GOLD: $1354.60 UP $4.60 (COMEX TO COMEX CLOSINGS)

Silver: $16.68 UP 11 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1353.50

silver: $16.70

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1348.40

NY PRICING AT THE EXACT SAME TIME: $1348.40

LONDON SECOND GOLD FIX 10 AM: $1352.40

NY PRICING AT THE EXACT SAME TIME. $1352.90

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR 31 FOR 3100 OZ

For silver:

MARCH

1 NOTICE(S) FILED TODAY FOR

5,000 OZ/

Total number of notices filed so far this month: 5307 for 26,535,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8110/OFFER $8,180: DOWN $495(morning)

Bitcoin: BID/ $7883/offer $7953: DOWN $716 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY SIZED 712 contracts from 216,910 RISING TO 217,622 DESPITE FRIDAY’S STRONG 19 CENT GAIN IN SILVER PRICING. WE OBVIOUSLY HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 710 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 710 CONTRACTS. WITH THE TRANSFER OF 710 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 710 CONTRACTS TRANSLATES INTO 3.55 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

40,580 CONTRACTS (FOR 18 TRADING DAYS TOTAL 40,580 CONTRACTS) OR 202.900 MILLION OZ: AVERAGE PER DAY: 2254 CONTRACTS OR 11.272 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 202.900 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 28.98% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 684.73 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A TINY SIZED GAIN IN COMEX OI SILVER COMEX OF 712 WITH THE 23 CENT RISE IN SILVER PRICE. HOWEVER, WE ALSO HAD A FAIR SIZED EFP ISSUANCE OF 710 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 710 EFP’S FOR THE MONTH OF MARCH WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A GOOD 1422 OI CONTRACTS i.e. 710 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 712 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 19 CENTS AND A CLOSING PRICE OF $16.59 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.088 BILLION TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

In gold, the open interest FELL BY A CONSIDERABLE SIZED 6122 CONTRACTS DOWN TO 564,301 DESPITE THE HUGE SIZED RISE IN PRICE IN FRIDAY’ TRADING ( GAIN OF $23.30). WE ARE NOW ENTERING THE LAST WEEK BEFORE FIRST DAY NOTICE OF AN ACTIVE GOLD COMEX CONTRACT MONTH AND HERE WE GENERALLY SEE A CONTRACTION AT THE COMEX WITH A CORRESPONDING HIGHER EFP ISSUED AND THAT IS WHAT WE GOT. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 17,571 CONTRACTS : APRIL SAW THE ISSUANCE OF 16,971 CONTRACTS, JUNE SAW THE ISSUANCE OF 600 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 564,301. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A STRONG OI GAIN IN CONTRACTS: 6,122 OI CONTRACTS DECREASED AT THE COMEX AND A HUGE SIZED 17,571 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 11,449 CONTRACTS OR 1,144,900 OZ =35.61 TONNES

FRIDAY, WE HAD 8031 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 182,802 CONTRACTS OR 18,280,200 OZ OR 568.58 TONNES (18 TRADING DAYS AND THUS AVERAGING: 10,155 EFP CONTRACTS PER TRADING DAY OR 1,015,500 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 18 TRADING DAYS IN TONNES: 568.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 568.58/2550 x 100% TONNES = 22.29% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1861.92 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX DESPITE THE STRONG RISE IN PRICE IN GOLD TRADING YESTERDAY ($23.30 GAIN). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 17,571 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 17,571 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 11,449 contracts ON THE TWO EXCHANGES:

17,571 CONTRACTS MOVE TO LONDON AND 6122 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 35.61 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $23.30 : NO CHANGE IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 850.54 tonnes.

SLV/

WITH SILVER UP 11 CENTS TODAY: NO CHANGE

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A TINY 712 contracts from 216,910 UP TO 217,622 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE STRONG RISE IN PRICE OF SILVER (19 CENTS WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 710 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 712 CONTRACTS TO THE 710 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1422 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 7.11 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE STRONG RISE IN SILVER PRICING FRIDAY (19 CENT RISE IN PRICE) . BUT WE ALSO HAD ANOTHER WEAK SIZED 710 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 19.60 POINTS OR 0.66% /Hang Sang CLOSED UP 239.48 POINTS OR 0.79% / The Nikkei closed UP 148.24/Australia’s all ordinaires CLOSED DOWN 0.46%/Chinese yuan (ONSHORE) closed UP at 6.2796/Oil UP to 65.78 dollars per barrel for WTI and 70.39 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2796 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2662 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS HAPPY TODAY (STRONGER CURRENCY AND GOOD CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED/STRONGER GLOBAL MARKET

3a)THAILAND/SOUTH KOREA/NORTH KOREA

South Korea

Both sides supposedly reach a trade deal yet nothing concrete on the red lines. South Korea did announce that they would lower the amount of steel entering the USA

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

Hours after the Petro Yuan contracts started to trade in Shanghai, supposedly the USA and China are said to be near a deal to avert a trade war

( zerohedge)

4. EUROPEAN AFFAIRS

European trading/European stocks enter correction mode//banks continually battered/Euro rises

(zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Sultan to be Erdogan announces a military incursion into Iraq threatening to take the Sinjar region home to many Kurds. He is also threatening Americans who hold positions in North west Syria (Manbij)

( zerohedge)

ii)Russia/USA

USA expels 60 Russian diplomats as well as closing the Seattle consulate due to their proximity to a naval base.

Europeans also expel Russians diplomats (see below)

( zerohedge)

This will surely get Russia very angry: the UK Government is now preparing to confiscate Russian capital of “dubious origin” It will now be difficult for Russian oligarchs to call London home

(zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

i)The Kiss of death

The new Petro yuan future oil contract started to trade last night and over 10 billion yuan (1.5 billion USA) traded in the first hour. The sellers of oil will then take their yuan and convert to gold. Gold will travel form London through Switzerland and onto Shanghai to complete the trade. This will no doubt cause a major default in the precious metal sector in London.

( zerohedge)

ii)A good commentary outlining the problems Russia is facing delivering natural gas through the Ukraine. You will recall that the Ukraine won a court battle against Russia’s Gazprom. The argument is basically about fees. Russia wants to bypass the Ukraine entirely through pipeline Nord Steam No 2 which will provide natural gas to Germany.

The west is totally against this pipeline as it would give too much power to Russia

(courtesy Paraskova/OilPrice.com)

(courtesy zero hedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Interesting, a West Virginia congressman introduces a gold back standard legislation

( Wall Street Journal/ Mooney/GATA)

10. USA stories which will influence the price of gold/silver

i)TRADING THIS MORNING: dollar dumps to 6 week lows as stocks rebound.

(zero hedge)

ii)Only words being offered by China and nothing concrete: the lower dollar sends a strong message that the uSA will be unsuccessful in getting China to lower its tariffs on autos etc. They may allow USA financial services to enter China but that will be of no use to the Americans.

( zerohedge)

iii)Friday night.

Trump is ready to expel dozens of Russian diplomats in response to the Skripal poisoning. The real announcement came Monday morning.

( zerohedge)

iv)Part I/David Stockman

( David Stockman)

v)SWAMP STORIES

a)McCabe tries to come clean but blows it with his “inaccuracies” caused by confusion and distraction

( zerohedge)

b)John Bolton ready to clean house

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:492,692 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 595,273 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY 712 CONTRACTS FROM 216,910 UP TO 217,622 DESPITE OUR STRONG 19 CENT RISE IN SILVER PRICING/ FRIDAY’). ALSO,WE WERE ALSO INFORMED THAT WE HAD 710 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3465. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1422 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 712 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 710 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 1422 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 30 contracts FALLING TO 80 contracts. We had 36 contracts filed YESTERDAY, so we GAINED 6 contracts or an additional 30,000 OZ will stand in this active delivery month of March

April LOST 14 contracts FALLING TO 403 .

The next big active delivery month for silver will be May and here the OI LOST 555 contracts DOWN to 151,257

We had 1 notice(s) filed for 5,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 26/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

477 contracts

(47700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

31 notices

3100 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (31) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (477 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 50,800 oz, the number of ounces standing in this nonactive month of MARCH (1.5800 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (31 x 100 oz or ounces + {(477)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 50,800 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 3 CONTRACTS OR AN ADDITIONAL 300 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

80,009.233

oz

SCOTIA

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

1

CONTRACT(S

(5,000 OZ)

|

| No of oz to be served (notices) |

79 contracts

(395,000 oz)

|

| Total monthly oz silver served (contracts) | 5344 contracts

(26,720,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) all others nil oz

total deposits today: nil oz

we had 1 withdrawals from the customer account;

i) Scotia; 80,009.23 oz

total withdrawals;80,009.23 oz

we had 0 adjustments

total dealer silver: 59.383 million

total dealer + customer silver: 258.923 million oz

The total number of notices filed today for the March. contract month is represented by 1 contract(s) FOR 5,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5344 x 5,000 oz = 26,720,000 oz to which we add the difference between the open interest for the front month of Mar. (80) and the number of notices served upon today (1 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5344(notices served so far)x 5000 oz + OI for front month of March(80) -number of notices served upon today (1)x 5000 oz equals 27,115,000 oz of silver standing for the March contract month.

We GAINED 6 contracts or 30,000 additional silver oz will stand for delivery at the comex

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 83,482 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 111,851 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 111,851 CONTRACTS EQUATES TO 592 MILLION OZ OR 84.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.89% (MARCH 26/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.78% to NAV (March 22/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.89%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.78%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.47%: NAV 13.92/TRADING 13.57//DISCOUNT 2.47.

END

And now the Gold inventory at the GLD/

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 26/2018/ Inventory rests tonight at 850.54 tonnes

*IN LAST 349 TRADING DAYS: 90.50 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 299 TRADING DAYS: A NET 65.80 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 26/2018: NO CHANGE IN SILVER INVENTORY

Inventory 318.069 million oz

end

6 Month MM GOFO 2.09/ and libor 6 month duration 2.45

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.09%

libor 2.45 FOR 6 MONTHS/

GOLD LENDING RATE: .36%

XXXXXXXX

12 Month MM GOFO

+ 2.45%

LIBOR FOR 12 MONTH DURATION: 2.67

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.22

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– London house prices falling at fastest pace since 2009

– Values fell by 2.6% in year through January

– London house prices likely to be weakest in UK over next five years

– Inflated prices make London property more exposed to economic and political shocks

– Worries over house prices are having a knock-on effect in wider economy

– Physical gold to act as much needed hedge against falling property prices

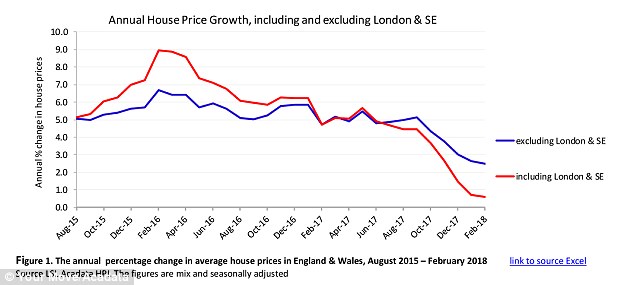

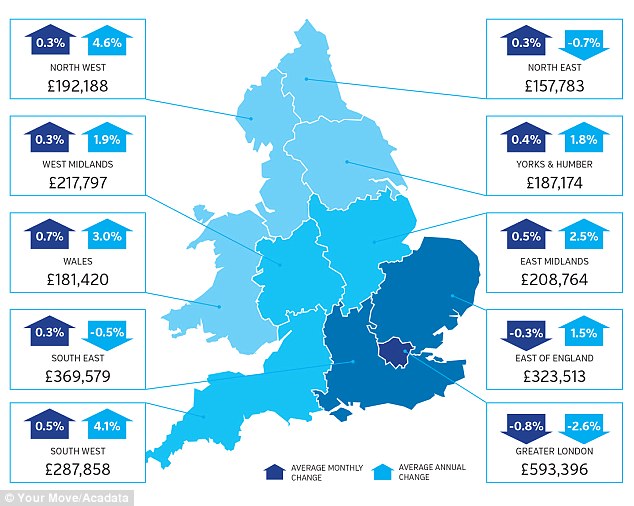

A new study by Acadata as covered by Bloomberg has found house prices in London are falling at their fastest pace since 2009. In the year through to January, London house prices have fallen by 2.6%. In the Greater London area they are down 0.8% in the last month alone.

Excluding London and the South West, annual house prices for the UK grew 2.5%. For estate agents this is a sign that the market is moving to meet the demands of buyers. For outsiders it may well look like the calm before the storm.

London feeling the pinch

Source: ONS

Source: ONS

London is the capital of the UK and has experienced significantly higher inflation than other areas when it comes to property prices. This means it is bound to be more vulnerable to both political and economic factors. But, these same factors will still apply to areas outside of London, the ripples just haven’t spread that far.

Demand in London has been dampened initially thanks to increased stamp duty, a tax change for landlords and loan limits in Singapore. But it is increased interest rates and the Brexit-effect that are having the greatest impact and will continue to do so over the long-run. This is particularly the case for Brexit, for as long as the outcome remains uncertain.

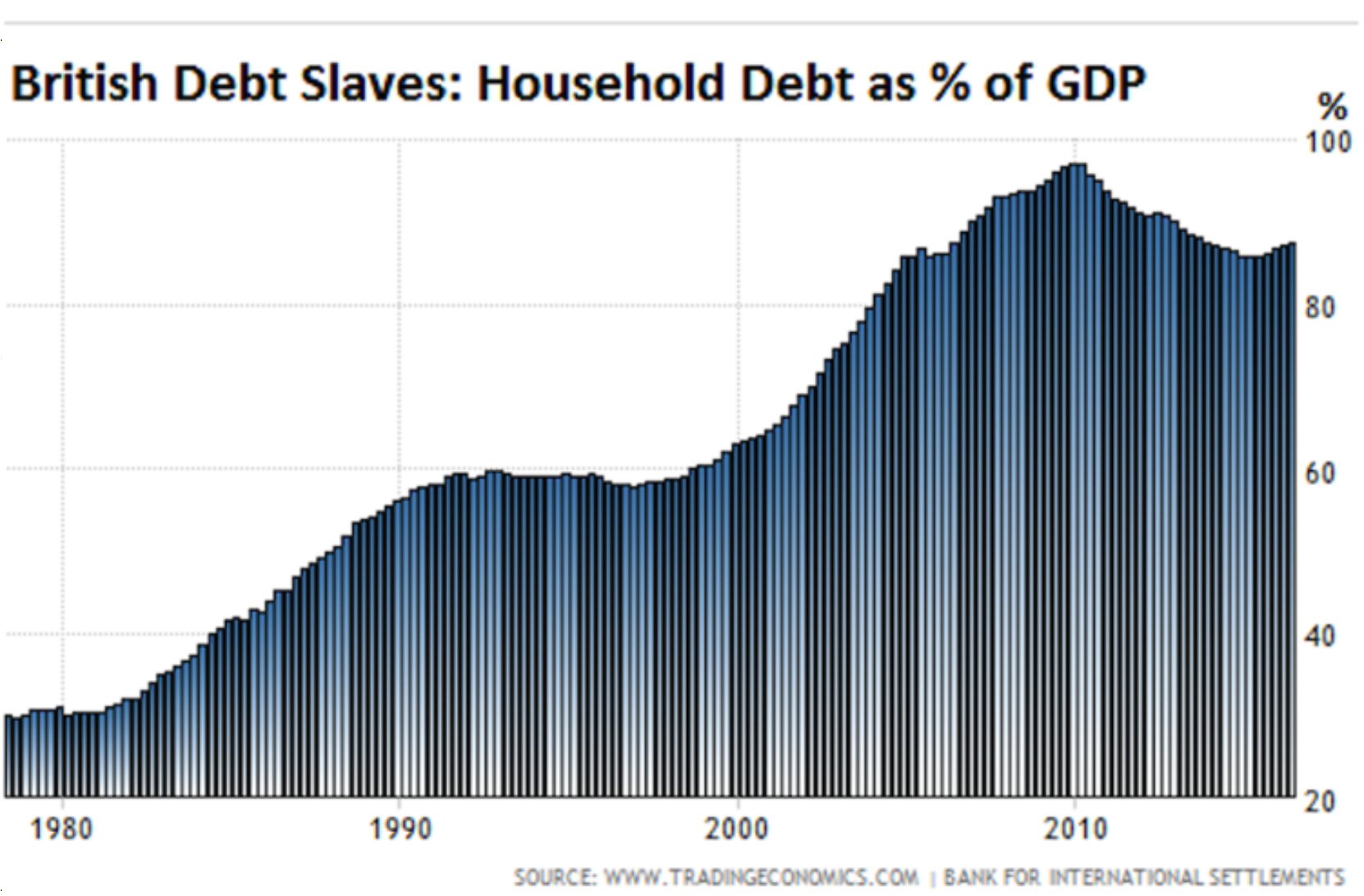

The UK’s obsession with house prices puts home owners in jeopardy when it comes to changes in both monetary and political. They are extremely exposed to the housing market which was worth a record £6.8trillion (3.7 times more than the country’s GDP) at the start of 2017. In 2001, the housing stock was worth just 1.6 times more than GDP.

Whilst the house price crunch is reportedly only happening in London and the outskirts, in the UK the repercussions are being felt everywhere. A report by Visa has found that last month consumer spending, fell for the ninth month in the last 10. This suggests that Brits are worried about a collapse in house prices.

We’re very proud of our house values here in the UK. There comes a huge ‘wealth effect’ from owning property; as property values rise so does spending and ultimately GDP. The impact of a declining wealth effect could be disastrous for the economy.

This seems strange given an increase in house prices is really quite meaningless when one thinks about it. You might be overjoyed that your family house has gone up 300% but what can you do about it? Increase the mortgage? Ok, so now you’re in more debt. Sell the house? Ok, but where will you live that hasn’t experienced a similar climb?

This is the myth that so many Brits fall for. The London data and spending figures suggests that soon many will be waking up to the scam they’ve all fallen for, realising the ‘wealth effect’ means very little when a major economic downturn is on its way.

The house price myth

Britons have been sold a big bottle of snake oil when it comes to property markets. Unlike our European contemporaries we are brought up from a very early age that owning our own home is a badge of honour, the seal of adulthood if you will.

This hasn’t always been the case. At the turn of the 20th Century just 23% of Brits owned their own home, fast forward over one hundred years and only 35% of us rent. This is in significant contrast to the likes of France where rental conditions mean many do not feel the need to do a deal with the devil that is a life time of debt. It is not surprising then to learn that Britons are amongst the most indebted in Europe, so sure are we that agreeing to many hundreds of thousands of pounds in debt is the right thing to do.

We are, according to Wolf Richter, the eighth most indebted country in the world when it comes to household debt. As Richter points out, all of those in the top ten are ‘The countries with highly indebted households, so the top of the list, are mostly countries were central-bank policy rates are very low or even negative, and where mortgage rates are super low.’

A 2017 report by the National Institute of Economic and Social Research found that our obsession with owning our own property is costing us our future wealth security. It concluded that mortgage holders should expect their private pension income to be around 15% per year lower than it should be.

Given the increase in housing stock value relative to GDP it is clear the reliance the British economy and public have on the property market. The wealth effect generated from higher house prices is something that is pumped up by politicians, incredibly irresponsibly.

The fall in London house prices is likely a warning shot before prices begin to fall elsewhere. Policy makers and the government should pay close attention. This will prove to be a lesson in how pumped up asset prices and low interest rates are no way to support a growing economy.

How can you hedge your own home?

Reading this is should do more than just provide you with good fodder for the next dinner party conversation. It should be making you realise how exposed the British economy is to falling house prices.

A fall in prices does not just mean that property is finally affordable. It means thousands of people will face negative equity, industries such as home builders will collapse and consumer spending will fall. All this against a backdrop of increased interest rates, rising inflation and uncertainty over Brexit.

Usually one might consider selling a depreciating asset but that’s impossible when it’s your home. And don’t think you’re in the clear if you rent or have other arrangements. Exposure to a potential property crisis does not just come about if you own or rent a property.

All investors, savers and consumers are exposed, as we all have dependencies on the UK banking, financial and economic systems. All of which will be vulnerable as prices fall.

Luckily, gold will likely act as a hedge against falling asset prices. It’s lack of correlation to other assets and counter cyclical nature, should see it again act as a good hedge in a downturn or indeed a much-dreaded property crash.

This won’t happen tomorrow, so you have time to diversify and decide on a reasonable allocation to gold bullion. When choosing to invest in bullion choose to own physical gold coins and bars held in allocated and segregated storage in safer, less economically uncertain jurisdictions. The tax treatment of different types of gold investment should also be considered as certain formats can be capital gains tax (CGT) free, making them much more attractive to companies, investors and pension owners.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related reading

London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

Brexit Risks Increase – London Property Market and Pound Vulnerable

London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

London Property Crash Looms As Prices Drop To 2 1/2 Year Low

News and Commentary

Gold hits 5-week high on global trade war fears (Reuters.com)

U.S., China said to be talking behind the scene to avoid trade war (MarketWatch.com)

Asian markets continue to pull back amid trade-war fears (MarketWatch.com)

Death knell tolls for the euro as more European nations repatriate gold – expert to RT (RT.com)

Here’s why the Dow tumbled on the threat of a trade war (MarketWatch.com)

Source: MarketWatch

A Stunning Silver COT Report: One For the Ages (GoldSeek.com)

Central Bank Money Rules the World (DailyReckoning.com)

The 2017 Stock-Market Rally Minted 700,000 New American Millionaires (ZeroHedge.com)

Silver Speculators Have Never Been This Short (DollarCollapse.com)

The performance of gold before and after Fed rate hikes, in one table (BusinessInsider.com)

Gold Prices (LBMA AM)

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

21 Mar: USD 1,316.35, GBP 935.53 & EUR 1,071.64 per ounce

20 Mar: USD 1,312.75, GBP 935.60 & EUR 1,066.22 per ounce

19 Mar: USD 1,311.70, GBP 934.59 & EUR 1,066.41 per ounce

16 Mar: USD 1,320.05, GBP 945.42 & EUR 1,071.09 per ounce

Silver Prices (LBMA)

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

21 Mar: USD 16.25, GBP 11.56 & EUR 13.23 per ounce

20 Mar: USD 16.25, GBP 11.60 & EUR 13.22 per ounce

19 Mar: USD 16.29, GBP 11.59 & EUR 13.24 per ounce

16 Mar: USD 16.48, GBP 11.79 & EUR 13.36 per ounce

Recent Market Updates

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Crock Of Gold Hidden In Ireland? Happy Saint Patrick’s Day

– Buy Silver And Sell Gold Now

– Stephen Hawking – Doomsday Prophet’s Top Five Predictions

– Gold Cup At Cheltenham – Gold Is For Winners, Not For the Gamblers

– Hungary’s Gold Repatriation Adds To Growing Protest Against US Dollar Hegemony

– Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

– Gold Protects As Cashless Society Threatens Vulnerable

– Women’s Pension Crisis Highlights Dangers To Savers

– London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

end

Interesting, a West Virginia congressman introduces a gold back standard legislation

(courtesy Wall Street Journal/ Mooney/GATA)

West Virginia congressman introduces gold standard legislation …

Submitted by cpowell on Mon, 2018-03-26 01:08. Section: Daily Dispatches

… and The Wall Street Journal actually lets him publicize it.

* * *

Steel and Aluminum? Let’s Talk About Gold

How Fiat Money Hurts My West Virginia Constituents

By U.S. Rep. Alex X. Mooney

The Wall Street Journal

Sunday, March 25, 2018

https://www.wsj.com/articles/steel-and-aluminum-lets-talk-about-gold-152…

I believe in free trade, but I still understand why President Trump is imposing tariffs on steel, aluminum and a range of Chinese products. America’s industrial workers have suffered for a long time, and Mr. Trump is fighting to create middle-class jobs.

Achieving that will take more than righting the last administration’s wrongs on taxes and regulation, a task already well under way. Blue-collar prosperity was eroded along with American manufacturing. From 2000-10, U.S. manufacturing employment shrank by a third after holding steady for 30 years.

President Trump has rightly blamed bad trade deals, particularly those with Mexico and China, for contributing to this meltdown. But the Federal Reserve deserves a share of the blame, too, since its inflationary policies priced out U.S. manufacturers from global trade. Since 2000, their prices have risen nearly 50%, compared with about 25% for German competitors — mirroring the domestic inflation rates in each country. As a result, manufacturers fled the U.S., much the way American families have fled high-tax states.

The solution is to take control of the money supply away from the Fed and give it back to the American people—in other words, to return to the gold standard. Gold gets a bad rap in some history books because of its misuse during the 20th century. This ignores its peacetime record of high growth and nil inflation between 1834 and 1913.

Clouding the historical picture are two fake gold standards. The Depression-era gold standard was constructed to make prices fall toward the levels that prevailed before World War I, with the disastrous result of deflation. Then, under the Bretton Woods version after World War II, only foreign central banks could convert dollars into gold. This deformity caused inflation, which skyrocketed after the Fed gained total control of the money supply in the early 1970s.

Since then the U.S. has seesawed between too much and too little money in the economy. The Fed has the impossible task of guessing the market’s demand in real time. Its performance worsened in the 2000s because the Fed began to grade itself by how its money creation boosted the financial markets. Today many people are so disillusioned with the dollar’s prospects that they have embraced cryptocurrencies like bitcoin.

My constituents in West Virginia get little of the upside from the Fed’s money creation and most of the downside. They don’t benefit from speculative investment returns, but they do lose their jobs and homes when the local plant decides to close because it’s too expensive to compete from the U.S.

The current Federal Reserve system benefits elites. The gold standard is equitable and puts “we the people” in control of the money supply. That’s why it was part of America’s founding and has been a key to the country’s long economic success.

On Thursday I introduced a bill that would return the dollar to the gold standard—the first such attempt since Jack Kemp’s Gold Standard Act of 1984. Under this legislation the Fed would still exist, but it would administer the money supply rather than dictate it. Instead the market would be in charge, the supply and demand for money would match up, and prices would be shaped by economics rather than the instincts of bureaucrats.

Like President Trump, I believe that success is again possible for Americans who go to work every day and build things. Mr. Trump’s vision of how the American economy could and should work resonated with voters in 2016. Returning to the gold standard is a way for the president to deliver on his promise of American working-class prosperity.

—–

Mr. Mooney, a Republican, represents West Virginia’s Second Congressional District.

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.2796 /shanghai bourse CLOSED DOWN 19.60 POINTS OR 0.66% / HANG SANG CLOSED UP 239.48 POINTS OR 0.79%

2. Nikkei closed UP 148.24 POINTS OR 0.72% /USA: YEN RISES TO 105.12/

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 89.67/Euro RISES TO 1.2338

3b Japan 10 year bond yield: FALLS TO . +.024/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.12/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.78 and Brent: 70.39

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.539%/Italian 10 yr bond yield UP to 1.913% /SPAIN 10 YR BOND YIELD DOWN TO 1.272%

3j Greek 10 year bond yield FALLS TO : 4.394?????????????????

3k Gold at $1348.40 silver at:16.63 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 46/100 in roubles/dollar) 56.84

3m oil into the 65 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.12 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.94758as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1774 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.539%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.841% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.085% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Soar, Global Stocks Rebound As Trade War “Perfect Storm” Fears Fade

It seems that “Black Monday” has been averted, with global risk sentiment making a full reversal to start the week, and the precipitous selloff from Thursday and (Black) Friday turning into a furious rally on Monday, starting in Asian markets and proceeding to Europe and US stock futures, which are up 1.4%, and back over the key 2,610 support level.

In other words, once again the 200DMA at 2,585 has proven a key support for the S&P500.

“It was the week when one bad thing led to another, it was a perfect storm,” said Jim Paulsen, chief investment strategist at Leuthold Weeden Capital Management. “You took the starch out of the FANGs, you saw banks, industrials, discretionary companies reacting to negative news. What investors are not pricing in is a potential impact on companies’ profit margins.”

On Monday, the perfect storm had faded, although it remained to be seen if this was just the eye of the hurricane.

What prompted the surge: the most commonly cited reason is that jitters over brewing trade tensions between the U.S. and China have again eased, after Treasury Secretary Steven Mnuchin told Fox News that he’s “cautiously hopeful” the U.S. can reach a trade deal with China that will avert the need for Trump to impose up to $60BN in tariffs on China – of course, what else would he say?

There was also renewed optimism that the United States and China are set to begin negotiations on trade, following reports in both the FT and WSJ, further easing fears about a trade war between the world’s two largest economies. MSCI’s world equity index turned positive on the day, having earlier hit its lowest level since February 9, after a Wall Street Journal report that Treasury Secretary Mnuchin was considering a visit to Beijing to begin negotiations.

“I don’t think that long-term the tariffs will continue to be enforced,” Scot Lance, managing director at California-based Titus Wealth Management, said by phone. “They’ll pull them off the table at some point, I just don’t know if that will be a week, a month, a quarter? Could it last a whole year? I don’t necessarily think it’ll last for a long time.”

All of the uncertainty has kept the once-reliable dip buyers on the sidelines this time. Consider: as Bloomberg notes, the S&P 500 has closed lower than the midpoint of its daily range for 10 straight days, the longest stretch since at least 1982. That suggests traders are finding reasons to dump shares in the afternoon rather than buy dips.

That sentiment may have reversed this morning, however: “It appears that the market is not expecting a full-blown trade war, and a currency war for competitive advantage is not a likely option at this moment,” said Mizuho’s Ken Cheung, who will clearly retract and say the opposite should futures reverse their gain and slump. “Risk sentiment, as being reflected by Asian equities, and further responses from the Chinese authorities to the trade war will drive the market.”

Also overnight, as we reported previously, the U.S. and South Korea reached an agreement on revising their trade deal, with South Korea avoiding steel tariff, which was also to be expected, as the target of Trump’s trade war – it has become especially obvious by now – is not Europe, and not all of Asia, but simply China. As a result, S&P futures are sharply higher in early trade, and the S&P trying to undo all of its 2.1% losses from Friday, although it may have a harder time to offset last week’s 6% loss, which was the biggest weekly drop since early 2016.

European shares headed for their first gain in four days as investors assess the latest developments in a trade conflict between the world’s two largest economies. European bourses are higher across the board (Eurostoxx +0.4%) with the exception of the FTSE MIB (-0.3%), shrugging off Friday’s negative sentiment. Sectors are making broad gains, healthcare is outperforming after a positive drug update from Roche (+1.6%) and energy is underpinned despite slightly softer oil prices.

Asian markets also stabilized, with the ASX 200 down -0.5% led lower by its largest-weighted financials sector after the harsher losses seen in its US counterparts, while the Nikkei 225 fell to a near 6-month low, before staging a late rally back into positive territory, closing 0.6% higher after dropping -1.3%. Elsewhere, Shanghai the Shanghai Composite dropped -0.6%, weighed by trade tensions and rising Chinese money market rates (HKD 12-month HIBOR at 9-year high), while the KOSPI (+0.8%) bucked the trend after news that US and South Korea agreed in principal to a revised FTA and with South Korea to be exempted from US tariffs.

In macro and FX, the risk on sentiment sent the yen sliding from a 16-month high as calm returned, if only for the time being, to world markets amid signs U.S.-China trade frictions may be easing. The USD/JPY rose 0.3% to 105.10 after earlier falling to 104.56, lowest since November 2016.

“Risk aversion seems to have come a full circle with the first reaction to U.S.-China trade tensions last week, and it may be difficult to buy up the yen further without additional negative factors,” said Koji Fukaya, CEO at FPG Securities.

On the other side, Daisuke Karakama, chief market economist at Mizuho Bank in Tokyo said that “markets are now in the phase of waiting for Nikkei stock average to fall below 20,000 and USD/JPY to drop towards 100, so it’s meaningless to give specific projections before those levels.”

Meanwhile, bond markets this week will see another deluge of issuance, and bond traders will be tested this week as the Treasury will auction about $294 billion of bills and notes, the largest slate of supply ever. China last week did not rule out scaling back its purchases of U.S. debt as part of its response to proposed tariffs. The 10-year yield held near 2.84%.

Concerns over the formation of a new anti-establishment government in Italy weighed on Southern European debt on Monday, though this was counterbalanced to an extent by a ratings upgrade for Spain late on Friday. Italian bonds underperformed, with 10-year yields rising as much as 4.5 basis points in early trade, on further signs the anti-establishment 5-Star Movement and the anti-migrant League might explore an alliance to form a government. But the euro was still on a positive trajectory, hitting a 10-day high of $1.2393 at one stage.

In commodities, international Brent crude futures opened above $70 per barrel for the first time since January but the gains could not be sustained as the ongoing trade disputes weighed on global markets. Spot gold had hit five-week highs early but turned negative as the session wore on and was marginally lower on the day at $1,345.

In M&A, Smurfit Kappa rejected International Paper’s revised takeover bid, while the U.K.’s JD Sports Fashion agreed to buy Finish Line in a $558 million deal. Red Hat and Paychex are among companies reporting earnings today.

Bulletin Headline Summary from RanSquawk

- European bourses shrug off trade concerns with China looking to step up efforts in trade negotiations with the US

- A softer USD has seen EUR/USD and GBP/USD reclaim 1.2400 and 1.4200 to the upside respectively

- Looking ahead, highlights include ECB’s Weidmann, Fed’s Dudley and Mester

Market Snapshot

- S&P 500 futures up 1.35% to 2,632.50

- MSCI Asia Pac up 0.4% to 172.60

- MSCI Asia Pac ex Japan up 0.5% to 567.49

- Nikkei up 0.7% to 20,766.10

- Topix up 0.4% to 1,671.32

- Hang Seng Index up 0.8% to 30,548.77

- Shanghai Composite down 0.6% to 3,133.72

- Sensex up 1% to 32,924.47

- Australia S&P/ASX 200 down 0.5% to 5,790.47

- Kospi up 0.8% to 2,437.08

- STOXX Europe 600 up 0.4% to 367.17

- German 10Y yield rose 0.9 bps to 0.536%

- Euro up 0.3% to $1.2388

- Italian 10Y yield fell 0.9 bps to 1.622%

- Spanish 10Y yield fell 1.0 bps to 1.259%

- Brent Futures down 0.2% to $70.30/bbl

- Gold spot little changed at $1,347.94

- U.S. Dollar Index down 0.2% to 89.28

Top Overnight News

- China and the U.S. are said to quietly have started negotiating to improve U.S. access to Chinese markets, the WSJ reported, with talks being led by Chinese President Xi Jinping’s top economic aide, Liu He, U.S. Treasury Secretary Steven Mnuchin, and U.S. trade representative Robert Lighthizer

- Mnuchin says he is ‘hopeful’ that a truce can be reached with China on trade; WSJ reports that China and U.S. quietly started negotiating to improve U.S. access to Chinese markets, according to sources

- China is conducting research on second and third lists of U.S. imports subject to the tariffs, China Daily reports; likely to cover airplanes, computer chips and tourism industry

- SF Fed’s Williams is the leading candidate to become next president of the Federal Reserve Bank of New York, WSJ reports, citing sources

- Italy’s Northern League leader Salvini says that he’s ready to start govt. talks with everyone including Five Star

- Trump is preparing to expel dozens of Russian diplomats from the U.S. in response to the nerve-agent poisoning of a former Russian spy in the U.K; likely to be announced today according to people familiar

- Guo Shuqing, a high-profile banking regulator and ally of Jinping in cleaning up the financial system, is said to have been appointed as Communist Party secretary of the People’s Bank of China

- China launched its first ever crude-futures contract as the world’s biggest oil buyer seeks to wield greater power over pricing and challenge benchmarks in the U.S. and Europe

- New Zealand’s central bank agreed to target maximum employment alongside price stability in anticipation of a dual mandate being enshrined in law later this year

- League leader Matteo Salvini said he would start talks with Luigi Di Maio of the anti-establishment Five Star Movement and other party leaders on forming Italy’s next government, with pension reform, tax cuts and curbs on immigration as his priorities

- U.S. President Donald Trump is poised to take his most aggressive actions yet against Russia on Monday, when he’s likely to announce the expulsion of dozens of diplomats in response to the nerve-gas attack on a former Russian spy living in the U.K.

Asian stocks began the week mostly negative as trade concerns remained at the forefront of market focus and following last week’s losses on Wall St where stocks posted their worst weekly performance in over 2 years and the DJIA slipped into correction territory. ASX 200 (-0.5%) was negative with the index led lower by its largest-weighted financials sector after the harsher losses seen in its US counterparts, while Nikkei 225 (+0.6%) fell to a near 6-month low, before staging a late rally back into positive territory. Elsewhere, Shanghai Comp. (-0.6%) was weighed by trade tensions and rising Chinese money market rates (HKD 12-month HIBOR at 9-year high), while KOSPI (+0.8%) bucked the trend after news that US and South Korea agreed in principal to a revised FTA and with South Korea to be exempted from US tariffs. Finally, 10yr JGBs were subdued as prices failed to benefit from a risk-averse tone with demand dampened amid a lack of Rinban announcement by the BoJ, while a tier-1 US firm was said to be

cautious on 2yr JGBs amid expectations for an increase in auction supply.

Top Asian News

- The Builder of One of the World’s Largest Airports Revives IPO

- TPG Said to Near Deal for $1.2 Billion Indian Hospital Chain

- In Xi’s China Even the Central Bank Has a Party Boss at the Helm

- Thailand’s Red Bull Rival Slumps From Top to Bottom of World

European equities are higher across the board (Eurostoxx +0.3%) with the exception of the FTSE MIB (-0.3%), shrugging off the negative sentiment on Wall Street and Asia dictated by looming trade disputes between China and the US. Sectors are making broad gains, healthcare is outperforming after a positive drug update from Roche (+1.6%) and energy is underpinned despite slightly softer oil prices. In terms of individual movers, Fresnillo (+5.5%) is the outperformer in the FTSE100 after an upgrade from Goldman Sachs whereas Smurfit Kappa (-4.3%) is the laggard following its refusal of the takeover offer from International Paper.

Top European News

- Catalan Separatists Face Reality Check After Puigdemont Detained

- Givaudan Taps Organic Food Trend With $1.6 Billion Naturex Deal

- Murray & Roberts Jumps by Record on Unsolicited Takeover Bid

In FX, Nzd/Usd nudging back up towards the 0.7300 level on a surprise NZ trade surplus and broader uptick in risk sentiment overnight as global trade war fears wane somewhat, with market contacts also reporting some decent buy orders in Nzd/Jpy as Usd/Jpy bounces off new recent lows not far off 104.50 to just over 105.00. Note, however, the headline pair has been capped amidst hefty option expiry interest at the big figure today and on Tuesday (around 2.5 bn in total). Aud/Usd is back above 0.7700 and approaching 0.7750 despite a couple of short trades of the week via crosses (vs Jpy and Cad), while Cable has breached the 1.4200 level on a mixture of hawkish BoE impulses and Brexit transition deal optimism. On that note, contacts also note some stopsales in Eur/Gbp from circa 0.8730 to 0.8723, which is the low of the range up to 0.8743. Nevertheless, Eur/Usd remains firm and has popped above 1.2400 on extended gains from trend-line support (1.2349) and its 30 DMA (1.2337). Usd/Cad looking at bids near and under 1.2850 amidst a broadly soft Greenback as the DXY remains sub-89.500 and trade/protectionism concerns continue to weigh.

In commodities, oil futures are modestly lower, albeit remaining in close proximity to recent highs, as price action is centred around China with WTI crude futures failing to hold above USD 66/bbl with demand sapped as the debut of CNY-denominated oil futures contracts stole the limelight and rose 6% in early trade. In the metals bloc, gold is range-bound at around 5-week highs as a subdued greenback and risk-averse tone kept the safe-haven afloat, while copper weakened alongside losses in Chinese metals prices in which Shanghai Rebar dropped to its lowest since July.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0.2, prior 0.1

- 10:30am: Dallas Fed Manf. Activity, est. 33.5, prior 37.2

- 12:30pm: Fed’s Dudley Speaks on the Future of Financial Regulation

- 4:30pm: Fed’s Mester Speaks on Monetary Policy

- 7:10pm: Fed’s Quarles to Speak in Atlanta

DB’s Jim Reid concludes the overnight wrap

Well that was a week that most won’t forget in a hurry. For anyone that was lucky enough to escape to a desert island last week, switched your phone off and only returned this morning then this is a 125-word summary of what you’ve missed:

The seeds for the opening salvo of a trade war appear to have now been sown with President Trump and China trading blows, and it feels like it’s only the start with China signaling a willingness to go toe-to-toe. This transpired in a week in which the Fed showed that it remained committed to staying on a gradual rate hike course, concerns that global growth could be starting to roll over following the latest flash PMIs, the centre of the bull market – the tech sector – roiled by data leakage accusations at the hands of Facebook, and finally the White House revolving door continuing with the appointment of John Bolton – a man who had strongly supported an invasion of Iraq – as the national security advisor.

That perfect storm of events resulted in some of the worst weeks for risk assets in years. Using the S&P 500 as an example, the index fell -5.95% last week, the biggest weekly decline since January 2016. Every sector closed lower so there was nowhere to hide although tech fell a fairly staggering -7.88%. The broader index is now easily in the red again for the year (-3.19%) and it also means that we have seen three separate 5% dips for the index in the last two months. What perhaps stood out the most about the price action last week was that any buy the dip mentality appeared to just disappear. In fact, that has been the case for the last two weeks with the S&P closing lower than the midpoint of its intraday range every single day. That’s the longest streak since at least 1982.

Across other markets, the Nasdaq 100 – which bore the brunt of the Facebook news – fell -7.29% and the most since August 2015. The export heavy Nikkei and DAX fell -4.88% and -4.06% respectively. The Shanghai Comp was down -3.58%. Indeed, it’s now difficult to find a market which is positive YTD, although the FTSE MIB is one which can still just claim that. Meanwhile, it might not have been the volatility spike of early February but the VIX still rose over 9pts last week and closed just below 25 on Friday which is the highest since February 13th. Remember that the VIX average through the whole of 2017 was about 11. Elsewhere, credit certainly wasn’t immune. Moves for CDS indices are complicated by the rolls however CDX IG was still 15bps wider last week and is now at the widest since December 2016, while iTraxx Main and Crossover were 12bps and 41bps wider last week, respectively. Cash European and US high yield spreads were 21bps and 14bps wider.

Given all the above, you might have thought that Treasury yields would be markedly lower. However, 10y yields were just 3bps lower last week having closed at 2.814%, and in fact they have closed with a 2.8% handle for 21 straight days which is fairly remarkable all things considered. Bunds were ‘only’ 4bps lower last week however it’s worth noting that they are now 24bps off their YTD yield highs.

Unsurprisingly, the weekend news flow is filled with reaction to last week’s trade war developments. China’s Vice Premier Liu He, following a phone call with US Treasury Secretary Steven Mnuchin, said that “China is prepared and has the ability to defend its national interests”. China has also suggested that it may issue an official complaint to the WTO about Trump’s steel and aluminum tariffs, with China not exempt from the levies. Remember that Trump has already threatened to remove the US from the WTO. Interestingly, Mnuchin has also been reported as saying that he is hopeful that the US and China can come to an agreement that will “forestall the need to impose the tariff’s that Trump has ordered on at least $50bn of goods” according to Bloomberg. The article quotes an interview Mnuchin had with Fox News, with the Treasury Secretary also quoted as saying that the US will proceed with the tariffs “unless we have an acceptable agreement that the President signs off on”. So perhaps some signs of a softening stance.

This morning, the US and South Korea have reached an agreement on the principles of amending their bilateral trade deal, which includes the US permanently exempting South Korea from the steel tariffs. In return, South Korea will set quotas for steel exports to the US and will be more flexible on imposing safety / environment regulations on US made cars. In Asia, the Kospi is up +0.34% while other bourses have pared back steeper losses with the Nikkei (-0.33%), Hang Seng (-0.57%), ASX 200 (-0.45%) and Shanghai Comp. (-1.64%) all down as we type. There’s better news for US equity futures with the S&P 500 currently up +0.55%, while Treasury yields are also up close to 2bps.

There’s also been some non-tariff talk over the weekend with the newly appointed PBOC Governor Yi noting that China has three major tasks for the financial system – “i) implement prudent monetary policy, ii) push forward financial reforms and opening up and iii) win the battle against financial risks”. He added that the “opening up of the financial sector must be accompanied by the development of financial regulations” and it will proceed in coordination with reforms in China’s FX rate mechanism and capital account convertibility. Elsewhere, the WSJ has reported John Williams is the front runner to succeed William Dudley as the Head of the NY Fed.

So, while it’s hard to see anything other than trade war developments really dominating markets this week, it’s worth noting that we do also have some inflation data due out in the holiday-shortened four days ahead. Specifically, Thursday’s PCE report in the US is scheduled. In terms of what to expect, the consensus is for a +0.2% mom core and deflator reading for February. The former would imply a jump of one-tenth in the annual rate to +1.6% yoy. Our economists also expect a +0.2% core print and they note that the report should take on a little more focus given the recent upgrade in the Fed’s forecast to above 2% core PCE for 2019. As a reminder too, the March data is when we see the wireless services print annualized which should add about 20bps and 10bps to the annual core CPI and PCE prints, respectively.

Away from that we also have some flash March CPI data due in Europe this week with Germany on Thursday and France and Italy both reporting on Friday. Other than that, there is a decent flow of Fedspeak this week which if anything could help shape where FOMC participants’ median dots are now. Dudley (neutral) and Mester (hawk) kick things off today, followed by Quarles (neutral) and Bostic (neutral) on Tuesday, Bostic again on Wednesday and then Harker (dove) on Thursday. So expect the market to be looking out for where their rate expectations lie.

Quickly recapping Friday, in terms of central bankers speak, the Fed’s Bostic and Kaplan both noted their base case was three rate hikes for this year (i.e. 2 more), but are “open minded and we’ll see how the year unfolds”. Elsewhere, the Fed’s Kashkari noted he supports the recent rate hike because it “represented continuity” at Powell’s first meeting, but added that the data does not support a rate hike at this point. In the UK, BOE’s Vlieghe noted “the current central outlook is….consistent with one or two 25bp rate increase per year over the forecast period”.

Datawise, in the US, the February core durable goods orders (+1.2% mom vs. +0.5% expected) and core capital goods orders (+1.8% mom vs. +0.9% expected) were both above consensus. The February new home sales print fell -0.6% mom to 618k (vs. 620k expected) while the final reading for France’s 4Q wages growth was slightly higher at +0.2% qoq (vs. +0.1% expected).

end

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 19.60 POINTS OR 0.66% /Hang Sang CLOSED UP 239.48 POINTS OR 0.79% / The Nikkei closed UP 148.24/Australia’s all ordinaires CLOSED DOWN 0.46%/Chinese yuan (ONSHORE) closed UP at 6.2796/Oil UP to 65.78 dollars per barrel for WTI and 70.39 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED UP AT 6.2796 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.2662 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS HAPPY TODAY (STRONGER CURRENCY AND GOOD CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED/STRONGER GLOBAL MARKETS )

3 a NORTH KOREA/USA

/SOUTH KOREA/USA

Both sides supposedly reach a trade deal yet nothing concrete on the red lines. South Korea did announce that they would lower the amount of steel entering the USA

(courtesy zerohedge)

US Reaches Trade Deal With South Korea; Mnuchin “Hopeful” Of Trade Truce With China

In some welcome news amid escalating global trade war fears, on Sunday the U.S. and South Korea reached an agreement on revising the existing 6-year-old bilateral trade deal as well as Trump’s plan to impose tariffs on steel imports, Treasury Secretary Steven Mnuchin said.

Speaking on Fox News Sunday, Mnuchin said U.S. Trade Representative Robert Lighthizer reached “a very productive understanding” with South Korea on the tariffs to reduce imports and the existing trade deal known as Korus, and added that he expects “to sign that agreement soon.” The resolution means that the US now has tariff exemptions with the EU, Australia, Brazil, Argentina, and South Korea.

As a result of the agreement, which he called “an absolute win-win”, South Korea “will reduce the amount of steel that they send into the United States.”

South Korea – the world’s 7th largest export economy, whose exports amount to a whopping 45% of GDP – had a trade surplus with the U.S. of about $18 billion in 2017, down from $23 billion in 2016, with cars accounting for more than 70% of the value of the surplus.

Bloomberg adds that S.Korea Trade Minister Kim Hyun-chong also said trade negotiators from the two countries agreed “in principle” on both issues. Oddly, Kim said South Korea made no concessions to further open its agricultural market to U.S. exporters – something he described as a red line. He also said that there’s been “no retreat” on tariffs removed in Korus, which is strange because somehow the two sides are said to have reached a compromise, yet neither admits to “retreating” on policy issues.

Previously, frictions over Korus emerged when Trump blamed the U.S.’s large trade deficit with South Korea on the “horrible” agreement, and as a result, the open issue has been seen as a potential wedge between the allies as both their leaders plan for expected meetings with North Korean leader Kim Jong Un.

The Trade Ministry said Kim will brief on the outcome of the trade negotiation to media Monday morning.

* * *

Separately, Mnuchin also said he’s optimistic that the U.S. can reach a agreement with China that will eliminate the need to impose the tariffs that Trump ordered on a least $50 billion of goods from that country. “We’re having very productive conversations with them,” Mnuchin also told Fox on Sunday. “I’m cautiously hopeful we reach an agreement.”

A day after Trump’s announcement, China unveiled $3 billion in tariffs on U.S. imports in response to steel and aluminum duties ordered by Trump earlier this month. While the retaliation appeared modest, as we reported on Friday citing the editor in chief of China’s state owned Global Times, that $3 billion was in response to the previous, Section 232 round of tariffs, and had nothing to do with the latest round of $50BN in Section 301 tariffs.

I learned that Chinese govt is determined to strike back. Friday’s plan to impose $3b tariffs is to retaliate tariffs on steel and aluminum products. China’s retaliation lists against the 301 investigation will target US products worth $ tens of billions. It is in the making.

I learned that Chinese govt is determined to strike back. Friday’s plan to impose $3b tariffs is to retaliate tariffs on steel and aluminum products. China’s retaliation lists against the 301 investigation will target US products worth $ tens of billions. It is in the making.

And while we still wait what China’s full-blown response will be to the “301” sanctions, the White House also declared a temporary exemption for the European Union and other nations on those levies, making the focus on China clear.

The U.S. will proceed with tariffs “unless we have an acceptable agreement that the president signs off on” Mnuchin said, adding that “we’re not afraid of a trade war, but that’s not our objective. In a negotiation you have to be prepared to take action.”

Meanwhile, in the latest not so veiled threat, on Saturday the People’s Daily newspaper on Saturday listed U.S. companies that’d be “most damaged” if a trade war began, and included Apple, Intel and Boeing. Should there be no immediate resolution to the China-US trade war, look for these three companies to take the brunt of the market pain in the coming week.

And sure enough, Apple’s Tim Cook – who coincidentally was in a forum in Beijing on Saturday – said he’s going to encourage that “calm heads prevail” on the potential trade war. China is Apple’s single most important market outside the U.S. “The countries that embrace openness do exceptional and the countries that don’t, don’t,” he said. “It’s not a matter of carving things up between sides.” And, if it is, it will be Apple that will be among the companies most impacted as a result of its massive trans-Pacific supply chains.

3 b JAPAN AFFAIRS

END

c) REPORT ON CHINA

Hours after the Petro Yuan contracts started to trade in Shanghai, supposedly the USA and China are said to be near a deal to avert a trade war

(courtesy zerohedge)

US, China Said To Near Deal To Avert “Tit-For-Tat” Trade War

With its long-anticipated petroyuan contract only hours old, senior government officials in Beijing are reportedly working with the US to try and reach an agreement that would stave off a tit-for-tat trade war between the world’s two largest economies, according to the Financial Times and Wall Street Journal.

Treasury Secretary Steve Mnuchin along with trade representative Robert Lighthizer on one side, and Vice Premier Liu He, effectively China’s economy czar and President Xi Jinping’ “real second-in-command” on the other, have been negotiating behind the scenes, according to the FT.

And although nothing has been finalized, Liu has assured Mnuchin that China would cave on several US demands, including allowing foreign investment in Chinese securities firms and offering to buy more semiconductors from US semiconductor firms, the FT reported. There’s also been talks that China could loosen restrictions on foreign investment in manufacturing, telecom, medical and education.

Mnuchin, who is reportedly considering whether he should plan a trip to Beijing to expedite the negotiations, said Sunday after the US and South Korea reached a trade deal to exempt the South from US aluminum and steel tariffs that he was optimistic the US might reach a similar agreement with China. The Treasury secretary has reportedly handed Liu a list of US priorities, including loosening restrictions on US auto imports.

Late last week, President Trump announced that he planned to impose $60 billion in tariffs on Chinese industrial exports to reduce China’s nearly $400 million merchandise trade surplus with the US. Beijing subsequently announced it would retaliate with sanctions on a just $3 billion of US imports, with threats of more sanctions to come.

Chinese officials had initially been working to allow foreign majority control of securities companies by June 30, but Liu is now aiming for formal State Council approval as early as May. The liberalization would raise the 49% foreign ownership ceiling for securities firms to 51%. It was first outlined by China’s finance ministry in November. At the time, Zhu Guangyao, vice-finance minister, also said the cap would be lifted within three years.

Furthermore, more moves to ease foreign ownership limits in China’s commercial banking and insurance sectors could be revealed next week when President Xi addresses the Boao Forum for Asia, an annual meeting modeled on the World Economic Forum and hosted by the Chinese government on the southern island province of Hainan.