GOLD: $1320.40 DOWN $3.00

Silver: $16.52 DOWN 8 CENTS

Closing access prices:

Gold $1323.20

silver: $16.53

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1329.15 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1322.90

PREMIUM FIRST FIX: $6.20

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1331.10

NY GOLD PRICE AT THE EXACT SAME TIME: $1322.40

PREMIUM SECOND FIX /NY:$8.70

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1317.23

NY PRICING AT THE EXACT SAME TIME: $1320.50 ??

LONDON SECOND GOLD FIX 10 AM: $1319.15

NY PRICING AT THE EXACT SAME TIME. $1317.60???

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:4 FOR 400 OZ

For silver:

MARCH

101 NOTICE(S) FILED TODAY FOR

505,000 OZ/

Total number of notices filed so far this month: 4828 for 24,140,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9772/OFFER $9,842: UP $826(morning)

Bitcoin: BID/ $8795/offer $8867: DOWN $149 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY SIZED 436 contracts from 196,520 RISING TO 196,956 DESPITE FRIDAY’S STRONG 21 CENT RISE IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1107 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1107 CONTRACTS. WITH THE TRANSFER OF 1107 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1107 CONTRACTS TRANSLATES INTO 5.535 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

19,463 CONTRACTS (FOR 8 TRADING DAYS TOTAL 19,463 CONTRACTS OR 97.315 MILLION OZ: AVERAGE PER DAY: 2432 CONTRACTS OR 12.160 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 97.315 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.90% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 589.79 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A SMALL SIZED GAIN IN COMEX OI SILVER COMEX OF 436 DESPITE THE STRONG 21 CENT RISE IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1107 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1107 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 1543 OI CONTRACTS i.e. 1107 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 436 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 21 CENTS AND A CLOSING PRICE OF $16.70 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.984 BILLION TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 101 NOTICE(S) FOR 505,000 OZ OF SILVER

In gold, the open interest FELL BY A FAIR SIZED 1618 CONTRACTS DOWN TO 495,769 DESPITE THE STRONG REBOUND IN PRICE ON FRIDAY YESTERDAY ( GAIN OF$2.25) HOWEVER FOR TODAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN GOOD SIZED 6847 CONTRACTS THE ISSUANCE OF, APRIL SAW THE ISSUANCE OF 6847 CONTRACTS , JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 497,187. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS: 1618 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 6847 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 5229 CONTRACTS OR 522,900 OZ =16.26 TONNES

FRIDAY, WE HAD 7106 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 75,643 CONTRACTS OR 7,564,300 OZ OR 235.28 TONNES (8 TRADING DAYS AND THUS AVERAGING: 9455 EFP CONTRACTS PER TRADING DAY OR 945,500 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 8 TRADING DAYS IN TONNES: 235.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 235.28/2550 x 100% TONNES = 9.21% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1485,62 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX WITH THE STRONG REBOUND IN PRICE IN GOLD TRADING FRIDAY ($2.25 ULTIMATE GAIN). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6847 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6847 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 5229 contracts ON THE TWO EXCHANGES:

6874 CONTRACTS MOVE TO LONDON AND 1618 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 16.26 TONNES).

we had: 0 notice(s) filed upon for nil oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $3.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER DOWN 8 CENTS TODAY:

A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 O

/INVENTORY RESTS AT 319.012 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 436 contracts from 196,520 UP TO 196,956 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE STRONG REBOUND AND GAIN IN PRICE OF SILVER (21 CENT RISE WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2686 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 436 CONTRACTS TO THE 1107 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1543 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 7.715 MILLION OZ!!!

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE STRONG REBOUND AND RISE IN SILVER PRICING ON FRIDAY (21 CENTS GAIN IN PRICE) . BUT WE ALSO HAD ANOTHER GOOD SIZED 1107 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/LATE FRIDAY NIGHT: Shanghai closed UP 19.83 POINTS OR 0.59% /Hang Sang CLOSED UP 598.12 POINTS OR 1.93% / The Nikkei closed UP 354.83 POINTS OR 1.63%/Australia’s all ordinaires CLOSED UP 0.53%/Chinese yuan (ONSHORE) closed UP at 6.3277/Oil UP to 61.05 dollars per barrel for WTI and 65.16 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3277 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3257 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS INITIATED/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

Last year , we reported to you on the Japanese “kindergarten” scandal. It roiled Japanese markets for weeks only to be saved by North Korean rockets flying over Japan. It has now resurfaced and there are reports of altered documents involving Abe’s wife. The tax department also has to answer for this. The deputy finance minister, Aso is has the tax department reporting to him so he may have to resign and that will put the entire Japanese economic “recovery” in jeopardy

( zerohedge)

3 c CHINA

Here is how China might retaliate against those tariffs initiated by Trump

( zerohedge)

4. EUROPEAN AFFAIRS

i)England/Russia

Theresa May is set to blame sovereign Russia for the nerve gas attack on that ex Russian spy. They seem to have chemical markets connected to a Russian laboratory. How this is proof that Putin is behind this is your guess, but England is set to initiate more sanctions and she is asking the world to join her with their additional sanctions

( zerohedge)

i b)Theresa May declares Russia is clearly responsible for the Skripal poisoning and that this act “amounts to unlawful use of force against the UK”

however I doubt if she will do anything..

( zerohedge)

ii)Poland

( GEFIRA)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Trump realizes that Iran’s high unemployment and lack of growth is causing internal problems for that country. He is now demanding major changes to the Obama-Iran agreement. He wants Iran to withdraw from sponsoring terrorism throughout the middle east. Trump in May will not re certify the deal.

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

(courtesy Irina Slava/OilPrice.com

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Alabama becomes the 37th state to exempt sales tax on gold and silver bullion as well as coins

( GATA>Numismatic News.Iola Wisconsin)

ii)Ralph Benko explains beautifully by the USA had continual trade deficits in order to maintain its status as the world’s reserve currency. The USA exported paper dollars which cost them a few pennies and got real goods for that paper money but this occurred with a curse..the USA manufacturers were decimated. Now Trump is attempting to stop this..

a good read//

(Ralph Benko/GATA)

10. USA stories which will influence the price of gold/silver

A. i)Trading: Early this afternoon

(zerohedge)

2) We have been highlighting this to you for the past several weeks: i.e. the rise in risks to banks. The Libor-OIS spread shows an increasing risk for banks to lend to one another. No doubt a major part of this risk has been the dollar repatriation from Europe back to the USA

C i)SWAMPVILLE

b)Over the weekend, Trump is said to be ready to clean house. That means that Kelly, McMaster, Kushner and Ivanka Trump may all be on their way out

c)The Wall Street Journal is set to be close to completion of the Trump obstruction probe but it does not look like it is so( zerohedge)

d)A good one.. a former CIA officer highlights the criminal Clinton Foundation as the biggest sscandal in USA history

(Greg Hunter/USAWatchdog/)

e)Michael Snyder explains why he is running for Congress and how he must drain the swamp

( zerohedge)

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 230,582 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 396,559 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A SMALL 436 CONTRACTS FROM 196,520 UP TO 196,956 DESPITE FRIDAY’S STRONG 21 CENT REBOUND AND RISE IN FRIDAY TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 1107 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1107. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1543 SILVER OPEN INTEREST CONTRACTS 436 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1107 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:1563 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 140 contracts FALLING TO 499 contracts. We had 173 contracts filed upon yesterday, so we GAINED 33 contracts or an additional 165,000 will stand in this active delivery month of March.(AS SOMEBODY IS IN GREAT NEED OF PHYSICAL SILVER)

April LOST 3 contracts FALLING TO 427 .

The next big active delivery month for silver will be May and here the OI LOST 1835 contracts DOWN to 143,245

We had 101 notice(s) filed for 850,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 12/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

400 OZ

|

| No of oz to be served (notices) |

543 contracts

(54300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

4 notices

400 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (4) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (543 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 54700 oz, the number of ounces standing in this nonactive month of MARCH (1.7013 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (4 x 100 oz or ounces + {(543)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 54700 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 17 CONTRACTS OR AN ADDITIONAL 1700 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

173,610.010 oz

Brinks

CNT

Scotia

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

101

CONTRACT(S

(505,000 OZ)

|

| No of oz to be served (notices) |

398 contracts

(1,990,000 oz)

|

| Total monthly oz silver served (contracts) | 4828 contracts

(24,140,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 0 deposits into the customer account

i) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

JPMorgan did not add any silver into its warehouses (official) today.

total deposits today: nil oz

we had 3 withdrawals from the customer account;

i) Out of brinks 2,999.300 oz

ii) Out of CNT:: 63,331.230 oz

iii) Out of Scotia: 107,279.480 oz

total withdrawals; 173,610.010 oz

we had 0 adjustments

total dealer silver: 59.419 million

total dealer + customer silver: 252.110 million oz

The total number of notices filed today for the March. contract month is represented by 101 contract(s) FOR 505,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4828 x 5,000 oz = 24,140,000 oz to which we add the difference between the open interest for the front month of Mar. (499) and the number of notices served upon today (101 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4828(notices served so far)x 5000 oz + OI for front month of March(499) -number of notices served upon today (101)x 5000 oz equals 26,130,000 oz of silver standing for the March contract month.

We GAINED an additional 33 contracts or 165,000 additional silver oz will stand for delivery at the comex as somebody was in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 52,584 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 100,143 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 100,143 CONTRACTS EQUATES TO 502 MILLION OZ OR 71.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.08% (MARCH 12/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.50% to NAV (March 12/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.08%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.50%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.03%: NAV 13.67/TRADING 13.28//DISCOUNT 3.13.

END

And now the Gold inventory at the GLD/

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 12/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 340 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 270 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 12/2018: A BIG CHANGE TO SILVER INVENTORY/ A DEPOSIT OF 943,000 OZ

Inventory 319.012 million oz

end

6 Month MM GOFO 1.99/ and libor 6 month duration 2.27

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.99%

libor 2.27 FOR 6 MONTHS/

GOLD LENDING RATE: .28%

XXXXXXXX

12 Month MM GOFO

+ 2.38%

LIBOR FOR 12 MONTH DURATION: 2.54

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.16

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Protects As Cashless Society Threatens Vulnerable

Gold Protects As Cashless Society Threatens Vulnerable

– Swedish authorities concerned cashless society is happening ‘too quickly’ and heading into ‘negative spiral’

– Only 25% of Swedes paid in cash at least once a week in 2017, 36% never use cash

– Cash usage in Sweden falling both as share of GDP and in nominal terms

– Sweden may be world’s first economy to introduce a cryptocurrency, the e-krona

– Cashless is not a disincentive for illegal drug trade, Guardian finds

– Gold in safe jurisdictions will protect against raids on cash and wealth

The total value of cash payments in Sweden is just 2% of GDP. Two-thirds of people rarely use cash and even homeless Big Issue sellers are accepting cards. These are the statistics of Sweden’s cashless society. A country, which is often touted as the most cashless on earth, is in part proud of these numbers but also wonders if it might be too much too soon.

The total value of cash payments in Sweden is just 2% of GDP. Two-thirds of people rarely use cash and even homeless Big Issue sellers are accepting cards. These are the statistics of Sweden’s cashless society. A country, which is often touted as the most cashless on earth, is in part proud of these numbers but also wonders if it might be too much too soon.

A campaign, called Kontantupproret (“the cash insurgency), demands that the future of money should be a democratic decision, not left just to banks and businesses. Many believe that the cashless society is leaving the old, unbanked and vulnerable behind.

The concerns are so great that a parliamentary review has been launched and central bank, Riksbank, is planning on launching a study into the unintended consequences of the cashlesss society, this summer.

“If this development with cash disappearing happens too fast, it can be difficult to maintain the infrastructure” for handling cash, said Mats Dillen, the head of the parliamentary review. ““One may get into a negative spiral which can threaten the cash infrastructure,” Dillen said.

Banks are now so loathed to work with cash that Riksbank Governor Stefan Ingves has said they may consider forcing banks to provide cash to customers. But this is tricky when the wider economy is no longer set up to accept it.

As we have highlighted before, going cashless may make sense to many businesses in terms of keeping costs down but it makes the most sense to the government and banks who gain full oversight and access to your money once it can only be kept in digital form.

This cashless dream is likely to turn into a nightmare. Not only for the vulnerable but also for anyone who likes to have the final say on what happens to their wealth.

Sweden’s Gone Too Far

The value of cash in circulation has fallen to its lowest level since 1990 and is more than 40% below its 2007 peak. The extreme push for cashless has seen the amount of cash in circulation fall, especially dramatically in 2016 and 2017.

Strangely the central bank are now looking into launching the e-krona, a digital currency which will work as a complement rather than a replacement to cash. The jury is out on whether or not this is as much a PR stunt as it is a further ‘solution’ for the cashless economy.

Sweden may have moved too quickly as protest groups are beginning to rally against the cashless economy. Some declare the refusal to accept cash as undemocratic whilst the elderly are being rapidly locked out of services that would have previously been open to cash payments.

If you have the means to pay in the legal tender (in this case krone) then who is to say how you can pay? After all, currently cash is not illegal, so why are so many people being made to feel like they’re wrong to use it?

Going cashless arguably increases the number of vulnerable economic participants. This isn’t meant in reference to those who are unbanked. In fact, the opposite: Those who are currently society’s least vulnerable – those with savings, investment portfolios and a good banking relationship – could become extremely vulnerable.

How do you go cashless without a bank?

There is also the issue of those who are simply unable to offer anything other than cash – the unbanked.

“The beauty of cash is that it’s a direct and simple transaction between all kinds of different people, no matter how rich or poor,” financial writer Dominic Frisby told The Guardian. “If you begin to insist on cashlessness, it does put pressure on you to be banked and signed up to financial system, and many of the poorest are likely to remain outside of that system. So there is this real danger of exclusion.”

In Sweden, the unbanked is not a major issue. But, in the likes of America where 7% are unbanked and in developing countries it is a problem.

Banks and governments are keen to ‘on-board’ these customers as easily as possible, but in some cases it is just not worth it.

“Billions of poor people in the developing world depend on cash to buy goods for very small amounts, often mere cents,” Srinivasan Sivabalan wrote in Bloomberg. “It may be too costly to host those transactions on a network. That could create a second-class citizenry of people who don’t have equal access to banking services.”

Criminalising cash thanks to its criminal links

One of the major arguments against cash, by governments, is that it facilitates illegal activities such as money laundering and the drug trade. Last year, we highlighted the Swedish authorities’ role in making cash an almost criminal possession:

“In general, the rule of thumb in Scandinavia is: ‘If you have to pay in cash, something is wrong,’” writes Mikael Krogerus for Credit Suisse. Arvidsson explains that “At the offices which do handle banknotes and coins, the customer must explain where the cash comes from, according to the regulations aimed at money laundering and terrorist financing,” The hassle, for the depositor, is enough to make them go cashless.

Here in the UK, cash as a criminal’s payment of choice has been widely touted but it might not be so relevant. The Guardian spoke to several individuals and businesses about how cashless could or was impacting them. One of them was a drug dealer who fundamentally disagreed that the push for cashless would stop drug dealing:

People always go on about how the cashless society will spell the end of drug dealing but although I started selling for cash on the street, my trade has been entirely online for the last couple of years at least. There are different ways customers can pay for drugs on the darknet. They can use Bitcoins, localbitcoins, virtual private networks or [an operating system called] Tails. Buying on the darknet is more risky for dealers than customers.

Compared to selling on the street, the darknet is easier and safer for me – and also more profitable because I sell in bulk rather than dealing with individual pills and small bags of weed. And because I’m selling in bulk, my prices are lower than when I dealt on the street, so it’s a win-win.

I’ve heard some people say the darknet is the next generation of drug dealing. But from where I’m looking, it’s this generation’s way of buying drugs. Cash never comes anywhere near buyer or seller, so all the government’s promises that the cashless society would outlaw drug dealing are a lie.

Making the stronger, weaker.

By demanding one pays just with digital cash – by card, by digital currency etc. then you are demanding that a person store their wealth with a counterparty.

Of course, the majority of us do this for many elements of our wealth, especially that which we use for day-to-day expenses. But, currently we have the option to hold some in cash and some in digital form. If we go cashless then we can no longer do this.

This makes us vulnerable to huge forces, beyond our control. Namely, malicious hackers and the banks with their all-too-easy-to-invoke bail-in policies.

As interest rates turn negative and the risk of bail-ins grows closer by the day, holding cash appears increasingly attractive but also unattractive for those politicians and bankers who want an easy way out of another financial crisis.

Physical assets such as gold and silver, when held in segregated, allocated accounts cannot fall victim to these sticky fingered forces. As Dr. Constantin Gurdgiev reminds us:

Cash and monetary assets, such as gold, cannot be expropriated or bailed-in as long as they are held in physical form and under proper storage. Cashless accounts amplify the importance of monetary assets, such as gold, in fulfilling the function of being safe havens against systemic risks – risks that are associated with high probability of Government expropriation.

Once all of your money is in the digital banking system you are immediately vulnerable. You can get ready for it to be frozen, taken to fund a bail-in and even taxed. And in the meantime, enjoy governments, banks and possibly large corporations knowing what you’re spending your money on.

What’s the alternative?

Of course, if you find yourself in Sweden or any other country pushing the cashless agenda you may feel there is little you can do to ‘opt out’ of the new regime.

There is one thing you can do and that’s in regard to your savings. Of course, your day to day spending money will have to be in the form of fiat-based cashless payments but what you decide to keep in the bank in the short-term does not have to be cash.

Cash and other forms of intangible assets are difficult to protect in this digital era.

Dostoevsky wrote, ‘Money is coined liberty’. Sadly this only remains true for one form of money: gold and silver. It is no longer the case for cash. History shows multiple attempts of wealth confiscation and restrictions on freedom, each time individuals and governments have returned to gold and silver in order to protect their savings and their privacy.

The role of precious metals in a cashless society are key and investors should remember the importance of diversification and holding assets, under direct ownership, outside of the vulnerable and exposed banking system.

Recommended reading

The Alternative Fact of the Cashless Society

Cashless Society – Risks Posed By The War On Cash

Threats Posed By “Bank Holidays” and “Cashless Society”

News and Commentary

Stocks in Japan, South Korea surge on news of Trump-Kim meeting (MarketWatch.com)

Stocks Rise in Asia on Trump-Kim Summit; Yen Drops (Bloomberg.com)

Gold dips as dollar firms amid hopes for easing U.S.-N.Korea tensions (Reuters.com)

Stocks, Bonds Rise as Trump Signs Off on Tariffs (Bloomberg.com)

U.S. Household Debt Rose Last Quarter at Fastest Rate Since 2007 (Bloomberg.com)

Image source: Bloomberg

Reuters exclusive: Five banks open up trillion-dollar gold club (Reuters.com)

Trump’s Historic Bet on Kim Summit Shatters Decades of Orthodoxy (Bloomberg.com)

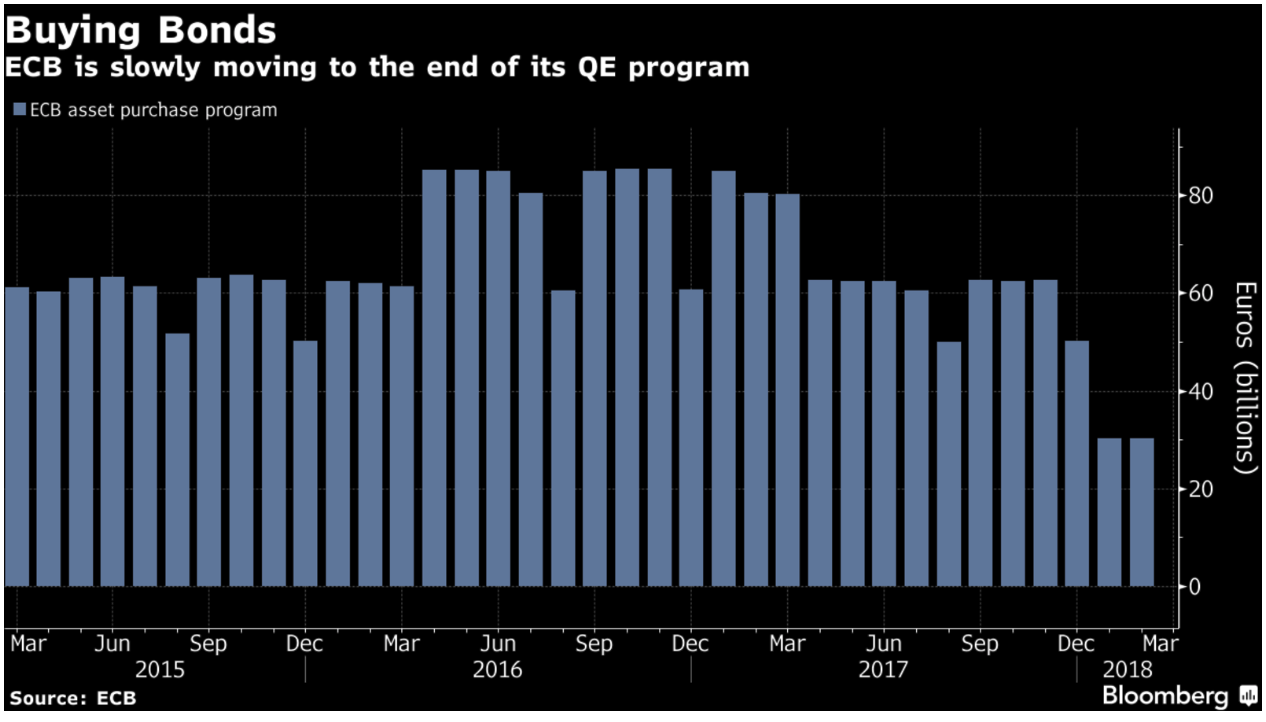

ECB Assumes Final QE Push Totaling 30 Billion Euros (Bloomberg.com)

Hungarian National Bank Decides to Bring Gold Reserves Back Home (HungaryToday.hu)

Gold Prices (LBMA AM)

09 Mar: USD 1,319.35, GBP 955.21 & EUR 1,072.50 per ounce

08 Mar: USD 1,325.40, GBP 955.08 & EUR 1,070.39 per ounce

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

Silver Prices (LBMA)

09 Mar: USD 16.49, GBP 11.92 & EUR 13.40 per ounce

08 Mar: USD 16.48, GBP 11.89 & EUR 13.31 per ounce

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

Recent Market Updates

– London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

– Gold Does Not Fear Interest Rate Hikes

– RaboDirect Closing – Gold May Protect From Irish Banks Going “Belly Up Again” – Finuncane

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

THE FOLLOWING CAME FROM KOOS JANSEN:

YOU WILL NOTE THAT FOR THE FIRST TIME EVER CHINA EXPORTED GOLD TO LONDON.

THE QUESTION IS WHY?

I ASKED MY GOOD FRIEND REG HOWE FOR HIS THOUGHTS ON THIS AND WE AGREE THAT THERE ARE TWO POSSIBILITIES: 1) THAT THERE IS EXTREME SHORTAGE IN LONDON AND A MAJOR BANK COULD NOT DELIVER UPON ALONG OVER THERE.. CHINA WOULD BE ASKING FOR A BIG QUID PRO QUO FOR PROVIDING THE NECESSARY PHYSICAL. (IT MAKES SENSE IN THE FACT THAT GOLD IS IN BACKWARDATION IN LONDON)

2. TO HELP IN THE FACILITATION OF THE NEW OIL FOR YUAN FOR GOLD NEW FORMAT OR SOME FUTURE MEASURE THAT CHINA WILL REQUIRE OR AT LEAST BENEFIT FROM ADDITION PHYSICAL LIQUIDITY IN LONODN..

REGARDLESS, IT SHOWS SCARCITY OVER THERE.

FROM REG HOWE TO ME:

“Have read speculation that it may have to do with the mechanics of settling the new oil and gold contracts in physical. More generally, I would guess it’s one of two things: (1) Chinese help in containing some serious stress in the gold market due to lack of physical, e.g., some central bank or major bullion bank unable to deliver, in which case there is likely a big quid pro quo; or (2) a positioning to facilitate some (other) future measure by China that will require or at least benefit from additional physical liquidity in London. In any event, seems to be more evidence of severe shortage of physical in London, otherwise they would just buy it there at today’s suppressed prices.”

END

Alabama becomes the 37th state to exempt sales tax on gold and silver bullion as well as coins

(courtesy GATA>Numismatic News.Iola Wisconsin)

Alabama exempts gold and silver bullion and coins from sales tax

Submitted by cpowell on Sat, 2018-03-10 15:15. Section: Daily Dispatches

ICTA Wins Another One for Coin Buyers

By Dave Harper

Numismatic News, Iola, Wisconsin

Thursday, March 8, 2018

The Industry Council for Tangible Assets has notched another sales tax win.

Congratulations.

Alabama becomes the 37th state to exempt sales of gold, silver, platinum, and palladium bullion and money, ICTA’s David Crenshaw reports.

Numismatic commerce can blossom thanks to Gov. Kay Ivey. She signed into law Senate Bill 156 on March 6 to create a sales and use tax exemption on U.S. coins and currency and precious metals bullion sales.

Of course she isn’t the only one who deserves the high praise of collectors.

“The bill’s author, Sen. Tim Melson, along with its House sponsor, Rep. Ron Johnson, championed the bill through the legislature,” said Phil Darby (J&P Coins and Currency in Helena).

“Alabama coin businesses and collectors owe them a debt of gratitude,” Darby said. …

… For the remainder of the report:

http://www.numismaticnews.net/buzz/icta-wins-another-one-coin-buyers

END

Ralph Benko explains beautifully by the USA had continual trade deficits in order to maintain its status as the world’s reserve currency. The USA exported paper dollars which cost them a few pennies and got real goods for that paper money but this occurred with a curse..the USA manufacturers were decimated. Now Trump is attempting to stop this..

a good read//

(Ralph Benko/GATA)

Ralph Benko: Trade deficits are the price of issuing the world reserve currency

Submitted by cpowell on Mon, 2018-03-12 00:30. Section: Daily Dispatches

8:30p ET Sunday, March 11, 2018

Dear Friend of GATA and Gold:

Financial writer and gold standard advocate Ralph Benko this week joined those explaining that huge trade deficits are inevitable for any country that enjoys the “exorbitant privilege” of issuing the world reserve currency.

Benko writes:

“World War II — in which my heroic father Max Benko fought along with millions of others — left America relatively unscathed. After V-Day our allies and our vanquished enemies’ economies lay in shambles. We could (and did) give ourselves a treat while extending an invisible helping hand — one much greater than the Marshall Plan — to war-torn Europe and Japan.

“How? After World War II, the world, led by America, entered into an arrangement called Bretton Woods. This made the U.S. dollar the world’s ‘reserve currency.’

“In practice, Bretton Woods meant that Americans could consume more than we produce — an exorbitant privilege — by exporting dollars rather than goods. How, exactly, did that work? ….

“As American economist Barry Eichengreen summarized: ‘It costs only a few cents for the Bureau of Engraving and Printing to produce a hundred-dollar bill, but other countries had to pony up $100 of actual goods in order to obtain one.’

“That privilege, which made great sense during the period immediately after World War II, became a curse.

“How did our ‘exorbitant privilege’ transform into a curse? By inequitably prejudicing our manufacturers.

“The key element — the reserve currency status of the dollar — of the Bretton Woods ‘Calvinball’ monetary treaty remains in place. Time to end that … as Donald Trump seems to almost preternaturally intuit.”

Benko’s commentary is headlined “Exit Gary Cohn. Enter Lewis Lehrman, Steve Forbes, or Larry Kudlow?” and it’s posted at Forbes here:

https://www.forbes.com/sites/ralphbenko/2018/03/09/exit-gary-cohn-enter-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee

CPowell@GATA.org

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3277 /shanghai bourse CLOSED UP 19.53 POINTS OR 0.59% / HANG SANG CLOSED UP 598.12 POINTS OR 1.93%

2. Nikkei closed UP 354.83 POINTS OR 1.65% /USA: YEN FALLS TO 106.53/

3. Europe stocks OPENED DEEPLY IN THE GREEN EXCEPT LONDON /USA dollar index FALLS TO 90.08/Euro RISES TO 1.2309

3b Japan 10 year bond yield: FALLS TO . +.053/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.53/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.65 and Brent: 65.16

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.636%/Italian 10 yr bond yield UP to 2.023% /SPAIN 10 YR BOND YIELD DOWN TO 1.423%

3j Greek 10 year bond yield FALLS TO : 4.184?????????????????

3k Gold at $1315.60 silver at:16.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 16/100 in roubles/dollar) 56.82

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9502 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1685 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.636%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.896% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.154% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets Rally, S&P Back Over 2,800 On “Goldilocks” Mood Ahead Of Treasury Deluge

The “goldilocks” mood that was unleashed after Friday’s jobs report (high growth, low inflation) has spread around the globe, sending Asian and European markets higher as trade-war concerns took a back seat to economic optimism. The dollar slipped and Treasuries held strady even as the US Treasury prepares to sell $145 billion in debt today (including both 3Y and 10Y Paper), while most commodities fell.

“Friday’s U.S. employment data was about as perfect a set of figures as you can get from a policy maker’s point of view. The increase in jobs was nothing short of amazing,” said ACLS Global’s Marshall Gittler. “In other words, it was a ‘Goldilocks’ report: not too hot, not too cold, just right.”

“Our customers are still bullish,” Chris Brankin, chief executive officer at TD Ameritrade Singapore, told Bloomberg TV. “You saw the jobs report last Friday, which was a perfect scenario — you had an uptick in wages, but not too much. Investors have taken that opportunity to buy the market dips and we look for the bull market to continue.”

European shares shot up across the board, following their Asian counterparts, while emerging market currencies strengthened as investors bought up so-called riskier assets and sold safe haven securities such as gold and government bonds. After the S&P surged 1.7% on Friday – its second best day of the year – S&P futures have continued to levitate overnight, and are back above 2,800 and fast approaching their late January all time highs of 2,883.

The Stoxx Europe 600 Index rose for a sixth day, poised for the longest winning streak since October as utility companies set the pace following a bid by EON for RWE’s Innogy. Germany’s DAX led gains in Europe, rising 0.9% while MSCI’s world equity index hit a two-week high. Concerns over tariffs have been weighing on European stocks, with the main European stock index hitting a seven-month low at the start of the month. It has recovered somewhat from that trough to rise 0.3% on Monday.

Earlier, the MSCI Asia-Pacific ex-Japan Index climbed 1.4 percent, poised for a third session of gains. South Korea rose 1%, while Australia’s main index added 0.7 percent, boosted by mining shares on news that Australia could be exempt from new U.S. trade tariffs on steel and aluminum imports. Hong Kong stocks climbed with other Asian markets after Friday’s U.S. jobs report showed an increase in hiring without rapid wage gains: the Hang Seng gained 1.9%, its third day of gains, and the highest since Feb. 5. The Hang Seng China Enterprises Index jumped 2.1%, also up for third session, while on the maindland, the Shanghai Composite added 0.6% and the ChiNext Index of smaller shares rose 1.4%.

In global FX, investors shifted their focus to politics sending the Aussie higher after the country secured an exemption from U.S. tariffs on steel and aluminum and as politicians from a wide range of other countries joined the chorus to also be on the list of Trump tariff exemptions. Meanwhile, as noted last night, the yen jumped after Japan’s Finance Minister Taro Aso refused to step down despite news that his name and that of Prime Minister Shinzo Abe were removed from documents connected with a land-sale scandal, creating uncertainty around the future of Abenomics. The advance however was pared after Aso said he won’t resign.

Commenting on the USDJPY, Masashi Murata, a currency strategist at Brown Brothers Harriman in Tokyo said that “The theme for 2018 is the risk of the dollar-yen breaking 100,” adding that the yen above that level “wouldn’t look excessive from the perspective of its fundamentals.” Separately, Goldman analysts said that the BOJ and the Japanese government have “very limited” policy options for reining in yen appreciation, and they are most likely to take a wait-and-see stance until the latest round of gains comes to an end.

Investors had trimmed holdings of yen last week on news U.S. President Donald Trump was prepared to meet with North Korean leader Kim Jong Un, a potential breakthrough in nuclear tensions in the region. U.S. officials on Sunday defended Trump’s decision, saying the move was not just for show and not a gift to Pyongyang. “Now the U.S. is back to goldilocks at least for now, the tariffs are less severe, and Kim and Trump are to meet,” said Shane Oliver, Sydney-based chief economist at AMP. “We still expect more volatility this year as many of these issues have further go run, but the broad trend in shares likely remains up.”

The dollar edged lower a second day as markets digested Friday’s jobs report, which kept stocks in Asia and Europe underpinned.

In geopolitical news, North Korea reportedly wants a peace treaty and to build ties with US, while its leader Kim also wants a US embassy in Pyongyang.

In Brexit news, UK and EU companies reportedly could face an additional GBP 58bln in annual costs in the event of a no-deal Brexit. Meanwhile, UK consumer spending suffered its weakest start to the year since 2012, according to data compiled by Visa.

In rates, the yield on 10-year Treasuries climbed less than one basis point to 2.90%,the highest in more than two weeks. Germany’s 10-year yield dipped one basis point to 0.64%, while Britain’s 10-year Gilt rose less than one basis point to 1.493 percent.

Today, US rates traders will have a very busy day with the US set to sell $145BN in sells 3- and 6-month bills, as well as a 3-year notes and 10-year notes reopening. Big concessions into the auctions are expected to help soak up the massive supply. As a reminder the last time that the market faced a 3y and 10y auction on the same day last year Treasuries sold off following weak demand in the latter auction.

Oil prices pared back gains seen on Friday with WTI (-0.5%) and Brent (-0.6%) seen lower amid concerns of rising US output looming in the market despite a slowdown in rig drilling activity recorded at the back end of last week. In the metals complex, following the US steel and aluminium tariffs, Chinese iron ore future fell for a 3rd straight session hitting near four-month lows closing down 2.6%. The steelmaking raw materials are under pressure from softer demand and high product inventories held by trading companies. The WSJ reported that OPEC is reported to be divided regarding views on the right price of oil with Iran said to prefer USD 60/bbl, while Saudi Arabia would prefer prices to be at USD 70/bbl. There were also reports that Iran Oil Minister Zanganeh stated that OPEC could agree in June to begin relaxing oil output cuts for 2019.

Bulletin Headline summary from RanSquawk

- DAX outperforms amid multi-billion revamp in German utility sector.

- USD-index hovers around 90, having trimmed earlier losses.

- Looking ahead, highlights include the Eurogroup meeting, 3- and 10-year note auctions from the US

Market Snapshot

- S&P 500 futures up 0.3% to 2,798.25

- STOXX Europe 600 up 0.3% to 379.19

- MXAP up 1.6% to 178.46

- MXAPJ up 1.4% to 588.82

- Nikkei up 1.7% to 21,824.03

- Topix up 1.5% to 1,741.30

- Hang Seng Index up 1.9% to 31,594.33

- Shanghai Composite up 0.6% to 3,326.70

- Sensex up 1.2% to 33,713.20

- Australia S&P/ASX 200 up 0.6% to 5,996.12

- Kospi up 1% to 2,484.12

- German 10Y yield unchanged at 0.649%

- Euro up 0.2% to $1.2328

- Italian 10Y yield rose 2.5 bps to 1.753%

- Spanish 10Y yield unchanged at 1.436%

- Brent futures down 0.6% to $65.10/bbl

- Gold spot down 0.3% to $1,320.39

- U.S. Dollar Index down 0.1% to 89.98

Top Overnight News

- North Korean leader Kim Jong Un wants to sign a peace treaty and establish diplomatic relations with the U.S., which includes having a U.S. embassy in Pyongyang, Dong-A Ilbo newspaper reports, citing an unidentified senior official at South Korean President Moon Jae-in’s office

- China’s trade minister Zhong Shan warned that a trade war with the U.S. would bring disaster to the global economy, but said his nation won’t start one and that talks with the Trump administration continue

- China, Canada and Hong Kong are among the economies most at risk of a banking crisis, according to early-warning indicators compiled by the Bank for International Settlements

- Add one more thing to the list of worries for the world’s most indebted nation: weakening demand at its bond auctions. While there’s no danger of the U.S. being unable to borrow as much as it needs, over the past two years, the drop-off has been unmistakable

- Britain may soon start to see the beginning of the end of austerity, as the Chancellor of the Exchequer prepares to announce the smallest deficit in a decade during his Spring Statement on Tuesday

- London house prices are falling at the fastest pace since the depths of the recession almost a decade ago, with the capital’s most expensive areas seeing the biggest declines, according to a report published by Acadata on Monday

Asia stocks were higher across the board as the region took its first opportunity to react to Friday’s rally on Wall St and jobs data from US where NFP smashed expectations, but wage growth slowed which in turn provided a goldilocks backdrop for stocks. ASX 200 (+0.6%) was led by commodity names after crude rallied over 3% on Friday and PM Turnbull confirmed Australia is to be exempted from US tariffs. Nikkei 225 (+1.6%) outperformed but closed off its best levels as the cronyism scandal continued to haunt PM Abe after Japan’s Finance Ministry confirmed documents had been doctored in a land-sale to a school operator which allegedly used ties to PM Abe’s wife to get a cheap deal on state-owned land. Elsewhere, Hang Seng (+1.5%) and Shanghai Comp. (+0.7%) also gained although the mainland got off to a slow start as US-China trade war concerns somewhat lingered and as participants also mulled over Xi’s power consolidation after China’s legislature voted to formally scrap presidential term limits from its constitution. Finally, 10yr JGBs are flat with demand constrained amid the heightened appetite for risk, while the BoJ were also in the market but kept its Rinban amounts unchanged from the prior. The PBoC injected CNY 50bln via 7-day reverse repos and CNY 40bln via 28-day reverse repos; the PBoC also set CNY mid-point at 6.3333 (Prev. 6.3451).

As reported last night, Japanese Finance Minister Aso is under pressure to resign over a report regarding alleged favours to a school with connections to the Japanese PM Abe. The prime minister told parliament in February last year that he’d resign if any link emerges between himself or his wife Akie and the land deal.

Top Asian News

- China Banking Crisis Warning Signal Still Flashing, BIS Says

- JPMorgan Sees Busiest Mideast Year With IPOs, M&A Driving Deals

- Japan Finance Minister Under Fire as Abe School Scandal Deepens; Stock Investors Are Nonchalant for Now as Abe’s Scandal Deepens

- China’s Mystery Russia Oil Partner Seen Delaying $9 Billion Deal

The European cash open mimicked the strong positive sentiment seen in Asia and in the US on Friday following US NFP data beating expectations but wage growth slowing down providing a goldilocks backdrop for stocks. Major bourses are in the green (Euro Stoxx 50 +0.45%) with the exception of the FTSE 100 underperforming weighed down by a strong sterling. DAX 30 is supported by the utilities sector outperforming following reports of RWE (+8.8%) agreeing to swap control of Innogy (+12.9%) for renewable assets with rival E.ON (+5.4%). E.ON has agreed to purchase Innogy from RWE as part of a deal valuing at EUR 20bln, marking one of the largest shake-ups of the European power supply market. This could however place doubt on the deal between Innogy’s Npower and UK listed SSE (-2.2%). Following months of attempted takeover, Melrose (-2.9%) has submitted their final offer to engineering group GKN (+0.8%) of GBP 8.1bln following their previous offer of GBP 7.4bln which GKN described as “fundamentally” undervaluing its business and the approach as “entirely opportunistic”.

Top European News

- Elkem to Raise $670 Million in Biggest Norway IPO Since 2010

- May Faces Calls to Retaliate Against Russia After Spy Attack

- Ruble Is Top Pick for $25 Billion Investor After Czech Bonanza

In FX, it has been a quiet start to the week, but the Greenback is weaker vs all G10 counterparts bar the Loonie, as Usd/Cad hovers above 1.2800 after last Friday’s mixed US and Canadian jobs data (to recap, the former blew away forecasts at 300k+, but latter just missed and would have been negative without part-time workers). The Kiwi is outperforming amidst equity market gains and mostly risk-on trade as it regains 0.7300 status vs the Usd, but Usd/Jpy has pulled back from marginal 107.00+ highs post-NFP to around 106.50 on the land sale scandal involving PM Abe and Finance Minister Aso. Note also, tech resistance around the 21 DMA at 106.79 is capping the pair, but hefty option expiries at 107.00 run off this Thursday and could keep the headline afloat. Aud another relative gainer and firmer within a 0.7845-80 range as Australia negotiates a security deal with the US to avoid aluminium and steel tariffs. Usd/Chf is probing back below 0.9500, Eur/Usd is sitting in a tight band above 1.2300 and Cable is holding between 1.3850-80 ahead of Tuesday’s UK Budget. Back to option expiries, but for today there is 1 bn either side of 1.2300 in Eur/Usd at 1.2275 and 1.2330 and just over 300 mn in Nzd/Usd at 0.7300.

In commodities, oil prices pared back gains seen on Friday with WTI (-0.5%) and Brent (-0.6%) seen lower amid concerns of rising US output looming in the market despite a slowdown in rig drilling activity recorded at the back end of last week. In the metals complex, following the US steel and aluminium tariffs, Chinese iron ore future fell for a 3rd straight session hitting near four-month lows closing down 2.6%. The steelmaking raw materials are under pressure from softer demand and high product inventories held by trading companies. The WSJ reported that OPEC is reported to be divided regarding views on the right price of oil with Iran said to prefer USD 60/bbl, while Saudi Arabia would prefer prices to be at USD 70/bbl. There were also reports that Iran Oil Minister Zanganeh stated that OPEC could agree in June to begin relaxing oil output cuts for 2019.

Looking at the day ahead, as is the norm post payrolls, it’s a quiet start to the week on Monday with the only data of note being the US monthly budget statement for February. Politics should remain at the forefront, however, with Germany’s Chancellor Merkel expected to sign a coalition pact with the Social Democrats in Berlin and Italy’s Democratic Party due to hold a leaders’ meeting to replace Matteo Renzi. EU government officials will also kick off the four-day meeting to discuss the EU’s Brexit position.

US Event Calendar

- 10:30am: U.S. to Sell USD45 Bln 6-Month Bills

- 10:30am: U.S. to Sell USD28 Bln 3-Year Notes

- 12pm: U.S. to Sell USD51 Bln 3-Month Bills

- 12pm: U.S. to Sell USD21 Bln 10-Year Notes Reopening

- 2pm: Monthly Budget Statement, est. $216.0b deficit, prior $192.0b deficit

DB concludes the overnight wrap

So, another week and another hotly anticipated US inflation print for markets to be wary of. In fact, it should be a fairly busy week ahead with plenty of US data despite it being a post payrolls week, bumper Treasury supply which should be a decent test for bond markets and of course unpredictable politics to keep everyone on their toes. Indeed, no doubt the uncertainty fuelled by steel and aluminium tariffs tit-for-tat could continue, while markets will also be waiting for potential further details about President Trump’s meeting with North Korea leader Kim Jong Un. One of the big question marks is where they’ll meet exactly and we can’t help but feel that we could see some sort of Olympics style pitch between nations to host this hotly anticipated event.

On a more serious note the reaction to the proposed meeting has actually been fairly mixed. The optimistic view is that a summit between the US and North Korea could offer a genuine opportunity to reduce tensions on the Korean peninsula, particularly in light of the failures of past agreements. However there appears to be an equal amount of scepticism with some suggesting that it could be an opportunity for North Korea to secure sanctions relief and buy time on nuclear efforts. Only time will tell but it’s clearly a very significant moment for geopolitics globally. Over the weekend CIA Director Mike Pompeo confirmed that the US will be making no concessions to North Korea and that discussions, if they do indeed occur, “will play out over time”.

Back to that big data release for this week, as of this morning the market consensus is for a +0.2% mom headline reading and +0.2% core reading for US CPI on Tuesday. Our US economists expect +0.1% mom and +0.2% mom respectively. The latter should hold at +1.8% yoy should we see that, and in fact our colleagues add that the annual growth rate of core CPI will mechanically rise by around 20bps in the March data release just from annualizing the -10% decline in wireless telephone services.

Meanwhile, also due tomorrow is the Special Congressional election in Pennsylvania which shouldn’t be underestimated as it will likely be seen as a decent bellwether for the prospect of Republicans holding onto majorities in the House and Senate at the November midterms. So that should be interesting. On the same day we’ll have the UK Spring Statement although our rates team and economists aren’t expecting any big policy announcements. The market should instead be focused on the publication of the 2018-19 Gilt remit. You can see a preview of the Statement here. In terms of other snippets, Germany’s Merkel and the Social Democrats are expected to sign a coalition pact today, while Italy’s Democratic Party will also start the search for their new party leader. Brexit related newsflow should also continue with the European Council and European Commission expected to make a statement on Tuesday while the four-day EU ambassadors meeting kicks off today.

All that to look forward to then. Over the weekend it’s actually been fairly quiet for newsflow with the most notable coming from China with the – as expected – announcement that the presidential term limit has been repealed, which in turn will allow President Xi Jingping to in theory hold onto power indefinitely. The other story worth noting is the latest BIS quarterly report which notes that China, Canada and Hong Kong are among those economies most at risk of a banking crisis, based on early warning indicators. The report also pointed towards the dangers of increased passive investing, particularly with regards to “encouraging aggregate leverage”. Elsewhere, on the big protectionist theme reverberating through markets at the moment, China’s trade minister Zhong noted “there are no winners in a trade war…China does not wish to fight a trade war, nor will China initiate one, but we…will resolutely defend the interests of our country”. In Germany, Economy Minister Zypries noted “Trump’s policies are putting the order of a free global economy at risk” and that Europe needs to avoid being divided by Trump’s offer to exempt some countries such as Canada, Mexico and Australia.

So, with the likely highlight for markets this week being Tuesday’s CPI report, it of course follows the softer than expected average hourly earnings data from Friday’s employment report. In fairness, it only just missed consensus as the unrounded +0.1498% mom compared to expectations for +0.2% mom however downward revisions to prior months meant the annual rate dropped to +2.6% yoy from +2.8% and back to the lowest since November. On the other hand, the other big takeaway from the report was the bumper payrolls number. The 313k print not only smashed expectations for 205k but was also the highest since July 2016. The two prior months were also revised higher by a cumulative 54k. Away from those usual headline grabbers’ one interesting aspect of the report, and which typically flies more under the radar, that our US economists pointed out was the increase in prime-age participation. Fed Chair Powell previously noted in his testimony that still low prime-age labour force participation is one remaining potential source of labour market slack. However, it was noticeable to see this climb four-tenths last month and to the highest since mid-2010. The bottom line is that this could still lend argument to the fact there is still some slack left in the labour market.

All-in-all a bit of a double-edged sword sort of report then. Markets certainly appreciated the goldilocks nature of it with the S&P 500 rallying to a +1.74% gain by the close of play – and touching the highest level since February 1st -and 10y Treasuries climbing to 2.895% (+3.7bps). Fed Funds contracts are now implying odds of just under 25% for 4 rate hikes this year. We’ll of course find out in 9 days time at the next FOMC meeting if the data is enough to support an increase in the median dot to 4. Speaking of bond markets, it’s worth noting that the Treasury market is likely to face a bit of a supply test today as we’ll get both a 3y and 10y auction. As a reminder the last time that the market faced a 3y and 10y auction on the same day last year Treasuries sold off following weak demand in the latter auction.

This morning risk assets are broadly higher in Asia following the positive US lead, with the Nikkei (+1.49%), Kospi (+0.99%), Hang Seng (+1.48%), ASX 200 (+0.55%) and China’s CSI 300 (+0.49%) all up as we type. Markets in Japan have pared back gains slightly following news that Finance Minister Taro Aso is supposedly coming under pressure to quit according to Bloomberg due to his involvement in a scandal related to the sale of public land to a school.

Moving on. In terms of other markets on Friday. The Nasdaq rose +1.79% and to a fresh record high. European equities were broadly higher with the Stoxx 600 up for the fifth straight day (+0.43%) while the DAX was the laggard (-0.07%). Government bonds were weaker with core 10y bond yields up 2-3bp (Bunds & Gilts +1.9bp) while peripherals slightly underperformed. In FX, the USD dollar index fell 0.10% while the Euro was marginally down and Sterling gained 0.28%. Finally, WTI oil was up for the first time in three days (+3.19% to $62.09/bbl) while precious metals gained slightly.

Away from markets, three unnamed sources told Reuters that ECB staff put forward a scenario to policy makers at last week’s ECB meeting suggesting the bank will end QE this year after winding down for three months followed by a rate increase in the middle of next year. One source noted these are “assumptions…. (and they) don’t have policy relevance because they are not commitments”. Notably, sources noted the hypothesis was met favourably by policy makers from the Euro area’s richer Northern countries, but less so by the Southern neighbours.

On Friday we also heard from a couple of Fed speakers post the employment report. The Fed’s Rosengren noted that “I expect that it will be appropriate to remove monetary policy accommodation at a regular but gradual pace – and perhaps a bit faster than the three (rate hikes) envisioned for this year”. He also added that as the labour market continues to tighten “….one would expect to see continued upward pressure on wages”. Elsewhere, the Fed’s Evans noted the payroll report was a “very strong number” and was “looking forward to strong wage growth”. On rates, he noted that he continues to be nervous about inflation running below the Fed’s 2% target and believes “…we have the ability to be cautious”.

With regards to the other economic data on Friday. In the US, the unemployment rate was steady mom at its 17 year low and slightly higher than expected at 4.1% (vs. 4.0%). Elsewhere, the final reading for January wholesale inventories was revised up 0.1ppt to 0.8%. Factoring in the above, the Atlanta Fed’s estimate of Q1 GDP growth was revised down 0.3ppts to 2.5% saar. In Europe, the January IP was broadly lower than expectations. In Germany, it was -0.1% mom (vs. +0.6% expected) weighted down by lower activity in the construction sector. Notably, annual growth is still solid at +5.5% yoy. France and the UK’s IP were both lower than expected at +1.2% yoy (vs. +3.8% expected) and +1.6% yoy (vs. +1.9% expected) respectively. Elsewhere, Germany’s January trade surplus was less than expected at €17.4bln (vs. €18.1bln) as exports weakened in the month, while the UK’s January trade deficit was -£3.1bln (vs. – £3.4bln expected).

As is the norm post payrolls, it’s a quiet start to the week on Monday with the only data of note being the US monthly budget statement for February. Politics should remain at the forefront, however, with Germany’s Chancellor Merkel expected to sign a coalition pact with the Social Democrats in Berlin and Italy’s Democratic Party due to hold a leaders’ meeting to replace Matteo Renzi. EU government officials will also kick off the four-day meeting to discuss the EU’s Brexit position.

end

3. ASIAN AFFAIRS

i)MONDAY MORNING/LATE FRIDAY NIGHT: Shanghai closed UP 19.83 POINTS OR 0.59% /Hang Sang CLOSED UP 598.12 POINTS OR 1.93% / The Nikkei closed UP 354.83 POINTS OR 1.63%/Australia’s all ordinaires CLOSED UP 0.53%/Chinese yuan (ONSHORE) closed UP at 6.3277/Oil UP to 61.05 dollars per barrel for WTI and 65.16 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3277 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3257 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS INITIATED/ )

3 a NORTH KOREA/USA

/NORTH KOREA/USA

3 b JAPAN AFFAIRS

Last year , we reported to you on the Japanese “kindergarten” scandal. It roiled Japanese markets for weeks only to be saved by North Korean rockets flying over Japan. It has now resurfaced and there are reports of altered documents involving Abe’s wife. The tax department also has to answer for this. The deputy finance minister, Aso is has the tax department reporting to him so he may have to resign and that will put the entire Japanese economic “recovery” in jeopardy

(courtesy zerohedge)

Japan Markets Roiled As Moritomo Scandal Returns, Abe May Be Forced To Resign