GOLD: $1326.60 DOWN $16.30 (COMEX TO COMEX CLOSINGS)

Silver: $16.27 DOWN 27 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1325.60

silver: $16.29

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $N/A DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $N/A

PREMIUM FIRST FIX: $N/A

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $N/A

NY GOLD PRICE AT THE EXACT SAME TIME: $N/A

PREMIUM SECOND FIX /NY:$XX

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1341.05

NY PRICING AT THE EXACT SAME TIME: $1341.25

LONDON SECOND GOLD FIX 10 AM: $1332.45

NY PRICING AT THE EXACT SAME TIME. $1331.85

end

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT:475 NOTICE(S) FOR 47,500 OZ.

TOTAL NOTICES SO FAR 506 FOR 50,600 OZ

For silver:

MARCH

4 NOTICE(S) FILED TODAY FOR

20,000 OZ/

Total number of notices filed so far this month: 5348 for 26,740,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8012/OFFER $8082: UP $81(morning)

Bitcoin: BID/ $7884/offer $7954: DOWN $47 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE SIZED 1719 contracts from 217,799 RISING TO 219,518 DESPITE YESTERDAY’S 14 CENT DROP IN SILVER PRICING. WE OBVIOUSLY HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GIGANTIC SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 3168 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 3168 CONTRACTS. WITH THE TRANSFER OF 3168 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3168 CONTRACTS TRANSLATES INTO 15.84 MILLION OZ ON TOP OF THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

44,401 CONTRACTS (FOR 20 TRADING DAYS TOTAL 44,401 CONTRACTS) OR 222.00 MILLION OZ: AVERAGE PER DAY: 2220 CONTRACTS OR 11.110 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 222.00 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 31.7% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 703.83 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.95 MILLION OZ

RESULT: WE HAD A GOOD SIZED GAIN IN COMEX OI SILVER COMEX OF 1719 WITH THE 14 CENT FALL IN SILVER PRICE. HOWEVER, WE ALSO HAD A HUGE SIZED EFP ISSUANCE OF 3168 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 3168 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED A HUGE 4887 OI CONTRACTS i.e. 3168 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 1719 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 14 CENTS AND A CLOSING PRICE OF $16.54 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A HUGE AMOUNT OF SILVER STANDING AT THE COMEX THIS MONTH.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.097 BILLION TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 80 NOTICE(S) FOR 400,000 OZ OF SILVER

In gold, the open interest FELL BY A HUMONGOUS SIZED 121,930 CONTRACTS DOWN TO 529,690 WITH THE FAIR SIZED FALL IN PRICE IN YESTERDAY TRADING ( LOSS OF $11.70). WE ARE NOW ENTERING THE LAST WEEK BEFORE FIRST DAY NOTICE OF AN ACTIVE GOLD COMEX CONTRACT MONTH AND HERE WE GENERALLY SEE A CONTRACTION AT THE COMEX WITH A CORRESPONDING HIGHER EFP ISSUED AND THAT IS WHAT WE GOT. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 16,331 CONTRACTS : APRIL SAW THE ISSUANCE OF 5410 CONTRACTS, JUNE SAW THE ISSUANCE OF 10,331 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 529,690. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A SMALL OI LOSS IN CONTRACTS: 21,930 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 16,331 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI LOSS: 5599 CONTRACTS OR 559,900 OZ =14.41 TONNES

YESTERDAY, WE HAD 14,247 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 213,380 CONTRACTS OR 21,338,000 OZ OR 663.70 TONNES (20 TRADING DAYS AND THUS AVERAGING: 10,669 EFP CONTRACTS PER TRADING DAY OR 1,066,900 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 20 TRADING DAYS IN TONNES: 663.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 663.70/2550 x 100% TONNES = 26.02% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1957.02 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX WITH THE CONSIDERABLE SIZED FALL IN PRICE IN GOLD TRADING YESTERDAY ($11.70 LOSS). HOWEVER, WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,331 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,331 EFP CONTRACTS ISSUED, WE HAD A SMALL NET LOSS IN OPEN INTEREST OF 5599 contracts ON THE TWO EXCHANGES:

16,331 CONTRACTS MOVE TO LONDON AND 21,930 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 17.41 TONNES).

we had: 12 notice(s) filed upon for 1200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $16.30 : AND OUR USUAL RAID ON OPTIONS EXPIRY WEEK: THIS AGAIN WAS TO EXPECTED: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD /A WITHDRAWAL OF 1.18 TONNES OF GOLD WHICH WAS USED IN THE RAID

Inventory rests tonight: 846.12 tonnes.

SLV/

WITH SILVER DOWN 27 CENTS TODAY: NO CHANGE

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 1719 contracts from 217,799 UP TO 219,677 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE GOOD SIZED FALL IN PRICE OF SILVER (14 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 3168 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 1719 CONTRACTS TO THE 3168 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 4887 OPEN INTEREST CONTRACTS. WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 24.43 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE CONSIDERABLE FALL IN SILVER PRICING YESTERDAY (14 CENT FALL IN PRICE) . BUT WE ALSO HAD ANOTHER VERY STRONG SIZED 3168 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 44.36 POINTS OR 1.40% /Hang Sang CLOSED DOWN 768.30 POINTS OR 2.50% / The Nikkei closed DOWN 286.01/Australia’s all ordinaires CLOSED DOWN 0.75%/Chinese yuan (ONSHORE) closed DOWN at 6.2936/Oil DOWN to 64.76 dollars per barrel for WTI and 69.89 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.2936 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.2796 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY POOR CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED WEAKER GLOBAL MARKETS/WEAKER CURRENCY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

North Korea/China

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

France/GermanyGermany and France clash over what to do with USA car tariffs. Germany due to its huge export business wants to make concessions. France says no concessions. However it is ultimately the EU and not just Germany and France that must make that decision

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

Oil and gasoline fall after a huge Cushing OK build. Crude continues to have record production

( zerohedge)

8. EMERGING MARKET

VENEZUELA

We are now witnessing child gangs forming in order to fight for food scraps

( Mac Slavo/SHFTplan.com)

9. PHYSICAL MARKETS

i)Due to protectionist policies, hedge funds make their move away from the dollar

( Greifeld/Bloomberg)

ii)Mike Kosares: the Petro-Yuan could displace the petro dollar and thus the USA dollar hegemony

( Kosares/GATA)

10. USA stories which will influence the price of gold/silver

( zerohedge)

iii)Wholesale inventories surge but not retail inventories. We must wait and see if these numbers correspond to sales.This will be a plus to Q1 GDP final numbers

( zerohedge)

iv)Pending home sales tumble year over year but gain month over month: 3.1%

(courtesy zerohedge)

a)My goodness!! The USA is heading for civil war: The California AG is now using Trump over the wording of citizenship in the new 2020 census

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:407,765 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 603,786 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A STRONG 1719 CONTRACTS FROM 217,799 UP TO 219,518 DESPITE OUR 14 CENT FALL IN SILVER PRICING/ YESTERDAY’). ALSO,WE WERE ALSO INFORMED THAT WE HAD A VERY STRONG 3168 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 3168. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND WE ALSO HAVE A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS ACTIVE OF MARCH AS WELL AS THE CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 4887 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1719 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 3168 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:4887 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 4 contracts FALLING TO 80 contracts. We had 4 contracts filed YESTERDAY, so we GAINED 0 contracts or an additional NIL OZ will stand in this active delivery month of March

April LOST 34 contracts FALLING TO 362 .

The next big active delivery month for silver will be May and here the OI GAINED 49 contracts UP to 149,212

We had 80 notice(s) filed for 400,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 28/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

12 notice(s)

1200 OZ

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz gold served (contracts) so far this month |

518 notices

51800 OZ

1.6111 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 12 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (518) x 100 oz or 51,800 oz, to which we add the difference between the open interest for the front month of FEB. (12 contracts) minus the number of notices served upon today (12 x 100 oz per contract) equals 51,800 oz, the number of ounces standing in this nonactive month of MARCH (1.6114 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (518 x 100 oz or ounces + {(12)OI for the front month minus the number of notices served upon today (12 x 100 oz )which equals 51,800 oz standing in this nonactive delivery month of March . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 12 CONTRACTS OR AN ADDITIONAL 1200 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH

IN THE LAST 18 MONTHS 72 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

62,061.010

oz

SCOTIA

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

600,571.100 oz

Malca

|

| No of oz served today (contracts) |

80

CONTRACT(S

(400,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 5428 contracts

(27,190,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 137 million oz of total silver inventory or 53.6% of all official comex silver.

JPMorgan deposited zero into its warehouses (official) today.

ii) into Malca: 600,571.100 oz

total deposits today: 600,571.100 oz

we had 2 withdrawals from the customer account;

i) Scotia; 60,028.510 oz

ii) Out of Delaware: 2032.00

total withdrawals; 62,061.010 oz

we had 0 adjustments

total dealer silver: 59.383 million

total dealer + customer silver: 259.035 million oz

The total number of notices filed today for the March. contract month is represented by 80 contract(s) FOR 400,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5428 x 5,000 oz = 27,190,000 oz to which we add the difference between the open interest for the front month of Mar. (80) and the number of notices served upon today (80 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5428(notices served so far)x 5000 oz + OI for front month of March(80) -number of notices served upon today (80)x 5000 oz equals 27,190,000 oz of silver standing for the March contract month.

We GAINED 0 contracts or NIL additional silver oz will stand for delivery at the comex

FIRST DAY NOTICE IS THIS THURSDAY.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 94,412 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 112,631 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 112,631 CONTRACTS EQUATES TO 563 MILLION OZ OR 80.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.12% (MARCH 28/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.71% to NAV (March 28/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.12%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.71%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.02%: NAV 13.62/TRADING 13.20//DISCOUNT 3.02.

END

And now the Gold inventory at the GLD/

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

GOLD DOWN 5.45 TODAY.

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 28/2018/ Inventory rests tonight at 846/12 tonnes

*IN LAST 351 TRADING DAYS: 94.92 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 301 TRADING DAYS: A NET 61.38 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

MARCH 27/2018: NO CHANGE IN SILVER INVENTORY

Inventory 318.069 million oz

end

6 Month MM GOFO 2.15/ and libor 6 month duration 2.45

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.15%

libor 2.45 FOR 6 MONTHS/

GOLD LENDING RATE: .30%

XXXXXXXX

12 Month MM GOFO

+ 2.51%

LIBOR FOR 12 MONTH DURATION: 2.67

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.18

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Eurozone Faces Many Threats Including Trade Wars and “Eurozone Time-Bomb” In Italy

– Eurozone threatened by trade wars, Italy and major political and economic instability

– Trade war holds a clear and present danger to stability and economic prospects

– Italy represents major source of potential disruption for the currency union

– Financial markets fail to reflect the “eurozone time-bomb” in Italy

– Financial volatility concerns in Brussels & warning of ‘sharp correction’ on horizon

– Euro and global currency debasement and bank bail-in risks

Editor: Mark O’Byrne

Source: Wikimedia

Donald Trump believes trade wars are easy to win. Winning depends on who your opponent is. At the moment Trump’s target is seemingly China but it is becoming increasingly clear that the Eurozone (and wider EU) is very much also at the top of his protectionist agenda.

This is a problem for the single market. It is not in a strong position when it comes to facing off the strong arm tactics of the President of the United States. Germany is the powerhouse of the EU when it comes to successful trade and industry, but its exporting machine is also vulnerable to US trade tariffs.

The Eurozone (and EU) are facing some major political and financial threats. This was already the case without Trump’s nationalist agenda, but trade tariffs combined with Italy’s political instability and increased market volatility risk now have the single market facing a precarious future.

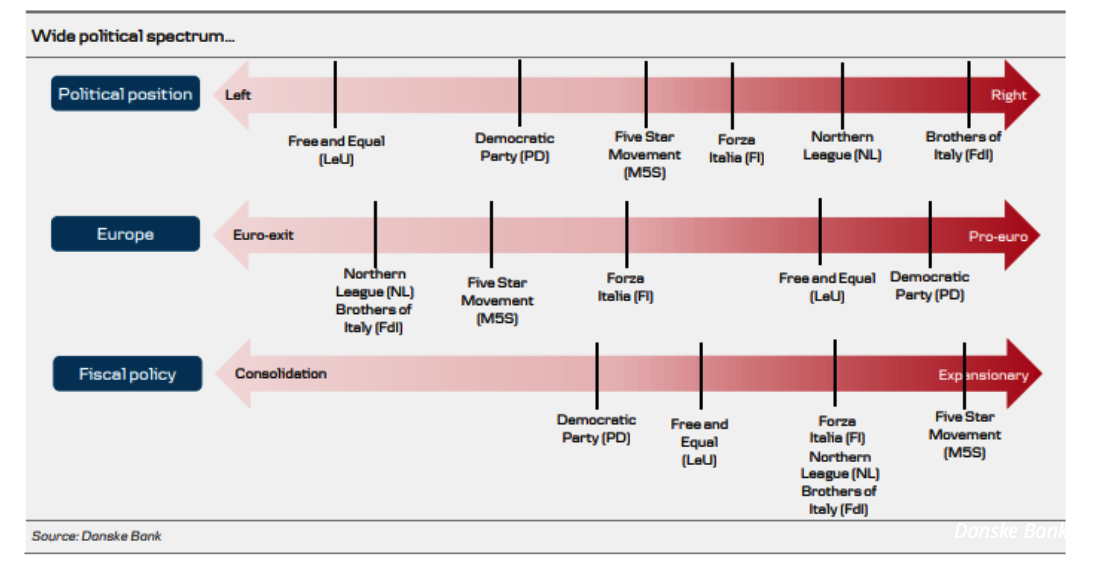

Italy is a serious political and financial threat

As outlined in the introduction, Trump’s trade wars have brought a number of problems to the fore for the Eurozone but it is Italy that is the most foreseeable threat to economic instability at this moment.

The election in early March and its uncertain result spooked markets somewhat but not enough to offer a real reflection of the risks posed. The result (which is still to be decided, overall) will pose major difficulties for the Eurozone that requires an Italian government focused on economic reforms and fiscal austerity.

Neither party brokering a deal to enter the leadership will be offering this on a silver platter.

Not only are the Five Star Movement and League yet another threat to the ‘one vision’ federal aims of the Eurozone elites but they have also shown very little interest in fiscal restraint. This is the only pathway for the Italian economy to returning to a sustainable footing according to the ECB.

This coming Autumn the (new) government (if appointed) will pass a new budget. Whilst this is pivotal for any new government, it will be more important to watch the politics surrounding the budget.

Considering over 60% of the parliament is made up of populist politicians the chances of an austerity budget being passed are beyond slim.

The two leading parties likely to form a government, The Five Star Movement and League, have made promises they cannot afford to break but are in direct contradiction with EU demands.

Five Star has promised a universal basic income, League has been elected on the promise of a flat income tax. Further inconsistencies with EU reforms are both parties’ promises to reverse pension changes.

At the moment markets do not seem too upset by the political situation in Italy. This is both short-sighted and naive.

Spending policies of both parties challenge EU rules. Whilst Mario Draghi in the ECB has previously been able to keep the country in line, this was with the help of Europhile Mario Monti. Monti is no more and Italians have shown their eagerness to elect more radical politicians who are reacting to the backlash of two punishing decades in which young people were out of work and the elderly lost their savings.

This backlash is something which is being felt throughout Europe. Astonishingly markets and commentators believed Eurosceptisim was on the back burner (despite various election results in 2017).

Italy’s own political outcome should serve as a much needed wakeup call that the euroscepticism within the bloc remain and will likely be reawakened. It may even bring back the existential threat to eurozone stability so many had long thought diminished. In turn, this will reduce the support the euro is currently enjoying.

As is becoming increasingly apparent, Italy is quite the dilemma for the Eurozone, they cannot afford to let it fail but equally it is seemingly too big to save.

This is very much the calm before the storm, as another economic crisis no doubt looms on the horizon.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Is the euro-area as strong as they think?

The ‘shock’ of the Italian election outcome has caused dementia within commentary circles regarding eurozone strength. To hear them talk about the eurozone one would think it was the epitome of health prior to the 4th March Italian election.

It was not. For example, not only is Brexit still threatening a major existential crisis on the single market but 2017 brought in the destruction of the French two-tier political system and the total wipeout of the centrist majority in German parliament – two things Europhiles thought they could be sure of.

Instead there are a number of looming issues that will no doubt create further divisions and anti-EU sentiments. This is despite markets remaining optimistic.

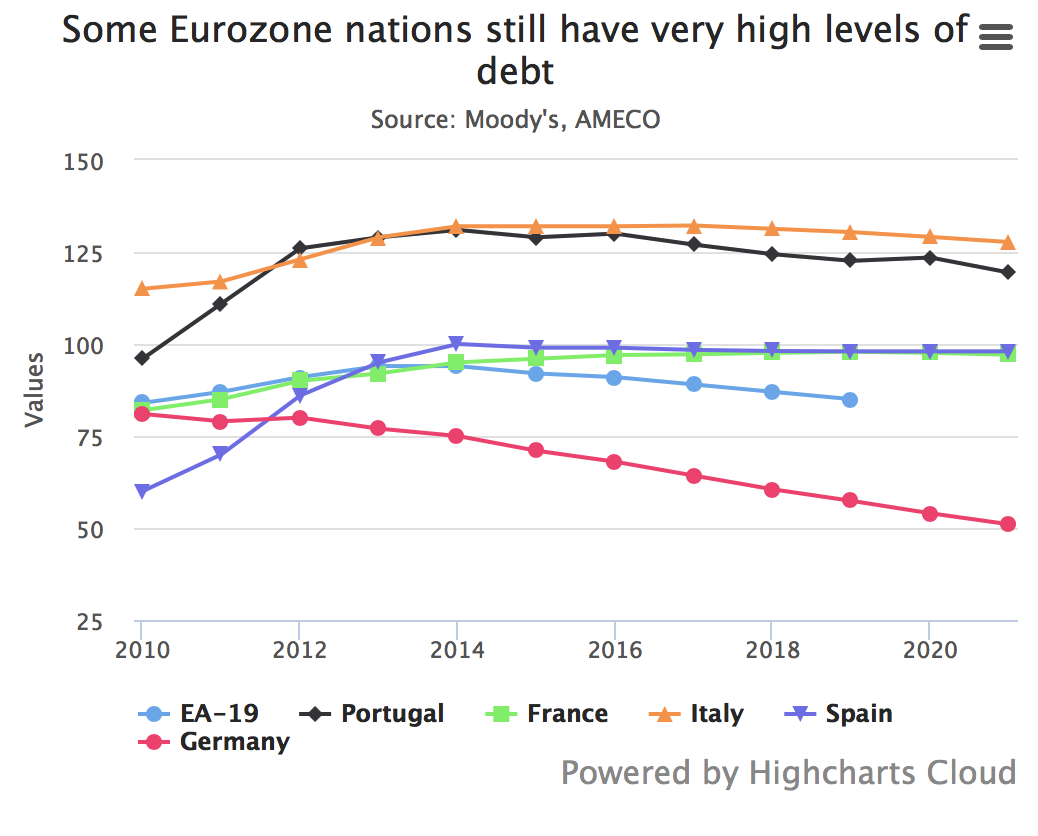

By all accounts, the forecasts for eurozone growth are pretty optimistic. The European Commission has recently revised upwards its expectations for growth in 2018 and 2019, having been surprised by the performance in 2017.

However, they also warn of a potential ‘sharp correction in financial markets’ . In a 44-page forecast the EC warned of asset price vulnerability to ‘a reassessment of fundamentals and risks [that] could expose debt overhand in a number of Member States.’

Ratings agency Moody have also put a dampener on any self-congratulatory moves, a recent report finds that high-national debt is a long-term threat to the single currency union’s prosperity:

“As the economic cycle inevitably turns and growth slows, high public debt will become an increasingly important constraint on sovereign credit profiles.” A downturn could hit national finances hard, “rendering them vulnerable.”

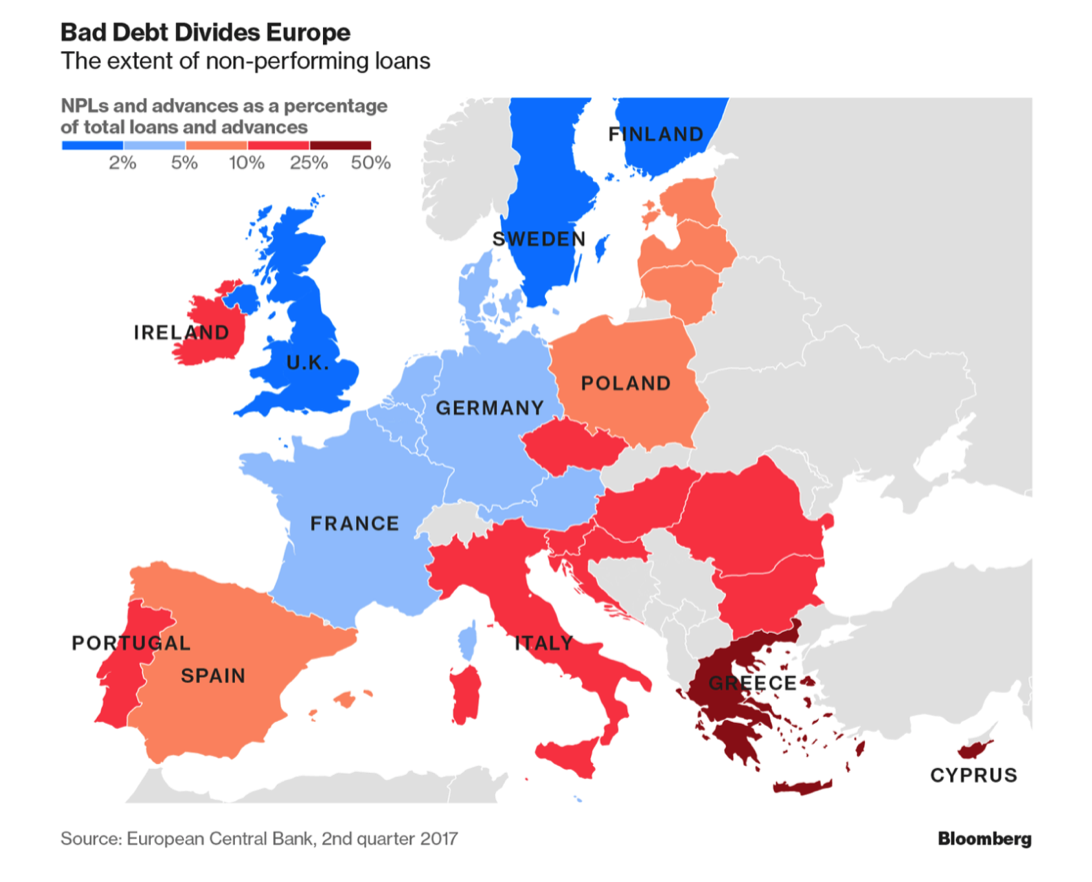

Brexit is not going to send the single currency market spinning out of control but there are major unresolved issues and looming ones which may well do this. Both French and German parties put forward major Eurozone reforms in 2017, no one has agreed on anything. The main issue politicians and bureaucrats are working to resolve is the never-ending interdependence between sovereigns and banks.

The solution that will no doubt be agreed upon will be a banking union. The chances of this being at all fully functioning are extremely slim given the different economic and political interests of each eurozone member. Needless to say the union will not be perfect and therefore the main problems in the single currency market will remain – there will be overdependent financial systems, highly leverage banks, increasingly unimaginable imbalances between member states and more booms and shocks.

All in all, there will not be the tools to deal with ‘shocks’, pushing the ECB further into the red and further away from reform.

America first, consequences second

The EU’s lack of financial reforms, growing euroskepticism and growing debt levels are nothing new. All that was required was a catalyst to cause them to tip the financial union into crisis.

President Donald Trump may well be that catalyst. The US is the only country to have trade featured in the first article of its constitution. This explains why protectionism fits in so nicely with Trump’s ‘America First’ agenda.

Since the end of the Second World War European countries have taken the approach that trade is a means by which nations can find common ground so the risks of going to war are far more costly than just military. Paradoxically the US see trade as a means of exerting ones force and independence on the world – it is a demonstration of sovereignty. This has come at a bit of a shock to the EU.

For years the EU has sailed along arrogantly assuming that current account surpluses from the likes of Germany are not going to be an issue. They are an issue, but one that is usually taken up with the G20, or even the WTO (with who the US wins more than 85% of the dispute-settlement cases). Instead, Trump has taken matters into his own hand and now the eurozone’s own bastion of stability – Germany is in the firing line.

Currently Germany has an 8% current account surplus, whilst the eurozone also runs at a huge 3.5%. This makes them both vulnerable to trade wars. This is a swift lesson in why the ECB’s strategy to prevent a crisis since 2012 has been short-sighted and costly. It has resulted on a current account surplus and now (inevitably) other nations don’t want to take it. The single currency market has opened itself up to protectionist measures.

Should Trump follow through with his threats and put a 35% tariff on European cars then it will lose the economy an estimated €17bn a year. Add to this the ongoing problems in the diesel car market and Germany are in a real bind when it comes to strategic industries.

Of course, the EU can respond to US measures but they are very much on the backfoot. They rely on the US for security support and (until now) to turn a blind eye to their current account surplus. Now, Trump has realised that he has a double-edged sword – his trade tariffs will not only influence the EU’s trade policies but also the defence spending of NATO allies.

The US can get away with protectionist measures as it is far less reliant on foreign trade than the likes of the EU plus it has a relatively insignificant social welfare system. This means there is a significantly lower risk to the economy by engaging in protectionism.

In contrast, the EU is far more reliant on foreign trade particularly due to the impact an increase in protectionism will have on its developed welfare system. The costs are too great to let these measures get the better of them, but with Trump hanging military spending and support over their heads what can the EU do in this new Cold War era?

Should Italy, Tariffs and Trump worry our portfolios?

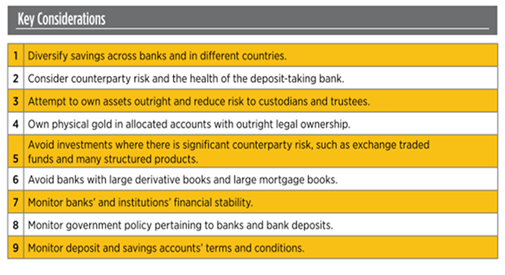

Anything that impacts the financial situation of a country will have an effect on your savings and investment portfolio. This may just be in terms of currency risk or stock market performance. Alternatively it could be worse than that and it could result in bail-ins confiscating money straight from your savings account.

Two years ago, the ECB approved the bail-in tool. In simple terms it gave them the right to remove money from individuals’ and companies deposit accounts in times of financial crisis.

It is now not difficult to see the looming threats to the stability of the European financial system.

Investors would be wise to redirect their attention from the politicking around Italian elections and trade war disagreements, instead fusing their energies on securing their wealth.

Savers should be looking for means in which they can keep their money within instant reach and their reach only. Gold and silver bullion, if owned in the safest manner, remain one of the best options in this regard.

Physical, allocated and segregated bullion coin and bars ownership gives you outright legal ownership and total liquidity. There are no counter parties who can claim it is legally theirs (unlike with cash in the bank or shares) or legislation that rules that deposits can be confiscated to bail out failing banks.

Gold and silver are the financial insurance against bail-ins, political mismanagement, and overreaching government and financial institutions.

To read more about how you can protect your savings in the bail-in era then read our free bail-in guide here.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Related reading

Eurozone Banks ‘As Likely To Fail Now As In 2008’ – Bail-ins?

Bank Bail-In Risk In European Countries Seen In 5 Key Charts

Happy 2nd Birthday Bail-in Tool! We Suggest Gold As The Perfect Gift

News and Commentary

Asia Stocks Fall After U.S. Tech Slump; Yen Drops (Bloomberg.com)

Gold prices edge higher on softer U.S. dollar (Reuters.com)

Tumbling tech stocks lead Asian-market slide (MarketWatch.com)

Tech Rout Punishes U.S. Stocks as Treasuries Surge | (Bloomberg.com)

OPEC, Russia consider 10-20 year oil alliance – Saudi Crown Prince (Reuters.com)

Source: Bloomberg.com

Stock Market Can’t Decide How to Trade Tariff Threats (Bloomberg.com)

Sell Bitcoin, Buy Gold? (Bloomberg.com)

Bank Sector In Peril As Refi Activity Crashes Amid Rising Rates (ZeroHedge.com)

The Lesson From Stock Corrections Past? 200 Days of Pain (Bloomberg.com)

West Virginia congressman introduces gold standard legislation (WSJ.com)

Gold Prices (LBMA AM)

28 Mar: USD 1,341.05, GBP 946.24 & EUR 1,082.23 per ounce

27 Mar: USD 1,350.65, GBP 954.64 & EUR 1,087.41 per ounce

26 Mar: USD 1,348.40, GBP 949.27 & EUR 1,086.95 per ounce

23 Mar: USD 1,342.35, GBP 952.80 & EUR 1,088.65 per ounce

22 Mar: USD 1,328.85, GBP 939.36 & EUR 1,078.10 per ounce

21 Mar: USD 1,316.35, GBP 935.53 & EUR 1,071.64 per ounce

20 Mar: USD 1,312.75, GBP 935.60 & EUR 1,066.22 per ounce

Silver Prices (LBMA)

28 Mar: USD 16.46, GBP 11.63 & EUR 13.28 per ounce

27 Mar: USD 16.64, GBP 11.79 & EUR 13.41 per ounce

26 Mar: USD 16.61, GBP 11.67 & EUR 13.39 per ounce

23 Mar: USD 16.53, GBP 11.70 & EUR 13.39 per ounce

22 Mar: USD 16.52, GBP 11.64 & EUR 13.41 per ounce

21 Mar: USD 16.25, GBP 11.56 & EUR 13.23 per ounce

20 Mar: USD 16.25, GBP 11.60 & EUR 13.22 per ounce

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

end

Due to protectionist policies, hedge funds make their move away from the dollar

(courtesy Greifeld/Bloomberg)

* * *

As trade war heats up, biggest currency whales make their move

Submitted by cpowell on Wed, 2018-03-28 00:58. Section: Daily Dispatches

By Katherine Greifeld

Bloomberg News

Monday, March 26, 2018

For the first time in a decade, the world’s central banks are looking beyond the dollar to build their currency reserves.

With U.S. protectionism on the rise, a number of Wall Street strategists say the case for the euro has rarely been better. Existential crises that hobbled the European experiment have receded. A resurgent economy has spurred talk the region’s central bank will curb policies that drove euro yields below zero. And as President Donald Trump threatens a trade war with China, the European Union is pursuing free-trade deals all across Asia and Latin America.

Of course the dollar commands most of the world’s $11.3 trillion of international reserves and most expect it to remain that way. But even a small shift — whether as a hedge against Trump’s trade policies or in the name of diversification — could have big consequences. After shunning the common currency for years because of negative interest rates and the region’s persistent turmoil, reserve managers at some of the biggest central banks are now looking to add more euros, according to two heads of foreign-exchange strategy who’ve held regular discussions with them. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-03-26/as-trade-war-heats-up…

END

Mike Kosares: the Petro-Yuan could displace the petro dollar and thus the USA dollar hegemony

(courtesy Kosares/GATA)

Mike Kosares: Petro-yuan could displace petro-dollar

Submitted by cpowell on Wed, 2018-03-28 01:18. Section: Daily Dispatches

9:20a SST Wednesday, March 28, 2018

Dear Friend of GATA and Gold:

The new “petro-yuan,” created by the oil futures contract that began trading in Shanghai this week, could mean a lot for the dollar and gold by displacing the petro-dollar, USAGold’s Mike Kosares writes. His analysis is headlined “‘This Is the Single Biggest Change in Capital Markets, Maybe of All Time’ — Union Bank Switzerland” and it’s posted at USAGold here:

http://www.usagold.com/cpmforum/2018/03/27/the-single-biggest-change-in-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.2936 /shanghai bourse CLOSED DOWN 44.36 POINTS OR 1.40% / HANG SANG CLOSED DOWN 768.30 POINTS OR 2.50%

2. Nikkei closed DOWN 286.01 POINTS OR 1/34% /USA: YEN RISES TO 105.92/

3. Europe stocks OPENED RED /USA dollar index RISES TO 89.49/Euro FALLS TO 1.2393

3b Japan 10 year bond yield: RISES TO . +.039/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.92/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 64.76 and Brent: 69.89

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.489%/Italian 10 yr bond yield DOWN to 1.858% /SPAIN 10 YR BOND YIELD DOWN TO 1.231%

3j Greek 10 year bond yield FALLS TO : 4.376?????????????????

3k Gold at $1336.80 silver at:16.47 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 11/100 in roubles/dollar) 57.56

3m oil into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.92 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9517 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1794 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.489%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.7607% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.016% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Rebound From Tech Wreck, But 10Y Yield Breaks Key Support

Following yesterday’s violent and unexpected equity selloff, driven by a so-called “tech wreck” as the FANG+ index dropped by 5.7%, the most on record, and stood on the edge of a key support line precipice…

… this morning, global stocks are predictably lower across the globe, as the tech sector fallout spreads across Asia and Europe…

… although S&P futures are off session lows, with 2,600 providing a support level for the time being, and should that fail, all eyes will be on the 200-DMA, some 15 points lower.

As noted yesterday, on Tuesday US tech shares suffered their worst drop since the February rout, as investors were spooked by bad news from companies including Nvidia, Twitter and Facebook. As Bloomberg notes, the latest leg down for tech shares, which have been the driving force for much of the current bull market in global equities and represent the most popular investment for the hedge fund community, comes at a sensitive time. Stock markets trading with high valuations and tighter liquidity are already being shaken by protectionist moves by Donald Trump. His administration is mulling a crackdown on Chinese investments in technologies the U.S. considers sensitive, the latest step in his plan to punish China for violations of intellectual-property rights.

The tech rout spooked Asia, where the ASX 200 (-0.7%) and Nikkei 225 (-1.3%) tumbled, while weakness in commodities also contributed to the glum. Elsewhere, KOSPI (-1.3%) pharmaceutical and metal stocks joined the tech underperformance after reports stated South Korea steel exports to US would decline 30% under the new trade agreement and that South Korea will amend its premium pricing program for pharmaceuticals to allow participation of US drug makers. Hang Seng (-2.5%) and Shanghai Comp. (-1.4%) were also dragged by the tech slide, while encouraging earnings from big 4 banks ICBC and China Construction Bank only provided brief support and was eventually engulfed by the stock rout.

Europe was no better, with equities (Eurostoxx -1.0%) extending the risk-averse tone seen in the US and Asia, triggered by a tech sell-off which prompted losses within the IT sector in Europe this morning, augmented by month- end flows. As such, semiconductors are the laggards with Dialog Semiconductors (-13.0%), Infineon (-4.0%), ASML Holding (-4.4%) and STMicroelectronics (-5.2%) the worst performers whereas utilities remain slightly supported. In terms of individual movers, Shire (+15.5%) is leading the FTSE 100 and lifting the healthcare sector (+0.5%) after Takeda confirmed to be considering an offer for the company.

Meanwhile, with most attention on equities, the big action overnight was in 10Y yields, where the growing tech turmoil forced 10Y yields out of the 20-bps range that’s held since early February. On Wednesday, the 10Y benchmark dropped as much as three basis points Wednesday to 2.74 percent, the lowest level since Feb. 6, following an eight basis-point drop Tuesday.

The yield has broken below the key 50-day moving average for the first time since mid-December.

Commenting on the move, FTN strategist Jim Vogel wrote in a note that for those caught off-guard by the extent of the bond rally, the shift is “still not alarming but definitely worth watching current rates if equities can’t find their way home. As various tech and social media stories continue to get pummeled on a regular basis, however, trading at 2.805 percent and below is gaining ground.”

It could get worse: as Mark Cudmore warned this morning, positioning in Treasuries signals a shakeout could be in the offing. As of last week, hedge funds and other large speculators had a net short position in 10-year Treasury futures that was the close to record highs. A break of technical levels like moving averages could shift momentum and lead them to cover their bets to protect from further losses. In this context, BMO Capital now expects 2.671% as the next level in sight for the 10-year maturity, which may pause at 2.752 percent. BMO earlier this month said they’re confident that that yields already peaked for 2018.

Also notable, as Bloomberg points out it’s not just the 10-year maturity grappling with re-pricing. Eurodollars advanced by as much as five basis points on Wednesday, while the OIS market is now pricing in less than two Federal Reserve rate hikes for the remainder of the year.

In FX, just like yesterday, the USD has rallied against most G-10 peers again, with month/quarter end positioning still providing support, while the Yen is at session lows, with the USDJPY trading just shy of 105.90 after overnight China officially confirmed that Kim Jong Un met with Xi Jinping and discussed the upcoming meeting with Trump and his eagerness to denuclearize the Korean peninsula.

GBP an early outperformer after reports of an imminent proposal on the Irish border issue. In addition to the summit between China and North Korea, the yen also weakened following news that Japan’s Takeda is hoping to acquire the now bigger Shire PLC.

All core fixed income markets well supported, UST 2s10s re-approach flattest level of the year. Crude futures hold overnight losses after bearish API data, spot gold weighted by USD rally.

Bulletin Headine Summary from RanSquawk

- European equities have extended losses after tech slipped on Wall St. and Asia

- USD firmer vs. all G10 approaching quarter and Japanese financial year end

- Looking ahead, highlights include US GDP, PCE Prices, Pending Home Sales, DoEs and Fed’s Bostic

Top Overnight News

- The Trump administration is considering a crackdown on Chinese investments in technologies the U.S. deems sensitive by invoking a law reserved for national emergencies, among other options, according to people familiar with the matter

- China confirmed Wednesday that Kim met with President Xi Jinping on a surprise visit to Beijing, and said the North Korean leader would be willing to give up his nuclear weapons and hold a summit with the U.S.

- In this bull market alone there’s been five other corrections like this one, and it’s taken around seven months on average for equities to climb out of their hole. Based on that path, the current jitters won’t be fully eradicated until August

- Japan Prime Minister Shinzo Abe says sanctions against North Korea must be kept until the country takes concrete steps to abandon nuclear weapons and missiles

- China considers allowing more derivatives trading under bond connect and the country will steadily accelerate pace of bond market opening up, PBOC official Gao Fei says

- Irish officials have been told to expect new plans “imminently” from U.K. on how it plans to avoid a post-Brexit hard border, The Times reports, citing sources

- The U.S. Treasury finished its slate of bill auctions for the month, with their sale Tuesday of 4-week securities seeing good demand

- Thanks to fresh blows to companies from Nvidia Corp. to Facebook Inc., the biggest industry in the S&P 500 Index dropped 3.5 percent, the biggest decline since the broad-market selloff reached its worst point on Feb. 8

Market Snapshot

- S&P 500 futures down 0.2% to 2,609.75

- STOXX Europe 600 down 1% to 363.90

- MXAP down 1.4% to 172.41

- MXAPJ down 1.6% to 562.73

- Nikkei down 1.3% to 21,031.31

- Topix down 1% to 1,699.56

- Hang Seng Index down 2.5% to 30,022.53

- Shanghai Composite down 1.4% to 3,122.29

- Sensex down 0.4% to 33,035.44

- Australia S&P/ASX 200 down 0.7% to 5,789.47

- Kospi down 1.3% to 2,419.29

- German 10Y yield fell 1.8 bps to 0.486%

- Euro down 0.04% to $1.2398

- Italian 10Y yield fell 3.7 bps to 1.619%

- Spanish 10Y yield unchanged at 1.236%

- Brent futures down 0.6% to $69.69/bbl

- Gold spot down 0.3% to $1,340.98

- U.S. Dollar Index up 0.1% to 89.47

Asian equity markets traded negative across the board as the region followed suit from the losses on Wall St where trade concerns lingered and tech sold-off, while some also attributed the exacerbated pressure to flows heading into month-end and Easter break. As such, ASX 200 (-0.7%) and Nikkei 225 (-1.3%) were lower as tech stocks conformed to the losses in their counterparts stateside, while weakness in commodities also contributed to the glum. Elsewhere, KOSPI (-1.3%) pharmaceutical and metal stocks joined the tech underperformance after reports stated South Korea steel exports to US would decline 30% under the new trade agreement and that South Korea will amend its premium pricing program for pharmaceuticals to allow participation of US drug makers. Hang Seng (-2.5%) and Shanghai Comp. (-1.4%) were also dragged by the tech slide, while encouraging earnings from big 4 banks ICBC and China Construction Bank only provided brief support and was eventually engulfed by the stock rout. Finally, 10yr JGBs saw a tale of two-halves as they initially tracked the gains in T-notes amid a flight to quality from the stock market sell-off and with the BoJ also present in the market under its bond buying program, before gains were then pared on return from the Tokyo break in which prices returned flat

Top Asian News

- JPMorgan Looks Beyond Finance to Hire Tech, Math Grads in Asia

- Bank Indonesia’s Incoming Governor Pledges Growth, Stability

- Time Is Running Out for the Philippine Exchange Merger Deal

- Sri Lanka Plans Dollar Loans and Bonds as Maturing Debt Looms

- Chung Family to Overhaul Hyundai Motor Group Ownership Structure

European equities (Eurostoxx -1.0%) have extended on the risk-averse tone seen in the US and Asia, triggered by a tech sell-off which prompted losses within the IT sector in Europe this morning, augmented by month-end flows. As such, semiconductors are the laggards with Dialog Semiconductors (-13.0%), Infineon (-4.0%), ASML Holding (-4.4%) and STMicroelectronics (-5.2%) the worst performers whereas utilities remain slightly supported. In terms of individual movers, Shire (+15.5%) is leading the FTSE 100 and lifting the healthcare sector (+0.5%) after Takeda confirmed to be considering an offer for the Co., although considerations are at a prelim stage and no approach has been made yet. Elsewhere, Melrose (-0.5%) have continued to defend their approach for GKN ahead of tomorrow’s deadline.

Top European News

- Banca Carige Says Conditions Not Right for Planned Tier 2 Deal

- Faurecia Says Signed Record Contract for Seats With BMW

- It’s Back to the 80s for Brexit-Hit Broadcasters Without Deal

In FX, another rebalancing model is Usd positive for month, quarter and Japanese financial year end, albeit ‘moderately’, while a separate bank is looking to buy the Greenback vs the Pound, Loonie, Aud and Nok if global stocks fall further. Hence, the Dollar retains an underlying bid on dips and is firmer vs all G10 peers bar the Gbp, which is deriving some independent support on latest Brexit headlines (reports that an Irish border resolution is in the offing). Cable and Eur/Gbp are bucking the broader trend, with the former hovering just below 1.4200 after a retreat to test the first layer of bids said to be macro-related in the 1.4135-25 area, and the latter seeing some resistance around 0.8750. Eur/Usd is also holding up relatively well near 1.2400 where decent option expiry interest lies (1.6 bn), but also as tech support at the 100 HMA (1.2379) holds. In fact, the Eur is defying some end of March ‘strong’ selling calls and outperforming other majors, like the Sek and Nok in wake of weaker than expected retail sales data from both Scandi nations overall. Even the Chf is weaker despite the resurgence of risk aversion, while its traditional safe- haven counterpart, Jpy, is caught between the aforementioned downturn in sentiment and more positive geopolitical vibes on the NK-SK-US front. Usd/Jpy rangy between 105.69 and 105.96 200 HMA and Fib levels respectively. Usd/Cad is back around 1.2900 despite constructive NAFTA negotiations, while Aud/Usd and Nzd/Usd remain bearish, as the former has breached its recent 0.7672 low and the latter tests support/bids at 0.7250.

In commodities, the commodities complex continues to be subdued amid the dampened risk appetite. WTI (-0.9%) and Brent (-0.6%) futures are extending losses with prices pressured by the surprise build in API crude inventories (5.321M vs. Exp. -0.300M). Additionally, the Iraqi oil Minister Luaibi stated that Iraq will not deviate from any OPEC decisions on crude supply; this follows the Saudi Crown Prince stating OPEC seeks a 10 to 20-year supply co-operation with Russia as well as other producers. Gold (-0.1%) slipped from a 5-week high as a firmer dollar is weighing on the yellow metal. Fears of a trade war continue to cast a shadow over the base metal market with copper (-0.6%) lower and Dalian iron ore futures slipping to their lowest since June shortly after the open.

Looking at the day ahead, datawise all eyes will be on the US with the third and final revisions due to be made for Q4 GDP, while the February advance goods trade balance, wholesale inventories and pending home sales data are also due out. The Fed’s Bostic is due to again make comments in the late afternoon.

US event calendar

- 8:30am: GDP Annualized QoQ, est. 2.7%, prior 2.5%

- Personal Consumption, est. 3.8%, prior 3.8%

- GDP Price Index, est. 2.3%, prior 2.3%

- Core PCE QoQ, est. 1.9%, prior 1.9%

- 8:30am: Advance Goods Trade Balance, est. $74.4b deficit, prior $74.4b deficit, revised $75.3b deficit

- 8:30am: Retail Inventories MoM, prior 0.8%, revised 0.7%; Wholesale Inventories MoM, est. 0.5%, prior 0.8%

- 10am: Pending Home Sales MoM, est. 2.0%, prior -4.7%; NSA YoY, prior -1.7%

DB’s Craig Nicol concludes the overnight wrap

Well, at least we can say that we’re getting used to this now. After things appeared eerily quiet throughout the morning and all the way up until the European close, US equities suffered more huge falls last night, undoing much of the good work on Monday. The S&P 500 finished -1.73% – although stayed just above the 200-day moving average – and the Dow ended -1.43%. To put some perspective on things, the last four days have seen points moves for the Dow of 345, 669, 425 and 724. That’s an average of 541 points. The average daily move in 2017 was just 68 points and there were only 3 days last year when there was a move of at least 300 points. Incredible.

What was striking about yesterday though was that bonds also finally got in on the act with 10y Treasury yields finally snapping out of a 22-day range to close below 2.80% for the first time since February 5th, eventually finishing at 2.776% (-7.7bps). The curve flattened too with 2s10s 7.0bps flatter. That puts it at the flattest since early January. Bunds also crept under 0.50% for the first time since January and they are now down 26bps from the 2018 high. We also couldn’t help but notice that the value of negative yielding bonds around the globe is back up to $8.8tn. This is after the combined value fell below $7.0tn in early February.

Anyway, the blame yesterday for equity markets – and the broader risk-off tone – was firmly placed at the hands of the tech sector again where it appears that there are more than a few chinks in the armour now. Indeed, tech names were down -3.47% in the S&P 500 while the Nasdaq tumbled -2.93% and notched up its fourth consecutive session whereby the index has moved at least 2% in either direction. The last time that happened was in late September 2011. The NYSE FANG index – which includes 10 of the largest global tech names – fell a whopping -5.63% and the most since 2014 when the index first started. It also lost a combined $134bn in market cap yesterday, which now means those names have lost $320bn in value since the index peaked back on March 12th. Facebook tumbled -4.87% and seems to be at the centre of any selloff related to the sector at the moment however news that Nvidia was suspending self-driving car testing and Tesla was undergoing another investigation related to a crash last year just compounded the pain. The Nasdaq equivalent of the VIX rose to 29.01 last night (up nearly 4 points from Monday) and is closing back in on the February high of 33.89.

Overnight, some of the focus has shifted to the news that China has confirmed North Korea’s leader Kim Jong Un has indeed visited Beijing and met with China’s President Xi. Local Chinese press Xinhua reported Kim as saying that “the issue of denuclearization of the Korean Peninsula can be resolved, if South Korea and the United States respond to our efforts with goodwill, create an atmosphere of peace and stability while taking progressive and synchronous measures for the realization of peace”. While there is no sign that an agreement has been made, the language is clearly a lot more conciliatory ahead of a proposed meeting between Kim and President Trump. Despite that development, bourses in Asia have followed the negative US lead from last night and are trading lower with the Nikkei (-1.77%), Kospi (-1.32%), Hang Seng (-1.03%), ASX 200 (-0.68%) and Shanghai Comp (-0.61%) all down as we type. The Yen is a shade weaker while the Korean won has been the biggest gainer this morning.

Moving on. As we noted at the top the wave of selling really started after Europe went home yesterday with the Stoxx 600 and DAX actually rebounding with +1.21% and +1.56% gains. There was a slight mid-afternoon blip which came after headlines hit the wires saying that the US was moving to curb Chinese investments in the US. However, that news was nothing new and it was pointed out that the share of foreign direct investment held by China in the US, while growing, is still very small and the bigger issue remains trade policies in this ongoing game of chess between the two nations.

So, while the moves late in the evening for the tech sector dominated, there were some other snippets worth highlighting from the last 24 hours. Over at the Fed, an interview by the WSJ with Atlanta Fed’s Bostic (neutral/voter) revealed that the Fed President is an advocate of gradually raising rates, however cited that he was unsure over how the economy might respond to the planned tax cuts and increased government spending next year, which in turn could complicate the outlook for monetary policy.

The ECB’s Nowotny also spoke yesterday morning and stuck to the largely consensus playbook that the ECB should be able to cut stimulus after September, with a decision likely to be made in the summer. Nowotny also cited that there are two lessons to learn from the Fed, one being to act when necessary and the other is to be careful and communicate in a timely fashion. There was also some data in Europe yesterday and it was a touch on the softer side. The first was the economic sentiment index for the Euro area which fell a little bit more than expected in February to 112.6 (vs. 113.3 expected) from 114.2 in January – matching the decline in the PMIs somewhat. The money and credit aggregates report from the ECB also showed a deceleration in M3 money supply to 4.2% yoy from 4.6% while on the credit side growth slowed to 3.0% from 3.2%. It’s worth pointing out that a measure of economic surprises in the Eurozone is hovering at the lowest since March 2016 right now which is in contrast to a similar measure in the US which is only just off the December 2017 highs and the highest since the GFC.

Staying with Europe, local Italian press and Bloomberg reported yesterday morning that Five Star was supposedly offering some ministerial positions to the Northern League. The read-through was that this showed 5SM’s intention to win support from the NL and in turn pressing the latter to form a government, but without the whole centre-right. The bigger question is how the NL balance potentially trying to reach a deal with the 5SM, but without losing centre-right support, which could jeopardize Salvini’s (leader of the NL) ability to become prime minister. As we said yesterday there is still a long way to go so it’s likely that this ebbs and flows for some time.

Here in the UK, the Times newspaper has reported overnight that the UK is to offer a hard border resolution imminently, with details beyond just the so-called backstop plan. Sterling is up another +0.22% this morning and is approaching the February highs again of $1.426.

For completeness, in terms of the remaining data flow from yesterday, in the US the March conference board consumer confidence index fell 2.3pts from last month’s 17 year high to a still solid level of 127.7 (vs. 131.0 expected), with a modest mom decline in both the present situation and expectations index. The Richmond Fed manufacturing index was below consensus at 15 (vs. 22 expected) while the January S&P Corelogic house price index was above market at +0.75% mom (vs. +0.6% expected), leading to annual growth of +6.4% yoy. Back in Europe, the final reading on the Euro area’s March consumer confidence was unrevised at 0.1 while the business climate index was a touch below at 1.34 (vs. 1.36 expected). Elsewhere, Spain’s March CPI was below market at +1.3% yoy (vs. 1.5% expected).

Looking at the day ahead, datawise all eyes will be on the US with the third and final revisions due to be made for Q4 GDP, while the February advance goods trade balance, wholesale inventories and pending home sales data are also due out. The Fed’s Bostic is due to again make comments in the late afternoon. In Europe consumer confidence prints in Germany and France as well as March CBI retail sales data in the UK is due.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 44.36 POINTS OR 1.40% /Hang Sang CLOSED DOWN 768.30 POINTS OR 2.50% / The Nikkei closed DOWN 286.01/Australia’s all ordinaires CLOSED DOWN 0.75%/Chinese yuan (ONSHORE) closed DOWN at 6.2936/Oil DOWN to 64.76 dollars per barrel for WTI and 69.89 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.2936 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.2796 /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY POOR CHINESE MARKETS/WITH NEW TRUMP TRADE DEALS DISCUSSED WEAKER GLOBAL MARKETS/WEAKER CURRENCY )

3 a NORTH KOREA/USA

North Korea/China

end

3 b JAPAN AFFAIRS

END

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

France/Germany

Germany and France clash over what to do with USA car tariffs. Germany due to its huge export business wants to make concessions. France says no concessions. However it is ultimately the EU and not just Germany and France that must make that decision

(courtesy zerohedge)

France And Germany Clash Over US Car Tariffs

With several weeks remaining until steel and aluminum tariffs introduced a few weeks ago by the Trump administration take effect, the US and its largest trading partners are mired in behind-the-scenes negotiations to strike a deal that could win them an exemption from some or all of the tariffs.

And while recent leaks have focused primarily on the talks between Treasury Secretary Steven Mnuchin,Trade Representative Robert Lighthizer and Chinese economy czar Liu He, Bloomberg today reported that there’s a growing rift between Germany and France regarding how they should respond to the US tariffs.

Germany is willing to offer the US some concessions to protect its export-led economy; however, other EU members – including France – believe the bloc should offer no concessions. The EU is still trying to work out a common response to the Trump tariffs.

At stake is a trade relationship worth some $640 billion in 2016. Germany is in favor of any EU deal covering new rules on tariffs for a series of products including cars, machinery, foodstuffs and pharmaceuticals. That stance is not shared by France, which wants to focus on pressuring China over issues such as subsidies and overcapacity in the steel industry.

Chancellor Angela Merkel and her government are already feeling out the German car industry and whether they might be able to convince it to support a reduction to the EU’s 10% tariff on auto imports. Carmakers reportedly responded positively to the idea.

“Dialogue with the US must continue at the highest political level,” the VDA German car industry body said in a statement when asked about the report. “We advocate sustainable and reliable agreements that are WTO-compliant. In the interests of fair and free trade, it is necessary to dismantle each other’s trade barriers and to agree a new framework.”

German Economy Minister Peter Altmaier, who met last week with US Commerce Secretary Wilbur Ross, recently told reporters that he hadn’t made an offer. He later denied reports that he pitched lowering auto tariffs.

“It is only the EU which negotiates, united and together. I have neither made any offers nor any promises,” he said. A spokeswoman for his ministry added that he had kept EU Trade Commissioner Cecilia Malmstrom fully informed on the discussions.

Trump spoke on Tuesday with both Merkel and French President Emmanuel Macron, according to separate statements from the White House. Trump and Merkel discussed joining forces to counter China. Macron reminded Trump that European steel and aluminum exports are not a security threat to the US. Trump has largely predicated his protectionist push on national security concerns.

Merkel is trying to persuade Trump to give up on forging bilateral agreements with each European state and instead agree to common EU guidelines in accordance with WTO rules. Under those rules, countries can only offer concessions that lower trade barriers below the WTO standard if the reduction covers “substantially all” commerce – not individual products and sectors. The average EU tariff on US imports is around 3%, while the US average duty is around 2.4%.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia/Germany/Denmark

Germany Approves Russia-Led Nord Stream 2 Gas Pipeline

Authored by Tsvetana Paraskova via OilPrice.com,

Germany approved on Tuesday the construction and operation of the Russia-led Nord Stream 2 gas pipeline in its territorial waters, thus issuing all necessary permits for the German section of the project that has torn Europe and EU member states over the implications of Russia’s gas giant Gazprom gaining even more foothold on the European gas market.

Hailing the project as necessary to cover Europe’s future supply gap and contributing to the “security of supply and competition in the EU gas market,” the pipeline company Nord Stream 2 AG said on Tuesday that the permitting procedures in the other four countries along the route – Russia, Finland, Sweden and Denmark – were proceeding as planned.

“Further permits are expected to be issued in the coming months. Accordingly, scheduled construction works are to be implemented in 2018 as planned,” the company said.

Germany is the key beneficiary of Nord Stream 2 and supports the project on the grounds that it is an economic issue.

Other EU states, however–including Poland and the Baltic states, as well as the European Union institutions–argue that the project further solidifies Russia’s grip on Europe’s gas market and undermines efforts to diversify supplies.

For Russia, Nord Stream 2 – a project to twin the existing Nord Stream pipeline between Russia and Germany via the Baltic Sea — not only boosts its gas supplies to the EU, but also bypasses the Ukrainian transit route.

With the spy poisoning scandal in the UK and the West-Russia tension high, Nord Stream 2 has taken center stage in energy policies again in recent weeks. Earlier this month, U.S. Senators urged the U.S. Administration “to utilize all of the tools at its disposal to prevent its construction.

Last week, the Energy Committee at the European Parliament approved draft amendments to the EU rules to state that all gas pipelines from third countries into the EU must comply fully with EU gas market rules on EU territory, including Nord Stream 2, which is far from complying with those.

While it’s no surprise that Germany has now issued all permits to Nord Stream 2, other countries along the pipeline route, Denmark in particular, could block the proposed route in its waters on security grounds, but Danish officials are not rushing the decision.

end

good reason to whack gold

(courtesy zerohedge)

Russia Warns West Risks “Hot War” After Mass Expulsion Of Diplomats

After a legion of western nations announced this week that they would expel Russian diplomats in solidarity with the UK, one Russian ambassador warned during an impromptu unscripted speech that, by hastily blaming Moscow for the poisoning of a former Russian spy at a shopping center in Salisbury, the West was risking a return to the Cold War. A second Russian ambassador took the warning a step further, and claimed the West has inadvertently risked a “hot war” with Russia.

So far, 23 countries have expelled over 130 Russian diplomats since the UK pointed the finger at Russia, accusing it of organizing an assassination plot that involved poisoning former Russian spy Sergei Skripal with a Soviet-era nerve agent called Novichok.

The UK demanded that Russia explain how the nerve agent came to be used in the attack, if it wasn’t ordered by senior officials in the Russian government, per Newsweek.

Grigory Logvinov

Russia responded by demanding a sample of the chemical used, and offered to assist the UK in its investigation, but has been rebuffed. Meanwhile, the UK media reports say Skripal and his daughter Yulia Skripal may never fully recover from the attack.