GOLD: $1312.15 down $5.75

Silver: $16.20 down 13 CENTS

Closing access prices:

Gold $1310.70

silver: $16.20

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1323.94 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1316.50

PREMIUM FIRST FIX: $7.44

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1323.95

NY GOLD PRICE AT THE EXACT SAME TIME: $1316.25

PREMIUM SECOND FIX /NY:$7.70

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1312.75

NY PRICING AT THE EXACT SAME TIME: $1316.25 ???

LONDON SECOND GOLD FIX 10 AM: $1311.00

NY PRICING AT THE EXACT SAME TIME. $1309.60 ???? SIGNALS CROSSED?

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:4 NOTICE(S) FOR 400 OZ.

TOTAL NOTICES SO FAR 28 FOR 2800 OZ

For silver:

MARCH

27 NOTICE(S) FILED TODAY FOR

135,000 OZ/

Total number of notices filed so far this month: 5186 for 25,930,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8430/OFFER $8,500: DOWN $133(morning)

Bitcoin: BID/ $8931/offer $9002: UP $369 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A GOOD SIZED 1319 contracts from 210,242 RISING TO 211.635 DESPITE YESTERDAY’S TINY 5 CENT GAIN IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1929 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1929 CONTRACTS. WITH THE TRANSFER OF 1929 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1929 CONTRACTS TRANSLATES INTO 9.645 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

30,997 CONTRACTS (FOR 14 TRADING DAYS TOTAL 30,997 CONTRACTS) OR 154.985 MILLION OZ: AVERAGE PER DAY: 2214 CONTRACTS OR 11.070 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 154.985 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.14% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 636.809 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A GOOD SIZED GAIN IN COMEX OI SILVER COMEX OF 1319 DESPITE THE 5 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1929 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1929 EFP’S FOR THE MONTH OF MARCH WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 3240 OI CONTRACTS i.e. 1929 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 1319 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 5 CENTS AND A CLOSING PRICE OF $16.43 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.051 BILLION TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 28 NOTICE(S) FOR 140,000 OZ OF SILVER

In gold, the open interest ROSE BY A STRONG SIZED 6790 CONTRACTS UP TO 540,677 WITH THE FAIR SIZED RISE IN PRICE YESTERDAY ( GAIN OF $5.25) HOWEVER FOR MONDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN HUGE SIZED 12,906 CONTRACTS : APRIL SAW THE ISSUANCE OF 12,656 CONTRACTS, JUNE SAW THE ISSUANCE OF 250 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 540,677. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUMONGOUS OI GAIN IN CONTRACTS: 6,790 OI CONTRACTS INCREASED AT THE COMEX AND A HUGE SIZED 12,906 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 19,696 CONTRACTS OR 1,969,600 OZ =62.52 TONNES

YESTERDAY, WE HAD 11,571 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 131,453 CONTRACTS OR 13,145,300 OZ OR 408.86 TONNES (14 TRADING DAYS AND THUS AVERAGING: 9390 EFP CONTRACTS PER TRADING DAY OR 939,000 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 14 TRADING DAYS IN TONNES: 408.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 408.86/2550 x 100% TONNES = 16.03% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1711.54 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX WITH THE SMALLISH RISE IN PRICE IN GOLD TRADING YESTERDAY ($5.25 GAIN). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,906 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,906 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 19,696 contracts ON THE TWO EXCHANGES:

12,906 CONTRACTS MOVE TO LONDON AND 6790 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 62.52 TONNES).

we had: 4 notice(s) filed upon for 400 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $5.75 : A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD / A DEPOSIT OF 11.49 TONNES OF GOLD

Inventory rests tonight: 850.64 tonnes.

SLV/

WITH SILVER DOWN 13 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 319.671 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A FAIR 1329 contracts from 210,242 UP TO 211,561 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE RISE IN PRICE OF SILVER (5 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1929 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 1393 CONTRACTS TO THE 1929 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 3322 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 16.61 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FALL IN SILVER PRICING YESTERDAY (5 CENTS RISE IN PRICE) . BUT WE ALSO HAD ANOTHER FAIR SIZED 1929 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 11.39 POINTS OR 0.35% /Hang Sang CLOSED UP 36.17 POINTS OR 0.11% / The Nikkei closed DOWN 99.93 POINTS OR 0.47%/Australia’s all ordinaires CLOSED DOWN 0.39%/Chinese yuan (ONSHORE) closed UP at 6.3308/Oil UP to 62.76 dollars per barrel for WTI and 66.91 for Brent. Stocks in Europe OPENED GREEN EXCEPT SPAIN . ONSHORE YUAN CLOSED UP AT 6.3308 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3266 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY & MARKETS/BUT NEW TRUMP TARIFFS INITIATED/WEAKER GLOBAL MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

i)Trump is set to unleash a huge $60 billion China tariffs on Friday as he tries to tackle their “theft” of intellectual property and other Chinese transgressions

( zerohedge)

ii)Xi delivers a stark warning to Trump: keep your hands off Taiwan after he signs into law the “Taiwanese Travel Act”. Relations between Taiwan and Central have been antagonistic lately as the new Taiwan leader, Tsai, is against the “One China Policy” which stipulates that Taiwan is only a province of mainland China.

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Erdogan, after his victory in Afrin has sights on Eastern Syria and Sinjar Iraq as he will no doubt “cleanse” the area of PKK ( Kurdish) supporters

( zerohedge)

6 .GLOBAL ISSUES

(courtesy zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

Chris Powell answers Dr Keith Weiner beautifully on central bank gold suppression

( Chris Powell/GATA)

10. USA stories which will influence the price of gold/silver

i)This is not good: a package bound for Austin exploded at a Texas Fed Ex warehouse

( zerohedge)

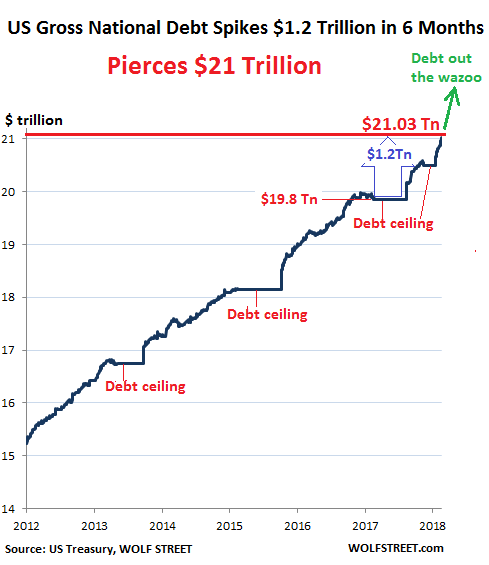

ii)The USA national debt at 21 trillion dollars is growing 36% faster than the uSA economy. This is a time bomb

(courtesy Simon Black/SovereignMan.com)

( zerohedge)

(courtesy Kranzler/Roberts)

v)Another great commentary from David Stockman on where the uSA economy is heading

( David Stockman)

vi)SWAMP STORIES

a)Trump to hand over written documents to Mueller/but provide a narrative of the White House view and not Trump’s personal view

( zerohedge)

b)First Stormy Daniels and now ex Playboy model, McDougal is suing the parent of the National Enquirer, AMI to break the silence on their affair. In essence she wants to be paid. The CEO of AMI is a close friend of Donald Trump

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:354.161 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 321,719 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A FAIR SIZED 1393 CONTRACTS FROM 210,242 UP TO 211,561 WITH OUR 5 CENT GAIN IN YESTERDAY’S TRADING). ALSO,WE WERE ALSO INFORMED THAT WE HAD 1929 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1929. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A STRONG SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 3240 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1319 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1929 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 3240 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month GAINED 95 contracts RISING TO 225 contracts. We had 24 contracts filed YESTERDAY, so we GAINED 119 contracts or an additional 595,000 OZ will stand in this active delivery month of March.(AS SOMEBODY IS IN URGENT NEED OF CONSIDERABLE PHYSICAL SILVER)

April GAINED 3 contracts RISING TO 417 .

The next big active delivery month for silver will be May and here the OI GAINED 172 contracts UP to 150,528

We had 27 notice(s) filed for 135,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 20/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

9840.61 oz

Brinks

Scotia

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

4 notice(s)

400 OZ

|

| No of oz to be served (notices) |

494 contracts

(49400 oz)

|

| Total monthly oz gold served (contracts) so far this month |

28 notices

2800 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (28) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (498 contracts) minus the number of notices served upon today (4 x 100 oz per contract) equals 52,200 oz, the number of ounces standing in this nonactive month of MARCH (1.6238 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (28 x 100 oz or ounces + {(498)OI for the front month minus the number of notices served upon today (4 x 100 oz )which equals 52,000 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 2 CONTRACTS OR AN ADDITIONAL 200 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

5071.859 oz

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

599,140.700 oz

CNT

|

| No of oz served today (contracts) |

27

CONTRACT(S

(135,000 OZ)

|

| No of oz to be served (notices) |

198 contracts

(990,000 oz)

|

| Total monthly oz silver served (contracts) | 5186 contracts

(25,930,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into CNT: 599,140.700 oz

ii) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

total deposits today: 599,140.700 oz

we had 1 withdrawals from the customer account;

i) Out of Delaware: 5071.859 oz

total withdrawals; 5071.859 oz

we had 0 adjustments

total dealer silver: 59.203 million

total dealer + customer silver: 257.451 million oz

The total number of notices filed today for the March. contract month is represented by 27 contract(s) FOR 135,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5186 x 5,000 oz = 25,930,000 oz to which we add the difference between the open interest for the front month of Mar. (225) and the number of notices served upon today (27 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5186(notices served so far)x 5000 oz + OI for front month of March(225) -number of notices served upon today (27)x 5000 oz equals 26,920,000 oz of silver standing for the March contract month.

We GAINED an additional 119 contracts or 595,000 additional silver oz will stand for delivery at the comex as somebody was in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 69,847 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 77,589 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 77,589 CONTRACTS EQUATES TO 387 MILLION OZ OR 55.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.37% (MARCH 20/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.62% to NAV (March 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.37%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.62%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.87%: NAV 13.50/TRADING 13.10//DISCOUNT 2.87.

END

And now the Gold inventory at the GLD/

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.42 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 20/2018/ Inventory rests tonight at 850.64 tonnes

*IN LAST 345 TRADING DAYS: 90.50 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 275 TRADING DAYS: A NET 65.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.671 MILLION OZ

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 20/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 319.671 million oz

end

6 Month MM GOFO 1.98/ and libor 6 month duration 2.39

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.98%

libor 2.39 FOR 6 MONTHS/

GOLD LENDING RATE: .41%

XXXXXXXX

12 Month MM GOFO

+ 2.39%

LIBOR FOR 12 MONTH DURATION: 2.633

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

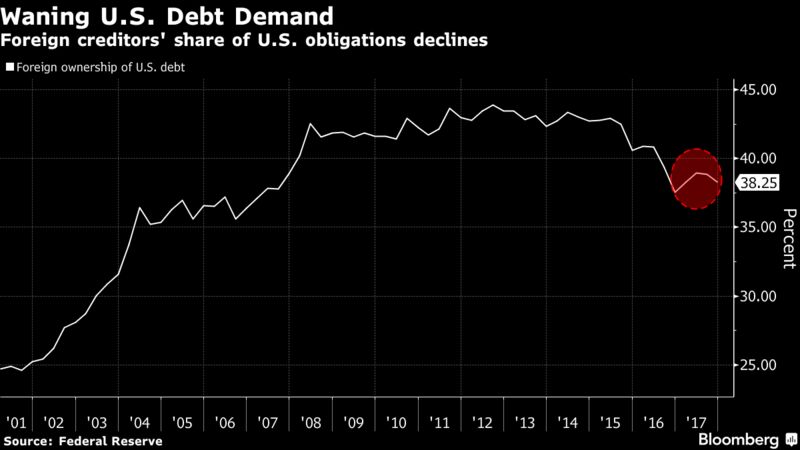

Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Rising and record U.S. debt load may cause financial stress, weaken dollar and see gold go higher

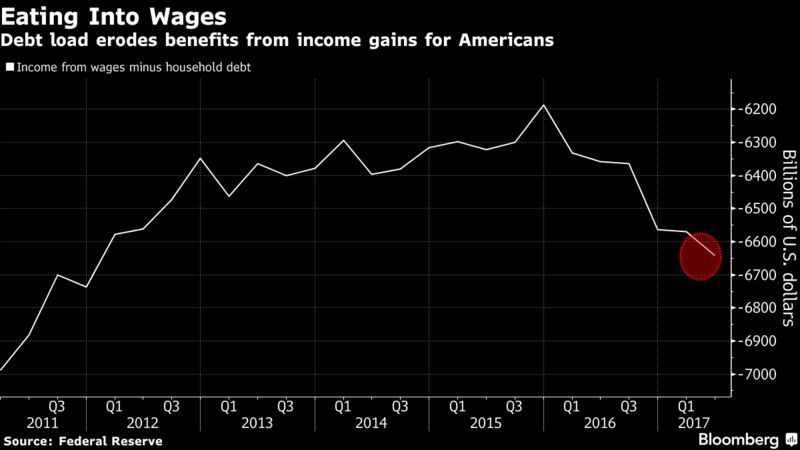

– Massive government and consumer debt eroding benefits of wage growth (see chart)

Rising U.S. interest rates, usually bad news for gold, are instead feeding signs of financial stress among debt-laden consumers and helping drive demand for the metal as a haven.

That’s the argument of Sprott Inc., a precious-metals-focused fund manager that oversees $8.8 billion in assets. The following four charts lay out the case for why gold could be poised to rise even as the Federal Reserve tightens monetary policy.

Gold futures have managed to hold on to gains this year, staying above $1,300 an ounce even as the Fed raised borrowing costs in December for a fifth time since 2015 and is expected to do so again next week.

The increases followed years of rates near zero that began in 2008. Low rates coupled with the Fed’s bond-buying spree contributed to the precious metal’s advance to a record in 2011. Higher rates typically hurt the appeal of gold because it doesn’t pay interest.

Paper Losses

The U.S. posted a $215 billion budget deficit in February, the biggest in six years, as revenue declined, Treasury Department data show. That’s boosting the government debt load, fueling forecasts for higher yields and raising the specter of paper losses for international investors who own $6.3 trillion of U.S. debt.

Slowing demand for Treasuries from overseas buyers is contributing to dollar weakness against the currency’s major peers, helping support gold prices, according to Trey Reik, a senior portfolio manager at Sprott’s U.S. unit.

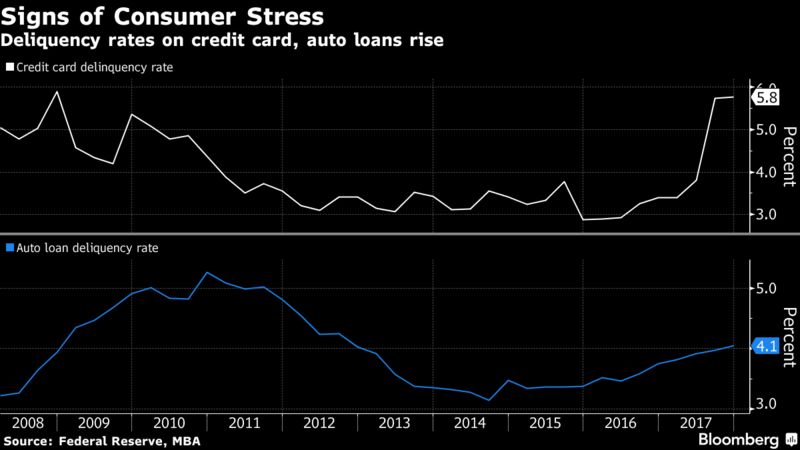

Debt-Laden Shoppers

The yield on the 10-year U.S. Treasury, which has been in decline for more than three decades, has risen over 40 basis points this year as the Fed raised rates and U.S. debt ballooned to more than $20 trillion.

That has ramifications for American households already struggling to pay down their credit cards and auto loans, dimming the outlook for consumer spending that helped fuel U.S. growth.

Those concerns have been widely overlooked by investors but will spur demand for haven assets like gold, Reik said.

“With as much debt as there is in the system, if you have a backup in rates, you’re going to see a default wave pretty quickly,” Reik said in an interview at Bloomberg’s headquarters in New York. “You’re going to have personal bankruptcies flare up. Gold really does well when financial stress starts to take hold in the system.”

In December, Fed officials signaled they may boost interest rates three times this year amid improving U.S. economic growth and a tightening labor market that could spur wage growth and push inflation toward the central bank’s target of 2 percent.

Even with a synchronized global expansion, though, consumer debt is likely to erode the benefits of rising wages, undercutting the argument from gold bears that an improving world economy will damp haven demand for gold, Reik said.

Related Content

Fed Increases Rates 0.25% – Rising Interest Rates Positive For Gold

What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

Prepare For Interest Rate Rises And Global Debt Bubble Collapse

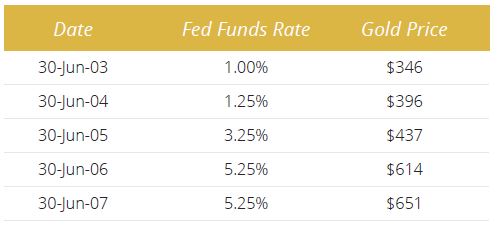

Data shows rising interest rates is positive for gold as seen in 1970s and again from 2003 to 2007. Source: New York Federal Reserve for Fed Funds Rate, LBMA.org.uk for Gold (PM fix)

Stocks Struggle After Tech Selloff; Dollar Rises (Bloomberg.com)

Gold prices inch down on stronger dollar, Fed in focus (Reuters.com)

Tech stocks weigh on Asian markets after Wall Street selloff (MarketWatch.com)

Global stocks sink in worst slide since November; eyes on Fed meeting (Reuters.com)

U.S. bans transactions with Venezuela’s digital currency (Reuters.com)

10 years after the fall of Bear Stearns, D.C. is poised to cause another financial crisis (LATimes.com)

A decade later, three lessons from the financial crisis (Reuters.com)

Central banks manipulating & suppressing gold prices (RT.com)

Iran’s break with the dollar is easier said than done (Al-Monitor.com)

Why the U.S. Treasury likes a weak dollar – Englander (Bloomberg.com)

Gold Prices (LBMA AM)

20 Mar: USD 1,312.75, GBP 935.60 & EUR 1,066.22 per ounce

19 Mar: USD 1,311.70, GBP 934.59 & EUR 1,066.41 per ounce

16 Mar: USD 1,320.05, GBP 945.42 & EUR 1,071.09 per ounce

15 Mar: USD 1,323.35, GBP 949.24 & EUR 1,070.72 per ounce

14 Mar: USD 1,324.95, GBP 949.59 & EUR 1,071.35 per ounce

13 Mar: USD 1,318.70, GBP 948.94 & EUR 1,069.60 per ounce

12 Mar: USD 1,317.25, GBP 950.66 & EUR 1,069.87 per ounce

Silver Prices (LBMA)

20 Mar: USD 16.25, GBP 11.60 & EUR 13.22 per ounce

19 Mar: USD 16.29, GBP 11.59 & EUR 13.24 per ounce

16 Mar: USD 16.48, GBP 11.79 & EUR 13.36 per ounce

15 Mar: USD 16.52, GBP 11.86 & EUR 13.37 per ounce

14 Mar: USD 16.61, GBP 11.88 & EUR 13.42 per ounce

13 Mar: USD 16.51, GBP 11.88 & EUR 13.38 per ounce

12 Mar: USD 16.46, GBP 11.88 & EUR 13.39 per ounce

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

* * *

END

Chris Powell answers Dr Keith Weiner beautifully on central bank gold suppression

(courtesy Chris Powell/GATA)

Does Weiner really know what central bankers think better than they themselves do?

Submitted by cpowell on Tue, 2018-03-20 03:21. Section: Daily Dispatches

11:05a ICT Tuesday, March 19, 2018

Dear Friend of GATA and Gold:

Thanks to Keith Weiner of Monetary Metals for at least attempting a reply to your secretary/treasurer’s recent commentary —

— disputing his assertion that central banks don’t care about gold and aren’t manipulating its price.

But in his new commentary, “Standing Ready to Lease Gold,” posted at GoldSeek here —

http://news.goldseek.com/GoldSeek/1521468000.php

— 24hGold here —

http://www.24hgold.com/english/news-gold-silver-standing-ready-to-lease-…

— and ZeroHedge here —

https://www.zerohedge.com/news/2018-03-19/standing-ready-lease-gold-repo…

— Weiner just reiterates that assertion, addresses only two of the many documents of gold price suppression cited to him, and evades the points of those.

“Central bankers do not think about gold,” Weiner writes again, just days after Hungary’s central bank announced that it is repatriating its gold reserves from London:

http://www.gata.org/node/18103

Could such repatriation have been decided without thinking? If Hungary’s central bankers don’t think about gold, wouldn’t they have just forgotten the metal in London?

As for the recent explosive increase in gold derivatives on the books of the Bank for International Settlements —

— Weiner says nothing. Could those derivatives have been undertaken without thinking too?

Weiner characterizes as “conspiracy theorists” those who complain about gold price suppression. Perhaps he will explain in his next commentary what it is when government officials meet secretly to decide and implement a course of action. Conspiracy is defined by the Federal Reserve Board’s monthly meetings in Washington to the monthly meetings of the board of the BIS in Basle, Switzerland. Weiner should try attending one of those meetings.

Weiner argues at length that the purpose of the meeting of U.S. Secretary of State Henry Kissinger and his deputy, Thomas O. Enders, at the State Department in April 1974 was not about suppressing the gold price:

http://www.gata.org/node/13310

Yet Enders was explicit: that since the Western Europeans collectively had obtained more gold than the United States, “this gives them the dominant position in world reserves and the dominant means of creating reserves. … If they have the reserve-creating instrument, by having the largest amount of gold and the ability to change its price periodically, they have a position relative to ours of considerable power.”

Plainly, control of the world’s currency and financial system was at stake for the United States. This explains the motive for gold price suppression by the United States particularly, though of course other countries might consider gold a threatening competitor to their own currencies as well.

Weiner writes that “gold is not in the system anymore.” This is rank nonsense.

All major central banks book gold as a financial asset.

The International Monetary Fund considers gold so powerful and sensitive an asset that the agency allows its member central banks to fudge their accounting so that leased gold cannot be distinguished from gold unimpaired in the vault, lest accurate accounting interfere with their surreptitious interventions in the gold and currency market:

http://www.gata.org/node/12016

The Reserve Bank of Australia noted in its annual report in 2003: “Foreign currency reserve assets and gold are held primarily to support intervention in the foreign exchange market. In investing these assets, priority is therefore given to liquidity and security, in order to ensure that the assets are always available for their intended policy purposes”:

http://www.gata.org/files/ReserveBankOfAustraliaAnnualReport2003.pdf

How could central bankers intervene in the gold market without thinking about gold?

Weiner offers a long digression about Federal Reserve Chairman Alan Greenspan’s testimony to Congress in 1998 opposing the regulation of derivatives, in which Greenspan mentioned gold leasing by central banks:

https://www.federalreserve.gov/boarddocs/testimony/1998/19980724.htm

Weiner’s digression is mere distraction from the point your secretary/treasurer sought to make: that in his testimony Greenspan acknowledged that the objective of gold leasing is price suppression, not what Weiner continues to pretend, the earning of income for central banks.

Weiner asserts that in the long run gold leasing does not suppress prices because the leased gold has to be returned. Not true. For central banks that leased gold in the 1990s sold gold heavily in the following decade. Since the gold price rose steadily in the 2000s despite the regular announcements of those sales, most likely the “sold” gold never hit the market when the announcements were made because those sales were really just the cash settlement of the gold leases from the previous decade.

Besides, since central banks are so secretive and unaccountable about their gold and their activity in the gold market, how does Weiner or anyone really know what they’re doing at any particular moment?

Weiner does not address the broader point of why the Federal Reserve should have been opposing the regulation of derivatives, which generally are thought to pose certain dangers to the world financial system. But a more than plausible answer is implied by Greenspan’s acknowledgment that central banks lease gold to keep its price down.

That is, what if central banks already were using derivatives to control not only the gold market but all major commodity and financial markets? Filings by CME Group, operator of the major U.S. futures exchanges, with the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission, as well as postings at CME Group’s own internet site show that governments and central banks indeed are secretly trading all major futures contracts:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

http://www.gata.org/node/17976

If, when Greenspan testified, governments and central banks were already controlling markets secretly with their own trading, congressional regulation of derivatives might have exposed and impaired that.

Three years after Greenspan testified against regulating derivatives, the British economist Peter Warburton put it all together in an essay titled “The Debasement of World Currency — It Is Inflation, But Not as We Know It”:

Warburton suspected that central banks were using investment banks to issue derivatives throughout the commodity futures markets to siphon away from real assets the money that might seek a hedge against inflation, money that was seeking to use real assets, not financial assets, as a store of value. Use of real assets that way would make inflation more visible in consumer price indexes.

Warburton wrote: “How much capital would it take to control the combined gold, oil, and commodity markets? Probably no more than $200 billion, using derivatives. Moreover, it is not necessary for the central banks to fight the battle themselves, although central bank gold sales and gold leasing have certainly contributed to the cause. Most of the world’s large investment banks have overtraded their capital so flagrantly that if the central banks were to lose the fight on the first front, then the stock of the investment banks would be worthless. Because their fate is intertwined with that of the central banks, investment banks are willing participants in the battle against rising gold, oil, and commodity prices.”

As the saying goes: “The futures markets are not manipulated. The futures markets are the manipulation.”

But there is little need for hypothesis when frank admissions of gold market rigging long have been available from central bankers themselves.

For example, William R. White, then the director of the monetary and economic department of the Bank for International Settlements, told a BIS conference in Basel in June 2005 that a primary purpose of international central bank cooperation is “the provision of international credits and joint efforts to influence asset prices — especially gold and foreign exchange — in circumstances where this might be thought useful”:

A president of the Netherlands Central Bank who was also president of the Bank for International Settlements, Jelle Zijlstra, wrote in his memoirs in 1992 that the gold price was suppressed at the behest of the United States:

http://www.gata.org/node/11304

So what is Weiner thinking when he writes that central bankers don’t think about gold? Does Weiner know their thoughts better than they themselves do? And exactly how does he know? He never cites any authority for his mind-reading.

A disappointing detail here: While Weiner’s disinformation lately has been welcomed at 24hGold and ZeroHedge, those internet sites have declined requests to post GATA’s replies.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3308 /shanghai bourse CLOSED UP 11.39 POINTS OR 0.35% / HANG SANG CLOSED UP 36.19 POINTS OR 0.11%

2. Nikkei closed DOWN 99.93 POINTS OR 0.47% /USA: YEN RISES TO 106.44/

3. Europe stocks OPENED IN THE GREEN /USA dollar index RISES TO 90.09/Euro FALLS TO 1.2309

3b Japan 10 year bond yield: RISES TO . +.047/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.44/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 62.76 and Brent: 66.91

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.581%/Italian 10 yr bond yield DOWN to 1.932% /SPAIN 10 YR BOND YIELD DOWN TO 1.306%

3j Greek 10 year bond yield FALLS TO : 4.193?????????????????

3k Gold at $1312.50 silver at:16.28 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 3/100 in roubles/dollar) 57.80

3m oil into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.44 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9529 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1730 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.578%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.865% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.098% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Struggle To Rebound After Tech Drubbing As Rate Hike Looms

After yesterday’s violent selloff which was sparked by a series of negative tech stories including Facebook’s escalating data scandal and a fatal accident involving an Uber self-driving car, Tuesday trading has so far been relatively calm and muted with Europe bourses paring early gains and Asian stocks trading slightly lower…

… while S&P futures were hugging the unchanged line as Nasdaq futures pointed to more tech declines.

The tech dump, which took place one day after we noted that “FANG + Apple Now Account For A Quarter Of The Nasdaq, And Some Are Getting Worried” is prompting even more fears among investors that the glory days of the tech momentum trade are over.

“There certainly are some stocks where valuations look somewhat stretched … so we’re focusing our exposure within the technology sector on the cheaper end of the market,” said Mike Bell, global market strategist at JPM Asset Management. “We’re a bit more cautious on the more expensive and some of the more popular names in the sector.”

Gains are also muted as investors braced for new Federal Reserve Chairman Jerome Powell’s first policy meeting starting later in the day and amid concerns that U.S. President Donald Trump could impose additional protectionist trade measures.

“Investors lightened their positions ahead of the Fed’s policy meeting. The markets are completely split on whether the Fed will project three rate hikes this year or four,” said Hiroaki Mino, senior strategist at Mizuho Securities.

Following the tech selloff and with a Fed rate hike imminent, bullish sentiment appears scarce. Compounding concerns was a late Monday report that the White House plans to impose $60BN in tariffs on Chinese products as part of a battle over safeguarding intellectual property. It would be the latest phase of President Donald Trump’s protectionist agenda, and threatens to increase market fears of a trade war.

Underscoring the lack of an upside case, Morgan Stanley’s chief equity strategist suggested that the highs of the year have already been seen.

Looking at regional markets, European shares eked modest gains as investors awaited Fed Chair Jay Powell’s first meeting as the Federal Reserve’s new chairman while eyeing Facebook headlines. The Stoxx 600 Index gained 0.2%, after dropping the most in two weeks on Monday. Sectors are broadly in the red, with the exception of materials which has been supported after Rio Tinto (+0.6%) announced the sale of its Hail Creek and Valeria units in a USD 1.7bln deal with Glencore.

Earlier in Asia, stocks traded lower across the board following on bearish momentum from the US. Australia’s ASX 200 (-0.4%) was weaker with miners pressured in Australia as Dalian iron ore futures extended on losses due to rising inventories, while Nikkei 225 (-0.5%) underperformed despite a weaker currency. Elsewhere, Hang Seng (+0.1%) & Shanghai Comp. (+0.3%) were subdued for a bulk of the session although the Shanghai Composite pushed back into positive territory in the latter stages of trade, after the PBoC skipped liquidity operations and amid trade war concerns with US President Trump said to be preparing a $60BN package of tariffs for China.

In FX, the USD slowly strengthened across G-10 and EMFX, while the pound was a notable mover, erasing early gains after U.K. inflation missed expectations, leaving the currency defending Monday’s advance as progress in the Brexit talks turns focus to Thursday’s BOE decision where Carney is expected to set the stage for a May rate hike. The dollar fluctuated amid lack of U.S. economic data before edging higher, while the yen whipsawed.

The Japanese yen was pushed lower after Japan’s Trade Minister said the nation is likely to get exemptions to U.S. tariffs, only to whipsaw higher later after comments from Deputy Governor Amamiya hit that the BOJ may adjust rates before the inflation target is hit (very unlikely). Separately, deputy governor Wakatabe stated that the BOJ will not hesitate to ease further if necessary, but any changes must not be premature. He also believes it is possible for monetary policy to be updated. Below are the key FX moves from Bloomberg:

- Sterling erased its advance after data showed U.K. inflation slowed more than forecast in February, but the currency stayed above 1.40; GBP/USD little changed 1.4024, holding its 0.6% advance in the past two days; it strengthened 0.1% to 87.84 pence per euro

- The Bloomberg Dollar Spot Index gains 0.2% as markets await Wednesday’s Fed policy decision; Treasuries dip with the 10-year yield rising to 2.87%

- The yen pared an earlier decline after remarks from BOJ’s Amamiya that while there was no current need to hike rates, it is something they wouldn’t rule out; USD/JPY climbs 0.3% to 106.41, having earlier touched 106.61

- The euro reversed early gains to trade 0.2% lower at 1.2307 amid light volumes

While long-term U.S. bond yields were muted, short-dated yields rose ahead of an expected rate hike from the U.S. Federal Reserve after its two-day policy meeting starting on Tuesday. The yield on 10-year Treasuries was little changed at 2.857%, 10 basis points below the four-year high of 2.957% touched a month ago. But the yield on two-year notes hit a 9 1/2-year high of 2.32% on Monday as the Fed appears set to bump up its policy interest rates to 1.50-1.75 percent from the current 1.25-1.50 percent. Still, with a Fed rate rise already fully priced in, the dollar barely gained from the prospect of a rate hike.

In geopolitical news, US and South Korea agreed to resume joint military exercises on April 1st following the postponement due to Winter Olympics, while North Korea has been notified of the schedule for the drills. In the US, Saudi Crown Prince Bin Salman and US President Trump will discuss Iran nuclear deal this Tuesday, according to a senior administration official.

In commodities, WTI and Brent remain in close proximity to yesterday’s highs which were seen after reports that the US was exploring sanctions on Venezuelan oil. Elsewhere, energy newsflow remains light with markets now awaiting the latest API report. In metals markets, gold is sat in negative territory albeit modestly so alongside the slightly firmer USD. Elsewhere, Chinese iron ore continued its decline overnight after yesterday’s slump as mounting inventories and soft domestic demand hampers prices while copper was also lacklustre amid the risk-averse tone.

No major economic data is expected. FedEx is among companies set to report earnings.

Bulletin Headline Summary From RanSquawk

- European equities sit in modest positive territory in what has been a relatively choppy session thus far

- BoJ Deputy Governor (Amamiya) suggested that rates could be adjusted before inflation reaches the 2% target

- Looking ahead, today sees a lack of tier 1 highlights

Top Overnight News from Bloomberg

- Trump may plan to impose $60b in annual tariffs against China by Friday, double what senior aides had proposed, Washington Post reports, citing people familiar

- German Mar. ZEW Expectations: 5.1 vs 13.0 est; Current Situation 90.7 vs 90.0 est.

- U.K Feb. CPI y/y: 2.7% vs 2.8% est; Core CPI 2.4% vs 2.5% est, ONS cites base effects of GBP depreciation starting to fall out of the calculation

- BOJ’s Amamiya: does not rule out the BOJ adjusting rates before inflation hits 2%; however no need to consider a rate hike now

- China made further promises to protect the intellectual property of foreigners investing in its economy, addressing a long- standing U.S. grievance as President Donald Trump plans new tariffs aimed at Beijing

- Japan will keep pressing for exemptions from U.S. tariffs and it’s highly likely that it will secure them for specific goods, Japanese Trade Minister Hiroshige Seko said at a press conference in Tokyo on Tuesday

- The EU will consider offering the U.K. “improved equivalence” for financial services after Brexit, according to the bloc’s latest negotiating guidelines, a system Britain has rejected as “wholly inadequate”

- The broad transition deal announced on Monday might be too late to stop some of the Brexit fallout: nearly one in seven EU companies with U.K. suppliers have moved some of their business out of Britain, according to the Chartered Institute of Procurement & Supply. Ministers of the bloc are set to sign off to EU Summit conclusions, post-Brexit relationship negotiating guidelines later Tuesday

- Facebook Inc. has failed to contain the fallout from the Cambridge Analytica revelations as the company’s efforts to get ahead of the media firestorm backfired

- Norwegian krone pares Monday’s drop after Justice Minister Sylvi Listhaug resigned to avert a government crisis ahead of a no-confidence vote in parliament

Market Snapshot

- S&P 500 futures up 0.06% to 2,724.50

- STOXX Europe 600 up 0.2% to 374.44

- MXAP down 0.2% to 176.54

- MXAPJ up 0.08% to 583.57

- Nikkei down 0.5% to 21,380.97

- Topix down 0.2% to 1,716.29

- Hang Seng Index up 0.1% to 31,549.93

- Shanghai Composite up 0.4% to 3,290.64

- Sensex up 0.1% to 32,958.29

- Australia S&P/ASX 200 down 0.4% to 5,936.38

- Kospi up 0.4% to 2,485.52

- German 10Y yield rose 1.2 bps to 0.581%

- Euro up 0.02% to $1.2338

- Brent Futures up 0.8% to $66.55/bbl

- Italian 10Y yield fell 1.8 bps to 1.708%

- Spanish 10Y yield fell 1.5 bps to 1.326%

- Brent Futures up 0.8% to $66.55/bbl

- Gold spot down 0.2% to $1,314.31

- U.S. Dollar Index up 0.2% to 89.92

Asian stocks traded lower across the board amid a spill-over effect from Wall St where all majors saw firm losses heading into the week’s key risk events and amid a sell-off in tech led by Facebook on reports of data breaches. ASX 200 (-0.4%) was weaker with miners pressured in Australia as Dalian iron ore futures extended on losses due to rising inventories, while Nikkei 225 (-0.5%) underperformed despite a weaker currency. Elsewhere, Hang Seng (+0.1%) & Shanghai Comp. (+0.3%) were subdued for a bulk of the session (Shanghai Comp. ebbed back into positive territory in the latter stages of trade) after the PBoC skipped liquidity operations and amid trade war concerns with US President Trump said to be preparing a USD 60bln package of tariffs for China. Finally, 10yr JGBs were lacklustre alongside subdued trade in T-note futures during Asia hours, and with price action also restricted amid an enhanced liquidity auction for long to super-long bonds which saw a lower b/c then prior.

Top Asian News

- U.S. Is Said to Plan Heavy China Tariff Hit as Soon as This Week

- China Pledges Action on Tech Transfer as Trump Plans Tariff Hit

European stocks have seen a choppy session thus far (Eurostoxx 50 +0.2%) following a softer US and Asia-Pac session. Sectors are broadly in the red, with the exception of materials which has been supported after Rio Tinto (+0.6%) announced the sale of its Hail Creek and Valeria units in a USD 1.7bln deal with Glencore. The media-sector initially outperformed at the open after the world’s third-largest advertising group Publicis (-0.5%) reported its latest strategy action, before Co. shares were dragged lower as markets continued to digest the update. Elsewhere, banks are showing mild gains across the region lifting financials, ahead of tomorrow’s widely expected Fed rate hike.

Top European News

- U.K. Will Be Colder Than Normal in April, Weather Co. Says

- Crisis Ends as Norway’s Listhaug Resigns Claiming ‘Witch Hunt’

- EU Offers U.K. ‘Improved Equivalence’ for Financial Services

- Glencore Buys Rio’s Stake in Hail Creek, Valeria for $1.7B Cash

In FX, the Jpy extended overnight losses amidst what seemed to be a stop-driven run in early European trade, with Usd/Jpy up through 106.50 and its 20 DMA (106.50-55) to circa 106.60 at one stage, while Eur/Jpy spiked to around 131.70 as the single currency retains a bid in its own right on hawkish ECB source reports. However, recent comments from one of the new BoJ Deputy Governor’s (Amamiya) suggesting that rates could be adjusted before inflation reaches the 2% target has prompted some Jpy demand/short covering. Meanwhile, Eur/Usd has rallied further above 1.2300, reaching 1.2355 at best and eyeing offers at 1.2360 next, while bids are seen in the 1.2330-20 area, but in terms of the G20 arena overall, Sterling remains the top performer after yesterday’s UK-EU Brexit transition deal and despite weaker than expected UK inflation data almost across the board that only sparked a knee-jerk Pound sell-off. Cable is back to mid-range between 1.4067-20 parameters and Eur/Gbp still sub-0.8800 as attention switches to the latest labour/wage update on Wednesday and then the BoE on Thursday. At the opposite end of the spectrum the Aud and Nzd remain laggards with the former not helped by very neutral, still in wait and see mode RBA minutes or a further dump in iron ore prices and around 0.7700 vs the Usd, while the Kiwi is just keeping its head above 0.7200 vs the Greenback awaiting the RBNZ. Conversely, Usd/Cad is attempting to retrace a bit further below 1.3100 on better NAFTA vibes.

In commodities, WTI and Brent crude futures remain in close proximity to yesterday’s highs which were seen after reports that the US was exploring sanctions on Venezuelan oil. Elsewhere, energy newsflow remains light with markets now awaiting the latest API report. In metals markets, gold is sat in negative territory albeit modestly so alongside the slightly firmer USD. Elsewhere, Chinese iron ore continued its decline overnight after yesterday’s slump as mounting inventories and soft domestic demand hampers prices while copper was also lacklustre amid the risk-averse tone.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

A bit like this nasty cold spell in the UK, markets received a fairly rude awakening yesterday as a freefalling tech sector spread collateral damage across most risk assets. Much of the blame was placed at the hands of Facebook with the stock plummeting -6.77% for the biggest one-day fall since March 2014. This followed the news that a political advertising company had retained information on 50 million of its users without consent. In addition, the Apple news concerning efforts to develop its own screens and a European Commission proposal suggesting that large digital companies operating in the EU could face a 3% tax on their gross revenues also added to the pain for the sector. Indeed a broad measure of large tech stocks including the FAANG names fell -2.90% yesterday for the biggest decline since February 8th while the Nasdaq tumbled -1.84%, also the biggest drop in over 5 weeks.

That tech tantrum seemed to ricochet across other markets with the likes of the S&P 500 (-1.42%) down for the fifth time in the last six sessions, and the Stoxx 600 (-1.07%) and DAX (-1.39%) also down prior to this in Europe. The VIX also spiked above 20 at one stage before paring back at the close to finish just above 19, albeit up 3pts from Friday. Credit indices weren’t immune either with CDX IG and iTraxx Main about 1.5bps wider while 10y Treasuries rallied nearly 5bps fromearly highs and Gold was up about +0.70% from the lows as safe havens were quick to outperform.

So some decent moves. Yesterday might well be an isolated case but it fits in with our view that we are likely to see more tantrums in markets this year, certainly relative to the incredible calm that was 2017. Indeed, it’s fairly amazing that the S&P 500 has now seen 16 days of plus or minus 1% moves in either direction since the start of February, which compares to only 10 occasions through the 13 months ending in January.

This morning in Asia it’s been more of the same with bourses broadly lower across the board, although moves are slightly more modest, with the Nikkei (-0.66%), Hang Seng (-0.49%), ASX 200 (-0.39%) and Kospi (-0.02%) all down as we type. Speaking at the conclusion of the NPC, China’s Premier Li noted that China “will further reduce the overall tax level for imported goods”, particularly on consumer products and will pursue a further opening up in sectors such as pensions, financial services and manufacturing. Li addressed the trade war debate by saying that “there’s no winner in a trade war, and war is going against the rules of trade”.

In other news, away from markets there was better news to come from the latest Brexit developments with the UK and EU agreeing to the terms around a 21- month transition period. This will kick in at the Brexit date of 30th March 2019, or 376 days for those counting down the days. The biggest news to come from yesterday’s announcement though was that in reaching the transition the UK also agreed to the principle of the EU’s backstop solution for Northern Ireland post Brexit. As DB’s Oliver Harvey noted yesterday, this is a bigger surprise, and while details have yet to be agreed, enhances the credibility of yesterday’s deal.

This implied that the UK has backed down from PM May’s initial stance. David Davis confirmed in the press conference that the UK’s preferred solution to the Northern Ireland border remains a close enough future UK/EU relationship that no hard border is needed, or technological solutions. However, that doesn’t take away from the fact that the agreement is a positive and unless there is a huge walk back, we should get official signoff at this week’s EU Council on Thursday and Friday, where the EU will also formally release guidelines for negotiations on the future economic relationship. Sterling rallied as much as +1.26% at one stage to close in on $1.41, before settling down to close at $1.402 and the highest since mid-Feb. The stronger Pound did weigh on the FTSE 100 (-1.69%) however which all of a sudden is at the lowest since December 2016.

The Euro was also kept busy yesterday by headlines suggesting that ECB policymakers have begun shifting the debate towards the steepness of the rate path with even the most dovish members accepting that QE should end this year. Specifically, it was a Reuters story which caused a few heads to turn. The story also suggested that policy makers were comfortable with market pricing, including for a rate hike by mid-2019, but that no big decision was likely to be made at the April meeting and instead only small changes to the statement is expected for now. Confirmation of the market pricing isn’t a huge surprise but – if the story has some legs to it – the prospect of ECB officials already moving to debate around rate hikes is fairly significant. The story helped 10y Bund yields actually rise nearly 4bps and back above 0.60% at one stage before the broad flight to safety across markets put the brakes on that move and saw Euro bond markets close more or less unchanged by the end of play.

Staying with the ECB, one of the bank’s policy makers, Yves Mersch, noted yesterday that inflation has recently risen “more significantly than foreseen in October” and that “given the improving inflation outlook, we can gradually reduce our net purchases while maintaining a sufficiently loose monetary policy” He also added that “the trend in wages and underlying inflation seem to have turned a corner”. It’s worth noting that Mersch is considered one of the more

hawkish ECB officials.

Across the pond, it won’t come as a great surprise to hear that the White House wasn’t kept fully out of the headlines yesterday. Indeed, news that President Trump could be preparing to fire Special Counsel Robert Mueller quickly spread across the wires although a White House spokesman announced last night that the President is just “frustrated by the ongoing investigation”, rather than preparing to dismiss Mueller. Away from this there was an Axios story suggesting that Trump wasn’t done with just the aluminium and steel tariffs, and his administration was in fact tentatively planning to put tariffs on hundreds of Chinese products by the end of this month. In the late afternoon Canadian Prime Minister Justin Trudeau also told a conference that President Trump was “enthusiastic” about getting to a NAFTA deal, although the story was slightly light on specifics so the devil will really be in the details.

Over at the G20 meetings, most global finance chiefs warned against protectionism with BOJ Governor Kuroda noting “the G20 will continue to emphasize the importance of free trade” while France’s Finance Minister Le Maire reiterated that there will only be losers in a trade war and that EU members want a full exemption from US steel and aluminium tariffs. On the other side, a senior unnamed US Treasury official told Reuters that the President strongly believes in free trade, but “where the expectation is America totally subordinates its national interest for free trade, is just one we don’t accept” and that instead “we believe in free trade with reciprocal terms that leads to more balance trade relationships”. Earlier on, senior EU officials told Bloomberg that the US will grant waivers to tariffs provided the EU meet five conditions, including limiting exports of the two materials to the US and actively addressing China’s various trade distorting practices.

Finally, it was mostly second tier economic data releases yesterday but for completeness, the Euro area’s January trade surplus was below market at €19.9bn (vs. €22.5bn expected), while Italy’s January IP fell more than expected at -1.9% mom (vs. -0.6% expected).

Looking at the day ahead, the main focus will likely be the UK’s February CPI, RPI and PPI data. German PPI for February will also be released, while the March ZEW survey should also be closely watched. In the afternoon the Euro area consumer confidence reading for March is due out. Away from this President Trump is scheduled to meet with Saudi Crown Prince Mohammed bin Salman. Illinois will also hold a primary election for governor and congressional seats ahead of the midterms later in the year.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 11.39 POINTS OR 0.35% /Hang Sang CLOSED UP 36.17 POINTS OR 0.11% / The Nikkei closed DOWN 99.93 POINTS OR 0.47%/Australia’s all ordinaires CLOSED DOWN 0.39%/Chinese yuan (ONSHORE) closed UP at 6.3308/Oil UP to 62.76 dollars per barrel for WTI and 66.91 for Brent. Stocks in Europe OPENED GREEN EXCEPT SPAIN . ONSHORE YUAN CLOSED UP AT 6.3308 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3266 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY & MARKETS/BUT NEW TRUMP TARIFFS INITIATED/WEAKER GLOBAL MARKETS )

3 a NORTH KOREA/USA

/NORTH KOREA/USA

3 b JAPAN AFFAIRS

END

c) REPORT ON CHINA

Trump is set to unleash a huge $60 billion China tariffs on Friday as he tries to tackle their “theft” of intellectual property and other Chinese transgressions

(courtesy zerohedge)

Trump Set To Unleash $60bn China Tariffs On Friday

Having rejected a plan for imposing $30 billion in tariffs on Chinese imports last week, saying they weren’t big enough; President Trump is reportedly planning to unveil by Friday, a package of $60 billion in annual tariffs against China

.

Trump is following through on a long-time threat that he says will punish China for intellectual property infringement and create more American jobs, and, as The Washington Post reports, the timing of the tariff package, which Trump plans to unveil by Friday, was confirmed by four senior administration officials.

The package could be applied to more than 100 products, which Trump argues were developed by using trade secrets the Chinese stole from U.S. companies or forced them to hand over in exchange for market access.

WaPo also notes that many of the financial ministers at the G-20 meeting have also alleged that China should make changes to its trade policies, but so far most have tried to cajole Beijing multilaterally, a strategy that Trump has said doesn’t work.

Trump this month announced 25 percent tariffs on imported steel and 10 percent for aluminum and they will also take effect Friday.

As Bloomberg reminds us, Canada and Mexico are already excluded from the levies, and the Trump administration has left the door open for Australia and possibly other allies to win a similar concession if they can show they are trading fairly and are national-security partners. Planned retaliation from the European Union to China has triggered concerns over a global trade war.

And as we warned previously, the recently announced global steel and aluminum tariffs (with various exemptions) by the Trump administration were just a (Section 232) preview of the main event: Trump’s imminent trade war with China, which as Credit Suisse previews, will be unveiled any moment in the form of tariffs and restrictions on trade with China, reportedly in retaliation for Chinese IP violations.

First, a reminder on the all-important Section 301:

- What is Section 301? Section 301 of the 1974 Trade Act allows the President to, among other things, “impose duties or other import restrictions on the products of [a] foreign country,” if the President determines that that country is violating a trade agreement or “engages in discriminatory or other acts or policies which are unjustifiable or unreasonable and which burden or restrict United States commerce.“ The U.S. relied heavily on the provision during the Reagan era (an administration in which the current USTR Robert Lighthizer served as Deputy USTR) into the early 1990s, but it has been used infrequently since the World Trade Organization was formed in 1995 and provided a forum for dispute resolution.

How will Section 301 figure in the upcoming US-Chinese trade war, and what are the key points:

- Last August, President Trump instructed his U.S. Trade Representative Robert Lighthizer to initiate a Section 301 investigation into China’s forced technology transfer policies.

- While the results of the 301 investigation are not due until August 2018, the President appears poised to act on the issue in the coming weeks.

- The President is reported to be seriously considering a package of tariffs on Chinese imports (targeting between $30BN and $60BN worth).

- Reports have stated that Administration officials have used China’s manufacturing roadmap, “Made in China 2025,” in deciding what goods to impose tariffs on. This will likely further concern Chinese leaders.

- In addition, the Administration has discussed rescinding licenses for Chinese businesses and employing other such methods to restrict Chinese investment in the United States. The President’s recent decision to block a Singaporean company’s bid to takeover a U.S. company underscores his aversion to Chinese direct investment (the company had Chinese affiliations).

- As part of the 301 action, the Administration has also reportedly discussed visa restrictions and a mandate that U.S. stock exchanges limit who can list in a U.S. market. It remains unclear whether the restrictions will go this far, but the President has, to date, been hawkish in his trade policy and there seem to be fewer and fewer moderating voices in the White House.

- The 301 investigation and potential actions resulting from it seem to complement congressional efforts to restrict Chinese investment through legislation broadening the jurisdiction of the Committee on Foreign Investment in the United States (CFIUS). We believe this legislation is on track to be signed into law in Q3 2018.

What to expect? here are some high-level thoughts from Credit Suisse:

- The Chinese will likely respond in kind, beginning a succession of tit-for-tat trade policies between the two countries.

- The United States has the option to take a multilateral approach and work with allied nations to initiate their own WTO dispute regarding Chinese technology transfer policies. However, at this point, the U.S. appears more likely to instead take unilateral retaliatory action without WTO authorization, which may run afoul of the U.S.’s WTO obligations.

- If the U.S. acts unilaterally (as it appears it will), China will likely bring a challenge before the World Trade Organization (WTO).

- The President appears committed to maintaining his “tough on China” stance. Even after losing top advisor Gary Cohn after the imposition of steel and aluminum tariffs, the President appears steadfast in his campaign against China’s trade practices and Chinese investment in the U.S, and we expect continued restrictive trade policies with respect to China.

- The President’s actions may not receive the congressional backlash that his steel and aluminum tariffs did. Many U.S. corporations are frustrated with China’s policy requiring foreign companies to turn over source code and other proprietary technology in exchange for access to the Chinese market. However, if the President takes this as far as he currently seems to be planning to, punitive measures by China coupled with the chilling of foreign investment could be a major concern for U.S. corporations.

In terms of specifics, the US trade deficit last year hit an all time high of $375BN.

The Trump administration is planning imposing tariffs on up to $60bn of Chinese goods, or roughly 13% of goods import from China ($505BN), and 2.75% of total US goods import according to Danske Bank; the tariffs will target tech products, telecoms & clothing.

A snapshot of the key aspect of the US-China trade relationship:

- the US exports soybeans, pharmaceuticals, vehicles and aircraft.

- the US imports textiles,clothing, manufactures of metals,electronics and toys.

How to trade it?

As noted last week, when discussing which industries and companies would be impacted, we said that there are some obvious sectors such as industrials (cars, planes), agriculture, and technology. Below, courtesy of Strategas, is a list of US companies which derive the largest percentage of their total revenue from China.As trade war looms, it would be prudent for investors to start thinking about potential risks to the companies they own if they have sufficient business in China.

END