GOLD: $1350.00 UP $23.30 (COMEX TO COMEX CLOSINGS)

Silver: $16.59 UP 19 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1347.50

silver: $16.56

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1342.35

NY PRICING AT THE EXACT SAME TIME: $1341.60

LONDON SECOND GOLD FIX 10 AM: $1346.60

NY PRICING AT THE EXACT SAME TIME. $1347.70

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 31 FOR 3100 OZ

For silver:

MARCH

36 NOTICE(S) FILED TODAY FOR

180,000 OZ/

Total number of notices filed so far this month: 5307 for 26,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $86428/OFFER $8,498: DOWN $246(morning)

Bitcoin: BID/ $8599/offer $8669: DOWN $75 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUGE SIZED 2862 contracts from 214,048 RISING TO 216,910 DESPITE YESTERDAY’S TINY 1 CENT LOSS IN SILVER PRICING. WE OBVIOUSLY HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 434 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 434 CONTRACTS. WITH THE TRANSFER OF 434CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 434 CONTRACTS TRANSLATES INTO 2.17 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

39,870 CONTRACTS (FOR 17 TRADING DAYS TOTAL 39,870 CONTRACTS) OR 199.35 MILLION OZ: AVERAGE PER DAY: 2345 CONTRACTS OR 11.73 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 199.35 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 28.42% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 681.18 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A STRONG SIZED GAIN IN COMEX OI SILVER COMEX OF 2862 DESPITE THE 1 CENT FALL IN SILVER PRICE. HOWEVER, WE ALSO HAD A WEAK SIZED EFP ISSUANCE OF 434 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 434 EFP’S FOR THE MONTH OF MARCH WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A GOOD 3296 OI CONTRACTS i.e. 434 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2894 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 1 CENT AND A CLOSING PRICE OF $16.50 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.085 BILLION TO BE EXACT or 155% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 36 NOTICE(S) FOR 180,000 OZ OF SILVER

In gold, the open interest ROSE BY A HUMONGOUS SIZED 11,566 CONTRACTS UP TO 570,423 WITH THE FAIR SIZED RISE IN PRICE YESTERDAY ( GAIN OF $5.90) HOWEVER FOR FRIDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 8031 CONTRACTS : APRIL SAW THE ISSUANCE OF 7531 CONTRACTS, JUNE SAW THE ISSUANCE OF 500 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 570,423. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE AN ATMOSPHERIC OI GAIN IN CONTRACTS: 11,566 OI CONTRACTS INCREASED AT THE COMEX AND A HUGE SIZED 8031 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 19,597 CONTRACTS OR 1,959,700 OZ =60.95 TONNES

YESTERDAY, WE HAD 13,566 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 165,231 CONTRACTS OR 16,523,100 OZ OR 513.93 TONNES (17 TRADING DAYS AND THUS AVERAGING: 9719 EFP CONTRACTS PER TRADING DAY OR 971,900 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 17 TRADING DAYS IN TONNES: 513.93 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 513.93/2550 x 100% TONNES = 20.11% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1816.60 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX WITH THE RISE IN PRICE IN GOLD TRADING YESTERDAY ($5.90 GAIN). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8031 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,566 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 19,597 contracts ON THE TWO EXCHANGES:

8031 CONTRACTS MOVE TO LONDON AND 11,566 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 60.95 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $23.30 : NO CHANGE IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 850.54 tonnes.

SLV/

WITH SILVER UP 19 CENTS TODAY: THIS MAKES NO SENSE AT ALL!!!!!!!

A BIG CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.602 MILLION OZ

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A STRONG 2862 contracts from 214,048 UP TO 216,910 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY FALL IN PRICE OF SILVER (1 CENT WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 434 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2862 CONTRACTS TO THE 434 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 3296 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 16.480 MILLION OZ!!!

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FALL IN SILVER PRICING YESTERDAY (1 CENT FALL IN PRICE) . BUT WE ALSO HAD ANOTHER WEAK SIZED 434 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 110.72 POINTS OR 3.39% /Hang Sang CLOSED DOWN 761.72 POINTS OR 2.45% / The Nikkei closed DOWN 974.13/Australia’s all ordinaires CLOSED DOWN 1.89%/Chinese yuan (ONSHORE) closed UP at 6.3220/Oil DOWN to 64.53 dollars per barrel for WTI and 68.99 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AT 6.3220 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3180 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (WEAKER CURRENCY AND POOR CHINESE MARKETS/WITH NEW TRUMP TARIFFS INITIATED/WEAKER GLOBAL MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

3 c CHINA

i)China/Japan and the rest of Asia

Markets plunge in response to the trade wars

( zerohedge)

iii)China announces that they are about to launch tens of billions more in tariffs( zerohedge)

4. EUROPEAN AFFAIRS

Another hostage situation unfolding in Southern France of which ISIS is claiming responsibility. Two are dead.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

the culprit: the repatriation of all of those USA dollars held overseas back into the USA due to Trump’s favourable tax reform. This has created a massive shortage of dollars in Europe. Traders had originally levered those dollars multiple times over and now those dollars are gone and the mess is left behind

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

SOUTH AFRICA

This is not good: opposition party leader Malema blasts the Australian government for fast tracking the acceptance of fleeing white farmers. There have been many murders as blacks ascend onto white farms and this is causing the exodus of farmers to safety.

South Africa is now heading for civil war…

( zerohedge)

9. PHYSICAL MARKETS

ii)Great fundamentals for gold and silver but manipulation

( Bill Murphy GATA)

iii)Hyperinflation at its finest: Maduro knocks off 3 zeros from his currency hoping that it will help his ailing country

( reuters/GATA)

iv)The world’s largest cryptocurrency exchange by trading value is locating to Malta:

10. USA stories which will influence the price of gold/silver

i)Early morning trading

( zerohedge)

ii)US DATA FOR THIS MORNING

New home sales tumble for the 3rd straight month

( zerohedge)

iii)War spending durable goods order rebounds sharply by 3.1% month over month

iv)Afternoon tradingVIX surges and futures of VIX inverts meaning no dip buyers

( zerohedge)

( zerohedge)

vi)Trump temporarily suspends tariffs on basically all nations for steel and aluminum except China and Japan until May 1.2018

( zerohedge)

vii)Brandon Smith writes a powerful commentary on the Swamp. The operas that we are watching in real time is meant to distract us from the real global dangers that we are going to face..

a must read..

(courtesy Brandon Smith/Alt-Market.com)

viii)SWAMP STORIES

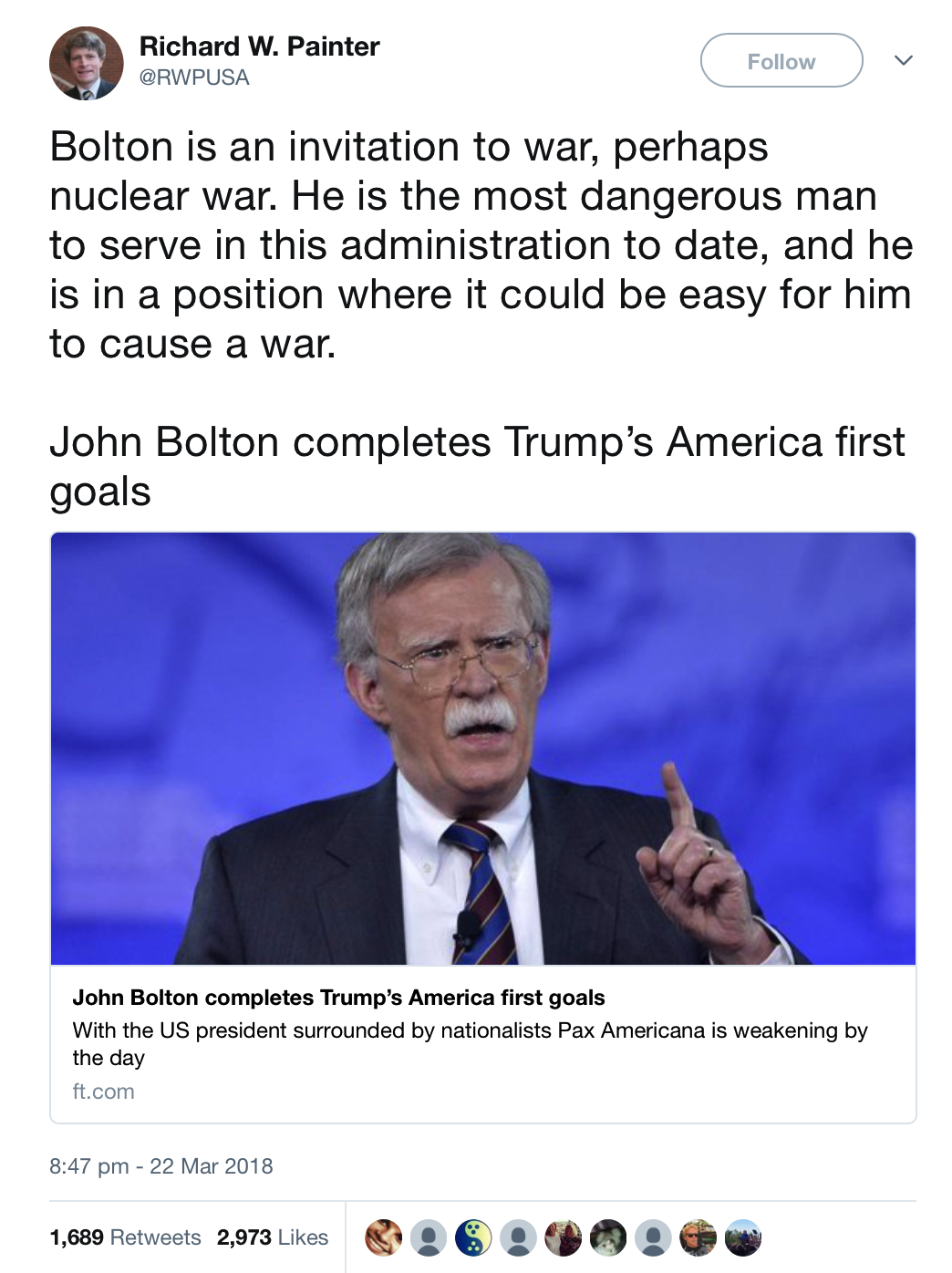

a)Uber hawk John Bolten joins uber hawk Pompeo as Gen McMaster has been fired. Bolton becomes the 3rd national security advisor for Trump following Michael Flynn and McMaster.

( zerohedge)

b)Then lawyer for Trump’s team Don McGahn is planning his exit;:

( zerohedge)

c)FBI informant speaks to the Hill and says that the Feds are asking new questions about the Clintons

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:545,609 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 443,891 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE 2862 CONTRACTS FROM 214,048 DOWN TO 216,910 DESPITE OUR 1 CENT FALL IN SILVER PRICING YESTERDAY’). ALSO,WE WERE ALSO INFORMED THAT WE HAD 434 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3465. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD SOME LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 3296 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2862 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 434 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 3296 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 16 contracts FALLING TO 110 contracts. We had 16 contracts filed YESTERDAY, so we GAINED 0 contracts or an additional 230,000 OZ will stand in this active delivery month of March

April LOST 4 contracts FALLING TO 431 .

The next big active delivery month for silver will be May and here the OI LOST 3517 contracts DOWN to 150,407

We had 36 notice(s) filed for 180,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 23/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

480 contracts

(48000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

31 notices

3100 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (31) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (480 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 51,100 oz, the number of ounces standing in this nonactive month of MARCH (1.5894 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (31 x 100 oz or ounces + {(481)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 51,100 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

106,790.44

oz

DELAWARE

SCOTIA

|

| Deposits to the Dealer Inventory |

179,950.05

oz

BRINKS

|

| Deposits to the Customer Inventory |

1,117,445.790 oz

JPM

SCOTIA

|

| No of oz served today (contracts) |

36

CONTRACT(S

(180,000 OZ)

|

| No of oz to be served (notices) |

110 contracts

(550,000 oz)

|

| Total monthly oz silver served (contracts) | 5343 contracts

(26,715,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

i) Into Brinks: 179,950.05 oz

total dealer deposits: 179,950.05 oz

we had 2 deposits into the customer account

i) Into JPMorgan: 538,269.100 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) Into Scotia: 579,176.690 oz

total deposits today: 1,117,445.790 oz

we had 2 withdrawals from the customer account;

i) Out of Delaware: 25,036.740 oz

ii) Out of CNT; 81,753.711

total withdrawals; 106,790.440 oz

we had 0 adjustments

total dealer silver: 59.383 million

total dealer + customer silver: 259.003 million oz

The total number of notices filed today for the March. contract month is represented by 36 contract(s) FOR 180,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5343 x 5,000 oz = 26,715,000 oz to which we add the difference between the open interest for the front month of Mar. (110) and the number of notices served upon today (36 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5347(notices served so far)x 5000 oz + OI for front month of March(110) -number of notices served upon today (36)x 5000 oz equals 27,085,000 oz of silver standing for the March contract month.

We GAINED 0 contracts or NIL additional silver oz will stand for delivery at the comex

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 98,965 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 87,491CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 87,491 CONTRACTS EQUATES TO 437 MILLION OZ OR 62/4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.89% (MARCH 22/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.88% to NAV (March 22/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.89%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.88%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.24%: NAV 13.84/TRADING 13.23//DISCOUNT 3.24.

END

And now the Gold inventory at the GLD/

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 23/2018/ Inventory rests tonight at 850.54 tonnes

*IN LAST 348 TRADING DAYS: 90.50 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 278 TRADING DAYS: A NET 65.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 23/2018: NO CHANGE IN SILVER INVENTORY

Inventory 318.069 million oz

end

6 Month MM GOFO 2.09/ and libor 6 month duration 2.45

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.09%

libor 2.45 FOR 6 MONTHS/

GOLD LENDING RATE: .36%

XXXXXXXX

12 Month MM GOFO

+ 2.45%

LIBOR FOR 12 MONTH DURATION: 2.69

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.21

end

Ans now for our useless COT report which is released at 3:30 pm

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 223,882 | 75,151 | 102,004 | 173,307 | 340,577 | 499,193 | 517,732 |

| Change from Prior Reporting Period | ||||||

| -10,549 | 8,668 | 19,291 | 11,703 | -9,837 | 20,445 | 18,122 |

| Traders | ||||||

| 178 | 90 | 96 | 51 | 60 | 278 | 205 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 46,306 | 27,767 | 545,499 | ||||

| -1,708 | 615 | 18,737 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, March 20, 2018 | |||||

Our large speculators

those large specs that have been long in gold pitched (transferred through EFP) 10,549 contracts

those large specs that have been short in gold added 8668 contracts to their short side

Our commercials

those commercials that have been long in gold added 11,703 contracts to their long side

those commercials that have been short in gold covered (transferred) 9837 contracts from their short side

Our small specs

those small specs who have been long in gold pitched (transferred) 1708 contracts from their long side

those small specs who have been short in gold added 615 contracts.

Conclusions: comex is a fraud

silver cot

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 63,813 | 76,329 | 36,415 | 84,080 | 87,789 | |

| -2,894 | 12,569 | 7,940 | 8,718 | -6,846 | |

| Traders | |||||

| 104 | 63 | 44 | 46 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 216,042 | Long | Short | |

| 31,734 | 15,509 | 184,308 | 200,533 | ||

| 2,184 | 2,285 | 15,948 | 13,764 | 13,663 | |

| non reportable positions | Positions as of: | 170 | |||

Our large speculators

those large specs that have been long in silver pitched (transferred through efp) 2894 contracts from their long side

those large specs that have been short in silver added 12,569 contracts to their short side???

Our commercials

those commercials that have been long in silver added a net 8718 contracts to their long side

those commercials that have been short in silver pitched (transferred through EFP) 6846 contracts

Our small specs

those small specs that have been long in silver added 2184 contracts to their long side

those small specs that have been short in silver added 2285 contracts to their short side

Conclusions: fraud

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

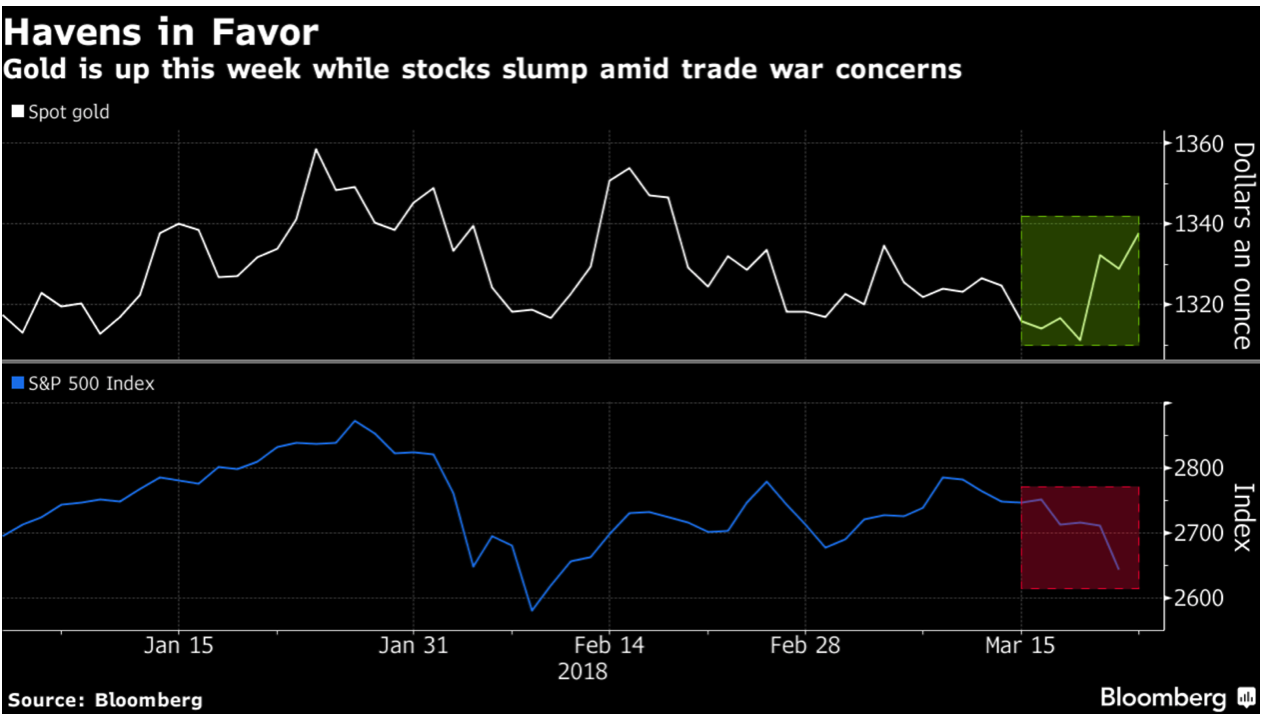

Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Market turmoil as trade war concerns deepen and Trump appoints war hawk Bolton

– Oil, gold and silver jump as ‘Russia China Hawk’ Bolton appointed

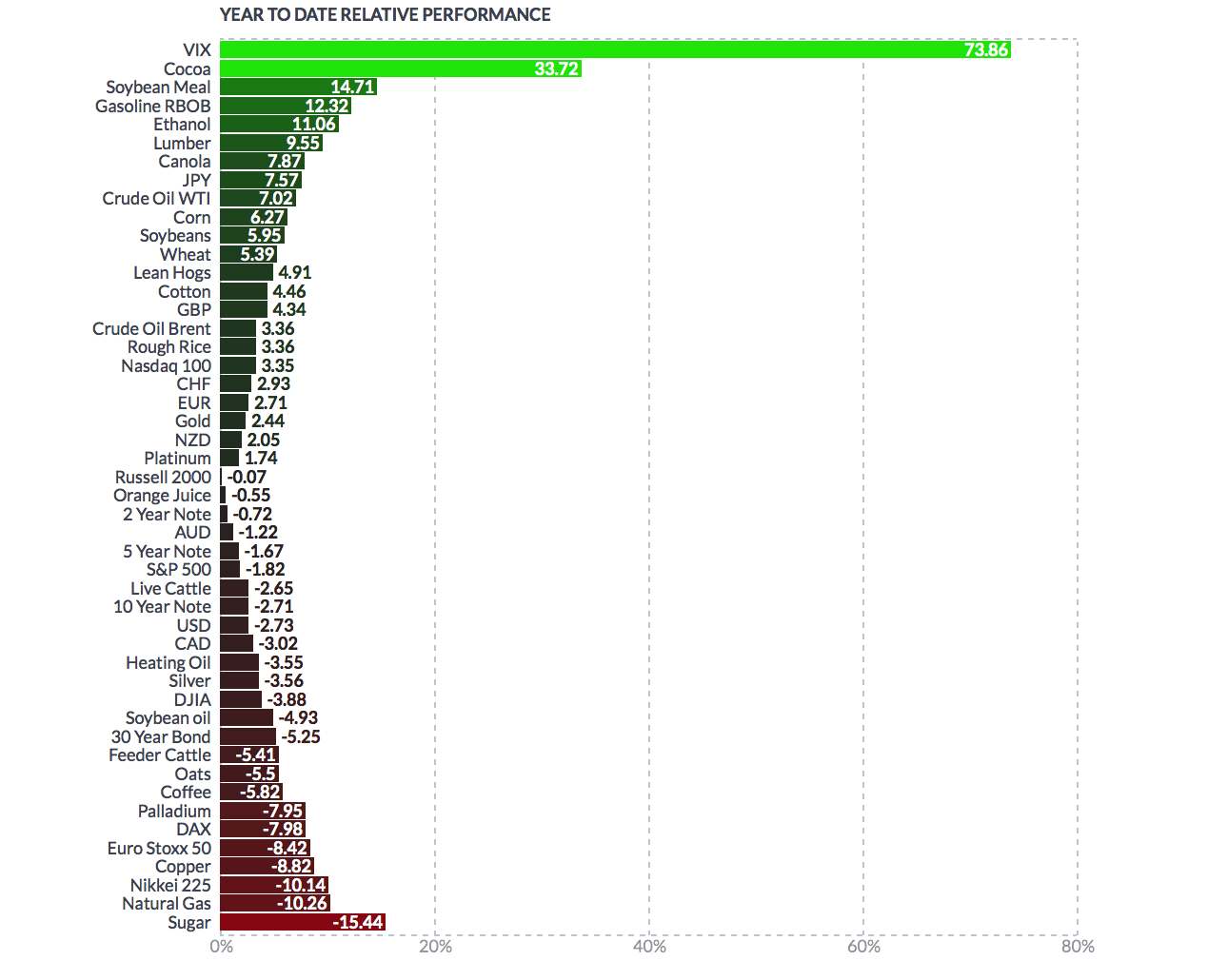

– Oil up 4%, gold up 2.2% and silver up 1.6% this week (see table)

– Stocks down sharply – Nikkei down 4.5%, S&P 4.3% & Nasdaq 5.5%

– Bolton scares jittery markets already shell-shocked by US’ tariffs against China

– Currency wars and trade wars tend to proceed actual wars

– Gold now outperforming stocks year to date (see table)

Editor: Mark O’Byrne

1 Week Relative Performance (Finviz.com)

Gold and silver have gained another 1% today as market turmoil deepens on concerns about global trade wars and actual war after the appointment of uber hawk John Bolton as national security adviser.

In response to increasing economic and geo-political risks, key stock market indices have fallen sharply this week as investors again diversify into the safe havens of gold and silver. At the time of writing the Nikkei is down by 4.5%, the S&P by 4.3% and Nasdaq 5.5%. Gold and silver have climbed by over 2.2% and 1.4% respectively this week (see table above).

Gold is now outperforming stocks year to date (see table below). Year to date, gold is 2.5% higher while stocks have now turned negative and some are down very significantly for the year. The S&P is down 2%, the DJIA 4%, EuroStoxx 8.4% and the Nikkei 10% year to date (see table below).

Gold is again acting as a good hedge – exactly when investors need a hedge. We are in an environment of increasing and heightened uncertainty – conditions in which safe havens thrive.

America is on a path to war. Currently it’s a trade war, predominantly with China, but collateral damage is already showing itself. China has responded with its own tariffs whilst EU leaders are today meeting and trade is at the top of their agenda.

The appointment of war hawk Bolton has also confirmed Trump’s instinct to be aggressive in what are currently simmering geopolitical tensions – namely with Russia, Iran, North Korea and the “Elephant in the room,” America’s hegemonic rival China.

The appointment of “chicken hawk” Bolton has delivered further blows to both political establishments and fragile markets which were already nervous following tariff announcements.

As history clearly shows trade wars, currency wars and economic and geo-political sabre-rattling frequently lead to actual wars. Markets do not tend to like such conditions and they frequently result in sharp market corrections (especially in stock markets), in bear markets in stocks and indeed in financial crashes.

Finviz.com

Finviz.com

Trade War breaks out

Yesterday President Trump instructed Trade Representative Robert Lighthizer to place tariffs of $50 billion on Chinese imports. Beijing said they would fight any such move “to the end” and announced tariffs of $3 billion.

The restrained reaction from China suggests that there are likely to be further counter-reactions on the way. As we have found with the PRC’s dealings with the Trump administration, they like to take their time.

In the early hours of this morning Beijing called on the United States to “pull back from the brink”. In a statement the Chinese commerce ministry said:

“China doesn’t hope to be in a trade war, but is not afraid of engaging in one.”

At present there is a temporary stay-of-execution for the European Union and other nations in regard to the tariffs, making the focus on China perfectly clear. The lingering threat that controls could be implemented in a matter of months has alarmed leaders. Those in the EU have pushed trade talks to the top of their agenda, for today’s meeting.

According to Reuters, ‘The European Commission has proposed that, if tariffs are imposed, the bloc should challenge them at the World Trade Organization, consider measures to prevent metal flooding into Europe and impose import duties on U.S. products to “rebalance” EU-U.S. trade.’

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Make America great again? Make it even poorer…

Trade wars are always dangerous and often pre-empt real wars. How this will play out will depend very much on what form tariffs end up taking. It’s most likely that it will be America that suffers the most, with a huge uptick in both producer and consumer prices.

The danger of this trade war is that markets really are unprepared for it. The other factor in the US this week was the Federal Reserve meeting. Markets have been prepared for its outcome for months. Whilst the tone might have been slightly more hawkish than expected, it was certainly not a major shock.

In contrast a trade war such as the one which appears to be coming is far from priced into complacent markets – especially U.S. stock markets which remain near all time highs.

Right now markets have little idea how these trade announcements will hit the US and global economy. The only thing for sure is that equity markets will likely bear much of the initial brunt. How long it will take for the Federal Reserve to respond is anyone’s guess, but it is likely to mess with with their carefully timetabled tightening of monetary policy.

Trade agreements came into their own following the Second World War, leaders saw them as a way to maintain peace between nations. The idea that if everyone had vested interests then they would be less likely to engage in damaging behaviour.

Tariffs are very often the bully’s response. They are preferred over months of renegotiation over multilateral rules. The presence of tariffs and controls significantly raise the risk of escalation of conflict as they break down the separation between commerce and national security.

This is where Trump may well be playing the long game. The appointment of war hawk Bolton suggests that the US President is well aware of where his provocations may get him. But, how will this play out with the electorate when they realise the dire economic and human consequences?

Bolton’s appointment is at odds with the electorate and Trump’s promises

Much of Trump’s election was on the back of promising to take down China and no longer engage in ‘pointless’ wars such as Iraq. The irony of the last 24 hours is that both of these announcements will end up doing damage to not only the US but also to Trump’s popularity.

Bolton’s appointment is very much at odds with the electorate. During the election campaign Trump told voters:

We’ve spent $4 trillion trying to topple various people that, frankly, if they were there and if we could have spent that $4 trillion in the United States to fix our roads, our bridges, and all of the other problems—our airports and all the other problems we have—we would have been a lot better off, I can tell you that right now. We have done a tremendous disservice not only to the Middle East—we’ve done a tremendous disservice to humanity. The people that have been killed, the people that have been wiped away—and for what?

It’s not like we had victory.

It’s a mess. The Middle East is totally destabilized, a total and complete mess. I wish we had the $4 trillion or $5 trillion. I wish it were spent right here in the United States on schools, hospitals, roads, airports, and everything else that are all falling apart!

During the same period of Trump’s campaign, the now new Security Adviser John Bolton was telling anyone who would listen that ‘the decision to overthrow Saddam was correct. I think decisions made after that decision were wrong, although I think the worst decision made after that was the 2011 decision to withdraw U.S. and coalition forces. The people who say, ‘Oh, things would have been much better if you didn’t overthrow Saddam,’ miss the point’

Bolton is extremely dangerous to the global situation. He will be a position of enormous influence. His previous declarations that there should be U.S. military action to prevent Saddam Hussein, Ayatollah Khamenei, Kim Jong Un from amassing weapons of mass destruction, are music to Trump’s ears.

As the Atlantic reminds us of a recent Bolton interview on Fox News:

“Question: How do you know that the North Korean regime is lying? Answer: Their lips are moving,” he said on Fox News shortly after news broke that Trump and Kim Jong Un had agreed to participate in direct talks on “denuclearization” by May. The North Koreans aren’t going to voluntarily abandon their goal of obtaining nuclear-tipped long-range missiles, he argued. “They want to buy time: three months, six months, 12 months—whatever it is they need to get across the finish line. What Trump did … is foreshorten that period” by organizing a meeting that can quickly expose North Korea insincerity about relinquishing its nuclear program anytime soon. (“I may leave fast or we may sit down and make the greatest deal for the world,” Trump himself recently predicted.) “Rather than having the low-level negotiations rising to the mid-level negotiations rising to the high-level negotiations, finally rising to a summit meeting—that’ll be two years from now, they’ll have deliverable nuclear weapons,” Bolton explained. “That we cannot allow.”

As Trump correctly points out, wars cost the economy huge amounts of money with little obvious upside. Yet, as we have seen in the last year he has been keen to poke the bear that had previously been left dozing – see Iran, Russia and North Korea for a start. We know that Trump likes to make impulsive decisions and is inclined to listen to the loudest voice in the room. Right now, Bolton suits this approach.

Trump thinks the electorate wants America to show its strength. He believes the country will be happily distracted from domestic policy issues by going to war. However, wars cost money, drive up inflation and ultimately pay little attention to the needs of the marketplace or the real economy.

Geo-political risks will support precious metals

At the beginning of the week, market chatter was in regard to the upcoming central bank meetings, namely in the UK and US.

These now seem a distant memory. However the underlying economic situation should not be forgotten when considering the future of gold and silver prices. Ultimately central bank announcements have very little direct impact on the price of precious metals. It is the fallout from their decisions that most impact prices.

Both gold and silver ticked up following the Fed’s decision to increase rates. Now, policy makers have to contend with nervous markets concerned about the economic damage to the US as a result of Trump’s latest decisions. This is just an extra cherry on top of what was already a dangerously piled high ice-cream Sundae of very significant financial and economic risks.

Gold has performed very well, not only since Trump’s election, but also since the start of the year. The foundations of this are the debasement of currency and theft through inflation and low to negative interest rates. Another fundamental support for precious metals is the uncertainty that comes with global leaders such as Trump and potentially Xi Jinping deciding they don’t have time for diplomacy or hard-fought deals.

Keep calm and diversify into gold

For all of Trump’s peacocking around Russia, China, Iran and North Korea there has been (in comparison) very little officially done. As Luxembourg’s Xavier Bettel reminded us:

“Even in America laws are passed by signature, not by tweet.”

That is to say Trump can go ahead declaring his delight at declaring a trade war or appointing a war monger but the laws that have to accompany his intended outcomes must be approved of by a huge number of lawmakers.

There is a very good chance that both sides of the house will not see the apparent benefits of going to (trade/currency) war with China and the rest of Asia. Or, wish to engage in violent war with North Korea, Iran or more powerful Russia and China.

However, Trump has proven to be a force unto himself. One who is clearly disinterested in a contradictory opinion, no matter how experienced.

The dismissal of key aides who had felt differently about decisions regarding the likes of Russia, China and Iran is as good an indication as any that President Trump fully intends to act upon his plan to ‘Make America Great Again’, no matter the financial or human cost.

Editors Note: There is little we as individuals or companies can do to influence or change the actions of our “great leaders.” What we do control and what we can do is protect our wealth from their actions by a few simple steps.

Reduce leverage and debt, re-balance portfolios and diversify. Prudent asset allocation and real diversification involves owning gold. The safest way to hedge these risks is to own allocated and segregated physical gold and silver coins and or bars.

Precious metals held in this way have shown themselves to reduce the risk in an investment portfolio during stock market downturns, periods of uncertainty and wars (of any kind).

We appear to be in the calm before the storm. This provides an opportunity to get investment and pension portfolios in order before the financial, economic and geo-political situation deteriorates further.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Surges Above $1350 As Dollar Hits Trade-War Lows

Yesterday’s dead-cat-bounce in the dollar – post-trade-war – is over as the dollar index tumbles to fresh lows…

Sparking a bid in precious metals with gold above $1350 at 6-week highs…

On the week, gold is leading the PMs as the dollar sinks…

As Bonds (red) and Bullion (orange) continue to outperform post-Powell…

END

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Great fundamentals for gold and silver but manipulation

(courtesy Bill Murphy GATA)

Great fundamentals, awful futures action in silver, GATA chairman tells GoldSeek Radio

Submitted by cpowell on Fri, 2018-03-23 09:24. Section: Daily Dispatches

4:21p ICT Friday, March 231, 2018

Dear Friend of GATA and Gold:

GoldSeek Radio’s Chris Waltzek this week interviewed GATA Chairman Bill Murphy about developments in the gold market and especially the silver market, where JPMorganChase dominates trading. Murphy says fundamentals for silver are strong but action in the futures market is terrible. The interview is 14 minutes long and can be heard at GoldSeek here:

http://radio.goldseek.com/nuggets/murphy.03.22.18.mp3

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Hyperinflation at its finest: Maduro knocks off 3 zeros from his currency hoping that it will help his ailing country

(courtesy reuters/GATA)

Venezuela knocks three zeros off ailing currency amid hyperinflation

Submitted by cpowell on Fri, 2018-03-23 10:20. Section: Daily Dispatches

By Corina Pons and Deisy Buitrago

Reuters

Thursday, March 22, 2018

CARACAS, Venezuela — Venezuela’s President Nicolas Maduro ordered a re-denomination of the ailing bolivar currency today by knocking three zeroes off amid hyperinflation and a crippling economic crisis.

The measure to divide the so-called bolivar fuerte — or “strong bolivar” — currency by 1,000 would take effect from June 4, the socialist leader said. It would not have any impact on the bolivar’s value.

The move illustrates the collapse of the bolivar, which has fallen 99.99 percent against the U.S. dollar on the black market since Maduro came to power in April 2013. A $100 purchase of bolivars then would now be worth just a single U.S. cent. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-economy/venezuela-knocks-th…

Crypto has just found a friendly island in the sun

Submitted by cpowell on Fri, 2018-03-23 10:27. Section: Daily Dispatches

By Yuji Nakamura

Bloomberg News

Friday, March 23, 2018

Binance, the world’s largest cryptocurrency exchange by traded value, is seeking a fresh start in the Mediterranean.

The company, founded last year in Hong Kong, is planning to open an office in Malta, said founder Zhao Changpeng in an interview from Hong Kong. Binance will soon start a “fiat-to-crypto exchange” on the European island nation and is close to securing a deal with local banks that can provide access to deposits and withdrawals, he said, without providing a timeframe.

“We are very confident we can announce a banking partnership there soon,” Zhao said. “Malta is very progressive when it comes to crypto and fintech.”

Regulators from China to the United States have been cracking down on cryptocurrency exchanges and businesses since last year, leaving many like Binance struggling to find a permanent base. The company had an office in Japan and was trying to get a license to operate but decided to remove its staff to avoid a clash with local regulators, Zhao said. Japan’s Financial Services Agency issued a warning to the venue today for operating without approval. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-03-23/the-world-s-biggest-c…

end

SWISS EXPORTS OF GOLD (KILOBARS) INTO CHINA TOTALED A WHOPPING 67 TONNES LAST MONTH.

just about all of Switzerland’s exports are landing in China either through Shanghai or Hong Kong. Of course of the other biggy is our usual good gold loving citizens over in India.

(COURTESY LAWRIE WILLIAMS)

LAWRIE WILLIAMS: Mainland China’s big gold imports in February

Switzerland, with its plethora of specialist refineries converting gold doré bullion, gold scrap and LBMA good delivery bars into the sizes and quality in demand in eastern markets, remains one of the best indicators of gold flows from Western to Eastern markets. As such its officially-published monthly gold bullion import and export figures are watched keenly by gold market analysts with exports tending to go primarily (+80%) to Asian and Middle Eastern recipients. In particular gold exports to Greater China (Mainland and Hong Kong) and India – the world’s biggest consumers – are always watched particularly closely.

The small European nation, which most years exports a quantity of gold which comes to around 60% plus of global new mined gold output, has just published its gold import and export figures for February, and that month fully 87.7% of its gold exports were destined for South and East Asia and the Middle East – see the barchart below from Nick Laird’s excellent http://www.goldchartsrus.com service :

As can be seen the biggest February recipient of these gold exports was Mainland China, taking 67.2 tonnes. With Hong Kong accounting for another 19.3 tonnes, Greater China alone accounted for around 58.3% of the Swiss gold exports. India, the world’s other major gold consumer in its own right, acquired 28.2 tonnes of Swiss gold that month. Most of the remainder went to Thailand, the United Arab Emirates, Malaysia and Singapore with 5.7 tonnes going to France, 3.2 tonnes re-exported to the UK, 2.5 tonnes to Austria and 2.1 tonnes to Italy making Europe the second largest area recipient, but hugely behind the eastern offtake.

February, of course, was the month in which fell the Chinese New Year this year which tends to boost demand there given the Chinese tradition of New Year gift giving, but it was the highest monthly level of Swiss exports to China since December 2016 when a massive 154 tonnes wended their way from Switzerland directly to the Chinese mainland. (See: China 154, Hong Kong 39. Swiss Dec gold exports show remarkable gold flows)

The latest figures though do continue to emphasise that Hong Kong is proving to be ever less of a prime conduit for Chinese gold imports with many exporters, like Switzerland, choosing to ship gold directly to the mainland and thus avoiding transit through Hong Kong altogether. There is still an element of the world’s media which tends to report Hong Kong’s own monthly- reported gold export trends to mainland China as a proxy for the latter’s overall gold demand, but this is less and less the case and such intimations should be disregarded.

23 Mar 2018

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3220 /shanghai bourse CLOSED DOWN 110.72 POINTS OR 3.39% / HANG SANG CLOSED DOWN 761.76 POINTS OR 2.45%

2. Nikkei closed DOWN 974;13 POINTS OR 4.51% /USA: YEN RISES TO 105.05/

3. Europe stocks OPENED RED /USA dollar index FALLS TO 89.67/Euro RISES TO 1.2338

3b Japan 10 year bond yield: FALLS TO . +.024/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.05/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.53 and Brent: 68.99

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.530%/Italian 10 yr bond yield DOWN to 1.898% /SPAIN 10 YR BOND YIELD DOWN TO 1.306%

3j Greek 10 year bond yield RISES TO : 4.420?????????????????

3k Gold at $1341.80 silver at:16.54 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 8/100 in roubles/dollar) 57.17

3m oil into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.05 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9474 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1686 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.530%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.830% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.082% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks “Clobbered” As Trade War Breaks Out Amid Fears Of Political Instability

“The equity markets are getting clobbered, which is not that surprising with fears of a trade war breaking out” – Paul Fage, TD Securities

Global equities are melting as they take the full brunt of a break out in trade wars after China announced it plans $3BN in tariffs on US imports in retaliation to the $50BN in US sanctions, while the latest personnel turnover in the White House (with both Dowd and McMaster out) adds to fears of rising political uncertainty.

World stocks are down 3.4% since Monday, are on course for their worst week since early February, when a spike in volatility sent markets into a tailspin.

In the US, S&P futures are trading in the red, down 9 ticks as VIX make a trip back to the 25 handle, although they have since rebounded from the session’s worst levels.

Trade Wars

Overnight, China announced it plans tariffs on USD 3bln of US imports, in which it plans 15% tariffs on US steel pipes, wine and fruits, while it also plans tariffs of 25% on US pork and pork products. Furthermore, there were also comments from Mofcom that China doesn’t want a trade war but is not afraid of one, while the ministry added it hopes US will be prudent in its decisions and pulls back from the ‘brink’. Some tangential events:

- Russia’s Ministry of Trade and Industry said they are preparing restrictions on US imports as a response to US aluminium and steel tariffs.

- EU’s Tusk states that EU leaders have called for a permanent exemption from US tariffs.

- The US launched a WTO complaint over China’s “discriminatory technology licensing requirements”.

- Source reports indicate that China intervened overnight to support its stock market after tariff announcements triggered losses.

Asian stocks saw hefty losses amid trade war fears with ASX 200 (-2.0%) led lower by miners as Chinese metals prices slumped on steel demand and tariff concerns, while Nikkei 225 (-4.5%) was the worst performer and briefly fell over 1000 points as selling pressure was magnified by a firmer JPY. Elsewhere, Hang Seng (-2.5%) and Shanghai Comp. (-3.4%) conformed to the sell-off as Chinese stocks felt the pinch from the US trade offensive, while the PBoC refrained from open market operations for a net weekly drain of CNY 320bln

European stocks tumbled at the open, down 2% to the lowest level since February 2017, although they since cut the drop in half, with the Stoxx 600 currently down about 1%; basic resources (-1.9%), auto & parts (-1.9%) and banks (1.6%) are the three worst performers; there’s one bright spot: the telecom sector is up on the day.

As Bloomberg notes, it has been a miserable week for higher-risk markets globally, as a trade war edged closer, the tech sector was roiled by Facebook Inc.’s privacy scandal and data showed European growth sputtering. Traders had already been bracing for the possibility of slowing expansion as the Federal Reserve reiterated its commitment to further interest-rate increases after Wednesday’s hike.

“The window from coming back from an all-out trade war is still open, but closing fast, and obviously leaves a lot of uncertainty over the next two to three weeks,” said Kay Van-Petersen, a Singapore-based global macro strategist with Saxo Capital Markets. It is “classic risk-off for equities today and potentially over the next few days.”

In FX, the USD/JPY slides below 105, a level not seen US election night, and has been holding in tight range, while in China the USD/CNH retraces half of yesterday’s rally; the TRY spikes considerably lower in Asian trading with officials blaming thin liquidity. BBG summarizes some of the key FX moves below:

- The euro comes off session highs in early European hours before resuming its advance; U.S. 10-year Treasuries pare gains after the yield earlier tested a near-term support around 2.80%

- GBP/USD steady around 1.41; heads for weekly gain buoyed by Brexit transition deal and BOE signal that investors can expect another rate hike; EU leaders will sign off on the Brexit negotiating guidelines and transition deal at the second day of a summit Friday, after U.K. PM Theresa May praised the deal Thursday

- Scandinavian currencies tumble amid the wider risk-off mood; Swedish krona was also weighed down by a continued dovish repricing of Riksbank and a central bank survey which showed concerns surrounding the housing market persisted

- USD/JPY breaks below 105 for the first time since November 2016 as Nikkei 225 tumbles to a 5-month low, breaking the 200-DMA; Japan’s 10-year yield falls 1.4bps to ~0.02%, lowest since November

- Australian and New Zealand dollars rose against the greenback, pares earlier losses versus the yen amid cross-related demand by Tokyo funds; Aussie also buoyed by news that U.S. will exempt Australia from tariffs

There has been some stability in core fixed income which has rallied further, although not with the same momentum as yesterday, with the 10y bund yield close to 50bps; even as peripheral EGBs continue to selloff.

Understandably, spot gold underpinned consistently, Dalian iron ore futures close -4.3% and crude futures grind lower from overnight highs.

For those who missed them, here are the key events in the turbulent overnight session, courtesy of Bloomberg:

- China is slowly hitting back after Donald Trump fired the first shots in what may be an extended trade war, with President Xi Jinping making it clear he’s going to wait before unleashing his country’s formidable arsenal in response

- China announced plans for reciprocal tariffs of $3 billion in response to Trump’s steel and aluminum tariffs, while the Commerce Ministry said it has a plan to act further on the planned levies on $50 billion worth of Chinese imports announced Thursday

- In Europe, there are signs Mario Draghi’s success in reviving the euro-area economy could, ironically, delay the European Central Bank’s exit from extraordinary stimulus

- The bloc’s broadest expansion in history is drawing workers back to the job market and spurring companies to invest to replace aging equipment, increasing the degree of slack in the economy

- Russia cut rates on Friday, as the central bank kept to its slow but steady pace of monetary easing. The one-week auction rate was lowered to 7.25 percent from 7.5 percent in a fifth consecutive cut — a move predicted by all but four of 38 economists surveyed by Bloomberg

- Japan’s key inflation gauge has finally reached half of its 2 percent goal, even as a strengthening yen and global trade battles threaten to curb that progress

US 10Y yields fell almost 8 basis points on Thursday, were set for their biggest two-week fall since September; on Friday they briefly dipped below 2.8%, before steadying above that level. In Europe, benchmark issuer Germany’s 10-year bond yield hovered close to 10-week lows struck a day earlier at around 0.52 percent and was on track for its biggest two-week drop since August, down 13 basis points.

Oil prices climbed amid worries that Bolton would pursue a hard-line stance against Iran. Safe-haven spot gold rose 1 percent to $1,341 an ounce, highest since Feb. 20. Copper and iron prices both fell, as investors bet demand for the metals would suffer in a trade war.

Economic data on Friday include durable goods orders and new home sales data

Market Snapshot

- S&P 500 futures down 0.2% to 2,637.00

- STOXX Europe 600 down 1.1% to 365.04

- German 10Y yield fell 1.0 bps to 0.519%

- MXAP down 2.6% to 172.06

- MXAPJ down 2.2% to 565.65

- Nikkei down 4.5% to 20,617.86

- Topix down 3.6% to 1,664.94

- Hang Seng Index down 2.5% to 30,309.29

- Shanghai Composite down 3.4% to 3,152.76

- Sensex down 1.2% to 32,627.04

- Australia S&P/ASX 200 down 2% to 5,820.73

- Kospi down 3.2% to 2,416.76

- Euro up 0.3% to $1.2334

- Brent Futures up 0.7% to $69.39/bbl

- Italian 10Y yield fell 4.6 bps to 1.63%

- Spanish 10Y yield fell 0.8 bps to 1.284%

- Brent Futures up 0.7% to $69.39/bbl

- Gold spot up 0.9% to $1,340.34

- U.S. Dollar Index down 0.2% to 89.65

Top Overnight News

- China said it doesn’t fear a trade war and announced plans for reciprocal tariffs on $3 billion of imports from the U.S. in the first response to President Donald Trump’s ordering of levies on Chinese metal exports

- Trump signs order to exclude the EU, Argentina, Australia, Brazil, Canada, Mexico and South Korea from steel and aluminum tariffs through May 1

- The U.S. president is replacing White House National Security Adviser H.R. McMaster with John Bolton, a former U.S. Ambassador to the United Nations famed for his hawkish views, in the latest shakeup of his administration.

- Senate passes $1.3t spending bill to fund govt for rest of fiscal year and avert a partial govt shutdown, sending the measure to Trump for his signature.

- Investors withdrew $19.9b from equity funds this week following last week’s record inflow, analysts at Bank of America Merrill Lynch write in research note citing EPFR Global data for week ending March 21

- Japan won’t retaliate on U.S. tariffs as it could lead to the collapse of the free-trade system, Japanese Trade Minister Hiroshige Seko said

- EU leaders will discuss trade on Friday after they were left in limbo on Thursday awaiting confirmation from President Trump that the bloc was indeed exempt from the new levies

- ECB interest-rate hike expectations have been retreating after a series of dovishly perceived central bank speakers and softening data, though interest to fade the move via put ladders has emerged via Euribor options

Asian stocks saw hefty losses on trade war fears after the US announced USD 50bln of tariffs on China and with the latter planning tariffs of USD 3bln in retaliation, while it was also reported that National Security Advisor McMasters was replaced by policy hawk John Bolton. The intensified trade tensions triggered a bloodbath across stock markets with ASX 200 (-2.0%) led lower by miners as Chinese metals prices slumped on steel demand and tariff concerns, while Nikkei 225 (-4.5%) was the worst performer and briefly fell over 1000 points as selling pressure was magnified by a firmer JPY. Elsewhere, Hang Seng (-2.5%) and Shanghai Comp. (-3.4%) conformed to the sell-off as Chinese stocks felt the pinch from the US trade offensive, while the PBoC refrained from open market operations for a net weekly drain of CNY 320bln. Finally, 10yr JGBs traded higher to track the gains in T-notes amid a safe-haven bid and with the BoJ present in the market under its massive bond buying program. This helped 10yr JGB prices back above 151.00 and saw the 10yr yield slip to below 0.025% which was its lowest since November.

European equities are suffering heavy losses across the board with the Eurostoxx (-1.4%) hitting its lowest point since August 2017, continuing to remain hampered by the risk-off sentiment seen in US and Asia, after US announced USD 50bln tariffs on China triggering a retaliation of USD 3.1bln on US imports. Taking a closer look at sectors, materials (-1.8%) and industrials (-1.6%) are lagging behind due to their vast exposure to the Chinese market and are immediately followed by IT (-1.9%), financials (-1.6%) and consumer discretionary (-1.3%). On the flip side, Next (+7.5%) is leading the FTSE100 after maintaining its profit guidance this morning and against the recent backdrop of the retail sector whilst GSK (+3.6%) is the outperformer in the index after it officially announced its withdrawal for its takeover of Pfizer’s health unit, following its rival Reckitt Benckiser who ended talks over the acquisition of the unit yesterday. Elsewhere, Indivior sank more than 20% at the open after the US court turned against the co. and is said to favour its competitor Alvogen. In the DAX, Deutsche Bank is down 12.7% for the week, extending losses over the widening LIBOR – OIS spread which is believed to provide a headwind for the bank.

FX markets continue to be swayed by the prospect of ongoing ‘trade wars’ which have adopted more of a bilateral dynamic over the past 24 hours with exemptions for Argentina, Australia, Brazil, Canada, Mexico, South Korea and EU. In terms of the follow through for FX markets, the DXY is softer and back below 90.00 but largely a by-product of the safe-haven bid into JPY which knocked USD/JPY (temporarily) below 105.00 after the pair breached the YTD low at 105.23 during yesterday’s trade. From a technical perspective, some analysts are pointing towards 103.64 as a key level which marks the 76.4% Fib from the 99.00-118.66 recovery seen in 2016; a view held by IFR. Elsewhere, the USD softness has provided a modest lift to EUR/USD holding onto 1.2300, however GBP/USD gave up the 1.4100 handle. For EUR/USD, barring any major macro developments and amid a light data docket for the EZ, 2.3bln in expiries between 1.2250 and 1.2300 could act as a guiding force for prices. Back to GBP and amid the fallout of yesterday’s BoE release, focus for the UK will likely be on developments in Brussels at the EU council meeting (albeit seen as somewhat of a rubber stamp process). N.b. BoE Vlieghe to speak at 1230GMT. Elsewhere, AUD has also benefited from the softer USD despite the risk environment, albeit the pair may struggle to make any meaningful progress above 0.7730-40. Interestingly, despite concerns over potential faltering demand from China (Australia’s major trading partner), some suggest AUD could benefit if China opts to use Australian goods as a substitute for US ones. Moving forward, CAD will likely come into focus later today amid domestic CPI and retail sales releases. Traders will be looking to see if today’s releases conform to the recent slew of soft data whilst NAFTA concerns linger in the background. If this materialises, USD/CAD could make a firmer reclaiming of the 1.3000 level to the upside but would still have some way to go to hit the 2018 high around 1.3125.

In commodities , WTI (+0.1%) and Brent Crude (+0.3%) are underpinned by the latest comment from Saudi Energy Minister Al-Falih stating that there is still time to go before OPEC+ supply cut oil inventories to “normal levels” adding that OPEC/Non-OPEC will still require coordination in 2019. Additionally, the latest White House replacement of National Security Adviser HR McMaster with hardliner John Bolton, ahead of a key decision on May 12th regarding whether to maintain the Iran nuclear deal, raises the prospect of sanctions against Iran’s oil sales. Something to be aware of, with driving season edging closer, refineries are stocking up on crude oil to meet the seasonal demand for the summer driving season commencing in a few weeks. Moving onto metals, Gold (+1.0%) prices hit highs last seen in early February, boosted as investors flock into the traditional safe haven following the eruption of a trade war between US and China. Furthermore, a softer dollar this week has been supporting the yellow metal. Base metals on the other hand have fallen amid escalating trade concerns. Chinese steel futures fell more than 6%, hitting their lowest level in more than eight months while Dalian iron ore also shed over 6% hitting lows last seen in June 2017

Looking at the day ahead, the most significant data comes in the US with preliminary February durable and capital goods orders data, along with February new home sales. A number of Fed speakers are also scheduled to speak including Bostic, Kashkari, Kaplan and Rosengren, as well as the BoE’s Vlieghe.

US Event Calendar

- 8:30am: Durable Goods Orders, est. 1.6%, prior -3.6%;

- Durables Ex Transportation, est. 0.5%, prior -0.3%

- Cap Goods Orders Nondef Ex Air, est. 0.85%, prior -0.3%

- Cap Goods Ship Nondef Ex Air, est. 0.47%, prior -0.1%

- 10am: New Home Sales, est. 620,000, prior 593,000; MoM, est. 4.55%, prior -7.8%

DB’s Craig Nicol concludes the overnight wrap

If there is one positive that we can take from 2018 so far, it’s that it is at least a lot more interesting. While you’d be hard pressed to find anyone who thought that we’d see even less volatility this year compared to 2017, the frequency or extent to which we’re having these mini shocks in markets right now is a surprise. Yesterday was seemingly a perfect storm for this. While markets were already awaiting Trump’s tariff announcement, the fact that it came post a Fed which had already made it known that the direction of trade policy was a concern, and then after optimism about global growth took a hit post the softening flash PMIs, seemed to be the trigger that markets needed to sell anything risky in a hurry.

Indeed, by the end of play the S&P 500 closed down an eye watering -2.52% for the biggest one-day decline since February 8th. That’s also the 7th time in the last 9 sessions that the index has fallen and it also notches up the 17th time that the index has moved by at least 1% up or down since the start of February. As a reminder, there were only 10 such occasions in the 13 months to January. The Dow (-2.93%) and Nasdaq (-2.43%) also capitulated (the Dow is actually down over -4% from the pre-FOMC highs), while in Europe the Stoxx 600 and DAX finished -1.55% and -1.70% respectively. European Banks (-2.27%) are also now the lowest in 11 months. Meanwhile the VIX rose 5.5pts and closed above 23 for the first time in over 5 weeks. Credit markets also felt the pain with CDX IG over 4bps wider and iTraxx Main nearly 2bps wider. In a nutshell, these are the biggest moves that we’ve seen since the vol shock last month.

Those following bond markets were focused on whether or not Bunds might crack 0.50% and Treasuries 2.80% to the downside. Yesterday they tested that with Treasuries briefly touching an intraday low of 2.797%, however they are holding just above that this morning. Bunds fell 6.3bps by the closing bell yesterday to 0.524% and are now at the lowest since mid-January. Other European bond markets were down a similar amount although Gilts stood out with benchmark 10y yields rallying 8.8bps post the BoE (more on that later).

Moving onto the tariffs, for those that missed it President Trump has authorised US Trade Representative Robert Lighthizer to impose 25% tariffs on as much as $60bn in annual imports from China. It’s expected that 10 key sectors will be targeted which were identified under President Xi Jinping’s ‘Made in China 2025’ plan. A detailed list is expected in the coming days. In addition to that, the President has also ordered the US Treasury to start plans for imposing restrictions on Chinese investments in certain sectors. Adding fuel to the fire, Trump said that “this is the first of many”. China’s ambassador to the US said that while “we don’t want a trade war” we “are not afraid of it” and “we will certainly fight back and retaliate”.

This morning, China retaliated with the Commerce Ministry announcing plans for reciprocal tariffs on $3bn of imports from the US, including a 25% tariff on US pork and recycled aluminium as well as 15% tariffs on US steel pipes, fruit and wine. The general feeling is that China’s response has been relatively contained and measured. Markets in Asia are extending the sell-off however with the Nikkei in particular down -4.41%, while the Hang Seng (-3.02%), Shanghai Comp (-2.98%), Kospi (-2.25%) and ASX 200 (-1.95%) have also been hit hard. S&P 500 futures are also down -0.60%. Gold (+0.70%) and the Yen (+0.45%) are the assets benefiting from the flight to safety while bond markets across the board are stronger with 10y JGBs in particular down at 0.015% and the lowest since November.

Back to those PMIs, after Japan was the first to disappoint early in the morning yesterday (0.9pt decline in the manufacturing to 53.2), Europe did little to boost optimism. Indeed, the Euro area manufacturing reading was reported as falling a full 2pts to 56.6 which compared to expectations for a much more modest decline of half a point. That is the lowest since July last year while the services reading also slid 1.2pts to 55.0 (vs. 56.0 expected). That put the composite at 55.3 (vs. 56.8 expected) and down 1.8pts from February, and also the lowest since January last year. Regionally, Germany’s manufacturing print tumbled 2.2pts to 58.4 (vs. 59.8 expected) which means it’s down a shade under 5pts from the December high. France (53.6 vs. 55.5 expected; 55.9 previously) didn’t fare much better with the data also overall implying a decline for the non-core.

That also means that we’ve had two consecutive months of bigger than expected declines for Germany and France with the manufacturing readings in particular suggesting that the external boost to growth might be running out of legs a bit. Our European economists noted in a report yesterday that the question is whether we are seeing some moderate rebalancing or an inflection point into a new weaker regime. The team’s view has been and remains that Euro area GDP growth will slow gradually this year. They note that having dropped the QE bias in March, the ECB has the benefit of time to assess the state of the cycle before facing the next exit step. The moderately dovish tone in ECB commentary lately already suggests risk of a short delay to their baseline exit trajectory and the possibility of moves to limit the risk to financial conditions from the ending of QE.

On the other side of the pond, there was some hope that the US data might be a little more upbeat and while the manufacturing print rose 0.4pts to 55.7 and a bit more than expected, it was notable that the services PMI tumbled 1.8pts to 54.1 (vs. 56.0 expected). As a result, the composite finished down 1.5pts at 54.3.

Away from the tariffs and PMIs, the BoE was also under the spotlight yesterday following the MPC meeting outcome. As expected there was no change in policy with the committee voting to keep rates on hold by 7-2, with McCafferty and Saunders the dissenters which came as a slight surprise. Our UK economists noted that, broadly speaking, the tone and language of the minutes was in line with market pricing for a May hike. They also note that given the prospect of excess demand over the forecast horizon, the BoE continues to reiterate its view of an ongoing tightening in monetary policy at a “gradual pace and to a limited extent”.

Before we wrap up, a quick mention that this morning our European Equity Strategy team have published a report following yesterday’s soft PMI data. Our European equity strategist Sebastian Raedler highlights that as a consequence of the sharp fall in the March Euro flash PMI yesterday, Euro area PMI momentum – the six-month change in PMIs and a key driver of European equities – has turned meaningfully negative for the first time since August 2016. His models now imply a fall in the fair-value for the Stoxx 600 to 360 by mid-year, continued underperformance by European banks and further relative downside for European relative to US equities over the coming months.