GOLD: $1321.80 UP $9.65

Silver: $16.41 UP 21 CENTS

Closing access prices:

Gold $1332.50

silver: $16.58

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1323.95 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1313.45

PREMIUM FIRST FIX: $10.50

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1323.55

NY GOLD PRICE AT THE EXACT SAME TIME: $1313.35

PREMIUM SECOND FIX /NY:$10.20

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1316.35

NY PRICING AT THE EXACT SAME TIME: $1316.80

LONDON SECOND GOLD FIX 10 AM: $1321.35

NY PRICING AT THE EXACT SAME TIME. $1320.50

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:2 NOTICE(S) FOR 200 OZ.

TOTAL NOTICES SO FAR 30 FOR 3000 OZ

For silver:

MARCH

105 NOTICE(S) FILED TODAY FOR

525,000 OZ/

Total number of notices filed so far this month: 5291 for 26,455,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9068/OFFER $9,137: UP $195(morning)

Bitcoin: BID/ $8867/offer $8937: DOWN $5 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUMONGOUS SIZED 4481 contracts from 211,635 RISING TO 216,042 DESPITE YESTERDAY’S 13 CENT FALL IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 4974 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 4974 CONTRACTS. WITH THE TRANSFER OF 4974 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4974 CONTRACTS TRANSLATES INTO 24.87 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

35,971 CONTRACTS (FOR 15 TRADING DAYS TOTAL 35,971 CONTRACTS) OR 179.855 MILLION OZ: AVERAGE PER DAY: 2398 CONTRACTS OR 11.990 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 179.855 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.71% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 661.68 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED GAIN IN COMEX OI SILVER COMEX OF 4481 DESPITE THE 13 CENT FALL IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 4974 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 4974 EFP’S FOR THE MONTH OF MARCH WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A MONSTROUS 9455 OI CONTRACTS i.e. 4974 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 4481 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 13 CENTS AND A CLOSING PRICE OF $16.30 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.080 BILLION TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 105 NOTICE(S) FOR 525,000 OZ OF SILVER

In gold, the open interest ROSE BY A STRONG SIZED 4823 CONTRACTS UP TO 545,499 DESPITE THE GOOD SIZED FALL IN PRICE YESTERDAY ( LOSS OF $5.75) HOWEVER FOR WEDNESDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN HUGE SIZED 10,181 CONTRACTS : APRIL SAW THE ISSUANCE OF 6,181 CONTRACTS, JUNE SAW THE ISSUANCE OF 4000 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 545,499. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUMONGOUS OI GAIN IN CONTRACTS: 4823 OI CONTRACTS INCREASED AT THE COMEX AND A HUGE SIZED 10,181 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 15,004 CONTRACTS OR 1,504,000 OZ =46.78 TONNES

YESTERDAY, WE HAD 12.906 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 141,634 CONTRACTS OR 14,163,400 OZ OR 440.54 TONNES (15 TRADING DAYS AND THUS AVERAGING: 9442 EFP CONTRACTS PER TRADING DAY OR 944,200 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 14 TRADING DAYS IN TONNES: 440.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 440.54/2550 x 100% TONNES = 17.37% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1743.21 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX DESPITE THE FALL IN PRICE IN GOLD TRADING YESTERDAY ($5.75 LOSS). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,181 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,181 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 15,004 contracts ON THE TWO EXCHANGES:

10,181 CONTRACTS MOVE TO LONDON AND 4823 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 46.78 TONNES).

we had: 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $9.65 : NO CHANGE IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 850.54 tonnes.

SLV/

WITH SILVER UP 21 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 319.671 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUMONGOUS 4481 contracts from 211,561 UP TO 216,042 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN PRICE OF SILVER (13 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 4974 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 4481 CONTRACTS TO THE 4974 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 9455 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 47.275 MILLION OZ!!!

RESULT: A HUMONGOUS SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FALL IN SILVER PRICING YESTERDAY (13 CENTS FALL IN PRICE) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 4974 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 9.69 POINTS OR 0.29% /Hang Sang CLOSED DOWN 135.41 POINTS OR 0.43% / The Nikkei closed HOLIDAY/Australia’s all ordinaires CLOSED UP 0.20%/Chinese yuan (ONSHORE) closed UP at 6.3295/Oil UP to 64.23 dollars per barrel for WTI and 68.09 for Brent. Stocks in Europe OPENED MIXED . ONSHORE YUAN CLOSED UP AT 6.3295 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3272 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY BUT POOR CHINESE MARKETS/BUT NEW TRUMP TARIFFS INITIATED/WEAKER GLOBAL MARKETS

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

My goodness; a German spy agency now admits that North Korea’s rockets can hit Europe

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

i)China is set to retaliate against USA tariffs but they are going to use the stick and carrot approach. They are set to allow some foreign investment into the country (the carrot). However if Trump continues with his strong 60 billion dollars worth of tariffs, then China will target the farm belt agricultural sector as well as hogs which are both huge USA exports into China

( zerohedge)

4. EUROPEAN AFFAIRS

Our good friends over at Deutsche Bank, the world’s largest derivative player is having its problems. Today they warned that the Euro strength and higher funding costs are weighing in on revenue on their securities this quarter

The credit default swaps on Deutsche bank skyrocketed…

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( zerohedge)

a must read..

( Gorka/Strategic Culture Foundation)

a must read…

( Mish Shedlock/Mishtalk)

7. OIL ISSUES

i)Oil and gasoline on a tear this morning after another surprise crude drawdown. Production is still at new record highs.

( zerohedge)

ii)A very important commentary from Irina today. China is going to initiate a larger storage fees for oil as 95 cents in total contrast to the 25 cents in the uSA. The Chinese do not want volatility which is trademark of the west. They want true markets and with the conversion into gold for their yuan, the sellers will be happy as well as the buyers.

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)As we has been outlining to you on several occasions, Russia has been hoarding gold at the fastest pace in 12 years:

( RT/GATA)

ii)The following is a must read. The only difference between Ted and myself on this issue is the ownership of that silver. It is my belief that JPMorgan is holding this huge hoard of silver on behalf of the USA government who is holding it for sovereign China. You will recall that in 2003 the USA ran out of its 2 billion oz of physical silver (Manhattan Project) and they needed a huge source of silver. The only nation on earth with a huge physical official reserves was China. China went along with the lending/suppression scheme as they pocketed gold on the cheap. China it was rumoured to have between 400 million oz to 1 billion oz stored away. It is quite conceivable that China lent some of their official silver to acquire gold.

Butler talks about the July Banking Participation Report which was part of my testimony in Washington. My testimony is on the right side of my blog and I urge you all to hear it.

( Butler/Harvey, GATA)

iii)Ronan Manly discusses why central banks hold gold and it is their words as he surveyed them

( Ronan Manly/Bullionstar/GATA)

iv)Another great commentary from Chris Powell who answers Keith Weiner

( Chris Powell/.GATA)

10. USA stories which will influence the price of gold/silver

i)USA data release this morning

Mixed bag this morning: a little bounce from last month’s fall in existing home sales but Condo sales still slump

( zerohedge)

The following is extremely important. You will recall me telling you that the huge increases in Libor and its sister Libor-OIS is playing havoc with our banks. The chief culprit to the rise in Libor is the disappearance of USA dollars especially form Europe. Trump has given tax breaks so companies can repatriate their dollars back into the USA. The problem is that banks have levered those dollars hundreds times over and when you remove those dollars the banks are left with a bagful of derivatives with nothing backing them.

this is the reason we are witnessing a huge rise in Libor and that is causing Hibor to rise (Hong Kong Interactive bank) as well Australia

( zerohedge)

iii)The Omnibus 1.3 trillion spending bill is nearing compromise but still elusive

( zerohedge)

iv)This is fascinating: the uSA has developed technology to blast drones out of the sky with lasers

( zerohedge)

( zerohedge)

vi)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:415,582 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 336,063 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUMONGOUS SIZED 4481 CONTRACTS FROM 211,561 UP TO 216,042 DESPITE OUR 13 CENT LOSS IN YESTERDAY’S TRADING). ALSO,WE WERE ALSO INFORMED THAT WE HAD 4974 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 4974. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A HUMONGOUS SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 9455 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 4481 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 4974 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 9455 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 40 contracts FALLING TO 185 contracts. We had 27 contracts filed YESTERDAY, so we LOST 13 contracts or an additional 65,000 OZ will NOT stand in this active delivery month of March BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

April GAINED 18 contracts RISING TO 435 .

The next big active delivery month for silver will be May and here the OI GAINED 3396 contracts UP to 153,924

We had 105 notice(s) filed for 525,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 21/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

493 contracts

(49300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

30 notices

3000 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (30) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (495 contracts) minus the number of notices served upon today (2 x 100 oz per contract) equals 52,300 oz, the number of ounces standing in this nonactive month of MARCH (1.6267 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (30 x 100 oz or ounces + {(495)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 52,300 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 1 CONTRACT OR AN ADDITIONAL 100 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

843,956.840 oz

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,204,968.800 oz

JPMorgan

|

| No of oz served today (contracts) |

105

CONTRACT(S

(525,000 OZ)

|

| No of oz to be served (notices) |

80 contracts

(400,000 oz)

|

| Total monthly oz silver served (contracts) | 5291 contracts

(26,455,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: 1,204,968.800 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

total deposits today: 1,204,968.800 oz

we had 1 withdrawals from the customer account;

i) Out of CNT: 843,956.840 oz

total withdrawals; 843,956.840 oz

we had 0 adjustments

total dealer silver: 59.203 million

total dealer + customer silver: 257.812 million oz

The total number of notices filed today for the March. contract month is represented by 105 contract(s) FOR 525,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5291 x 5,000 oz = 26,455,000 oz to which we add the difference between the open interest for the front month of Mar. (185) and the number of notices served upon today (105 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5291(notices served so far)x 5000 oz + OI for front month of March(185) -number of notices served upon today (105)x 5000 oz equals 26,855,000 oz of silver standing for the March contract month.

We LOST an additional 13 contracts or 65,000 additional silver oz will NOT stand for delivery at the comex BUT THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 95,411 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 69,841 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 69,841 CONTRACTS EQUATES TO 349 MILLION OZ OR 49.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.46% (MARCH 21/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.63% to NAV (March 21/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.46%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.63%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.93%: NAV 13.75/TRADING 13.35//DISCOUNT 2.93.

END

And now the Gold inventory at the GLD/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 21/2018/ Inventory rests tonight at 850.54 tonnes

*IN LAST 346 TRADING DAYS: 90.50 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 276 TRADING DAYS: A NET 65.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 21/2018: NO CHANGE IN SILVER INVENTORY

Inventory 319.671 million oz

end

6 Month MM GOFO 1.99/ and libor 6 month duration 2.41

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.99%

libor 2.41 FOR 6 MONTHS/

GOLD LENDING RATE: .42%

XXXXXXXX

12 Month MM GOFO

+ 2.41%

LIBOR FOR 12 MONTH DURATION: 2.65

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.24

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

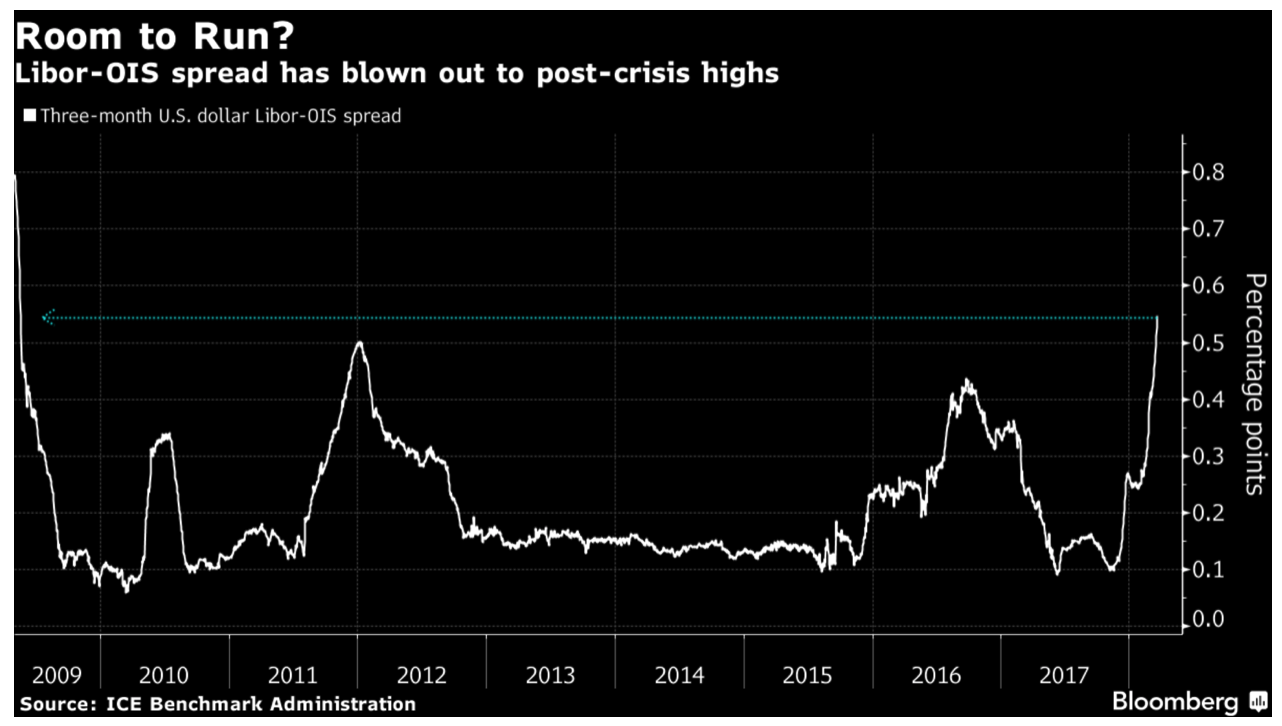

Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

March 21 2018

Key Metric LIBOR OIS Signals Major Credit Concerns

– Widening of the spread between LIBOR OIS (overnight index swap) rate raises concerns

– Spread jumped to 9 year widest spread, rising to 54.6bps, most since May 2009.

– Libor recently moved to over 2% for first time since 2008

– Wider spread usually associated with heightened credit concerns

Editor: Mark O’Byrne

Major credit concerns are back as one of the key U.S. metrics, the LIBOR-OIS spread has been climbing sharply and is now higher than levels seen during the height of the eurozone sovereign debt crisis of late 2011 and early 2012. Indeed, it has risen to levels last seen at the height of the blogal financial crisis in 2009.

The spread has doubled since January and in the last month it has widened by 15 basis points, putting it above 0.50%.

Usually this kind of divergence between the two rates is not seen without some kind of credit issue. Only now are investors beginning to ask how much wider it can go and what it says about financial markets.

LIBOR rising

The London Interbank Offered Rate (LIBOR) is the key benchmark interest rate for short-term loans around the world.It is the point of reference for the majority of leveraged loans, interest-rate swaps and, of course, some mortgages.

It is this rate which is primarily responsible for the widening of the spread.

LIBOR has been on the up since February 7th, reaching 2.25%, its highest level since 2008. Markets are concerned that this isn’t the highest we will see it go, as there may be more room for it to run.

LIBOR-OIS spread is a warning sign

At the moment much of the mainstream media and banks are passing of the increased rate as something caused by technicals. The most frequently cited explanation is the increase in T-bill issuance since the debt-ceiling was raised but additionally the recent US tax overhaul and Fed tightening is also being blamed.

However, these are the very obvious and somewhat easy explanations. As Zerohedge pointed out yesterday, there are six possible explanations for the increase in the spread, the latter three arguably the most realistic and concerning.

– an increase in short-term bond (T-bill) issuance

– rising outflow pressures on dollar deposits in the US owing to rising short-term rates

– repatriation to cope with US Tax Cuts and Jobs Act (TCJA) and new trade policies, and concerns on dollar liquidity outside the US

– risk premium for uncertainty of US monetary policy

– recently elevated credit spreads (CDS) of banks

– demand for funds in preparation for market stress

The reality, however, is that without a specific diagnosis what is causing the sharp surge wider, and thus without a predictive context of high much higher it could rise, and how it will impact the various unsecured funding linkages of the financial system, it remains anyone’s guess how much wider the Libor OIS spread can move before it leads to dire consequences for the financial system.

Usually a widening of the spread is accompanied by heightened credit concerns. There are now questions being asked as to how damaging this will be and this is bringing an increase in nervousness around risk assets.

At present the widening of the spread is not simply due to a reluctance by banks to lend to one- another, as has been the case with previous LIBOR increases. But, it is an indication of tightening financial conditions. This move will have an adverse affect on both funding and lending costs.

“What this means is that rates on more than $350 trillion of debt and derivatives contracts hitched to the U.S. benchmark are on the rise…Overleveraged entities will be in for a spot of trouble. We have a situation where half of the investment-grade bond market in the USA is BBB,” – Marketwatch quoted David Rosenberg, chief economist and strategist at Gluskin Sheff.

Consider the fact that the last time dollars cost this much for banks to borrow we didn’t know if the Eurozone was going to survive. Prior to that the global financial system was just coming back from a near-total collapse. Right now there are few signs of increasing stress in the interbank dollar lending markets, as there were a few years back but this doesn’t mean there isn’t stress elsewhere.

The rise above 50 basis points will serve as a key psychological level and it will be interesting to see how much further it strays. Despite the belief that the gap can’t widen much further this is wishful thinking. Not only could the spread widen further but general market sentiment could then sour if excess reserves of banks at the Fed start to fall.

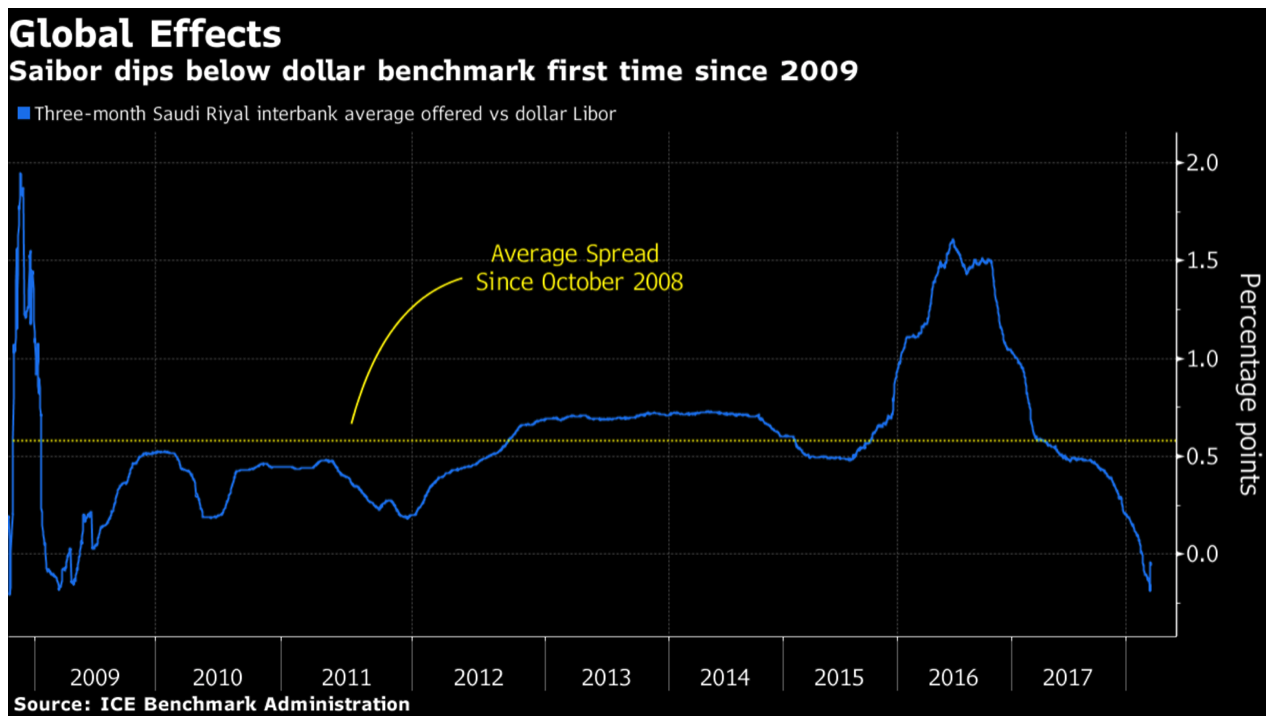

LIBOR impact felt around the world

Earlier today Bloomberg outlined how LIBOR’s increase will be felt in funding markets around the world. Attention was drawn to the impact on Saudi Arabia, Hong Kong and Australia.

Libor’s rise is complicating Saudi Arabia’s efforts to stem the risk of capital flight as the Fed is poised to continue raising rates.

Rising Libor is also fueling uncertainty surrounding Hong Kong’s peg to the U.S. dollar.

The leap in Libor is also being felt in Australia’s financing markets.

It’s made overseas borrowing more expensive for the country’s banks, which could push up domestic issuance.

Both Zerohedge and Citi’s Matt King believe “the blow out in Libor OIS not only matters, but could have very direct – and dire – consequence on equities in the coming weeks.”

What does this mean for me?

LIBOR is most likely on most people’s radars thanks to the LIBOR scandal. Today, it should be on your radar because of what it’s increase and influence on financial markets means for the global banking and financial system.

In short, no one is making too many noises about the uptick in LIBOR and the widening spread between LIBOR and OIS. However, it will be on the radar of central banks, namely the Fed.

At present, the Fed claims to be on a path to tightening monetary policy. If lending conditions between banks and credit markets become a cause for concern then the US central bank may be forced to or have an excuse to step away from their plan. This would see a return to the easy money era which has barely managed to keep economies afloat.

As we have explained previously, central bankers are pretty much all out of monetary tools for when it comes to attempting to “fix” money markets and the economy again.

Investors should take note that LIBOR OIS spread is indicating that all is not ‘Goldilocks’ like in the U.S. credit markets and there are risks that the debt laden financial system may experience difficulties again.

-END-

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

* * *

END

As we has been outlining to you on several occasions, Russia has been hoarding gold at the fastest pace in 12 years:

(courtesy RT/GATA)

Russia Is Hoarding Gold At The Fastest Pace In 12 Years

De-dollarization is accelerating…

Russia is adding gold to its reserves at the fastest pace in 12 years …and dumping US Treasuries at the fastest pace since 2011.

The Central Bank of Russia (CBR) has been increasing its holdings of gold every month since March 2015.The country is currently the sixth-largest gold owner after the United States, Germany, Italy, France and China.

According to the CBR, gold reserves spiked to $455.2 billion between March 2 and 9 hitting a historic high not seen since September 2014.

“Our international reserves increased by $2.9 billion or 0.6 percent in a single week, mainly on the strength of positive re-evaluation,” said the regulator.

And in fact 2018 has seen the fastest increase in the value of Russia’s gold reserves since 2006…

In January, RT notes that Russia surpassed China, which reportedly held 1,843 tons of the precious metal at that time. Over the last 15 years, Moscow and Beijing have been aggressively accumulating gold reserves to reduce their dependence on the US dollar.

According to World Gold Council data, last year the CBR became a world leader in stockpiling gold.

The bank has more than doubled the pace of its gold purchases, statistics showed. It has been increasing Russia’s gold reserves to meet the goal set by President Vladimir Putin to make it less vulnerable to geopolitical risks. The Russian gold cache has increased by more than 500 percent since 2000.

And while the Russian central bank is buying gold with both hands and feet, it is dumping US Treasuries at the fastest pace for a January since 2011…

Is it any wonder that Washington is so pissed off at Putin?

END

The following is a must read. The only difference between Ted and myself on this issue is the ownership of that silver. It is my belief that JPMorgan is holding this huge hoard of silver on behalf of the USA government who is holding it for sovereign China. You will recall that in 2003 the USA ran out of its 2 billion oz of physical silver (Manhattan Project) and they needed a huge source of silver. The only nation on earth with a huge physical official reserves was China. China went along with the lending/suppression scheme as they pocketed gold on the cheap. China it was rumoured to have between 400 million oz to 1 billion oz stored away. It is quite conceivable that China lent some of their official silver to acquire gold.

Butler talks about the July Banking Participation Report which was part of my testimony in Washington. My testimony is on the right side of my blog and I urge you all to hear it.

(courtesy Butler/Harvey, GATA)

Ted Butler: Bear Stearns — a different opinion

Submitted by cpowell on Tue, 2018-03-20 16:42. Section: Daily Dispatches

11:40p ICT Tuesday, March 20, 2018

Dear Friend of GATA and Gold:

Silver market analyst Ted Butler, in commentary posted today at GoldSeek’s companion site, SilverSeek, and 24hGold, explains how he discerned that JPMorganChase inherited the silver short position of Bear Stearns when the latter bank collapsed in 2008. Butler’s commentary is headlined “Bear Stearns — a Different Opinion” and it’s posted here:

http://silverseek.com/commentary/bear-stearns-%E2%80%93-different-opinio…

And here:

http://www.24hgold.com/english/news-gold-silver-bear-stearns–a-differen…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Comnittee Inc.

CPowell@GATA.org

END

Bear Stearns – A Different Opinion

|

March 20, 2018 – 9:30am

No doubt that the ten-year anniversary of the failure of the prominent investment bank, Bear Stearns, and its takeover by JPMorgan is cause for reflection. Bear Stearns was a force to be reckoned with and held a storied past on Wall Street and its fall was a seminal financial event. To that end, there have been any number of retrospective articles, most often offering the perspective of the major players involved and what the takeover meant to the acquirer, JPMorgan.

The general theme is that Bear Stearns failed because of mortgage securities gone bad and that JPMorgan, had it realized the enormous legal fees and fines it would be forced to pay as a result of the takeover, would not do so again. Like many, I was transfixed by the daily events that led up to that fateful weekend in 2008 when Bear’s failure and JPMorgan’s acquisition occurred. About the very last thing on my mind at the time was any direct connection with silver or gold. It would be months before I came to realize that JPMorgan’s takeover of Bear Stearns would be the most important development in the modern history of silver.

To this day, I have never seen any mainstream media article even mention silver and gold in connection with the takeover of Bear Stearns, and after ten years I wouldn’t expect that to change. Never mind that Bear Stearns failure coincided, to the day, with gold hitting all-time highs (over $1000) and silver hitting 30 year highs ($21). Even though it’s easy to calculate that Bear lost more than $2 billion in being short gold and silver from yearend 2007 to mid-March 2008, never is that fact mentioned in any mainstream account.

But in a turn of events quite personal, but supported by any number of verifiable facts, a completely different picture emerged to me. In fact, there were a series of events that would follow JPMorgan’s takeover of Bear Stearns in March 2008 that make it clear just how important the takeover was in the history of silver.

On May 14, 2008, barely two months after JPM’s takeover, the CFTC issued its second 16 page public letter in four years, denying there was any problem with a concentration on the short side of COMEX silver by large entities. Both public letters were in response to numerous complaints by readers received by the Commission about a silver price manipulation alleged in articles I had written. The public letters were widely trumpeted as proving there was no manipulation (mostly by those previously convinced there was no manipulation to begin with). Naturally, I was disappointed and disagreed with the agency’s findings, but at that point, I was still completely in the dark and unaware of any Bear Stearns connection.

http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/silverfuturesmarketreport0508.pdf

All that changed a few months later when I happened to check on a report regularly issued by the CFTC in the form of the monthly Bank Participation Report of August 2008. The BPR was hardly followed by anyone at that time and, truth be told, in all the years I had reviewed this report, I never learned much from it (other than knowing that banks were generally on the short side of COMEX gold and silver futures). So when I first reviewed the Bank Participation Report of August 2008 (about two weeks after it had been published), I expected a rehash of what I had always experienced before, namely, a report that added little to my understanding of silver and gold. Instead, what I discovered would change my understanding of silver and gold tremendously.

Having first reviewed the report early in the evening, what I found was so confounding that I wouldn’t sleep at all that night, made worse by not being able to bounce my findings off anyone, given the late hour. What I found was a shockingly large increase in the short positions in COMEX silver and gold futures by one or two US banks from the July Bank Participation Report. I took the shockingly large increase at face value, namely that a big US bank (or banks) had sharply increased its gold and silver short positions over the prior month. Since this was at the heart of what I had been alleging for more than 20 years to that point, I concluded that the CFTC had a good bit of explaining to do.

http://silverseek.com/commentary/smoking-gun-17159

As a result of the article and the attention it received, the CFTC announced it had opened an investigation into an alleged silver market manipulation by its Enforcement Division in September 2008, even though it had concluded just months earlier in its second public letter in four years that no manipulation existed. The new investigation would last five years before it was closed in 2013 (no, I was never contacted in connection to that investigation).

http://www.cftc.gov/PressRoom/PressReleases/pr6709-13

As luck would have it, a number of readers were concerned enough about my allegations in the “The Smoking Gun” article that they took it on themselves to write to their elected officials who, in turn, wrote to the agency seeking comment on my findings. The CFTC responded to the various congressmen and senators that I had it all wrong, in that there was no big increase from July to August in the US bank category for short positions in COMEX silver and gold. Instead, the increase in the 2008 August Bank Participation Report represented the finalization of a merger earlier in the year of an investment bank by a commercial bank. Bingo! – Another Eureka moment.

Since Bear Stearns was classified at the time as an investment bank, not a commercial bank, it’s massive short positions in COMEX silver and gold were never included in the Bank Participation Report and I had no idea that it was the big short seller (same with AIG Trading which was the largest short seller before Bear Stearns). Of course, I knew there was an unusually large concentrated short position in COMEX silver for many years, but I could only guess at who the biggest short might be. But all that changed when JPMorgan took over Bear Stearns, although I would have to wait until the Bank Participation Report of August 2008 and the subsequent letters from the CFTC to various lawmakers confirmed it was JPMorgan who was now the big silver crook and manipulator.

The revelation that JPMorgan was the biggest COMEX silver and gold short changed everything. No longer would I have to confine my allegations of manipulation to some unnamed financial institutions, now I could point to JPMorgan as the big silver and gold market crook of crooks. Not only could I now provide the name of the biggest market crook, I could do so with complete immunity from blowback from JPMorgan, arguably the most powerful financial institution in the world (although I wasn’t so sure of no blowback at the time). I certainly didn’t waste any time in pointing the finger at JPMorgan in the fall of 2008 (a year before I started this subscription service) and I have continued to point the finger at these crooks for almost ten years non-stop.

The discovery, in September 2008, that JPMorgan was now the largest short seller in COMEX gold and silver made it clear that the CFTC lied in its previous public letters denying there was no problem with big shorts in the silver market. Two months before the CFTC said there was no problem for the second time publicly (in May 2008), the biggest short went under and needed to be taken over, most likely because its big silver and gold short positions moved drastically against it. No problem indeed.

So clear was the proof that JPMorgan was now the central precious metals manipulator that I took to looking at the market through the eyes of JPM. In doing so, I believe I have come to look at silver and gold in the most realistic manner possible. Without the CFTC’s letters to lawmakers confirming both Bear Stearns’ previous role and JPMorgan’s subsequent role in silver and gold, I’m not sure if anyone, including myself, would be aware of what JPMorgan has wrought over the past ten years. I suppose I would have picked up on JPMorgan’s massive accumulation of physical silver which started in early 2011 at some point absent the great revelations of 2008, but nowhere near as quickly as I did.

My version of what really occurred in the takeover of Bear Stearns by JPMorgan includes JPMorgan being subsequently caught off guard by the big run up in silver prices into April 2011, which I contend was as a result of a physical market tightened by investment buying and not by positioning in COMEX futures contracts. With JPMorgan caught short on COMEX contracts and facing severe potential damages, it set about to do two things; one, extricate itself from the silver run up by setting off a series of price smashes starting on May 1, 2011, designed to kill off physical investment buying (mostly in silver ETFs) and two, insuring it never faced a similar predicament by buying as much physical silver as possible as a means of covering its massive COMEX paper short position. That JPMorgan accomplished both of its objectives starting in April 2011 is now a matter of public record.

Only after JPMorgan bought enough physical silver by 2012 to 2013 to cover its COMEX paper short position, did it realize it didn’t have to stop accumulating metal as a defensive measure; but that it had the means, motive and opportunity to turn what was a highly defensive original motive into a highly offensive one in terms of an unprecedented pure money making opportunity. Why else would JPMorgan, perhaps the purest example of a profit making machine, go on to buy 700 million ounces of physical silver, if not to profit? Not that it may matter much when JPMorgan switched from defense to offense, but none of this would have probably occurred had JPMorgan not taken over Bear Stearns. That’s why I feel the takeover is the most important development in the modern history of silver.

Ted Butler

March 20, 2018

END

Ronan Manly discusses why central banks hold gold and it is their words as he surveyed them

( Ronan Manly/Bullionstar/GATA

Ronan Manly: Why central banks hold gold, in their own words

Submitted by cpowell on Wed, 2018-03-21 05:09. Section: Daily Dispatches

12:08p ICT Wednesday, March 21, 2018

Dear Friend of GATA and Gold:

Bullion Star’s Ronan Manly today reports the results of his survey of central banks as to their reasons for holding gold. For the most part they acknowledge it as a special reserve financial asset, being highly liquid, available in emergencies, lacking counterparty risk, and without much correlation with other reserve assets. Interestingly, two central banks heavily connected to interventions in the gold market, the European Central Bank and the Bank for International Settlements, were among the least responsive.

Manly’s report is headlined “Why the World’s Central Banks Hold Gold — In Their Own Words” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/worlds-central-banks-hold-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Another great commentary from Chris Powell who answers Keith Weiner

( Chris Powell/.GATA)

No, gold leased from central banks doesn’t always have to be returned

Submitted by cpowell on Wed, 2018-03-21 06:08. Section: Daily Dispatches

1:17p ICT Wednesday, March 21, 2018

Dear Friend of GATA and Gold:

One could spend a lifetime trying to correct the unsupported beliefs about the gold market expressed by Keith Weiner of Monetary Metals, but your secretary/treasurer has his own failings to correct, like his own omission yesterday, in “Does Weiner Really Know What Central Bankers Think Better Than They Themselves Do?” —

— of another telling detail refuting a major assertion by Weiner in his latest essay, “Standing Ready to Lease Gold”:

http://news.goldseek.com/GoldSeek/1521468000.php

Weiner argued that gold leasing by central banks has little effect on the gold price because leased gold has to be returned eventually: “A lease allows the lessee to put the physical commodity into the market to alleviate the shortage, and get it back later when the shortage has passed.”

In response your secretary/treasurer noted yesterday that a decade of gold leasing by central banks, the 1990s, was followed by a decade of gold selling by central banks, the 2000s. If the gold sold in the latter decade was the same gold as was leased in the former decade, the leased gold was not returned.

But documents refuting Weiner were not provided.

The first is a statement issued in February 2006 by the most notorious borrower of central bank gold, Barrick Gold, which touted the generous terms of its gold leasing contracts, which it called master trading agreements.

The Barrick statement said: “In most cases, under the terms of the MTAs, the period over which we are required to deliver gold is extended annually by one year, or kept ‘evergreen,’ regardless of the intended delivery dates, unless otherwise notified by the counterparty. This means that, with each year that passes, the termination date of most MTAs is extended into the future by one year”:

https://www.barrick.com/investors/news/news-details/2006/BarrickEarnsMil…

And in PDF format:

http://gata.org/files/BarrickReleaseLeasing-02-22-2006.pdf

That is, central banks really didn’t want their gold back at any particular time at all. They wanted to keep it circulating, preventing supply shortages that might increase the gold price.

In the second document, produced in 2003, Barrick was even more explicit. In its motion filed in U.S. District Court for the Eastern District of Louisiana in New Orleans, seeking to dismiss a lawsuit accusing it of manipulating the gold market, Barrick went so far as to claim to share the sovereign immunity of central banks against suit, because in leasing gold and selling it into the market, Barrick claimed to be helping to implement central bank policy:

The court denied Barrick’s motion and the mining company soon settled the lawsuit by promising to stop hedging its future gold production. Barrick went on to reduce its hedge book of borrowed gold.

GATA has produced many documents, including admissions by central bankers themselves, confirming an international central bank policy, largely surreptitious, of controlling the price of gold to protect government currencies and bonds and to control interest rates, a policy of manipulating markets deceptively:

http://www.gata.org/taxonomy/term/21

The effectiveness of various aspects of this policy may be questioned, but its general objective is plain, and to refute Weiner it is not necessary to understand fully every detail of the policy.

For Weiner’s primary assertion is as broad as it is unsupported: that central banks don’t care about gold, even as practically every week produces new proof that they care desperately.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3295 /shanghai bourse CLOSED DOWN 9.69 POINTS OR 0.29% / HANG SANG CLOSED DOWN 135.41 POINTS OR 0.43%

2. Nikkei closed HOLIDAY /USA: YEN RISES TO 106.34/

3. Europe stocks OPENED MIXED /USA dollar index FALLS TO 90.15/Euro RISES TO 1.2277

3b Japan 10 year bond yield: FALLS TO . +.043/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.34/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.23 and Brent: 68.09

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.599%/Italian 10 yr bond yield DOWN to 1.919% /SPAIN 10 YR BOND YIELD UP TO 1.317%

3j Greek 10 year bond yield RISES TO : 4.218?????????????????

3k Gold at $1315.350 silver at:16.25 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 3/100 in roubles/dollar) 57.80

3m oil into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.34 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9535 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1706 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.599%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8997% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.1317% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Markets On Edge, Dollar Slides Ahead Of FOMC Amid Ongoing Facebook Rout

Global shares traded in the red, and the dollar slumped before a hike in US interest rates, while awaiting key guidance on how many more to expect for this year. S&P futures were little changed, while markets in Europe and Asia dropped; Japan’s Nikkei was closed for holiday.

MSCI’s all-country equity index flatlined and is now 6 percent off record highs hit at the end of January, pressured by fears of a global trade war ignited by President Trump and the possibility that the Fed could end up raising interest rates more than three times this year. Markets are also on edge because of the selloff in U.S. tech shares, which has wiped almost $50 billion off the value of Facebook this week amid uproar over the alleged misuse of users’ data. The Facebook losses have filtered through other tech shares in the United States and overseas, with shares in Twitter falling more than 10%.

The losses are likely to have hit investors hard, with Bank of America Merrill Lynch’s monthly survey showing global funds heavily positioned in tech shares just before the rout began.

“There are tensions between potential bad news and good news in the market. The bad news is the problem facing the tech sector, which has been the leading light of U.S. and Asian equity markets for over a year,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments. “The good news is we must recall why the Fed is tightening policy. It’s because of the underlying strength of the U.S. and global economy.”

Europe slumped in early trading after Asian shares dropped into the close and copper sagged again. Adding to Europe’s uncertainty was the report in La Repubblica that Italian ex-premier Silvio Berlusconi is open to possible center-right coalition pact with anti-establishment Five Star Movement which is spooking markets. The Stoxx 600 fell 0.2%, led lower by travel and leisure sector with airlines hurt by a surge in oil prices: the SXTP was down 0.7%, with Air France-KLM down 2%, easyJet down 1.7%, Lufthansa down 1.2%.

Earlier, Asia stocks followed the US example where the major indices rebounded from the recent tech sell-off. ASX 200 (+0.2%) and KOSPI (+0.1%) were marginally positive as Australia’s energy sector tracked the outperformance seen in its US counterparts, although gains were contained approaching today’s FOMC and with Japan closed for Vernal Equinox national holiday. Elsewhere, Hang Seng (+1.1%) and Shanghai Comp. (+0.4%) led the region as focus turned to earnings with the top performers in Hong Kong spurred by recent financial results. However, as China closed local market slumped, with the China’s ChiNext Index of small caps and tech stocks sliding 1.9% Wednesday afternoon, wiping out earlier 0.7% gain. PC makers, pharmaceutcial stocks led the losses. Insurers surged in morning session but tumbled before close following a bearish S&P report on a crackdown.

As previewed overnight, today’s highlight will be the FOMC decision, where there market implied odds of a rate hike are above 90%. Analysts are split over whether the Fed will raise policy tightening expectations until more price pressures are clearly evident, especially given outside risks to the economy such as a possible global trade war.

“A prudent institution would probably give more weight to the facts, at least for the moment,” Roberto Perli, a former Fed economist who is now a partner at Cornerstone Macro, wrote in a note predicting the Fed would stick with three projected rate increases for this year.

With futures markets anticipating another increase in June, Powell’s Fed could leave its rate outlook unchanged until then to see how the economy absorbs the $1.8 trillion in stimulus expected from the Trump administration tax cuts and planned spending.

“We might have significant changes in communication compared with what we’ve seen under (previous chair Janet) Yellen,” said Chris Scicluna, head of economic research at Daiwa Capital Markets. “The economic situation post tax cuts also justifies a significant shift upwards in the dot plot,” he added, referring to fears the Fed’s de facto policy forecast chart could signal four rate rises rather than three, due to the economic boost delivered by Trump’s tax reforms.

The dollar extends its slide and now stands lower on a weekly basis as traders seem less confident that the Fed will signal four rate hikes this year and may not sound as hawkish as previously thought. As Bloomberg notes, leveraged names were seen trimming their long-dollar as Powell could adopt a more balanced stance. The greenback fell against all of its peers apart from the kiwi after Tuesday’s rally when U.S. benchmark yields gained for a fourth session.

The Bloomberg Dollar Spot Index slipped 0.3%, the most in two weeks; the Fed is expected to raise rates by 25bps on Wednesday, according to median estimate in a Bloomberg survey.

Traders will also focus on whether policy makers change their wording about the near-term economic risks are “roughly” balanced, as well as on any commentary about protectionism and the long-term federal funds rate. Strategists see it as a close call whether U.S. policy makers will add a fourth dot to the rate-hike path at the Federal Open Market Committee review.

Volumes in the currency market were low in anticipation of Powell’s first post-decision press conference and as Japan was closed for a holiday. The pound was boosted by wage data, while the euro approached the $1.23 handle once more.

A summary of notable overnight FX moves from BBG:

- EUR/USD rises toward the 55-DMA at 1.2293 amid broad dollar weakness, with volumes staying low after London open while Tokyo holiday kept Asia volumes contained

- GBP/USD climbs as much as 0.6% to 1.4075 as data showed U.K. wages rising at their fastest pace since the end of 2016; EUR/GBP reverses its advance and drops 0.2% to 0.8725, the lowest since Feb. 1

- USD/JPY edges lower after testing the 21-DMA at 106.50 and with Japanese markets closed; large option strikes due to expire in New York and before the Fed decision include $3.22b at 106 and $1.25b at 107

- The Mexican peso and the Canadian dollar advance against the greenback following the Globe and Mail report that Trump administration dropped a demand that all vehicles made in Canada and Mexico for export to the U.S. contain at least 50% U.S. content

In other global news, Treasury Secretary Mnuchin said he has had very direct talks with China and that dialogue will continue, while he added that the general G20 view is to see China open its markets. China Vice Commerce Minister said the nation will actively take steps to safeguard interests of its domestic industries following US trade investigations.

South Korean President Moon suggested that a 3-way summit between US, South Korea and North Korea is possible, while there were separate reports that South Korea offered to hold a high-level meeting with North Korea on March 29th.

In the UK, Trade Secretary Fox said that a FTA is not the UK’s only approach to relationships and that the government will also look at incremental steps to improve trade. Separately, three of the nine members of the The Times’s BoE shadow monetary policy committee called for an immediate quarter-point increase. Two said they would raise rates in May and two others added that the Bank should lay the groundwork for rises this year.

Market Snapshot

- S&P 500 futures down 0.05% to 2,722.25

- STOXX Europe 600 down 0.2% to 375.47

- MSCI Asia Pacific down 0.07% to 176.60

- MSCI Asia Pacific Ex Japan down 0.2% to 583.63

- Nikkei down 0.5% to 21,380.97

- Topix down 0.2% to 1,716.29

- Hang Seng Index down 0.4% to 31,414.52

- Shanghai Composite down 0.3% to 3,280.95

- Sensex up 0.5% to 33,162.61

- Australia S&P/ASX 200 up 0.2% to 5,950.27

- Kospi down 0.02% to 2,484.97

- German 10Y yield rose 0.7 bps to 0.592%

- Euro up 0.4% to $1.2286

- Brent Futures up 0.2% to $67.58/bbl

- Italian 10Y yield fell 6.7 bps to 1.641%

- Spanish 10Y yield rose 1.0 bps to 1.318%

- Gold spot up 0.5% to $1,317.29

- U.S. Dollar Index down 0.3% to 90.14

Top Overnight News from BBG

- Trump administration has dropped demands that all vehicles made in Canada and Mexico for export to the U.S. contain at least 50% U.S. content, Globe & Mail reports, citing people familiar

- Federal offices in Washington area closed all day due to weather

- U.K. Jan. Avg. Weekly Earnings 2.8% vs 2.6% est (prev. revised to 2.7% from 2.5%); Unemployment Rate 4.3% vs 4.4% est.

- Italian ex- premier Silvio Berlusconi open to possible center-right coalition pact with anti-establishment Five Star Movement, according to newspaper La Repubblica, raising the chance of populist parties taking power

- API inventories according to people familiar w/data: Crude -2.7m, Cushing +1.6m, Gasoline -1.1m, Distillates -1.9m

- A newspaper affiliated with China’s ruling Communist Party urged “strong restrictive measures” against alleged U.S. soybean dumping, underscoring concern that trade disputes pressed by President Donald Trump could extend into other sectors

- EU President Donald Tusk sought to play down the impact of potential U.S. tariffs on steel and aluminum imports as Europe braces for more conflict with President Donald Trump

Asian stocks took impetus from Wall St. where the major indices rebounded from the recent tech sell-off. ASX 200 (+0.2%) and KOSPI (+0.1%) were marginally positive as Australia’s energy sector tracked the outperformance seen in its US counterparts, although gains were contained approaching today’s FOMC and with Japan closed for Vernal Equinox national holiday. Elsewhere, Hang Seng (+1.1%) and Shanghai Comp. (+0.4%) led the region as focus turned to earnings with the top performers in Hong Kong spurred by recent financial results.

Top Asian News

- Chinese Insurance Stocks Slide After S&P Report on Crackdown

- Hong Kong Exchange’s Big Bet on China Is Suddenly Under Threat

- Tencent Profit Beats Estimates as WeChat Games Drive Growth

- Volvo Owner’s Chinese Unit Sees Overseas Deals Fueling Growth

European equities opened with a lack of firm direction, before edging lower (Eurostoxx 50 -0.3%) ahead of the FOMC meeting. The utilities sector is boosted following upgrades of Italy’s A2A (+2.3%) and Germany’s E.ON (+1.9%) by Kepler Chevreux. The FTSE 100 is weighed on by a firmer sterling. Simultaneously, UK retailers are taking a hit amid signs of consumer spending downturn; Moss Bros (-19.8%) crashing after the issue of a profit warning. Carpetright (-0.3%) has taken a loan from a significant shareholder to cover short-term capital requirements, Kingfisher (-6.8%) amongst the laggards following the Co. reporting a fall in earnings and expressing concerns on the outlook for the retail sector, warning that the UK market is tough. On the flip side, LSE (+0.9%) is at the top of the FTSE 100 amid talks that the 21-month Brexit transition deal agreed this week could prompt Intercontinental Exchange (ICE) of the US to make another bid approach.

Top European News

- BofA’s Pullback on Margin Loans Followed Sweeping Internal Probe

- Deutsche Telekom to Buy Hellenic Telecom Stake for EU284m

- BMW’s Muted Forecast in Step With Daimler Amid E-Car Stretch

- Telenor to Sell Central, East Europe Units for $3.4 Billion

In FX markets, CAD and MXN were the biggest overnight movers with the currencies lifted on news that the US dropped the contentious auto-content proposal in NAFTA discussions last week. Elsewhere, the rest of currency markets were uneventful ahead of the upcoming Fed decision and dot-plot projections, in which EUR/USD faintly nursed losses and hovered near 1.2250 where there are large option expiries for today’s New York cut. Furthermore, GBP/USD just about held on the 1.4000 handle after the prior day’s losses which were triggered by the CPI miss, while USD/JPY was relatively unchanged amid the absence of market participants in Japan.

In commodities, crude prices held on to the gains from yesterday’s rally in which prices rose above USD 63/bbl and also briefly tested USD 64/bbl to the upside. The advances were attributed to ongoing Saudi-Iran tensions and further Venezuelan output declines, while the latest API inventory report was also supportive with headline crude stockpiles at a surprise drawdown. Elsewhere, gold found mild support as the USD pared back some of the strength heading into the FOMC decision later, while copper traded sideways and failed to benefit from the improvement in risk appetite. OPEC are said to be discussing a change of measures for success for the OPEC cut deal and that the Vienna meeting looked at a change to its inventory target.

Looking at the day ahead, the big highlight is of course the FOMC meeting outcome at 6pm GMT. Shortly after that Fed Chair Powell will also deliver his first post-meeting press conference as Chair. Away from that it’s another fairly quiet day for data with January/February employment data and February public sector net borrowing data due in the UK, while in the US the Q4 current account balance and February existing home sales data will be released.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 0.9%

- 8:30am: Current Account Balance, est. $125.0b deficit, prior $100.6b deficit

- 10am: Existing Home Sales, est. 5.4m, prior 5.38m; MoM, est. 0.37%, prior -3.2%

- 2pm: FOMC Rate Decision

DB’s Craig Nicol concludes the overnight wrap

With markets really struggling to build up any sort of momentum at the moment, today’s Fed meeting should be seen as a welcome distraction. The meeting takes on a little bit more focus as it’s of course Fed Chair Powell’s debut in the hot seat. So there will be plenty of eyes on what he has to say and what changes in style or messaging he might signal. Indeed, with a 25bp hike as good as certain today our US economists believe that Powell’s performance, along with the answers to whether or not the Committee still sees risks as “roughly balanced” and if the median dots move up, are the three key questions that investors should be looking out for.

As a reminder, our colleagues expect the Committee to sound a bit more upbeat (though not yet worried) about inflation developments, and while consumer spending indicators have softened a bit recently, their message about economic activity can remain little changed. They also expect FOMC participants to likely raise their growth forecasts and reduce unemployment forecasts. With regards to the hotly anticipated dots, the team believe that it makes sense to raise the path of rates sooner rather than later. On this basis, they expect the median forecast to move up to four rate hikes this year, from three, although caveat that it could be a close call. Perhaps of more significance for the market though, they expect the entire path of rate hikes to shift up modestly including the terminal rate forecast to 3.3% in 2020 from 3.1% in December. With regards to Powell, the team expect his message to centre on the signs of an overheating economy, and that the Fed’s current tightening action is clearly in order, which would signal that another rate hike is on the way in June.

Markets are going into today’s Fed meeting coming off the back of a difficult week and a half. Yesterday the S&P 500 (+0.15%), Nasdaq (+0.27%) and Dow (+0.47%) held their heads above water although were routinely tested with the tech sector again seemingly at the centre of things. Monday’s main culprit – Facebook – fell another -2.56% yesterday (although bounced well off the intraday lows) and is down -9.15% in the last two days. That story seemed to kick up another gear yesterday with the news that the social network company is being probed by the US Federal Trade Commission over the possible violation of a 2011 consent decree, while company officials have also supposedly agreed to brief members of the House Judiciary Committee, possibly as soon as today. The VIX actually edged down less than 1pt yesterday to 18.20. European bourses were broadly higher with the Stoxx 600 (+0.51%), DAX (+0.74%) and FTSE (+0.26%) all up, partly aided by the lower Euro (-0.75%) and energy stocks as WTI Oil rose to the highest in nearly 3 weeks (+2.27%).

Bond markets have been a bit more contained by comparison in recent days which is probably as much to do with anticipation over today’s Fed meeting. 10y Treasuries finished 4.1bps higher yesterday at 2.897% and continue to be stuck in this 2.80-2.90% range where they’ve been for most of the last month. 10y Bunds were also +1.5bps yesterday although there was a notable outperformance in the periphery despite no obvious drivers with Italy (-6.7bp), Spain (-3.1bp) and Portugal (-1.6bp) all down.