goldman Sachs, was declined, sources in LPMCL member banks said. …

… For the remainder of the report:

https://uk.reuters.com/article/uk-gold-clearing-lpmcl-exclusive/exclusiv…

end

Sound money returns to Wyoming as they pass a bill to end taxation on gold and silver

(courtesy Cortez/Sound Money Defense League/GATA)

Wyoming legislature passes bill to end taxation of gold and silver

Submitted by cpowell on Thu, 2018-03-08 02:21. Section: Daily Dispatches

By J.P. Cortez

Sound Money Defense League

via EIN Presswire, Washington, D.C.

Wednesday, March 7, 2018

https://www.einnews.com/pr_news/435728627/wyoming-legislature-passes-bil…

CHEYENNE, Wyoming — Following a 44-14 vote in the Wyoming House last week, the Wyoming State Senate today overwhelmingly approved a bill that helps restore constitutional, sound money in Wyoming.

Wyoming senators voted 25-5 to pass the Wyoming Legal Tender Act (House Bill 103), sending the measure introduced by Rep. Roy Edwards, R-Gillette, to Gov. Matt Mead’s desk. Sound money activists are already contacting Governor Mead urging that he sign the bill.

Backed by the Sound Money Defense League, Campaign for Liberty, and Money Metals Exchange, HB 103 is a bill that removes all state taxation from gold and silver bullion and reaffirms their legal tender status in Wyoming, in keeping with Article 1, Section 10 of the U.S. Constitution.

Testifying before the Senate Minerals, Business, and Economic Development Committee, Sound Money Defense League Policy Director J.P. Cortez made the case to Wyoming legislators that assessing taxes on purchases of gold and silver is unjust and undermines their constitutional status as money.

Representative Edwards said in support of HB 103, “Imagine going to the grocery store and asking the clerk for change for a $20 bill and being charged 80 cents in tax. That’s what we’re doing in Wyoming by charging sales taxes on precious metals and we’re taking steps to change that.”

Wyoming does not have an income tax. However, it does have a sales tax and it assesses this tax against precious metals bullion. If Governor Mead signs HB 103, Wyoming would join all its neighboring states (South Dakota, Idaho, Utah, Colorado, Nebraska) and more than 30 other states that do not assess a sales tax against precious metals.

Other states have eliminated income taxation on gold and silver (Arizona and Utah) or have established precious metals depositories to help citizens save and transact in gold and silver bullion (Texas).

Cortez’s testimony highlighted the harmful effects of inflation that flow from the Federal Reserve System and explained how erecting barriers to precious metal ownership harms those most vulnerable to currency debasement — wage earners, savers, those on a fixed income — and local business owners who lose business to out-of-state dealers that don’t subject buyers to unfair taxation.

“Governor Mead should sign the Wyoming Legal Tender Act into law without delay and help Wyoming businesses as well as all citizens harmed by inflation,” Cortez said.

The Sound Money Defense League is an Idaho-based public policy group working nationally to bring back gold and silver as America’s constitutional money. For comment or more information, call 1-208-577-2225 or email jp.cortez@soundmoneydefense.org.

end

Japanese regulators crackdown on 7 crypto exchanges and shut down two more

(courtesy zerohedge)

Japanese Regulators Crackdown On 7 Crypto Exchanges, Shut Down 2 More

Following yesterday’s extremely heavy volume (Tokyo Whale?) plunge in Bitcoin, regulators in Japan have cracked down on seven cryptocurrency exchanges (and ordered month-long suspensions for two more).

Interestingly, prices were relatively stable as the news hit (perhaps yesterday’s selling was pre-emptive?)

As CoinTelegraph reports, the Japanese Financial Services Agency (FSA) has sent “punishment notices” to seven crypto exchanges and temporarily halted the activities of two more after a round of inspections prompted by January’s Coincheck hack, CNBC reports Thursday, March 8.

The FSA issued business improvement orders for a lack of “the proper and required internal control systems” to seven exchanges, including Coincheck, which was specifically cited as lacking a system for preventing money laundering and the financing of terrorism.

image courtesy of CoinTelegraph

Exchanges Bit Station and FSHO are to be closed for one month from today, according to CNBC. The FSA reported that a senior Bit Station official used exchange customers’ Bitcoin (BTC) for personal purposes, and Bit Station has ended its application for registering as an exchange.

The hack of more than $500 mln of NEM from the Japanese Coincheck crypto exchange has been attributed to the fact that the coins were stored on a low-security hot wallet. In the aftermath of the hack, the FSA inspected Coincheck and ordered all Japanese crypto exchanges to submit reports on their risk management systems.

The FSA also announced in mid-February on-site inspections of 15 Japanese crypto exchanges, those currently awaiting registration, of their computer safety system measures.

Coincheck had promised customers to refund all stolen coins, a statement supported by the FSA, who confirmed through CNBC that Coincheck had enough funds to do so and would be releasing a reimbursement plan later today.

end

I guess the explosion of EFP’s into London is swamping our boys as the now intend to delay gold and silver price fixing auctions

(courtesy Ronan Manly)

Ronan Manly: LBMA stalls daily gold and silver price auction fix reports

Submitted by cpowell on Thu, 2018-03-08 17:00. Section: Daily Dispatches

12:02p ET Thursday, March 8, 2018

Dear Friend of GATA and Gold:

The London Bullion Market Association, gold researcher Ronan Manly discloses today, has stopped providing timely reports of the daily gold and silver auction price fixes and has against postponed its plans to publish trade data about the monetary metals.

Manly writes: “It must be obvious to everyone that the LBMA and its bullion bank members do not want the transparency that gold and silver trade reporting would provide. Otherwise they would not have spent four years on a project that any individual investment bank could start and complete within less than three months.”

Manly’s report is headlined “LBMA Alchemy and the London Gold and Silver Markets: 2 Steps Back” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/lbma-alchemy-london-gold-m…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Butler and I are miles apart on the silver situation. I can categorically state that JPMorgan has accumulated a massive amount of silver. I think it is somewhere north of 600 million oz. Butler believes it is 700 million. We differ in the fact that I believe JPMorgan is holding it for China on behalf of the USA government. The USA government needed silver as they ran out in 2002 and called upon China to supply silver and keep the suppression game alive. China obliged because they picked up huge amounts of gold at suppressed prices.

Other than that, we are identical..

(courtesy Butler)

JPMorgan’s Motivation

Theodore Butler | March 8, 2018

To be sure, there are many who reject, out of hand, my allegation that JPMorgan has accumulated a massive amount of physical silver over the past seven years, amounting to 700 million ounces or more. That’s completely understandable, since I can’t document and point out all 700 million oz and few have taken the time to review the basis of my claim. It doesn’t matter that I first picked up on JPMorgan’s quest to acquire physical silver four years ago, by which time it had already accumulated 300 million oz and have been monitoring and reporting on it ever since – if I can’t show every ounce belonging to JPM, some will remain skeptical.

Heck, there are still some who doubt that the 135 million oz of silver that JPMorgan has moved into its own COMEX warehouse since 2011 belong to the bank, despite most of the silver being brought in as a result of JPMorgan taking delivery of that metal in its own name in futures contract deliveries. In this case, even seeing is still disbelieving. And please remember, it is in JPMorgan’s best interest that its physical metal ownership remain largely unknown, so the bank can’t be expected to confirm its holdings.

The highly visible 135 million oz of silver that JPMorgan holds in its own COMEX warehouse is more silver than ever owned by any private entity in history, eclipsing the amounts held by the Hunt Bros in 1980 or Warren Buffett’s Berkshire Hathaway in 1998. To those who wonder how JPMorgan could buy the most silver ever without driving prices higher (as was the case with the Hunt Bros and Buffett), look no further than the fact that JPMorgan was also the largest paper short seller in COMEX silver futures over the entire seven years of its physical accumulation.

Yes, I still believe Buffett came to sell short paper COMEX silver contracts after he acquired physical silver (that’s how he came to lose his metal in 2006); the big difference with JPMorgan is that the bank was the biggest paper short seller on the COMEX both before and during its epic accumulation of physical silver. Not only does this answer the question of why prices didn’t rise despite JPMorgan buying so much actual silver over the past seven years, it also presents the clearest evidence of commodity market price manipulation, a matter I will avoid today, even though it remains the overarching issue.

The issue today is the motivation behind JPMorgan’s epic accumulation of actual metal. To those who will remain unconvinced of the physical accumulation, this will matter little; but among those who accept that JPMorgan owns anywhere from 135 million to more than 700 million oz of silver (in the form of industry standard 1000 oz bars), I’ve detected differences of opinion as to JPM’s motivation for the accumulation.

My opinion, as I’ve consistently maintained, is that JPMorgan first began acquiring physical silver as the one surefire solution of covering its massive paper short position without driving prices sharply higher. Then, after acquiring enough physical metal to neutralize its dominant paper short position early on (by 2012), JPMorgan continued to accumulate hundreds of millions of physical ounces of metal with the sole intent of someday selling that silver at as high a price as possible.

Just to be clear, I don’t think JPMorgan envisioned in 2011 that it would amass the largest stockpile of silver in history at artificial low prices; no one could be that prescient. But JPM’s decision to buy physical metal as the solution to covering its otherwise impossible to cover massive paper short position was nothing less than a stroke of manipulative genius. And JPMorgan was smart enough to realize that once it had effectively covered its paper short position, any additional physical ounces acquired could be sold at a great profit someday.

But even among those who accept that JPMorgan has amassed epic amounts of physical metal, not all agree with my take on the motivation behind the accumulation. Many feel that the main motivation for JPMorgan accumulating physical silver is not to profit by someday by selling at a very high price, but instead to use the physical metal to prolong and extend the manipulation for as long as possible. Invariably, those feeling this way also sense this is related to JPMorgan acting on behalf of the US Government for various reasons, ranging from the US insuring it has adequate supplies of this vital material to keeping the price contained so as not to set off a price disruption in gold and broader financial markets.

I think I do understand why many feel this way and it revolves around the natural fatigue that sets in after years of truly rotten price performance and the very natural tendency to extrapolate current price levels into the future. And just to be objective, let me admit that any single entity holding a large physical position could be considered potentially bearish, since the possibility of sale clearly exists. But the same could be said of the massive physical accumulations of gold by Russia, China, India and elsewhere, where the possibility of sale also exists. But let me deal with the most popular alternative version that has been advanced for the silver manipulation continuing, namely, it is orchestrated by the US Government.

My immediate reaction to JPMorgan running the silver market as a front for the USG is who exactly in the government is running the show? Certainly not anyone I’ve observed over the past half-century of my adult life. And presently, the USG is more dysfunctional than any time in memory (if not in the history of the republic). But my list of reasons for seriously doubting the US Government is behind the manipulation doesn’t stop there. We did run up in silver to $50 fairly quickly in 2011 and I don’t recall any financial market upheaval or even much reaction in gold which rose around $100 (less than 10%) as silver climbed 250%. If silver’s price rise didn’t affect other markets back then, why would it in the future?

As far as the US Government using JPMorgan to build up a strategic stockpile of silver for the future collective good of the country, the same government spent 50 years, from 1950 to 2000, disposing of our existing national stockpile of silver and removing it from strategic status, thanks to the underhanded efforts of the Silver Users Association. Suddenly and with absolutely no public notice, the US Government secretly began stockpiling silver? Such an initiative would have had to have started in the Obama administration and have been fully embraced and continued by the Trump administration. I don’t think so.

It is unrealistic, in my opinion, to believe that the US Government would single out silver as the one commodity it should be stockpiling without any apparent reason or evidence it was doing so. That’s the problem with conspiracy theories – once you go down that path, it never ends and you have to suspend rational thinking to explain everything. As I said, I understand the need to rationalize the rotten price behavior of silver over the past 7 years. Further, I have gone on record stating that the USG did make a secret agreement with JPM on the occasion of its takeover of Bear Stearns, but if the USG has been calling the shots in silver over the past 7 years then I’ll go out and buy a hat and eat it.

As far as JPMorgan accumulating 700 million oz of physical silver for the purpose of continuing the manipulation indefinitely, I can’t see why. For one thing, JPMorgan certainly hasn’t had any need for physical silver to this point to continue the manipulation; it has been doing just fine in capping prices with paper short sales alone. There has been no big physical silver buying from anyone other than JPMorgan, so one has to accept the notion that JPMorgan is prepared to sacrifice and sell at a loss or little profit the 700 million oz it holds. Does that sound like JPMorgan to you? I see a giant financial institution on the constant move, like a great white shark, seeking to maximize profits in any manner possible, from (over) charging folks on checking accounts and credit cards and mortgages to playing every nook and cranny of our capital markets in order to make a buck. Suddenly, JPM is going to forgo and pass up making a giant profit on its accumulated silver so that the price will never go up? Again, I don’t think so.

JPMorgan’s prime reason for existence, just like any for-profit organization is to make profits and that automatically becomes the default motivation behind its massive accumulation of physical silver over the past 7 years. In fact, because JPMorgan has been able to accumulate silver to this day and is not in the slightest conceivable way unable to continue that accumulation because it is running out of buying power, this is also the prime reason why the silver manipulation has lasted for so long. The price of silver will explode when JPMorgan decides it will explode and that won’t come until there is not enough physical silver for it to buy. I admit the timetable has lasted much longer than I (or you) would have preferred, but so what? Who has always gotten whatever he wanted when he wanted it? Not me.

But it’s not just that the profit motive is most likely behind JPMorgan’s massive physical accumulation of silver, it’s much more than that. JPM’s accumulation provides the one critical ingredient missing over the past 33 years in which I have studied silver closely. The accumulation creates something heretofore always lacking for a great run up – that someone very large was in position to profit immensely on an explosion in the price of silver. Warren Buffett wasn’t interested in a silver price explosion because he had sold short an amount equivalent to Berkshire’s physical holdings in COMEX futures contracts and was largely fully-hedged. As such, he wouldn’t have benefited from a silver price explosion.

JPMorgan’s physical position is far larger than its paper COMEX short position and, therefore, it is the first big entity fully prepared for a dramatic liftoff in price. I’m not kidding when I say that JPMorgan’s massive physical position is the single most bullish factor I’ve run across in silver in all my studies over the past three decades.

Ted Butler

March 8, 2018

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3385 /shanghai bourse CLOSED UP 16.74 POINTS OR 0.51% / HANG SANG CLOSED UP 457.60 POINTS OR 1.52%

2. Nikkei closed UP 115.35 POINTS OR 0.54% /USA: YEN FALLS TO 106.11/ DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 89.81/Euro FALLS TO 1.2384

3b Japan 10 year bond yield: RISES TO . +.054/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.11/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.98 and Brent: 64.04

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.674%/Italian 10 yr bond yield UP to 2.038% /SPAIN 10 YR BOND YIELD DOWN TO 1.435%

3j Greek 10 year bond yield RISES TO : 4.187?????????????????

3k Gold at $1324.05 silver at:16.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 15/100 in roubles/dollar) 56.99

3m oil into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.11 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9457 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1710 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.653%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.878% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.158% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, Futures Rise Ahead Of ECB As Trade War Tensions Ease

As trade war fears ease (again) following news late on Wednesday that the White House would consider tariff “carve outs” for Canada and Mexico, markets are modestly higher ahead of a fresh monetary policy catalyst from the ECB this morning. Mario Draghi will be the center of attention today as investors wait to see whether there will be any moves toward an exit from stimulus measures amid the threat of a potential trade war. That said, the ECB is unlikely to make major changes to guidance at today’s meeting as inflation remains far below a target of just under 2%, even with stronger economic growth.

Meanwhile, European stocks drift higher, led by technology shares following strong gains in Asia. Nasdaq futures climb steadily toward session highs, mirroring those gains, while the S&P has also found a bid in recent bid.

The European cash open mimicked the lead seen on Wall St. and overnight in Asia, with major bourses recouping prior losses (Eurostoxx 50 +0.2%) with the exception of the DAX 30 (-0.2%) which sees Merck (-3.0%) at the bottom of the index after the release of its earnings this morning. Material and Energy names are the session laggards, with BHP Billiton (-3.9%), Anglo American (-2.0%) underperforming in the FTSE and Arcelormittal (-1.0%) in the CAC. Elsewhere, the Telecom sector (+1.0%) outperformance has been supported by phone operators Vodafone (+1.3%), Orange (+0.54%) and DT Telekom (+0.7%).

The strong European open followed another green session out of Asia, with Australia’s ASX 200 (+0.7%) and Nikkei 225 (+0.5%) higher with sentiment also underpinned by economic releases including encouraging trade figures in Australia and stronger than expected Japanese Final Q4 GDP. Elsewhere, Hang Seng (+1.5%) outperformed and Shanghai Comp. (+0.7%) initially lagged after the PBoC refrained from liquidity operations, before better than expected Chinese trade data provided some inspiration.

Bunds retrace some of yesterday’s advance as underperformance in the belly of the curve leads to bear flattening in the 5s30s; Italy outperforms with the rest of the periphery amid speculation of a coalition between euroskeptic and center-left parties.

The Bloomberg Dollar Spot Index rallies, pressuring EUR/USD below 1.2400 and pulling CAD, MXN back from overnight highs. WTI crude holds above $61/barrel amid bullish demand outlooks from Exxon Mobil and Goldman Sachs.

Market Snapshot

- S&P 500 futures little changed at 2,729.50

- STOXX Europe 600 up 0.4% to 374.01

- MXAP up 0.7% to 175.10

- MXAPJ up 0.9% to 576.15

- Nikkei up 0.5% to 21,368.07

- Topix up 0.4% to 1,709.95

- Hang Seng Index up 1.5% to 30,654.52

- Shanghai Composite up 0.5% to 3,288.41

- Sensex up 1.2% to 33,433.90

- Australia S&P/ASX 200 up 0.7% to 5,942.87

- Kospi up 1.3% to 2,433.08

- German 10Y yield rose 1.0 bps to 0.665%

- Euro down 0.2% to $1.2388

- Italian 10Y yield fell 4.2 bps to 1.687%

- Spanish 10Y yield fell 0.5 bps to 1.445%

- Brent futures little changed at $64.30/bbl

- Gold spot little changed at $1,325.63

- U.S. Dollar Index up 0.1% to 89.74

Top Overnight News

- The ECB’s new forecasts will show growth and inflation similar to the picture of solid economic momentum seen three months ago, according to euro-area officials familiar with the matter

- The EU’s top financial-services official has told member states and lawmakers to get on with plans to hand the bloc’s main markets regulator new powers over investment funds and derivatives clearinghouses

- China’s Foreign Minister Wang Yi vowed a “justified and necessary response” to any efforts to incite a trade war, in the country’s most forceful response yet to Trump’s threatened tariff actions

- Purchases of foreign bonds by Japanese banks’ trust accounts, often seen as a proxy for the nation’s pension funds, reached a record 841.7 billion yen in February

- China Feb. exports rise 44.5% y/y in dollar terms, est. 11.0%; gain 36.2% y/y in yuan terms, est. 7.4%

- Japan revised 4Q GDP rises annualized 1.6% q/q; est. +1%

Asian stocks recouped some of the prior day’s losses with gains across the region after trade protectionism concerns somewhat eased and amid a continued friendlier tone from North Korea, with the nation said to offer a conditional halt to its ICBM program. ASX 200 (+0.7%) and Nikkei 225 (+0.5%) were higher with sentiment also underpinned by economic releases including encouraging trade figures in Australia and stronger than expected Japanese Final Q4 GDP. Elsewhere, Hang Seng (+1.5%) outperformed and Shanghai Comp. (+0.7%) initially lagged after the PBoC refrained from liquidity operations, before better than expected Chinese trade data provided some inspiration. Finally, 10yr JGBs were subdued as demand lacked amid the improved risk appetite and following an uneventful enhanced-liquidity auction, while the BoJ also began their latest 2-day policy meeting which is not expected to provide any fireworks

Top Asian News

- Hong Kong Seen Draining Liquidity as Currency Drops to 1984 Low; Hong Kong Stocks Rise as Volatility Builds in Topsy-Turvy Week

- Coincheck to Start Paying Back Victims of $500 Million Heist

- BNP Paribas Expects Noble Group to Skip March 9 Coupon Payment

- L Catterton-Backed Brand GXG Is Said to Plan $300 Million IPO

As trade war fears are easing, the European cash open mimicked the lead seen on Wall St. and overnight in Asia, with major bourses recouping prior losses (Eurostoxx 50 +0.2%) with the exception of the DAX 30 (-0.2%) which sees Merck (-3.0%) at the bottom of the index after the release of its earnings this morning. Material and Energy names are the session laggards, with BHP Billiton (-3.9%), Anglo American (-2.0%) underperforming in the FTSE and Arcelormittal (-1.0%) in the CAC. Elsewhere, the Telecom sector (+1.0%) outperformance has been supported by phone operators Vodafone (+1.3%), Orange (+0.54%) and DT Telekom (+0.7%). So far, newsflow has been on the lighter side as participants await the ECB decision, in which there is rising speculation that the central bank could drop its QE easing bias.

Top European News

- German Factory Orders Drop After Demand Surged at End of 2017

- ECB Outlook Is Said to See Solid Growth Similar to December View

- Aviva Falls After Claims Surge Hits Profit at Canadian Unit

- John Lewis Warns of Further Profit Squeeze After a Tough Year

- Adidas Leads DAX Gains; Discount to Peers Unwarranted, BofA Says

In FX, the DXY is mildly firmer within a relative narrow 89.770-545 band, as the Greenback ekes out relatively small gains vs all its G10 rivals on more reports that Canada, Mexico and possibly other nations may be given exemptions from US import tariffs that are expected to be officially signed off later today or on Friday. This has calmed global trade war fears to an extent, while North Korea continues its charm initiative on the nuclear front by offering a conditional ICBM suspension. However, the impending ECB meeting provides potential more currency market activity with expectations very split on whether the QE easing bias will dropped or not. Eur/Usd currently towards the lower end of a tight range around the 1.2400 level amidst reports that new ECB Staff forecasts will be largely the same as in December, but latest forward guidance and the tone of President Draghi’s press conference/Q&A are key along with the aforementioned pledge to increase and/or extend asset buying if needed. Options break-even pricing assigns a circa +/- 67 pip move on the eventuality as a benchmark. Elsewhere, Usd/Jpy also remains largely anchored around a big figure – 106.00 where a hefty expiry runs off (1.1 bn), and now awaiting the BoJ for more independent impetus. The Aud and Nzd continue to underperform around 0.7800 and 0.7250 vs the Usd as the partial Dollar revival weighs on commodity prices, and the Aud fails to derive any sustained benefit from a big trade data beat overnight. Elsewhere, some Nok weakness vs the Eur after Stats Norway trimmed its 2018 inflation and growth forecasts (cross nudging towards 9.7300) and Usd/Hkd is close to the top of its peg tolerance ceiling with the HKMA indicating that 7.8500 is the line in the sand (vs 7.8300 at present). USD/TRY also firmer this morning, after Moody’s downgraded Turkey’s sovereign rating deeper into junk territory with the outlook negative.

In commodities, oil prices hovering around yesterday’s lows with WTI back at USD 61/bbl (-0.1%), while Brent is around the low USD 60s (-0.2%) amid the slight firming of the USD index. Price action has been quiet, with crude futures trading within a tight range thus far. In terms of newsflow, Platts reported that Libya could restart their 90k bpd Elephant field after reaching a deal with guards. China Feb. iron ore imports 84.66mln tons vs. Prev. 100.3mln tons M/M, while crude oil imports 32.26mln tons vs. Prev. 40.6mln tons M/M. Saudi Energy Minister Al-Falih says energy demand is growing at a rate not seen for decades. Libya could restart 90k bpd Elephant field after reaching a deal with guards. Of note, The field was shut down on Feb. 23rd due to protests by local guards over environmental concerns

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -2.8%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 210,000

- 8:30am: Continuing Claims, est. 1.92m, prior 1.93m

- 9:45am: Bloomberg Consumer Comfort, prior 56.2

- 12pm: Household Change in Net Worth, prior $1.74t

end

3. ASIAN AFFAIRS

i)THURSDAY MORNING/LATE WEDNESDAY NIGHT: Shanghai closed UP 16.74 POINTS OR 0.51% /Hang Sang CLOSED UP 457.60 POINTS OR 1.52% / The Nikkei closed UP 115.35 POINTS OR 0.54%/Australia’s all ordinaires CLOSED UP 0.69%/Chinese yuan (ONSHORE) closed DOWN at 6.3385/Oil DOWN to 60.98 dollars per barrel for WTI and 64.03 for Brent. Stocks in Europe OPENED GREEN EXCEPT GERMAN DAX . ONSHORE YUAN CLOSED DOWN AT 6.3385 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3388 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS TO BE INITIATED/ )

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

A nightmare scenario for the Euro: Berlusconi backs Northern League to a form a coalition. Berlusconi’s centre right garnered 14% and northern league got 17%. Together with the 5 star at 31%, they can form a government.

(courtesy zerohedge)

Silvio Berlusconi Backs Leader Of Euroskeptic Party To Form Italy’s Next Government

In what’s probably a nightmare scenario for the millions of Italians who supported left or center-left candidates, Forza Italia leader and former four-time prime minister Silvio Berlusconi has decided to support Matteo Salvini, the candidate of the euroskeptic Northern League, in his attempt to form a government after Euroskeptic and anti-establishment parties performed (once again) far better than expected.

Italy’s March 4 election was widely viewed as a victory for Berlusconi and the other members of his “center-right” coalition with two far-right parties. And now Berlusconi has confirmed that the coalition will unify behind the candidate of the anti-immigrant Norther League.

Berlusconi’s Forza Italia garnered just 14% of the vote compared with 17% for the North Northern League, and the members of the coalition had agreed before the vote to support whoever received the largest share. Before the vote, polls expected Forza Italia to win the largest share of the vote. Still, with a combined 37% of the vote total, the coalition still fell short of the 40% threshold needed to form a government, setting Italy up for a leadership showdown that could last for months.

“I am happy for Matteo Salvini and the League,” the 81 year-old said. Berlusconi didn’t run for office because of a law banning him because of his criminal convictions.

Still, Berlusconi emphasized that he’s still the center-right coalition’s indispensable power broker in what ended up being his first public statement since the vote, according to EuroNews.

“I confirm that…I remain Forza Italia’s leader, I will be the coordinator of the centre-right, I will be the guarantor for the unity of the coalition.”

Both the League an the 5-Star Movement say Italy’s president should name the leader of their own parties as prime minister.

end

The Euro rises along with Bund yields as Draghi drops his pledge to increase QE if needed. It looks like these guys are going to taper in September

(courtesy zerohedge)

EURUSD, Bund Yields Spike After ECB Drops Pledge To Increase QE If Needed