GOLD: $1327.70 UP $5.90 (COMEX TO COMEX CLOSINGS)

Silver: $16.40 DOWN 1 CENT (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1329.20

silver: $16.40

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1328.35????

NY PRICING AT THE EXACT SAME TIME: $1331.30????

LONDON SECOND GOLD FIX 10 AM: $1329.15

NY PRICING AT THE EXACT SAME TIME. $1330.20

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:1 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR 31 FOR 3100 OZ

For silver:

MARCH

16 NOTICE(S) FILED TODAY FOR

80,000 OZ/

Total number of notices filed so far this month: 5307 for 26,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8649/OFFER $8,718: DOWN $209(morning)

Bitcoin: BID/ $8563/offer $8634: DOWN $293 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY A FAIR SIZED 1994 contracts from 216,042 FALLING TO 214,048 DESPITE YESTERDAY’S 21 CENT RISE IN SILVER PRICING. WE OBVIOUSLY HAD SOME COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 3465 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 3465 CONTRACTS. WITH THE TRANSFER OF 3465 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3465 CONTRACTS TRANSLATES INTO 17.33 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

39,436 CONTRACTS (FOR 16 TRADING DAYS TOTAL 39.436 CONTRACTS) OR 197.18 MILLION OZ: AVERAGE PER DAY: 2465 CONTRACTS OR 12.32 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 197.18 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 28.17% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 679.01 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A FAIR SIZED LOSS IN COMEX OI SILVER COMEX OF 1994 DESPITE THE 21 CENT RISE IN SILVER PRICE. HOWEVER, WE ALSO HAD A STRONG SIZED EFP ISSUANCE OF 3465 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 3465 EFP’S FOR THE MONTH OF MARCH WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A GOOD 1471 OI CONTRACTS i.e. 3465 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1994 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 21 CENTS AND A CLOSING PRICE OF $16.51 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.070 BILLION TO BE EXACT or 153% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 105 NOTICE(S) FOR 525,000 OZ OF SILVER

In gold, the open interest ROSE BY A HUMONGOUS SIZED 13,358 CONTRACTS UP TO 558,857 WITH THE STRONG SIZED RISE IN PRICE YESTERDAY ( GAIN OF $9.65) HOWEVER FOR THURSDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN HUGE SIZED 15,566 CONTRACTS : APRIL SAW THE ISSUANCE OF 15,461 CONTRACTS, JUNE SAW THE ISSUANCE OF 105 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 558,857. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE AN ATMOSPHERIC OI GAIN IN CONTRACTS: 13.358 OI CONTRACTS INCREASED AT THE COMEX AND A HUGE SIZED 15,566 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 28,924 CONTRACTS OR 2,892,400 OZ =89.96 TONNES

YESTERDAY, WE HAD 10,181 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 157,200 CONTRACTS OR 15,720,000 OZ OR 488.95 TONNES (16 TRADING DAYS AND THUS AVERAGING: 9825 EFP CONTRACTS PER TRADING DAY OR 982,500 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 16 TRADING DAYS IN TONNES: 488.96 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 488.96/2550 x 100% TONNES = 19.17% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1791.63 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX WITH THE RISE IN PRICE IN GOLD TRADING YESTERDAY ($9.65 GAIN). HOWEVER, WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,566 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,566 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 31,003 contracts ON THE TWO EXCHANGES:

15,566 CONTRACTS MOVE TO LONDON AND 15,437 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 89.97 TONNES).

we had: 1 notice(s) filed upon for 100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $5.90 : NO CHANGE IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 850.54 tonnes.

SLV/

WITH SILVER DOWN 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 319.671 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A FAIR 994 contracts from 216,552 DOWN TO 214,048 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE RISE IN PRICE OF SILVER (21 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 4974 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 1994 CONTRACTS TO THE 3465 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1471 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 7.355 MILLION OZ!!!

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE RISE IN SILVER PRICING YESTERDAY (21 CENTS GAIN IN PRICE) . BUT WE ALSO HAD ANOTHER STRONG SIZED 3465 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 17.47 POINTS OR 0.53% /Hang Sang CLOSED DOWN 343.47 POINTS OR 1.09% / The Nikkei closed UP 211.02/Australia’s all ordinaires CLOSED UP 0.99%/Chinese yuan (ONSHORE) closed DOWN at 6.3320/Oil UP to 64.94 dollars per barrel for WTI and 69.24 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED UP AT 6.3295 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3320 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (WEAKER CURRENCY BUT POOR CHINESE MARKETS/AND NEW TRUMP TARIFFS INITIATED/WEAKER GLOBAL MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

AN EXCELLENT LOOK AT WHAT IS GOING ON INSIDE JAPAN FROM SIMON BLACK WHO LIVES THERE

( SIMON BLACK/SOVEREIGN MAN)

3 c CHINA

i)We have outlined to you how the new oil priced in yuan is going to replace the USA Petro- dollar scheme. Nick Giambruno of InternationalMan.com describes the mechanism beautifully

( Nick Giambruno/InternationalMan.com)

ii)it begins: the Chinese trade war started at 12:30 pm est today

( zerohedge)

iii)China now braces for a trade war with the uSA. They accuse the USA of repeated abusing of WTO rules

iv)This morning, the USA will file suit against China for trade law violations. They also are looking at exemption Brazil, Argentina and the EU for the aluminum and steel tariffs. It now seems that the USA target is and has always been China

( zerohedge)

v)This to going to anger China. There is some good news in that the uSA will impose only duties of 25% on some products but they are also targeting the aerospace and information technology and associated machinery: basically high tech stuff.

(courtesy zerohedge)

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

UK

i)Cable (Br Pound /USA dollar) spikes on a hawkish 7;2 split at the Bank of England. However the rate rise will happen in May.However it fell back to par

( zerohedge)

Houston..we have a problem.

( zerohedge)

go figure…

( zerohedge)

iv)UK Russia

Oh this is good: The Russian ambassador now hints that the UK nerve poisoning was a false flag.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

VENEZUELAThis is what we can expect to find when a country goes into hyperinflation. Believe it or not, Venezuela’s inflation is projected at 13,000% next year and cash has disappeared. Now we witness Elorza which will become Venezuela’s largest city to launch its own community currency..similar to what we witnessed in Argentina when provinces created their own currency for trade..

( zerohedge)

9. PHYSICAL MARKETS

i)Craig Hemke at Sprott discusses JPMorgan’s domination of silver futures and “ownership” of physical silver. Chris Powell also comments that JPMorgan is no doubt rigging silver as they have in their possession physical silver along with their massive short. He also asserts what I believe: that the JPMorgan is holding silver for the USA government who in turn is holding the metal for China having received it as a loan way back in 2002.

importance discussion…

( Craig Hemke/Sprott/GATA)

ii)here is a tour of Russia’s gold reserves:

( GATA)

iii)Usually Russia releases its official gold reserves on the 19th of the month but for some reason they delayed it by a few days. They have added more than usual: today another 25 tonnes is added to its official reserves. Most of their official reserves is gold bought from their own mining operations. Russia has increased its gold production last year was 307 tonnes or 25 tonnes/month and that is what they added to official reserves.

(courtesy Lawrie Williams/Sharp Pixley)

10. USA stories which will influence the price of gold/silver

i)THIS MORNING’S EARLY TRADING:

(COURTESY ZEROHEDGE)

iv)Supposedly Congress has reached a deal on their huge omnibus spending budget deal. Let us see if this comes to fruition( zerohedge)

v)Stockman describes the rate shock we will receive as the Fed rolls off 600 billion of bonds. Yields must rise and that will break the stock market and the bond market

vi)SWAMP STORIES

a)Unbelievable!! There are reports that McCabe had ordered the FBI to investigate his boss Jeff Sessions on his testimony prior to becoming Attorney General

( zerohedge)

b)More and more California cities are now defying Sanctuary city laws and joining Trump. The town of Los Alamitos is in total rebellion

( zerohedge)

c)The House Intel Committee formally votes to end the Russian probe and release their findings to the public

d)Dowd resigns as Trump’s lead lawyer in the Mueller probe as he is increasing ignoring his legal advice. It looks like DiGenova, who is very aggressive will be the lead lawyer.( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:412,072 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 556,264 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A FAIR SIZED 1994 CONTRACTS FROM 216,042 DOWN TO 214,048 DESPITE OUR 21 CENT GAIN IN YESTERDAY’S TRADING). ALSO,WE WERE ALSO INFORMED THAT WE HAD 3465 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3465. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD SOME LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1975 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1994 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 3465 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 1471 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 59 contracts FALLING TO 126 contracts. We had 105 contracts filed YESTERDAY, so we GAINED 46 contracts or an additional 230,000 OZ will stand in this active delivery month of March

April LOST 4 contracts FALLING TO 431 .

The next big active delivery month for silver will be May and here the OI LOST 3517 contracts DOWN to 150,407

We had 16 notice(s) filed for 80,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 22/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

1 notice(s)

100 OZ

|

| No of oz to be served (notices) |

480 contracts

(48000 oz)

|

| Total monthly oz gold served (contracts) so far this month |

31 notices

3100 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (31) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (481 contracts) minus the number of notices served upon today (1 x 100 oz per contract) equals 51,100 oz, the number of ounces standing in this nonactive month of MARCH (1.5894 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (31 x 100 oz or ounces + {(481)OI for the front month minus the number of notices served upon today (1 x 100 oz )which equals 51,100 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 12 CONTRACTS OR AN ADDITIONAL 1200 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

oz

nil

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

16

CONTRACT(S

(80,000 OZ)

|

| No of oz to be served (notices) |

110 contracts

(550,000 oz)

|

| Total monthly oz silver served (contracts) | 5307 contracts

(26,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

total deposits today: nil oz

we had 0 withdrawals from the customer account;

total withdrawals; nil oz

we had 0 adjustments

total dealer silver: 59.203 million

total dealer + customer silver: 257.812 million oz

The total number of notices filed today for the March. contract month is represented by 16 contract(s) FOR 80,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5307 x 5,000 oz = 26,535,000 oz to which we add the difference between the open interest for the front month of Mar. (126) and the number of notices served upon today (16 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 52307(notices served so far)x 5000 oz + OI for front month of March(126) -number of notices served upon today (16)x 5000 oz equals 27,085,000 oz of silver standing for the March contract month.

We GAINED an additional 46 contracts or 230,000 additional silver oz will stand for delivery at the comex

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 78,753 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 122,746CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 122,746 CONTRACTS EQUATES TO 613 MILLION OZ OR 87.67% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.83% (MARCH 22/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (March 22/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.83%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.89%: NAV 13.67/TRADING 13.25//DISCOUNT 2.89.

END

And now the Gold inventory at the GLD/

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 22/2018/ Inventory rests tonight at 850.54 tonnes

*IN LAST 347 TRADING DAYS: 90.50 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 277 TRADING DAYS: A NET 65.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 22/2018: NO CHANGE IN SILVER INVENTORY

Inventory 319.671 million oz

end

6 Month MM GOFO 2.05/ and libor 6 month duration 2.43

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.05%

libor 2.43 FOR 6 MONTHS/

GOLD LENDING RATE: .38%

XXXXXXXX

12 Month MM GOFO

+ 2.48%

LIBOR FOR 12 MONTH DURATION: 2.68

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.20

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

March 22

– Gold gained 1.8% and silver 2.5% to $1,333/oz and $16.60/oz yesterday

– Gold climbs as Fed increases interest rates by 0.25% – now 1.5% to 1.75% range

– Dovish Fed Chair Powell plans fewer than expected rate hikes in 2018

– Markets disappointed at lack of hawkish comments from new Fed Chair

– Dollar LIBOR rises to highest level since November 2008 – $200 trillion worth of dollar-denominated financial products including mortgages based off LIBOR

– Trade wars look set to escalate and Trump expected to announce tariffs on Chinese imports today

Editor: Mark O’Byrne

Gold in USD – 1 Week (GoldCore)

Gold gained 1.7% and silver 2.5% to $1,333/oz and $16.60/oz respectively yesterday after the Federal Reserve announced a 25 basis point increase in rates to the slightly higher range of 1.5% to 1.75%. Gold and silver consolidated on those gains overnight in Asia and this morning in European trading, as markets digested the Federal Reserve’s post-announcement comments.

The first Federal Reserve meeting chaired by Jerome Powell offered little in the way of surprise. A hawkish tone was expected from new Chair Powell, however his statement was slightly more dovish despite what he claimed was a strengthened economic outlook and confidence that tax cuts and government spending will provide an much needed boost.

Source: @JohnFeeney10

The Fed confirmed that there would be just three rate hikes this year, as stated in the December 2017 minutes. Currently the interest rate remains 50bp below LIBOR which continues to climb, widening the spread between itself and OIS.

Should this continue to worsen the impact could be greater on the economy and wealth, than Fed set interest rates. On this basis, the Powell and co. may well decide on additional rate hikes on top of the two expected this year and those forecast for 2019 and 2020.

Yesterday CME Group reported that speculative betting on future Fed rate rises in June are 84.4% likely (up from 58.5% a month ago) and September’s meeting 52.2% (jumping from 37.3% a month ago).

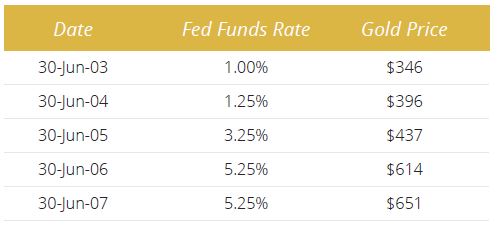

Data shows rising interest rates is positive for gold as seen in 1970s and again from 2003 to 2007. Source: New York Federal Reserve for Fed Funds Rate, LBMA.org.uk for Gold (PM fix)

Gold to find further support in trade wars

Later today President Trump will almost certainly announce tariffs on Chinese imports. The White House is said to be considering between $30bn-$60bn in tariffs and measures that would restrict investment. Yesterday the country’s top trade negotiator, Robert Lighthizer, told Congress the US will put “maximum pressure on China and minimum pressure on US consumers”.

Any changes to current trade arrangements will no doubt increase tension between the super powers. Many expect retaliation from Beijing (to any US measures) prompting a trade war and there is also the real of currency wars returning with a vengeance.

Elsewhere, EU leaders will today consider how best to respond to Trump’s decision to place tariffs on aluminium and steel imports, another move likely to trigger a trade war.

Recent Fed meetings and interest rate announcements have coincided with short term lows in the gold price and a good entry point for those looking to accumulate on the dip (see chart above).

We expect the same on this occasion and we should again test resistance at $1,360/oz in the coming weeks. Growing uncertainty and deepening risks will provide further support for gold and should see higher gold prices.

-END-

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Craig Hemke at Sprott discusses JPMorgan’s domination of silver futures and “ownership” of physical silver. Chris Powell also comments that JPMorgan is no doubt rigging silver as they have in their possession physical silver along with their massive short. He also asserts what I believe: that the JPMorgan is holding silver for the USA government who in turn is holding the metal for China having received it as a loan way back in 2002.

importance discussion…

(courtesy Craig Hemke/Sprott/GATA)

Craig Hemke at Sprott Money: Morgan’s domination of silver futures

Submitted by cpowell on Wed, 2018-03-21 15:27. Section: Daily Dispatches

10:30p ICT Wednesday, March 21, 2018

Dear Friend of GATA and Gold:

Writing for Sprott Money, Craig Hemke of the TF Metals Report today examines JPMorganChase’s huge position in physical silver and Comex silver futures, a position so large that it appears to violate ordinary commodity position limits imposed by the U.S. Commodity Futures Trading Commission. Hemke’s analysis is headlined “JPMorgan’s Domination of Silver Futures” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/jpmorgans-domination-of-comex-silver-cr…

Your secretary/treasurer would elaborate on Hemke’s analysis. For six years ago, just after JPMorganChase began accumulating silver — perhaps doing so, as silver market rigging foe Ted Butler has written, to offset the short position the bank had assumed with its acquisition of Bear Stearns — JPMorganChase proclaimed that it had no positions of its own in the monetary metals, just client positions.

See:

https://www.youtube.com/watch?v=gc9Me4qFZYo

https://www.benzinga.com/media/cnbc/12/04/2478161/jp-morgan-commodities-…

https://www.ft.com/content/efc5618a-7e66-11e1-b20a-00144feab49a

https://www.zerohedge.com/news/blythe-masters-blogosphere-silver-manipul…

Of course back then nobody asked the bank to identify its “clients” in monetary metals trading. Given the strategic sensitivity of the monetary metals, it is a fair assumption that the bank’s clients in the metals are governments, and to rig a market a government or its broker probably would maintain both long and short positions.Further, it seems unlikely that any U.S. investment bank enjoying a privileged position as a primary dealer in U.S. government securities, as JPMorganChase does, would do anything in strategic markets without the government’s approval.

Of course it’s also possible that JPMorganChase is running monetary metals positions for other governments, like China’s, with the approval of the U.S. government.

This would answer the question posed the other day by Keith Weiner of Monetary Metals in his commentary “Standing Ready to Lease Gold”:

http://news.goldseek.com/GoldSeek/1521468000.php

Weiner wrote: “If the mechanism of alleged gold price suppression is central bank leasing, then that leaves silver lacking an explanation. Central banks have no silver. The price of silver has fallen to 1/80th of the price of gold, which needs to be explained. If gold is suppressed, and silver is not, then how do we explain why silver is cheap relative to gold?”

But as the British economist Peter Warburton noted in 2001 —

— with enough money in derivatives the price of anything traded in a futures market can be suppressed. If Weiner really wants to pursue an explanation for silver’s awful chart, he might start by looking in JPMorganChase’s silver vault and derivatives book.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

here is a tour of Russia’s gold reserves:

(courtesy GATA)

An exclusive tour of Russia’s gold reserve

Submitted by cpowell on Thu, 2018-03-22 03:08. Section: Daily Dispatches

10:05a ICT Thursday, March 22, 2018

Dear Friend of GATA and Gold:

Brandon White of bullion dealer BMG Group in Ontario calls attention to a recent report in the major Russian newspaper Komsomolskaya Pravda by two journalists who were given an exclusive tour of the vault containing Russia’s gold reserve.

White has provided a translation that may be better than an ordinary internet translation, and it is appended. But the translation is interrupted by captions for the photographs accompanying the story, which you’ll want to see and which can’t be reproduced here. The article, in Russia, of course, and the photos are posted together at the Komsomolskaya Pravda internet site here:

https://www.kp.ru/putevoditel/lichnye-finansy/zolotoj-zapas-rossii/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

This Is How Our Nest Egg Gold Is Stored for a Rainy Day

The correspondents of KP, Evgeny Belyakov and Vladimir Velengurin, are the first journalists in the country to get to visit the main gold vaults of the Russian central bank.

Text by Eugene Belyakov

Photos by Vladimir Velengurin

Komsomolskaya Pravda, Moscow

January 2018

https://www.kp.ru/putevoditel/lichnye-finansy/zolotoj-zapas-rossii/

The sensations were strange. I was in the same room with hundreds of tons of gold. In Money it is almost a trillion rubles. To accumulate such an amount, the average sportsman would have to work several million years. My legs shake only from the realization of one highly relevant fact: this kind of wealth has led to innumerable wars and fallen empires.

A ton of gold-per square meter. “Well, do you think they would notice if we stole just one bar?” asked my colleague and photojournalist Vladimir Velengurinym upon arrival at the vault. Admission to the central bank’s vault is strictly limited. The central bank made an exception for KP.

We imagined the storage system differently. I imagined Scrooge McDuck’s storage, where you can dive. Well, or at least juggle coins and ingots. Volodya imagined it as a mountain of ingots, exposed and stacked in giant pyramids for picturesque effect. Everything turned out to be much more banal. Lattice containers, tampered and folded one on another, stand equal rows along the whole premise. The scale is impressive. The appearance — not very.

Now the volume of gold in the international reserves of the central bank exceeds 1,800 tons. Russia is the sixth-place gold holder on the world index. Ten years ago the share of gold in our international reserves was 3 percent. But in recent years the central bank has started to increase its reserves — now the share has risen to 17 percent.

The gold reserve is a security cushion for the country. In case of crisis or shortage of foreign exchange reserves, gold can always be sold or deposited. It is still in demand in world markets, though earlier its value in this regard was much higher.

Gold played the role of world currency. It was a world trade settlement tool. In addition, the amount of gold in the country’s reserves determined the value of the national currency. Each banknote was initially provided with some quantity of this metal. That is, the country could print more money only if the reserves added more gold. This kept the currency from inflating. Until 1944 all countries kept their reserves only in gold.

Now the value of gold as a nation’s reserve is less than it used to be. The U.S. dollar plays a major role in global trade settlement. Most countries hold most of their international reserves in dollars. Although there are nuances: In developed countries the share of gold in reserves is 60-70 percent. But they do not have as much savings as in developing countries.

However, gold is still used as a protective tool. In crisis it is possible to sell it for money.

Dictionary time: “Monetary gold” is the central bank’s and the Russian government’s standard for gold bars and coins and must be made with a metal purity of not less than 995/1000.

International reserves have the same standard for gold as a currency reserve. The country’s money is now stored not only in precious metals and world currencies, but also in other financial instruments. For example, the structure of Russian reserve assets have a reserve position in the International Monetary Fund using Special Drawing Rights (SDR). In fact, in Russian, the SDR literally translates as “pseudo-value.” The SDR was invented by the IMF as a universal tender. The IMF’s SDRs are not widely disseminated as they remain used only between the IMF member central banks.

In theory, the structure of reserves should take into account the structure of export and import operations of the country.

… History of Russian gold stocks

— The gold reserve of the Empire in the beginning of 1914 was 1,312 tons. Back then Russia was among the three largest gold squirrels, along with the United States and France.

— 10 years after the revolution the gold reserve of the Soviet Union depleted to 150 tons. This was the result of the First World War and spending of the new Soviet power.

— After Joseph Stalin came to power, the gold reserve of the Soviet Union began to grow rapidly. By 1941 it reached 2,800 tons. (This is the historical maximum.)

— In 1991 the legacy of the Union of New Russia was only 290 tons of gold. The accumulation had to start almost from scratch.

It’s interesting how the gold bars are poured.

KP photojournalist Vladimir Velengurin visited the Novosibirsk refinery, where the nation’s gold is refined. Novosibirsk is in Siberia and is farther from any ocean than all but one of the world’s cities.

One bar is worth 30 million rubles

I never thought that gold was so heavy. The bar is small but it is not easy to raise it. He pulls 12-13 kilograms. So you can safely swing the biceps. I’m sure some rich guys do. Why else would they have so much money?

Ingots are neatly stacked in lattice containers (20 pieces each). Each of them sealed.

In whose hands is all the gold of the world?

It is difficult to estimate the amount of gold available on the planet. The approximate calculation is 190,000. More than half of that is in private ownership of the public (mostly in the form of jewelry). Still, about 33,500 tons are official reserves in the vaults of the countries of the world. The rest is used for investment purposes by large companies and foundations or is applied in dentistry, electronics, and other industries.

The sign of “evil” means “gold refined.” On the ingot is a trademark of the manufacturer, where you can find the place of production of a particular ingot, year of manufacture, sample, and weight of the ingot.

Ingots have a sample purity from 99.95 to 99.995. It means that the gold content there is from 99.95 to 99.995 percent respectively. The remainder is impurities.

Each ingot has a document of its quality. In addition to gold in the ingot there are also impurities of other metals. For example, iron, platinum, palladium, rhodium, lead, silver, copper, nickel, and others. But that part of the bar tends towards zero.

The market value of gold is constantly changing. The price is quoted on the stock exchange. On average at the time of publication one standard bar costs 30 million rubles. The whole box weighs about 250 kilogram, worth 600 million rubles.

The biggest win in the history of Russian lotteries is 506 million rubles. (In the middle of November this year the winner of the Russian lottery became a resident of the Voronezh region.)

A question to consider is this: Is gold too expensive?

There is a popular opinion that gold is always expensive. This is proclaimed by many high-profile analysts. If you look at the price dynamics, it’s nothing like that. In some periods gold experiences long-term growth, and in other periods there is stagnation for decades. Therefore, it is impossible to predict how gold will behave in the coming years. It would be possible to interview 10 analysts on this topic, but probably only half of them would guess correctly.

For example, in 2011-2012 the demand for gold was at its climax. The price per troy ounce (31.1 grams) reached $1,900 and experts competed among themselves predicting a higher price. The most notable seems to be the chief executive officer of Euro Pacific Capital, Peter Schiff. He predicted that an ounce of the metal would soon rise to $5,000 and added that “that won’t be the limit.” He advised all private investors to buy gold.

“Whoever does this will get a huge profit,” Schiff said. Those who followed his advice suffered losses. So we will not give predictions.

A financial adviser once said to me: “You need to buy gold only in case of atomic warfare. Then it can be changed to bread. If you believe in a quick apocalypse, buy it. … Or for its beauty.”

There are several ways to invest your money in gold. Almost all of them involve additional commissions, overpayments, and inconveniences. Whether it is worth the cost is for you to decide.

Oh, hard work — hauling billions every day!

The team’s work is heavy. Carrying 13 kilograms of ingots is not easy. Plus, they have to follow a lot of instructions. Each action of the employee is strictly regulated.

Workers treat ingots very carefully. They are not allowed to damage the ingots. The gold in the vault should be in perfect condition.

The table for weighing is covered in green cloth, as on a billiard table. This protects the metal from scratches and other damage.

… Epilogue …

Storage workers call gold simply “metal” and all together (with banknotes and coins) — “values.” And after one hour in the vault you stop perceiving gold as something expensive and exotic. Your legs stop trembling and you lose the desire to possess it. Metal is metal. It sparkles but does not attract. Probably in a place similar to this arose the saying, “Happiness is not born in money.” For this reason it is a pity that access to the vault is strictly limited. We should encourage excursions to the vault for all our oligarchs.

END

Usually Russia releases its official gold reserves on the 19th of the month but for some reason they delayed it by a few days. They have added more than usual: today another 25 tonnes is added to its official reserves. Most of their official reserves is gold bought from their own mining operations. Russia has increased its gold production last year was 307 tonnes or 25 tonnes/month and that is what they added to official reserves.

(courtesy Lawrie Williams/Sharp Pixley)

LAWRIE WILLIAMS: Russia adds another 25 tonnes to its gold reserves

President Putin gets re-elected in a landslide and Russia continues to build its gold reserves adding another 800,000 ounces (24.88 tonnes) in February. It’s ‘déjà vu all over again’ in the words of the late Yogi Berra.

Putin is seen to be a believer in gold both as a key asset in the global monetary system and as a foreign reserve diversifier away from the U.S. dollar. The next step may well be to repatriate any Russian gold stored elsewhere in the world – we shall see. Russia no doubt feels that the U.S.-led West is ganging up on it following the latest allegations by the UK of Russian state involvement in what appears to have been an assassination attempt on a former double agent and his daughter using a Russian-developed nerve agent. Strong circumstantial evidence points to Russia, but so far there has been no definitive proof of state involvement.

Currently, Russia appears to be one of the few countries expanding its new mined gold output as global production peaks and maybe is beginning to turn down. According to the country’s Finance Ministry Russian gold production last year was 306.9 tonnes which would put it in second place among global gold mining nations. See: Russia may now be World No. 2 Gold Miner. One suspects that the major independent gold analysts like Metals Focus and GFMS, when they produce their annual gold publications next month, may put the production level a little lower and it will be interesting to see if they assess Russia as the global No.2 or 3 producer. It is vying with Australia for this position and the latter, which was No. 2 in 2016, is also seen to have been increasing its output last year but perhaps by not as much as Russia. (See: Peak gold maybe but Australian and Russian output still rising)

In terms of reported gold reserves to the IMF, Russia is already the world’s fifth biggest national holder of gold, moving ahead of China in January – but we don’t really believe the Chinese figure given that it has reported a zero increase in its gold reserves for 15 straight months now. We think it may be reverting to its old pattern of gold reserve reporting where it only reports increases at multi-year intervals claiming that some of its gold was being held in non-reportable accounts – see: Chinese CB officially adds zero to gold reserves in February

The latest Russian figure now brings the country’s gold reserve to around 1,882 tonnes, as compared with the official Chinese holding of 1,842.6 tonnes, still well short of the U.S., German, Italian and French totals, but closing the gap as neither the USA, or big European gold holders have changed their reported holdings for a number of years now. Interestingly, in terms of officially reported reserves Russia and China combined hold around 3,725 tonnes of gold – well in excess of world no.2 individual holder, Germany’s, 3,373.6 tonnes Gold truly is seen to be moving east!

But of course Russia is still adding to its gold reserves month in month out and China’s figure may well be significantly understated. It would not surprise us if that in reality China and Russia combined may even hold more gold than the reported U.S figure of 8,133.5 tonnes. It looks like the two nations may well see a future role for gold in the ever-changing world financial order which is largely being ignored by the West.

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3320 /shanghai bourse CLOSED DOWN 17.47 POINTS OR 0.53% / HANG SANG CLOSED DOWN 343.47 POINTS OR 1.09%

2. Nikkei closed UP 211.02 POINTS OR .99% /USA: YEN FALLS TO 105/58/

3. Europe stocks OPENED RED /USA dollar index FALLS TO 89.69/Euro FALLS TO 1.2324

3b Japan 10 year bond yield: FALLS TO . +.038/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105/58/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.94 and Brent: 69.24

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.554%/Italian 10 yr bond yield DOWN to 1.896% /SPAIN 10 YR BOND YIELD DOWN TO 1.305%

3j Greek 10 year bond yield RISES TO : 4.258?????????????????

3k Gold at $1329.65 silver at:16.53 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 9/100 in roubles/dollar) 56.95

3m oil into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9467 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1669 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.599%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.848% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0705% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Tumble, Stocks Slide Ahead Of Trump’s China Trade War; Facebook Selling Resumes

Yesterday, we showed that according to Wall Street, the biggest tail risk facing investors right now is a “trade war”…

… and that should trade tensions escalate, lower stock prices would be the immediate result (and that managers would sell stocks in advance).

Well so far this morning, they are being proven right (or simply selling), because a jittery overnight session for stock futures which saw the S&P close at session lows after yesterday’s Fed rate hike (due to the “snowstorm” according to a dead serious Marko Kolanovic), turned increasingly volatile just before dawn in New York, as investors prepared for today’s China trade war announcement from President Trump that could levy tariffs on more than 100 types of Chinese goods, and is due just after noon ET.

As a result, S&P futures slid for much of the session, dropping below 2,700 and hugging the key support level as we hit save (we wonder what weather phenomenon JPM will blame for today’s swoon).

“Investors are increasingly nervous about the escalation in the narrative towards a trade war between the U.S. and China, it makes markets quite volatile,” Stephane Ekolo, equity strategist at TFS Derivatives, told Bloomberg.

It wasn’t just US futures though, and it wasn’t just the imminent US trade war with China, as several other factors converged, leading to a sea of red in global stock markets, resulting from continued pressure on technology stocks led by Facebook, as well as a sharp deterioration in European PMI data, oh and of course asset valuations which remain at all time high; Nasdaq futures slide to below Monday’s low which was start of tech sector focus, while e-mini S&P futures testing 100-DMA.

The Fed did not help to boost sentiment, tightening financial conditions by raising its key rate another 25 basis points to 1.75 percent on Wednesday and flagged at least two more increases were likely this year. But it stopped short of pointing to the three that some economists had been predicting. China also nudged up its borrowing costs overnight, as Beijing braced for new tariffs from U.S. President Donald Trump on Chinese imports worth as much as $60 billion.

Not all Fed bulls were discouraged, though. “Over the balance of the year we do think they will move to four hikes,” said JP Morgan’s Seamus Mac Gorain, highlighting the impact of recent fiscal stimulus. “Trade tariffs are a risk, of course, but more open economies,” such as Mexico or the euro zone “could be more at risk than the U.S.”

European equities found some support through cash open before fading further, led by underperformance in the tech and bank sectors. The Stoxx Europe 600 Index dropped 0.9%, with 18 of 19 industry groups in the red. Technology, chemicals and lender shares are the worst sector decliners. Reckitt Benckiser rose 6.5% after the company ended discussions about buying a portion of Pfizer’s consumer health business.

Thursday’s European retreat worsened after latest PMI data showed the continent’s private-sector economy cooled in March as manufacturing growth contracted sharply. The Markit composite purchasing managers’ index dropped to 55.3 from 57.1, below the median estimate of 56.7, and a 14 month low.

- EU Markit Manufacturing Flash PMI (Mar) 56.6 vs. Exp. 58.1 (Prev. 58.6)

- EU Markit Comp Flash PMI (Mar) 55.3 vs. Exp. 56.7 (Prev. 57.1)

- EU Markit Services Flash PMI (Mar) 55.0 vs. Exp. 56.0 (Prev. 56.2)

Meanwhile, economic confidence in Europe’s exporting powerhouse – Germany – continues to shrink as Europe is likely next on Trump’s deficit-shrinking, trade war radar. In today’s IFO Business Confidence reading, both current conditions and expectations continued to shrink.

“The threat of protectionism is dampening the mood in the German economy,” said Clemens Fuest, the chief of the Munich-based Ifo institute, which published the business sentiment data.

The MSCI Asia Pacific index rose for first time in five days although Chinese stocks declined sharply at the close after the PBOC matched the Fed’s rate hike, and raised interest rates on reverse repo operations and funding facilities by five basis points. The Shanghai Composite fell 0.5% while the ChiNext index dropped 0.7%. In Hong Kong, the Hang Seng Index fell 1.1% while the Hang Seng China Enterprises Index closes down 0.8%, wiping out 1.6% rise in morning. Tencent weighed on the Hang Seng Index, falling 5% – most since Feb. 6 – after posting results Wednesday evening; analysts lowered profit forecasts based on the company’s spending plans.

Meanwhile, Zuckerberg’s CNN appearance last night did little to calm the growing fears, and Facebook was down another -2.0% in pre-market.

In other overnight news, US House and Senate leaders agreed to USD 1.3TN spending bill which they hope to pass prior to the government shutdown deadline at midnight this Friday, although there were also reports that US House Freedom Caucus said it is against the omnibus spending measure. In Europe, the EU expects US President Trump to announce tariff waiver today according to sources.

The ECB released its economic bulletin, which showed that Indicators suggest strong growth momentum with possible better expansion in the near term, adding that developments support a gradual upward trend in wage growth. Also overnight, Riksbank’s Floden said sticking to the current interest rate path is the fastest way to get interest rates up adding that the latest inflation outcomes are clearly lower than expectations.

In FX, the British pound was the notable mover, surging to its highest in more than a month after British wage data published on Wednesday bolstered expectations the Bank of England would signal a May rate increase after its monetary policy meeting due in just over an hour.

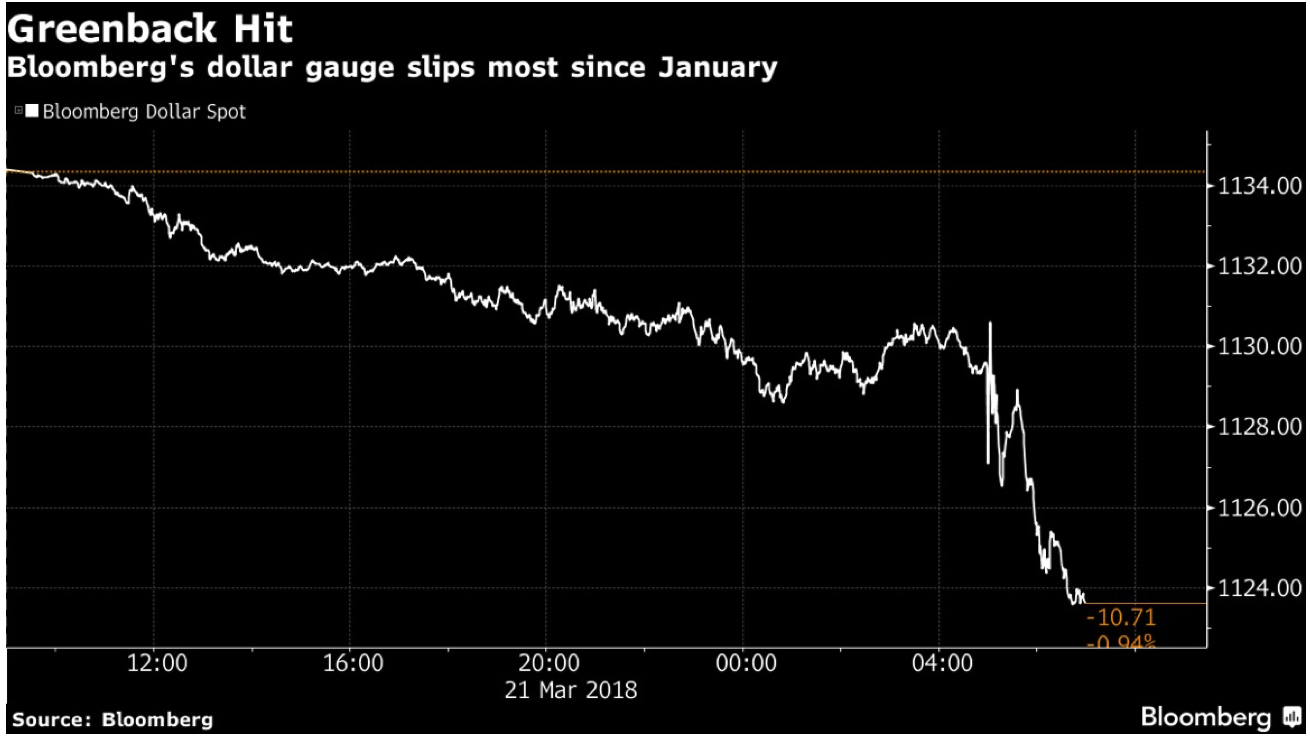

Meanwhile, the dollar initially weakened further in follow-through from FOMC digestion and unchanged 2018 median dots; however the risk-off environment leads to slow grind higher against G-10, except for USD/JPY, which goes through Asian low. As Bloomberg adds, the dollar erased its decline, holding steady as President Trump readies to announce about $50 billion of tariffs against China over intellectual-property violations. The pound maintains its bullish momentum, while the euro erases gains as PMI data out of Germany and France missed forecasts. Some highlights of key FX pairs below, from BBG:

- The Bloomberg Dollar Spot Index was little changed, close to a one-month low, and most G-10 crosses traded in narrow ranges

- The euro edged up toward 1.24 against the dollar before erasing gains; the pound rose amid speculation that the BOE will pave the way for an interest-rate increase in May while gilts rallied on profit taking

- USD/JPY slipped amid Japan’s political uncertainty and concern about U.S. protectionism; the yen was also boosted by seasonal demand by Japanese operators ahead of the fiscal year-end book closing and a softer dollar after the Fed’s rate decision was considered less hawkish than what some traders expected

- The Aussie reversed earlier gains and a test of the 100-DMA at 0.7778 after February jobs data missed estimates and with traders are also waiting on expected U.S. announcement levying $50 billion of tariffs against China

Meanwhile, Treasuries extended their gains from Wednesday, with gilts pushing higher ahead of the Bank of England decision, as global bond yields fell broadly. Borrowing costs on 30-year German debt hit their lowest level of the year. Two-year U.S. yields slipped to 2.304% from 9 1/2-year high of 2.366%. The 10-year yield fell below 2.85%, its biggest move in three weeks.

In commodities, crude drifted sideways near $65.30 while iron ore traded in China was 1.5% stronger. WTI (-0.8%) and Brent Crude (-0.6%) took a breather from yesterday’s post-DOE rally with both benchmarks hovering just below their highest level since early February amid rising concerns of US output threatening to disrupt the tightening market; WTI has recently given back the USD 65/bbl handle. Moving onto metals, despite a softer USD and general risk-aversion thus far, gold prices are seen modestly lower after spot gold hit highs of USD 1334.8/oz overnight. Elsewhere in base metals, copper climbed off its lowest level in three months, Dalian iron ore rose 0.9% after recouping recent losses, steel futures were seen lower overnight as demand concerns continue to hamper sentiment.

Economic data on Thursday include initial jobless claims, Markit PMI data. Nike, Micron and Accenture are among companies due to release results

Market Snapshot

- S&P 500 futures down 0.8% to 2,696.25

- STOXX Europe 600 down 0.4% to 373.59

- MSCI Asia Pacific up 0.3% to 177.01

- MSCI Asia Pacific ex Japan down 0.3% to 581.48

- Nikkei up 1% to 21,591.99

- Topix up 0.7% to 1,727.39

- Hang Seng Index down 1.1% to 31,071.05

- Shanghai Composite down 0.5% to 3,263.48

- Sensex down 0.07% to 33,114.27

- Australia S&P/ASX 200 down 0.2% to 5,937.15

- Kospi up 0.4% to 2,496.02

- German 10Y yield fell 2.4 bps to 0.568%

- Euro up 0.2% to $1.2360

- Brent Futures down 0.5% to $69.16/bbl

- Italian 10Y yield rose 3.5 bps to 1.676%

- Spanish 10Y yield fell 3.4 bps to 1.301%

- Gold spot down 0.1% to $1,330.94

- U.S. Dollar Index down 0.3% to 89.54

Top Overnight Headlines

- U.S. will announce China tariffs today; to target more than 100 different types of Chinese goods totalling $50b, according to people familiar

- EU expects that it will be exempted from U.S. import tariffs on steel and aluminum, according to people familiar

- European Mar. P Composite PMIs: France 56.2 vs 57.0 est; Germany 55.4 vs 57.0 est; 55.3 vs 56.8 est.

- Riksbank Deputy Governor Martin Floden says inflation data below Riksbank’s forecast, weaker krona than expected lately are “two developments that speak in different directions in terms of what should happen with monetary policy”

- German Mar. IFO Business Climate: 114.7 vs 114.6 est; Expectations 104.4 est; Current Assessment 125.9 vs 125.6 est.

- U.K. Feb. Retail Sales y/y 1.5% vs 1.4% est;ONS notes underlying three-month picture is one of falling sales, mainly due to strong declines across all sectors in December

- PBOC hikes reverse repo rate by 5bps to 2.55% in reaction to Fed

Asian stocks traded mixed as the region digested the fallout from the FOMC. ASX 200 (-0.2%) and Nikkei 225 (+1.0%) were varied with commodity-related stocks underpinned by gains in crude and the metals complex due to a softer USD, while the KOSPI (+0.4%) also gained amid US tariff exemption hopes after US Trade Representative Lighthizer named South Korea as one of the countries likely to be exempted. Conversely, Hang Seng (-1.1%) and Shanghai Comp. (-0.5%) underperformed with the US set to announce tariffs on China later today and after both the HKMA and PBoC raised rates in response to the Fed. Finally, 10yr JGBs were higher by around 10ticks as they tracked the gains seen in T-notes which found relief from the unchanged 2018 Fed rate hike projections, while the BoJ were also in the market for JPY 710bln of JGBs in the belly to super-long end with its Rinban amounts kept unchanged.

The PBoC stated that the increase in reverse repo rates meets market expectations and is a normal response to the Fed rate hike, while the Hong Kong Monetary Authority also raised rates by 25bps to 2.00% in lockstep with the Fed.

Top Asian News

- China’s Central Bank Raises Borrowing Costs After Fed Hikes

- Philippines Keeps Key Rate at 3% as Seen by Most Economists

- Tencent Among Top Decliners After Margins Warning: Asia Movers

- UBS Sees India’s External Finances at Risk Despite High Reserves

- Tesla to Supply Batteries for Solar Project in Australian State

European equities kicked the session off on the backfoot (Eurostoxx 50 -1.1%) with losses emanating largely from the fallout of yesterday’s FOMC release and proposed US tariff measures today on China which are set to be unveiled at 1630GMT. Equities then staged a mild recovery before once again taking another turn lower in what has been a choppy session of trade thus far since the open. In terms of sector specifics, all ten sectors trade lower with some modest outperformance in energy names in-fitting with price action in the complex as WTI held onto the USD 65/bbl level (has since lost this level). Individual movers include Reckitt Benckiser (+5.5%) who have confirmed they have dropped out of the running for Pfzier’s consumer health business which has subsequently paved the way open for GSK (-1.0%) to make an approach.

Top European News

- Rio Tinto to Sell Winchester South to Whitehaven for $200m

- Ted Baker Sees Challenging Market Conditions After Bad Weather

- StanChart Is Said to Start Sale Process for Private Equity Unit

- Volatile Volatility Leaves Europe’s Investment Banks Whipsawed

- Deutsche Bank Raised ‘A Lot of Money,’ Needs to Deploy It: CEO

In FX: USD: Initially a choppy reaction from the FOMC’s rate hike decision yesterday, however the greenback ultimately softened after members maintained 2018 rate path view of 3 rate hikes (1 member away from median projection at 4). Additionally, the central bank steepened the path of rate hikes for 2019-2020, however the council did soften language around activity. DXY trading above mid-89 with losses stemmed after finding support at the March lows of 89.40. Trade wars remain at the forefront of investors’ minds amid reports that Trump will announce China tariffs today (1230EDT) with the value said to be around USD 50bln (lower than the previously touted USD 60bln). Retaliation from China is likely, as evidenced by yesterday’s WSJ report. Subsequently, the increased uncertainty could take USD/JPY back down to the 2018 low (105.23) prompting a test of the 105 handle. Antipodeans (AUD,NZD): RBNZ kept interest rates unchanged at 1.75%, as expected. Market pricing for a rate hike is not seen until mid-19. As such, NZD saw a muted reaction upon release, the central bank struck a rather balanced tone after remaining upbeat over global growth, but highlighted downside risks to inflation. NZD currently trading in a tight 40pip with price action likely to be driven by risk. A firm break above 0.7260 could see the spot price back at 0.7350, however, trade war uncertainty may see gains tempered. Elsewhere, AUD has been pressured by the jobs report overnight with the headline employment change falling short of expectations (17.5 vs. Exp. 20k), while the unemployment rate saw an unexpected uptick.

In commodities, WTI (-0.8%) and Brent Crude (-0.6%) are taking a breather from yesterday’s post-DOE rally with both benchmarks hovering just below their highest level since early February amid rising concerns of US output threatening to disrupt the tightening market; WTI has recently given back the USD 65/bbl handle. Moving onto metals, despite a softer USD and general risk-aversion thus far, gold prices are seen modestly lower after spot gold hit highs of USD 1334.8/oz overnight. Elsewhere in base metals, copper climbed off its lowest level in three months, Dalian iron ore rose 0.9% after recouping recent losses, steel futures were seen lower overnight as demand concerns continue to hamper sentiment.

Looking at the day ahead, EU leaders will today meet in Brussels to sign off on Brexit guidelines (continuing through to Friday). Meanwhile it’s a busy day for data, highlighted by the release of those flash March PMIs in Europe and the US. The BoE monetary policy meeting outcome is the other big highlight. Other notable data releases include March confidence indicators in France, the January current account balance reading for the Euro area, Germany’s IFO survey

for March, UK retail sales for February and weekly initial jobless claims, January FHFA house price index, February leading index and March Kansas City Fed PMI in the US. Late in the evening we’ll also get the February CPI report in Japan. ECB speak will also be a focus with Lautenschlaeger and Nouy due to speak at separate events. German Chancellor Merkel is also due to deliver a speech in parliament likely outlining her policy goals.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 225,000, prior 226,000; Continuing Claims, est. 1.87m, prior 1.88m

- 9am: FHFA House Price Index MoM, est. 0.4%, prior 0.3%

- 9:45am: Bloomberg Economic Expectations, prior 54.5; Consumer Comfort, prior 56.2

- 9:45am: Markit US Manufacturing PMI, est. 55.5, prior 55.3

- Markit US Services PMI, est. 56, prior 55.9

- Markit US Composite PMI, prior 55.8

- 10am: Leading Index, est. 0.5%, prior 1.0%

- 11am: Kansas City Fed Manf. Activity, est. 17, prior 17

DB’s Jim Reid concludes the overnight wrap

Unsurprisingly, the big focus over the past 24 hours has been the Fed and to be honest, we’ve been left scratching our heads a little as how best to sum up the meeting. By the end of day the market was seemingly left feeling a little

bit underwhelmed given that Treasury yields closed well off their highs and the Greenback tumbled by the most in nearly two months. However, it feels like that was perhaps just reflective of what were elevated hawkish expectations going into it as the message for us was one that while economic data for now is not necessarily strong enough to justify a faster hiking cycle this year, the Fed does appear to be a lot more upbeat further down the line.

Indeed, that was reflected initially in the statement with the addition of the line “the economic outlook has strengthened in recent months”. The hotly anticipated dot plot projections revealed that the median for 2018 was left at a total of three rate hikes, however only just as it would have only taken one more voter below the median to have moved higher in order to shift the median to four. Further out, the median for 2019 is now at 2.9% which implies three rate hikes, an increase of one from December, while the 2020 median is now at 3.4% which is up from 3.1% in December.

Meanwhile the stronger outlook was reflected in the more optimistic median projections for growth, unemployment and inflation. Indeed, GDP has been revised up by two-tenths this year to 2.7% and by three-tenths in 2019 to 2.4% while unemployment was revised down one-tenth this year to 3.8% and down three-tenths next year to 3.6%. As for inflation, the median committee member still expects core inflation this year of 1.9% which was perhaps a small surprise given the data so far, however median readings for 2019 and 2020 were both lifted to 2.1% and a tenth more than previously expected. That’s interesting as it also implies that the Fed is willing to accept a slight overshoot which is something that Evans has emphasized with regards to the symmetry of the 2% target.

As for new Fed Chair Jerome Powell, well in golfing terms it felt like he struck it straight down the middle of the fairway. That’s to say that he largely gave away an impression of one of continuity under his new role as Chair, and an emphasis still on the Fed sticking with its gradual approach to tightening. In other words, he didn’t appear like he was willing to deviate off the well beaten path and into the rough. Indeed, his tone was fairly balanced while he sought to down play the importance of the median dot plots as well as adding “there is no sense in the data that we’re on the cusp of an acceleration in inflation”.

Overall, DB’s Peter Hooper noted that the FOMC statement and Powell’s inaugural press conference were close to his expectations, marking a shift in a hawkish direction relative to December, although perhaps slightly less so than he had anticipated given recent Fed rhetoric. More specifically, he thought Powell’s debut performance was strong and highlighted that the Committee is likely going to need to see evidence that wage and price inflation are picking up meaningfully before becoming concerned about significant overheating associated with the tightening labour market. For more details, refer to Peter’s note.

As for markets then, as we noted at the top US Treasuries ended the day lower in yield across the curve with the 2y, 10y and 30y down -4.0bps, -1.3bps and -1.1bps respectively. However, they were down anywhere from -3.6bps to -5.1bps versus the intraday yield highs as the initial reaction was a spike higher, before that move was quickly reversed. Meanwhile the USD index closed -0.65% while equities also weakened and tumbled from their highs. The S&P 500 ended -0.18% after being up as much as +0.82% while there was similar price action for the Dow (-0.18%) and Nasdaq (-0.26%). In fairness early gains were helped by a rally for Oil (WTI +2.57%) while the ongoing alleged issues with users privacy at Facebook still seems unresolved so equity markets were certainly kept busy.

This morning, markets in Asia are a bit mixed with the Nikkei (+0.71%) and Kospi (+0.53%) up slightly while the Hang Seng (-0.49%), ASX 200 (-0.22%) and Shanghai Comp (-0.84%) are all down as we type. Treasuries have continued to firm with yields another basis point or so lower. News (Reuters) has emerged overnight that the US is a step closer to avoiding another government shutdown with the release of a $1.3tn spending draft bill to fund the government through September with more funds for border security, infrastructure and the military. The lower House may vote on the bill today, then followed by the Senate. Elsewhere, China’s PBOC has raised the rates it charges on reverse repo agreements by 5bps following the Fed’s rate hike, with the PBOC noting that the move is “in line with market expectations and a normal reaction the Fed’s rate hike”.

So, one central bank down and one to go with the Bank of England decision due out at 12pm GMT today. The consensus is for no change in policy while market pricing also assigns a low 16% probability of a hike. The bigger question is whether or not we see a more hawkish BoE centre in light of yesterday’s stronger than expected wages numbers. Indeed, pricing for a May hike is over 80% and our UK economists yesterday changed their view to a rate hike (from a hold) for two months’ time. Yesterday, weekly earnings were reported as rising one-tenth to +2.6% yoy in the three months to January, while the broader measure of earnings jumped to +2.8% yoy, beating consensus by two-tenths. In addition, yesterday we had the announcement that the NHS is lifting the pay cap on staff with a 6.5% salary increase agreed over three years.

Also on the cards today are the flash March PMIs from across the globe. This morning we’ve already had Japan’s manufacturing PMI which came in at 53.2 versus 54.1 last month. For Europe, the consensus expects a 0.3pt decline in the composite to 56.8 driven by a 0.5pt decline for the manufacturing print (to 58.1) and 0.2pt decline for the services reading to 56.0. Both Germany (-0.8pts to 59.8) and France (-0.4pts to 55.5) are expected to see declines in their manufacturing prints too. The US in the afternoon is expected to buck the trend with a 0.2pt increase expected at the manufacturing level.

Back to yesterday, unsurprisingly it was hard to keep the tariff debate fully out of the headlines. The WSJ reported that China is planning countermeasures against Trump’s tariffs with US agriculture exports on the list. Reuters headlines in the afternoon also suggested that the White House will today make its announcement over China intellectual-property violations with suggestions it will be around $50bn of tariffs, however more significant is that there may also be investment restrictions based on Lighthizer’s comments. So that will no doubt be a focus for markets today too.