GOLD: $1342.90 DOWN $11.70 (COMEX TO COMEX CLOSINGS)

Silver: $16.54 DOWN 14 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1344.40

silver: $16.51

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1350.65

NY PRICING AT THE EXACT SAME TIME: $1350.30

LONDON SECOND GOLD FIX 10 AM: $1341.45

NY PRICING AT THE EXACT SAME TIME. $1342.45 ???

Nicholas to Bill Murphy and myself on the London fixes:

The first London Gold fix meeting was held on 12th Sept 1919.Now look at the extracts taken direct from the LBMA website:

‘The gold, silver, platinum and palladium price auctions take place in London on a daily basis. All of these prices are internationally regarded as the pricing mechanism for a variety of precious metal transactions and products.

From 1 April 2018, the LBMA Gold and Silver Prices on this page will not be available until midnight London time on the date that the prices are set. This is in line with the revised arrangements for delayed redistribution of the LBMA Gold Price and LBMA Silver Price recently announced by ICE Benchmark Administration (IBA) and is consistent with the timing of the publication of the LBMA Platinum and Palladium prices.’

If you are intrigued as to why the existence of this ‘ICE Benchmark Administration’ should provide cogent or even fair and reasonable grounds for the discontinuation of the promulgation of the daily London gold fix pricings until midnight, you are welcome to do your own research, but I have given up are expending too much redundant effort.

Everything happens for a reason. The last intraday promulgation of the LBMA gold price fix will, in fact be on Thursday afternoon (before Good Friday). Give the LBMA some credit. They were clearly aware of the potential tsunami about to impact the Shanghai physical gold market if the new petro/yuan futures contract gained some transaction. Now, given the volume of trading on the first day (yesterday), the word ‘potential’ should be dropped from the above sentence. All or any doubts can now laid to rest-the advent of petro yuan futures yesterday is a seminal date in the development of the globalized monetary framework, as momentous as the Bretton Woods conference, the TV announcement by Nixon in 1971 re the “temporary’ suspension of the convertibility of the USD and the process whereby Kissinger implemented the petro dollar. In the West, the only promulgation of gold market prices next month will be via the ubiquitous COMEX/GLOBEX platform, and this charade is a pure manipulated paper price only. At least these LBMA London fixes provide(d) (allegedly) some assurance that physical gold actually was exchanged at the quoted fix price.

Bill,

Now you and Harvey and other good men will have to be extra vigilant in seeking to ensure that the differential between the Shanghai physical gold price and COMEX/GLOBEX abomination is given widespread headlines.

Regards

Nicholas

end

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:475 NOTICE(S) FOR 47,500 OZ.

TOTAL NOTICES SO FAR 506 FOR 50,600 OZ

For silver:

MARCH

4 NOTICE(S) FILED TODAY FOR

20,000 OZ/

Total number of notices filed so far this month: 5348 for 26,740,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7909/OFFER $7,981: DOWN $241(morning)

Bitcoin: BID/ $7891/offer $7961: DOWN $261 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A TINY SIZED 177 contracts from 216,910 RISING TO 217,799 DESPITE YESTERDAY’S GOOD 11 CENT GAIN IN SILVER PRICING. WE OBVIOUSLY HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 653 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 653 CONTRACTS. WITH THE TRANSFER OF 653 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 653 CONTRACTS TRANSLATES INTO 3.265 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

41,233 CONTRACTS (FOR 19 TRADING DAYS TOTAL 41,233 CONTRACTS) OR 206.165 MILLION OZ: AVERAGE PER DAY: 2170 CONTRACTS OR 10.851 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 206.17 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 29.45% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 687.99 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A TINY SIZED GAIN IN COMEX OI SILVER COMEX OF 177 WITH THE 11 CENT RISE IN SILVER PRICE. HOWEVER, WE ALSO HAD A FAIR SIZED EFP ISSUANCE OF 653 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A GOOD 830 OI CONTRACTS i.e. 653 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 177 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 11 CENTS AND A CLOSING PRICE OF $16.70 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.091 BILLION TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 4 NOTICE(S) FOR 20,000 OZ OF SILVER

In gold, the open interest FELL BY A CONSIDERABLE SIZED 12,681 CONTRACTS DOWN TO 551,620 DESPITE THE FAIR SIZED RISE IN PRICE IN YESTERDAY’ TRADING ( GAIN OF $4.60). WE ARE NOW ENTERING THE LAST WEEK BEFORE FIRST DAY NOTICE OF AN ACTIVE GOLD COMEX CONTRACT MONTH AND HERE WE GENERALLY SEE A CONTRACTION AT THE COMEX WITH A CORRESPONDING HIGHER EFP ISSUED AND THAT IS WHAT WE GOT. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 14,247 CONTRACTS : APRIL SAW THE ISSUANCE OF 9,531 CONTRACTS, JUNE SAW THE ISSUANCE OF 4716 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 551,620. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A FAIR OI GAIN IN CONTRACTS: 12,681 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 14,247 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 1566 CONTRACTS OR 156,600 OZ =4.87 TONNES

YESTERDAY, WE HAD 17,571 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 197,049 CONTRACTS OR 19,704,900 OZ OR 612.905 TONNES (19 TRADING DAYS AND THUS AVERAGING: 10,371 EFP CONTRACTS PER TRADING DAY OR 1,037,100 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 19 TRADING DAYS IN TONNES: 612.905 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 612.905/2550 x 100% TONNES = 24.03% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1906.23 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX DESPITE THE STRONG RISE IN PRICE IN GOLD TRADING YESTERDAY ($4.60 GAIN). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 14,247 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 14,247 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 1566 contracts ON THE TWO EXCHANGES:

14,247 CONTRACTS MOVE TO LONDON AND 12,681 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 4.87 TONNES).

we had: 475 notice(s) filed upon for 47,500 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $11.70 : AND A RAID ORCHESTRATED THIS WAS TO EXPECTED: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD /A WITHDRAWAL OF 3.26 TONNES OF GOLD WHICH WAS USED IN THE RAID

Inventory rests tonight: 847.30 tonnes.

SLV/

WITH SILVER DOWN 14 CENTS TODAY: NO CHANGE

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A TINY 177 contracts from 217,622 UP TO 217,799 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE STRONG RISE IN PRICE OF SILVER (11 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 710 EFP CONTRACTS FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 177 CONTRACTS TO THE 653 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 830 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 4.15 MILLION OZ!!!

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE STRONG RISE IN SILVER PRICING YESTERDAY (11 CENT RISE IN PRICE) . BUT WE ALSO HAD ANOTHER WEAK SIZED 653 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 32.93 POINTS OR 1.05% /Hang Sang CLOSED UP 242.06 POINTS OR 0.79% / The Nikkei closed UP 551.22/Australia’s all ordinaires CLOSED UP 0.72%/Chinese yuan (ONSHORE) closed DOWN at 6.2823/Oil UP to 65.76 dollars per barrel for WTI and 70.35 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED DOWN AT 6.2826 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.2692 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR . CHINA IS HAPPY TODAY GOOD CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED/STRONGER GLOBAL MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

North Korea/China

b) REPORT ON JAPAN

3 c CHINA

i)Early this morning, the USA unveiled its Chinese tariff list. We are now waiting for Beijing to respond.

( zerohedge)

ii)Despite all this morning’s “happy” talk, stocks are fading as the USA confirms USA curbs on Chinese investments. China very angry.

( zerohedge)

4. EUROPEAN AFFAIRS

i)ECB

We have known for quite a while, the total of European non performing loans has been approximately 1 trillion euros. Now you can add another 10 billion euros to this list due to miscalculations. It seems that banks are lying as to the real value of the collateral that they hold. Both Germany and France has 250 billion euros of non performing loans but the ring leader is Italy at over 360 billion euros. Interesting enough Italy is complaining that the ECB is not paying attention to the huge risk in derivatives held by some of European banks, with the ring leader in that category: Deutsche bank

( zerohedge)

ii)Deutsche bank is preparing to oust its CEO John Cryan

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( zerohedge)

7. OIL ISSUES

ii)Both WTI and Gasoline extend losses after another large crude build( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)China has a long way to go before it supplants the dollar. However the new yuan for oil for gold is a terrific start. Chinese yuan represents only 1.1% of total reserves. The USA dollar is 63.5%

( Mike Bird/Wall Street Journal)

ii)Mine production is of the decline but there is still plenty of paper gold upon which obligations to provide physical is probably not there

( Clint Siegner/GATA)

iii)A good reason why Russia and China are stockpiling gold: to replace the dominance of the USA as the reserve currency of the world

( Tom Lewis/GoldTelegraph.com)

iv)Briscoe believes as do I that China’s new oil futures contract will threaten the USA dollars primacy

(courtesy Reuters/Duguid)

10. USA stories which will influence the price of gold/silver

i)USA data reports:

Despite poor number of homes being built, we still see a surge in home prices and the jump with this report is the largest in 4 years with all cities up in home prices

( zerohedge)

ii)Consumer confidence falters as “hope” plunges to new lows

iiib) LATE TRADING

iv)Wow!! we were totally unaware of this: The uSA exports a huge percentage of its waste material to China. Now China is ready to strike back if the USA imposes tariffs on steel and aluminum products plus other items

(courtesy zerohedge)

v)Jim Grant states that they may replace Libor with an another rate called SOFR which will probably give us a better picture of risk to the banks and thus a key figure to be used by investors around the world to price in risk( Jim Grant/Interest Rate observer)

vi) David Stockman/part ii/Train wreck

vii)SWAMP STORIES

a)Stormy Daniel’s slaps Trump’s lawyer, Cohen with a defamation suit. Then Trump’s team sends a cease and desist letter to Stormy. The 60 Minutes interview had the highest ratings in over 10 years.

Greg Gutfeld had the best line on this 60 Minute interview:

“Finding out Donald Trump slept with a porn star is like finding out Mike Pence didn’t…”

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:553,366 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 534,476 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A TINY 177 CONTRACTS FROM 217,622 UP TO 218,323 DESPITE OUR STRONG 11 CENT RISE IN SILVER PRICING/ YESTERDAY’). ALSO,WE WERE ALSO INFORMED THAT WE HAD 653 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 653. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 830 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 177 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 653 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 830 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month GAINED 4 contracts RISING TO 84 contracts. We had 1 contract filed YESTERDAY, so we GAINED 5 contracts or an additional 25,000 OZ will stand in this active delivery month of March

April LOST 7 contracts FALLING TO 396 .

The next big active delivery month for silver will be May and here the OI LOST 2094 contracts DOWN to 149,163

We had 4 notice(s) filed for 20,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 27/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

475 notice(s)

47,500 OZ

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz gold served (contracts) so far this month |

506 notices

50600 OZ

1.5738 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 475 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 113 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (506) x 100 oz or 50,600 oz, to which we add the difference between the open interest for the front month of FEB. (475 contracts) minus the number of notices served upon today (475 x 100 oz per contract) equals 50,600 oz, the number of ounces standing in this nonactive month of MARCH (1.738 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (506 x 100 oz or ounces + {(475)OI for the front month minus the number of notices served upon today (475 x 100 oz )which equals 50,600 oz standing in this nonactive delivery month of March . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 2 CONTRACTS OR AN ADDITIONAL 200 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS.

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

26,104.990

oz

SCOTIA

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

599,792.26 oz

Scotia

|

| No of oz served today (contracts) |

4

CONTRACT(S

(20,000 OZ)

|

| No of oz to be served (notices) |

80 contracts

(400,000 oz)

|

| Total monthly oz silver served (contracts) | 5348 contracts

(26,740,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) into Scotia: 599,792.260 oz

total deposits today: 599,792.260 oz

we had 2 withdrawals from the customer account;

i) Malca; 25,104.990 oz

ii) Out of Delaware: 999.90

total withdrawals;26,104.89 oz

we had 0 adjustments

total dealer silver: 59.383 million

total dealer + customer silver: 259.496 million oz

The total number of notices filed today for the March. contract month is represented by 4 contract(s) FOR 20,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5348 x 5,000 oz = 26,740,000 oz to which we add the difference between the open interest for the front month of Mar. (84) and the number of notices served upon today (4 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5348(notices served so far)x 5000 oz + OI for front month of March(84) -number of notices served upon today (4)x 5000 oz equals 27,140,000 oz of silver standing for the March contract month.

We GAINED 5 contracts or 25,000 additional silver oz will stand for delivery at the comex

FIRST DAY NOTICE IS THIS THURSDAY.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 87,806 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 111,165 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 111,165 CONTRACTS EQUATES TO 555 MILLION OZ OR79,2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.51% (MARCH 27/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.81% to NAV (March 27/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.51%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.81%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.65%: NAV 13.82/TRADING 13.44//DISCOUNT 2.65.

END

And now the Gold inventory at the GLD/

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 27/2018/ Inventory rests tonight at 847.30 tonnes

*IN LAST 350 TRADING DAYS: 93.74 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 300 TRADING DAYS: A NET 62.56 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 27/2018: NO CHANGE IN SILVER INVENTORY

Inventory 318.069 million oz

end

6 Month MM GOFO 2.12/ and libor 6 month duration 2.45

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.12%

libor 2.45 FOR 6 MONTHS/

GOLD LENDING RATE: .33%

XXXXXXXX

12 Month MM GOFO

+ 2.47%

LIBOR FOR 12 MONTH DURATION: 2.67

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.20

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Silver Futures Report and JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– Silver Futures Report, JP Morgan Record Silver Bullion Holding Is Extremely Bullish

– JP Morgan Continues Adding To Massive Silver Bullion Holdings (see chart)

– Silver Speculators Go Short – Which Is Extremely Bullish

– Stunning Silver COT Report: One For the Ages (see chart)

The silver futures Commitment of Traders (COT) report released last Friday was extremely positive and has most silver analysts calling for higher silver prices in the near term.

ZeroHedge.com

The COT data signaled we are close to bottoming and suggest that both gold and silver should make gains in the coming weeks and months. The data showed that the hedge funds and “Managed Money traders,” the “dumb money” speculators now have record short positions in silver.

At the same time, the large commercials and including large bullion banks such as JP Morgan, the “smart money” and the “inside money” have reduced their shorts dramatically and are now long.

The COT report shows ‘Managed money’ silver specs have their largest short position in at least 28 years and maybe ever. From a contrarian perspective this is very bullish.

Goldchartsrus.com

Another less reported bullish factor is JP Morgan continuing to add to its massive silver bullion holdings. They rose to a new record high last week at 139.12 million troy ounces. Either JP Morgan themselves or their clients or both are acquiring physical silver bullion in a big way and are clearly bullish silver.

Goldchartsrus.com

The notes by Ed Steer and Jon Rubino about this are well worth a read and below are the key snippets:

Ed Steer from EdSteerGoldSilver.com in Stunning Silver COT Report: One For the Ages put it this way

The Commitment of Traders Report, for positions held at the close of COMEX trading on Tuesday was right on the money in gold as far as Ted estimates were concerned, but in silver the decline in the Commercial net short position exceeded even his most bullish expectations. Considering the very modest price decline in silver during the reporting week, I thought his “5,000 to 10,000 contract improvement” estimate to be wildly optimistic. How wrong I was!

In silver, the Commercial net short position dropped by an eye-watering 15,564 contracts, or 77.8 million troy ounces of paper silver. Wow!

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube above

Jon Rubino from Dollar Collapse in Silver Speculators Go Short – Which Is Extremely Bullish put it this way:

Silver is a whole different story, with speculators going aggressively net short, something very seldom seen, and commercials almost in balance, which is also unusual. Looked at in a vacuum, this is hyper-bullish.

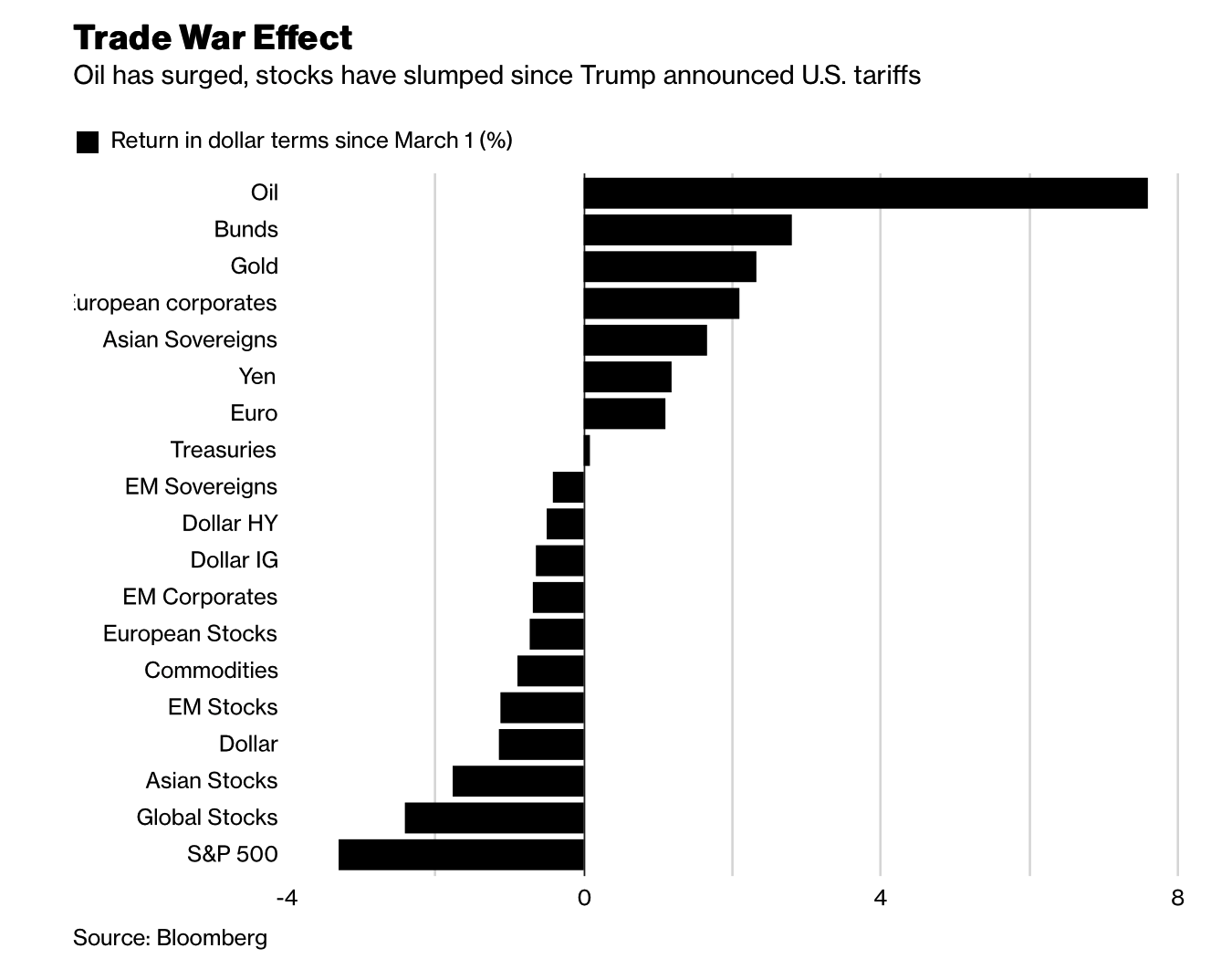

But of course the games futures traders play aren’t all that matters. Between trade wars, massive ongoing government deficits and spiking stock market volatility, the reasons for owning safe haven assets like gold and silver are both multiplying and gaining urgency.

Editors Note: Silver remains very undervalued in the short term and on a long term historical basis. It is also undervalued against gold as seen in the gold silver ratio at over 80:1.

Gold is beginning to receive some interest again from a small minority of retail investors but silver remains the preserve of relatively few contrarian investors. The media and financial press rarely, if ever, covers silver and almost never in a positive manner despite its strong fundamentals.

Yet silver is quite likely in the early stages of a new bull market that will rival or surpass that of the 1970s and thus merits an allocation in investment and pension portfolios.

Related Reading

Money and Markets Infographic Shows Silver Most Undervalued Asset

Buy Silver – “Best Precious Metals Trade”

JP Morgan Cornering Silver Market?

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube above

News and Commentary

Gold marks longest streak of session gains since January (MarketWatch.com)

Gold at more than five-week high as U.S. expels Russian diplomats (Reuters.com)

Dow rises after last week’s rout as trade tensions show signs of cooling (MarketWatch.com)

Stocks Roar Back, Dollar Falls as Trade Angst Ebbs (Bloomberg.com)

World stocks bounce on report of U.S.-China trade talks (Reuters.com)

Source: Bloomberg.com

The World’s Most Controversial Interest Rate Is Haunting Us Again (Bloomberg.com)

As Trade War Heats Up, Biggest Currency Whales Make Their Move (Bloomberg.com)

Mortgage approvals fall 11 percent in February (Reuters.com)

Gold Prices (LBMA AM)

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

21 Mar: USD 1,316.35, GBP 935.53 & EUR 1,071.64 per ounce

20 Mar: USD 1,312.75, GBP 935.60 & EUR 1,066.22 per ounce

19 Mar: USD 1,311.70, GBP 934.59 & EUR 1,066.41 per ounce

Silver Prices (LBMA)

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

21 Mar: USD 16.25, GBP 11.56 & EUR 13.23 per ounce

20 Mar: USD 16.25, GBP 11.60 & EUR 13.22 per ounce

19 Mar: USD 16.29, GBP 11.59 & EUR 13.24 per ounce

Recent Market Updates

– London House Prices Falling Sharply – UK’s Much Needed Wake-Up Call

– Global Trade War Fears See Precious Metals Gain And Stocks Fall

– Gold +1.8%, Silver +2.5% As Fed Increases Rates And Trade War Looms

– Credit Concerns In U.S. Growing As LIBOR OIS Surges to 2009 High

– Four Charts: Debt, Defaults and Bankruptcies To See Higher Gold

– Crock Of Gold Hidden In Ireland? Happy Saint Patrick’s Day

– Buy Silver And Sell Gold Now

– Stephen Hawking – Doomsday Prophet’s Top Five Predictions

– Gold Cup At Cheltenham – Gold Is For Winners, Not For the Gamblers

– Hungary’s Gold Repatriation Adds To Growing Protest Against US Dollar Hegemony

– Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

– Gold Protects As Cashless Society Threatens Vulnerable

– Women’s Pension Crisis Highlights Dangers To Savers

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

end

China has a long way to go before it supplants the dollar. However the new yuan for oil for gold is a terrific start. Chinese yuan represents only 1.1% of total reserves. The USA dollar is 63.5%

(courtesy Mike Bird/Wall Street Journal)

China’s attempts to supplant dollar face historic difficulties

Submitted by cpowell on Mon, 2018-03-26 15:09. Section: Daily Dispatches

By Mike Bird

The Wall Street Journal

Monday, March 26, 2018

https://www.wsj.com/articles/chinas-attempts-to-supplant-dollar-face-his…

The world’s first yuan-denominated oil contracts launched today, as part of China’s drive to turn its currency into a global force in markets.

The history of international currency markets suggests that may be a difficult task, though not impossible if Beijing eases the capital controls that make it hard for foreigners to buy up domestic assets, economists say.

Those capital controls and investors’ concerns over the opaqueness of Chinese government and central bank policy mean that the yuan remains a minnow in international finance, despite China being the world’s largest exporter.

The dollar and euro are global currencies because central banks hold them in their reserves and they are used to buy services and goods both in and outside their home markets.

In launching new yuan-denominated crude-oil futures, Beijing hopes to create an oil benchmark to rival those in New York and London and challenge the dollar’s role as the dominant commodity-pricing currency by making it possible for crude exporters to sell oil in another currency.

Professor Barry Eichengreen of the University of California, Berkeley, who writes about the history of currencies in the international financial system, believes the dollar’s grip on oil pricing isn’t guaranteed.

“As financial markets continue to develop — as there are liquid markets in more currencies, and currency trading becomes cheaper—- traditional arguments for why one currency should monopolize this function become even weaker,” Mr. Eichengreen said.

Still, “I don’t think the renminbi will displace the dollar from the global oil market any time soon. Lack of liquidity and accessibility continue to limit its usage,” he added.

China’s currency has some way to go. The yuan’s share of global foreign exchange reserves is just 1.1 percent of the global total, behind currencies like the Australian and Canadian dollars. The U.S. dollar’s share is 63.5 percent.

The yuan makes up only 1.1 percent share of international payments, placing it behind seven others, according to payments firm SWIFT. That share has dipped in recent years, from as high as 2.8 percent in August 2015. Currently almost all oil and most commodities are bought and sold in dollars.

However, even in modern history, it hasn’t always been this way. Economists point to the demise of the British pound’s dominance in world trade as showing that the tide can turn quickly against one currency in favor of another, especially during a crisis.

The London Metal Exchange benchmark copper contract was denominated in sterling until 1993. Even today cocoa trading is priced in sterling.

Though crude has a longer history of being denominated in dollars, due to the U.S.’s status as a major producer, as late as the 1970s oil-producing countries received around a fifth of their royalty payments in sterling, according to economic historian Professor Catherine Schenk.

Before the outbreak of the World War I, dollar-denominated international trade credit was almost nonexistent and British banks dominated the sector. By the mid-1920s the dollar and sterling-denominated trade credit occupied similar market shares.

The economic impact of the First and World War II left London’s influence in international finance and trade dramatically weakened, leaving the dollar firmly in the driving seat by the second half of the 20th century.

Sheer economic heft isn’t enough to guarantee a currency international primacy. The U.S. economy supplanted the U.K.’s as the world’s largest in the 1870s, around half a century before the dollar began to replace sterling as the world’s dominant currency.

That is a lesson to China, as its economy catches up with the U.S. and by some measures has already taken over.

One factor currently limiting the adoption of the yuan as a global currency is Beijing’s capital controls, which place limits on investment in China. Beijing keeps a tight grip of money coming in and out of the country to maintain control of the country’s economy and prevent sudden outflows of capital.

Currently, selling a yuan-denominated future means investors must either exchange the currency back into dollars — partly defeating the purpose of the contract — or find assets denominated in the Chinese currency to invest in.

There is no shortage of Chinese assets. The IHS Markit iBoxx Asia China index, a broad index of Chinese bonds, has more than doubled in size in the last 4 1/2 years, to over $11 trillion.

Some of the government controls have already been loosened. In 201, China launched a “bond-connect program” to allow global investors with trading accounts in Hong Kong to access China’s interbank bond market.

Just because more foreigners can now buy Chinese bonds, it doesn’t mean they will. Some investors say Beijing will have to open up its economy more for that to happen.

“Firstly, China will have to remove, or substantially reduce, capital controls for [renminbi] priced oil trading to take off,” said Hayden Briscoe, head of fixed income Asia Pacific at UBS Asset Management.

Mr. Briscoe added that the inclusion of Chinese bonds in major indexes would boost outside investment in the country’s debt, given investors and passive funds track such benchmarks.

“When that happens, we’re expecting a major reallocation of capital into China’s onshore bond markets,” Mr. Briscoe said.

Bloomberg LP said Friday it would add Chinese bonds to its Bloomberg Barclays Global Aggregate Index in 2019.

However, the country’s controls on capital flows aren’t the only concerns. The Chinese government’s propensity to intervene in domestic commodity markets and the lack of transparency about the country’s monetary policy are also unlikely to find favor among investors.

END

Briscoe believes as do I that China’s new oil futures contract will threaten the USA dollars primacy

(courtesy Reuters/Duguid)_

China’s oil futures launch may threaten dollar’s primacy, UBS analyst says

Submitted by cpowell on Tue, 2018-03-27 01:20. Section: Daily Dispatches

By Kate Duguid

Reuters

Monday, March 26, 2018

NEW YORK — China’s launch of its crude futures exchange today will improve the clout of the yuan in financial markets and could threaten the international primacy of the dollar, argues a new report by Hayden Briscoe, APAC head of fixed income at UBS Asset Management.

“This is the single biggest change in capital markets, maybe of all time,” Briscoe said in a follow-up telephone interview.

The launch of the oil futures denominated in China’s renminbi currency, also known as the yuan, is China’s first commodity derivative open to foreign investors. This marked the culmination of a decade-long push by the Shanghai Futures Exchange to give the world’s largest energy consumer more power in pricing crude sold to Asia.

Already today Unipec, the trading arm of Asia’s largest refiner Sinopec, has inked a deal with a Western oil major to buy Middle East crude priced against the newly-launched Shanghai crude futures contract.

This helps cement the exchange’s viability and challenges the petro-dollar system, in which oil deals are executed in dollars. This would decrease demand for the greenback and boost U.S. inflation. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-oil-futures-dollar/china-oil-fu…

END

Mine production is of the decline but there is still plenty of paper gold upon which obligations to provide physical is probably not there

(courtesy Clint Siegner/GATA)

Clint Siegner: Mine production may decline but there’s still plenty of ‘paper gold’

Submitted by cpowell on Tue, 2018-03-27 04:56. Section: Daily Dispatches

12:56p SST Tuesday, March 27, 2018

Dear Friend of GATA and Gold:

Annual world gold production seems to be about to decline, Clint Siegner of Money Metals Exchange writes this week, but there’s never any shortage of “paper gold,” claims to gold that may not exist.

“When it comes to trading in gold futures,” Siegner writes, “the physical supply and demand for the metal is barely a consideration. Practically no one trading contracts cares about getting delivery. During periods of high speculative demand in the futures markets, the bullion banks stand ready to sell a virtually unlimited number of fresh new contracts. Physical gold may be scarce, but available paper gold has been limitless.”

Siegner adds: “Someday the confidence in gold (and silver) futures is likely to collapse. Some event will prompt traders to look at the shocking amount of leverage built into the contracts. They will suddenly be uncomfortable with how little physical metal there is supporting the enormous paper trade. When too many begin standing for delivery of bars, they will be handed cash instead, provided their counterparties are solvent.”

His commentary is headlined “Physical Gold Production May Be Peaking, But There Is No Shortage In Paper Gold” and it’s posted at Money Metals here —

https://www.moneymetals.com/news/2018/03/26/paper-gold-vs-physical-gold-…

— and at GoldSeek here:

http://news.goldseek.com/GoldSeek/1522094389.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A good reason why Russia and China are stockpiling gold: to replace the dominance of the USA as the reserve currency of the world

(courtesy Tom Lewis/GoldTelegraph.com)

Russia Stockpiles Gold, But Why?

Authored by Tom Lewis via GoldTelegraph.com,

The US’s overhang of debt and looming trade war is worrisome on many levels as the value of the dollar keeps decreasing and the national debt spiraling. So, what should we make of the fact that the Central Bank of Russia has been steadily amassing vast gold reserves since 2015? By the end of 2017, its total gold reserves rose to 1,828.56 tons, usurping China’s place as the country with the fifth largest gold reserves.

Russia has been aggressively increasing its gold reserves for a reason. It has seen the US dollar dominate as a global currency and is working with China to end the US/Western currency supremacy. Their strategy appears to be working. Russia and China are in the midst of rumors of introducing gold-backed futures to circumvent the U.S dollar.

The US dollar has had no gold-backing since 1933, nor has the US increased its gold reserves for a decade. See chart below.

With speculation of Russia and China working on a gold-backed currency, a shift in monetary power from the West to the East seems to be their ambitions. The situation between East and West is exacerbated by recent tensions between Russia and the UK, since the alleged Kremlin poisoning of former spy Sergei Skripal and his daughter. British Prime Minister Theresa May has ousted 23 Russian diplomats from Great Britain. Geopolitical tension is once again, high.

It seems Russian may have tossed aside Das Kapital as its economic guidebook. Not only is creating a gold-backed currency appearing more likely month over month, but Russia has also brought inflation way down over the past decade. More importantly, Russia continues to lower their national debt, while the US has been increasing its debt to a record $21 trillion.

Russia’s financial strategy is making the country less vulnerable to volatile geopolitics. Not only is it a significant player in gold, but it is also the world’s third-largest gold producer, with the Central Bank of Russia buying up its supplies. During the past decade, Russian has mined more than 2,000 tons of gold, with tonnage expected to increase by 400 tons annually by 2030.

Russia and China understand the value of real, physical gold, a lesson that the US has forgotten while reveling in worthless paper currency.

If Russia and China establish a 100 percent gold-backed currency, it inevitably changes the game in the West. The dollar will continue to devalue against gold at a rapid rate.

Ultimately, the battle will not be Eastern vs. Western dominance. The real battle long term will be between the US dollar (fiat) and gold.

But remember:

(GATA) No, GATA never took Russian central banker or Greenspan out of context

Submitted by cpowell on 02:32PM ET Tuesday, March 27, 2018. Section: Daily Dispatches

10:39p Tuesday, March 27, 2018

Dear Friend of GATA and Gold:

In commentary posted today at GoldSeek, headlined “GATA Is at It Again” —

http://news.goldseek.com/GoldSeek/1522155660.php

— financial letter writer Avi Gilburt accuses GATA of routinely taking quotes out of context, starting with the mention made of GATA by the deputy chairman of the Bank of Russia, Oleg Mozhaiskov, in his address to the London Bullion Market Association meeting in Moscow in June 2004.

But GATA has never taken Mozhaiskov out of context. To the contrary, soon after Mozhaiskov gave his address and we heard that he had mentioned us, we strove to obtain a copy of his complete remarks and have often referred to his full remarks when citing him:

Mozhaiskov’s speech was notable for establishing that while GATA at that time had never to our knowledge had any contact with the Russian government or, for that matter, anyone in Russia, the Bank of Russia was following our work. We construed Mozhaiskov’s reference to GATA as signifying that the Bank of Russia shared GATA’s suspicion about the activity of the U.S. government and its allies in the gold market.

In any case soon after Mozhaiskov’s speech Russia began repatriating its gold from the Bank of England and Russian President Vladimir Putin announced that he had instructed the Bank of Russia to start buying gold on all markets — the very policy that GATAs research seemed to argue for.

Gilburt construes Mozhaiskov’s remarks about GATA as ridicule. But Mozhaiskov told the LBMA that there was reason to believe that the gold market was operating under something other than free-market forces. If Mozhaiskov really found GATA so ridiculous, would he have taken so much time to call its work to the LBMA’s attention? Or was this his way of letting the bullion bankers know that Russia was on to them and the Western central banks for which they were fronting?

A little background here supplies more context than Gilburt can. When GATA heard of Mozhaiskov’s remarks from a participant in the LBMA conference in Moscow, we were told that the LBMA had a copy of his speech. So we asked the LBMA to share it with us. The LBMA refused, apparently construing the speech as unfavorable to the bullion banks. Whereupon your secretary/treasurer located a fax number for the Bank of Russia in Moscow and sent a letter to Mozhaiskov, asking if he would provide a copy of his speech. Your secretary/treasurer told Mozhaiskov that a copy in the original Russian would do fine, since at that time your secretary/treasurer worked with a U.S. graduate student in Russian studies who was fluent in the language and would gladly translate the speech for us.

Remarkably Mozhaiskov replied within hours, agreeing to provide a copy of his speech but adding that he wanted his own friend, the president of Moscow Narodny Bank in London, to do the translation into English.

Sure enough, a month or so later the translation arrived in the surface mail from London and GATA published it in full on the day it was received.

If Mozhaiskov found GATA as ridiculous as Gilburt does, the central bankers courtesy was all the more amazing. As his speech discloses, Mozhaiskov knew full well what GATA was about and surely was aware of how GATA was likely to construe his remarks. Neither Mozhaiskov nor anyone else at the Bank of Russia has ever complained that GATA has misconstrued him. Only Gilburt has made such an allegation, as if he knows what central bankers think better than they themselves do.

But anyone can read Mozhaiskovs speech and draw his own conclusions precisely because GATA alone has provided the original document from the source and repeatedly has called attention to it to guard against any taking it out of context.

Then Gilburt disputes GATAs interpretation of Federal Reserve Chairman Alan Greenspans famous testimony to Congress in July 1998 that central banks were ready to lease gold to suppress its price:

https://www.federalreserve.gov/boarddocs/testimony/1998 /19980724.htm

Gilburt says GATA has mistakenly construed this as an admission that the Fed itself was leasing gold, but he is mistaken. He cites no authority for his assertion.

If Gilburt had done a little research he would have found that in 2000 GATA extracted and publicized a statement from Greenspan denying that the Fed was leasing gold but acknowledging that other central banks were:

Perhaps Gilburt is confusing gold leasing by the Fed with gold swapping by the Fed. For in 2009 GATA extracted a statement from a member of the Feds Board of Governors, Kevin M. Warsh, admitting that the Fed has gold swap arrangements with foreign banks and refuses to disclose them:

Is Gilburt really incapable of wondering why, if the Fed’s gold swap arrangements are innocent, they cannot be disclosed or explained? And is Gilburt incapable of understanding that a gold swap by the Fed with another central bank or with a bullion bank could be quickly turned into a gold lease by that other central bank or bullion bank?

Gilburt writes: “Again, it deserves repeating. Mr. Greenspan did not admit that the Fed manipulates gold. Mr. Greenspan did not even note that there was anyone who manipulated gold. Rather, he was saying that if someone attempted to manipulate the gold market, the Fed may have a tool to combat such manipulation attempts. More importantly, he never even opined as to whether such a tool would or could even be successful.”

If this “deserves repeating” it is only because Gilburt himself has been misquoting GATA about Greenspan. GATA maintains that Greenspans 1998 testimony about gold leasing is important mainly for acknowledging that gold leasing is a mechanism of price suppression far more than it is what others have called it, a mechanism by which central banks try to earn a little money on a supposedly dead asset.

But Greenspan did assure Congress that gold leasing would work to suppress the gold price — presumably because he knew from experience that it already had done so.

Gilburt continues: “GATA and its ilk will often point to evidence of small price manipulations and suggest that these ‘paper cuts’ have caused the market to bleed to death.”

Not so. Of course GATA has called attention to charges and admissions of gold and silver market manipulation involving investment banks and various traders outside government. But our primary complaint long has been that governments and central banks are the primary manipulators of the monetary metals markets, the real parties in interest in gold price control.

Gilburt also suggests that GATA blames central banks for the entirety of every move down in monetary metals prices every day. This is nonsense and again Gilburt fails to support his charge with anything published by GATA.

Rather, GATA maintains that central banks are meddling in the gold market surreptitiously “nearly on a daily basis,” to use the words of the director of market operations for the Banque de France, Alexander Gautier, in his address to another LBMA meeting, this one in Rome in September 2013:

http://www.gata.org/node/13373

No one but central banks themselves can know exactly how much of any days price move they cause. But since central banks are authorized to produce infinite money, they can move markets as much as they want in any direction.

GATA has produced documentation that governments and central banks are surreptitiously trading all futures markets in the United States, according to filings with the U.S. Securities and Exchange Commission and Commodity Futures Trading Commission:

http://www.gata.org/node/14385

http://www.gata.org/node/14411

GATA readily admits that it doesnt know everything governments and central banks are doing surreptitiously in the monetary metals markets. But we have compiled enormous documentation of that involvement and the longstanding policy of Western central banks to suppress the gold price to defend their currencies, government bond prices, and interest rates against market forces.

http://www.gata.org/taxonomy/term/21

By contrast Gilburt concludes his latest misrepresentations by proclaiming his great success at predicting monetary metals prices, as if that is somehow a rebuttal to GATAs work and not just egotism.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.2826 /shanghai bourse CLOSED UP 32.93 POINTS OR 1.05% / HANG SANG CLOSED UP 242.06 POINTS OR 0.79%

2. Nikkei closed UP 551.22 POINTS OR 2.65% /USA: YEN RISES TO 105.75/

3. Europe stocks OPENED GREEN /USA dollar index RISES TO 89.44/Euro FALLS TO 1.2398

3b Japan 10 year bond yield: RISES TO . +.038/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.75/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.76 and Brent: 70.35

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.529%/Italian 10 yr bond yield DOWN to 1.887% /SPAIN 10 YR BOND YIELD DOWN TO 1.234%

3j Greek 10 year bond yield FALLS TO : 4.383?????????????????

3k Gold at $1347.20 silver at:16.65 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 57.23

3m oil into the 65 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.75 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9481 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1760 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.529%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.850% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0865% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Trump’s “Happy” Tweet Sends Global Stocks Soaring As Trade Tensions Ease Further

Just as Trump sent stocks into a tailspin last week with his bellicose trade overtures against China, so the near record (point) rebound in the Dow on Monday is being attributed to a much more diplomatic tone out of the Trump administration, when first Mnuchin, then Peter Navarro played down the threat of a trade war and instead said that the administration is “actively” involved in talks with China to resolve the recent trade tensions between the two nations. Various unconfirmed media reports then also suggested that trade war with China may never materialize (of course, as Mark Cudmore explained this morning, it very well still may). It culminated with a “happy” tweet from Trump himself on Monday night, in which the stock-picking president, hours after confirming his delight with the spike in the market, tweeted “trade talks going on with numerous countries that, for many years, have not treated the United States fairly. In the end, all will be happy!”

Trade talks going on with numerous countries that, for many years, have not treated the United States fairly. In the end, all will be happy!

And so, just like yesterday morning, this morning global markets and US equity futures are a sea of green, which once again is being attributed to fading chances of an “all-out global trade war.”

The fresh surge in risk appetite emerged as the Trump administration was said to be urging China to lower tariffs on cars and open its market to U.S. financial services as part of talks to resolve trade tensions. Treasury Secretary Steven Mnuchin and his Chinese counterpart have been discussing the trade deficit between the two countries and were committed to finding a mutually agreeable way to reduce the gap and help China avoid tariffs on $50 billion of exports to the U.S. Ironically, after yesterday’s upside rout, US and global stocks are almost unchanged since March 1, with the bulk of assets since March 1 now positive.

Only, unlike yesterday when the dollar was tumbling, serving as a key component of the risk-on narrative, today the USD has rebounded and erased almost all of yesterday’s losses. At the same time, the euro weakened as economic confidence in the region continued to slide in March.

“Our base case is that there won’t be an all-out trade war,” Aberdeen Standard Investments’ global head of fixed income, Craig MacDonald, , told Bloomberg. “It’s a way of applying pressure to get some wins by Trump.” Still, it will lead to more volatility, MacDonald added. “Our sense is that they will get some wins rather than all out war, but it’s not something you can just dismiss. The tail risk is higher.”

Meanwhile in the aftermath of yesterday’s massive US rally, the euphoria was everywhere, as European shares headed for their first gain in five sessions, with the Stoxx 600 Index jumping the most in six weeks, up 1.4% and joining the global relief rally seen between US and Asia overnight as, what else, “trade tensions ease.” 19 out of 19 Stoxx 600 sectors rise; technology sector has the biggest volume at 111% of its 30-day average; 584 Stoxx 600 members gain, 7 decline. In terms of sector specifics, materials (+2.0%) are the outperformers, enjoying a strong rebound from yesterday’s losses. Looking at individual movers, Casino (+3.4%) spiked at the open after its Monoprix chain has agreed to sell products on Amazon, GSK (+6.0%) is a top performer in the FTSE 100 after it announced to purchase a 36.5% stake in Novartis’ healthcare unit for USD 13bln.

Earlier in Asia shares were green across the board, with Japan’s Topix Index jumping the most since November 2016. South Korea’s won was the best performer among major currencies as Kim Jong Un was said to be making an unannounced visit to Beijing, his first known trip outside North Korea since taking power in 2011. The ASX 200 (+0.7%) and Nikkei 225 (+2.7%) were higher with mining names and financials leading Australia, while the Japanese benchmark outperformed as the index coat-tailed on gains in USD/JPY and following the testimony by former tax office chief Sagawa who declared there were no instructions made by PM Abe or his close circle to alter the documents related to the land sale scandal.

Specifically, Japan’s former tax agency chief Sagawa said there was no report to the PM’s office of documents being altered and added that there were no instructions from PM Abe, his wife, Finance Minister Aso or their aides to doctor the documents. In related news, there were also comments from Finance Minister Aso that PM Abe’s office was not involved with document alterations in the controversial land sale.

Mainland China and Hong Kong shares advance along with other equity markets on hopes that talks with the U.S. will resolve trade tensions. Hang Seng Index rises 0.8%; Hang Seng China Enterprises Index adds 0.9%; Shanghai Composite Index closed up 1.1% after weathering some downward pressure in the last hour of trade; it was its first gain in five sessions.

As noted above, in FX, the dollar reversed earlier losses, with demand picking up amid month-end flows as the London session gets under way. EUR/USD rallied briefly in early London trading to a five-week high of 1.2476 on dollar supply and euro demand against crosses, before reversing the move; in the Asian session, the pair had traded in a very narrow range. Sterling led losses in G-10, partly driven by strong demand in euro-pound, and weighed by EUR/GBP bids amid month-end flows supportive of the greenback. The yen slid as much as 0.3% against the dollar after heavy buying in the U.S. currency across the Tokyo fix took the pair to session high of 105.75 as trade tensions between the U.S. and China eased. The Aussie fell with local bond yields as capital flows are redirected back into emerging markets; the South Korean won rallied as much as 1.2% and the onshore Chinese yuan briefly touched the strongest level since the 2015 devaluation before gains were erased Elsewhere, China’s currency touched the highest level in almost three years.

In geopolitical developments, the Russian Deputy Foreign Minister warned of ‘harsh’ response to expulsion of diplomats from the US, but still open to cooperation.

Euro-area bonds traded in the green, as do longer-dated Treasuries. Bunds initially rallied to make another test of 50bps in yield before fading; TSYs in a tight range with curve marginally flatter amid focus on this weeks heavy supply, with large early buying seen in white eurodollars, leading to a tightening in the FRA/OIS spread further from recent blowout.

In commodities, crude futures unchanged, spot gold weighed by USD rally and industrial metals hold Asian session gains. Bitcoin edged higher, nearing the $8,000 level. And copper broke out of a three-day trading slump, climbing as much as 1.8%.

Market Snapshot

- S&P 500 futures up 0.6% to 2,676.00

- STOXX Europe 600 up 1.2% to 367.37

- MSCI Asia Pacific up 1.4% to 175.31

- MSCI Asia Pacific ex Japan up 0.9% to 573.94

- Nikkei up 2.7% to 21,317.32

- Topix up 2.7% to 1,717.13

- Hang Seng Index up 0.8% to 30,790.83

- Shanghai Composite up 1.1% to 3,166.65

- Sensex up 0.5% to 33,224.00

- Australia S&P/ASX 200 up 0.7% to 5,832.30

- Kospi up 0.6% to 2,452.06

- German 10Y yield fell 0.8 bps to 0.516%

- Euro down 0.01% to $1.2443

- Italian 10Y yield rose 3.4 bps to 1.656%

- Spanish 10Y yield fell 2.0 bps to 1.241%

- Brent futures up 0.4% to $70.38/bbl

- Gold spot down 0.3% to $1,350.16

- U.S. Dollar Index up 0.3% to 89.25

Top Overnight News

- The Trump administration is urging China to lower tariffs on cars and open its market to U.S. financial services as part of talks to resolve a rise in trade tensions that has shaken global markets, according to a person familiar with the matter

- President Donald Trump ordered 60 Russian diplomats the U.S. considers spies to leave the country and closed Russia’s consulate in Seattle in response to the nerve-agent attack on a former Russian spy in the U.K., as European allies and Canada took similar measures.

- Federal Reserve Governor Randal Quarles says “our economy is performing well, and unemployment is low. However, many households and communities continue to face financial challenges.”

- Federal Reserve Bank of Cleveland President Loretta Mester says she doesn’t see excessive financial imbalances, but the need to avoid them building up is another argument for “gradually taking away accommodation.”

- Kim Jong Un made a surprise visit to Beijing on his first known trip outside North Korea since taking power in 2011, three people with knowledge of the visit said.

- The ECB can only have “deeper discussions” about the next policy changes when its projections are published in June, Governing Council member Vitas Vasiliauskas says in a news conference in Vilnius

- Euro-area economic confidence dropped for a third month in March as the region showed signs of entering a period of more moderate growth. Optimism slipped in the region’s five biggest economies, taking the overall index to its lowest in six months

- The ECB alerted auditors that lenders could try to take advantage of the transition to new accounting standards to spread the hit on loan losses over years instead of reflecting them in their 2017 financial results, three people familiar with the matter said

- The U.K.’s withdrawal from the European Union poses “material risks” to the availability of financial services, especially in areas where fixes must be put in place by both British and EU authorities, the Bank of England said

Central bank speakers:

- Fed’s Quarles (Voter, Neutral) said US economy is performing well and unemployment is at a low level, although he added that financial challenges remain for many households and communities.

- Fed’s Mester (Voter, Hawk) said she sees further interest rate hikes this year and next despite seeing more slack, while Mester added that tariffs and NAFTA renegotiations pose risks to economic outlook.

- Fed’s Bostic (Voter, Dovish) said he supports plans to gradually raise interest rates, but uncertainty over how the economy would respond next year to tax cuts and increased government spending could complicate monetary policy.

- ECB’s Vasiliauskas (Hawkish) expects more detailed talks on policy changes in June and agrees with market forecast for a mid-2019 rate hike. This follows ECB’s Weidmann yesterday, saying he expects a mid-2019 rate hike.

- ECB’s Liikanen (Neutral) says EZ inflation is sustainable when ECB’s objective can be met without very accommodative monetary policy. He adds that the ECB needs patience as underlying inflation is lower than expected.

- ECB’s Nowotny (Hawkish) believes asset purchases should be gradually reduce. Adding that If things continue as they are, they will be able to reduce asset purchases significantly and must decide by summer. Furthermore, stating we must be careful not to fall behind the curve.

Asian stocks were positive across the board as the region took impetus from the gains on Wall St where stocks rebounded with a vengeance from the prior week’s worst performance in 2 years. The sharp recovery was spurred by easing trade war concerns after reports of US and China negotiating on trade and saw the largest percentage increase in all US majors since August 2015, while DJIA also gained by the most points in nearly a decade. ASX 200 (+0.7%) and Nikkei 225 (+2.7%) were higher in which mining names and financials led Australia, while the Japanese benchmark outperformed as the index coat-tailed on gains in USD/JPY and following the testimony by former tax office chief Sagawa who declared there were no instructions made by PM Abe or his close circle to alter the documents related to the land sale scandal. Hang Seng (+0.8%) and Shanghai Comp. (+1.0%) conformed to the upbeat tone as trade war concerns eased and as corporate financial results took centre stage in China, with the big 4 banks underpinned after AgBank beat estimates as it kicked off the earnings releases amongst China’s banking behemoths. Finally, 10yr JGBs were weaker amid the gains in riskier assets and with demand also shunned following a mixed 40yr auction. Japan former tax agency chief Sagawa said there was no report to the PM’s office of documents being altered and added that there were no instructions from PM Abe, his wife, Finance Minister Aso or their aides to doctor the documents. In related news, there were also comments from Finance Minister Aso that PM Abe’s office was not involved with document alterations in the controversial land sale.

Top Asian News

- China’s Risky Debt Heads Overseas as Deleveraging Rolls On

- Troubled Chinese Firm to Put $3.2 Billion of Properties For Sale

- Xiaomi’s CEO Disses the iPhone in Unveiling $500 Marquee Device

- PBOC Signals Yi to Run China’s Monetary Policy, Guo in ‘Support’

- China’s Yuan Jumps to Highest Since 2015 as Trade Tensions Ease

European equities have joined the global relief rally (Eurostoxx +1.4%) seen between US and Asia overnight as trade tensions ease. In terms of sector specifics, materials (+2.0%) are the outperformers, enjoying a strong rebound from yesterday’s losses. Looking at individual movers, Casino (+3.4%) spiked at the open after its Monoprix chain has agreed to sell products on Amazon, GSK (+6.0%) is a top performer in the FTSE 100 after it announced to purchase a 36.5% stake in Novartis’ healthcare unit for USD 13bln. Elsewhere, Akzo Nobel (+3.0%) received a boost after Carlyle has won the bid to acquire the chemical arm unit for approx. EUR 10bln

Top European News

- Euro-Area Economic Confidence Extends Slide Into Third Month

- Marubeni to Sell Stake in U.K. Offshore Wind Farm Near Yorkshire

- Liikanen Urges Caution Against Tightening ECB Policy Too Soon

- Japan Tobacco Said to Plan Poland Plant Amid Overseas Push

- Painful Pivot West Starts to Pay Off for Ukraine’s Exporters